UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2007

Commission file no: 0-22955

BAY BANKS OF VIRGINIA, INC.

(Exact name of registrant as specified in its charter)

| | |

| VIRGINIA | | 54-1838100 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

100 SOUTH MAIN STREET, KILMARNOCK, VIRGINIA 22482

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: 804.435.1171

Securities registered under Section 12(b) of the Exchange Act: None

Securities registered under Section 12(g) of the Exchange Act:

Common Stock ($5.00 Par Value)

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ¨ NO x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES ¨ NO x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES x NO ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| | |

Large accelerated filer ¨ | | Accelerated filer ¨ |

| |

Non-accelerated filer ¨ | | Smaller Reporting Company x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). YES ¨ NO x

The aggregate market value of voting stock held by non-affiliates of the registrant at June 30, 2007, based on the closing sale price of the registrant’s common stock on June 30, 2007, was $34,350,747.

The number of shares outstanding of the registrant’s common stock as of March 25, 2008 was 2,363,917.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement for its Annual Meeting of Shareholders to be held on May 19, 2008 are incorporated by reference into Part III of this Form 10-K.

BAY BANKS OF VIRGINIA

INDEX

2

PART I

ITEM 1: BUSINESS

GENERAL

Bay Banks of Virginia, Inc. (the “Company”) is a bank holding company that conducts substantially all of its operations through its subsidiaries, Bank of Lancaster (the “Bank”) and Bay Trust Company (the “Trust Company”). Bay Banks of Virginia, Inc., was incorporated under the laws of the Commonwealth of Virginia on June 30, 1997, in connection with the holding company reorganization of the Bank of Lancaster.

The Bank is a state-chartered bank and a member of the Federal Reserve System. The Bank services individual and commercial customers, the majority of which are in the Northern Neck of Virginia, by providing a full range of banking and related financial services, including checking, savings, other depository services, commercial and industrial loans, residential and commercial mortgages, home equity loans, consumer installment loans, investment brokerage services, insurance, credit cards, and online banking.

The Bank has two offices located in Kilmarnock, Virginia, and one office each in White Stone, Warsaw, Montross, Heathsville, and Callao, Virginia. As of this writing, an eighth branch is under construction in Burgess, Virginia, and a ninth branch is being planned for Colonial Beach, Virginia. A substantial amount of the Bank’s deposits are interest bearing, and the majority of the Bank’s loan portfolio is secured by real estate. Deposits of the Bank are insured by the Deposit Insurance Fund of the Federal Deposit Insurance Corporation (the “FDIC”). The Bank opened for business in 1930 and has partnered with the community to ensure responsible growth and development since that time.

In August of 1999, Bay Banks of Virginia formed Bay Trust Company. This subsidiary of the Company was created to purchase and manage the assets of the trust department of the Bank of Lancaster. The sale and transfer of assets from the Bank to the Trust Company was completed as of the close of business on December 31, 1999. As of January 1, 2000, the Bank of Lancaster no longer owned or managed the trust function, and thereby no longer receives an income stream from the trust department. Income generated by the Trust Company is consolidated with the Bank’s income and the Company’s income for the purposes of the Company’s consolidated financial statements. The Trust Company opened for business on January 1, 2000, in its permanent location on Main Street in Kilmarnock, Virginia.

The Company’s marketplace is situated on the “Northern Neck” peninsula of Virginia, plus Middlesex County. The “Northern Neck” includes the counties of Lancaster, Northumberland, Richmond, and Westmoreland. Smaller, retired households with relatively high per capita incomes dominate the Company’s primary trading area. Growth in households, employment, and retail sales is moderate but the local economic conditions are stable as growth has been positive for several years. Health care, tourism, and related services are the major employment sectors in the “Northern Neck.”

The Company had total assets of $326.3 million, deposits of $259.6 million, and shareholders equity of $27.1 million as of December 31, 2007.

Through the Bank of Lancaster and Bay Trust Company, Bay Banks of Virginia provides a wide range of services to its customers in its market area. These services are summarized as follows.

Real Estate Lending. The Bank’s real estate loan portfolio is the largest segment of the loan portfolio. The majority of the Bank’s real estate loans are adjustable rate mortgages on one-to-four family residential properties. These mortgages are underwritten and documented within the guidelines of the regulations of the Board of Governors of the Federal Reserve System (the “Federal Reserve”). The Bank underwrites mainly adjustable rate mortgages as the marketplace allows. Home equity lines of credit are also offered. Construction loans with a twelve-month term are another component of the Bank’s portfolio. Underwritten at 80% loan to value, and to qualified builders and individuals, these loans are disbursed as construction progresses and verified by Bank inspection. The Bank also offers commercial loans that are secured by real estate. These loans are typically written at a maximum of 80% loan to value and either vary with the prime rate of interest, or adjust in one, three, or five year terms.

The Company also offers secondary market loan origination. Through the Bank, customers may apply for a home mortgage that will be underwritten in accordance with the guidelines of either the Federal Home Loan Mortgage Corporation (“FHLMC”) or the Federal National Mortgage Corporation (“FNMA”). These loans are then sold into the secondary market or to FNMA on a loan-by-loan basis. The Bank earns origination fees through offering this service.

Consumer Lending. In an effort to offer a full range of services, the Bank’s consumer lending includes automobile and boat financing, home improvement loans, and unsecured personal loans. These loans historically entail greater risk than loans secured by real estate, but also offer a higher return.

Commercial Lending. Commercial lending activities include small business loans, asset based loans, and other secured and unsecured loans and lines of credit. Commercial lending may entail greater risk than residential mortgage lending, and is therefore underwritten with strict risk management standards. Among the criteria for determining the borrower’s ability to repay is a cash flow analysis of the business and business collateral.

Business Development. The Bank offers several services to commercial customers. These services include analysis checking, cash management deposit accounts, wire services, direct deposit payroll service, online banking, telephone banking, remote deposit, and a full line of commercial lending options. The Bank also offers Small Business Administration loan products to include the 504 Program, which provides long term funding for commercial real estate and long-lived equipment. This allows commercial customers to apply for favorable rate loans for the development of business opportunities, while providing the Bank with a partial guarantee of the outstanding loan balance.

Bay Services Company, Inc. The Bank has one wholly owned subsidiary, Bay Services Company, Inc., a Virginia corporation organized in 1994 (“Bay Services”). Bay Services owns an interest in a land title insurance agency, Bankers Title of Fredericksburg, and an investment and insurance services company, Bankers Investment Group. Bankers Title of Fredericksburg sells title insurance to mortgage loan customers, including customers of the Bank of Lancaster and the other financial institutions that have an ownership interest in the agency. Bankers Investment Group provides the Bank’s non-deposit products department with insurance and investment products for marketing within the Bank’s primary marketing area. At the time of this report, Bankers Investment Group is merging with and into Infinex Investments, Inc., with the latter becoming the surviving entity. Management expects this transition to be transparent to the Company’s customers because the clearing agent will remain unchanged. Also, Bankers Title of Fredericksburg is merging into Bankers Title of Shenandoah, with the latter becoming the surviving entity. Management expects this merger will reap efficiencies and will likewise be transparent to the Company’s customers.

Bay Trust Company. The Trust Company offers a broad range of investment services as well as traditional trust and related fiduciary services. Included are estate planning and settlement, revocable and irrevocable living trusts, testamentary trusts, custodial accounts, investment management accounts, and managed, as well as self-directed rollover Individual Retirement Accounts.

COMPETITION

The Company’s marketplace is highly competitive. The Company is subject to competition from a variety of commercial banks and financial service companies, large national and regional financial institutions, large regional credit unions, mortgage companies, consumer finance companies, mutual funds and insurance companies. Competition for loans and deposits is affected by numerous factors, including interest rates and institutional reputation.

SUPERVISION AND REGULATION

Bank holding companies and banks are regulated under both federal and state law. The Company is subject to regulation by the Federal Reserve. Under the Bank Holding Company Act of 1956, the Federal Reserve exercises supervisory responsibility for any non-bank acquisition, merger or consolidation. In addition, the Bank Holding Company Act limits the activities of a bank holding company and its subsidiaries to that of banking, managing or controlling banks, or any other activity that is closely related to banking. In addition, the Company is registered under the bank holding company laws of Virginia, and as such is subject to regulation and supervision by the Virginia State Corporation Commission’s Bureau of Financial Institutions.

The following description summarizes the significant state and Federal laws to which the Company and the Bank are subject. To the extent statutory or regulatory provisions or proposals are set forth the description is qualified in its entirety by reference to the particular statutory or regulatory provisions or proposals.

