UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

FORM 10-K

(Mark One)

[X] Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended May 31, 2018

or

[ ] Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from ________________ to ________________

Commission file number: 000-22893.

AEHR TEST SYSTEMS

(Exact name of registrant as specified in its charter)

| CALIFORNIA | 94-2424084 |

| (State or other jurisdiction of | (IRS Employer Identification Number) |

| incorporation or organization) | |

| | |

| 400 KATO TERRACE, FREMONT, CA | 94539 |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (510) 623-9400

Securities registered pursuant to Section 12(b) of the Act:

Common Stock, $0.01 par value

Name of each exchange on which registered: The NASDAQ Capital Market

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act (Check one):

| Large accelerated filer [ ] | Accelerated filer [ ] |

| | |

| Non-accelerated filer [ ] | Smaller reporting company [X] |

| (Do not check if a smaller reporting company) | |

| | |

| Emerging growth company [ ] | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes [ ] No [X]

The aggregate market value of the registrant’s common stock, par value $0.01 per share, held by non-affiliates of the registrant, based upon the closing price of $2.55 on November 30, 2017, as reported on the NASDAQ Capital Market, was $48,946,434. For purposes of this disclosure, shares of common stock held by persons who hold more than 5% of the outstanding shares of common stock (other than such persons of whom the Registrant became aware only through the filing of a Schedule 13G filed with the Securities and Exchange Commission) and shares held by officers and directors of the Registrant have been excluded because such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily conclusive for other purposes.

The number of shares of registrant’s common stock, par value $0.01 per share, outstanding at July 31, 2018 was 22,220,019.

AEHR TEST SYSTEMS

FORM 10-K

FISCAL YEAR ENDED MAY 31, 2018

TABLE OF CONTENTS

PART I

| Item 1. Business | 4 |

| Item 1A. Risk Factors | 9 |

| Item 1B. Unresolved Staff Comments | 16 |

| Item 2. Properties | 16 |

| Item 3. Legal Proceedings | 16 |

| Item 4. Mine Safety Disclosures | 16 |

| | |

| | |

| PART II |

| | |

| Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 17 |

| Item 6. Selected Consolidated Financial Data | 18 |

| Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations | 20

|

| Item 7A. Quantitative and Qualitative Disclosures about Market Risk | 26 |

| Item 8. Financial Statements and Supplementary Data | 27 |

| Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 54 |

| Item 9A. Controls and Procedures | 54 |

| Item 9B. Other Information | 54 |

| | |

| | |

| PART III |

| | |

| Item 10. Directors, Executive Officers and Corporate Governance | 55 |

| Item 11. Executive Compensation | 55 |

| Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 55 |

| Item 13. Certain Relationships and Related Transactions | 55 |

| Item 14. Principal Accountant Fees and Services | 55 |

| | |

| | |

| PART IV |

| | |

| Item 15. Exhibits, Financial Statement Schedules | 56 |

| | |

| | |

| Signatures | 60 |

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the Section 27A of the Securities Act of 1933, as amended (the Securities Act), and Section 21E of the Securities Exchange Act of 1934, as amended (the Exchange Act). All statements contained in this Annual Report on Form 10-K other than statements of historical fact, including statements regarding our future results of operations and financial position, our business strategy and plans, and our objectives for future operations, are forward-looking statements. The words “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “plan,” “intend,” “expect,” “could,” “target,” “project,” “should,” “predict,” “potential,” “would,” “seek” and similar expressions and the negative of those expressions are intended to identify forward-looking statements. These forward-looking statements are subject to a number of risks, uncertainties and assumptions that are difficult to predict. Therefore, actual results may differ materially and adversely from those expressed in any forward-looking statements. These risks include but are not limited to those factors identified in “Risk Factors” beginning on page 9 of this Annual Report on Form 10-K, those factors that we may from time to time identify in our periodic filings with the Securities and Exchange Commission, as well as other factors beyond our control. We undertake no obligation to revise or update publicly any forward-looking statements for any reason. Unless the context requires otherwise, references in this Form 10-K to “Aehr Test,” the “Company,” “we,” “us” and “our” refer to Aehr Test Systems.

PART I

Item 1. Business

THE COMPANY

Aehr Test was incorporated in the state of California on May 25, 1977. We develop, manufacture and sell systems which are designed to reduce the cost of testing and to perform reliability screening, or burn-in, of complex logic devices, memory ICs, sensors and optical devices. These systems can be used to simultaneously perform parallel testing and burn-in of packaged integrated circuits, or ICs, singulated bare die or ICs still in wafer form. Increased quality and reliability needs of the Automotive, Mobility and flash memory integrated circuit markets are driving additional testing requirements, capacity needs and opportunities for Aehr Test products in package and wafer level testing. Leveraging its expertise as a long-time leading provider of burn-in equipment, with over 2,500 systems installed worldwide, the Company has developed and introduced several innovative product families, including the ABTSTM and FOXTM systems, the WaferPakTM cartridge and the DiePak® carrier. The latest ABTS family of packaged part burn-in and test systems can perform test during burn-in of complex devices, such as digital signal processors, microprocessors, microcontrollers and systems-on-a-chip, and offers individual temperature control for high-power advanced logic devices. The FOX systems are full wafer contact parallel test and burn-in systems designed to make contact with all pads of a wafer simultaneously, thus enabling full wafer parallel test and burn-in. They are also used for parallel test and burn-in singulated die or very small multi-IC modules. The WaferPak cartridge includes a full-wafer probe card for use in testing wafers in FOX systems. The DiePak carrier is a reusable, temporary package that enables IC manufacturers to perform cost-effective test and burn-in of singulated bare die or very small multi-IC modules.

INDUSTRY BACKGROUND

Semiconductor manufacturing is a complex, multi-step process, and defects or weaknesses that may result in the failure of an integrated circuit, or IC, may be introduced at any process step. Failures may occur immediately or at any time during the operating life of an IC, sometimes after several months of normal use. Semiconductor manufacturers rely on testing and reliability screening to identify and eliminate defects that occur during the manufacturing process.

Testing and reliability screening involve multiple steps. The first set of tests is typically performed by IC manufacturers before the processed semiconductor wafer is cut into individual die, in order to avoid the cost of packaging defective die into their packages. This “wafer probe” testing can be performed on one or many die at a time, including testing the entire wafer at once. After the die are packaged and before they undergo reliability screening, a short test is typically performed to detect packaging defects. Most leading-edge microprocessors, microcontrollers, digital signal processors, memory ICs, sensors and optical devices (such as vertical-cavity surface-emitting lasers, or VCSELs) then undergo an extensive reliability screening and stress testing procedure known as “burn-in” or “cycling,” depending on the application. The burn-in process screens for early failures by operating the IC at elevated voltages and temperatures, up to 150 degrees Celsius (302 degrees Fahrenheit), for periods typically ranging from 2 to 48 hours. A typical burn-in system can process thousands of ICs simultaneously. After burn-in, the ICs undergo a final test process using automatic test equipment, or testers. The cycling process screens flash memory devices for failure to meet write/erase cycling endurance requirements.

PRODUCTS

The Company manufactures and markets full wafer contact test systems, test during burn-in systems, test fixtures and related accessories.

All of the Company’s systems are modular, allowing them to be configured with optional features to meet customer requirements. Systems can be configured for use in production applications, where capacity, throughput and price are most important, or for reliability engineering and quality assurance applications, where performance and flexibility, such as extended temperature ranges, are essential.

