Piedmont Office Realty Trust, Inc.

Quarterly Supplemental Information

Index

| | | | | | | | | | | | | | |

| Page | | | Page |

| | | | |

| Introduction | | | Other Investments | |

| Corporate Data | | | Other Investments Detail | |

| Investor Information | | | Supporting Information | |

| Earnings Release | | | Definitions | |

| Key Performance Indicators | | | Research Coverage | |

| Financials | | | Non-GAAP Reconciliations | |

| Balance Sheets | | | In-Service Portfolio Detail | |

| Income Statements | | | Major Leases Not Yet Commenced and Major Abatements | |

| Funds From Operations / Adjusted Funds From Operations | | | Risks, Uncertainties and Limitations | |

| Same Store Analysis | | | | |

| Capitalization Analysis | | | | |

| Debt Summary | | | | |

| Debt Detail | | | | |

| Debt Covenant & Ratio Analysis | | | | |

| Operational & Portfolio Information - Office Property Investments | | | | |

| Tenant Diversification | | | | |

| Tenant Credit Rating & Lease Distribution Information | | | | |

| Leased Percentage Information | | | | |

| Rental Rate Roll Up / Roll Down Analysis | | | | |

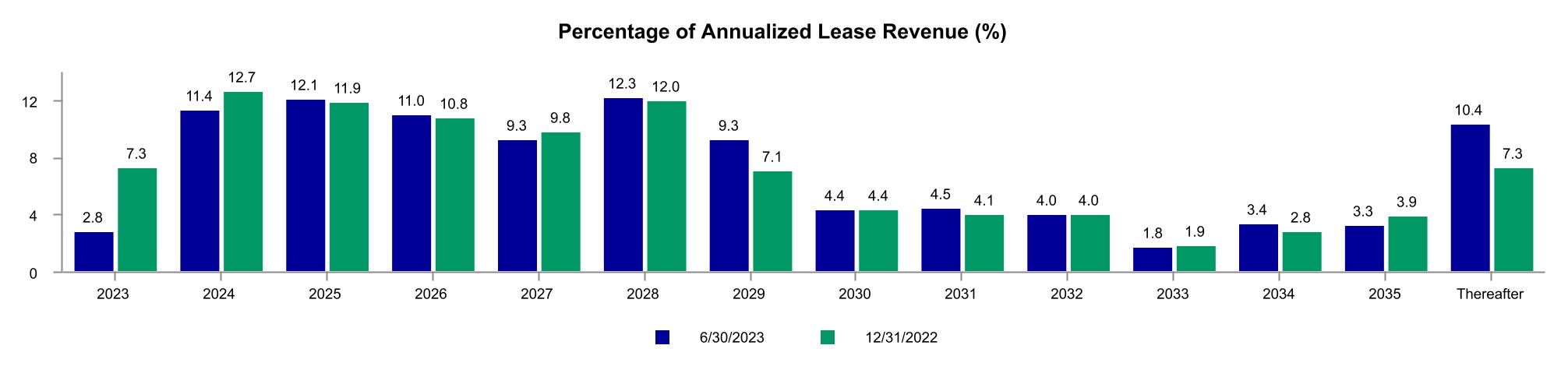

| Lease Expiration Schedule | | | | |

| Quarterly Lease Expirations | | | | |

| Annual Lease Expirations | | | | |

| Contractual Tenant Improvements & Leasing Commissions | | | | |

| Geographic Diversification | | | | |

| Geographic Diversification by Location Type | | | | |

| Industry Diversification | | | | |

| Property Investment Activity | | | | |

| | |

| Notice to Readers: |

Please refer to page 40 for a discussion of important risks related to the business of Piedmont Office Realty Trust, Inc., as well as an investment in its securities, including risks that could cause actual results and events to differ materially from results and events referred to in the forward-looking information. Considering these risks, uncertainties, assumptions, and limitations, the forward-looking statements about leasing, financial operations, leasing prospects, acquisitions, dispositions, etc. contained in this quarterly supplemental information report may differ from actual results. |

| Certain prior period amounts have been reclassified to conform to the current period financial statement presentation. In addition, many of the schedules herein contain rounding to the nearest thousands or millions and, therefore, the schedules may not total due to this rounding convention. |

To supplement the presentation of the Company’s financial results prepared in accordance with U.S. generally accepted accounting principles (GAAP), this report contains certain financial measures that are not prepared in accordance with GAAP, including FFO, Core FFO, AFFO, Same Store NOI, Property NOI, EBITDAre and Core EBITDA. Definitions and reconciliations of these non-GAAP measures to their most comparable GAAP metrics are included beginning on page 33. Each of the non-GAAP measures included in this report has limitations as an analytical tool and should not be considered in isolation or as a substitute for an analysis of the Company’s results calculated in accordance with GAAP. In addition, because not all companies use identical calculations, the Company’s presentation of non-GAAP measures in this report may not be comparable to similarly titled measures disclosed by other companies, including other REITs. The Company may also change the calculation of any of the non-GAAP measures included in this report from time to time in light of its then existing operations. |

|

Piedmont Office Realty Trust, Inc.

Corporate Data

Piedmont Office Realty Trust, Inc. (also referred to herein as "Piedmont" or the "Company") (NYSE: PDM) is an owner, manager, developer, redeveloper and operator of high-quality, Class A office properties located primarily in major U.S. Sunbelt markets. The Company is a fully-integrated, self-managed real estate investment trust ("REIT") with local management offices in each of its markets and is investment-grade rated by Standard & Poor’s and Moody’s. The Company was designated an Energy Star Partner of the Year for 2021, 2022 and 2023, and it was the only office REIT headquartered in the Southeast to receive those designations. Currently, approximately 87% of the Company's square footage is Energy Star certified and approximately 64% is LEED certified. Piedmont is headquartered in Atlanta, GA.

