UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-08217

| Name of Fund: | BlackRock MuniHoldings New York Quality Fund, Inc. (MHN) |

| Fund Address: | 100 Bellevue Parkway, Wilmington, DE 19809 |

Name and address of agent for service: John M. Perlowski, Chief Executive Officer, BlackRock MuniHoldings New York Quality Fund, Inc., 55 East 52nd Street, New York, NY 10055

Registrant’s telephone number, including area code: (800) 882-0052, Option 4

Date of fiscal year end: 08/31/2022

Date of reporting period: 02/28/2022

Item 1 – Report to Stockholders

(a) The Report to Shareholders is attached herewith.

| FEBRUARY 28, 2022 |

| 2022 Semi-Annual Report (Unaudited) | ||

BlackRock MuniHoldings New York Quality Fund, Inc. (MHN)

BlackRock Virginia Municipal Bond Trust (BHV)

| Not FDIC Insured • May Lose Value • No Bank Guarantee |

Supplemental Information (unaudited)

Section 19(a) Notices

BlackRock MuniHoldings New York Quality Fund, Inc.’s (MHN) and BlackRock Virginia Municipal Bond Trust’s (BHV) (collectively the “Trusts”, or individually a “Trust”) amounts and sources of distributions reported are estimates and are being provided pursuant to regulatory requirements and are not being provided for tax reporting purposes. The actual amounts and sources for tax reporting purposes will depend upon each Trust’s investment experience during the year and may be subject to changes based on tax regulations. Each Trust will provide a Form 1099-DIV each calendar year that will tell you how to report these distributions for U.S. federal income tax purposes.

February 28, 2022

| Total Cumulative Distributions for the Fiscal Period | % Breakdown of the Total Cumulative Distributions for the Fiscal Period | |||||||||||||||||||||||||||||||||||||||

| Trust Name | Net Income | Net Realized Capital Gains Short-Term | Net Realized Capital Gains Long-Term | Return of Capital (a) | Total Per Common Share | Net Income | Net Realized Capital Gains Short-Term | Net Realized Capital Gains Long-Term | Return of Capital | Total Per Common Share | ||||||||||||||||||||||||||||||

MHN | $ | 0.324974 | $ | — | $ | — | $ | 0.002026 | $ | 0.327000 | 99 | % | — | % | — | % | 1 | % | 100 | % | ||||||||||||||||||||

BHV | 0.273000 | — | — | — | 0.273000 | 100 | — | — | — | 100 | ||||||||||||||||||||||||||||||

| (a) | The Trust estimates that it has distributed more than its net income and net realized capital gains; therefore, a portion of the distribution may be a return of capital. A return of capital may occur, for example, when some or all of the shareholder’s investment in the Trust is returned to the shareholder. A return of capital does not necessarily reflect the Trust’s investment performance and should not be confused with “yield” or “income.” When distributions exceed total return performance, the difference will reduce the Trust’s net asset value per share. |

Section 19(a) notices for the Trusts, as applicable, are available on the BlackRock website at blackrock.com.

| 2 | 2 0 2 2 B L A C K R O C K S E M I - A N N U A L R E P O R T T O S H A R E H O L D E R S |

Dear Shareholder,

The 12-month reporting period as of February 28, 2022 saw a continuation of the resurgent growth that followed the initial coronavirus (or “COVID-19”) pandemic reopening, albeit at a slower pace. The global economy weathered the emergence of several variant strains and the resulting peaks and troughs in infections amid optimism that increasing vaccinations and economic adaptation could help contain the pandemic’s disruptions. However, rapid changes in consumer spending led to supply constraints and elevated inflation. Moreover, while the foremost effect of Russia’s invasion of Ukraine has been a severe humanitarian crisis, the invasion has presented challenges for both investors and policymakers.

Equity prices were mixed, as persistently high inflation drove investors’ expectations for higher interest rates, which particularly weighed on relatively high valuation growth stocks and economically sensitive small-capitalization stocks. Overall, small-capitalization U.S. stocks declined, while large-capitalization U.S. stocks posted a solid advance. International equities from developed markets gained slightly, although emerging market stocks declined, pressured by rising interest rates and a strengthening U.S. dollar.

The 10-year U.S. Treasury yield (which is inversely related to bond prices) rose during the reporting period as the economy expanded rapidly and inflation reached its highest annualized reading in decades. In the corporate bond market, the improving economy assuaged credit concerns and led to modest returns for high-yield corporate bonds, outpacing the negative return of investment-grade corporate bonds.

The U.S. Federal Reserve (the “Fed”) maintained accommodative monetary policy during the reporting period by keeping near-zero interest rates. However, the Fed’s tone shifted during the period, as it reduced its bond-buying program and raised the prospect of higher rates in 2022. Continued high inflation and the Fed’s new stance led many analysts to anticipate that the Fed will raise interest rates multiple times throughout the year.

Looking ahead, however, the horrific war in Ukraine has significantly clouded the outlook for the global economy. Sanctions on Russia and general wartime disruption are likely to drive already-high commodity prices even further upwards, and we have already seen spikes in energy and metal markets. While this will exacerbate inflationary pressure, it could also constrain economic growth, making the Fed’s way forward less clear. Its challenge will be combating inflation without stifling a recovery that is now facing additional supply shocks.

In this environment, we favor an overweight to equities, as we believe low interest rates and continued economic growth will support further gains, albeit likely more modest than what we saw in 2021. Sectors that are better poised to manage the transition to a lower-carbon world, such as technology and health care, are particularly attractive in the long term. U.S. and other developed market equities have room for further growth, while we believe Chinese equities stand to gain from a more accommodative monetary and fiscal environment. We are underweight long-term credit, but inflation-protected U.S. Treasuries, Asian fixed income, and emerging market local-currency bonds offer potential opportunities. We believe that international diversification and a focus on sustainability can help provide portfolio resilience, and the disruption created by the coronavirus appears to be accelerating the shift toward sustainable investments.

Overall, our view is that investors need to think globally, extend their scope across a broad array of asset classes, and be nimble as market conditions change. We encourage you to talk with your financial advisor and visit blackrock.com for further insight about investing in today’s markets.

Sincerely,

Rob Kapito

President, BlackRock Advisors, LLC

Rob Kapito

President, BlackRock Advisors, LLC

| Total Returns as of February 28, 2022 | ||||

| 6-Month | 12-Month | |||

U.S. large cap equities (S&P 500® Index) | (2.62)% | 16.39% | ||

U.S. small cap equities (Russell 2000® Index) | (9.46) | (6.01) | ||

International equities (MSCI Europe, Australasia, Far East Index) | (6.78) | 2.83 | ||

Emerging market equities (MSCI Emerging Markets Index) | (9.81) | (10.69) | ||

3-month Treasury bills (ICE BofA 3-Month U.S. Treasury Bill Index) | 0.02 | 0.04 | ||

U.S. Treasury securities (ICE BofA 10-Year U.S. Treasury Index) | (3.94) | (1.67) | ||

U.S. investment grade bonds (Bloomberg U.S. Aggregate Bond Index) | (4.07) | (2.64) | ||

Tax-exempt municipal bonds (Bloomberg Municipal Bond Index) | (3.09) | (0.66) | ||

U.S. high yield bonds (Bloomberg U.S. Corporate High Yield 2% Issuer Capped Index) | (3.07) | 0.64 | ||

Past performance is not an indication of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index. | ||||

T H I S P A G E I S N O T P A R T O F Y O U R F U N D R E P O R T | 3 |

| Page | ||||

| 2 | ||||

| 3 | ||||

Semi-Annual Report: | ||||

| 5 | ||||

| 6 | ||||

| 6 | ||||

| 7 | ||||

Financial Statements: | ||||

| 11 | ||||

| 21 | ||||

| 22 | ||||

| 23 | ||||

| 24 | ||||

| 25 | ||||

| 27 | ||||

| 36 | ||||

| 39 | ||||

| 4 |

Municipal Market Overview For the Reporting Period Ended February 28, 2022

Municipal Market Conditions

Municipal bonds posted modestly negative total returns during the period amid rising interest rates spurred by strong economic growth and above trend inflation, waning COVID-19 variant fears, and hawkish Fed monetary policy expectations. The asset class benefited from favorable supply and demand dynamics and improved credit fundamentals on the back of considerable fiscal stimulus and a quicker than expected rebound in state and local government revenues. As a result, municipal bonds generated positive excess returns versus comparable U.S. Treasuries. However, the market faced heightened volatility and a considerable valuation-based correction late in the period. Longer duration and lower credit quality strategies outperformed.

Technical support was helpful as robust demand outpaced supply. During the 12 months ended February 28, 2022, municipal bond funds experienced net inflows totaling $51 billion (based on data from the Investment Company Institute). However, the post-pandemic inflow cycle, which spanned 92-weeks and garnered $149 billion, came to an end late in the period as performance turned negative. At the same time, the market absorbed $448 billion in issuance, slightly above the $442 billion issued during the prior 12-month period. Taxable municipal issuance was proportionally elevated and helped to make tax-exempt supply even more easily digestible. |

| Bloomberg Municipal Bond Index Total Returns as of February 28, 2022

6 months: (3.09)%

12 months: (0.66)% | ||

A Closer Look at Yields

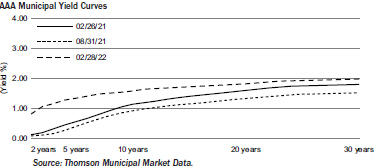

| From February 28, 2021 to February 28, 2022, yields on AAA-rated 30-year municipal bonds increased by 18 basis points (“bps”) from 1.80% to 1.98%, while ten-year rates increased by 44 bps from 1.14% to 1.58% and five-year rates increased by 78 bps from 0.56% to 1.34% (as measured by Thomson Municipal Market Data). As a result, the municipal yield curve flattened over the 12-month period with the spread between two- and 30-year maturities flattening by 69 bps, led by 43 bps of flattening between two- and ten-year maturities.

