FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16 of

the Securities Exchange Act of 1934

For the month of October, 2020

Brazilian Distribution Company

(Translation of Registrant’s Name Into English)

Av. Brigadeiro Luiz Antonio,

3142 São Paulo, SP 01402-901

Brazil

(Address of Principal Executive Offices)

(Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F)

Form 20-F X Form 40-F

(Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule

101 (b) (1)):

Yes ___ No X

(Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule

101 (b) (7)):

Yes ___ No X

(Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.)

Yes ___ No X

|

GPA - 3Q20 Results

Highlights ✔ Strong gross sales growth of 61.0% (21.0% pro forma) ✔ Assaí exceeded R$10 billion in revenue, up 33.4%, with high EBITDA margin of 7.8% ✔ Food e-commerce sales increased 240%, even with a strong base in the previous year, accounting for 12.4% of Pão de Açúcar sales ✔ Yet another quarter with Multivarejo recording EBITDA margin growth, reaching 8.1% ✔ Consolidated net income more than doubled in relation to 3Q19

|

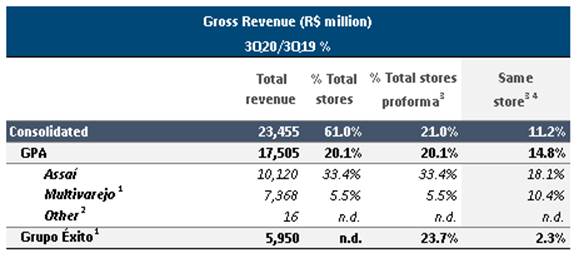

| Operating and Financial Performance | Consolidated gross sales of R$ 23.5 billion, reflecting the strong growth in both Brazilian and international operations. ▪ GPA Food Brazil: R$ 17.5 billion, significant growth of 20.0%, with 14.8% on same-store basis excluding gas stations and drugstores: ✔ Assaí: strong revenue of R$10.1 billion, up R$2.5 billion from the previous year. On a same-store basis, growth was 18.1%, the highest evolution since the end of 2016. This growth was driven by the outstanding contribution from the 42 stores opened in the last 24 months, the gradual resumption of food service and the continued growth in the participation of individual customers. ✔ Multivarejo: R$7.4 billion, growth of 10.4% on a same-store basis excluding gas stations and drugstores. Noteworthy growth of 11% in the food category and 11% in the non-food category (home appliances, home products and textiles). Additionally, online sales continued to grow significantly, up 240% vs. 3Q19 and already correspond to 6% and 12.4% of total Multivarejo and Pão de Açúcar sales, respectively. ▪ Grupo Éxito: R$ 6.0 billion, up 23.7% in pro forma total sales and 2.3% on a same-store basis excluding gas stations and in constant currency. Notable performance by Éxito Wow (+8% in total sales) and Carulla FreshMarket (+24% in total sales) and the development of the omnichannel strategy across all regions, which was accelerated by the scenario of higher restrictions on the circulation of people during the pandemic. The quarter registered record sales through the omnichannel platform, which totaled approximately R$1.5 billion in 9M20 and already represent 18.1% of total sales in Colombia.

Consolidated Adjusted EBITDA of R$ 1.7 billion, up 29.7% pro forma, with margin of 7.8% (+80 bps). Profitability increased across all businesses. ▪ GPA Food Brazil: R$ 1.3 billion (+28.1%), with strong Adjusted EBITDA margin of 7.9%, up 60 bps from 3Q19: ✔ Assaí: R$ 718 million, strong increase of 48%. Margin expanded 80 bps, reaching an impressive 7.8%. ✔ Multivarejo: R$ 546 million and margin of 8.1%, an increase of 50 bps, being the third consecutive quarter of profitability growth. ▪ Grupo Éxito: R$436 million, with margin of 8.2%, up 60 bps, mainly driven by the outstanding retail performance boosted by innovation and omnichannel strategy, and the contribution of the Tuya financial operation. Net income attributable to controlling shareholders amounted to R$386 million, up 2.5 times from the same period last year, with net margin of 1.8%, reflecting the operational improvement in Brazil and the consolidation of international operations. | |

| Leverage | ▪ Net debt/EBITDA ratio stood at 2.1x, in line with 2Q20 (2.2x). ▪ Solid financial position, with cash balance of R$7.3 billion, corresponding to 124% of short-term debt (12 months), which demonstrates an adequate level of liquidity in relation to the Company’s future obligations. |