This data supplements the information provided in our reports filed with the Securities and Exchange Commission and should be reviewed in conjunction with such filings.

| | | | | | | | | | | |

| | | |

| As of | | As of |

| June 30, 2023 | | December 31, 2022 |

Number of consolidated in-service office properties (1) | 51 | | 51 |

Rentable square footage (in thousands) (1) | 16,672 | | 16,658 |

Percent leased (2) | 86.2 | % | | 86.7 | % |

| Capitalization (in thousands): | | | |

| Total debt - GAAP | $2,049,236 | | $1,983,681 |

| Total principal amount of debt outstanding (excludes premiums, discounts, and deferred financing costs) | $2,062,000 | | $1,997,000 |

Equity market capitalization (3) | $899,238 | | $1,131,941 |

Total market capitalization (3) | $2,961,238 | | $3,128,941 |

Total principal amount of debt / Total market capitalization (3) | 69.6 | % | | 63.8 | % |

Average net principal amount of debt to Core EBITDA - quarterly (4) | 6.4 x | | 6.4 x |

Average net principal amount of debt to Core EBITDA - trailing twelve months (5) | 6.3 x | | 6.0 x |

Total principal amount of debt / Total gross assets (6) | 38.4 | % | | 37.6 | % |

| Common stock data: | | | |

| High closing price during quarter | $7.39 | | $10.92 |

| Low closing price during quarter | $6.10 | | $8.80 |

| Closing price of common stock at period end | $7.27 | | $9.17 |

| Weighted average fully diluted shares outstanding during quarter (in thousands) | 123,749 | | 123,633 |

| Shares of common stock issued and outstanding at period end (in thousands) | 123,692 | | 123,440 |

Annual regular dividend per share (7) | $0.84 | | $0.84 |

| Ratings (Standard & Poor's / Moody's) | BBB / Baa2 | | BBB / Baa2 |

| Employees | 147 | | 149 |

| | | |

| | | | | |

| (1) | As of June 30, 2023, our consolidated office portfolio consisted of 51 properties (exclusive of one 127,000 square foot property that was out of service for redevelopment, 222 South Orange Avenue in Orlando, FL). |

| (2) | Calculated as square footage associated with commenced leases plus square footage associated with executed but uncommenced leases for vacant spaces at our in-service properties, divided by total rentable in-service square footage, all as of the relevant date, expressed as a percentage. Please refer to page 22 for additional analyses regarding Piedmont's leased percentage. |

| (3) | Reflects common stock closing price, shares outstanding and principal amount of debt outstanding as of the end of the reporting period, as appropriate. |

| (4) | For the purposes of this calculation, we annualize the Core EBITDA for the quarter and use the average daily principal balance of debt outstanding during the quarter, less cash and cash equivalents and escrow deposits and restricted cash as of the end of each month of the quarter. |

| (5) | For the purposes of this calculation, we use the sum of Core EBITDA for the trailing four quarters and the average daily principal balance of debt outstanding for the trailing four quarters, less the average of cash and cash equivalents and escrow deposits and restricted cash as of the end of each month in the trailing four quarter period. |

| (6) | Total gross assets is defined as total assets with the add-back of accumulated depreciation and accumulated amortization related to real estate assets and accumulated amortization related to deferred lease costs. |

| (7) | Total of the regular dividends per share for which record dates occurred over the last four quarters. |

Piedmont Office Realty Trust, Inc.

| | |

| Corporate |

| 5565 Glenridge Connector, Suite 450 |

| Atlanta, Georgia 30342 |

| 770.418.8800 |

| www.piedmontreit.com |

| | | | | | | | | | | |

| Executive Management |

| | | |

| C. Brent Smith | Robert E. Bowers | George Wells | |

| Chief Executive Officer, President | Chief Financial and Administrative Officer | Chief Operating Officer and | |

| and Director | and Executive Vice President | Executive Vice President | |

| | | |

| Kevin D. Fossum | Edward H. Guilbert, III | Christopher A. Kollme | Damian J. Miller |

| Executive Vice President, | Executive Vice President, Finance, | Executive Vice President, | Executive Vice President, |

| Property Management | Assistant Secretary and Treasurer | Investments | Dallas |

| Investor Relations Contact | | |

| | | |

| Laura P. Moon | Alex Valente | Robert K. Wiberg | |

| Chief Accounting Officer and | Executive Vice President, | Executive Vice President, | |

| Senior Vice President | Southeast Region | Northeast Region and Co-Head of | |

| | Development | |

| | | |

| Board of Directors |

| | | |

| Frank C. McDowell | Dale H. Taysom | Kelly H. Barrett | Glenn G. Cohen |

| Director, Chair of the Board of Directors, and | Director, Vice Chair of the | Director, Chair of the Audit Committee, | Director, Chair of the Compensation |

| Member of the Compensation and Governance | Board of Directors, and Member of the | and Member of the Governance Committee | Committee, and Member of the Audit |

| Committees | Audit and Capital Committees | | and Capital Committees |

| | | |

| Venkatesh S. Durvasula | Mary Hager | Barbara B. Lang | C. Brent Smith |

| Director and Member of the Capital Committee | Director and Member of the | Director, Chair of the Governance Committee | Chief Executive Officer, President |

| Governance Committee | (including ESG), and Member of the | and Director |

| | Compensation Committee | |

| Jeffrey L. Swope | | | |

| Director, Chair of the Capital | | | |

| Committee, and Member of the | | | |

| Compensation Committee | | | |

| | | |

| | | | | | | | | | | |

| Transfer Agent | Corporate Counsel | Institutional Analyst Contact | Investor Relations |

| | | |

| Computershare | King & Spalding | Phone: 770.418.8592 | Phone: 866.354.3485 |

| P.O. Box 43006 | 1180 Peachtree Street, NE | research.analysts@piedmontreit.com | investor.services@piedmontreit.com |

| Providence, RI 02940-3078 | Atlanta, GA 30309 | | www.piedmontreit.com |

| Phone: 866.354.3485 | Phone: 404.572.4600 | | |

Piedmont Office Realty Trust, Inc.

Earnings Release

Piedmont Office Realty Trust Reports Second Quarter 2023 Results

ATLANTA, July 20, 2023--Piedmont Office Realty Trust, Inc. ("Piedmont" or the "Company") (NYSE:PDM), an owner of Class A office properties located primarily in major U.S. Sunbelt markets, announced today that its operating partnership, Piedmont Operating Partnership, LP, has completed the issuance of $400 million aggregate principal amount of 9.25% senior unsecured notes due 2028 (the "2028 Notes"), rated BBB by S&P and Baa2 by Moody's. The net proceeds from the issuance will be used to fund the Company's pending tender offer for its outstanding unsecured senior notes due 2024 (the "2024 Notes").

