UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 13D

Under the Securities Exchange Act of 1934

(Amendment No. 1)*

| The Hartford Financial Services Group, Inc. |

(Name of Issuer)

| Common Stock |

(Title of Class of Securities)

| 416515104 |

(CUSIP Number)

Stuart L. Merzer General Counsel & Chief Compliance Officer Paulson & Co. Inc. 1251 Avenue of the Americas New York, New York 10020 (212) 956-2221 |

with a copy to:

Scott J. Davis

Mayer Brown LLP

71 S. Wacker Drive

Chicago, IL 60606

(312) 701-7311

(Name, Address and Telephone Number of Person Authorized to Receive Notices and Communications)

| March 9, 2012 |

(Date of Event which Requires Filing of this Statement)

If the filing person has previously filed a statement on Schedule 13G to report the acquisition that is the subject of this Schedule 13D, and is filing this schedule because of §§240.13d-1(e), 240.13d-1(f) or 240.13d-1(g), check the following box. ¨

Note: Schedules filed in paper format shall include a signed original and five copies of the schedule, including all exhibits. See §240.13d-7 for other parties to whom copies are to be sent.

| * | The remainder of this cover page shall be filled out for a reporting person’s initial filing on this form with respect to the subject class of securities, and for any subsequent amendment containing information which would alter disclosures provided in a prior cover page. |

The information required on the remainder of this cover page shall not be deemed to be “filed” for the purpose of Section 18 of the Securities Exchange Act of 1934 (“Act”) or otherwise subject to the liabilities of that section of the Act but shall be subject to all other provisions of the Act (however, see the Notes).

| CUSIP No. 416515104 |

| 1. | Names of Reporting Persons.

Paulson & Co. Inc. | |||||

| 2. | Check the Appropriate Box if a Member of a Group (See Instructions) (a) ¨ (b) x

| |||||

| 3. | SEC Use Only:

| |||||

| 4. | Source of Funds (See Instructions):

AF | |||||

| 5. | Check if Disclosure of Legal Proceedings Is Required Pursuant to Items 2(d) or 2(e):

| |||||

| 6. | Citizenship or Place of Organization:

State of Delaware | |||||

Number of Shares Beneficially by Owned by Each Reporting Person With | 7. | Sole Voting Power:

37,540,676 (See Notes 1 and 2 to Item 5 below) | ||||

| 8. | Shared Voting Power:

None | |||||

| 9. | Sole Dispositive Power:

37,540,676 (See Notes 1 and 2 to Item 5 below) | |||||

| 10. | Shared Dispositive Power:

None | |||||

11. | Aggregate Amount Beneficially Owned by Each Reporting Person: 37,540,676 (See Notes 1 and 2 to Item 5 below)

| |||||

12. | Check if the Aggregate Amount in Row (11) Excludes Certain Shares (See Instructions): ¨

| |||||

13. | Percent of Class Represented by Amount in Row (11): 8.5% (See Note 3 to Item 5 below)

| |||||

14. | Type of Reporting Person (See Instructions):

IA | |||||

| Item 1. | Security and Issuer |

This Amendment No. 1 amends the Schedule 13D filed on February 14, 2012 by Paulson & Co. Inc. (the “Original Filing”), relating to the common stock (“Common Stock”) and warrants to purchase Common Stock expiring June 26, 2019 (“Warrants”) of The Hartford Financial Services Group, Inc., a Delaware corporation (the “Issuer”). Capitalized terms not defined herein shall have the meanings given to them in the Original Filing.

| Item 4. | Purpose of Transaction |

Item 4 of the Original Filing is hereby amended by adding the following:

As part of the Reporting Person’s continuing discussions or communications with the Issuer’s management, board of directors and shareholders, and public statements, relating to the Issuer’s possible spin-off of its property and casualty insurance business, the Reporting Person has used the presentation filed herewith.

| Item 5. | Interest in Securities of the Issuer |

Item 5 of the Original Filing is hereby amended and restated in its entirety as follow:

(a) Amount beneficially owned: 37,540,676 (See Notes 1 and 2)

Percent of class: 8.5% (See Note 3)

(b) Number of shares of Common Stock and number of Warrants as to which the Reporting Person has:

| (i) | Sole power to vote or direct the vote: 37,540,676 (See Notes 1 and 2) |

| (ii) | Share power to vote or direct the vote: 0 |

| (iii) | Sole power to dispose or direct disposition of: 37,540,676 (See Notes 1 and 2) |

| (iv) | Shared power to dispose or direct the disposition of: 0 |

(c) The following table sets forth all transactions with respect to the Common Stock of the Issuer effected since February 14, 2012, the date of the Original Filing, inclusive of any transactions effected through 5:00 p.m., New York City time, on March 8,2012. All such transactions were effected in the open market.

