Exhibit 99.1

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Searchable text section of graphics shown above

Forward Looking Statement Note

This presentation may contain projections and other forward-looking statements that involve risks and uncertainties. These statements may differ materially from actual future events or results. Readers are referred to the documents filed by us with the Securities and Exchange Commission, specifically the most recent reports which identify important risk factors that could cause actual results to differ from those contained in the forward-looking statements, including but not limited to: access line losses due to increased competition, including from technology substitution of our access lines with wireless and cable alternatives; our substantial indebtedness, and our inability to complete any efforts to de-lever our balance sheet through asset sales or other transactions; any adverse outcome of the current investigation by the U.S. Attorney’s office in Denver into certain matters relating to us; adverse results of increased review and scrutiny by regulatory authorities, media and others (including any internal analyses) of financial reporting issues and practices or otherwise; rapid and significant changes in technology and markets; any adverse developments in commercial disputes or legal proceedings, including any adverse outcome of current or future legal proceedings related to matters that are the subject of governmental investigations, and, to the extent not covered by insurance, if any, our inability to satisfy any resulting obligations from funds available to us, if any; potential fluctuations in quarterly results; volatility of our stock price; intense competition in the markets in which we compete including the likelihood of certain of our competitors emerging from bankruptcy court protection, consolidating with others or otherwise reorganizing their capital structure to more effectively compete against us; changes in demand for our products and services; acceleration of the deployment of advanced new services, such as broadband data, wireless and video services, which could require substantial expenditure of financial and other resources in excess of contemplated levels; higher than anticipated employee levels, capital expenditures and operating expenses; adverse changes in the regulatory or legislative environment affecting our business; changes in the outcome of future events from the assumed outcome included in our significant accounting policies; our ability to utilize net operating losses in projected amounts; and our inability to provide any assurance as to whether we will be successful in our effort to acquire MCI, Inc., whether in the event of an acquisition we realize synergies in the amounts, at the times and at the related costs projected and whether regulatory approvals will be received within the timeframe projected and that such approvals will not be materially adverse to the projected operations of the combined company following the merger.

The information contained in this release is a statement of Qwest’s present intention, belief or expectation and is based upon, among other things, the existing regulatory environment, industry conditions, market conditions and prices, the economy in general and Qwest’s assumptions. Qwest may change its intention, belief or expectation, at any time and without notice, based upon any changes in such factors, in Qwest’s assumptions or otherwise. The cautionary statements contained or referred to in this release should be considered in connection with any subsequent written or oral forward-looking statements that Qwest or persons acting on its behalf may issue. This release may include analysts’ estimates and other information prepared by third parties for which Qwest assumes no responsibility.

By including any information in this release, Qwest does not necessarily acknowledge that disclosure of such information is required by applicable law or that the information is material. The Qwest logo is a registered trademark of Qwest Communications International Inc. in the U.S. and certain other countries.

This material is not a substitute for the prospectus/proxy statement Qwest and MCI would file with the Securities and Exchange Commission if a negotiated agreement with MCI is reached. Investors are urged to read any such prospectus/proxy statement, when available, which would contain important information, including detailed risk factors. The prospectus/proxy statement would be, and other documents filed by Qwest and MCI with the Securities and Exchange Commission are, available free of charge at the SEC’s website (www.sec.gov) or by directing a request to Qwest, 1801 California Street, Denver, Colorado, 80202 Attn: Investor Relations; or by directing a request to MCI, 22001 Loudoun County Parkway, Ashburn, Virginia 20147 Attention: Investor Relations.

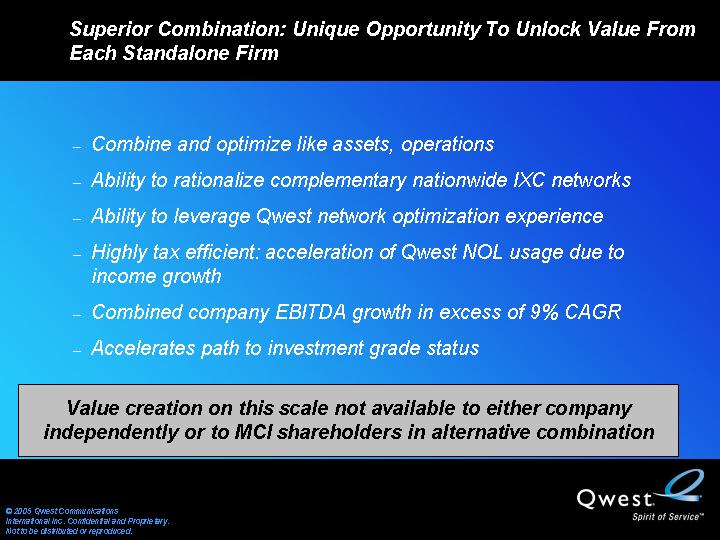

Superior Combination: Unique Opportunity To Unlock Value From Each Standalone Firm

• Combine and optimize like assets, operations

• Ability to rationalize complementary nationwide IXC networks

• Ability to leverage Qwest network optimization experience

• Highly tax efficient: acceleration of Qwest NOL usage due to income growth

• Combined company EBITDA growth in excess of 9% CAGR

• Accelerates path to investment grade status

Value creation on this scale not available to either company

independently or to MCI shareholders in alternative combination

© 2005 Qwest Communications

International Inc. Confidential and Proprietary.