Additionally, the Company announced its results for the quarter ended June 30, 2023 as set forth below and is rescheduling its second quarter earnings call to this afternoon at 5pm ET in order to provide analysts and investors with a real time update regarding the refinancing activity, quarterly results, and revised guidance.

Commenting on the refinancing activity, Brent Smith, Piedmont's President and Chief Executive Officer, said, "With the completion of our latest unsecured notes offering, we have now addressed all of the Company’s debt previously scheduled to mature in 2023 and 2024. The offering was successful despite the extreme volatility and increased economic uncertainty weighing on the financing markets which has drastically reduced new unsecured offerings and mortgage originations, particularly for the office sector. Raising debt capital at this scale in the most challenging commercial real estate market since the global financial crisis is a testament to the strength and credit worthiness of the Piedmont balance sheet.” Continuing, Smith said "Operationally, quarterly results continued to demonstrate the resiliency of our leasing pipeline with over 580,000 square feet leased with an approximately 70% retention ratio and over 14% higher cash rental rates. Furthermore, 240,000 square feet were leased to new tenants, building on the success of the past several quarters. Our well-capitalized, flexible balance sheet and strategic focus on small to medium enterprises continues to drive leasing success. Today, the pipeline remains robust with approximately 250,000 square feet of leasing already in documentation in the third quarter and we continue to project that we will be approximately 87% leased by the end of 2023."

Highlights for the Three Months Ended June 30, 2023:

Financial Results:

| | | | | | | | | | | |

| Three Months Ended | | |

| (in 000s other than per share amounts) | June 30, 2023 | June 30, 2022 | | | |

| Net income/(loss) applicable to Piedmont | $(1,988) | $7,966 | | | |

| Net income/(loss) per share applicable to common stockholders - diluted | $(0.02) | $0.06 | | | |

| | | | | |

| | | | | |

| Interest expense | $23,389 | $13,775 | | | |

| Core Funds From Operations ("Core FFO") applicable to common stock | $55,535 | $61,620 | | | |

| Core FFO per diluted share | $0.45 | $0.50 | | | |

| | | | | |

| | | | | |

| Adjusted Funds From Operations applicable to common stock | $44,444 | $48,900 | | | |

•Net loss applicable to Piedmont for the three months ended June 30, 2023 was $2.0 million, as compared to net income applicable to Piedmont of $8.0 million for the three months ended June 30, 2022.

•Core FFO was $0.45 per diluted share for the second quarter of 2023, as compared to $0.50 per diluted share for the second quarter of 2022. The $0.05 per diluted share decrease was almost exclusively attributable to a $9.6 million, or $0.08 per diluted share, increase in interest expense during the second quarter of 2023, partially offset by continued growth in Property Net Operating Income, as compared to the second quarter of 2022.

Leasing:

| | | | | | | |

| Three Months Ended June 30, 2023 | | |

| # of lease transactions | 49 | | | |

| Total leasing sf | 581,031 | | |

| New tenant leasing sf | 236,448 | | |

| Cash rent roll up | 14.3 | % | | |

| Accrual rent roll up | 19.6 | % | | |

| Quarterly retention ratio | 69.3 | % | | |

| Leased percentage as of period end | 86.2 | % | | |

•The Company completed approximately 581,000 square feet of leasing transactions during the second quarter, over 40% of which, or approximately 236,000 square feet, was for new tenant leasing.

•The average size lease executed during the second quarter of 2023 was approximately 12,000 square feet and the weighted average lease term was approximately six years.

•The two largest leases completed during the quarter were both for new tenants at Galleria Atlanta:

◦An insurance company leased approximately 70,000 square feet through 2036 at Galleria 300; and

◦An owner operator of single family residences leased approximately 51,000 square feet through 2035 at Galleria 600.

•Cash and accrual basis rents on leases executed during the quarter ended June 30, 2023 for space vacant one year or less increased approximately 14% and 20%, respectively.

•The Company's scheduled lease expirations for the remainder of 2023 represent less than 3% of its annualized lease revenue.

•During the second quarter of 2023, Same Store NOI - Cash basis increased 0.2% as new leases commencing or with expiring abatements began to outweigh leases that expired during the first six months of 2023. Same Store NOI on an accrual basis decreased 3.7% during the three months ended June 30, 2023 as compared to the same period in the prior year. The decrease was attributable to a combination of a decline in our overall leased percentage during the current period as compared to the prior period; an increase in leases under operating expense abatement due to recent leasing activity; and an increase in leases which are executed but not yet commenced.

•As of June 30, 2023, the Company had approximately 1.3 million square feet of executed leases for vacant space yet to commence or under rental abatement, representing approximately $37 million of future additional annual cash revenue; consequently, the Company continues to estimate that Same Store NOI, on both a cash and accrual basis, will increase approximately 1-3% on an annual basis in 2023.

•The Company's leased percentage as of June 30, 2023 increased slightly to 86.2% from 86.1% at March 31, 2023. The Company projects its estimated year end leased percentage will be approximately 87%.

Balance Sheet:

| | | | | | | | | | | |

| (in 000s except for ratios) | June 30, 2023 | | December 31, 2022 |

| | | |

| Total Real Estate Assets | $3,512,128 | | $3,500,624 |

| Total Assets | $4,094,349 | | $4,085,525 |

| | | |

| | | |

| Total Debt | $2,049,236 | | $1,983,681 |

| Weighted Average Cost of Debt | 4.49 | % | | 3.89 | % |

| Debt-to-Gross Assets Ratio | 38.4 | % | | 37.6 | % |

| Average Net Debt-to-Core EBITDA (ttm) | 6.3 x | | 6.0 x |

•During the three months ended June 30, 2023, the Company repaid $350 million of maturing unsecured senior notes utilizing $170 million of cash and investments on hand and its $600 million line of credit. The balance outstanding on the line of credit as of June 30, 2023 was $200 million.

ESG and Operations:

•The Company published its 2022 ESG report which is available electronically at www.piedmontreit.com/ ESG / Annual ESG Reports.

•The Company renewed its WELL Health-Safety Rating for its entire 17 million square foot portfolio spanning 51 managed properties.

•US Bancorp Center in Minneapolis, MN won an International The Outstanding Building of the Year ("TOBY") award.