| Capex | ▪ Gross investments of consolidated GPA totaled R$ 640 million, with the opening of 7 new Assaí stores in the quarter (5 organic and 2 Hiper conversions), 1 Mini Extra and 1 gas station, plus 8 Extra Super stores converted to the Mercado Extra format. In Colombia, the strategy of expanding innovative formats continues, with 2 stores converted into the Surtimayorista banner and 2 stores into the Éxito Wow format. |

| |

Spin-off Study

| ▪ On September 9, the Board of Directors of GPA authorized studies to segregate its Cash & Carry operation (Assaí) through the partial spin-off of the Company and its subsidiary Sendas. Key pillars: (i) increased strategic focus to bring greater agility to each segment; (ii) eliminating corporate inefficiencies for operationally distinct businesses; (iii) more efficient capital allocation, prioritizing investments by business and with greater access to capital markets; and (iv) creating value for shareholders through better assessment of business units. ▪ All the work fronts are in progress according to the schedule expected by the Company. |

"We wrap up the third quarter with very positive performance by our Brazilian and our international operations. Our net income attributable to controlling shareholders was 2.5 times higher than in the same period last year, we registered consecutive growth in Multivarejo's profitability, resuming our growth trajectory through significant advances in our omnichannel strategy, and witnessed the Assaí banner posting record quarterly sales growth, following a positive and consistent trajectory and a successful expansion plan. At the Grupo Éxito, we posted record sales in the omnichannel platform, driven by growth and penetration at surprising rates. We expect a fourth quarter with important seasonal dates and have streamlined our strategic plan by adjusting our portfolio, expanding profitable businesses and strengthening our digital ecosystem to ensure greater purchase recurrence, frequency and engagement from consumers."

Peter Estermann, Chief Executive Officer of GPA

| |

São Paulo, October 28, 2020 – GPA [B3: PCAR3; NYSE: CBD] announces its results for the 3rd quarter of 2020. All comparisons are with the same period in 2019, except where stated otherwise. In addition, starting from 2019, the results include the effects of IFRS 16/CPC 06 (R2) – Leases, which eliminates the distinction between operating and financial leases and requires the recognition of a financial asset and liability related to future leases discounted to present value for virtually all lease agreements of our stores.

3Q20 RESULTS

Consolidated GPA:

3Q20

(1) Same-store performance does not include revenue from gas stations and drugstores

(2) Other: Includes the operations of more recent initiatives such as James Delivery, Cheftime and Stix Fidelidade.

(3) Pro forma variation includes the results of Grupo Éxito in 3Q19 as if they were part of the group in the past, which is presented only for comparison purposes.

(4) Includes increases in constant exchange rate for international operations.

(1) GPA Brazil results do not include others (Stix Fidelidade, James Delivery and Cheftime); (2) Operating income before interest, tax, depreciation and amortization; (3) Adjusted for Other Operating Income and Expenses. Note: Tax credits were not materially different from previous quarters.

In 3Q19, in compliance with CVM resolution, there was a reclassification concerning the application of IFRS 16. Hence, figures presented here differ from those published previously, resulting in a reclassification of R$8 million in EBITDA of GPA Food and Consolidated.

| |

I. OPERATING PERFORMANCE BY BUSINESS

Assaí:

3Q20

(1)There was no calendar effect in the quarter.

Gross sales came to R$10.1 billion, up 33.4%, adding R$2.5 billion, the banner's all-time record quarterly growth. Same-store sales posted strong growth of 18.1%, demonstrating the wide acceptance of the model and its rapid capacity to adapt to diverse market scenarios.

The quarter's performance was driven by the outstanding contribution from the stores opened in the last 24 months, the gradual resumption of food service, the continued growth in the participation of individual customers and inflation in the commodities categories. Successful commercial actions were rolled out, such as “Two-Week Merchant Festival,” “It’s time to resume good deals,” “Father’s Day” and the “46th anniversary of the banner.” As a result, average ticket grow well above inflation.

In line with the strategy to expand the banner’s nationwide presence, 7 new stores were opened in 5 different states (5 organic openings and 2 conversions from Extra Hiper). In addition, 8 stores are under construction and 3 Extra Hiper stores are being converted.

The Passaí card, an important loyalty-building instrument among individual customers, already has over 1.2 million plastics issued, and purchases made using it presented a 40% higher ticket on average. Moreover, the Passaí credit and debit POS machines, focused on business clients and available at all Assaí stores, continue to enjoy wide acceptance among clients.

Gross profit amounted to R$1.5 billion (+32.9%). Gross margin reached 16.6%, despite the numerous stores under maturation, which shows that the format remains presenting adequate commercial competitiveness.