4

The Bank is supervised and regularly examined by the Federal Reserve and the Virginia State Corporation Commission’s Bureau of Financial Institutions. These on-site examinations verify compliance with regulations governing corporate practices, capitalization, and safety and soundness. Further, the Bank is subject to the requirements of the Community Reinvestment Act (the “CRA”). The CRA requires financial institutions to meet the credit needs of the local community, including low to moderate-income needs. Compliance with the CRA is monitored through regular examination by the Federal Reserve.

Federal Reserve regulations permit bank holding companies to engage in non-banking activities closely related to banking or to managing or controlling banks. These activities include the making or servicing of loans, performing certain data processing services, and certain leasing and insurance agency activities.

The Company owns 100% of the stock of the Bank of Lancaster. The Bank is prohibited by the Federal Reserve from holding or purchasing its own shares except in limited circumstances. Further, the Bank is subject to certain requirements as imposed by state banking statutes and regulations. The Bank is limited by the Federal Reserve regarding what dividends it can pay the Company. Any dividend in excess of the total of the Bank’s net profit for that year plus retained earnings from the prior two years must be approved by the proper regulatory agencies. Further, under the Federal Deposit Insurance Corporation Improvement Act of 1991 (the “FDICIA”), insured depository institutions are prohibited from making capital distributions, if, after making such distributions, the institution would become “undercapitalized” as defined by regulation. Based upon the Bank’s current financial position, it is not anticipated that this statute will impact the continued operation of the Bank.

As a bank holding company, Bay Banks of Virginia is required to file with the Federal Reserve an annual report and such additional information as it may require pursuant to the Bank Holding Company Act. The Federal Reserve may also conduct examinations of the Company and any or all of its subsidiaries.

CAPITAL REQUIREMENTS

The Federal Reserve, the Office of the Comptroller of the Currency and the FDIC have issued substantially similar risk-based and leverage capital guidelines applicable to banking organizations. In addition, those regulatory agencies may from time to time require that a banking organization maintain capital above the minimum levels because of its financial condition or actual or anticipated growth. Under the risk-based capital requirements of these federal bank regulatory agencies, the Company and the Bank are required to maintain a minimum ratio of total capital to risk-weighted assets of 8%. At least half of the total capital is required to be “Tier 1 capital”, which consists principally of common and certain qualifying preferred shareholders’ equity, less certain intangibles and other adjustments. The remainder (“Tier 2 capital”) consists of a limited amount of subordinated and other qualifying debt (including certain hybrid capital instruments) and a limited amount of the general loan loss allowance. The Tier 1 and total capital to risk-weighted asset ratios of the Company as of December 31, 2007 were 9.8% and 10.8%, respectively.

In addition, each of the federal regulatory agencies has established a minimum leverage capital ratio (Tier 1 capital to average risk-weighted assets) (“Tier 1 leverage ratio”). These guidelines provide for a minimum Tier 1 leverage ratio of 4% for banks and bank holding companies that meet certain specified criteria, including that they have the highest regulatory examination rating and are not contemplating significant growth or expansion. The Tier 1 leverage ratio of the Company as of December 31, 2007, was 7.6%, which is well above the minimum requirement. The guidelines also provide that banking organizations that are experiencing internal growth or making acquisitions will be expected to maintain strong capital positions substantially above the minimum supervisory levels, without significant reliance on intangible assets.

DEPOSIT INSURANCE

The FDIC insures the deposits of the Bank up to the limits set forth under applicable law. On February 15, 2006, federal legislation to reform federal deposit insurance was enacted. The new law merged the old Bank Insurance Fund and Savings Association Insurance Fund into the single Deposit Insurance Fund (the “DIF”), increased deposit insurance coverage for IRAs to $250,000, provides for the further increase of deposit insurance on all accounts by indexing the coverage to the rate of inflation, authorizes the FDIC to set the reserve ratio of the DIF at a level between 1.15% and 1.50%, and permits the FDIC to establish assessments to be paid by insured banks to maintain the minimum ratios.

5

On November 2, 2006, the FDIC adopted final regulations establishing a risk-based assessment system that is intended to more closely tie each bank’s deposit insurance assessments to the risk it poses to the DIF. Under the new risk-based assessment system, which became effective in the beginning of 2007, the FDIC will evaluate each bank’s risk based on three primary factors: (1) its supervisory rating, (2) its financial ratios, and (3) its long-term debt issuer rating, if any. The new rate for the Bank is 6.14 cents for every $100 of domestic deposits, per the assessment invoice dated March 15, 2008.

Applied to the Bank’s assessment base of approximately $260 million, these new regulations translate to an annual deposit premium of approximately $160 thousand. Most banks, including Bank of Lancaster, have not been required to pay any deposit insurance premiums since 1995. As part of the reform, Congress provided credits to institutions that paid high premiums in the past to bolster the FDIC’s insurance reserves. As a result, the Bank had assessments credits to initially offset all of its premiums in 2007. The assessment credit is being recognized on a go-forward basis to reduce future deposit premiums. These assessment credits will be exhausted in the fourth quarter of 2008, resulting in higher general and administrative expenses of approximately $40,000 in 2008. As the level of annual deposit premiums is dependent on the amount of the Bank’s deposit assessment base, and assuming the deposit base grows to approximately $273 million in 2009, the annual deposit premiums will result in higher general and administrative expenses of approximately $168 thousand in 2009.

SAFETY AND SOUNDNESS REGULATIONS

The FDIC has adopted guidelines that establish standards for safety and soundness of banks. They are designed to identify potential safety and soundness problems and ensure that banks address those concerns before they pose a risk to the deposit insurance fund. If the FDIC determines that an institution fails to meet any of these standards, the agency can require the institution to prepare and submit a plan to come into compliance. If the agency determines that the plan is unacceptable or is not implemented, the agency must, by order, require the institution to correct the deficiency. The federal banking agencies have broad powers under current federal law to make prompt corrective action to resolve problems of insured depository institutions. The extent of these powers depends upon whether the institution in question is considered “well capitalized,” “adequately capitalized,” “under capitalized,” “significantly under capitalized,” or “critically undercapitalized.” All such terms are defined under uniform regulation defining such capital levels issued by each of the federal banking agencies. The Bank is considered well capitalized.

The FDIC also has safety and soundness regulations and accompanying guidelines on asset quality and earnings standards. The guidelines provide six standards for establishing and maintaining a system to identify problem assets and prevent those assets from deteriorating. The guidelines also provide standards for evaluating and monitoring earnings and for ensuring that earnings are sufficient to maintain adequate capital and reserves. If an institution fails to comply with a safety and soundness standard, the agency may require the institution to submit and implement an acceptable compliance plan, or face enforcement action.

THE GRAMM-LEACH BLILEY ACT OF 1999

The Gramm-Leach-Bliley Act of 1999 (“GLBA”) was signed into law on November 12, 1999. The main purpose of GLBA is to permit greater affiliations within the financial services industry, primarily banking, securities and insurance. The provisions of GLBA that are believed to be of most significance to the Company are discussed below.

GLBA repealed sections 20 and 32 of the Glass-Steagall Act, which separated commercial banking from investment banking, and substantially amends the Bank Holding Company Act, which prior to GLBA limited the ability of bank holding companies to engage in the securities and insurance businesses. To achieve this purpose, GLBA created a new type of company, the “financial holding company.” A financial holding company may engage in or acquire companies that engage in a broad range of financial services, including

| | • | | securities activities such as underwriting, dealing, brokerage, investment and merchant banking; and |

| | • | | insurance underwriting, sales and brokerage activities. |

6

A bank holding company may elect to become a financial holding company only if all of its depository institution subsidiaries are well-capitalized, well-managed and have at least a satisfactory CRA rating. While the Bank meets these criteria, the Company has not elected to be treated as a financial holding company.

GLBA established a system of functional regulation under which the federal banking agencies regulate the banking activities of financial holding companies and banks’ financial subsidiaries, the Securities and Exchange Commission (“SEC”) regulates their securities activities, and state insurance regulators will regulate their insurance activities.

GLBA and certain regulations issued by federal banking agencies also provide protection against the transfer and use by financial institutions of consumers’ nonpublic personal information. A financial institution must provide to its customers, at the beginning of the customer relationship and annually thereafter, the institution’s policies and procedures regarding the handling of customers’ nonpublic personal financial information. The privacy provisions generally prohibit a financial institution from providing a customer’s personal financial information to unaffiliated third parties unless the institution discloses to the customer that the information may be so provided and the customer is given the opportunity to opt out of such disclosure.

Neither the provisions of GLBA nor the Act’s implementing regulations have had a material impact on the Company’s or the Bank’s regulatory capital ratios (as discussed above) or ability to continue to operate in a safe and sound manner.