•All five Atlanta Galleria properties, as well as 4250 North Fairfax in Arlington, VA, achieved LEED Gold status, bringing the percentage of the portfolio that is LEED certified to 64%.

•The Company increased its financial needs-based scholarship program to six students for the 2023-24 academic year at Howard University in Washington, D.C. and Morehouse College in Atlanta, GA.

Guidance for 2023

The Company is updating its previously issued guidance for the year ending December 31, 2023 to reflect the continuing rise in interest rates and to specifically reflect the net impact of additional interest expense associated with the issuance of $400 million in aggregate principal amount of 2028 Notes discussed above and the anticipated extinguishment of $300 million of its outstanding $400 million in aggregate principal amount of 2024 Notes in connection with the Company's pending tender offer as follows:

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Previous | | Revised | |

| (in millions, except per share data) | Low | | High | | Low | | High | | | |

| Net income/(loss) | $ | (1) | | | $ | 1 | | | $ | (19) | | | $ | (17) | | | | |

| Add: | | | | | | | | | | |

| Depreciation | 144 | | | 151 | | | 148 | | | 151 | | | | |

| Amortization | 80 | | | 84 | | | 87 | | | 89 | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| Core FFO applicable to common stock | $ | 223 | | | $ | 236 | | | $ | 216 | | | $ | 223 | | | | |

| Core FFO applicable to common stock per diluted share | $1.80 | | $1.90 | | $1.74 | | $1.80 | | | |

| | | | | | | | | | |

The approximately 5% difference between the stated interest rate on the 2024 Notes and the new 2028 Notes will result in an approximately $20.2 million increase in annual interest expense.

This guidance is based on information available to management as of the date of this release and reflects management's view of current market conditions. This guidance assumes that the Company’s pending tender offer to purchase any and all of the Company’s outstanding 2024 Notes is completed as expected and that the Company repurchases $300 million of the outstanding $400 million in aggregate principal amount of 2024 Notes pursuant to the tender offer. No speculative acquisitions or dispositions are included in the above guidance. The Company will adjust guidance throughout the year as such transactions occur, and if interest rate impacts differ from current assumptions.

Note that actual results could differ materially from these estimates and individual quarters may fluctuate on both a cash basis and an accrual basis due to the timing of any future dispositions, significant lease commencements and expirations, abatement periods, repairs and maintenance expenses, capital expenditures, capital markets activities, seasonal general and administrative expenses, accrued potential performance-based compensation expense, one-time revenue or expense events, the actual results of the Company's pending tender offer, and other factors discussed under "Risks, Uncertainties and Limitations" below.

Piedmont Office Realty Trust, Inc.

Key Performance Indicators

Unaudited (in thousands except for per share data and ratios)

| | |

This section of our supplemental report includes non-GAAP financial measures, including, but not limited to, Earnings Before Interest, Taxes, Depreciation, and Amortization for real estate (EBITDAre), Core Earnings Before Interest, Taxes, Depreciation, and Amortization (Core EBITDA), Funds from Operations (FFO), Core Funds from Operations (Core FFO), Adjusted Funds from Operations (AFFO), and Same Store Net Operating Income (Same Store NOI). Definitions of these non-GAAP measures are provided on page 33 and reconciliations are provided beginning on page 35. |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| Selected Operating Data | 6/30/2023 | | 3/31/2023 | | 12/31/2022 | | 9/30/2022 | | 6/30/2022 | | |

| | | | | | | | | | |

| Percent leased | 86.2 | % | | 86.1 | % | | 86.7 | % | | 86.8 | % | | 87.0 | % | | |

Percent leased - economic (1) | 80.0 | % | | 79.6 | % | | 81.1 | % | | 80.6 | % | | 80.7 | % | | |

| Total revenues | $143,072 | | $142,367 | | $147,208 | | $144,100 | | $136,309 | | |

| Net income / (loss) applicable to Piedmont | -$1,988 | | -$1,367 | | $75,569 | | $3,331 | | $7,966 | | |

| Net income / (loss) per share applicable to common stockholders - diluted | -$0.02 | | -$0.01 | | $0.61 | | $0.03 | | $0.06 | | |

| Core EBITDA | $79,212 | | $78,541 | | $82,186 | | $78,805 | | $75,591 | | |

| Core FFO applicable to common stock | $55,535 | | $56,344 | | $61,235 | | $61,352 | | $61,620 | | |

| Core FFO per share - diluted | $0.45 | | $0.46 | | $0.50 | | $0.50 | | $0.50 | | |

| AFFO applicable to common stock | $44,444 | | $36,792 | | $47,082 | | $43,482 | | $48,900 | | |

Gross regular dividends (2) | $25,975 | | $25,965 | | $25,918 | | $25,913 | | $25,912 | | |

Regular dividends per share (2) | $0.21 | | $0.21 | | $0.21 | | $0.21 | | $0.21 | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

Same store net operating income - accrual basis (3) | -3.7 | % | | -2.8 | % | | -0.7 | % | | 0.3 | % | | 2.8 | % | | |

Same store net operating income - cash basis (3) | 0.2 | % | | -1.5 | % | | 1.6 | % | | -0.3 | % | | 1.8 | % | | |

| Rental rate roll up / roll down - accrual rents | 19.6 | % | | 9.9 | % | | 11.5 | % | | 37.6 | % | | 12.2 | % | | |

| Rental rate roll up / roll down - cash rents | 14.3 | % | | 5.7 | % | | 6.5 | % | | 33.1 | % | | 2.5 | % | | |

| Selected Balance Sheet Data | | | | | | | | | | | |

| Total real estate assets, net | $3,512,128 | | $3,486,797 | | $3,500,624 | | $3,572,591 | | $3,139,587 | | |

| Total assets | $4,094,349 | | $4,237,460 | | $4,085,525 | | $4,185,493 | | $3,695,554 | | |

| Total liabilities | $2,297,015 | | $2,417,363 | | $2,236,270 | | $2,388,162 | | $1,879,891 | | |

| Ratios & Information for Debt Holders | | | | | | | | | | | |

| Core EBITDA to total revenues | 55.4 | % | | 55.2 | % | | 55.8 | % | | 54.7 | % | | 55.5 | % | | |

Fixed charge coverage ratio (4) | 3.2 x | | 3.4 x | | 3.8 x | | 4.3 x | | 5.1 x | | |

