FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16 of

the Securities Exchange Act of 1934

For the month of January, 2021

Brazilian Distribution Company

(Translation of Registrant’s Name Into English)

Av. Brigadeiro Luiz Antonio,

3142 São Paulo, SP 01402-901

Brazil

(Address of Principal Executive Offices)

(Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F)

Form 20-F X Form 40-F

(Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule

101 (b) (1)):

Yes ___ No X

(Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule

101 (b) (7)):

Yes ___ No X

(Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.)

Yes ___ No X

Free translation |

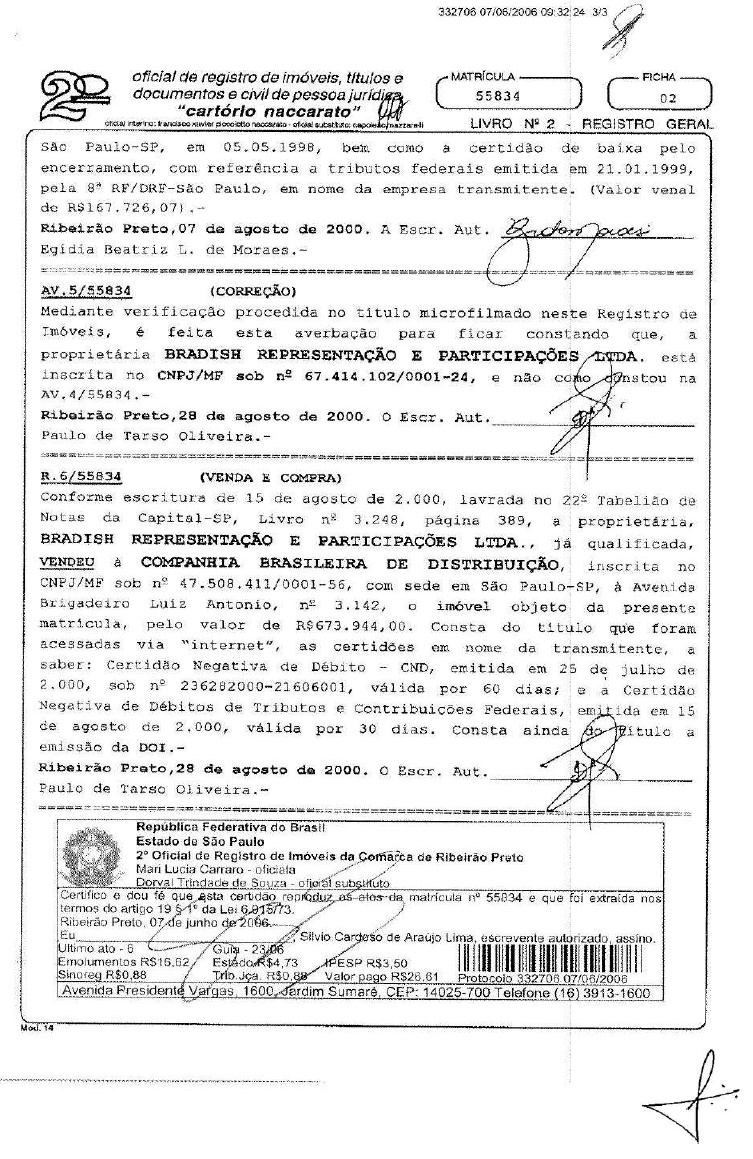

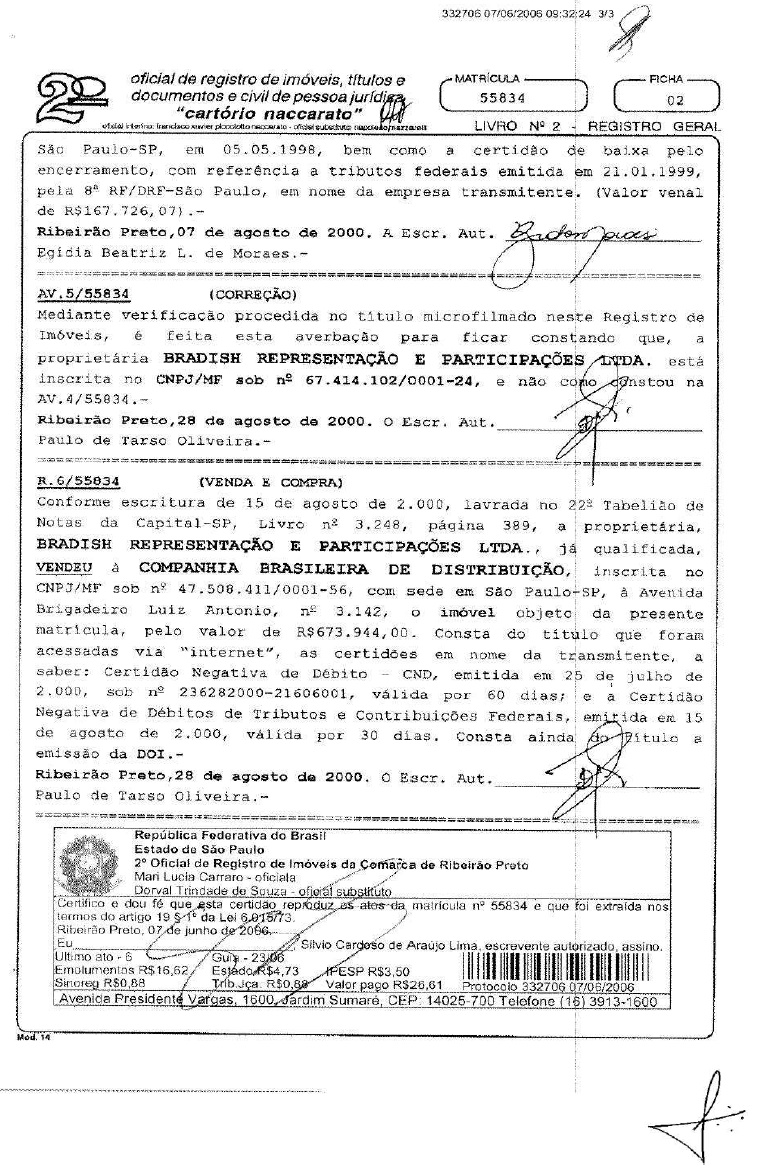

COMPANHIA BRASILEIRA DE DISTRIBUIÇÃO

Publicly-Held Company of Authorized Capital

CNPJ nº 47.508.411/0001- 56

NIRE No.: 35.300.089.901

MINUTES OF THE EXTRAORDINARY GENERAL MEETING

HELD ON DECEMBER 31, 2020

1. Date, Time and Venue: On December 31, 2020, at 10:00 a.m., held exclusively digitally and remotely by videoconference, pursuant to the Brazilian Securities and Exchange Commission Instruction No. 481, of December 17, 2009.

2. Call Notice and Attendance: Call notice published in the Official Gazette of the State of São Paulo, in the issues of days December 15, 16 and 17, 2020, on pages 18, 14 and 16, respectively, and in the newspaper Folha de S. Paulo in the issues of days December 15, 16 and 17, 2020, on pages A18, A20 and A21, respectively, that shall be filed on the head office of the Company.

3. Attendance: Meeting convened with the presence of shareholders representing one hundred and seventy-two million, six hundred and eighty-nine thousand, two hundred and one (172,689,201) ordinary shares, representing, approximately, 64,41% of the total voting shares of the Company, according to the signatures contained in the Shareholders Attendance Book, as well as Mr. Christophe José Hidalgo, Interim CEO, Finance and Invertors Relations VP.

4. Board: Chairman: Christophe José Hidalgo; Secretary: Marcelo Acerbi de Almeida.

5. Agenda: To resolve on the following matters:

5.1. Sendas Partial Spin-Off with Merger of Sendas’ Spun Off by the Company: In relation to the partial spin-off of Sendas Distribuidora S.A., a corporation enrolled with the CNPJ/ME under No. 06.057.223/0001-71 (“Sendas”), com reverse spun-off to the Company (“Sendas’ Spin-Off”), comprised by (a) equity interest equivalent to approximately 90.93% (ninety point ninety-three percent) of the total shares of Almacenes Éxito S.A., a corporation organized and existent under the law of Colômbia, with headquarters in Envigado, Departamento de Antioquia, Colombia, enrolled with

Free translation |

the CNPJ/ME under No. 23.041.875/0001-37 (“Éxito”), held by Sendas, corresponding to 393,010,656 (three hundred and ninety-three million, ten thousand, six hundred and fifty-six) shares, and equivalent to approximately 87.80% (eighty-seven point eighty percent) of all shares issued by Éxito (“Éxito Interest”); and (b) assets related to 6 (six) gas stations held by the Company (“Operating Assets”, being the Operating Assets, together with the Éxito Interest, hereinafter jointly referred to as “Sendas’ Spun Off”): (i) the ratification of the appointment and hiring of appraisal firm for the appraisal of Sendas’ Spun Off, namely, Magalhães Andrade S/S Auditores Independentes, registered with the Regional Accounting Council of the State of São Paulo under nº 2SP000233/O-3 and CNPJ/ME nº 62.657.242/0001-00, with registered office in the city of São Paulo, State of São Paulo, at Av. Brigadeiro Faria Lima, nº 1.893, 6th floor, Jardim Paulistano, CEP 01451-001 (“Appraisal Firm”); (ii) the approval of the appraisal report of Sendas’ Spun Off prepared by the Appraisal Firm (“Sendas’ Appraisal Report”), contained in Exhibit 5.1.(ii); (iii) the ratification of the entering into of the “Protocol and Justification of Sendas’ Partial Spin-Off with the Merger of the Spun off by the Company (“Sendas’ Protocol”), contained in Exhibit 5.1.(iii); (iv) the Sendas’ Spin-Off, with the merger of Sendas’ Spun Off by the Company, and other procedures described in the Sendas’ Protocol, pursuant to Sendas’ Protocol; e (v) the authorization of members of the Company’s management to perform any and all acts that may be necessary, useful and/or proper to the merger of Sendas’ Spin-Off, as well as other procedures described in the Sendas’ Protocol, under the terms of the Sendas’ Protocol;

5.2. Company’s Partial Spin-Off: In relation to the partial spin-off of Company, with the spun off reverse to Sendas itself (“CBD’s Spin-Off”), comprised by the total shares representing the capital stock of Sendas held by the Company, corresponding to 100% (one hundred percent) of the common, nominative shares with no par value issued by Sendas (“Spun Off CBD”): (i) the ratification of the appointment and hiring of the Appraisal Firm responsible for the appraisal of the CBD’Spun off; (ii) the approval of the CDB’ Spun Off appraisal report, as prepared by the Appraisal Firm (“CBD’ Appraisal Report”), contained in Exhibit 5.2.(ii); (iii) the ratification of the entering into of the “Protocol and Justification of the Partial Spin-Off of Companhia Brasileira de Distribuição with the Merger of the Spun off by Sendas” (“CBD’s Protocol”), contained in Exhibit 5.2.(iii); (iv) CBD’s Spin-Off and other procedures described in the CBD’s Protocol; and (v) the authorization of the members of the Company’s management to perform any and all acts that may be necessary, useful and/or proper to the merger of CBD’s Spin-Off;

Free translation |

5.3. To approve the amendment to Article 4 of the Company’s By-Laws as a result of the capital reduction resulting from CBD's Spin-Off, under the terms and conditions provided for in the CBD Protocol, if approved, as well as to reflect the capital increase approved at the meeting of the Company's Board of Directors held on October 28, 2020 and registered with the São Paulo Board of Trade in session held on December 01, 2020, under no. 516.276/20-7; and

5.4. To approve the Company’s By-Laws restatement, so as to incorporate the amendments above mentioned.

6. Resolutions: Being the guidelines and voting declarations filed at the Company's head office and initialed by the Chairman and Secretary, duly registered, the Shareholders unanimously waived the reading of the Call Notice and approved the drawing up of these minutes in the form of a summary of the facts that occurred and that its publication is made with the omission of the signatures of the shareholders present, as permitted by article 130, paragraph 1, of Law 6,404/76 (“Corporation Law”).

6.1. Regarding Sendas' Spin-Off: (i) by a majority of votes, being counted 172.286.439 in favor, 402.449 abstentions and 313 contrary votes, to ratify the appointment and hiring of the Appraisal Firm responsible for the appraisal of Sendas’ Spun Off; (ii) by a majority of votes, being counted 169.884.374 in favor, 2.804.114 abstentions and 713 contrary votes, to approve the Sendas’ Appraisal Report related to Sendas’ Spun Off, comprised by the Éxito Interest and the Operating Assets, pursuant to Exhibit 5.1.(ii); (iii) by a majority of votes, being counted 172.668.795 in favor, 19.543 abstentions and 863 contrary votes,, to ratify the entering into of the Sendas’ Protocol, pursuant to Exhibit 5.1.(iii); (iv) by a majority of votes, , being counted 172.668.549 in favor, 19.523 abstentions and 1.129 contrary votes, to approve, pursuant to the Sendas’ Protocol, Sendas’ Spin-Off with the merger of Sendas’ Spun Off by the Company, as well as other procedures described in the Sendas’ Protocol. Whereas Sendas is a whole-owned subsidiary of the Company, and that its assets is partially spun-off, with the merger of Sendas’ Spun Off by the Company, Sendas’ Spin-Off shall not result in a capital increase or issuance of new shares by the Company, remaining the capital stock of the Company, totally subscribed and paid in, at 6.865.829.549,07 (six billion, eight hundred and sixty-five million, eight hundred and twenty-nine thousand, five hundred and forty-nine Reais and seven cents), divided into 268.351.567 (two hundred and sixty-eight million, three hundred and fifty-one thousand, five hundred and sixty-seven) common, registered, book entry shares with no par value; and (v) by a majority of votes,

Free translation |

being counted 172.667.464 in favor, 20.527 abstentions and 1.210 contrary votes, to authorize the members of the Company’s management to perform any and all acts that may be necessary, useful and/or proper to implement Sendas’ Spin-Off, as well as other procedures described in the Sendas’ Protocol, under the terms of the Sendas’ Protocol;

6.2. Regarding the CBD's Spin-Off: (i) by more than a half of the voting shares, being counted 172.285.897 in favor, 402.567 abstentions and 737 contrary votes, to ratify the appointment and hiring of the Appraisal Firm responsible for the appraisal of CBD’ Spun Off; (ii) by more than a half of the voting shares, being counted 169.884.431 in favor, 2.804.061 abstentions and 709 contrary votes, to approve the CBD Appraisal Report, comprising exclusively by the equity interest held by the Company in Sendas, after Sendas’ Spin-Off, pursuant to Exhibit 5.2.(ii); (iii) by more than a half of the voting shares, being counted 172.668.970 in favor, 19.495 abstentions and 736 contrary votes, to ratify the entering into of the CBD Protocol, pursuant to Exhibit 5.2.(iii); (iv) by more than a half of the voting shares, being counted 172.668.970 in favor, 19.495 abstentions and 736 contrary votes, to approve, under the terms of the CBD Protocol, CBD’s Spin-Off with the merger of CBD’ Spun Off by Sendas, as well as other procedures described in the CBD Protocol; and (v) by more than a half of the voting shares, being counted 172.668.428 in favor, 19.647 abstentions and 1.126 contrary votes, to authorize the members of the Company’s management to perform any and all acts that may be necessary, useful and/or proper to implement CBD’s Spin-Off;

Under the terms of the CBD’s Protocol, the 268,351,567 (two hundred and sixty-eight million, three hundred and fifty-one thousand, five hundred and sixty-seven) common, registered shares with no par value, issued by Sendas and held by the Company shall be delivered directly to the Company shareholders in proportion to their respective interests in the Company’s capital stock. This distribution shall occur after Sendas has obtained the listing of the shares issued by it in Novo Mercado segment of B3 S.A. - Brasil, Bolsa, Balcão (“B3”), and the listing of ADSs representing shares of the Company in the New York Stock Exchange (“NYSE”), on a date to be subsequently informed in a Notice to the Shareholders of the Company and Sendas.

As a result of CBD’s Spin-Off, the Company’s subscribed and paid-up capital stock will be reduced by R$ 1.215.962.963,38 (one billion, two hundred and fifteen million, nine hundred and sixty-two thousand, nine hundred and sixty-three reais and thirty-eight cents), going from R$ 6.865.829.549,07 (six billion, eight hundred and sixty-five

Free translation |

million, eight hundred and twenty-nine thousand, five hundred and forty-nine reais and seven cents) to R$ 5.649.866.585,69 (five billion, six hundred and forty-nine million, eight hundred and sixty-six thousand, five hundred and eighty-five reais and sixty-nine cents), keeping the same number of common, registered shares with no par value issued by it, remaining the new capital stock divided into 268,351,567 (two hundred and sixty-eight million, three hundred and fifty-one thousand, five hundred and sixty-seven) common, registered shares with no par value.

6.3. Due to the reduction of the Company's capital resulting from CBD's Spin-Off, as well as to reflect the capital increase approved at the meeting of the Company's Board of Directors held on October 28, 2020, to approve, by a majority of votes, being counted 172.668.265 in favor, 20.104 abstentions and 832 contrary votes, the amendment to Article 4 of the Company's By-Laws, which shall become effective with the following wording:

“ARTICLE 4 – The Company’s capital stock is of R$ 5.649.866.585,69 (five billion, six hundred and forty-nine million, eight hundred and sixty-six thousand, five hundred and eighty-five reais and sixty-nine cents), fully subscribed and paid in, divided into 268,351,567 (two hundred and sixty-eight million, three hundred and fifty-one thousand, five hundred and sixty-seven) common, registered, book entry shares with no par value.”

6.4. As a result of the resolution approved above, by a majority of votes, being counted 172.668.871 in favor, 19.493 abstentions and 837 contrary votes, to restate the Company's By-Laws in order to incorporate the above amendments, which shall become effective pursuant to Exhibit 6.4.

7. Closing and Drawing up: Having no further matters, the work was suspended for the necessary time to draw up these minutes. The session was reopened, these minutes were read, found to be in compliance and signed electronically by all present.

8. Filed Documents: It is filed on the Company’s head office the publications of the Call Notice, the Management Proposal, Sendas’s Appraisal Report; Sendas’s Protocol, CBD’s Appraisal Report; CBD’s Protocol, the detailed final voting map, as well as the voting guidelines and protests received and authenticated by the Chairman and Secretary.

Free translation |

9. Signatures: Board: Chairman: Christophe José Hidalgo; Secretary: Marcelo Acerbi de Almeida. Attending Shareholders: (i) with attorney-in-fact Mayara Zolko: WILKES PARTICIPAÇÕES S.A. SEGISOR KING LLC HELICCO PARTICIPACOES LTDA. DANIELA SABBAG PAPA JORGE FAIÇAL FILHO FREDERICO AUGUSTO ALONSO RONALDO IABRUDI DOS SANTOS PEREIRA LUIZ HENRIQUE RODRIGUES COSTA ANTONIO SERGIO SALVADOR DOS SANTOS BELMIRO DE FIGUEIREDO GOMES RODRIGO ADURA ROBERTA BECHELLI SAMIR DE ARAÚJO JARROUJ ISABELA MARIA CADENASSI BATISTA SPX RAPTOR MASTER FUNDO DE INVESTIMENTO NO EXTERIOR MULTIMERCADO CRÉDITO PRIVADO SPX PATRIOT MASTER FIA SPX NIMITZ MASTER FUNDO DE INVESTIMENTO MULTIMERCADO SPX LANCER PREVIDENCIÁRIO FUNDO DE INVESTIMENTO MULTIMERCADO SPX FALCON MASTER FUNDO DE INVESTIMENTO DE AÇÕES SPX APACHE MASTER FUNDO DE INVESTIMENTO DE AÇÕES CANADIAN EAGLE PORTFOLIO LLC OCEANA INDIAN FUNDO DE INVESTIMENTO EM AÇÕES OCEANA B PREVIDÊNCIA FUNDO DE INVESTIMENTOS EM AÇÕES MÁSTER OCEANA LONG BIASED MASTER FUNDO DE INVESTIMENTO MULTIMERCADO OCEANA 03 MASTER FUNDO DE INVESTIMENTO MULTIMERCADO OCEANA LITORAL FUNDO DE INVESTIMENTO EM AÇÕES OCEANA LONG BIASED PREV FUNDO DE INVESTIMENTO MULTIMERCADO OCEANA LONG BIASED MASTER FUNDO DE INVESTIMENTO DE AÇÕES OCEANA VALOR MASTER FUNDO DE INVESTIMENTO DE AÇÕES OCEANA SELECTION MASTER FUNDO DE INVESTIMENTO DE AÇÕES OCEANA QP8 FUNDO DE INVESTIMENTO EM AÇÕES OCEANA VALOR II MASTER FUNDO DE INVESTIMENTO EM AÇÕES FUNDO DE INVESTIMENTO EM AÇÕES RVA EMB III OCEANA LONG BIASED B PREVIDENCIA FIFE FIM ÖLBERG FUNDO DE INVESTIMENTO MULTIMERCADO INVESTIMENTO NO EXTERIOR HSSP FUNDO DE INVESTIMENTO MULTIMERCADO INVESTIMENTO NO EXTERIOR VOKIN K2 LONG BIASED FUNDO DE INVESTIMENTO EM AÇÕES VOKIN PÃO DE AÇÚCAR FUNDO DE INVESTIMENTO MULTIMERCADO INVESTIMENTO NO EXTERIOR FDI 2 FUNDO DE INVESTIMENTO EM AÇÕES RBC – FUNDO DE INVESTIMENTO EM AÇÕES INVESTIMENTO NO EXTERIOR S4 FUNDO DE INVESTIMENTO MULTIMERCADO CRÉDITO PRIVADO INVESTIMENTO NO EXTERIOR VOKIN EVOLUTION FUNDO DE INVESTIMENTO MULTIMERCADO INVESTIMENTO NO EXTERIOR VOKIN ARARAT FUNDO DE INVESTIMENTO MULTIMERCADO MOSQUETEIROS FUNDO DE INVESTIMENTO EM AÇÕES FIA VOKIN ACONCAGUA MASTER

Free translation |

LONG ONLY ITAÚ NAVI LONG SHORT PREVIDÊNCIA FUNDO DE INVESTIMENTO MULTIMERCADO NAVI LONG BIASED MASTER FUNDO DE INVETIMENTO MULTIMERCADO NAVI LONG SHORT MASTER FUNDO DE INVESTIMENTO MULTIMERCADO NAVI LONG SHORT PREVIDÊNCIA FIFE FUNDO DE INVESTIMENTO MULTIMERCADO CRÉDITO PRIVADO NAVI LONG SHORT XP SEGUROS PREVIDÊNCIA FUNDO DE INVESTIMENTO MULTIMERCADO NAVI B PREVIDÊNCIA FUNDO DE INVESTIMENTO EM AÇÕES MÁSTER NAVI B PREVIDÊNCIA FIFE MASTER FUNDO DE INVESTIMENTO EM AÇÕES NAVI COMPASS MASTER FUNDO DE INVESTIMENTO EM AÇÕES NAVI CRUISE MASTER FUNDO DE INVESTIMENTO EM AÇÕES NAVI FENDER MASTER FUNDO DE INVESTIMENTO EM AÇÕES NAVI INSTITUCIONAL MASTER FUNDO DE INVESTIMENTO EM AÇÕES DUO HIX CAPITAL FUNDO DE INVESTIMENTO DE AÇÕES HIX AUSTRAL FUNDO DE INVESTIMENTO EM AÇÕES HIX CAPITAL MASTER FUNDO DE INVESTIMENTO EM AÇÕES HIX PREV 100 MASTER FUNDO DE INVESTIMENTO MULTIMERCADO HIX CAPITAL INSTITUCIONAL MASTER FUNDO DE INVESTIMENTO EM AÇÕES HIX CAPITAL EQUITIES LLC VELT MASTER PREV FUNDO DE INVESTIMENTO EM AÇÕES VELT MASTER FUNDO DE INVESTIMENTO EM AÇÕES VELT BV FUNDO DE INVESTIMENTO EM AÇÕES - INVESTIMENTO NO EXTERIOR VELT ALÍSIO FUNDO DE INVESTIMENTO EM AÇÕES VELT MASTER INSTITUCIONAL FUNDO DE INVESTIMENTO EM AÇÕES VELT PARTNERS FUND LLC FOURTH SAIL LONG SHORT LLC FOURTH SAIL DISCOVERY LLC "TAVOLA ABSOLUTO MASTER FUNDO DE INVESTIMENTO MULTIMERCADO" TAVOLA ABSOLUTO MASTER FIA TAVOLA LONG SHORT FIM HELIUS LUX LONG BIASED MASTER FUNDO DE INVESTIMENTO MULTIMERCADO; (ii) with attorney-in-fact Livia Beatriz Silva do Prado: STICHTING JURIDISCH EIGENAAR ACTIAM BELEGGINGSFONDSEN BEST INVESTMENT CORPORATION AGFIQ EMERGING MARKETS EQUITY ETF ARROWSTREET (CANADA) ACWI MINIMUM VOLATILITY ALPHA EXTENSION FUND I ARROWSTREET (CANADA) GLOBAL WORLD ALPHA EXTENSION FUND I ARROWSTREET ACWI ALPHA EXTENSION FUND III (CAYMAN) LIMITED ARROWSTREET ACWI ALPHA EXTENSION FUND V (CAYMAN) LIMITED ARROWSTREET CAPITAL GLOBAL EQUITY ALPHA EXTENSION FUND LIMITED ARROWSTREET CAPITAL GLOBAL EQUITY LONG/SHORT FUND LIMITED ARROWSTREET US GROUP TRUST ASCENSION ALPHA FUND, LLC BLACKWELL PARTNERS LLC SERIES A

Free translation |

BOSTON PARTNERS EMERGING MARKETS FUND BOSTON PARTNERS EMERGING MARKETS LONG/SHORT FUND BRITISH COLUMBIA INVESTMENT MANAGEMENT CORPORATION BRUNEI INVESTMENT AGENCY CALIFORNIA STATE TEACHERS RETIREMENT SYSTEM CANADA PENSION PLAN INVESTMENT BOARD CAUSEWAY EMERGING MARKETS FUND CAUSEWAY INTERNATIONAL OPPORTUNITIES FUND CHANG HWA COMMERCIAL BANK, LTD., IN ITS CAPACITY AS MASTER CUSTODIAN OF NOMURA BRAZIL FUND CITY OF NEW YORK GROUP TRUST COLLEGE RETIREMENT EQUITIES FUND COMMONWEALTH SUPERANNUATION CORPORATION CONSULTING GROUP CAPITAL MARKETS FUNDS - EMERGING MARKETS EQUITY FUND DESJARDINS EMERGING MARKETS MULTIFACTOR - CONTROLLED VOLATILITY ETF EATON VANCE MANAGEMENT FIDELITY RUTLAND SQUARE TRUST II: STRATEGIC ADVISERS EMERGING MARKETS FUND FIDELITY SALEM STREET TRUST: FIDELITY FLEX INTERNATIONAL INDEX FUND FIDELITY SALEM STREET TRUST: FIDELITY INTERNATIONAL SUSTAINABILITY INDEX FUND FIDELITY SALEM STREET TRUST: FIDELITY SERIES GLOBAL EX U.S. INDEX FUND FIRST TRUST LATIN AMERICA ALPHADEX FUND FRANKLIN TEMPLETON ETF TRUST - FRANKLIN FTSE BRAZIL ETF FRANKLIN TEMPLETON ETF TRUST - FRANKLIN FTSE LATIN AMERICA ETF FUTURE FUND BOARD OF GUARDIANS GAM MULTISTOCK GOVERNMENT EMPLOYEES SUPERANNUATION BOARD IBM 401(K) PLUS PLAN INVESCO PUREBETASM FTSE EMERGING MARKETS ETF INVESTERINGSFORENINGEN DANSKE INVEST INDEX GLOBAL AC RESTRICTED – ACCUMULATING KL ITAÚ FUNDS - LATIN AMERICA EQUITY FUND JANA EMERGING MARKETS SHARE TRUST JAPAN TRUSTEE SERVICES BANK, LTD. RE: RTB NIKKO BRAZIL EQUITY ACTIVE MOTHER FUND JAPAN TRUSTEE SERVICES BANK, LTD. RE: STB DAIWA EMERGING EQUITY FUNDAMENTAL INDEX MOTHER FUND JNL MULTI-MANAGER ALTERNATIVE FUND JOHN HANCOCK FUNDS II INTERNATIONAL STRATEGIC EQUITY ALLOCATION FUND JOHN HANCOCK FUNDS II STRATEGIC EQUITY ALLOCATION FUND JOHN HANCOCK VARIABLE INSURANCE TRUST INTERNATIONAL EQUITY INDEX TRUST KAISER FOUNDATION HOSPITALS KAISER PERMANENTE GROUP TRUST LACM GLOBAL EQUITY FUND L.P. LEGAL & GENERAL FUTURE WORLD CLIMATE CHANGE EQUITY FACTORS INDEX FUND LEGAL & GENERAL GLOBAL EQUITY INDEX FUND LOS ANGELES COUNTY EMPLOYEES RETIREMENT

