FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16 of

the Securities Exchange Act of 1934

For the month of May, 2021

Brazilian Distribution Company

(Translation of Registrant’s Name Into English)

Av. Brigadeiro Luiz Antonio,

3142 São Paulo, SP 01402-901

Brazil

(Address of Principal Executive Offices)

(Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F)

Form 20-F X Form 40-F

(Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule

101 (b) (1)):

Yes ___ No X

(Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule

101 (b) (7)):

Yes ___ No X

(Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.)

Yes ___ No X

|

GPA maintains its pace of improved profitability |

| Financial Highlights | Consolidated(1) | GPA Brazil | Grupo Éxito(2) | ||||||

| R$ million, except when indicated | 1Q21 | 1Q20 | Δ | 1Q21 | 1Q20 | Δ | 1Q21 | 1Q20 | Δ |

| Gross Revenue | 13,722 | 13,095 | 4.8% | 7,135 | 7,342 | -2.8% | 6,571 | 5,742 | 14.4% |

| Net Revenue | 12,452 | 11,876 | 4.9% | 6,574 | 6,769 | -2.9% | 5,866 | 5,095 | 15.1% |

| Gross Profit | 3,245 | 2,942 | 10.3% | 1,696 | 1,699 | -0.2% | 1,539 | 1,242 | 23.9% |

| Gross Margin | 26.1% | 24.8% | 130bps | 25.8% | 25.1% | 70bps | 26.2% | 24.4% | 180bps |

| Selling, General and Adm. Expenses | (2,355) | (2,242) | 5.1% | (1,203) | (1,274) | -5.6% | (1,105) | (945) | 16.9% |

| Other Operating (Revenue) Expenses | (60) | (214) | -71.9% | (44) | (102) | -57.4% | (16) | (111) | -85.3% |

| Adjusted EBITDA (3)(4) | 935 | 688 | 36.0% | 538 | 485 | 10.9% | 484 | 289 | 67.4% |

| Adjusted EBITDA Margin (3)(4) | 7.5% | 5.8% | 170bps | 8.2% | 7.2% | 100bps | 8.2% | 5.7% | 250bps |

| Net Income - Controlling Shareholders (5) | 113 | (246) | n.d. | 81 | (99) | n.d. | 110 | (63) | n.d. |

| Net margin - Controlling Shareholders (5) | 0.9% | -2.1% | 300bps | 1.2% | -1.5% | 270bps | 1.9% | -1.2% | 310bps |

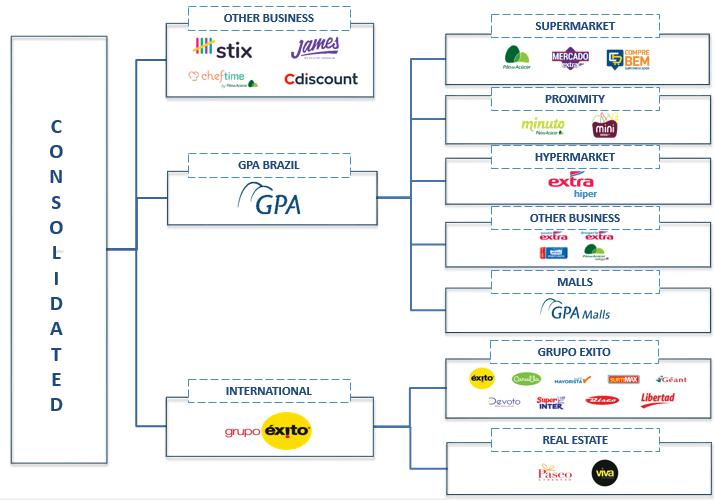

(1) Consolidated figures include the results of GPA Brazil, Grupo Éxito (Colombia, Uruguay and Argentina), other businesses (Stix Fidelidade, Cheftime and James Delivery) and Cdiscount (in the equity income line).

(2) Sales in R$, which include a positive exchange variation of 22%, due to the appreciation of the Colombian peso against the real (from 0.001257 to 0.001540).

(3) Operating income before interest, taxes, depreciation and amortization.

(4) Adjusted for Other Operating Revenue and Expenses.

(5) Continuing Operations.

Operational & Financial Highlights

| § | Total consolidated sales of R$13.7 billion, up 4.8%, supported by: |

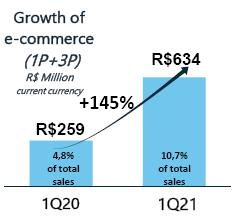

| o | Solid growth in online sales in all the countries where we operate: +137% in GPA Brazil and +145% in Grupo Éxito, with continued leadership in food e-commerce; |

| o | Growth in the proximity formats and remodeled supermarkets at GPA Brazil; |

| o | Evolution of the Éxito Wow and Carulla FreshMarket innovative formats at Grupo Éxito; and |

| o | 41 stores closed at GPA Brazil throughout 2020, with a negative impact in the quarter of 210 bps. |

| § | The sales scenario continued to improve in the quarter, despite the challenges mainly related to the macroeconomic context and the pandemic, with strict restrictive measures involving the closure of stores on weekends, reduced working hours and prohibition of sale of some categories (alcoholic beverages, home appliances, kitchen utensils and textile, among others). |

| § | Adjusted EBITDA grew by a substantial 36.0%, totaling R$935 million, driven by comercial efficiency and control of SG&A expenses at GPA Brazil and the contribution of the Viva Malls real estate development division at Grupo Éxito. |

| § | Other Income and Expenses decreased sharply, from R$214 million in 1Q20 to R$60 million in 1Q21, reflecting lower non-operating expenses. |

| § | These effects led to an R$359 million increase in net income attributable to controlling shareholders in continuing operations compared to 1Q20, reaching R$113 million. |

Strategic priorities of GPA Brazil and Grupo Éxito for 2021

| § | Escalate the Digital Platform in all the countries where we operate: increase in 1P and 3P offer of products, expansion of delivery formats (new distribution centers and partnerships with last-mile carriers) and operation as a seller in third-party marketplaces; |

| § | Organic Expansion of the Pão de Açúcar and Minuto Pão de Açúcar formats in Brazil; |

| § | Rollout and Maturation of the new supermarket concepts: Compre Bem, Mercado Extra and Pão de Açúcar G7 in Brazil and FreshMarket in Colombia and Uruguay; |

| § | Repositioning of the hypermarket model through the rollout of the new Extra Hiper in Brazil and conversion into Éxito Wow in Colombia; and |

§ Deleverage at GPA Consolidated.

| 3 |

| |

Message from the CEO

“The results recorded in the first quarter of 1Q20 reflect profitable growth, underlining the strength of GPA as one the largest food retail groups in South America. Our efforts to reduce SG&A expenses in the last three years, combined with portfolio changes and the evolution of digital initiatives in all the countries where we are present, led to a substantial increase in EBITDA and income, although the quarter was still marked by even more stringent restrictions due to the pandemic.

Our digital ecosystem continues its solid growth trajectory. Online penetration more than doubled, and online sales accounted for 6% of GPA Brazil’s food sales and 11% of Grupo Éxito’s total sales, which shows our enormous future potential. We continue to grow through our own platform and to develop our partnerships.

In the physical stores, we continued to move forward with our plans, repositioning hypermarkets with a low price policy and resuming the expansion plans for Pão de Açúcar and proximity supermarkets. We will open more than 150 new Pão and Minuto stores all over the country over the next three years. At Grupo Éxito, I highlight the continuation of conversions into the innovative formats Éxito Wow and Carulla FreshMarket.

We remain confident and focused on expanding the omnichannel initiatives - the group’s strategic priority -, moving forward with conversions and resuming the organic expansion of physical stores, in order to provide the best shopping experience for the customers who go to our stores, use our apps and make purchases on our website. This is what will guarantee our competitiveness and profitability in the coming periods.”

Jorge Faiçal

GPA’s CEO

OPERATING PERFORMANCE

SALES PERFORMANCE

| GROSS REVENUE | 1Q21/1Q20 | ||||||

| (R$ million) | Selling | % Stores total | % Stores total Constant Currency | Same stores (2) | Covid Impact |

Same stores (2) ex Covid Impact | |

| GPA Consolidated | 13,722 | 4.8% | -2.7% | -0.7% | -5.5% | 4.8% | |

| GPA | 7,151 | -2.8% | -2.8% | 1.1% | -3.9% | 5.0% | |

| GPA Brazil | 7,135 | -2.8% | -2.8% | 1.1% | -3.9% | 5.0% | |

| Others (1) | 16 | 32.8% | 32.8% | n.d. | n.d. | n.d. | |

| Grupo Éxito | 6.571 | 14.4% | -2.6% | -2.7% | -7.2% | 4.5% | |

| Colombia | 5,019 | 18.0% | -3.6% | -3.9% | -6.0% | 2.1% | |

| Uruguay | 1,148 | 8.9% | -3.6% | -4.3% | -9.6% | 5.2% | |

| Argentina | 405 | -7.4% | 17.5% | 20.7% | -14.8% | 35.6% | |

(1) Other businesses includes Stix Fidelidade, Cheftime and James Delivery.

