Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-08257

GE INSTITUTIONAL FUNDS

(Exact name of registrant as specified in charter)

1600 Summer Street

Stamford, Connecticut 06905

(Address of principal executive offices)(Zip code)

GE Asset Management, Inc.

1600 Summer Street

Stamford, Connecticut 06905

(Name and Address of Agent for Service)

Registrant’s telephone number, including area code: 800-242-0134

Date of fiscal year end: 09/30

Date of reporting period: 09/30/15

Table of Contents

| Item 1. | Reports to Stockholders |

Table of Contents

GE Institutional Funds

Annual Report

September 30, 2015

Table of Contents

GE Institutional Funds

| 1 | ||||

Manager Reviews and Schedules of Investments | ||||

| 2 | ||||

| 9 | ||||

| 21 | ||||

| 27 | ||||

| 33 | ||||

| 43 | ||||

| 50 | ||||

| 73 | ||||

| 87 | ||||

Financial Statements | ||||

| 88 | ||||

| 96 | ||||

| 98 | ||||

| 100 | ||||

| 102 | ||||

| 106 | ||||

| 120 | ||||

| 121 | ||||

| 122 | ||||

| 124 | ||||

This report has been prepared for shareholders and may be distributed to others only if accompanied with a current prospectus and/or summary prospectus.

Table of Contents

| Notes to Performance | September 30, 2015 (Unaudited) |

The information provided on the following performance pages relates to the GE Institutional Funds (the “Funds”, and individually, the “Fund”).

Total returns take into account changes in share price and assume reinvestment of dividends and capital gains distributions, if any. Total returns shown are net of Fund expenses.

The performance data quoted represents past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate. Accordingly, your shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Periods less than one year are not annualized. Please call toll-free (800) 242-0134 or visit the Fund’s website at http://www.geam.com for the most recent month-end performance data.

An investment in a Fund is not a deposit of any bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. An investment in a Fund is subject to risk, including possible loss of principal invested.

The Standard & Poor’s (“S&P”) 500® Composite Price Index of stocks (“S&P 500 Index”) is an unmanaged market capitalization-weighted index of stocks of 500 large U.S. companies, which is widely used as a measure of large-cap U.S. stock market performance.

The Russell 1000® Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes companies in the Russell 1000® Index with higher price-to-book ratios and higher forecasted growth values. It is a subset of the Russell 3000® Index and includes approximately 1,000 of the largest securities based on a combination of their market cap and current index membership.

The Russell 2000® Index is a market capitalization-weighted index consisting of 2,000 of the smallest U.S.-domiciled publicly traded common stocks that are included in the Russell 3000® Index. The Russell 3000® Index is comprised of the 3,000 largest U.S.-domiciled companies.

The Morgan Stanley Capital International Europe, Australasia, and Far East Index (MSCI® EAFE®) is a market capitalization-weighted index of equity securities of companies domiciled in various countries. The index is designed to represent the performance of developed stock markets outside the U.S. and Canada and excludes certain market segments unavailable to U.S. based investors.

GE Investment Distributors, Inc., member of FINRA & SIPC is the principal underwriter and distributor of the GE Institutional Funds and a wholly owned subsidiary of GE Asset Management Incorporated, the investment adviser of the Funds.

The Morgan Stanley Capital International All Country World Index Ex-U.S. (MSCI® ACWI Ex-U.S.) is a market capitalization-weighted index designed to provide a broad measure of stock performance throughout the world, with the exception of U.S.-based companies. The MSCI ACWI Ex-U.S. Index includes both developed and emerging markets.

The Barclays U.S. Aggregate Bond Index is an unmanaged market value-weighted index of taxable investment grade debt issues, including government, corporate, asset-backed and mortgage-backed securities, with maturities of one year or more. The index is designed to represent performance of the U.S. investment-grade fixed rate bond market.

The 90 Day U.S. T-Bill is an unmanaged measure/index of the performance of the most recently auctioned 90 day U.S. Treasury bills (i.e., having a total maturity of 90 days) currently available in the marketplace.

The results shown for the foregoing indices assume the reinvestment of net dividends or interest and do not reflect fees, expenses, or taxes. As such, index returns do not reflect the actual cost of investing in the instruments that comprise an index.

The peer universe of the underlying open end funds used for the peer group average annual total return calculation is based on a blend of Morningstar peer categories, as shown. Morningstar is an independent mutual fund rating service. A Fund’s performance may be compared to or ranked within a universe of mutual funds with investment objectives and policies similar but not necessarily identical to that of the Fund.

©2015 Morningstar, Inc. All Rights Reserved. The Morningstar information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damage or losses relating from any use of this information. Past performance does not guarantee future results.

The S&P 500 Index Fund is not sponsored, endorsed, sold or promoted by Standard & Poor’s, and Standard & Poor’s makes no representation or warranty, express or implied, to the investors of the Fund or any member of the public regarding the advisability of investing in the securities generally or in this Fund particularly or the ability of the S&P 500 Index Fund to track general stock market performance.

Russell Investment Group owns the Russell Index data, including all applicable trademarks and copyrights, used by GE Asset Management Incorporated in these materials. Any unauthorized use or redistribution of such Russell Index data is strictly prohibited. Russell Investment Group is not responsible for the configuration of this material or for any inaccuracy in GE Asset Management Incorporated’s presentation thereof.

The views, expressed in this document, reflect our judgment as of the publication date and are subject to change at any time without notice.

1

Table of Contents

| U.S. Equity Fund | (Unaudited) |

David B. Carlson

Chief Investment

Officer — U.S. Equities

Stephen V. Gelhaus

Senior Vice President

Paul C. Reinhardt

Senior Vice President

The U.S. Equity Fund is managed by a team of portfolio managers that includes David B. Carlson, Stephen V. Gelhaus and Paul C. Reinhardt. Each of the foregoing portfolio managers manages one of three sub-portfolios, which comprise the Fund. A sub-portfolio refers to the portion of the Fund’s assets that are allocated to, and managed by, a particular portfolio manager on the Fund’s portfolio management team. The three sub-portfolios are managed independently of each other and the portfolio managers have full discretion over their sub-portfolio. However, as lead portfolio manager for the Fund, Mr. Carlson is vested with the authority to adjust the allocation of assets to each sub-portfolio. See portfolio managers’ biographical information beginning on page 124.

| Q. | How did the GE Institutional U.S. Equity Fund perform compared to its benchmark and Morningstar peer group for the twelve-month period ended September 30, 2015? |

| A. | For the twelve-month period ended September 30, 2015, the GE Institutional U.S. Equity Fund returned -3.57% for the Investment Class shares and -3.83% for the Service Class shares. The Fund’s benchmark, the S&P 500 Index returned -0.61% and the Fund’s Morningstar peer group of 1,658 US Large Blend funds returned an average of -2.67% over the same period. |

| Q. | What market conditions impacted the Fund’s performance? |

| A. | In the past year the growth style of investing has significantly outperformed value. Several macro themes have driven the market, including the strengthening U.S. dollar, and falling interest rates and energy prices. Energy dropped close to 30% — the worst performing S&P 500 sector. Growth concerns stemming from China and the emerging markets exacerbated commodity weakness, creating headwinds for many multi-national companies. In this risk-off environment, consumer staples and utilities (both +7%) were the best-performing S&P 500 sectors — and |

| defensive positioning mattered. Portfolios that were tilted to higher interest rates struggled on a relative basis, as the Federal Reserve’s initial rate hike was pushed out. |

| Q. | What were the primary drivers behind Fund performance? |

| A. | The Fund’s sector allocation effect was positive, bolstered by overweights in consumer discretionary and health care; two of the period’s strongest performing S&P 500 sectors. In these sectors, Boston Scientific (+24%), Advance Auto Parts (+19%) and Actavis (+6%) contributed most positively to portfolio returns. Underweighting the struggling energy and materials sectors was another positive factor. Underperformance for the Fund, therefore, was driven mostly by positioning for higher interest rates and individual stock selections within sectors. |

| Fed tightening expectations receded over the year, and we were not positioned for this scenario, with an underweight in the high yielding REITs, and a tilt toward interest-rate and market sensitive financials holdings (e.g., Invesco -19%, Ameriprise -10% and State Street -7%). American Express underperformed as profit outlook dimmed, losing key customers (we eliminated the name). Stock selection among technology companies was a key driver of Fund performance relative to the S&P 500. Baidu (-40%) weighed most on returns as the Chinese Internet search provider invested in new businesses to bolster its leading on-line presence. We believe its margin compression will be short lived and added to the position on weakness. Qualcomm (-26%) suffered unexpected market share losses and we reduced the position. Other lagging older-line tech names included Hewlett Packard (-35% and eliminated) and EMC (-18% and reduced). As oil prices pulled back, commodity-sensitive companies like United Rentals (-34%), Hess (-31%) and Monsanto (-27%) underperformed. |

2

Table of Contents

| (Unaudited) |

| Q. | Were there any significant changes in the Fund during the period? |

| A. | During the twelve-month period the Fund reduced its exposure to areas of the market negatively impacted by weak oil and other commodities, including materials, a new energy sector underweight. The Fund added to the industrials sector, with a focus on more domestically-oriented industries including defense/aerospace, professional services, and the airlines which benefitted from falling oil prices. The Fund reduced it overweight in financials, reflecting the heightened volatility around the Fed’s course of action on interest rate normalization. Many proceeds were invested into the consumer discretionary sector — a new overweight in the last 12-months (with the thought consumers are benefiting from improving employment statistics and the “tax break” of lower gasoline prices). At year-end, the Fund’s largest sector overweights were in health care and consumer discretionary. Despite any changes in positioning, the Fund maintained its bottom-up stock selection approach with a focus on the long-term investment horizon. We believe the Fund is well-positioned to add value through active stock selection going into the next year. |

3

Table of Contents

| U.S. Equity Fund | (Unaudited) |

Understanding Your Fund’s Expenses

As a shareholder of the Fund you incur ongoing costs. Ongoing costs include portfolio management fees, distribution and service fees (for Service Class shares), professional fees, administrative fees and other Fund expenses. The following example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

To illustrate these ongoing costs, we have provided an example and calculated the expenses paid by investors in each share class of the Fund during the period. The information in the following table is based on an investment of $1,000, which is invested at the beginning of the period and held for the entire six-month period ended September 30, 2015.

Actual Expenses

The first section of the table provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the

number given for your class under the heading “Expenses paid during the period” to estimate the expenses you paid on your account during the period.

Hypothetical Example for Comparison Purposes

The second section of the table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholders reports of other funds.

Please note that the expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect transaction costs, such as sales charges or redemption fees, if any. Therefore, the second section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds.

