| | | | | | | | | | | | | | | | | |

| INDEX | | | | | |

| | Page | |

| FINANCIAL HIGHLIGHTS AND BUSINESS DEVELOPMENTS | | - | | |

| DEBT AND CAPITALIZATION | | | | |

| Unsecured Notes Covenant Ratios and Credit Ratings | | | | |

| Liquidity and Capitalization | | | | |

| Net Debt to EBITDAre, As Adjusted / Debt Snapshot | | | | |

| Hedging Instruments | | | | |

| Consolidated Debt Maturities | | - | | |

| PROPERTY STATISTICS | | | | |

| Top 15 Tenants | | | | |

| Lease Expirations | | | | |

| DEVELOPMENT ACTIVITY | | | | |

| PENN District Active Development/Redevelopment Summary | | | | |

| APPENDIX: NON-GAAP RECONCILIATIONS | | - | | |

Certain statements contained herein constitute forward-looking statements as such term is defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements are not guarantees of performance. They represent our intentions, plans, expectations and beliefs and are subject to numerous assumptions, risks and uncertainties. Our future results, financial condition and business may differ materially from those expressed in these forward-looking statements. You can find many of these statements by looking for words such as "approximates," "believes," "expects," "anticipates," "estimates," "intends," "plans," "would," "may" or other similar expressions in this supplemental package. We also note the following forward-looking statements: in the case of our development and redevelopment projects, the estimated completion date, estimated project cost, projected incremental cash yield, stabilization date and cost to complete; and estimates of future capital expenditures. Many of the factors that will determine the outcome of these and our other forward-looking statements are beyond our ability to control or predict. Currently, some of the factors are the increase in interest rates and inflation and the continuing effect of the COVID-19 pandemic on our business, financial condition, results of operations, cash flows, operating performance and the effect that these factors have had and may continue to have on our tenants, the global, national, regional and local economies and financial markets and the real estate market in general. For further discussion of factors that could materially affect the outcome of our forward-looking statements, see "Item 1A. Risk Factors" in Part I of our Annual Report on Form 10-K for the year ended December 31, 2022. For these statements, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995. You are cautioned not to place undue reliance on our forward-looking statements, which speak only as of the date of this supplemental package. All subsequent written and oral forward-looking statements attributable to us or any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. We do not undertake any obligation to release publicly any revisions to our forward-looking statements to reflect events or circumstances occurring after the date of this supplemental package. This supplemental package includes certain non-GAAP financial measures, which are accompanied by what Vornado Realty Trust and subsidiaries (the "Company") considers the most directly comparable financial measures calculated and presented in accordance with accounting principles generally accepted in the United States of America ("GAAP"). These include Earnings Before Interest, Taxes, Depreciation and Amortization for Real Estate ("EBITDAre"). Quantitative reconciliations of the differences between the most directly comparable GAAP financial measures and the non-GAAP financial measures presented are provided within this supplemental package. Definitions of these non-GAAP financial measures and statements of the reasons why management believes the non-GAAP measures provide useful information to investors about the Company's financial condition and results of operations, and, if applicable, the purposes for which management uses the measures, can be found in the Appendix of this supplemental package.This supplemental package should be read in conjunction with the Company’s Annual Report on Form 10-K for the year ended December 31, 2022 and the Company’s Supplemental Operating and Financial Data package for the quarter and year ended December 31, 2022, both of which can be accessed at the Company’s website www.vno.com.

| | | | | | | | | | | | | | |

| FINANCIAL HIGHLIGHTS AND BUSINESS DEVELOPMENTS (unaudited) |

2022 Financial Highlights

Quarter Ended December 31, 2022

Net loss attributable to common shareholders for the quarter ended December 31, 2022 was $493,280,000, or $2.57 per diluted share, compared to net income of $11,269,000, or $0.06 per diluted share, for the prior year's quarter. Adjusting for the items that impact period-to-period comparability, net income attributable to common shareholders, as adjusted (non-GAAP) for the quarter ended December 31, 2022 was $19,954,000, or $0.10 per diluted share, and $22,977,000, or $0.12 per diluted share for the prior year’s quarter.

EBITDAre, as adjusted (non-GAAP) for the quarter ended December 31, 2022 was $281,271,000, compared to $255,634,000 for the prior year’s quarter.

Year Ended December 31, 2022

Net loss attributable to common shareholders for the year ended December 31, 2022 was $408,615,000, or $2.13 per diluted share, compared to net income attributable to common shareholders of $101,086,000, or $0.53 per diluted share, for the year ended December 31, 2021. Adjusting for the items that impact period-to-period comparability, net income attributable to common shareholders, as adjusted (non-GAAP) for the year ended December 31, 2022 was $126,468,000, or $0.66 per diluted share, and $88,153,000, or $0.46 per diluted share, for the year ended December 31, 2021.

EBITDAre, as adjusted (non-GAAP) for the year ended December 31, 2022 was $1.1 billion, compared to $948,976,000 for the year ended December 31, 2021.

Non-Cash Impairment Charges

Net loss attributable to common shareholders for the quarter and year ended December 31, 2022 includes $595,488,000 of non-cash impairment charges, of which $483,037,000 relates to Vornado’s common equity investment in the Fifth Avenue and Times Square joint venture (“Retail JV”).

By way of background, in April 2019, we recognized a $2.559 billion gain upon the transfer of seven properties to the Retail JV, which included a GAAP required write-up to fair value of its retained interest in the properties. The $483,037,000 impairment charge recognized this quarter together with the $409,060,000 impairment charge previously recognized in 2020, effectively reverse a portion of the $2.559 billion gain attributable to the 2019 required write-up.

Liquidity

As of December 31, 2022, we have $3.4 billion of liquidity comprised of $1.0 billion of cash and cash equivalents and restricted cash, $472,000,000 of investments in U.S. Treasury bills and $1.9 billion available on our $2.5 billion revolving credit facilities.

PENN District Development

As of December 31, 2022, we have expended $1.9 billion of cash with an estimated $497,795,000 remaining to be spent across The Farley Building, PENN 1, PENN 2, and PENN districtwide improvements. There can be no assurance that these projects will be completed, completed on schedule or within budget.

Please refer to the Appendix for reconciliations of GAAP to non-GAAP measures.

| | | | | | | | | | | | | | |

| FINANCIAL HIGHLIGHTS AND BUSINESS DEVELOPMENTS (unaudited) |

2022 Business Developments

350 Park Avenue

On January 24, 2023, we and the Rudin family (“Rudin”) completed agreements with Citadel Enterprise Americas LLC (“Citadel”) and with an affiliate of Kenneth C. Griffin, Citadel’s Founder and CEO (“KG”), for a series of transactions relating to 350 Park Avenue and 40 East 52nd Street.

Citadel will master lease 350 Park Avenue, a 585,000 square foot Manhattan office building, on an “as is” basis for ten years, with an initial annual net rent of $36,000,000. Per the terms of the lease, no tenant allowance or free rent is being provided. Citadel will also master lease Rudin’s adjacent property at 40 East 52nd Street (390,000 square feet).

In addition, we have entered into a joint venture with Rudin (“Vornado/Rudin”) to purchase 39 East 51st Street for $40,000,000 and, upon formation of the KG joint venture described below, will combine that property with 350 Park Avenue and 40 East 52nd Street to create a premier development site (collectively, the “Site”).

From October 2024 to June 2030, KG will have the option to either:

•acquire a 60% interest in a joint venture with Vornado/Rudin that would value the Site at $1.2 billion ($900,000,000 to Vornado and $300,000,000 to Rudin) and build a new 1,700,000 square foot office tower (the “Project”) pursuant to East Midtown Subdistrict zoning with Vornado/Rudin as developer. KG would own 60% of the joint venture and Vornado/Rudin would own 40% (with Vornado owning 36% and Rudin owning 4% of the joint venture along with a $250,000,000 preferred equity interest in the Vornado/Rudin joint venture).

◦at the joint venture formation, Citadel or its affiliates will execute a pre-negotiated 15-year anchor lease with renewal options for approximately 850,000 square feet (with expansion and contraction rights) at the Project for its primary office in New York City;

◦the rent for Citadel’s space will be determined by a formula based on a percentage return (that adjusts based on the actual cost of capital) on the total Project cost;

◦the master leases will terminate at the scheduled commencement of demolition;

•or, exercise an option to purchase the Site for $1.4 billion ($1.085 billion to Vornado and $315,000,000 to Rudin), in which case Vornado/Rudin would not participate in the new development.