(2) Gross same-store sales performance:

- Does not consider revenue from gas stations and drugstores

- ‘Same store’ presented in growth with constant exchange rate for international operation;

- Excluding calendar effect. In order to reflect the calendar effect, we added 70 bps in GPA Brazil and 30 bps in Grupo Éxito (10 bps in Colombia, 80 bps in Uruguay and 110 bps in Argentina)

| | 4 |

| |

GPA Brazil |

Digital Strategy

Leadership in the e-commerce, with ample avenues for growth to explore

Our digital platform is being developed at full speed. We continued to record three-digit growth, with successive progressions in our 1P and 3P supply of products. We are increasingly closer to consumers, expanding our delivery radius, improving our service level to ratios above 95% and reducing wait time with the fast-paced evolution of our partnership with last-mile carriers. Our loyalty program and the Stix coalition are also at the core of our strategy, as they increase the value created for customers by our platform. Other major deliveries are in the pipeline: our fulfillment service for marketplace sellers is already being tested; our digital wallet is under development; we are advancing in the construction of our customer knowledge platform in order to increase their lifetime value; and we are making progress in the monetization of insights with third parties.

We are working towards making our customers increasingly multichannel and digital: the number of customers who made purchases on our digital platforms grew 60% over 1Q20, with a 40% increase in omnichannel customers. The omnichannel has also been consolidating its position as a driver of share of wallet growth, as omnichannel customers spend 2.9x more than physical store customers. |

|

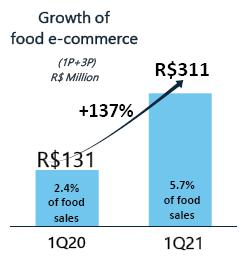

| In 1Q21, GPA consolidated its position as the largest food e-commerce player (1P – Ebit Nielsen basis), closing the quarter with a 71% share of self-service. Food e-commerce (1P + 3P) grew 137% year on year, accounting for 5.7% of the Group’s total food sales and 15% of food sales at Pão de Açúcar. The GMV of online operations totaled R$ 1.3 billion in the last twelve months. In addition to rapid sales growth, profitability – which was already positive - increased by an additional 190 bps in the period, thanks to the better commercial assertiveness and greater dilution of operating costs, with continuous improvement in our service level indicators.

We have continuously improved our logistics network and expanded our delivery models. The next-hour and same-day delivery categories together accounted for 68% of total online sales. |

Delivery Models

Express and Click & Collect (same day): At the end of the quarter, 290 stores had Express and Click & Collect services, an addition of 164 stores over 1Q20. Our ship-from-store model currently represents approximately 50% of total online sales.

Traditional Delivery (next day): The Company continues to benefit from the expansion of distribution centers held in 2020, and traditional delivery currently accounts for 32% of total online sales.

Last Mile (next hour): This quick delivery model accounted for 18% of total online sales in 1Q21, 900 bps higher than in 1Q20. This surprising improvement was driven by ongoing growth in James Delivery operations and new partnerships initiated at the end of the quarter.

| | 5 |

| |

| o | James Delivery: James Delivery, our integrated last-mile activity that is now open to the market, continued to grow substantially. The service is now available in 323 stores, up from 134 stores in 1Q20, with an increase of 292% in GMV and 142% in the number of orders. |

| o | Open Platform: In order to be where the customer is, we have entered into partnerships with Rappi and Cornershop, and our operational capacity has enabled us to quickly escalate operations: we already have 138 stores active on Rappi and 310 stores active on Cornershop. The increase in GMV generated by the new partnerships was incremental to the James operation, which did not slow down its growth after the inclusion of new partners. The launch of operations on the iFood, Mercado Livre and B2W/Americanas Mercado platforms has been confirmed for the second quarter. |

Marketplace

As for GPA’s Marketplace (3P), we continue to follow our commercial strategy of seeking partners to multiply our assortment and boost the main existing assets, focusing on verticals that complement our food core business, such as Wine, Spirits, Craft Beer, Home Care, Baby Care, Beauty and Pet Care.

In 1Q21, we tripled the number of sellers compared to 4Q20, with 4x more offers available on the platform. GMV has been continuously growing week after week, and we have quadrupled sales between January and early April. Our onboarding process is at full speed, with several technology integration projects in progress to further maximize the number of SKUs available. In the quarter, we entered into partnerships with well-known brands, such as Chopp Fast (Heineken), Grand Cru, Café Store, Melitta, Hershey's, Ri Happy, Cobasi, Madesa and Probel, which have joined a portfolio of partners that includes The Bar, Red Bull, Lego, Mobly, Etna and Spicy. The first complete quarter with the MarketPlace operations was important for the stabilization of all service level indicators at satisfactory levels.

Loyalty Program and App Evolution

We continue to consolidate our robust customer base through Loyalty programs (Cliente Mais and Clube Extra) and the Stix coalition: approximately 70% of our total sales are identified (90% in Pão de Açúcar and 60% in Extra). Also, our most loyal customers - who benefit from personalized discounts (“Meu Desconto” - My Discount) and achieve at least one goal (“Meus Prêmios” - My Rewards) - spend 10.2x more than customers who do not use these features.

In order to further encourage loyal customers to join this program, in early April we released a new version of the “Meus Prêmios” program, with important advances in the simplification of the program features on the app. As a result, our customers earned 2 million Stix points in 1Q21, with 334,000 redemptions.

We have an ongoing mission to provide our customers with the best shopping channel. In 1Q21, we made significant improvements in our digital products, such as: automation of self-service processes, integrating FAQ into the app’s chatbot; the simplification of the password reset process; the implementation of geo-targeted offerings; the expansion of means of payment; and, due to the country’s social and economic situation, credit card purchases of food items may now be paid for in installments. We are also proud to announce that we have an app that is almost fully tagged for visually impaired persons, reinforcing our commitment to inclusion and diversity.

GPA continues to strengthen its partnership with innovation ecosystems, with more than 100 active startups in GPA Labs’ portfolio. More than 40 multidisciplinary squads are working to deliver various improvements over the coming months, with initiatives fully aligned and integrated with our digital platform. We currently have over 450 professionals fully dedicated to GPA’s digital development.

| | 6 |

| |

Sales Performance

Strong growth in the online channel and supermarket and Proximity formats

| GROSS REVENUE | 1Q21/1Q20 | ||||

| (R$ million) | Selling | % Stores total | Same stores (3) | Covid Impact | Same stores (3) ex Covid Impact |

| GPA Brazil(1) | 7,135 | -2.8% | 0.3% | -2.9% | 3.2% |

| Extra Hiper | 2,820 | -7.2% | -3.9% | -3.3% | -0.5% |

| Pão de Açúcar | 1,898 | -3.5% | -1.0% | -5.4% | 4.4% |

| Mercado Extra / Compre Bem | 1,310 | 2.3% | 5.0% | -2.5% | 7.5% |

| Proximity | 525 | 34.1% | 37.9% | -4.1% | 42.0% |

| Gas Stations and Drugstores | 495 | -16.4% | -9.7% | 7.5% | -17.2% |

| Other businesses (2) | 88 | 25.8% | n.d. | n.d. | n.d. |

| GPA Brazil ex gas stations & drugstores(1) | 6,640 | -1.6% | 1.1% | -3.9% | 5.0% |

(1) GPA Brazil’s figures do not include the results of Stix Fidelidade, Cheftime and James Delivery.

(2) Revenue from lease of commercial centers.

(3) In order to reflect the calendar effect, we added 80 bps at GPA Brazil and 70 bps at GPA Brazil ex gas stations and drugstores in 1Q21.

| GPA Brazil’s total sales reached R$7.1 billion in 1Q21, positively impacted by the following key factors: (i) evolution of GPA’s Digital Platform, with 137% year-on-year growth in online sales and increase in penetration to 5.7% in the food category, as well as continued use of the omnichannel strategy as a driver of growth in the share of wallet; (ii) evolution of converted supermarket formats; and (iii) impressive growth in the Proximity formats, fueled by the performance of Minuto Pão de Açúcar and the success of the Aliados program, with continued expansion in the number of partners. It’s important to mention the growth of ‘same store sales’ excluding gas station and drugstore of +7.6% in GPA Brazil comparing to 1Q19, when there was no pandemic. |

In the quarter, sales were impacted by challenges mainly related to the macroeconomic context and the Covid-19, such as (i) a strong comparison base in March 2020, as consumers were stocking up on supplies at the beginning of the pandemic; (ii) end of emergency aid payments in the quarter; (iii) strict restrictive measures imposed by local governments, including the closure of stores on weekends, reduced working hours and prohibition of sale of some non-essential categories (home appliances, kitchen utensils, textile and alcoholic beverages among others); (iv) cancellation of Carnival and related sales dynamics; (v) 41 stores closed during 2020 as part of the portfolio optimization process, with a negative impact of 210 bps on the quarter's performance, and (vi) an unfavorable calendar effect, since 1Q20 had one extra day (February 29, a Saturday nonetheless) compared to 1Q21.

| | 7 |

| |

Hypermarkets

Extra Hiper

The hypermarket segment underwent a major transformation in recent years, with adjustments in the store portfolio through conversions and closures, ending 2020 with a 24% share of GPA’s consolidated revenue. In the second half of 2020, GPA developed a model that aims to strengthen its value proposition through (i) competitive prices in mass consumption categories, operating with constantly lower prices and fewer promotions and (ii) exploration of the format’s differential advantages by improving quality and customer service in the perishables areas and specializing the assortment of non-food products. At the end of 1Q21, 45 of the 103 Extra Hiper stores were already operating under the new concept, and 22 stores were repositioned in the quarter. It is worth noting that the stores repositioned until then recorded a sales performance higher than that of other stores. According to the plan, all the stores in this format will be repositioned by the end of 3Q21. We can also see an increase in the banner’s e-commerce sales, which reached penetration peaks of 5.5%. |  |

Restrictions on store operations had a negative impact on the banner’s performance, as most stores had some kind of restriction, in particular 32 stores with more stringent restrictions, especially in non-essential sectors, including electronics. Excluding the impact of the pandemic, the performance of the banner was almost stable at -0.5% on a same-store sales basis.