April 1, 2015 – September 30, 2015

| Account value at the beginning of the period ($) | Account value at the end of the period ($) | Expenses paid during the period ($)* | |||||||||||||

Actual Fund Return | |||||||||||||||

Investment Class | 1,000.00 | 921.60 | 1.78 | ||||||||||||

Service Class | 1,000.00 | 920.50 | 2.98 | ||||||||||||

Hypothetical 5% Return (2.5% for the period) |

| ||||||||||||||

Investment Class | 1,000.00 | 1,023.21 | 1.88 | ||||||||||||

Service Class | 1,000.00 | 1,021.96 | 3.14 | ||||||||||||

| * | Expenses are equal to the Fund’s annualized net expense ratio of 0.37% for Investment Class shares and 0.62% for Service Class shares (for the period April 1, 2015 – September 30, 2015), multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). |

4

Table of Contents

| U.S. Equity Fund | (Unaudited) |

| Investment Profile |

A mutual fund designed for investors who seek long-term growth of capital. The Fund seeks to achieve its investment objective by investing at least 80% of its net assets under normal circumstances in equity securities of U.S. companies, such as common and preferred stocks.

| Morningstar Performance Comparison |

Based on average annual returns for periods ended September 30, 2015

| One Year | Five Year | Ten Year | ||||||||||

Number of funds in peer group | 1,658 | 1,419 | 1,201 | |||||||||

Peer group average annual total return | -2.67 | % | 11.20 | % | 5.62 | % | ||||||

Morningstar Category in peer group: Large Blend |

| |||||||||||

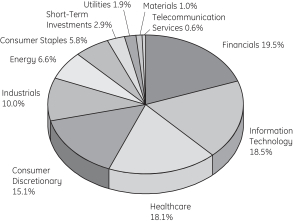

| Top Ten Largest Holdings | ||||||

as of September 30, 2015 (as a % of Fair Value) (a)(b)

Allergan PLC | 3.04% | |||

Apple Inc. | 2.67% | |||

JPMorgan Chase & Co. | 2.64% | |||

Amgen Inc. | 2.53% | |||

Cisco Systems Inc. | 2.13% | |||

PepsiCo Inc. | 1.99% | |||

QUALCOMM Inc. | 1.81% | |||

Comcast Corp., Class A | 1.81% | |||

Lowe’s Companies Inc. | 1.80% | |||

American International Group Inc. | 1.78% |

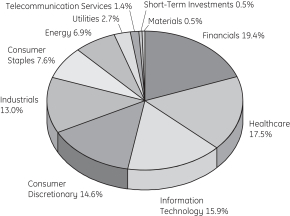

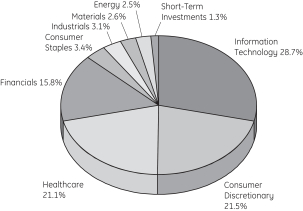

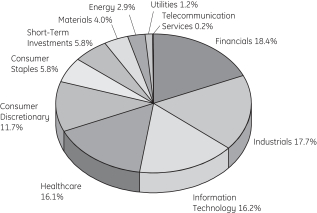

| Sector Allocation as of September 30, 2015 |

Portfolio composition as a % of Fair Value of $614,250 (in thousands) as of September 30, 2015 (a)(b)

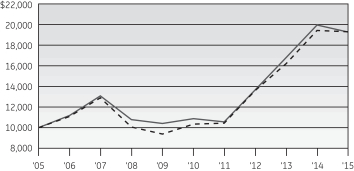

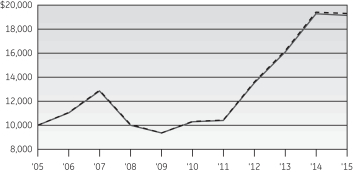

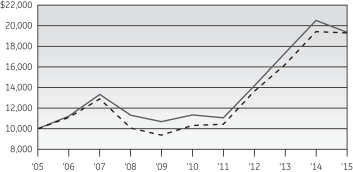

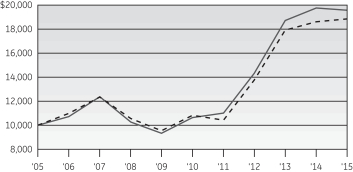

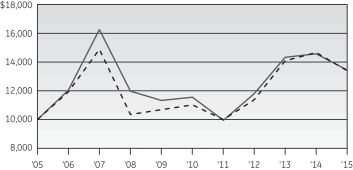

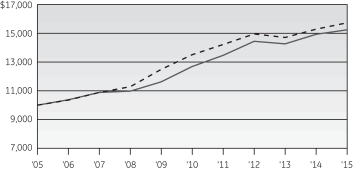

| Change in Value of a $10,000 Investment |

Investment Class Shares

| Average Annual Total Return |

for the periods ended September 30, 2015

| Investment Class Shares (Inception date: 11/25/97) | ||||||||||||||||||||

| One Year | Five Year | Ten Year | Ending Value of a $10,000 Investment | |||||||||||||||||

U.S. Equity Fund | -3.57% | 12.12% | 6.77% | $19,252 | ||||||||||||||||

S&P 500 Index | -0.61% | 13.34% | 6.80% | $19,304 | ||||||||||||||||

Service Class Shares

| Average Annual Total Return |

for the periods ended September 30, 2015

| Service Class Shares (Inception date: 1/3/01) | ||||||||||||||||||||

| One Year | Five Year | Ten Year | Ending value of a $10,000 investment | |||||||||||||||||

U.S. Equity Fund | -3.83% | 11.98% | 6.65% | $19,032 | ||||||||||||||||

S&P 500 Index | -0.61% | 13.34% | 6.80% | $19,304 | ||||||||||||||||

| (a) | Fair Value basis is inclusive of short-term investment in State Street Institutional U.S. Government Money Market Fund Premier Class. |

| (b) | The securities information regarding holdings, allocations and other characteristics is presented to illustrate examples of securities that the Fund has bought and the diversity of areas in which the Fund may invest as of a particular date. It may not be representative of the Fund’s current or future investments and should not be construed as a recommendation to purchase or sell a particular security. |

See Notes to Performance beginning on page 1 for further information, including an explanation of Morningstar peer categories.

Past performance does not predict future performance. The performance shown in the graphs and tables does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

5

Table of Contents

U.S. Equity Fund

| Schedule of Investments | September 30, 2015 |

| U.S. Equity Fund |

| Number of Shares | Fair Value | |||||||||

Common Stock — 95.6%† |

| |||||||||

Aerospace & Defense — 4.0% |

| |||||||||

General Dynamics Corp. | 54,493 | $ | 7,517,310 | |||||||

Hexcel Corp. | 106,662 | 4,784,857 | ||||||||

Honeywell International Inc. | 91,006 | 8,617,358 | ||||||||

The Boeing Co. | 26,002 | 3,404,962 | ||||||||

| 24,324,487 | ||||||||||

Agricultural Products — 1.1% |

| |||||||||

Archer-Daniels-Midland Co. | 159,882 | 6,627,109 | ||||||||

Air Freight & Logistics — 0.4% |

| |||||||||

United Parcel Service Inc., Class B | 24,895 | 2,456,888 | ||||||||

Airlines — 1.1% |

| |||||||||

Delta Air Lines Inc. | 156,286 | 7,012,553 | ||||||||

Apparel, Accessories & Luxury Goods — 0.1% |

| |||||||||

Coach Inc. | 11,065 | 320,110 | ||||||||

Application Software — 0.7% |

| |||||||||

Intuit Inc. | 47,024 | 4,173,380 | ||||||||

Asset Management & Custody Banks — 4.3% |

| |||||||||

Ameriprise Financial Inc. | 81,601 | 8,905,117 | ||||||||

Invesco Ltd. | 274,953 | 8,586,782 | ||||||||

State Street Corp. | 137,753 | 9,258,379 | (e) | |||||||

| 26,750,278 | ||||||||||

Auto Parts & Equipment — 0.8% |

| |||||||||

BorgWarner Inc. | 20,614 | 857,336 | ||||||||

Delphi Automotive PLC | 51,173 | 3,891,195 | ||||||||

| 4,748,531 | ||||||||||

Automobile Manufacturers — 0.6% |

| |||||||||

Ford Motor Co. | 276,613 | 3,753,638 | (h) | |||||||

Automotive Retail — 0.7% |

| |||||||||

Advance Auto Parts Inc. | 22,129 | 4,194,109 | ||||||||

Biotechnology — 5.0% |

| |||||||||

Alexion Pharmaceuticals Inc. | 30,981 | 4,845,119 | (a) | |||||||

Amgen Inc. | 112,305 | 15,534,028 | ||||||||

Gilead Sciences Inc. | 107,602 | 10,565,440 | ||||||||

| 30,944,587 | ||||||||||

Broadcasting — 0.2% |

| |||||||||

CBS Corp., Class B | 35,960 | 1,434,804 | ||||||||

| Number of Shares | Fair Value | |||||||||

Cable & Satellite — 4.3% |

| |||||||||

Comcast Corp., Class A | 195,012 | $ | 11,092,283 | |||||||

Comcast Corp., Special Class A | 110,645 | 6,333,320 | ||||||||

Liberty Global PLC, Class C | 163,202 | 6,694,546 | (a) | |||||||

Sirius XM Holdings Inc. | 553,226 | 2,069,065 | (a) | |||||||

| 26,189,214 | ||||||||||

Casinos & Gaming — 0.3% |

| |||||||||

Las Vegas Sands Corp. | 45,918 | 1,743,506 | ||||||||

Communications Equipment — 3.9% |

| |||||||||

Cisco Systems Inc. | 497,903 | 13,069,954 | ||||||||

QUALCOMM Inc. | 206,906 | 11,117,059 | ||||||||

| 24,187,013 | ||||||||||

Consumer Finance — 0.7% |

| |||||||||

Discover Financial Services | 80,218 | 4,170,534 | ||||||||

Data Processing & Outsourced Services — 1.9% |

| |||||||||

PayPal Holdings Inc. | 99,581 | 3,090,994 | (a) | |||||||

Visa Inc., Class A | 121,710 | 8,478,319 | ||||||||

| 11,569,313 | ||||||||||

Diversified Banks — 5.5% |

| |||||||||

Bank of America Corp. | 550,460 | 8,576,167 | ||||||||

Citigroup Inc. | 38,726 | 1,921,197 | ||||||||

JPMorgan Chase & Co. | 265,548 | 16,190,461 | ||||||||

Wells Fargo & Co. | 136,923 | 7,030,996 | ||||||||

| 33,718,821 | ||||||||||

Drug Retail — 1.7% |

| |||||||||

CVS Health Corp. | 107,879 | 10,408,166 | ||||||||

Electric Utilities — 0.6% |

| |||||||||

NextEra Energy Inc. | 38,726 | 3,777,721 | ||||||||

Electrical Components & Equipment — 0.5% |

| |||||||||

Rockwell Automation Inc. | 27,661 | 2,806,762 | ||||||||

Fertilizers & Agricultural Chemicals — 0.8% |

| |||||||||

Monsanto Co. | 58,089 | 4,957,315 | ||||||||

General Merchandise Stores — 2.4% |

| |||||||||

Dollar General Corp. | 103,730 | 7,514,201 | ||||||||

Target Corp. | 91,282 | 7,180,242 | ||||||||

| 14,694,443 | ||||||||||

Healthcare Distributors — 0.6% |

| |||||||||

Cardinal Health Inc. | 48,407 | 3,718,626 | ||||||||

Healthcare Equipment — 4.2% |

| |||||||||

Abbott Laboratories | 124,476 | 5,006,424 | ||||||||

Boston Scientific Corp. | 508,968 | 8,352,165 | (a) | |||||||

See Notes to Schedules of Investments and Notes to Financial Statements.