Average net principal amount of debt to Core EBITDA - quarterly (5) | 6.4 x | | 6.3 x | | 6.4 x | | 6.1 x | | 5.5 x | | |

| Total gross real estate assets | $4,576,943 | | $4,518,003 | | $4,506,328 | | $4,587,669 | | $4,117,177 | | |

| Total debt - GAAP | $2,049,236 | | $2,197,955 | | $1,983,681 | | $2,145,408 | | $1,674,778 | | |

Net principal amount of debt (6) | $2,051,778 | | $2,037,224 | | $1,977,400 | | $2,146,156 | | $1,681,144 | | |

| | | | | |

| (1) | Economic leased percentage excludes the square footage associated with executed but not commenced leases for currently vacant spaces and the square footage associated with tenants receiving rental abatements (after proportional adjustments for tenants receiving only partial rental abatements). Due to variations in rental abatement structures, there will be variability to the economic leased percentage over time as abatements commence and expire. |

| (2) | Dividends are reflected in the quarter in which the record date occurred. |

| (3) | Please refer to the three pages starting with page 13 for reconciliations to net income and additional same store net operating income information. The statistic provided for each of the prior quarters is based on the same store property population applicable at the time that the metric was initially reported. |

| (4) | The fixed charge coverage ratio is calculated as Core EBITDA divided by the sum of interest expense, principal amortization (none during periods presented), capitalized interest and preferred dividends (none during periods presented). The Company had capitalized interest of $1.4 million for the quarter ending June 30, 2023, $1.2 million for the quarter ending March 31, 2023, $1.0 million for the quarter ended December 31, 2022, $1.1 million for the quarter ended September 30, 2022, and $1.1 million for the quarter ended June 30, 2022. |

| (5) | For the purposes of this calculation, we annualize the Core EBITDA for the quarter and use the average daily principal balance of debt outstanding during the quarter, less cash and cash equivalents and escrow deposits and restricted cash as of the end of each month of the quarter. |

| (6) | Net principal amount of debt is calculated and defined as the total principal amount of debt outstanding minus cash and cash equivalents and escrow deposits and restricted cash all as of the end of the period. |

Piedmont Office Realty Trust, Inc.

Consolidated Balance Sheets

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 6/30/2023 | | 3/31/2023 | | 12/31/2022 | | 9/30/2022 | | 6/30/2022 |

| Assets: | | | | | | | | | |

| Real estate, at cost: | | | | | | | | | |

| Land assets | $ | 567,244 | | | $ | 567,244 | | | $ | 567,244 | | | $ | 578,722 | | | $ | 521,789 | |

| Buildings and improvements | 3,768,456 | | | 3,714,572 | | | 3,682,000 | | | 3,751,722 | | | 3,389,650 | |

| Buildings and improvements, accumulated depreciation | (981,052) | | | (947,209) | | | (915,010) | | | (926,357) | | | (892,131) | |

| Intangible lease asset | 182,127 | | | 190,180 | | | 205,074 | | | 212,248 | | | 164,194 | |

| Intangible lease asset, accumulated amortization | (83,763) | | | (83,997) | | | (90,694) | | | (88,721) | | | (85,459) | |

| Construction in progress | 59,116 | | | 46,007 | | | 52,010 | | | 44,977 | | | 41,544 | |

| | | | | | | | | |

| | | | | | | | | |

| Total real estate assets | 3,512,128 | | | 3,486,797 | | | 3,500,624 | | | 3,572,591 | | | 3,139,587 | |

| | | | | | | | | |

| Cash and cash equivalents | 5,167 | | | 170,593 | | | 16,536 | | | 10,653 | | | 6,397 | |

| Tenant receivables, net of allowance for doubtful accounts | 5,387 | | | 6,280 | | | 4,762 | | | 7,796 | | | 5,164 | |

| Straight line rent receivable | 180,339 | | | 176,320 | | | 172,019 | | | 173,122 | | | 168,797 | |

| | | | | | | | | |

| Escrow deposits and restricted cash | 5,055 | | | 4,183 | | | 3,064 | | | 2,191 | | | 1,459 | |

| Prepaid expenses and other assets | 23,566 | | | 26,810 | | | 17,152 | | | 23,925 | | | 26,955 | |

| Goodwill | 82,937 | | | 82,937 | | | 82,937 | | | 98,918 | | | 98,918 | |

| Interest rate swap | 5,693 | | | 2,899 | | | 4,183 | | | 3,760 | | | 996 | |

| | | | | | | | | |

| Deferred lease costs, gross | 482,149 | | | 486,694 | | | 505,979 | | | 510,936 | | | 459,038 | |

| Deferred lease costs, accumulated amortization | (208,072) | | | (206,053) | | | (221,731) | | | (218,399) | | | (211,757) | |

| | | | | | | | | |

| | | | | | | | | |

| Total assets | $ | 4,094,349 | | | $ | 4,237,460 | | | $ | 4,085,525 | | | $ | 4,185,493 | | | $ | 3,695,554 | |

| Liabilities: | | | | | | | | | |

| Unsecured debt, net of discount | $ | 1,852,236 | | | $ | 2,000,955 | | | $ | 1,786,681 | | | $ | 1,948,408 | | | $ | 1,674,778 | |

| Secured debt | 197,000 | | | 197,000 | | | 197,000 | | | 197,000 | | | — | |

| Accounts payable, accrued expenses, and accrued capital expenditures | 107,629 | | | 98,464 | | | 135,663 | | | 111,262 | | | 99,724 | |

| Deferred income | 89,815 | | | 67,056 | | | 59,977 | | | 70,798 | | | 72,422 | |

| Intangible lease liabilities, less accumulated amortization | 50,335 | | | 53,494 | | | 56,949 | | | 60,694 | | | 32,967 | |

| Interest rate swaps | — | | | 394 | | | — | | | — | | | — | |

| | | | | | | | | |

| Total liabilities | 2,297,015 | | | 2,417,363 | | | 2,236,270 | | | 2,388,162 | | | 1,879,891 | |

| Stockholders' equity: | | | | | | | | | |

| Common stock | 1,237 | | | 1,236 | | | 1,234 | | | 1,234 | | | 1,234 | |

| Additional paid in capital | 3,712,688 | | | 3,710,767 | | | 3,711,005 | | | 3,709,234 | | | 3,707,833 | |