FULL WAFER CONTACT SYSTEMS

The FOX-XP test and burn-in system, introduced in July 2016, is designed for devices in wafer, singulated die, and module form that require test and burn-in times typically measured in hours. The FOX-XP system can test and burn in up to 18 wafers at a time. For high reliability applications, such as automotive, mobile devices, sensors, and SSDs, the FOX-XP system is a cost-effective solution for producing tested and burned-in die for use in multi-chip packages. Using Known-Good Die, or KGD, which are fully burned-in and tested die, in multi-chip packages helps assure the reliability of the final product and lowers costs by increasing the yield of high-cost multi-chip packages. Wafer-level burn-in and test enables lower cost production of KGD for multi-chip modules, 3-D stacked packages and systems-in-a-package. The FOX-XP system has been extended for burn-in and test of small multi-die modules by using DiePak carriers. The DiePak carrier with its multi-module sockets and high wattage dissipation capabilities has a capacity of hundreds of modules, much higher than the capacity of a traditional burn-in system with traditional single-die sockets and heat sinks. This capability was introduced in March 2017.

The FOX-15 full wafer parallel test system, the predecessor to the FOX-XP system, was introduced in October 2007 and was designed for full-wafer test and burn-in. The FOX-15 system is nearing the end of its lifecycle and limited shipments are expected in the future.

The FOX-1P full wafer parallel test system, introduced in October 2014, is designed for massively parallel test of devices at wafer level. The FOX-1P system is designed to make electrical contact to and test all of the die on a wafer in a single touchdown. The FOX-1P test head and WaferPak contactor are compatible with industry-standard 300 mm wafer probers which provide the wafer handling and alignment automation for the FOX-1P system. The FOX-1P pattern generator is designed to functionally test industry-standard memory devices such as flash and DRAMs, plus it is optimized to test memory or logic ICs that incorporate design for testability, or DFT, and built-in self-test, or BIST. The FOX-1P universal per-pin architecture to provide per-pin electronics and per-device power supplies is tailored to full-wafer functional test. The Company believes that the FOX-1P system can significantly reduce the cost of testing IC wafers. The Company’s FOX-1P system was partially funded through a development agreement with a leading semiconductor manufacturer. The Company received the first production order of this new system and shipped the first system in July 2016.

One of the key components of the FOX systems is the patented WaferPak cartridge system. The WaferPak cartridge contains a full-wafer single-touchdown probe card which is easily removable from the system. Traditional probe cards contact only a portion of the wafer, requiring multiple touchdowns to test the entire wafer. The unique design is intended to accommodate a wide range of contactor technologies so that the contactor technology can evolve along with the changing requirements of the customer’s wafers. The WaferPak cartridges are custom designed for each device type, each of which has a typical lifetime of 2 to 7 years, depending on the device life cycle. Therefore, multiple sets of WaferPak cartridges could be purchased over the life of a FOX system.

A key new component of the FOX-XP systems is the patent-pending DiePak carrier system. The DiePak carrier contains many multi-module sockets with very fine-pitch probes which are easily removable from the system. Traditional sockets contact only a single device, requiring multiple large numbers of sockets and burn-in boards to test a production lot of devices. The unique design is intended to accommodate a wide range of socket sizes and densities so that the DiePak carrier technology can evolve along with the changing requirements of the customer’s devices. The DiePak carriers are custom designed for each device type, each of which has a typical lifetime of 2 to 7 years, depending on the device life cycle. Therefore, multiple sets of DiePak carriers could be purchased over the life of a FOX-XP system.

Another key component of our FOX-XP and FOX-15 test cell is the WaferPak Aligner. The WaferPak Aligner performs automatic alignment of the customer’s wafer to the WaferPak cartridge so that the wafer can be tested and burned-in by the FOX-XP and FOX-15 systems. Typically one WaferPak Aligner can support several FOX-XP or FOX-15 systems.

Similar to the WaferPak Aligner for WaferPak cartridges, Aehr Test offers a DiePak Loader for DiePak carriers. The DiePak Loader performs automatic loading of the customer’s modules to the DiePak carrier so that the modules can be tested and burned-in by the FOX-XP system. Typically one DiePak Loader can support several FOX-XP systems.

The full wafer contact systems product category accounted for approximately 44%, 51% and 60% of the Company’s net sales in fiscal 2018, 2017 and 2016, respectively.

SYSTEMS FOR PACKAGED PARTS

Test during burn-in, or TDBI, systems consist of several subsystems: pattern generation and test electronics, control software, network interface and environmental chamber. The test pattern generator allows duplication of most of the functional tests performed by a traditional tester. Pin electronics at each burn-in board, or BIB, position are designed to provide accurate signals to the ICs being tested and detect whether a device is failing the test.

Devices being tested are placed on BIBs and loaded into environmental chambers which typically operate at temperatures from 25 degrees Celsius (77 degrees Fahrenheit) up to 150 degrees Celsius (302 degrees Fahrenheit) (optional chambers can produce temperatures as low as -55 degrees Celsius (-67 degrees Fahrenheit)). A single BIB can hold up to several hundred ICs, and a production chamber holds up to 72 BIBs, resulting in thousands of memory or logic devices being tested in a single system.

The Advanced Burn-in and Test System, or ABTS, was introduced in fiscal 2008. The ABTS family of products is based on a hardware and software architecture that is intended to address not only today’s devices, but also future devices for many years to come. The ABTS system can test and burn-in both high-power logic and low-power ICs. It can be configured to provide individual device temperature control for devices up to 70W or more and with up to 320 I/O channels.

The MAX system family, the predecessor to the ABTS family, was designed for monitored burn-in of memory and logic devices. The MAX system is nearing the end of its lifecycle and limited shipments are expected in the future.

This packaged part systems product category accounted for approximately 56%, 49% and 40% of the Company’s net sales in fiscal 2018, 2017 and 2016, respectively.

TEST FIXTURES

The Company sells, and licenses others to manufacture and sell, custom-designed test fixtures for its systems. The test fixtures include BIBs for the ABTS parallel test and burn-in system and for the MAX monitored burn-in system. These test fixtures hold the devices undergoing test or burn-in and electrically connect the devices under test to the system electronics. The capacity of each test fixture depends on the type of device being tested or burned-in, ranging from several hundred in memory production to as few as eight for high pin-count complex Application Specific Integrated Circuits, or ASICs, or microprocessor devices. Test fixtures are sold both with new Aehr Test systems and for use with the Company’s installed base of systems. Test fixtures are also available from third-party suppliers.

The Company has received patents or applied for patents on certain features of the FOX, ABTS and MAX4 test fixtures. The Company has licensed or authorized several other companies to provide MAX4 BIBs from which the Company receives royalties. Royalties and revenue for the test fixtures product category accounted for less than 1% of net sales in fiscal 2018, 2017 and 2016.

CUSTOMERS

The Company markets and sells its products throughout the world to semiconductor manufacturers, semiconductor contract assemblers, electronics manufacturers and burn-in and test service companies.