6

Table of Contents

U.S. Equity Fund

| Schedule of Investments | September 30, 2015 |

| Number of Shares | Fair Value | |||||||||

Medtronic PLC | 156,286 | $ | 10,461,785 | |||||||

Stryker Corp. | 23,789 | 2,238,545 | ||||||||

| 26,058,919 | ||||||||||

Healthcare Supplies — 0.7% |

| |||||||||

The Cooper Companies Inc. | 30,427 | 4,529,363 | ||||||||

Home Improvement Retail — 1.8% |

| |||||||||

Lowe’s Companies Inc. | 160,436 | 11,057,249 | ||||||||

Independent Power Producers & Energy Traders — 0.4% |

| |||||||||

Calpine Corp. | 96,815 | 1,413,499 | (a) | |||||||

NRG Energy Inc. | 77,452 | 1,150,162 | ||||||||

| 2,563,661 | ||||||||||

Industrial Machinery — 0.8% |

| |||||||||

Ingersoll-Rand PLC | 98,198 | 4,985,512 | ||||||||

Integrated Oil & Gas — 3.3% |

| |||||||||

Cenovus Energy Inc. | 254,484 | 3,857,977 | ||||||||

Exxon Mobil Corp. | 103,730 | 7,712,326 | ||||||||

Occidental Petroleum Corp. | 135,540 | 8,965,971 | ||||||||

| 20,536,274 | ||||||||||

Integrated Telecommunication Services — 0.5% |

| |||||||||

Verizon Communications Inc. | 77,452 | 3,369,937 | ||||||||

Internet Retail — 1.3% |

| |||||||||

Amazon.com Inc. | 16,044 | 8,212,763 | (a) | |||||||

Internet Software & Services — 5.3% |

| |||||||||

Baidu Inc. ADR | 38,173 | 5,245,352 | (a,h) | |||||||

eBay Inc. | 143,839 | 3,515,425 | (a) | |||||||

Facebook Inc., Class A | 44,258 | 3,978,794 | (a) | |||||||

Google Inc., Class A | 13,831 | 8,829,296 | (a) | |||||||

Google Inc., Class C | 13,831 | 8,415,057 | (a) | |||||||

LinkedIn Corp., Class A | 13,277 | 2,524,356 | (a) | |||||||

| 32,508,280 | ||||||||||

Investment Banking & Brokerage — 0.9% |

| |||||||||

The Charles Schwab Corp. | 199,161 | 5,688,038 | ||||||||

Life & Health Insurance — 0.5% |

| |||||||||

Lincoln National Corp. | 60,855 | 2,888,178 | ||||||||

Life Sciences Tools & Services — 0.2% |

| |||||||||

PerkinElmer Inc. | 23,512 | 1,080,612 | (h) | |||||||

Movies & Entertainment — 2.2% |

| |||||||||

The Walt Disney Co. | 53,110 | 5,427,842 | ||||||||

Time Warner Inc. | 114,794 | 7,892,088 | ||||||||

| 13,319,930 | ||||||||||

| Number of Shares | Fair Value | |||||||||

Multi-Line Insurance — 3.4% |

| |||||||||

American International Group Inc. | 192,246 | $ | 10,923,417 | |||||||

The Hartford Financial Services Group Inc. | 212,992 | 9,750,774 | ||||||||

| 20,674,191 | ||||||||||

Multi-Utilities — 0.8% |

| |||||||||

Dominion Resources Inc. | 72,473 | 5,100,650 | ||||||||

Oil & Gas Equipment & Services — 1.8% |

| |||||||||

FMC Technologies Inc. | 65,004 | 2,015,124 | (a,h) | |||||||

Schlumberger Ltd. | 128,902 | 8,890,371 | ||||||||

| 10,905,495 | ||||||||||

Oil & Gas Exploration & Production — 1.4% |

| |||||||||

Hess Corp. | 141,073 | 7,062,114 | ||||||||

Marathon Oil Corp. | 113,411 | 1,746,530 | ||||||||

| 8,808,644 | ||||||||||

Packaged Foods & Meats — 1.1% |

| |||||||||

Mondelez International Inc., Class A | 157,669 | 6,601,601 | ||||||||

Paper Packaging — 0.2% |

| |||||||||

Packaging Corporation of America | 19,363 | 1,164,878 | ||||||||

Pharmaceuticals — 7.3% |

| |||||||||

Allergan PLC | 68,600 | 18,646,166 | (a) | |||||||

Johnson & Johnson | 60,855 | 5,680,814 | (h) | |||||||

Merck & Company Inc. | 214,375 | 10,587,982 | ||||||||

Pfizer Inc. | 323,637 | 10,165,438 | ||||||||

| 45,080,400 | ||||||||||

Railroads — 0.3% |

| |||||||||

CSX Corp. | 69,153 | 1,860,216 | ||||||||

Research & Consulting Services — 1.3% |

| |||||||||

Nielsen Holdings PLC | 182,565 | 8,118,666 | ||||||||

Semiconductor Equipment — 0.8% |

| |||||||||

Applied Materials Inc. | 351,298 | 5,160,568 | ||||||||

Soft Drinks — 2.0% |

| |||||||||

PepsiCo Inc. | 129,731 | 12,233,633 | ||||||||

Specialized Finance — 2.1% |

| |||||||||

CME Group Inc. | 80,218 | 7,439,417 | ||||||||

McGraw Hill Financial Inc. | 60,855 | 5,263,958 | ||||||||

| 12,703,375 | ||||||||||

Specialized REITs — 1.9% |

| |||||||||

American Tower Corp. | 113,411 | 9,977,900 | ||||||||

Extra Space Storage Inc. | 22,129 | 1,707,473 | (h) | |||||||

| 11,685,373 | ||||||||||

See Notes to Schedules of Investments and Notes to Financial Statements.

7

Table of Contents

U.S. Equity Fund

| Schedule of Investments | September 30, 2015 |

| Number of Shares | Fair Value | |||||||||

Specialty Stores — 0.5% |

| |||||||||

Dick’s Sporting Goods Inc. | 60,855 | $ | 3,019,017 | |||||||

Systems Software — 0.6% |

| |||||||||

Oracle Corp. | 99,581 | 3,596,866 | ||||||||

Technology Hardware, Storage & Peripherals — 5.3% |

| |||||||||

Apple Inc. | 148,818 | 16,414,625 | ||||||||

EMC Corp. | 105,113 | 2,539,530 | ||||||||

Hewlett-Packard Co. | 237,887 | 6,092,286 | ||||||||

Western Digital Corp. | 94,049 | 7,471,253 | ||||||||

| 32,517,694 | ||||||||||

Trading Companies & Distributors — 0.5% |

| |||||||||

United Rentals Inc. | 55,323 | 3,322,146 | (a) | |||||||

Total Common Stock | 588,034,037 | |||||||||

Exchange Traded Funds — 1.4% |

| |||||||||

Financial Select Sector SPDR Fund | 72,629 | 1,645,773 | (m) | |||||||

Industrial Select Sector SPDR Fund | 131,838 | 6,577,398 | (m) | |||||||

Total Exchange Traded Funds | 8,223,171 | |||||||||

Total Investments in Securities | 596,257,208 | |||||||||

| Fair Value | ||||||||

Short-Term Investments — 2.9% | ||||||||

State Street Institutional U.S. Government Money Market Fund — Premier Class 0.00% | $ | 17,993,117 | (d,m) | |||||

Total Investments | 614,250,325 | |||||||

Other Assets and Liabilities, | 877,374 | |||||||

|

| |||||||

NET ASSETS — 100.0% | $ | 615,127,699 | ||||||

|

| |||||||

Other Information: | ||||||||

The Fund had the following long futures contracts open at September 30, 2015:

| Description | Expiration date | Number of Contracts | Current Notional Value | Unrealized Depreciation | |||||||||||||

S&P 500 Emini Index Futures | December 2015 | 80 | $ | 7,634,800 | $ | (201,251 | ) | ||||||||||

See Notes to Schedules of Investments and Notes to Financial Statements.

8

Table of Contents

| S&P 500 Index Fund | (Unaudited) |

SSgA Funds Management, Inc. (“SSgA FM”) is the sub-adviser to the S&P 500 Index Fund. SSgA FM is registered with the SEC as an investment adviser under the Investment Advisers Act of 1940, as amended, and is a wholly owned subsidiary of State Street Corporation (“State Street”), a publicly held bank holding company. SSgA FM, State Street and other advisory affiliates of State Street make up State Street Global Advisors (“SSgA”), the investment management arm of State Street.

SSgA FM manages portfolios using a team of investment professionals. The team approach is used to create an environment that encourages the flow of investment ideas. The portfolio managers within the team work together in a cohesive manner to develop and enhance techniques that drive the investment process for the respective investment strategy. This approach requires portfolio managers to share a variety of responsibilities including investment strategy and analysis while retaining responsibility for the implementation of the strategy within any particular portfolio. The approach also enables the team to draw upon the resources of other groups within the firm. Each portfolio management team is overseen by the SSgA FM Investment Committee. Key professionals involved in the day-to-day portfolio management for the Fund include Karl A. Schneider, CAIA and John Tucker, CFA. See portfolio managers’ biographical information beginning on page 124.

