| To Our Shareholders | Exhibit 99.1 |

This may be a new year but, at this writing, 2021 still feels a lot like 2020… the COVID pandemic remains a significant health risk; normal life continues to be disrupted; gatherings and travel are still restricted; and office building occupancy remains low.

We grieve for the 555,000 lives lost and are in awe of the healthcare providers.

COVID has had a negative effect on our 2020 numbers.

Net (Loss)/Income attributable to common shares for the year ended December 31, 2020 was ($348.7) million, ($1.83) per diluted share, compared to $3,097.8 million, $16.21 per diluted share, for the previous year. This decrease is primarily attributable to the non-recurring gain on the Retail Joint Venture transaction in 2019. See page 8.

Funds from Operations, as Adjusted (an apples-to-apples comparison of our continuing business, eliminating certain one-timers) for the year ended December 31, 2020 was $483.0 million, $2.53 per diluted share, compared to $666.2 million, $3.49 per diluted share, for the previous year, a decrease of $0.96 per share. This decrease is detailed on page 5.

Funds from Operations, as Reported (apples-to-oranges including one-timers) for the year ended December 31, 2020 was $750.5 million, $3.93 per diluted share, compared to $1,003.4 million, $5.25 per diluted share, for the previous year. See page 5 for a reconciliation of Funds from Operations, as Reported, to Funds from Operations, as Adjusted.

Here are our financial results (presented in Net Operating Income format) by business unit:

| | | Net Operating Income | |

| ($ IN MILLIONS) | | 2020

Same Store

% (Decrease)/

Increase | | | % of 2020 | | | 2020 | | | 2019 | | | 2018 | |

| New York: | | | | | | | | | | | | | | | | | | | | |

| Office(1) | | | (5.5 | )% | | | 69.8 | % | | | 672.5 | | | | 717.7 | | | | 719.9 | |

| Retail(1) | | | (32.6 | )% | | | 15.3 | % | | | 147.3 | | | | 244.2 | | | | 260.4 | |

| Retail Joint Venture(1) | | | N/A | | | | N/A | | | | — | | | | 35.8 | | | | 116.2 | |

| Residential | | | (11.6 | )% | | | 2.1 | % | | | 20.7 | | | | 23.4 | | | | 23.5 | |

| Alexander’s | | | (19.0 | )% | | | 3.7 | % | | | 35.9 | | | | 44.3 | | | | 45.1 | |

| Hotel Pennsylvania | | | N/A | | | | (4.4 | )% | | | (42.5 | ) | | | 7.4 | | | | 11.9 | |

| Total New York | | | (12.7 | )% | | | 86.5 | % | | | 833.9 | | | | 1,072.8 | | | | 1,177.0 | |

| | | | | | | | | | | | | | | | | | | | | |

| theMART | | | (32.5 | )% | | | 7.2 | % | | | 69.2 | | | | 102.1 | | | | 90.9 | |

| 555 California Street | | | 0.6 | % | | | 6.3 | % | | | 60.3 | | | | 59.7 | | | | 54.7 | |

| | | | | | | | 100.0 | % | | | 963.4 | | | | 1,234.6 | | | | 1,322.6 | |

| Other (see below for details) | | | | | | | | | | | 9.2 | | | | 25.2 | | | | 60.0 | |

| Total Net Operating Income | | | | | | | | | | | 972.6 | | | | 1,259.8 | | | | 1,382.6 | |

Other Net Operating Income is comprised of:

| ($ IN MILLIONS) | | 2020 | | | 2019 | | | 2018 | |

| Pennsylvania REIT | | | — | | | | 9.8 | | | | 20.0 | |

| 666 Fifth Avenue Office Condominium | | | — | | | | — | | | | 12.1 | |

| Urban Edge Properties | | | — | | | | 4.9 | | | | 11.8 | |

| Other | | | 9.2 | | | | 10.5 | | | | 16.1 | |

| Total | | | 9.2 | | | | 25.2 | | | | 60.0 | |

This letter and Annual Report contain forward-looking statements as such term is defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements are not guarantees of performance. The Company’s future results, financial condition and business may differ materially from those expressed in these forward-looking statements. These forward-looking statements are subject to numerous assumptions, risks and uncertainties. Currently, one of the most significant factors is the ongoing adverse effect of the COVID-19 pandemic on our business, financial condition, results of operations, cash flows, operating performance and the effect it has had and may continue to have on our tenants, the global, national, regional and local economies and financial markets and the real estate market in general. The extent of the impact of the COVID-19 pandemic will depend on future developments, including the duration of the pandemic, which are highly uncertain at this time but that impact could be material. Moreover, you are cautioned that the COVID-19 pandemic will heighten many of the risks identified in "Item 1A. Risk Factors" in Part I of our Annual Report on Form 10-K for the year ended December 31, 2020, a copy of which accompanies this letter or can be viewed at www.vno.com.

| 1 | On April 18, 2019 we completed the transfer of a 45.4% common equity interest in Vornado’s portfolio of flagship high street retail assets on Upper Fifth Avenue and Times Square to a group of institutional investors (“Retail Joint Venture”). For comparability, the historical financial results of the portion of the Retail Joint Venture assets that were transferred have been removed from the Office and Retail lines and reflected on the Retail Joint Venture line for all periods presented. |

The following chart reconciles Funds from Operations, as Reported, to Funds from Operations, as Adjusted:

| ($ IN MILLIONS, EXCEPT PER SHARE) | | 2020 | | | 2019 | |

| Funds from Operations, as Reported | | | 750.5 | | | | 1,003.4 | |

| Less adjustments for certain items that impact FFO: | | | | | | | | |

| After-tax gain on sale of 220 Central Park South units | | | 332.1 | | | | 502.6 | |

Lease Liability extinguishment gain and non-cash impairment loss and related

write-off on 608 Fifth Avenue | | | 70.3 | | | | (77.1 | ) |

| Severance accrual related to Hotel Pennsylvania closing | | | (6.1 | ) | | | -- | |

| Transaction related costs | | | (7.1 | ) | | | (4.6 | ) |

| Credit losses on loans receivable | | | (13.4 | ) | | | -- | |

| Severance and other reduction in force-related expenses | | | (23.4 | ) | | | -- | |

| Prepayment penalty on redemption of $400 million 5% senior unsecured notes | | | -- | | | | (22.5 | ) |

| Real Estate Fund(2) | | | (63.1 | )(2) | | | (48.8 | ) |

| Other, primarily noncontrolling interests’ share of above adjustments | | | (21.8 | ) | | | (12.4 | ) |

| Total adjustments | | | 267.5 | | | | 337.2 | |

| Funds from Operations, as Adjusted | | | 483.0 | | | | 666.2 | |

| Funds from Operations, as Adjusted per share | | | 2.53 | | | | 3.49 | |

Funds from Operations, as Adjusted decreased by $183.2 million in 2020 to $2.53 per share from $3.49 per share, a decrease of $0.96 per share. Here is the detail:

| | | Increase/(Decrease) | |

| ($ IN MILLIONS, EXCEPT PER SHARE) | | Amount | | | Per Share | |

| Variable Business (Hotel Penn 40.3, Tradeshows 18.7, Signage 11.7, BMS 7.5 and Garages 4.6) | | | (82.8 | ) | | | (0.43 | ) |

| Tenant Related (including straight line write-offs of 48.4 and bad debt write-offs of 27.8) | | | (88.2 | ) | | | (0.46 | ) |

| Interest expense | | | 36.2 | | | | 0.19 | |

| Interest income | | | (16.6 | ) | | | (0.09 | ) |

| Asset sales | | | (31.8 | ) | | | (0.17 | ) |

| General and Administrative expenses | | | 11.0 | | | | 0.06 | |

| THE PENN DISTRICT out of service | | | (23.0 | ) | | | (0.12 | ) |

| Other | | | 12.0 | | | | 0.06 | |

| Decrease in FFO, as Adjusted | | | (183.2 | ) | | | (0.96 | ) |

With reference to the table above, the financial impact of COVID on our business falls into three buckets:

| · | The decline of $82.8 million in our variable businesses whose performance varies with activity; |

| · | Bad debt write-offs of $27.8 million; and |

| · | Write-off of straight-line rent receivable of $48.4 million from converting weak tenants to cash basis accounting. |

Since the write-off of straight-line rent receivables is non-cash, the cash portion of the above is $110.6 million.

In recognition of all this and to protect our balance sheet, at our July board meeting, we reduced our dividend by an annual rate of $106 million.(3)

| 2 | Our $800 million Real Estate Fund was formed in 2010. Over the life of the Fund, all invested capital has been returned and the Fund has earned 5.8%, 1.2x. We account for the Fund on a fair value, mark-to-market basis and, as such, the Fund’s performance has caused volatility in our numbers. The Fund is in final stages of wind-down; it still retains several assets (a hotel and a few retail assets). The Fund’s 2020 number shown in the table above represents the final non-cash markdowns to zero of the remaining assets. This should be the end of it. |

| 3 | A word about our dividend policy… Our Company, in accordance with IRS REIT rules, pays out by dividend all of its taxable earnings. Our intention is to have a smooth and predictable dividend that increases with our growth. We believe the dividend is sort of sacred, but not more sacred than our balance sheet, our financial strength, and our liquidity. While we certainly have the wherewithal to overpay the dividend, our management and Board believe that, in this crisis period, our dividend should mirror our taxable earnings. Accordingly, in July 2020, the Board concluded to right-size the dividend to 53 cents per quarter. |

Over the last ten years, our taxable income aggregated $5.1 billion, our regular dividends were $4.4 billion and we paid special dividends of $600 million. In addition, we distributed, as dividends, shares of Urban Edge Properties and JBG SMITH in tax-free spin-offs, valued at $2.4 billion and $3.6 billion, respectively.