Sales to the Company’s five largest customers accounted for approximately 86%, 93%, and 94% of its net sales in fiscal 2018, 2017 and 2016, respectively. During fiscal 2018, Texas Instruments Incorporated, or Texas Instruments, STMicroelectronics, Inc., and Astronics Test Systems, Inc., accounted for approximately 34%, 26% and 13%, respectively, of the Company’s net sales. During fiscal 2017, Texas Instruments Incorporated, or Texas Instruments, STMicroelectronics, Inc., Intel Corporation and Cypress Semiconductor, accounted for approximately 45%, 19%, 17% and 10%, respectively, of the Company’s net sales. During fiscal 2016, Apple Inc. and Texas Instruments accounted for approximately 47% and 32%, respectively, of the Company’s net sales. No other customers accounted for more than 10% of the Company’s net sales for any of these periods. The Company expects that sales of its products to a limited number of customers will continue to account for a high percentage of net sales for the foreseeable future. In addition, sales to particular customers may fluctuate significantly from quarter to quarter. Such fluctuations may result in changes in utilization of the Company’s facilities and resources. The loss of or reduction or delay in orders from a significant customer or a delay in collecting or failure to collect accounts receivable from a significant customer could materially and adversely affect the Company’s business, financial condition and operating results.

MARKETING, SALES AND CUSTOMER SUPPORT

The Company has sales and service operations in the United States, Japan, Germany and Taiwan, dedicated service resources in China, South Korea, and the Philippines, and has established a network of distributors and sales representatives in certain key parts of the world. See “REVENUE RECOGNITION” in Item 7 under “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for a further discussion of the Company’s relationship with distributors, and its effects on revenue recognition.

The Company’s customer service and support program includes system installation, system repair, applications engineering support, spare parts inventories, customer training and documentation. The Company has applications engineering and field service personnel located near and sometimes co-located at our customers and includes resources at the corporate headquarters in Fremont, California, at customer locations in Texas, at the Company’s subsidiaries in Japan and Germany, at its branch office in Taiwan, and also through 3rd party agreements in China, South Korea, and the Philippines. The Company’s distributors provide applications and field service support in other parts of the world. The Company customarily provides a warranty on its products. The Company offers service contracts on its systems directly and through its subsidiaries, distributors and representatives. The Company maintains customer support personnel in the Philippines, China and South Korea. The Company believes that maintaining a close relationship with customers and providing them with ongoing engineering support improves customer satisfaction and will provide the Company with a competitive advantage in selling its products to the Company’s customers.

BACKLOG

At May 31, 2018, the Company’s backlog was $8.4 million compared with $12.7 million at May 31, 2017. The Company’s backlog consists of product orders for which confirmed purchase orders have been received and which are scheduled for shipment within 12 months. Due to the possibility of customer changes in delivery schedules or cancellations and potential delays in product shipments or development projects, the Company’s backlog as of a particular date may not be indicative of net sales for any succeeding period.

RESEARCH AND PRODUCT DEVELOPMENT

The Company historically has devoted a significant portion of its financial resources to research and development programs and expects to continue to allocate significant resources to these efforts. Certain research and development expenditures related to non-recurring engineering milestones have been transferred to cost of goods sold, reducing research and development expenses. The Company’s research and development expenses during fiscal 2018, 2017 and 2016 were $4.2 million, $4.7 million and $4.3 million, respectively.

The Company conducts ongoing research and development to design new products and to support and enhance existing product lines. Building upon the expertise gained in the development of its existing products, the Company has developed the FOX family of systems for performing test and burn-in of entire processed wafers, rather than individual die or packaged parts. The Company has extended the FOX-XP product to also perform test and burn-in of devices in singulated die and module form. The Company is developing enhancements to the ABTS and FOX families of products, intended to improve the capability and performance for testing and burn-in of future generation ICs and provide the flexibility in a wide variety of applications.

MANUFACTURING

The Company assembles its products from components and parts manufactured by others, including environmental chambers, power supplies, metal fabrications, printed circuit assemblies, ICs, burn-in sockets, high-density interconnects, wafer contactors and interconnect substrates. Final assembly and testing are performed within the Company’s facilities. The Company’s strategy is to use in-house manufacturing only when necessary to protect a proprietary process or when a significant improvement in quality, cost or lead time can be achieved and relies on subcontractors to manufacture many of the components and subassemblies used in its products. The Company’s principal manufacturing facility is located in Fremont, California. The Company’s facility in Utting, Germany provides limited manufacturing and product customization.

COMPETITION

The semiconductor equipment industry is intensely competitive. Significant competitive factors in the semiconductor equipment market include price, technical capabilities, quality, flexibility, automation, cost of ownership, reliability, throughput, product availability and customer service. In each of the markets it serves, the Company faces competition from established competitors and potential new entrants, many of which have greater financial, engineering, manufacturing and marketing resources than the Company.

The Company’s FOX full wafer contact systems face competition from larger systems manufacturers that have significant technological know-how and manufacturing capability. Competing suppliers of full wafer contact systems include Advantest Corporation, Chroma ATE Inc., Teradyne Inc., Micronics Japan Co., Ltd., and Tokyo Electron Limited.

The Company’s ABTS TDBI systems face increasingly severe competition, especially from several regional, low-cost manufacturers and from systems manufacturers that offer higher power dissipation per device under test. Some users of such systems, such as independent test labs, build their own burn-in systems, while others, particularly large IC manufacturers in Asia, acquire burn-in systems from captive or affiliated suppliers. The market for burn-in systems is highly fragmented, with many domestic and international suppliers. Competing suppliers of burn-in and functional test systems that compete with ABTS systems include Dong-Il Corporation, Micro Control Company, Incal Technology and Advantest Corporation.

The Company’s WaferPak products are facing and are expected to face increasing competition. Several companies have developed or are developing full-wafer and single-touchdown probe cards. As the full-wafer test market develops, the Company expects that other competitors will emerge. The primary competitive factors in this market are cost, performance, reliability and assured supply. Competing suppliers of full-wafer probe cards include FormFactor, Inc., Japan Electronic Materials Corporation and Micronics Japan Co., Ltd.

The Company’s test fixture products face numerous regional competitors. There are limited barriers to entry into the BIB market, and as a result, many companies design and manufacture BIBs, including BIBs for use with the Company’s ABTS and MAX systems. The Company has granted royalty-bearing licenses to several companies to make BIBs for use with the Company’s MAX4 systems and the Company may grant additional licenses as well. Sales of MAX4 BIBs by licensees result in royalties to the Company.

The Company expects that its DiePak products for burning-in and testing multiple singulated die and small modules will face significant competition. The Company believes that several companies have developed or are developing products which are intended to enable test and burn-in of multiple bare die, and small modules. The Company expects that other competitors will emerge. The Company expects that the primary competitive factors in this market will be cost, performance, reliability and assured supply. Suppliers with products that compete with our single die DiePak products include Chroma ATE Inc.

The Company expects its competitors to continue to improve the performance of their current products and to introduce new products with improved price and performance characteristics. New product introductions by the Company’s competitors or by new market entrants could cause a decline in sales or loss of market acceptance of the Company’s products. The Company has observed price competition in the systems market, particularly with respect to its less advanced products. Increased competitive pressure could also lead to intensified price-based competition, resulting in lower prices which could adversely affect the Company’s operating margins and results. The Company believes that to remain competitive it must invest significant financial resources in new product development and expand its customer service and support worldwide. There can be no assurance that the Company will be able to compete successfully in the future.

PROPRIETARY RIGHTS

The Company relies primarily on the technical and creative ability of its personnel, its proprietary software, and trade secrets and copyright protection, rather than on patents, to maintain its competitive position. The Company’s proprietary software is copyrighted and licensed to the Company’s customers. At May 31, 2018, the Company held fifty issued United States patents with expiration date ranges from 2018 to 2029 and had several additional United States patent applications and foreign patent applications pending.