Premium Supermarkets

Pão de Açúcar

Pão de Açúcar, GPA’s premium supermarket banner, has been improving over the last three years, in line with changes in customer profile and consumption. The latest store concept, or seventh generation (G7), features a store with a wide assortment of products, ranging from basic to highly sophisticated; health items and unique ready-to-eat and ready-to-go solutions; specialized customer service in the butcher, bakery, rotisserie and wine sections; a more social environment with living and interaction spaces and cafes; and a frictionless shopping experience thanks to digital technology.

Of the 182 Pão de Açúcar stores, distributed in 13 Brazilian states, 46 have already been renovated under the G7 concept. Still in 2021, we will roll out the main successful concepts of the model in the other Pão de Açúcar stores, strengthening the prominence of fresh products. The store opening plan should be resumed in the second half of 2021, with 50 new stores planned for the next three years, 5 of which as early as 4Q21. We also continued to expand new management projects and operational automation, including self-checkout models, reaching 48 stores at the end of 1Q21, with plans to reach a total of 57 stores at the end of 2Q21. |  |

It is also worth noting the important contribution of e-commerce and G7 stores, which continued to outperform the other stores. Pão de Açúcar’s online sales grew 128% - reaching penetration peaks of 15% in the quarter. The recent partnerships should contribute to accelerate the sales of Pão de Açúcar.

The banner’s sales were impacted by the effects of the Covid-19 pandemic, in particular changes in the habits of increasingly digitalized consumers and the migration of customers from large cities (to the countryside and the seacost region). Excluding the effects of Covid-19, Pão de Açúcar sales grew 4.4%, led by growth in stores located in coastal regions, which posted a substantial increase of approximately 14% in sales.

| | 8 |

| |

Mainstream Supermarkets

Compre Bem and Mercado Extra supermarkets performed well in the quarter as a result of the success of the formats’ value proposition with their target audience. Same-store sales increased 7.5%, excluding the Covid impact.

Mercado Extra

The quarter marked the conclusion of the conversion of Extra Super stores into Mercado Extra, which began around three years ago, with the conversion of the 6 last stores (2 of which in April), totaling 147 stores in 6 states. The changes include new layout, product mix and visual identity that have pleased C and D class customers. Service quality and better customer service are also requirements of the Mercado Extra concept, which also has competitive prices and a wide assortment of GPA private label brands, such as Qualitá, Taeq and Nous, representing 25% of Mercado Extra’s sales.

Mercado Extra continues to accelerate the integration of its units into Extra’s food e-commerce operation. The Express model, which ensures deliveries in up to 4 hours after the order confirmation, went from 10 stores in 1Q20 to 57 Mercado Extra stores in 1Q21. In addition, last-mile sales also accelerated significantly.

Compre Bem

Compre Bem is a local supermarket operation launched in 2018, as a result of the conversion of Extra Super stores. The format has important differential advantages in the perishables category, especially in the fruits and vegetables, bakery and butcher sections, with assortment and services appropriate to the needs of consumers in the neighborhoods where the stores are located. The chain has 28 stores, most of which are located in São Paulo state outside the state capital.

In 1Q21, the banner recorded impressive double-digit growth in sales, as a result of the success of the format’s value proposition, despite the strong comparison base (13 stores operating for 2 years and 15 stores operating for 1 year under the new format). In 2021, the banner’s main strategies are i) IT systems and commercial integration and ii) consolidation of the model in all the cities where it operates, as part of an ongoing operational efficiency process.

Proximity

GPA’s Proximity formats continued to record substantial sales growth of 37.9% this quarter, despite the pressure on stores near offices and more stringent circulation restrictions. Excluding the impact of the pandemic, the performance of the banner was 42.0% on a same-store sales basis. As a result, it reached the mark of 11 consecutive quarters of double-digit sales growth.

Minuto Pão de Açúcar and Mini Extra

Minuto Pão de Açúcar is GPA’s premium Proximity format; it offers a unique assortment in an environment that combines practicality, convenience and quality, as well as personalized services and customer service.

GPA intends to resume growth in the Minuto format in the second half of 2021, inaugurating 100 new Minuto units over the next 3 years, approximately 20 of which scheduled for 2021. It is worth noting that the Proximity formats have an exclusive Distribution Center, located in São Paulo, which ensures the necessary agility in product replacement for these formats.

Aliados Mini Mercado Program

The Aliados Mini Mercado program is GPA’s B2B business model to supply neighborhood stores, such as grocery stores and other commerce channels that wish to boost their operations through a partnership with GPA. Focused on São Paulo and served by the Distribution Center of the Proximity formats, optimizing costs and logistics routes, the model recorded substantial year-on-year growth of 2.7x, reaching around 1,200 partners in 1Q21 (+37.5% over 1Q20). |  |

| | 9 |

| |

Private Label Brands

At the moment, our private label portfolio is composed of the following brands: Quality (day-to-day items, focused on food), Taeq (healthy food), Casino (imported and differentiated products), Cheftime (ready-to-eat solutions, take away or prepare, in addition to gastronomic kits), Club des Sommeliers (wine of different nationalities), Fábrica 1959 (craft beer), Finlandek (household items) and, more recently, Nous (beauty products).

With great untapped potential in Brazil, the private label brands represent one of the main strategic aspects for building customer loyalty and increasing customer traffic at our stores. We already have a food assortment of around 5,200 SKUs.

In 1Q21, the share of private label brands reached 20.9%, and ticket penetration data were very positive: around 80% of our customers acquire at least one private label brand product.

Grupo Éxito

Digital Strategy

| Grupo Éxito’s digital strategy continued to present solid positive sales results, with growth in online sales, in addition to the establishment of partnerships with last-mile carriers and stronger positioning with loyalty programs.

We describe below the main details of the omnichannel and digital transformation strategies adopted by Grupo Éxito in all the countries where it operates. The variations below considers local currency excepted when indicated. |

Colombia

Omnichannel sales grew 118% in 1Q21 and accounted for 13.0% of sales (vs. 5.7% in 1Q20). Orders increased 60% year on year, totaling 2 million. The omnichannel performance reflected a strong and profitable platform that already covers Grupo Éxito’s three segments in Colombia and fully meets customer preferences.

Éxito.com and carulla.com recorded a 2.1x expansion in 1Q21 sales, increasing by 45.8% the number of visits.

The marketplace accounted for 14% of total omnichannel sales, mainly represented by non-food categories, such as electronics, household items and apparel. In 1Q21, the business unit recorded a 1.5x increase in GMV, with around 18,000 units sold (1.8x vs. 1Q20). The Company continues to strengthen the functionalities of its platform while including its ecosystem and capabilities to develop and strengthen this business unit.

The last-mile and home-delivery services reached 2 million orders, driven by the group’s own capacity and the partnership with Rappi. In 1Q21, orders served through Grupo Éxito logistic platform grew 2.8x in the food and non-food categories.

The Company also innovated in omnichannel proposals, such as the Click/Call & Collect service and last-mile delivery in the three low-cost banners, Super Inter, Surtimax and Surtimayorista.

| | 10 |

| |

The Éxito and Carulla apps complement other initiatives integrated into the Company’s business ecosystem, such as the Puntos Colombia loyalty program, Tuya Pay and the sale of insurance policies. The apps included additional developments, such as smart shopping lists and a virtual line for customers at the store. Both apps exceeded 1.3 million active downloads in 1Q21 (+28.7%), 1.5 million tickets and 1.0 million discounts were activated in “My Discount” functionality. The “Misurtii” app also contributed to digitalizing food sales, especially in the “mom & pop” category.

Grupo Éxito continues to implement improvements in contactless technology, customer service, data analytics, logistics, supply chain, and HR management in line with the strategy designed for 2021-2023. In addition, the Company continued to promote the loyalty coalition: Puntos Colombia, a loyalty program with over 100 partners, enabled around 1.7 million customers to redeem more than 6,600 million points in 1Q21, of which Éxito accounted for 76%. The Company focused its efforts on continuing to consolidate its marketplace integrated into Grupo Éxito’s ecosystem (Apps, VIVA tenants, travel, insurance, mobile, etc.).

Other complementary businesses include omnichannel sales of VIVA malls, strengthened by Viva Online, Click & Collect and its own delivery service; the TUYA financial business; the mobile business unit, which continues to grow, driven by online channels and integration with the company's ecosystem; and the travel business unit.