Report Card

Since I have run Vornado from 1980, total shareholder returns have been 13% per annum, but subpar lately. Dividends have represented 3.6 percentage points of Vornado’s annual return.

Here is a table that shows Vornado’s total return to shareholders compared to our New York-centric peers and two REIT indices for various periods ending December 31, 2020:

| | | Vornado | | | NY REIT Peers(4) | | | Office

REIT

Index | | | MSCI

Index | |

| One-year | | | (40.5 | )% | | | (29.2 | )% | | | (18.4 | )% | | | (7.6 | )% |

| Three-year | | | (43.7 | )% | | | (34.6 | )% | | | (8.4 | )% | | | 11.0 | % |

| Five-year | | | (42.3 | )% | | | (35.8 | )% | | | 9.2 | % | | | 26.7 | % |

| Ten-year | | | (9.6 | )% | | | -- | | | | 64.8 | % | | | 122.0 | % |

| Fifteen-year | | | 11.4 | % | | | -- | | | | 83.4 | % | | | 157.3 | % |

| Twenty-year | | | 228.5 | % | | | -- | | | | 242.6 | % | | | 506.7 | % |

The table above is skewed negatively by the effect of COVID on 2020 numbers. You may be interested in the table below which shows the same statistics, 2019 version, pre-COVID.

| | | Vornado | | | NY REIT Peers(4) | | | Office

REIT

Index | | | MSCI

Index | |

| One-year | | | 12.0 | % | | | 15.1 | % | | | 31.4 | % | | | 25.8 | % |

| Three-year | | | (11.9 | )% | | | (8.8 | )% | | | 18.3 | % | | | 26.2 | % |

| Five-year | | | (9.2 | )% | | | (11.1 | )% | | | 34.2 | % | | | 40.5 | % |

| Ten-year | | | 82.2 | % | | | -- | | | | 139.2 | % | | | 208.7 | % |

| Fifteen-year | | | 109.9 | % | | | -- | | | | 154.4 | % | | | 212.2 | % |

| Twenty-year | | | 569.9 | % | | | -- | | | | 468.9 | % | | | 732.4 | % |

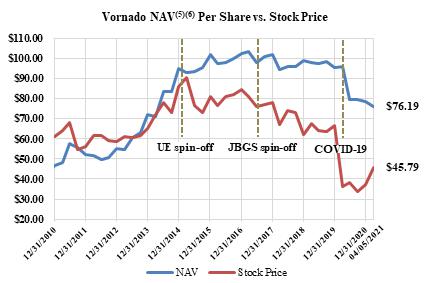

Our stock price for the last six years has been disappointing and, in my mind, chronically disconnected from the value of our assets. The graph below demonstrates that case. Over the last ten years, our NAV(5) (a surrogate for private market values) has compounded at 4.9%, but our stock price has compounded at a negative 2.8%. In my letter to shareholders three years ago, I made the point that public shareholders price CBD office buildings at a significant discount to private value. That pricing mismatch has been chronic and continues. It is difficult to guesstimate our NAV post-COVID but I suggest that, even in these volatile times, our NAV is still significantly higher than our stock price. Something is obviously wrong.

| 4 | Comprised of New York City-centric peers: SL Green, Empire State Realty Trust and Paramount Group. |

| 5 | Per Green Street Advisors. |

| 6 | NAV has been reduced by $10 for the Urban Edge spin-off and $23 for the JBG SMITH spin-off. |

Ten-Year Earnings Record

As is our custom, we present the table below that traces our ten-year record, both in absolute dollars and per share amounts:

| ($ AND SHARES | | | | | | | |

IN MILLIONS,

EXCEPT PER | | | NOI(7) | | | FFO, As Adjusted | | | Shares | |

| SHARE DATA) | | | Amount | | | % Change | | | Amount | | | % Change | | | Per Share | | | Outstanding | |

| 2020 | | | | 989.6 | | | | (17.4 | )% | | | 483.0 | | | | (27.5 | )% | | | 2.53 | | | | 203.8 | |

| 2019 | | | | 1,198.3 | | | | (0.6 | )% | | | 666.2 | | | | (6.6 | )% | | | 3.49 | | | | 203.1 | |

| 2018 | | | | 1,205.5 | | | | (0.6 | )% | | | 713.5 | | | | 0.1 | % | | | 3.73 | | | | 202.3 | |

| 2017 | | | | 1,212.7 | | | | 3.5 | % | | | 712.9 | | | | 4.7 | % | | | 3.73 | | | | 201.6 | |

| 2016 | | | | 1,171.5 | | | | 2.1 | % | | | 681.0 | | | | 4.7 | % | | | 3.58 | | | | 200.5 | |

| 2015 | | | | 1,147.9 | | | | 8.7 | % | | | 650.3 | | | | 21.5 | % | | | 3.43 | | | | 199.9 | |

| 2014 | | | | 1,056.5 | | | | 5.4 | % | | | 535.1 | | | | 8.0 | % | | | 2.84 | | | | 198.5 | |

| 2013 | | | | 1,002.0 | | | | 12.8 | % | | | 495.6 | | | | 29.5 | % | | | 2.64 | | | | 197.8 | |

| 2012 | | | | 888.3 | | | | 0.7 | % | | | 382.8 | | | | 2.9 | % | | | 2.05 | | | | 197.3 | |

| 2011 | | | | 882.3 | | | | 2.6 | % | | | 371.9 | | | | 6.0 | % | | | 1.94 | | | | 196.5 | |

As shown on the following page, in the last ten years we have been a net seller to the tune of $12.7 billion, notably including $2.7 billion in the Retail Joint Venture transaction and $9.7 billion of tax-free spin-offs. This activity has enriched shareholders but has punished our earnings. The table below compares our published FFO per share period-by-period to what our FFO per share would have been had we not sold or spun assets:

| | | | FFO, As Adjusted | |

| | | As Published | | | Pro Forma

To Include

Sold Properties | |

| 2020 | | | | 2.53 | | | | 5.14 | |

| 2019 | | | | 3.49 | | | | 6.79 | |

| 2018 | | | | 3.73 | | | | 6.92 | |

| 2017 | | | | 3.73 | | | | 6.86 | |

| 2016 | | | | 3.58 | | | | 6.50 | |

| 7 | All years include only the properties owned at the end of 2020. |

Acquisitions/Dispositions

Here is a ten-year schedule of acquisitions and dispositions.(8)

| ($ IN MILLIONS) | | | Number of

Transactions | | | Net Acquisitions/

(Dispositions) | | | Acquisitions | | | Dispositions | | | Gain | |

| 2020 | | | | 3 | | | | 3.7 | | | | 3.7 | | | | -- | | | | -- | |

| 2019 | | | | 7 | | | | (2,818.6 | ) | | | 67.1 | | | | 2,885.7 | | | | 1,384.1 | |

| 2018 | | | | 9 | | | | 336.0 | | | | 573.5 | | | | 237.5 | | | | 170.4 | |

| 2017 | | | | 9 | | | | (5,901.9 | ) | | | 145.7 | | | | 6,047.6 | | | | 5.1 | |

| 2016 | | | | 11 | | | | (875.1 | ) | | | 147.4 | | | | 1,022.5 | | | | 664.4 | |

| 2015 | | | | 25 | | | | (3,717.1 | ) | | | 955.8 | | | | 4,672.9 | | | | 316.7 | |

| 2014 | | | | 17 | | | | (412.3 | ) | | | 648.1 | | | | 1,060.4 | | | | 523.4 | |

| 2013 | | | | 26 | | | | (616.5 | ) | | | 813.3 | | | | 1,429.8 | | | | 434.1 | |

| 2012 | | | | 33 | | | | 142.9 | | | | 1,365.2 | | | | 1,222.3 | | | | 454.0 | |

| 2011 | | | | 19 | | | | 1,109.9 | | | | 1,499.1 | | | | 389.2 | | | | 137.8 | |

| | | | | 159 | | | | (12,749.0 | ) | | | 6,218.9 | | | | 18,967.9 | | | | 4,090.0 | |

Over the ten-year period, our dispositions totaled $19.0 billion and we were a net seller of $12.7 billion.

2019 includes $2.665 billion for the Retail Joint Venture (resulting in a gain of $1.205 billion(9)) and $100 million for 330 Madison Avenue, both sold at a 4.5% cap rate, as well as 3040 M Street and 86th and Madison Avenue. 2017 includes $5.997 billion for the JBG SMITH spin-off and 2015 includes $3.700 billion for the Urban Edge Properties spin-off. No gain was recognized on the spin-offs.

The action here takes place on the 45th floor where our acquisitions/dispositions team resides. Thanks to Michael Franco and to SVPs Cliff Broser, Adam Green, Michael Schnitt, Jared Toothman and to VPs Brian Cantrell, Brian Feldman, Tatiana Melamed.

| 8 | Excludes marketable securities. |

| 9 | The gain reported in our published financial statements was $2.571 billion, the difference being the gain recognized on the step up in basis to fair value of the retained portion of the assets. |

Lease…Lease…Lease

The mission of our business is to create value for shareholders by growing our asset base through the addition of carefully selected properties and by adding value through intensive and efficient management. Our operating platform is where the rubber meets the road. In our business, leasing is the main event. In New York, theMART and 555 California Street, we leased 3.2 million square feet in 2020.

