UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

ANNUAL REPORT PURSUANT TO SECTION 13 OF THE SECURITIES EXCHANGE

ACT OF 1934 FOR THE FISCAL YEAR ENDED SEPTEMBER 30, 2005

Commission File No. 0-29320

EIGER TECHNOLOGY, INC.

(Exact name of Registrant as specified in its charter)

Ontario, Canada

(Jurisdiction of incorporation or organization)

144 Front Street West, Suite 700

Toronto, Ontario M5J 2L7

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act:None

Securities registered or to be registered pursuant to Section 12(g) of the Act:

Common Shares, without par value

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

Indicate the number of outstanding shares of each of the Issuer's classes of capital or common stock as of the close of the period covered by the annual report: 38,860,174 Common Shares without par value.

Check whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [ X ]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes [ X ] No [ ]

Indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 [ ] Item 18 [ X ]

The Index to Exhibits

is found at Page 38

FORWARD LOOKING STATEMENTS

Forward-Looking Information is Subject to Risk and Uncertainty. This report contains certain “forward-looking statements” within the meaning of the U.S. Private Securities Litigation Reform Act of 1995. When used in this report, the words "estimate," "project," "intend," "expect," “anticipate” and similar expressions are intended to identify forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this report. These statements are subject to risks and uncertainties that could cause actual results to differ materially from those contemplated in such forward-looking statements. Such risks and uncertainties include, but are not limited to, those identified under the subheading “Risk Factors” in Item 3 hereof.

GLOSSARY

The following is a glossary of some terms that appear in the discussion of the business of Eiger Technology, Inc. (“the Company”) as contained in this Annual Report.

The following is a glossary of some terms that appear in the discussion of the business of the Company as contained in this Annual Information Form.

| “electronic ballast” | A component that starts a fluorescent lamp. |

| “peripherals” | A peripheral is a device, which can be attached to a PC and is controlled by its processor. Examples include printers and modems. |

| “VoIP” | Voice over Internet Protocol is a term used in telecommunications for a set of facilities for managing the delivery of voice information over broadband. A major advantage of VoIP is that it avoids the tolls charged by ordinary telephone service. |

| 2 |

TABLE OF CONTENTS

Page

| 3 |

PART I

Item 1. Identity of Directors, Senior Management and Advisers

Not Applicable.

Item 2. Offer Statistics and Expected Timetable

Not Applicable.

Item 3. Key Information

A.Selected financial data.

The selected consolidated financial information set out below has been obtained from financial statements that reflect the Company’s business operations. The financial statements have been prepared in accordance with accounting principles generally accepted in Canada. For reconciliation to US GAAP refer to Note 17 of the attached audited statements. The following table summarizes information pertaining to operations of the Company for the last five years ended September 30, 2005.

| 2005 | 2004 | 2003 | 2002 | 2001 | |

| Working Capital | ($1,743,000) | ($3,255,000) | ($409,000) | $4,941,000 | $4,942,000 |

| Revenue | $4,904,000 | $5,754,000 | $4,932,000 | $1,917,000 | $234,000 |

| Income (Loss) from | |||||

| Operations: | ($1,460,000) | ($1,940,000) | ($1,184,000) | ($3,032,000) | ($940,000) |

| Income (Loss) from | |||||

| Continuing Operations: | ($1,460,000) | ($2,276,000) | ($1,184,000) | ($3,032,000) | ($940,000) |

| Net Income (Loss): | ($3,946,000) | ($6,180,000) | ($7,551,000) | ($5,032,000) | ($20,327,000) |

| Earnings (Loss) per Share: | ($0.10) | ($0.16) | ($0.21) | ($0.14) | ($0.59) |

| Total Assets: | $1,940,000 | $7,309,000 | $15,778,000 | $23,758,000 | $30,721,000 |

| Net Assets: | ($176,000) | $3,532,000 | $9,317,000 | $16,418,000 | $21,127,000 |

| Long Term Debt: | $0 | $82,000 | $163,000 | $590,000 | $1,014,000 |

| Total Liabilities: | $2,116,000 | $3,777,000 | $6,461,000 | $7,340,000 | $10,265,000 |

| Share Capital: | $43,297,000 | $43,297,000 | $42,685,000 | $42,235,000 | $42,235,000 |

| Retained Earnings | |||||

| (Deficit): | ($44,806,000) | ($39,765,000) | ($33,585,000) | ($26,034,000) | ($21,091,000) |

| Number of Shares: | 38,860,174 | 38,860,174 | 37,608,951 | 36,615,853 | 36,215,853 |

| 4 |

CURRENCY EXCHANGE INFORMATION

The Company’s accounts are maintained in Canadian dollars. In this Annual Report, all dollar amounts are expressed in Canadian dollars except where otherwise indicated.

The following table sets forth, for the periods indicated, the high and low rates of exchange of Canadian dollars into United States dollars, the average of such exchange rates on the close of each day during the periods, and the end of period rates. Such rates are shown as, or are derived from, the reciprocals of the Bank of Canada nominal noon exchange rates in Canadian dollars.

| Fiscal Year Ended | |||||

| September 30 | |||||

| 2005 | 2004 | 2003 | 2002 | 2001 | |

| High | 0.8630 | 0.7912 | 0.7506 | 0.6654 | 0.6711 |

| Low | 0.7840 | 0.7159 | 0.6254 | 0.6179 | 0.6319 |

| Average | 0.8176 | 0.7550 | 0.6854 | 0.6359 | 0.6515 |

| Period | 0.8630 | 0.7912 | 0.7408 | 0.6300 | 0.6335 |

On March 17, 2006 the exchange rate of Canadian dollars into United States dollars, based upon the Bank of Canada nominal noon exchange rate was Cdn. $1.00 equals U.S. $0.8630.

The following table sets forth, for the most recent previous six months, the high and low rates of exchange of Canadian dollars into United States dollars. The latest practicable date for March was on March 17, 2006.

| MAR | FEB | JAN | DEC | NOV | OCT | |

| 2006 | 2006 | 2006 | 2005 | 2005 | 2005 |

| High | 0.8832 | 0.8787 | 0.8742 | 0.8690 | 0.8597 | 0.8613 |

| Low | 0.8607 | 0.8637 | 0.8528 | 0.8522 | 0.8361 | 0.8413 |

| 5 |

B.Capitalization and indebtedness.

Not Applicable.

C.Reasons for the offer and use of proceeds.

Not Applicable.

D.Risk factors.

The Company’s operations are subject to a variety of risks and uncertainties. The following factors are to be considered a list of known material risks that are specific to the Company or its industries.

Management of the Growth of the Company

The implementation of the Company’s business strategy could result in a period of rapid growth. This growth could place a strain on the Company’s managerial, operational and financial resources and information systems. Future operating results will depend on the ability of senior management to manage rapidly changing business conditions, and to implement and improve the Company’s technical, administrative, financial control and reporting systems. No assurance can be given that the Company will succeed in these efforts. The failure to effectively manage and improve these systems could increase the Company’s costs and adversely affect its ability to sell and deliver its products and services.

Competition

The Company faces competition in each of its markets and has competitors, many of which are larger and have greater financial resources than the Company. There can be no assurance that the Company will be able to continue to compete successfully in its markets. Because the Company competes, in part, on the technical advantages and cost of its products, significant technical advances by competitors or the achievement by such competitors of improved operating effectiveness that enable them to reduce prices could reduce the Company’s competitive advantage in these products and thereby adversely affect the Company’s business and financial results.

New Products and Technological Change

The market for the Company’s products is characterized by rapidly changing technology, evolving industry standards and frequent new product introductions, which may be comparable or superior to the Company’s products. The Company’s success will depend upon market acceptance of its existing products and its ability to enhance its existing products and to introduce new products and features to meet changing customer requirements. There can be no assurance that the Company will be successful in identifying, manufacturing and marketing new products or enhancing its existing

| 6 |

products on a timely and cost-effective basis or, that such new products will achieve market acceptance. In addition, there can be no assurance that products or technologies developed by others will not render the Company’s products or technologies non-competitive or obsolete.

