UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

| o | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended September 30, 2009 |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| o | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| Commission file number 000-29320 |

GAMECORP LTD.

(Exact name of Registrant as specified in its charter)

| Ontario, Canada | 3565 King Road, Suite 102 King City, Ontario L7B 1M3 | |

| (Jurisdiction of incorporation or organization) | (Address of principal executive offices) |

John Simmonds jgs@gamecorp.com 905-833-5844

3565 King Road, Suite 102 King City, Ontario L7B 1M3

(Name, telephone, email, and address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act: None

Securities registered or to be registered pursuant to Section 12(g) of the Act:

Common Shares, without par value

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the Issuer’s classes of capital or common stock as of September 30, 2009: 9,207,017 Common Shares without par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

o Yes | x No |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

x Yes | o No |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer” and “large accelerated filer” in Rule 12b-2 of the Exchange Act

Large accelerated filer o | Accelerated filer o | Non-accelerated filer x |

Indicate by check mark which basis of accounting the registrant has used to prepare financial statements included in this filing:

U.S. GAAP o | International Reporting Standards as issued by the International Accounting Standards Board o | Other x |

If “Other” has been checked in response to the previous questions, indicate by check mark which financial statement item the registrant has elected to follow.

o Item 17 | x Item 18 |

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act)

o Yes | x No |

FORWARD LOOKING STATEMENTS

Forward-Looking Information is Subject to Risk and Uncertainty. This report contains certain “forward-looking statements” within the meaning of the U.S. Private Securities Litigation Reform Act of 1995. When used in this report, the words "estimate," "project," "intend," "expect," “anticipate” and similar expressions are intended to identify forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this report. These statements are subject to risks and uncertainties that could cause actual results to differ materially from those contemplated in such forward-looking statements. Such risks and uncertainties include, but are not limited to, those identified under the subheading “Risk Factors” in Item 3 hereof.

GLOSSARY

The following is a glossary of some terms that appear in the discussion of the business of Gamecorp Ltd. (“the Company”) as contained in this Annual Report.

| “Interamerican” | Interamerican Gaming, Inc. an entity in which the Company has an investment. Interamerican is developing Latin American gaming opportunities through its subsidiaries Interamerican Operations, Inc. and IAG Peru S.A.C. |

| “Gate To Wire” | Gate To Wire Solutions Inc. an entity in which the Company has an investment. Gate To Wire’s focus is on distributing live horseracing signals in Latin America. |

| “Baymount” | Baymount Inc., an entity in which the Company has an investment. Baymount is redeveloping a horseracing entity in Canada. |

| “Newlook” | Newlook Industries Corp., an entity in which the Company has an investment. Newlook invests in wireless ventures. |

| “Wireless Age” | Wireless Age Communications, Inc., a majority owned subsidiary of Newlook. |

TABLE OF CONTENTS

| PART I | ||

| Item 1. | Identity of Directors, Senior Management and Advisers | 4 |

| Item 2. | Offer Statistics and Expected Timetable | 4 |

| Item 3. | Key Information | 4 |

| Item 4. | Information on the Company | 6 |

| Item 5. | Operating and Financial Review and Prospects | 9 |

| Item 6. | Directors, Senior Management and Employees | 13 |

| Item 7. | Major Shareholders and Related Party Transactions | 17 |

| Item 8. | Financial Information | 18 |

| Item 9. | The Offer and Listing. | 19 |

| Item 10. | Additional Information. | 20 |

| Item 11. | Quantitative and Qualitative Disclosures About Market Risk. | 24 |

| Item 12. | Description of Securities other than Equity Securities. | 24 |

PART II | ||

| Item 13. | Defaults, Dividend Arrearages and Delinquencies. | 25 |

| Item 14. | Material Modifications to the Rights of Security Holders and Use of Proceeds. | 25 |

| Item 15T. | Controls and Procedures. | 25 |

| Item 16. | [Reserved] | 26 |

| Item 16A. | Audit committee financial expert. | 26 |

| Item 16B. | Code of Ethics. | 26 |

| Item 16C. | Principal Accountant Fees and Services Item 16.D.Exemptions from the Listing Standards for Audit Committees | 26 |

| Item 16E. | Purchases of Equity Securities by the Issuer and Affiliated Purchasers | 26 |

| Item 16F. | Change in Registrant’s Certifying Accountant | 26 |

PART III | ||

| Item 17. | Financial Statements. | 27 |

| Item 18. | Financial Statements. | 27 |

| Item 19. | Exhibits. | 27 |

| SIGNATURES | 28 |

3

PART I

Item 1. Identity of Directors, Senior Management and Advisers

| A. | Directors and Senior Management |

| Not Applicable. |

| B. | Advisers |

| Not applicable |

| C. | Auditors |

| SF Partnership LLP |

4950 Yonge Street 4th Floor |

| Toronto, Ontario M2N 6K1 |

| Item 2. Offer Statistics and Expected Timetable |

| Not Applicable. |

| Item 3. Key Information |

| A. | Selected Financial data |

The selected consolidated financial information set out below has been obtained from financial statements that reflect the Company’s business operations. The financial statements have been prepared in accordance with accounting principles generally accepted in Canada. For reconciliation to US GAAP refer to Note 18 of the attached audited statements. The following table summarizes information pertaining to operations of the Company for the last five years ended September 30, 2009.

| 2009 | 2008** | 2007 | 2006* | 2005* Restated | ||||||||||||||||

| Working Capital | $ | (1,562,000) | $ | (614,000 | ) | $ | (2,193,000 | ) | $ | (1,829,000 | ) | $ | (1,751,000 | ) | ||||||

| Revenue | $ | 242,000 | $ | 311,000 | $ | 47,000 | $ | 130,000 | $ | - | ||||||||||

| Earnings (Loss) from | ||||||||||||||||||||

| Continuing Operations: | $ | (2,718,000) | $ | 2,383,000 | $ | (877,000 | ) | $ | 506,000 | $ | (703,000 | ) | ||||||||

| Earnings (Loss) from | ||||||||||||||||||||

| Discontinued Operations: | $ | (234,000) | $ | 445,000 | $ | (979,000 | ) | $ | (414,000 | ) | $ | 453,000 | ||||||||

| Net Earnings (Loss): | $ | (2,952,000) | $ | 2,828,000 | $ | (1,856,000 | ) | $ | 92,000 | $ | (250,000 | ) | ||||||||

| Earnings (Loss) per share from | ||||||||||||||||||||

| Continuing Operations: | $ | (0.34) | $ | 0.56 | $ | (0.022 | ) | $ | 0.013 | $ | (0.018 | ) | ||||||||

| Earnings (Loss) per share from | ||||||||||||||||||||

| Discontinued Operations: | $ | (0.03) | $ | 0.11 | $ | (0.024 | ) | $ | (0.011 | ) | $ | 0.012 | ||||||||

| Earnings (Loss) per Share: | $ | (0.37) | $ | 0.67 | $ | (0.046 | ) | $ | 0.002 | $ | (0.006 | ) | ||||||||

| Total Assets: | $ | 383,000 | $ | 2,801,000 | $ | 3,869,000 | $ | 2,901,000 | $ | 1,932,000 | ||||||||||

| Shareholders’ Equity (Deficit) | $ | (1,235,000) | $ | 1,951,000 | $ | (1,864,000 | ) | $ | (28,000 | ) | $ | (492,000 | ) | |||||||

| Long Term Debt: | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||||

| Total Liabilities: | $ | (1,618,000) | $ | 850,000 | $ | 2,853,000 | $ | 2,234,000 | $ | 2,424,000 | ||||||||||

| Share Capital: | $ | 45,407,000 | $ | 44,286,000 | $ | 44,286,000 | $ | 43,839,000 | $ | 43,839,000 | ||||||||||

| Retained Earnings (Deficit): | $ | (47,552,000 | ) | $ | (44,600,000 | ) | $ | (47,428,000 | ) | $ | (45,572,000 | ) | $ | (45,664,000 | ) | |||||

| Number of Shares:** | 9,207,017 | 4,226,093 | 42,389,054 | 38,860,174 | 38,860,174 | |||||||||||||||

*Reclassified to reflect discontinued operations of Newlook Industries Corp. **On June 24, 2008 the Company completed a share consolidation on a one post-consolidation common share for ten pre consolidation common shares. | ||||||||||||||||||||

4

CURRENCY EXCHANGE INFORMATION

The Company’s accounts are maintained in Canadian dollars. In this Annual Report, all dollar amounts are expressed in Canadian dollars except where otherwise indicated.