Selling, general and administrative expenses corresponded to 8.9% of net sales, important dilution of 80 bps from 3Q19, thanks to the robust sales growth in the quarter.

Adjusted EBITDA totaled R$718 million, a strong growth of 47.9% (higher than the gross revenue growth of 145 bps), with an impressive margin of 7.8%, representing a sharp increase of 80 bps, which demonstrates the success of the format and its value proposition.

| |

(1) Earnings before interest, tax, depreciation and amortization. (2) Adjusted for Other Operating Income and Expenses

Note: In 3Q19, in compliance with CVM resolution, there was a reclassification concerning the application of IFRS 16. Hence, the figures presented here differ from those published previously, resulting in a reclassification of R$8 million in EBITDA.

The strategy of strong expansion of Assaí stores continues to prove successful, and we maintain the plan to open more than 25 new stores per year in the coming years, serving new regions and consolidating more and more this format in Brazil.

Moreover, it must be noted that the banner’s results have been driven by the high productivity of the stores opened in recent years – both organic and conversions - which have helped profitability growth, as the image shows, making us very confident of the strategy adopted.

Evolution of monthly sales per square meter and EBITDA margin

| |

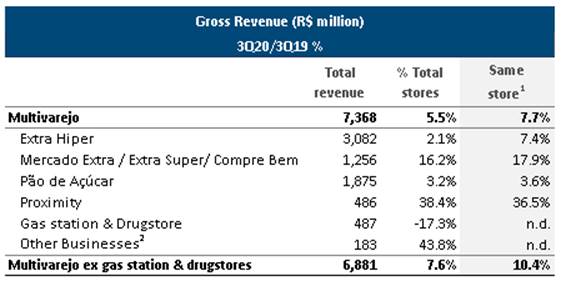

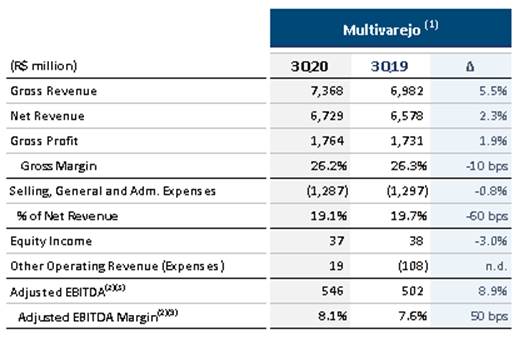

Multivarejo:

3Q20

(1)There was no calendar effect in the quarter.

(2) Includes e-commerce sales with deliveries straight from the DC and revenues from lease of commercial centers.

Total sales excluding gas stations and drugstores (which performed better than in 2Q20 but still present a negative impact) came to 10.4%, due to the strong performance by the portfolio of renovated stores and the rapid growth of food e-commerce (+240%). There was an 11% growth in both the food and non-food (home appliances, home products and textiles) categories.

Highlights per banner:

| ● | Hiper: significant growth of 7.4% in same-store sales, marked by the consistent value proposition of the non-food segment, which maintained double-digit growth even after the reopening of establishments selling non-essential items. |

We advanced in the process of store renovation and in consolidating the value proposition and appeal of the format through initiatives such as: i) more competitive prices in categories that increase customer traffic at stores; ii) further improving customer service, especially in perishable goods; iii) review of non-food portfolio; and iv) simplifying the assortment per store in order to better meet customer demand.

| ● | Pão de Açúcar: same-store sales of 3.6%, with the G7 model stores growing by noteworthy 7.0% in the period. There was significant sales growth in regions distant from major cities, such as coastal towns and towns in the countryside during the quarantine period. Some stores located in large cities registered lower customer traffic, while stores in these towns posted same-store growth of more than 30%, proving this migration movement of consumers. The 156 stores with e-commerce express operations registered growth of 170% in this delivery format. |

| ● | Mercado Extra: significant increase in same-store revenue (+17.6%) during one more quarter, reflecting the rapid maturation of stores converted to this format and the successful commercial campaigns during the period, showing the strength of the value proposition of this format to the target public. In 3Q20, 8 stores were converted from Extra Super to Mercado Extra and 30 more stores should be converted during 4Q20, practically concluding the conversion process planned by the Company. |

| ● | Compre Bem: The 28 converted stores continue to mature rapidly, with strong growth in same-store sales (+35.5%), even with the strong comparison base. The number of new customers increased significantly during the quarter, proving the strong acceptance of this model in response to consumer needs. |

| |

In line with the portfolio optimization strategy, we plan to conclude the conversion of Extra Super stores to the Mercado Extra and Compre Bem formats by 1Q21, which will drive revenue growth and profitability of the format.