After maintaining historically tight valuations for most of the reporting period, the recent market correction has restored value to the asset class and reset municipal-to-Treasury ratios to levels near their 5-year averages. |

Financial Conditions of Municipal Issuers

Buoyed by successive federal aid injections, vaccine distribution, and the re-opening of the economy, states and many local governments experienced revenue growth above forecasts in 2021. Prolonged inflation in a post-Covid recovery would adversely affect state and local entities. However, wage pressures, less consumer spending, and higher interest rates could be offset by increased revenue collections, particularly sales and personal income tax receipts. While the war in Ukraine is not expected to have negative effects on credit fundamentals, higher energy prices could hurt consumer spending and eventually become a headwind to economic growth and employment expansion. At this point, tax receipts could come under pressure, although states with significant oil and gas production would benefit. While municipal utilities typically benefit from autonomous rate-setting that allows them to adjust for rising fuel costs, rising commodity prices over a prolonged period could test affordability and the political will to raise rates to balance operations. State housing authority bonds, flagship universities, and strong national and regional health systems may also be pressured but are better poised to absorb the impact of the economic shock. Critical providers (safety net hospitals, mass transit systems, airports) with limited resources may still experience fiscal strain from the economic fallout from rising inflation, but aid and the re-opening of the economy will continue to support operating results through 2022. Work-from-home policies remain headwinds for mass transit farebox revenue and commercial real estate values. BlackRock anticipates that a small subset of the market, mainly non-rated stand-alone projects, will remain susceptible to credit deterioration.

The opinions expressed are those of BlackRock as of February 28, 2022 and are subject to change at any time due to changes in market or economic conditions. The comments should not be construed as a recommendation of any individual holdings or market sectors. Investing involves risk including loss of principal. Bond values fluctuate in price so the value of your investment can go down depending on market conditions. Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. There may be less information on the financial condition of municipal issuers than for public corporations. The market for municipal bonds may be less liquid than for taxable bonds. Some investors may be subject to Alternative Minimum Tax (“AMT”). Capital gains distributions, if any, are taxable.

The Bloomberg Municipal Bond Index, a broad, market value-weighted index, seeks to measure the performance of the U.S. municipal bond market. All bonds in the index are exempt from U.S. federal income taxes or subject to the AMT. Past performance is not an indication of future results. Index performance is shown for illustrative purposes only. It is not possible to invest directly in an index.

M U N I C I P A L M A R K E T O V E R V I E W | 5 |

The Benefits and Risks of Leveraging

The Trusts may utilize leverage to seek to enhance the distribution rate on, and net asset value (“NAV”) of, their common shares (“Common Shares”). However, there is no guarantee that these objectives can be achieved in all interest rate environments.

In general, the concept of leveraging is based on the premise that the financing cost of leverage, which is based on short-term interest rates, is normally lower than the income earned by a Trust on its longer-term portfolio investments purchased with the proceeds from leverage. To the extent that the total assets of each Trust (including the assets obtained from leverage) are invested in higher-yielding portfolio investments, each Trust’s shareholders benefit from the incremental net income. The interest earned on securities purchased with the proceeds from leverage (after paying the leverage costs) is paid to shareholders in the form of dividends, and the value of these portfolio holdings (less the leverage liability) is reflected in the per share NAV.

To illustrate these concepts, assume a Trust’s Common Shares capitalization is $100 million and it utilizes leverage for an additional $30 million, creating a total value of $130 million available for investment in longer-term income securities. If prevailing short-term interest rates are 3% and longer-term interest rates are 6%, the yield curve has a strongly positive slope. In this case, a Trust’s financing costs on the $30 million of proceeds obtained from leverage are based on the lower short-term interest rates. At the same time, the securities purchased by a Trust with the proceeds from leverage earn income based on longer-term interest rates. In this case, a Trust’s financing cost of leverage is significantly lower than the income earned on a Trust’s longer-term investments acquired from such leverage proceeds, and therefore the holders of Common Shares (“Common Shareholders”) are the beneficiaries of the incremental net income.

However, in order to benefit Common Shareholders, the return on assets purchased with leverage proceeds must exceed the ongoing costs associated with the leverage. If interest and other costs of leverage exceed a Trust’s return on assets purchased with leverage proceeds, income to shareholders is lower than if a Trust had not used leverage. Furthermore, the value of the Trusts’ portfolio investments generally varies inversely with the direction of long-term interest rates, although other factors can influence the value of portfolio investments. In contrast, the amount of each Trust’s obligations under its respective leverage arrangement generally does not fluctuate in relation to interest rates. As a result, changes in interest rates can influence the Trusts’ NAVs positively or negatively. Changes in the future direction of interest rates are very difficult to predict accurately, and there is no assurance that a Trust’s intended leveraging strategy will be successful.

The use of leverage also generally causes greater changes in each Trust’s NAV, market price and dividend rates than comparable portfolios without leverage. In a declining market, leverage is likely to cause a greater decline in the NAV and market price of a Trust’s Common Shares than if the Trust were not leveraged. In addition, each Trust may be required to sell portfolio securities at inopportune times or at distressed values in order to comply with regulatory requirements applicable to the use of leverage or as required by the terms of leverage instruments, which may cause the Trust to incur losses. The use of leverage may limit a Trust’s ability to invest in certain types of securities or use certain types of hedging strategies. Each Trust incurs expenses in connection with the use of leverage, all of which are borne by Common Shareholders and may reduce income to the Common Shares. Moreover, to the extent the calculation of each Trust’s investment advisory fees includes assets purchased with the proceeds of leverage, the investment advisory fees payable to the Trusts’ investment adviser will be higher than if the Trusts did not use leverage.

To obtain leverage, each Trust has issued Variable Rate Demand Preferred Shares (“VRDP Shares” or “Preferred Shares”) and/or leveraged its assets through the use of tender option bond trusts (“TOB Trusts”) as described in the Notes to Financial Statements.

Under the Investment Company Act of 1940, as amended (the “1940 Act”), each Trust is permitted to issue debt up to 33 1/3% of its total managed assets or equity securities (e.g., Preferred Shares) up to 50% of its total managed assets. A Trust may voluntarily elect to limit its leverage to less than the maximum amount permitted under the 1940 Act. In addition, a Trust may also be subject to certain asset coverage, leverage or portfolio composition requirements imposed by the Preferred Shares’ governing instruments or by agencies rating the Preferred Shares, which may be more stringent than those imposed by the 1940 Act.

If a Trust segregates or designates on its books and records cash or liquid assets having a value not less than the value of a Trust’s obligations under the TOB Trust (including accrued interest), then the TOB Trust is not considered a senior security and is not subject to the foregoing limitations and requirements imposed by the 1940 Act.

Derivative Financial Instruments

The Trusts may invest in various derivative financial instruments. These instruments are used to obtain exposure to a security, commodity, index, market, and/or other assets without owning or taking physical custody of securities, commodities and/or other referenced assets or to manage market, equity, credit, interest rate, foreign currency exchange rate, commodity and/or other risks. Derivative financial instruments may give rise to a form of economic leverage and involve risks, including the imperfect correlation between the value of a derivative financial instrument and the underlying asset, possible default of the counterparty to the transaction or illiquidity of the instrument. The Trusts’ successful use of a derivative financial instrument depends on the investment adviser’s ability to predict pertinent market movements accurately, which cannot be assured. The use of these instruments may result in losses greater than if they had not been used, may limit the amount of appreciation a Trust can realize on an investment and/or may result in lower distributions paid to shareholders. The Trusts’ investments in these instruments, if any, are discussed in detail in the Notes to Financial Statements.

| 6 | 2 0 2 2 B L A C K R O C K S E M I - A N N U A L R E P O R T T O S H A R E H O L D E R S |

Trust Summary as of February 28, 2022

|

BlackRock MuniHoldings New York Quality Fund, Inc. (MHN) |

Investment Objective

BlackRock MuniHoldings New York Quality Fund, Inc.’s (MHN) (the “Trust”) investment objective is to provide shareholders with current income exempt from U.S. federal income tax and New York State and New York City personal income taxes. The Trust seeks to achieve its investment objective by investing, under normal market conditions, at least 80% of its assets in investment grade (as rated or, if unrated, considered to be of comparable quality at the time of investment by the Trust’s investment adviser) New York municipal obligations exempt from U.S. federal income taxes (except that the interest may be subject to the U.S. federal alternative minimum tax) and New York State and New York City personal income taxes (“New York Municipal Bonds”), except at times when, in the judgment of its investment adviser, New York Municipal Bonds of sufficient quality and quantity are unavailable for investment by the Trust. At all times, except during temporary defensive periods, the Trust invests at least 65% of its assets in New York Municipal Bonds. The Trust invests, under normal market conditions, at least 80% of its assets in municipal obligations with remaining maturities of one year or more. The Trust may invest up to 20% of its managed assets in securities that are rated below investment grade, or are considered by BlackRock to be of comparable quality, at the time of purchase. The Trust may invest directly in such securities or synthetically through the use of derivatives.

No assurance can be given that the Trust’s investment objective will be achieved.

Trust Information

Symbol on New York Stock Exchange | MHN | |

Initial Offering Date | September 19, 1997 | |

Yield on Closing Market Price as of February 28, 2022 ($12.94)(a) | 5.05% | |

Tax Equivalent Yield(b) | 10.46% | |

Current Monthly Distribution per Common Share(c) | $0.0545 | |

Current Annualized Distribution per Common Share(c) | $0.6540 | |

Leverage as of February 28, 2022(d) | 40% |

| (a) | Yield on closing market price is calculated by dividing the current annualized distribution per share by the closing market price. Past performance is not an indication of future results. |

| (b) | Tax equivalent yield assumes the maximum marginal U.S. federal and state tax rate of 51.7%, which includes the 3.8% Medicare tax. Actual tax rates will vary based on income, exemptions and deductions. Lower taxes will result in lower tax equivalent yields. |

| (c) | The distribution rate is not constant and is subject to change. A portion of the distribution may be deemed a return of capital or net realized gain. |

| (d) | Represents VRDP Shares and TOB Trusts as a percentage of total managed assets, which is the total assets of the Trust, including any assets attributable to VRDP Shares and TOB Trusts, minus the sum of its accrued liabilities. Does not reflect derivatives or other instruments that may give rise to economic leverage. For a discussion of leveraging techniques utilized by the Trust, please see The Benefits and Risks of Leveraging and Derivative Financial Instruments. |

Market Price and Net Asset Value Per Share Summary

| 02/28/22 | 08/31/21 | Change | High | Low | ||||||||||||||||

Closing Market Price | $ | 12.94 | $ | 14.74 | (12.21 | )% | $ | 14.92 | $ | 12.80 | ||||||||||

