Exhibit 99.3

| | | | | | | | |

| Value-based strategy. | | | | | | 1903 Newton County Bank chartered in Jasper, Arkansas |

| People-centered approach. | | | | | | 1937 Bank of Ozark chartered in Ozark, Arkansas |

| | “Building meaningful relationships with our customers has made us the strong bank we are today.” -Chairman and CEO George Gleason | | | | | | 1979 Gleason purchases Bank of Ozark 1983 Gleason purchases Newton County Bank; assumes charter 1994 With five offices, launches de novo branching plan; changes name to Bank of the Ozarks 1995 Relocates headquarters to Little Rock, Arkansas 1997 Bank of the Ozarks, Inc., holds initial public stock offering (OZRK) |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| In 1979, George Gleason had a vision to create a bank where people | | | | | | 1998 Begins Central Arkansas expansion |

| would genuinely want to do business. And today, that bank not only | | | | | | 2002 Becomes $1 billion organization |

| exists, it’s nationally recognized for providing safe, sound and secure | | | | | | based on assets 2003 |

| banking solutions and customer service unmatched in the market | | | | | | Celebrates 100th anniversary 2004 |

place. | | | | | | Pushesdenovoexpansion into Texas with three offices |

| From the beginning, Mr. Gleason has instilled a personal commitment | | | | | | 2005 Becomes $2 billion organization |

| to excellence, fair dealing and exceptional customer service, and | | | | | | based on assets 2006 |

| has built his team with individuals having the same mindset. The | | | | | | Opens 11 new offices, a Company record 2008 |

| philosophy has always been to do what’s best for the customer; first by | | | | | | Becomes $3 billion organization based on assets |

| listening to and understanding their needs, and then by helping them | | | | | | Opens new headquarters in Little Rock, Arkansas |

find the best financial solutions. | | | | | | 2009 |

| This values-based strategy influences all the Bank’s decisions and has | | | | | | Named second and third-best performing bank in America byABABankingJournalandU.S.Banker |

| kept Bank of the Ozarks strong throughout the financial crisis of the | | | | | | 2010 |

| mid- to late 2000s. | | | | | | Named second-best performing bank in America byBankDirectormagazine |

| | | | | | George Gleason named Community Banker of the Year byAmericanBankermagazine |

| The Bank’s goal is not necessarily to be the largest financial institution – | | | | | | 2011 & 2012 Named best performing bank in America |

| but to simply be the best one. Regardless of organizational size, we | | | | | | byABABankingJournal |

| will always be deeply committed to developing friendships with our | | | | | | 2012 Named best performing regional bank in |

| customers and relationships with the communities we serve. Our | | | | | | America bySNLFinancial 2013 & 2014 |

| success is built upon our exceptional service to every customer, large | | | | | | Named best performing bank in America byBankDirectormagazine |

| and small – and we will keep that truth in focus as we build on our | | | | | | 2015 Named best performing regional bank in |

| past. | | | | | | America bySNLFinancialandbest performing bank in America byBankDirector magazine |

This Transition Is All About People -

A Powerful Union Of Two Great Bank Teams

| | |

• Carefully Considered | |  |

• Well Thought-Out | |

• Customer Friendly | |

• Shareholder Friendly | |

• Employee Friendly | |

Excellence Recognized

| | |

| Community Banker of the Year: | |

Youhaveafriendhere® |

| American Banker, December 2010 | |

| Ranked Top Performing Bank: | |

| ABA Banking Journal, April 2011 | |

| |

| Ranked Top Performing Bank: | | Ranked Top Performing Bank: |

| ABA Banking Journal, April 2012 | | Bank Director Magazine, August 2014 |

| |

| Ranked Top Performing Regional Bank: | | Ranked Top Performing Regional Bank: |

| SNL Financial, April 2012 | | SNL Financial, April 2015 |

| |

| Ranked Top Performing Bank: | | Ranked Top Performing Bank: |

| Bank Director Magazine, August 2013 | | Bank Director Magazine, August 2015 |

The Mission Statement

| • | | Our mission is to be the best banking organization in each of the markets we serve as determined by our customers, shareholders, employees and regulators. |

| • | | We strive to be the best bank for customers by offering a broad array of banking products and services at competitive prices and with the highest quality of personal service. |

| • | | We strive to be the best bank for shareholders by maximizing long-term value through strong year-to-year growth in assets, loans, deposits and net income while maintaining profit margins, asset quality and operating efficiency more favorable than industry averages. |

| • | | We strive to be the best bank for our employees by providing favorable compensation and benefits, opportunities for growth and advancement, a share in the success of the company, and a positive workplace and culture. |

| • | | We strive to be the best bank for regulators by adhering to safe, sound and prudent banking practices, striving to comply with all applicable laws and regulations, and giving appropriate attention to capital adequacy, asset quality, management, earnings, liquidity and market sensitivity. |