| ● | Proximity: significant same-store growth of 36.5%, with 3Q20 being the ninth consecutive quarter of double-digit growth. The Minuto Pão de Açúcar and Mini Extra formats continued to deliver healthy performance, positively impacted by the strong growth of neighborhood stores, which account for a greater share of sales in the formats and offset the sharp decline in traffic at street and office stores. Outstanding performance of convenience stores opened in 2019 (10 stores), which already outperform profitability and sales results posted by mature Minuto stores, which showcases the successful expansion of the format. The “Aliados” program continues to add new customers to its base, contributing to the format. |

Private-Label Brands registered penetration of 20.2% in the food category, thanks to an optimum value proposition, which contributed to a positive price-quality perception among consumers.

Gross profit amounted to R$1.8 billion, with margin of 26.2% in 3Q20, the third consecutive quarter of improvement in gross margin, thanks to the successful promotional campaigns and better management of shrinkage level.

Selling, general and administrative expenses corresponded to 19.1% of net sales revenue in the quarter, important dilution of 60 bps from 3Q19, mainly due to the constant control of expenses and improvement of operational productivity at stores and distribution centers. Administrative expenses presented a reduction mainly in marketing and corporate expenses.

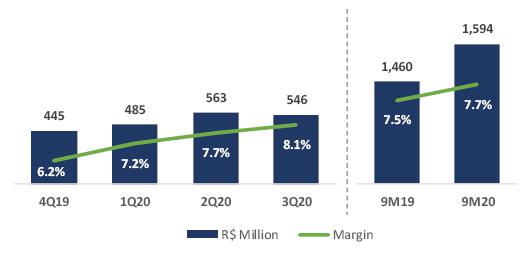

As a result of the above factors, Adjusted EBITDA came to R$546 million, growing 8.9% in relation to 3Q19. Adjusted EBITDA margin reached 8.1%, up 50 bps vs. 3Q19, presenting a sequentially increase in relation to the previous quarters, as shown in the chart below.

| (1) | Multivarejo results do not include the result of Other (Stix Fidelidade, Cheftime and James Delivery). (2) Earnings before interest, tax, |

depreciation and amortization. (3). Adjusted by Other Operating Income and Expenses.

Note: In 3Q19, in compliance with CVM resolution, there was a reclassification concerning the application of IFRS 16. Hence, the figures presented here differ from those published previously, resulting in a reclassification of R$1 million in EBITDA.

| |

Sequential improvement in EBITDA margin

Digital Ecosystem

The digital ecosystem continues to be one of the biggest growth levers of Multivarejo, supported by 3 integrated recurrent drivers: food e-commerce, customer relations and multichannel convenience.

Food e-commerce:

Our food e-commerce offers unique and complementary options that provide consumers with a complete shopping journey. Our online food sales already account for 6% of total Multivarejo sales and 12.4% of Pão de Açúcar sales, and customers may choose from among various delivery methods, such as: a) traditional delivery in up to 1 day, b) express delivery in the same day, c) delivery in up to 2 hours via James Delivery and d) click & collect.

Food e-commerce sales grew 240% from the same period last year, even with a strong prior year comparison, driven by the significant increase in new customers (+202%) and higher average ticket in all delivery channels (+10.4% vs. 3Q19 ex-James). The Express delivery channel expanded from 113 stores in 3Q19 to 295 stores in 3Q20, while James Delivery grew from 31 stores in 3Q19 to 347 stores in 3Q20. James Delivery registered GMV growth of 577% in the quarter, while the number of orders increased 358% from the same period last year.

Also noteworthy was the successful strategy in the online wine category, which grew more than 5 times from 3Q19 and reached the impressive milestone of more than 1.2 million bottles sold in the period. This was due to the combination of a consistent commercial strategy, innovative actions in the online market, the group's logistics capacity and broad reach.

Customer relations:

We have a comprehensive relationship platform consisting of loyalty programs and apps designed to provide an increasingly personalized buying experience, bringing greater engagement, better experience and more recurring purchases by our customers. Moreover, in October this year we changed the loyalty program "My Rewards" and embedded it into the STIX platform - transforming the traditional stamp dynamics into purchase missions that lead to accumulating points and earning benefits for millions of loyal consumers. With STIX, we started to have a new, fully integrated rewards program with a strong value proposition for the consumer. This program, launched in partnership with Raia Drogasil, was born with a solid base of over 60 million loyal customers.

| |

The loyalty apps of Extra and Pão de Açúcar have already registered more than 14 million active downloads (+40% vs. 3Q19) and account for about 30% of Multivarejo's sales and 40% of online sales. This large database enables us to identify 70% of Multivarejo’s total sales (90% at Pão de Açúcar and 62% at Extra).