Net Asset Value | 14.09 | 15.21 | (7.36 | ) | 15.21 | 14.01 | ||||||||||||||

Performance

Returns for the period ended February 28, 2022 were as follows:

| Average Annual Total Returns | ||||||||||||||||

| 6-month | 1 Year | 5 Years | 10 Years | |||||||||||||

Trust at NAV(a)(b) | (5.18 | )% | (0.96 | )% | 3.97 | % | 4.43 | % | ||||||||

Trust at Market Price(a)(b) | (10.14 | ) | (2.36 | ) | 3.44 | 3.15 | ||||||||||

New York Customized Reference Benchmark(c) | (3.05 | ) | (0.09 | ) | 3.33 | N/A | ||||||||||

Bloomberg Municipal Bond Index(d) | (3.09 | ) | (0.66 | ) | 3.24 | 3.15 | ||||||||||

S&P® Municipal Bond Index(e) | (2.79 | ) | (0.37 | ) | 3.18 | 3.22 | ||||||||||

Lipper New York Municipal Debt Funds at NAV(f) | (4.76 | ) | (0.29 | ) | 3.60 | 4.16 | ||||||||||

Lipper New York Municipal Debt Funds at Market Price(f) | (11.10 | ) | (3.52 | ) | 2.75 | 3.18 | ||||||||||

| (a) | All returns reflect reinvestment of dividends and/or distributions at actual reinvestment prices. Performance results reflect the Trust’s use of leverage. |

| (b) | The Trust’s discount to NAV widened during the period, which accounts for the difference between performance based on market price and performance based on NAV. |

| (c) | The New York Customized Reference Benchmark is comprised of the Bloomberg Municipal Bond: New York Exempt Total Return Index Unhedged (90%) and the New York Bloomberg Municipal Bond: High Yield (non-Investment Grade) Total Return Index (10%). Effective October 1, 2021, the Trust changed its benchmarks from S&P Municipal Bond Index and Lipper New York Municipal Debt Funds to Bloomberg Municipal Bond Index and the New York Customized Reference Benchmark. The investment adviser believes the new benchmarks are more appropriate reporting benchmarks for the Trust. The New York Customized Reference Benchmark commenced on September 30, 2016. |

| (d) | An unmanaged index that tracks the U.S. long term tax-exempt bond market, including state and local general obligation bonds, revenue bonds, pre-refunded bonds, and insured bonds. |

| (e) | A broad, market value-weighted index that seeks to measure the performance of the U.S. municipal bond market. |

| (f) | Average return. Returns reflect reinvestment of dividends and/or distributions at NAV on the ex-dividend date as calculated by Lipper. |

Performance results may include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles. Past performance is not an indication of future results.

T R U S T S U M M A R Y | 7 |

Trust Summary as of February 28, 2022 (continued)

|

BlackRock MuniHoldings New York Quality Fund, Inc. (MHN) |

The Trust is presenting the performance of one or more indices for informational purposes only. The Trust is actively managed and does not seek to track or replicate the performance of any index. The index performance shown is not intended to be indicative of the Trust’s investment strategies, portfolio components or past or future performance.

More information about the Trust’s historical performance can be found in the “Closed End Funds” section of blackrock.com.

The following discussion relates to the Trust’s absolute performance based on NAV:

Municipal bonds lost ground in the six-month period, ending a stretch of positive performance that began in mid-2020. Rising inflation prompted the Fed to shift toward tighter monetary policy, weighing heavily on the performance of fixed-income assets.

In this environment, the downturn in prices offset the contribution from income. Longer-duration securities, including longer-dated and lower-coupon bonds, were generally the largest detractors. (Duration is a measure of interest rate sensitivity.) The Trust’s use of leverage, while augmenting income, amplified the effect of falling prices. At the sector level, housing and transportation issues were notable laggards due to their longer duration.

On the positive side, the Trust’s use of U.S. Treasury futures to manage interest rate risk contributed to results. Pre-refunded bonds, while posting negative returns, held up well on a relative basis due to their short duration. The investment adviser believed pre-refunded bonds provided a defensive anchor and were a relatively liquid source of funds.

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

Overview of the Trust’s Total Investments

SECTOR ALLOCATION

| Sector(a)(b) | 02/28/22 | 08/31/21 | ||||||

Transportation | 27 | % | 30 | % | ||||

County/City/Special District/School District | 20 | 18 | ||||||

State | 13 | 12 | ||||||

Utilities | 12 | 12 | ||||||

Education | 10 | 10 | ||||||

Housing | 9 | 9 | ||||||

Health | 3 | 3 | ||||||

Corporate | 3 | 2 | ||||||

Tobacco | 2 | 2 | ||||||

Other | 1 | 2 | ||||||

CALL/MATURITY SCHEDULE

| Calendar Year Ended December 31,(a)(c) | Percentage | |||

2022 | 6 | % | ||

2023 | 12 | |||

2024 | 10 | |||

| 2025 | 10 | |||

2026 | 8 | |||

CREDIT QUALITY ALLOCATION

| Credit Rating(a)(d) | 02/28/22 | 08/31/21 | ||||||

AAA/Aaa | 12 | % | 11 | % | ||||

AA/Aa | 53 | 55 | ||||||

A | 23 | 22 | ||||||

BBB/Baa | 5 | 5 | ||||||

BB/Ba | 1 | 1 | ||||||

B | — | (e) | — | (e) | ||||

N/R(f) | 6 | 6 | ||||||

| (a) | Excludes short-term securities. |

| (b) | For Trust compliance purposes, the Trust’s sector classifications refer to one or more of the sector sub-classifications used by one or more widely recognized market indexes or rating group indexes, and/or as defined by the investment adviser. These definitions may not apply for purposes of this report, which may combine such sector sub-classifications for reporting ease. (c) Scheduled maturity dates and/or bonds that are subject to potential calls by issuers over the next five years. |

| (d) | For financial reporting purposes, credit quality ratings shown above reflect the highest rating assigned by either S&P Global Ratings or Moody’s Investors Service, Inc. if ratings differ. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change. |

| (e) | Rounds to less than 1% of total investments. |

| (f) | The investment adviser evaluates the credit quality of unrated investments based upon certain factors including, but not limited to, credit ratings for similar investments and financial analysis of sectors and individual investments. Using this approach, the investment adviser has deemed certain of these unrated securities as investment grade quality. As of February 28, 2022 and August 31, 2021, the market value of unrated securities deemed by the investment adviser to be investment grade represents 1% and 2%, respectively, of the Trust’s total investments. |

| 8 | 2 0 2 2 B L A C K R O C K S E M I - A N N U A L R E P O R T T O S H A R E H O L D E R S |

| Trust Summary as of February 28, 2022 |

BlackRock Virginia Municipal Bond Trust (BHV) |

Investment Objective

BlackRock Virginia Municipal Bond Trust’s (BHV) (the “Trust”) investment objective is to provide current income exempt from regular U.S. federal income tax and Virginia personal income taxes. The Trust seeks to achieve its investment objectives by investing primarily in municipal bonds exempt from U.S. federal income taxes (except that the interest may be subject to the U.S. federal alternative minimum tax) and Virginia personal income taxes. The Trust invests, under normal market conditions, at least 80% of its managed assets in municipal bonds that are investment grade quality at the time of investment or, if unrated, determined to be of comparable quality at the time of investment by the Trust’s investment adviser. The Trust may invest directly in such securities or synthetically through the use of derivatives.

No assurance can be given that the Trust’s investment objective will be achieved.

Trust Information

Symbol on New York Stock Exchange | BHV | |

Initial Offering Date | April 30, 2002 | |

Yield on Closing Market Price as of February 28, 2022 ($18.11)(a) | 3.01% | |

Tax Equivalent Yield(b) | 5.63% | |

Current Monthly Distribution per Common Share(c) | $0.0455 | |

Current Annualized Distribution per Common Share(c) | $0.5460 | |

Leverage as of February 28, 2022(d) | 41% |

| (a) | Yield on closing market price is calculated by dividing the current annualized distribution per share by the closing market price. Past performance is not an indication of future results. |

| (b) | Tax equivalent yield assumes the maximum marginal U.S. federal and state tax rate of 46.55%, which includes the 3.8% Medicare tax. Actual tax rates will vary based on income, exemptions and deductions. Lower taxes will result in lower tax equivalent yields. |

| (c) | The distribution rate is not constant and is subject to change. |

| (d) | Represents VRDP Shares and TOB Trusts as a percentage of total managed assets, which is the total assets of the Trust, including any assets attributable to VRDP Shares and TOB Trusts, minus the sum of its accrued liabilities. Does not reflect derivatives or other instruments that may give rise to economic leverage. For a discussion of leveraging techniques utilized by the Trust, please see The Benefits and Risks of Leveraging and Derivative Financial Instruments. |

Market Price and Net Asset Value Per Share Summary

| 02/28/22 | 08/31/21 | Change | High | Low | ||||||||||||||||

Closing Market Price | $ | 18.11 | $ | 18.75 | (3.41 | )% | $ | 19.73 | $ | 17.09 | ||||||||||

Net Asset Value | 14.73 | 15.73 | (6.36 | ) | 15.73 | 14.64 | ||||||||||||||

Performance

Returns for the period ended February 28, 2022 were as follows:

| Average Annual Total Returns | ||||||||||||||||

| 6-month | 1 Year | 5 Years | 10 Years | |||||||||||||

Trust at NAV(a)(b) | (4.88 | )% | (1.25 | )% | 2.84 | % | 3.61 | % | ||||||||

Trust at Market Price(a)(b) | (1.89 | ) | 15.77 | 6.85 | 3.79 | |||||||||||

Virginia Customized Reference Benchmark(c) | (2.53 | ) | (0.36 | ) | 3.37 | N/A | ||||||||||

Bloomberg Municipal Bond Index(d) | (3.09 | ) | (0.66 | ) | 3.24 | 3.15 | ||||||||||

S&P® Municipal Bond Index(e) | (2.79 | ) | (0.37 | ) | 3.18 | 3.22 | ||||||||||

Lipper Other States Municipal Debt Funds at NAV(f) | (4.28 | ) | (0.37 | ) | 3.89 | 3.97 | ||||||||||

Lipper Other States Municipal Debt Funds at Market Price(f) | (10.08 | ) | 0.46 | 4.24 | 3.73 | |||||||||||

| (a) | All returns reflect reinvestment of dividends and/or distributions at actual reinvestment prices. Performance results reflect the Trust’s use of leverage. |

| (b) | The Trust’s premium to NAV widened during the period, which accounts for the difference between performance based on market price and performance based on NAV. |

| (c) | The Virginia Customized Reference Benchmark is comprised of the Bloomberg Municipal Bond: Virginia Exempt Total Return Index Unhedged (90%) and the Virginia Bloomberg Municipal Bond: High Yield (non-Investment Grade) Total Return Index (10%). Effective October 1, 2021, the Trust changed its benchmarks from S&P Municipal Bond Index and Lipper Other States Municipal Debt Funds to Bloomberg Municipal Bond Index and the Virginia Customized Reference Benchmark. The investment adviser believes the new benchmarks are more appropriate reporting benchmarks for the Trust. The Virginia Customized Reference Benchmark commenced on September 30, 2016. |

| (d) | An unmanaged index that tracks the U.S. long term tax-exempt bond market, including state and local general obligation bonds, revenue bonds, pre-refunded bonds, and insured bonds. (e) A broad, market value-weighted index that seeks to measure the performance of the U.S. municipal bond market. |

| (f) | Average return. Returns reflect reinvestment of dividends and/or distributions at NAV on the ex-dividend date as calculated by Lipper. |

Performance results may include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles. Past performance is not an indication of future results.