| Q. | How did the GE Institutional S&P 500 Index Fund perform compared to its benchmark and Morningstar peer group for the twelve-month period ended September 30, 2015? |

| A. | For the twelve-month period ended September 30, 2015, the GE Institutional S&P 500 Index Fund returned -0.68% for the Investment Class shares and -0.95% for the Service Class shares. The Fund’s benchmark, the S&P 500 Index returned -0.61% and the Fund’s Morningstar peer group of 1,658 U.S. Large Blend funds returned an average of -2.67% over the same period. |

| Q. | What market conditions impacted the Fund’s performance? |

| A. | After mixed performance in the beginning of the year, markets for much of July returned focus to some of the themes that dominated the first half of 2015. In a month where Canada and Sweden both cut interest |

| rates and the U.S. Federal Reserve being seen as ready to move towards a rate liftoff sometime before the end of the year, the U.S. dollar index rose to a three month high on a renewed policy divergence thematic. Commodities resumed their descent in July after some stabilization in the second quarter. A primary contributor to that decline was energy generally and crude oil specifically where total production remained at record high levels and new supply was expected to hit the market in coming months with the removal of sanctions on Iran. Both WTI and Brent Crude fell into new bear markets in July, falling 21% and 18% respectively for the month in addition to small declines in June. After the market selloff in August, expectations that the Federal Reserve would make good on the median forecast of Federal Reserve Board members and bank presidents in June that rates would increase in two increments for the remainder of the year beginning in September 2015 were brought into question. That the Federal Reserve had concerns similar to the market was highlighted by the U.S. Federal Reserve Open Market Committee statement of September 17th that cited “recent global and financial developments” that “may restrain economic activity somewhat and are likely to put further downward pressure on inflation.” These concerns prompted the Fed to abstain from a long awaited “liftoff” in interest rates at the September meeting and the cautionary language of the post meeting statement challenged expectations that the Fed would raise rates at all in the near term. |

| Q. | What were the primary drivers behind Fund performance? |

| A. | Consumer discretionary and consumer staples were the strongest contributing sectors for the reporting period. Energy and materials were the main detractors from the Fund’s performance. On a security level, Apple, Amazon.com and Home Depot were the strongest contributors to the Fund’s performance. Exxon mobile, Chevron, and IBM were the main detractors from the Fund’s performance. |

9

Table of Contents

| S&P 500 Index Fund | (Unaudited) |

Understanding Your Fund’s Expenses

As a shareholder of the Fund you incur ongoing costs. Ongoing costs include portfolio management fees, distribution and service fees (for Service Class shares), professional fees, administrative fees and other Fund expenses. The following example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

To illustrate these ongoing costs, we have provided an example and calculated the expenses paid by investors in each share class of the Fund during the period. The information in the following table is based on an investment of $1,000, which is invested at the beginning of the period and held for the entire six-month period ended September 30, 2015.

Actual Expenses

The first section of the table provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the

number given for your class under the heading “Expenses paid during the period” to estimate the expenses you paid on your account during the period.

Hypothetical Example for Comparison Purposes

The second section of the table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholders reports of other funds.

Please note that the expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect transaction costs, such as sales charges or redemption fees, if any. Therefore, the second section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds.

April 1, 2015 – September 30, 2015

| Account value at the beginning of the period ($) | Account value at the end of the period ($) | Expenses paid during the period ($)* | |||||||||||||

Actual Fund Return |

| ||||||||||||||

Investment Class | 1,000.00 | 939.50 | 0.78 | ||||||||||||

Service Class | 1,000.00 | 937.80 | 1.99 | ||||||||||||

Hypothetical 5% Return (2.5% for the period) |

| ||||||||||||||

Investment Class | 1,000.00 | 1,024.27 | 0.81 | ||||||||||||

Service Class | 1,000.00 | 1,023.01 | 2.08 | ||||||||||||

| * | Expenses are equal to the Fund’s annualized net expense ratio of 0.16% for Investment Class shares and 0.41% for Service Class shares (for the period April 1, 2015 – September 30, 2015), multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). |

10

Table of Contents

| S&P 500 Index Fund | (Unaudited) |

| Investment Profile |

A mutual fund designed for investors who seek growth of capital and accumulation of income that corresponds to the investment return of the S&P 500® Composite Stock Index (S&P 500® Index). The Fund seeks to replicate the return of the S&P 500® Index while holding transaction costs low and minimizing portfolio turnover.

| Morningstar Performance Comparison |

Based on average annual returns for periods ended September 30, 2015

One Year | Five Year | Ten Year | ||||||||||

Number of funds in peer group | 1,658 | 1,419 | 1,201 | |||||||||

Peer group average annual total return | -2.67 | % | 11.20 | % | 5.62 | % | ||||||

| Morningstar Category in peer group: Large Blend | ||||||||||||

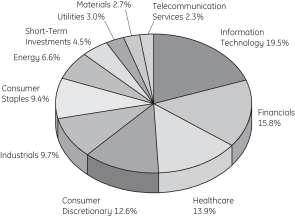

| Top Ten Largest Holdings |

as of September 30, 2015 (as a % of Fair Value) (a)(b)

Apple Inc. | 3.55% | |||

Microsoft Corp. | 2.00% | |||

Exxon Mobil Corp. | 1.74% | |||

Johnson & Johnson | 1.46% | |||

General Electric Co. | 1.44% | |||

Berkshire Hathaway Inc., Class B | 1.38% | |||

Wells Fargo & Co. | 1.36% | |||

JPMorgan Chase & Co. | 1.27% | |||

Facebook Inc., Class A | 1.15% | |||

AT&T Inc. | 1.13% |

| Sector Allocation as of September 30, 2015 |

Portfolio composition as a % of Fair Value of $26,878 (in thousands) as of September 30, 2015 (a)(b)

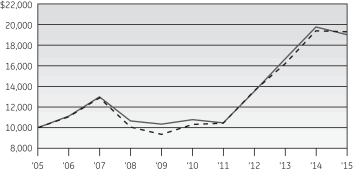

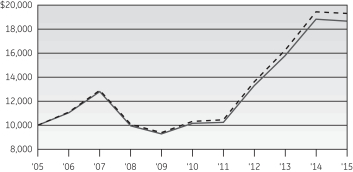

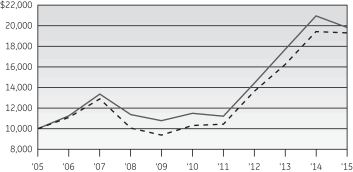

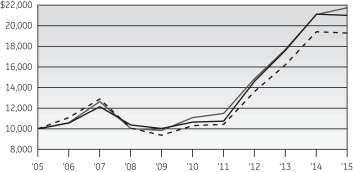

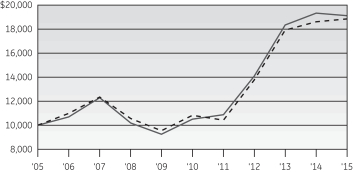

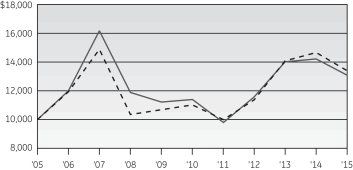

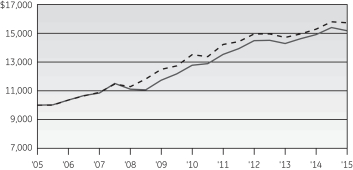

| Change in Value of a $10,000 Investment |

Investment Class Shares

| Average Annual Total Return |

for the periods ended September 30, 2015

| Investment Class Shares (Inception date: 11/25/97) | ||||||||||||||||||||

One Year | Five Year | Ten Year | Ending Value of a $10,000 Investment | |||||||||||||||||

S&P 500 Index Fund | -0.68% | 13.20% | 6.71% | $19,140 | ||||||||||||||||

S&P 500 Index | -0.61% | 13.34% | 6.80% | $19,304 | ||||||||||||||||

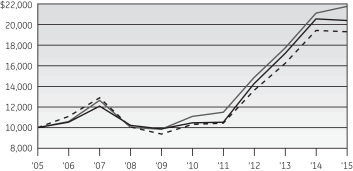

Service Class Shares

| Average Annual Total Return |

for the periods ended September 30, 2015

| Service Class Shares (Inception date: 9/30/05) | ||||||||||||||||||||

One Year | Five Year | Ten Year | Ending value of a $10,000 investment | |||||||||||||||||

S&P 500 Index Fund | -0.95% | 12.92% | 6.43% | $18,652 | ||||||||||||||||

S&P 500 Index | -0.61% | 13.34% | 6.80% | $19,304 | ||||||||||||||||

| (a) | Fair Value basis is inclusive of short-term investment in State Street Institutional U.S. Government Money Market Fund Premier Class. |

| (b) | The securities information regarding holdings, allocations and other characteristics is presented to illustrate examples of securities that the Fund has bought and the diversity of areas in which the Fund may invest as of a particular date. It may not be representative of the Fund’s current or future investments and should not be construed as a recommendation to purchase or sell a particular security. |

See Notes to Performance beginning on page 1 for further information, including an explanation of Morningstar peer categories.

Past performance does not predict future performance. The performance shown in the graphs and tables does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