Free translation |

ASSOCIATION MANAGED PENSION FUNDS LIMITED MERCER QIF FUND PLC NATIONAL COUNCIL FOR SOCIAL SECURITY FUND NATWEST TRUSTEE AND DEPOSITARY SERVICES LIMITED AS TRUSTEE OF ST. JAMES'S PLACE STRATEGIC MANAGED UNIT TRUST NEW YORK STATE TEACHERS RETIREMENT SYSTEM NEW ZEALAND SUPERANNUATION FUND NORGES BANK NORTHERN TRUST INVESTMENT FUNDS PLC NORTHERN TRUST UCITS FGR FUND NTGI - QM COMMON DAILY ALL COUNTRY WORLD EX-US INVESTABLE MARKET INDEX FUND - LENDING NUVEEN EMERGING MARKETS EQUITY FUND OHIO POLICE AND FIRE PENSION FUND PARAMETRIC EMERGING MARKETS FUND PARAMETRIC TAX-MANAGED EMERGING MARKETS FUND SCHLUMBERGER INTERNATIONAL STAFF RETIREMENT FUND, FCP-SIF SCHWAB EMERGING MARKETS EQUITY ETF SCHWAB FUNDAMENTAL EMERGING MARKETS LARGE COMPANY INDEX ETF SCHWAB FUNDAMENTAL EMERGING MARKETS LARGE COMPANY INDEX FUND SPARTAN GROUP TRUST FOR EMPLOYEE BENEFIT PLANS: SPARTAN EMERGING MARKETS INDEX POOL SPDR MSCI EMERGING MARKETS FOSSIL FUEL FREE ETF SPDR MSCI EMERGING MARKETS STRATEGICFACTORS ETF SPDR S&P EMERGING MARKETS FUND SSGA MSCI ACWI EX-USA INDEX NON-LENDING DAILY TRUST SSGA SPDR ETFS EUROPE I PLC STANLIB FUNDS LIMITED STATE OF ALASKA RETIREMENT AND BENEFITS PLANS STATE OF NEW JERSEY COMMON PENSION FUND D STATE STREET EMERGING MARKETS EQUITY INDEX FUND STATE STREET GLOBAL ADVISORS LUXEMBOURG SICAV STATE STREET GLOBAL ADVISORS LUXEMBOURG SICAV - STATE STREET EMERGING MARKETS SRI ENHANCED EQUITY FUND STATE STREET GLOBAL ADVISORS LUXEMBOURG SICAV - STATE STREET ENHANCED EMERGING MARKETS EQUITY FUND STATE STREET GLOBAL ADVISORS LUXEMBOURG SICAV - STATE STREET GLOBAL EMERGING MARKETS INDEX EQUITY FUND STATE STREET GLOBAL ADVISORS TRUST COMPANY INVESTMENT FUNDS FOR TAX EXEMPT RETIREMENT PLANS STATE STREET GLOBAL ALL CAP EQUITY EX-U.S. INDEX PORTFOLIO STATE STREET IRELAND UNIT TRUST STATE STREET MSCI ACWI EX USA IMI SCREENED NON-LENDING COMMON TRUST FUND STATE STREET MSCI BRAZIL INDEX NON-LENDING COMMON TRUST FUND STICHTING PENSIOENFONDS ING SUNSUPER SUPERANNUATION FUND TEACHER RETIREMENT SYSTEM OF TEXAS THE BOARD OF THE PENSION PROTECTION FUND THE MASTER TRUST BANK OF JAPAN, LTD. AS

Free translation |

TRUSTEE OF NIKKO BRAZIL EQUITY MOTHER FUND THE NOMURA TRUST AND BANKING CO., LTD. RE: INTERNATIONAL EMERGING STOCK INDEX MSCI EMERGING NO HEDGE MOTHER FUND THE SEVENTH SWEDISH NATIONAL PENSION FUND- AP 7 EQUITY FUND THRIVENT CORE EMERGING MARKETS EQUITY FUND THRIVENT INTERNATIONAL ALLOCATION FUND THRIVENT INTERNATIONAL ALLOCATION PORTFOLIO TIAA-CREF FUNDS - TIAA-CREF EMERGING MARKETS EQUITY FUND TIAA-CREF FUNDS - TIAA-CREF EMERGING MARKETS EQUITY INDEX FUND TRUST & CUSTODY SERVICES BANK, LTD. RE: EMERGING EQUITY PASSIVE MOTHER FUND UTAH STATE RETIREMENT SYSTEMS VANGUARD FUNDS PUBLIC LIMITED COMPANY VANGUARD INVESTMENT SERIES PLC VANGUARD INVESTMENTS FUNDS ICVC-VANGUARD FTSE GLOBAL ALL CAP INDEX FUND VANGUARD TOTAL WORLD STOCK INDEX FUND, A SERIES OF VANGUARD INTERNATIONAL EQUITY INDEX FUNDS VERDIPAPIRFONDET KLP AKSJE FREMVOKSENDE MARKEDER FLERFAKTOR VERDIPAPIRFONDET KLP AKSJE FREMVOKSENDE MARKEDER INDEKS I VICTORYSHARES EMERGING MARKET VOLATILITY WTD ETF WASHINGTON STATE INVESTMENT BOARD WELLS FARGO FACTOR ENHANCED EMERGING MARKETS PORTFOLIO WEST VIRGINIA INVESTMENT MANAGEMENT BOARD WISDOMTREE EMERGING MARKETS EX-STATE-OWNED ENTERPRISES FUND WM POOL - EQUITIES TRUST NO. 75 BRITISH COAL STAFF SUPERANNUATION SCHEME BUREAU OF LABOR FUNDS - LABOR RETIREMENT FUND BUREAU OF LABOR FUNDS-LABOR INSURANCE FUND BUREAU OF LABOR FUNDS-LABOR PENSION FUND COMMINGLED PENSION TRUST FUND EMERGING MARKETS RESEARCH ENHANCED EQUITY OF JPMORGAN CHASE BANK NA JNL/MELLON EMERGING MARKETS INDEX FUND JP MORGAN DIVERSIFIED FUND JPMORGAN EMERGING MARKETS RESEARCH ENHANCED EQUITY FUND JPMORGAN FUNDS MINEWORKERS`PENSION SCHEME NATIONAL PENSION INSURANCE FUND NEW SOUTH WALES TREASURY CORPORATION AS TRUSTEE FOR THE TCORPIM EMERGING MARKET SHARE FUND PUBLIC EMPLOYEES RETIREMENT SYSTEM OF OHIO SAS TRUSTEE CORPORATION POOLED FUND SBC MASTER PENSION TRUST SCRI - ROBECO QI CUSTOMIZED EMERGING MARKETS ENHANCED INDEX EQUITIES FUND SKAGEN KON-TIKI VERDIPAPIRFOND STICHTING DEPOSITARY APG EMERGING MARKETS EQUITY POOL THE MASTER TRUST BANK OF JAPAN, LTD. AS TRUSTEE FOR MTBJ400045828 THE MASTER TRUST BANK OF

Free translation |

JAPAN, LTD. AS TRUSTEE FOR MTBJ400045829 THE MASTER TRUST BANK OF JAPAN, LTD. AS TRUSTEE FOR MTBJ400045835 THE MASTER TRUST BANK OF JAPAN, LTD. AS TRUSTEE FOR MUTB400045792 THE MASTER TRUST BANK OF JAPAN, LTD. AS TRUSTEE FOR MUTB400045794 THE MASTER TRUST BANK OF JAPAN, LTD. AS TRUSTEE FOR MUTB400045795 VANGUARD EMERGING MARKETS SHARES INDEX FUND VANGUARD EMERGING MARKETS STOCK INDEX FUND VANGUARD TOTAL INTERNATIONAL STOCK INDEX FUND, A SERIES OF VANGUARD STAR FUNDS AMUNDI FUNDS AMUNDI INDEX SOLUTIONS GLOBAL MULTI-FACTOR EQUITY FUND MORGAN STANLEY INVESTMENT FUNDS GLOBAL BALANCED DEFESINVE FUND WITH CVM: 22918.000043.336912.1-6 MORGAN STANLEY INVESTMENT FUNDS GLOBAL BALANCED FUND WITH CVM: 22918.000043.336920.1-7 MORGAN STANLEY INVESTMENT FUNDS GLOBAL BALANCED INCOME FUND WITH CVM: 22918.000043.295779.1-5 J.P MORGAN CHASE BANK NA; (iii) with attorney-in-fact Karen Sanchez Guimarães: GWI ASSET MANAGEMENT S.A.; (iv) with attorney-in-fact Debora de Souza Morsch: CONTINENTAL FUNDO DE INVESTIMENTO EM AÇÕES HAYP FUNDO DE INVESTIMENTO EM AÇÕES; (v) CHRISTOPHE JOSÉ HIDALGO; and (vi) SERGIO FEIJÃO FILHO.

São Paulo, December 31, 2020

This is a true copy of the minutes drawn up in the proper book.

___________________________ Christophe José Hidalgo Chairman Signed electronically | ___________________________ Marcelo Acerbi de Almeida Secretary Signed electronically |

Free translation |

PROTEST

Shareholder CAISSE DE DEPOT ET PLACEMENT DU QUEBEC

As the legal representative of the shareholder CAISSE DE DEPOT ET PLACEMENT DU QUEBEC, the present protest is drawn up in view of the Company's non-acceptance of the power of attorney presented to the GSM held on this date, due to the alleged allegation of power of attorney unfit to participate, which does not match the document previously presented since the notary acknowledged the signatory of the power of attorney and it has fulfilled all legal procedures for regularization, as set out below by the Company.

“We clarify that some of the funds represented by us are non-resident investors, incorporated abroad and as already informed, their powers are verified in the act of notarization, I ask you to note that despite the lack of signature of one of the signatories, this power of attorney is duly certified responsible notary (Page 7), recognizing the validity of the instrument, even with the material error now pointed out.”

In these terms, we ask that said protest be authenticated and received by the board of the present Extraordinary General Meeting of Companhia Brasileira de Distribuição.

São Paulo, December 31,2020.

Free translation |

Exhibit 5.1(ii)

Sendas’ Appraisal Report

| SENDAS DISTRIBUIDORA S.A. | ||

| Appraisal report at book value on the net assets for purposes of spin-off with merger | ||

| November 23, 2020 | 1 00 036/20 | |

Free translation |

Dear Shareholders of

SENDAS DISTRIBUIDORA S.A. and of

COMPANHIA BRASILEIRA DE DISTRIBUIÇÃO

MAGALHÃES ANDRADE S/S AUDITORES INDEPENDENTES, audit and consulting firm, enrolled with the Regional Accounting Council of the State of São Paulo under number 2SP000233/O-3, registered with the National Registry of Legal Entities under number 62.657.242/0001-00 and located at Av. Brigadeiro Faria Lima, 1893 – 6th floor, Jardim Paulistano, São Paulo, Capital, appointed by you as expert to carry out the appraisal of the net assets at fair value of SENDAS DISTRIBUIDORA S.A., for purposes of partial spin-off with merger into the equity of COMPANHIA BRASILEIRA DE DISTRIBUIÇÃO, fulfilled the diligences and verifications required for the performance of its work, presents this instrument.

APPRAISAL REPORT

which is subscribed.

São Paulo, November 23, 2020

MAGALHÃES ANDRADE S/S

Auditores Independentes

CRC2SP000233/O-3

GUY ALMEIDA ANDRADE

Accountant CRC1SP116758/O-6

Free translation |

INTRODUCTION

| 1. | The purpose of this spin-off and merger transaction is to separate certain assets of SENDAS DISTRIBUIDORA S.A. (SENDAS), which shall be merged into COMPANHIA BRASILEIRA DE DISTRIBUIÇÃO (CBD), in order to release the potential cash & carry business developed by SENDAS and the traditional retail business to be developed by CBD and its subsidiaries, for purposes of independent operation, with separate management and focused on the respective business models and market opportunities. In addition, by virtue of the Sendas’ Spin-off, each business shall have direct access to the capital market and other financing sources, to focus on the investment needs according to the profile of each company, creating, therefore, more value to the respective shareholders. |

| 2. | The spun-off company SENDAS is the wholly-owned subsidiary of the merging company CBD. |

| 3. | Therefore, the present Report, has the purpose of determining the book value of the net assets to be spun-off and merged, taking into account the financial position of SENDAS on September 30, 2020. |

| 4. | Accordingly, we analyzed the SENDAS’ balance sheet on the base appraisal date. |

MANAGEMENT’S RESPONSIBILITY FOR ACCOUNTING INFORMATION

| 5. | The SENDAS’ management is responsible for the bookkeeping of the accounting books and the preparation of the accounting information in accordance with the accounting practices adopted in Brazil and for the adjustments to market prices, as well as for the relevant internal controls deemed necessary for the preparation of such accounting information free and clear from relevant distortion, regardless if caused by fraud or error. The main accounting practices adopted by the Company and determined by management are described in EXHIBIT 2 of the Appraisal Report. |

COVERAGE OF WORK AND LIABILITY OF THE ACCOUNTANT

| 6. | Our responsibility is to express a conclusion on the value of the SENDAS’ partial net assets as at September 30, 2020, based on the work conducted in conformity with Technical Communication CTG 2002, approved by the Federal Accounting Council (CFC), which provides for the application of procedures in the analysis of the balance sheet for issuance of the Appraisal Report. Therefore, we have executed the appraisal of said SENDAS’ balance sheet in accordance to the Brazilian and the international audit regulations, which require the compliance of ethical requirements by the accountant, as well as ensure that the work is planned and the executed with the purposes of obtaining reasonable assurance that the shareholders’ equity calculated for the preparation of our appraisal report, is free from any material misstatement. |

| 7. | The issuance of the appraisal report involves the performance of selected procedures for purposes of verification of the amounts included in the Appraisal Report. The procedures selected depend on the |

Free translation |

accountant’s judgment, including the assessment of the risks of material misstatement of the shareholders’ equity, whether due to fraud or error. In the evaluation of risks, we consider the relevant internal controls for preparation and proper presentation of the SENDAS’ balance sheet to determine the most appropriate procedures under the circumstances, however without expressing an opinion on these internal controls. Our work also includes an evaluation of the adequacy of the accounting policies adopted and reasonability of the management’s accounting estimates. We believe that the evidence obtained is sufficient and appropriate to substantiate our conclusion.