Uruguay

In Uruguay, the operation continued to strengthen its digital channels in 1Q21 to respond with agility to consumers’ needs. Therefore, omnichannel sales grew 1.3x vs. 1Q21 and accounted for 3.3% total sales (+90 bps. vs. 2020).

In e-commerce, 1Q21 online sales grew 1.6x and accounted for 1.3% of total sales (+50 bps vs. 1Q20). In home delivery, sales went up 1.5x in 1Q21 and deliveries totaled 57,000 (vs. 30,500 in 1Q20). The Click & Collect service is available in 41 stores and totaled around 5,400 orders (vs. almost 4,000 in 1Q20). The app, in turn, reached 55,000 downloads and 5,000 orders were sent in the quarter.

In addition, Grupo Éxito selected seven startups for mentoring and currently works on initiatives focused on sustainability, last mile, logistics and innovation.

Argentina

The operation in Argentina continued to strengthen its digital initiatives, and omnichannel sales accounted for 1.9% of total sales and the website had over 935,000 visits.

The Click & Collect/Click and Carry service was implemented in 15 stores, totaling 12,800 orders in the quarter. In the last-mile & home-delivery services, we entered into a partnership with Rappi and Pedidos Ya. Therefore, the last-mile service was implemented in 21 stores in 1Q21 (11 hyper and 10 Proximity stores). Sales increased 6.2x over the same period in 2020 and 407,000 units were sold through more than 43,000 orders (+5x vs. 1Q20).

| | 11 |

| |

Sales Performance

|

| GROSS REVENUE | 1Q21/1Q20 | |||||

| (R$ million) | Selling | % Stores total | % Stores Total Constant Currency | Same stores (2) | Covid Impact | Same stores (2) ex Covid Impact |

| Grupo Éxito | 6,571 | 14.4% | -2.6% | -2.7% | -7.2% | 4.5% |

| Colombia | 5,019 | 18.0% | -3.6% | -3.9% | -6.0% | 2.1% |

| Éxito | 3,440 | 19.8% | -2.2% | -2.7% | -4.9% | 2.3% |

| Carulla | 687 | 15.3% | -5.8% | -4.8% | -8.7% | 3.9% |

| Low Cost and other businesses (1) | 892 | 13.5% | -7.3% | -8.6% | -21.9% | 13.3% |

| Uruguay | 1,148 | 8.9% | -3.6% | -4.3% | -9.6% | 5.2% |

| Argentina | 405 | -7.4% | 17.5% | 20.7% | -14.8% | 35.6% |

| Grupo Éxito ex gas stations | 6,507 | 14.4% | -2.6% | -2.7% | -7.2% | 4.5% |

(1) Includes the Surtimayorista, VIVA, Aliados and Other Businesses formats.

(2) Same-store sales performance:

- Considers growth at a constant exchange rate; and

- In order to reflect the calendar effect, we added 30 bps at Grupo Éxito (10 bps in Colombia, 80 bps in Uruguay and 110 bps in Argentina)

Grupo Éxito's total sales totaled R$ 6.6 billion in the quarter, an increase of 14.4%. This growth includes a positive exchange rate impact, reflecting the appreciation of the Colombian peso in relation to the real. At constant exchange rates, Grupo Éxito's total sales decreased by 2.6%, which can be attributed mainly to the strong comparison base of 1Q20, when sales were driven by the stocking movement of consumers in the three countries where Grupo Éxito operates, started in the second half of March, in addition to greater restrictions to combat Covid-19, including the temporary closure of stores in the quarter. In the 'same stores' concept, the Grupo Éxito presented a drop of 2.7%. However, excluding Covid's impact, 'same store' sales grew by 4.5% in the quarter. Compared to 1Q19, when the pandemic did not exist, ‘same store’ sales excluding gas station grew by 9.0%. |  |

Colombia

Éxito

The Éxito banner comprises hypermarkets, supermarkets and express stores, mostly located in large urban areas in Colombia. These stores provide a broad range of products, including food and non-food categories, and are set up like department stores.

Éxito Wow is an innovative model that allows digitally connected hypermarkets to integrate digital channels and brick-and-mortar services provided by Éxito with other services, including banking services, co-working areas, gourmet food courts, omnichannel areas, among others. This model was rolled out to 11 stores, which accounted for 23% of total sales and grew 900 bps faster than the other stores.

The 1Q21 performance was impacted by an increase in store closures, mobility restrictions and lockdowns in the quarter in the main cities, in addition to a strong comparison base in 1Q20, as consumers were stocking up on supplies at the beginning of the pandemic, in mid-March. However, these impacts were partially offset by the Éxito Wow performance, growth of non-food category and “Éxito’s Anniversary” event.

| | 12 |

| |

Carulla

Carulla is a premium banner that comprises supermarkets and express stores, mostly located in the major cities in Colombia.

Carulla FreshMarket is an innovative model designed to strengthen the fresh products category, focusing on quality, as well as renovating the store layout. This model includes digital initiatives, such as apps, improved customer service experience and a greater supply of key items, such as wine, pasta, cheese and coffee, mainly.

The 1Q21 performance was impacted by more stringent restrictions in the main stores of the banner, in Bogotá and Medellín, which offset (i) the strong contribution of omnichannel sales and (ii) the performance of the 14 Carulla FreshMarket stores, whose sales grew at a pace 750 bps faster than the other stores and accounted for approximately 31.6% of Carulla banner’s total sales in 1Q21. |  |

Low Cost and other businesses

In 1Q21, performance was impacted by (i) lockdowns in the hotel sector and significant store closures in the main markets of the banners, especially in January, due to the pandemic, (ii) the strong comparison base in 1Q20 as consumers were stocking up on supplies due to Covid-19 as of mid-March 2020, as well as the sale of properties, and (iii) store base optimization with some closures and remodeling.

Surtimax and Super Inter: low-cost supermarkets, providing a full supply of basic-need items, high-quality meat, fresh fruit and vegetables, and a broad range of bulk grains at low prices. These stores have a regional approach, providing products in accordance with the local consumer needs.

Surtimayorista: the banner that has been operating in the cash-and-carry segment in Colombia for more than three years, focusing on selling products to both retail and institutional consumers, such as food retailers (including restaurants, pizza parlors and diners), conventional retailers (such as grocery stores and local supermarkets) and end customers (including schools, small businesses, churches and hospitals). It provides more than 2,100 grocery items, perishable foods, beverages, packaging, personal care and cleaning products, and others. The banner comprises 34 stores and has been increasing its portfolio by both opening new stores and converting Surtimax and Super Inter low-cost format stores.

Other businesses: Grupo Éxito’s purpose is to play a leading role by fostering innovation and integrating businesses into a comprehensive ecosystem, including (i) services; (ii) complementary businesses, such as real estate, credit card, travel services, insurance, mobile and money transfer; and (iii) royalties, financial services, marketing and others.

Uruguay

Sales performance in the country was strongly affected by the strong comparison base in 1Q20, as consumers were stocking up on supplies due to Covid-19, the closure of borders during the holiday period and a decline in traffic in the main cities. The positive highlights were the solid growth in omnichannel sales (1.3x vs. 2020), with a higher share of sales compared to 2020, and growth in non-food sales.

Argentina

Amid the country’s difficult scenario, Libertad sales were negatively influenced by (i) a strong comparison base in 1Q20, mobility restrictions and curfews, (ii) expansion of the policy of restricting price increases, and (iii) import restrictions. The Libertad banner reduced its promotional activities to protect cash in a challenging competitive market.

| | 13 |

| |

Financial Performance |

GPA BRAZIL

| (R$ million) | GPA Brazil (1) | ||

| 1Q21 | 1Q20 | Δ | |

| Gross Revenue | 7,135 | 7,342 | -2.8% |

| Net Revenue | 6,574 | 6,769 | -2.9% |

| Gross Profit | 1,696 | 1,699 | -0.2% |

| Gross Margin | 25.8% | 25.1% | 70bps |

| Selling, General and Adm. Expenses | (1,203) | (1,274) | -5.6% |

| % of Net Revenue | 18.3% | 18.8% | -50bps |

| Equity Income | 15 | 28 | -46.1% |

| Adjusted EBITDA (2) | 538 | 485 | 10.9% |

| Adjusted EBITDA Margin (2) | 8.2% | 7.2% | 100bps |

(1) GPA Brazil’s figures do not include the results of other businesses (Stix Fidelidade, Cheftime and James Delivery).

(2) Earnings before Interest, taxes, depreciation and amortization. Adjusted for Other Operating Revenue (Expenses).

GPA Brazil’s Gross Profit totaled R$1.7 billion, and gross margin was 25.8% (up 70 bps over 1Q20), chiefly due to more efficient commercial dynamics and the optimization of logistics costs.

Selling, General and Administrative Expenses totaled R$1.2 billion, representing 18.3% of net revenue, down significant 50 bps, as a result of the Company’s ongoing expense control, driven by an improvement in operational productivity in stores and distribution centers and the optimization of marketing expenses.

Equity income totaled R$15 million, reflecting the Company’s 18% interest held in FIC (Financeira Itaú CBD). The year-on-year decrease is due to the transfer of 50% of the Company’s interest to Sendas, as a result of a spin-off (in 1Q20, the Company held a 36% interest).