The parties intend to immediately commence design of the project and process approvals.

Further, Vornado/Rudin will have the option from October 2024 to September 2030 to put the Site to KG for $1.2 billion ($900,000,000 to Vornado and $300,000,000 to Rudin). For ten years following any put option closing, unless the put option is exercised in response to KG’s request to form the joint venture or KG makes a $200,000,000 termination payment, Vornado/Rudin will have the right to invest in a joint venture with KG on the terms described above if KG proceeds with development of the Site.

The operating and financial metrics presented in this supplemental package for the quarter and year ended December 31, 2022 do not reflect the impact of Citadel’s master lease of 350 Park Avenue described above as the transaction closed in the first quarter of 2023.

Dividend

On January 18, 2023, Vornado’s Board of Trustees declared a reduced quarterly dividend of $0.375 per share.

| | | | | | | | | | | | | | |

| FINANCIAL HIGHLIGHTS AND BUSINESS DEVELOPMENTS (unaudited) |

2022 Business Developments - continued

Disposition Activity

220 Central Park South (“220 CPS”)

During the three months ended December 31, 2022, we closed on the sale of two condominium units and ancillary amenities at 220 CPS for net proceeds of $71,895,000 resulting in a financial statement net gain of $34,844,000 which is included in "net gains on disposition of wholly owned and partially owned assets" on our consolidated statements of income. In connection with these sales, $5,071,000 of income tax expense was recognized on our consolidated statements of income. During the year ended December 31, 2022, we closed on the sale of three condominium units and ancillary amenities at 220 CPS for net proceeds of $88,019,000 resulting in a financial statement net gain of $41,874,000 which is included in "net gains on disposition of wholly owned and partially owned assets" on our consolidated statements of income. In connection with these sales, $6,016,000 of income tax expense was recognized on our consolidated statements of income. From inception to December 31, 2022, we have closed on the sale of 109 units and ancillary amenities for net proceeds of $3,094,915,000 resulting in financial statement net gains of $1,159,129,000. As of December 31, 2022, we are 97% sold.

SoHo Properties

On January 13, 2022, we sold two Manhattan retail properties located at 478-482 Broadway and 155 Spring Street for $84,500,000 and realized net proceeds of $81,399,000. In connection with the sale, we recognized a net gain of $551,000 which is included in "net gains on disposition of wholly owned and partially owned assets" on our consolidated statements of income.

Center Building (33-00 Northern Boulevard)

On June 17, 2022, we sold the Center Building, an eight-story 498,000 square foot office building located at 33‑00 Northern Boulevard in Long Island City, New York, for $172,750,000. We realized net proceeds of $58,946,000 after repayment of the existing $100,000,000 mortgage loan and closing costs. In connection with the sale, we recognized a net gain of $15,213,000 which is included in "net gains on disposition of wholly owned and partially owned assets" on our consolidated statements of income.

484-486 Broadway

On December 15, 2022, we sold 484-486 Broadway, a 30,000 square foot retail and residential building for $23,520,000, and realized net proceeds of $22,430,000. In connection with the sale, we recognized a net gain of $2,919,000 which is included in "net gains on disposition of wholly owned and partially owned assets" on our consolidated statements of income.

40 Fulton Street

On December 21, 2022, we sold 40 Fulton Street, a 251,000 square foot Manhattan office and retail building, for $101,000,000, and realized net proceeds of $96,566,000. In connection with the sale, we recognized a net gain of $31,876,000 which is included in "net gains on disposition of wholly owned and partially owned assets" on our consolidated statements of income.

| | | | | | | | | | | | | | |

| FINANCIAL HIGHLIGHTS AND BUSINESS DEVELOPMENTS (unaudited) |

2022 Business Developments - continued

Financing Activity

100 West 33rd Street

On June 15, 2022, we completed a $480,000,000 refinancing of 100 West 33rd Street, a 1.1 million square foot building comprised of 859,000 square feet of office space and 255,000 square feet of retail space. The interest-only loan bears a rate of SOFR plus 1.65% (5.96% as of December 31, 2022) through March 2024, increasing to SOFR plus 1.85% thereafter. The interest rate on the loan was swapped to a fixed rate of 5.06% through March 2024, and 5.26% through June 2027. The loan matures in June 2027, with two one-year extension options subject to debt service coverage ratio and loan-to-value tests. The loan replaces the previous $580,000,000 loan that bore interest at LIBOR plus 1.55% and was scheduled to mature in April 2024.

770 Broadway

On June 28, 2022, we completed a $700,000,000 refinancing of 770 Broadway, a 1.2 million square foot Class A Manhattan office building. The interest-only loan bears a rate of SOFR plus 2.25% (6.48% as of December 31, 2022) and matures in July 2024 with three one-year extension options (July 2027 as fully extended). The interest rate on the loan was swapped to a fixed rate of 4.98% through July 2027. The loan replaces the previous $700,000,000 loan that bore interest at SOFR plus 1.86% and was scheduled to mature in July 2022.

Unsecured Revolving Credit Facility

On June 30, 2022, we amended and extended one of our two revolving credit facilities. The $1.25 billion amended facility bears interest at a rate of SOFR plus 1.15% (5.47% as of December 31, 2022). The term of the facility was extended from March 2024 to December 2027, as fully extended. The facility fee is 25 basis points. On August 16, 2022, the interest rate on the $575,000,000 drawn on the facility was swapped to a fixed interest rate of 3.88% through August 2027. Our other $1.25 billion revolving credit facility matures in April 2026, as fully extended, and bears a rate of SOFR plus 1.19% with a facility fee of 25 basis points.

Unsecured Term Loan

On June 30, 2022, we extended our $800,000,000 unsecured term loan from February 2024 to December 2027. The extended loan bears interest at a rate of SOFR plus 1.30% (5.62% as of December 31, 2022) and is currently swapped to a fixed rate of 4.05%.

330 West 34th Street land owner joint venture

On August 18, 2022, the joint venture that owns the fee interest in the 330 West 34th Street land, in which we have a 34.8% interest, completed a $100,000,000 refinancing. The interest-only loan bears interest at a fixed rate of 4.55% and matures in September 2032. In connection with the refinancing, we realized net proceeds of $10,500,000. The loan replaces the previous $50,150,000 loan that bore interest at a fixed rate of 5.71%.

697-703 Fifth Avenue (Fifth Avenue and Times Square JV)

On December 21, 2022, the 697-703 Fifth Avenue $450,000,000 non-recourse mortgage loan matured and was not repaid, at which time the lenders declared an event of default. During December 2022, $29,000,000 of property-level funds were applied by the lenders against the principal balance resulting in a $421,000,000 loan balance as of December 31, 2022. The loan bears default interest at the Prime Rate plus 1.00% (8.50% as of December 31, 2022). The Fifth Avenue and Times Square JV is in negotiations with the lenders regarding a restructuring but there can be no assurance as to the timing and ultimate resolution of these negotiations. We do not believe that the resolution of these negotiations will result in further impairment losses on our investment in the Fifth Avenue and Times Square JV.

| | | | | | | | | | | | | | |

| FINANCIAL HIGHLIGHTS AND BUSINESS DEVELOPMENTS (unaudited) |

2022 Business Developments - continued

Financing Activity - continued

Interest Rate Hedging Activities

During the year ended December 31, 2022, we entered into $2.0 billion of interest rate swap arrangements and extended a $500,000,000 interest rate swap arrangement, reducing our variable rate debt at share as a percentage of our total debt at share to 27% from 47% (excluding our participation in the 150 West 34th Street mortgage loan which was repaid on January 9, 2023). The exposure to LIBOR/SOFR index increases on our $2.8 billion of unswapped variable rate debt is partially mitigated over the next year by $2.2 billion of interest rate caps and by an increase in interest income on our cash, cash equivalents, restricted cash and investments in U.S. Treasury bills. See page 12 for further detail on our interest rate swap and cap arrangements. The table below presents the interest rate swap arrangements entered into during the year ended December 31, 2022.