As is our practice, we present below leasing and occupancy statistics for our businesses.

| (square feet in thousands) | | | New York | | | theMART | | | 555

California St. | |

| | | | Office | | | Street

Retail | | | | | | | |

| 2020 | | | | | | | | | | | | | | | | | |

| Square feet leased | | | | 2,231 | | | | 238 | | | | 379 | | | | 371 | |

| Initial Rent | | | | 89.33 | | | | 136.29 | | | | 49.74 | | | | 108.92 | (10) |

| GAAP Mark-to-Market | | | | 11.0 | % | | | 1.3 | % | | | 1.5 | % | | | 54.7 | % |

| Cash Mark-to-Market | | | | 4.6 | % | | | (5.9 | )% | | | (1.9 | )% | | | 39.7 | % |

| Number of transactions | | | | 54 | | | | 35 | | | | 52 | | | | 6 | |

| | | | | | | | | | | | | | | | | | |

| 2019 | | | | | | | | | | | | | | | | | |

| Square feet leased | | | | 987 | | | | 238 | | | | 286 | | | | 172 | |

| Initial Rent | | | | 82.17 | | | | 175.35 | | | | 49.43 | | | | 88.70 | |

| GAAP Mark-to-Market | | | | 5.5 | % | | | 12.9 | % | | | 10.7 | % | | | 64.9 | % |

| Cash Mark-to-Market | | | | 4.6 | % | | | 9.8 | % | | | 4.6 | % | | | 38.1 | % |

| Number of transactions | | | | 102 | | | | 39 | | | | 62 | | | | 7 | |

| | | | | | | | | | | | | | | | | | |

| Occupancy rate: | | | | | | | | | | | | | | | | | |

| 2020 | | | | 93.4 | % | | | 78.8 | % | | | 89.5 | % | | | 98.4 | % |

| 2019 | | | | 96.9 | % | | | 94.5 | % | | | 94.6 | % | | | 99.8 | % |

| 2018 | | | | 97.2 | % | | | 97.3 | % | | | 94.7 | % | | | 99.4 | % |

| 2017 | | | | 97.1 | % | | | 96.9 | % | | | 98.6 | % | | | 94.2 | % |

| 2016 | | | | 96.3 | % | | | 97.1 | % | | | 98.9 | % | | | 92.4 | % |

| 2015 | | | | 96.3 | % | | | 96.2 | % | | | 98.6 | % | | | 93.3 | % |

| 2014 | | | | 96.9 | % | | | 96.5 | % | | | 94.7 | % | | | 97.6 | % |

| 2013 | | | | 96.6 | % | | | 97.4 | % | | | 96.4 | % | | | 94.5 | % |

| 2012 | | | | 95.8 | % | | | 96.8 | % | | | 95.2 | % | | | 93.1 | % |

| 2011 | | | | 96.2 | % | | | 95.6 | % | | | 90.3 | % | | | 93.1 | % |

Notwithstanding the headwinds of the pandemic, 2020 was a year of significant leasing accomplishments.

| · | In August, at the very height of the health crisis, we completed the largest lease of the year, 730,000 square feet with Facebook at our Farley development.(11) Our dealmakers here were Glen with Josh Glick and Eddie Riguardi; |

| · | We also completed the second largest lease of the year, with NYU Langone for 633,000 square feet at One Park Avenue; |

| · | Importantly, we attracted Apple for 337,000 square feet at PENN 11; and |

| · | We also did the largest deal of the year in San Francisco, the renewal of Bank of America for 247,000 square feet at 555 California Street. Our dealmakers here were Glen with Paul Heinen. |

The west side of New York has become tech-central. Facebook, Apple, Google and Amazon are located in our buildings (2.5 million square feet). Facebook, Apple, Google, Amazon, and Disney are located in other buildings in the neighborhood (all told, over 13 million square feet). Tenants are speaking…the west side is the place to be.

Thanks to our leasing captains: Glen Weiss and Haim Chera. Also thanks to the New York leasing machine: Ed Hogan, Josh Glick, Jared Solomon, Jared Silverman, Edward Riguardi, Ryan Levy, Jason Morrison, Anthony Cugini, and to Paul Heinen who runs leasing at theMART and 555 California Street. Our thanks to our in-house attorneys, Pam Caruso, Elana Butler and Sara O’Toole, supported by Randall Greenman, who completed hundreds of leases and almost a thousand documents in total this year.

| 10 | 2020 initial rent and GAAP and cash mark-to-markets exclude a 247,000 square feet lease, as the starting rent for this space will be determined in 2024 based on fair market value. |

| 11 | From my remarks in our second quarter conference call: “This important commitment by Facebook answered the questions ‘will even a great company such as Facebook commit in the middle of a global pandemic crisis?’ ‘will they commit to physical space in light of work-from-home?’ ‘will they continue to expand in New York?’ We now know the answer is YES. This commitment is a dramatic statement from one of the most important global tech companies that, even in the midst of a pandemic, commerce must continue. This deal reinforces New York City as a great and unique place to do business with a large and highly educated workforce. New York continues to be the place to be.” |

From Governor Andrew Cuomo’s August 3, 2020 press release: “Vornado's and Facebook's investment in New York and commitment to further putting down roots here – even in the midst of a global pandemic – is a signal to the world that our brightest days are still ahead and we are open for business. This public-private partnership fortifies New York as an international center of innovation.”

Capital Markets

At year-end, we had $3.9 billion of immediate liquidity consisting of $1.7 billion of cash and restricted cash and $2.2 billion available on our $2.75 billion revolving credit facilities. Today, we have the same $3.9 billion of immediate liquidity. We also have $7.9 billion of unencumbered assets.

Since January 1, 2020, we have executed eight capital markets transactions totaling $2.2 billion. Our capital markets team had another strong year. Thank you to EVP Mark Hudspeth, SVP Jan LaChapelle and VP Tatiana Melamed.

In February, we increased our unsecured term loan balance to $800 million (from $750 million) by exercising an accordion feature. Pursuant to an existing swap agreement, $750 million of the loan bears interest at a fixed rate of 3.87% through October 2023, and the balance of $50 million floats at a current rate of 1.11% (LIBOR plus 1.00%). The entire $800 million will float thereafter for the duration of the loan through February 2024.

In August, we amended the $700 million mortgage loan on 770 Broadway, a 1.2 million square foot Manhattan office building, to extend the term one year through March 2022.

In September, Alexander’s, Inc., in which we have a 32.4% ownership interest, amended and extended the $350 million mortgage loan on the retail condominium of 731 Lexington Avenue. Under the terms of the amendment, Alexander’s paid down the loan by $50 million to $300 million, extended the maturity date to August 2025 and guaranteed the interest payments and certain leasing costs. The principal of the loan is non-recourse to Alexander’s. The interest-only loan bears a current rate of 1.50% (LIBOR plus 1.40%), which has been swapped to a fixed rate of 1.72%.

In October, we completed a $500 million refinancing of PENN 11, a 1.2 million square foot Manhattan office building. The interest-only loan bears a current rate of 2.85% (LIBOR plus 2.75%) and matures in October 2025, as fully extended. The loan replaces the previous $450 million loan that bore interest at a fixed rate of 3.95% and was scheduled to mature in December 2020.

In October, Alexander’s, Inc. completed a $94 million financing of The Alexander, a 312-unit residential building that is part of Alexander’s residential and retail complex located in Rego Park, Queens, New York. The interest-only loan bears a fixed rate of 2.63% and matures in November 2027.

In November, we unencumbered our land under a portion of the Borgata Hotel and Casino complex by repaying the $52.5 million mortgage loan. The 10-year fixed-rate amortizing loan bore interest at 5.14% and was scheduled to mature in February 2021.

In November, we sold 12 million 5.25% Series N cumulative redeemable preferred shares at a price of $25.00 per share, pursuant to an effective registration statement. We received aggregate net proceeds of $291 million, after underwriters’ discount and issuance costs.

In February 2021, a joint venture in which we have a 55% interest completed a $525 million refinancing of One Park Avenue, a 943,000 square foot Manhattan office building. The interest-only loan bears a current rate of 1.21% (LIBOR plus 1.107%) and matures in March 2026, as fully extended. The loan replaces the previous $300 million loan that bore interest at LIBOR plus 1.75% and was scheduled to mature in March 2021. Our share of the net proceeds was approximately $105 million.

In March 2021, we completed a $350 million refinancing of 909 Third Avenue, a 1.4 million square foot Manhattan office building.(12) The interest-only loan bears a fixed rate of 3.23% and matures in April 2031. The loan replaces the previous $350 million loan that bore interest at a fixed rate of 3.91% and was scheduled to mature in May 2021.