New Market Development

There can be no assurance that the Company will be able to identify, develop and export to countries or geographic areas in which it is not presently selling.

Going Concern

The Company’s continued existence as a going concern is dependent upon the Company’s ability to raise additional capital, to increase sales, and ultimately become profitable. Should the Company be unable to continue as a going concern, it may be unable to realize the carrying value of its assets and to meet its liabilities as they become due.

Intellectual Property

The Company has not obtained patent protection nor registered trademarks or copyrights for all of its proprietary technology or products. As the Company has not protected all of its intellectual property, its business may be adversely affected by competitors copying or otherwise exploiting features of the Company’s technology, products, information or services.

Dependence on Key Personnel and Skilled Employees

The success of the Company is dependent, in large part, on certain key personnel and on the ability to motivate, retain and attract highly skilled persons. The employment market for skilled technology employees is tight. There can be no assurance that the Company will be able to attract and retain employees with the necessary technical and technological skills given the competitive state of the employment market for these individuals. The loss of such services or the failure by the Company to continue to attract and retain other key personnel may have a material adverse effect on the Company, including its ability to develop new products, its ability to grow earnings and its ability to accelerate revenue growth.

Relationship with Production Employees

Although the employees of the Company are not unionized, there can be no assurance that this will not occur. Management of the Company is of the opinion that the unionization of its operations would have a detrimental effect on the Company’s ability to remain competitive.

Uncertain Operating Results

The Company’s operating results have varied and may continue to vary significantly depending on such factors as the timing of new product announcements, increases in the cost of raw materials and changes in pricing policies of the Company and its competitors. The market price of the Shares may be highly volatile in response to such fluctuations.

| 7 |

Foreign Exchange Rate

Material depreciation of the Canadian dollar against the U.S. dollar may increase certain costs impacting the Company’s profitability and cash flow.

Employment Contracts/Reliance Upon Officers

The Corporation has not entered into an employment contract with all of its executive officers, upon whose personal efforts and abilities the Corporation is largely dependent. The loss or unavailability to the Corporation of these individuals may have a materially adverse effect upon the Corporation's business.

Legal Proceedings Against Foreign Persons

The Corporation’s jurisdiction of incorporation falls under the laws of the Province of Ontario, Canada, and all of the Corporation’s officers and directors are residents of Canada. Consequently, it may be difficult for United States investors to affect service of process within the United States upon the Corporation or its officers and directors, or to realize in the United States upon judgments of United States courts predicated upon civil liabilities under U.S. securities laws. Furthermore, it may be difficult for investors to enforce judgments of the U.S. against the Company or any of the Company’s non-U.S. resident executive officers or directors. There is substantial doubt whether an original lawsuit could be brought successfully in Canada against any of such persons or the Corporation predicated solely upon civil liabilities arising under U.S. securities laws.

Item 4. Information on the Company

A.History and development of the company.

The Company entered the energy efficient lighting business in 1991. The Company’s two main operating subsidiaries in this non-core business have been K-Tronik International Corp. (“KTI”) and ADH Custom Metal Fabricators Inc. (“ADH”). ADH operated from the Company’s 55,000 square foot manufacturing and engineering facility located in Stratford, Ontario. ADH manufactured and distributed transformer housings, switch housings and electronic data racks, as well as fluorescent light fixtures and reflectors. ADH was wound-up in August 2003.

On April 1, 1998, the Company purchased 53% of the common stock of KTI for $275,000, plus options entitling the holders to acquire up to 250,000 common shares of the Company. During fiscal 1998, the Company consolidated two of its South Korean subsidiaries, Energy Products, Inc. (its South Korean energy saving products sales arm) and (a manufacturer of electronic ballasts) and, which were eventually combined under the name “K-Tronik Asia, Inc.” (“KTA”). The Company currently is a 64% shareholder of KTI. On September 15, 2000, the Company sold its 60% interest in Lexatec VR Systems, Inc. to facilitate focussing on Eiger’s core business at the time. On December 15, 2004, KTI entered into an agreement to sell all of its interest in K-Tronik N.A. Inc. (“KTNA”) and the fixed assets of its subsidiary, KTA. Thus, KTI is no longer engaged in the business of manufacturing, distributing or selling electronic ballasts.

| 8 |

The Company entered the computer peripheral business following a series of transactions in September 1999 that has since resulted in the Company owning a 58% interest in Eiger Net of South Korea. This was affected through payment of a US $1,000,000 cash consideration and 500,000 common shares of the Company issued for a combined aggregate value of US $1,500,000. Additionally, 600,000 common shares of the Company were issued on February 29, 2000 pursuant to this agreement. On July 31, 2004, the remaining operating management shareholders of Eiger Net, Inc. in South Korea acquired Eiger’s interest in Eiger Net, Inc. for a nominal sum as required by South Korean law. As such, the purchasers will assume all of the outstanding liabilities of Eiger Net, Inc. as at that date.

The Company entered into the VoIP telecom services business when, through Onlinetel Corp., it acquired 100% of the shares of Onlinetel, Inc. through a Share Exchange agreement under the provisions of Chapter 92a of the NGCL (Nevada General Corporate Law). 99.97% of Onlinetel’s shares have been exchanged pursuant to the Share Exchange Agreement. Eiger has issued 1,800,000 shares on a pro rata basis for 100% of the shares of Onlinetel, Inc.

As consideration for the acquisition of Onlinetel, Inc. Eiger would issue a maximum of 9,000,000 common shares, which would be comprised of 1,800,000 shares issued to the former shareholders of Onlinetel and up to an additional 7,200,000 shares pursuant to an earn out provision totalling 1,800,000 shares per year, over a period of four years, with possible extension provisions for an additional period of four years, based on Onlinetel’s ability to meet the following operating benchmarks and Eiger’s approval:

| 2002 | 2003 | 2004 | 2005 | |

| REVENUE | $19,083,488 | $37,347,766 | $50,849,180 | $59,867,184 |

| NET INCOME | $2,442,015 | $6,212,532 | $9,352,747 | $13,848,741 |

Under the formula in the agreements, if any of the above targets was not met in any of the above noted years, any gross sales or net income earned or achieved in that year would be added to the targets of subsequent years. The common shares of the Company to be issued in respect of those targets would be considered cumulative and could be achieved in any subsequent year in respect of the terms of the agreement, if extensions were granted by Eiger.

On March 18, 2004, Newlook Industries Corp. (“Newlook”) completed an agreement to acquire 100% of the outstanding common shares of Onlinetel by issuing 12,727,273 common shares of Newlook to Eiger. A further 7,272,727 common shares were issued to Eiger in settlement of $1,200,000 of debt owing from Onlinetel to Eiger. Immediately prior to the transaction, Eiger owned 100% of the shares of Onlinetel, and over 80% of the shares of Newlook.

| 9 |

Recent Financings

2006 Newlook Private Placement

On February 8, 2006, subsidiary Newlook closed a non-brokered private placement of 500,000 units in its securities at a price of $0.75 per unit. Each unit is comprised of one share and one-half share purchase warrant. The warrants, each of which is convertible to one common share upon exercise, are exercisable for a period of one year at an exercise price of $1.00 per warrant. As the private placement was fully subscribed, Newlook received proceeds of $375,000. If the warrants are fully exercised, Newlook will receive an additional $250,000.

2004 Newlook Private Placement

On March 18, 2004, subsidiary Newlook closed a private placement of 1,000,000 units of its securities at a price of $1.00 per unit. Each unit is comprised of one share and one warrant. Each warrant is convertible to one common share for a period of two years at an exercise price of $0.50 per share. The private placement was fully subscribed, for which Newlook received proceeds of $1,000,000.

March 2003 Private Placement

On March 27, 2003, the Company closed a private placement of units at $0.45 with a 1-year warrant to purchase an additional share for $0.55. The shares and warrants comprising the private placement carried a hold period of four months commencing from the date of their issuance, being July 26, 2003. Insiders of the company purchased a total of 310,598 units at $0.46 per unit. The higher price to insiders resulted in the issuance of 993,098 units for total proceeds of $450,000.