As a result of these impacts, GPA Brazil’s Adjusted EBITDA reached R$538 million, up 10.9% over 1Q20, and EBITDA margin increased 100 bps to 8.2%. This reinforces the importance of the portfolio transformation, the evolution of the digital initiatives and strict control of expenses.

| | 14 |

| |

GRUPO ÉXITO

| (R$ million) | Grupo Éxito | ||

| 1Q21 | 1Q20 | Δ | |

| Gross Revenue | 6,571 | 5,742 | 14.4% |

| Net Revenue | 5,866 | 5,095 | 15.1% |

| Gross Profit | 1,539 | 1,242 | 23.9% |

| Gross Margin | 26.2% | 24.4% | 180bps |

| Selling, General and Adm. Expenses | (1,105) | (945) | 16.9% |

| % of Net Revenue | 18.8% | 18.5% | 30bps |

| Equity Income | 20 | (29) | n.d. |

| Adjusted EBITDA (1) | 484 | 289 | 67.4% |

| Adjusted EBITDA Margin (1) | 8.2% | 5.7% | 250bps |

(1) Earnings before Interest, taxes, depreciation and amortization. Adjusted for Other Operating Revenue (Expenses).

Grupo Éxito’s Gross Profit totaled R$1.5 billion, and gross margin was 26.2% (up 180 bps over 1Q20), benefiting from revenue related to Viva Malls’ real estate development division, as a result of the final delivery of 2 projects (Viva Envigado and Viva Tunja). This division is responsible for developing projects, managing construction works and leasing the properties. The retail operation’s gross margin increase 20 bps compared to 1Q20.

Selling, General and Administrative Expenses totaled R$1.1 billion, up 16.9%. In local currency, expenses decreased year on year, driven by cost control initiatives implemented over the past 12 months, mainly focused on increasing productivity and optimizing marketing expenses.

Equity Income totaled R$20 million in 1Q21, reflecting the results of the Company’s 50% interest in “Puntos Colombia” and the finance company “Tuya” (both of them joint ventures with Bancolombia).

As a result of these impacts, Adjusted EBITDA reached R$484 million, up 67.4% over 1Q20, and EBITDA margin was up 250 bps, to 8.2%.

| | 15 |

| |

OTHER OPERATING REVENUE (EXPENSES)

“Other Income and Expenses” decreased sharply, from R$ 214 million in 1Q20 to R$ 60 million in 1Q21, and are related to restructuring expenses in both GPA Brazil (R$ 44 million) and Grupo Éxito (R$ 16 million).

FINANCIAL RESULT

| FINANCIAL RESULT | Consolidated | ||

| (R$ million) | 1Q21 | 1Q20 | Δ |

| Financial Revenue | 40 | 61 | -34.9% |

| Financial Expenses | (148) | (166) | -10.9% |

| Cost of Debt | (62) | (92) | -32.8% |

| Cost of Receivables Discount | (11) | (15) | -26.1% |

| Other financial expenses | (74) | (56) | 33.1% |

| Net exchange variation | (1) | (3) | -73.5% |

| Net Financial Revenue (Expenses) | (108) | (105) | 3.0% |

| % of Net Revenue | -0.9% | -0.9% | 0bps |

| Interest on lease liabilities | (183) | (165) | 11.2% |

| Net Financial Revenue (Expenses) - Post IFRS 16 | (291) | (270) | 8.1% |

| % of Net Revenue - Post IFRS 16 | -2.3% | -2.3% | 0bps |

GPA’s consolidated net financial result was an expense of R$291 million, equivalent to 2.3% of net revenue and stable year on year. Excluding interest on lease liabilities, this expense amounted to R$108 million, 0.9% of net revenue – also in line with 1Q20.

The main changes in the financial result were as follows:

| ● | Financial revenue decreased, mainly due to a lower CDI (Interbank Deposit Rate) compared to 1Q20; |

| ● | Financial expenses (including cost of receivables discount) reached R$148 million in 1Q21 (compared to R$166 million in 1Q20), mainly as a result of a decrease in the cost of debt and discount of receivables, due to lower interest rates. |

| | 16 |

| |

NET DEBT

| INDEBTEDNESS | Consolidated | |

| (R$ million) | 1Q21 | 1Q20 |

| Short Term Debt | (2,974) | (5,137) |

| Loans and Financing | (366) | (2,175) |

| Debentures | (2,608) | (2,963) |

| Long Term Debt | (5,760) | (12,222) |

| Loans and Financing | (4,259) | (1,428) |

| Debentures | (1,501) | (10,793) |

| Total Gross Debt | (8,734) | (17,359) |

| Cash and Financial investments | 3,891 | 6,152 |

| Net Debt | (4,843) | (11,207) |

| Adjusted EBITDA(1) | 2,798 | 4,315 |

| On balance Credit Card Receivables not discounted | 126 | 433 |

| Net Debt incl. Credit Card Receivables not discounted | (4,717) | (10,774) |

| Net Debt incl. Credit Card Receivables not discounted / Adjusted EBITDA(1) | -1.7x | -2.5x |

(1) Last twelve months Adjusted EBITDA (pre-IFRS 16).

(2) Debt and EBITDA figures for March 31, 2020 include Assaí’s results.

Consolidated GPA’s net debt including not discounted receivables reached R$4.7 billion in 1Q21, down R$6.1 billion, of which R $ 5.8 billion related to the deconsolidation of cash and carry operations and R$ 250 million from operating generation from continuing activities. Thus, the Company maintains its leverage at a low level, with a -1.7x net debt/Adjusted EBITDA ratio, and a strong R$3.9 billion cash position.

| | 17 |

| |

INVESTMENTS

| (R$ million) | Consolidated | ||

| 1Q21 | 1Q20(1) | Δ | |

| New stores and land acquisition | 13 | 27 | -52.5% |

| Store renovations, conversions and maintenance | 92 | 107 | -13.6% |

| IT, Digital and Logistics | 86 | 159 | -46.2% |

| Total Investments GPA Brazil | 191 | 293 | -34.9% |

| Total Investments Grupo Éxito | 140 | 82 | 71.8% |

| Total Investments Consolidated | 331 | 375 | -11.7% |

(1) Does not consider Assaí in 2020

Capex totaled R$ 331 million in 1Q21, of which R$ 191 million in Brazil and R$ 140 million in the Grupo Éxito.

In Brazil, investments are concentrated in store renovations/conversions, innovation and acceleration of digital transformation projects, including systems, marketplace and last milers, IT infrastructure and logistics and other efficiency improvement projects.

In the Grupo Éxito, near to 50% of capex was allocated to innovation, omnichannel and digital transformation activities during the period and the remainder to maintenance and support of operational structures, IT systems updates and logistics.

BREADOWN OF STORE CHANGES BY BANNER

In 1Q21, 4 Extra Super stores were converted into Mercado Extra, 1 Minuto Pão de Açúcar store was opened and 1 Éxito Wow store was converted in Colombia.

| 4Q20 | 1Q21 | ||||||

| Stores | Openings | Openings by conversion | Closing | Closing to Conversion | Stores | Sales Area ('000 sq. m.) | |

| GPA Brazil | 873 | 1 | 4 | - | -4 | 874 | 1,195 |

| Pão de Açúcar | 182 | - | - | - | - | 182 | 234 |

| Extra Hiper | 103 | - | - | - | - | 103 | 638 |

| Extra Supermercado | 6 | - | - | - | -4 | 2 | 2 |

| Mercado Extra | 141 | - | 4 | - | - | 145 | 163 |

| Compre Bem | 28 | - | - | - | - | 28 | 33 |

| Mini Extra | 150 | - | - | - | - | 150 | 37 |

| Minuto Pão de Açúcar | 86 | 1 | - | - | - | 87 | 21 |

| Other business | 177 | - | - | - | - | 177 | 66 |

| Gas stations | 74 | - | - | - | - | 74 | 59 |

| Drugstores | 103 | - | - | - | - | 103 | 8 |

| Grupo Éxito | 629 | - | 1 | -14 | -2 | 614 | 1,026 |

| Colombia | 513 | - | 1 | -14 | -2 | 498 | 829 |

| Uruguay | 91 | - | - | - | - | 91 | 92 |

| Argentina | 25 | - | - | - | - | 25 | 106 |

| Total Group | 1,502 | 1,488 | 2,221 | ||||

| | 18 |

| |

ESG

Agenda for society and the environment

GPA Brazil has made a commitment to being a mobilizing agent in the construction of a new social, environmental and governance agenda for a more inclusive and sustainable society. This objective is intrinsic and interconnected to its business model.

Based on drivers such as (i) our stakeholders’ material social and environmental issues, (ii) Casino Group's global guidelines and commitments and (iii) the UN Sustainable Development Goals (SDGs), we have prioritized and designed our sustainability strategy, which is based on minimizing social and environmental risks and creating value for our stakeholders based on the following cornerstones:

| o | Promotion of diversity and inclusion (SDGs 1, 5, 8 and 10); |

| o | Social impact and promotion of opportunities (SDGs 1, 2, 4, 8, 10 and 17); |

| o | Fight against climate change (SDGs 2, 7, 12, 13 and 17); |

| o | Value chains committed to the environment, people and animal welfare (SDGs 2, 3, 8, 10, 12, 13, 15 and 17); and |

| o | Integrated management and transparency (SDGs 8, 15, 16 and 17). |

In order to support these cornerstones, we rely on our top management’s commitment, the engagement of employees and business partners and a consistent governance structure, such as the Sustainability and Diversity Committee, an advisory body to the Board of Directors, to monitor GPA’s sustainability strategy.