11

Table of Contents

S&P 500 Index Fund

| Schedule of Investments | September 30, 2015 |

| S&P 500 Index Fund |

| Number of Shares | Fair Value | |||||||||

Common Stock — 95.1%† |

| |||||||||

Advertising — 0.1% | ||||||||||

Omnicom Group Inc. | 354 | $ | 23,328 | |||||||

The Interpublic Group of Companies Inc. | 714 | 13,659 | ||||||||

| 36,987 | ||||||||||

Aerospace & Defense — 2.6% |

| |||||||||

General Dynamics Corp. | 472 | 65,112 | ||||||||

Honeywell International Inc. | 1,187 | 112,397 | ||||||||

L-3 Communications Holdings Inc. | 119 | 12,438 | ||||||||

Lockheed Martin Corp. | 401 | 83,131 | ||||||||

Northrop Grumman Corp. | 304 | 50,449 | ||||||||

Precision Castparts Corp. | 218 | 50,077 | ||||||||

Raytheon Co. | 464 | 50,697 | ||||||||

Rockwell Collins Inc. | 233 | 19,069 | ||||||||

Textron Inc. | 386 | 14,529 | ||||||||

The Boeing Co. | 967 | 126,629 | ||||||||

United Technologies Corp. | 1,242 | 110,525 | ||||||||

| 695,053 | ||||||||||

Agricultural & Farm Machinery — 0.1% |

| |||||||||

Deere & Co. | 473 | 35,002 | ||||||||

Agricultural Products — 0.1% |

| |||||||||

Archer-Daniels-Midland Co. | 983 | 40,745 | ||||||||

Air Freight & Logistics — 0.7% |

| |||||||||

CH Robinson Worldwide Inc. | 253 | 17,148 | ||||||||

Expeditors International of Washington Inc. | 332 | 15,621 | ||||||||

FedEx Corp. | 392 | 56,440 | ||||||||

United Parcel Service Inc., Class B | 1,034 | 102,046 | ||||||||

| 191,255 | ||||||||||

Airlines — 0.6% |

| |||||||||

American Airlines Group Inc. | 1,100 | 42,713 | ||||||||

Delta Air Lines Inc. | 1,256 | 56,357 | ||||||||

Southwest Airlines Co. | 1,022 | 38,877 | ||||||||

United Continental Holdings Inc. | 600 | 31,830 | (a) | |||||||

| 169,777 | ||||||||||

Alternative Carriers — 0.1% |

| |||||||||

Level 3 Communications Inc. | 444 | 19,398 | (a) | |||||||

Aluminum — 0.1% |

| |||||||||

Alcoa Inc. | 1,893 | 18,286 | ||||||||

Apparel Retail — 0.6% |

| |||||||||

L Brands Inc. | 390 | 35,151 | ||||||||

| Number of Shares | Fair Value | |||||||||

Ross Stores Inc. | 644 | $ | 31,215 | |||||||

The Gap Inc. | 371 | 10,573 | ||||||||

The TJX Companies Inc. | 1,031 | 73,634 | ||||||||

Urban Outfitters Inc. | 218 | 6,405 | (a) | |||||||

| 156,978 | ||||||||||

Apparel, Accessories & Luxury Goods — 0.5% |

| |||||||||

Coach Inc. | 385 | 11,138 | ||||||||

Fossil Group Inc. | 75 | 4,191 | (a) | |||||||

Hanesbrands Inc. | 600 | 17,364 | ||||||||

Michael Kors Holdings Ltd. | 290 | 12,250 | (a) | |||||||

PVH Corp. | 113 | 11,519 | ||||||||

Ralph Lauren Corp. | 83 | 9,807 | ||||||||

Under Armour Inc., Class A | 253 | 24,486 | (a) | |||||||

VF Corp. | 496 | 33,832 | ||||||||

| 124,587 | ||||||||||

Application Software — 0.7% |

| |||||||||

Adobe Systems Inc. | 756 | 62,158 | (a) | |||||||

Autodesk Inc. | 320 | 14,125 | (a) | |||||||

Citrix Systems Inc. | 223 | 15,450 | (a) | |||||||

Intuit Inc. | 436 | 38,695 | ||||||||

salesforce.com Inc. | 919 | 63,806 | (a) | |||||||

| 194,234 | ||||||||||

Asset Management & Custody Banks — 1.1% |

| |||||||||

Affiliated Managers Group Inc. | 96 | 16,415 | (a) | |||||||

Ameriprise Financial Inc. | 283 | 30,884 | ||||||||

BlackRock Inc. | 191 | 56,817 | ||||||||

Franklin Resources Inc. | 560 | 20,866 | ||||||||

Invesco Ltd. | 611 | 19,081 | ||||||||

Legg Mason Inc. | 199 | 8,280 | ||||||||

Northern Trust Corp. | 313 | 21,334 | ||||||||

State Street Corp. | 637 | 42,813 | (e) | |||||||

T Rowe Price Group Inc. | 401 | 27,869 | ||||||||

The Bank of New York Mellon Corp. | 1,685 | 65,968 | ||||||||

| 310,327 | ||||||||||

Auto Parts & Equipment — 0.3% |

| |||||||||

BorgWarner Inc. | 320 | 13,309 | ||||||||

Delphi Automotive PLC | 424 | 32,241 | ||||||||

Johnson Controls Inc. | 1,002 | 41,442 | ||||||||

| 86,992 | ||||||||||

Automobile Manufacturers — 0.5% |

| |||||||||

Ford Motor Co. | 5,992 | 81,311 | ||||||||

General Motors Co. | 2,189 | 65,714 | ||||||||

| 147,025 | ||||||||||

Automotive Retail — 0.4% |

| |||||||||

Advance Auto Parts Inc. | 100 | 18,953 | ||||||||

AutoNation Inc. | 155 | 9,018 | (a) | |||||||

AutoZone Inc. | 46 | 33,296 | (a) | |||||||

CarMax Inc. | 304 | 18,033 | (a) | |||||||

O’Reilly Automotive Inc. | 145 | 36,250 | (a) | |||||||

| 115,550 | ||||||||||

See Notes to Schedules of Investments and Notes to Financial Statements.

12

Table of Contents

S&P 500 Index Fund

| Schedule of Investments | September 30, 2015 |

| Number of Shares | Fair Value | |||||||||

Biotechnology — 3.4% |

| |||||||||

AbbVie Inc. | 2,503 | $ | 136,188 | |||||||

Alexion Pharmaceuticals Inc. | 343 | 53,642 | (a) | |||||||

Amgen Inc. | 1,146 | 158,515 | ||||||||

Baxalta Inc. | 814 | 25,649 | ||||||||

Biogen Inc. | 356 | 103,884 | (a) | |||||||

Celgene Corp. | 1,204 | 130,237 | (a) | |||||||

Gilead Sciences Inc. | 2,210 | 217,000 | (h) | |||||||

Regeneron Pharmaceuticals Inc. | 113 | 52,561 | (a) | |||||||

Vertex Pharmaceuticals Inc. | 367 | 38,219 | (a) | |||||||

| 915,895 | ||||||||||

Brewers — 0.1% |

| |||||||||

Molson Coors Brewing Co., Class B | 276 | 22,914 | ||||||||

Broadcasting — 0.2% |

| |||||||||

CBS Corp., Class B | 719 | 28,688 | ||||||||

Discovery Communications Inc., Class A | 240 | 6,247 | (a) | |||||||

Discovery Communications Inc., Class C | 466 | 11,319 | (a) | |||||||

Scripps Networks Interactive Inc., Class A | 137 | 6,739 | ||||||||

TEGNA Inc. | 378 | 8,464 | ||||||||

| 61,457 | ||||||||||

Building Products — 0.1% |

| |||||||||

Allegion PLC | 177 | 10,206 | ||||||||

Masco Corp. | 491 | 12,363 | ||||||||

| 22,569 | ||||||||||

Cable & Satellite — 1.1% |

| |||||||||

Cablevision Systems Corp., Class A | 388 | 12,598 | ||||||||

Comcast Corp., Class A | 3,779 | 214,950 | (h) | |||||||

Time Warner Cable Inc. | 420 | 75,335 | ||||||||

| 302,883 | ||||||||||

Casinos & Gaming — 0.0%* |

| |||||||||

Wynn Resorts Ltd. | 113 | 6,003 | ||||||||

Coal & Consumable Fuels — 0.0%* |

| |||||||||

CONSOL Energy Inc. | 312 | 3,058 | ||||||||

Commodity Chemicals — 0.2% |

| |||||||||

LyondellBasell Industries N.V., Class A | 563 | 46,932 | ||||||||

Communications Equipment — 1.5% |

| |||||||||

Cisco Systems Inc. | 7,697 | 202,046 | (h) | |||||||

F5 Networks Inc. | 127 | 14,707 | (a) | |||||||

Harris Corp. | 194 | 14,191 | ||||||||

Juniper Networks Inc. | 528 | 13,575 | ||||||||

Motorola Solutions Inc. | 244 | 16,685 | ||||||||

QUALCOMM Inc. | 2,450 | 131,638 | ||||||||

| 392,842 | ||||||||||

| Number of Shares | Fair Value | |||||||||

Computer & Electronics Retail — 0.1% |

| |||||||||

Best Buy Company Inc. | 405 | $ | 15,033 | |||||||

GameStop Corp., Class A | 137 | 5,646 | ||||||||

| 20,679 | ||||||||||

Construction & Engineering — 0.1% |

| |||||||||

Fluor Corp. | 202 | 8,555 | ||||||||

Jacobs Engineering Group Inc. | 173 | 6,475 | (a) | |||||||

Quanta Services Inc. | 291 | 7,045 | (a) | |||||||

| 22,075 | ||||||||||

Construction Machinery & Heavy Trucks — 0.4% |

| |||||||||

Caterpillar Inc. | 906 | 59,216 | ||||||||

Cummins Inc. | 261 | 28,339 | ||||||||

Joy Global Inc. | 151 | 2,255 | ||||||||

PACCAR Inc. | 506 | 26,398 | ||||||||

| 116,208 | ||||||||||

Construction Materials — 0.1% |

| |||||||||

Martin Marietta Materials Inc. | 102 | 15,499 | ||||||||

Vulcan Materials Co. | 222 | 19,802 | ||||||||

| 35,301 | ||||||||||

Consumer Electronics — 0.1% |

| |||||||||

Garmin Ltd. | 202 | 7,248 | ||||||||

Harman International Industries Inc. | 114 | 10,943 | ||||||||

| 18,191 | ||||||||||

Consumer Finance — 0.7% |

| |||||||||

American Express Co. | 1,319 | 97,778 | ||||||||

Capital One Financial Corp. | 832 | 60,337 | ||||||||

Discover Financial Services | 694 | 36,081 | ||||||||

Navient Corp. | 564 | 6,339 | ||||||||

| 200,535 | ||||||||||

Data Processing & Outsourced Services — 2.3% |

| |||||||||

Alliance Data Systems Corp. | 91 | 23,567 | (a) | |||||||

Automatic Data Processing Inc. | 722 | 58,020 | ||||||||

Computer Sciences Corp. | 194 | 11,908 | ||||||||

Fidelity National Information Services Inc. | 404 | 27,100 | ||||||||

Fiserv Inc. | 347 | 30,054 | (a) | |||||||

Mastercard Inc., Class A | 1,516 | 136,622 | ||||||||

Paychex Inc. | 462 | 22,005 | ||||||||

PayPal Holdings Inc. | 1,677 | 52,054 | (a) | |||||||

The Western Union Co. | 906 | 16,634 | ||||||||

Total System Services Inc. | 313 | 14,220 | ||||||||

Visa Inc., Class A | 2,940 | 204,800 | ||||||||

Xerox Corp. | 1,511 | 14,702 | ||||||||

| 611,686 | ||||||||||

Department Stores — 0.2% |

| |||||||||

Kohl’s Corp. | 285 | 13,198 | ||||||||

Macy’s Inc. | 493 | 25,301 | ||||||||

Nordstrom Inc. | 245 | 17,569 | ||||||||

| 56,068 | ||||||||||

See Notes to Schedules of Investments and Notes to Financial Statements.