Not to be distributed or reproduced.

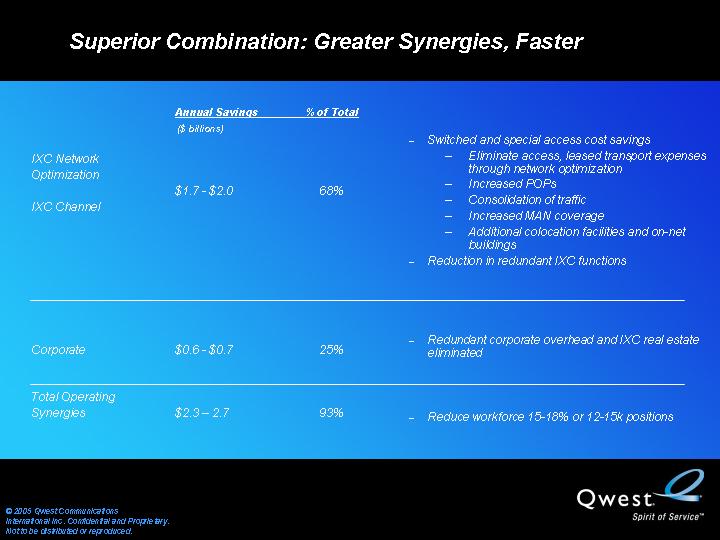

Superior Combination: Greater Synergies, Faster

|

| Annual Savings |

| % of Total |

|

|

|

| ($ billions) |

|

|

|

|

|

|

|

|

|

| • Switched and special access cost savings |

IXC Network |

|

|

|

|

| • Eliminate access, leased transport expenses through network optimization |

|

| $1.7 - $2.0 |

| 68 | % | • Increased POPs |

IXC Channel |

|

|

|

|

| • Consolidation of traffic |

|

|

|

|

|

| • Increased MAN coverage |

|

|

|

|

|

| • Additional colocation facilities and on-net buildings |

|

|

|

|

|

| • Reduction in redundant IXC functions |

|

|

|

|

|

|

|

Corporate |

| $0.6 - $0.7 |

| 25 | % | • Redundant corporate overhead and IXC real estate eliminated |

|

|

|

|

|

|

|

Total Operating Synergies |

| $2.3 – 2.7 |

| 93 | % | • Reduce workforce 15-18% or 12-15k positions |

|

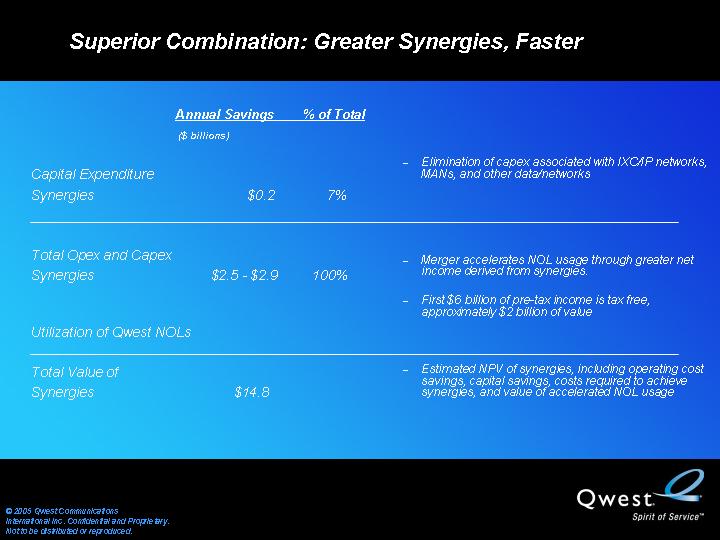

| Annual Savings |

| % of Total |

|

|

|

| ($ billions) |

|

|

|

|

Capital Expenditure Synergies |

|

|

|

|

| • Elimination of capex associated with IXC/IP networks, |

|

| $0.2 |

| 7 | % | MANs, and other data/networks |

|

|

|

|

|

|

|

Total Opex and Capex |

|

|

|

|

| • Merger accelerates NOL usage through greater net |

Synergies |

|

|

|

|

| income derived from synergies. |

|

| $2.5 - $2.9 |

| 100 | % | • First $6 billion of pre-tax income is tax free, approximately |

|

|

|

|

|

| $2 billion of value |

|

|

|

|

|

|

|

Utilization of Qwest NOLs |

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Value of Synergies |

| $14.8 |

|

|

| • Estimated NPV of synergies, including operating cost and |

|

|

|

|

|

| savings, capital savings, costs required to achieve synergies, and value of accelerated NOL usage |