The Trust is presenting the performance of one or more indices for informational purposes only. The Trust is actively managed and does not seek to track or replicate the performance of any index. The index performance shown is not intended to be indicative of the Trust’s investment strategies, portfolio components or past or future performance.

More information about the Trust’s historical performance can be found in the “Closed End Funds” section of blackrock.com.

T R U S T S U M M A R Y | 9 |

| Trust Summary as of February 28, 2022 (continued) |

BlackRock Virginia Municipal Bond Trust (BHV) |

The following discussion relates to the Trust’s absolute performance based on NAV:

Municipal bonds lost ground in the six-month period, ending a stretch of positive performance that began in mid-2020. Rising inflation prompted the Fed to shift toward tighter monetary policy, weighing heavily on the performance of fixed-income assets.

Most sectors and rating categories detracted from performance due to the broad nature of the market downturn. Positions in long-dated securities with maturities of greater than 20 years detracted from results. Higher-rated securities in the AA and single A categories, notably those in the dedicated tax and university sectors, also hurt performance. Non-rated high yield debt lagged as well. The underperformance was especially pronounced in the tobacco sector, where the Trust holds zero-coupon tobacco bonds with above-average interest rate sensitivity.

Holdings in pre-refunded debt further detracted. The market segment, which entered the period trading at rich levels, was adversely affected by its shorter-dated average maturities given expectations for Fed rate hikes.

On the positive side, the Trust’s use of U.S. Treasury futures to manage interest rate risk contributed to results. Holdings in short-dated securities with maturities of less than a year, which were less affected by the sell-off, also contributed modestly to performance.

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

Overview of the Trust’s Total Investments

SECTOR ALLOCATION

| Sector(a)(b) | 02/28/22 | 08/31/21 | ||||||

Transportation | 31 | % | 31 | % | ||||

Health | 20 | 19 | ||||||

State | 13 | 10 | ||||||

Education | 8 | 12 | ||||||

Tobacco | 8 | 7 | ||||||

Utilities | 7 | 7 | ||||||

County/City/Special District/School District | 7 | 7 | ||||||

Housing | 5 | 6 | ||||||

Corporate | 1 | 1 | ||||||

CALL/MATURITY SCHEDULE

| Calendar Year Ended December 31,(a)(c) | Percentage | |||

2022 | 17 | % | ||

2023 | 6 | |||

2024 | 4 | |||

| 2025 | 2 | |||

2026 | 7 | |||

CREDIT QUALITY ALLOCATION

| Credit Rating(a)(d) | 02/28/22 | 08/31/21 | ||||||

AAA/Aaa | 7 | % | 8 | % | ||||

AA/Aa | 49 | 48 | ||||||

A | 11 | 11 | ||||||

BBB/Baa | 9 | 6 | ||||||

BB/Ba | — | (e) | — | (e) | ||||

B | 4 | 4 | ||||||

N/R(f) | 20 | 23 | ||||||

| (a) | Excludes short-term securities. |

| (b) | For Trust compliance purposes, the Trust’s sector classifications refer to one or more of the sector sub-classifications used by one or more widely recognized market indexes or rating group indexes, and/or as defined by the investment adviser. These definitions may not apply for purposes of this report, which may combine such sector sub-classifications for reporting ease. |

| (c) | Scheduled maturity dates and/or bonds that are subject to potential calls by issuers over the next five years. |

| (d) | For financial reporting purposes, credit quality ratings shown above reflect the highest rating assigned by either S&P Global Ratings or Moody’s Investors Service, Inc. if ratings differ. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change. |

| (e) | Rounds to less than 1% of total investments. |

| (f) | The investment adviser evaluates the credit quality of unrated investments based upon certain factors including, but not limited to, credit ratings for similar investments and financial analysis of sectors and individual investments. Using this approach, the investment adviser has deemed certain of these unrated securities as investment grade quality. As of February 28, 2022 and August 31, 2021, the market value of unrated securities deemed by the investment adviser to be investment grade represents 6% and 5%, respectively, of the Trust’s total investments. |

| 10 | 2 0 2 2 B L A C K R O C K S E M I - A N N U A L R E P O R T T O S H A R E H O L D E R S |

Schedule of Investments (unaudited) February 28, 2022 |

BlackRock MuniHoldings New York Quality Fund, Inc. (MHN) (Percentages shown are based on Net Assets) |

| Security | Par (000) | Value | ||||||

Municipal Bonds |

| |||||||

Guam — 0.1% |

| |||||||

| Utilities — 0.1% | ||||||||

Guam Government Waterworks Authority, RB, Series A, | $ | 525 | $ | 617,512 | ||||

|

| |||||||

New York — 139.8% |

| |||||||

| Corporate — 4.4% | ||||||||

New York Liberty Development Corp., Refunding RB, 5.25%, 10/01/35 | 9,685 | 12,706,294 | ||||||

New York State Environmental Facilities Corp., RB, AMT, 2.75%, 09/01/50(a) | 970 | 994,176 | ||||||

New York Transportation Development Corp., RB | ||||||||

AMT, 5.00%, 10/01/35 | 525 | 626,755 | ||||||

AMT, 5.00%, 10/01/40 | 1,485 | 1,738,732 | ||||||

New York Transportation Development Corp., Refunding ARB | ||||||||

AMT, 2.25%, 08/01/26 | 1,830 | 1,834,954 | ||||||

AMT, 3.00%, 08/01/31 | 1,465 | 1,503,941 | ||||||

|

| |||||||

| 19,404,852 | ||||||||

| County/City/Special District/School District — 31.1% | ||||||||

City of New York, GO | ||||||||

Series F-1, 5.00%, 03/01/50 | 2,270 | 2,751,864 | ||||||

Sub-Series D-1, 5.00%, 08/01/31 | 945 | 994,191 | ||||||

Sub-Series D-1, 5.00%, 10/01/33 | 2,770 | 2,778,213 | ||||||

Sub-Series F-1, 5.00%, 04/01/43 | 4,550 | 5,313,203 | ||||||

City of New York, Refunding GO | ||||||||

Series E, 5.00%, 02/01/23(b) | 2,000 | 2,074,804 | ||||||

Series E, 5.50%, 08/01/25 | 2,710 | 2,875,822 | ||||||

Series E, 5.00%, 08/01/32 | 2,000 | 2,103,312 | ||||||

Series I, 5.00%, 08/01/22(b) | 490 | 498,872 | ||||||

City of Yonkers New York, GO | ||||||||

Series B, (AGM), 4.00%, 02/15/36 | 170 | 194,533 | ||||||

Series B, (AGM), 4.00%, 02/15/37 | 275 | 314,060 | ||||||

Series B, (AGM), 4.00%, 02/15/38 | 295 | 335,784 | ||||||

Series B, (AGM), 3.00%, 02/15/39 | 275 | 286,491 | ||||||

County of Nassau New York, GO | ||||||||

Series A, 5.00%, 01/15/31 | 1,400 | 1,619,481 | ||||||

Series B, (AGM), 5.00%, 07/01/45 | 1,815 | 2,132,928 | ||||||

County of Nassau New York, Refunding GO | ||||||||

Series A, (AGM), 4.00%, 04/01/50 | 3,720 | 4,194,579 | ||||||

Series C, 5.00%, 10/01/31 | 1,980 | 2,325,771 | ||||||

County of Suffolk New York, Refunding GO, Catholic Health Services, (BAM), 2.00%, 06/15/34 | 3,250 | 3,045,656 | ||||||

Erie County Industrial Development Agency, Refunding RB, Series A, (SAW), 5.00%, 05/01/28 | 1,685 | 1,895,660 | ||||||

Hudson Yards Infrastructure Corp., Refunding RB | ||||||||

Series A, 5.00%, 02/15/39 | 2,285 | 2,629,743 | ||||||

Series A, 5.00%, 02/15/42 | 5,975 | 6,856,127 | ||||||

Series A, 4.00%, 02/15/44 | 2,425 | 2,632,755 | ||||||

Ithaca City School District, Refunding GO | ||||||||

(BAM SAW), 2.00%, 06/15/33 | 365 | 355,614 | ||||||

(BAM SAW), 2.00%, 06/15/34 | 720 | 695,069 | ||||||

Mahopac Central School District, Refunding GO, (SAW), 2.00%, 06/01/32 | 555 | 554,222 | ||||||

New York City Industrial Development Agency, RB, CAB, (AGC), 0.00%, 03/01/39(c) | 1,380 | 858,457 | ||||||

New York City Industrial Development Agency, Refunding RB | 1,830 | 1,723,123 | ||||||

| Security | Par (000) | Value | ||||||

| County/City/Special District/School District (continued) | ||||||||

New York City Industrial Development Agency, Refunding RB (continued) | ||||||||

Series A, AMT, 5.00%, 07/01/28 | $ | 820 | $ | 828,913 | ||||

New York City Transitional Finance Authority Future Tax Secured Revenue, RB | ||||||||