In process are refinancings of 555 California Street’s existing $534 million loan and theMART’s existing $675 million loan. On deck are 1290 Avenue of the Americas and 770 Broadway which have existing loans of $950 million and $700 million, respectively.

| 12 | Loan proceeds here are about $400 per square foot for the office portion, excluding the 497,000 square foot post office space (where the lease expires in 2038, as extended). |

Below is the right-hand side of our balance sheet at December 31, 2020 and 2019.

| ($ in millions) | | 2020 | | | 2019 | |

| Secured debt | | | 5,608 | | | | 5,670 | |

| Unsecured debt | | | 1,825 | | | | 1,775 | |

| Share of non-consolidated debt | | | 2,873 | | | | 2,803 | |

| Noncontrolling interests’ share of consolidated debt | | | (483 | ) | | | (483 | ) |

| Total debt | | | 9,823 | | | | 9,765 | |

| Cash and restricted cash | | | (1,835 | ) | | | (1,347 | ) |

| Projected cash proceeds from 220 Central Park South in excess of debt | | | (275 | ) | | | (1,200 | ) |

| Net debt | | | 7,713 | | | | 7,218 | |

| | | | | | | | | |

| EBITDA as adjusted | | | 879 | | | | 1,144 | |

| | | | | | | | | |

| Net debt/EBITDA as adjusted | | | 8.8 | x | | | 6.3 | x |

The decline in our credit statistics is largely the result of COVID-related reductions in our income of $265 million.(13) This resulted in a downgrade by S&P to BBB-.(14) We will earn our rating back and then some as our income reverts and improves as our variable businesses recover and our PENN DISTRICT projects come online.

Fixed-rate debt accounted for 53% of debt with a weighted average interest rate of 3.7% and a weighted average term of 3.1 years; floating-rate debt accounted for 47% of debt with a weighted average interest rate of 1.8% and a weighted average term of 3.4 years.(15)

81% of our debt is recourse solely to individual assets. The fair value of the assets pledged is $14.1 billion, resulting in a loan-to-value of 56.6%. We have approximately $7.9 billion of unencumbered assets.

Vornado remains committed to maintaining our investment grade rating.

| 13 | Please see page 34 for detail. |

| 14 | Moody’s and Fitch have us on negative watch. All of our New York peers and most of the CBD office REITs are in the same boat. |

| 15 | I have maintained over the years a contrarian view that fixed-rate debt may be more risky than floating-rate debt, which has the added benefit of being freely prepayable. We have more floating-rate debt than most, which is intentional. |

This page intentionally left blank.

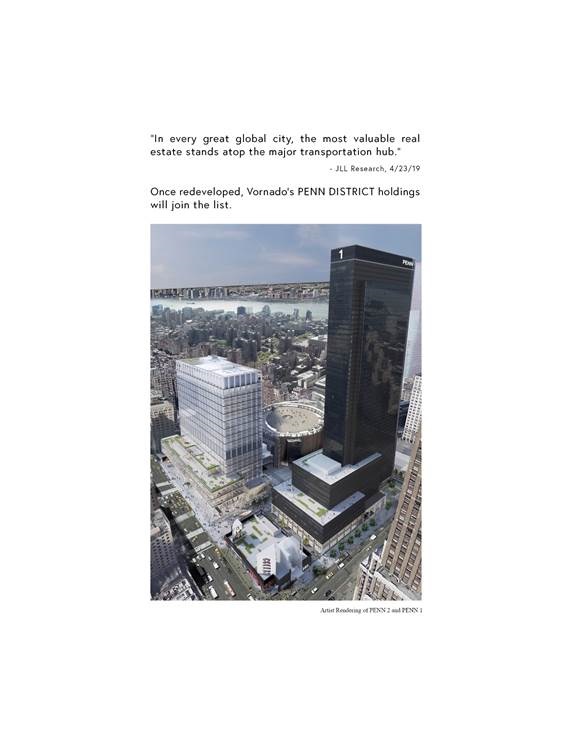

We are the largest owner in THE PENN DISTRICT with over 9 million square feet. THE PENN DISTRICT’s time has come, the district being validated by the neighboring Hudson Yards and Manhattan West. Our assets sit literally on top of Penn Station, the region’s major transportation hub, adjacent to Macy’s and Madison Square Garden. Day and night, THE PENN DISTRICT is teeming with activity. Here’s where we stand:

THE PENN DISTRICT is different from our other office assets…it is a large multi-building complex, it is long-term and it is development focused (development and long-term are two of the dirtiest words in REITland). THE PENN DISTRICT is our moonshot, the highest growth opportunity in our portfolio.

We intend to separate THE PENN DISTRICT through a tracking stock. It seems to me appropriate that we give investors the ability to choose between the higher growth but longer-term PENN DISTRICT or our other Class A, traditional core assets, or both.

Our development plans for Farley, PENN 1 and PENN 2 were outlined in my letter to shareholders last year. Images, budgets, returns and delivery dates are on our website. Each of these three large, exciting projects is now under construction and when completed will constitute the debut of our vision for THE PENN DISTRICT.

In THE PENN DISTRICT, we are creating a campus, a city within a city, which will become the very beating heart of the NEW New York. Over time, we hope to grow our interconnected campus by as much as 10 million square feet of new-builds. And over time, our PENN DISTRICT campus will almost certainly command premium pricing.

We have begun with 5 million square feet in three existing buildings – Farley, PENN 1 and PENN 2 – all interconnected either above or below ground. Here we are investing $2.4 billion(16) to create a unique environment for work, to bring to 22nd century standards, and to totally transform. In the middle of everything are PENN 1 and PENN 2, where we are creating a two-building, 4.4 million square foot campus directly on top of Penn Station. It will include a three-block plaza along 7th Avenue covered by a giant new bustle across the entire 430-foot frontage of PENN 2. This bustle will extend out 70 feet from the face of the building and will be 45 feet above the street. It will be striking, extraordinary and unique, creating a huge covered plaza in front of our PENN 2 and the main entrance to Penn Station. At PENN 2, we will also be removing the skin of the entire building and replacing it with a new, exciting, 22nd century curtainwall featuring floor-to-ceiling windows, see page 21. This architecture (designed by Dan Shannon, MdeAS Architects) will bring the neighborhood into the modern age. The bustle and penthouse conversion will create 140,000 square feet of valuable new, high ceilinged, best-in-class creative space. Images of these designs are posted on our website at www.vno.com.

Essential to our strategy here is interconnectivity and scale which will allow us to provide our tenants with an unparalleled amenity package,(17) even a giant leap forward from what we created at theMART a few years ago. But, there’s more – the scale of this campus will allow us to provide our tenants with flexibility for their growth and expansion. A 300,000 square foot tenant in a 500,000 square foot building is boxed in. But we could almost certainly provide this same 300,000 square foot tenant in this 4.4 million square foot campus multiple expansion availabilities and unrivaled flexibility. So, scale really matters.

Sitting here today, we are more confident than ever in our design and programming of the 4.4 million square foot campus at the combined PENN 1 and PENN 2. With unique and outstanding architectural design and amenities, sitting on top of New York’s main transportation hub, with Apple and Facebook anchor tenancies in other of our adjacent buildings, and with the Governor’s plan for significant additional investment in the Penn Station area, we couldn’t be more excited.

| 16 | $1.1 billion spent to date, with $1.3 billion left to go. Rate of spend will be about $700 million in 2021, $300 million in 2022, and $300 million in 2023. |

| 17 | Our 4.4 million square foot PENN 1 and PENN 2 campus is programmed to have over 200,000 square feet of amenity space, about 5%. Think about this – 5% of even a large million square footer would be only a noncompetitive 50,000 square foot amenity package, so scale really matters. |

THE PENN DISTRICT is taking shape as a series of building blocks one on top of the other on top of the other. We take note of the following important accomplishments:

| · | It has long been a goal of government to improve the capacity and user experience of Penn Station.(18) It has long been a precept of urban planning that density belongs at transit hubs. Recognizing these two important objectives which complement each other, Empire State Development Corporation is working to establish a General Project Plan (“GPP”), the purpose of which is to revitalize the area around Penn Station, provide significant public realm and subway improvements, and generate funds from new density to help overhaul and expand the station itself. The GPP process was announced in February by the Governor in a press release that can be accessed here. |

| · | In December 2020, the grand new Moynihan Train Hall(19) opened to the public to rave reviews, further cementing PENN as the transportation center of New York and our PENN DISTRICT as the bullseye. Vornado was honored to be a major principal in the Moynihan public/private partnership. |

| · | In August 2020, in the height of the pandemic, we completed our lease with Facebook for all 730,000 square feet of the office portion at Farley. This lease was the largest lease in New York last year. The first phase of Facebook’s space was delivered in January and the remainder will be delivered later this year. This space will house 3,000 Facebook employees. |

| 18 | In normal, non-COVID times, Penn Station struggles mightily to handle three times the traffic it was originally designed for. |

| 19 | A little explanation of terminology and geography may help. The historic Farley Post Office is the entire building; the Moynihan Train Hall sits in the eastern half of the Post Office Building; our Farley is the western half of the Post Office Building where Facebook and our retail are. |

| · | The new Long Island Railroad 33rd Street entrance, situated between PENN 1 and PENN 2, also opened in December. Its futuristic design is unique, exciting and that is intentional. |

| · | In December, we finalized our agreement with the MTA to redevelop the Long Island Railroad concourse. The retail stores on the north side of the concourse are ours and sit in our PENN 1 footprint. This project will double the width of the concourse, relieve overcrowding, raise the ceiling to a grand 18 feet and create a vastly improved concourse for the hundreds of thousands of commuters who use it each day. Construction is now underway, and our retail has been taken out of service. As part of the deal here, we will gain long-term control of an additional 22,000 square feet of retail on the south side, so we will now have all the retail along both sides of the heavily trafficked Long Island Railroad concourse. And we have all the retail in the adjacent Moynihan Train Hall and Farley. Taken together, this concentration of transit-oriented retail is a very significant asset. In normal times Penn Station is teeming with traffic and our retail does really well here. |

We have owned Hotel Penn, PENN 1 and PENN 2 for 22/23 years. Since everything about these buildings is about to change, this seems a perfect time to review the financial performance we have enjoyed so far from these buildings over our ownership period.

| ($ in millions) | | PENN 1 | | | PENN 2 | | | HOTEL PENN | |

| Initial Acquisition(20) | | | 450 | | | | 218 | | | | 152 | |

| Cash NOI | | | 1,539 | | | | 873 | | | | 458 | |

| Capex | | | 459 | | | | 204 | | | | 130 | |

| IRR, Unlevered(20) | | | 13.5 | % | | | 12.5 | % | | | 13.2 | % |

In 1997, when we acquired the Mendik portfolio which marked our entry into New York real estate, our first move was to go after the Hotel Pennsylvania which we bought in three separate transactions over three years. The hotel business is competitive and cyclical which made the hotel in some years a large profit producer and in others not so much. But to us, the hotel was always a taxpayer, carrying a great development site. The hotel math has deteriorated significantly over the last five years, a victim of oversupply, relentlessly rising costs and taxes and an aging physical plant. In April 2020, in response to the pandemic shutdown, we announced a temporary closing of the hotel and booked one-time losses of $42 million.

