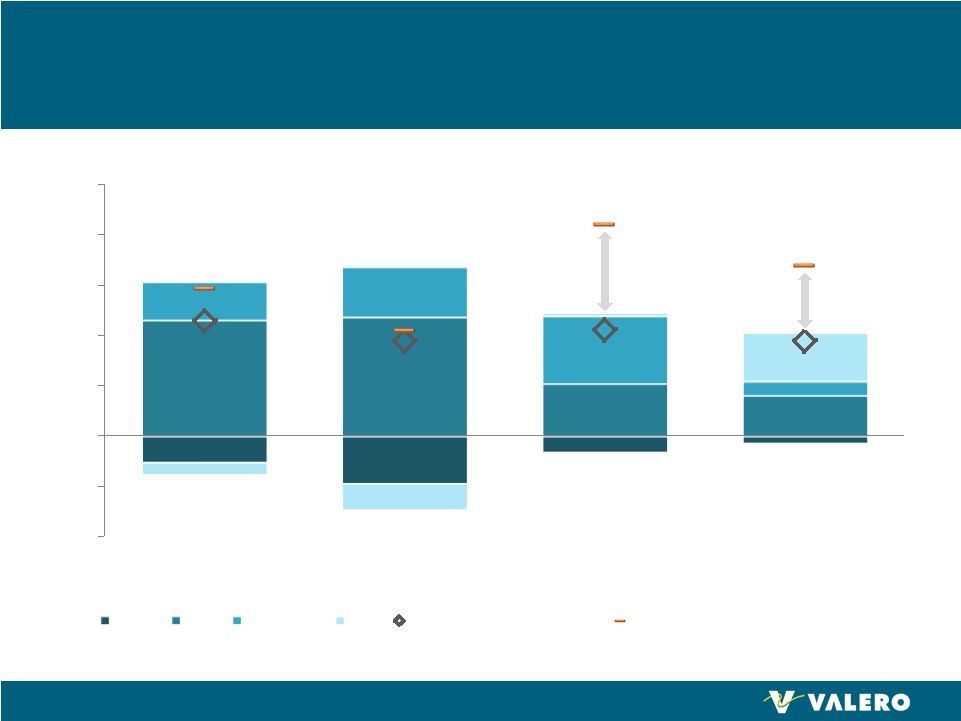

30 Non-GAAP Disclosures We define EBITDA as net income before income tax expense, interest expense, and depreciation expense. We define distributable cash flow as EBITDA less cash payments during the period for interest, income taxes, and maintenance capital expenditures, plus adjustments related to minimum throughput commitments, capital projects prefunded by Valero, and certain other items. We define coverage ratio as the ratio of distributable cash flow to the total distribution declared. EBITDA, distributable cash flow, and coverage ratio are supplemental financial measures that are not defined under GAAP. They may be used by management and external users of our financial statements, such as industry analysts, investors, lenders, and rating agencies, to: • describe our expectation of forecasted earnings; • assess our operating performance as compared to other publicly traded limited partnerships in the transportation and logistics industry, without regard to historical cost basis or, in the case of EBITDA, financing methods; • assess the ability of our business to generate sufficient cash to support our decision to make distributions to our unitholders; • assess our ability to incur and service debt and fund capital expenditures; and • assess the viability of acquisitions and other capital expenditure projects and the returns on investment of various investment opportunities. We believe that the presentation of EBITDA provides useful information to investors in assessing our financial condition and results of operations. The GAAP measures most directly comparable to EBITDA are net income and net cash provided by operating activities. EBITDA should not be considered an alternative to net income or net cash provided by operating activities presented in accordance with GAAP. EBITDA has important limitations as an analytical tool because it excludes some, but not all, items that affect net income or net cash provided by operating activities. EBITDA should not be considered in isolation or as a substitute for analysis of our results as reported under GAAP. Additionally, because EBITDA may be defined differently by other companies in our industry, our definition of EBITDA may not be comparable to similarly titled measures of other companies, thereby diminishing its utility. We use distributable cash flow to measure whether we have generated from our operations, or “earned,” an amount of cash sufficient to support the payment of the minimum quarterly distributions. Distributable cash flow is not necessarily indicative of the actual cash we have on hand to distribute or that we are required to distribute. We use the distribution coverage ratio to reflect the relationship between our distributable cash flow and the total distribution declared. |