Regarding social and environmental initiatives, in the first quarter of 2021, we highlight in GPA Brazil:

| o | Promotion of diversity and inclusion: we seek to develop our business based on relationships that reduce inequalities and generate more inclusive opportunities. From this perspective, one of our priority issues is the pursuit of gender equality in leadership positions. In March 2021, we reached 36.6% of women in management positions and above. We continue our strategy of not only hiring, but also developing and recognizing internal talents, in 2021, for the third consecutive year, we launched the Female Leadership Program, which trained 475 employees in the last two years and this year will reach another 390 women who hold positions from analyst to current manager and another 160 employees who are attending new maintenance training. Another priority issue on the diversity agenda is racial equity. In March 2021, 49% of employees self-declared black, a 200 bps increase over the same period last year, reaching 36% of black people in leadership positions. |

| o | Social impact and promotion of opportunities: as the pandemic intensified social and economic challenges, GPA has reinforced and maintained its commitment and solidarity to the vulnerable population. We believe we can and should be part of a mobilization network together with our customers, employees and organized civil society. In 2021, we will continue to donate essential items, such as food, personal hygiene and cleaning products. |

| | 19 |

| |

| o | Value chains committed to the environment, people and animal welfare: we constantly assess social and environmental risks in the supply chain, both to approve suppliers and product choices, and to encourage innovation and new and more sustainable practices in the production process. We have policies to confront and combat deforestation, including a specific policy for approval of beef purchases, updated in 2020, with approval procedures and criteria for all domestic suppliers in all the Company’s businesses in order to identify the direct origin and ensure compliance with social and environmental criteria. Since the implementation of the policy, 29 suppliers were blocked and all GPA’s current suppliers are authorized to supply the business units only if they are fully applying the policy for all beef lots sent to the Group and if their farms are in compliance with the criteria set out by it. The Social and Environmental Beef Purchasing Policy can be accessed here. |

| o | Fight against climate change: as announced at the beginning of the year, we have linked greenhouse gas reduction targets to the variable compensation of our executives, aligning the Company’s leadership with the climate crisis agenda. As a result of our constant efforts to reduce the environmental impacts of our operations, we closed 1Q21 with 325 stores migrated to the free energy market, a 37% increase over the same period last year – this corresponds to 75% of the Company’s energy consumption. We also improved the efficiency of waste management, with a 24% decline in landfill disposal compared to 2020. In addition, we also continue with the strategy to reduce the environmental impact related to waste generation in our operation, closing 1Q21 with a decline of 23% in total waste generation compared to the same period in the previous year. |

| o | Integrated Management and Transparency: we highlight the adhesion to two multisectoral groups: to the GTPS (Sustainable Livestock Working Group), which GPA had already been a signatory of and returned as a member at the beginning of this year, and the adhesion in February to the Brazil Clima Coalition, Forests and Agriculture. |

Grupo Éxito's operation also has the same drivers for its strategy and, through its own sustainability committee, the strategic sustainability axes have been redefined:

| o | Zero malnutrition: Through the Éxito Foundation, we will contribute to reaching, in 2030, the first generation with zero chronic malnutrition in Colombia. More than 23,371 children benefited in 1Q21, a monthly average 16% higher than the average for the previous year. |

| o | Sustainable trade: promoting a value-added relationship with our suppliers and partners, through the promotion of sustainable practices and development support programs. |

| o | My planet: focus on reducing, mitigating and offsetting the environmental impacts of the operation and contributing to the environmental awareness of our stakeholders. In this regard, we highlight the commitment and support to our customers for the correct disposal and recycling of post-consumer packaging. In 1Q21 we reached 130 tons of recycled waste, 96% higher than the average collected in 1Q20, practically already reaching the total volume recovered in 2020. |

| o | Healthy living: mobilization of customers, employees and suppliers for healthier lifestyles, through a portfolio offering that generates more quality of life and healthy habits. |

| o | Our people: Improving the quality of life of our employees by promoting diversity, inclusion and social dialogue. |

| o | Integrity: integrating performance, through governance, ethics, transparency and respect for human rights: we stand out in this quarter the review of its consultation about the materiality of social and environmental risks, establishing the following priority strategic themes: 1) Fight against climate change, 2) Support to the local economy and inclusive development, 3) Talent attraction, retention and development, 4) Circular economy, 5) Diversity and inclusion and 6) Protection of biodiversity. It also published its 2020 sustainability report (https://www.grupoexito.we.co/es/informe-sostenibilidad-2020.pdf). |

| | 20 |

| |

CONSOLIDATED FINANCIAL STATEMENTS

Balance Sheet

Balance Sheet BALANCE SHEET | |||||||

| (R$ million) | ASSETS | ||||||

| Consolidated | GPA Brazil | Grupo Éxito | |||||

| 03.31.2021 | 03.31.2020 | 03.31.2021 | 03.31.2020 | 03.31.2021 | 03.31.2020 | ||

| Current Assets | 13,650 | 20,718 | 7,627 | 13,931 | 5,913 | 6,740 | |

| Cash and Marketable Securities | 3,891 | 6,152 | 2,418 | 3,454 | 1,401 | 2,664 | |

| Accounts Receivable | 596 | 980 | 279 | 716 | 312 | 261 | |

| Credit Card | 82 | 433 | 86 | 433 | - | - | |

| Sales Vouchers and Trade Account Receivable | 508 | 500 | 141 | 206 | 358 | 292 | |

| Allowance for Doubtful Accounts | (48) | (36) | (1) | (5) | (47) | (31) | |

| Resulting from Commercial Agreements | 54 | 83 | 53 | 83 | 1 | - | |

| Inventories | 6,775 | 9,713 | 3,669 | 6,992 | 3,103 | 2,720 | |

| Recoverable Taxes | 1,538 | 1,548 | 784 | 933 | 753 | 614 | |

| Noncurrent Assets for Sale | 111 | 1,034 | 78 | 982 | 33 | 52 | |

| Prepaid Expenses and Other Accounts Receivables | 740 | 1,291 | 398 | 854 | 311 | 429 | |

| Noncurrent Assets | 36,383 | 39,377 | 16,694 | 23,091 | 19,614 | 16,235 | |

| Long-Term Assets | 4,749 | 4,828 | 4,476 | 4,668 | 288 | 167 | |

| Accounts Receivables | 44 | 0 | 39 | 0 | 5 | - | |

| Credit Cards | 44 | 0 | 39 | 0 | 5 | - | |

| Recoverable Taxes | 2,930 | 3,167 | 2,930 | 3,167 | - | - | |

| Deferred Income Tax and Social Contribution | 79 | 399 | 64 | 398 | - | (0) | |

| Amounts Receivable from Related Parties | 219 | 100 | 138 | 51 | 110 | 59 | |

| Judicial Deposits | 591 | 794 | 587 | 794 | 3 | - | |

| Prepaid Expenses and Others | 888 | 369 | 718 | 259 | 170 | 108 | |

| Investments | 1,316 | 617 | 785 | 303 | 531 | 314 | |

| Investment Properties | 3,764 | 3,248 | - | - | 3,764 | 3,248 | |

| Property and Equipment | 20,275 | 24,248 | 9,384 | 15,166 | 10,883 | 9,078 | |

| Intangible Assets | 6,278 | 6,436 | 2,050 | 2,954 | 4,148 | 3,427 | |

| TOTAL ASSETS | 50,034 | 60,095 | 24,322 | 37,023 | 25,527 | 22,975 | |

(*) Considers Assaí in 2020

| | 21 |

| |

CONSOLIDATED FINANCIAL STATEMENTS

Balance Sheet

| (R$ million) | LIABILITIES | ||||||

| Consolidated | GPA Brazil | Grupo Éxito | |||||

| 03.31.2021 | 03.31.2020 | 03.31.2021 | 03.31.2020 | 03.31.2021 | 03.31.2020 | ||

| Current Liabilities | 15,727 | 22,422 | 8,398 | 14,157 | 7,162 | 8,200 | |

| Suppliers | 7,763 | 12,038 | 3,376 | 8,074 | 4,367 | 3,961 | |

| Loans and Financing | 366 | 2,608 | 22 | 1,155 | 343 | 1,453 | |

| Debentures | 2,608 | 2,963 | 2,608 | 1,985 | - | 978 | |

| Lease Liability | 947 | 920 | 564 | 622 | 382 | 297 | |

| Payroll and Related Charges | 814 | 1,031 | 483 | 757 | 314 | 269 | |

| Taxes and Social Contribution Payable | 737 | 648 | 359 | 351 | 376 | 296 | |

| Dividends Proposed | 536 | 228 | 257 | 156 | 279 | 72 | |

| Financing for Purchase of Fixed Assets | 108 | 133 | 55 | 102 | 52 | 31 | |

| Debt with Related Parties | 230 | 192 | 115 | 104 | 84 | 61 | |

| Advertisement | 29 | 42 | 28 | 41 | - | - | |

| Provision for Restructuring | 16 | 41 | 11 | 7 | 5 | 34 | |

| Unearned Revenue | 260 | 292 | 36 | 189 | 133 | 76 | |

| Others | 1,314 | 1,286 | 485 | 612 | 825 | 673 | |

| Long-Term Liabilities | 17,124 | 23,735 | 12,560 | 14,182 | 4,562 | 9,552 | |

| Loans and Financing | 4,264 | 1,439 | 2,967 | 588 | 1,297 | 851 | |

| Debentures | 1,501 | 10,793 | 1,501 | 4,832 | - | 5,962 | |

| Lease Liability | 7,453 | 7,960 | 5,412 | 6,293 | 2,041 | 1,668 | |

| Financing by purchasing assets | 108 | - | - | - | 108 | - | |

| Related Parties | 167 | - | 167 | - | - | - | |

| Deferred Income Tax and Social Contribution | 1,038 | 1,230 | 93 | 292 | 944 | 936 | |