Today, I announce that we will permanently close and raze the hotel to create the premier development site in town. The process from today to the fully demolished and ready-to-go site will take less than two years. We are working with Foster + Partners to design a unique building, the 22nd century workplace of the future. Initial designs for this building, now addressed PENN 15, can be seen at our website www.vno.com.

This decision was inevitable… the Pennsylvania may have been a grande dame in its time, but it is decades past its glory and sell-by date.(21)

We have history here – a megadeal that went away. In 2007, we shook hands and drew docs for a deal to build the world headquarters of Merrill Lynch on the Hotel Penn site. The papers were done, César Pelli designed a towering HQ building and we had a ULURP approval (now expired) for this 2.8 million square foot financial services headquarters building. This deal was swept away by the Great Recession.

| 20 | Current value of these buildings is multiples of our initial acquisition cost, which is baked into the IRR. |

| 21 | We will retain PEnnsylvania 6-5000 (famously performed by Glenn Miller), the oldest continuously in-service telephone number in New York. |

PENN 2 is a unique asset. It has a 60,000 square foot footprint, it sits on a 120,000 square foot two-block wide site, it is directly on top of Penn Station. The site could support a building three times larger and so, a few years ago, we considered an audacious plan… to raze PENN 2, a building worth well more than a billion dollars, to bring back a much larger five, six or seven million square foot building, utilizing trapped air rights that we own with Madison Square Garden. This scheme was too large, even for us, and would have taken the better part of seven years, so it was a no-go.(22) Recognizing the scale of our site and that we sit directly on top of the station, we have also considered other schemes. Nonetheless, we are now fully committed and full speed ahead with our bustle transformation plan for PENN 2… and it’s a beauty. Steel and curtainwall are on order, sidewalk sheds are up, and we’re off to the races.

To showcase our vision for the District, we have just opened our new PENN DISTRICT Experience Center (a fancy word for sales center) located on the 7th floor at PENN 1, appropriately in the heart of the action. This marketing center (12,000 square feet of showroom, conference, meeting, models, and video walls and 14,000 square feet of gardens and terraces overlooking the entire district) is the best I’ve ever seen. It really tells our story and brings our plans to life, and even more, it’s a proper environment for dealmaking. It will be the venue for our leasing and development teams to present and showcase our projects to the brokerage community and prospective tenants. Early feedback from brokers and tenants has been fantastic. When gatherings are again permitted, we look forward to hosting all of you. In the meantime, please visit our website for the latest images of our plans for THE PENN DISTRICT. Creating this sales center was a labor of love around here. Everything had to be perfect. Thanks to Barry Langer, Glen Weiss, Lisa Vogel and their teams. Architecture and design was by Brad Zizmor of A+I.

| 22 | While we are reminiscing, all this is Penn Station 2.0. Back ten years ago was Penn Station 1.0 where we, Related and Madison Square Garden pursued another bold plan, to relocate MSG to the western half of the Farley Post Office. The three private sector partners committed in writing and the ball was in the public sector’s court. After years of trying, we pulled the plug as it became clear that this dream wasn’t going to happen. Looking back, everyone, the press, the civics, elected officials all had remorse over this unique, missed opportunity. |

In our business, the deals are the drama… buying, selling, leasing. But in the end, we are a customer-centric business… in a manner of speaking, we are in the hospitality business. I reprint here two important paragraphs from last year’s letter.

Talent is our New Client We are in a service business. We put our best foot forward when we take a page out of the hospitality industry. Our tenants appreciate and deserve to be treated like guests. Coffee and welcoming greetings go a long way. In keeping with that spirit, our PENN DISTRICT marketing campaign features the slogan, “Talent is our New Client,” the point being that everything we do, in every phase of our business, must be geared to pleasing, even delighting, our clients, defined as the talented employees of our tenants. After all, we recognize that real estate is a recruiting tool for our tenants.

Further, we are pushing the envelope of design. There is a place for Park Avenue-style financial services buildings and a place for West Side creative-type buildings. In THE PENN DISTRICT, we are creating a 22nd century work environment featuring lobbies with areas to sit, congregate, surf or just hang and chill, a warm palette, welcome libraries, conference centers, gyms, an auditorium, food service, outdoor space and gardens and more. In a word, we will create a hospitality-rich communal workplace for our PENN DISTRICT tenants. The images below are a tiny sampling – additional images are posted at www.vno.com.

At Vornado, we have made great progress using technology to enhance our tenants’ experience and make their lives more efficient. Our small dedicated staff of technologists is continuously working to improve our customers’ experience. For further information, please see www.vno.com/technology-innovation.

Our PENN DISTRICT development team is led by Barry Langer with David Bellman, Judy Kessler, Sandy Reis, Brian Thompson, and Alan Reagan.

Disclaimer: There can be no assurance that these projects will be completed, completed on schedule or within budget. There can be no assurance that the Company will be successful in leasing the properties on the expected schedule or at the budgeted rental rates.

Retail

The retail industry is going through a vicious period of challenging, disruptive, secular change.

Nonetheless, we are making deals – Fendi, Berluti, Sephora, Whole Foods…

Individually, and collectively, we own great assets… a portfolio of 65 properties, 2.7 million square feet of flagship street retail concentrated on the best high streets – Fifth Avenue, Times Square, THE PENN DISTRICT, Madison Avenue, and SoHo. Please see www.vno.com for portfolio details and images. Here is the math for our retail business:

($ IN MILLIONS,

EXCEPT | | | Number of | | | NOI | |

| PROPERTIES) | | Properties | | | GAAP Basis | | | Cash Basis | |

| 2022 guesstimated | | | | | | | | | | | 160.0 | |

| 2021 guesstimated | | | | | | | | | | | 135.0 | |

| 2020 | | | 65 | | | | 147.3 | | | | 158.7 | |

| 2019 | | | 64 | | | | 273.2 | | | | 267.7 | |

| 2018 | | | 65 | | | | 353.4 | | | | 324.2 | |

| 2017 | | | 65 | | | | 359.9 | | | | 324.3 | |

| 2016 | | | 64 | | | | 363.7 | | | | 292.0 | |

| 2015 | | | 60 | | | | 341.7 | | | | 259.2 | |

Here is a reconciliation of retail cash basis NOI from 2018 (the top-tick year for the retail segment) to our guesstimated 2021 number. We also include a guesstimate of what 2022 cash NOI might be.

| ($ IN MILLIONS) | | 2018 to 2022 Bridge

(At Share) | |

| 2018 Cash NOI | | | 324.2 | |

| Retail Joint Venture transaction | | | (82.8 | ) |

| Sold properties | | | (18.9 | ) |

| THE PENN DISTRICT out of service | | | (23.0 | ) |

| | | | 199.5 | |

| Tenant issues: | | | | |

| Manhattan Mall: JCPenney | | | (19.5 | ) |

| 1540 Broadway: Forever 21 | | | (10.6 | ) |

| 478-486 Broadway: Topshop | | | (8.1 | ) |

| Other, net (Zara, John Varvatos, Berluti, Planet Hollywood, Gucci, Forever 21, Elie Tahari, Necessary Clothing) | | | (26.3 | ) |

| 2021 Cash NOI, guesstimated | | | 135.0 | |

| Rent steps | | | 5.3 | |

| Signed leases | | | 8.8 | |

| Farley/other leasing, net | | | 10.9 | |

| 2022 Cash NOI, guesstimated | | | 160.0 | |

Here are our 2020 results by submarket:

| | | NOI | |

| | | GAAP Basis | | | Cash Basis | |

| ($ IN MILLIONS, EXCEPT %) | | Amount | | | % | | | Amount | | | % | |

| Fifth Avenue | | | 74.5 | | | | 50.6 | | | | 64.7 | | | | 40.8 | |

| Times Square | | | 25.2 | | | | 17.1 | | | | 25.7 | | | | 16.2 | |

| THE PENN DISTRICT | | | 9.9 | | | | 6.7 | | | | 26.7 | | | | 16.8 | |

| Madison Avenue | | | (1.4 | ) | | | (1.0 | ) | | | 5.2 | | | | 3.3 | |

| SoHo | | | 13.6 | | | | 9.2 | | | | 10.4 | | | | 6.6 | |

| Other | | | 25.5 | | | | 17.4 | | | | 26.0 | | | | 16.3 | |

| Total | | | 147.3 | | | | 100.0 | | | | 158.7 | | | | 100.0 | |

In 2020, in conjunction with the JV’s appraisals, we wrote down our investment in the Retail Joint Venture by $409 million to $2.8 billion; there may be more to come. In accordance with our annual asset review, we impaired other retail assets by $236 million.