The following table sets forth, for the periods indicated, the high and low rates of exchange of Canadian dollars into United States dollars, the average of such exchange rates for each day during the periods, and the end of period rates. Such rates are shown as, or are derived from, the reciprocals of the Bank of Canada nominal noon exchange rates in Canadian dollars.

--------------------------------------------------------------------------------------------------------------------------------------------------------------------

Fiscal Year Ended

September 30

| 2009 | 2008 | 2007 | 2006 | 2005 | |

| High | 0.9435 | 1.0905 | 1.0069 | 0.9099 | 0.8613 |

| Low | 0.7692 | 0.9263 | 0.8437 | 0.8361 | 0.7859 |

| Average | 0.8475 | 0.9909 | 0.8983 | 0.8753 | 0.8176 |

| Period End | 0.9327 | 0.9435 | 1.0037 | 0.8966 | 0.8613 |

On March 26, 2010 the exchange rate of Canadian dollars into United States dollars, based upon the Bank of Canada nominal noon exchange rate was Cdn. $1.00 equals U.S. $0.9723

The following table sets forth, for the most recent previous six months, the high and low closing rates of exchange of Canadian dollars into United States dollars. The latest practicable date for March was on March 26, 2009.

| Mar | Feb | Jan | Dec | Nov | Oct | |

| 2010 | 2010 | 2010 | 2009 | 2009 | 2009 | |

| High | 0.9938 | 0.9611 | 0.9771 | 0.9580 | 0.9565 | 0.9748 |

| Low | 0.9470 | 0.9307 | 0.9352 | 0.9343 | 0.9243 | 0.9221 |

B. Capitalization and indebtedness.

Not Applicable.

C. Reasons for the offer and use of proceeds.

Not Applicable.

D. Risk factors.

The Company’s operations are subject to a variety of risks and uncertainties. The following factors are to be considered a list of known material risks that are specific to the Company or its industries.

Going Concern

The Company’s continued existence as a going concern is dependent upon the Company’s ability to raise additional capital and sustain profitable operations. There is doubt about the Company's ability to continue as a going concern as the Company has a working capital deficiency of $1,562,000 and an accumulated deficit of $47,552,000 as at September 30, 2009. Should the Company be unable to continue as a going concern, it may be unable to realize the carrying value of its assets and to meet its liabilities as they become due.

The Company believes that future share issuances and certain related party efforts will provide sufficient cash flow for it to continue as a going concern in its present form, however there can be no assurances that the Company will achieve such results.

5

Accordingly, the consolidated financial statements do not include any adjustments related to the recoverability and classification of recorded asset amounts or the amount and classification of liabilities or any other adjustments that might be necessary should the Company be unable to continue as a going concern.

Management of the Growth of the Company

The implementation of the Company’s investment strategy could result in a period of rapid growth. This growth could place a strain on the Company’s managerial and financial resources. Future operating results will depend on the ability of senior management to manage rapidly changing business conditions, and to implement and improve the Company’s investee’s technical, administrative, financial control and reporting systems. No assurance can be given that the Company will succeed in these efforts. The failure to effectively manage and improve these systems could increase the Company’s costs and devalue the Company’s investments.

Competition

The Company faces competition in each of its markets with many competitors that may be larger and have greater financial resources. There can be no assurance that the Company’s investments will be able to continue to compete successfully in its markets. Because the investee’s compete, in part, on the technical advantages and cost of their products, significant technical advances by competitors or the achievement by such competitors of improved operating effectiveness that enable them to reduce prices could reduce the investee’s competitive advantage in these products and thereby adversely affect the Company’s financial results and the value of its investments.

Intellectual Property

The Company’s investees have not obtained patent protection nor registered trademarks or copyrights for all of their proprietary technology or products. As the investees have not protected all of their intellectual property, their business may be adversely affected by competitors’ copying or otherwise exploiting features of their technology, products, information or services, which could damage the value of the Company’s investments.

Dependence on Key Personnel and Skilled Employees

The success of the Company is dependent, in large part, on certain key personnel and on the ability to motivate, retain executive level strategic leadership. There can be no assurance that the Company will be able to attract and retain employees with the necessary technical, technological and specialized skills given the competitive state of the employment market for these individuals. The loss of such services or the failure by the Company to continue to attract and retain other key personnel may have a material adverse effect on the Company, including its ability to make key strategic investments, its ability to grow earnings and its ability to realize on its investments.

Uncertain Operating Results

The Company’s financial operating results may vary and significantly depend on such factors as the timing of new product announcements, increases in supply costs and changes in pricing policies of the Company’s investments and its competitors. The market price of the Shares may be highly volatile in response to such fluctuations.

New Investment Development

There can be no assurance that the Company will be able to identify, develop and invest in new entities or ventures that it currently does not participate in.

Foreign Exchange Rate

Material depreciation of the Canadian dollar against the U.S. dollar and/or other foreign currencies may increase certain costs impacting the Company’s profitability and cash flow.

Item 4. Information on the Company

A. History and development of the company.

Gamecorp Ltd. (the "Company" or "Gamecorp") was originally incorporated as Alexa Ventures Inc. on September 8, 1986 under the laws of British Columbia. Currently, the Company is in good standing, operating under the laws of Ontario. On May 28, 2008, the Company changed its name from Eiger Technology, Inc. to Gamecorp Ltd. The Company is listed as an issuer on the CNSX and a foreign issuer on the NASD Over-the-Counter Bulletin Board.

6

The Company is an investment and merchant banking enterprise focused on the development of its investments. The Company’s current primary investments are in the Gaming and Technology sectors. InterAmerican Gaming, Inc. (“InterAmerican”) (formerly Racino Royale, Inc.), and Gate To Wire Solutions, Inc. (“Gate To Wire”) (formerly TrackPower, Inc.) are development stage enterprises involved in international gaming ventures. The Company previously invested in Baymount Incorporated (“Baymount”) (TSX Venture: BYM), which is developing a gaming entertainment centre in Belleville, Ontario and disposed of its investment during the year ended September 30, 2009. Gamecorp has a legacy investment stake in Newlook Industries Corp. (“Newlook”) (TSX Venture Exchange: NLI), an enterprise with techno logy investments. During the year ended September 30, 2009, the Company disposed of non-strategic investments in Copernic Inc. (“Copernic”) and Gametech International Inc. (“Gametech”).

In general, the Company participates in the early-stage development of gaming projects. Gamecorp provides management, administration, early funding and other assistance to its investees. Strategic leadership of the Company is provided by the Company’s Chief Executive Officer, John G. Simmonds. Mr. Simmonds has extensive business experience in sourcing, reorganizing and operating businesses in various operating segments.

Gamecorp is a public company listed as symbol “GGG” on the Canadian National Stock Exchange (CNSX) and as “GAIMF” on the OTCBB.

Gamecorp’s corporate office is located at 3565 King Road, Suite 102, King City, Ontario L7B 1M3 and has four executive staff members being the officers of the Company. As of September 30, 2009, there were 9,207,017 common shares outstanding.

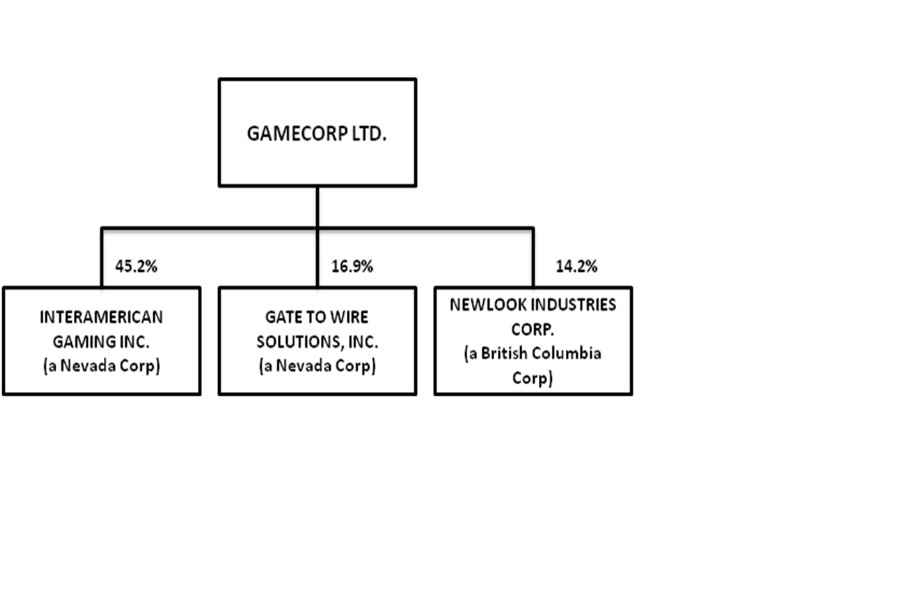

As of September 30, 2009, the Company held a 45.2% ownership position in InterAmerican, and a 16.9% ownership position in Gate To Wire. The Company’s ownership interest in Newlook was 14.2% at September 30, 2009.