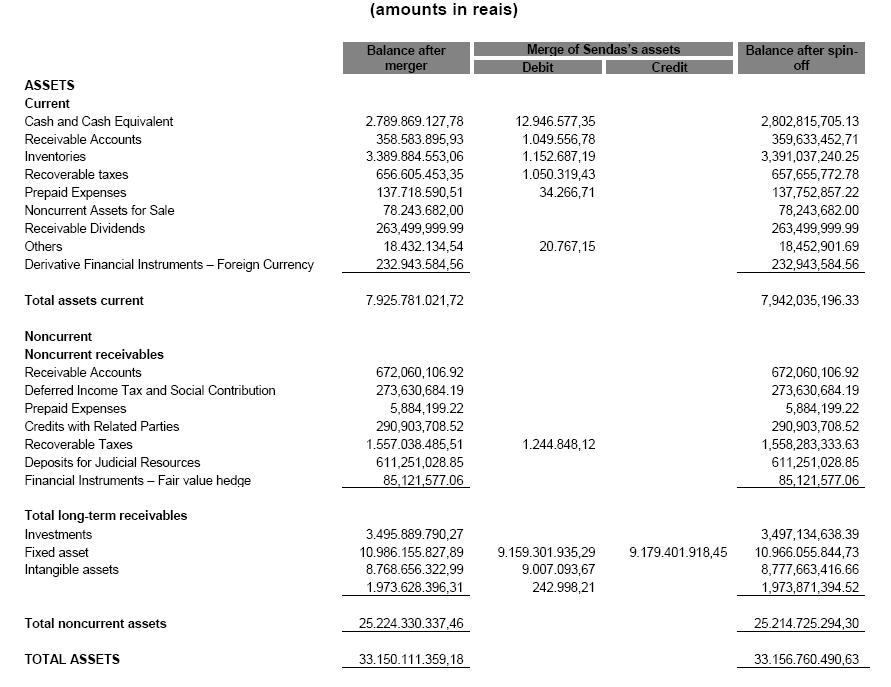

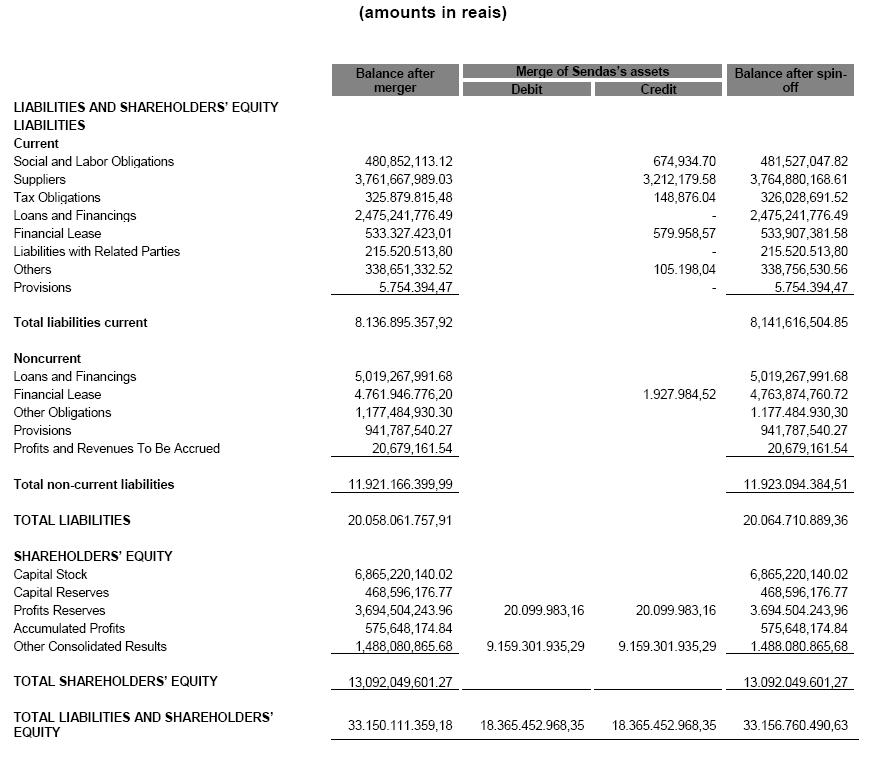

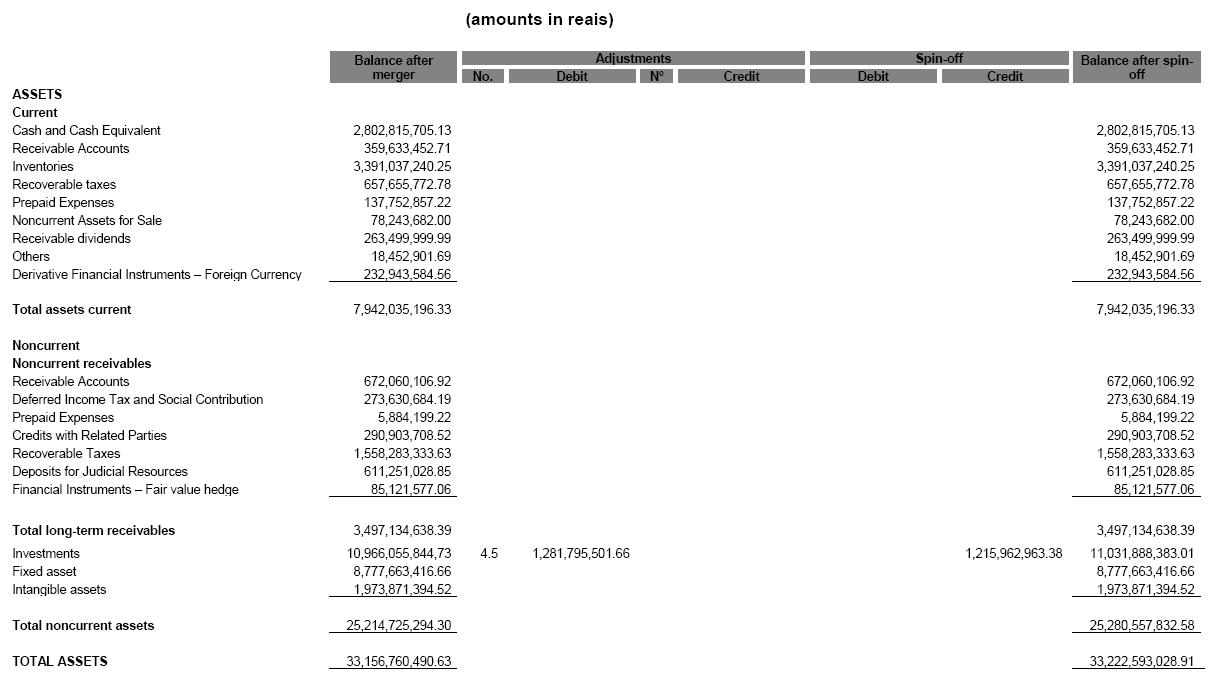

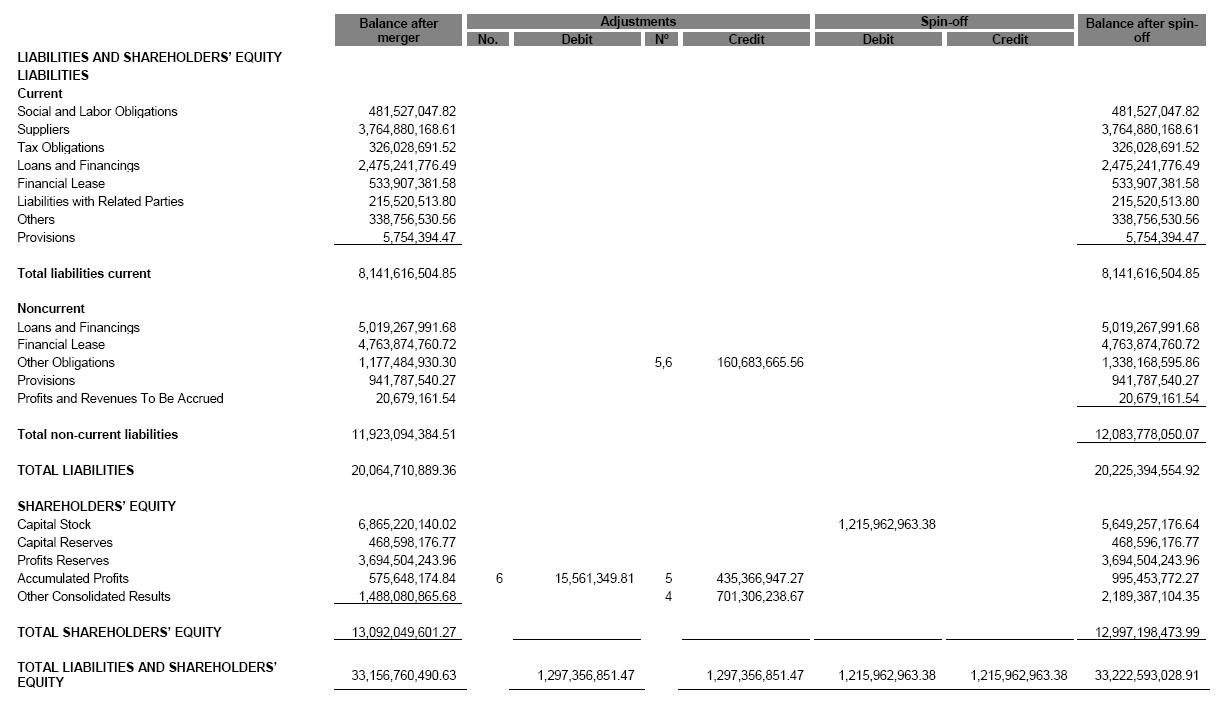

SENDAS’ FINANCIAL POSITION

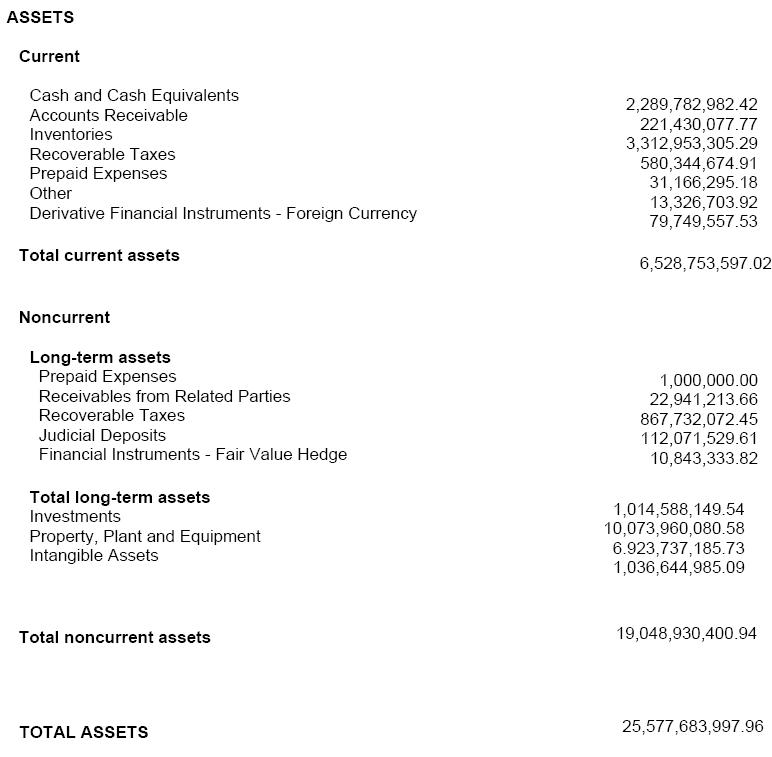

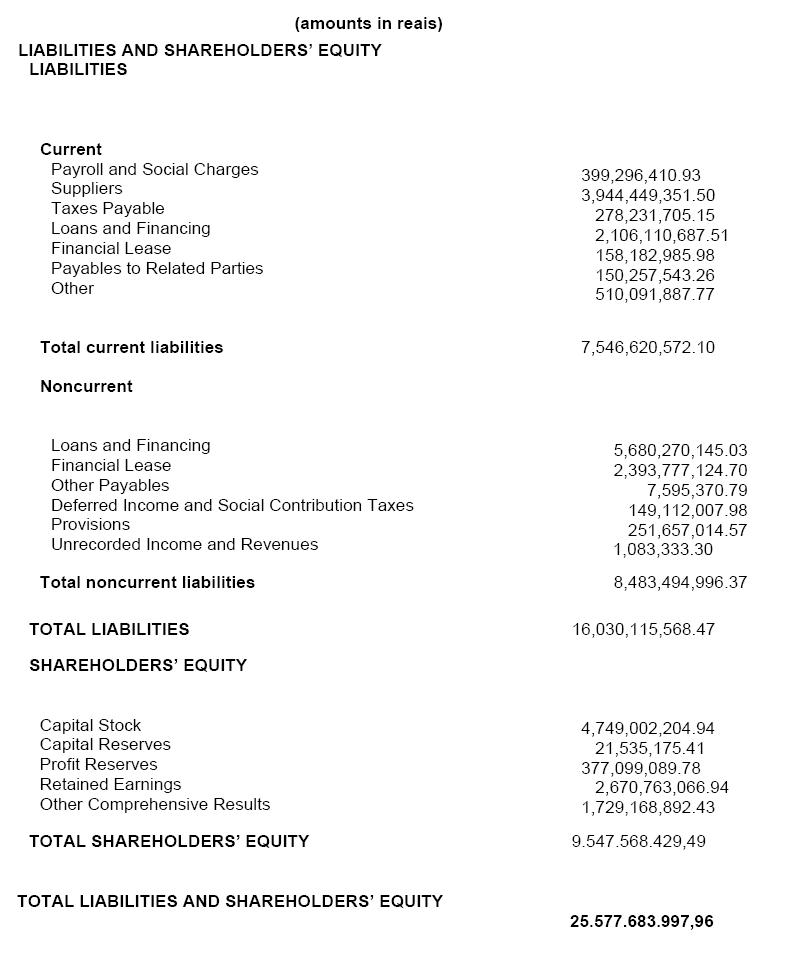

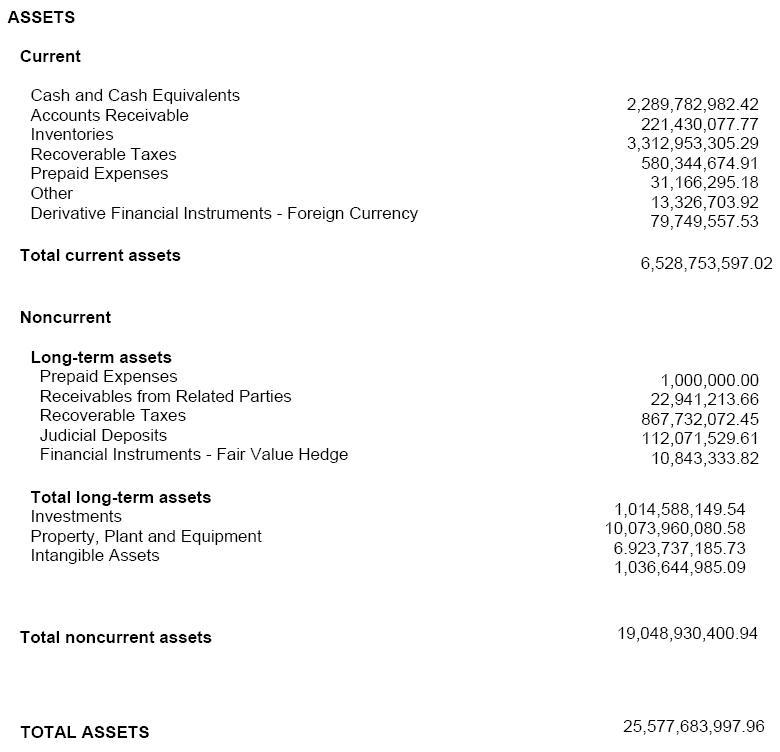

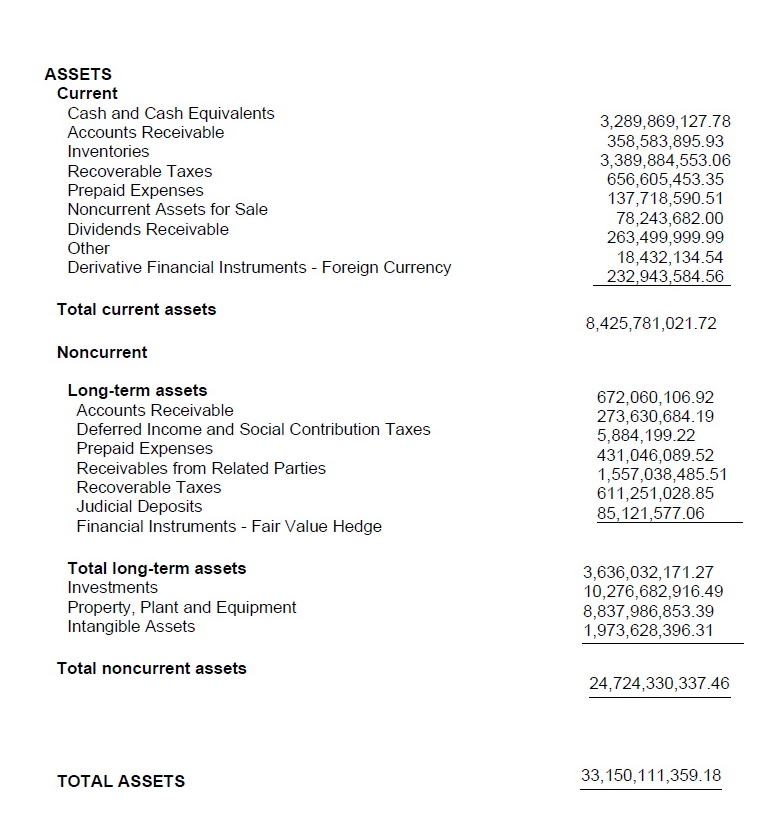

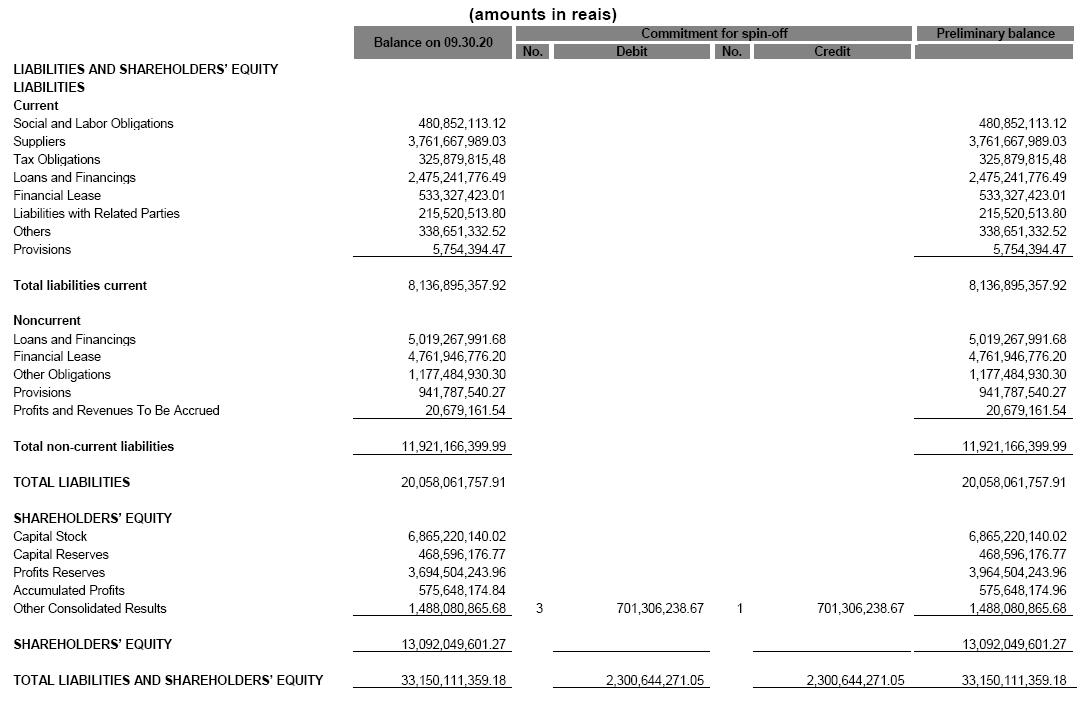

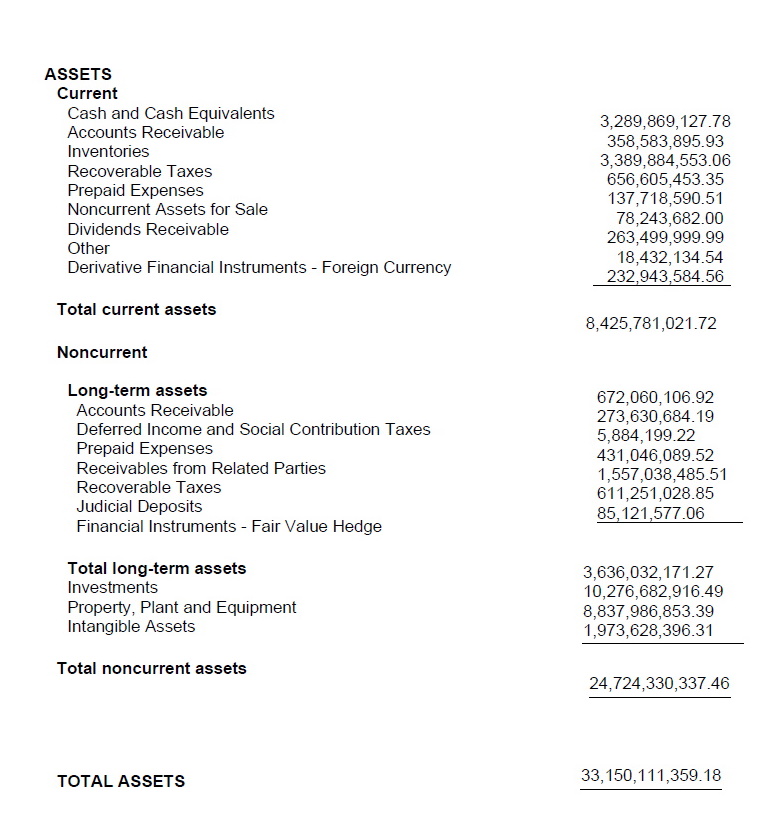

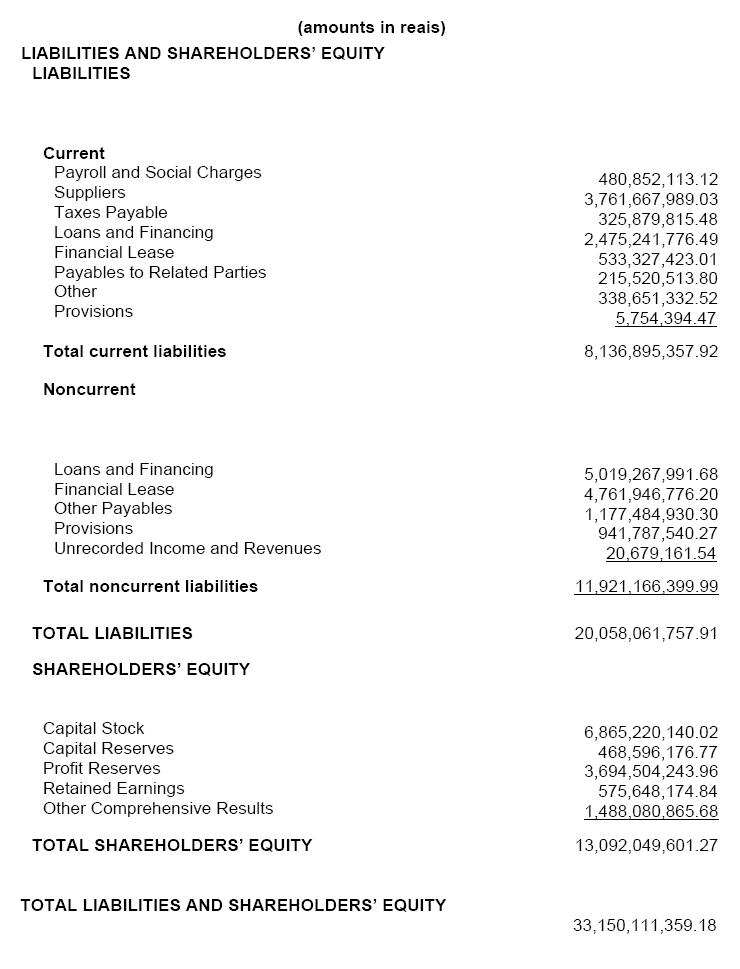

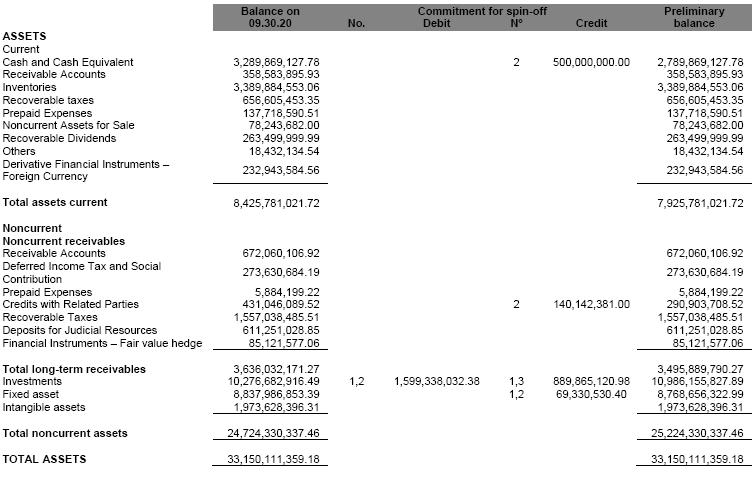

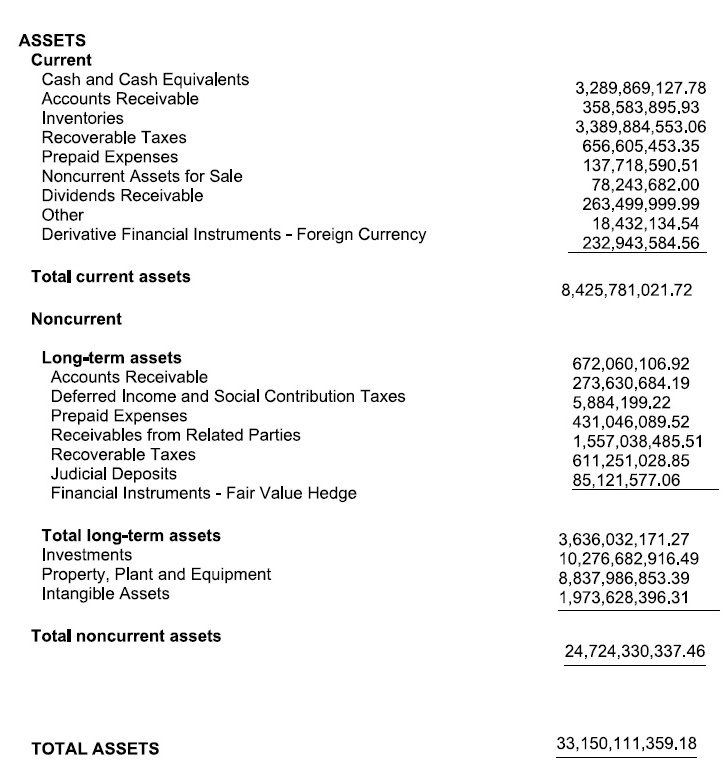

| 8. | The SENDAS’ financial position as at September 30, 2020, at book value, is reflected in the balance sheet, included in EXHIBIT 1, summarized as follows: |

| ASSET | 25.577.683.997,96 |

| (-) LIABILITY | 16.030.115.568,47 |

| SHAREHOLDER’S EQUITY | 9.547.568.429,49 |

| 9. | SENDAS keeps its accounting regular, and its operations registered in own book and its balances duly composed and reconciled. |

| 10. | SENDAS’ accounting procedures are compliant with the accounting practices adopted in Brazil, based on the technical pronouncements issued by the Accounting Pronouncements Committee (CPC) and, therefore, the accounting balances recognize the value of the investments stated at the value of the investees’ equity. EXHIBIT 2 shows the main accounting practices adopted by the management in order to prepare SENDAS’ balance sheet. |

| 11. | The accounting procedures consider, for purposes of evaluation of the assets and liabilities, that the Company may continue as a going concern. Our evaluation also considered that the Company may continue as a going concern. |

EXTRA-ACCOUNTING ADJUSTMENTS TO REFLECT PRE-SPIN-OFF AGREEMENTS

| 12. | Before the spin-off, however after the base date of the equity evaluation, SENDAS and CBD agreed the exchange of assets, which shall be considered for purposes of this appraisal. |

| 13. | SENDAS holds four hundred and thirty-two million, two hundred and fifty-six thousand and six hundred and sixty-eight (432.256.668) common shares of Almacenes Èxito S.A. (Èxito), representing 96,57% of |

Free translation |

Èxito’s capital at the book value of R$ 10.073.960.080,58 (ten billion, seventy-three million, nine hundred and seventy thousand and eighty reais and fifty-eight cents). The book value of this asset, which was currently acquired, is consistent with its respective market price.

| 14. | Through exchange, SENDAS delivers to CBD 39.205.678 shares of Éxito’s capital stock, representing nine point zero seven nine four three percent (9.07943%) of that company’s capital stock at the fair value of R$914.658.145,29 (nine hundred and fourteen million, six hundred and fifty-eight thousand, one hundred and forty-five reais and twenty-nine cents). |

15. As a contra entry, SENDAS shall receive from CBD the following assets:

| Assets | Book value | Fair value |

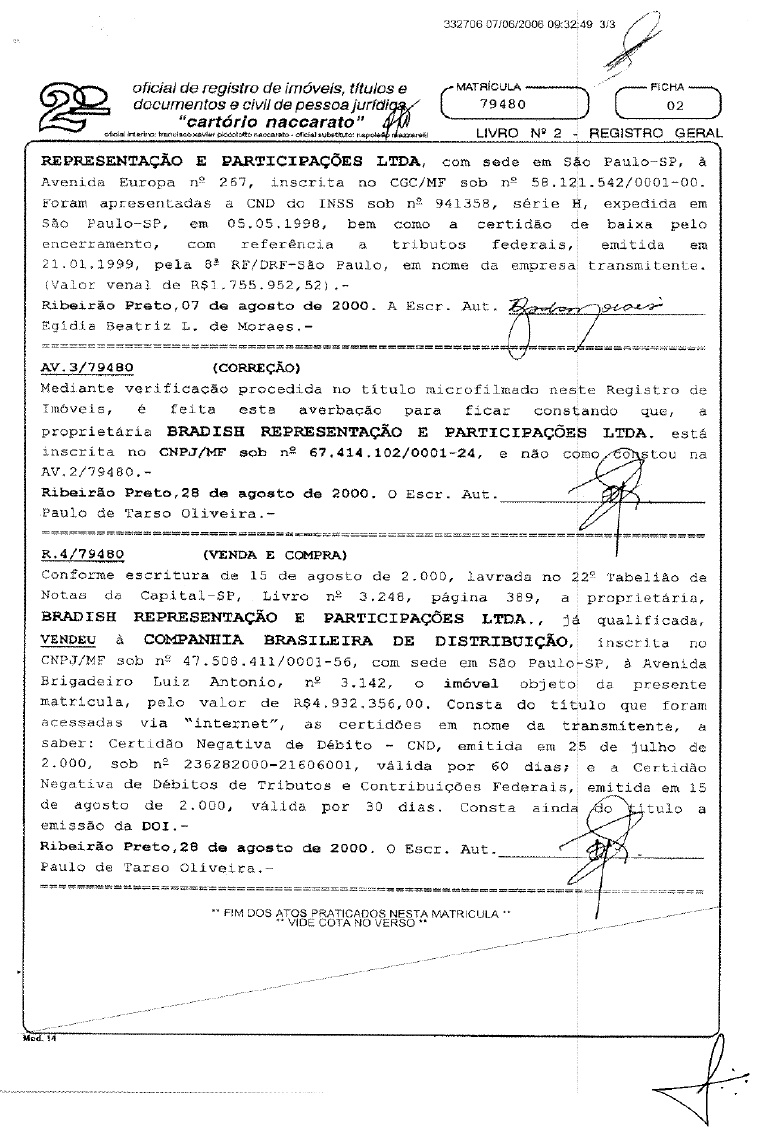

| 6.941.378.937 quotas of capital stock of Bellamar Empreendimento e Participações S.A. | 188.558.882,31 | 769.048.145,29 |