| Tax Installments | 225 | 349 | 218 | 348 | 7 | 1 | |

| Provision for Contingencies | 1,387 | 1,313 | 1,255 | 1,208 | 132 | 106 | |

| Unearned Revenue | 18 | 23 | 18 | 23 | - | - | |

| Provision for loss on investment in Associates | 676 | 561 | 676 | 561 | - | - | |

| Others | 286 | 65 | 254 | 37 | 33 | 28 | |

| Shareholders' Equity | 17,183 | 13,938 | 3,364 | 8,683 | 13,805 | 5,223 | |

Attributed to controlling shareholders | 14,007 | 11,240 | 3,364 | 8,683 | 10,629 | 2,532 | |

| Capital | 5,650 | 6,859 | 5,650 | 6,859 | - | - | |

| Capital Reserves | 270 | 456 | 270 | 457 | - | - | |

| Profit Reserves | 6,250 | 3,434 | (4,393) | 877 | 10,435 | 2,142 | |

| Other Comprehensive Results | 1,837 | 491 | 1,837 | 491 | 194 | 390 | |

| Minority Interest | 3,176 | 2,698 | - | - | 3,176 | 2,691 | |

| TOTAL LIABILITIES | 50,035 | 60,095 | 24,322 | 37,023 | 25,528 | 22,975 | |

(*) Considers Assaí in 2020

| | 22 |

| |

INCOME STATEMENT – 1ST QUARTER OF 2021

| R$ - Million | Consolidated (1) | GPA Brazil | Grupo Éxito | ||||||

| 1Q21 | 1Q20 | Δ | 1Q21 | 1Q20 | Δ | 1Q21 | 1Q20 | Δ | |

| Gross Revenue | 13,722 | 13,095 | 4.8% | 7,135 | 7,342 | -2.8% | 6,571 | 5,742 | 14.4% |

| Net Revenue | 12,452 | 11,876 | 4.9% | 6,574 | 6,769 | -2.9% | 5,866 | 5,095 | 15.1% |

| Cost of Goods Sold | (9,148) | (8,880) | 3.0% | (4,848) | (5,038) | -3.8% | (4,297) | (3,832) | 12.1% |

| Depreciation (Logistic) | (59) | (54) | 10.8% | (29) | (32) | -8.8% | (30) | (21) | 40.1% |

| Gross Profit | 3,245 | 2,942 | 10.3% | 1,696 | 1,699 | -0.2% | 1,539 | 1,242 | 23.9% |

| Selling Expenses | (1,890) | (1,841) | 2.6% | (1,036) | (1,123) | -7.8% | (825) | (702) | 17.5% |

| General and Administrative Expenses | (466) | (401) | 16.2% | (168) | (151) | 10.6% | (280) | (243) | 15.4% |

| Selling, General and Adm. Expenses | (2,355) | (2,242) | 5.1% | (1,203) | (1,274) | -5.6% | (1,105) | (945) | 16.9% |

| Equity Income(2) | (14) | (66) | -78.5% | 15 | 28 | -46.1% | 20 | (29) | n.d. |

| Other Operating Revenue (Expenses) | (60) | (214) | -71.9% | (44) | (102) | -57.4% | (16) | (111) | -85.3% |

| Depreciation and Amortization | (488) | (433) | 12.8% | (287) | (262) | 9.5% | (199) | (170) | 17.2% |

| Earnings before interest and Taxes - EBIT | 327 | (13) | n.d. | 178 | 88 | 101.5% | 238 | (13) | n.d. |

| Financial Revenue | 82 | 141 | -41.7% | 27 | 76 | -63.9% | 55 | 65 | -16.1% |

| Financial Expenses | (374) | (411) | -9.0% | (248) | (303) | -18.3% | (125) | (107) | 17.2% |

| Net Financial Result | (292) | (270) | 8.1% | (220) | (228) | -3.1% | (71) | (42) | 68.8% |

| Income (Loss) Before Income Tax | 36 | (282) | n.d. | (43) | (139) | -69.3% | 168 | (55) | n.d. |

| Income Tax | 92 | 57 | 61.6% | 124 | 41 | 206.0% | (40) | 15 | n.d. |

| Net Income (Loss) Company - continuing operations | 128 | (225) | n.d. | 81 | (99) | n.d. | 127 | (41) | n.d. |

| Net Result from discontinued operations | (1) | 106 | n.d. | (0) | (6) | -91.3% | (0) | (0) | -97.6% |

| Net Income (Loss) - Consolidated Company | 127 | (119) | n.d. | 81 | (104) | n.d. | 127 | (41) | n.d. |

| Net Income (Loss) - Controlling Shareholders - continuing operations(3) | 113 | (246) | n.d. | 81 | (99) | n.d. | 110 | (63) | n.d. |

| Net Income (Loss) - Controlling Shareholders - discontinued operations(3) | (1) | 106 | n.d. | (0) | (6) | -91.3% | (0) | (0) | -97.6% |

| Net Income (Loss) - Consolidated Controlling Shareholders(3) | 112 | (140) | n.d. | 81 | (104) | n.d. | 110 | (63) | n.d. |

| Minority Interest - Non-controlling - continuing operations | 15 | 21 | -28.2% | - | - | n.d. | 17 | 22 | -22.7% |

| Minority Interest - Non-controlling - discontinued operations | (0) | (0) | -97.6% | - | - | n.d. | (0) | (0) | -97.6% |

| Minority Interest - Non-controlling - Consolidated | 15 | 21 | -28.2% | - | - | n.d. | 17 | 22 | -22.7% |

| Earnings before Interest, Taxes, Depreciation, Amortization - EBITDA | 875 | 474 | 84.6% | 494 | 382 | 29.2% | 468 | 178 | 162.6% |

| Adjusted EBITDA (4) | 935 | 688 | 36.0% | 538 | 485 | 10.9% | 484 | 289 | 67.4% |

| Earnings per share | 0.42 | (0.52) | n.d. | 0.30 | (0.39) | n.d. | 0.25 | (0.14) | n.d. |

| % of Net Revenue | Consolidated (1) | GPA Brazil | Grupo Éxito | |||

| 1Q21 | 1Q20 | 1Q21 | 1Q20 | 1Q21 | 1Q20 | |

| Gross Profit | 26.1% | 24.8% | 25.8% | 25.1% | 26.2% | 24.4% |

| Selling Expenses | 15.2% | 15.5% | 15.8% | 16.6% | 14.1% | 13.8% |

| General and Administrative Expenses | 3.7% | 3.4% | 2.5% | 2.2% | 4.8% | 4.8% |

| Selling, General and Adm. Expenses | 18.9% | 18.9% | 18.3% | 18.8% | 18.8% | 18.5% |

| Equity Income(2) | 0.1% | 0.6% | 0.2% | 0.4% | 0.3% | 0.6% |

| Other Operating Revenue (Expenses) | 0.5% | 1.8% | 0.7% | 1.5% | 0.3% | 2.2% |

| Depreciation and Amortization | 3.9% | 3.6% | 4.4% | 3.9% | 3.4% | 3.3% |

| Earnings before interest and Taxes - EBIT | 2.6% | 0.1% | 2.7% | 1.3% | 4.1% | 0.3% |

| Net Financial Result | 2.3% | 2.3% | 3.4% | 3.4% | 1.2% | 0.8% |

| Income (Loss) Before Income Tax | 0.3% | 2.4% | 0.7% | 2.1% | 2.9% | 1.1% |

| Income Tax | 0.7% | 0.5% | 1.9% | 0.6% | 0.7% | 0.3% |

| Net Income (Loss) Company - continuing operations | 1.0% | 1.9% | 1.2% | 1.5% | 2.2% | 0.8% |

| Net Income (Loss) - Consolidated Company | 1.0% | 1.0% | 1.2% | 1.5% | 2.2% | 0.8% |

| Net Income (Loss) - Controlling Shareholders - continuing operations(3) | 0.9% | 2.1% | 1.2% | 1.5% | 1.9% | 1.2% |

| Net Income (Loss) - Consolidated Controlling Shareholders(3) | 0.9% | 1.2% | 1.2% | 1.5% | 1.9% | 1.2% |

| Minority Interest - Non-controlling - continuing operations | 0.1% | 0.2% | 0.0% | 0.0% | 0.3% | 0.4% |

| Minority Interest - Non-controlling - Consolidated | 0.1% | 0.2% | 0.0% | 0.0% | 0.3% | 0.4% |

| Earnings before Interest, Taxes, Depreciation, Amortization - EBITDA | 7.0% | 4.0% | 7.5% | 5.6% | 8.0% | 3.5% |

| Adjusted EBITDA (4) | 7.5% | 5.8% | 8.2% | 7.2% | 8.2% | 5.7% |

(1) Consolidated figures include the results of other complementary businesses; (2) Equity income includes Cdiscount’s results in the Consolidated figures; (3) Net income after non-controlling interest; (4) Adjusted for Other Operating Revenue and Expenses. (4) Adjusted for Other Operating Income and Expenses.