USA PATRIOT ACT OF 2001

In October, 2001, the USA Patriot Act of 2001 was enacted in response to the terrorist attacks in New York, Pennsylvania and Northern Virginia, which occurred on September 11, 2001. The Patriot Act is intended to strengthen U.S. law enforcements’ and the intelligence communities’ abilities to work cohesively to combat terrorism on a variety of fronts. The continuing and potential impact of the USA Patriot Act and related regulations and policies on financial institutions of all kinds is significant and wide ranging. The USA Patriot Act contains sweeping anti-money laundering and financial transparency laws, and imposes various regulations, including standards for verifying client identification at account opening, and rules to promote cooperation among financial institutions, regulators and law enforcement entities in identifying parties that may be involved in terrorism or money laundering.

CHECK 21

On October 28, 2003, President Bush signed into law the Check Clearing for the 21st Century Act, also known as Check 21. Check 21 gives “substitute checks,” such as a digital image of a check, and copies made from that image, the same legal standing as the original paper check. Some of the major provisions of Check 21 include:

| | • | | allowing check truncation without making it mandatory; |

| | • | | demanding that every financial institution communicate to accountholders in writing a description of its substitute check processing program and their rights under the law; |

| | • | | legalizing substitutions for and replacements of paper checks without agreement from consumers; |

| | • | | retaining the previously mandated electronic collection and return of checks between financial institutions only when individual agreements are in place; |

| | • | | requiring that when accountholders request verification, financial institutions produce the original check (or a copy that accurately represents the original) and demonstrate that the account debit was accurate and valid; and |

| | • | | requiring reaccrediting of funds to an individual’s account on the next business day after a consumer proves that the financial institution has erred. |

7

This legislation will likely affect bank capital spending as many financial institutions assess whether technological or operational changes are necessary to stay competitive and take advantage of the new opportunities presented by Check 21.

REPORTING OBLIGATIONS UNDER SECURITIES LAWS

The Company is subject to the periodic reporting requirements of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), including the filing of annual, quarterly and other reports with the SEC. As an Exchange Act reporting company, the Company is directly affected by the Sarbanes-Oxley Act of 2002 and regulations promulgated thereunder by the SEC, which are aimed at improving corporate governance and reporting procedures. The Company is complying with the rules and regulations implemented pursuant to the Sarbanes-Oxley Act and intends to comply with any applicable rules and regulations implemented in the future.

ITEM 1A: RISK FACTORS

Not required.

ITEM 1B: UNRESOLVED STAFF COMMENTS

Not required.

ITEM 2: PROPERTIES

The Company, through its subsidiaries, owns or leases buildings that are used in the normal course of business. The main office is located at 100 South Main Street, Kilmarnock, Virginia, in a building owned by the Company. The Company’s subsidiaries own various other offices in the counties or towns in which they operate.

Unless otherwise noted, the properties listed below are owned by the Company and its subsidiaries as of December 31, 2007.

| | |

| Corporate Headquarters: | | 100 South Main Street, Kilmarnock, Virginia |

| |

| Bank of Lancaster: | | 100 South Main Street, Kilmarnock, Virginia |

| | 708 Rappahannock Drive, White Stone, Virginia |

| | 432 North Main Street, Kilmarnock, Virginia |

| | 4935 Richmond Road, Warsaw, Virginia |

| | 15648 Kings Highway, Montross, Virginia |

| | 6941 Northumberland Highway, Heathsville, Virginia |

| | 18 Sandy Street, Callao, Virginia |

| | 23 West Church Street, Kilmarnock, Virginia |

| | 15104 Northumberland Highway, Burgess, Virginia (construction in progress) |

| |

| Bay Trust Company: | | 1 North Main Street, Kilmarnock, Virginia |

| | 15648 Kings Highway, Montross, Virginia |

ITEM 3: LEGAL PROCEEDINGS

In the ordinary course of its operations, the Company is a party to various legal proceedings. Based upon information currently available, management believes that such legal proceedings, in the aggregate, will not have a material adverse effect on the business, financial condition, or results of operations of the Company.

8

ITEM 4: SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

There were no matters submitted to a vote of security holders during the fourth quarter of the year-ended December 31, 2007.

PART II

ITEM 5: MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

The Company’s common stock trades on the OTC Bulletin Board under the symbol “BAYK” and transactions generally involve a small number of shares. There were 2,363,917 shares of the Company’s stock outstanding at the close of business on December 31, 2007, which were held by 701 shareholders of record.

The following table summarizes the high and low closing sales prices and dividends declared for the two years ended December 31, 2007.

| | | | | | | | | | | | | | | | | | |

| | | Market Values | | | | |

| | | 2007 | | 2006 | | Declared Dividends |

| | | High | | Low | | High | | Low | | 2007 | | 2006 |

First Quarter | | $ | 14.99 | | $ | 14.25 | | $ | 15.00 | | $ | 13.35 | | $ | 0.165 | | $ | 0.16 |

Second Quarter | | | 15.25 | | | 13.90 | | | 15.40 | | | 13.40 | | | 0.165 | | | 0.16 |

Third Quarter | | | 14.75 | | | 13.00 | | | 14.75 | | | 13.60 | | | 0.165 | | | 0.16 |

Fourth Quarter | | | 14.00 | | | 12.15 | | | 15.23 | | | 14.00 | | | 0.17 | | | 0.165 |

A discussion of certain restrictions and limitations on the ability of the Bank to pay dividends to the Company and the ability of the Company to pay dividends on its common stock, is set forth in Part I, Business, of this Form 10-K under the heading “Supervision and Regulation.”

The dividend amount on the Company’s common stock is established by the Board of Directors on a quarterly basis with dividends paid on a quarterly basis. In making its decision on the payment of dividends on the Company’s common stock, the Board considers operating results, financial condition, capital adequacy, regulatory requirements, shareholder return, and other factors.

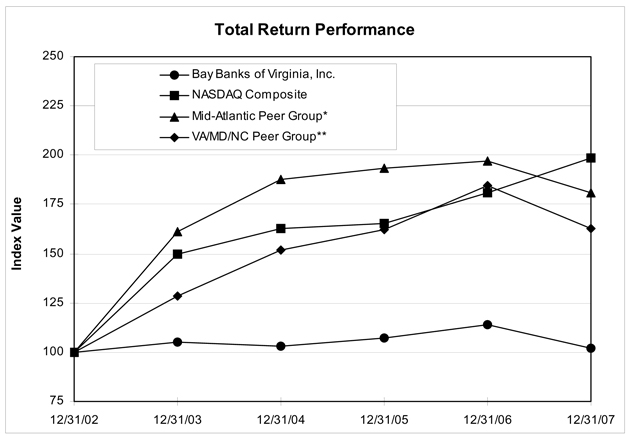

Stock Performance Graph

The graph and table below compares the cumulative total shareholder return on the Company’s common stock with the cumulative total return on the NASDAQ Stock Market Composite Index and two peer group indices, the “Mid-Atlantic Peer Group Index” and the “VA/MD/NC Peer Group Index.” The Mid-Atlantic Peer Group Index includes banks from the SNL Securities Mid-Atlantic Bank Index (the “SNL Index”) with less than $500 million in total assets. The SNL Index is a published industry index of financial institutions located in the Mid-Atlantic states of Delaware, Maryland, New Jersey, New York, Pennsylvania, and Washington D.C. The Mid-Atlantic Peer Group Index is a subset of the SNL Index, and includes only those financial institutions with less than $500 million in total assets. The VA/MD/NC Peer Group Index includes publicly traded banks in the states of Virginia, Maryland, and North Carolina, with less than $500 million in total assets. Each index shown provides a market capitalization weighted measure of total return for the five year period ended December 31, 2007, assuming that an investment of $100 was made on December 31, 2002 and dividends were reinvested. The comparisons in the graph below are based upon historical data and are not indicative of, nor intended to forecast, future performance of the Company’s stock.

9

Total Return Performance

Bay Banks of Virginia, Inc.

| | | | | | | | | | | | |

| | | Period Ending |

Index | | 12/31/02 | | 12/31/03 | | 12/31/04 | | 12/31/05 | | 12/31/06 | | 12/31/07 |

Bay Banks of Virginia, Inc. | | 100.00 | | 105.34 | | 103.03 | | 107.03 | | 113.81 | | 101.80 |

NASDAQ Composite | | 100.00 | | 150.01 | | 162.89 | | 165.13 | | 180.85 | | 198.60 |

Mid-Atlantic Peer Group* | | 100.00 | | 161.22 | | 187.84 | | 193.33 | | 196.83 | | 180.93 |

VA/MD/NC Peer Group** | | 100.00 | | 128.25 | | 151.96 | | 162.26 | | 184.79 | | 162.86 |

| * | Mid-Atlantic Peer Group consists of 104 Mid-Atlantic Banks with Assets <$500 million. |

| ** | VA/MD/NC Peer Group consists of 93 publicly traded banks in Virginia (VA), Maryland (MD), and North Carolina (NC), with $500 million or less in total assets. |

10

The Company began a share repurchase program in August of 1999 and has continued the program into 2007. The combined plans authorize the repurchase of 180,000 shares.

| | | | | | | | | |

| | | Total Number

of Shares

Purchased | | Average

Price Paid

per Share | | Total Number of Shares Purchased

as Part of Publicly Announced

Plans or Programs | | Maximum Number of Shares

that May Yet Be Purchased

Under the Plans or Programs |

October, 2007 | | 400 | | $ | 14.25 | | 400 | | 85,928 |

November, 2007 | | — | | | — | | — | | 85,928 |

December, 2007 | | 1,700 | | | 13.57 | | 1,700 | | 84,228 |

| | | | | | | | | |

Total | | 2,100 | | $ | 13.70 | | 2,100 | | |

| | | | | | | | | |

ITEM 6: SELECTED FINANCIAL DATA

Not required.