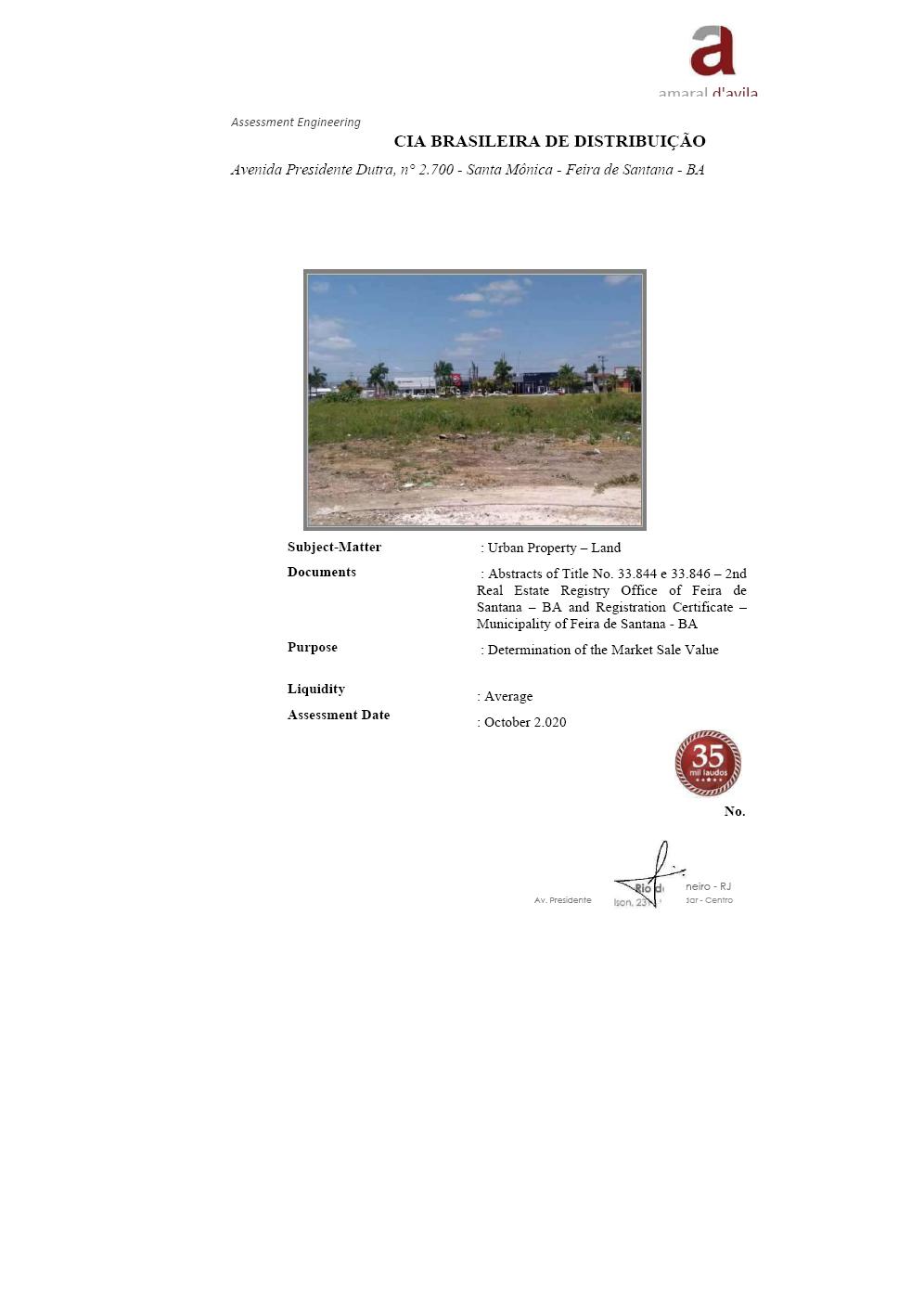

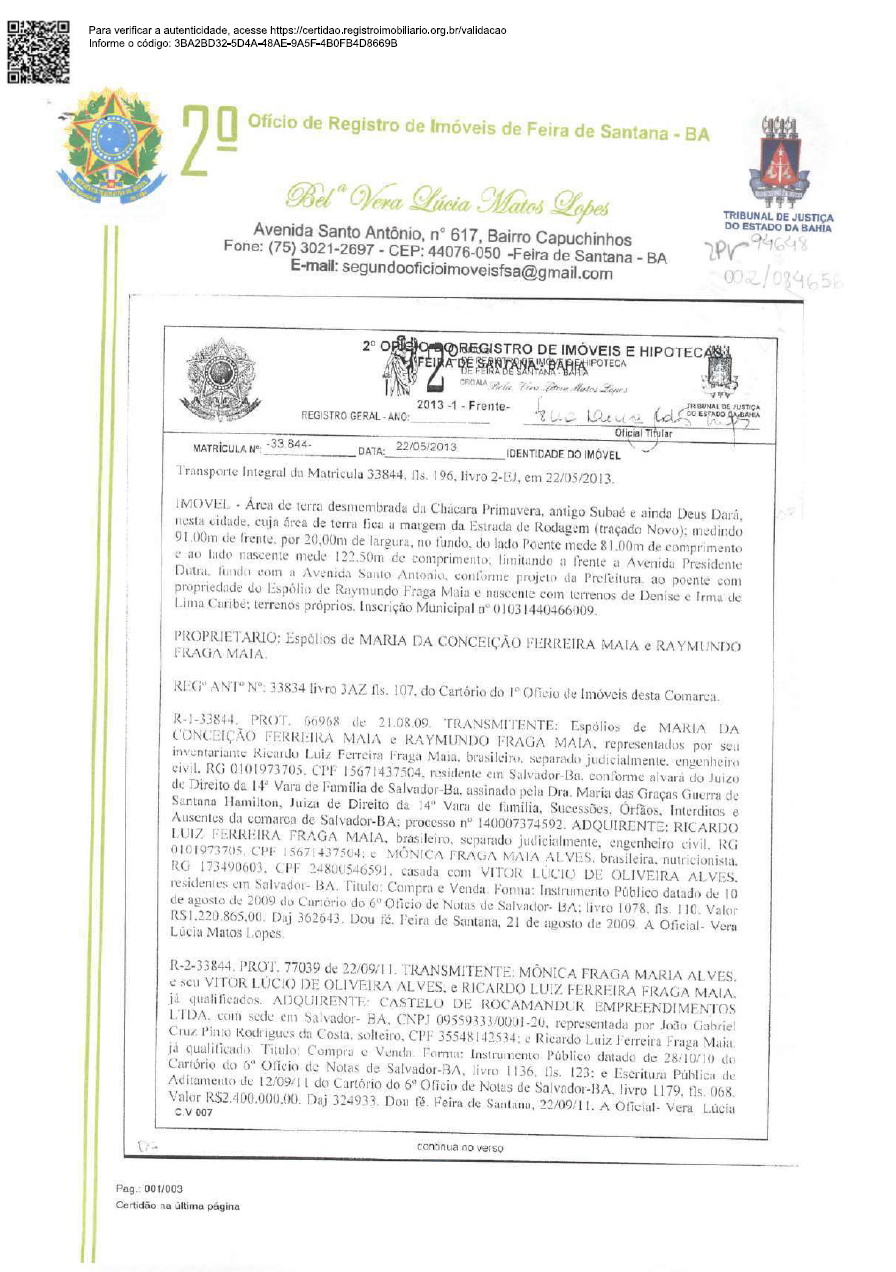

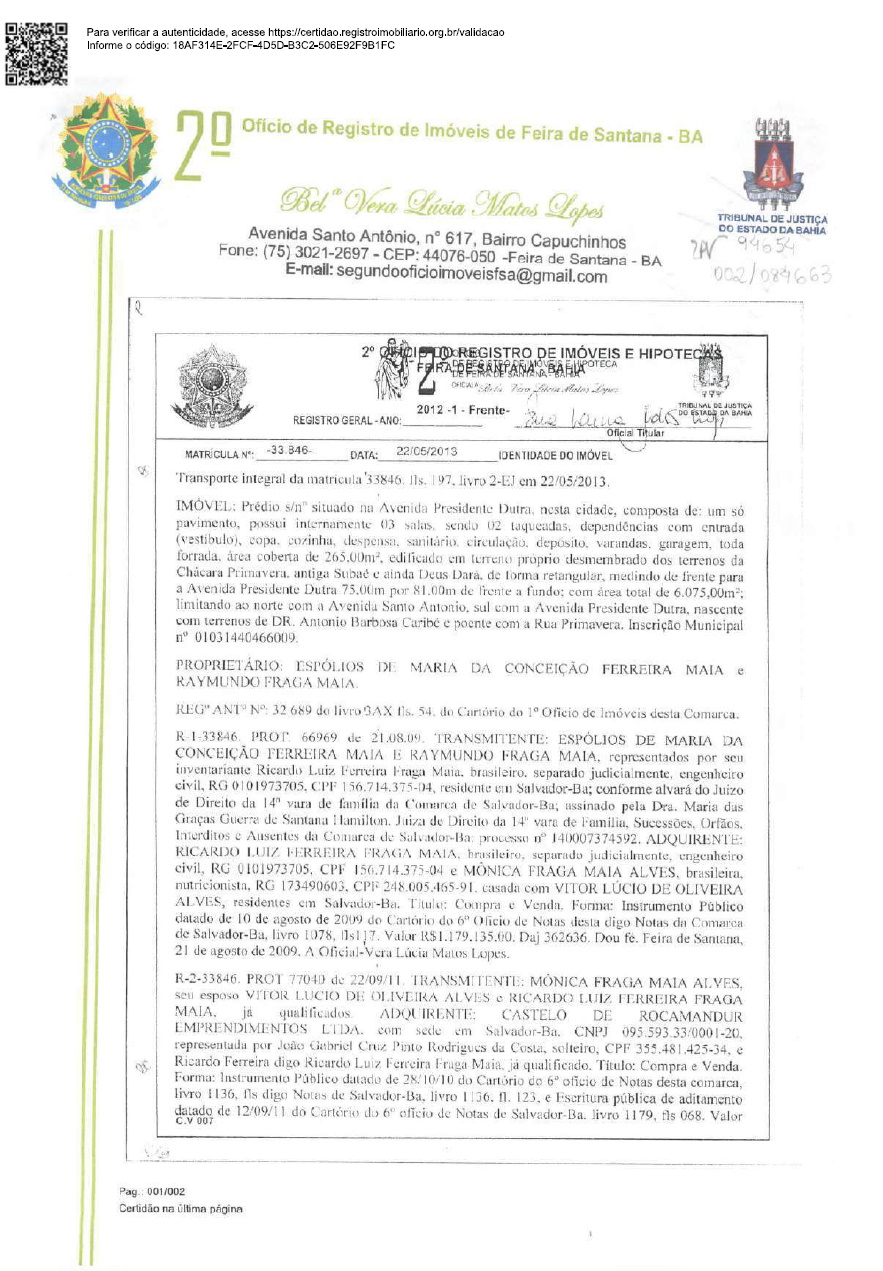

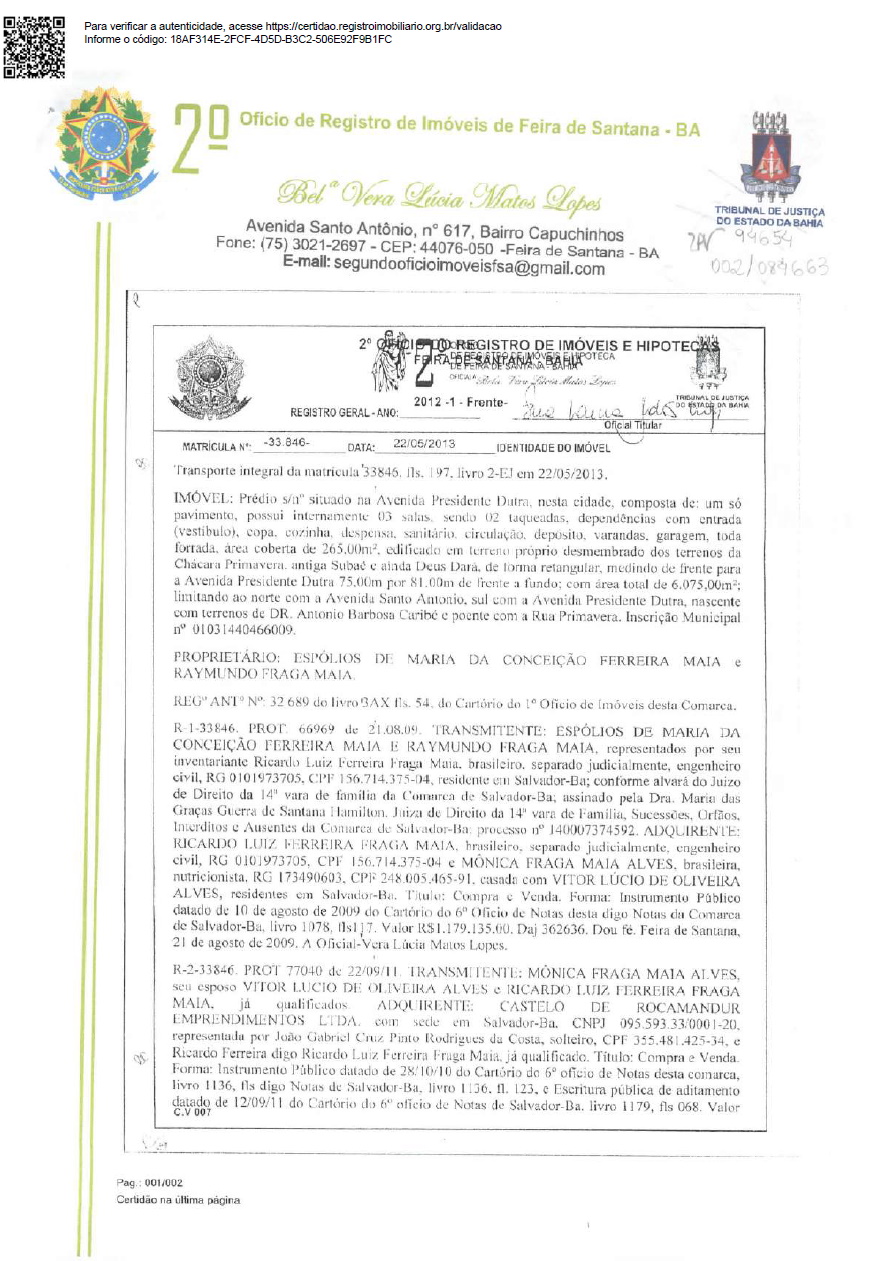

| Land Feira de Santana | 13.286.435,20 | 15.070.000,00 |

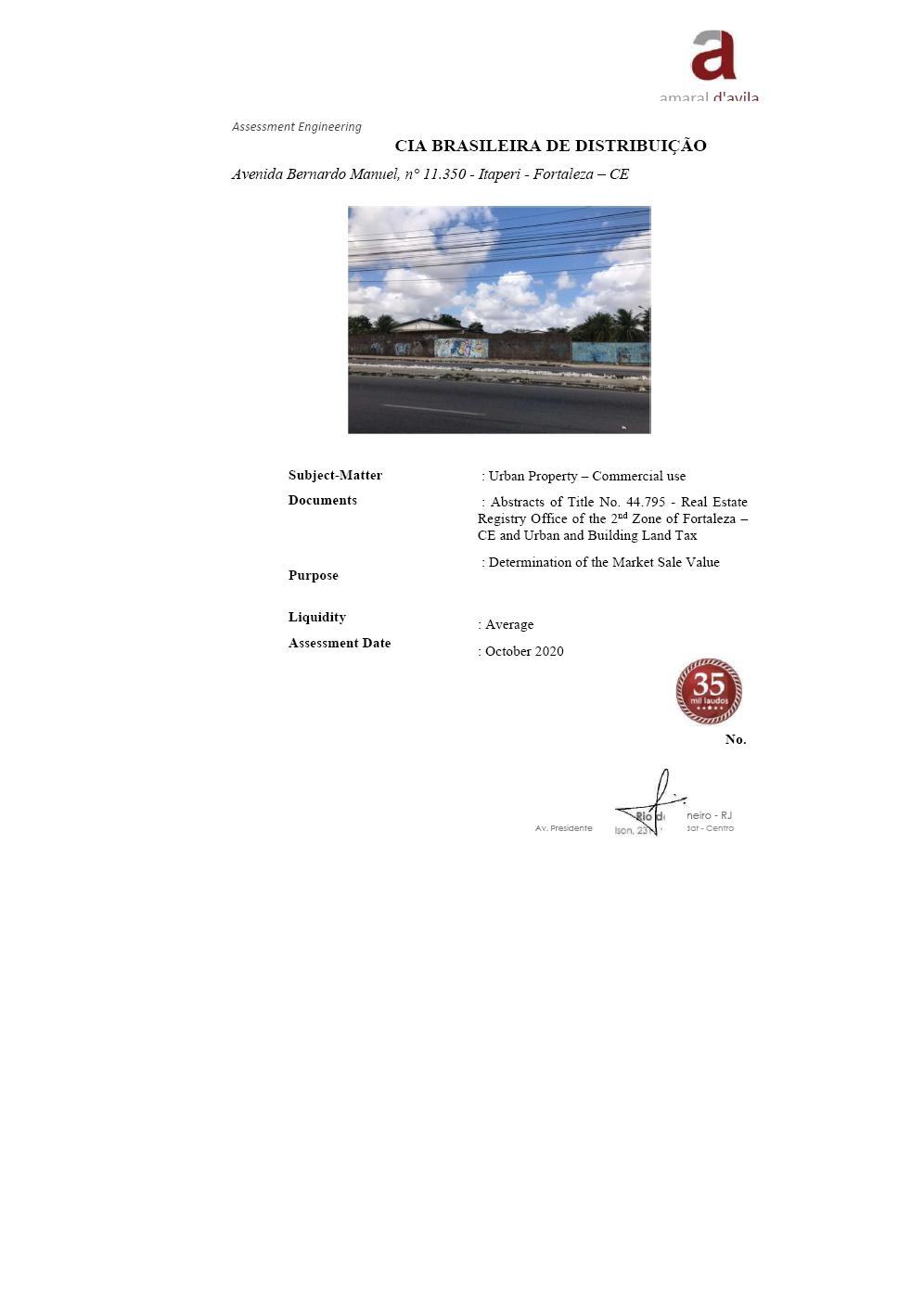

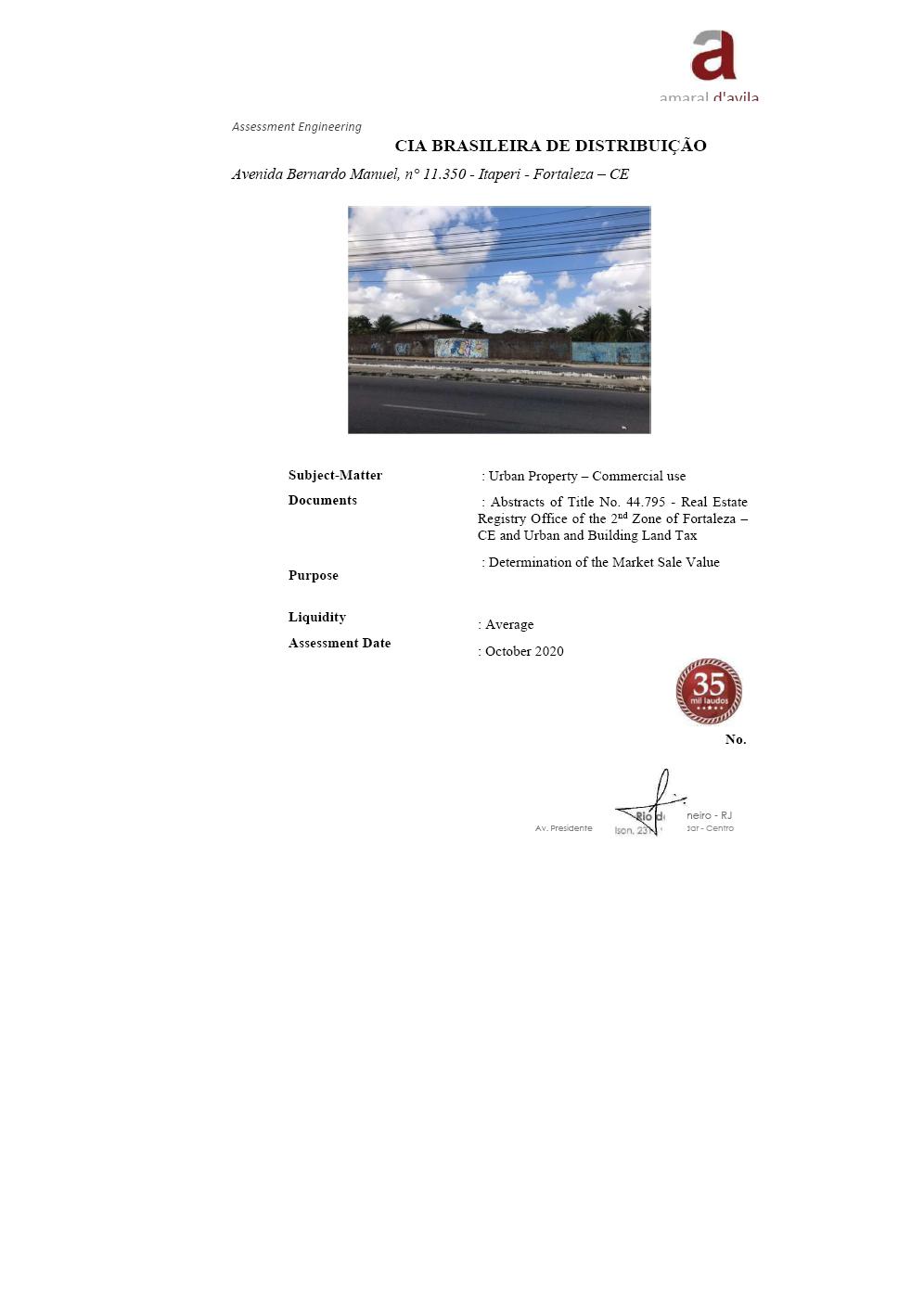

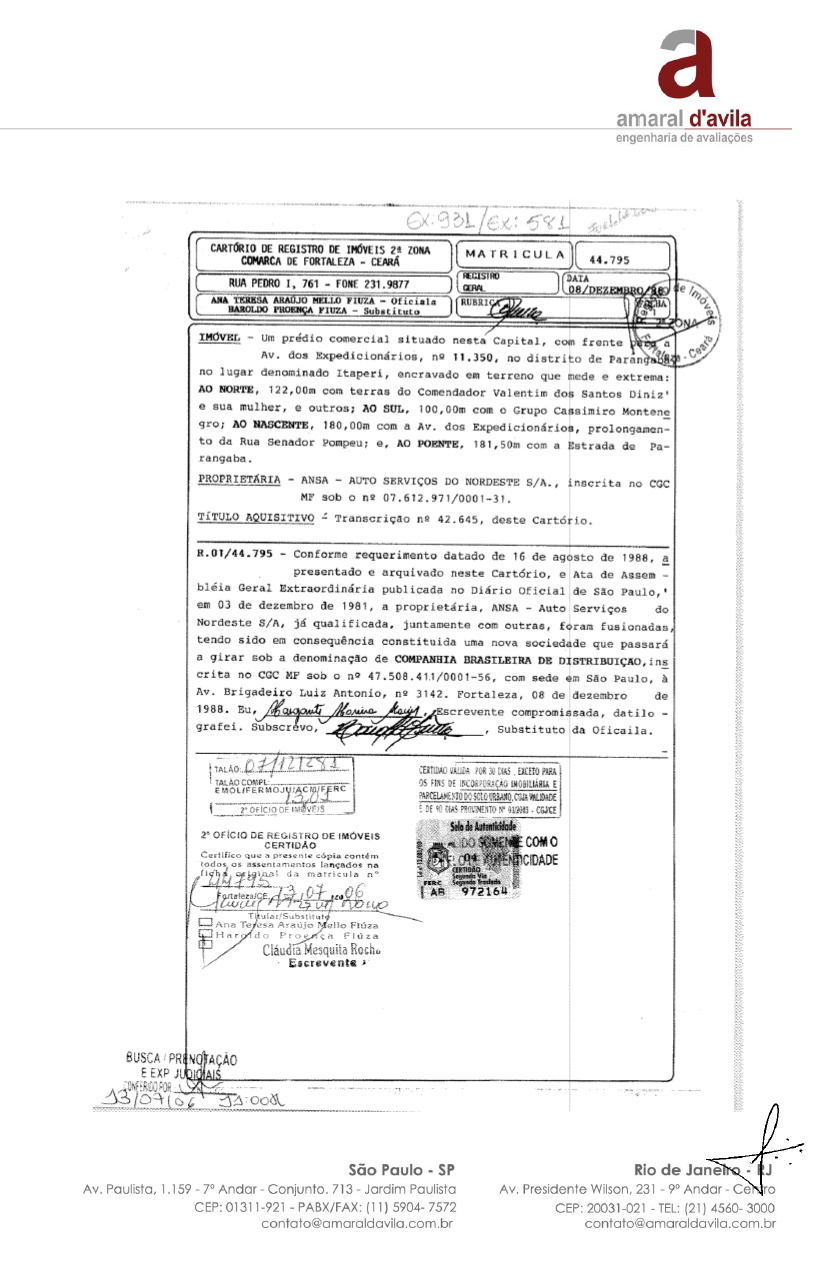

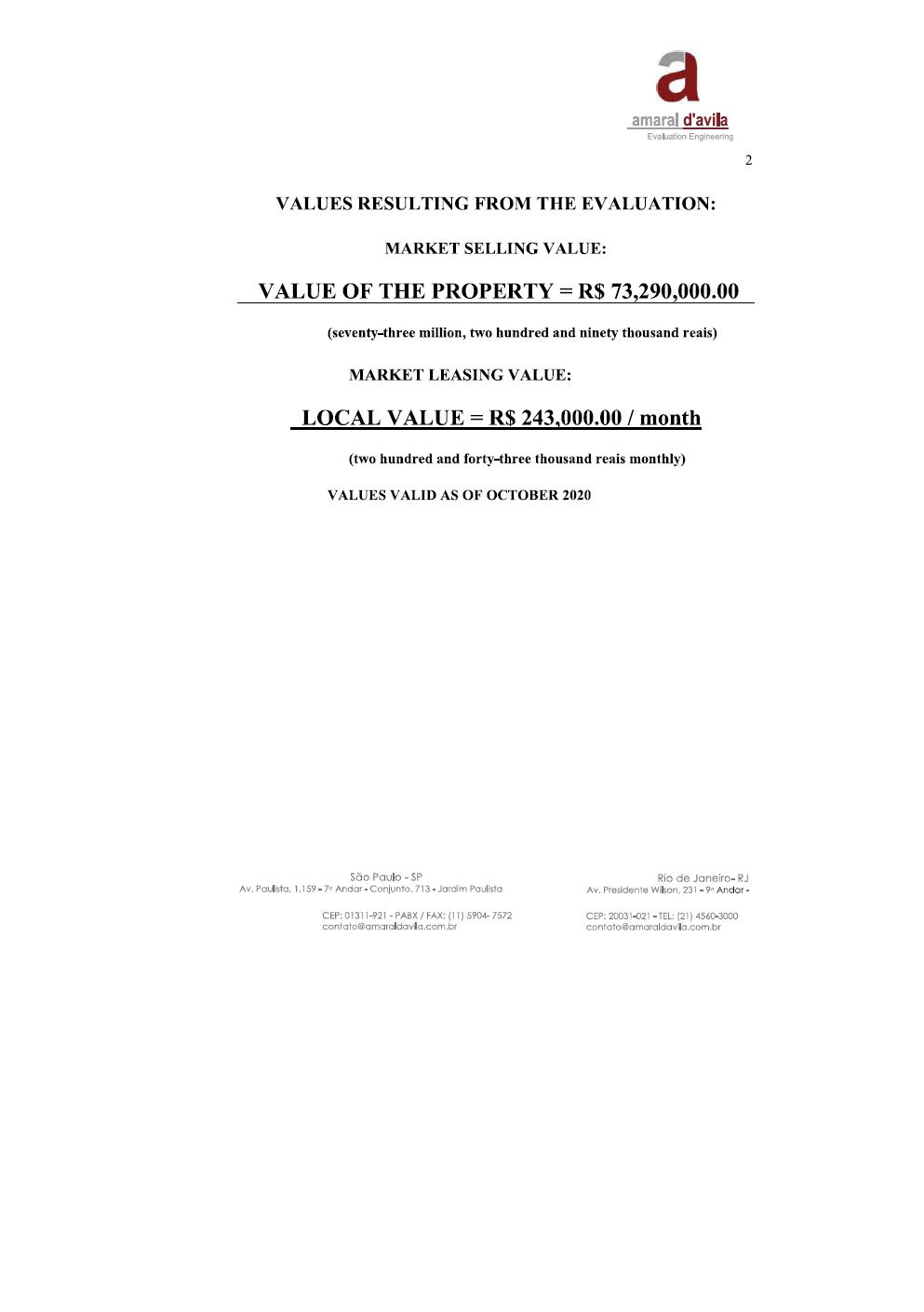

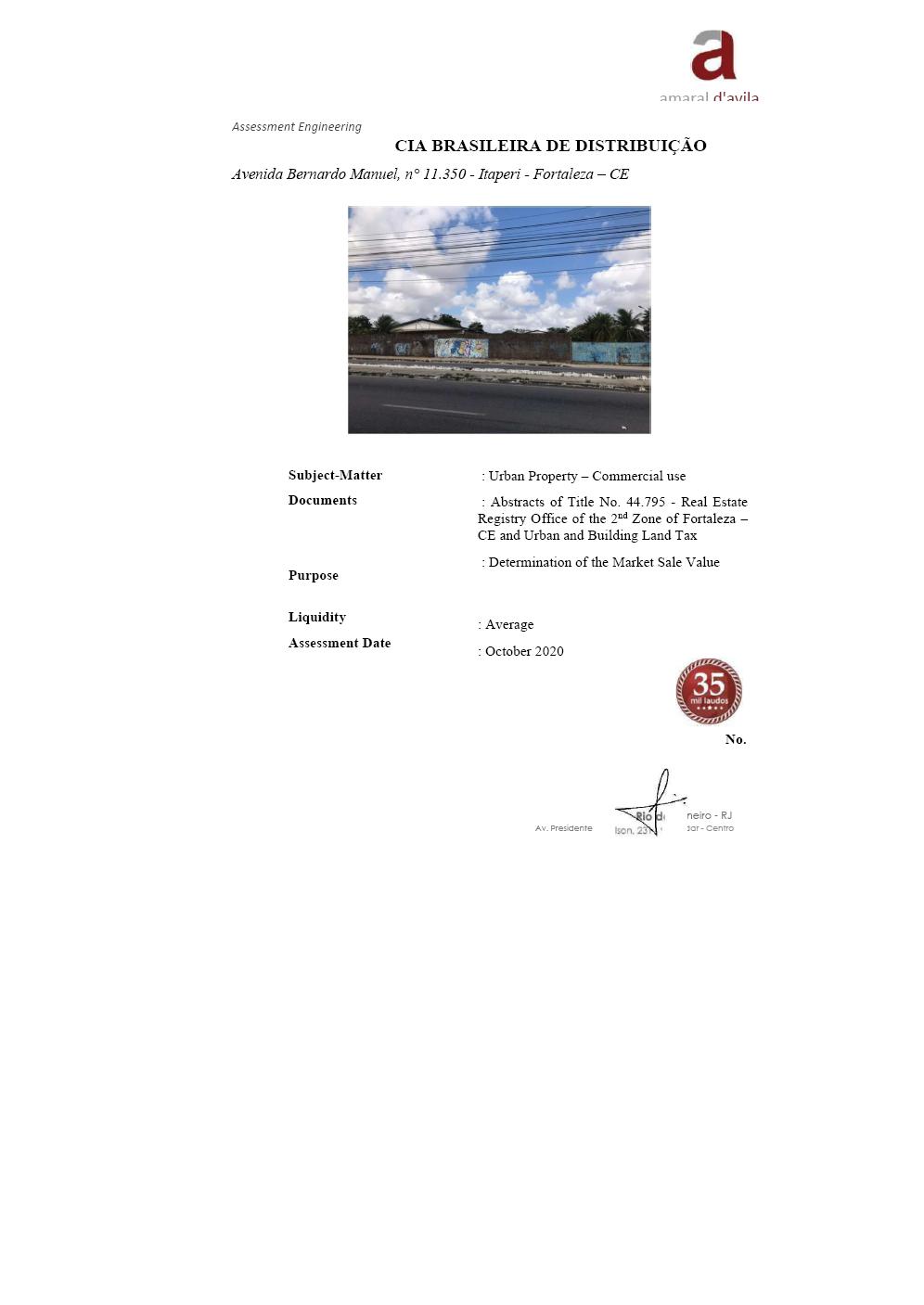

| Land Itaperi – Av. dos Expedicionários | 109.377,50 | 13.610.000,00 |

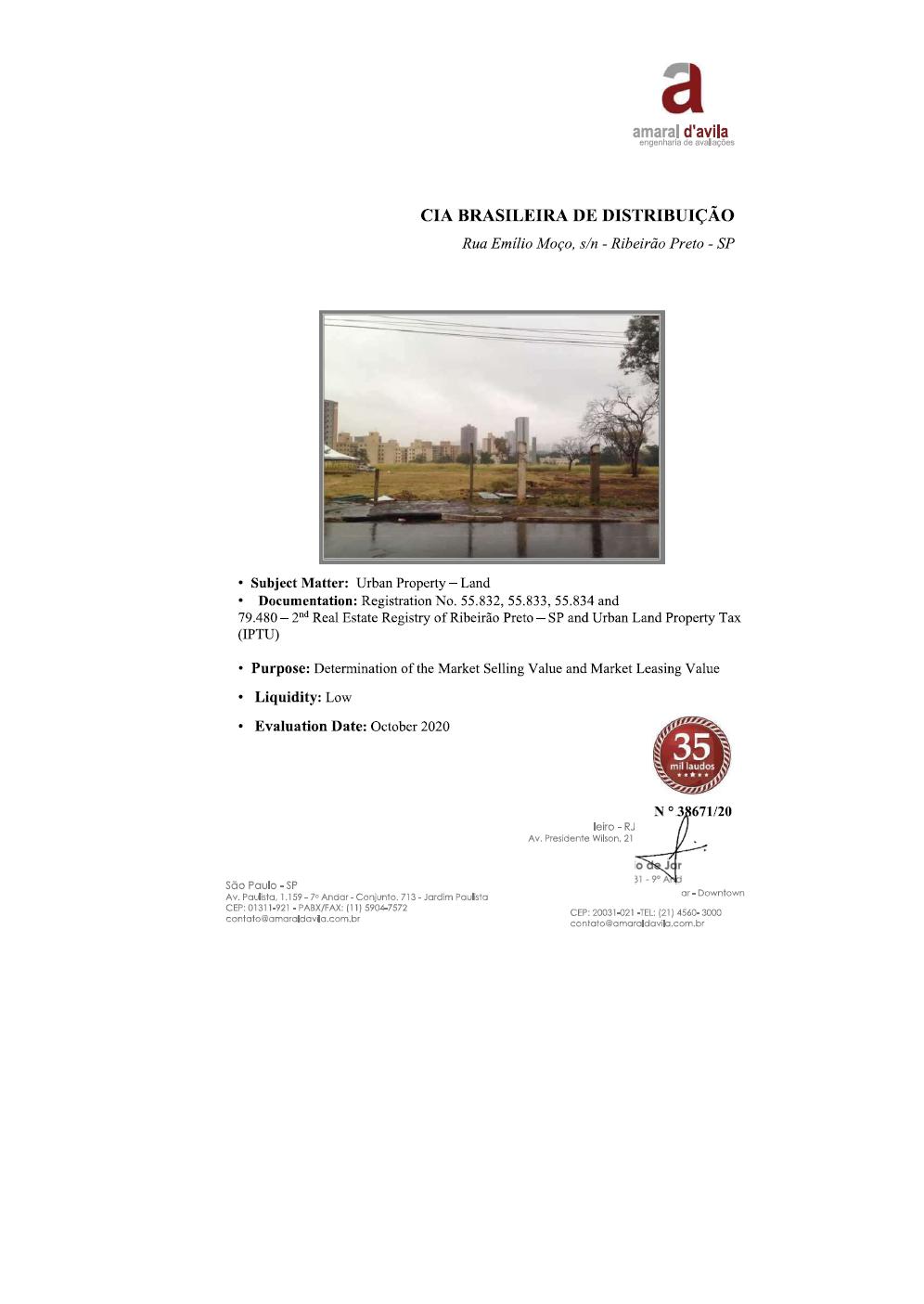

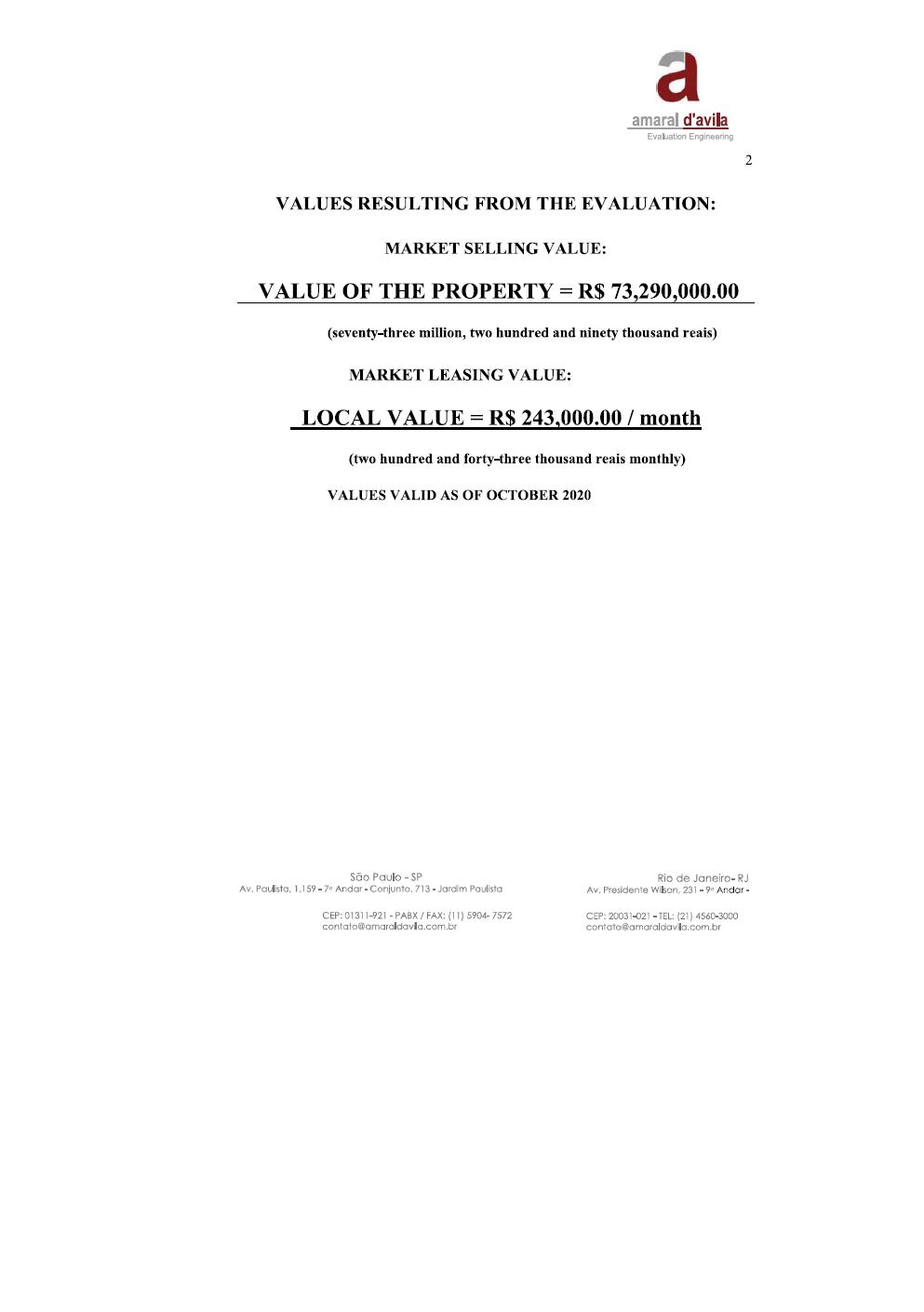

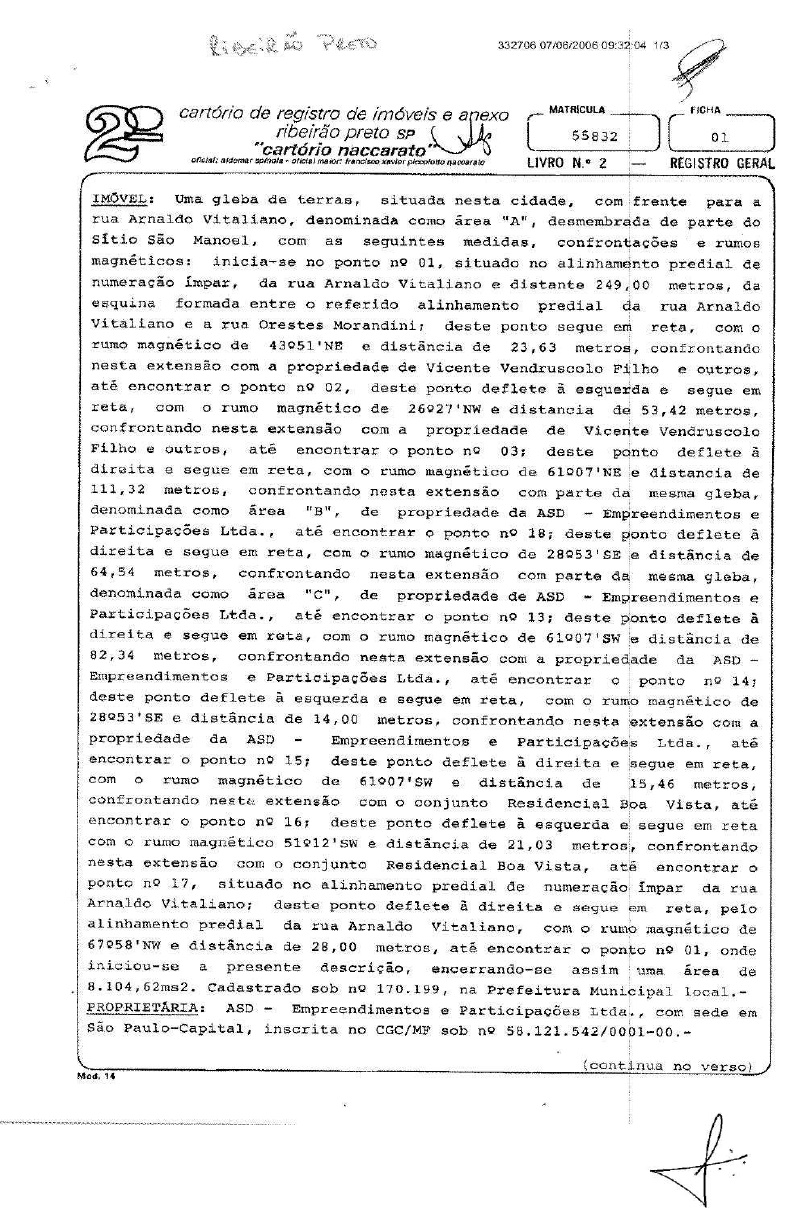

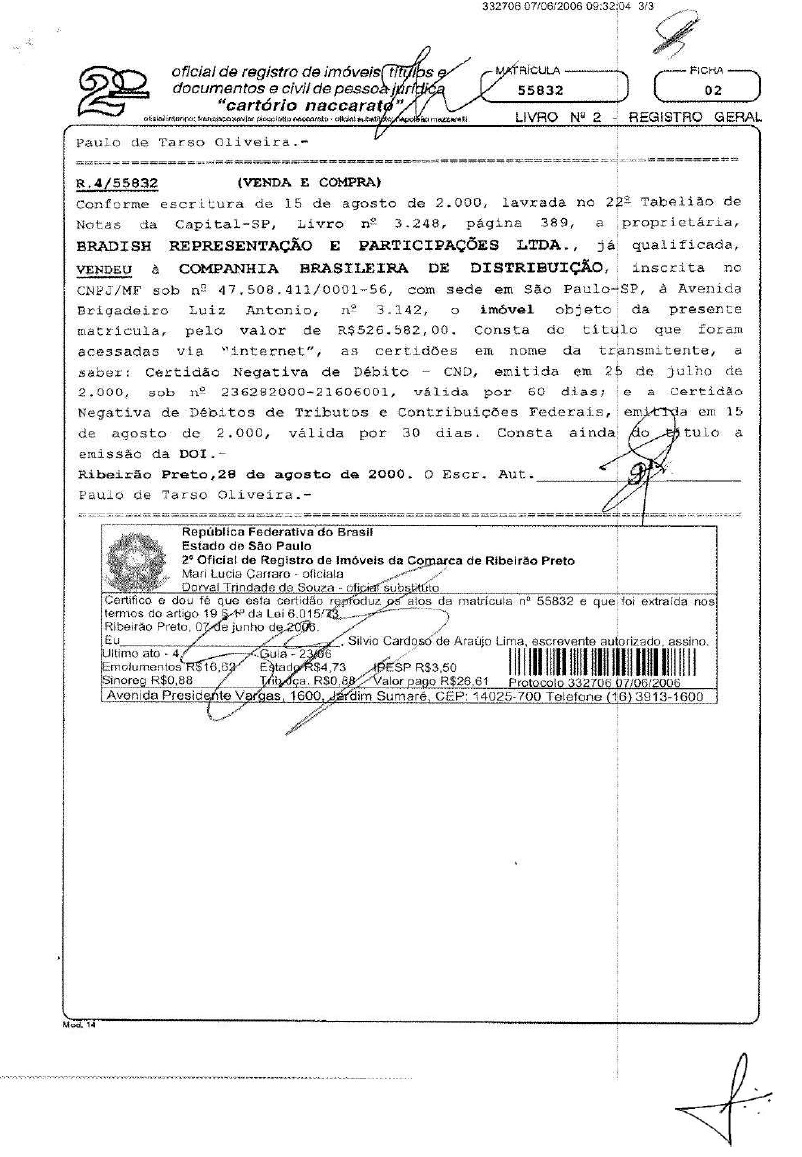

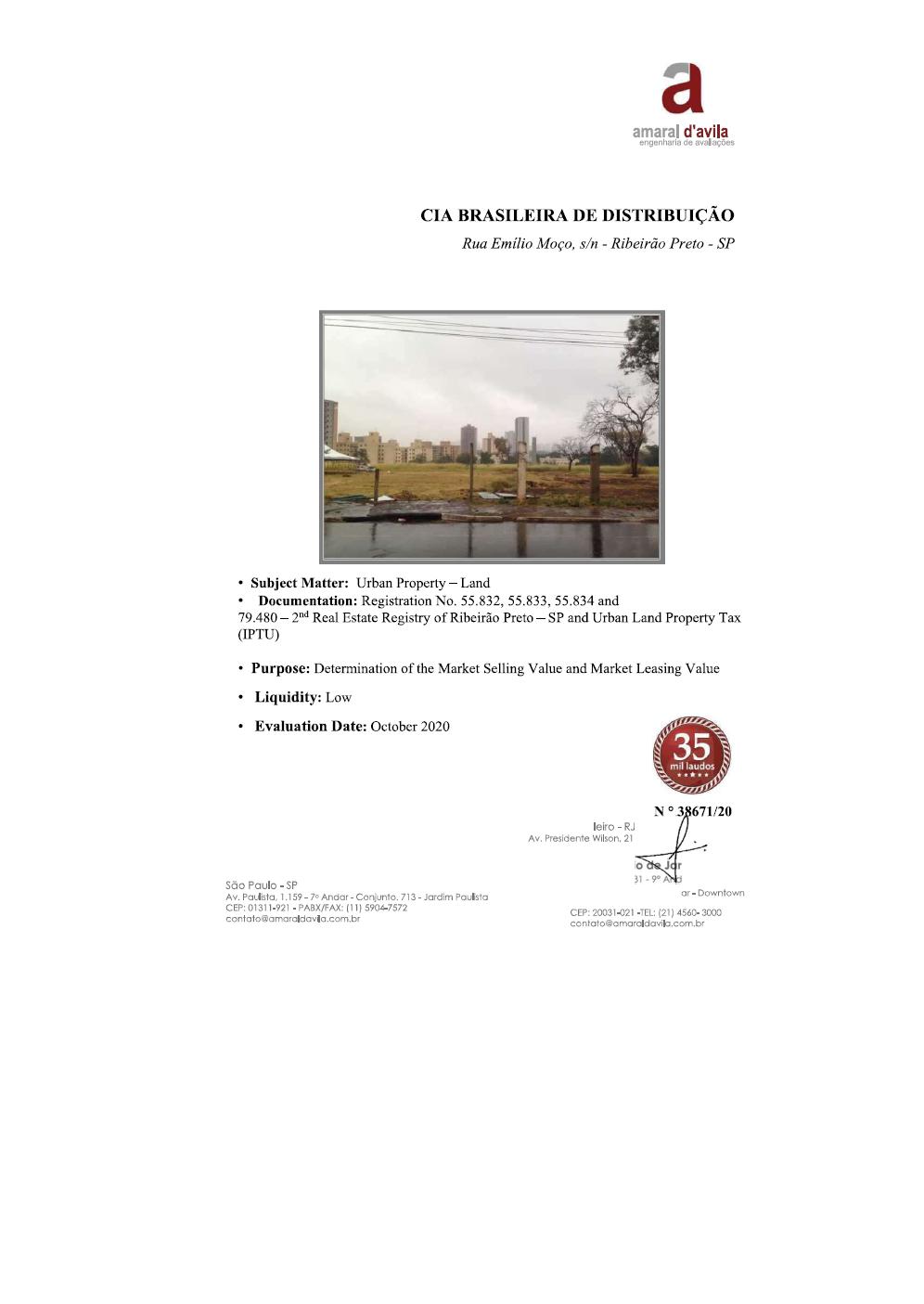

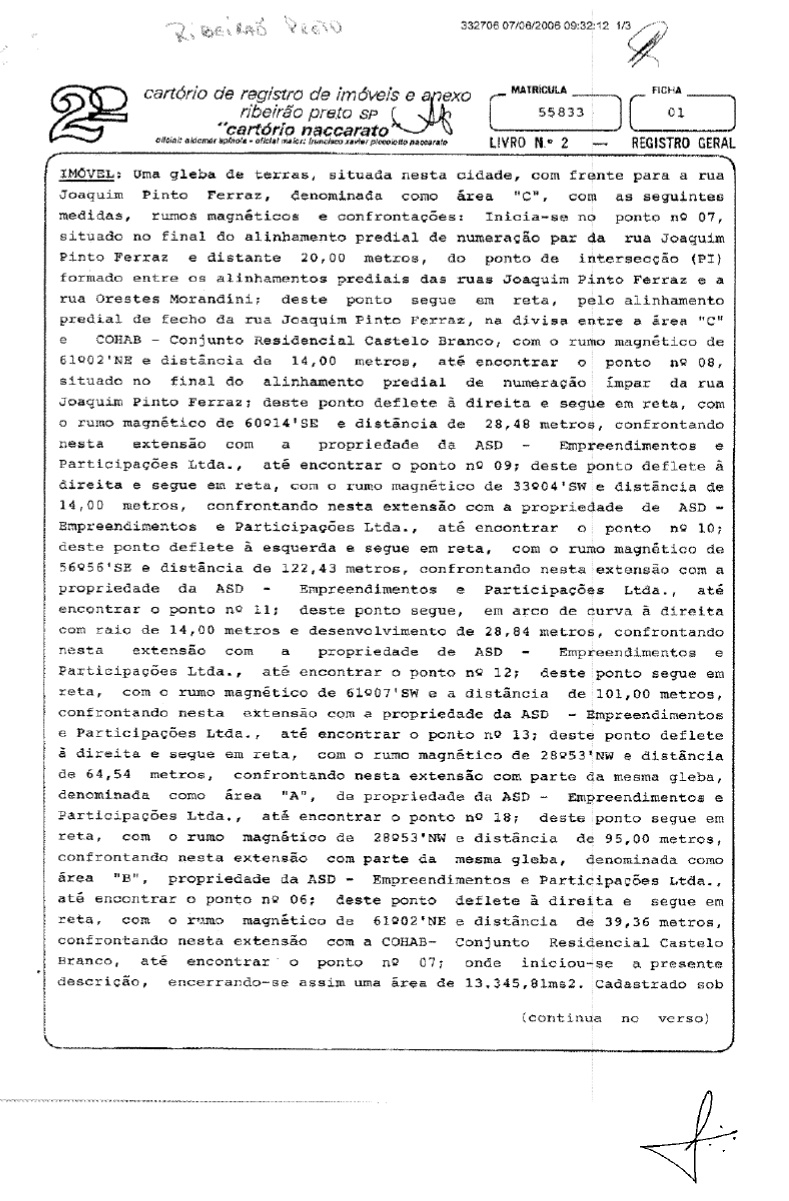

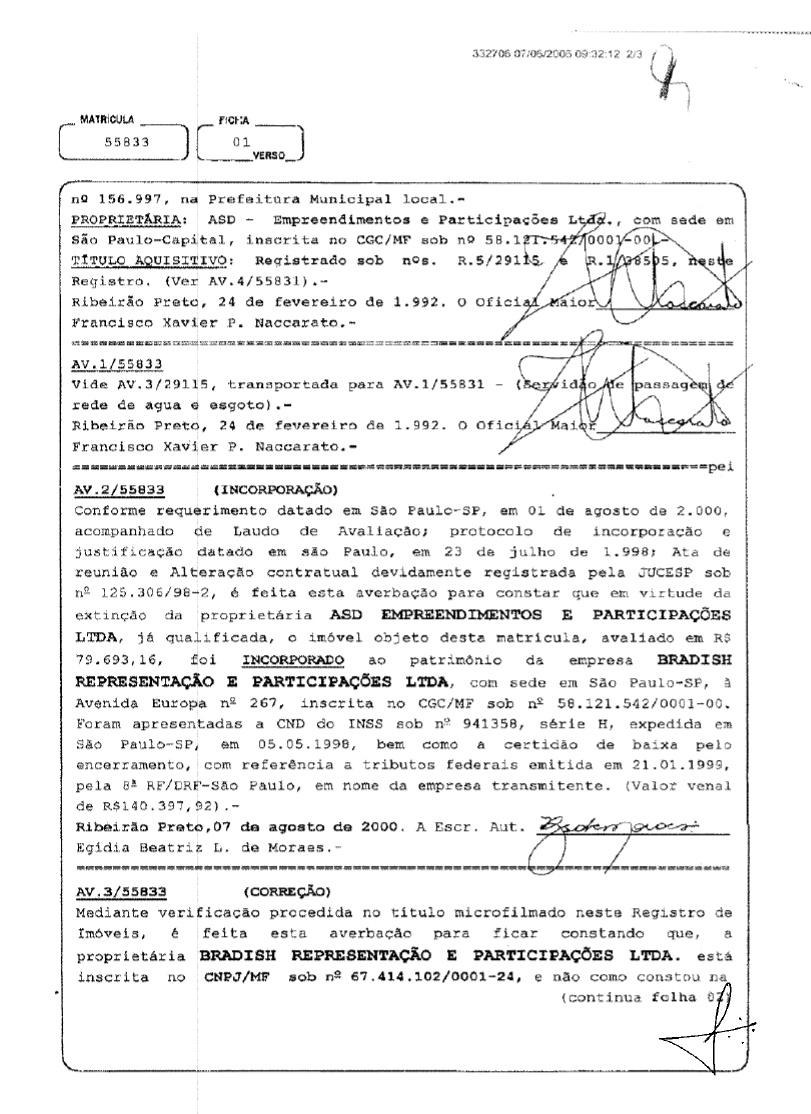

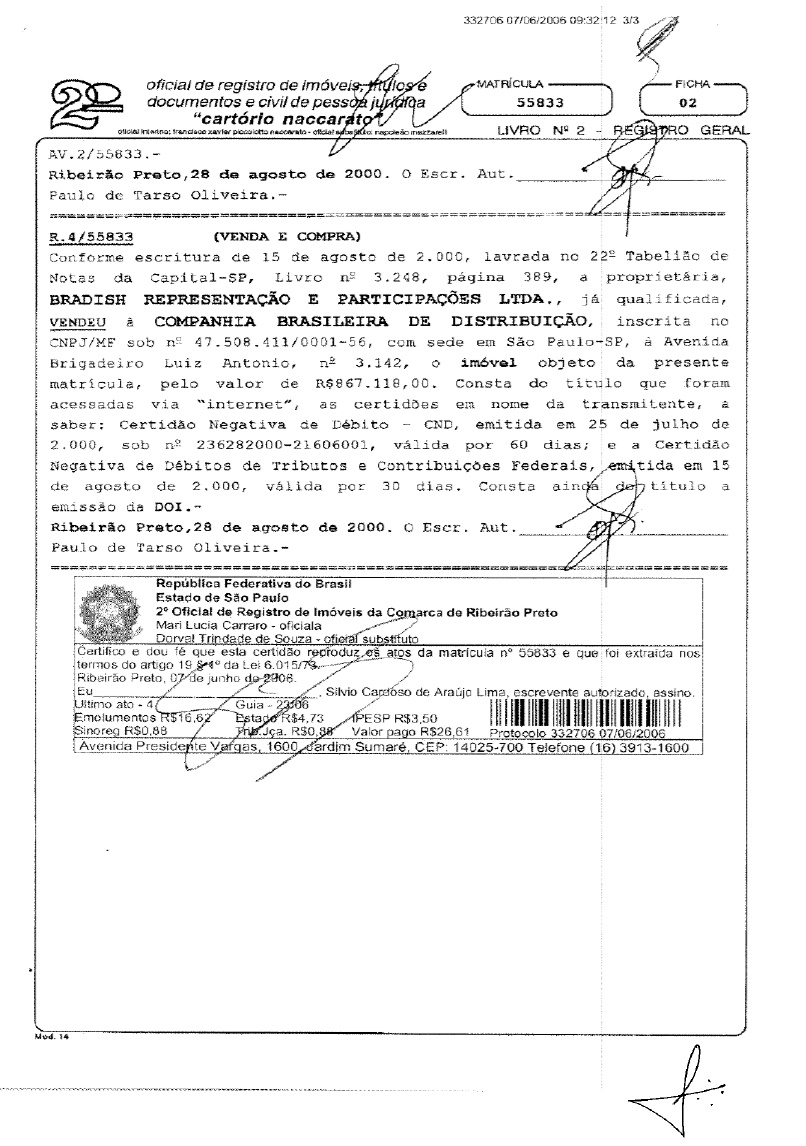

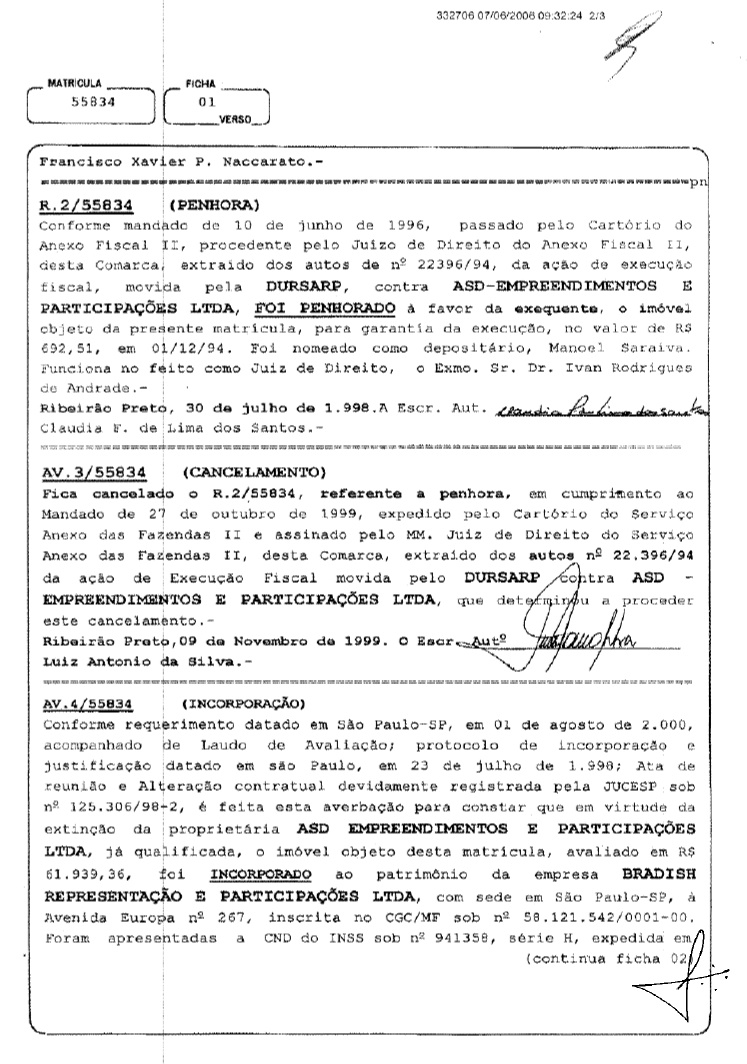

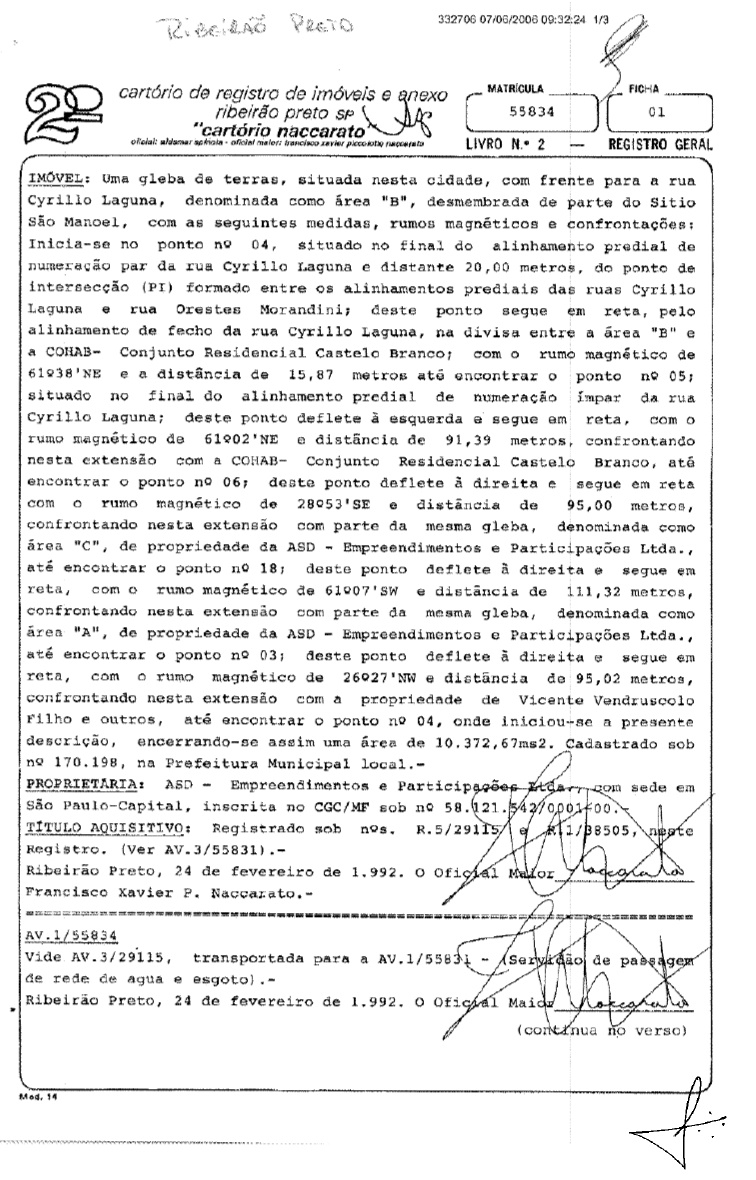

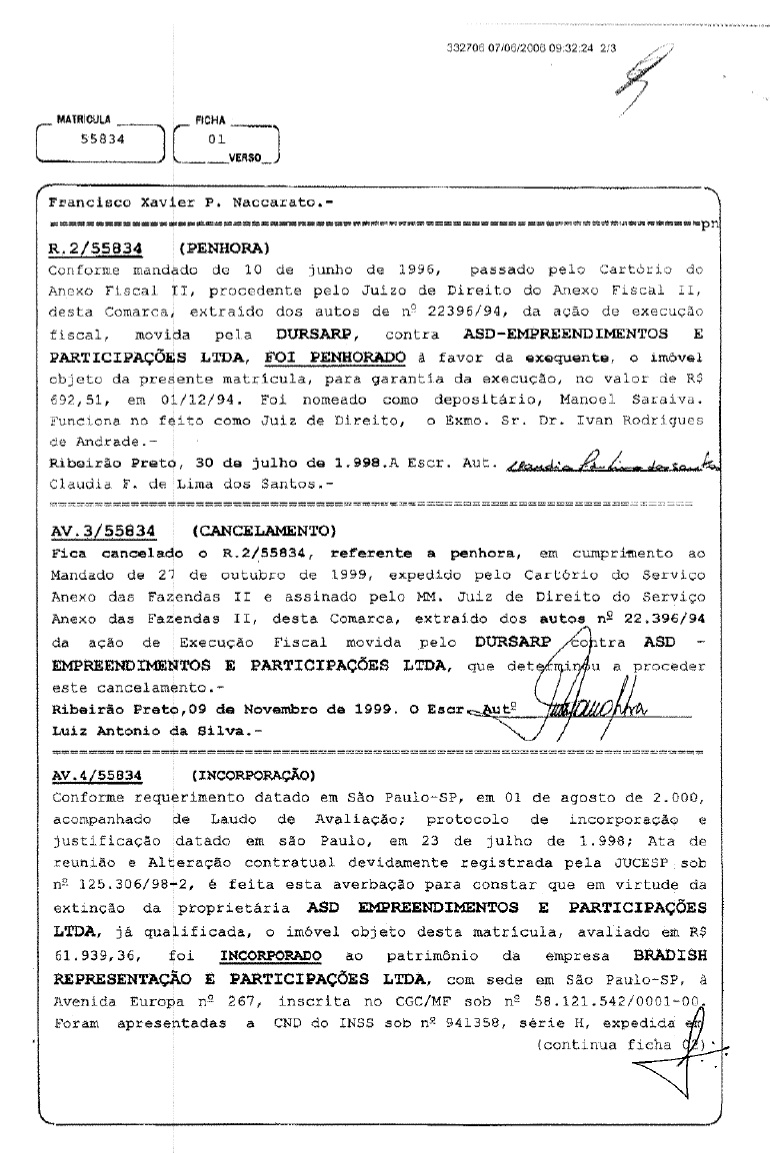

| Land Ribeirão Preto – Av. Castelo Branco | 7.000.000,00 | 73.290.000,00 |

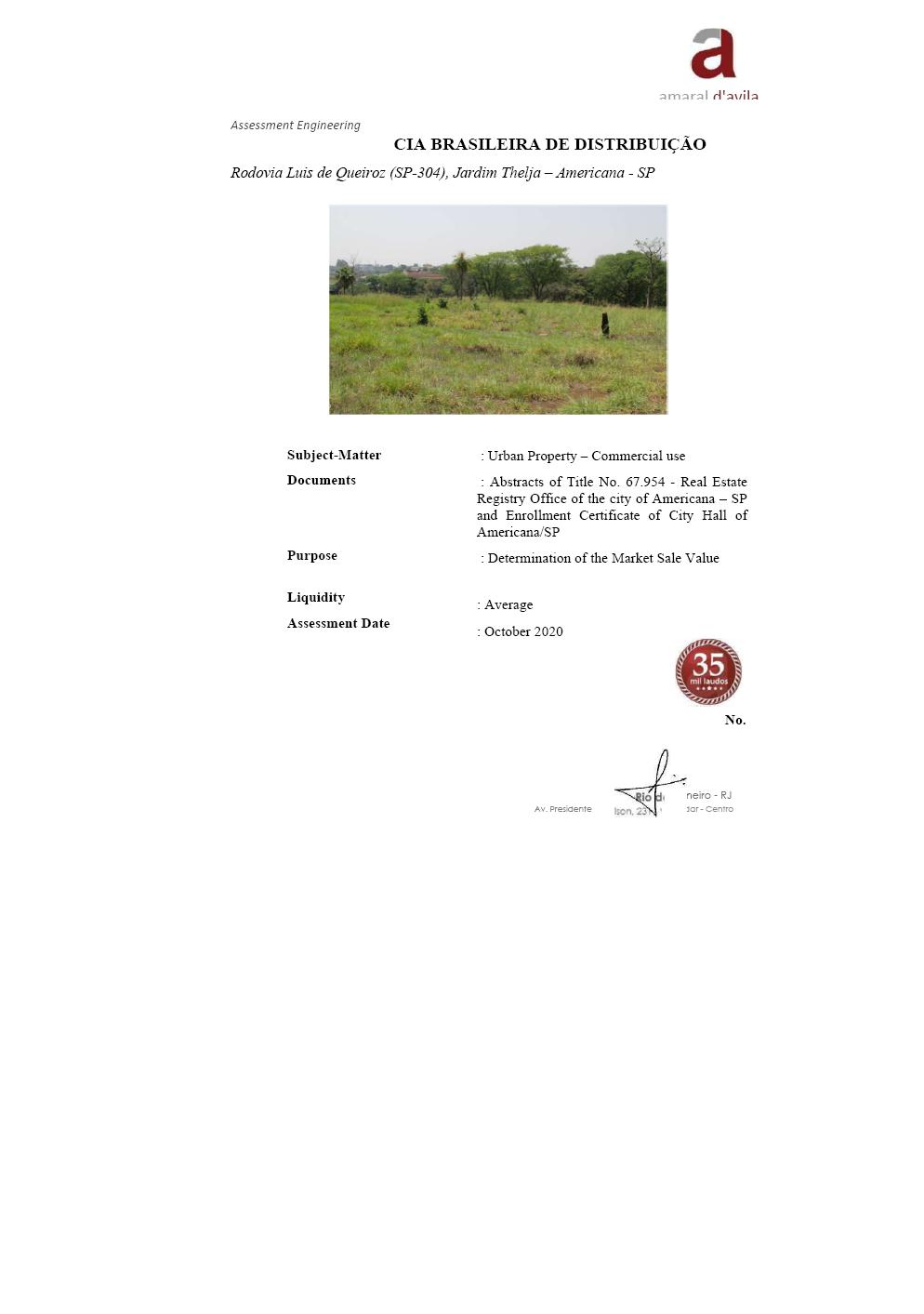

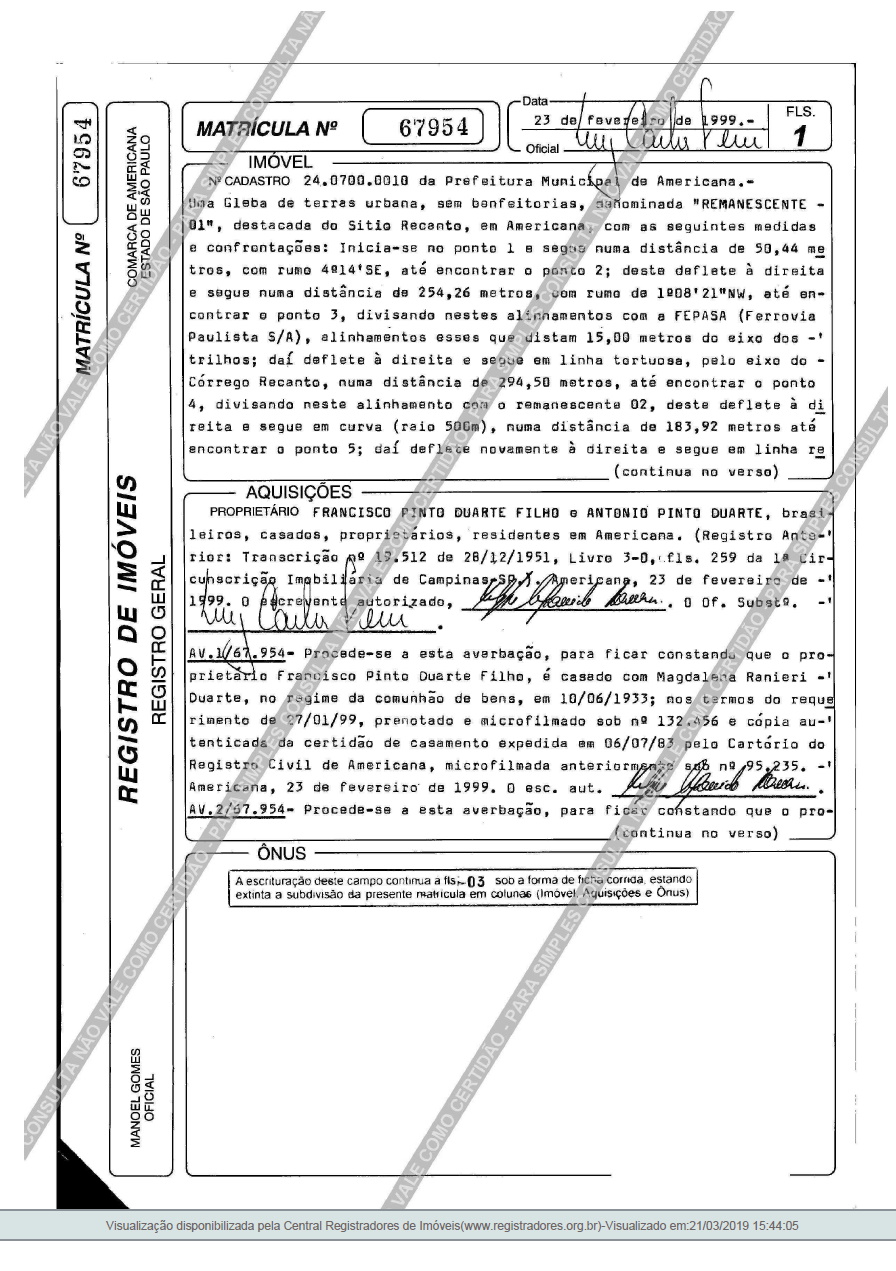

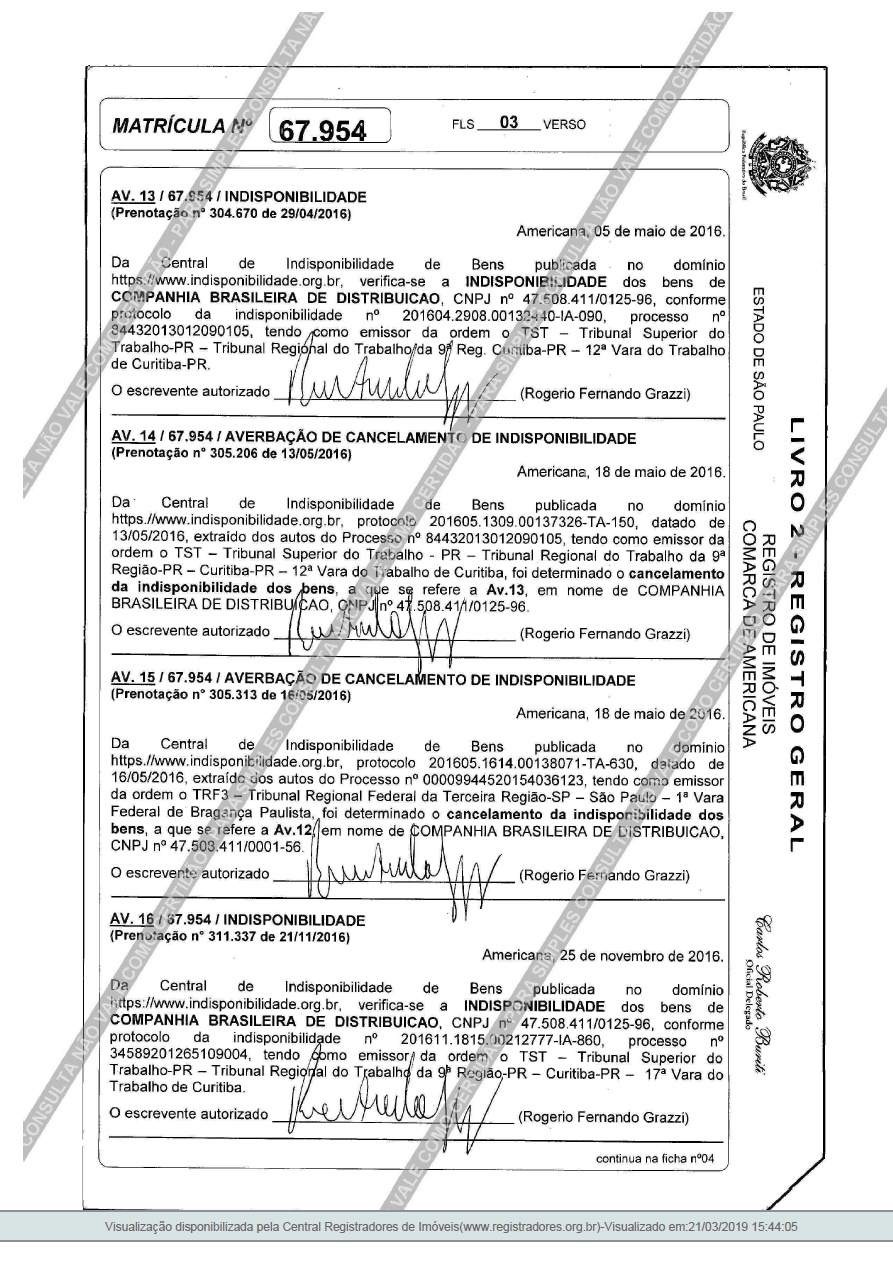

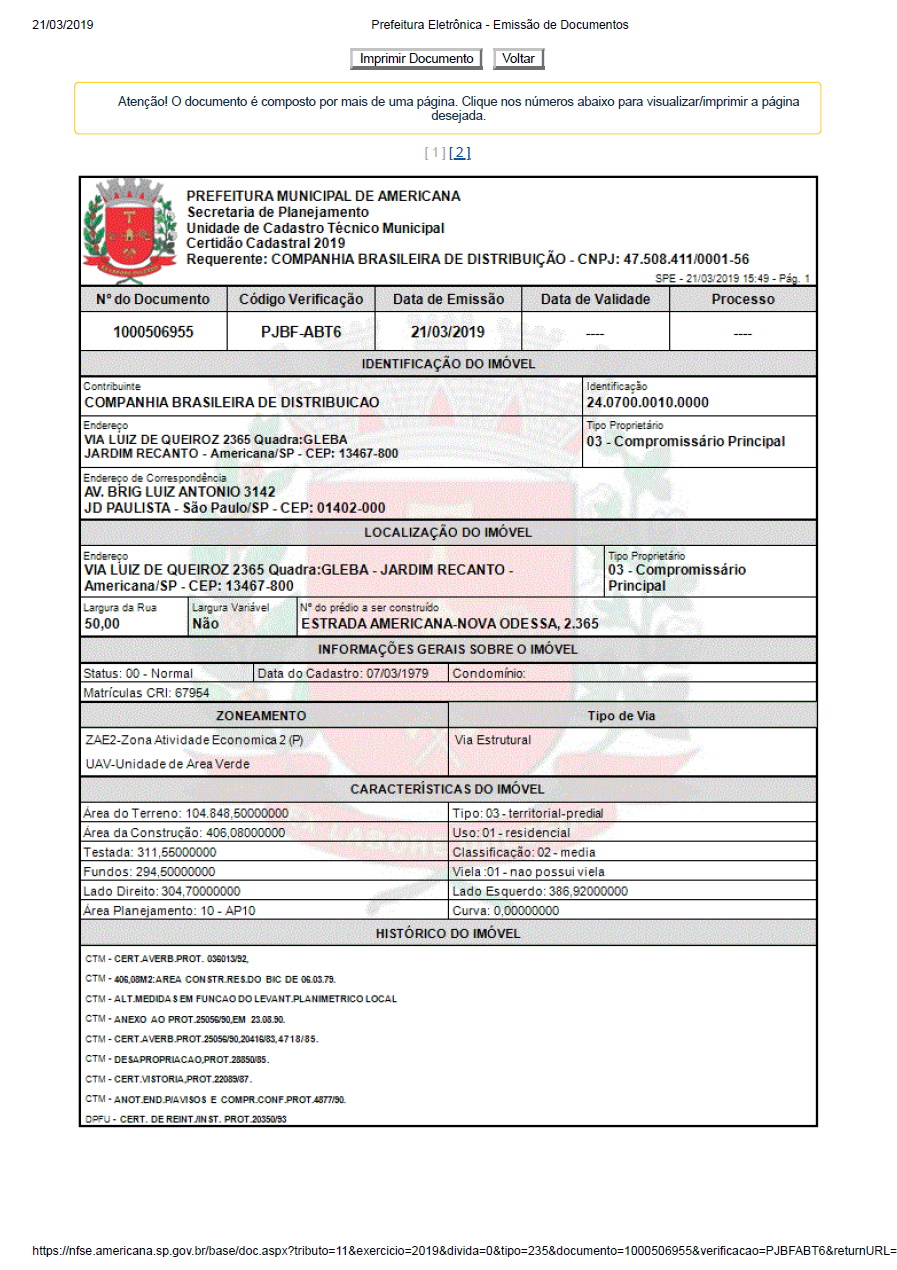

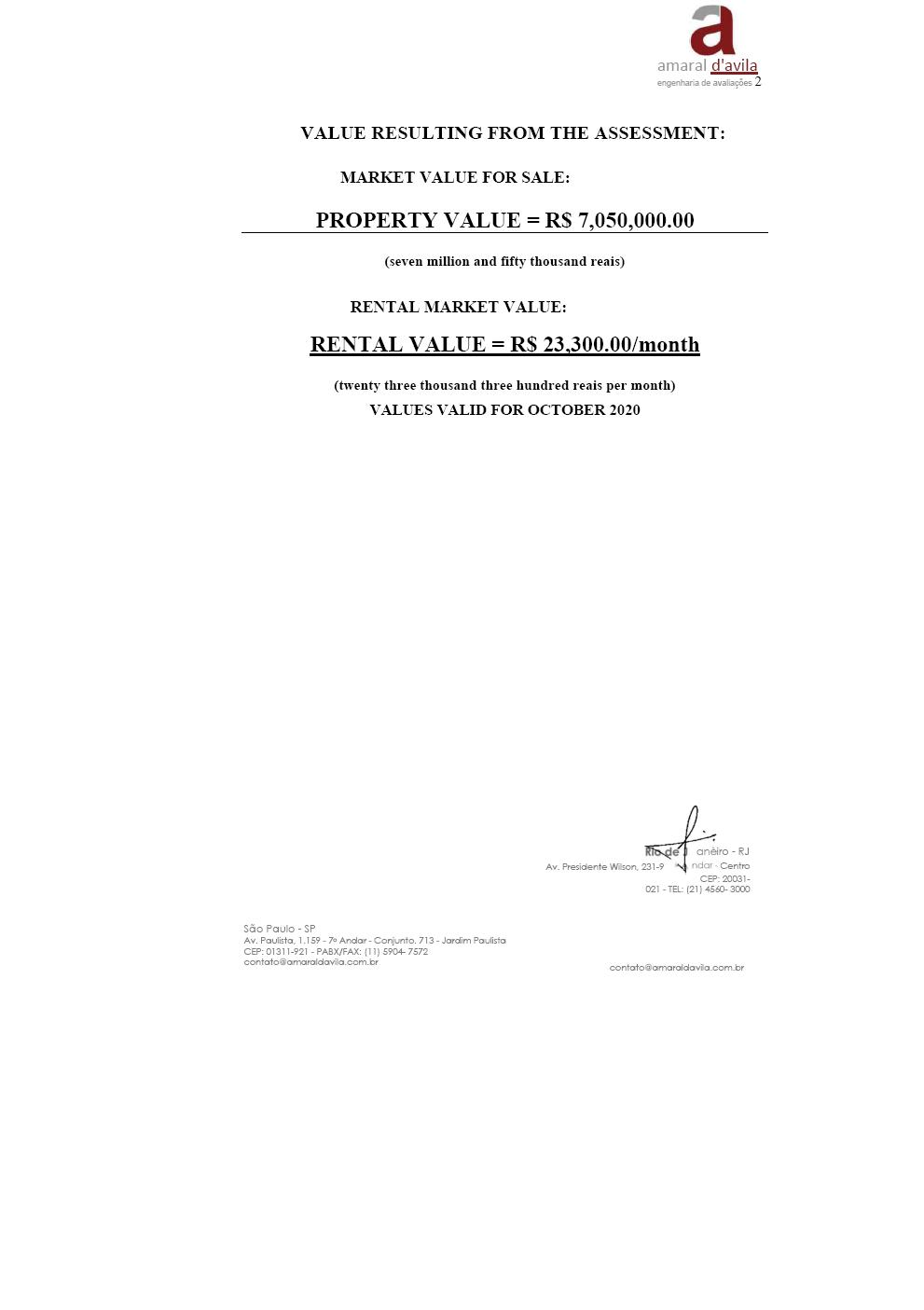

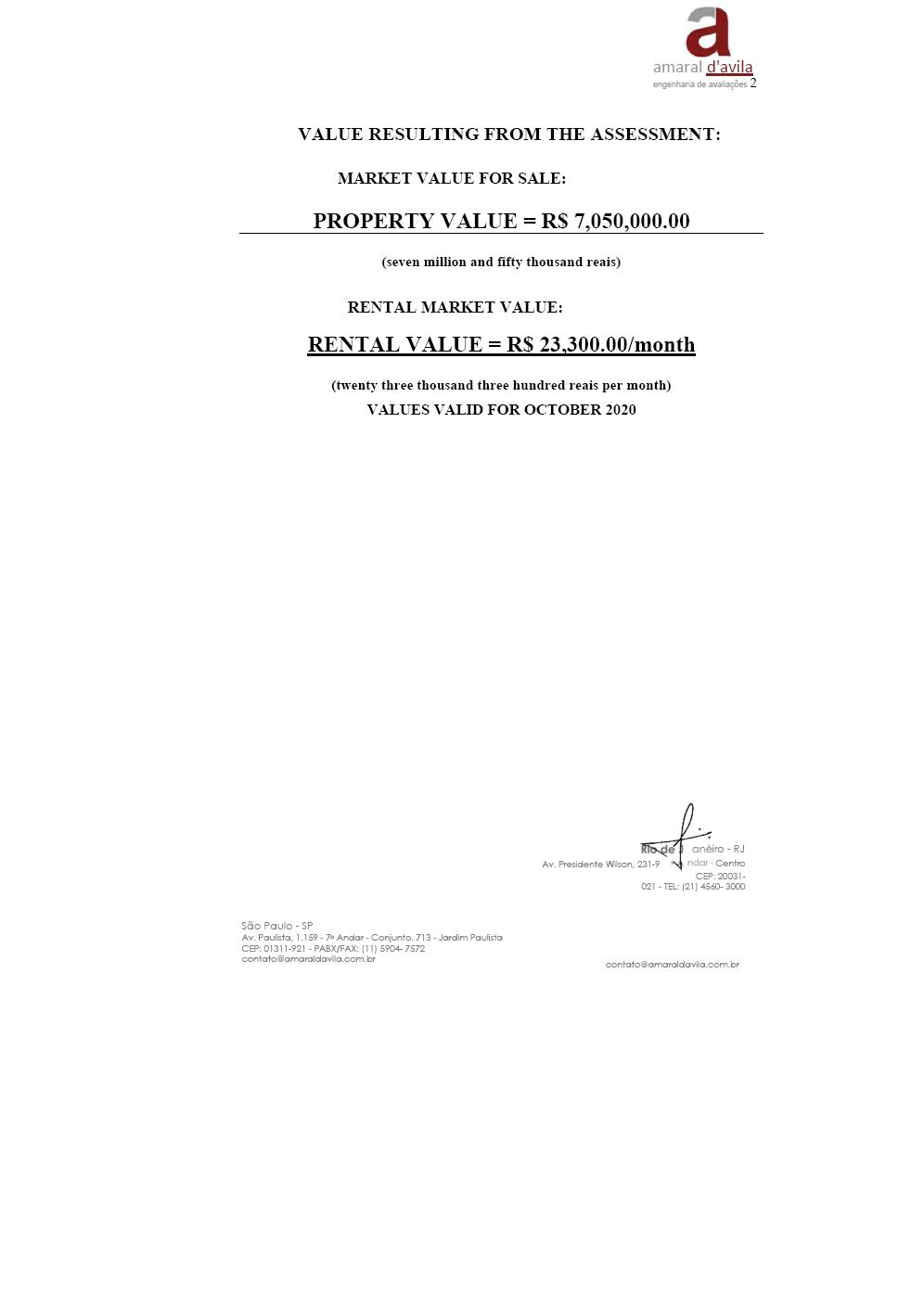

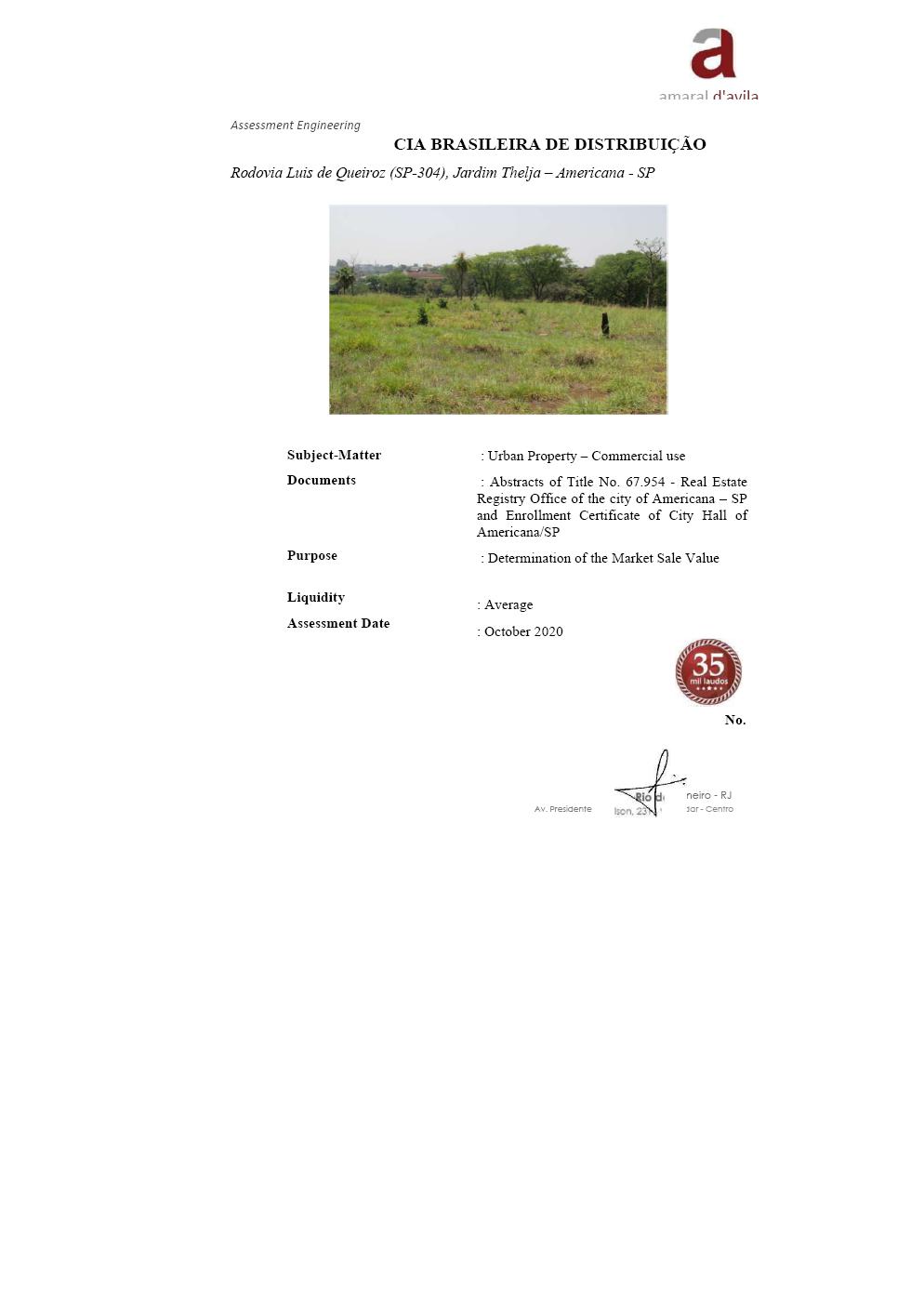

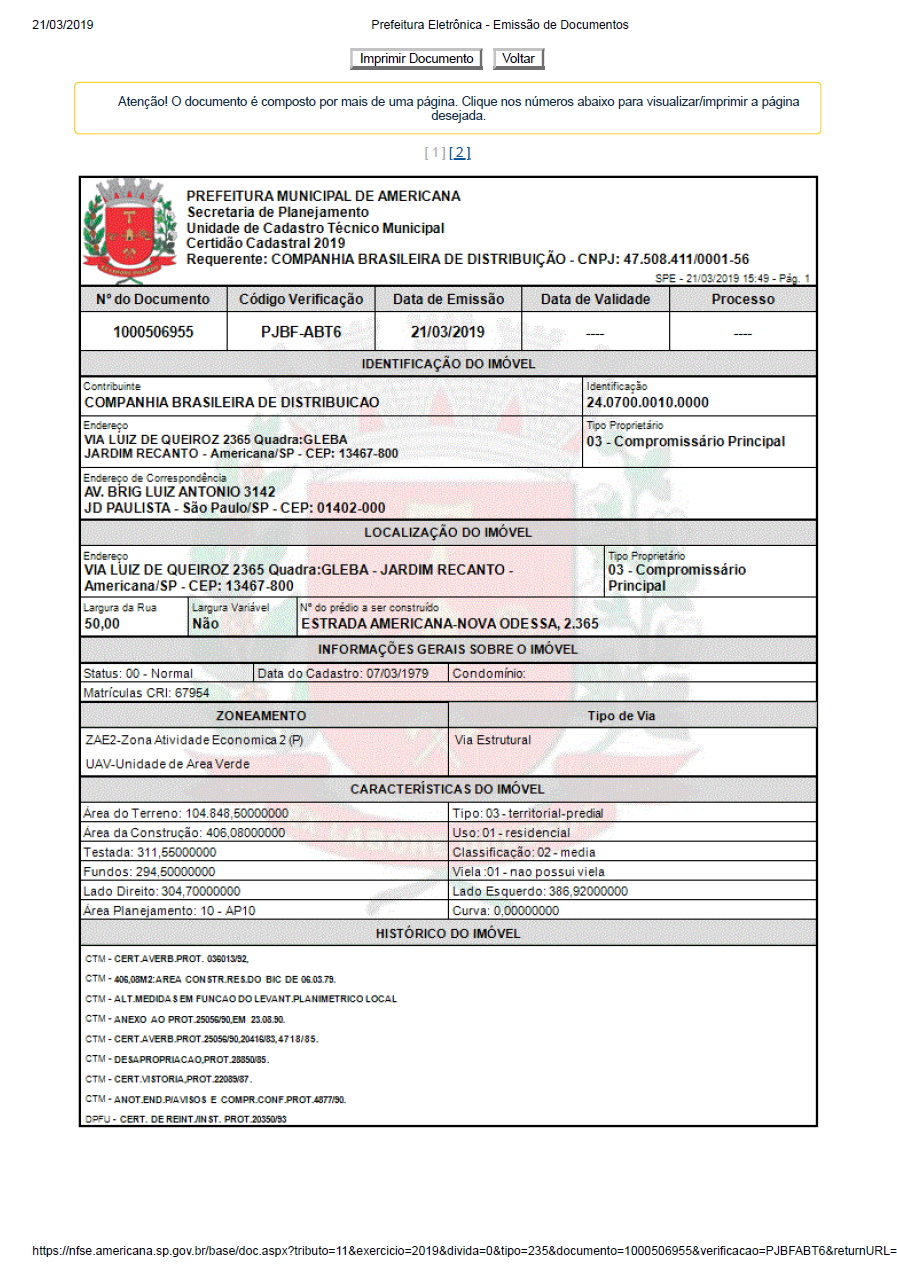

| Land Americana – Rod. Luiz de Queiroz | 1.947.211,61 | 36.590.000,00 |

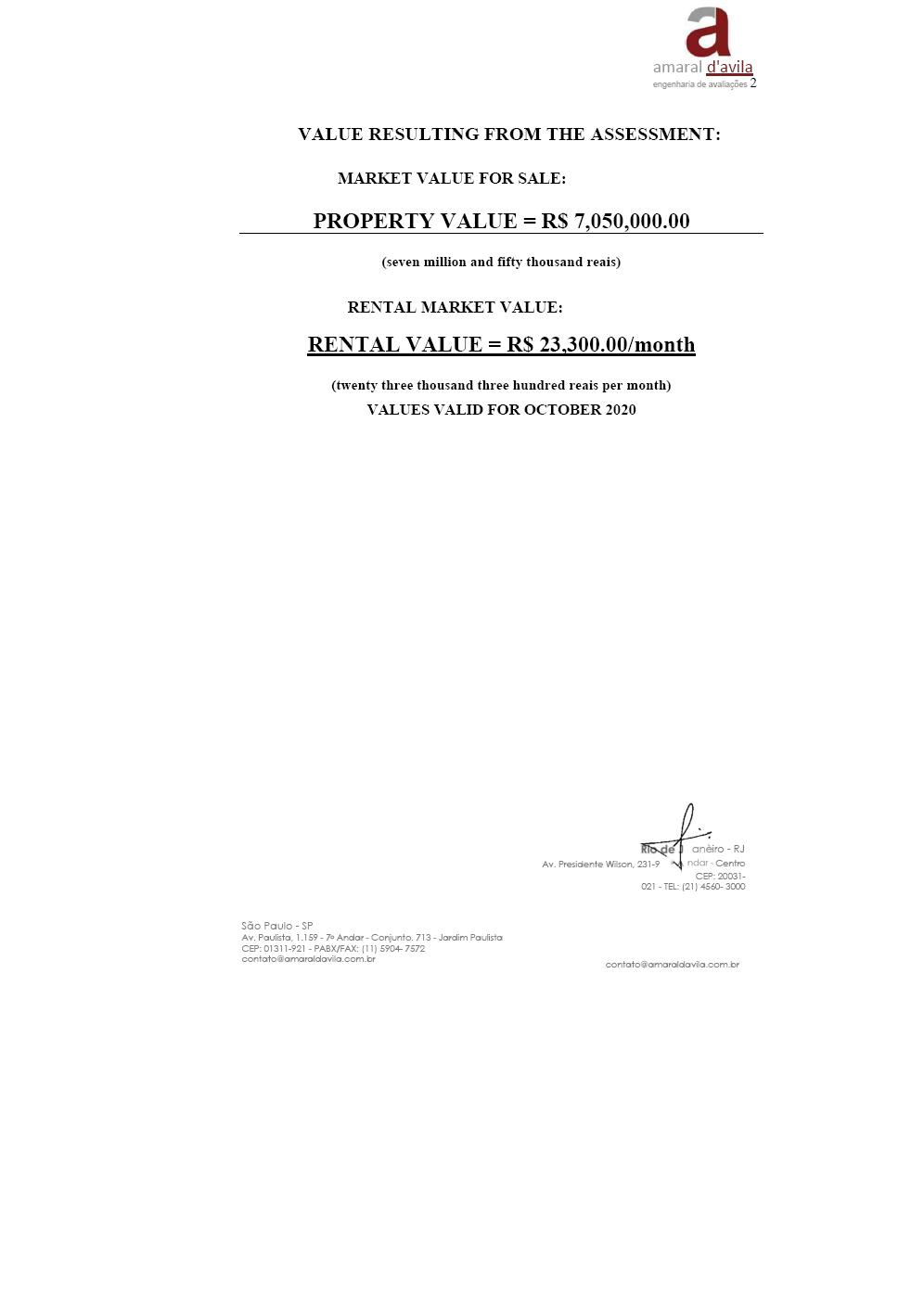

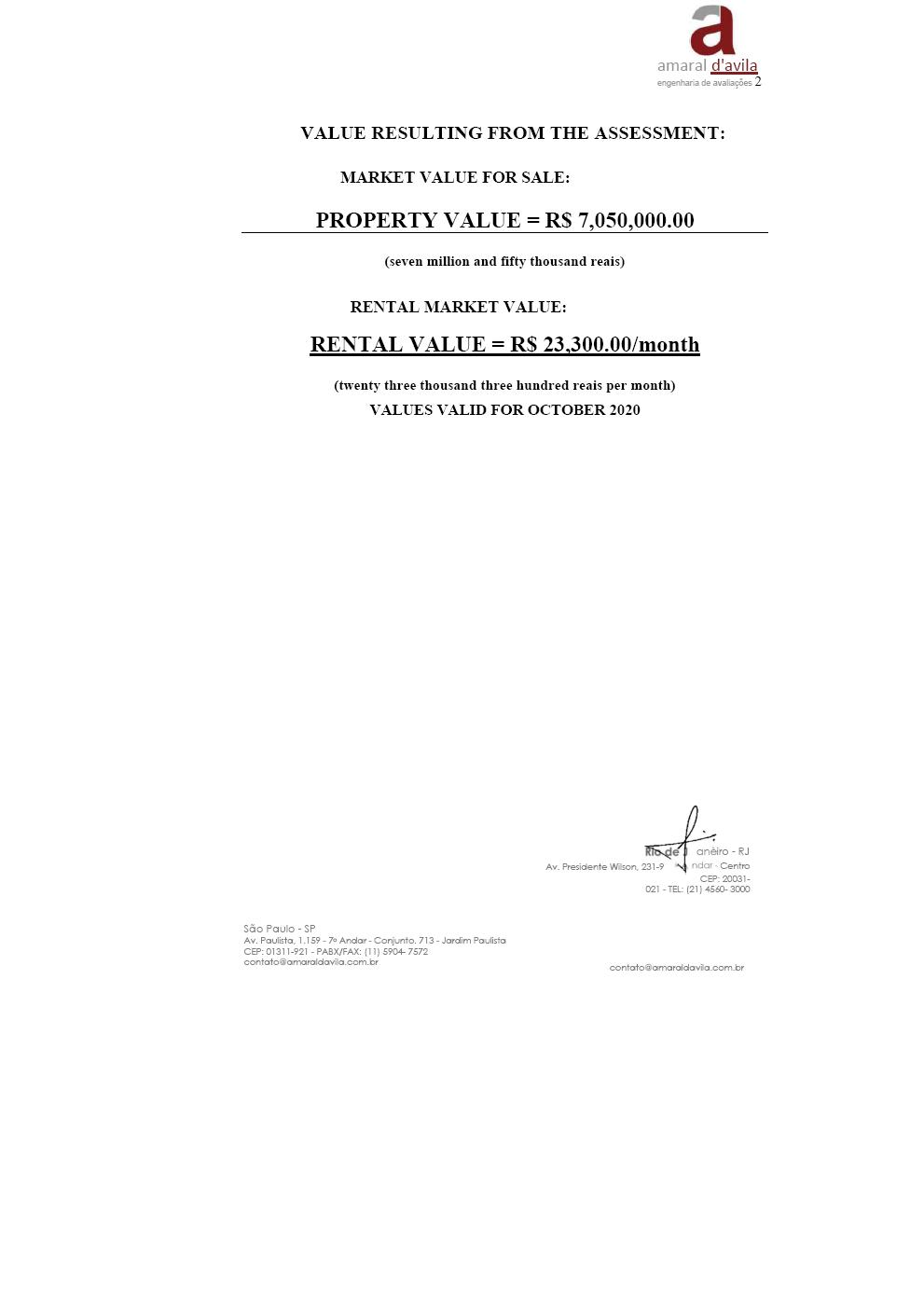

| Land Campo Grande | 2.450.000,00 | 7.050.000,00 |