Multichannel Convenience:

We continue to develop new multichannel convenience solutions, with options that complement other growth drivers of the digital platform, such as Cheftime - which offers gastronomic kits and ready and semi-ready-to-eat meals. Currently, Cheftime's gastronomic solutions are available in 284 stores of the Group, growing 56% vs. 2Q20, while the number of meals sold more than doubled during the period.

We are developing the GPA Marketplace, which should be launched in November and will have strong and diversified partners. We have already signed agreements with the brand leaders in the categories that will be prioritized (household items such as furniture, decor, towels and linens and domestic utensils, toys, children's line, cosmetics and personal care, automotive such as tires, pet shop, sports and leisure, food supplements, food and beverages).

Sales through online platforms have the potential to reach R$1 billion[1] in 2020 (almost three times the sales in 2019), mainly driven by the increase in operational capacity and the gain in food e-commerce market share- which was more than 71% in 3Q20 according to EBIT Nielsen (self-service food channel), proving the immense business potential.

[1] It is a mere estimate and should not be understood or treated as guidance.

| |

Grupo Éxito:

3Q20

GPA acquired 96.57% of the capital stock of Grupo Éxito on November 27, 2019. Hence, the results of Grupo Éxito are included in the GPA Consolidated results only in 3Q20, and changes in relation to 3Q19 are presented merely for comparison purposes.

(1) To reflect the calendar effect, the following reductions were made in 3Q20: 0 bps in Grupo Éxito, 0 bps in Colombia, 20 bps in Uruguay and 60 bps in Argentina.

(2) Includes the formats Surtimayorista, VIVA, Aliados and Other Businesses. (3) Same store presented in growth in constant currency.

Gross revenue reached R$ 6.0 billion, growing 23.7% in the quarter (+0.7% in constant currency). The omnichannel strategy evolved to all the countries where it operates demonstrating its capacity to quickly adapt to the pandemic scenario. Moreover, there was a gradual resumption of the non-food segment, which, just like the malls segment, had been affected by restrictions on circulation in major Colombian cities.

Same-store sales, excluding gas stations, grew 2.3%, affected by the restrictions on mobility in Colombia, which involved reduced business hours at stores, purchases limited to once a week in July and August and four times a week since September, dry law enforcement on some weekends and curfew in the main Colombian cities.

Following are the highlights by country:

| ● | Colombia: same-store sales in Colombia declined slightly from the same period last year, due to the stringent restrictions imposed by the government during most of 3Q20. Nevertheless, the innovative formats delivered a very positive performance, driven by the quality of fresh products and service excellence at stores, as well as the excellent performance of the omnichannel strategy, which witnessed record sales in the quarter. Around 73 stores - representing 30% of the sales – registered lower customer traffic due to the restrictions on circulation, and this was also observed in low-cost banners, which explain the unusually negative same-store performance in some formats. |

| ● | Uruguay: Solid same-store performance of 11.0%, mainly driven by the double-digit growth in the Devoto and Geant banners. This growth demonstrates the successful commercial actions, the consistent progress of the omnichannel strategy and the strong performance of the food category. |

| ● | Argentina: same-store sales of 12.7% despite a challenging scenario of major restrictions on circulation, reduced business hours of stores and stiff competition due to the decline in production among local suppliers, especially in technology-related categories. The omnichannel strategy continued to expand through the addition of new stores served by last miler partners (such as Rappi and Pedidos Ya). |

| |

Gross profit was R$ 1.3 billion, up 20.0% from 3Q19, with margin of 24.6%. Gross margin compared with pro forma margin in 3Q19 was explained by: (i) the challenges related to the pandemic scenario, which led to a lower distribution of royalties in Tuya (-100 bps); and (ii) the increase in the gross margin of the retail operation due to better terms negotiated with suppliers (+30 bps).

Selling, general and administrative expenses totaled R$ 971 million, equivalent to 18.2% of net sales revenue, stable in relation to the same period last year, demonstrating the Group's unwavering commitment to controlling expenses.

Adjusted EBITDA totaled R$ 436 million (+32.7% vs. 3Q19), with strong 60 bps growth in EBITDA margin, which stood at 8.2%. This evolution was due to the improvement in retail operation, as well as Tuya's higher net income through equity income explained by: i) reduction of royalties, ii) actions to reduce costs and renovation of key contracts and iii) reversal of provision for lower expected default.