The Company plans to participate in the development of various gaming initiatives through its investments in Interamerican, Baymount and Gate To Wire. The Company also plans to realize gains through disposing of its legacy investment in Newlook.

The Issuer is an investment and merchant banking enterprise and accordingly its primary assets are its equity stake in its investees. Occasionally, the Issuer purchases and/or sells the common shares of its investees in the open market.

During the year ended September 30, 2009, the Issuer sold 1,194,500 Newlook common shares for net proceeds of $296,000.

Recent Financings

On July 1, 2009, the company issued an additional 1,000,000 common shares pursuant to a private placement at $0.10 per share.

Other Recent Developments

On September 23, 2009, the Company entered into an agreement with Function Mobile Inc. (“FMI”) to acquire the irrevocable world-wide exclusive right to participate in any pending and future mobile lottery, gaming or sweepstakes projects, proposals, services and products that FMI and its subsidiaries and affiliates has or will undertake.

B. Business Overview

Gamecorp is an investment and merchant banking enterprise focused on the development of its investments in the Gaming and Technology sectors. InterAmerican and Gate To Wire are development stage enterprises involved in international gaming ventures. Newlook, a legacy investment, is a merchant banking entity assembling investments in renewable energy and technology opportunities in Canada.

In general, the Issuer participates in the early-stage development of gaming projects. The Issuer provides management, administration, early funding and other assistance to its investees.

Description of Current Business Plan

The Company plans to focus on participating in international mobile lottery, gaming and sweepstakes opportunities, pursuant to recent agreement with Function Mobile Inc. The first project expected to take form in the first quarter of fiscal 2010 is in Panama and will require an investment of approximately $116,000 prior to the venture obtaining break-even operations.

7

InterAmerican

InterAmerican is a development stage entity whose business objective is to invest in international gaming development opportunities. InterAmerican acquired InterAmerican Gaming, Corp. which is involved in Latin American and Caribbean gaming opportunities.

On April 22, 2009, InterAmerican announced it had entered into a non-binding Letter of Intent (“LOI”) with Signature Gaming Management Peru, S.A.C.("SGM").

SGM, a private entity formed to pursue gaming opportunities in Peru, has entered into certain agreements with the Jockey Club of Arequipa ("JCA") located in Arequipa, Peru, including management of the newly constructed Carro Colorado Racetrack and leasing space in the JCA-owned Social Club, located in the historical city center of Arequipa.

In December 2009, as a result of due diligence on the proposed transaction, the Company and SGM mutually agreed to terminate the letter of intent. The parties continue to discuss the involvement of the Company in the project.

Gate To Wire

Gate To Wire is a development stage entity whose business strategy and direction is to develop and operate a horseracing video distribution venture in international markets.

Gate To Wire and InterAmerican often market their business opportunities in a coordinated manner.

Baymount

Baymount is a development stage entity that is seeking and developing opportunities within the Canadian horseracing industry. Baymount’s objective is to create entertainment destinations for consumers while providing investors an opportunity to participate in the growth of Canadian gaming at racetracks.

Baymount has an agreement with the Belleville Agricultural Society to build a facility to relocate Quinte Exhibition and Raceway in Belleville, Ontario.

The Company disposed of its investment in Baymount during the year ended September 30, 2009.

Newlook

Newlook is a merchant banking entity assembling investments in renewable energy and technology opportunities in Canada. The operations of Newlook have been categorized as discontinued operations. The Company intends to dispose of its investment in Newlook in order to generate capital for investment in gaming opportunities.

During June 2007, Newlook acquired a 53% ownership interest in Wireless Age Communications, Inc. (“Wireless Age”), a public entity trading on the OTCBB under the symbol “WLSA”. Wireless Age operated retail cellular stores in Western Canada and distributed two-way radio products and other ancillary communications products in Canada. On January 9, 2009, operating subsidiaries (Wireless Age Communications Ltd. and Wireless Source Distribution Ltd.) of Newlook’s majority owned subsidiary Wireless Age Communications, Inc. were placed into receivership.

Newlook also sold a portfolio of products and services through its wholly-owned subsidiary, Onlinetel Corp. (“Onlinetel”), in Canada. Newlook has disposed of all of its Onlinetel businesses and currently reflects those operations as discontinued operations. Newlook has also provided loans to development stage entities in the photo luminescent signage and safety way guidance systems sector and in the mobile marketing solutions business arena.

Newlook recently entered into an agreement with PowerPlay Energy Corp. pursuant to which it will potentially acquire the exclusive rights to participate in plasma gasification and renewable energy projects within Canada. Closing is subject to various consents and approvals including shareholders and security regulators.

C. Organizational structure.

The following is a list of each material subsidiary of the Company and the jurisdiction of incorporation and the direct or indirect percentage ownership by the Company of each subsidiary at the fiscal year ended September 30, 2009:

| Name of Subsidiary | Jurisdiction of Organization | Percentage of Voting Securities Owned of Controlled |

| Interamerican Gaming Inc. | Nevada | 45.2% |

| Gate To Wire Solutions, Inc. | Nevada | 16.9% |

| Newlook Industries Corp. | Ontario | 14.2% |

8

The following is an organizational chart showing the Company’s material subsidiaries:

D. Property, plants and equipment.

The Company’s current property, plants and equipment are comprised primarily of furniture, fixtures and computer equipment located in Ontario, Canada. The Company currently owns no real estate.

Item 5. Operating and Financial Review and Prospects

The information provided in this section endeavors to summarize the company’s financial condition and results of operations for the periods specified, including the causes for material changes to provide an understanding of the company’s business as a whole. The information also attempts to relate all separate segments of the company. The discussion provided therein should be read in conjunction with the Company’s consolidated financial statements and related notes.

A. Operating results.

Comparative Analysis Between Fiscal 2009 and 2008

CONTINUING OPERATIONS

The Company recorded a loss from continuing operations of $2,718,000 during the year ended September 30, 2009 compared to earnings of $2,383,000 during the year ended September 30, 2008. The primary reasons for the loss in fiscal 2009 was a significant increase in the share of loss of an equity accounted investee and impairments in amounts due from related parties. The significant earnings in fiscal 2008 is attributed to the Company recording a gain of $3,410,000 arising from fair value adjustments to financial instruments.

Revenues of continuing operations during fiscal 2009 were $242,000 compared to $311,000 during fiscal 2008. The revenues of the Company during fiscal 2009 are management fees charged to its investees and miscellaneous interest income. During fiscal 2009, the Company earned $240,000 in management fees ($180,000 charged to InterAmerican and $60,000 to Gate To Wire). During fiscal 2008 interest income arose from amounts loaned to Newlook and other related entities. Management expects as some of its investees achieve revenue generating stage, management fees will be increased to levels where they would be sufficient to fully offset cash operating expenses.

General and administrative expenses were $1,101,000 during the year ended September 30, 2009 up from $1,052,000 during the year ended September 30, 2008. The marginal increase in general and administrative costs is attributable to rising levels of consulting, travel and legal costs associated with new gaming initiatives. The Company is intimately involved in the development of its investments. The Company compensates its officers for strategic leadership and hires consultants, either directly in the investee or at the Gamecorp level, to assist in the development of investee projects.