Other Recent Developments

Eiger takes Onlinetel Public

Newlook closed its acquisition of all the issued and outstanding shares of Onlinetel from Eiger on March 18, 2004. On November 18, 2003, Newlook entered into the agreement to acquire all of the issued and outstanding shares of Onlinetel from Eiger. As consideration for the acquisition, Newlook was to issue a total of 20,000,000 common shares to Eiger at $0.165 per share for a deemed value for the transaction of $3,200,000. On February 18, 2004, Newlook entered into an agreement to settle $1,200,000 of debt which was owed by Onlinetel to Eiger by issuing 7,272,727 common shares to Eiger. Concurrently with the signing of the debt settlement agreement, the Onlinetel agreement was amended to reduce to 12,727,273 the number of shares issued to Eiger as consideration for the Onlinetel shares. The February 18, 2004 amendment to the Onlinetel agreement and the debt settlement agreement did not change the total number of shares to be issued to Eiger by the Company. This number remained at 20,000,000. The 20,000,000 shares of Newlook issued to Eiger under the terms of the Onlinetel agreement and the debt settlement agreement are subject to a six year Tier II surplus security escrow agreement.

| 10 |

Eiger takes K-Tronik Public

On January 21, 2004, Eiger’s majority-owned subsidiary, KTI commenced trading on the NASDAQ OTCBB under the symbol “KTRK”. Eiger currently owns 14.4 million common shares or 64% of KTI. KTI has since ceased active operations (see “Business Overview” below).

B.Business overview.

The Company has two principal subsidiaries, namely, Newlook Industries Corp. and K-Tronik International Corp.

NEWLOOK INDUSTRIES CORP.

Newlook has a 100% ownership stake in Onlinetel Corp., a next-generation telecommunications software and services company, which harnesses the power of proprietary soft-switch technology to deliver state-of-the-art Voice over Internet Protocol (VoIP) communication services to individuals, businesses and carriers. Utilizing soft switch technology, Onlinetel converts analog voice conversations to digital I.P. packets and routes voice calls, phone-to-phone, over broadband from any wireless or landline connection. The integration of voice and data networks eliminates the need for traditional telecom services and provides a substantial increase in communication cost efficiencies.

By leveraging its technology platform and scalable network infrastructure, Onlinetel has taken advantage of disruptive pricing and delivers multiple communication offerings to its customers. Onlinetel offers telephony services for international calling, long distance calling subscriptions plans and Internet access. Through its Intelliswitch application, Onlinetel has pioneered and developed a new media for advertisers, enabling individuals and businesses to benefit from free long distance while sponsors benefit from one-to-one advertisements to callers. Through the use of the proprietary “Ad-Tree” software, sponsors are able to focus on a targeted consumer base.

Onlinetel delivers toll-quality communications at some of the most competitive long distance rates possible. With reduced investment cost burdens, Onlinetel’s soft-switch technology reliably scales to service millions of callers. Onlinetel’s continued expansion of its own national network along with seamless and virtual connections worldwide with leading carriers extends Onlinetel’s reach to the global community. Onlinetel’s operations have been serving the Canadian market for over 15 years.

K-TRONIK INTERNATIONAL CORP.

KTI is no longer engaged in the business of manufacturing, distributing or selling electronic ballasts and is considered to have re-entered the development stage at December 15, 2004. KTI is currently seeking another acquisition or business opportunity.

Description of Principal Products

Newlook serves the retail and business market segments of the long distance industry across Canada through its subsidiary, Onlinetel. Onlinetel’s foundation blocks are a national and scalable VoIP network infrastructure, toll-quality service and offering

| 11 |

competitive long distance rates. Upon these foundation blocks, Onlinetel provides multiple products and services, producing four main revenue streams. These revenue streams include:

| 1. | Call Zone/Call World – Free, sponsor-subsidized, ad-based provincial calling with no-ad international calling. | |

| 2. | Subscription Plans – Traditional long distance and Internet plans for the residential and small office/home office (“SOHO”) market. | |

| 3. | Advertising - New media services for sponsors on the Call Zone free calling network. | |

| 4. | 10-10-580 - Dial-around services for pay-per-call domestic and international calling. |

| Sales and Revenue Analysis | |||

| Sales | Fiscal 2005 | Fiscal 2004 | Fiscal 2003 |

| Telecommunication Services | $ 4,904,000 | $ 5,754,000 | $ 4,932,000 |

The VoIP-based telecommunication services are offered to the Canadian market. The electronic ballasts, computer peripherals and fabricated products businesses have been discontinued. The Company’s main business is not materially seasonal.

Marketing and Distribution Channels

The Company’s Newlook subsidiary markets its telephony services through various advertising and promotional medium, including its own advertising based calling network and internal sales staff. By focusing on delivering Canadians a toll-quality, premium-value service offering competitive national rates, the subscription base has expanded through customers’ word of mouth.

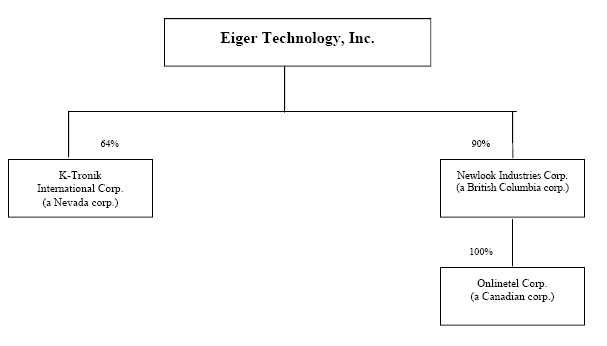

C.Organizational structure.

The following is a list of each material subsidiary of the Company and the jurisdiction of incorporation and the direct or indirect percentage ownership by the Company of each subsidiary:

| Jurisdiction of | Percentage of Voting | |

| Name of Subsidiary | Organization | Securities Owned of |

| Controlled | ||

| Newlook Industries Corp. (“Newlook”) | British Columbia | 90% |

| K-Tronik International Corp. (“KTI”) | Nevada | 64% |

The following is an organizational chart showing the Company’s material subsidiaries:

| 12 |

D. Property, plants and equipment.

The Company’s current property, plants and equipment are comprised primarily of telecommunications and computer equipment. The Company currently owns no real estate.

Item 5. Operating and Financial Review and Prospects

The information provided in this section endeavors to summarize the company’s financial condition and results of operations for the periods specified, including the causes for material changes to provide an understanding of the company’s business as a whole. The information also attempts to relate all separate segments of the company. The discussion provided therein should be read in conjunction with the Company’s consolidated financial statements and related notes.

A.Operating results.

Comparative Analysis Between Fiscal 2005 and 2004

For the fiscal year ended September 30, 2005, Eiger’s net loss from continuing operations of $1.5 million ($0.04 per share) improved 36% from $2.3 million ($0.06 per share) during the prior year. These include net non-cash expenses amounting to $943,000 in fiscal 2005 and $38,000 in fiscal 2004. Reported net loss (including non-recurring and discontinued operations) of $4.0 million ($0.10 per share) compared to $6.2 million ($0.16 per share) during the previous year. Revenues for the period were $4.9 million, compared to $5.8 million in the preceding year.

| 13 |

Eiger’s consolidated operating expenses from continuing operations of $2.5 million (including 700,000 of non-cash items) for the year ended September 30, 2005 decreased 30% from $3.6 million (including 334,000 of non-cash items) in fiscal 2004. The largest component of operating expenses is selling, general and administrative expenses (“SG&A”), which consists primarily of salaries and benefits, and the operating costs associated with sales. Consolidated SG&A of $1.7 million for the year ended September 30, 2005 decreased 44% from $3.0 million in fiscal 2004.

On December 15, 2004, KTI entered into an agreement to sell all of its interest in KTNA and the fixed assets of its subsidiary, KTA. As such, KTI is no longer engaged in the business of manufacturing, distributing or selling electronic ballasts and therefore, KTI results for the fiscal year are presented as discontinued operations on the financial statements for fiscal 2005.