Purchase and sale transactions for the same quantities of shares on a given day typically reflect rebalancing of positions among the various Funds based on their relative capital levels, which may change from time to time.

Date of Transaction | Amount of Securities | Price Per Share | Type of Transaction | |||

| 3/6/12 | 156,247 | $19.4147 | Sell | |||

| 3/6/12 | 156,247 | $19.4300 | Buy |

| (d) | Not applicable. |

| (e) | Not applicable. |

Note 1: The amount listed consists of 37,470,676 shares of Common Stock and 70,000 Warrants. In addition, the Funds currently hold cash-settled swaps positions relating to an additional 221,424 shares of Common Stock and 3,251,000 Warrants, but because neither the Reporting Person nor the Funds have any power to vote, to direct the vote, to dispose or to direct the disposition of the shares of Common Stock and Warrants that its counterparty may hold in connection with such swaps positions, such shares of Common Stock and Warrants are not included in the amount listed in Item 5.

3 of 5

Note 2: The Reporting Person, an investment advisor that is registered under the Investment Advisers Act of 1940, furnishes investment advice to and manages the Funds. In its role as investment advisor, or manager, the Reporting Person possesses voting and/or investment power over the securities of the Issuer described in this schedule that are owned by the Funds. All securities reported in this schedule are owned by the Funds. The Reporting Person disclaims beneficial ownership of such securities.

Note 3: The percentages reported in this Amendment No. 1 are based upon 440,237,475 shares of Common Stock outstanding as of February 17, 2012 (as reported in the Annual Report on Form 10-K filed by the Issuer on February 24, 2012).

| Item 7. | Material to Be Filed as Exhibits |

The following document is filed as an exhibit:

EXHIBIT IV: Presentation dated March 9, 2012.

4 of 5

SIGNATURE

After reasonable inquiry and to the best of my knowledge and belief, I certify that the information set forth in this statement is true, complete and correct.

Dated: March 9, 2012

| PAULSON & CO. INC. | ||

| By: | /s/ Stuart L. Merzer | |

| Name: | Stuart L. Merzer | |

| Title: | General Counsel & Chief Compliance Officer | |

INC. & CO. PAULSON HARTFORD Spin-Off of P&C Business Would Increase Shareholder Value By 60% Investment Management 1251 Avenue of the Americas New York, NY 10020 Phone: (212) 956-2221 Fax: (212) 977-9505 www.paulsonco.com March 9, 2012 CONFIDENTIAL |

PAULSON & CO. INC. 1 LEGAL DISCLAIMER This document does not constitute an offer to sell or a solicitation of an offer to buy any securities, and may not be relied upon in connection with any offer or sale of securities. This document should be read in conjunction with, and is qualified in its entirety by, information appearing in the Confidential Private Offering Memorandum (and a Limited Partnership Agreement for domestic partnerships), which should be carefully reviewed prior to investing. Certain statements included herein may constitute forward-looking statements, including, but not limited to, those identified by the expressions “expect”, “intend”, “will” and similar expressions to the extent they relate to the investment vehicles discussed herein. The forward-looking statements are not historical facts but reflect Paulson & Co’s current expectations regarding future results or events. These forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations. Although Paulson & Co believes that the assumptions inherent in the forward-looking statements are reasonable, forward-looking statements are not guarantees of future performance and, accordingly, readers are cautioned not to place undue reliance on such statements due to the inherent uncertainty therein. Paulson & Co undertakes no obligation to update publicly or otherwise revise any forward-looking statement or information whether as a result of new information, future events or other such factors which affect this information, except as required by law. An investment in a hedge fund is speculative and involves a high degree of risk, which each investor must carefully consider. An investor in hedge funds could lose all or a substantial amount of his or her investment. Returns generated from an investment in a hedge fund may not adequately compensate investors for the business and financial risks assumed. While hedge funds are subject to market risks common to other types of investments, including market volatility, hedge funds employ certain trading techniques, such as the use of leveraging and other speculative investment practices that may increase the risk of investment loss. Products may involve above-average risk. Risks associated with hedge fund investments include, but are not limited to, the fact that hedge funds can be highly illiquid; they are not required to provide periodic pricing or valuation information to investors; they may involve complex tax structures and delays in distributing important tax information; they are not subject to the same regulatory requirements as mutual funds; they often charge higher fees and the high fees may offset the funds’ trading profits; they may have a limited operating history; they can have performance that is volatile; they may have a fund manager who has total trading authority over the fund and the use of a single adviser applying generally similar trading programs could mean a lack of diversification, and consequentially, higher risk; they may not have a secondary market for an investor’s interest in the fund and none may be expected to develop; they may have restrictions on transferring interests in the fund; and may effect a substantial portion of their trades on foreign exchanges. All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. |