General and administrative expenses during the year ended September 30, 2009 included; management fees of $468,000 paid and/or accrued to officers, consulting fees and/or accrued (including administrative salaries) of $294,000, corporate filing fees (including director fees) of $83,000, legal and accounting costs of $80,000, marketing and promotional costs of $52,000, $70,000

9

in travel expenses, rent of $27,000, and miscellaneous costs of $27,000. General and administrative expenses for the year ended September 30, 2008 included; management fees of $472,000 paid to officers, consulting fees (including administrative salaries) of $242,000, corporate filing fees (including directors fees) of $125,000, legal and accounting costs of $83,000, marketing and promotional costs of $61,000, $40,000 in travel expenses and rent of $29,000. Management expects the general and administrative expenses to trend higher during fiscal 2010 as projects of investees become more material.

Amortization of equipment totaled $8,000 in the current year and $11,000 in 2008. The Company’s equipment primarily represents furniture, fixtures and data processing equipment at the corporate office. As the Company is an investment and merchant banking undertaking, management does not expect significant investment in capital equipment.

The Company recorded foreign exchange gains of $44,000, during the year ended September 30, 2009 and $71,000 during the comparative period in the prior year. Foreign exchange gains and losses arise from the translation of US dollar assets and liabilities translated into Canadian dollars during a period of Canadian dollar increasing vis-à-vis the US dollar. The Company does not hedge this translation risk.

As a result of the costs incurred partially offset by management fee and interest income, the Company incurred a loss from operations of $823,000 during fiscal 2009, compared to $681,000 in the prior year. As described above management is hopeful that the gap between costs incurred that are not recovered from charges to investees will decrease in the future. Operating costs that are not recovered are paid from the proceeds of the sale of investments and from related party loans; however the business of the Company is to develop new investments rather than cover operatings costs from the proceeds of the sale of its investments.

The Company recorded other expense items totaling $1,895,000 in fiscal 2009 compared to other income items totaling $3,064,000 in 2008.

Interest expense during fiscal 2009 was $15,000 compared to $41,000 during fiscal 2008. Interest expense during fiscal 2009 arose from amounts loaned to the Company by Newlook and an officer of the Company. Amounts due to Newlook bear interest at the Bank of Canada’s prime rate plus 2%, are unsecured and have no specific repayment dates. The loan provided by the officer bears an interest rate of 12% per annum. Management anticipates higher levels of interest expense in 2010 due to comparatively higher levels of utilization of loans to fund day to day expenses rather than the sale of investments.

During fiscal 2007, the Company opted to dispose of its investment in Newlook. The Company sold 14,263,000 common shares and also granted options to various investors to acquire 14,000,000 additional shares. The Company recorded an expense of $4,567,000 representing the fair value of the grant of the options and the adjustment to its fair value as of September 30, 2007. During fiscal 2008, options to acquire 1,970,000 shares were exercised in March 2008. Also in March 2008, certain optionees agreed to acquire 3,702,000 Newlook common shares formerly under option and the Company agreed to pay a $0.30 cancellation fee on 4,178,000 options. These transactions effectively cancelled all remaining options. Accordingly, during fiscal 2008, the Company recorded a $3,405,000 adjustment to the fair value of the (option) financial instrument. In addition, the Company recorded a $5,000 loss associated with the fair value of a non-interest bearing note receivable issued by the former optioness and a $10,000 gain associated with the fair value of a non-interest bearing note payable issued to certain other former optionees (note 14).

During fiscal 2009, the Company recorded a $4,000 loss associated with the fair value of a non-interest bearing note receivable issued by the former optionees and a $1,000 loss associated with the fair value of a non-interest bearing note payable issued to certain other former optionees (note 14).

The Company recorded a $1,021,000 equity share of InterAmerican losses during fiscal 2009. The Company holds approximately 45.2 % of InterAmerican at September 30, 2009. Equity losses are expected to continue as a result of InterAmerican pursuing various international gaming opportunities.

During the twelve months ended September 30, 2009 the Company advanced InterAmerican $396,000 and advanced Gate To Wire $300,000. There is doubt about InterAmerican and Gate To Wire’s ability to continue as a going concern as they have significant working capital deficiencies and are largely reliant upon the Company to finance current operations. InterAmerican and Gate To Wire have not been able to successfully execute profitable operations and are not expected to in the immediate future. As such the Company has determined the collection of the amounts due from InterAmerican and Gate To Wire is doubtful and has therefore recorded a charge to income of $696,000 at fiscal yearend 2009.

During the year ended September 30, 2009 and 2008, the Company recorded losses of $5,000 and $9,000, respectively, on the write down of an advance to a corporation.

During the twelve month period ended September 30, 2009, the Company recorded $130,000 as a loss from disposal of investments. The Company sold; 1) 1,516,000 Baymount common shares for net proceeds of $22,000 and recorded a loss of $128,000 on disposal, and 2) 2,300 Gametech common shares for net proceeds of $3,000 and recorded a loss of $2,000 on the transaction. Lastly, the Company sold 19,300 Copernic common shares at cost (for proceeds of $4,000) and recorded no gain or loss on the sale.

10

During the fiscal year ended September 30, 2009, the Company relocated its offices and disposed of all furniture, fixtures and computer equipment for $Nil proceeds. For the period, the Company recorded a $33,000 loss on disposition.

Loss per share from continuing operations during the year ended September 30, 2009 were $(0.34) compared to earnings per share of $0.56 in the previous year. Management anticipates continuing losses due to all of its investments being in the development stage.

Discontinued Operations

As described earlier in this report, during fiscal 2007, management made the decision to dispose of its investment in Newlook. For this reason, the operating results of Newlook have been regarded as discontinued operations in the consolidated statement of operating results. The Company recorded a $234,000 loss from discontinued operations during the fiscal period ended September 30, 2009. The Company recorded $530,000 as its equity share of Newlook loss during the fiscal year ended September 30, 2009, offset by the sale of 1,194,500 Newlook common shares for net proceeds of $296,000. The Newlook shares were carried at $Nil and therefore the full amount of the proceeds received represented a gain on disposal.

Loss per share from discontinued operations during the year ended September 30, 2009 was $0.03.

During fiscal 2008, the Company recorded $59,000 of its share of equity earnings of Newlook and recognized a $212,000 impairment loss in its investment in Newlook during fiscal 2008. The Company also received proceeds of $269,000 from the exercise of 1,970,000 options by former optionees and recorded a gain of $189,000 and lastly as a result of the sale of 3,702,000 Newlook shares to former optionees in March 2008 the Company recorded a $409,000 gain representing overall earnings per share from discontinued operations of $0.11. The impairment loss arose from substantially all of Newlook’s majority owned subsidiary Wireless Age Communications, Inc. operating subsidiaries being placed into receivership.

B. Liquidity and capital resources.

The most significant assets of the Company are its investments in InterAmerican, Gate To Wire and Newlook. The carrying amount of these investments at September 30, 2009 were $327,000. In addition the Company holds notes receivable, valued at $23,000 from former optionees and sundry receivables (GST) of $25,000.

On September 30, 2009, the Company held 30,662,600 InterAmerican common shares carried at $176,000, representing a 45.2% interest.

During fiscal 2009, the Company acquired 90,000 shares of Gate To Wire for a cash payment of $11,000. On September 30, 2009, the Company held 4,690,000 Gate To Wire common shares carried at $151,000 representing an 16.9% interest.

At September 30, 2008, the Company held investments in Baymount, Copernic and Gametech, all of which were disposed of in Fiscal 2009.

As of September 30, 2009, the Newlook investment balance was $Nil.

Management is in the process of liquidating the Newlook investment in order to generate capital to reinvest in InterAmerican and Gate To Wire. These entities are development stage enterprises requiring additional cash investment.

Total liabilities were $1,618,000 at September 30, 2009 up substantially from $850,000 at September 30, 2008. The increase is primarily attributable to a $715,000 increase in amounts due to related parties and increases in accounts payable and accrued charges.

Accounts payable and accrued charges increased to $790,000 at September 30, 2009 from $205,000 at September 30, 2008. The increase arose from a higher levels of business activity associated with the development of business gaming investment opportunities and certain related party services remaining unpaid.

Amounts due to related parties at September 30, 2009 were $266,000 up from $10,000 on September 30, 2008. Amounts due to Newlook bear interest at the Canadian Revenue Agency’s prescribed rate, are unsecured and have no specific repayment date. An officer of the Company provided a loan in exchange for an unsecured promissory note at an annual interest rate of 12%. As at September 30,2009, the value of the promissory note was $97,000.