ITEM 7: MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion provides information about the major components of the results of operations and financial condition, liquidity and capital resources of Bay Banks of Virginia, Inc., and its subsidiaries. This discussion and analysis should be read in conjunction with the Consolidated Financial Statements and Notes to Consolidated Financial Statements presented in Item 8, Financial Statements and Supplementary Data, in this Form 10-K.

EXECUTIVE SUMMARY

Interest margins were management’s primary challenge in 2007. The yield curve had been flat to inverted for nearly two years before it started to show signs of a positive slope in the fourth quarter. A related consequence of the flat yield curve was increased competition for deposits, causing deposit rates to rise, and the Bank’s cost of funds to rise as a result. At the same time, market rates on loans remained essentially unchanged, causing compression on the Bank’s margin. So, although interest income grew as a result of increased loan balances, interest expense grew faster because of higher deposit rates. The consequence of these effects was that net interest income, the Company’s major source of revenue, ended up shrinking slightly.

Management did several things in 2007 to mitigate the effects of margin compression on the Company’s net earnings. Efforts were made to grow the types of loans that earn higher rates. Time deposits were taken on shorter maturities, so that when deposit competition returns to a more normal level and rates start to fall, the Bank would be able to renew these deposits at lower rates. This is actually happening as of the date of this report.

Below the net interest income line, management made efforts to improve non-interest income and control non-interest expense. The Score-to-Win program was launched to promote growth in checking accounts and use of the Bank’s more cost-efficient service channels, like Online Advantage and receipt of account statements electronically through eVue Advantage. Score-to-Win awards points for debit card usage which can be redeemed for merchandise. The program also awards bonus points for opening a checking account with a Check-N-Advantage debit card, and for adding Online Advantage, eVue Advantage, online bill-pay, and a savings account. Increased interchange income has been the result of the related increase in debit card usage.

Another new product introduction in 2007 was eDeposit. This allows customers who deposit large numbers of checks to make their deposits remotely via a secure internet connection.

In the non-interest expense area, management has controlled salaries and benefits expense by restructuring responsibilities among existing employees as attrition has occurred. Delays in capital expenditures, with their related depreciation expense, have been deferred for non-mission-critical projects.

11

However, management remains focused on growth, and believes investments made in technology and related infrastructure over the last several years will allow this growth to reap benefits sooner than might otherwise be expected.

We have previously discussed the issue of subprime loans, which surfaced in early 2007, and their impact on lenders and homebuilders. Let us reiterate that we anticipate no direct impact to our Bank and minimal, if any, to homebuilders served by the Bank. We follow a formal set of guidelines and controls in our lending process, and both the Bank and area homebuilders serve a public steeped in a tradition of honoring its obligations. It has always been our philosophy to plan long term for our customers and investors, rather than allowing short to intermediate term influences alter our steady and measured growth policy.

CRITICAL ACCOUNTING POLICIES

GENERAL. The Company’s financial statements are prepared in accordance with accounting principles generally accepted in the United States (“GAAP”). The financial information contained within our statements is, to a significant extent, financial information that is based on measures of the financial effects of transactions and events that have already occurred. A variety of factors could affect the ultimate value that is obtained either when earning income, recognizing an expense, recovering an asset or relieving a liability. We use historical loss factors as one factor in determining the inherent loss that may be present in our loan portfolio. Actual losses could differ significantly from the historical factors that we use. In addition, GAAP itself may change from one previously acceptable method to another method. Although the economics of our transactions would be the same, the timing of events that would impact our transactions could change.

ALLOWANCE FOR LOAN LOSSES. The allowance for loan losses is an estimate of the losses that may be sustained in our loan portfolio. The allowance is based on two basic principles of accounting: (1) Statement of Financial Accounting Standards (“SFAS”) No. 5,Accounting for Contingencies, which requires that losses be accrued when they are probable of occurring and estimable and (2) SFAS No. 114,Accounting by Creditors for Impairment of a Loan, which requires that losses be accrued based on the differences between the value of collateral, present value of future cash flows or values that are observable in the secondary market and the loan balance. The use of these values is inherently subjective and our actual losses could be greater or less than the estimates.

The allowance for loan losses is increased by charges to income and decreased by charge-offs (net of recoveries). Management’s periodic evaluation of the adequacy of the allowance is based on past loan loss experience, known and inherent risks in the portfolio, adverse situations that may affect the borrower’s ability to repay, the estimated value of any underlying collateral, and current economic conditions.

OVERVIEW

2007 Compared to 2006

Bay Banks of Virginia, Inc. recorded earnings for 2007 of $1,808,602, or $0.76 per basic and diluted share, as compared to 2006 earnings of $2,328,745 and $0.98 per basic and diluted share. This is a decrease in net income of 22.3% as compared to 2006. Net interest income for 2007 decreased 0.4% to $10,746,824, as compared to $10,788,049 for 2006. Non-interest income for 2007, before net securities gains, was $3,053,730 as compared to 2006 non-interest income, before net securities gains, of $3,087,580, a decrease of 1.1%. Non-interest expenses increased 4.5% to $11,053,209, as compared to 2006 non-interest expenses of $10,575,140.

Performance as measured by the Company’s return on average assets (“ROA”) was 0.6% for the year ended December 31, 2007 compared to 0.8% for 2006. Performance as measured by return on average equity (“ROE”) was 6.8% for the year ended December 31, 2007, compared to 8.8% for 2006.

12

Return on Equity & Assets

| | | | | | | | |

Years Ended December 31, | | 2007 | | | 2006 | |

Net Income | | $ | 1,808,602 | | | $ | 2,328,745 | |

Average Total Assets | | $ | 318,611,401 | | | $ | 305,971,002 | |

Return on Assets | | | 0.6 | % | | | 0.8 | % |

| | |

Average Equity | | $ | 26,406,060 | | | $ | 26,531,452 | |

Return on Equity | | | 6.8 | % | | | 8.8 | % |

| | |

Dividends declared per share | | $ | 0.665 | | | $ | 0.645 | |

Average Shares Outstanding | | | 2,368,611 | | | | 2,370,901 | |

Average Diluted Shares Outstanding | | | 2,370,045 | | | | 2,375,339 | |

Net Income per Share | | $ | 0.76 | | | $ | 0.98 | |

Net Income per Diluted Share | | $ | 0.76 | | | $ | 0.98 | |

Dividend Payout Ratio | | | 87.1 | % | | | 65.7 | % |

Average Equity to Assets Ratio | | | 8.3 | % | | | 8.7 | % |

RESULTS OF OPERATIONS

Net Interest Income

The principal source of earnings for the Company is net interest income. Net interest income is the amount by which interest income exceeds interest expense. The net interest margin is net interest income expressed as a percentage of interest earning assets. Changes in the volume and mix of interest earning assets and interest bearing liabilities, the associated yields and rates, and the volume of non-performing assets have a significant impact on net interest income, the net interest margin, and net income.

Net interest income, on a fully tax equivalent basis, which reflects the tax benefits of nontaxable interest income, was $11.1 million in 2007 and $11.2 million in 2006. This represents a negligible decrease in net interest income of 0.5% for 2007 as compared to 2006.

The Company’s net interest margin decreased to 3.73% for 2007 as compared to 3.90% for 2006. The yield on earning assets increased to 6.75% for 2007 as compared to 6.51% for 2006. The cost of interest-bearing liabilities increased to 3.61% for 2007 as compared to 3.16% for 2006. Average earning assets increased 4.2% to $298.5 million for 2007 as compared to $286.5 million for 2006. Average interest bearing liabilities increased to $249.5 million in 2007 as compared to $235.9 million in 2006.