(1) Earnings before interest, tax, depreciation and amortization. (2). Adjusted by Other Operating Income and Expenses. (3) Pro forma for comparison purposes only.

| |

II. EQUITY INCOME

Consolidated equity income totaled R$91 million in 3Q20, an increase of R$73 million from the same period last year, driven mainly by the result of interest held in financial operations in Brazil (36% of FIC) and Colombia (50% of Tuya / Puntos Colombia).

III. OTHER INCOME AND EXPENSES

Other Income and Expenses resulted in an expense of R$33 million in 3Q20, compared to an expense of R$121 million in 3Q19. This amount is mainly composed of:

i) expenses incurred to optimize the portfolio of stores in operation in Brazil, totaling approximately R$100 million, which involved store closures and asset write-offs, projects and other restructuring costs, which mostly do not impact cash and contribute to the sales and profitability growth strategy;

ii) positive impact of approximately R$110 million from the capital gain on the sale and leaseback operations already announced in 2Q20.

iii) tax contingencies of approximately R$10 million and expenses of about R$35 million in the international operations.

It is important to mention that no reclassification was applied for expenses related to COVID-19 this quarter.

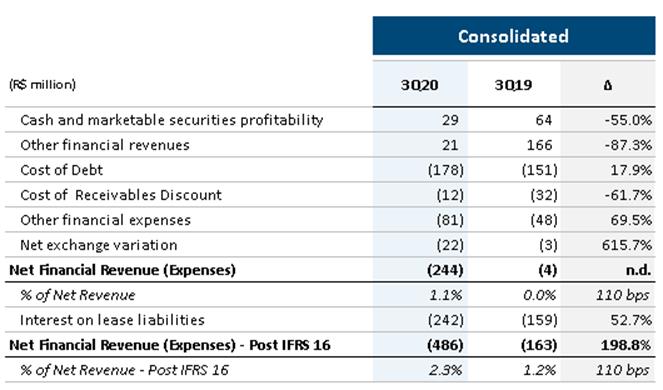

IV. FINANCIAL RESULT

The net financial result of GPA Consolidated was an expense of R$486 million, corresponding to 2.3% of net sales revenue, remaining stable in relation to 2Q20. The increase as a percentage of net revenue compared to last year was mainly due to the higher non-recurring financial revenue in 3Q19.

With the adoption of IFRS 16, the financial result now includes Interest on lease liabilities, which was an expense of R$242 million in the quarter.

| |

The main variations in the net financial result were:

| ● | Finance income: lower than in 3Q19 due to the non-recurring effects that did not repeat in 3Q20, such as: the divestment of interest in Via Varejo, entry of funds for the acquisition of Grupo Éxito and income from inflation adjustment. |

| ● | Financial expenses (including the cost of selling receivables): increase from 3Q19, mainly due to interest expenses coming from the increase in gross debt; |

| ● | Net effect of exchange variation: increase in expenses compared to 3Q19 due to the depreciation of the Colombian peso in the period. |

V. NET INCOME

Consolidated GPA ended 3Q20 with consolidated net income from controlling shareholders of R$386 million, up 2.5 times from the same period last year, while net income from continuing operations doubled to R$339 million.

The 3Q20 results underline the success of the strategies executed by the group, resulting in sequential improvement at Multivarejo, excellent performance by Assaí and strong results from the Grupo Éxito.

| |

VI. NET DEBT

To calculate the indicators in the table, the Company does not consider the lease liabilities related to IFRS 16.

(1) Adjusted EBITDA before IFRS 16 in the last 12 months.

Net debt adjusted by the balance of receivables not discounted reached R$ 9.6 billion in consolidated GPA, compared to R$ 2.2 billion in 3Q19, mainly reflecting the funds raised for the acquisition of Grupo Éxito.

The ratio of net debt/Adjusted EBITDA(1) was 2.1x at the end of 3Q20, in line with 2Q20 (2.2x) and within the Company’s expectations.

Cash balance at the end of the quarter was R$7.3 billion, equivalent to 124% of short-term debt, which represents an adequate level of liquidity in relation to the Company's future obligations. Balance of unsold receivables totaled R$194 million.

| |

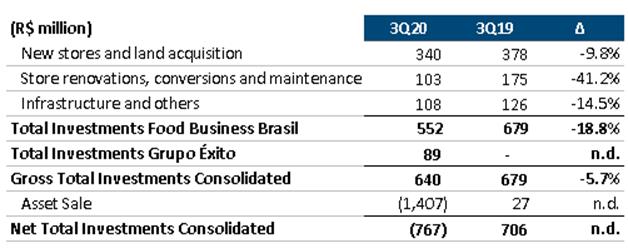

VII. INVESTMENTS

Gross investments in the quarter totaled R$640 million, and went to: i) the opening of 7 new Assaí stores (5 organic and 2 conversions from Hiper), and 11 stores are currently under construction; ii) 1 Mini Extra store; iii) 1 gas station; iv) conversion of 8 Extra Super stores into Mercado Extra; v) conversion of 2 stores into Surtimayorista; and vi) conversion of 2 stores into Éxito Wow.