PAULSON & CO. INC. 2 HARTFORD P&C: THE CROWN JEWEL OF HARTFORD FINANCIAL SERVICES 200 year old P&C company Dominant commercial P&C franchise Serving high-margin small businesses Largest consumer affinity business: AARP Exclusive endorsement 40mm members Strong management: CEO Doug Elliot But buried within Hartford Financial Services All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. |

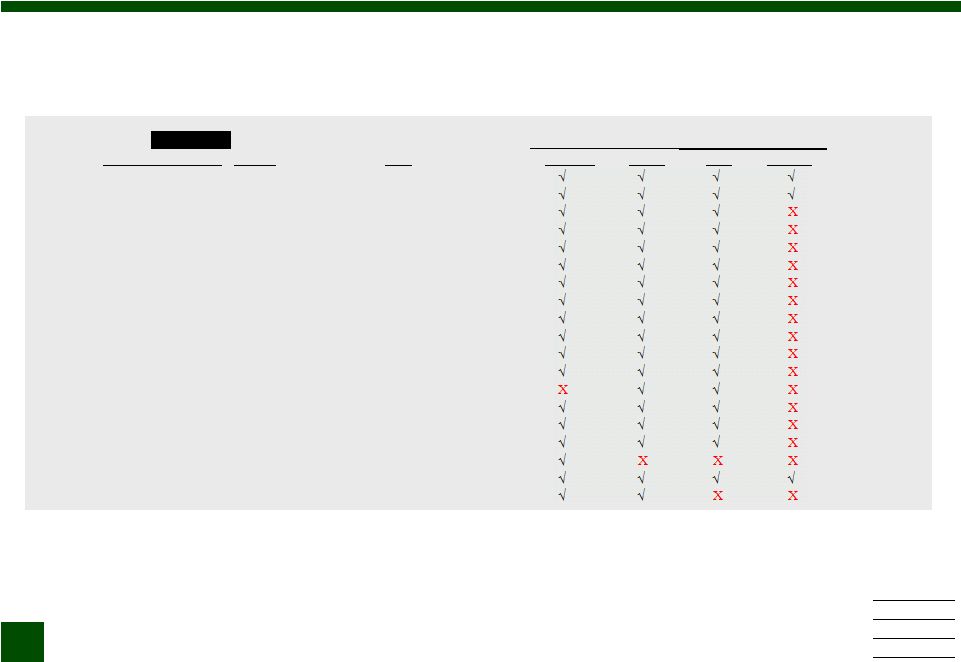

PAULSON & CO. INC. 3 BECAUSE HARTFORD P&C IS BURIED WITHIN HIG, FEW P&C ANALYSTS COVER IT. OF THE 19 P&C ANALYSTS, ONLY 3 COVER HARTFORD. P&C Covers: Inst. Investor Ranking Analyst Bank HIG Life 1) Jay Cohen BAC X 2) Jay Gelb Barclays 3) Matt Heimermann JPM X X RU Keith Walsh Citi X X RU Josh Shanker DB X X RU Brian Meredith UBS X X Vinay Misquith Evercore X X Michael Nannizzi GS X X Larry Greenberg Janney Montgomery X X Cliff Gallant KBW X X Alan Zimmermann Macquarie X X Greg Locraft MS X X Michael Grasher Piper Jaffray X X Mark Dwelle RBC X X Paul Newsome Sandler O'Neil X X Josh Stirling Sanford Bernstein X X Dan Farrell Sterne Agee X X Michael Paisan Stifel X Adam Klauber Wiilliam Blair X X All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. |

PAULSON & CO. INC. 4 P&C Covers: Inst. Investor Ranking Analyst Bank Travelers Chubb ACE Hartford 1) Jay Cohen BAC 2) Jay Gelb Barclays 3) Matt Heimermann JPM RU Keith Walsh Citi RU Josh Shanker DB RU Brian Meredith UBS Vinay Misquith Evercore Michael Nannizzi GS Larry Greenberg Janney Montgomery Cliff Gallant KBW Alan Zimmermann Macquarie Greg Locraft MS Michael Grasher Piper Jaffray Mark Dwelle RBC Paul Newsome Sandler O'Neil Josh Stirling Sanford Bernstein Dan Farrell Sterne Agee Michael Paisan Stifel Adam Klauber Wiilliam Blair WHILE ONLY 3 OF 19 P&C ANALYSTS COVER HARTFORD, 18 COVER TRAVELERS, 18 COVER CHUBB, AND 17 COVER ACE All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. |

PAULSON & CO. INC. 5 Buy ratings: ACE Travelers Chubb Hartford 15 13 8 1 P&C ANALYSTS ARE BULLISH ON THE P&C SECTOR. ACE HAS 15 BUY RECOMMENDATIONS, TRAVELERS HAS 13, CHUBB HAS 8. HARTFORD HAS ONLY 1. All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. |