13

Average Balances, Income and Expenses, Yields and Rates

| | | | | | | | | | | | | | | | | | |

| (Fully taxable equivalent basis) | | Average Balances, Income and Expense, Yields and Rates | |

| Years ended December 31, | | 2007 | | | 2006 | |

| (Dollars in Thousands) | | Average

Balance | | Income/

Expense | | Yield/

Rate | | | Average

Balance | | Income/

Expense | | Yield/

Rate | |

INTEREST EARNING ASSETS: | | | | | | | | | | | | | | | | | | |

Taxable Investments | | $ | 21,042 | | $ | 1,037 | | 4.93 | % | | $ | 22,029 | | $ | 1,043 | | 4.73 | % |

Tax-Exempt Investments (1) | | | 19,697 | | | 1,114 | | 5.65 | % | | | 19,835 | | | 1,145 | | 5.77 | % |

| | | | | | | | | | | | | | | | | | |

Total Investments | | | 40,739 | | | 2,151 | | 5.28 | % | | | 41,864 | | | 2,188 | | 5.23 | % |

| | | | | | |

Gross Loans (2) | | | 252,925 | | | 17,745 | | 7.02 | % | | | 241,668 | | | 16,315 | | 6.75 | % |

Interest-bearing Deposits | | | 260 | | | 15 | | 5.77 | % | | | 154 | | | 10 | | 6.18 | % |

Federal Funds Sold | | | 4,589 | | | 228 | | 4.97 | % | | | 2,807 | | | 128 | | 4.55 | % |

| | | | | | | | | | | | | | | | | | |

Total Interest Earning Assets | | $ | 298,513 | | $ | 20,139 | | 6.75 | % | | $ | 286,493 | | $ | 18,641 | | 6.51 | % |

| | | | | | |

INTEREST-BEARING LIABILITIES: | | | | | | | | | | | | | | | | | | |

Savings Deposits | | $ | 54,374 | | $ | 1,656 | | 3.05 | % | | $ | 58,324 | | $ | 1,682 | | 2.88 | % |

NOW Deposits | | | 37,105 | | | 394 | | 1.06 | % | | | 40,531 | | | 325 | | 0.80 | % |

Time Deposits => $100,000 | | | 41,213 | | | 1,966 | | 4.77 | % | | | 32,835 | | | 1,413 | | 4.30 | % |

Time Deposits < $100,000 | | | 65,044 | | | 2,904 | | 4.46 | % | | | 65,706 | | | 2,634 | | 4.01 | % |

Money Market Deposit Accounts | | | 17,079 | | | 525 | | 3.07 | % | | | 14,605 | | | 320 | | 2.19 | % |

| | | | | | | | | | | | | | | | | | |

Total Deposits | | $ | 214,815 | | $ | 7,445 | | 3.47 | % | | $ | 212,001 | | $ | 6,374 | | 3.01 | % |

| | | | | | |

Federal Funds Purchased | | $ | 642 | | $ | 36 | | 5.61 | % | | $ | 1,251 | | $ | 71 | | 5.69 | % |

Securities Sold Under Repurchase Agreements | | | 5,982 | | | 228 | | 3.81 | % | | | 5,778 | | | 232 | | 4.02 | % |

FHLB Advances | | | 28,105 | | | 1,306 | | 4.65 | % | | | 16,877 | | | 785 | | 4.65 | % |

| | | | | | | | | | | | | | | | | | |

Total Interest-Bearing Liabilities | | $ | 249,544 | | $ | 9,015 | | 3.61 | % | | $ | 235,907 | | $ | 7,462 | | 3.16 | % |

| | | | | | |

Net Yield on Earning Assets | | | | | $ | 11,124 | | 3.73 | % | | | | | $ | 11,179 | | 3.90 | % |

Notes:

(1)-Income and yield is tax-equivalent assuming a federal tax rate of 34%

(2)-Includes Visa credit card program, nonaccrual loans, and fees.

From year-end 2006 to year-end 2007, loan balances grew 6.1% and deposit balances increased 3.2%. Loan growth was primarily composed of single-family residential adjustable-rate mortgages and construction loans secured by real estate. Increases in deposits were due mainly due to time deposits, even though savings and demand deposit balances declined. The balance sheet is liability sensitive, which management believes is favorable in the current rate environment.

The marketplace experienced significant competition for deposits in 2007, creating a need to increase deposit rates, mainly for time deposits, and causing the average cost of interest-bearing deposits to increase. The Company has also experienced a shift in the mix of deposits from lower-rate savings and demand deposits to higher-rate time deposits, which has also contributed to the increased cost of interest-bearing liabilities.

On the asset side, adjustable-rate mortgages (ARM) continue to reprice upward, providing increases in interest income and the corresponding average yield on loans, which is up to 7.02% in 2007 from 6.75% in 2006.

Overall, the increase in the average yield on earning assets has not been sufficient to offset the increase in the average cost of interest-bearing liabilities, causing the net interest margin to decrease to 3.73% in 2007 from 3.90% in 2006. Management expects the current falling rate environment to provide relief to the cost of interest-bearing liabilities in 2008, and therefore to improve the net interest margin.

14

Volume and Rate Analysis of Changes in Net Interest Income

| | | | | | | | | | | | |

Years Ended December 31, | | 2007 vs. 2006

Increase (Decrease)

Due to Changes in: | |

| |

| (Dollars in Thousands) | | Volume (1) | | | Rate (1) | | | Total | |

Earning Assets: | | | | | | | | | | | | |

Taxable investments | | $ | (49 | ) | | $ | 43 | | | $ | (6 | ) |

Tax-exempt investments (2) | | | (7 | ) | | | (24 | ) | | | (31 | ) |

Gross Loans | | | 736 | | | | 694 | | | | 1,430 | |

Interest-bearing deposits | | | 4 | | | | 1 | | | | 5 | |

Federal funds sold | | | 87 | | | | 13 | | | | 100 | |

| | | | | | | | | | | | |

Total earning assets | | $ | 771 | | | $ | 727 | | | $ | 1498 | |

| | | |

Interest-Bearing Liabilities: | | | | | | | | | | | | |

NOW checking | | $ | (31 | ) | | $ | 100 | | | $ | 69 | |

Savings deposits | | | (126 | ) | | | 100 | | | | (26 | ) |

Money market accounts | | | 57 | | | | 148 | | | | 205 | |

Certificates of deposit < $100,000 | | | (40 | ) | | | 310 | | | | 270 | |

Certificates of deposit >= $100,000 | | | 387 | | | | 166 | | | | 553 | |

Federal funds purchased | | | (33 | ) | | | (2 | ) | | | (35 | ) |

Securities sold under repurchase agreements | | | 8 | | | | (12 | ) | | | (4 | ) |

FHLB advances | | | 523 | | | | (2 | ) | | | 521 | |

| | | | | | | | | | | | |

Total interest-bearing liabilities | | $ | 745 | | | $ | 808 | | | $ | 1553 | |

Change in net interest income | | $ | 26 | | | $ | (81 | ) | | $ | (55 | ) |

| | | | | | | | | | | | |

Notes:

| (1) | Changes caused by the combination of rate and volume are allocated based on the percentage caused by each. |

| (2) | Income and yields are reported on a tax-equivalent basis, assuming a federal tax rate of 34%. |

Interest Sensitivity

Earnings performance and the maintenance of sufficient liquidity depend on careful management of the interest sensitivity gap. The interest sensitivity gap is the difference between interest sensitive assets and interest sensitive liabilities in a specific time interval. The interest sensitivity gap can be managed by repricing variable-rate assets or liabilities, by replacing an asset or liability at maturity or by adjusting the interest rate during the life of the asset or liability. By managing the volume of assets and liabilities that mature or reprice in various time intervals, the Company can manage interest rate risk and minimize the impact of rising or falling rates.

The Company employs a variety of measurement techniques to identify and manage its exposure to changing interest rates and subsequent changes in liquidity. The Company utilizes a simulation model that estimates interest income volatility and interest rate risk. In addition, the Company utilizes an Asset Liability Committee (the “ALCO”) composed of appointed members from management and the Board of Directors. Through the use of simulation, the ALCO reviews the overall magnitude of interest rate risk and then formulates policy with which to manage asset growth and pricing, funding sources and pricing, and off-balance sheet commitments. These decisions are based on management’s expectations regarding future interest rate movements, economic conditions both locally and nationally, and other business and risk factors.

Non-Interest Income

Total non-interest income decreased by $59 thousand, or 1.9%, in 2007 as compared to 2006. Of that $59 thousand total decrease, secondary market lending fees decreased $38 thousand. Securities gains decreased by $25 thousand.

15

However, other service charges and fees increased by $75 thousand, or 5.7%. This is comprised of the VISA program, which contributed $77 thousand to this increase, ATM interchange income, which contributed $46 thousand to this increase, and the Investment Advantage program, which reduced the increase by $58 thousand. The increase in ATM interchange income is related to increased debit card usage by the Bank’s customers, which is attributable to the Score-to-Win program. This program awards points for debit card usage, which can be redeemed for various merchandise. Secondary market lending fees decreased 17.2% to $183 thousand in 2007 from $221 thousand in 2006. These fees are generated when a loan is sold into the secondary market. When the Bank is evaluating a potential loan, many factors influence the determination of whether that loan will be sold or held in the Bank’s own portfolio, including the size of the desired loan, the term, the rate, the structure and management’s intention to grow the Bank’s loan portfolio or not. The Bank originates both secondary market and portfolio loans. Loans are sold into the secondary market both with servicing retained and released.