13

Table of Contents

S&P 500 Index Fund

| Schedule of Investments | September 30, 2015 |

| Number of Shares | Fair Value | |||||||||

Distillers & Vintners — 0.2% |

| |||||||||

Brown-Forman Corp., Class B | 160 | $ | 15,504 | |||||||

Constellation Brands Inc., Class A | 261 | 32,680 | ||||||||

| 48,184 | ||||||||||

Distributors — 0.1% |

| |||||||||

Genuine Parts Co. | 216 | 17,904 | ||||||||

Diversified Banks — 4.8% |

| |||||||||

Bank of America Corp. | 15,820 | 246,476 | (h) | |||||||

Citigroup Inc. | 4,558 | 226,122 | (h) | |||||||

Comerica Inc. | 306 | 12,577 | ||||||||

JPMorgan Chase & Co. | 5,619 | 342,590 | ||||||||

U.S. Bancorp | 2,451 | 100,515 | ||||||||

Wells Fargo & Co. | 7,093 | 364,226 | ||||||||

| 1,292,506 | ||||||||||

Diversified Chemicals — 0.6% |

| |||||||||

Eastman Chemical Co. | 258 | 16,698 | ||||||||

EI du Pont de Nemours & Co. | 1,343 | 64,733 | ||||||||

The Dow Chemical Co. | 1,759 | 74,581 | ||||||||

| 156,012 | ||||||||||

Diversified Metals & Mining — 0.1% |

| |||||||||

Freeport-McMoRan Inc. | 1,484 | 14,380 | ||||||||

Diversified Support Services — 0.0%* |

| |||||||||

Cintas Corp. | 133 | 11,405 | ||||||||

Drug Retail — 1.0% |

| |||||||||

CVS Health Corp. | 1,697 | 163,726 | (h) | |||||||

Walgreens Boots Alliance Inc. | 1,327 | 110,274 | ||||||||

| 274,000 | ||||||||||

Electric Utilities — 1.7% |

| |||||||||

American Electric Power Company Inc. | 748 | 42,531 | ||||||||

Duke Energy Corp. | 1,057 | 76,041 | ||||||||

Edison International | 465 | 29,328 | ||||||||

Entergy Corp. | 254 | 16,535 | ||||||||

Eversource Energy | 449 | 22,728 | ||||||||

Exelon Corp. | 1,314 | 39,026 | ||||||||

FirstEnergy Corp. | 594 | 18,598 | ||||||||

NextEra Energy Inc. | 699 | 68,187 | ||||||||

Pepco Holdings Inc. | 476 | 11,529 | ||||||||

Pinnacle West Capital Corp. | 149 | 9,557 | ||||||||

PPL Corp. | 1,023 | 33,647 | ||||||||

The Southern Co. | 1,349 | 60,300 | ||||||||

Xcel Energy Inc. | 718 | 25,424 | ||||||||

| 453,431 | ||||||||||

Electrical Components & Equipment — 0.4% |

| |||||||||

AMETEK Inc. | 345 | 18,051 | ||||||||

Eaton Corporation PLC | 724 | 37,141 | ||||||||

Emerson Electric Co. | 1,041 | 45,981 | ||||||||

| Number of Shares | Fair Value | |||||||||

Rockwell Automation Inc. | 192 | $ | 19,482 | |||||||

| 120,655 | ||||||||||

Electronic Components — 0.2% |

| |||||||||

Amphenol Corp., Class A | 439 | 22,371 | ||||||||

Corning Inc. | 1,957 | 33,504 | ||||||||

| 55,875 | ||||||||||

Electronic Equipment & Instruments — 0.0%* |

| |||||||||

FLIR Systems Inc. | 308 | 8,621 | ||||||||

Electronic Manufacturing Services — 0.1% |

| |||||||||

TE Connectivity Ltd. | 621 | 37,192 | ||||||||

Environmental & Facilities Services — 0.2% |

| |||||||||

Republic Services Inc. | 350 | 14,420 | ||||||||

Stericycle Inc. | 146 | 20,339 | (a) | |||||||

Waste Management Inc. | 609 | 30,335 | ||||||||

| 65,094 | ||||||||||

Fertilizers & Agricultural Chemicals — 0.4% |

| |||||||||

CF Industries Holdings Inc. | 350 | 15,715 | ||||||||

FMC Corp. | 223 | 7,562 | ||||||||

Monsanto Co. | 723 | 61,701 | ||||||||

The Mosaic Co. | 447 | 13,906 | ||||||||

| 98,884 | ||||||||||

Food Distributors — 0.1% |

| |||||||||

Sysco Corp. | 909 | 35,424 | ||||||||

Food Retail — 0.3% |

| |||||||||

The Kroger Co. | 1,474 | 53,167 | ||||||||

Whole Foods Market Inc. | 513 | 16,237 | ||||||||

| 69,404 | ||||||||||

Footwear — 0.5% |

| |||||||||

NIKE Inc., Class B | 1,035 | 127,274 | ||||||||

Gas Utilities — 0.0%* |

| |||||||||

AGL Resources Inc. | 197 | 12,025 | ||||||||

General Merchandise Stores — 0.5% |

| |||||||||

Dollar General Corp. | 466 | 33,757 | ||||||||

Dollar Tree Inc. | 323 | 21,531 | (a) | |||||||

Target Corp. | 948 | 74,570 | ||||||||

| 129,858 | ||||||||||

Gold — 0.0%* | ||||||||||

Newmont Mining Corp. | 700 | 11,249 | ||||||||

Health Care REITs — 0.3% | ||||||||||

HCP Inc. | 654 | 24,362 | ||||||||

Ventas Inc. | 508 | 28,478 | ||||||||

Welltower Inc. | 528 | 35,756 | ||||||||

| 88,596 | ||||||||||

See Notes to Schedules of Investments and Notes to Financial Statements.

14

Table of Contents

S&P 500 Index Fund

| Schedule of Investments | September 30, 2015 |

| Number of Shares | Fair Value | |||||||||

Healthcare Distributors — 0.6% |

| |||||||||

AmerisourceBergen Corp. | 320 | $ | 30,397 | |||||||

Cardinal Health Inc. | 505 | 38,794 | ||||||||

Henry Schein Inc. | 131 | 17,386 | (a) | |||||||

McKesson Corp. | 345 | 63,836 | ||||||||

Patterson Companies Inc. | 145 | 6,271 | ||||||||

| 156,684 | ||||||||||

Healthcare Equipment — 1.9% |

| |||||||||

Abbott Laboratories | 2,233 | 89,811 | ||||||||

Baxter International Inc. | 814 | 26,740 | ||||||||

Becton Dickinson and Co. | 303 | 40,196 | ||||||||

Boston Scientific Corp. | 2,038 | 33,443 | (a) | |||||||

CR Bard Inc. | 112 | 20,867 | ||||||||

Edwards Lifesciences Corp. | 151 | 21,468 | (a) | |||||||

Intuitive Surgical Inc. | 52 | 23,898 | (a) | |||||||

Medtronic PLC | 2,136 | 142,984 | ||||||||

St Jude Medical Inc. | 407 | 25,677 | ||||||||

Stryker Corp. | 457 | 43,004 | ||||||||

Varian Medical Systems Inc. | 138 | 10,182 | (a) | |||||||

Zimmer Biomet Holdings Inc. | 241 | 22,637 | ||||||||

| 500,907 | ||||||||||

Healthcare Facilities — 0.2% |

| |||||||||

HCA Holdings Inc. | 486 | 37,597 | (a) | |||||||

Tenet Healthcare Corp. | 149 | 5,501 | (a) | |||||||

Universal Health Services Inc., Class B | 126 | 15,726 | ||||||||

| 58,824 | ||||||||||

Healthcare Services — 0.5% |

| |||||||||

DaVita Healthcare Partners Inc. | 298 | 21,554 | (a) | |||||||

Express Scripts Holding Co. | 1,026 | 83,065 | (a) | |||||||

Laboratory Corporation of America Holdings | 144 | 15,620 | (a) | |||||||

Quest Diagnostics Inc. | 246 | 15,122 | ||||||||

| 135,361 | ||||||||||

Healthcare Supplies — 0.0%* |

| |||||||||

DENTSPLY International Inc. | 259 | 13,098 | ||||||||

Healthcare Technology — 0.1% |

| |||||||||

Cerner Corp. | 434 | 26,023 | (a) | |||||||

Home Building — 0.1% |

| |||||||||

DR Horton Inc. | 456 | 13,388 | ||||||||

Lennar Corp., Class A | 301 | 14,487 | ||||||||

PulteGroup Inc. | 453 | 8,548 | ||||||||

| 36,423 | ||||||||||

Home Entertainment Software — 0.2% |

| |||||||||

Activision Blizzard Inc. | 800 | 24,712 | ||||||||

Electronic Arts Inc. | 442 | 29,945 | (a) | |||||||

| 54,657 | ||||||||||

Home Furnishing Retail — 0.1% |

| |||||||||

Bed Bath & Beyond Inc. | 260 | 14,825 | (a) | |||||||

| Number of Shares | Fair Value | |||||||||

Home Furnishings — 0.1% |

| |||||||||

Leggett & Platt Inc. | 265 | $ | 10,931 | |||||||

Mohawk Industries Inc. | 106 | 19,270 | (a) | |||||||

| 30,201 | ||||||||||

Home Improvement Retail — 1.2% |

| |||||||||

Lowe’s Companies Inc. | 1,443 | 99,452 | ||||||||

The Home Depot Inc. | 1,953 | 225,552 | ||||||||

| 325,004 | ||||||||||

Hotel & Resort REITs — 0.1% |

| |||||||||

Host Hotels & Resorts Inc. | 1,071 | 16,933 | ||||||||

Hotels, Resorts & Cruise Lines — 0.4% |

| |||||||||

Carnival Corp. | 703 | 34,939 | ||||||||

Marriott International Inc., Class A | 302 | 20,596 | ||||||||

Royal Caribbean Cruises Ltd. | 234 | 20,847 | ||||||||

Starwood Hotels & Resorts Worldwide Inc. | 251 | 16,687 | ||||||||

Wyndham Worldwide Corp. | 216 | 15,530 | ||||||||

| 108,599 | ||||||||||

Household Appliances — 0.1% |

| |||||||||

Whirlpool Corp. | 110 | 16,199 | ||||||||

Household Products — 1.7% |

| |||||||||

Colgate-Palmolive Co. | 1,367 | 86,750 | ||||||||

Kimberly-Clark Corp. | 559 | 60,953 | ||||||||

The Clorox Co. | 182 | 21,026 | ||||||||

The Procter & Gamble Co. | 4,120 | 296,393 | ||||||||

| 465,122 | ||||||||||

Housewares & Specialties — 0.1% |

| |||||||||

Newell Rubbermaid Inc. | 377 | 14,971 | ||||||||

Human Resource & Employment Services — 0.0%* |

| |||||||||

Robert Half International Inc. | 186 | 9,516 | ||||||||

Hypermarkets & Super Centers — 0.9% |

| |||||||||

Costco Wholesale Corp. | 650 | 93,970 | ||||||||

Wal-Mart Stores Inc. | 2,378 | 154,190 | ||||||||

| 248,160 | ||||||||||

Independent Power Producers & Energy Traders — 0.1% |

| |||||||||

AES Corp. | 1,134 | 11,102 | ||||||||

NRG Energy Inc. | 462 | 6,861 | ||||||||

| 17,963 | ||||||||||

Industrial Conglomerates — 2.3% |

| |||||||||

3M Co. | 966 | 136,950 | ||||||||

Danaher Corp. | 914 | 77,882 | ||||||||

General Electric Co. | 15,333 | 386,698 | (h,k) | |||||||

Roper Technologies Inc. | 142 | 22,251 | ||||||||

| 623,781 | ||||||||||

See Notes to Schedules of Investments and Notes to Financial Statements.