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| (Amounts in thousands) | | Notional Amount | | All-In Swapped Rate | | Swap Expiration Date | | Variable Rate Spread |

| 770 Broadway mortgage loan | | $ | 700,000 | | | 4.98% | | 07/27 | | S+225 |

| Unsecured revolving credit facility | | 575,000 | | | 3.88% | | 08/27 | | S+115 |

Unsecured term loan(1) | | 50,000 | | | 4.04% | | 08/27 | | S+130 |

Unsecured term loan (effective 10/23)(1) | | 500,000 | | | 4.39% | | 10/26 | | S+130 |

| 100 West 33rd Street mortgage loan | | 480,000 | | | 5.06% | | 06/27 | | S+165 |

888 Seventh Avenue mortgage loan(2) | | 200,000 | | | 4.76% | | 09/27 | | S+180 |

____________________

(1)On February 7, 2023, we entered into a forward interest rate swap arrangement for $150,000 of the $800,000 unsecured term loan. The unsecured term loan, which matures in December 2027, is subject to various interest rate swap arrangements through August 2027, see below for details:

| | | | | | | | | | | | | | | | | | | | |

| | Swapped Balance | | All-In Swapped Rate | | Unswapped Balance

(bears interest at S+130) |

| Through 10/23 | | $ | 800,000 | | | 4.05% | | $ | — | |

| 10/23 through 7/25 | | 700,000 | | | 4.53% | | 100,000 | |

| 7/25 through 10/26 | | 550,000 | | | 4.36% | | 250,000 | |

| 10/26 through 8/27 | | 50,000 | | | 4.04% | | 750,000 | |

(2)The remaining $77,800 amortizing mortgage loan balance bears interest at a floating rate of SOFR plus 1.80%.

| | | | | | | | | | | |

| FINANCIAL HIGHLIGHTS AND BUSINESS DEVELOPMENTS (unaudited) |

Leasing Activity

The leasing activity and related statistics below are based on leases signed during the period and are not intended to coincide with the commencement of rental revenue in accordance with GAAP. Second generation relet space represents square footage that has not been vacant for more than nine months and tenant improvements and leasing commissions are based on our share of square feet leased during the period.

For the Three Months Ended December 31, 2022

154,000 square feet of New York Office space (147,000 square feet at share) at an initial rent of $84.58 per square foot and a weighted average lease term of 7.6 years. The changes in the GAAP and cash mark-to-market rent on the 135,000 square feet of second generation space were positive 17.2% and positive 9.8%, respectively. Tenant improvements and leasing commissions were $10.32 per square foot per annum, or 12.2% of initial rent.

20,000 square feet of New York Retail space (15,000 square feet at share) at an initial rent of $284.73 per square foot and a weighted average lease term of 11.8 years. The 20,000 square feet was first generation space. Tenant improvements and leasing commissions were $26.98 per square foot per annum, or 9.5% of initial rent.

24,000 square feet at theMART (all at share) at an initial rent of $59.45 per square foot and a weighted average lease term of 6.5 years. The changes in the GAAP and cash mark-to-market rent on the 23,000 square feet of second generation space were negative 7.3% and negative 12.1%, respectively. Tenant improvements and leasing commissions were $6.60 per square foot per annum, or 11.1% of initial rent.

For the Year Ended December 31, 2022

894,000 square feet of New York Office space (753,000 square feet at share) at an initial rent of $84.51 per square foot and a weighted average lease term of 8.9 years. The changes in the GAAP and cash mark-to-market rent on the 498,000 square feet of second generation space were positive 9.0% and positive 5.4%, respectively. Tenant improvements and leasing commissions were $11.84 per square foot per annum, or 14.0% of initial rent.

111,000 square feet of New York Retail space (100,000 square feet at share) at an initial rent of $266.25 per square foot and a weighted average lease term of 11.6 years. The changes in the GAAP and cash mark-to-market rent on the 42,000 square feet of second generation space were negative 38.3% and negative 34.2%, respectively. Tenant improvements and leasing commissions were $22.68 per square foot per annum, or 8.5% of initial rent.

299,000 square feet at theMART (all at share) at an initial rent of $52.40 per square foot and a weighted average lease term of 7.2 years. The changes in the GAAP and cash mark-to-market rent on the 244,000 square feet of second generation space were negative 4.8% and negative 5.4%, respectively. Tenant improvements and leasing commissions were $10.48 per square foot per annum, or 20.0% of initial rent.

210,000 square feet at 555 California Street (147,000 square feet at share) at an initial rent of $96.40 per square foot and a weighted average lease term of 5.9 years. The changes in the GAAP and cash mark-to-market rent on the 135,000 square feet of second generation space were positive 24.3% and positive 13.6%, respectively. Tenant improvements and leasing commissions were $7.15 per square foot per annum, or 7.4% of initial rent.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| UNSECURED NOTES COVENANT RATIOS AND CREDIT RATINGS (unaudited) | | |

| (Amounts in thousands) | | As of |

Unsecured Notes Covenant Ratios(1) | | Required | | December 31, 2022 | | September 30,

2022 | | June 30,

2022 | | March 31,

2022 |

Total outstanding debt/total assets(2) | | Less than 65% | | 48% | | 47% | | 47% | | 48% |

| Secured debt/total assets | | Less than 50% | | 32% | | 32% | | 31% | | 33% |

| Interest coverage ratio (annualized combined EBITDA to annualized interest expense) | | Greater than 1.50 | | 2.29 | | 2.53 | | 3.02 | | 3.29 |

| Unencumbered assets/unsecured debt | | Greater than 150% | | 342% | | 354% | | 362% | | 360% |

| | | | | | | | |

Consolidated Unencumbered EBITDA(1) (non-GAAP): | | Q4 2022

Annualized |

| New York | | $ | 251,072 | |

| Other | | 106,772 | |

| Total | | $ | 357,844 | |

| | | | | | | | | | | | | | |

Credit Ratings(3): | | Rating | | Outlook |

| Moody’s | | Baa3 | | Stable |

| S&P | | BBB- | | Stable |

| Fitch | | BBB- | | Negative |

| | | | | | | | |

| | |

| (1) | Our debt covenant ratios and consolidated unencumbered EBITDA are computed in accordance with the terms of our senior unsecured notes. The methodology used for these computations may differ significantly from similarly titled ratios and amounts of other companies. For additional information regarding the methodology used to compute these ratios and amounts, please see our filings with the SEC of our senior debt indentures and applicable prospectuses and prospectus supplements. |

| (2) | Total assets include EBITDA capped at 7.0% per the terms of our senior unsecured notes covenants. |

| (3) | Credit ratings are provided for informational purposes only and are not a recommendation to buy or sell our securities. |

| | | | | | | | | | | |

| LIQUIDITY AND CAPITALIZATION (unaudited) |

| (Amounts in millions, except per share amounts) | |

| | | | | | | | | | | | | | |

| | | | |

| (1) | Prior to June 30, 2022, the $1.25 billion revolving credit facility maturing in 2027, as fully extended, had full capacity of $1.5 billion. |

| (2) | The debt balances presented represent contractual debt balances. See reconciliation on page iii in the Appendix of consolidated debt, net as presented on our consolidated balance sheets to consolidated contractual debt as of December 31, 2022. |

| (3) | Based on the Vornado Realty Trust (NYSE: VNO) December 31, 2022 quarter end closing common share price of $20.81. |