Subsidiary Newlook’s total revenues for fiscal 2005 were $4.9 million versus $5.7 million in the previous year. Net loss from continuing operations for the fiscal year was $541,000 ($0.02 per share), compared to $2.4 million ($0.14 per share) in fiscal 2004. Net loss was $580,000 ($0.02 per share; including $39,000 from discontinued operations) vis a vis a net loss of $2.7 million ($0.14 per share; including $288,000 from discontinued operations) in the prior year.

During the fiscal year, Newlook’s gross margin increased to $1.3 million (27% margin) in fiscal 2005 from $960,000 (17% margin) over the prior period, despite a 15% decline in revenues year-over-year. The mix in revenues changed substantially during the fiscal year as the Newlook focused on Call Zone, a sponsor-subsidized, ad-based provincial calling service launched in October 2003 as well as the Call World international calling service launched in March 2004 that is made available to all Call Zone subscribers. Call World currently offers special rates such as to Canada and the U.S. for 2.9 cents per minute among others.

The improvement in Newlook’s gross profit margin in the year was due mainly to a change in the composition of sales and lower network costs. A significant portion of revenues in fiscal 2005 came from a corporate focus on Call Zone, which was more established relative to the prior “launch” year. In fiscal 2004, the Newlook launched its own proprietary ad-based calling network. As such, the focus over fiscal 2004 had been to build up a proprietary subscriber base at the expense of generating a large proportion of revenues from advertising. To attract sponsors to advertise on the Call Zone network, a large enough pool of advertising capacity has to be created to be able to offer the exposure certain sponsors require to meet their basic advertising demands. It is anticipated that the initiatives developed in fiscal 2004 and 2005 to build, develop and expand the proprietary ad-based network will provide the Newlook significant opportunities to sell sponsor time on the network in fiscal 2006 and into the future. As advertising becomes a greater component of overall revenues in the future, it is anticipated that gross margins will increase accordingly.

| 14 |

Newlook’s SG&A expenses decreased in fiscal 2005 by 49% to $1.2 million from $2.3 million in the prior year due mainly to a strategy to reduce costs such as advertising, promotion, human resources and those related to the development and deployment of the expanded VoIP system. A major advertising and promotional campaign was embarked in fiscal 2004 to coincide with the expansion of the Call Zone in Ontario and Quebec. The initiative was not met with any success. In fiscal 2005, the size of management had been scaled back and all call centre functions became in-house after having been expanded and outsourced to accommodate for enhanced hours of operation and French-speaking capabilities in the previous year. Additionally, Onlinetel was located in Toronto for the entire year, having been in Kitchener for most of fiscal 2004.

Newlook’s financial expenses decreased to $157,000 during the fiscal year from $268,000 in the prior year chiefly due to the interest paid as part of the equipment lease obligations the Newlook made in order to expand its VoIP network and establish Call Zone in Ontario, Quebec and Alberta during fiscal 2004. The lease terms established were aggressive, in that they are to be paid over a 24 month period. As these terms expire between May 31, 2005 to March 31, 2006, financial expenses will likely decline and the resultant cash flow is anticipated to increase dramatically.

For fiscal 2005, Newlook’s positive EBITDA (earnings before interest, taxes, depreciation and amortization) of $56,000 (including $70,000 of non-cash expenses) improved significantly from an EBITDA loss of $1,363,000 in the prior year. Cash EPS was $0.00 for the fiscal year versus negative $0.09 in the previous year.

In 2004, Newlook had overpaid commodity taxes to the provincial government in the amount of $258,000. Even though this overpayment was discovered and refunded in 2005, the correction of this error has been accounted for retroactively with a restatement of the prior year’s amounts. As a result of this restatement, Newlook’s fiscal 2004 sales and accounts receivable were increased by $258,000 and the net loss from continuing operations decreased by $258,000.

During fiscal 2004, Newlook management determined that there was an impairment of the goodwill and as a result, goodwill of $336,172 was charged to income for the year. Additionally, a $98,000 future income tax asset taken in fiscal 2003 was reversed during the subsequent year as management determined that it not likely at this point to be realized through the reduction of future income tax payments.

Eiger believes it has sufficient capital to support expected operating levels at its current subsidiaries. Consolidated cash and marketable securities at September 30, 2005 was $33,000 compared to $27,000 at September 30, 2004. The Company’s consolidated accounts receivable decreased to $586,000 from $1.1 million and consolidated accounts payable, accrued liabilities and other payable increased to $2.0 million from $1.9 million over the year ended September 30, 2004. Total consolidated debt (capital lease obligations) at fiscal year end was $82,000 compared to $462,000 at September 30, 2004.

| 15 |

At September 30, 2005, Newlook’s cash position of $39,000 had not changed significantly from $55,000 at the prior year-end. Net equipment decreased by 27% to $1.1 million at year-end due to amortization taken on the telecommunications equipment acquired for the expansion of Onlinetel’s VoIP telecom network in Ontario, Quebec and Alberta.

Newlook’s accounts receivable of $584,000 dropped from $999,000 over the year as a lower emphasis was put on the dial-around business, which relies on a third party for billing and collection services. To a lesser extent, the wholesale business was more prevalent in fiscal 2004, and is more collection-intensive than the other revenue streams. Additionally, the fiscal 2004 year end receivables balance has been restated to include $258,000 owing from the provincial government for commodity tax overpayments discovered in 2005.

Newlook’s accounts payable and accrued charges of $727,000 and other payable of $923,000 at September 30, 2005 were collectively lower than $1.9 million in the prior year as positive cash flow was applied to pay down supplier accounts. Long-term debt including current portion decreased to $82,000 at year end from $462,000 at the previous year as a result of the equipment leases being paid down and expiring. Deferred revenue of $387,000 in fiscal 2005 relates to subscription fees for the Call Zone calling plan launched during the prior year. As the subscription is for a one-year term of service, the fee is amortized on a monthly basis over the one-year period and the revenue is deferred until earned. Advances from parent company increased marginally over the year to $2,289,000 from $2,052,084 to reflect payments made by Eiger for Newlook.

Concurrent with the closing of the Onlinetel acquisition in fiscal 2004, Newlook closed a private placement of 1,000,000 units of its securities at a price of $1.00 per unit. Each unit was comprised of one share and one warrant. Each warrant is convertible to one common share for a period of two years at an exercise price of $0.50 per share. The private placement was fully subscribed, for which Newlook received proceeds of $1,000,000. If all warrants are exercised, Newlook will receive an additional $500,000 in fiscal 2006.

Comparative Analysis Between Fiscal 2004 and 2003

For the fiscal year ended September 30, 2004, net loss before non-recurring items of $1,940,000 ($0.05 per share) increased 64% from $1,184,000 ($0.03 per share) during the prior year. Reported net loss (including discontinued operations and non-recurring items) of $6,180,000 ($0.16 per share) decreased 18% from $7,551,000 ($0.21 per share) during the previous year. Revenues for the period were $5,754,000, compared to $4,932,000 in the preceding year.

Consolidated operating expenses from continuing operations of $3,548,000 for the year ended September 30, 2004 increased 39% from $2,544,000 in fiscal 2003 due largely from an increase in selling, general and administrative expenses (“SG&A”), which consists primarily of salaries and benefits, and the operating costs associated with sales.

| 16 |

Consolidated SG&A of $2,944,000 for the year ended September 30, 2004 increased 40% from $2,108,000 in fiscal 2003.

During the year, Company management determined that there was an impairment of the goodwill and as a result, goodwill of $336,172 was charged to income for the year. Additionally, a $98,000 future income tax asset taken in fiscal 2003 was reversed during the year as management determined that it not likely at this point to be realized through the reduction of future income tax payments.