We reiterate our expectations of ending 2020 with 19 Assaí stores opened (16 organic and 3 conversions) and 38 renovations of Extra Super to Mercado Extra in Brazil. At Grupo Éxito, we expect to open, renovate and convert between 5 and 7 stores by the end of the year, with the focus on innovative models: Éxito WOW, Carulla FreshMarket and Surtimayorista.

| |

VIII. STORE PORTFOLIO CHANGES BY BANNER

In Brazil, 7 Assaí stores (5 organic and 2 conversions from Extra Hiper), 1 Mini Extra and 1 gas station were opened, while 8 Extra Super were converted to Mercado Extra. Continuing the portfolio adjustment process, 1 Hiper store, 4 Extra Super stores and 18 drugstores were closed. At Grupo Éxito, 2 stores were converted to the cash and carry format under the Surtimayorista banner and 2 Hipers were converted into the Éxito Wow model. Ten stores were closed: 6 Éxito and 3 Surtimax (Colombia) and 1 Devoto (Uruguay).

| |

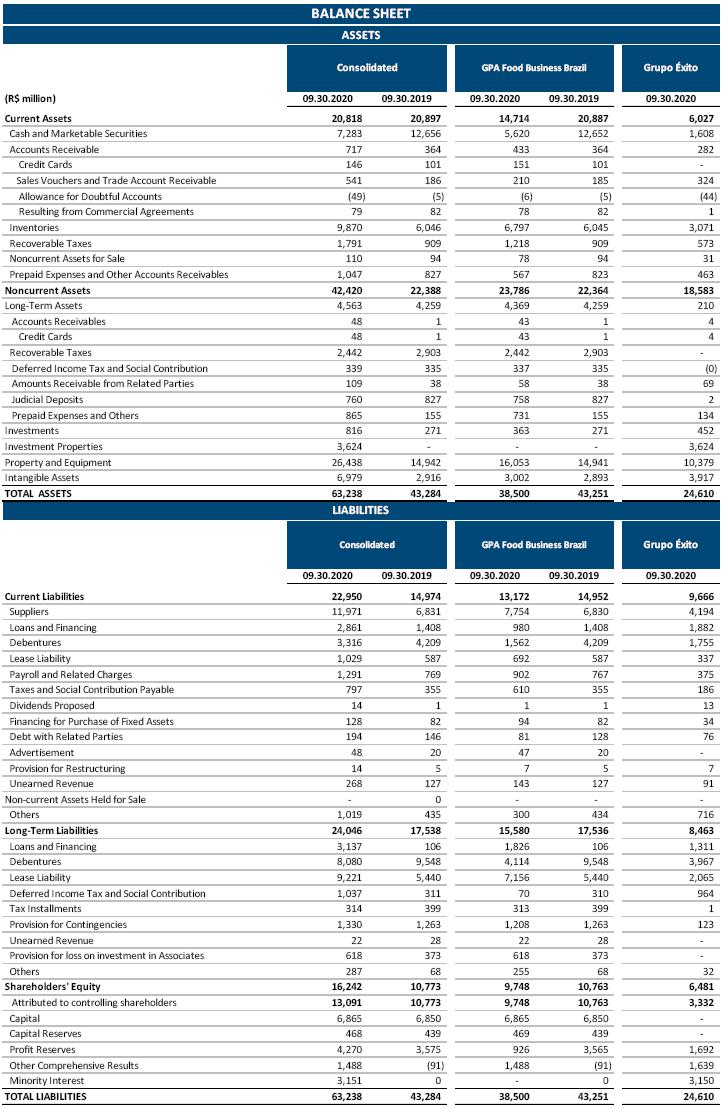

IX. CONSOLIDATED FINANCIAL STATEMENTS

Balance Sheet

| |

Income Statement - 3rd Quarter 2020

(1) Consolidated includes results of other complementary businesses; (2) Equity income includes Cdiscount’s results in the Consolidated figures; (3) Net income after non-controlling interest; (4) Adjusted for Other Operating Income and Expenses.

| |

Cash Flow – Consolidated (*)

| |

X. BREAKDOWN OF SALES BY BUSINESS - BRAZIL

(1) Includes sales by Extra Supermercado, Mercado Extra, Extra Hiper and Compre Bem. (2) Includes sales by Mini Extra and Minuto Pão de Açúcar.