| Cumulative distributions in excess of earnings | (1,911,188) | | | (1,883,225) | | | (1,855,893) | | | (1,905,544) | | | (1,882,962) | |

| Other comprehensive loss | (6,977) | | | (10,266) | | | (8,679) | | | (9,194) | | | (12,050) | |

| Piedmont stockholders' equity | 1,795,760 | | | 1,818,512 | | | 1,847,667 | | | 1,795,730 | | | 1,814,055 | |

| Non-controlling interest | 1,574 | | | 1,585 | | | 1,588 | | | 1,601 | | | 1,608 | |

| Total stockholders' equity | 1,797,334 | | | 1,820,097 | | | 1,849,255 | | | 1,797,331 | | | 1,815,663 | |

| Total liabilities, redeemable common stock and stockholders' equity | $ | 4,094,349 | | | $ | 4,237,460 | | | $ | 4,085,525 | | | $ | 4,185,493 | | | $ | 3,695,554 | |

| Common stock outstanding at end of period | 123,692 | | | 123,643 | | | 123,440 | | | 123,395 | | | 123,390 | |

Piedmont Office Realty Trust, Inc.

Consolidated Statements of Income

Unaudited (in thousands except for per share data)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended |

| | 6/30/2023 | | 3/31/2023 | | 12/31/2022 | | 9/30/2022 | | 6/30/2022 |

| Revenues: | | | | | | | | | | |

Rental income (1) | | $ | 112,238 | | | $ | 112,560 | | | $ | 117,148 | | | $ | 114,280 | | | $ | 110,244 | |

Tenant reimbursements (1) | | 25,265 | | | 24,269 | | | 24,958 | | | 25,292 | | | 21,907 | |

| Property management fee revenue | | 437 | | | 507 | | | 395 | | | 303 | | | 326 | |

| Other property related income | | 5,132 | | | 5,031 | | | 4,707 | | | 4,225 | | | 3,832 | |

| | 143,072 | | | 142,367 | | | 147,208 | | | 144,100 | | | 136,309 | |

| Expenses: | | | | | | | | | | |

| Property operating costs | | 58,368 | | | 57,791 | | | 59,763 | | | 59,039 | | | 53,634 | |

| Depreciation | | 36,475 | | | 35,797 | | | 34,788 | | | 34,941 | | | 32,372 | |

| Amortization | | 21,333 | | | 22,031 | | | 23,915 | | | 23,290 | | | 21,480 | |

Impairment loss (2) | | — | | | — | | | 25,981 | | | — | | | — | |

| General and administrative | | 7,279 | | | 7,691 | | | 7,915 | | | 6,590 | | | 7,027 | |

| | 123,455 | | | 123,310 | | | 152,362 | | | 123,860 | | | 114,513 | |

| Other income / (expense): | | | | | | | | | | |

| Interest expense | | (23,389) | | | (22,077) | | | (20,739) | | | (17,244) | | | (13,775) | |

| Other income / (expense) | | 1,787 | | | 1,656 | | | 408 | | | 335 | | | (57) | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

Gain / (loss) on sale of real estate (2) | | — | | | — | | | 101,055 | | | — | | | 1 | |

| Net income / (loss) | | (1,985) | | | (1,364) | | | 75,570 | | | 3,331 | | | 7,965 | |

| Less: Net (income) / loss applicable to noncontrolling interest | | (3) | | | (3) | | | (1) | | | — | | | 1 | |

| Net income / (loss) applicable to Piedmont | | $ | (1,988) | | | $ | (1,367) | | | $ | 75,569 | | | $ | 3,331 | | | $ | 7,966 | |

| Weighted average common shares outstanding - diluted | | 123,671 | | | 123,550 | | | 123,633 | | | 123,697 | | | 123,679 | |

| Net income / (loss) per share applicable to common stockholders - diluted | | $ | (0.02) | | | $ | (0.01) | | | $ | 0.61 | | | $ | 0.03 | | | $ | 0.06 | |

| Common stock outstanding at end of period | | 123,692 | | | 123,643 | | | 123,440 | | | 123,395 | | | 123,390 | |

| | | | | |

| (1) | The presentation method used for this line is not in conformance with GAAP. To be in conformance with the current GAAP standard, the Company would combine amounts presented on the rental income line with amounts presented on the tenant reimbursements line and present that aggregated figure on one line entitled "rental and tenant reimbursement revenue." |

| (2) | The gain on sale of real estate reflected in the fourth quarter of 2022 was primarily related to the sales of One Brattle Square and 1414 Massachusetts Avenue, both in Cambridge, MA. The impairment loss reflected in the fourth quarter of 2022 was related to (a) a partial write down of the Company's goodwill balance; and (b) the write down of one property. |

Piedmont Office Realty Trust, Inc.

Consolidated Statements of Income

Unaudited (in thousands except for per share data)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended | | Six Months Ended |

| 6/30/2023 | 6/30/2022 | | Change ($) | Change (%) | | 6/30/2023 | 6/30/2022 | | Change ($) | Change (%) |

| Revenues: | | | | | | | | | | | |

Rental income (1) | $ | 112,238 | | $ | 110,244 | | | $ | 1,994 | | 1.8 | % | | $ | 224,798 | | $ | 219,976 | | | $ | 4,822 | | 2.2 | % |

Tenant reimbursements (1) | 25,265 | | 21,907 | | | 3,358 | | 15.3 | % | | 49,534 | | 44,087 | | | 5,447 | | 12.4 | % |

| Property management fee revenue | 437 | | 326 | | | 111 | | 34.0 | % | | 944 | | 977 | | | (33) | | (3.4) | % |

| Other property related income | 5,132 | | 3,832 | | | 1,300 | | 33.9 | % | | 10,163 | | 7,418 | | | 2,745 | | 37.0 | % |

| 143,072 | | 136,309 | | | 6,763 | | 5.0 | % | | 285,439 | | 272,458 | | | 12,981 | | 4.8 | % |

| Expenses: | | | | | | | | | | | |

| Property operating costs | 58,368 | | 53,634 | | | (4,734) | | (8.8) | % | | 116,159 | | 107,256 | | | (8,903) | | (8.3) | % |

| Depreciation | 36,475 | | 32,372 | | | (4,103) | | (12.7) | % | | 72,272 | | 63,887 | | | (8,385) | | (13.1) | % |