The $1.828 billion preferred that we hold on five of the seven Retail Joint Venture assets which was originally sized at 50% of value is now at, say, 61% of value per appraisal. As a reminder, this preferred is cumulative, non-call, the senior “liability” position on those five assets, bears a coupon of 4.25% until 2024 when it rises to 4.75% for the next five years and is formulaic thereafter. We still get questions regarding the terms of the Retail Joint Venture deal. Please see www.vno.com for a description of that deal from my 2018 letter to shareholders.

220 Central Park South

To use the analogy of a parent celebrating a child’s growth and development (pun), 220 Central Park South has completed its development phase and is entering adulthood; about a third of the apartments are now occupied by delighted resident-owners enjoying the restaurant, amenities and the environment we have created.

Sales to date have totaled $2.869 billion. We are 91% sold with, I guesstimate, $250-$300 million still to come from future sales.

In 2020, 220 Central Park South accounted for all ten of the top ten (by sales price) condo sales in New York and 16 of the top 20. That’s never been done before and likely will never be done again.

Considering our great success, proven abilities and unique franchise in this space, I now take a page out of my friend Michael Bilerman’s playbook. Let’s take an instant poll – should we take on another similar condo project?

Kudos to our development team led by Barry Langer with Eli Zamek, Mel Blum, supported by Alejandro Knopoff, Andrew Hunt, and Sedge Hahm. Sales were all Deborah Kern.

Public service messaging during the pandemic at our flagship assets, clockwise from left: 731 Lexington Avenue, the home of Bloomberg’s World Headquarters in New York City; theMART, the world’s largest commercial building and design center located in Chicago; and 1535 Broadway in Times Square, one of the largest LED screens in the world, in New York City.

G&A

As 2020 came to a close, we executed a G&A reduction program designed to save $35 million annually.(23) Compensation represents 80% of our G&A expense and, accordingly, we targeted $30 million of the reduction from compensation, including a Reduction In Force.

$10 million of the reduction in compensation came from me as well as David Greenbaum and Joe Macnow, both of whom are retiring. It was appropriate that we eliminate the redundancies and overlapping skillsets in our senior team. David, Joe and I agreed it was time. David and Joe may be irreplaceable but, be assured, their successors – Michael, Glen, Barry, Tom and Matt – are very talented, seasoned, proven and up to the task.

The program involved a one-time expense for severance, etc., of $23 million. We undertook this program partially as a COVID-induced belt tightening and, even more, as simply good business practice.

Our team captains in this unpleasant activity were Michael Franco and Joe Macnow… and all of our senior department heads chipped in. Kudos to them for an extremely professional and efficient process that was well-explained to staff. This was something that had to be done and our hardworking staff accepted that. The 70 people who left us were treated generously and with compassion.

A comparison of our G&A levels to our peers is complicated. The numbers and classifications are all over the place. But here’s a summary, as best as we can make it: Giving account, pro forma, for the $35 million reduction, our G&A would be 5.55% as measured against revenue and 62 basis points as measured against enterprise value. These metrics are in the ballpark of our peer group.

| 23 | Technically, $28.6 million will reduce “general and administrative” expense on our income statement, $3.2 million will reduce “operating” expense on our income statement and the final $3.2 million will reduce capitalized expenses. |

Some Thoughts, 2020 Version

| · | I begin with a shoutout and a thank you to our amazing and talented Vornado people in New York, Paramus, Chicago and San Francisco. To our leasing teams who did the Facebook and NYU deals, and more; to our development teams responsible for 220 CPS, Farley, PENN 1, PENN 2 and more; to our Paramus team who collect the rents, pay the bills, prepare our financial statements, and are masters of control, control, control; and to our operations teams who keep the trains running on time, follow all protocols and have our buildings sanitized and ready to welcome our tenants home… you are all A+, at the head of the class, and we say thank you. And a double thank you this year since most of your work was done from home without skipping a beat (enabled by Robert Entin and his IT team). |

| · | If there is a lesson from this horrible COVID year, it is that we must always be prepared for the out-of-the-blue, unexpected black swan event…and we were and we are. |

| · | Our portfolio is populated with the highest quality assets in all of REITland: 555 California Street; theMART; our Fifth Avenue and Times Square retail assets; 1290 Avenue of the Americas; 770 Broadway, etc., etc. to name a few; AND, the most exciting development opportunity in all of REITland, THE PENN DISTRICT; AND the two best development sites in town, 350 Park Avenue and the Hotel Pennsylvania. |

| · | The pandemic has forced everyone out of the office, out of their normal workplace to shelter in-place, i.e. into isolation in their homes. Technology (Zoom) allowed companies to carry on as best as they could with a remote workforce. Work-from-home or work-from-anywhere sounds to me a lot like the age-old freelancing, i.e. working alone. Will work-from-home disrupt the office and the structure of work, much like Amazon disrupted retail? I think not. Remember after the tragedy of 9/11, companies fled New York, split into multiple locations and shunned view space at the top of tall buildings. This all reversed quickly. In the early stages of the pandemic, many of our corporate leaders were quick to pronounce that their workforces could work from anywhere forever, or something like that. And almost to a one, those dictums have now been reversed. Time will tell, but I have to assume work-from-home in some hybrid form, in some modest percentage of the office population is here to stay. But the success of our businesses will continue to depend upon talented workers gathering together. I guess the kitchen table has a place for some but I continue to believe the urban office is the future of work. |

| · | The competition between high-tax, densely populated urban centers and smaller, low-tax/no-tax cities is the topic du jour. We continue to believe that New York, our hometown, will be a big winner. New York wins in infrastructure. It is the economic and cultural capital of the United States (there is a reason the Statue of Liberty is in New York Harbor), it is the finance center of the world, it attracts the best and the brightest and has a large and growing highly educated and diverse workforce, eight professional sports teams, Lincoln Center and Carnegie Hall, Broadway, great museums, great restaurants and nightlife, the best hospitals and universities, and, of course, the largest concentration of Fortune 500 headquarters and is now a large and growing tech center… you get the message. And think about this, just the space that tech companies have recently leased in New York or currently have under construction will require 20,000 new talented employees. There is maybe only one other city in the country with the scale to satisfy that requirement. |

| · | We listen to our tenants and, so, I am convinced that the way they want to work is rapidly changing from the rigid, closed office door Uptown model to the less formal, creative West Side model. Of New York’s 400 million square feet, I’m guessing only about half of that space really qualifies for the workplace of the future. |

| · | I agree with the conventional wisdom that the COVID lockdown will shortly turn into a BOOM. The stock market says so, the tsunami of trillions of stimulus will make it so, so too will pent-up consumer demand. New York will be a primary beneficiary of the stimulus and of the boom. |

| · | Gaming is now all around us. There are as many as 30 gaming venues within an easy drive of Manhattan. Internet gaming is the next big thing, predicted to have a much larger audience than even brick-and-mortar casinos (I understand one can even bet on the coin toss or each down or each free throw). New York State has authorized seven casino licenses, four of which have already been issued Upstate (I understand they are not doing well) with a seven-year head start on three Downstate licenses. The enabling legislation has a prohibition against gaming in Manhattan. There is a rising level of chatter (to use a term out of the government’s intelligence guidebook) that the issuance of the Downstate licenses will be accelerated and that Manhattan will be in play. There are two Downstate racetrack licenses (slot machines only) at Yonkers Raceway and Aqueduct Raceway that are performing well. My guess is that these two will win two of the three full Downstate casino licenses and then where will the third go? To my mind, it makes little sense for the third license to go to another venue in either Long Island or Westchester which would split revenue with the existing Yonkers or Aqueduct. It makes perfect sense for the third and final license to go to Manhattan. Being the center of everything, Manhattan will generate by far the highest revenue for our education system; after all, aren’t we in it to maximize the tax revenue? And Manhattan has, by far, the largest number of hotel rooms, restaurants, museums, tourist attractions, and the region’s transportation network was designed with Manhattan as its hub. We have heard the chatter and have been approached. |

| · | Our property business produces a stream of income which comes from almost a hundred buildings and 1,200 tenants with generally longish-term leases and high credit profiles. Our income taken as a whole is very stable. At our current stock price, our 2019 income is at an 8.2% cap rate, our COVID-depressed 2020 income is at a 6.7% cap rate. Think about this: the senior third of our income stream is rock-solid and would undoubtedly be rated AAA or even AAAA and might be valued at, say, a 2.5% cap rate. This pushes the junior two-thirds into double digits, and that sounds crazy to me. We are studying how to isolate that senior third of super highly rated income either through credit instruments or a fee/ground lease split. With our large existing portfolio, we could create quite a new business here. |

| · | Homelessness is a nationwide tragedy growing to epic proportions. Something must be done to help the victims and, at the same time, make our streets livable. Isn’t this what government is supposed to do? |

| · | During the COVID lockdown, I must say the best investment I ever made is my Netflix subscription. I now understand why the soundstage business is booming. While we certainly aren’t going Hollywood, we have been approached and are intrigued. |