The Most Important Thing: Our Values Are More Important Than Our Financial Results.

| | | | |

• Character | | • Integrity | | • Diversity and Inclusion |

• Ethics | | • Fair Dealing | | • Honor |

Together We Are Strategically

Positioned For Great Growth

What Happens Next

| • | | It’s business as usual – take great care of our customers |

| • | | Cooperate with our teams who will help you prepare for the future |

| • | | Filing for regulatory approvals |

| • | | Anticipate closing in late Q1 2016 or early Q2 2016 |

| • | | Post closing we will operate as Bank of the Ozarks |

| • | | Training on Bank of the Ozarks’ policies and culture |

| • | | Systems conversions to Fiserv Premier planned for Q3 2016 |

| • | | You will receive outstanding support and training so you can confidently and comfortably continue to deliver the highest levels of customer service |

What Your Customers Need To Know

| • | | “It’s business as usual” – Nothing will change for many months, and customers should not experience any negative impacts from the transaction |

| • | | “We are still going to be here for you” – Bank of the Ozarks shares a commitment to exceptional customer service and minimal, if any, changes are planned for offices or any staff dealing with customers |

| • | | Bank of the Ozarks is one of America’s strongest banks bringing unparalleled safety, soundness and security to our customers |

| • | | After our systems are converted, our customers will have access to approximately 222 offices and exciting new banking products and services |

| • | | Bottom line: “This combination will be great for our customers” |

| • | | Refer to bankozarks.com for more information about Bank of the Ozarks |

Growth Is Critical To Our Shared Success

Together we are an outstanding, high-performing banking organization with expectations for continued growth and expansion.

Growth and expansion provide meaningful career opportunities in a premier regional banking franchise.

Answers to Questions You May Have

Bank of the Ozarks, Inc., the holding company for Bank of the Ozarks, and Community & Southern Holdings, Inc., the holding company for Community & Southern Bank (CSB) announced on October 19, 2015 that the two companies entered into a definitive agreement and plan of merger. The transaction is expected to close late in the first quarter of 2016 or early in the second quarter of 2016. The combined companies and banks will operate as Bank of the Ozarks, Inc. and Bank of the Ozarks.

What should I know about this merger?

| | • | | CSB and Bank of the Ozarks are working closely to make this transition as seamless and smooth as possible. |

| | • | | All deposit account types and account numbers will remain the same and customers will continue to use their existing checks, ATM/debit cards and online and mobile banking/bill pay services and make loan payments as usual. |

| | • | | At this time, no changes to banking hours, policies, products, interest rates, staff, and, most importantly, the banking culture are expected.It’s business as usual. |

| | • | | CSB will retain its name until the transaction is officially completed, which is expected to be late in the first quarter of 2016 or early in the second quarter of 2016. At that time all locations will operate under the Bank of the Ozarks name. |

| | • | | CSB employees and customers will still originate accounts using Community & Southern Bank products and services until the Community & Southern Bank and Bank of the Ozarks operating systems are combined, which is currently planned for the third quarter of 2016. There will be a period of time from the closing of the transaction late in the first quarter of 2016 or early in the second quarter of 2016, until the operating systems are combined in the third quarter of 2016, when the former CSB offices will operate as Bank of the Ozarks, but continue to offer the former CSB’s products and services. |

Do customers need to do anything about their account(s)?

| | • | | There is no need to do anything.Customers can continue banking exactly as they have been. Customers can continue to access their money by writing checks, using ATM and debit cards and/or online and mobile banking. Checks drawn on CSB will continue to be accepted. Loan payments should also continue to be made as usual. |

| | • | | Customers of both banks can expect to have a high level of convenience and customer service and expanded banking locations once the transaction is officially completed and banking systems are combined. |

| | • | | Advance notice will be given to customers prior to any material change to their account(s). |

Will customers’ checking/savings/CD account(s) number change?

| | • | | All account numbers will remain the same at this time. If any changes to account numbers are required in the future, we will communicate such changes to any affected customers well in advance of those changes. |

What about direct deposits/Social Security?

| | • | | Current arrangements for direct deposit(s), including Social Security checks, will continue as normal without interruption. |

What about online banking access?

| | • | | CSB customers will continue to access online banking throughmycsbonline.com and no changes to online services will occur until the banking systems are combined. |

Are deposits still safe?