PAULSON & CO. INC. 6 HARTFORD IS VIEWED AS A LIFE COMPANY AND IS COVERED BY LIFE ANALYSTS. OF THE 15 LIFE ANALYSTS WHO COVER HARTFORD , ONLY 3 ALSO COVER ITS P&C PEERS .. Life Covers: Inst. Investor Ranking Analyst Bank HIG P&C 1) Jimmy Bhullar JPM X 2) Andrew Kligerman UBS X 3) Tom Gallagher CS X RU Suneet Kamath Sanford Bernstein X RU Ed Spehar BAC X RU Nigel Dally MS X Alan Devlin Altantic Equities Mark Finklestein Evercore X Randy Binner FBR Chris Giovanni GS X Bob Glasspiegal Janney Montgomery X Jeff Schuman KBW X Eric Berg RBC X Ed Shields Sandler O'Neil X X John Nadel Sterne Agee X John Hall Wells Fargo All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. |

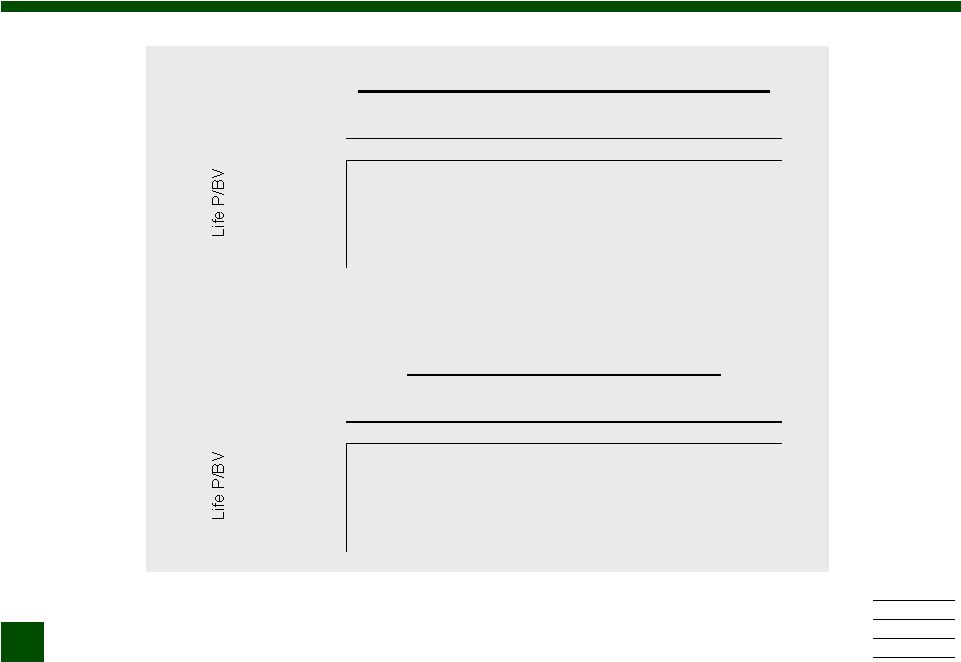

7 HARTFORD TRADES AT A HUGE DISCOUNT TO P&C PEERS: 45% OF BOOK VALUE COMPARED 102% FOR P&C PEERS (1) As of March 7, 2012. 0.45x 0.91x 0.98x 1.02x 1.18x 0.00x 0.20x 0.40x 0.60x 0.80x 1.00x 1.20x 1.40x PAULSON & CO. INC. All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. |

PAULSON & CO. INC. 8 (1) Average of core earnings estimates by BAC, Barclays, JPM, UBS, CS & MS. (2) (3) Average P&C peer multiple for Hartford P&C. LNC multiple for Hartford Life. (4) 2012 (1) If-quoted value 4Q11 Core If-quoted Implied BV ex AOCI Earnings ROE P/BV (3) P/E Total Per share P&C 9,851 817 Net debt (2) (2,200) (94) Corp. other (4) 508 8 Net 8,159 731 8.6% 1.02x 10.2x 8,322 16.20 Life 15,003 1,148 Net debt (2) (3,000) (214) Corp. other (4) 1,036 8 Net 13,039 941 7.0% 0.60x 8.4x 7,864 15.31 P&C + Life 21,197 1,672 7.6% 0.76x 9.7x 16,186 31.51 Diluted shares 514 Share price as of 7-Mar-12 19.49 Upside 62% P&C net debt consists of $2.5bn gross debt and $300mm cash, Life net debt consists of $4.3bn gross debt and $1.3bn cash. Assumes Corporate excluding debt and cash is allocated 50/50 between P&C and Life. Assumes $528mm discount for Allianz jr. sub debt added back to Life Corporate. A SPINOFF OF P&C WOULD UNLOCK SIGNIFICANT VALUE. IF P&C AND LIFE WERE SEPARATED, WE BELIEVE THE COMBINED VALUE WOULD BE APPROXIMATELY $31, A 62% INCREASE All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. |