| 213.351.906,62 | 914.658.145,29 |

| 16. | The shareholding interest held by CBD in Bellamar, stated at book value and market price, is described in EXHIBIT 3, including the respective book value. |

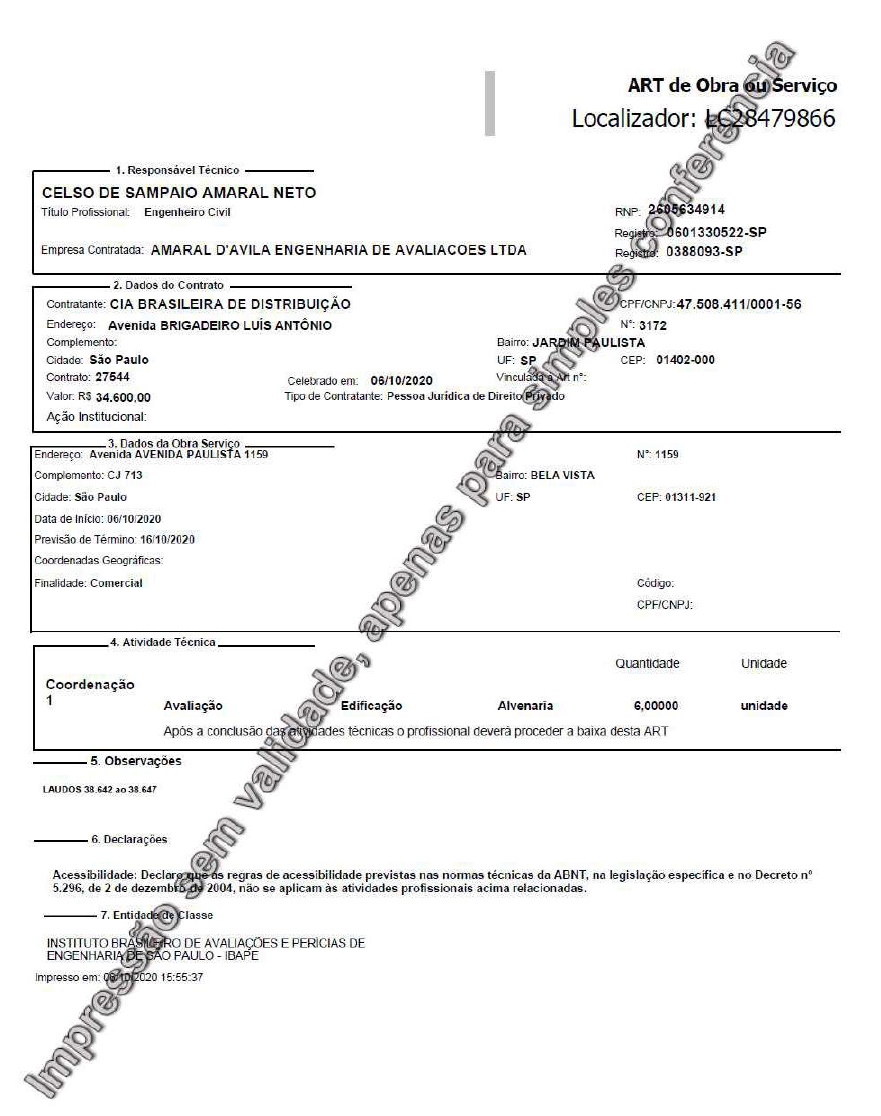

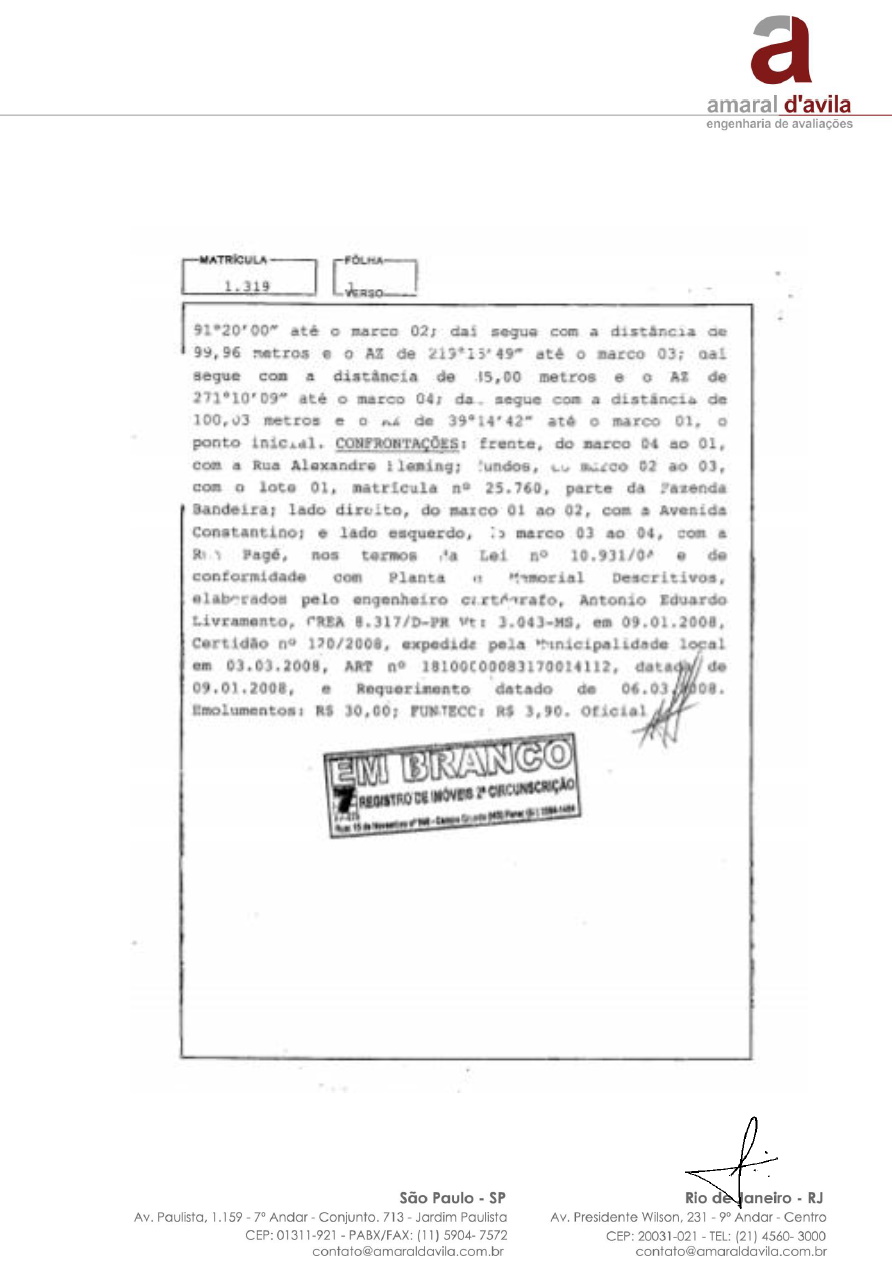

| 17. | The land exchanged is described in EXHIBIT 4, which includes the Appraisal Reports at Market Value of each land. |

| 18. | The exchange is performed and demonstrated at fair value. |

| 19. | Before the spin-off, in addition to the Exchange, CBD agreed to contribute with two capital increases in SENDAS, in December, in the total amount of six hundred and eighty-four million, six hundred and seventy-nine thousand, eight hundred and eighty-seven reais and nine cents (R$684.679.887,09), in order to increase the shareholding interest value. The capital increases are broken down as follows: |

Free translation |

| Current accounts asset balances between CBD and Sendas | 140.142.381,00 |

| CBD’s properties delivered to SENDAS (Tancredo Neves and Santo Amaro) | 44.537.506,09 |

| Cash capital contribution | 500.000.000,00 |

| 684.679.887,09 |

| 20. | The real estates received as capital payment are described in EXHIBIT 5. |

| 21. | In addition, SENDAS and CBD signed an agreement, whereby CBD will indemnify SENDAS in the event of materialization of the provisions for contingencies recorded in its activity liabilities that were transferred to CBD. As a result of this agreement, SENDAS provisioned an account receivable with CBD and the reversal of deferred tax on the liability provision, in the total amount of R$ 163.116.565,25. |