| | | | | | | | | | | | | | |

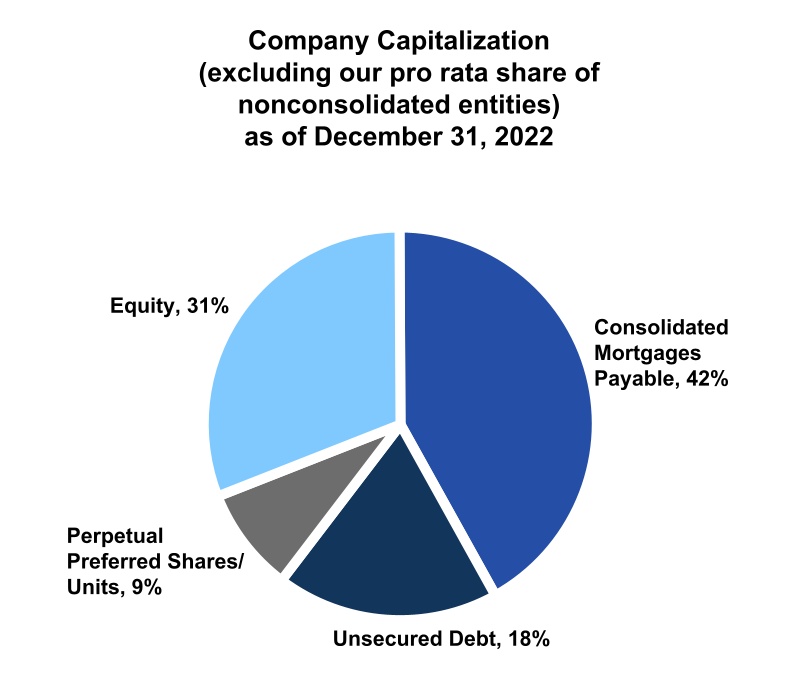

Company capitalization(2): | Amount | | % Total |

| Consolidated mortgages payable (at 100%) | $ | 5,878 | | | 42% |

| Unsecured debt (contractual) | 2,575 | | | 18% |

| Perpetual preferred shares/units | 1,223 | | | 9% |

Equity(3) | 4,342 | | | 31% |

| Total | 14,018 | | | 100% |

| Pro rata share of debt of non-consolidated entities | 2,697 | | | |

| Less: Noncontrolling interests' share of consolidated debt | (682) | | | |

| Total at share | $ | 16,033 | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| NET DEBT TO EBITDAre, AS ADJUSTED (unaudited) | | | | | |

| (Amounts in millions) | | | | | | | | |

| As of and For the Year Ended December 31, | |

| 2022 | | 2021 | | 2020 | | 2019 | |

| | | | | | | | |

| Secured debt | $ | 5,878 | | | $ | 6,099 | | | $ | 5,608 | | | $ | 5,670 | | |

| Unsecured debt | 2,575 | | | 2,575 | | | 1,825 | | | 1,775 | | |

| Pro rata share of debt of non-consolidated entities | 2,697 | | | 2,700 | | | 2,873 | | | 2,803 | | |

| Less: Noncontrolling interests’ share of consolidated debt | (682) | | | (682) | | | (483) | | | (483) | | |

| Company’s pro rata share of total debt | $ | 10,468 | | | $ | 10,692 | | | $ | 9,823 | | | $ | 9,765 | | |

| % Unsecured debt | 25% | | 24% | | 19% | | 18% | |

| | | | | | | | |

| Company’s pro rata share of total debt | $ | 10,468 | | | $ | 10,692 | | | $ | 9,823 | | | $ | 9,765 | | |

| Less: Cash and cash equivalents, restricted cash and investments in U.S. Treasury bills | (1,493) | | | (1,930) | | | (1,730) | | | (1,242) | | (1) |

Less: Participation in 150 West 34th Street mortgage loan(2) | (105) | | | (105) | | | (105) | | | (105) | | |

| Less: Projected cash proceeds from 220 Central Park South | (90) | | | (148) | | | (275) | | | (1,200) | | |

| Net debt | $ | 8,780 | | | $ | 8,509 | | | $ | 7,713 | | | $ | 7,218 | | |

| EBITDAre, as adjusted (non-GAAP) | $ | 1,091 | | | $ | 949 | | | $ | 910 | | | $ | 1,136 | | |

| Net debt / EBITDAre, as adjusted | 8.0 | x | | 9.0 | x | | 8.5 | x | | 6.4 | x | |

______________________________

(1)2019 includes $33 of investments in marketable securities sold in January 2020 and is reduced by a $398 accrual of a special dividend/distribution paid in January 2020.

(2)On January 9, 2023, our $105 participation in the $205 mortgage loan on 150 West 34th Street was repaid.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| DEBT SNAPSHOT (unaudited) | | | | | | | | | | | |

| (Amounts in millions) | | | | | | | | | | | |

| As of December 31, 2022 |

| Total | | Variable | | Fixed |

| (Contractual debt balances) | Amount | | Weighted

Average

Interest Rate | | Amount | | Weighted

Average

Interest Rate | | Amount | | Weighted

Average

Interest Rate |

Consolidated debt(1) | $ | 8,453 | | | 4.16% | | $ | 2,308 | (2) | 5.67% | | $ | 6,145 | | 3.59% |

| Pro rata share of debt of non-consolidated entities | 2,697 | | | 4.87% | | 1,250 | | 6.19% | | 1,447 | | 3.72% |

| Total | 11,150 | | 4.33% | | 3,558 | | 5.85% | | 7,592 | | 3.61% |

| Less: Noncontrolling interests' share of consolidated debt (primarily 1290 Avenue of the Americas and 555 California Street) | (682) | | | | | (682) | | | | — | | | |

| Company's pro rata share of total debt | $ | 10,468 | | | 4.23% | | $ | 2,876 | (2) | 5.87% | | $ | 7,592 | | 3.61% |

| | | | | | | | | | | |

| | | | | | | | | | | |

________________________________

(1)See reconciliation on page iii in the Appendix of consolidated debt, net as presented on our consolidated balance sheets to consolidated contractual debt as of December 31, 2022.

(2)Includes our $105 participation in the loan. On January 9, 2023, our $105 participation in the $205 mortgage loan on 150 West 34th Street was repaid.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| HEDGING INSTRUMENTS AS OF DECEMBER 31, 2022 (unaudited) |

| (Amounts in thousands) | | | | | | | | | | | | |

| | Debt Information | | Swap / Cap Information |

| | Balance

at Share | | Variable Rate Spread | | Maturity Date(1) | | Notional Amount

at Share | | All-In Swapped Rate | | Swap Expiration Date |

| Interest Rate Swaps: | | | | | | | | | | | | |

| Consolidated: | | | | | | | | | | | | |

| 555 California Street mortgage loan | | $ | 840,000 | | | L+193 | | 05/28 | | $ | 840,000 | | | 2.26% | | 05/24 |

| 770 Broadway mortgage loan | | 700,000 | | | S+225 | | 07/27 | | 700,000 | | | 4.98% | | 07/27 |

| PENN 11 mortgage loan | | 500,000 | | | S+206 | | 10/25 | | 500,000 | | | 2.22% | | 03/24 |

| Unsecured revolving credit facility | | 575,000 | | | S+115 | | 12/27 | | 575,000 | | | 3.88% | | 08/27 |

| Unsecured term loan | | 800,000 | | | S+130 | | 12/27 | | 800,000 | | (2) | 4.05% | | 10/23 |

| 100 West 33rd Street mortgage loan | | 480,000 | | | S+165 | | 06/27 | | 480,000 | | | 5.06% | | 06/27 |

| 888 Seventh Avenue mortgage loan | | 277,800 | | | S+180 | | 12/25 | | 200,000 | | | 4.76% | | 09/27 |

| 4 Union Square South mortgage loan | | 120,000 | | | S+150 | | 08/25 | | 100,000 | | | 3.74% | | 01/25 |

| Unconsolidated: | | | | | | | | | | | | |

| 640 Fifth Avenue mortgage loan | | 259,925 | | | L+101 | | 05/24 | | 259,925 | | | 3.07% | | 05/23 |

| 731 Lexington Avenue - retail condominium mortgage loan | | 97,200 | | | S+151 | | 08/25 | | 97,200 | | | 1.76% | | 05/25 |

| 50-70 West 93rd Street mortgage loan | | 41,667 | | | L+153 | | 12/24 | | 41,168 | | | 3.14% | | 06/24 |

| | $ | 4,691,592 | | | | | | | 4,593,293 | | | | | |

| | | | | | | | | | | | |

| Interest Rate Caps: | | | | | | | | | | Index Strike Rate | | |

| Consolidated: | | | | | | | | | | | |

| 1290 Avenue of the Americas mortgage loan | | $ | 665,000 | | | L+151 | | 11/28 | | 665,000 | | | 4.00% | | 11/23 |

| One Park Avenue mortgage loan | | 525,000 | | | S+122 | | 03/26 | | 525,000 | | (3) | 4.39% | | 03/23 |

| 150 West 34th Street mortgage loan | | 205,000 | | | S+199 | | 05/24 | | 100,000 | | (4) | 4.10% | | 06/24 |

| 606 Broadway mortgage loan | | 37,060 | | | S+191 | | 09/24 | | 37,060 | | | 4.00% | | 09/24 |