In an effort to focus on the long-term profitability of its core publicly-traded subsidiaries, the Company reached an agreement, effective July 31, 2004, to sell its interest in Eiger Net, Inc. to the non-controlling shareholders for a nominal amount. The purchasers assumed all of the outstanding liabilities of Eiger Net as at that date. On November 30, 2004, Alexa Properties sold its property in Stratford, Ontario and no longer has active business operations. On December 15, 2004, K-Tronik International Corp. entered into an agreement to sell all of its interest in K-Tronik North America Corp. and the fixed assets of its subsidiary, K-Tronik Asia Corp. As such, K-Tronik International Corp. will no longer be engaged in the business of manufacturing, distributing or selling electronic ballasts. Therefore, Eiger Net, Alexa Properties and K-Tronik results for the fiscal year are presented as discontinued operations on the Statement of Operations and Retained Earnings. This loss from discontinued operations is comprised of $2,504,000 from operational losses and $1,400,000 from disposal of assets. In comparison, the loss from discontinued operations for fiscal 2003 is comprised of $3,735,000 from operational losses and $2,632,000 from disposal of assets.

Subsidiary Newlook’s total revenues for fiscal 2004 were $5,738,877 versus $4,931,993 in the previous year. Operating loss before non-recurring items (relating to a write-down of goodwill and loss on disposal of assets due to the discontinuance of operations of ADH Custom Metal Fabricators Inc.) for the fiscal year was $1,940,120, compared to $263,101 in fiscal 2003. Net loss (including non-recurring items) for the fiscal year was $2,661,955 versus $2,095,512 in the previous year.

During the fiscal year, Newlook experienced an 16% increase in overall revenues. The mix in revenues changed substantially during the fiscal year relative to the prior year as new revenue streams were added, which currently are the focus of future growth and development. These include Call Zone, a sponsor-subsidized, ad-based provincial calling service launched in October 2003 as well as the Call World international calling service launched in March 2004 that was made available to all Call Zone subscribers. Call World currently offers special rates such as to Canada and the U.S. of 2.9 cents per minute among others.

Newlook’s gross profit margin declined from 23% in fiscal 2003 to 17% in the year due mainly to a change in the composition of sales. A significant portion of revenues in fiscal 2003 were the result of higher margin advertising revenue from a promotion with a major advertiser. For fiscal 2004, Newlook launched its own proprietary ad-based calling network. As such, the focus over fiscal 2004 had been to build up a proprietary subscriber

| 17 |

base at the expense of generating a large proportion of revenues from advertising. To attract sponsors to advertise on the Call Zone network, a large enough pool of advertising capacity has to be created to be able to offer the exposure certain sponsors require to meet their basic advertising demands. It is anticipated that the initiatives developed in fiscal 2004 to build, develop and expand the proprietary ad-based network will provide Newlook significant opportunities to sell sponsor time on the network in the future. As advertising becomes a greater component of overall revenues in the future, it is anticipated that gross margins will increase accordingly.

Newlook’s selling, general and advertising expenses increased in fiscal 2004 to $2,323,251 from $1,041,964 in the prior year due mainly to an increase in advertising, promotion, human resources and increased costs related to the development and deployment of the expanded VoIP system. A major advertising and promotional campaign was embarked in the fiscal year to coincide with the expansion of the Call Zone in Ontario and Quebec. The initiative was not met with any success. Human resource costs increased as a result of an initiative to increase the level of telecom management expertise within Newlook. Additionally, certain call centre functions were expanded and outsourced such as the hours of operation and French-speaking capabilities. Today, the level of management has been scaled back and all call centre functions are in-house once again.

Newlook’s financial expenses increased to $268,292 during the fiscal year from $63,713 in the prior year chiefly due to the interest paid as part of the equipment lease obligations Newlook made in order to expand its VoIP network and establish Call Zone in Ontario, Quebec and Alberta. The lease terms established were aggressive, in that they are to be paid over a 24 month period. As these terms expire between May 31, 2005 to April 30, 2006, financial expenses as the resultant cash flow is anticipated to increase.

B.Liquidity and capital resources.

Eiger believes it has sufficient capital to support expected operating levels at its current subsidiaries. Consolidated cash and marketable securities at September 30, 2005 was $33,000 compared to $27,000 at September 30, 2004. The Company’s consolidated accounts receivable decreased to $586,000 from $1.1 million and consolidated accounts payable, accrued liabilities and other payable increased to $2.0 million from $1.9 million over the year ended September 30, 2004. Total consolidated debt (capital lease obligations) at fiscal year end was $82,000 compared to $462,000 at September 30, 2004.

At September 30, 2005, Newlook’s cash position of $39,000 had not changed significantly from $55,000 at the prior year-end. Net equipment decreased by 27% to $1.1 million at year-end due to amortization taken on the telecommunications equipment acquired for the expansion of Onlinetel’s VoIP telecom network in Ontario, Quebec and Alberta.

Newlook’s accounts receivable of $584,000 dropped from $999,000 over the year as a lower emphasis was put on the dial-around business, which relies on a third party for

| 18 |

billing and collection services. To a lesser extent, the wholesale business was more prevalent in fiscal 2004, and is more collection-intensive than the other revenue streams. Additionally, the fiscal 2004 year end receivables balance has been restated to include $258,000 owing from the provincial government for commodity tax overpayments discovered in 2005.

Newlook’s accounts payable and accrued charges of $727,000 and other payable of $923,000 at September 30, 2005 were collectively lower than $1.9 million in the prior year as positive cash flow was applied to pay down supplier accounts. Long-term debt including current portion decreased to $82,000 at year end from $462,000 at the previous year as a result of the equipment leases being paid down and expiring. Deferred revenue of $387,000 in fiscal 2005 relates to subscription fees for the Call Zone calling plan launched during the prior year. As the subscription is for a one-year term of service, the fee is amortized on a monthly basis over the one-year period and the revenue is deferred until earned. Advances from parent company increased marginally over the year to $2,289,000 from $2,052,084 to reflect payments made by Eiger for Newlook.

On February 8, 2006, Newlook completed a non-brokered private placement of units in its securities at a price of $0.75 per unit. Each unit is comprised of one share and one-half share purchase warrant. The warrants, each of which is convertible to one common share upon exercise, are exercisable for a period of one year at an exercise price of $1.00 per warrant. The private placement had a maximum subscription of 500,000 Units. The private placement was fully subscribed and Newlook received proceeds of $375,000. If the warrants are exercised, Newlook will receive an additional $250,000.

Concurrent with the closing of the Onlinetel acquisition on March 18, 2004, Newlook closed a private placement of 1,000,000 units of its securities at a price of $1.00 per unit. Each unit was comprised of one share and one warrant. Each warrant was convertible to one common share for a period of two years at an exercise price of $0.50 per share. The private placement was fully subscribed, for which Newlook received proceeds of $1,000,000. Newlook received an additional $470,000 from the exercise of warrants in fiscal 2006.

C.Research and development, patents and licenses, etc.

Research and development expenses were nil (nil: 2004; nil: 2003) for the year ended September 30, 2005.

D.Trend information.

The Company is currently affected by several industry trends. One trend is that of the expansion of Voice over Internet Protocol (VoIP) usage in North America. VoIP is expected to a high growth market over the next few years. For example, IDC Canada forecasts that the VoIP market in Canada will have an annual growth rate of 85% and will reach over $442 million in 2006.

| 19 |

According to IDC Canada, total retail VoIP minutes in Canada were estimated at 153 million minutes in 2001 and are expected to grow to 5.5 billion minutes by 2006, for a CAGR of 105%. The impetus for this growth is the competitive threat that VoIP poses to providers of traditional telecom services. Essentially, VoIP substantially increases communication cost efficiencies by running voice and data over a single integrated infrastructure and bypassing traditional per minute telecommunication usage rates.

Through its majority-owned subsidiary, Newlook, Eiger is positioned to play a principal role in the Canadian VoIP services market. Advertising based calling networks have been launched nationally in order to significantly expand its user base and introducing several potentially lucrative VoIP products to its growing user base including lowest cost 10-10 based international calling and residential and corporate flat rate subscription plans for unlimited calling between major centers nationally.

E.Off-balance sheet arrangements.

The Company has no off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on the Company's financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources that are material to investors.

F.Tabular disclosure of contractual obligations.

The following table sets forth the Company’s contractual obligations for the periods indicated:

| Payments Due By Period | |||||

| Contractual Obligations: | Total | < 1 year | 1-3 years | 4-5 years | > 5 years |

| Long-Term Debt(1) | $1,050,000 | $1,050,000 | nil | nil | nil |

| (1)For details of the composition of Company debt, see notes 10 and 11 to the consolidated financial statements. | |||||

Item 6. Directors, Senior Management and Employees

A.Directors and senior management.