Series A-1, 5.00%, 11/01/38 | 950 | 1,006,241 | ||||||

Series A-2, 5.00%, 08/01/38 | 3,440 | 3,997,903 | ||||||

Sub-Series A-1, 5.00%, 08/01/40 | 860 | 1,010,264 | ||||||

Sub-Series A-3, 4.00%, 08/01/43 | 2,790 | 3,040,135 | ||||||

Sub-Series B-1, 5.00%, 11/01/35 | 2,100 | 2,261,389 | ||||||

Sub-Series B-1, 5.00%, 11/01/36 | 1,690 | 1,816,786 | ||||||

Sub-Series B-1, 5.00%, 11/01/38 | 1,455 | 1,632,546 | ||||||

Sub-Series E-1, 5.00%, 02/01/39 | 2,730 | 3,153,240 | ||||||

Sub-Series E-1, 5.00%, 02/01/43 | 2,510 | 2,867,723 | ||||||

Sub-Series F-1, 5.00%, 05/01/42 | 8,825 | 10,146,226 | ||||||

New York Convention Center Development Corp., RB, CAB(c) | ||||||||

Series B, Sub Lien, 0.00%, 11/15/32 | 565 | 426,190 | ||||||

Series B, Sub Lien, 0.00%, 11/15/42 | 2,185 | 1,118,294 | ||||||

Series B, Sub Lien, 0.00%, 11/15/47 | 5,600 | 2,336,443 | ||||||

Series B, Sub Lien, 0.00%, 11/15/48 | 2,665 | 1,106,417 | ||||||

Series B, Sub Lien, (AGM-CR), 0.00%, 11/15/55 | 2,485 | 771,235 | ||||||

Series B, Sub Lien, (AGM-CR), 0.00%, 11/15/56 | 3,765 | 1,126,172 | ||||||

New York Convention Center Development Corp., Refunding RB | ||||||||

5.00%, 11/15/40 | 6,150 | 6,898,443 | ||||||

5.00%, 11/15/45 | 12,215 | 13,614,973 | ||||||

New York Liberty Development Corp., Refunding RB | ||||||||

3.13%, 09/15/50(d) | 3,105 | 3,060,471 | ||||||

Class 2, 5.00%, 09/15/43 | 3,430 | 3,435,011 | ||||||

Series 1, Class 1, 5.00%, 11/15/44(e) | 5,075 | 5,439,847 | ||||||

Series A, 2.88%, 11/15/46 | 1,625 | 1,544,944 | ||||||

New York State Dormitory Authority, RB, Series A, 5.00%, 02/15/23(b) | 4,995 | 5,188,674 | ||||||

New York State Dormitory Authority, Refunding RB, Series A, 5.00%, 07/01/22(b) | 1,490 | 1,511,613 | ||||||

South Glens Falls Central School District, Refunding GO | ||||||||

Series A, (SAW), 2.00%, 07/15/34 | 1,160 | 1,132,159 | ||||||

Series A, (SAW), 2.00%, 07/15/35 | 685 | 662,130 | ||||||

Town of Oyster Bay New York, Refunding GO, Series A, (AGM), 2.00%, 03/01/35 | 375 | 352,548 | ||||||

Trust for Cultural Resources of The City of New York, Refunding RB, Series A, 5.00%, 08/01/23(b) | 2,840 | 2,998,736 | ||||||

|

| |||||||

| 136,526,000 | ||||||||

| Education — 14.4% | ||||||||

Albany Capital Resource Corp., Refunding RB | ||||||||

4.00%, 07/01/41 | 740 | 754,789 | ||||||

4.00%, 07/01/51 | 765 | 749,929 | ||||||

Series A, 5.00%, 12/01/30 | 250 | 270,823 | ||||||

Series A, 5.00%, 12/01/32 | 100 | 108,193 | ||||||

Series A, 4.00%, 12/01/34 | 110 | 114,543 | ||||||

Build NYC Resource Corp., RB, 4.00%, 06/15/41 | 415 | 441,382 | ||||||

Build NYC Resource Corp., Refunding RB | ||||||||

4.00%, 08/01/42 | 525 | 571,071 | ||||||

5.00%, 08/01/47 | 535 | 615,610 | ||||||

Series A, 5.00%, 06/01/43 | 450 | 482,958 | ||||||

Dobbs Ferry Local Development Corp., RB, 5.00%, 07/01/39 | 750 | 808,856 | ||||||

S C H E D U L E O F I N V E S T M E N T S | 11 |

Schedule of Investments (unaudited) (continued) February 28, 2022 |

BlackRock MuniHoldings New York Quality Fund, Inc. (MHN) (Percentages shown are based on Net Assets) |

| Security | Par (000) | Value | ||||||

| Education (continued) | ||||||||

Dutchess County Local Development Corp., RB | ||||||||

5.00%, 07/01/43 | $ | 570 | $ | 670,274 | ||||

5.00%, 07/01/48 | 855 | 999,646 | ||||||

Dutchess County Local Development Corp., Refunding RB | ||||||||

5.00%, 07/01/42 | 985 | 1,136,602 | ||||||

4.00%, 07/01/46 | 1,865 | 2,004,799 | ||||||

Hempstead Town Local Development Corp., Refunding RB | ||||||||

5.00%, 07/01/47 | 1,030 | 1,185,134 | ||||||

Series A, 3.00%, 07/01/51 | 2,320 | 2,284,295 | ||||||

Madison County Capital Resource Corp., RB | ||||||||

Series B, 5.00%, 07/01/40 | 685 | 760,490 | ||||||

Series B, 5.00%, 07/01/43 | 2,480 | 2,744,708 | ||||||

Monroe County Industrial Development Corp., Refunding RB | ||||||||

Series A, 5.00%, 07/01/23(b) | 1,240 | 1,305,952 | ||||||

Series A, 4.00%, 07/01/39 | 350 | 374,291 | ||||||

New York State Dormitory Authority, RB 1st Series, (AMBAC), | ||||||||

5.50%, 07/01/40 | 3,500 | 4,913,429 | ||||||

Series A, 5.00%, 07/01/46 | 250 | 298,618 | ||||||

Series A, 5.00%, 07/01/51 | 590 | 703,228 | ||||||

Series B, 5.00%, 07/01/22(b) | 3,000 | 3,043,515 | ||||||

New York State Dormitory Authority, Refunding RB 5.00%, 07/01/44 | 1,900 | 2,047,803 | ||||||

Series A, 5.00%, 07/01/22(b) | 7,180 | 7,286,027 | ||||||

Series A, 5.25%, 07/01/23(b) | 11,190 | 11,818,173 | ||||||

Series A, 5.00%, 07/01/27(b) | 1,540 | 1,807,758 | ||||||

Series A, 5.00%, 07/01/35 | 1,030 | 1,139,797 | ||||||

Series A, 4.00%, 07/01/37 | 510 | 544,432 | ||||||

Series A, 5.00%, 07/01/37 | 2,005 | 2,207,288 | ||||||

Series A, 5.00%, 07/01/43 | 1,520 | 1,682,070 | ||||||

Orange County Funding Corp., Refunding RB | ||||||||

Series A, 5.00%, 07/01/37 | 715 | 722,649 | ||||||

Series A, 5.00%, 07/01/42 | 445 | 449,573 | ||||||

Troy Capital Resource Corp., Refunding RB 4.00%, 09/01/30 | 190 | 223,926 | ||||||

4.00%, 09/01/31 | 105 | 123,558 | ||||||

4.00%, 09/01/32 | 160 | 187,179 | ||||||

4.00%, 09/01/33 | 45 | 52,240 | ||||||

4.00%, 09/01/34 | 75 | 86,350 | ||||||

4.00%, 09/01/35 | 90 | 103,065 | ||||||

4.00%, 09/01/36 | 125 | 142,651 | ||||||

4.00%, 09/01/40 | 1,320 | 1,493,835 | ||||||

Trust for Cultural Resources of The City of New York, Refunding RB | ||||||||

Series A, 5.00%, 07/01/37 | 1,775 | 1,920,319 | ||||||

Series A, 5.00%, 07/01/41 | 750 | 808,140 | ||||||

Yonkers Economic Development Corp., Refunding RB | ||||||||

Series A, 5.00%, 10/15/40 | 320 | 364,836 | ||||||

Series A, 5.00%, 10/15/50 | 540 | 605,107 | ||||||

|

| |||||||

| 63,159,911 | ||||||||

| Health — 5.5% | ||||||||

Dutchess County Local Development Corp., RB, | ||||||||

Series B, 4.00%, 07/01/41 | 4,595 | 4,940,066 | ||||||

Dutchess County Local Development Corp., Refunding RB | ||||||||

Series B, 4.00%, 07/01/37 | 260 | 281,264 | ||||||

Series B, 4.00%, 07/01/38 | 275 | 296,737 | ||||||

Huntington Local Development Corp., RB, Series A, 5.25%, 07/01/56 | 240 | 258,467 | ||||||

| Security | Par (000) | Value | ||||||

| Health (continued) | ||||||||

Monroe County Industrial Development Corp., RB | ||||||||

4.00%, 12/01/41 | $ | 545 | $ | 572,697 | ||||

5.00%, 12/01/46 | 800 | 883,584 | ||||||

Series A, 5.00%, 12/01/37 | 1,180 | 1,210,593 | ||||||

Monroe County Industrial Development Corp., Refunding RB | ||||||||

3.00%, 12/01/40 | 1,010 | 949,773 | ||||||

4.00%, 12/01/46 | 2,415 | 2,616,744 | ||||||

New York State Dormitory Authority, RB | ||||||||

Series C, 4.25%, 05/01/39 | 1,000 | 1,004,622 | ||||||

Series D, 4.25%, 05/01/39 | 685 | 688,166 | ||||||

New York State Dormitory Authority, Refunding RB | ||||||||

1st Series, 5.00%, 07/01/42 | 2,200 | 2,554,704 | ||||||

Series A, 5.00%, 05/01/32 | 2,645 | 2,923,460 | ||||||

Catholic Health Services, 4.00%, 07/01/45 | 675 | 687,278 | ||||||

Oneida County Local Development Corp., Refunding RB, (AGM), 3.00%, 12/01/44 | 2,540 | 2,600,223 | ||||||