The Company’s ability to compete successfully is dependent in part upon its ability to protect its proprietary technology and information. Although the Company attempts to protect its proprietary technology through patents, copyrights, trade secrets and other measures, there can be no assurance that these measures will be adequate or that competitors will not be able to develop similar technology independently. Further, there can be no assurance that claims allowed on any patent issued to the Company will be sufficiently broad to protect the Company’s technology, that any patent will be issued to the Company from any pending application or that foreign intellectual property laws will protect the Company’s intellectual property. Litigation may be necessary to enforce or determine the validity and scope of the Company’s proprietary rights, and there can be no assurance that the Company’s intellectual property rights, if challenged, will be upheld as valid. Any such litigation could result in substantial costs and diversion of resources and could have a material adverse effect on the Company’s business, financial condition and operating results, regardless of the outcome of the litigation. In addition, there can be no assurance that any of the patents issued to the Company will not be challenged, invalidated or circumvented or that the rights granted thereunder will provide competitive advantages

to the Company. Also, there can be no assurance that the Company will have the financial resources to defend its patents from infringement or claims of invalidity.

There are currently no pending claims against the Company regarding infringement of any patents or other intellectual property rights of others. However, the Company may, from time to time, receive communications from third parties asserting intellectual property claims against the Company. Such claims could include assertions that the Company’s products infringe, or may infringe, the proprietary rights of third parties, requests for indemnification against such infringement or suggest the Company may be interested in acquiring a license from such third parties. There can be no assurance that any such claim made in the future will not result in litigation, which could involve significant expense to the Company, and, if the Company is required or deems it appropriate to obtain a license relating to one or more products or technologies, there can be no assurance that the Company would be able to do so on commercially reasonable terms, or at all.

EMPLOYEES

As of May 31, 2018, the Company, including its two foreign subsidiaries and one branch office, employed 86 persons collectively, on a full-time basis, of whom 21 were engaged in research, development and related engineering, 27 were engaged in manufacturing, 25 were engaged in marketing, sales and customer support and 13 were engaged in general administration and finance functions. In addition, the Company from time to time employs a number of contractors and part-time employees, particularly to perform customer support and manufacturing. The Company’s success is in part dependent on its ability to attract and retain highly skilled workers, who are in high demand. None of the Company’s employees are represented by a union and the Company has never experienced a work stoppage. The Company’s management considers its relations with its employees to be good.

BUSINESS SEGMENT DATA AND GEOGRAPHIC AREAS

The Company operates in a single business segment, the designing, manufacturing and marketing of advanced test and burn-in products to the semiconductor manufacturing industry in several geographic areas. Selected financial information, including net sales and property and equipment, net for each of the last three fiscal years, by geographic area is included in Part II, Item 8, Note 14 “Segment Information” and certain risks related to such operations are discussed in Part I, Item 1A, under the heading “We sell our products and services worldwide, and our business is subject to risks inherent in conducting business activities in geographic regions outside of the United States.”

AVAILABLE INFORMATION

The Company’s common stock trades on the NASDAQ Capital Market under the symbol “AEHR.” The Company’s annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to these reports that are filed with the United States Securities and Exchange Commission, or SEC, pursuant to Section 13(a) or 15(d) of the Exchange Act, are available free of charge through the Company’s website at www.aehr.com as soon as reasonably practicable after we electronically file them with, or furnish them to the SEC.

The public may read and copy any materials filed by the Company with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. The public may obtain information on the operations of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site, www.sec.gov, that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC.

In addition, information regarding the Company’s code of conduct and ethics and the charters of its Audit, Compensation and Nominating and Governance Committees, are available free of charge on the Company’s website listed above.

Item 1A. Risk Factors

You should carefully consider the risks described below. These risks are not the only risks that we may face. Additional risks and uncertainties that we are unaware of, or that we currently deem immaterial, also may become important factors that affect us. If any of the following risks occur, our business, financial condition or results of operations could be materially and adversely affected which could cause our actual operating results to differ materially from those indicated or suggested by forward-looking statements made in this Annual Report on Form 10-K or presented elsewhere by management from time to time.

We generate a large portion of our sales from a small number of customers. If we were to lose one or more of our large customers, operating results could suffer dramatically.

The semiconductor manufacturing industry is highly concentrated, with a relatively small number of large semiconductor manufacturers and contract assemblers accounting for a substantial portion of the purchases of semiconductor equipment. Sales to our five largest customers accounted for approximately 86%, 93%, and 94% of our net sales in fiscal 2018, 2017 and 2016, respectively. During fiscal 2018, Texas Instruments, STMicroelectronics, Inc., and Astronics Test Systems, Inc., accounted for approximately 34%, 26% and 13%, respectively, of the Company’s net sales. During fiscal 2017, Texas Instruments, STMicroelectronics, Inc., Intel, and Cypress Semiconductor, accounted for approximately 45%, 19%, 17% and 10%, respectively, of the Company’s net sales. During fiscal 2016, Apple and Texas Instruments accounted for approximately 47% and 32%, respectively, of our net sales. No other customers accounted for more than 10% of our net sales for any of these periods.

We expect that sales of our products to a limited number of customers will continue to account for a high percentage of net sales for the foreseeable future. In addition, sales to particular customers may fluctuate significantly from quarter to quarter. The loss of, reduction or delay in an order, or orders from a significant customer, or a delay in collecting or failure to collect accounts receivable from a significant customer could adversely affect our business, financial condition and operating results.

The semiconductor equipment industry is intensely competitive. In each of the markets we serve, we face competition from established competitors and potential new entrants, many of which have greater financial, engineering, manufacturing and marketing resources than us.

Our FOX wafer level and singulated die/module test and burn in systems face competition from larger systems manufacturers that have significant technological know-how and manufacturing capability. Our ABTS Test During Burn-in (TDBI) systems have faced and are expected to continue to face increasingly severe competition, especially from several regional, low-cost manufacturers and from systems manufacturers that offer higher power dissipation per device under test. Some users of such systems, such as independent test labs, build their own burn-in systems, while others, particularly large IC manufacturers in Asia, acquire burn-in systems from captive or affiliated suppliers. Our WaferPak products are facing and are expected to face increasing competition. Several companies have developed or are developing full-wafer and single-touchdown probe cards.

We expect our competitors to continue to improve the performance of their current products and to introduce new products with improved price and performance characteristics. New product introductions by our competitors or by new market entrants could cause a decline in sales or loss of market acceptance of our products. We have observed price competition in the systems market, particularly with respect to its less advanced products. Increased competitive pressure could also lead to intensified price-based competition, resulting in lower prices which could adversely affect our operating margins and results. We believe that to remain competitive we must invest significant financial resources in new product development and expand our customer service and support worldwide. There can be no assurance that we will be able to compete successfully in the future.

We rely on increasing market acceptance for our FOX system, and we may not be successful in attracting new customers or maintaining our existing customers.