Non-Interest Expense

During 2007, total non-interest expenses increased 4.5%, to $11.1 million from $10.6 million in 2006. Non-interest expenses are comprised of salaries and benefits, occupancy expense, state bank franchise tax, Visa program expense, telephone expense and other operating expenses.

Salaries and benefits expense continues to be the major component of non-interest expenses. Salaries and benefits expense increased 4.4% to $6.0 million in 2007, as compared to $5.7 million in 2006. This increase is the result of additional personnel hired in preparation for the planned branch expansions into Burgess and Colonial Beach, plus planned growth in commercial lending, Investment Advantage, and Bay Trust Company. As attrition has occurred, management has restructured responsibilities wherever possible to avoid unnecessary hiring.

Occupancy expense increased 2.1% to $1.8 million in 2007, as compared to $1.7 million in 2006. Bank franchise tax expense increased 10.4% to $196 thousand in 2007 as compared to $177 thousand for 2006. Expenses related to the VISA program increased by 11.9% to $608 thousand in 2007 as compared to $543 thousand for 2006. However, when considering the non-interest income generated by the VISA program, its net positive contribution to the Company was $136 thousand in 2007, up $30 thousand from 2006. Telephone expense increased 0.8% to $192 thousand in 2007 as compared to $190 thousand for 2006. Other expense increased by 4.8%, to $2.3 million, as compared to 2006. Management continues its program of identifying variable expenses that can be reduced or eliminated, especially in light of expected increases in fixed costs related to branch expansion in 2008.

Income Taxes

Income tax expense in 2007 was $640 thousand and $872 thousand in 2006. Income tax expense corresponds to an effective rate of 26.2% and 27.4% for the two years ended December 31, 2007 and 2006, respectively. Note 13 to the Consolidated Financial Statements provides reconciliation between the amounts of income tax expense computed using the federal statutory income tax rate and actual income tax expense. Also included in Note 13 to the Consolidated Financial Statements is information regarding deferred taxes for 2007 and 2006.

Loans

Per the following table, loan production remained positive during 2007, with balances growing by 6.1% to $259.8 million as of December 31, 2007, compared to December 31, 2006 balances of $244.8 million. Loans secured by real estate represent the largest category, comprising 89.1% of the loan portfolio at December 31, 2007. Of these balances, 1-4 family residential loans grew by $9.0 million, or 6.6%, other real estate loans grew by $8.3 million, or 25.5%, but construction loans decreased by $2.3 million, or 4.8%. Although commercial loan balances increased by $176 thousand, or 1.0%, they were 7.0% of total loans at year-end 2007 as compared to 7.4% at year-end 2006. Consumer installment and other loans increased by $408 thousand, or 4.3% in 2007.

16

Types of Loans

| | | | | | | | | | | | |

Years ended December 31, | | 2007 | | | 2006 | |

(Dollars in thousands) | | | | | | | | | | | | |

Commercial | | $ | 18,254 | | 7.0 | % | | $ | 18,078 | | 7.4 | % |

Real Estate – Construction | | | 45,698 | | 17.6 | % | | | 47,977 | | 19.6 | % |

Real Estate – Mortgage | | | 185,883 | | 71.6 | % | | | 169,194 | | 69.1 | % |

Installment and Other (includes Visa program) | | | 9,922 | | 3.8 | % | | | 9,514 | | 3.9 | % |

| | | | | | | | | | | | |

Total | | $ | 259,757 | | 100.0 | % | | $ | 244,763 | | 100.0 | % |

| | | | | | | | | | | | |

Notes: | | | | | | | | | | | | |

| | | | |

Deferred loan costs and fees not included. | | | | | | | | | | | | |

Allowance for loan losses not included. | | | | | | | | | | | | |

Loan Maturity Schedule of Selected Loans

as of December 31, 2007

| | | | | | | | | | | | | | | | | | |

| | | One Year or Less | | One to Five Years | | Over Five Years |

| (Dollars in Thousands) | | Fixed Rate | | Variable Rate | | Fixed Rate | | Variable Rate | | Fixed Rate | | Variable Rate |

Commercial | | $ | 2,096 | | $ | 10,554 | | $ | 3,717 | | $ | 620 | | $ | 1,267 | | $ | — |

Real Estate – Construction | | | 3,084 | | | 8,305 | | | 23,522 | | | — | | | 10,787 | | | — |

Real Estate – Mortgage | | | 3,103 | | | 77,634 | | | 11,424 | | | 80,256 | | | 13,389 | | | 77 |

Installment and Other | | | 2,592 | | | 1,093 | | | 6,055 | | | — | | | 181 | | | — |

| | | | | | | | | | | | | | | | | | |

Totals | | $ | 10,875 | | $ | 97,586 | | $ | 44,718 | | $ | 80,876 | | $ | 25,624 | | $ | 77 |

Notes:

Loans with immediate repricing are shown in the ‘One Year or Less’ category.

Variable rate loans are categorized based on their next repricing date.

Deferred loan costs and fees are not included

Asset Quality-Provision and Allowance for Loan Losses

The provision for loan losses is a charge against earnings that is necessary to maintain the allowance for loan losses at a level consistent with management’s evaluation of the loan portfolio’s inherent risk. The allowance for loan losses is analyzed for adequacy on a quarterly basis to determine the required amount of provision. A loan-by-loan review is conducted on all adversely classified loans. Inherent losses on these individual loans are determined and these losses are compared to historical loss data for each loan type. Management then reviews the various analyses and determines the appropriate allowance. As of December 31, 2007, management considered the allowance for loan losses to be a reasonable estimate of potential loss exposure inherent in the loan portfolio.

17

Allowance for Loan Losses

| | | | | | | | |

Years Ended December 31, | | 2007 | | | 2006 | |

(Dollars in Thousands) | | | | | | | | |

Balance, beginning of period | | $ | 2,235 | | | $ | 2,157 | |

| | |

Loans charged off: | | | | | | | | |

Commercial | | $ | — | | | $ | — | |

Real estate - construction | | | — | | | | — | |

Real estate - mortgage | | | (106 | ) | | | (19 | ) |

Installment & Other (including Visa program) | | | (104 | ) | | | (66 | ) |

| | | | | | | | |

Total loans charged off | | $ | (210 | ) | | $ | (85 | ) |

| | | | | | | | |

Recoveries of loans previously charged off: | | | | | | | | |

Commercial | | $ | — | | | $ | — | |

Real estate - construction | | | — | | | | — | |

Real estate - mortgage | | | — | | | | — | |

Installment & Other (including Visa program) | | | 24 | | | | 38 | |

| | | | | | | | |

Total recoveries | | $ | 24 | | | $ | 38 | |

| | | | | | | | |

Net charge offs | | $ | (186 | ) | | $ | (47 | ) |

| | |

Provision for loan losses | | | 298 | | | | 125 | |

| | |

Balance, end of period | | $ | 2,347 | | | $ | 2,235 | |

| | | | | | | | |

Average loans outstanding during the period | | $ | 252,925 | | | $ | 241,668 | |

| | | | | | | | |

Ratio of net charge-offs during the period to average loans outstanding during the period | | | 0.07 | % | | | 0.02 | % |

| | | | | | | | |

Management maintains a list of loans that have potential weakness that may need special attention. Such loans are monitored and used in the determination of the sufficiency of the Company’s allowance for loan losses. As of December 31, 2007, the allowance for loan losses was $2.3 million or 0.9% of total loans as compared to $2.2 million or 0.9% as of December 31, 2006.

Allocation of the Allowance for Loan Losses

| | | | | | | | | | | | |

| Years Ended December 31, | | 2007 | | | 2006 | |

| (Dollars in Thousands) | | Allocation of Allowance | | | Allocation of Allowance | |

Commercial | | $ | 434 | | 18.5 | % | | $ | 553 | | 24.8 | % |

Real estate - construction | | | 251 | | 10.7 | % | | | 279 | | 12.5 | % |

Real estate - mortgage | | | 1,006 | | 42.8 | % | | | 990 | | 44.3 | % |

Installment & Other | | | 216 | | 9.2 | % | | | 276 | | 12.3 | % |

Unallocated | | | 440 | | 18.7 | % | | | 137 | | 6.1 | % |

| | | | | | | | | | | | |

Total | | $ | 2,347 | | 100.0 | % | | $ | 2,235 | | 100.0 | % |

18

Nonperforming Assets

As of December 31, 2007, nonperforming assets as a percentage of total loans and other real estate owned (“OREO”) was 0.8%, up from year-end 2006, but still low compared to industry averages. Other real estate owned, including foreclosed property, at year-end 2007 increased to $795 thousand from $562 thousand at year-end 2006. This figure represents two properties, one commercial real estate and one residential real estate. After foreclosure, management periodically performs valuations and the real estate is carried at the lower of carrying amount or fair value less cost to sell. Management expects a net gain on the combined sales of these properties. The increase in non-accrual loans represents a conservative approach to the application of related accounting standards taken in the fourth quarter. Since December 31, 2007, $776 thousand of the $1.3 million shown in the following table has been cleared.