| · | In June, we announced that we were going to market to explore alternatives for two large, highest-quality assets, 555 California Street, which has to be a top 5 in the nation trophy, and 1290 Avenue of the Americas, one of the premier buildings on Manhattan’s Corporate Row. We understood that this was a contrarian move in the face of the pandemic, but we felt that the world was awash with liquidity and there were no great assets then in the marketplace. We found investors to be uncertain, distracted, and handicapped by inability to travel. We were unable to achieve our price objective and we withdrew. We are now in the process of refinancing 555 California Street. As markets improve, we may well revisit other alternatives for these two buildings. |

| · | In investing, buy-low sell-high is the golden rule. Our stock is once again stupid cheap, although the first small leg off the bottom may be behind us. My friend Steve Sakwa, the highly regarded REIT analyst, recently published a report that our current stock price values our office buildings in the $500s per square foot. With replacement cost in the $1,200-$1,400 per square foot range, that discount is a bell ringer. There’s more, COVID-inspired work-from-anywhere has driven apartment occupancies down to the 70%’s and apartment rents down by 25%... that’s never happened before… another bell ringer. So, Manhattan is now on sale and that’s a buy signal and one of the reasons I believe New York will grow from strength to strength. |

| · | I will resist questioning the wisdom of raising taxes in the face of a New York economy that is in the early innings of reopening and recovering, especially when Washington has balanced the city and state budgets. But I will, for the third year in a row, question the wisdom of the New York State estate tax. I repeat here what I have said before: |

There is one vulnerability I would like to point out. In New York State, the top 2% pay a full 50% of personal income taxes so it is critical that they remain tax-paying residents. The vulnerability comes with the 1%-ers, who are at the end of their careers. Most of the folks I know are willing to pay higher income taxes for the privilege of living in New York, but hate the prospect of a 16% toll for the privilege of dying in New York. New York State’s estate tax brings in only about 1/150th of the state’s annual budget. The estate tax should be repealed. Keeping our highest taxpayers through the end of their lives is both good economic policy and good politics. By the way, high-tax California has no estate tax, New Jersey repealed its estate tax last year.

| · | The Principles by Which We Run Our Business are reprinted as Appendix A. |

Environmental, Social and Governance (“ESG”)

Dan Egan is our industry acclaimed Senior Vice President, Sustainability. What follows is Dan’s summary of 2020 accomplishments and goals. Thank you, Dan.

The various crises we endured in 2020 – economic, public health, social justice, and climate, to name a few – underscore the importance and urgency of ESG. ESG remains a priority for all of us at Vornado and is further supported with oversight from our Board.

Climate change risks are imminent, as climate-driven events wreak havoc across the globe, damaging infrastructure and adversely impacting vulnerable communities. As corporate citizens, we must do our part to reduce our impact on the environment and manage the associated risks. Last year, we published our commitment to making our buildings carbon neutral by the year 2030. Our six-point plan, known as Vision 2030, is discussed fully in our ESG Report, found at www.vno.com. We have committed to aligning this plan with the Science-Based Target Initiative.

We have been focused on energy efficiency for over ten years. In fact, we reduced our energy consumption 24% between 2009 and 2019. We prioritize energy efficiency as the primary means to reduce our carbon emissions; we can and should do more, with less. To that end, below is an inventory of carbon emissions from our buildings in 2020, according to the Financial Control Method(24), measured in metric tons:

| | | Total | | | Scope(24) | |

| | | MTCO2e | | | 1 | | | 2 | | | 3 | |

| New York | | | 163,424 | | | | 23,559 | | | | 105,456 | | | | 34,409 | |

| theMART | | | 20,996 | | | | 4,367 | | | | 16,612 | | | | 17 | |

| 555 California Street | | | 8,405 | | | | 37 | | | | 8,368 | | | | — | |

| Other | | | 13,359 | | | | 1,227 | | | | 3,561 | | | | 8,571 | |

| Total | | | 206,184 | | | | 29,190 | | | | 133,997 | | | | 42,997 | |

We realized a 20% reduction in our emissions from 2019 to 2020, mostly due to COVID-related dormancy in our office and retail spaces. We expect emissions to increase from these values, at least partially, with the return of our tenants in 2021.

Carbon emissions have a complex relationship with real estate. As property owners, we can control the emissions generated by our energy consumption, but we also must be aware of the resources expended to generate this energy. A “green” electrical grid is fully supported by renewable energy and other zero-carbon resources, like hydropower and nuclear. If the grid is green, a building whose sole energy source is electricity could become carbon neutral. Both New York State and California have mandates to achieve green grids (New York by 2040; California by 2045). Such regulation compels us to consider electrifying our buildings as a plausible path to carbon neutrality. We are actively doing so in THE PENN DISTRICT and elsewhere. We have a seat at the table with climate policymakers at City, State, and Federal levels to advise not only on what role buildings must play in climate change mitigation, but also how it can be done.

We responded to COVID with determination to ensure that our tenants, employees, and visitors remain healthy and safe. We fortified our buildings with protections that include thermal scanning, social distancing and PPE requirements, HVAC and Indoor Air Quality, and more recently, onsite COVID testing locations. This infrastructure is further reinforced with our green cleaning program and our best-in-class operations team.

We have also provided our employees with the resources, support, and flexibility needed through the pandemic. We enhance our human capital by sponsoring continuing education and career development. We have actively engaged with our workforce and solicit their feedback through our divisional leaders and employee surveys.

Our Board, and particularly our Corporate Governance and Nominating Committee, is assigned with oversight of ESG, which includes climate change risk. A discussion on our corporate governance is included in our proxy statement, which can be viewed at www.vno.com/proxy and the governance section of our website at www.vno.com/governance.

We proudly celebrate our continued achievements and recognition as a leader in ESG. In 2020, we were recognized by NAREIT as a Leader in the Light (11 years running), we achieved ENERGY STAR Partner of the Year with Sustained Excellence (6th time with this distinction) and we earned accolades from the Global Real Estate Sustainability Benchmark (8th year with “Green Star” Ranking, top quintile of performers, and an “A” grade for our public disclosure). We own and operate more than 27 million square feet of LEED certified buildings, representing 95% of our office portfolio, with over 23 million square feet at LEED Gold or better.

Our ESG narrative is told with transparency and supported by data. We have expanded our climate scenario analysis as recommended by the Taskforce on Climate-related Financial Disclosures and have updated our disclosures according to the Sustainability Accounting Standards Board and the Global Reporting Initiative. All can be found at www.vno.com.

| 24 | We have chosen to report our emissions according to the Financial Control Method, as discussed in the World Resource Institute’s Greenhouse Gas Protocol: A Corporate Accounting and Reporting Standard: Revised Edition. Our Scope 1 emissions include onsite combustion from oil and natural gas; Scope 2 emissions include our district steam consumption and electricity consumption, including electricity consumed by our submetered tenants; Scope 3 emissions include other utility consumption within the direct control of our tenants. |

Cover of 2020 ESG Report which can be found on our website at www.vno.com.

David and Joe

David Greenbaum and Joe Macnow stepped back at year end from day-to-day roles and became senior advisors. Vornado is indebted to them and thanks them for their immense contributions. These two are giants and deserve much credit for building the great company that Vornado has become.

Joe started with me at the very beginning, 40 years ago. David joined 24 years ago when we acquired the Mendik Company (which, by the way, was Mike Fascitelli’s first deal with us). David was with the Mendik Company for 15 years prior, so, rounding you might say that David is also a member of the 40-year club. I note (with tongue in cheek) that it will take five of our really talented leaders to replace these two giants – Glen Weiss and Barry Langer in the case of David, and Michael Franco, Tom Sanelli and Matt Iocco in the case of Joe. So be it. But, believe me the “new” five are up to the task.

David Moves to Arizona…Glen Weiss and Barry Langer Step Up

David Greenbaum and I first met when Vornado acquired the Mendik Company in 1997. For the last 24 years, he has been my partner and the leader of our New York business. A lot has happened since then and he has had a hand in every day and every deal. David is the consummate real estate professional…at the head of the class. What’s more, David is the smartest, most competent and most upstanding man I know. David has chosen to kick himself upstairs, continuing his leadership as Vice Chairman, working from both New York and Arizona.

Joe Retires as CFO… Michael Franco Steps Up

Joe Macnow is the dean of REIT CFOs. He and I have worked together for 40 years. You all know him. He’s as smart as they come. He has participated in all of the good stuff we have done over the years. He is, of course, an accounting wiz, an A player in management and pretty darn good at strategy, if a little stubborn.

A little history here. When Mike Fascitelli stepped down in 2013, I brought Joe into New York to work even more closely with me and we recruited Steve Theriot from Deloitte, our auditor, to be Vornado’s CFO. Fast forward to 2017, when we spin-merged our Washington business into JBG SMITH (our shareholders had 73% of NewCo, so I look at it as OurCo), we contributed 12 million square feet of buildings, multiple land sites, including the Crystal City land that is now Amazon HQ2 (Matt Kelly and his JBGS team did a great job… but I can’t resist taking a little credit) and we transferred Steve Theriot, who had intimate knowledge of our assets, to JBG SMITH as their CFO. At that point, we did an external search for a successor Vornado CFO. After a thorough search headed by a first-rank search firm, we concluded that Joe, even a little long in tooth, was by far the best around and he reassumed the Vornado CFO job. Fast forward again to a few months ago when, in connection with our G&A review, we mutually decided, it was time. We threw most of Joe’s compensation into the G&A savings pool and he remains an involved senior advisor.