| | 23 |

| |

CASH FLOW – CONSOLIDATED(*)

| STATEMENT OF CASH FLOW | ||

| (R$ million) | Consolidated | |

| 03.31.2021 | 03.31.2020 | |

| Net Income (Loss) for the period | 127 | (119) |

| Deferred income tax | (114) | (97) |

| Loss (gain) on disposal of fixed and intangible assets | 32 | 114 |

| Depreciation and amortization | 548 | 609 |

| Interests and exchange variation | 246 | 387 |

| Equity Income | 14 | 66 |

| Provision for contingencies | 3 | 27 |

| Share-Based Compensation | 7 | 9 |

| Allowance for doubtful accounts | 18 | 2 |

| Provision for obsolescence/breakage | (19) | - |

| Appropriable revenue | (91) | (265) |

| Loss (gain) on write-off of lease liabilities | (21) | (86) |

| Asset (Increase) decreases | ||

| Accounts receivable | 51 | (287) |

| Inventories | (151) | (920) |

| Taxes recoverable | (343) | (329) |

| Other Assets | (99) | (116) |

| Related parties | (48) | (11) |

| Restricted deposits for legal proceeding | (29) | 2 |

| Liability (Increase) decrease | ||

| Suppliers | (3,766) | (3,071) |

| Payroll and charges | (95) | 39 |

| Taxes and Social contributions payable | 168 | 111 |

| Other Accounts Payable | 158 | (36) |

| Contingencies | (24) | (42) |

| Deferred revenue | 47 | 178 |

| Taxes and Social contributions paid | (117) | - |

| Net cash generated from (used) in operating activities | (3,498) | (3,835) |

| Acquisition of property and equipment | (270) | (625) |

| Increase Intangible assets | (61) | (47) |

| Sales of property and equipment | 11 | 3 |

| Acquisition of property for investment | (93) | (6) |

| Net cash flow investment activities | (413) | (675) |

| Cash flow from financing activities | ||

| Increase of capital | - | 2 |

| Funding and refinancing | 1,015 | 3,310 |

| Payments of loans and financing | (1,528) | (321) |

| Dividend Payment | (36) | (17) |

| Resources obtained from the offering of shares and non-controlling shareholders | 7 | 3 |

| Transactions with minorities | (2) | - |

| Lease liability payments | (430) | (425) |

| Net cash generated from (used) in financing activities | (974) | 2,552 |

| Monetary variation over cash and cash equivalents | 65 | 156 |

| Increase (decrease) in cash and cash equivalents | (4,820) | (1,802) |

| Cash and cash equivalents at the beginning of the year | 8,711 | 7,954 |

| Cash and cash equivalents at the end of the year | 3,891 | 6,152 |

| Change in cash and cash equivalents | (4,820) | (1,802) |

(*) Considers Assaí in 2020

| | 24 |

| |

BREAKDOWN OF SALES BY BUSINESS – BRAZIL

| (R$ million) | Breakdown of Gross Sales by Business | ||||

| 1Q21 | % | 1Q20 | % | Δ | |

| GPA Brazil | 7,135 | 99.8% | 7,342 | 99.8% | -2.8% |

| Extra Hiper | 2,820 | 39.4% | 3,041 | 41.4% | -7.3% |

| Pão de Açúcar | 1,898 | 26.5% | 1,967 | 26.7% | -3.5% |

| Mercado Extra/Compre Bem | 1,310 | 18.3% | 1,281 | 17.4% | 2.3% |

| Proximity (1) | 525 | 7.3% | 391 | 5.3% | 34.1% |

| Gas Stations and Drugstores | 495 | 6.9% | 592 | 8.0% | -16.4% |

| Other Businesses (2) | 88 | 1.2% | 70 | 0.9% | 25.8% |

| GPA (3) | 7,151 | 100.0% | 7,353 | 100.0% | -2.7% |

| (R$ million) | Breakdown of Net Sales by Business | ||||

| 1Q21 | % | 1Q20 | % | Δ | |

| GPA Brazil | 6,574 | 99.8% | 6,769 | 99.8% | -2.9% |

| Extra Hiper | 2,548 | 38.7% | 2,751 | 40.6% | -7.4% |

| Pão de Açúcar | 1,733 | 26.3% | 1,801 | 26.6% | -3.7% |

| Mercado Extra/Compre Bem | 1,225 | 18.6% | 1,199 | 17.7% | 2.2% |

| Proximity (1) | 497 | 7.5% | 368 | 5.4% | 35.0% |

| Gas Stations and Drugstores | 492 | 7.5% | 588 | 8.7% | -16.3% |

| Other Businesses (2) | 78 | 1.2% | 62 | 0.9% | 25.5% |

| GPA(3) | 6,586 | 100.0% | 6,780 | 100.0% | -2.9% |

(1) Includes sales of Mini Extra, Minuto Pão de Açúcar and Aliados.

(2) Revenue from lease of commercial centers and delivery.

(3) GPA figures include the results of James Delivery, Stix Fidelidade and Cheftime.

BREAKDOWN OF SALES (% of Net Sales) - GPA BRAZIL

| SALES BREAKDOWN | GPA Brazil | |

| (% of Net Sales) | 1Q21 | 1Q20 |

| Cash | 47.0% | 43.3% |

| Credit Card | 42.7% | 47.5% |

| Food Voucher | 10.3% | 9.2% |

| | 25 |

| |

APPENDIX Company’s Business:

|

GLOSSARY

Grupo Éxito: The amounts reported refer to Grupo Éxito's operations in Colombia, Uruguay and Argentina. GPA acquired 96.57% of the capital stock of Grupo Éxito on November 27, 2019.

Consolidated: The amounts reported refer to the sum of the operations of GPA Brazil, Grupo Éxito and other businesses of the Company (CDiscount, Cheftime, James Delivery and Stix).

Discontinued activities: They refer to Via Varejo operations until May 2019, Assaí operations until December 2020 and other effects related to the write-off of investments.

EBITDA: EBITDA is calculated in accordance with Instruction 527 issued by the Brazilian Securities and Exchange Commission (CVM) on October 4, 2012.

Adjusted EBITDA: Adjusted EBITDA is a measure of profitability calculated by excluding Other Operating Revenue and Expenses from EBITDA. Management uses this measure in its analysis as it eliminates nonrecurring expenses and revenue and other nonrecurring items that could compromise the comparability and analysis of results.

Earnings per share: Diluted earnings per share are calculated as follows:

| ● | Numerator: profit for the year adjusted for the dilutive effects of stock options granted by subsidiaries. |

| ● | Denominator: number of shares of each category adjusted to include potential shares corresponding to dilutive instruments (stock options), less the number of shares that could be bought back in the market, as applicable. |

Equity instruments that will or may be settled with the shares of the Company and its subsidiaries are only included in the calculation when their settlement has a dilutive impact on earnings per share.

Same-store growth: All same-store growth mentioned in this document is adjusted for the calendar effect in each period.

Growth and changes: The growth and changes presented in this document refer to changes from the same period in the previous year, unless stated otherwise.

Retail vertical: It corresponds to sales of James Delivery in the Pão de Açúcar, Extra and Minuto Pão de Açúcar operations.

| | 26 |

SIGNATURES

Pursuant to the requirement of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| COMPANHIA BRASILEIRA DE DISTRIBUIÇÃO | |||

| Date: May 5, 2021 | By: /s/ Jorge Faiçal | ||

| Name: | Jorge Faiçal | ||

| Title: | Chief Executive Officer | ||

| By: /s/ Isabela Cadenassi | |||

| Name: | Isabela Cadenassi | ||

| Title: | Investor Relations Officer | ||

FORWARD-LOOKING STATEMENTS

This press release may contain forward-looking statements. These statements are statements that are not historical facts, and are based on management's current view and estimates offuture economic circumstances, industry conditions, company performance and financial results. The words "anticipates", "believes", "estimates", "expects", "plans" and similar expressions, as they relate to the company, are intended to identify forward-looking statements. Statements regarding the declaration or payment of dividends, the implementation of principal operating and financing strategies and capital expenditure plans, the direction of future operations and the factors or trends affecting financial condition, liquidity or results of operations are examples of forward-looking statements. Such statements reflect the current views of management and are subject to a number of risks and uncertainties. There is no guarantee that the expected events, trends or results will actually occur. The statements are based on many assumptions and factors, including general economic and market conditions, industry conditions, and operating factors. Any changes in such assumptions or factors could cause actual results to differ materially from current expectations.