On March 31, 2008, the Company agreed to issue non-interest bearing promissory notes to certain former Newlook option holders (parties formerly holding a right to acquire Newlook common shares from the Company) totaling $1,253,000 representing a cancellation fee of $0.30 per option on 4,178,000 cancelled Newlook options. The Company did not make payments as originally contemplated, however as of September 30, 2008, the Company reduced the promissory notes with cash payments totaling $398,000 and a credit of $240,000, to a note holder who agreed to subscribe for common shares. On September 30, 2009, the Company remains in default and $573,000 is unpaid under these promissory notes. At September 30, 2009, the fair value of the notes payable was $562,000.

11

During fiscal 2008, the Company received approval to issue up to 4,000,000 additional common shares at $0.25 per share for total proceeds of $1,000,000 under a non-brokered private placement. At September 30, 2008, the Company received subscriptions totaling $800,000 and recorded such amount as unissued share liability within shareholders’ equity. On November 10, 2008, the Company closed the full $1,000,000 private placement.

During fiscal 2009 the Company closed a private placement of 1,000,000 common shares at $0.10 per share.

The Company’s consolidated financial statements for the year ended September 30, 2009 have been prepared on a going concern basis, in accordance with Canadian generally accepted accounting principles and accounting principles generally accepted in the United States of America. The going concern basis of presentation assumes that the Company will continue in operations for the foreseeable future and will be able to realize its assets and discharge its liabilities and contingencies in the normal course of operations.

There is doubt about the Company's ability to continue as a going concern as the Company has a working capital deficit of $1,562,000 and an accumulated deficit of $47,552,000 as at September 30, 2009. The Company's ability to continue as a going concern is dependent upon the Company's ability to raise additional capital, to realize on its agreements to dispose of investments and sustain profitable operations. Should the Company be unable to continue as a going concern, it may be unable to realize the carrying value of its assets and to meet its liabilities as they become due.

The Company believes that future shares issuance and proceeds received from the divestiture of its investments will provide sufficient cash flow for it to continue as a going concern in its present form, however, there can be no assurances that the Company will achieve such results. Accordingly, the consolidated financial statements do not include any adjustments related to the recoverability and classification of recorded asset amounts or the amount and classification of liabilities or any other adjustments that might be necessary should the Company be unable to continue as a going concern.

CAPITAL RESOURCES

The Company financed operations during fiscal 2009 primarily from the following sources:

| 1. | The Company received approval for an equity financing during fiscal 2009 and generated $300,000. |

| 2. | The Company also disposed of shares of Newlook, Baymount, Copernic and Gametech and received cash proceeds of $326,000. |

| 3. | The Company collected $151,000 from a note receivable. |

Cash from the above sources were primarily used to make advances to its investees, repay notes payable and fund the cash operating shortfall.

The business objective of the Company is fund early stage development of gaming opportunities by participating in the management of the investees. The philosophy is to dispose of mature investments at a gain and utilize the cash proceeds in the development of future operations within an investee. At this point in time, the Company is slowly disposing of its investment in Newlook, organizing additional equity private placements and obtaining loans primarily from related parties to fund the development of the gaming ventures. The Company occasionally disposes of a portion of its gaming investments in order to generate investment capital also.

However, none of potential sources for capital are certain and management although confident of the potential, cannot assure shareholders and interested parties that they will in fact be able to finance the Company going forward.

C. Research and development, patents and licenses, etc.

Research and development expenses were $Nil ($Nil: 2008; $Nil: 2007) for the year ended September 30, 2009.

On September 23, 2009, the Company entered into an agreement with Function Mobile Inc. to acquire the irrevocable world-wide exclusive right to participate in any pending and future mobile lottery, gaming or sweepstakes projects, proposals, services and products that FMI and its subsidiaries and affiliates has or will undertake.

D. Trend information.

The Issuer does not have any direct operations; however Gamecorp’s investments are subject to a variety of risks and uncertainties. The following factors are not to be considered a definitive list of all risks associated with the Issuer’s investments.

The Company has exposure to credit risk, foreign exchange risk and liquidity risk. The Company has established policies and procedures to manage these risks, with the objective of minimizing any adverse effect that changes in these variables could have on the consolidated financial statements.

12

Management believes the Company is well positioned with its gaming and technology investments to generate strong returns for its shareholders. The Company believes that prudent gaming investments will generate substantial gains. However, the gaming investments are capital intensive and will require incremental financing to ensure success. The Company continues to fund the development of its gaining investee’s businesses; primarily from additional related party loans and equity private placements. The Company plans to dispose of certain legacy technology investment over the medium term. However, the recent bankruptcy proceedings within Newlook may have an affect on the proceeds realized from the disposal of this investment in the near term. The Company also contemplates raising funds through debt and/or equity instruments to fund the initial development of the gaming ventures. Management has observed a significant tightening of availability of credit for gaming ventures. Multiples of forecasted earnings before interest, taxes, depreciation and amortization have fallen and only smaller transactions at extremely low multiples appear to be being completed. A substantial and material risk exists that debt markets will not provide funding for the Company’s investee projects and the Company will be pressured to contribute more to these projects.

Factors that could change the outlook for the Company include changes in regulatory restrictions in which the Company plans to make investments or general economic and financial market conditions. Some acquisition opportunities have recently been declined due to a perceived declining value in acquisition assets that has caused management to adopt a wait and see approach.

The implementation of the Issuer’s investment strategy could result in a period of rapid growth. This growth could place a strain on the Issuer’s managerial and financial resources. Future operating results will depend on the ability of senior management to manage rapidly changing business conditions, and to implement and improve the investee’s technical and administrative systems.

The investee’s face competition in each of its markets and has competitors, many of which are larger and have greater financial resources.

There can be no assurance that the Issuer will be able to identify, develop and invest in new entities or ventures that it currently does not participate in.

There is doubt about the Company's ability to continue as a going concern as the Company has a working capital deficiency of $1,562,000 as at September 30, 2009 (2008 - $614,000) and an accumulated deficit of $47,552,000 as at September 30, 2009. The Company's ability to continue as a going concern is dependent upon the Company's ability to raise additional capital, to increase management fees and interest income, and sustain profitable operations. Should the Company be unable to continue as a going concern, it may be unable to realize the carrying value of its assets and to meet its liabilities as they become due.

The Company believes that future share issuance and increased management fees to existing and future investees will provide sufficient cash flow for it to continue as a going concern in its present form, however, there can be no assurances that the Company will achieve such results. Accordingly, the consolidated financial statements do not include any adjustments related to the recoverability and classification of recorded asset amounts or the amount and classification of liabilities or any other adjustments that might be necessary should the Company be unable to continue as a going concern.

E. Off-balance sheet arrangements.

The Company has no off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on the Company's financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources that are material to investors.

F. Tabular disclosure of contractual obligations.

The Company has no contractual obligations at this time.

Item 6. Directors, Senior Management and Employees

A. Directors and senior management.

The following is a list of the current directors and senior officers of the Company, their municipalities of residence, their current position with the Company and their principal occupations:

| John G. Simmonds, 59 | King City ON | CEO and Chairman of Board |

Mr. Simmonds has served as a director of Gamecorp since September 2005 and as CEO since April 2007. . Mr. Simmonds has over 40 years experience in the communications sector. Mr. Simmonds currently also serves as Chief Executive Officer of Wireless Age Communications, Inc. Mr. Simmonds was appointed Chief Executive Officer of InterAmerican Gaming Corp., formerly Racino Royale Inc. in June 2006. Mr. Simmonds was appointed CEO of Newlook Industries Corp. (NLI:TXSV) in September 2005. He resigned as an officer of Newlook Industries Corp. in February 2007 and was reappointed in July 2007. In September 2004, Mr. Simmonds was appointed as Chief Executive Officer and Director of Lumonall Inc. and resigned as Chief Executive Officer in March 2008. Mr. Simmo nds was re appointed Chief Executive Officer in April 2009. Mr. Simmonds served as the Chief Executive Officer, of Gate to Wire Solutions, Inc. (OTCBB: GWIR) from 1998 to May 2004. In February 2007 Mr.