| 22. | The adjustments related to exchanges and capital increases are described in EXHIBIT 6. |

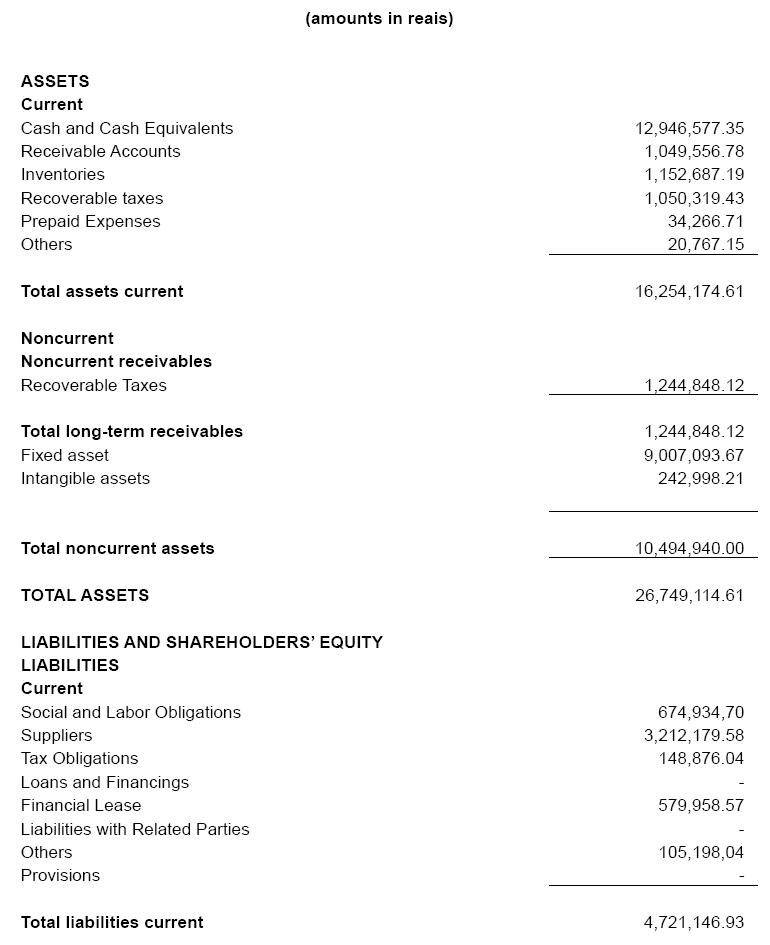

| 23. | The EXHIBIT 7 includes the balance sheet as at September 30, 2020, including the adjustments to the SENDAS’ financial position, after such adjustments, is broken down as follows: |

| ASSET | 26.236.338.069,30 |

| (-) LIABILITY | 15.840.973.187,47 |

| SHAREHOLDER’S EQUITY | 10.395.364.881,83 |

| 24. | SENDAS’ capital stock is divided into three billion, two hundred and sixty-nine million, nine hundred and ninety-two thousand and thirty-four (3.269.992.034) registered common shares, with no par value. SENDAS is the wholly-owned subsidiary of CBD, which holds SENDAS’ total shares. At SENDAS’ shareholders’ meeting, held on October 5, 2020 and rectified on November 10, 2020, the SENDAS’ common shares were grouped and, currently, the capital stock is represented by two hundred and sixty-eight million, three hundred and fifty-one thousand and five hundred and sixty-seven (268.351.567) registered common shares, with no par value. |

SENDAS’ SPIN-OFF

| 25. | The net asset to be spun off is represented by the assets and liabilities from the transactions in connection with the gas stations, in the amount of twenty million, ninety-nine thousand, nine hundred and eighty-three reais and sixteen cents (R$ 20.099.983,16), and the total remaining shares issued by Éxito and owned by SENDAS, in the amount of nine billion, one hundred forty-nine million, three hundred and one thousand, nine hundred and thirty-five reais and twenty-five cents (R$ 9.159.301.935,29), totaling nine billion, one |