The following is a list of the current directors and senior officers of the Company, their municipalities of residence, their current position with the Company and their principal occupations:

Gerry A. RacicotNorwich ON President, C.E.O., and Director Director since August 21, 1992.

Mr. Racicot has a long career in administration, management and self-employment. The majority of these years were spent as an Investment Account Executive at a major Canadian brokerage house (Burns Fry), import/export wholesale distribution and retail business (Red Mountain Holdings Inc. – Stedmans). Mr. Racicot is wholly involved in managing Eiger’s business operations.

| 20 |

Jason R. MorettoVaughan ON C.F.O. and Director Director since January 5, 2004.

Mr. Moretto is a Chartered Financial Analyst and Certified General Accountant whose previous experience includes equity research and practicing as an accountant in both industry and public practice. He also holds a Bachelor of Commerce degree from the University of Toronto. Mr. Moretto is wholly involved in managing Eiger’s business operations.

John G. SimmondsKing ON Director Director since September 20, 2005.

Mr. Simmonds is an entrepreneur with a track record of serving as an executive and on board positions with several communications, wireless and other businesses. Mr. Simmonds is founder of merchant bank Simmonds Capital Ltd., and currently serves as Chairman of Wireless Age Communications Inc., a consolidation of retail, wholesale and engineering businesses within the wireless products and services industry. Mr. Simmonds is involved in managing Eiger’s business operations.

Sidney S. HarkemaOrillia ON Director Director since August 22, 1992.

Mr. Harkema founded and built one of Canada’s largest privately owned transport and express companies (Harkema Trucking Group). He served as President and Chairman of the Board for 27 years. He has since sold the entire trucking operation, cartage equipment and all 18 terminals located throughout the country and has devoted his time to public service organizations (principally as Chairman of the Huntley St. Group of Ministries). Mr. Harkema is not involved in managing Eiger’s daily business operations.

Brian CatoAjax ON Director Director since March 21, 2006.

Mr. Cato has extensive experience in the telecommunications sector. He has held many senior positions with large multinational corporations that include Senior Vice-President and General Manager of ICG Communications, Inc., General Manager with S&P Data and General Manager of Onlinetel Corp. among others. Mr. Cato is a graduate of York University. Mr. Cato is not involved in managing Eiger’s daily business operations.

Neal RomanchychAurora ON Director Director since March 21, 2006.

Mr. Romanchych has over twenty years of experience in the telecommunications sector. Over that period, he has been involved with several successful start-ups and has held senior positions with large telecom companies. His past postings include ten years with Call Net/Sprint Canada (where he was appointed to the Board of Directors of CNE Fiber Development Corp., its U.S. operating subsidiary), Vice President of Primus, Vice President of Riptide Inc. and President of Newlook Industries Corp. Mr. Romanchych holds an Honors Bachelor of Administrative Studies from Trent University. Mr. Romanchych is not involved in managing Eiger’s daily business operations.

| 21 |

There are no arrangements or understandings between any of the officers or directors of the Company as to their election or employment, nor are there any family relationships.

B.Compensation.

For the year ended September 30, 2005 Gerry Racicot was compensated $150,000 for his role as President of the Company. For the same period, Jason Moretto received $150,000 for his role as CFO of the Company.

A total of 6 persons served as members of the administrative, supervisory or management bodies of the subsidiaries of the Company during fiscal 2005. The aggregate remuneration paid to such persons was approximately $500,000.

The following is a list of stock options granted during the last full financial year to members of the Company’s executives.

| Name | Quantity | Exercise price | Expiry | ||

| Gerry Racicot | 500,000 | $ 0.50 | October 5, 2009 | ||

| Jason Moretto | 250,000 | $ 0.50 | October 5, 2009 | ||

None of the above options were exercised during the Company’s most recently completed financial year.

There are no other arrangements under which, directors or members of the Company’s administrative, supervisory or management body, were compensated by the Company during the most recently completed financial year for their services.

No plan exists, and no amount has been set aside or accrued by the Company or any of its subsidiaries, to provide pension, retirement or similar benefits for directors or officers of the Company, or any of its subsidiaries.

C.Board practices.

The directors of the Company are elected annually and hold office until the next annual general meeting of the Company’s shareholders or until their successors in office are duly elected or appointed. All of the Company’s directors were elected at the Company’s most recent annual general meeting, which took place on March 21, 2006. Under theCompany Act(Ontario) the Company is required to hold an annual general meeting no more than 15 months after its most recent annual general meeting.

There are no service contracts with the Company or any of it subsidiaries for the directors providing benefits upon termination of their service.

The Company does not have an executive committee. The audit committee is currently comprised of Sidney Harkema, Brian Cato and Neal Romanchych, who are all

22

independent directors. The committee operates within the guidelines of the Toronto Stock Exchange.

D.Employees.

The Company and its subsidiaries employed approximately 16 staff worldwide during the last fiscal year. The following is a breakdown of persons employed by main category of activity and geographic location for the last full financial year:

| Administrative/ | Sales/ | ||

| Location | Clerical | Marketing | Manufacturing |

| Canada | 16 | 0 | 0 |

The reduction in the number of employees from 42 in the prior fiscal year was due to KTNA operations that were discontinued in fiscal 2005 and Eiger Net operations that were discontinued in fiscal 2004. These discontinued operations represented 9 and 17 staff, respectively, in fiscal 2004.

The Company and its subsidiaries have no involvement with labour unions. The Company and its subsidiaries do not employ a significant number of temporary employees.

E. Share ownership.

| Name and Address | Occupation | Director Since | Number of Voting Shares |

| Beneficially Owned or | |||

| Controlled Directly or Indirectly | |||

| Gerry A. Racicot | President, Chief Executive | August 21, 1992 | 1,724,880(1) |

| Norwich, ON | Officer and Director | ||

| Jason R. Moretto | Chief Financial Officer and | January 5, 2004 | 164,496(2) |

| Vaughan, ON | Director of the Company; | ||

| John G. Simmonds | Director of the Company; | September 20, 2005 | Nil(3) |

| King, ON | President & CEO of | ||

| Simmonds Mercantile & | |||

| Management Inc. | |||

| Sidney S. Harkema | Director of the Company; | August 21, 1992 | 1,514,100(4) |

| Orillia, ON | Retired | ||

| Brian Cato | Director of the Company; | March 21, 2006 | Nil(5) |

| Ajax, ON | Consultant | ||

| Neal Romanchych | Director of the Company; | March 21, 2006 | Nil(6) |

| Aurora, ON | Self-Employed | ||

| 23 |

(2) Mr. Moretto holds options to purchase 810,000 shares.

(3) Mr. Simmonds holds no options.

(4) Mr. Harkema holds options to purchase 185,000 shares.

(5) Mr. Cato holds no options.

(6) Mr. Romanchych holds no options.

| Number of Shares | ||

| Beneficially Owned or | ||

| Controlled Directly or | Percentage of Total Shares | |

| Name | Indirectly | Issued(1) |

| Directors and Officers as a Group | 3,403,476 | 8.8% |

At the discretion of the Board, the stock option plan may be exercised in consideration of services rendered and to be rendered by key personnel and consultants to the Company, its subsidiaries and affiliates.

Item 7. Major Shareholders and Related Party Transactions

A.Major shareholders.

To the Company’s knowledge no person holds five percent or more of the Company’s common shares. There has been no significant change in percentage ownership held by any major shareholder.

All common shareholders have identical voting rights.

There is no trading market for the common shares in the United States. The following table indicates the approximate number of record holders of common shares with U.S. addresses and portion and percentage of common shares so held in the U.S. The calculation is based on the total issued and outstanding as stated in item 6.E.

| Number of | Number of Common | % of Common shares |

| U.S. Holders | shares held in U.S. | held in U.S. |

| 13 | 2,654,021 | 6.83 % |

The computation of the number and percentage of common shares held in the United States is based upon the number of common shares held by record holders with United States addresses and by trusts, estates or accounts with United States addresses as disclosed to the Company following inquiry to all record holders known to the trustees, executors, guardians, custodians or the fiduciaries holding common shares for one or more trusts, estates, or accounts. United States residents may beneficially own common shares held of record by non-United States residents.