13

Simmonds was reappointed CEO of Gate to Wire Solutions Inc. Mr. Simmonds has also been involved with several other companies. Mr. Simmonds served as Chief Executive Officer, Chairman and Director of Phantom Fiber Corporation (OTCBB: PHMF), formerly Pivotal Self-Service Technologies, Inc. and resigned in June of 2004. Mr. Simmonds is the father of J. Graham Simmonds, a Director of the Company.

| Jason R. Moretto, 40 | Vaughan ON | President, COO and Director |

Mr. Moretto has been a director of Gamecorp since January 5, 2004, Newlook Industries Corp. since January 5, 2004 and InterAmerican since June 13, 2006. Mr. Moretto has been a director of Wireless Age since June 29, 2007. Mr. Moretto previously served in equity research within the institutional equity group of BMO Nesbitt Burns (now BMO Capital Markets), a full service investment dealer based in Toronto, Canada from September 1997 to February of 2003. From 1995 to 1997, Mr. Moretto was National Accounting Manager for Universal Concerts Canada (now Live Nation), Canada’s largest promoter of live music and entertainment and operator of the Molson Amphitheatre in Toronto. Prior to that, he practiced as an accountant in public practice. He also recently served a two year term as a Member of the Ontari o Securities Commission's Small Business Advisory Committee from 2005 to 2007. Mr. Moretto holds a Bachelor of Commerce degree from the University of Toronto, and is a Certified General Accountant and Chartered Financial Analyst.

J. Graham Simmonds, 36 | Toronto ON | Director |

Mr. Simmonds has been a director of the Company since June 5, 2008. In addition to his role at Gamecorp, Graham Simmonds is President, Chief Executive Officer and Director of Baymount Incorporated (TSXV: BYM). Baymount (www.bym.ca) is focused on developing horseracing properties and innovative wagering products. Baymount has successfully positioned itself in strong racing-related investments that include real estate assets and significant racetrack development opportunities and provides investors with a unique vehicle for participating in the rapid growth of the revitalized racing and gaming market. Mr. Simmonds has built upon a strong family background in horseracing, having spent most of his life involved in the industry. He has over ten years expe rience as a successful owner and breeder of race horses, and over a decade of experience in public company management and business development projects. Mr. Simmonds also sits on the Board of InterAmerican Gaming, Inc. (OTCBB: IAGM) (www.interamericangaming.com), an organization focused on developing gaming opportunities in Latin America. Mr. Simmonds is the son of John G. Simmonds, the Company’s CEO and Chairman of the Board.

| Neal Romanchych, 45 | Aurora ON | Director |

Mr. Romanchych has served as a director of the Company since March 21, 2006, in addition to his role at Gamecorp he is a Vice President of 411.ca. Mr. Romanchych has over twenty years of experience in the telecommunications sector. Over that period, he has been involved with several successful start-ups and has held senior positions with large telecom companies. His past postings include ten years with Call Net/Sprint Canada (where he was appointed to the Board of Directors of CNE Fiber Development Corp., its U.S. operating subsidiary), Vice President of Primus, Vice President of Riptide Inc. and President of Newlook Industries Corp. Mr. Romanchych holds an Honors Bachelor of Administrative Studies from Trent University.

| Gary Hokkanen, 54 | Thornhill ON | Chief Financial Officer |

Mr. Hokkanen has served as CFO of Gamecorp since July 2007. He has served as Wireless Age’s CFO since May 29, 2003. Mr. Hokkanen is an executive level financial manager with over 10 years experience in public company financial management. Mr. Hokkanen holds a Bachelor of Arts degree from the University of Toronto and is a CMA (Certified Management Accountant) and a member of the Society of Management Accountants, Ontario. From January 2001 to April 2003 Mr. Hokkanen was CFO of IRMG Inc., a Toronto based financial management consulting firm. Mr. Hokkanen served as CFO of Simmonds Capital Limited from July 1998 to January 2001 and served as CFO of Gate To Wire from February 1998 to June 2001. In May of 2005 Mr. Hokkanen was reappointed CFO of Gate To Wire, resigned in August 20 06 and was reappointed in June 2007. For the period April 1996 to July 1998, Mr. Hokkanen served as Treasurer of Simmonds Capital Limited. In November 2007, Mr. Hokkanen was appointed a director and officer of Sagittarius Capital Corporation (a TSX Venture Exchange capital pool company). He has also served as CFO for Newlook Industries Corp. (TSX Venture Exchange), Lumonall, Inc. (OTCBB) and InterAmerican (OTCBB) since July 2007 and as a director and officer of Sagittarius Capital Corp. (Capital pool company on the TSX Venture Exchange) since April 20, 2007.

| Carrie Weiler, 51 | Nobleton ON | Corporate Secretary |

Ms. Weiler was appointed Corporate Secretary on July 1, 2007. She was appointed Corporate Secretary of Wireless Age Communications, Inc. on May 29, 2003 and was appointed Director in February 2007. Ms. Weiler provides professional public company corporate secretarial services to various entities. Ms. Weiler is a member of the Canadian Society of Corporate Secretaries. Ms. Weiler was appointed Corporate Secretary of InterAmerican in September 2006. She has served as Corporate Secretary of Gate To Wire since 1998. On October 15, 2004 Ms. Weiler was appointed Corporate Secretary of Lumonall and continues to serve in such capacity. Ms. Weiler has served as Corporate Secretary of Newlook Industries Corp. and as a director since July 2007.

.

14

B. Compensation.

For the year ended September 30, 2009, John G. Simmonds was compensated with a salary of $180,000 for his role as Chief Executive Officer of the Company. For the same period, Jason Moretto received a salary of $180,000 for his role as President. Gary Hokkanen received $30,000 for his role as CFO of the Company.

A total of 3 persons served as members of the administrative, supervisory or management bodies of the subsidiaries of the Company during fiscal 2009. The aggregate remuneration paid to such persons was approximately $428,000.

There were no options granted during fiscal 2009.

No options were exercised during the Company’s most recently completed financial year.

There are no other arrangements under which directors or members of the Company’s administrative, supervisory or management body, were compensated by the Company, during the most recently completed financial year for their services.

C. Board practices.

The directors of the Company are elected annually and hold office until the next annual general meeting of the Company’s shareholders or until their successors in office are duly elected or appointed. All of the Company’s directors were elected at the Company’s most recent annual general meeting, which took place on August 7, 2009. Under the Company Act (Ontario) the Company is required to hold an annual general meeting no more than 15 months after its most recent annual general meeting.

There are no service contracts with the Company or any of its subsidiaries for the directors providing benefits upon termination of their service.

The Corporate Governance and Compensation committee is currently comprised of John Simmonds, Jason Moretto, and Neal Romanchych. The audit committee is currently comprised of J. Graham Simmonds and Neal Romanchych who are independent directors. The committee operates within the guidelines of the Toronto Stock Exchange.

D. Employees.

The Company and its subsidiaries employed approximately 3 staff during the last fiscal year, the same number as employed in the previous fiscal year. In April 2007, Mr. Gerry Racicot retired as the Chief Executive Officer, President and Director of the Company after founding the Company 16 years ago. Mr. John G. Simmonds has assumed the responsibility of the Chief Executive Officer. Mr. Jason Moretto, who had been the Chief Financial Officer of the Company, has been replaced by Mr. Gary Hokkanen. Mr. Moretto has assumed the responsibility of the President of the Company.

The Company and its subsidiaries have no involvement with labour unions. The Company and its subsidiaries do not employ a significant number of temporary employees.