15

Table of Contents

S&P 500 Index Fund

| Schedule of Investments | September 30, 2015 |

| Number of Shares | Fair Value | |||||||||

Industrial Gases — 0.3% |

| |||||||||

Air Products & Chemicals Inc. | 294 | $ | 37,509 | |||||||

Airgas Inc. | 92 | 8,218 | ||||||||

Praxair Inc. | 437 | 44,513 | ||||||||

| 90,240 | ||||||||||

Industrial Machinery — 0.6% |

| |||||||||

Dover Corp. | 231 | 13,209 | ||||||||

Flowserve Corp. | 229 | 9,421 | ||||||||

Illinois Tool Works Inc. | 540 | 44,447 | ||||||||

Ingersoll-Rand PLC | 377 | 19,140 | ||||||||

Parker-Hannifin Corp. | 211 | 20,530 | ||||||||

Pentair PLC | 262 | 13,373 | ||||||||

Snap-on Inc. | 98 | 14,792 | ||||||||

Stanley Black & Decker Inc. | 221 | 21,433 | ||||||||

Xylem Inc. | 244 | 8,015 | ||||||||

| 164,360 | ||||||||||

Industrial REITs — 0.1% |

| |||||||||

Prologis Inc. | 788 | 30,653 | ||||||||

Insurance Brokers — 0.3% |

| |||||||||

Aon PLC | 436 | 38,634 | ||||||||

Marsh & McLennan Companies Inc. | 815 | 42,559 | ||||||||

| 81,193 | ||||||||||

Integrated Oil & Gas — 2.9% |

| |||||||||

Chevron Corp. | 2,843 | 224,256 | (h) | |||||||

Exxon Mobil Corp. | 6,307 | 468,925 | (h) | |||||||

Occidental Petroleum Corp. | 1,152 | 76,205 | ||||||||

| 769,386 | ||||||||||

Integrated Telecommunication Services — 2.2% |

| |||||||||

AT&T Inc. | 9,342 | 304,362 | (h) | |||||||

CenturyLink Inc. | 815 | 20,473 | ||||||||

Frontier Communications Corp. | 1,366 | 6,489 | ||||||||

Verizon Communications Inc. | 6,132 | 266,803 | ||||||||

| 598,127 | ||||||||||

Internet Retail — 1.8% |

| |||||||||

Amazon.com Inc. | 582 | 297,920 | (a) | |||||||

Expedia Inc. | 168 | 19,770 | ||||||||

Netflix Inc. | 644 | 66,500 | (a) | |||||||

The Priceline Group Inc. | 78 | 96,475 | (a) | |||||||

TripAdvisor Inc. | 154 | 9,705 | (a) | |||||||

| 490,370 | ||||||||||

Internet Software & Services — 3.6% |

| |||||||||

Akamai Technologies Inc. | 249 | 17,196 | (a) | |||||||

eBay Inc. | 1,677 | 40,986 | (a,h) | |||||||

Facebook Inc., Class A | 3,432 | 308,537 | (a,h) | |||||||

Google Inc., Class A | 440 | 280,883 | (a) | |||||||

Google Inc., Class C | 445 | 270,747 | (a) | |||||||

VeriSign Inc. | 147 | 10,372 | (a) | |||||||

Yahoo! Inc. | 1,322 | 38,219 | (a) | |||||||

| 966,940 | ||||||||||

| Number of Shares | Fair Value | |||||||||

Investment Banking & Brokerage — 0.9% |

| |||||||||

E*TRADE Financial Corp. | 511 | $ | 13,455 | (a) | ||||||

Morgan Stanley | 2,336 | 73,584 | ||||||||

The Charles Schwab Corp. | 1,726 | 49,294 | ||||||||

The Goldman Sachs Group Inc. | 612 | 106,341 | ||||||||

| 242,674 | ||||||||||

IT Consulting & Other Services — 1.3% |

| |||||||||

Accenture PLC, Class A | 937 | 92,070 | ||||||||

Cognizant Technology Solutions Corp., Class A | 914 | 57,226 | (a) | |||||||

International Business Machines Corp. | 1,385 | 200,783 | ||||||||

Teradata Corp. | 266 | 7,703 | (a) | |||||||

| 357,782 | ||||||||||

Leisure Products — 0.1% |

| |||||||||

Hasbro Inc. | 153 | 11,037 | ||||||||

Mattel Inc. | 581 | 12,236 | ||||||||

| 23,273 | ||||||||||

Life & Health Insurance — 0.9% |

| |||||||||

Aflac Inc. | 689 | 40,052 | ||||||||

Lincoln National Corp. | 367 | 17,418 | ||||||||

MetLife Inc. | 1,687 | 79,542 | ||||||||

Principal Financial Group Inc. | 384 | 18,178 | ||||||||

Prudential Financial Inc. | 687 | 52,356 | ||||||||

Torchmark Corp. | 190 | 10,716 | ||||||||

Unum Group | 432 | 13,859 | ||||||||

| 232,121 | ||||||||||

Life Sciences Tools & Services — 0.4% |

| |||||||||

Agilent Technologies Inc. | 469 | 16,101 | ||||||||

PerkinElmer Inc. | 148 | 6,802 | ||||||||

Thermo Fisher Scientific Inc. | 598 | 73,123 | ||||||||

Waters Corp. | 115 | 13,594 | (a) | |||||||

| 109,620 | ||||||||||

Managed Healthcare — 1.4% |

| |||||||||

Aetna Inc. | 528 | 57,769 | ||||||||

Anthem Inc. | 405 | 56,700 | ||||||||

Cigna Corp. | 399 | 53,873 | ||||||||

Humana Inc. | 235 | 42,065 | ||||||||

UnitedHealth Group Inc. | �� | 1,446 | 167,750 | |||||||

| 378,157 | ||||||||||

Metal & Glass Containers — 0.1% |

| |||||||||

Ball Corp. | 236 | 14,679 | ||||||||

Owens-Illinois Inc. | 210 | 4,351 | (a) | |||||||

| 19,030 | ||||||||||

Motorcycle Manufacturers — 0.1% |

| |||||||||

Harley-Davidson Inc. | 301 | 16,525 | ||||||||

See Notes to Schedules of Investments and Notes to Financial Statements.

16

Table of Contents

S&P 500 Index Fund

| Schedule of Investments | September 30, 2015 |

| Number of Shares | Fair Value | |||||||||

Movies & Entertainment — 1.6% |

| |||||||||

The Walt Disney Co. | 2,347 | $ | 239,863 | |||||||

Time Warner Inc. | 1,243 | 85,456 | ||||||||

Twenty-First Century Fox Inc., Class A | 2,552 | 68,853 | ||||||||

Twenty-First Century Fox Inc., Class B | 100 | 2,707 | ||||||||

Viacom Inc., Class B | 566 | 24,423 | ||||||||

| 421,302 | ||||||||||

Multi-Line Insurance — 0.6% |

| |||||||||

American International Group Inc. | 2,005 | 113,924 | ||||||||

Assurant Inc. | 102 | 8,059 | ||||||||

Genworth Financial Inc., Class A | 912 | 4,214 | (a) | |||||||

Loews Corp. | 528 | 19,082 | ||||||||

The Hartford Financial Services Group Inc. | 612 | 28,017 | ||||||||

| 173,296 | ||||||||||

Multi-Sector Holdings — 1.4% |

| |||||||||

Berkshire Hathaway Inc., Class B | 2,845 | 370,988 | (a,h) | |||||||

Leucadia National Corp. | 430 | 8,712 | ||||||||

| 379,700 | ||||||||||

Multi-Utilities — 1.1% |

| |||||||||

Ameren Corp. | 336 | 14,203 | ||||||||

CenterPoint Energy Inc. | 737 | 13,295 | ||||||||

CMS Energy Corp. | 380 | 13,422 | ||||||||

Consolidated Edison Inc. | 416 | 27,810 | ||||||||

Dominion Resources Inc. | 875 | 61,582 | ||||||||

DTE Energy Co. | 249 | 20,012 | ||||||||

NiSource Inc. | 547 | 10,147 | ||||||||

PG&E Corp. | 728 | 38,438 | ||||||||

Public Service Enterprise Group Inc. | 722 | 30,439 | ||||||||

SCANA Corp. | 195 | 10,971 | ||||||||

Sempra Energy | 354 | 34,239 | ||||||||

TECO Energy Inc. | 302 | 7,931 | ||||||||

WEC Energy Group Inc. | 535 | 27,938 | ||||||||

| 310,427 | ||||||||||

Office REITs — 0.2% |

| |||||||||

Boston Properties Inc. | 218 | 25,811 | ||||||||

SL Green Realty Corp. | 154 | 16,657 | ||||||||

Vornado Realty Trust | 248 | 22,424 | ||||||||

| 64,892 | ||||||||||

Office Services & Supplies — 0.0%* |

| |||||||||

Pitney Bowes Inc. | 320 | 6,352 | ||||||||

Oil & Gas Drilling — 0.1% |

| |||||||||

Diamond Offshore Drilling Inc. | 177 | 3,062 | ||||||||

Ensco PLC, Class A | 467 | 6,575 | ||||||||

Helmerich & Payne Inc. | 146 | 6,900 | ||||||||

Transocean Ltd. | 700 | 9,044 | ||||||||

| 25,581 | ||||||||||

| Number of Shares | Fair Value | |||||||||

Oil & Gas Equipment & Services — 1.0% |

| |||||||||

Baker Hughes Inc. | 663 | $ | 34,502 | |||||||

Cameron International Corp. | 272 | 16,679 | (a) | |||||||

FMC Technologies Inc. | 322 | 9,982 | (a) | |||||||

Halliburton Co. | 1,273 | 45,001 | ||||||||

National Oilwell Varco Inc. | 616 | 23,192 | ||||||||

Schlumberger Ltd. | 1,940 | 133,802 | ||||||||

| 263,158 | ||||||||||

Oil & Gas Exploration & Production — 1.5% |

| |||||||||

Anadarko Petroleum Corp. | 760 | 45,897 | ||||||||

Apache Corp. | 539 | 21,107 | ||||||||

Cabot Oil & Gas Corp. | 577 | 12,613 | ||||||||

Chesapeake Energy Corp. | 713 | 5,226 | ||||||||

Cimarex Energy Co. | 148 | 15,167 | ||||||||

ConocoPhillips | 1,825 | 87,527 | ||||||||

Devon Energy Corp. | 592 | 21,957 | ||||||||

EOG Resources Inc. | 820 | 59,696 | ||||||||

EQT Corp. | 264 | 17,099 | ||||||||

Hess Corp. | 362 | 18,122 | ||||||||

Marathon Oil Corp. | 960 | 14,784 | ||||||||

Murphy Oil Corp. | 282 | 6,825 | ||||||||

Newfield Exploration Co. | 338 | 11,120 | (a) | |||||||

Noble Energy Inc. | 632 | 19,074 | ||||||||

Pioneer Natural Resources Co. | 213 | 25,909 | ||||||||

Range Resources Corp. | 231 | 7,420 | ||||||||

Southwestern Energy Co. | 525 | 6,662 | (a) | |||||||

| 396,205 | ||||||||||

Oil & Gas Refining & Marketing — 0.6% |

| |||||||||

Marathon Petroleum Corp. | 858 | 39,751 | ||||||||

Phillips 66 | 730 | 56,093 | ||||||||

Tesoro Corp. | 176 | 17,114 | ||||||||

Valero Energy Corp. | 796 | 47,840 | ||||||||

| 160,798 | ||||||||||

Oil & Gas Storage & Transportation — 0.6% |

| |||||||||

Columbia Pipeline Group Inc. | 547 | 10,005 | ||||||||

Kinder Morgan Inc. | 2,730 | 75,566 | ||||||||

ONEOK Inc. | 358 | 11,528 | ||||||||

Spectra Energy Corp. | 960 | 25,219 | ||||||||

The Williams Companies Inc. | 1,026 | 37,808 | ||||||||

| 160,126 | ||||||||||

Packaged Foods & Meats — 1.5% |

| |||||||||

Campbell Soup Co. | 245 | 12,417 | ||||||||

ConAgra Foods Inc. | 599 | 24,265 | ||||||||

General Mills Inc. | 921 | 51,696 | ||||||||

Hormel Foods Corp. | 203 | 12,852 | ||||||||

Kellogg Co. | 357 | 23,758 | ||||||||

Keurig Green Mountain Inc. | 172 | 8,968 | ||||||||

McCormick & Company Inc. | 178 | 14,628 | ||||||||

Mead Johnson Nutrition Co. | 288 | 20,275 | ||||||||

Mondelez International Inc., Class A | 2,495 | 104,466 | ||||||||

The Hershey Co. | 209 | 19,203 | ||||||||

See Notes to Schedules of Investments and Notes to Financial Statements.