9 BASED ON VARIOUS P/BV MULTIPLES, THE TOTAL VALUE CREATED FROM A SPINOFF COULD RANGE FROM 40-70% Potential Values Based on Different P/BV Multiples P&C P/BV 32 0.90x 1.00x 1.10x 1.20x 0.40x 25.20 26.59 27.99 29.43 0.50x 27.42 28.85 30.29 31.73 0.60x 29.71 31.15 32.59 34.02 0.70x 32.01 33.45 34.86 36.25 0.80x 34.30 35.69 37.09 38.49 Upside Based on 7-Mar-12 Share Price P&C P/BV 0 0.90x 1.00x 1.10x 1.20x 0.40x 29% 36% 44% 51% 0.50x 41% 48% 55% 63% 0.60x 52% 60% 67% 75% 0.70x 64% 72% 79% 86% 0.80x 76% 83% 90% 97% All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. PAULSON & CO. INC. |

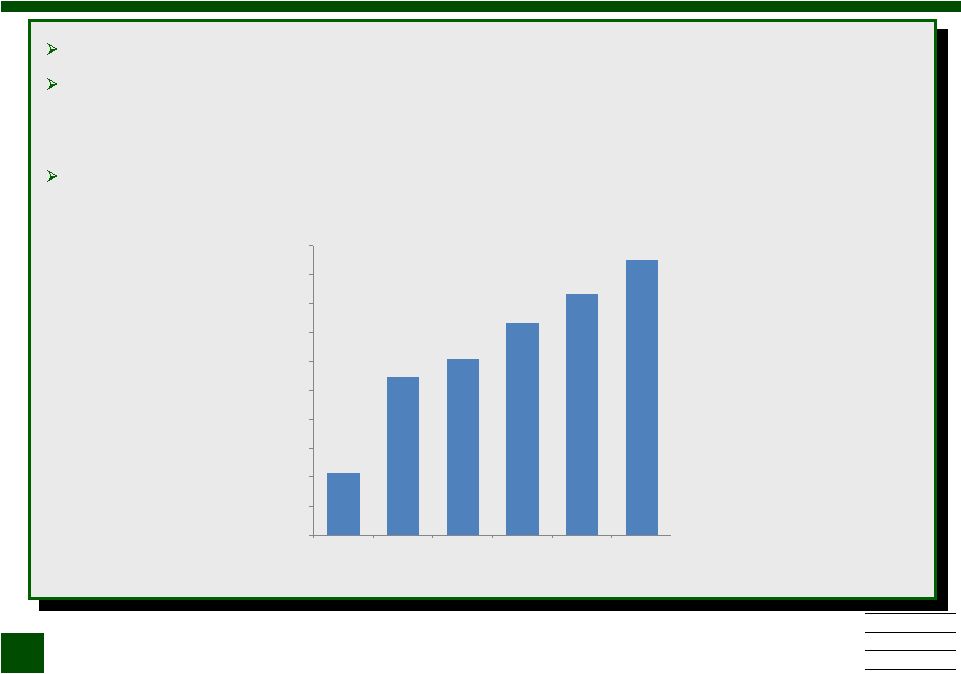

10 VALUE MAXIMIZATION The most important single value creating option is to split P&C from Life Additional value can be created by optimizing its balance sheet to pay down debt, divesting high value businesses like mutual funds, and cutting costs and freeing capital through a VA runoff. By successfully pursuing these actions, Hartford can achieve a peer level multiple P / BV: 0.43x 0.58x 0.60x 0.66x 0.71x 0.76x $19 $26 $27 $30 $32 $34+ $15 $17 $19 $21 $23 $25 $27 $29 $31 $33 $35 Statuos quo Spin off P&C Optimize balance sheet Sell MF & Inst. Annuity VA in runoff Separate runoff from other Life All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. PAULSON & CO. INC. |

PAULSON & CO. INC. 11 SPINOFF IMPLEMENTATION Hartford could contribute P&C into a debt-free Newco Newco could raise new low-cost debt ($2.5bn, 5 - 10 year maturities, 2.5% average coupon) Debt proceeds could be used to repurchase existing debt Remaining existing debt would stay with HIG (which would hold the Life businesses after the spin-off of P&C) Dividend Newco to HIG shareholders All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. |