A substantial number of common shares are held in “Street Name” by trustees, executors, guardians, custodians or other fiduciaries, including depositories, brokerage firms and financial institutions. Management is unable to determine the total number of individual shareholders that this represents.

| 24 |

To the Company’s knowledge, the Company is not directly or indirectly owned or controlled by another corporation(s) or by any foreign government.

The Management does not anticipate any change in the control of the Company.

B.Related party transactions.

No director, executive officer nor any of their associates or affiliates has or has had an interest in material transactions of the Company.

All transactions within the corporate group are in the normal course of business, are transacted at fair market value, are recorded at the carrying value at the time and are eliminated upon consolidation.

C.Interests of experts and counsel.

Not Applicable

Item 8. Financial Information

A.Consolidated Statements and Other Financial Information.

The following financial statements have been audited by an independent auditor, are accompanied by an audit report, and are attached and incorporated herein:

(a) balance sheet;

(b) income statement;

(c) statement showing changes in equity

(d) cash flow statement;

(e) related notes and schedules required by the comprehensive body of accounting standards pursuant to which the financial statements are prepared; and

(f) a note analyzing the changes in each caption of shareholders’ equity presented in the balance sheet.

Incorporated herewith are the comparative financial statements covering the latest two financial years, audited in accordance with a comprehensive body of auditing standards.

Export Sales

| Total Sales | Export Sales | Export Sales as % of Total Sales |

| $4,904,000 | $Nil | 0% |

| 25 |

Legal Proceedings

There are no material pending legal proceedings to which the Company is a party or of which any of its subsidiaries or properties are subject. Management is not aware of any material proceedings in which any director, any member of senior management, or any of the Company’s affiliates are a party adverse to, or have a material interest adverse to the Company or its subsidiaries.

Dividend Policy

The Company has not paid dividends on the common shares in any of its last five fiscal years. The directors of the Company will determine if and when dividends should be declared and paid in the future based on the Company’s financial position at the relevant time. All of the common shares of the Company are entitled to an equal share in any dividends declared and paid.

B.Significant Changes.

There have been no significant changes since the date of the annual financial statements included in this document.

Item 9. The Offer and Listing.

A.Offer and listing details.

Information regarding the price history of the stock.

| Calendar Period | High (Cdn$) | Low (Cdn$) | Volume |

| Month Ended | |||

| February, 2006 | 0.35 | 0.25 | 735,500 |

| January, 2006 | 0.40 | 0.26 | 2,130,000 |

| December, 2005 | 0.53 | 0.25 | 2,930,900 |

| November, 2005 | 0.30 | 0.19 | 1,320,100 |

| October, 2005 | 0.24 | 0.15 | 336,300 |

| Quarter Ended | |||

| September 30, 2005 | 0.28 | 0.12 | 2,879,900 |

| June 30, 2005 | 0.28 | 0.11 | 2,077,700 |

| March 31, 2005 | 0.34 | 0.14 | 2,552,400 |

| December 31, 2004 | 0.42 | 0.22 | 3,756,600 |

| September 30, 2004 | 0.63 | 0.36 | 2,233,400 |

| June 30, 2004 | 0.97 | 0.45 | 2,186,500 |

| March 31, 2004 | 1.40 | 0.75 | 7,447,600 |

| December 31, 2003 | 1.29 | 0.42 | 10,195,800 |

| Year Ended | |||

| September 30, 2003 | 0.85 | 0.42 | 14,546,807 |

| September 30, 2002 | 2.24 | 0.37 | 32,601,669 |

| September 30, 2001 | 3.24 | 0.35 | 16,397,600 |

| 26 |

Prior to October 11, 1996, all trades were cleared through the VSE and subsequent to that date all trades were cleared on the TSE.

B.Plan of distribution.

Not Applicable.

C.Markets.

The common shares of the Company were listed for trading on the Toronto Stock Exchange (the “TSE”) on October 11, 1996 and previous to this, on the Vancouver Stock Exchange (the “VSE”) on April 3, 1991 under the symbol “AXA”.

The common shares were listed on the NASD OTC Electronic Bulletin Board on October 8, 1997 and trade under the symbol “ETIFF”.

D.Selling shareholders.

Not Applicable.

F.Dilution.

Not Applicable.

F.Expenses of the issue.

Not Applicable.

Item 10. Additional Information.

A.Share capital.

Not Applicable.

B.Memorandum and articles of association.

The Company is incorporated under the laws of the Province of Ontario, Canada and has been assigned company number 942684, with its registered office situated at 144 Front St. W., Suite 700, Toronto, ON, M5J 2L7, Canada. The telephone number at that location is (416) 216-8659.

| 27 |

The purpose of the Company is to perform any and all corporate activities permissible under Ontario law. A director may vote in respect of any contract or arrangement in which such director has an interest notwithstanding. Such director’s interest and an interested director will not be liable to the Company for any profit realized through and such contract or arrangement by reason of such director holding the office of director. The remuneration of the directors shall, from time to time be determined by the Company by ordinary resolution. Directors of the Company are not required to own shares of the Company in order to serve as directors.

The share capital of the Company is an unlimited number of authorized common shares and 38,860,174 common shares outstanding as at the fiscal year end September 30, 2005 and 38,860,174 as of March 27, 2006.

All common shares rank equally with other common shares, entitling the common shareholder to one vote at the annual shareholder’s meeting.

There are no provisions for a classified board of directors or for cumulative voting for directors.

There are no limitations on the rights to own securities, including the rights of nonresident or foreign shareholders to hold or exercise voting rights on the securities.

There are no provisions in the Articles of Incorporation that would have the effect of delaying, deferring or preventing a change in control of the Company and that would operate only with respect to a merger, acquisition or corporate restructuring involving the Company (or any of its subsidiaries).

There are no provisions in the Articles of Incorporation governing the ownership threshold above which shareholder ownership must be disclosed. United States federal law and Ontario provincial securities law, however, requires that all directors, executive officers and holders of 10% or more of the stock of a company that has a class of stock registered under the Securities Exchange Act of 1934, as amended, disclose such ownership. In addition, holders of more than 5% of a registered equity security must disclose such ownership.

C.Material contracts.

The Company has not entered into any material contracts, other than in the ordinary course of business, during the preceding two years.

D.Exchange controls.

Canada has no system of currency exchange controls. There are no exchange restrictions on borrowing from foreign countries nor on the remittance of dividends, interest,

| 28 |

royalties and similar payments, management fees, loan repayments, settlements of trade debts or the repatriation of capital.

The Investment Canada Act (the “ICA”), enacted on June 20, 1985, requires prior notification to the Government of Canada on the “acquisition of control” of Canadian businesses by a non-Canadian, as defined by the ICA. Certain acquisitions of control, discussed below, are reviewed by the Government of Canada. The term “acquisition of control” is defined as one or more non-Canadian persons acquiring all or substantially all of the assets used in the Canadian business, or the acquisition of the voting shares of a Canadian corporation carrying on the Canadian business, or the acquisition of the voting interests of an entity controlling or carrying on the Canadian business. The acquisition of the majority of the outstanding shares is deemed to be an “acquisition of control” of a corporation. The acquisition of less than a majority, but one-third or more, of the voting shares of a corporation is presumed to be an “acquisition of control” of a corporation unless it can be established that the purchaser will not control the corporation.

Investments requiring notification and review are all direct acquisitions of Canadian business with assets of Cdn. $5,000,000 or more (subject to the comments below on WTO investors) and all indirect acquisitions of Canadian businesses (subject to the comments below on WTO investors) with assets of more than Cdn. $50,000,000 or with assets of between $5,000,000 and Cdn. $50,000,000 which represent more than 50% of the value of the total international transactions. In addition, specific acquisitions or new business in designated types of business activities related to Canada’s cultural heritage or national identity could be reviewed if the government of Canada considers that it is in the public interest to do so.