A principal element of our business strategy is to increase our presence in the test equipment market through system sales in our FOX wafer-level and singulated die/module test and burn-in product family. The market for the FOX systems is in the early stages of development. Market acceptance of the FOX system is subject to a number of risks. Before a customer will incorporate the FOX system into a production line, lengthy qualification and correlation tests must be performed. We anticipate that potential customers may be reluctant to change their procedures in order to transfer burn-in and test functions to the FOX system. Initial purchases are expected to be limited to systems used for these qualifications and for engineering studies. Market acceptance of the FOX system also may be affected by a reluctance of IC manufacturers to rely on relatively small suppliers such as us. As is common with new complex products incorporating leading-edge technologies, we may encounter reliability, design and manufacturing issues as we begin volume production and initial installations of FOX systems at customer sites. The failure of the FOX system to achieve increased market acceptance would have a material adverse effect on our future operating results, long-term prospects and our stock price.

We rely on continued market acceptance of our ABTS system and our ability to complete certain enhancements.

Continued market acceptance of the ABTS family is subject to a number of risks. It is important that we achieve customer acceptance, customer satisfaction and increased market acceptance as we add new features and enhancements to the ABTS product. To date, we have shipped ABTS systems to customers worldwide for use in both reliability and production applications. We have had a strengthening of ABTS product sales last two fiscal years. However, the failure of the ABTS family to grow revenues above current levels would have a material adverse effect on our future operating results.

A substantial portion of our net sales is generated by relatively small volume, high value transactions.

We derive a substantial portion of our net sales from the sale of a relatively small number of systems which typically range in purchase price from approximately $300,000 to well over $1 million per system. As a result, the loss or deferral of a limited number of system sales could have a material adverse effect on our net sales and operating results in a particular period. Most customer purchase orders are subject to cancellation or rescheduling by the customer with limited penalties, and, therefore, backlog at any particular date is not necessarily indicative of actual sales for any succeeding period. From time to time, cancellations and rescheduling of customer orders have occurred, and delays by our suppliers in providing components or subassemblies to us have caused delays in our shipments of our own products. There can be no assurance that we will not be materially adversely affected by future cancellations or rescheduling. For non-standard products where we have not effectively demonstrated the ability to meet specifications in the customer environment, we defer revenue until we have met such customer specifications. Any delay in meeting customer specifications could have a material adverse effect on our operating results. A substantial portion of net sales typically are realized near the end of each quarter. A delay or reduction in shipments near the end of a particular quarter, due, for example, to unanticipated shipment rescheduling, cancellations or deferrals by customers, customer credit issues, unexpected manufacturing difficulties experienced by us or delays in deliveries by suppliers, could cause net sales in a particular quarter to fall significantly below our expectations.

We may experience increased costs associated with new product introductions.

As is common with new complex products incorporating leading-edge technologies, we have encountered reliability, design and manufacturing issues as we began volume production and initial installations of certain products at customer sites. Some of these issues in the past have been related to components and subsystems supplied to us by third parties who have in some cases limited the ability of us to address such issues promptly. This process in the past required and in the future is likely to require us to incur un-reimbursed engineering expenses and to experience larger than anticipated warranty claims which could result in product returns. In the early stages of product development there can be no assurance that we will discover any reliability, design and manufacturing issues or, that if such issues arise, that they can be resolved to the customers’ satisfaction or that the resolution of such problems will not cause us to incur significant development costs or warranty expenses or to lose significant sales opportunities.

We sell our products and services worldwide, and our business is subject to risks inherent in conducting business activities in geographic regions outside of the United States.

Approximately 71%, 59%, and 80% of our net sales for fiscal 2018, 2017 and 2016, respectively, were attributable to sales to customers for delivery outside of the United States. We operate a direct sales, service and limited manufacturing organization in Germany and sales and service organizations in Japan and Taiwan as well as direct support through 3rd party agreements in China, South Korea, and the Philippines. We expect that sales of products for delivery outside of the United States will continue to represent a substantial portion of our future net sales. Our future performance will depend, in significant part, upon our ability to continue to compete in foreign markets which in turn will depend, in part, upon a continuation of current trade relations between the United States and foreign countries in which semiconductor manufacturers or assemblers have operations. A change toward more protectionist trade legislation in either the United States or such foreign countries, such as a change in the current tariff structures, export compliance or other trade policies, could adversely affect our ability to sell our products in foreign markets. In addition, we are subject to other risks associated with doing business internationally, including longer receivable collection periods and greater difficulty in accounts receivable collection, the burden of complying with a variety of foreign laws, difficulty in staffing and managing global operations, risks of civil disturbance or other events which may limit or disrupt markets, international exchange restrictions, changing political conditions and monetary policies of foreign governments.

Approximately 100%, 0% and 0% of our net sales for fiscal 2018 were denominated in U.S. Dollars, Euros and Japanese Yen, respectively. Although the percentages of net sales denominated in Euros and Japanese Yen were small in fiscal 2018, they have been larger in the past and could become significant again in the future. A large percentage of net sales to European customers are denominated in U.S. Dollars, but sales to many Japanese customers are denominated in Japanese Yen. Because a substantial portion of our net sales is from sales of products for delivery outside the United States, an increase in the value of the U.S. Dollar relative to foreign currencies would increase the cost of our products compared to products sold by local companies in such markets. In addition, since the price is determined at the time a purchase order is accepted, we are exposed to the risks of fluctuations in the U.S. Dollar exchange rate during the lengthy period from the date a purchase order is received until payment is made. This exchange rate risk is partially offset to the extent our foreign operations incur expenses in the local currency. To date, we have not invested in any instruments designed to hedge currency risks. Our operating results could be adversely affected by fluctuations in the value of the U.S. Dollar relative to other currencies.

We purchase materials from suppliers worldwide, which subjects the Company to increased risk.

We purchase components, sub-assemblies, and chambers from suppliers outside the United States. Increases in tariffs, additional taxes, or trade barriers may result in an increase in our manufacturing costs. A decrease in the value of the U.S. Dollar relative to foreign currencies would increase the cost of our materials. Should the Company increase its sales prices to recover the increase in costs, this could result in a decrease in the competitiveness of our products. In addition, we are subject to other risks associated with purchasing materials from suppliers worldwide. Government authorities may also implement protectionist policies or impose limitations on the transfer of intellectual property. This may limit our ability to obtain products from certain geographic regions and require us to identify and qualify new suppliers. The process of qualifying suppliers could be lengthy, and no assurance can be given that any additional sources would be available to us on a timely basis. Changes in trade relations, currency fluctuations, or protectionist policies could have a material adverse effect on our business, financial condition or results of operations.

The Company is exposed to cybersecurity threats or incidents.

We collect, maintain, and transmit data on information systems. These systems include those owned and maintained by the Company or by third parties. In addition, we use cloud-based enterprise resource planning, ERP, software to manage the business integrating all facets of operations, including manufacturing, finance, and sales and marketing. The data maintained on these systems includes confidential and proprietary information belonging to Aehr, our customers, suppliers, and others. While the Company devotes significant resources to protect its systems and data from unauthorized access or misuse, we are exposed to cybersecurity risks. Our systems are subject to computer viruses, data breach, phishing schemes, and other malicious software programs or attacks. We have experienced cyber threats and incidents in the past. Although past threats and incidents have not resulted in a material adverse effect, cybersecurity incidents may result in business disruption, loss of data, or unauthorized access to intellectual property which could adversely affect our business.

Our industry is subject to rapid technological change and our ability to remain competitive depends on our ability to introduce new products in a timely manner.