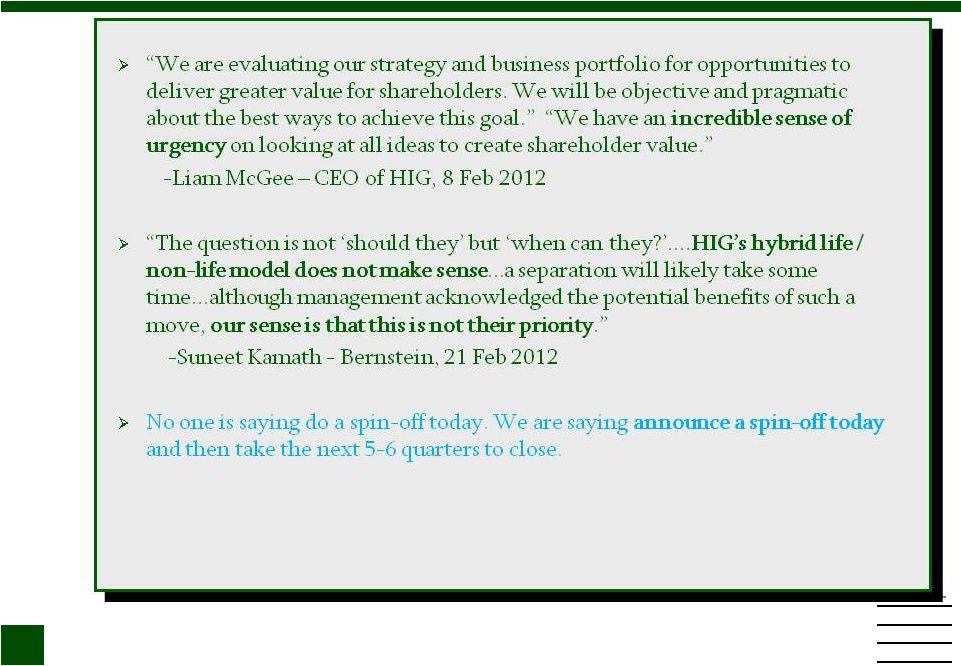

PAULSON & CO. INC. 12 MANAGEMENT RAISED CHALLENGES TO A SPIN-OFF IN THE 4Q11 EARNINGS PRESENTATION All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. 1. “Maintaining competitive ratings while allocating $6.8bn in holding company debt” “Life companies could assume no more than one-third of debt due to combination of their currently limited capacity to generate statutory earnings and dividends and “A” level interest coverage ratios” "P&C companies would need to assume at least two-thirds of debt, which could require potentially dilutive de-leveraging actions in order to meet “A” rating debt leverage ratios” 2. “Regulatory approval could be conditioned on capital contributions or keepwell agreements between the stand-alone companies” 3. “ Other items:” “Cost of securing bondholder approval of debt allocation” “Valuation impact of P&C company guarantee of certain life company obligations” “Potential write-off of a significant portion of the life companies' deferred tax asset” |

PAULSON & CO. INC. 13 CHALLENGE 1: “MAINTAINING COMPETITIVE RATINGS WHILE ALLOCATING $6.8BN OF HOLDING COMPANY DEBT” Numerous options exist to raise cash to reduce Holdco debt and maintain ratings without “dilutive de-leveraging actions” In addition, if necessary Hartford could consider divestitures of: VA runoff: expense cuts and capital return bolster strength to service debt Hartford Life should maintain an A-rating. Hartford P&C likely to be upgraded to A1 ($ in billions) Low High Cash at 4Q11 $1.6 $1.6 Retained earnings 0.3 0.7 XXX transaction 0.2 0.4 Hedge fund repackaging 1.1 1.1 Divestiture of FA runoff 0.8 1.0 Total $4.0 $4.8 ($ in billions) Low High Est. P /BV P /E Mutual funds $1.5 $1.5 5.40x 15.6x Retirement 0.5 0.7 0.53x 12.5x Group benefits 1.5 2.0 1.47x 12.5x Total $3.5 $4.2 1.56x 13.7x Grand total $7.5 $9.0 All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. |

PAULSON & CO. INC. 14 CHALLENGE 1: “MAINTAINING COMPETITIVE RATINGS WHILE ALLOCATING $6.8BN OF HOLDING COMPANY DEBT” Hartford Financial Services Group P&C Hartford Life & Accident Group somewhat credit ratings-sensistive Retirement Harford Life & Annuity Runoff VA (US & Japan) Individual Life (in runoff) not credit ratings-sensitive Mutual Funds However, even if Hartford Life were downgraded to BBB, credit sensitive businesses could be protected within P&C or through a divestiture to a strong buyer Conceptually, HIG could be divided into three businesses: P&C, Hartford Life & Accident, and Hartford Life & Annuity. This would produce the most value, even more than our previous indication Once the US VA business is put in run-off, an A-rating is not a constraint All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. |

PAULSON & CO. INC. 15 CHALLENGE 2: “REGULATORY APPROVAL COULD BE CONDITIONED ON CAPITAL CONTRIBUTIONS OR KEEPWELL AGREEMENTS BETWEEN THE STAND-ALONE COMPANIES” “I am aware of the shareholder filing regarding Hartford Financial Services. However, until the Department receives formal notice from the Company with respect to future plans we are not in a position to comment further. Certainly, in any such regulatory approval process that involves a Connecticut-based carrier, policyholder protection is paramount.” -Thomas Leonardi – CT Insurance Commissioner, 15 Feb 2012 Hartford has access to numerous sources of cash over the next 18 months to ensure that both P&C and Life policyholders will be protected and all regulatory conditions will be met All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. |