Suffolk County Economic Development Corp., RB, Series C, Catholic Health Services, 5.00%, 07/01/32 | 460 | 496,744 | ||||||

Westchester County Local Development Corp., Refunding RB, 5.00%, 07/01/46(e) | 1,140 | 1,186,705 | ||||||

|

| |||||||

| 24,151,827 | ||||||||

| Housing — 11.2% | ||||||||

New York City Housing Development Corp., RB, M/F Housing | ||||||||

4.00%, 11/01/43 | 640 | 661,049 | ||||||

Series A, (HUD SECT 8), 2.70%, 08/01/45 | 225 | 202,815 | ||||||

Series A, 2.90%, 11/01/50 | 2,725 | 2,535,286 | ||||||

Series B-1, 5.25%, 07/01/32 | 6,505 | 6,763,899 | ||||||

Series B-1, 5.00%, 07/01/33 | 1,375 | 1,422,394 | ||||||

Series D-1-B, 4.20%, 11/01/40 | 450 | 460,616 | ||||||

Series F-1, (FHA), 2.60%, 11/01/56 | 4,545 | 3,920,163 | ||||||

Series G-1, 3.90%, 05/01/45 | 450 | 454,284 | ||||||

Series H, 2.55%, 11/01/45 | 1,055 | 958,615 | ||||||

Series H, 2.60%, 11/01/50 | 1,810 | 1,574,177 | ||||||

Series I-1, (FHA), 2.55%, 11/01/45 | 3,180 | 2,839,826 | ||||||

Series I-1-A, 3.95%, 11/01/36 | 450 | 467,243 | ||||||

Series I-1-A, 4.05%, 11/01/41 | 450 | 466,332 | ||||||

Series J, 3.05%, 11/01/49 | 595 | 575,989 | ||||||

New York City Housing Development Corp., Refunding RB, Series F-1-A, 3.30%, 11/01/46 | 460 | 462,524 | ||||||

New York City Housing Development Corp., Refunding RB, M/F Housing | ||||||||

Series B-1-A, 3.65%, 11/01/49 | 1,040 | 1,049,684 | ||||||

Series B-1-A, 3.75%, 11/01/54 | 1,435 | 1,450,782 | ||||||

New York State Housing Finance Agency, RB, M/F Housing | ||||||||

Series B, (FHLMC SONYMA, FNMA, GNMA), 4.00%, 11/01/42. | 845 | 874,521 | ||||||

Series C, (FHLMC, FNMA, GNMA), 3.38%, 11/01/49 . | 170 | 170,523 | ||||||

Series D, (SONYMA), 3.80%, 11/01/49 | 1,700 | 1,737,024 | ||||||

Series E, (SONYMA), 3.80%, 11/01/49 | 945 | 965,581 | ||||||

Series H, 4.15%, 11/01/43 | 1,375 | 1,445,465 | ||||||

Series H, 4.20%, 11/01/48 | 905 | 943,518 | ||||||

Series J-1, (SONYMA HUD SECT 8), 3.00%, 11/01/61 | 675 | 606,533 | ||||||

Series J-1, (SONYMA HUD SECT 8), 3.10%, 05/01/66 | 910 | 825,709 | ||||||

Series M-1, (FHA, SONYMA), 2.65%, 11/01/54 | 1,635 | 1,419,859 | ||||||

Series P, 3.15%, 11/01/54 | 1,100 | 1,040,189 | ||||||

Series A, AMT, 4.65%, 11/15/38 | 1,000 | 1,001,213 | ||||||

| 12 | 2 0 2 2 B L A C K R O C K S E M I - A N N U A L R E P O R T T O S H A R E H O L D E R S |

Schedule of Investments (unaudited) (continued) February 28, 2022 |

BlackRock MuniHoldings New York Quality Fund, Inc. (MHN) (Percentages shown are based on Net Assets) |

| Security | Par (000) | Value | ||||||

| Housing (continued) | ||||||||

State of New York Mortgage Agency, RB, S/F Housing | ||||||||

Series 225, 2.45%, 10/01/45 | $ | 400 | $ | 363,468 | ||||

Series 239, (SONYMA), 2.70%, 10/01/47 | 1,365 | 1,283,709 | ||||||

State of New York Mortgage Agency, Refunding RB | ||||||||

Series 218, AMT, 3.60%, 04/01/33 | 905 | 935,502 | ||||||

Series 218, AMT, 3.85%, 04/01/38 | 155 | 159,062 | ||||||

State of New York Mortgage Agency, Refunding RB, S/F Housing | ||||||||

Series 190, 3.80%, 10/01/40 | 1,395 | 1,398,494 | ||||||

Series 231, 2.50%, 10/01/46 | 3,000 | 2,730,861 | ||||||

AMT, 2.00%, 04/01/30 | 855 | 815,891 | ||||||

Series 194, AMT, 3.80%, 04/01/28 | 2,065 | 2,105,040 | ||||||

Yonkers Industrial Development Agency, RB, AMT, (SONYMA), 5.25%, 04/01/37 | 2,000 | 2,003,954 | ||||||

|

| |||||||

| 49,091,794 | ||||||||

| Other — 1.9% | ||||||||

New York Liberty Development Corp., Refunding RB | ||||||||

2.75%, 11/15/41 | 2,700 | 2,565,200 | ||||||

Class 1, 4.00%, 09/15/35 | 885 | 885,875 | ||||||

Series-A, 3.00%, 11/15/51 | 4,860 | 4,678,114 | ||||||

|

| |||||||

| 8,129,189 | ||||||||

| State — 12.2% | ||||||||

Hudson Yards Infrastructure Corp. Refunding RB, 4.00%, 02/15/44 | 910 | 1,038,288 | ||||||

New York City Transitional Finance Authority Building Aid Revenue, RB, (SAW), 3.00%, 07/15/49 | 4,500 | 4,460,148 | ||||||

New York City Transitional Finance Authority Building Aid Revenue, Refunding RB, Series S-3, Subordinate, (SAW), 4.00%, 07/15/38 | 5,045 | 5,584,270 | ||||||

New York State Dormitory Authority, RB | ||||||||

Series 2015B-C, 5.00%, 03/15/37 | 1,500 | 1,676,748 | ||||||

Series A, 5.00%, 03/15/41 | 7,125 | 8,215,638 | ||||||

Series A, 5.00%, 02/15/42 | 7,500 | 8,489,647 | ||||||

Series B, 5.00%, 03/15/37 | 3,000 | 3,008,838 | ||||||

Series B, 5.00%, 03/15/38 | 1,000 | 1,154,196 | ||||||

Series B, 5.00%, 03/15/39 | 1,465 | 1,691,225 | ||||||

Series B, 5.00%, 03/15/42 | 4,600 | 4,613,101 | ||||||

New York State Dormitory Authority, Refunding RB | ||||||||

Series A, 4.00%, 03/15/46 | 5,100 | 5,656,874 | ||||||

Series C, 5.00%, 03/15/38 | 100 | 118,165 | ||||||

Series E, 5.00%, 03/15/41 | 2,800 | 3,345,608 | ||||||

New York State Urban Development Corp., RB, Series C, 5.00%, 03/15/32 | 2,000 | 2,078,482 | ||||||

Sales Tax Asset Receivable Corp., Refunding RB, Series A, 4.00%, 10/15/24(b) | 2,070 | 2,222,280 | ||||||

|

| |||||||

| 53,353,508 | ||||||||

| Tobacco — 2.8% | ||||||||

Chautauqua Tobacco Asset Securitization Corp., Refunding RB | ||||||||

4.75%, 06/01/39 | 1,875 | 1,955,299 | ||||||

5.00%, 06/01/48 | 680 | 706,054 | ||||||

New York Counties Tobacco Trust VI, Refunding RB | ||||||||

Series A-2-B, 5.00%, 06/01/45 | 2,010 | 2,179,061 | ||||||

Series A-2-B, 5.00%, 06/01/51 | 765 | 827,071 | ||||||

Series B, 5.00%, 06/01/41 | 575 | 629,491 | ||||||

Niagara Tobacco Asset Securitization Corp., Refunding RB 5.25%, 05/15/34 | 1,495 | 1,604,981 | ||||||

| Security | Par (000) | Value | ||||||

| Tobacco (continued) | ||||||||

Niagara Tobacco Asset Securitization Corp., Refunding RB (continued) | ||||||||

5.25%, 05/15/40 | $ | 1,500 | $ | 1,607,244 | ||||

TSASC, Inc., Refunding RB, Series A, 5.00%, 06/01/35 | 260 | 292,792 | ||||||

Westchester Tobacco Asset Securitization Corp., Refunding RB, Sub-Series C, 4.00%, 06/01/42 | 2,135 | 2,266,796 | ||||||

|

| |||||||

| 12,068,789 | ||||||||

| Transportation — 39.8% | ||||||||

Buffalo & Fort Erie Public Bridge Authority, RB | ||||||||

5.00%, 01/01/42 | 1,565 | 1,774,938 | ||||||

5.00%, 01/01/47 | 750 | 846,552 | ||||||

Metropolitan Transportation Authority, RB | ||||||||

Series A, 5.00%, 05/15/23(b) | 3,000 | 3,144,315 | ||||||

Series A, 5.00%, 11/15/42 | 3,500 | 4,016,439 | ||||||

Series A-1, 5.25%, 11/15/23(b) | 3,240 | 3,468,164 | ||||||

Series B, 5.25%, 11/15/44 | 1,000 | 1,062,950 | ||||||

Series E, 5.00%, 11/15/38 | 8,750 | 9,169,650 | ||||||

Sub-Series B-3, 5.00%, 11/15/23(b) | 1,000 | 1,066,215 | ||||||

Metropolitan Transportation Authority, Refunding RB | ||||||||

Series A, 5.00%, 11/15/41 | 1,000 | 1,023,389 | ||||||

Series A, (AGM), 4.00%, 11/15/46 | 855 | 921,103 | ||||||

Series A1, 5.00%, 11/15/37 | 1,500 | 1,680,486 | ||||||

Series C-1, 4.75%, 11/15/45 | 1,505 | 1,710,141 | ||||||

Series C-1, 5.00%, 11/15/56 | 1,920 | 2,093,136 | ||||||

Series D, 5.00%, 11/15/30 | 885 | 908,380 | ||||||

Sub-Series B-1, 5.00%, 11/15/31 | 4,000 | 4,245,448 | ||||||

Sub-Series B-1, 5.00%, 11/15/51 | 2,360 | 2,661,254 | ||||||

Sub-Series B-2, 4.00%, 11/15/34 | 2,500 | 2,768,725 | ||||||

Sub-Series C-1, 5.00%, 11/15/34 | 1,845 | 2,034,288 | ||||||

MTA Hudson Rail Yards Trust Obligations, Refunding RB, Series A, 5.00%, 11/15/56 | 5,410 | 5,681,544 | ||||||