Non-Performing Assets

| | | | | | | | |

(Dollars in Thousands) Years ended December 31, | | 2007 | | | 2006 | |

Non-accrual Loans | | $ | 1,295 | | | $ | 239 | |

Restructured Loans | | | — | | | | — | |

Foreclosed Properties | | | 795 | | | | 562 | |

| | | | | | | | |

Total Non-performing Assets | | $ | 2,090 | | | $ | 801 | |

| | | | | | | | |

Loans past due 90+ days as to principal or interest payments & accruing interest | | $ | 1,052 | | | $ | 1,069 | |

| | | | | | | | |

Allowance for Loan Losses | | $ | 2,347 | | | $ | 2,235 | |

| | | | | | | | |

Non-Performing Assets to Total Loans and OREO | | | 0.8 | % | | | 0.3 | % |

Allowance to Total Loans and OREO | | | 0.9 | % | | | 0.9 | % |

Allowance to Non-Performing Assets | | | 1.12 | | | | 2.79 | |

Securities

As of December 31, 2007, investment securities totaled $44.1 million, an increase of 13.5% as compared to 2006 year-end balances of $38.8 million. As an alternative to Federal Funds Sold, the Company held $8.0 million in auction rate securities at December 31, 2007. The increase in the investment portfolio balance was due mainly to the increase in auction rate securities.

The Company classifies the majority of the investment portfolio as available-for-sale in order that it may be considered a source of liquidity, if necessary. Securities available for sale are carried at fair market value, with after-tax market value gains or losses disclosed as an “unrealized” component of shareholder’s equity entitled “Accumulated other comprehensive income (loss).” As a result, other comprehensive income is impacted by rising or falling interest rates. As the market value of a fixed income investment will increase as interest rates fall, it will also decline as interest rates rise. The after tax unrealized gains or losses are recorded as a portion of other comprehensive income (loss) in the equity of the Company, but have no impact on earnings until such time as the investment is sold, or “realized.” As of December 31, 2007, the Company had accumulated other comprehensive gains net of deferred tax related to securities available-for-sale of $39 thousand as compared to losses of $175 thousand at year-end 2006.

The investment portfolio shows a net unrealized gain of $59 thousand on December 31, 2007, compared to a net unrealized loss of $265 thousand on December 31, 2006. This is due to the market forces in the fourth quarter of 2007, which drove up the prices of high quality debt securities. The unfortunate consequence of this market is that it makes the acquisition of additional securities unattractive, as their interest rates are now relatively lower.

19

The Company seeks to diversify its securities portfolio to minimize risk and to maintain a majority of its portfolio in securities issued by states and political subdivisions due to the tax benefits such securities provide. The Company owns no derivatives, and participates in no hedging activities.

For more information on the Company’s investment portfolio, please refer to Note 3 of the Consolidated Financial Statements, included in Item 8 of this Form 10-K.

| | | | | | | | | | | | | | | | | | | | |

| (Dollars in Thousands) | | One Year or

Less or No

Maturity | | | One to Five

Years | | | Five to Ten

Years | | | Over Ten

Years | | | Total | |

U.S. Government and Agencies: | | | | | | | | | | | | | | | | | | | | |

Book Value | | $ | 2,004 | | | $ | 5,697 | | | $ | 71 | | | $ | — | | | $ | 7,772 | |

Market Value | | $ | 1,999 | | | $ | 5,723 | | | $ | 67 | | | $ | — | | | $ | 7,789 | |

Weighted average yield | | | 3.98 | % | | | 4.50 | % | | | 4.01 | % | | | 0.00 | % | | | 4.36 | % |

States and Municipal Obligations: | | | | | | | | | | | | | | | | | | | | |

Book Value | | $ | 11,221 | | | $ | 17,558 | | | $ | 4,078 | | | $ | 1,179 | | | $ | 34,036 | |

Market Value | | $ | 11,212 | | | $ | 17,638 | | | $ | 4,050 | | | $ | 1,172 | | | $ | 34,072 | |

Weighted average yield | | | 5.26 | % | | | 5.30 | % | | | 5.29 | % | | | 5.58 | % | | | 5.30 | % |

Corporate Bonds: | | | | | | | | | | | | | | | | | | | | |

Book Value | | $ | 0 | | | $ | 0 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Market Value | | $ | 0 | | | $ | 0 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Weighted average yield | | | 0.00 | % | | | 0.00 | % | | | 0.00 | % | | | 0.00 | % | | | 0.00 | % |

Other Securities: | | | | | | | | | | | | | | | | | | | | |

Book Value | | $ | — | | | $ | — | | | $ | — | | | $ | 2,223 | | | $ | 2,223 | |

Market Value | | $ | — | | | $ | — | | | $ | — | | | $ | 2,223 | | | $ | 2,223 | |

Weighted average yield | | | 0.00 | % | | | 0.00 | % | | | 0.00 | % | | | 5.89 | % | | | 5.89 | % |

Total Securities: | | | | | | | | | | | | | | | | | | | | |

Book Value | | $ | 13,225 | | | $ | 23,255 | | | $ | 4,149 | | | $ | 3,402 | | | $ | 44,031 | |

Market Value | | $ | 13,211 | | | $ | 23,361 | | | $ | 4,117 | | | $ | 3,395 | | | $ | 44,084 | |

Weighted average yield | | | 5.06 | % | | | 5.11 | % | | | 5.27 | % | | | 5.78 | % | | | 5.16 | % |

Notes: | | | | | | | | | | | | | | | | | | | | |

|

Yields on tax-exempt securities have been computed on a tax-equivalent basis. | |

Average yields on securities held for sale are based on amortized cost. | | | | | |

Deposits

As of December 31, 2007, total deposits increased 3.1% to $259.6 million as compared to year-end 2006 deposits of $251.6 million. Non-interest bearing demand deposits decreased 13.0%, while time deposits increased 15.0%, demonstrating a mix shift to more costly deposits. This is a trend that has continued from 2006 and intensified in 2007 due to the highly competitive market for deposits.

20

Average Deposits & Rates

| | | | | | | | | | | | |

Years Ended December 31, (Thousands) | | 2007 | | | 2006 | |

| | Average

Balance | | Yield/

Rate | | | Average

Balance | | Yield/

Rate | |

Non-interest bearing Demand Deposits | | $ | 40,827 | | 0.00 | % | | $ | 41,853 | | 0.00 | % |

| | | | |

Interest bearing Deposits: | | | | | | | | | | | | |

NOW Accounts | | $ | 37,105 | | 1.06 | % | | $ | 40,531 | | 0.80 | % |

Regular Savings | | | 54,374 | | 3.05 | % | | | 58,324 | | 2.88 | % |

Money Market Deposit Accounts | | | 17,079 | | 3.07 | % | | | 14,605 | | 2.19 | % |

Time Deposits: | | | | | | | | | | | | |

CD’s $100,000 or more | | | 41,213 | | 4.77 | % | | | 32,835 | | 4.30 | % |

CD’s less than $100,000 | | | 65,045 | | 4.47 | % | | | 65,706 | | 4.01 | % |

| | | | | | | | | | | | |

Total Interest bearing Deposits | | $ | 214,816 | | 3.47 | % | | $ | 212,001 | | 3.01 | % |

| | | | |

Total Average Deposits | | $ | 255,643 | | 2.91 | % | | $ | 253,854 | | 2.51 | % |

| | | | | | | | | | | | |

Maturity Schedule of Time Deposits of $100,000 and over

As of December 31, 2007

| | | |

(Thousands) | | | |

3 months or less | | $ | 16,229 |

3-6 months | | | 8,404 |

6-12 months | | | 12,891 |

Over 12 months | | | 9,825 |

| | | |

Totals | | $ | 47,349 |

| | | |

CAPITAL RESOURCES

Capital resources represent funds, earned or obtained, over which a financial institution can exercise greater long-term control in comparison with deposits and borrowed funds. The adequacy of the Company’s capital is reviewed by management on an ongoing basis with reference to size, composition, and quality of the Company’s resources and consistency with regulatory requirements and industry standards. Management seeks to maintain a capital structure that will assure an adequate level of capital to support anticipated asset growth and to absorb potential losses, yet allow management to effectively leverage its capital to maximize return to shareholders.