PAULSON & CO. INC. 16 CHALLENGE 3: OTHER “Cost of securing bondholder approval of debt allocation” No bondholder approval needed to spinoff P&C business “We will not consolidate with or merge into any other corporation or convey, transfer or lease our properties and assets substantially as an entirety to any person...unless: the successor corporation expressly assumes our obligations relating to the notes” Many alternatives exist for restructuring and repurchasing debt “Valuation impact of P&C company guarantee of certain Life obligations” Minimal impact. P&C guarantee only applies to business written between 1990 and 1997 – small amount of VA policies that are well in the money, none from Japan “Potential write-off of a significant portion of the life companies' DTA” A non-cash, GAAP-only item that does not affect regulatory capital or the ability to use $2bn of capital loss-carryforwards to shelter tax on gains on divestitures All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. |

17 PAULSON & CO. INC. WHILE MULTI-LINE INSURANCE COMPANIES WERE POPULAR IN THE PAST, NEARLY ALL LEADING U.S. INSURERS ARE NOW PURE-PLAYS Segment earnings Historical 2011 Date P&C Life Health P&C Life Health Travelers (1) 2000 75% 25% 0% 100% 0% 0% CNA 2002 59% 41% 0% 100% 0% 0% Lincoln (2) 1996 40% 60% 0% 0% 100% 0% Aetna 1994 8% 42% 50% 0% 8% 92% Cigna 1996 20% 34% 46% 0% 18% 82% (1) Pro-forma combination of St. Paul and Citigroup insurance businesses (2) P&C includes reinsurance segment All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. |

PAULSON & CO. INC. 18 All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. Spinco Completion Parent Spinco Market cap Date Marathon Oil Marathon Petroleum 14,892 Jun-11 Motorola Motorola Mobility 11,996 Dec-10 Liberty Media Liberty Interactive 10,786 Sep-11 Expedia TripAdvisor 4,205 Dec-11 Williams Cos WPX Energy 3,631 Jan-12 Cablevision AMC Networks 3,192 Jun-11 Beam Fortune Brands 3,134 Oct-11 General Growth Howard Hughes 2,303 Nov-11 Northrup Grumman Huntington Ingalls 1,775 Mar-11 Sunoco SunCoke Energy 971 Jan-12 Marriott International Marriott Vacations 894 Nov-11 Forest Oil Lone Pine Resources 615 Sep-11 MANY FORTUNE 500 COMPANIES ARE SPINNING OFF 100% OF BUSINESS LINES TO CREATE SHAREHOLDER VALUE: COMPLETED |

PAULSON & CO. INC. 19 All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. MANY FORTUNE 500 COMPANIES ARE SPINNING OFF 100% OF BUSINESS LINES TO CREATE SHAREHOLDER VALUE: ANNOUNCED Announcement Parent Spinco Date Abbott Laboratories Research-based medicines Oct-11 Tyco ADT Home Security & Flow Control Sep-11 Kraft North American grocery business Aug-11 L-3 Government Services Jul-11 Ralcorp Post Foods Jul-11 ConocoPhillips Refining & marketing business Jul-11 Sears Orchard Supply Hardware Jun-11 Procter & Gamble Pringles Apr-11 Sara Lee Beverage business Jan-11 |

PAULSON & CO. INC. 20 THE OBJECTIVE IN ALL THESE SPIN-OFFS IS THE SAME, TO OPTIMIZE RETURNS TO SHAREHOLDERS Ralcorp’s 100% Tax-Free Spinoff of Post Foods We firmly believe the separation of Post Foods from Ralcorp by way of a tax-free spin-off will unlock significant value for our shareholders. As independent companies, both Ralcorp and Post Foods will be better positioned to focus on strategies specific to their particular businesses, thereby improving the opportunities to deliver increasing shareholder value. William Stiritz - Chairman of Ralcorp, 15 Jul 2011 Kraft’s 100% Tax-Free Spinoff of N. American Grocery Business The company believes creating two public companies would offer a number of opportunities: – Each business would focus on its distinct strategic priorities, with financial targets that best fit its own markets and unique opportunities. – Each would be able to allocate resources and deploy capital in a manner consistent with its strategic priorities in order to optimize total returns to shareholders. – Investors would be able to value the two companies based on their particular operational and financial characteristics and thus invest accordingly. Press release, 4 Aug 2011 All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. |

21 PAULSON & CO. INC. HOW LONG MIGHT WE HAVE TO WAIT FOR MANAGEMENT’S PLAN TO BE ANNOUNCED? AND COMPLETED? All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. |