New York City Transitional Finance Authority | 2,275 | 2,586,013 | ||||||

New York Liberty Development Corp., Refunding RB | ||||||||

Series 1, 4.00%, 02/15/43 | 2,725 | 2,989,039 | ||||||

Series 1, 2.75%, 02/15/44 | 2,845 | 2,639,563 | ||||||

Series1, 2.25%, 02/15/41 | 1,800 | 1,541,275 | ||||||

New York State Thruway Authority, RB | ||||||||

Series A-1, 3.00%, 03/15/48 | 2,250 | 2,250,808 | ||||||

Series N, 5.00%, 01/01/35 | 450 | 542,741 | ||||||

Series A, Junior Lien, 5.00%, 01/01/41 | 1,770 | 1,972,633 | ||||||

Series A, Junior Lien, 5.25%, 01/01/56 | 1,080 | 1,204,939 | ||||||

New York State Thruway Authority, Refunding RB | ||||||||

4.00%, 01/01/48 | 5,630 | 6,287,894 | ||||||

Series J, 5.00%, 01/01/41 | 5,000 | 5,304,585 | ||||||

Series K, 5.00%, 01/01/29 | 1,750 | 1,922,720 | ||||||

Series K, 5.00%, 01/01/31 | 1,000 | 1,097,431 | ||||||

Series L, 5.00%, 01/01/35 | 810 | 943,756 | ||||||

Series B, Subordinate, 3.00%, 01/01/53 | 225 | 215,658 | ||||||

Series B, Subordinate, 4.00%, 01/01/53 | 815 | 884,674 | ||||||

New York Transportation Development Corp., ARB | ||||||||

Series A, AMT, (AGM-CR), 4.00%, 07/01/41 | 1,250 | 1,287,244 | ||||||

Series A, AMT, 5.00%, 07/01/41 | 1,805 | 1,935,249 | ||||||

Series A, AMT, 5.00%, 07/01/46 | 1,885 | 2,014,104 | ||||||

Series A, AMT, 5.25%, 01/01/50 | 11,605 | 12,412,534 | ||||||

New York Transportation Development Corp., RB, AMT, 4.00%, 04/30/53 | 1,535 | 1,666,554 | ||||||

S C H E D U L E O F I N V E S T M E N T S | 13 |

Schedule of Investments (unaudited) (continued) February 28, 2022 |

BlackRock MuniHoldings New York Quality Fund, Inc. (MHN) (Percentages shown are based on Net Assets) |

| Security | Par (000) | Value | ||||||

| Transportation (continued) | ||||||||

New York Transportation Development Corp., Refunding RB | ||||||||

5.00%, 12/01/32 | $ | 1,550 | $ | 1,830,308 | ||||

5.00%, 12/01/36 | 2,125 | 2,502,221 | ||||||

Series A, AMT, 5.00%, 12/01/29 | 1,250 | 1,452,416 | ||||||

Series A, Class A, AMT, 4.00%, 12/01/41 | 225 | 240,446 | ||||||

Series A, Class A, AMT, 4.00%, 12/01/42 | 225 | 239,482 | ||||||

Niagara Frontier Transportation Authority, Refunding ARB | ||||||||

AMT, 5.00%, 04/01/34 | 100 | 118,952 | ||||||

AMT, 5.00%, 04/01/35 | 90 | 106,843 | ||||||

AMT, 5.00%, 04/01/36 | 95 | 112,486 | ||||||

AMT, 5.00%, 04/01/37 | 110 | 129,952 | ||||||

AMT, 5.00%, 04/01/38 | 55 | 64,879 | ||||||

AMT, 5.00%, 04/01/39 | 80 | 94,269 | ||||||

Port Authority of New York & New Jersey, ARB, Consolidated, 220th Series, AMT, 4.00%, 11/01/59 | 4,905 | 5,249,208 | ||||||

Port Authority of New York & New Jersey, Refunding ARB | ||||||||

Consolidated, 183th Series, 4.00%, 06/15/44 | 1,500 | 1,549,317 | ||||||

Series 179, 5.00%, 12/01/38 | 1,390 | 1,470,778 | ||||||

Series 211th, 4.00%, 09/01/43 | 5,000 | 5,524,710 | ||||||

178th Series, AMT, 5.00%, 12/01/43 | 750 | 791,338 | ||||||

195th Series, AMT, 5.00%, 04/01/36 | 1,400 | 1,590,021 | ||||||

Consolidated, 177th Series, AMT, 4.00%, 01/15/43 | 285 | 288,582 | ||||||

Consolidated, 206th Series, AMT, 5.00%, 11/15/42 | 2,375 | 2,721,360 | ||||||

Series 178th, AMT, 5.00%, 12/01/33 | 1,000 | 1,057,762 | ||||||

Series 223, AMT, 4.00%, 07/15/40 | 2,825 | 3,146,369 | ||||||

Triborough Bridge & Tunnel Authority, RB | ||||||||

Series A, 4.00%, 11/15/54 | 950 | 1,059,666 | ||||||

Series B, 5.00%, 11/15/40 | 940 | 1,056,737 | ||||||

Series B, 5.00%, 11/15/45 | 820 | 915,208 | ||||||

Series C-1A, Senior Lien, 5.00%, 05/15/51 | 2,275 | 2,804,042 | ||||||

Triborough Bridge & Tunnel Authority, Refunding RB | ||||||||

4.00%, 05/15/51 | 7,590 | 8,548,139 | ||||||

Series A, 5.00%, 11/15/36 | 1,000 | 1,026,042 | ||||||

Series A, 5.00%, 11/15/41 | 5,000 | 5,646,795 | ||||||

Series A, 5.25%, 11/15/45 | 1,280 | 1,426,954 | ||||||

Series A, 5.00%, 11/15/50 | 3,000 | 3,298,098 | ||||||

Series B, 5.00%, 11/15/38 | 8,225 | 9,546,971 | ||||||

Series C, 5.00%, 11/15/37 | 870 | 1,050,231 | ||||||

Triborough Bridge & Tunnel Authority, Refunding RB, CAB, Series B, 0.00%, 11/15/32(c) | 7,670 | 5,980,752 | ||||||

|

| |||||||

| 174,617,865 | ||||||||

| Utilities — 16.5% | ||||||||

Long Island Power Authority, RB 5.00%, 09/01/35 | 1,000 | 1,196,744 | ||||||

5.00%, 09/01/36 | 825 | 967,249 | ||||||

5.00%, 09/01/37 | 3,175 | 3,792,572 | ||||||

5.00%, 09/01/42 | 280 | 325,707 | ||||||

5.00%, 09/01/47 | 905 | 1,049,102 | ||||||

Long Island Power Authority, Refunding RB | ||||||||

Series B, 5.00%, 09/01/41 | 475 | 541,651 | ||||||

Series B, 5.00%, 09/01/46 | 660 | 749,313 | ||||||

New York City Water & Sewer System, RB | ||||||||

Series DD-1, 4.00%, 06/15/49. | 1,135 | 1,246,703 | ||||||

Series DD-1, 3.00%, 06/15/50 | 795 | 803,211 | ||||||

Series CC-1, Subordinate, 3.00%, 06/15/51 | 2,270 | 2,297,258 | ||||||

Series CC-1, Subordinate, 4.00%, 06/15/51 | 4,545 | 5,124,324 | ||||||

| Security | Par (000) | Value | ||||||

| Utilities (continued) | ||||||||

New York City Water & Sewer System, Refunding RB | ||||||||

Series DD, 5.25%, 06/15/47 | $ | 3,850 | $ | 4,452,506 | ||||

Series EE, 5.00%, 06/15/40 | 4,290 | 5,032,410 | ||||||

Series FF, 5.00%, 06/15/40 | 2,000 | 2,356,652 | ||||||

Series HH, 5.00%, 06/15/39 | 2,250 | 2,498,960 | ||||||

Sub-Series AA-1, 3.00%, 06/15/50 | 1,370 | 1,390,969 | ||||||

New York State Environmental Facilities Corp., RB | ||||||||

Series B, 5.00%, 09/15/40 | 3,170 | 3,503,487 | ||||||

Series B, Subordinate, 5.00%, 06/15/48 | 1,120 | 1,332,140 | ||||||

New York State Environmental Facilities Corp., Refunding RB | ||||||||

Series A, 5.00%, 06/15/40 | 1,545 | 1,720,273 | ||||||

Series A, 5.00%, 06/15/45 | 7,935 | 8,826,045 | ||||||

Series A, Subordinate, 4.00%, 06/15/46 | 1,000 | 1,092,905 | ||||||

Suffolk County Water Authority RB, Series B, 3.00%, 06/01/45 | 4,500 | 4,614,701 | ||||||

Utility Debt Securitization Authority, Refunding RB, | ||||||||

Series TE, Restructured, 5.00%, 12/15/41 | 15,490 | 16,430,878 | ||||||

Western Nassau County Water Authority, RB, Series A, 5.00%, 04/01/25(b) | 1,065 | 1,185,583 | ||||||

|

| |||||||

| 72,531,343 | ||||||||

|

| |||||||

Total Municipal Bonds in New York | 613,035,078 | |||||||

Puerto Rico — 5.0% |

| |||||||

| State — 5.0% | ||||||||

Puerto Rico Sales Tax Financing Corp. Sales Tax Revenue, RB | ||||||||

Series A-1, Restructured, 4.75%, 07/01/53 | 783 | 863,211 | ||||||

Series A-1, Restructured, 5.00%, 07/01/58 | 5,368 | 5,988,954 | ||||||

Series A-2, Restructured, 4.33%, 07/01/40 | 10,319 | 11,323,018 | ||||||

Series A-2, Restructured, 4.78%, 07/01/58 | 390 | 430,277 | ||||||

Series B-1, Restructured, 4.75%, 07/01/53 | 620 | 683,588 | ||||||

Series B-2, Restructured, 4.78%, 07/01/58 | 601 | 662,727 | ||||||

Puerto Rico Sales Tax Financing Corp. Sales Tax Revenue, RB, CAB, Series A-1, Restructured, 0.00%, 07/01/46(c) | 6,358 | 2,067,590 | ||||||

|

| |||||||

Total Municipal Bonds in Puerto Rico |

| 22,019,365 | ||||||

|

| |||||||

| Total Municipal Bonds — 144.9% (Cost: $608,684,626) | 635,671,955 | |||||||

|

| |||||||

Municipal Bonds Transferred to Tender Option Bond Trusts(f) |

| |||||||

New York — 19.8% | ||||||||

| County/City/Special District/School District — 1.2% | ||||||||

City of New York, GO, Sub-Series I-1, 5.00%, 03/01/36 | 2,500 | 2,675,436 | ||||||