E. Share ownership.

Directors and officers

The following table indicates the names and municipalities of residence for each director and officer of the Company. The table further indicates the date on which the following persons began acting as directors or officers of the Company, as the case may be, and states the number of voting shares of the Company which are beneficially owned by each of them or over which they have direct or indirect control as of September 30, 2009.

| Name and Address | Occupation | Director or Officer Since | Number of Voting Shares Beneficially Owned or Controlled Directly or Indirectly (1) | % of Voting Shares Beneficially Owned or Controlled Directly or Indirectly (1) |

John G. Simmonds King City, ON | CEO and Director of the Company | September 20, 2005 | 389,200 (3)(4) | 4.2% |

Jason R. Moretto Vaughan, ON | President, Chief Operating Officer and Director of the Company | January 5, 2004 | 246,450 (2)(3)(5) | 2.7% |

Neal Romanchych Aurora, ON | Director of the Company; VP Sales/Service, 411.ca | March 21, 2006 | Nil (2)(3) | 0% |

J. Graham Simmonds Toronto, ON | Director of the Company, President and CEO of Baymount Inc. | May 28, 2008 | Nil (2)(6) | 0% |

Gary N. Hokkanen Thornhill, ON | Chief Financial Officer | July 17, 2007 | 40,000 | 0.4% |

Carrie J. Weiler Nobleton, ON | Corporate Secretary | July 17, 2007 | 415,500 | 4.5% |

15

| Notes: |

| (1) | Includes Shares over which control or direction is exercised. The information as to Shares beneficially owned or controlled, not being within the knowledge of the Company, has been provided by the nominees. |

| (2) | Member of the Audit Committee. |

| (3) | Member of the Corporate Governance and Compensation Committee |

| (4) | Mr. Simmonds holds warrants to purchase 30,000 shares. |

| (5) | Mr. Moretto holds options to purchase 25,000 shares and warrants to purchase 90,000 shares. |

| (6) | Mr. Graham Simmonds owns approximately 40% of PowerPlay Energy which owns 10.86% of the Company. |

The following table indicates the total number of voting shares of the Company held by its directors and officers as a group, and the percentage that such shares form of the total number of voting shares of the Company issued and outstanding.

| Name | Number of Shares Beneficially Owned or Controlled Directly or Indirectly | Percentage of Total Shares Issued(1) |

| Directors and Officers as a Group | 1,090,650 | 11.8% |

In the fiscal year ended September 30, 2009, there were no grants of options to purchase Shares to the Named Executive Officers, pursuant to the Stock Option Plan.

The following table sets out the number of options to purchase Shares exercised during the Company’s most recently completed fiscal year, if any, by the Named Executive Officers, and the number of unexercised options and the value of unexercised “in the money” options held as at September 30, 2009, if any, by such persons:

| Name | Shares Acquired on Exercise (#) | Aggregate Value Realized ($) | Unexercised Options at September 30, 2008 (Exercisable/ Unexercisable) (#) | Value of Unexercised In-The-Money Options at September 30, 2008(Exercisable/ Unexercisable)(1) ($) |

| Jason R. Moretto | Nil | Nil | 25,000/Nil | Nil/Nil |

| John G. Simmonds | Nil | Nil | Nil/Nil | Nil/Nil |

| Gary Hokkanen | Nil | Nil | Nil/Nil | Nil/Nil |

16

Item 7. Major Shareholders and Related Party Transactions

A. Major shareholders.

Major Shareholders as of September 30, 2009:

| Name and Address | Ownership | Number of Shares | % of Common Shares Owned or Controlled | |||

PowerPlay Energy Corp. 330 University Ave. Suite 504Toronto, On M5G 1R7 | Direct | 1,000,000 | 10.86% |

| (1) | Mr. Graham Simmonds owns approximately 40% of PowerPlay Energy and is a director of Gamecorp Ltd. |

All common shareholders have identical voting rights.

The following table indicates the approximate number of record holders of common shares with U.S. addresses and portion and percentage of common shares so held in the U.S. The calculation is based on the total issued and outstanding as stated in item 6.E.

Number of U.S. Holders | Number of Common shares held in U.S. | % of Common shares held in U.S. |

| 112 | 354,780 | 4% |

The computation of the number and percentage of common shares held in the United States is based upon the number of common shares held by record holders with United States addresses and by trusts, estates or accounts with United States addresses as disclosed to the Company following inquiry to all record holders known to the trustees, executors, guardians, custodians or the fiduciaries holding common shares for one or more trusts, estates, or accounts. United States residents may beneficially own common shares held of record by non-United States residents.

A substantial number of common shares are held in “Street Name” by trustees, executors, guardians, custodians or other fiduciaries, including depositories, brokerage firms and financial institutions. Management is unable to determine the total number of individual shareholders that this represents.

To the Company’s knowledge, the Company is not directly or indirectly owned or controlled by another corporation(s) or by any foreign government.

The Management does not anticipate any change in the control of the Company.

B. Related party transactions.

Officers, directors and related parties of the Company were paid $468,000 in consulting fees during the year ended September 30, 2009. Accrued or paid fees for the year for officers of the Company were for the services of John Simmonds, our CEO, Gary Hokkanen, our CFO and Carrie Weiler our Corporate Secretary. Accrued or paid director fees were for the services of Jason Moretto, Neal Romanchych, Paul Duffy, Stephen Dulmage and Graham Simmonds. In addition, fees were paid to Wireless Age Communications, Inc., a related party due to certain common officers, directors and ownership for services of managerial level accounting.

Management fees earned from investees during the period totaled $240,000 (2008 - $195,000) and interest income earned from investees during the current period was $Nil (2008 - $116,000). The Company earned management fees of $180,000 from InterAmerican, a related party by virtue of certain common directors and officers and $60,000 from Gate To Wire, also an entity with certain common officers and directors.

Included in accounts payable are payables to directors, officers or corporations owned by management personnel of $556,000 (2008 - $105,000).

Interest incurred to related parties during the period totaled $15,000 (2008-$29,000).

During the year ended September 30, 2009, Newlook, a related party by virtue of certain common directors and officers loaned the Company $169,000.

All transactions within the corporate group listed in note 16 of the consolidated financial statements are in the normal course of business and are recorded at the exchange value agreed to by the related parties. Inter-company transactions and balances are eliminated upon consolidation.

17

C. Interests of Experts and Counsel.

Not Applicable

Item 8. Financial Information

A. Consolidated Statements and Other Financial Information.

The following financial statements have been audited by an independent auditor, are accompanied by an audit report, and are attached and incorporated herein:

(a) balance sheet;

(b) income statement;

(c) statement showing changes in equity

(d) cash flow statement;

(e) related notes and schedules required by the comprehensive body of accounting standards pursuant to which the financial statements are prepared; and

(f) a note analyzing the changes in each caption of shareholders’ equity presented in the balance sheet.

Incorporated herewith are the comparative financial statements covering the latest three financial years, audited in accordance with a comprehensive body of auditing standards.

Export Sales

| Total Sales | Export Sales | Export Sales as % of Total Sales |

| $Nil | $Nil | 0% |

Legal Proceedings

The Company was a party to a claim by a former employee for wrongful dismissal, alleged breach of contract, punitive and aggravated damages and costs. The Company was released from the claim pursuant to a settlement by a subsidiary of the Company’s investee, Newlook, which was sold to a third party. The Company will record a loss, if any, to the extent the third party defaults under the settlement agreement in the period that it occurs.

Dividend Policy

The Company has not paid dividends on the common shares in any of its last five fiscal years. The directors of the Company will determine if and when dividends should be declared and paid in the future based on the Company’s financial position at the relevant time. All of the common shares of the Company are entitled to an equal share in any dividends declared and paid.

B. Significant Changes.

On December 31, 2009, Mr. Stephen Dulmage resigned as a member of the Board of Directors and Chairman of the Audit Committee of the Company. Mr. Dulmage’s resignation was voluntary and did not involve a disagreement with the Company on any matter relating to the Company’s operations, policies or practices.

18

Item 9. The Offer and Listing.

A. Offer and listing details.

Information regarding the price history of the stock.

The following stock price ranges are from the CNSX under the symbol GGG The Company also trades on the NASD Over-the-Counter Bulletin Board under the symbol GAIMF but at substantially lower volumes.

Calendar Period | High (Cdn$) | Low (Cdn$) |

| Month Ended | ||

| February 2010 | 0.035 | 0.005 |

| January 2010 | 0.040 | 0.030 |

| December 2009 | 0.050 | 0.030 |

| November 2009 | 0.050 | 0.030 |

| October 2009 | 0.050 | 0.050 |

| September 2009 | 0.050 | 0.050 |

| Quarter Ended | High (Cdn$) | Low (Cdn$) |

| December 2009 | 0.05 | 0.03 |

| September 2009 | 0.08 | 0.05 |

| June 2009 | 0.08 | 0.07 |

| March 2009 | 0.11 | 0.08 |

| December 2008 | 0.40 | 0.05 |

| September 2008 | 0.50 | 0.20 |

| June 2008* | 0.25 | 0.02 |

| March 2008 | 0.08 | 0.05 |

| December 2007 | 0.08 | 0.05 |

Year Ended

| September 30, 2009 | 0.11 | 0.03 |

| September 30, 2008 | 0.50 | 0.02 |

| September 20, 2007 | 0.20 | 0.07 |

| September 30, 2006 | 0.53 | 0.12 |

| September 30, 2005 | 0.42 | 0.11 |

* Consolidation- On June 26, 2008, the Company completed a share consolidation on a one post-consolidation common share for ten pre-consolidation common shares.