| Amortization | 21,333 | | 21,480 | | | 147 | | 0.7 | % | | 43,364 | | 43,732 | | | 368 | | 0.8 | % |

| | | | | | | | | | | |

| General and administrative | 7,279 | | 7,027 | | | (252) | | (3.6) | % | | 14,970 | | 14,622 | | | (348) | | (2.4) | % |

| 123,455 | | 114,513 | | | (8,942) | | (7.8) | % | | 246,765 | | 229,497 | | | (17,268) | | (7.5) | % |

| Other income / (expense): | | | | | | | | | | | |

| Interest expense | (23,389) | | (13,775) | | | (9,614) | | (69.8) | % | | (45,466) | | (27,673) | | | (17,793) | | (64.3) | % |

| Other income / (expense) | 1,787 | | (57) | | | 1,844 | | 3,235.1 | % | | 3,443 | | 1,967 | | | 1,476 | | 75.0 | % |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

Gain / (loss) on sale of real estate (2) | — | | 1 | | | (1) | | (100.0) | % | | — | | 50,674 | | | (50,674) | | (100.0) | % |

| Net income / (loss) | (1,985) | | 7,965 | | | (9,950) | | (124.9) | % | | (3,349) | | 67,929 | | | (71,278) | | (104.9) | % |

| Less: Net (income) / loss applicable to noncontrolling interest | (3) | | 1 | | | (4) | | (400.0) | % | | (6) | | 1 | | | (7) | | (700.0) | % |

| Net income / (loss) applicable to Piedmont | $ | (1,988) | | $ | 7,966 | | | $ | (9,954) | | (125.0) | % | | $ | (3,355) | | $ | 67,930 | | | $ | (71,285) | | (104.9) | % |

| Weighted average common shares outstanding - diluted | 123,671 | | 123,679 | | | | | | 123,611 | | 123,617 | | | | |

| Net income / (loss) per share applicable to common stockholders - diluted | $ | (0.02) | | $ | 0.06 | | | | | | $ | (0.03) | | $ | 0.55 | | | | |

| Common stock outstanding at end of period | 123,692 | | 123,390 | | | | | | 123,692 | | 123,390 | | | | |

| | | | | |

| (1) | The presentation method used for this line is not in conformance with GAAP. To be in conformance with the current GAAP standard, the Company would combine amounts presented on the rental income line with amounts presented on the tenant reimbursements line and present that aggregated figure on one line entitled "rental and tenant reimbursement revenue." |

| (2) | The gain on sale of real estate for the six months ended June 30, 2022 was primarily related to the sales of 225 and 235 Presidential Way in Woburn, MA. |

| |

Piedmont Office Realty Trust, Inc.

Funds From Operations, Core Funds From Operations and Adjusted Funds From Operations

Unaudited (in thousands except for per share data) | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended | | Six Months Ended |

| | 6/30/2023 | | 6/30/2022 | | 6/30/2023 | | 6/30/2022 |

| | | | | | | | |

| GAAP net income / (loss) applicable to common stock | | $ | (1,988) | | | $ | 7,966 | | | $ | (3,355) | | | $ | 67,930 | |

Depreciation for real estate assets (1) | | 36,200 | | | 32,187 | | | 71,890 | | | 63,519 | |

Amortization (1) | | 21,323 | | | 21,468 | | | 43,344 | | | 43,708 | |

| | | | | | | | |

| Loss / (gain) on sale of properties | | — | | | (1) | | | — | | | (50,674) | |

| | | | | | | | |

| NAREIT funds from operations and core funds from operations applicable to common stock | | 55,535 | | | 61,620 | | | 111,879 | | | 124,483 | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| Adjustments: | | | | | | | | |

| Amortization of debt issuance costs and discounts on debt | | 1,312 | | | 763 | | | 2,551 | | | 1,541 | |

| Depreciation of non real estate assets | | 264 | | | 175 | | | 361 | | | 348 | |

Straight-line effects of lease revenue (1) | | (2,755) | | | (3,029) | | | (5,942) | | | (5,606) | |

| Stock-based compensation adjustments | | 2,095 | | | 1,718 | | | 2,278 | | | 1,166 | |

Amortization of lease-related intangibles (1) | | (3,119) | | | (3,009) | | | (6,531) | | | (6,171) | |

| | | | | | | | |

Non-incremental capital expenditures (2) | | | | | | | | |

| Building/Construction/Development | | (2,914) | | | (4,748) | | | (7,666) | | | (8,254) | |

| Tenant Improvements | | (2,228) | | | (3,402) | | | (7,927) | | | (14,908) | |

| Leasing Costs | | (3,746) | | | (1,188) | | | (7,767) | | | (5,123) | |

| Adjusted funds from operations applicable to common stock | | $ | 44,444 | | | $ | 48,900 | | | $ | 81,236 | | | $ | 87,476 | |

| | | | | | | | |

| Weighted average common shares outstanding - diluted | | 123,749 | | | 123,679 | | | 123,696 | | | 123,617 | |

| | | | | | | | |

| Funds from operations per share (diluted) | | $ | 0.45 | | | $ | 0.50 | | | $ | 0.90 | | | $ | 1.01 | |

| Core funds from operations per share (diluted) | | $ | 0.45 | | | $ | 0.50 | | | $ | 0.90 | | | $ | 1.01 | |

| | | | | | | | |

| Common stock outstanding at end of period | | 123,692 | | | 123,390 | | | 123,692 | | | 123,390 | |

| | | | | |

| (1) | Includes our proportionate share of amounts attributable to consolidated properties. |

| (2) | Non-incremental capital expenditures are defined on page 33. |

Piedmont Office Realty Trust, Inc.