| Unconsolidated: | | | | | | | | | | | | |

| 280 Park Avenue mortgage loan | | 600,000 | | | L+173 | | 09/24 | | 600,000 | | | 4.08% | | 09/23 |

| 61 Ninth Avenue mortgage loan | | 75,543 | | | S+146 | | 01/26 | | 75,543 | | | 4.39% | | 02/24 |

| 512 West 22nd Street mortgage loan | | 75,418 | | | L+200 | | 06/23 | | 75,418 | | | 4.00% | | 06/23 |

| Rego Park II mortgage loan | | 65,624 | | | S+145 | | 12/25 | | 65,624 | | | 4.15% | | 11/24 |

| Fashion Centre Mall/Washington Tower mortgage loan | | 34,125 | | | L+294 | | 05/26 | | 34,125 | | | 4.00% | | 05/24 |

| | $ | 2,282,770 | | | | | | | 2,177,770 | | (5) | | | |

| | | | | | | | | | | | |

| Fixed rate debt per loan agreements and Vornado’s $105 million participation in 150 West 34th Street mortgage loan | | | | 3,104,164 | | | | | |

| Variable rate debt not subject to interest rate swaps or caps | | | | | | | | 592,555 | | (5) | | | |

| Total debt at share | | | | | | | | $ | 10,467,782 | | | | | |

________________________________

(1)Assumes the exercise of as-of-right extension options.

(2)The unsecured term loan is subject to various interest rate swap arrangements during its term, See page 7 for details. (3)In December 2022, we entered into a forward cap for the $525,000 One Park Avenue mortgage loan effective upon the March 2023 expiration of the existing cap. The forward cap has a SOFR strike rate of 3.89% and expires in March 2024.

(4)Excludes our $105,000 participation in the loan. On January 9, 2023, our $105,000 participation in the $205,000 mortgage loan on 150 West 34th Street was repaid. The remaining $100,000 balance will bear interest at a floating rate of S+1.86% subject to the interest rate cap arrangement disclosed above.

(5)Our exposure to LIBOR/SOFR index increases is partially mitigated by an increase in interest income on our cash, cash equivalents, restricted cash and investments in U.S. Treasury bills.

| | | | | | | | | | | | | | |

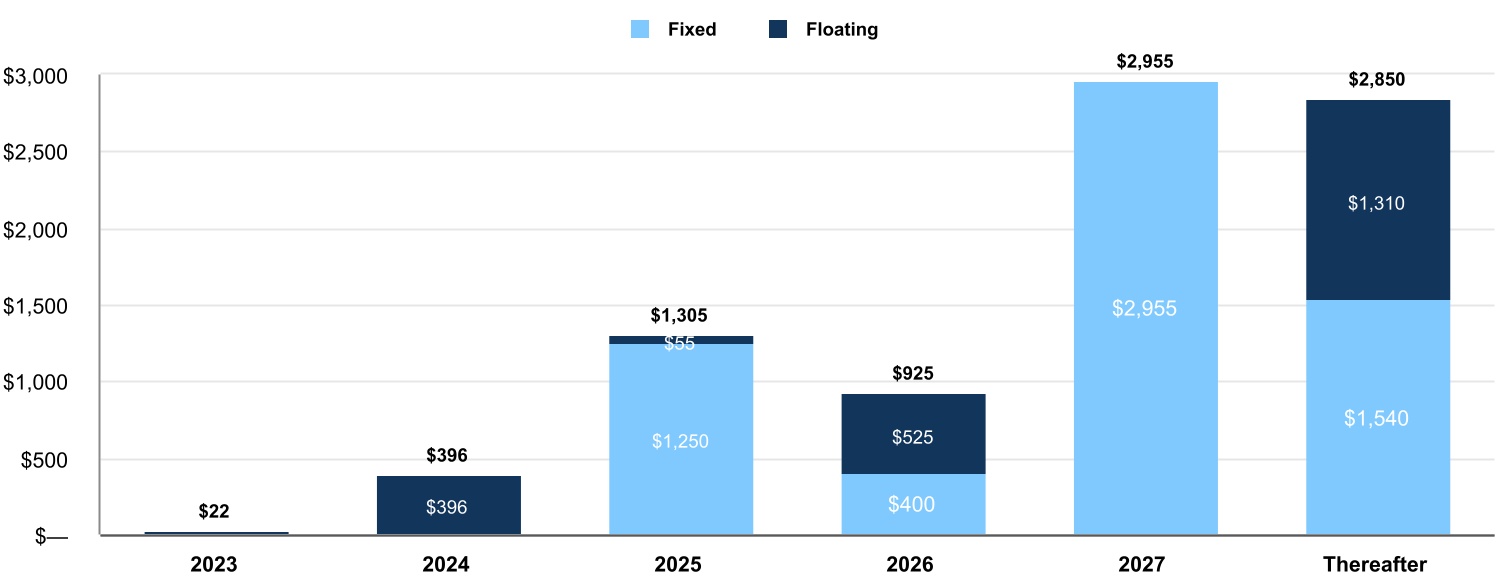

| CONSOLIDATED DEBT MATURITIES (CONTRACTUAL BALANCES) (unaudited) |

| (Amounts in millions) | | | | |

| | |

Consolidated Debt Maturity Schedule(1) as of December 31, 2022 (Excludes pro rata share of JV debt)(2) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Consolidated (100%): | | | | | | | | | | | | |

| Secured | $ | 22 | | | $ | 396 | | (3) | $ | 855 | | | $ | 525 | | | $ | 1,580 | | | $ | 2,500 | | |

| Unsecured | — | | | — | | | 450 | | | 400 | | | 1,375 | | | 350 | | |

| Total consolidated debt (100%) | $ | 22 | | | $ | 396 | | | $ | 1,305 | | | $ | 925 | | | $ | 2,955 | | | $ | 2,850 | | (4) |

| % of total consolidated debt | 0.3 | % | | 4.7 | % | | 15.4 | % | | 10.9 | % | | 35.0 | % | | 33.7 | % | |

| Debt maturities at share: | | | | | | | | | | | | |

| Consolidated debt (100%) | $ | 22 | | | $ | 396 | | | $ | 1,305 | | | $ | 925 | | | $ | 2,955 | | | $ | 2,850 | | |

| Pro rata share of debt of non-consolidated entities | 312 | | (5) | 1,064 | | | 505 | | | 581 | | | 40 | | | 195 | | |

| Less: Noncontrolling interests' share of consolidated debt | — | | | (37) | | | — | | | — | | | — | | | (645) | | |

| Total debt at share | $ | 334 | | | $ | 1,423 | | | $ | 1,810 | | | $ | 1,506 | | | $ | 2,995 | | | $ | 2,400 | | |

| % of total debt at share | 3.2 | % | | 13.6 | % | | 17.3 | % | | 14.4 | % | | 28.6 | % | | 22.9 | % | |

_______________________________

(1)Assumes the exercise of as-of-right extension options. Debt classified as fixed rate includes the effect of interest rate swap arrangements which may expire prior to debt maturity. See the previous page for information on interest rate swap arrangements entered into as of December 31, 2022.

(2)Vornado Realty L.P. guarantees $800 of JV partnership debt comprised of the $300 mortgage loan on 7 West 34th Street and the $500 mortgage loan on 640 Fifth Avenue included in the Fifth Avenue and Times Square JV. This $800 is excluded from the schedule presented above.

(3)We hold a $105 participation in the 150 West 34th Street mortgage loan which is included in “other assets” on our consolidated balance sheets. On January 9, 2023, our $105 participation in the $205 mortgage loan on 150 West 34th Street was repaid.

(4)Of the $1,310 floating rate debt expiring after 2027, $645 is attributable to noncontrolling interests.