17

Table of Contents

S&P 500 Index Fund

| Schedule of Investments | September 30, 2015 |

| Number of Shares | Fair Value | |||||||||

The JM Smucker Co. | 146 | $ | 16,657 | |||||||

The Kraft Heinz Co. | 884 | 62,393 | ||||||||

Tyson Foods Inc., Class A | 507 | 21,852 | ||||||||

| 393,430 | ||||||||||

Paper Packaging — 0.2% |

| |||||||||

Avery Dennison Corp. | 170 | 9,617 | ||||||||

Sealed Air Corp. | 292 | 13,689 | ||||||||

WestRock Co. | 398 | 20,473 | ||||||||

| 43,779 | ||||||||||

Paper Products — 0.1% |

| |||||||||

International Paper Co. | 606 | 22,901 | ||||||||

Personal Products — 0.1% |

| |||||||||

The Estee Lauder Companies Inc., Class A | 318 | 25,656 | ||||||||

Pharmaceuticals — 5.4% |

| |||||||||

Allergan PLC | 589 | 160,096 | (a) | |||||||

Bristol-Myers Squibb Co. | 2,499 | 147,941 | ||||||||

Eli Lilly & Co. | 1,454 | 121,685 | ||||||||

Endo International PLC | 316 | 21,893 | (a) | |||||||

Johnson & Johnson | 4,205 | 392,537 | (h) | |||||||

Mallinckrodt PLC | 164 | 10,486 | (a) | |||||||

Merck & Company Inc. | 4,289 | 211,834 | ||||||||

Mylan N.V. | 621 | 25,001 | (a) | |||||||

Perrigo Company PLC | 216 | 33,970 | ||||||||

Pfizer Inc. | 9,366 | 294,186 | ||||||||

Zoetis Inc. | 769 | 31,667 | ||||||||

| 1,451,296 | ||||||||||

Property & Casualty Insurance — 0.9% |

| |||||||||

ACE Ltd. | 498 | 51,493 | ||||||||

Cincinnati Financial Corp. | 200 | 10,760 | ||||||||

The Allstate Corp. | 641 | 37,332 | ||||||||

The Chubb Corp. | 338 | 41,456 | ||||||||

The Progressive Corp. | 890 | 27,270 | ||||||||

The Travelers Companies Inc. | 498 | 49,566 | ||||||||

XL Group PLC | 473 | 17,179 | ||||||||

| 235,056 | ||||||||||

Publishing — 0.0%* |

| |||||||||

News Corp., Class A | 684 | 8,632 | ||||||||

Railroads — 0.8% |

| |||||||||

CSX Corp. | 1,496 | 40,242 | ||||||||

Kansas City Southern | 155 | 14,086 | ||||||||

Norfolk Southern Corp. | 465 | 35,526 | ||||||||

Union Pacific Corp. | 1,340 | 118,470 | ||||||||

| 208,324 | ||||||||||

Real Estate Services — 0.0%* |

| |||||||||

CBRE Group Inc., Class A | 386 | 12,352 | (a) | |||||||

| Number of Shares | Fair Value | |||||||||

Regional Banks — 0.9% | ||||||||||

BB&T Corp. | 1,184 | $ | 42,150 | |||||||

Fifth Third Bancorp | 1,166 | 22,049 | ||||||||

Huntington Bancshares Inc. | 1,382 | 14,649 | ||||||||

KeyCorp | 1,212 | 15,768 | ||||||||

M&T Bank Corp. | 187 | 22,805 | ||||||||

People’s United Financial Inc. | 561 | 8,825 | ||||||||

Regions Financial Corp. | 1,932 | 17,407 | ||||||||

SunTrust Banks Inc. | 805 | 30,783 | ||||||||

The PNC Financial Services Group Inc. | 783 | 69,844 | ||||||||

Zions Bancorporation | 266 | 7,326 | ||||||||

| 251,606 | ||||||||||

Research & Consulting Services — 0.2% |

| |||||||||

Equifax Inc. | 168 | 16,326 | ||||||||

Nielsen Holdings PLC | 574 | 25,526 | ||||||||

The Dun & Bradstreet Corp. | 47 | 4,935 | ||||||||

| 46,787 | ||||||||||

Residential REITs — 0.4% |

| |||||||||

Apartment Investment & Management Co., Class A | 235 | 8,700 | ||||||||

AvalonBay Communities Inc. | 189 | 33,041 | ||||||||

Equity Residential | 547 | 41,091 | ||||||||

Essex Property Trust Inc. | 110 | 24,576 | ||||||||

| 107,408 | ||||||||||

Restaurants — 1.4% |

| |||||||||

Chipotle Mexican Grill Inc. | 47 | 33,852 | (a) | |||||||

Darden Restaurants Inc. | 169 | 11,583 | ||||||||

McDonald’s Corp. | 1,468 | 144,642 | ||||||||

Starbucks Corp. | 2,268 | 128,913 | ||||||||

Yum! Brands Inc. | 658 | 52,607 | ||||||||

| 371,597 | ||||||||||

Retail REITs — 0.6% |

| |||||||||

General Growth Properties Inc. | 891 | 23,139 | ||||||||

Kimco Realty Corp. | 706 | 17,247 | ||||||||

Realty Income Corp. | 357 | 16,918 | ||||||||

Simon Property Group Inc. | 462 | 84,879 | ||||||||

The Macerich Co. | 196 | 15,057 | ||||||||

| 157,240 | ||||||||||

Security & Alarm Services — 0.1% |

| |||||||||

The ADT Corp. | 235 | 7,027 | ||||||||

Tyco International PLC | 594 | 19,875 | ||||||||

| 26,902 | ||||||||||

Semiconductor Equipment — 0.2% |

| |||||||||

Applied Materials Inc. | 1,861 | 27,338 | ||||||||

KLA-Tencor Corp. | 285 | 14,250 | ||||||||

Lam Research Corp. | 223 | 14,569 | ||||||||

| 56,157 | ||||||||||

See Notes to Schedules of Investments and Notes to Financial Statements.

18

Table of Contents

S&P 500 Index Fund

| Schedule of Investments | September 30, 2015 |

| Number of Shares | Fair Value | |||||||||

Semiconductors — 2.1% |

| |||||||||

Altera Corp. | 424 | $ | 21,234 | |||||||

Analog Devices Inc. | 479 | 27,020 | ||||||||

Avago Technologies Ltd. | 381 | 47,629 | ||||||||

Broadcom Corp., Class A | 832 | 42,790 | ||||||||

First Solar Inc. | 139 | 5,942 | (a) | |||||||

Intel Corp. | 7,220 | 217,611 | ||||||||

Linear Technology Corp. | 333 | 13,437 | ||||||||

Microchip Technology Inc. | 341 | 14,694 | ||||||||

Micron Technology Inc. | 1,639 | 24,552 | (a) | |||||||

NVIDIA Corp. | 720 | 17,748 | ||||||||

Qorvo Inc. | 200 | 9,010 | (a) | |||||||

Skyworks Solutions Inc. | 300 | 25,263 | ||||||||

Texas Instruments Inc. | 1,577 | 78,093 | ||||||||

Xilinx Inc. | 368 | 15,603 | ||||||||

| 560,626 | ||||||||||

Soft Drinks — 1.9% |

| |||||||||

Coca-Cola Enterprises Inc. | 322 | 15,569 | ||||||||

Dr Pepper Snapple Group Inc. | 274 | 21,660 | ||||||||

Monster Beverage Corp. | 225 | 30,406 | (a) | |||||||

PepsiCo Inc. | 2,219 | 209,251 | ||||||||

The Coca-Cola Co. | 5,932 | 237,992 | ||||||||

| 514,878 | ||||||||||

Specialized Consumer Services — 0.1% |

| |||||||||

H&R Block Inc. | 469 | 16,978 | ||||||||

Specialized Finance — 0.6% | ||||||||||

CME Group Inc. | 513 | 47,576 | ||||||||

Intercontinental Exchange Inc. | 173 | 40,653 | ||||||||

McGraw Hill Financial Inc. | 415 | 35,898 | ||||||||

Moody’s Corp. | 261 | 25,630 | ||||||||

Nasdaq Inc. | 156 | 8,319 | ||||||||

| 158,076 | ||||||||||

Specialized REITs — 0.8% |

| |||||||||

American Tower Corp. | 630 | 55,427 | ||||||||

Crown Castle International Corp. | 510 | 40,224 | ||||||||

Equinix Inc. | 86 | 23,512 | ||||||||

Iron Mountain Inc. | 251 | 7,786 | ||||||||

Plum Creek Timber Company Inc. | 297 | 11,735 | ||||||||

Public Storage | 222 | 46,982 | ||||||||

Weyerhaeuser Co. | 745 | 20,368 | ||||||||

| 206,034 | ||||||||||

Specialty Chemicals — 0.5% |

| |||||||||

Ecolab Inc. | 412 | 45,205 | ||||||||

International Flavors & Fragrances Inc. | 112 | 11,565 | ||||||||

PPG Industries Inc. | 418 | 36,654 | ||||||||

Sigma-Aldrich Corp. | 169 | 23,478 | ||||||||

The Sherwin-Williams Co. | 117 | 26,065 | ||||||||

| 142,967 | ||||||||||

| Number of Shares | Fair Value | |||||||||

Specialty Stores — 0.2% |

| |||||||||

Signet Jewelers Ltd. | 121 | $ | 16,472 | |||||||