The semiconductor equipment industry is subject to rapid technological change and new product introductions and enhancements. Our ability to remain competitive depends in part upon our ability to develop new products and to introduce them at competitive prices and on a timely and cost-effective basis. Our success in developing new and enhanced products depends upon a variety of factors, including product selection, timely and efficient completion of product design, timely and efficient implementation of manufacturing and assembly processes, product performance in the field and effective sales and marketing. Because new product development commitments must be made well in advance of sales, new product decisions must anticipate both future demand and the technology that will be available to supply that demand. Furthermore, introductions of new and complex products typically involve a period in which design, engineering and reliability issues are identified and addressed by our suppliers and by us. There can be no assurance that we will be successful in selecting, developing, manufacturing and marketing new products that satisfy market demand. Any such failure would materially and adversely affect our business, financial condition and results of operations.

Because of the complexity of our products, significant delays can occur between a product’s introduction and the commencement of the volume production of such product. We have experienced, from time to time, significant delays in the introduction of, and technical and manufacturing difficulties with, certain of our products and may experience delays and technical and manufacturing difficulties in future introductions or volume production of our new products. Our inability to complete new product development, or to manufacture and ship products in time to meet customer requirements would materially adversely affect our business, financial condition and results of operations.

Our dependence on subcontractors and sole source suppliers may prevent us from delivering our products on a timely basis and expose us to intellectual property infringement.

We rely on subcontractors to manufacture many of the components or subassemblies used in our products. Our FOX and ABTS systems, WaferPak contactors and DiePak carriers contain several components, including environmental chambers, power supplies, high-density interconnects, wafer contactors, module contactors, signal distribution substrates, WaferPak Aligners, DiePak Loaders and certain ICs that are currently supplied by only one or a limited number of suppliers. Our reliance on subcontractors and single source suppliers involves a number of significant risks, including the loss of control over the manufacturing process, the potential absence of adequate capacity and reduced control over delivery schedules, manufacturing yields, quality and costs. In the event that any significant subcontractor or single source supplier is unable or unwilling to continue to manufacture subassemblies, components or parts in required volumes, we would have to identify and qualify acceptable replacements. The process of qualifying subcontractors and suppliers could be lengthy, and no assurance can be given that any additional sources would be available to us on a timely basis. Any delay, interruption or termination of a supplier relationship could adversely affect our ability to deliver products, which would harm our operating results.

Our suppliers manufacture components, tooling, and provide engineering services. During this process, our suppliers are allowed access to our intellectual property. While we maintain patents to protect from intellectual property infringement, there can be no assurance that technological information gained in the manufacture of our products will not be used to develop a new product, improve processes or techniques which compete against our products. Litigation may be necessary to enforce or determine the validity and scope of our proprietary rights, and there can be no assurance that our intellectual property rights, if challenged, will be upheld as valid.

Periodic economic and semiconductor industry downturns could negatively affect our business, results of operations and financial condition.

Periodic global economic and semiconductor industry downturns have negatively affected and could continue to negatively affect our business, results of operations, and financial condition. Financial turmoil in the banking system and financial markets has resulted, and may result in the future, in a tightening of the credit markets, disruption in the financial markets and global economy downturn. These events may contribute to significant slowdowns in the industry in which we operate. Difficulties in obtaining capital and deteriorating market conditions can pose the risk that some of our customers may not be able to obtain necessary financing on reasonable terms, which could result in lower sales. Customers with liquidity issues may lead to additional bad debt expense.

Turmoil in the international financial markets has resulted, and may result in the future, in dramatic currency devaluations, stock market declines, restriction of available credit and general financial weakness. In addition, flash memory and other similar device prices have historically declined, and will likely do so again in the future. These developments may affect us in several ways. The market for semiconductors and semiconductor capital equipment has historically been cyclical, and we expect this to continue in the future. The uncertainty of the semiconductor market may cause some manufacturers in the future to further delay capital spending plans. Economic conditions may also affect the ability of our customers to meet their payment obligations, resulting in cancellations or deferrals of existing orders and limiting additional orders. In addition, some governments have subsidized portions of fabrication facility construction, and financial turmoil may reduce these governments’ willingness to continue such subsidies. Such developments could have a material adverse effect on our business, financial condition and results of operations.

The current economic conditions and uncertainty about future economic conditions make it challenging for us to forecast our operating results, make business decisions, and identify the risks that may affect our business, financial condition and results of operations. If such conditions recur, and we are not able to timely and appropriately adapt to changes resulting from the difficult macroeconomic environment, our business, financial condition or results of operations may be materially and adversely affected.

Future changes in semiconductor technologies may make our products obsolete.

Future improvements in semiconductor design and manufacturing technology may reduce or eliminate the need for our products. For example, improvements in semiconductor process technology and improvements in conventional test systems, such as reduced cost or increased throughput, may significantly reduce or eliminate the market for one or more of our products. If we are not able to improve our products or develop new products or technologies quickly enough to maintain a competitive position in our markets, our business may decline.

If we are not able to reduce our operating expenses sufficiently during periods of weak revenue, or if we utilize significant amounts of cash to support operating losses, we may erode our cash resources and may not have sufficient cash to operate our business.

In recent years, in the face of a downturn in our business and a decline in our net sales, we implemented a variety of cost controls and restructured our operations with the goal of reducing our operating costs to position ourselves to more effectively meet the needs of the then weak market for test and burn-in equipment. While we took significant steps to minimize our expense levels and to increase the likelihood that we would have sufficient cash to support operations during the downturn, from fiscal 2009 through fiscal 2017, with the exception of fiscal 2014, we experienced operating losses. We anticipate that our existing cash balance together with income from operations, collections of existing accounts receivable, revenue from our existing backlog of products, the sale of inventory on hand, and deposits and down payments against significant orders will be adequate to meet our working capital and capital equipment requirements. Depending on our rate of growth and profitability, and our ability to obtain significant orders with down payments, we may require additional equity or debt financing to meet our working capital requirements or capital equipment needs. There can be no assurance that additional financing will be available when required, or if available, that such financing can be obtained on terms satisfactory to us.

Our stock price may fluctuate.

The price of our common stock has fluctuated in the past and may fluctuate significantly in the future. We believe that factors such as announcements of developments related to our business, fluctuations in our operating results, general conditions in the semiconductor and semiconductor equipment industries as well as the worldwide economy, announcement of technological innovations, new systems or product enhancements by us or our competitors, fluctuations in the level of cooperative development funding, acquisitions, changes in governmental regulations, developments in patents or other intellectual property rights and changes in our relationships with customers and suppliers could cause the price of our common stock to fluctuate substantially. In addition, in recent years the stock market in general, and the market for small capitalization and high technology stocks in particular, have experienced extreme price fluctuations which have often been unrelated to the operating performance of the affected companies. Such fluctuations could adversely affect the market price of our common stock.

We depend on our key personnel and our success depends on our ability to attract and retain talented employees.

Our success depends to a significant extent upon the continued service of Gayn Erickson, our President and Chief Executive Officer, as well as other executive officers and key employees. We do not maintain key person life insurance for our benefit on any of our personnel, and none of our employees are subject to a non-competition agreement with us. The loss of the services of any of our executive officers or a group of key employees could have a material adverse effect on our business, financial condition and operating results. Our future success will depend in significant part upon our ability to attract and retain highly skilled technical, management, sales and marketing personnel. There is a limited number of personnel with the requisite skills to serve in these positions, and it has become increasingly difficult for us to hire such personnel. Competition for such personnel in the semiconductor equipment industry is intense, and there can be no assurance that we will be successful in attracting or retaining such personnel. Changes in management could disrupt our operations and adversely affect our operating results.