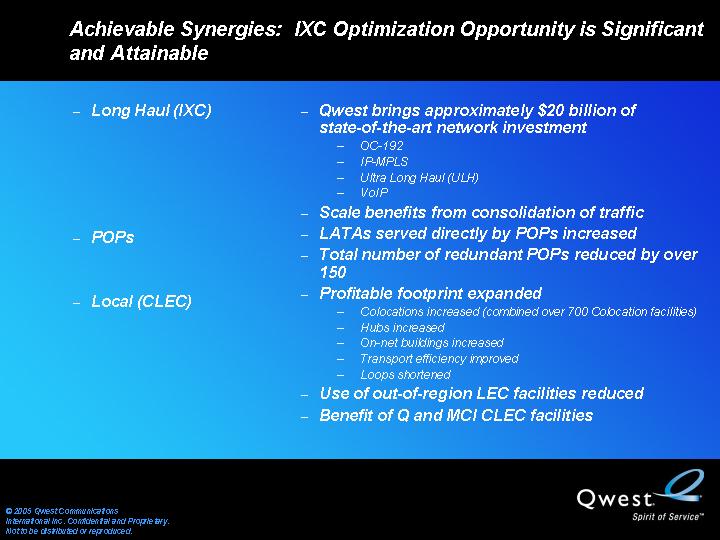

Achievable Synergies: IXC Optimization Opportunity is Significant and Attainable

• | Long Haul (IXC) | • | Qwest brings approximately $20 billion of state-of-the-art network investment | |

|

|

| • | OC-192 |

|

|

| • | IP-MPLS |

|

|

| • | Ultra Long Haul (ULH) |

|

|

| • | VoIP |

|

| • | Scale benefits from consolidation of traffic | |

• | POPs | • | LATAs served directly by POPs increased | |

|

| • | Total number of redundant POPs reduced by over 150 | |

|

|

|

| |

• | Local (CLEC) | • | Profitable footprint expanded | |

|

|

|

| |

|

|

| • | Colocations increased (combined over 700 Colocation facilities) |

|

|

| • | Hubs increased |

|

|

| • | On-net buildings increased |

|

|

| • | Transport efficiency improved |

|

|

| • | Loops shortened |

|

| • | Use of out-of-region LEC facilities reduced | |

|

| • | Benefit of Q and MCI CLEC facilities | |

Superior Combination: Powerful synergies ramp quickly

Synergy Ramp Up

($ in millions)

[CHART]

• Accelerated ramp due to nature of combination, complementary nationwide IXC networks

• Optimization versus integration

• Reasonable opex/capex investments required to unlock value

• Approximately $2.7 billion

• Cash flow and earnings accretive immediately

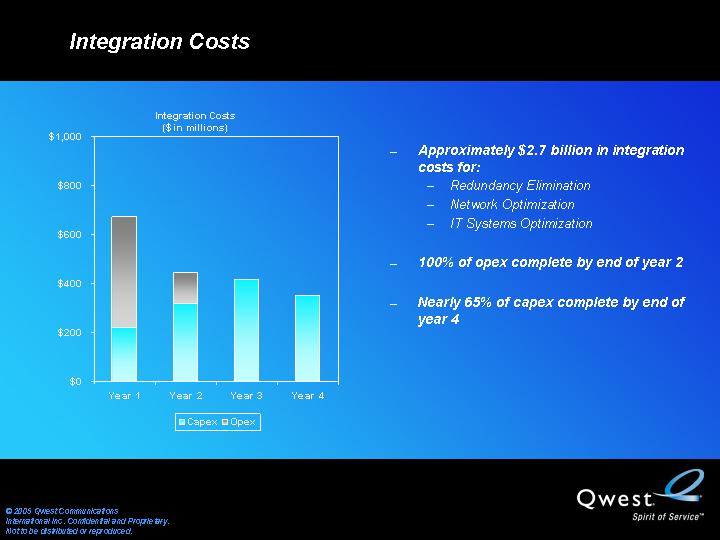

Integration Costs

Integration Costs

($ in millions)

[CHART]

• Approximately $2.7 billion in integration costs for:

• Redundancy Elimination

• Network Optimization

• IT Systems Optimization

• 100% of opex complete by end of year 2

• Nearly 65% of capex complete by end of year 4

Qwest + MCI is a Better Deal

• Greater value to shareowners, both now and in the future

• A management team with expertise in delivering operational improvements and a proven ability to execute

• Unique opportunity to combine and optimize like assets, operations

• The combined company is an industry leader