The ICA was amended with the implementation of the agreement establishing the World Trade Organization (“WTO”) to provide for special review of thresholds for “WTO investors”, as defined in the ICA. “WTO investors” generally means:

(a) an individual, other than a Canadian, who is a member of a WTO member (such as, for example, the United States), or who has the right of permanent residence in relation to that WTO member.

(b) governments of WTO members; and

(c) entities that are not Canadian controlled, but which are WTO investor controlled as determined by the rules specified in the ICA.

The special review thresholds for WTO investors do not apply, and general rules described above do not apply, to the acquisition of control of certain types of businesses specified in the ICA, including business that is a “cultural business”. If the WTO investor rules apply, an investment in the shares of the Company by or from a WTO investor will be reviewable only if it is an investment to acquire control of the Company and the value of the assets of the Company is equal to or greater than a specified amount (the “WTO Review Threshold”). The WTO Review Threshold is adjusted annually by

| 29 |

using a formula relating to increases in the nominal gross domestic product of Canada. The 1996 WTO Review Threshold is Cdn. $168,000,000.

If any non-Canadian, whether or not a WTO investor, acquires control of the Company by the acquisition of shares, but the transaction is not reviewable as described above, the non-Canadian is required to notify the Canadian government and to provide certain basic information relating to the investment. A non-Canadian, or non-WTO investor, is required to provide a notice to the government on the establishment of a new Canadian business. If the business of the Company is then a prescribed type of business activity related to Canada’s cultural heritage or national identity, and if the Canadian government considers it in the public interest to do so, then the Canadian government may give a notice in writing within 21 days requiring the investment to be reviewed.

For non-Canadian (other than WTO investors), and indirect acquisition of control, by the acquisition of voting interests of an entity that directly or indirectly controls the Company, is reviewable if the value of the assets of the Company is then Cdn. $50,000,000 or more. If the WTO investor rules apply, then this requirement does not apply to a WTO investor, or to a person acquiring the entity from a WTO investor. Special rules specified in the ICA apply if the assets of the Company is more than 50% of the value of the assets of the entity so acquired. By these special rules, if the non-Canadian (whether or not a WTO investor) is acquiring control of an entity that directly or indirectly controls the Company, and the value of the assets of the company and all other entities carrying on business in Canada, calculated in the manner provided by the ICA and the regulations under the ICA, of the assets of all entities, the control of which is acquired, directly or indirectly, in the transaction of which the acquisition of control of the Company forms a part, then the threshold for a direct acquisition of control as discussed above will apply, that is, a WTO Review Threshold of Cdn. $168,000,000 (n 1996) for a WTO investor or a threshold of CDN. $5,000,000 for non-Canadian other than a WTO investor. If the value exceeds that level the transaction must be reviewed in the same manner as a direct acquisition of control by the purchase of shares by the Company.

If an investment is renewable, an application for review in the form prescribed by the regulations is normally required to be filed with the Director appointed under the ICA (the “Director”) prior to the investment taking place and the investment may not be consummated until the review has been completed. There are, however, certain exceptions. Applications concerning indirect acquisitions may be filed up to 30 days after the investment is consummated and applications concerning reviewable investments in culture-sensitive sectors are required upon receipt of a notice for review. In addition, the Minister (a person designated as such under the ICA) may permit an investment to be consummated prior to completion of the review, if he is satisfied that the delay would cause undue hardship to the acquirer or jeopardize the operations of the Canadian business that is being acquired. The Director will submit the application to the Minister, together with any other information or written undertakings given by the acquirer and any representation submitted to the Director by a province that is likely to be of net benefit to

| 30 |

Canada, taking into account the information provided and having regard to certain factors of assessment where they are relevant. Some of the factors to be considered are:

(a) the effect of the investment on the legal economic activity in Canada, including the effect on employment, on resource processing, and on the utilization of parts, components and services produced in Canada;

(b) the effect of the investment on exports from Canada;

(c) the degree and significance of participation by Canadians in the Canadian business and in any industry in Canada of which it forms a part;

(d) the effect of the investment on productivity, industrial efficiency, technological development, product innovation and product variety in Canada;

(e) the effect of the investment on competition within any industry or industries in Canada;

(f) the compatibility of the investment with national, industrial, economic, and cultural policies;

(g) the compatibility of the investment with national, industrial, economic, and cultural policies taking into consideration industrial, economic, and cultural objectives enunciated by the government of legislature of any province likely to be significantly affected by the investment; and

(h) the contribution of the investment to Canada’s ability to compete in world markets.

To ensure prompt review, the ICA set certain time limits for the Director and the Minister. Within 45 days after a completed application has been received, the Minister must notify the acquirer that he is satisfied that the investment is likely to be of net benefit to Canada, or that he is unable to complete his review, in which case he shall have 30 additional days to complete his review (unless the acquirer agrees to longer period), or he is not satisfied that the investment is likely to be of net benefit to Canada.

Where the Minister has advised the acquirer that he is not satisfied that the investment is likely to be of net benefit to Canada, the acquirer has the right to make representations and submit undertakings within 30 days of the date of notice (or any period that is agreed upon between the acquirer and the Minister). On the expiration of the 30 day period (or the agreed-upon extension), the Minister must quickly notify the acquirer that he is not satisfied that the investment is likely to be of net benefit to Canada. In the latter case, the acquirer my not proceed with the investment or, if the investment has already been consummated, must divest itself of control of the Canadian business.

The ICA provides civil remedies for non-compliance with any provision. There are also criminal penalties for breach of confidentiality or providing false information.

| 31 |

Except as provided in the ICA, there are no limitations under the laws of Canada, the Province of British Columbia, or in any constituent documents of the Company on the right of non-Canadians to hold or vote the common shares of the Company.

E.Taxation.

Certain United States Federal Income Tax Consequences

The following is a general discussion of the material United States Federal income tax law for U.S. holders that hold such common shares as a capital asset, as defined under United States Federal income tax law and is limited to discussion of U.S. Holders that own less than 10% of the common stock. This discussion does not address all potentially relevant Federal income tax matters and it does not address consequences peculiar to persons subject to special provisions of Federal income tax law, such as those described below as excluded from the definition of a U.S. Holder. In addition, this discussion does not cover any state, local or foreign tax consequences.

The following discussion is based upon the sections of the Internal Revenue Code of 1986, as amended to the date hereof (the "Code"), Treasury Regulations, published Internal Revenue Service ("IRS") rulings, published administrative positions of the IRS and court decisions that are currently applicable, any or all of which could be materially and adversely changed, possibly on a retroactive basis, at any time. In addition, this discussion does not consider the potential effects, both adverse and beneficial, of any future legislation which, if enacted, could be applied, possibly on a retroactive basis, at any time. The following discussion is for general information only and it is not intended to be, nor should it be construed to be, legal or tax advice to any holder or prospective holder of common shares of the Company and no opinion or representation with respect to the United States Federal income tax consequences to any such holder or prospective holder is made. Accordingly, holders and prospective holders of common shares of the Company should consult their own tax advisors about the Federal, state, local, and foreign tax consequences of purchasing, owning and disposing of common shares of the Company.

U.S. Holders

As used herein, a "U.S. Holder" is a holder of common shares of the Company who or which is a citizen or individual resident (or is treated as a citizen or individual resident) of the United States for federal income tax purposes, a corporation or partnership created or organized (or treated as created or organized for federal income tax purposes) in the United States, including only the States and District of Columbia, or under the law of the United States or any State or Territory or any political subdivision thereof, or a trust or estate the income of which is includable in its gross income for federal income tax purposes without regard to its source, if, (i) a court within the United States is able to exercise primary supervision over the administration of the trust and (ii) one or more United States trustees have the authority to control all substantial decisions of the trust.

| 32 |

For purposes of this discussion, a U.S. Holder does not include persons subject to special provisions of Federal income tax law, such as tax-exempt organizations, qualified retirement plans, financial institutions, insurance companies, real estate investment trusts, regulated investment companies, broker-dealers and Holders who acquired their stock through the exercise of employee stock options or otherwise as compensation.

Distributions on common shares of the Company