We may be subject to litigation relating to intellectual property infringement which would be time-consuming, expensive and a distraction from our business.

If we do not adequately protect our intellectual property, competitors may be able to use our proprietary information to erode our competitive advantage, which could harm our business and operating results. Litigation may be necessary to enforce or determine the validity and scope of our proprietary rights, and there can be no assurance that our intellectual property rights, if challenged, will be upheld as valid. Such litigation could result in substantial costs and diversion of resources and could have a material adverse effect on our operating results, regardless of the outcome of the litigation. In addition, there can be no assurance that any of the patents issued to us will not be challenged, invalidated or circumvented or that the rights granted thereunder will provide competitive advantages to us.

There are no pending claims against us regarding infringement of any patents or other intellectual property rights of others. However, in the future we may receive communications from third parties asserting intellectual property claims against us. Such claims could include assertions that our products infringe, or may infringe, the proprietary rights of third parties, requests for indemnification against such infringement or suggestions that we may be interested in acquiring a license from such third parties. There can be no assurance that any such claim will not result in litigation, which could involve significant expense to us, and, if we are required or deem it appropriate to obtain a license relating to one or more products or technologies, there can be no assurance that we would be able to do so on commercially reasonable terms, or at all.

While we believe we have complied with all applicable environmental laws, our failure to do so could adversely affect our business as a result of having to pay substantial amounts in damages or fees.

Federal, state and local regulations impose various controls on the use, storage, discharge, handling, emission, generation, manufacture and disposal of toxic and other hazardous substances used in our operations. We believe that our activities conform in all material respects to current environmental and land use regulations applicable to our operations and our current facilities, and that we have obtained environmental permits necessary to conduct our business. Nevertheless, failure to comply with current or future regulations could result in substantial fines, suspension of production, alteration of our manufacturing processes or cessation of operations. Such regulations could require us to acquire expensive remediation equipment or to incur substantial expenses to comply with environmental regulations. Any failure to control the use, disposal or storage of or adequately restrict the discharge of, hazardous or toxic substances could subject us to significant liabilities.

If we fail to maintain effective internal control over financial reporting in the future, the accuracy and timing of our financial reporting may be adversely affected.

We are required to comply with Section 404 of the Sarbanes-Oxley Act of 2002. The provisions of the act require, among other things, that we maintain effective internal control over financial reporting and disclosure controls and procedures. Preparing our financial statements involves a number of complex processes, many of which are done manually and are dependent upon individual data input or review. These processes include, but are not limited to, calculating revenue, deferred revenue and inventory costs. While we continue to automate our processes and enhance our review and put in place controls to reduce the likelihood for errors, we expect that for the foreseeable future, many of our processes will remain manually intensive and thus subject to human error.

Our common stock may be delisted from The NASDAQ Capital Market if we cannot maintain compliance with NASDAQ’s continued listing requirements.

In order to maintain our listing on The NASDAQ Capital Market, we are required to maintain compliance with NASDAQ’s continued listing requirements. The continued listing requirements include, among others, a minimum bid price of $1.00 per share and any of: (i) a minimum stockholders’ equity of $2.5 million; (ii) a market value of listed securities of at least $35 million; or (iii) net income from continuing operations of $500,000 in the most recently completed fiscal year or in two of the last three fiscal years. There are no assurances that we will be able to sustain long-term compliance with NASDAQ’s continued listing requirements. On April 19, 2016, we were notified by NASDAQ that we were no longer in compliance with NASDAQ’s continued listing requirements as we did not have a minimum stockholders’ equity of $2.5 million. On October 3, 2016, we were notified by NASDAQ that we had regained compliance with NASDAQ’s continued listing requirements. If we fail to maintain compliance with the applicable NASDAQ continued listing requirements, our stock may be delisted.

If we are delisted, we would expect our common stock to be traded in the over-the-counter market, which could make trading our common stock more difficult for investors, potentially leading to declines in our share price and liquidity. Delisting from The NASDAQ Capital Market would also constitute an event of default under our convertible notes. In addition, delisting could result in negative publicity and make it more difficult for us to raise additional capital.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

The Company’s principal administrative and production facilities are located in Fremont, California, in a 51,289 square foot building. The Company’s lease was renewed in February 2018 and expires in July 2023. The Company’s facility in Japan is located in a 418 square foot office in Tokyo under a lease which expires in June 2019. The Company also maintains a 1,585 square foot warehouse in Yamanashi under a lease which expires in November 2019. The Company leases a 492 square foot sales and support office in Utting, Germany. The lease, which began February 1, 1992 and expires on January 31, 2020, contains an automatic twelve months renewal, at rates to be determined, if no notice is given prior to six months from expiry. The Company’s and its subsidiaries’ annual rental payments currently aggregate $587,000. The Company periodically evaluates its global operations and facilities to bring its capacity in line with demand and to provide cost efficient services for its customers. In prior years, through this process, the Company has moved from certain facilities that exceeded the capacity required to satisfy its needs. The Company believes that its existing facilities are adequate to meet its current and reasonably foreseeable requirements. The Company regularly evaluates its expected future facilities requirements and believes that alternate facilities would be available if needed.

Item 3. Legal Proceedings

None.

Item 4. Mine Safety Disclosures

Not Applicable

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of

Equity Securities

The Company’s common stock is publicly traded on the NASDAQ Capital Market under the symbol “AEHR”. The following table sets forth, for the periods indicated, the high and low sale prices for the common stock on such market. These quotations represent prices between dealers and do not include retail markups, markdowns or commissions and may not necessarily represent actual transactions.

| | | |

| Fiscal 2018: | | |

| First quarter ended August 31, 2017 | $4.60 | $2.62 |

| Second quarter ended November 30, 2017 | 4.10 | 2.50 |

| Third quarter ended February 28, 2018 | 3.37 | 2.16 |

| Fourth quarter ended May 31, 2018 | 2.80 | 2.12 |

| | | |

| Fiscal 2017: | | |

| First quarter ended August 31, 2016 | $3.42 | $0.96 |

| Second quarter ended November 30, 2016 | 3.58 | 2.05 |

| Third quarter ended February 28, 2017 | 5.28 | 2.15 |

| Fourth quarter ended May 31, 2017 | 6.10 | 3.37 |

At August 3, 2018, the Company had 139 holders of record of its common stock. A substantially greater number of holders of the Company’s common stock are “street name” or beneficial holders whose shares are held by banks, brokers and other financial institutions.

The Company has not paid cash dividends on its common stock or other securities. The Company currently anticipates that it will retain its future earnings, if any, for use in the expansion and operation of its business and does not anticipate paying any cash dividends on its common stock in the foreseeable future.

The Company did not repurchase any of its common stock during the fiscal year ended May 31, 2018.