New York Liberty Development Corp., Refunding RB, Class 1, 5.00%, 09/15/40 | 2,610 | 2,613,518 | ||||||

|

| |||||||

| 5,288,954 | ||||||||

| Education — 1.7% | ||||||||

Monroe County Industrial Development Corp., Refunding RB, 4.00%, 07/01/50 | 4,888 | 5,424,507 | ||||||

Trust for Cultural Resources of The City of New York, Refunding RB, Series A, 5.00%, 08/01/23(b) | 1,981 | 2,091,984 | ||||||

|

| |||||||

| 7,516,491 | ||||||||

| Housing — 3.6% | ||||||||

New York City Housing Development Corp., RB, M/F Housing, Series C-1A, 4.00%, 11/01/53 | 2,267 | 2,308,306 | ||||||

New York City Housing Development Corp., Refunding RB, Series A, 4.25%, 11/01/43 | 3,630 | 3,849,163 | ||||||

| 14 | 2 0 2 2 B L A C K R O C K S E M I - A N N U A L R E P O R T T O S H A R E H O L D E R S |

Schedule of Investments (unaudited) (continued) February 28, 2022 |

BlackRock MuniHoldings New York Quality Fund, Inc. (MHN) (Percentages shown are based on Net Assets) |

| Security | Par (000) | Value | ||||||

| Housing (continued) | ||||||||

New York City Housing Development Corp., Refunding RB, M/F Housing, Series B-1-A, 3.85%, 05/01/58 | $ | 2,175 | $ | 2,204,625 | ||||

New York State Housing Finance Agency, RB, M/F Housing, Series I, 4.05%, 11/01/48 | 4,543 | 4,695,408 | ||||||

New York State Housing Finance Agency, Refunding RB, Series C, 3.85%, 11/01/39 | 2,002 | 2,103,898 | ||||||

State of New York Mortgage Agency, Refunding RB, S/F Housing, Series 192, 3.80%, 10/01/31 | 360 | 364,798 | ||||||

|

| |||||||

| 15,526,198 | ||||||||

| State — 5.0% | ||||||||

New York State Dormitory Authority, RB, Series A, 5.00%, 03/15/32 | 2,000 | 2,377,971 | ||||||

New York State Dormitory Authority, Refunding RB, Series A, 5.00%, 03/15/40(g) | 2,950 | 3,486,533 | ||||||

New York State Urban Development Corp., Refunding RB, Series A, 5.00%, 03/15/45 | 1,471 | 1,627,491 | ||||||

Sales Tax Asset Receivable Corp., Refunding RB(b) | ||||||||

Series A, 4.00%, 10/15/24 | 6,000 | 6,441,393 | ||||||

Series A, 5.00%, 10/15/24 | 7,380 | 8,102,436 | ||||||

|

| |||||||

| 22,035,824 | ||||||||

| Transportation — 5.2% | ||||||||

New York State Thruway Authority, Refunding RB, Subordinate, Series B, 4.00%, 01/01/45(g) | 4,948 | 5,393,078 | ||||||

Port Authority of New York & New Jersey, ARB, AMT, Series 221, 4.00%, 07/15/60 | 2,325 | 2,499,766 | ||||||

Port Authority of New York & New Jersey, Refunding ARB, 194th Series, 5.25%, 10/15/55 | 3,405 | 3,809,773 | ||||||

Triborough Bridge & Tunnel Authority, Refunding RB, Series A, 5.00%, 11/15/46. | 10,000 | 11,277,265 | ||||||

|

| |||||||

| 22,979,882 | ||||||||

| Utilities — 3.1% | ||||||||

New York City Water & Sewer System, Refunding RB, 5.00%, 06/15/38(g) | 1,151 | 1,338,310 | ||||||

New York Power Authority, Refunding RB, Series A, 4.00%, 11/15/60 | 5,446 | 6,005,191 | ||||||

Utility Debt Securitization Authority, Refunding RB | ||||||||

Series A, Restructured, 5.00%, 12/15/35 | 3,000 | 3,407,723 | ||||||

Series B, 4.00%, 12/15/35 | 2,600 | 2,837,257 | ||||||

|

| |||||||

| 13,588,481 | ||||||||

|

| |||||||

Total Municipal Bonds in New York | 86,935,830 | |||||||

|

| |||||||

| Total Municipal Bonds Transferred to Tender Option Bond | ||||||||

Trusts — 19.8% (Cost: $83,878,704) |

| 86,935,830 | ||||||

|

| |||||||

| Total Long-Term Investments — 164.7% (Cost: $692,563,330) | 722,607,785 | |||||||

|

| |||||||

| Security |

Shares | Value | ||||||

Short-Term Securities | ||||||||

Money Market Funds — 1.1% | ||||||||

BlackRock Liquidity Funds New York Money Fund Portfolio, 0.01%(h)(i) | 4,654,462 | $ | 4,654,462 | |||||

|

| |||||||

| Total Short-Term Securities — 1.1% (Cost: $4,654,462) | 4,654,462 | |||||||

|

| |||||||

| Total Investments — 165.8% (Cost: $697,217,792) | 727,262,247 | |||||||

| Other Assets Less Liabilities — 0.6% | 2,371,466 | |||||||

Liability for TOB Trust Certificates, Including Interest Expense and Fees Payable — (10.9)%. |

| (47,743,492 | ) | |||||

VRDP Shares at Liquidation Value, Net of Deferred Offering Costs — (55.5)% |

| (243,303,331 | ) | |||||

|

| |||||||

Net Assets Applicable to Common Shares — 100.0% | $ | 438,586,890 | ||||||

|

| |||||||

| (a) | Variable rate security. Interest rate resets periodically. The rate shown is the effective interest rate as of period end. Security description also includes the reference rate and spread if published and available. |

| (b) | U.S. Government securities held in escrow, are used to pay interest on this security as well as to retire the bond in full at the date indicated, typically at a premium to par. |

| (c) | Zero-coupon bond. |

| (d) | When-issued security. |

| (e) | Security exempt from registration pursuant to Rule 144A under the Securities Act of 1933, as amended. These securities may be resold in transactions exempt from registration to qualified institutional investors. |

| (f) | Represent bonds transferred to a TOB Trust in exchange of cash and residual certificates received by the Trust. These bonds serve as collateral in a secured borrowing. See Note 4 of the Notes to Financial Statements for details. |

| (g) | All or a portion of the security is subject to a recourse agreement. The aggregate maximum potential amount the Trust could ultimately be required to pay under the agreements, which expire between June 15, 2025 to January 1, 2028, is $6,046,661. See Note 4 of the Notes to Financial Statements for details. |

| (h) | Affiliate of the Trust. |

| (i) | Annualized 7-day yield as of period end. |

For Trust compliance purposes, the Trust’s sector classifications refer to one or more of the sector sub-classifications used by one or more widely recognized market indexes or rating group indexes, and/or as defined by the investment adviser. These definitions may not apply for purposes of this report, which may combine such sector sub-classifications for reporting ease.

S C H E D U L E O F I N V E S T M E N T S | 15 |

Schedule of Investments (unaudited) (continued) February 28, 2022 |

BlackRock MuniHoldings New York Quality Fund, Inc. (MHN) |

Affiliates

Investments in issuers considered to be affiliate(s) of the Trust during the six months ended February 28, 2022 for purposes of Section 2(a)(3) of the Investment Company Act of 1940, as amended, were as follows:

| Affiliated Issuer | Value at 08/31/21 | Purchases at Cost | Proceeds from Sales | Net Realized Gain (Loss) | Change in Unrealized Appreciation (Depreciation) | Value at 02/28/22 | Shares Held at 02/28/22 | Income | Capital Gain Distributions from Underlying Funds | |||||||||||||||||||||||||||

BlackRock Liquidity Funds New York Money Fund Portfolio | $ | 4,480,163 | $ | 174,299 | (a) | $ | — | $ | — | $ | — | $ | 4,654,462 | 4,654,462 | $ | 195 | $ | — | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||

| (a) | Represents net amount purchased (sold). |

Derivative Financial Instruments Outstanding as of Period End

Futures Contracts

| Description | Number of Contracts | Expiration Date | Notional Amount (000) | Value/ Unrealized Appreciation (Depreciation) | ||||||||||||

Short Contracts | 80 | 06/21/22 | $ | 10,196 | $ | (85,130 | ) | |||||||||

U.S. Long Bond | 55 | 06/21/22 | 8,637 | (143,328 | ) | |||||||||||

5-Year U.S. Treasury Note | 123 | 06/30/22 | 14,547 | (101,863 | ) | |||||||||||

|

| |||||||||||||||

| $ | (330,321 | ) | ||||||||||||||

|

| |||||||||||||||

Derivative Financial Instruments Categorized by Risk Exposure

As of period end, the fair values of derivative financial instruments located in the Statements of Assets and Liabilities were as follows:

| Commodity Contracts | Credit Contracts | Equity Contracts | Foreign Currency Exchange Contracts | Interest Rate Contracts | Other Contracts | Total | ||||||||||||||||||||||

Liabilities — Derivative Financial Instruments | ||||||||||||||||||||||||||||

Futures contracts | ||||||||||||||||||||||||||||

Unrealized depreciation on futures contracts(a) | $ | — | $ | — | $ | — | $ | — | $ | 330,321 | $ | — | $ | 330,321 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||