B. Plan of Distribution.

Not Applicable.

C. Markets.

The common shares of the Company were listed for trading on the Toronto Stock Exchange (the “TSX”) on October 11, 1996 and previous to this, on the TSX-Venture Exchange (formerly the Vancouver Stock Exchange) (the “TSX-V”) on April 3, 1991 under the symbol “AXA”.

The common shares of the Company were listed on the Canadian National Stock Exchange (the “CNSX”) on April 28, 2008 and currently trade under the symbol “GGG”.

The common shares were listed on the NASD OTC Bulletin Board on October 8, 1997 and trade under the symbol “GAIMF”.

D. Selling shareholders.

Not Applicable.

19

E. Dilution.

Not Applicable.

F. Expenses of the issue.

Not Applicable.

Item 10. Additional Information.

A. Share capital.

Not Applicable.

B. Memorandum and articles of association.

The information required by Item 10.B. is hereby incorporated by reference from the Company's previous Report on Form 20-F filed in March of 2008 on the EDGAR system.

C. Material contracts.

The Company entered into a Settlement Agreement with its former President and CEO, Gerry Racicot, on August 24, 2007. Mr. Racicot retired as an officer and director of the Company on April 18, 2007. The Settlement Agreement and associated documents have been filed on SEDAR (www.sedar.com).

Details: The Company agreed to pay Mr. Racicot a retirement payment valued at $500,000. In respect of back pay owing by the Company to 1040614 Ontario Ltd., the Company agreed to pay 1040614 Ontario Ltd. a total sum of $538,325.37. Additionally, the Company paid Mr. Racicot $5,000, representing reimbursement of outstanding expenses incurred by Mr. Racicot prior to the Retirement Date in the course of his duties to the Company.

D. Exchange controls.

Canada has no system of currency exchange controls. There are no exchange restrictions on borrowing from foreign countries nor on the remittance of dividends, interest, royalties and similar payments, management fees, loan repayments, settlements of trade debts or the repatriation of capital.

The Investment Canada Act (the “ICA”), enacted on June 20, 1985, requires prior notification to the Government of Canada on the “acquisition of control” of Canadian businesses by a non-Canadian, as defined by the ICA. Certain acquisitions of control, discussed below, are reviewed by the Government of Canada. The term “acquisition of control” is defined as one or more non-Canadian persons acquiring all or substantially all of the assets used in the Canadian business, or the acquisition of the voting shares of a Canadian corporation carrying on the Canadian business, or the acquisition of the voting interests of an entity controlling or carrying on the Canadian business. The acquisition of the majority of the outstanding shares is deemed to be an “acquisition of c ontrol” of a corporation. The acquisition of less than a majority, but one-third or more, of the voting shares of a corporation is presumed to be an “acquisition of control” of a corporation unless it can be established that the purchaser will not control the corporation.

Investments requiring notification and review are all direct acquisitions of Canadian business with assets of Cdn. $5,000,000 or more (subject to the comments below on WTO investors) and all indirect acquisitions of Canadian businesses (subject to the comments below on WTO investors) with assets of more than Cdn. $50,000,000 or with assets of between $5,000,000 and Cdn. $50,000,000 which represent more than 50% of the value of the total international transactions. In addition, specific acquisitions or new business in designated types of business activities related to Canada’s cultural heritage or national identity could be reviewed if the government of Canada considers that it is in the public interest to do so.

The ICA was amended with the implementation of the agreement establishing the World Trade Organization (“WTO”) to provide for special review of thresholds for “WTO investors”, as defined in the ICA. “WTO investors” generally means:

(a) an individual, other than a Canadian, who is a member of a WTO member (such as, for example, the United States), or who has the right of permanent residence in relation to that WTO member.

(b) governments of WTO members; and

20

(c) entities that are not Canadian controlled, but which are WTO investor controlled as determined by the rules specified in the ICA.

The special review thresholds for WTO investors do not apply, and general rules described above do not apply, to the acquisition of control of certain types of businesses specified in the ICA, including business that is a “cultural business”. If the WTO investor rules apply, an investment in the shares of the Company by or from a WTO investor will be reviewable only if it is an investment to acquire control of the Company and the value of the assets of the Company is equal to or greater than a specified amount (the “WTO Review Threshold”). The WTO Review Threshold is adjusted annually by using a formula relating to increases in the nominal gross domestic product of Canada. The 1996 WTO Review Threshold is Cdn. $168,000,000.

If any non-Canadian, whether or not a WTO investor, acquires control of the Company by the acquisition of shares, but the transaction is not reviewable as described above, the non-Canadian is required to notify the Canadian government and to provide certain basic information relating to the investment. A non-Canadian, or non-WTO investor, is required to provide a notice to the government on the establishment of a new Canadian business. If the business of the Company is then a prescribed type of business activity related to Canada’s cultural heritage or national identity, and if the Canadian government considers it in the public interest to do so, then the Canadian government may give a notice in writing within 21 days requiring the investment to be reviewed.

For non-Canadian (other than WTO investors), and indirect acquisition of control, by the acquisition of voting interests of an entity that directly or indirectly controls the Company, is reviewable if the value of the assets of the Company is then Cdn. $50,000,000 or more. If the WTO investor rules apply, then this requirement does not apply to a WTO investor, or to a person acquiring the entity from a WTO investor. Special rules specified in the ICA apply if the assets of the Company is more than 50% of the value of the assets of the entity so acquired. By these special rules, if the non-Canadian (whether or not a WTO investor) is acquiring control of an entity that directly or indirectly controls the Company, and the value of the assets of the company and all other entities carrying on business in Canada, calculated in the manner provided by the ICA and the regulations under the ICA, of the assets of all entities, the control of which is acquired, directly or indirectly, in the transaction of which the acquisition of control of the Company forms a part, then the threshold for a direct acquisition of control as discussed above will apply, that is, a WTO Review Threshold of Cdn. $168,000,000 (n 1996) for a WTO investor or a threshold of CDN. $5,000,000 for non-Canadian other than a WTO investor. If the value exceeds that level the transaction must be reviewed in the same manner as a direct acquisition of control by the purchase of shares by the Company.

If an investment is renewable, an application for review in the form prescribed by the regulations is normally required to be filed with the Director appointed under the ICA (the “Director”) prior to the investment taking place and the investment may not be consummated until the review has been completed. There are, however, certain exceptions. Applications concerning indirect acquisitions may be filed up to 30 days after the investment is consummated and applications concerning reviewable investments in culture-sensitive sectors are required upon receipt of a notice for review. In addition, the Minister (a person designated as such under the ICA) may permit an investment to be consummated prior to completion of the review, if he is satisfied that the delay would cause undue hardship to the acquirer or jeopardize the operations of the Canadian business that is being acquired. The Director will submit the application to the Minister, together with any other information or written undertakings given by the acquirer and any representation submitted to the Director by a province that is likely to be of net benefit to Canada, taking into account the information provided and having regard to certain factors of assessment where they are relevant. Some of the factors to be considered are:

(a)the effect of the investment on the legal economic activity in Canada, including the effect on employment, on resource processing, and on the utilization of parts, components and services produced in Canada;

(b)the effect of the investment on exports from Canada;

(c)the degree and significance of participation by Canadians in the Canadian business and in any industry in Canada of which it forms a part;

(d)the effect of the investment on productivity, industrial efficiency, technological development, product innovation and product variety in Canada;

(e)the effect of the investment on competition within any industry or industries in Canada;

(f)the compatibility of the investment with national, industrial, economic, and cultural policies;

(g)the compatibility of the investment with national, industrial, economic, and cultural policies taking into consideration industrial, economic, and cultural objectives enunciated by the government of legislature of any province likely to be significantly affected by the investment; and

(h) the contribution of the investment to Canada’s ability to compete in world markets.

21