(5)2023 includes our $189 share of the 697-703 Fifth Avenue mortgage loan. On December 21, 2022, the 697-703 Fifth Avenue $450 non-recourse mortgage loan matured and was not repaid, at which time the lenders declared an event of default. During December 2022, $29 of property-level funds were applied by the lenders against the principal balance resulting in a $421 loan balance as of December 31, 2022. The Fifth Avenue and Times Square JV is in negotiations with the lenders regarding a restructuring but there can be no assurance as to the timing and ultimate resolution of these negotiations.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| CONSOLIDATED DEBT MATURITIES AT 100% (CONTRACTUAL BALANCES) (unaudited) |

| (Amounts in thousands) | | | | | | | | | | | | | | | | | | | | |

| Property | | Maturity Date(1) | | Spread over

LIBOR/SOFR | | Interest Rate(2) | | 2023 | | 2024 | | 2025 | | 2026 | | 2027 | | Thereafter | | Total |

| Secured Debt: | | | | | | | | | | | | | | | | | | | | |

| 435 Seventh Avenue | | 02/24 | | L+130 | | 5.47% | | $ | — | | $ | 95,696 | | $ | — | | $ | — | | $ | — | | $ | — | | $ | 95,696 |

| 150 West 34th Street | | 05/24 | | S+199 | | 6.15% | | — | | 205,000 | (3) | — | | — | | — | | — | | 205,000 |

| 606 Broadway (50.0% interest) | | 09/24 | | S+191 | | 5.91% | | — | | 74,119 | | — | | — | | — | | — | | 74,119 |

| 4 Union Square South | | 08/25 | | | | 4.05% | | — | | — | | 120,000 | | — | | — | | — | | 120,000 |

| PENN 11 | | 10/25 | | | | 2.22% | | — | | — | | 500,000 | | — | | — | | — | | 500,000 |

| 888 Seventh Avenue | | 12/25 | | | | 5.09% | | 21,600 | | 21,600 | | 234,600 | | — | | — | | — | | 277,800 |

| One Park Avenue | | 03/26 | | S+122 | | 5.56% | | — | | — | | — | | 525,000 | | — | | — | | 525,000 |

| 350 Park Avenue | | 01/27 | | | | 3.92% | | — | | — | | — | | — | | 400,000 | | — | | 400,000 |

| 100 West 33rd Street | | 06/27 | | | | 5.06% | | — | | — | | — | | — | | 480,000 | | — | | 480,000 |

| 770 Broadway | | 07/27 | | | | 4.98% | | — | | — | | — | | — | | 700,000 | | — | | 700,000 |

| 555 California Street (70.0% interest) | | 05/28 | | | | 3.36% | | — | | — | | — | | — | | — | | 1,200,000 | | 1,200,000 |

| 1290 Avenue of the Americas (70.0% interest) | | 11/28 | | L+151 | | 5.51% | | — | | — | | — | | — | | — | | 950,000 | | 950,000 |

| 909 Third Avenue | | 04/31 | | | | 3.23% | | — | | — | | — | | — | | — | | 350,000 | | 350,000 |

| Total Secured Debt | | | | | | | | 21,600 | | 396,415 | | 854,600 | | 525,000 | | 1,580,000 | | 2,500,000 | | 5,877,615 |

| Unsecured Debt: | | | | | | | | | | | | | | | | | | | | |

| Senior unsecured notes due 2025 | | 01/25 | | | | 3.50% | | — | | — | | 450,000 | | — | | — | | — | | 450,000 |

| $1.25 Billion unsecured revolving credit facility | | 04/26 | | S+119 | | 0.00% | | — | | — | | — | | — | | — | | — | | — |

| Senior unsecured notes due 2026 | | 06/26 | | | | 2.15% | | — | | — | | — | | 400,000 | | — | | — | | 400,000 |

| $1.25 Billion unsecured revolving credit facility | | 12/27 | | | | 3.88% | | — | | — | | — | | — | | 575,000 | | — | | 575,000 |

| $800 Million unsecured term loan | | 12/27 | | | | 4.05% | | — | | — | | — | | — | | 800,000 | | — | | 800,000 |

| Senior unsecured notes due 2031 | | 06/31 | | | | 3.40% | | — | | — | | — | | — | | — | | 350,000 | | 350,000 |

| Total Unsecured Debt | | | | | | | | — | | — | | 450,000 | | 400,000 | | 1,375,000 | | 350,000 | | 2,575,000 |

| Total Debt | | | | | | | | $ | 21,600 | | $ | 396,415 | | $ | 1,304,600 | | $ | 925,000 | | $ | 2,955,000 | | $ | 2,850,000 | | $ | 8,452,615 |

| Weighted average rate | | | | | | | | 5.92% | | 5.93% | | 3.32% | | 4.08% | | 4.38% | | 4.07% | | 4.16% |

| | | | | | | | | | | | | | | | | | | | |

Fixed rate debt(4) | | | | | | | | $ | — | | $ | — | | $ | 1,250,000 | | $ | 400,000 | | $ | 2,955,000 | | $ | 1,540,000 | | $ | 6,145,000 |

| Fixed weighted average rate expiring | | | | | | | | 0.00% | | 0.00% | | 3.21% | | 2.15% | | 4.38% | | 2.74% | | 3.59% |

| Floating rate debt | | | | | | | | $ | 21,600 | | $ | 396,415 | | $ | 54,600 | | $ | 525,000 | | $ | — | | $ | 1,310,000 | | $ | 2,307,615 |

| Floating weighted average rate expiring | | | | | | | | 5.92% | | 5.93% | | 5.81% | | 5.56% | | 0.00% | | 5.63% | | 5.67% |

________________________________

(1)Assumes the exercise of as-of-right extension options.

(2)Represents the interest rate in effect as of period end based on the appropriate reference rate as of the contractual reset date plus contractual spread, adjusted for hedging instruments, as applicable. See Page 12 for information on interest rate swap and interest rate cap arrangements entered into as of December 31, 2022

(3)We hold a $105,000 participation in the mortgage loan which is included in “other assets” on our consolidated balance sheets. On January 9, 2023, our $105,000 participation in the $205,000 mortgage loan on 150 West 34th Street was repaid. The remaining $100,000 balance will bear interest at a floating rate of S+1.86% subject to the interest rate cap arrangement disclosed on page 12.

(4)Debt classified as fixed rate includes the effect of interest rate swap arrangements which may expire prior to debt maturity. See page 12 for information on interest rate swap arrangements entered into as of December 31, 2022.

| | | | | | | | | | | | | | | | | | | | |

| TOP 15 TENANTS (unaudited) | | | | | | | |

| (Amounts in thousands, except square feet) | | | | | | | |

| | | | Square Footage At Share | | Annualized Escalated Rents At Share(1) | | % of Total Annualized Escalated Rents

At Share |

| Meta Platforms, Inc. | | | 1,451,153 | | | $ | 158,889 | | | 8.8 | % |

| IPG and affiliates | | | 967,552 | | | 67,279 | | | 3.6 | % |

| New York University | | | 685,290 | | | 45,013 | | | 2.5 | % |

| Google/Motorola Mobility (guaranteed by Google) | | | 759,446 | | | 41,220 | | | 2.2 | % |

| Bloomberg L.P. | | | 306,768 | | | 40,252 | | | 2.2 | % |

| Equitable Financial Life Insurance Company | | | 336,644 | | | 35,453 | | | 2.0 | % |

| Yahoo Inc. | | | 313,726 | | | 32,202 | | | 1.8 | % |

| Amazon (including its Whole Foods subsidiary) | | | 312,694 | | | 30,115 | | | 1.7 | % |

| Neuberger Berman Group LLC | | | 306,612 | | | 27,283 | | | 1.5 | % |

| Madison Square Garden & Affiliates | | | 412,551 | | | 27,143 | | | 1.5 | % |

| Swatch Group USA | | | 14,949 | | | 26,173 | | | 1.4 | % |

| AMC Networks, Inc. | | | 326,717 | | | 25,391 | | | 1.4 | % |

| Bank of America | | | 247,459 | | | 24,500 | | | 1.4 | % |

| Apple Inc. | | | 412,434 | | | 24,072 | | | 1.3 | % |

| LVMH Brands | | | 65,060 | | | 23,132 | | | 1.3 | % |

| | | | | | | | 34.6 | % |

________________________________

(1)Represents monthly contractual base rent before free rent plus tenant reimbursements multiplied by 12. Annualized escalated rents at share include leases signed but not yet commenced in place of current tenants or vacancy in the same space.