(3) Includes sales by Gas stations, Drugstores, Delivery and rental revenue from commercial centers. (4) GPA includes the results of James Delivery, Stix Fidelidade and Cheftime

XI. BREAKDOWN OF SALES (% of Net Sales) - BRAZIL

| |

3Q20 Results Conference Call and Webcast

Thursday, October 29, 2020

2:00 p.m. (Brasília) | 1:00 p.m. (New York) | 5:00 p.m. (London)

Conference call in Portuguese (original language)

+55 (11) 4210-1803 or +55 (11) 3181-8565

Conference call in English (simultaneous translation)

+1 (412) 717-9627 or +1 (844) 204-8942

Webcast: http://www.gpari.com.br

Replay

+55 11 3193-1012

Access code for audio in Portuguese: 1932275#

Access code for audio in English: 1779586#

http://www.gpari.com.br

Investor Relations Contacts

GPA Phone: +55 (11) 3886-0421 gpa.ri@gpabr.com www.gpari.com.br

|

Disclaimer: Statements contained in this release relating to the business outlook of the Company, projections of operating/financial results, growth prospects of the Company and market and macroeconomic estimates are merely forecasts and are based on the beliefs, plans and expectations of Management in relation to the Company’s future. These expectations are highly dependent on changes in the market, Brazil’s general economic performance, the industry and international markets, and hence are subject to change.

| |

APPENDIX

Company’s Business:

Adjusted EBITDA: Measure of profitability calculated by excluding Other Operating Income and Expenses from EBITDA. Management uses this measure in its analysis as it believes it eliminates nonrecurring expenses and revenues and other nonrecurring items that could compromise comparability and analysis of results.

Consolidated: Amounts reported refer to the sum of the operations of Food – Brazil, Grupo Éxito, Cdiscount and other businesses of the Company.

Discontinued Activities: Refer to Via Varejo operations until May 2019 and other subsequent effects related to the write-off of investments.

Earnings per share: Diluted earnings per share are calculated as follows:

| ● | Numerator: profit in the year adjusted by dilutive effects of stock options granted by subsidiaries. |

| ● | Denominator: number of shares of each category adjusted to include potential shares corresponding to dilutive instruments (stock options), less the number of shares that could be bought back in the market, as applicable. |

Equity instruments that will or may be settled with the shares of the Company and its subsidiaries are only included in the calculation when their settlement has a dilutive impact on earnings per share.

EBITDA: EBITDA is calculated in accordance with Instruction 527 issued by the Securities and Exchange Commission of Brazil (CVM) on October 4, 2012.

Grupo Éxito: Amounts reported refer to Grupo Éxito’s operations in Colombia, Uruguay and Argentina. GPA acquired 96.57% of the capital stock of Grupo Éxito on November 27, 2019.

Food – Brazil: Amounts reported refer to the sum of Assaí and Multivarejo operations.

| |

Growth and changes: The growth and changes presented in this document refer to variations from the same period last year, except where stated otherwise.

Retail vertical: Corresponds to sales of James Delivery in the Pão de Açúcar, Extra and Minuto Pão de Açúcar operations.

Same-store growth: Same-store growth, as mentioned in this document, is adjusted by the calendar effect in each period

SIGNATURES

Pursuant to the requirement of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| COMPANHIA BRASILEIRA DE DISTRIBUIÇÃO | ||

| Date: October 28, 2020 | By: /s/ Peter Estermann Name: Peter Estermann Title: Chief Executive Officer | |

| By: /s/ Christophe José Hidalgo Name: Christophe José Hidalgo Title: Investor Relations Officer | ||

FORWARD-LOOKING STATEMENTS

This press release may contain forward-looking statements. These statements are statements that are not historical facts, and are based on management's current view and estimates offuture economic circumstances, industry conditions, company performance and financial results. The words "anticipates", "believes", "estimates", "expects", "plans" and similar expressions, as they relate to the company, are intended to identify forward-looking statements. Statements regarding the declaration or payment of dividends, the implementation of principal operating and financing strategies and capital expenditure plans, the direction of future operations and the factors or trends affecting financial condition, liquidity or results of operations are examples of forward-looking statements. Such statements reflect the current views of management and are subject to a number of risks and uncertainties. There is no guarantee that the expected events, trends or results will actually occur. The statements are based on many assumptions and factors, including general economic and market conditions, industry conditions, and operating factors. Any changes in such assumptions or factors could cause actual results to differ materially from current expectations.