Free translation |

hundred and seventy-nine million, four hundred and one thousand, nine hundred and eighteen reais and forty-five cents (R$ 9.179.401.918,45), to be merged into CBD.

| 26. | The financial position, after the spin-off, is described in EXHIBIT 8, broken down as follows: |

| ASSET | 17.050.287.019,40 |

| (-) LIABILITY | 15.834.324.056,02 |

| SHAREHOLDER’S EQUITY | 1.215.962.963,38 |

| 27. | By virtue of the spin-off, SENDAS’ capital stock remains unchanged, as well as the number of common shares representing SENDAS’ capital stock. |

CONCLUSION

| 28 | Based on the tests, analyses and inspections, the balance of SENDAS’ net asset, to be merged into CBD, amounts to at least R$ 9,179,401,918.45 (nine billion, one hundred and seventy-nine million, four hundred and one thousand, nine hundred and eighteen reais and forty-five cents). |

This appraisal report is issued in 7 (seven) copies and it contains 5 (five) sheets and 8 (eight) exhibits, printed in only one side and initialed by the expert who subscribes this report.

São Paulo, November 23, 2020

MAGALHÃES ANDRADE S/S Auditores Independentes CRC2SP000233/O-3 | GUY ALMEIDA ANDRADE Contador CRC1SP116758/O-6 |

Free translation |

| SENDAS DISTRIBUIDORA S.A. |

| EXHIBIT 1 |

| Balance sheet on September 30, 2020 |

Free translation |

| SENDAS DISTRIBUIDORA S.A. |

| Balance sheet on September 30, 2020 |

Free translation |

EXHIBIT 2 |

SENDAS DISTRIBUIDORA S.A.