| | | | | | | | | | | | | | |

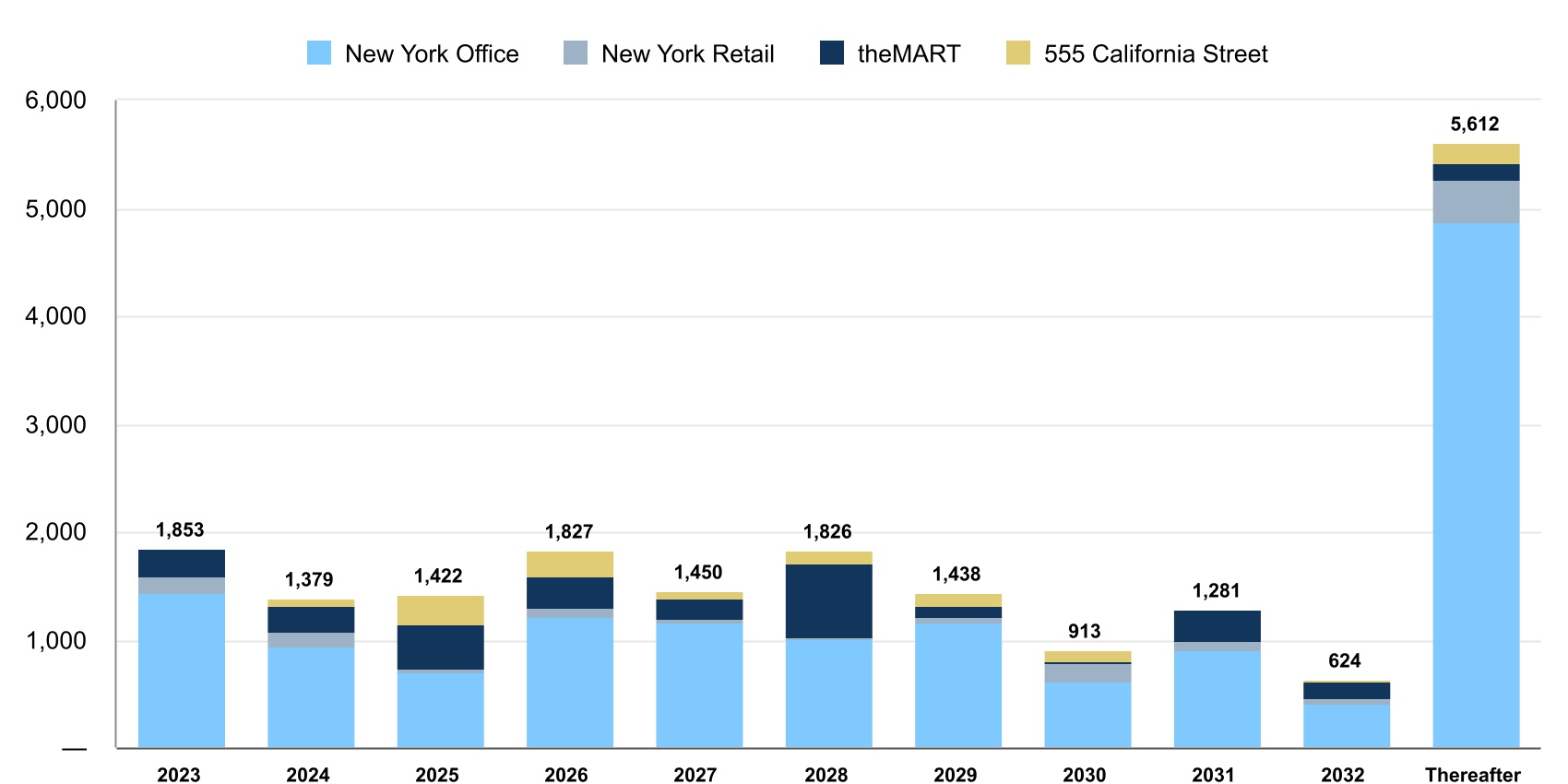

| LEASE EXPIRATIONS (unaudited) | | | | |

| (Amounts in thousands) | | | | |

| | |

Our Share of Square Feet of Expiring Leases

As of December 31, 2022 |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| New York Office | 1,444 | | | 943 | | | 699 | | | 1,217 | | | 1,160 | | | 1,003 | | | 1,161 | | | 623 | | | 899 | | | 404 | | | 4,867 | | | | |

| New York Retail | 149 | | | 133 | | | 40 | | | 82 | | | 34 | | | 27 | | | 50 | | | 155 | | | 88 | | | 55 | | | 390 | | | | |

| theMart | 254 | | | 233 | | | 409 | | | 290 | | | 191 | | | 684 | | | 111 | | | 29 | | | 294 | | | 160 | | | 167 | | | | |

| 555 California Street | 6 | | | 70 | | | 274 | | | 238 | | | 65 | | | 112 | | | 116 | | | 106 | | | — | | | 5 | | | 188 | | | | |

| Total | 1,853 | | | 1,379 | | | 1,422 | | | 1,827 | | | 1,450 | | | 1,826 | | | 1,438 | | | 913 | | | 1,281 | | | 624 | | | 5,612 | | | | |

| % of total | 9.4% | | 7.0% | | 7.2% | | 9.3% | | 7.4% | | 9.3% | | 7.3% | | 4.7% | | 6.5% | | 3.2% | | 28.7% | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| PENN DISTRICT | | | | | | | | | | | | | | | | |

| ACTIVE DEVELOPMENT/REDEVELOPMENT SUMMARY - AS OF DECEMBER 31, 2022 (unaudited) |

| (Amounts in thousands of dollars, except square feet) | | | | | | | | | | | | | | | | |

| | | | Property

Rentable

Sq. Ft. | | | | Cash Amount

Expended | | Remaining Expenditures | | Stabilization Year | | Projected Incremental Cash Yield |

| Active PENN District Projects | | Segment | | | Budget(1) | | | | |

| The Farley Building (95% interest) | | New York | | 846,000 | | | 1,120,000 | | (2) | 1,111,493 | | (2) | 8,507 | | (2) | (3) | | | 6.2% | |

| PENN 2 - as expanded | | New York | | 1,795,000 | | | 750,000 | | | 393,126 | | | 356,874 | | | 2025 | | | 9.5% | |

PENN 1 (including LIRR Concourse Retail)(4) | | New York | | 2,546,000 | | | 450,000 | | | 375,810 | | | 74,190 | | | N/A | | | 13.2% | (4)(5) |

| Districtwide Improvements | | New York | | N/A | | 100,000 | | | 41,776 | | | 58,224 | | | N/A | | | N/A | |

| Total Active PENN District Projects | | | | | | 2,420,000 | | | 1,922,205 | | | 497,795 | | | | | | 8.3% | |

___________________

(1)Excluding debt and equity carry.

(2)Net of 154,000 of historic tax credit investor contributions, of which 88,000 has been funded to date (at our 95% share).

(3)Office stabilized in 2022, Retail to stabilize in 2023/2024.

(4)Property is ground leased through 2098, as fully extended. Fair market value resets occur in 2023, 2048 and 2073. The 13.2% projected return is before the ground rent reset in 2023, which may be material.

(5)Projected to be achieved as pre-redevelopment leases roll, which have an approximate average remaining term of 3.6 years.

There can be no assurance that the above projects will be completed, completed on schedule or within budget. In addition, there can be no assurance that the Company will be successful in leasing the properties on the expected schedule or at the assumed rental rates.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