| | • | | Yes. Deposits with CSB and Bank of the Ozarks are safe, sound and readily accessible. All deposit accounts, which include checking, savings, money market, CDs and retirement accounts, will become Bank of the Ozarks accounts, regardless of the amount, upon closing of the transaction, which is expected late in the first quarter of 2016 or early in the second quarter of 2016. |

Why did CSB and Bank of the Ozarks decide to merge?

| | • | | The merger brings together two banks committed to excellence for their customers, shareholders and employees. The combined bank’s increased lending capacity, expanded footprint and combined capabilities position it well to continue meeting the needs and growing expectations of customers, shareholders and employees. |

How will the merger impact customers?

| | • | | The combined bank’s increased lending capacity, expanded footprint and combined technology capabilities will allow us to give our customers better access to the financial resources and the state-of-the-art technology they need to be successful. |

What will be the name of the new bank?

| | • | | Upon closing, CSB will adopt the Bank of the Ozarks name and the holding company will be Bank of the Ozarks, Inc. |

When will the merger be official? How will customers be notified?

| | • | | The transaction is expected to close late in the first quarter of 2016 or early in the second quarter of 2016 following the receipt of all customary regulatory approvals. All customers will be notified in writing and online. |

Should customers expect any changes to the personalized customer service and banking experience they currently enjoy?

| | • | | CSB and Bank of the Ozarks share a commitment to serving customers with excellence, and customers can expect this to continue. |

Will there be any new products or offerings as a result of the combined bank?

| | • | | The combined bank creates a stronger organization with the capital, funding, infrastructure and leadership to support continued expansion of products and services, giving our customers access to excellent banking products and technology. |

Will any banking offices be consolidated?

| | • | | We have no immediate plans to close or consolidate any branches. |

Should we slow down our business development activities?

| | • | | CSB and Bank of the Ozarks have achieved outstanding growth. We have expectations for continued growth and expansion as we move forward together. The staff of both banks will continue to strive to develop new business and customer relationships. |

What’s the benefit to the bank given our recent track record of strong growth?

| | • | | The merger will expand our loan platform for continued growth and increase our legal lending limit as well as expand our scale and footprint. |

Can we expect any changes to our culture?

| | • | | Our culture will continue to flourish in the way we interact with customers, operate in our communities and invest for the future. Both CSB and Bank of the Ozarks share a focus on driving continued, meaningful growth and delivering excellent, personalized customer service that has been a hallmark of both companies over the years. |

What should I do if someone from the media contacts me?

| | • | | Employees, officers and directors who are not authorized spokespersons should refer all requests to Susan Blair, Executive Vice President, Bank of the Ozarks. Susan can be reached at (501) 978-2217 orsblair@bankozarks.com. If for any reason Susan is not available, please take a message (name, publication, contact information) and forward it to her. |

Who should I talk to with questions?

| | • | | You should direct any questions or concerns to your direct supervisor. |

Where will our official bank headquarters be?

| | • | | The combined bank’s official headquarters will be in Little Rock, Arkansas. |

For more information about Bank of the Ozarks, please visitbankozarks.com.

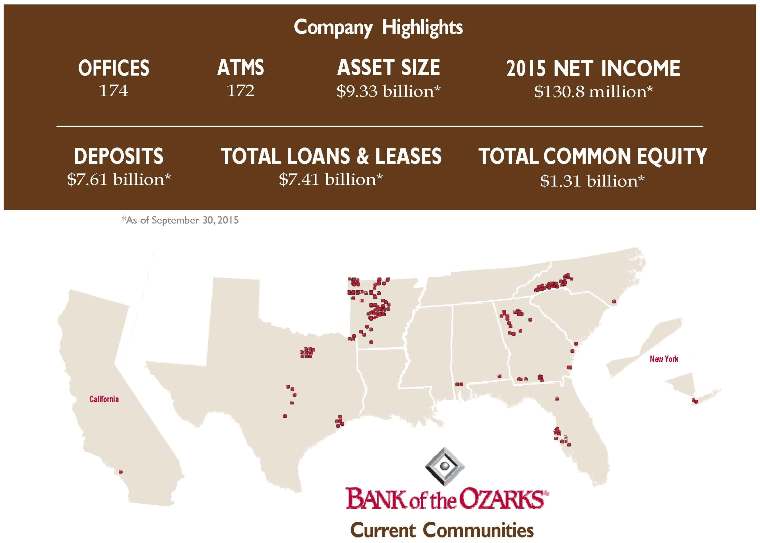

Bank of the Ozarks by the Numbers

With a solid record of long-term growth in loans, deposits and earnings, Bank of the Ozarks has earned respect as a great place to do business – and build successful relationships. We are successful because we always remain focused on strong fundamentals of banking: great customer service, prudent lending practices and sound management.