Principal accounting practices adopted

in the preparation of the Balance Sheet on September 30, 2020

1. Basis of preparation

The individual financial statements have been prepared according to the Brazilian accounting practices, Law No. 6,404/76, particularly the technical pronouncements and interpretations issued by the Committee of Accounting Pronouncements - CPC, ratified by the Brazilian Securities Commission - CVM.

The financial statements have been prepared based on the historical cost, except for certain financial instruments measured at their fair values. All material information related to the financial statements, and only to them, is being evidenced and corresponds to that used by Management in its management of Sendas’s activities.

2. Foreign-currency transactions

Foreign-currency transactions are initially recognized at the market value of the corresponding currencies on the date in which the transaction qualifies for recognition. Monetary assets and liabilities denominated in foreign currencies are translated into Real, according to the quotation of the respective currencies at the closing of the fiscal years. Differences in the payment or translation of monetary items are recognized in the financial result.

3. Adjustment at present value of assets and liabilities

Long-term assets and liabilities are adjusted at their present value, taking into consideration the contractual cash flows and the respective interest rate, explicit or implicit. Short-term assets and liabilities are not adjusted at present value.

4. Classification of assets and liabilities as current and noncurrent

Assets (except for deferred income and social contribution taxes) with estimated realization or intended for sale or consumption within 12 months, as of the balance sheet dates, are classified as current assets. Liabilities (except for deferred income and social contribution taxes) with estimated settlement within 12 months, as of the balance sheet dates, are classified as current. All the other assets and liabilities (including deferred taxes) are classified as “noncurrent”. Deferred tax assets and liabilities are classified as “noncurrent”, net per legal entity, as set forth in the corresponding accounting pronouncement.

5. Conversion of subsidiaries and associates located in other countries

The financial statements are presented in reais, which is the functional currency. Every entity defines its functional currency and all of their financial transactions are measured in that currency. The financial statements of subsidiaries located in other countries that use a functional currency different from that of the parent company are translated into reais, on the balance sheet date, according to the following criterion:

Free translation |

Principal accounting practices adopted

in the preparation of the Balance Sheet on September 30, 2020

| • | Assets and liabilities, including goodwill and market value adjustments, are translated into reais at the exchange rate in effect on the balance sheet date. |

| • | Statement of income and cash flow statement are translated into reais using the average rate, except if there are significant variations, in this case it is used the rate in effect on the date of the transaction. |

| • | Shareholders’ equity accounts are maintained at the historical balance in reais and the variation is recorded under the caption of equity adjustments as other comprehensive results. |

The differences of exchange variations are recognized directly in a separate item of the shareholders’ equity. When a foreign operation is sold, the accumulated value of exchange variation adjustment in the shareholders’ equity is recorded in the result for the year.

The effects of the conversion of the investment into a foreign operation are recognized in separate items of the shareholders’ equity and reclassified to the result for the year upon write-off of the investment.

| 6. | Accounting for shareholding interest at cost derived from corporate restructurings and carried out with related parties |

Sendas accounts for interest derived from corporate restructurings acquired from related parties with no economic essence. The difference between the balance of cost and the value acquired is recorded in the shareholders’ equity, when the transaction is made between companies under common control. The transactions do not qualify as business combination.

7. Adoption of principal accounting judgments, estimates and assumptions

The preparation of the individual and consolidated financial statements of Sendas requires judgments and estimates and adoption of assumptions affecting the amounts of income, expenses, assets and liabilities and the evidence of contingent liabilities in the analysis of the financial statements, however, the uncertainties relating to these assumptions and estimates may produce results that require material adjustments at the book value of assets or liabilities in future years.

In the process of application of Sendas’s accounting policies, it was adopted judgments which had greater effect on values recognized in the individual financial statements regarding:

• Reduction at recoverable value - impairment;

• Inventories: Recognition of provisions for expected losses;

• Recoverable taxes: Expected realization of tax credits;

Fair value of derivatives and other financial Instruments: Measurement of the fair value of derivatives;

| • | Provision for lawsuits: Recognition of provision for lawsuits representing expected probable losses estimated on reasonable basis; |

Free translation |

Principal accounting practices adopted

in the preparation of the Balance Sheet on September 30, 2020

• Income tax: Recognition of provisions based on reasonable estimates;

| • | Stock-based payments: Estimate of the fair value of the operations based on evaluation model; |

| • | Business combination: Estimates of the fair value of assets and liabilities acquired in the business combination and resulting goodwill; and |

| • | Lease: Definition of the term of the lease agreement and incremental interest rate. |

8. Cash and Cash Equivalents

Comprise cash, bank accounts and short-term investments of high liquidity, immediately convertible into known values of cash and subject to immaterial risk of change of value, with intention and possibility of redemption in up to 90 days from the date of investment.

9. Accounts Receivable

The balances of accounts receivable are recorded initially at the transaction value, which corresponds to the sales value, and are subsequently measured according to the portfolio: (i) at fair value through other comprehensive results (VJORA), for receivables from credit card companies and (ii) at amortized cost, for the other portfolios.

For all the portfolios, estimated losses are taken into consideration and are recognized based on quantitative and qualitative analyses, history of actual losses in the past 24 months, credit rating and considering information on projections of assumptions related to macroeconomic events such as unemployment rate and consumer trust, as well as the volume of past-due credits from the accounts receivable portfolio. Sendas opted to measure provisions for accounts receivable losses for an amount equal to the credit loss expected for the entire life, applying the practical expedient of adopting a matrix of losses for each maturity range.

Provision for losses on financial assets measured at amortized cost is deducted from the gross book value of the assets.

For financial Instruments measured at VJORA, the provision for losses is recognized in ORA, instead of reducing the book value of the asset.

In every date of presentation, Sendas evaluates if the financial assets recorded at amortized cost or VJORA have indications of loss on recoverable value. A financial asset has indication of loss on reduction to recoverable value when there is one or more event with adverse impact on the estimated future cash flows of the financial asset.

The accounts receivable are considered uncollectible and, therefore, written off from the accounts receivable portfolio when the payment is not made after 360 days from the maturity date.

At every annual closing of the balance sheets, Sendas evaluates if the assets or groups of financial assets presented loss on recoverable value.

10. Inventories

Accounted for at cost or net realizable value, whichever is lower. Inventories acquired are recorded at average cost, including storage and handling costs, to the extent they are required

Free translation |

Principal accounting practices adopted

in the preparation of the Balance Sheet on September 30, 2020

to bring the inventories to their sale condition in the stores, less commercial agreements received from suppliers.

The net realizable value is the sale price in the normal course of business, less estimated costs to make the sale, such as: (i) taxes on sale; (ii) personnel expenses directly tied to sales; (iii) cost of goods; and (iv) other costs required to bring the goods to sale condition.

Inventories are reduced to their recoverable value through estimates of losses, breaks, scrapping, slow turnover of goods and estimate of loss for goods that will be sold with negative gross margin, which is periodically analyzed and evaluated for adequacy.

The commercial agreements received from suppliers are measured and recognized based on the contracts and agreements signed, and recorded in the result as the corresponding inventories are sold. They comprise agreements by purchase volume, logistic and specific deals for recovery of margin, reimbursement of expenses, among other, and are recorded as reduction of balances payable to the respective suppliers, when the Company contractually has the right to settle the liabilities with suppliers at the net values receivable under commercial agreements.

11. Recoverable Taxes

The Company records tax credits whenever it has legal, documental and factual opinion on these credits that allow their recognition, including estimate of realization, where the ICMS is recognized as reduction of “cost of goods sold” and the PIS and COFINS as reduction of result accounts on which the credits are calculated.

The realization of these taxes is made based on growth projections, operating issues and generation of debits for use of these credits by the companies of the Group.

12. Investments in controlled companies and associates

12.1. Interest in controlled companies, subsidiaries and associates

The determination of which subsidiaries are controlled by the Company and the procedures for full consolidation follow the concepts and principles established by CPC 36 (R3).

The financial statements of the subsidiaries are prepared on the same date of analysis of the financial statements of the Company, adopting consistent accounting policies.

In the individual financial statements, interest is calculated considering the percentage held by GPA or its subsidiaries.

In the individual financial statements, investments in controlled companies are accounted for under the equity method.

12.2. Accounting information of the associates

Investments in associates are accounted for under the equity method since it is an entity in which the Company exerts significant influence, but not the control, since (a) it is part of the shareholders’ agreement, appointing part of the management and having veto right in certain relevant decisions; and (b) power over operating and financial decisions. The associates are: (i) FIC managed by Itaú Unibanco S.A., (ii) Cnova N.V. which operates

Free translation |

Principal accounting practices adopted

in the preparation of the Balance Sheet on September 30, 2020

mainly in the e-commerce in France; and (iii) Tuya, a finance investee of Éxito. There are no restrictions by the associates on transferring funds to the Company, for example as dividends.

13. Business combination and goodwill

Business combinations are accounted for under the acquisition method. The acquisition cost corresponds to the sum of the amount transferred, measured at fair value on the acquisition date, and the remaining amount of the noncontrolling shareholders’ interest in the acquired company. For every business combination, the buyer measures the noncontrolling shareholders’ interest in the acquired company at fair value or in proportion to the interest held in the identifiable net assets of the acquired company. The acquisition costs incurred are treated as expense and included in administrative expenses.

When the Company acquires a business, it evaluates the assets acquired and the financial liabilities assumed for the proper classification and designation according to the contractual terms, the economic circumstances and conditions on the acquisition date. This includes the separation of embedded derivatives in agreements by the acquired company.

Any contingent payment to be transferred by the buyer will be recognized at fair value on the acquisition date. Subsequent changes in the fair value of the contingent payment considered as asset or liability will be recognized through the result.

The goodwill is initially measured at cost, and the excess between the amount transferred and the amount recognized of noncontrolling shareholders’ interest on the assets acquired and liabilities assumed. If this payment is lower than the fair value of the net assets of the acquired subsidiary, the difference is recognized in the result as gain from advantageous purchase.

After the initial recognition, the goodwill is measured at cost, less non-recoverable losses. For purposes of test of loss on recoverable value, the goodwill acquired in a business combination is, since the acquisition date, allocated to each of the UGCs of the Company which should benefit from the business combination, regardless if other assets or liabilities of the acquired company are attributed to these UGCs.

Where the goodwill is part of an UGC and part of the operation within this unit is sold, the goodwill associated to the operation sold is included in the accounting value of the operation in the calculation of profit or loss on the sale of the operation. This goodwill is measured based on the values related to the operation sold and to the portion of the UGC that was maintained.

14. Properties for Investment

Properties for investment are measured at historical cost (including transaction costs), less accumulated depreciation and/or losses on non-recoverable losses, if any. The cost of properties for investment acquired in a business combination is calculated at fair value, pursuant to IFRS 3/ CPC 15 - Business Combination.

Properties for investment are written off when sold or when they are no longer permanently used and they are not expected to generate any future economic benefit from their sale. A property for investment is also transferred when there is intention to sell it and in this case it is classified as noncurrent assets held for sale. The difference between the net value from this sale and the book value of the asset is recognized in the statement of income for the year upon write-off.

Free translation |

Principal accounting practices adopted

in the preparation of the Balance Sheet on September 30, 2020

The properties for investment of the Company and its subsidiaries correspond to commercial areas and lots that are held for generation of income or future price appreciation.

The fair value of properties for investment is measured based on appraisals conducted by third parties.

15. Property, Plant and Equipment

The property, plant and equipment is stated at cost, net of accumulated depreciation and non-recoverable losses, if any. The cost includes the amount of acquisition of equipment and funding costs in connection with loans for long-term construction projects, provided that the recognition criteria are met. When significant items of property, plant and equipment are replaced, these items are recognized as individual assets, with specific useful lives and depreciations. Likewise, when a significant replacement is made, its cost is recognized in the book value of the equipment as replacement, provided that the recognition criteria are met. All the other repair and maintenance costs are recognized in the result for the year as incurred.

| Category of assets Annual average depreciation rate | |

| Buildings | 2.50% |

| Improvements in own and third-party properties | 4.17% |

| Machinery and equipment | 12.12% |

| Installations | 8.19% |

| Furniture and fixtures | 11.03% |

| Other | 20.00% |

Property, plant and equipment and any significant parts are written off upon disposal or when they are not expected to generate any future economic benefit from their use or disposal. Any gains or losses resulting from the write-off of the assets are included in the result for the year.

The residual value, useful life of the assets and depreciation methods are reviewed at the closing of every year, and adjusted on prospective basis, when applicable. The Company reviewed the useful life of the property, plant and equipment in the year 2019 and concluded that there are no changes to be made in this fiscal year.

Interest of loans directly attributable to the acquisition, construction or production of an asset, which demands a substantial period of time to be finished for the intended use or sale (eligible asset), is capitalized as part of the cost of the respective assets during the construction phase. As of the date of commencement of operation of the corresponding asset, the capitalized costs are depreciated over the estimated useful life of the asset.

15.1. Reduction at recoverable value of non-financial assets

The impairment test aims to present the actual net realizable value of an asset. The realization can be directly or indirectly, through sale or cash generation in the use of the asset in the Company’s activities.

Every year, the Company conducts the impairment test of its tangible and intangible assets or whenever there is internal or external evidence that the asset can present loss on recoverable value.

The recoverable value of an asset is defined as the highest between its fair value or the

Free translation |

Principal accounting practices adopted

in the preparation of the Balance Sheet on September 30, 2020

value in use of its cash generating unit - UGC, except if the asset does not generate cash inflows that are mostly independent from cash inflows from other assets or groups of assets.

If the book value of an asset or UGC exceeds its recoverable value, the asset is considered not recoverable and a provision is recognized in order to adjust the book value to its recoverable value. In the recoverable value evaluation, the estimated future cash flow is discounted to present value, adopting a discount rate, which represents the capital cost of the Company (WACC) which reflects current market evaluations in connection with the value of money over time and the specific risks of the asset.

16. Intangible Assets

Intangible assets acquired separately are measured at cost upon initial recognition, less amortization and non-recoverable losses, if any.

Internally generated intangible assets, excluding capitalized costs of development of software, are reflected in the result for the year in which they were incurred. Intangible assets comprise mainly software acquired from third parties, software developed for internal use, goodwill (right of use of stores), list of clients, advantageous lease agreements, advantageous agreements for supply of furniture and brands.

Intangible assets with definite useful life are amortized under the straight-line method. The period and amortization method are reviewed, at least, at the closing of the fiscal year. Changes in the estimated useful life or in the estimated standard use of the future economic benefits incorporated into the asset are accounted for by changing the amortization period or method, as appropriate, and treated as changes in accounting assumptions.

The costs of development of software recognized as asset are amortized over its definite useful life (5 to 10 years), whose amortization rate is 10.82%, and the amortization begins when the asset is put into operation.

Intangible assets with indefinite useful life are not amortized, but submitted to impairment tests at the closing of the fiscal year or whenever there is indication that their book value cannot be recovered, individually or at the level of the UGC. The evaluation is reviewed on annual basis to determine if the indefinite useful life remains valid. Otherwise, the useful life estimate is changed on prospective basis from indefinite to definite.

Gain or losses, when applicable, resulting from the derecognition of an intangible asset, are measured as the difference between net results from the disposal and the book value of the asset, being recognized in the result for the year upon write-off of the asset.

17. Financial Instruments

Financial assets are recognized when the Company assumes contractual rights to receive cash or other financial assets from contracts in which it is a party. Financial assets are derecognized when the rights to receive cash tied to financial assets expire or when the risks and benefits are substantially transferred to third parties. Assets and liabilities are recognized when rights or obligations are retained in the transfer by the Company.

Financial liabilities are recognized when the Company assumes contractual obligations for settlement in cash or assumes third-party obligations through a contract in which it is a party. Financial liabilities are derecognized when they are settled, extinguished or expired.

Free translation |

Principal accounting practices adopted

in the preparation of the Balance Sheet on September 30, 2020

Purchases or sales of financial assets requiring delivery of assets within a term defined by regulation or convention in the market (negotiations under normal conditions)

are recognized on the negotiation date, that is, on the date in which the Company agrees to purchase or sell the asset.

17.1. Classification and measurement of financial assets and liabilities

Upon initial recognition, a financial asset is classified as measured at: amortized cost; fair value through other results (“VJORA”) – or fair value through the result (“VJR”). The classification of financial assets is usually based on the business model where a financial asset is managed and has characteristics of contractual cash flows. Embedded derivatives in which the principal contract is a financial asset within the scope of the standard are never separated. In turn, the hybrid financial instrument is evaluated for classification as a whole.

A financial asset is measured at amortized cost if it satisfies the two conditions below and is not classified as measured at VJR:

| • | is maintained within a business model whose purpose is to maintain financial assets to receive contractual cash flows; and |

| • | its contractual terms generate, on specific dates, cash flows related to the payment of principal and interest on the outstanding principal. |

A debt instrument is measured at VJORA if it satisfies the two conditions below and is not classified as measured at VJR:

| • | is maintained within a business model whose purpose is attained by the receiving of contractual cash flows as well as by the sale of financial assets; and |

| • | its contractual terms generate, on specific dates, cash flows that are only payments of principal and interest on the outstanding principal. |

Upon initial recognition of an investment in equity instrument that is not held for trading, the Company may opt to irrevocably present subsequent changes in the fair value of investment in other Comprehensive Results (“ORA”). This option is made on investment by investment basis.

All financial assets not classified as measured at amortized cost or VJORA, as described above, are classified as VJR. This includes all derivative financial assets. Upon initial recognition, the Company may irrevocably designate a financial asset that otherwise meets the requirements to be measured at amortized cost, VJORA or VJR if this significantly eliminates or reduces an accounting mismatch which would otherwise arise (fair value option).

A financial asset (except for trade account receivable without a material financing component that is initially measured at the transaction price) is initially measured at fair value, plus, for an item not measured at VJR, transaction costs directly attributable to acquisition.

Financial assets measured at VJR - These assets are subsequently measured at fair value. The net result, including interest or income from dividends, is recognized in the result.

Free translation |

Principal accounting practices adopted

in the preparation of the Balance Sheet on September 30, 2020

Financial assets at amortized cost - These assets are subsequently measured at amortized cost under the effective interest method. The amortized cost is reduced by losses on reduction to recoverable value. Interest income, and exchange gains and losses are recognized in the result. Any gain or loss on derecognition is recognized in the result.

Financial assets at VJORA - These assets are subsequently measured at fair value. Interest income is calculated under the effective interest method, exchange gains and losses and losses on reduction to recoverable value are recognized in the result. Other net results are recognized in ORA. Upon derecognition, the accumulated result in ORA is reclassified to the result.

17.2. Derecognition of financial assets and liabilities

A financial asset (or, as appropriate, part of a financial asset or part of a group of similar financial assets) is derecognized when:

• The rights to receive cash flows expire.

| • | The Company transfers its rights to receive cash flows from the asset or the commitment to fully pay cash flows received to a third party, according to an onlending agreement; and (a) the Company has substantially transferred all the risks and benefits related to the asset; or (b) the Company did not transfer neither substantially retain all the risks and benefits related to the asset, but transferred its control. |

When the Company assigns its rights to receive cash flows from an asset or enters into onlending agreement, without having transferred or retained substantially all the risks and benefits related to the asset neither transferred the control of the asset, the asset is held and a corresponding liability is recognized. The transferred asset and the corresponding liability are measured in a way to reflect the rights and obligations retained by the Company.

A financial liability is derecognized when the underlying obligation is settled, cancelled or expired.

When a current financial liability is replaced by another from the same creditor, under substantially different terms, or when the terms of a current liability are substantially modified, this replacement or modification is treated as derecognition of the original liability and recognition of a new liability, and the difference between the respective book values is recognized in the result for the year.

17.3. Offsetting of financial Instruments

Financial assets and liabilities are offset and stated net in the financial statements, if, and only if, there is the right to offset values recognized and intention to settle on net basis or to realize the assets and settle the liabilities simultaneously.

18. Derivative Financial Instruments

The Company uses derivative financial instruments to put a limit on the exposure to the variation not related to the local market such as swaps of interest rates and swaps of exchange variation. These derivative financial instruments are initially recognized at fair value on the date in which the derivative contract is entered into and later remeasured at fair value at the closing of the fiscal years. The derivatives are recorded as financial assets when the fair value

Free translation |

Principal accounting practices adopted

in the preparation of the Balance Sheet on September 30, 2020

is positive and as financial liabilities when negative. Gains or losses resulting from changes in the fair value of derivatives are recorded directly in the result for the year.

At the beginning of the hedge relation, the Company formally designates and documents the hedge relation to which it intends to apply hedge accounting, and its purpose and risk management strategy to contract it. The documentation includes identification of the hedge instrument, the item or operation covered by hedge, the nature of the hedged risk and how the Company should evaluate the efficiency of the changes in the fair value of the hedge instrument on the neutralization of the exposure to changes in the fair value of the item covered by hedge or the cash flow attributable to the hedged risk. These hedges are expected to be highly efficient on the neutralization of changes in fair value or cash flow, and are constantly evaluated to determine if they are actually being highly efficient over all the fiscal years of the financial reports to which they have been designated.

They are recorded as fair value hedges, following the procedures below:

| • | The change in the fair value of a derivative financial instrument classified as fair value hedge is recognized as financial result. The change in the fair value of the hedged item is recorded as part of the book value of the hedged item, and is recognized in the statement of income for the year. |

| • | Upon calculation of fair value, debts and swaps are measured at rates disclosed in the financial market and projected until their maturity date. The discount rate used for calculation under the method of interpolation of foreign currency loans is obtained through DDI curves, clean Coupon and DI, indexes disclosed by B3 and, for local currency loans it is used the DI curve, index disclosed by CETIP and calculated under the exponential interpolation method. |

The Company uses financial instruments only for protection against identified risks limited to 100% of the value of these risks. Operations with derivatives are solely used to reduce exposure to foreign currency and interest rate fluctuation, so as to maintain the stability of the capital structure.

19. Cash flow hedge

Derivative instruments are recorded as cash flow hedge, following the procedures below:

| • | The efficient portion of gain or loss of the hedge instrument is recognized directly in the shareholders’ equity under Other Comprehensive Results, and if the hedge fails to meet the hedge ratio, but the risk management purpose remains unchanged, the Company should adjust (“rebalance”) the hedge ratio to meet the qualification criteria. |

| • | Any remaining gain or loss in the hedge instrument (including from the “rebalance” of the hedge ratio) is an inefficiency and, therefore, should be recognized in the result. |

| • | The values recorded under Other Comprehensive Results are immediately transferred to the statement of income together with the transaction object of hedge when affecting the result, for example, when a financial income or expense object of hedge is recognized or when an expected sale occurs. When the item object of hedge is the cost of a non-financial asset or liability, the values recorded in the shareholders’ equity are transferred to the initial book value of the non-financial asset or liability. |

Free translation |

• Principal accounting practices adopted

in the preparation of the Balance Sheet on September 30, 2020

| • | The Company should discontinue the hedge accounting on prospective basis only when the hedge relation fails to meet the qualification criteria (after taking into consideration any rebalance of the hedge relation). |

| • | If the occurrence of the estimated transaction or firm commitment is no longer expected, the values previously recognized in the shareholders’ equity are transferred to the statement of income. If the hedge instrument expires or is sold, discontinued or exercised without replacement or rollover, or if its classification as hedge is cancelled, the gains or losses previously recognized in the comprehensive result remain deferred in the shareholders’ equity under Other Comprehensive Results until the expected transaction or firm commitment affects the result. |

20. Loss on recoverable value of financial assets

The Company adopts the expected credit loss model, which applies to financial assets measured at amortized cost, contractual assets and debt instruments measured at VJORA, but which does not apply to investments in equity instruments (shares) or financial assets measured at VJR.

Provisions for losses are measured at one of the following bases:

| • | Credit losses expected for 12 months (general model): these credit losses result from possible events of default within 12 months from the balance sheet date, and subsequently, in case of deterioration of the credit risk, for the entire life of the instrument |

| • | Credit losses expected for the entire life (simplified model): these credit losses result from all possible events of default over the expected life of a financial instrument |

| • | Practical expedient: these credit losses are expected and consistent with reasonable and sustainable information available on the balance sheet date for past events, current conditions and forecast of future economic conditions, which allow to check future probable loss based on the historical loss occurred according to the maturity of the securities. |

The Company measures provisions for losses on accounts receivable and other receivables and contractual assets for a value equal to expected credit loss for the entire life, where for trade accounts receivable, whose portfolio of receivables is dispersed, leases receivable, wholesale accounts receivable and accounts receivable from carriers, it is applied the practical expedient through adoption of a matrix of losses for each maturity range.

When determining if the credit risk of a financial asset has significantly increased since the initial recognition and when estimating the expected credit losses, the Company considers reasonable and sustainable information that is relevant and available without excessive cost or effort. It includes information and quantitative and qualitative analyses, based on the historical experience of the Company, credit evaluation and considering information on projections.

The Company assumes that the credit risk of a financial asset has significantly increased if it is more than 90 days past due. The Company considers a financial asset as default when:

| • | it is unlikely that the debtor will fully pay its credit obligations to the Company without resorting to actions such as realization of guarantee (if any); or |

Free translation |

• Principal accounting practices adopted

in the preparation of the Balance Sheet on September 30, 2020

• the financial asset is past due for more than 90 days.

The Company determines the credit risk of a debt security based on analysis of the history of payments, current financial and macroeconomic conditions of the counterparty and evaluation of rating agencies when applicable, thus assessing each security individually.

The maximum period considered in the estimate of expected credit loss is the contractual period during which the Company is exposed to the credit risk.

Measurement of expected credit losses – Expected credit losses are estimates weighted by the probability of credit losses based historical losses and projections of related assumptions. Credit losses are measured at present value based on all cash shortages (that is, the difference between cash flows payable to the Company according to agreement and cash flows that the Company expects to receive).

Expected credit losses are discounted at the effective interest rate of the financial asset.

Financial assets with credit recovery issues – On each presentation date, the Company assesses if the financial assets stated at amortized cost and the debt securities measured at VJORA present indications of loss on recoverable value. A financial asset presents indications of loss on recoverable value when there is one or more events with negative impact on the estimated future cash flows of the financial asset.

Presentation of loss on reduction to recoverable value - Provision for losses for financial assets measured at amortized cost are deducted from the gross book value of the assets.

For financial Instruments measured at VJORA, the provision for losses is recognized in ORA, instead of reducing the book value of the asset.

Losses on reduction to recoverable value related to trade accounts receivable and other receivables, including contractual assets, are presented separately in the statement of income and ORA. Losses of recoverable values of other financial assets are presented in ‘selling expenses’.

Accounts receivable and contractual assets - The Company considers the model and certain assumptions adopted in the calculation of these expected credit losses as the principal sources of uncertainty of the estimate.

The positions in each group were segmented based on usual characteristics of credit risk, such as:

| • | Level of credit risk and history of losses – for wholesale clients and lease of properties; and |

| • | Default status, risk of default and history of losses - for credit card companies and other clients. |

21. Provision for lawsuits

The provisions are recognized when the Company has a present obligation (legal or not formalized) in view of a past event, it is probable that cash outflow will be required to settle the obligation, and it is possible to make a reliable estimate of the value of this obligation. Expenses related to the provision are recorded in the result for the year, net of reimbursement. For success fees, the Company and its subsidiaries recognize a provision when the fees are

Free translation |

Principal accounting practices adopted

in the preparation of the Balance Sheet on September 30, 2020

incurred, that is, upon final judgment of the lawsuits, being disclosed in the notes, the amounts involved in the lawsuits not yet concluded.