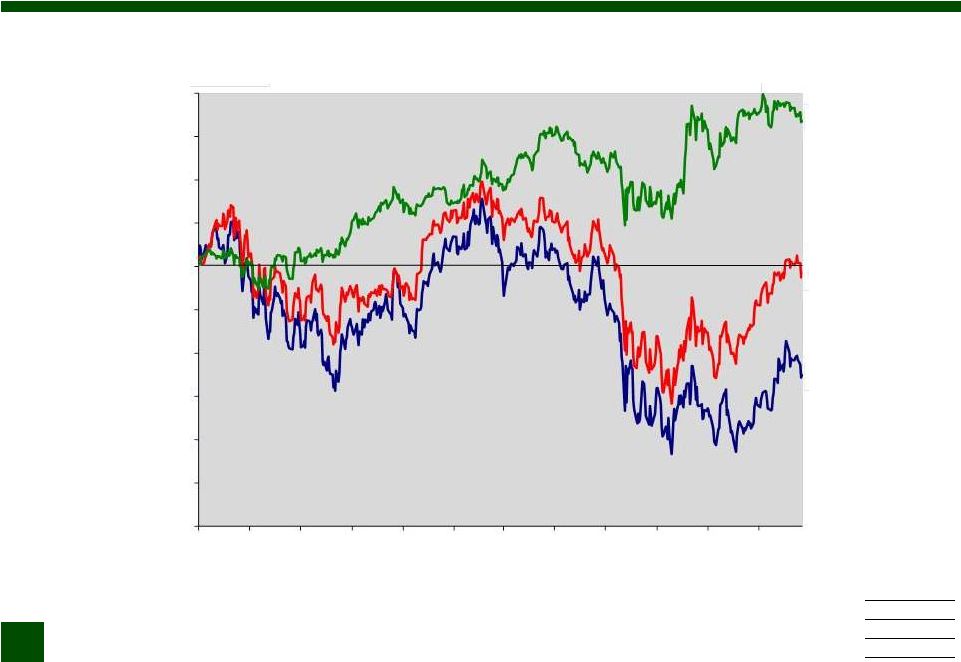

PAULSON & CO. INC. 22 (1) Life Peers: LNC, PFG, MET & PRU (2) P&C Peers: TRV, CB & ACE HARTFORD’S STOCK HAS DRAMATICALLY UNDERPERFORMED P&C PEERS BY 59% AND LIFE PEERS BY 24% SINCE RAISING NEW EQUITY CAPITAL TO MEET ITS STRESS TESTS Performance is unacceptable. No time to delay restructuring actions Since: Mar 16 (60%) (50%) (40%) (30%) (20%) (10%) 0% 10% 20% 30% 40% Mar-10 May-10 Jul-10 Sep-10 Nov-10 Jan-11 Mar-11 May-11 Jul-11 Sep-11 Nov-11 Jan-12 (25)% 34% (1)% P&C Life HIG Last Datapoint: 7 Mar 12 $2.15bn equity & convertible offering announced: 16 Mar 10 at $27.75 All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. |

PAULSON & CO. INC. 23 ANALYSTS VIEW A P&C SPINOFF AS VALUE ACCRETIVE All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. “We believe there is a strong opportunity for management to unlock shareholder value by reevaluating the multi-line strategy, placing annuities into run-off, and selling off its remaining life insurance operations. If executed, we see a potential fair value in the range of $26-27, roughly 50% above the stock’s level.” -Nigel Dally-Morgan Stanley, 1 Feb 2012 “We believe HIG’s P&C and life companies are worth more separately than together. If HIG’s valuation remains depressed, we expect HIG to reach a similar verdict over time, resulting in a potential spin-off of its P&C business.” [price target $28.32, 73% above the market price] - Chris Giovanni-Goldman Sachs, 9 Jan 2012 “We believe there remains 70% upside to Hartford’s valuation on a sum of the parts ($34.24), and if the company is willing to split the businesses or consider strategic alternatives, this value could be unlocked.” “In our view, the P&C operations alone are worth the current market cap ($8.4bn, $19/share)...the Life franchises are worth an additional $6.7bn or $15/share...based on its peers multiples. In a bidding process each individual unit could achieve a premium to the peer valuation.” -Alan Devlin-Atlantic Equities, 15 Feb 2012 |

PAULSON & CO. INC. 24 RECOMMENDED PLAN All material is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. The above represented are for illustrative purposes only. There is no guarantee that these securities will be held in the funds in the future. This material may not be distributed to other than the intended recipients. Unauthorized reproduction or distribution of all or any of this material is strictly prohibited. April [ ], 2012 Announcement Hartford plans to spin off 100% of Hartford P&C, subject to final Board and regulatory approval Estimated closing date: 2Q13 US VA will be put in run-off, effective immediately Substantial cost savings and accelerated return of capital Hartford Life will review the strategy and structure of its life businesses over the next twelve months |