APPENDIX NON-GAAP RECONCILIATIONS |

| | | | | | | | | | | | | | | | | | | | | | | |

NON-GAAP RECONCILIATIONS RECONCILIATION OF NET (LOSS) INCOME ATTRIBUTABLE TO COMMON SHAREHOLDERS TO NET INCOME ATTRIBUTABLE TO COMMON SHAREHOLDERS, AS ADJUSTED (unaudited) |

| (Amounts in thousands, except per share amounts) |

| For the Three Months Ended | | For the Year Ended |

| December 31, | | December 31, |

| 2022 | | 2021 | | 2022 | | 2021 |

| Net (loss) income attributable to common shareholders | $ | (493,280) | | | $ | 11,269 | | | $ | (408,615) | | | $ | 101,086 | |

| Per diluted share | $ | (2.57) | | | $ | 0.06 | | | $ | (2.13) | | | $ | 0.53 | |

| | | | | | | |

| Certain expense (income) items that impact net (loss) income attributable to common shareholders: | | | | | | | |

| Non-cash real estate impairment losses on wholly owned and partially owned assets | 595,488 | | | — | | | 595,488 | | | 7,880 | |

| Net gains on disposition of wholly owned and partially owned assets | (47,769) | | | (11,620) | | | (62,685) | | | (15,315) | |

| After-tax net gain on sale of 220 CPS condominium units and ancillary amenities | (29,773) | | | (13,584) | | | (35,858) | | | (44,607) | |

| Hotel Pennsylvania loss (primarily accelerated building depreciation expense) | 26,614 | | | 8,998 | | | 71,087 | | | 29,472 | |

| Deferred tax liability on our investment in The Farley Building (held through a taxable REIT subsidiary) | 3,482 | | | 9,180 | | | 13,665 | | | 10,868 | |

| Refund of New York City transfer taxes related to the April 2019 transfer to Fifth Avenue and Times Square JV | — | | | — | | | (13,613) | | | — | |

| Other | 3,449 | | | 19,569 | | | 7,289 | | | (2,436) | |

| 551,491 | | | 12,543 | | | 575,373 | | | (14,138) | |

| Noncontrolling interests' share of above adjustments | (38,257) | | | (835) | | | (40,290) | | | 1,205 | |

| Total of certain expense (income) items that impact net (loss) income attributable to common shareholders | $ | 513,234 | | | $ | 11,708 | | | $ | 535,083 | | | $ | (12,933) | |

| | | | | | | |

| | | | | | | |

| Net income attributable to common shareholders, as adjusted (non-GAAP) | $ | 19,954 | | | $ | 22,977 | | | $ | 126,468 | | | $ | 88,153 | |

| Per diluted share (non-GAAP) | $ | 0.10 | | | $ | 0.12 | | | $ | 0.66 | | | $ | 0.46 | |

| | | | | | | | | | | | | | | | | |

NON-GAAP RECONCILIATIONS CONSOLIDATED DEBT, NET TO CONSOLIDATED CONTRACTUAL DEBT (unaudited) | |

| (Amounts in thousands) |

| As of December 31, 2022 |

| Consolidated

Debt, Net | | Deferred Financing

Costs, Net and Other | | Consolidated Contractual Debt |

| Mortgages payable | $ | 5,829,018 | | $ | 48,597 | | $ | 5,877,615 |

| Senior unsecured notes | 1,191,832 | | 8,168 | | 1,200,000 |

| $800 Million unsecured term loan | 793,193 | | 6,807 | | 800,000 |

| $2.5 Billion unsecured revolving credit facilities | 575,000 | | | — | | 575,000 |

| $ | 8,389,043 | | $ | 63,572 | | $ | 8,452,615 |

| | | | | | | | | | | | | | | | | | | | | | | |

NON-GAAP RECONCILIATIONS RECONCILIATION OF NET (LOSS) INCOME TO EBITDAre (unaudited) |

| (Amounts in thousands) | | | | | |

EBITDAre (i.e., EBITDA for real estate companies) is a non-GAAP financial measure established by the National Association of Real Estate Investment Trusts ("NAREIT"), which may not be comparable to EBITDA reported by other REITs that do not compute EBITDA in accordance with the NAREIT definition. NAREIT defines EBITDAre as GAAP net income or loss, plus interest expense, plus income tax expense, plus depreciation and amortization, plus (minus) losses and gains on the disposition of depreciated property including losses and gains on change of control, plus impairment write-downs of depreciated property and of investments in unconsolidated joint ventures caused by a decrease in value of depreciated property in the joint venture, plus adjustments to reflect the entity's share of EBITDA of unconsolidated joint ventures. The Company has included EBITDAre because it is a performance measure used by other REITs and therefore may provide useful information to investors in comparing Vornado's performance to that of other REITs.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| For the Three Months Ended December 31, | | For the Year Ended December 31, |

| 2022 | | 2021 | | 2022 | | 2021 | | 2020 | | 2019 |

| Reconciliation of net (loss) income to EBITDAre (non-GAAP): | | | | | | | | | | | |

| Net (loss) income | $ | (525,002) | | | $ | 31,963 | | | $ | (382,612) | | | $ | 207,553 | | | $ | (461,845) | | | $ | 3,334,262 | |

| Less net loss (income) attributable to noncontrolling interests in consolidated subsidiaries | 10,493 | | | (3,691) | | | 5,737 | | | (24,014) | | | 139,894 | | | 24,547 | |

| Net (loss) income attributable to the Operating Partnership | (514,509) | | | 28,272 | | | (376,875) | | | 183,539 | | | (321,951) | | | 3,358,809 | |

| EBITDAre adjustments at share: | | | | | | | | | | | |

| Depreciation and amortization expense | 155,524 | | | 153,136 | | | 593,322 | | | 526,539 | | | 532,298 | | | 530,473 | |

| Interest and debt expense | 111,848 | | | 88,647 | | | 362,321 | | | 297,116 | | | 309,003 | | | 390,139 | |

| Income tax expense (benefit) | 7,913 | | | 10,744 | | | 23,404 | | | (9,813) | | | 36,253 | | | 103,917 | |

| Net gain on sale of real estate | (30,397) | | | (12,623) | | | (58,920) | | | (15,675) | | | — | | | (178,711) | |

| Real estate impairment losses | 595,488 | | | — | | | 595,488 | | | 7,880 | | | 645,346 | | | 32,001 | |

| | | | | | | | | | | |

| Net gain on transfer to Fifth Avenue and Times Square JV on April 18, 2019, net of $11,945 attributable to noncontrolling interests | — | | | — | | | — | | | — | | | — | | | (2,559,154) | |

| EBITDAre at share | 325,867 | | | 268,176 | | | 1,138,740 | | | 989,586 | | | 1,200,949 | | | 1,677,474 | |

| EBITDAre attributable to noncontrolling interests in consolidated subsidiaries | 18,137 | | | 23,266 | | | 71,786 | | | 75,987 | | | (91,155) | | | 8,150 | |

| EBITDAre (non-GAAP) | $ | 344,004 | | | $ | 291,442 | | | $ | 1,210,526 | | | $ | 1,065,573 | | | $ | 1,109,794 | | | $ | 1,685,624 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

NON-GAAP RECONCILIATIONS RECONCILIATION OF EBITDAre TO EBITDAre, AS ADJUSTED (unaudited) |

| (Amounts in thousands) | | | | | | | | | |

| For the Three Months Ended December 31, | | For the Year Ended December 31, |

| 2022 | | 2021 | | 2022 | | 2021 | | 2020 | | 2019 |

| EBITDAre (non-GAAP) | $ | 344,004 | | | $ | 291,442 | | | $ | 1,210,526 | | | $ | 1,065,573 | | | $ | 1,109,794 | | | $ | 1,685,624 | |

| | | | | | | | | | | |

| EBITDAre attributable to noncontrolling interests in consolidated subsidiaries | (18,137) | | | (23,266) | | | (71,786) | | | (75,987) | | | 91,155 | | | (8,150) | |

| | | | | | | | | | | |

| Certain (income) expense items that impact EBITDAre: | | | | | | | | | | | |

| Gain on sale of 220 CPS condominium units and ancillary amenities | (34,844) | | | (14,959) | | | (41,874) | | | (50,318) | | | (381,320) | | | (604,393) | |

| Net gains on disposition of wholly owned and partially owned assets | (17,372) | | | — | | | (17,372) | | | (643) | | | — | | | — | |

| Our share of loss (income) from real estate fund investments | 463 | | | (1,564) | | | (1,671) | | | (3,757) | | | 63,114 | | | 48,808 | |

| Hotel Pennsylvania loss (income) | — | | | — | | | — | | | 11,625 | | | 31,139 | | | (8,264) | |

| Mark-to-market decrease in PREIT common shares (accounted for as a marketable security from March 12, 2019 and sold on January 23, 2020) | — | | | — | | | — | | | — | | | 4,938 | | | 21,649 | |

| Other | 7,157 | | | 3,981 | | | 12,741 | | | 2,483 | | | (8,527) | | | 343 | |

| Total of certain income items that impact EBITDAre | (44,596) | | | (12,542) | | | (48,176) | | | (40,610) | | | (290,656) | | | (541,857) | |

| | | | | | | | | | | |

| EBITDAre, as adjusted (non-GAAP) | $ | 281,271 | | | $ | 255,634 | | | $ | 1,090,564 | | | $ | 948,976 | | | $ | 910,293 | | | $ | 1,135,617 | |