| | • | | Ranked the top-performing bank by Bank Director Magazine (2015, 2014, 2013) |

| | • | | Ranked the top-performing regional bank by SNL Financial (2015, 2012) |

| | • | | Ranked the top-performing bank in the U.S. by ABA Banking Journal (2012, 2011) |

| | • | | Rated as “well capitalized” – the highest available regulatory rating |

| | • | | Publicly traded company on the NASDAQ Global Select Market, symbol OZRK |

| | • | | Headquartered in Little Rock, Arkansas |

| | • | | Chartered in March 1903, a 112-year heritage |

ADDITIONAL INFORMATION

This communication is being made in respect of the proposed merger transaction involving Bank of the Ozarks, Inc. (“Company”) and Community & Southern Holdings, Inc. (“CSB”). This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval. In connection with the proposed merger, the Company will file with the Securities and Exchange Commission (“SEC”) a registration statement on Form S-4 that will include a joint proxy statement/prospectus of the Company and CSB and a prospectus of the Company. The Company also plans to file other documents with the SEC regarding the proposed merger transaction.

BEFORE MAKING ANY VOTING OR INVESTMENT DECISION, INVESTORS ARE URGED TO READ THE JOINT PROXY STATEMENT/PROSPECTUS REGARDING THE PROPOSED TRANSACTION AND ANY OTHER RELEVANT DOCUMENTS CAREFULLY IN THEIR ENTIRETY WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED TRANSACTION. The joint proxy statement/ prospectus, as well as other filings containing information about the Company will be available without charge, at the SEC’s Internet site (http://www.sec.gov). Copies of the joint proxy statement/prospectus and the filings with the SEC that will be incorporated by reference in the joint proxy statement/prospectus can also be obtained, when available, without charge, from the Company’s website athttp://www.bankozarks.com under the Investor Relations tab.

The Company and CSB, and certain of their respective directors, executive officers and other members of management and employees may be deemed to be participants in the solicitation of proxies from the shareholders of CSB and the Company in respect of the proposed merger transaction. Information concerning such participants’ ownership of common stock of the Company and CSB and any additional information regarding the interests of such participants will be included in the joint proxy statement/prospectus and other relevant documents regarding the proposed merger transaction filed with the SEC when they become available.

CAUTION ABOUT FORWARD-LOOKING STATEMENTS

This communication contains certain forward-looking information about the Company and CSB that is intended to be covered by the safe harbor for “forward-looking statements” provided by the Private Securities Litigation Reform Act of 1995. All statements other than statements of historical fact are forward-looking statements. In some cases, you can identify forward-looking statements by words such as “may,” “hope,” “will,” “should,” “expect,” “plan,” “anticipate,” “intend,” “believe,” “estimate,” “predict,” “potential,” “continue,” “could,” “future” or the negative of those terms or other words of similar meaning. These forward-looking statements include, without limitation, statements relating to the terms and closing of the proposed transaction between the Company and CSB, the proposed impact of the merger on the Company’s financial results, including any expected increase in the Company’s book value and tangible book value per common share and any expected increase in diluted earnings per common share, acceptance by CSB’s customers of the Company’s products and services, expectations regarding branch consolidation, if any, the opportunities to enhance market share in certain markets, market acceptance of the Company generally in new markets, and the integration of CSB’s operations. You should carefully read forward-looking statements, including statements that contain these words, because they discuss the future expectations or state other “forward-looking” information about the Company and CSB. A number of important factors could cause actual results or events to differ materially from those indicated by such forward-looking statements, many of which are beyond the parties’ control, including the parties’ ability to consummate the transaction or satisfy the conditions to the completion of the transaction, including the receipt of shareholder approval, the receipt of regulatory approvals required for the transaction on the terms expected or on the anticipated schedule; the parties’ ability to meet expectations regarding the timing, completion and accounting and tax treatments of the transaction; the possibility that any of the anticipated benefits of the proposed merger will not be realized or will not be realized within the expected time period; the risk that integration of CSB’s operations with those of the Company will be materially delayed or will be more costly or difficult than expected; the failure of the proposed merger to close for any other reason; the effect of the announcement of the merger on customer relationships and operating results (including, without limitation, difficulties in maintaining relationships with employees or customers); dilution caused by the Company’s issuance of additional shares of its common stock in connection with the merger; the possibility that the merger may be more expensive to complete than anticipated, including as a result of unexpected factors or events; general competitive, economic, political and market conditions and fluctuations; and the other factors described in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2014 and in its most recent Quarterly Reports on Form 10-Q filed with the SEC. The Company and CSB assume no obligation to update the information in this communication, except as otherwise required by law. Readers are cautioned not to place undue reliance on these forward-looking statements that speak only as of the date hereof.