PERFORMANCE MEASUREMENT COMPARISON

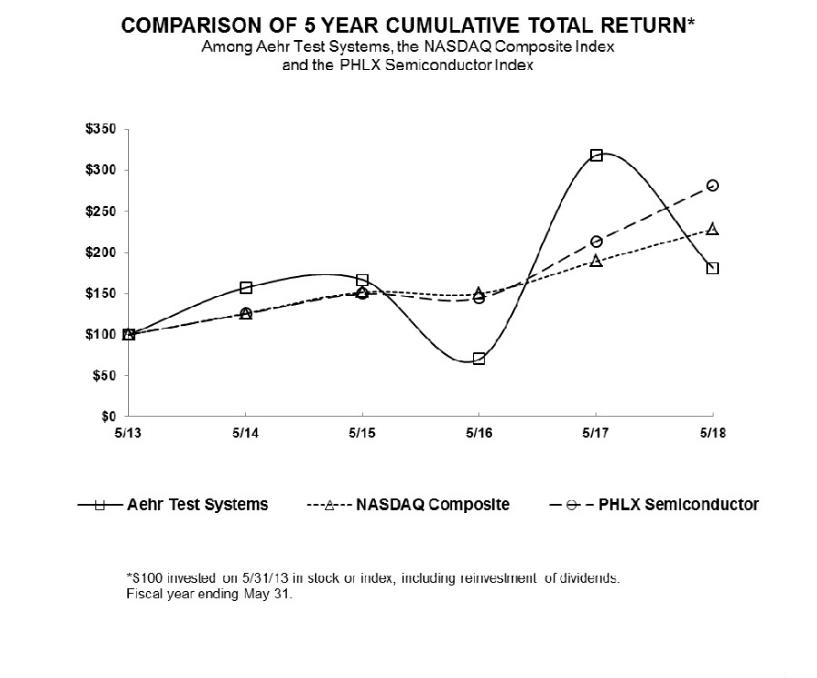

The following graph shows a comparison of total shareholder return for holders of the Company's common stock for the last five fiscal years ended May 31, 2018, compared with the NASDAQ Composite Index and the Philadelphia Semiconductor Index. The graph assumes that $100 was invested in the Company's common stock, in the NASDAQ Composite Index and the Philadelphia Semiconductor Index on May 31, 2013, and that all dividends were reinvested. The Company believes that while total shareholder return can be an important indicator of corporate performance, the stock prices of semiconductor equipment companies like us are subject to a number of market-related factors other than company performance, such as competitive announcements, mergers and acquisitions in the industry, the general state of the economy and the performance of other semiconductor equipment company stocks. Stock prices and shareholder returns over the indicated period should not be considered indicative of future stock prices or shareholder returns.

Item 6. Selected Consolidated Financial Data

The selected consolidated financial data set forth below should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and related notes included elsewhere in this Annual Report on Form 10-K. The selected consolidated financial data in this section are not intended to replace the consolidated financial statements and are qualified in their entirety by the consolidated financial statements and related notes thereto included elsewhere in this Annual Report on Form 10-K.

We derived the statements of operations data for the years ended May 31, 2018, 2017 and 2016 and the balance sheet data as of May 31, 2018 and 2017 from our audited consolidated financial statements and related notes, which are included elsewhere in this Annual Report on Form 10-K. We derived the statements of operations data for the years ended May 31, 2015 and 2014 and the balance sheet data as of May 31, 2016, 2015 and 2014 from our audited consolidated financial statements and related notes which are not included in this Annual Report on Form 10-K. We have not declared or distributed any cash dividends.

| | Fiscal Year Ended May 31, |

| | | | | | |

| | (In thousands, except per share data) |

| CONSOLIDATED STATEMENTS OF OPERATIONS: | | | | | |

| | | | | | |

| Net sales | $29,555 | $18,898 | $14,501 | $10,018 | $19,684 |

| | | | | | |

| Cost of sales | 17,169 | 12,118 | 9,356 | 6,180 | 9,462 |

| Gross profit | 12,386 | 6,780 | 5,145 | 3,838 | 10,222 |

| | | | | | |

| Operating expenses: | | | | | |

| Selling, general and administrative | 7,290 | 7,052 | 6,975 | 6,470 | 6,323 |

| Research and development | 4,181 | 4,657 | 4,324 | 4,062 | 3,402 |

| | | | | | |

| Total operating expenses | 11,471 | 11,709 | 11,299 | 10,532 | 9,725 |

| | | | | | |

| Income (loss) from operations | 915 | (4,929) | (6,154) | (6,694) | 497 |

| | | | | | |

| Interest expense | (399) | (678) | (605) | (130) | (26) |

| Other (expense) income, net | (61) | (21) | (16) | 211 | (64) |

| | | | | | |

| Income (loss) before income tax benefit (expense) | 455 | (5,628) | (6,775) | (6,613) | 407 |

| | | | | | |

| Income tax benefit (expense) | 73 | (25) | (10) | (34) | 15 |

| Net income (loss) | 528 | (5,653) | (6,785) | (6,647) | 422 |

| Less: Net income attributable to the noncontrolling interest | -- | -- | -- | -- | -- |

| | | | | | |

| Net income (loss) attributable to Aehr Test Systems common shareholders | $528 | $(5,653) | $(6,785) | $(6,647) | $422 |

| Net income (loss) per share: | | | | | |

| Basic | $0.02 | $(0.35) | $(0.52) | $(0.55) | $0.04 |

| Diluted | $0.02 | $(0.35) | $(0.52) | $(0.55) | $0.04 |

| | | | | | |

| Shares used in per share calculations | | | | | |

| Basic | 21,732 | 16,267 | 13,091 | 12,047 | 10,877 |

| Diluted | 22,782 | 16,267 | 13,091 | 12,047 | 11,889 |

| | |

| | | | | | |

| CONSOLIDATED BALANCE SHEETS: | | | | | |

| Cash and cash equivalents | $16,848 | $17,803 | $939 | $5,527 | $1,809 |

| Working capital | 18,308 | 21,494 | 4,068 | 7,776 | 6,556 |

| Total assets | 30,955 | 30,892 | 10,046 | 14,868 | 12,225 |

| | | | | | |

| Long-term obligations, less current portion | 522 | 6,214 | 6,089 | 3,799 | 79 |

Total shareholders' equity (deficit) | 19,285 | 16,794 | (723) | 4,550 | 7,029 |

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis of the financial condition and results of operations should be read in conjunction with our “Selected Consolidated Financial Data” and our consolidated financial statements and related notes included elsewhere in this Annual Report on Form 10-K.

OVERVIEW

We were founded in 1977 to develop and manufacture burn-in and test equipment for the semiconductor industry. Since our inception, we have over 2,500 systems installed at semiconductor manufacturers, semiconductor contract assemblers and burn-in and test service companies worldwide. Our principal products currently are the Advanced Burn-in and Test System, or ABTS, the FOX full wafer contact and singulated die/module parallel test and burn-in system, WaferPak Aligner, WaferPak contactors, DiePak Loader, the DiePak carriers and test fixtures.

Our net sales consist primarily of sales of systems, WaferPak Aligners and DiePak Loaders, WaferPak contactors, DiePak carriers, test fixtures, upgrades and spare parts, revenues from service contracts, and engineering development charges. Our selling arrangements may include contractual customer acceptance provisions, which are mostly deemed perfunctory or inconsequential, and installation of the product occurs after shipment and transfer of title.

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

Our discussion and analysis of our financial condition and results of operations are based upon our consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States of America. The preparation of these consolidated financial statements requires us to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses, and related disclosure of contingent assets and liabilities. On an ongoing basis, we evaluate our estimates, including those related to customer programs and incentives, product returns, bad debts, inventories, investments, income taxes, financing operations, warranty obligations and long-term service contracts, among others. Our estimates are derived from historical experience and on various other assumptions that are believed to be reasonable under the circumstances. Those results form the basis for making judgments about the carrying values of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates under different assumptions or conditions.