Now, we focused on multiple internal candidates to be Joe’s successor as Vornado’s CFO. Me, our Board, our senior leadership team and that same first-rank search firm went back to work. But I changed the ground rules. Vornado’s CFO has traditionally been sort of a Chief Accounting Officer. In Joe’s case, his talent allowed him to be that plus a jack-of-all-trades but I really wanted something more and different. It’s a little known fact that only 36% of Fortune 500 CFOs come out of accounting. The modern CFO runs the accounting and control department, usually through a deputy, but also runs the balance sheet, financings and, frequently, strategy…and dealmaking, too. He is often the CEO’s right hand and, many times, a CEO in waiting. With these criteria, Michael Franco emerged as the clear winner. He is doing the finance, strategy, dealmaking and right-hand man functions now. This was an easy choice and I am delighted that Michael has agreed to add the CFO title to his President title.

In connection with all of this, Tom Sanelli has stepped up. Tom is special, and in our group of math experts, he may be the best of the lot. Tom has been promoted to Executive Vice President - Finance & Chief Administrative Officer. He has been with Vornado since 2003. Tom trained as an accountant but received his PhD working for David on all manner of deals, analytics, and management. He has been our go-to guy and, for years, has worked hand-in-hand with Michael, Glen, and Barry. Among other functions, Tom will be Michael’s deputy overseeing Paramus. Most of you know Tom, he has been participating in investor meetings for years. And he will be our lead Investor Relations executive succeeding Cathy Creswell, who is retiring.

We continually broaden our leadership team through promotions from within our Company. Please join me in congratulating this year’s class; they deserve it.

Dana Fulton was promoted to Senior Vice President, Financial Planning and Analysis

Jonathan Sherick was promoted to Senior Vice President, New York Controller

Gene Nicotra was promoted to Senior Vice President, Hotel Pennsylvania

Tatiana Melamed was promoted to Vice President, Acquisitions & Capital Markets

Edward Riguardi was promoted to Vice President, Leasing

Bridget Cunningham was promoted to Vice President, Operations, Senior Property Manager

Anthony Moschitta was promoted to Vice President, New York Property Accounting

Hernando Risueno was promoted to Vice President, New York Property Accounting

Welcome Steven Borenstein, Senior Vice President and Corporation Counsel.

Our operating platform heads are the best in the business. I pay my respects to my partners, Michael Franco, Glen Weiss, Barry Langer, Haim Chera and Tom Sanelli. Our exceptional Division Executive Vice Presidents deserve special recognition and our thanks: Michael Doherty – BMS; Robert Entin, Chief Information Officer; Ed Hogan, Leasing – New York Retail; Mark Hudspeth, Capital Markets; Matthew Iocco, Chief Accounting Officer; Myron Maurer, Chief Operating Officer – theMART; Gaston Silva, Chief Operating Officer – New York; and Lisa Vogel, Marketing. Thank you as well to our very talented and hardworking 29 Senior Vice Presidents and 58 Vice Presidents who make the trains run on time, every day.

Thank you and congratulations to Steve Santora (37 years of service) and to Cathy Creswell (18 years of service), who are retiring. We will all miss them and wish them well.

Our Vornado Family has grown with 3 marriages and 13 births this year, 9 girls and 4 boys.

On behalf of Vornado’s Board, senior management and 2,899 associates, we thank our shareholders, analysts and other stakeholders for their continued support.

| | Steven Roth |

| | Chairman and CEO |

| | |

| | April 5, 2021 |

Broadway theatres hopefully will reopen in the fall. My wife is producing the first off-Broadway show to open post-COVID, Blindness, a thrilling socially distanced theatrical experience with immersive sound and light design, playing at the Daryl Roth Theatre in Union Square. Please call if I can help with tickets to Blindness or to any of my wife’s or son’s shows when Broadway reopens.

I salute my future: Rebecca - Yale ’22, Abigail - Dartmouth ’24, Emily - Horace Mann ’23, and Levi will begin kindergarten.

This page intentionally left blank.

Appendix A - Here Are The Principles By Which We Run Our Business:

We are a fully-integrated real estate operating company. We have the best leasing, operating and development teams in the business. We are laser focused.

We invest in the best buildings in the best locations.

We seek to acquire value-add assets where our unique skills will create shareholder value. We believe vacancy at the right price is an opportunity and that buildings, even in rundown condition (that we can reimagine) in great locations are also an opportunity.

We invest in our buildings to maintain, modernize and transform. The front of the house and the back of the house of our assets are as good as new (and are in locations where new could not be created). Our transformations have increased rents over $20 per square foot, yielding attractive double-digit returns. We also measure our success here by the quality of tenants we have been able to attract. We have transformed almost all of our fleet; THE PENN DISTRICT is on deck.

We are disciplined and patient and prepared to let flat 4% cap rate deals pass by, while we wait for the fat pitch.

While we have many million plus square foot buildings, we shy away from 500,000 square foot tenants who seem to always get the better of the deal, in strong markets or in weak. Our sweet spot is the 50,000 to 200,000 square foot tenant.

A few years ago, I coined the phrase, “The island of Manhattan is tilting to the West and to the South.” Today, the hottest submarkets in town run from Hudson Yards to THE PENN DISTRICT and extend South through Chelsea and Meatpacking. Anticipating these trends, we have structured our office portfolio so that half of our square footage is in this district.

We have a hospitality approach, treating our tenants as the valued customers that they are. This attitude begins at the leasing table (although that process can at times be contentious), through tenant fit up, to greeting at the front door. We believe this approach yields the highest renewal rate in the business; renewing tenants enhances our bottom line.

We treat the real estate brokerage community as if they are our customers, because they are. Brokers prefer dealing with us, we know what it takes to make a deal, we treat their clients well and we deliver every time.

We are in the amenity business. Our amenity poster child is the giant MART in Chicago, where we have dominant, state of the art, dining, workout, socializing and meeting spaces, etc.

Tenant mix is really important; companies and their employees care who they co-tenant with. The design and location of each of our buildings has a target market in mind. For example our new-builds in Chelsea are targeting the creative class and boutique financials (an interesting combination).

We maintain a fortress balance sheet with industry-leading liquidity.

All of this in the relentless pursuit of shareholder value.

Below is a reconciliation of Net (Loss) Income to NOI, As Adjusted (properties owned at the end of 2020):

| ($ IN MILLIONS) | | 2020 | | | 2019 | | | 2018 | | | 2017 | | | 2016 | | | 2015 | | | 2014 | | | 2013 | | | 2012 | | | 2011 | |

| Net (Loss) Income | | | (461.8 | ) | | | 3,334.3 | | | | 422.6 | | | | 264.1 | | | | 982.0 | | | | 859.4 | | | | 1,009.0 | | | | 564.7 | | | | 694.5 | | | | 740.0 | |

| Our share of loss (income) from partially owned entities | | | 329.1 | | | | (78.9 | ) | | | (9.1 | ) | | | (15.2 | ) | | | (168.9 | ) | | | 9.9 | | | | 58.5 | | | | 336.3 | | | | (428.9 | ) | | | (125.5 | ) |

| Our share of loss (income) from real estate fund | | | 226.3 | | | | 104.1 | | | | 89.2 | | | | (3.2 | ) | | | 23.6 | | | | (74.1 | ) | | | (163.0 | ) | | | (102.9 | ) | | | (63.9 | ) | | | (22.9 | ) |

| Interest and other investment loss (income), net | | | 5.5 | | | | (21.8 | ) | | | (17.1 | ) | | | (37.8 | ) | | | (29.6 | ) | | | (27.2 | ) | | | (38.6 | ) | | | 20.8 | | | | 252.7 | | | | (156.6 | ) |

| Net gains on disposition of assets | | | (381.3 | ) | | | (845.5 | ) | | | (246.0 | ) | | | (0.5 | ) | | | (160.4 | ) | | | (149.4 | ) | | | (13.6 | ) | | | (2.0 | ) | | | (4.9 | ) | | | (10.9 | ) |

| Net gain on transfer to Fifth Ave. and Times Square JV | | | -- | | | | (2,571.1 | ) | | | -- | | | | -- | | | | -- | | | | -- | | | | -- | | | | -- | | | | -- | | | | -- | |

| Purchase price fair value adjustment | | | -- | | | | -- | | | | (44.1 | ) | | | -- | | | | -- | | | | -- | | | | -- | | | | -- | | | | -- | | | | -- | |

| (Income) loss from discontinued operations | | | -- | | | | -- | | | | (0.6 | ) | | | 13.2 | | | | (404.9 | ) | | | (223.5 | ) | | | (686.9 | ) | | | (666.8 | ) | | | (378.1 | ) | | | (394.4 | ) |

| NOI attributable to noncontrolling interests | | | (72.8 | ) | | | (69.3 | ) | | | (71.2 | ) | | | (65.3 | ) | | | (66.2 | ) | | | (64.9 | ) | | | (55.0 | ) | | | (58.6 | ) | | | (45.3 | ) | | | (47.9 | ) |

| Depreciation, amortization expense and income taxes | | | 436.3 | | | | 522.6 | | | | 484.2 | | | | 470.4 | | | | 428.2 | | | | 294.8 | | | | 360.7 | | | | 342.5 | | | | 304.5 | | | | 309.2 | |