The Company is required to maintain minimum amounts of capital to total “risk weighted” assets, as defined by Federal Reserve Capital Guidelines. According toCapital Guidelines for Bank Holding Companies, the Company is required to maintain a minimum Total Capital to Risk Weighted Assets ratio of 8.0%, a Tier 1 Capital to Risk Weighted Assets ratio of 4.0% and a Tier 1 Capital to Adjusted Average Assets ratio (Leverage ratio) of 4.0%. As of December 31, 2007, the Company maintained these ratios at 10.8%, 9.8%, and 7.6%, respectively. At year-end 2006, these ratios were 11.4%, 10.5%, and 8.1%, respectively.

Total capital, before accumulated other comprehensive loss, increased 2.7% to $27.1 million as of year-end 2007 as compared to $26.4 million at year-end 2006. Accumulated other comprehensive loss was $350 thousand at year-end 2007, down 63.3% from a loss of $954 thousand at year-end 2006, mainly due to the effect of SFAS No. 158, Defined Benefit Pension and Other Postretirement Plans. The Company accounts for other comprehensive income in the investment portfolio by adjusting capital for any after tax effect of unrealized gains and losses on securities at the end of a given accounting period.

21

LIQUIDITY

Liquidity represents an institution’s ability to meet present and future financial obligations through either the sale or maturity of existing assets or the acquisition of additional funds through liability management. Liquid assets include cash, interest-bearing deposits with other banks, Federal Funds Sold and investments and loans maturing within one year. The Company’s ability to obtain deposits and purchase funds at favorable rates determines its liquidity. Management believes that the Company maintains overall liquidity that is sufficient to satisfy its depositors’ requirements and to meet its customers’ credit needs.

At December 31, 2007, liquid assets totaled $37.0 million or 11.3% of total assets. Additional sources of liquidity available to the Company include its capacity to borrow additional funds when necessary. The Bank maintains Federal Funds lines with regional banks totaling approximately $19.0 million. In addition, the subsidiary Bank has a line of credit with the Federal Home Loan Bank of Atlanta totaling approximately $65.0 million, with $35.0 million available.

The impact of contractual obligations is limited to three FHLB advances, one for $10 million, which matures in May of 2011, one for $15 million, which matures in September of 2016 and one for $5 million, which matures in May of 2011. For details on theses advances, please refer to Note 11 of the Consolidated Financial Statements in Item 8 of this Form 10-K.

OFF BALANCE SHEET COMMITMENTS

In the normal course of business, the Company offers various financial products to its customers to meet their credit and liquidity needs. These instruments frequently involve elements of liquidity, credit and interest rate risk in excess of the amount recognized in the Consolidated Balance Sheets. The Company’s exposure to credit loss in the event of nonperformance by the other party to the financial instruments for commitments to extend credit and standby-letters of credit is represented by the contractual amount of these instruments. Subject to its normal credit standards and risk monitoring procedures, the Company makes contractual commitments to extend credit. Commitments generally have fixed expiration dates or other termination clauses and may require payment of a fee. Since many of the commitments may expire without being completely drawn upon, the total commitment amounts do not necessarily represent future cash requirements. Conditional commitments are issued by the Company in the form of performance stand-by letters of credit, which guarantee the performance of a customer to a third-party. The credit risk of issuing letters of credit is essentially the same as that involved in extending loan facilities to customers.

Off Balance Sheet Arrangements

| | | | | | |

December 31, | | 2007 | | 2006 |

(Dollars in Thousands) | | | | | | |

Total Loan Commitments Outstanding | | $ | 41,085 | | $ | 41,289 |

Standby-by Letters of Credit | | | 550 | | | 860 |

The Company maintains liquidity and credit facilities with non-affiliated banks in excess of the total loan commitments and stand-by letters of credit. As these commitments are earning assets only upon takedown of the instrument by the customer, thereby increasing loan balances, management expects the revenue of the Company to be enhanced as these credit facilities are utilized.

STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This report contains statements concerning the Company’s expectations, plans, objectives, future financial performance and other statements that are not historical facts. These statements may constitute “forward-looking statements” as defined by federal securities laws. These statements may address issues that involve estimates and assumptions made by management, risks and uncertainties, and actual results could differ materially from historical results or those anticipated by such statements. Factors that could have a material adverse effect on the operations and future prospects of the Company include, but are not limited to, changes in: interest rates, general economic

22

conditions, the legislative/regulatory climate, monetary and fiscal policies of the U.S. Government, including policies of the U.S. Treasury and the Federal Reserve Board, the quality or composition of the loan or investment portfolios, demand for loan products, deposit flows, competition, demand for financial services in the Company’s market area and accounting principles, policies and guidelines. These risks and uncertainties should be considered in evaluating the forward-looking statements contained herein, and readers are cautioned not to place undue reliance on such statements, which speak only as of the date they are made.

ITEM 7A: QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Not required.

23

ITEM 8: FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

CONSOLIDATED BALANCE SHEETS

December 31, 2007 and 2006

| | | | | | | | |

| | | 2007 | | | 2006 | |

ASSETS | | | | | | | | |

Cash and due from banks | | $ | 5,015,762 | | | $ | 6,320,951 | |

Interest-bearing deposits | | | 375,008 | | | | 148,436 | |

Federal funds sold | | | 1,392,554 | | | | 4,636,278 | |

Securities available for sale, at fair value | | | 43,618,174 | | | | 38,393,648 | |

Securities held to maturity at amortized cost (fair value, $465,896 and $430,594) | | | 471,371 | | | | 457,091 | |

Loans, net of allowance for loan losses of $2,347,244 and $2,235,544 | | | 258,164,836 | | | | 243,372,412 | |

Premises and equipment, net | | | 10,783,844 | | | | 10,317,498 | |

Accrued interest receivable | | | 1,478,442 | | | | 1,418,214 | |

Other real estate owned | | | 795,054 | | | | 561,745 | |

Goodwill | | | 2,807,842 | | | | 2,807,842 | |

Other assets | | | 1,360,963 | | | | 1,258,970 | |

| | | | | | | | |

Total assets | | $ | 326,263,850 | | | $ | 309,693,085 | |

| | | | | | | | |

LIABILITIES | | | | | | | | |

Noninterest-bearing deposits | | $ | 38,476,633 | | | $ | 44,246,563 | |

Savings and interest-bearing demand deposits | | | 106,727,807 | | | | 107,915,874 | |

Time deposits | | | 114,363,000 | | | | 99,485,144 | |

| | | | | | | | |

Total deposits | | $ | 259,567,440 | | | $ | 251,647,581 | |

| | |

Federal Funds purchased and securities sold under repurchase agreements | | $ | 8,365,313 | | | $ | 5,248,876 | |

Federal Home Loan Bank advances | | | 30,000,000 | | | | 25,000,000 | |

Other liabilities | | | 1,258,234 | | | | 1,428,744 | |

Commitments and contingencies | | | — | | | | — | |

| | | | | | | | |

Total liabilities | | $ | 299,190,987 | | | $ | 283,325,201 | |

| | | | | | | | |

SHAREHOLDERS’ EQUITY | | | | | | | | |

Common stock ($5 par value; authorized - 5,000,000 shares; outstanding - 2,363,917 and 2,374,727 shares, respectively) | | $ | 11,819,583 | | | $ | 11,873,633 | |

Additional paid-in capital | | | 4,643,827 | | | | 4,722,592 | |

Retained Earnings | | | 10,959,793 | | | | 10,726,121 | |

Accumulated other comprehensive (loss), net | | | (350,340 | ) | | | (954,462 | ) |

| | | | | | | | |

Total shareholders’ equity | | $ | 27,072,863 | | | $ | 26,367,884 | |

| | | | | | | | |

Total liabilities and shareholders’ equity | | $ | 326,263,850 | | | $ | 309,693,085 | |

| | | | | | | | |

See Notes to Consolidated Financial Statements.

24

| | | | | | |

CONSOLIDATED STATEMENTS OF INCOME | | | | | | |

| Years Ended December 31, | | 2007 | | 2006 |

Interest Income | | | | | | |

Loans, including fees | | $ | 17,745,278 | | $ | 16,314,713 |

Securities: | | | | | | |

Taxable | | | 1,052,243 | | | 1,052,493 |

Tax-exempt | | | 734,853 | | | 755,463 |

Federal funds sold | | | 228,461 | | | 127,704 |

| | | | | | |

Total interest income | | $ | 19,760,835 | | $ | 18,250,373 |

| | | | | | |

Interest Expense | | | | | | |

Deposits | | $ | 7,444,739 | | $ | 6,373,352 |

Federal funds purchased | | | 35,821 | | | 71,175 |

Securities sold under repurchase agreements | | | 227,851 | | | 232,494 |

FHLB advances | | | 1,305,600 | | | 785,303 |

| | | | | | |

Total interest expense | | $ | 9,014,011 | | $ | 7,462,324 |