Same Store Net Operating Income (Cash Basis)

| | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended | | Six Months Ended |

| 6/30/2023 | | 6/30/2022 | | 6/30/2023 | | 6/30/2022 |

| Net income / (loss) applicable to Piedmont | $ | (1,988) | | | $ | 7,966 | | | $ | (3,355) | | | $ | 67,930 | |

| Net income / (loss) applicable to noncontrolling interest | 3 | | | (1) | | | 6 | | | (1) | |

| Interest expense | 23,389 | | | 13,775 | | | 45,466 | | | 27,673 | |

Depreciation (1) | 36,464 | | | 32,362 | | | 72,251 | | | 63,867 | |

Amortization (1) | 21,323 | | | 21,468 | | | 43,344 | | | 43,708 | |

| Depreciation and amortization attributable to noncontrolling interests | 21 | | | 22 | | | 41 | | | 44 | |

| | | | | | | |

| (Gain) / loss on sale of properties | — | | | (1) | | | — | | | (50,674) | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

EBITDAre and Core EBITDA (2) | 79,212 | | | 75,591 | | | 157,753 | | | 152,547 | |

| General & administrative expenses | 7,279 | | | 7,027 | | | 14,970 | | | 14,622 | |

| Non-cash general reserve for uncollectible accounts | — | | | (1,000) | | | (400) | | | (1,000) | |

Management fee revenue (3) | (254) | | | (203) | | | (546) | | | (565) | |

Other (income) / expense (1) (4) | (1,571) | | | 273 | | | (3,012) | | | (1,536) | |

Straight-line effects of lease revenue (1) | (2,755) | | | (3,029) | | | (5,942) | | | (5,606) | |

| Straight-line effects of lease revenue attributable to noncontrolling interests | (1) | | | (1) | | | (6) | | | (1) | |

Amortization of lease-related intangibles (1) | (3,119) | | | (3,009) | | | (6,531) | | | (6,171) | |

| Property net operating income (cash basis) | 78,791 | | | 75,649 | | | 156,286 | | | 152,290 | |

| Deduct net operating (income) / loss from: | | | | | | | |

Acquisitions (5) | (5,770) | | | — | | | (10,843) | | | — | |

Dispositions (6) | 48 | | | (2,704) | | | 74 | | | (5,785) | |

Other investments (7) | 173 | | | 138 | | | 337 | | | 328 | |

| Same store net operating income (cash basis) | $ | 73,242 | | | $ | 73,083 | | | $ | 145,854 | | | $ | 146,833 | |

| Change period over period | 0.2 | % | | N/A | | (0.7) | % | | N/A |

| | | | | |

| (1) | Includes our proportionate share of amounts attributable to consolidated properties. |

| (2) | The Company has historically recognized approximately $2 to $3 million of termination income on an annual basis. Given the size of its asset base and the number of tenants with which it conducts business, Piedmont considers termination income of that magnitude to be a normal part of its operations and a recurring part of its revenue stream; however, the recognition of termination income is typically variable between quarters and throughout any given year and is dependent upon when during the year the Company receives termination notices from tenants. During the three months ended June 30 2023, Piedmont recognized $0.2 million of termination income, as compared with $0.4 million during the same period in 2022. During the six months ended June 30, 2023, Piedmont recognized $0.4 million of termination income, as compared with $0.6 million during the same period in 2022. |

| (3) | Presented net of related operating expenses incurred to earn the revenue; therefore, the information presented on this line will not tie to the data presented on the income statements. |

| (4) | Figures presented on this line may not tie back to the relevant sources as some activity is attributable to property operations and is, therefore, presented in property net operating income. |

| (5) | Acquisitions includes 1180 Peachtree Street in Atlanta, GA, purchased in the third quarter of 2022. |

| (6) | Dispositions include Two Pierce Place in Itasca, IL and 225 and 235 Presidential Way in Woburn, MA, sold in the first quarter of 2022, and One Brattle Square and 1414 Massachusetts Avenue in Cambridge, MA, sold in the fourth quarter of 2022. |

| (7) | Other investments include active out-of-service redevelopment and development projects, land, and recently completed redevelopment and development projects. Additional information on our land holdings can be found on page 32.The operating results from 222 South Orange Avenue in Orlando, FL, are included in this line item. |

| |

Piedmont Office Realty Trust, Inc.

Same Store Net Operating Income (Accrual Basis)

Unaudited (in thousands)

| | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended | | Six Months Ended |

| 6/30/2023 | | 6/30/2022 | | 6/30/2023 | | 6/30/2022 |

| Net income / (loss) applicable to Piedmont | $ | (1,988) | | | $ | 7,966 | | | $ | (3,355) | | | $ | 67,930 | |

| Net income / (loss) applicable to noncontrolling interest | 3 | | | (1) | | | 6 | | | (1) | |

| Interest expense | 23,389 | | | 13,775 | | | 45,466 | | | 27,673 | |

Depreciation (1) | 36,464 | | | 32,362 | | | 72,251 | | | 63,867 | |

Amortization (1) | 21,323 | | | 21,468 | | | 43,344 | | | 43,708 | |

| Depreciation and amortization attributable to noncontrolling interests | 21 | | | 22 | | | 41 | | | 44 | |

| | | | | | | |

| (Gain) / loss on sale of properties | — | | | (1) | | | — | | | (50,674) | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

EBITDAre and Core EBITDA (2) | 79,212 | | | 75,591 | | | 157,753 | | | 152,547 | |

| General & administrative expenses | 7,279 | | | 7,027 | | | 14,970 | | | 14,622 | |

Management fee revenue (3) | (254) | | | (203) | | | (546) | | | (565) | |

Other (income) / expense (1) (4) | (1,571) | | | 273 | | | (3,012) | | | (1,536) | |

| Property net operating income (accrual basis) | 84,666 | | | 82,688 | | | 169,165 | | | 165,068 | |

| Deduct net operating (income) / loss from: | | | | | | | |

Acquisitions (5) | (7,612) | | | — | | | (14,980) | | | — | |

Dispositions (6) | 49 | | | (2,697) | | | 74 | | | (5,857) | |

Other investments (7) | 70 | | | 130 | | | 132 | | | 377 | |

| Same store net operating income (accrual basis) | $ | 77,173 | | | $ | 80,121 | | | $ | 154,391 | | | $ | 159,588 | |

| Change period over period | (3.7) | % | | N/A | | (3.3) | % | | N/A |

| | | | | |

| (1) | Includes our proportionate share of amounts attributable to consolidated properties. |

| (2) | The Company has historically recognized approximately $2 to $3 million of termination income on an annual basis. Given the size of its asset base and the number of tenants with which it conducts business, Piedmont considers termination income of that magnitude to be a normal part of its operations and a recurring part of its revenue stream; however, the recognition of termination income is typically variable between quarters and throughout any given year and is dependent upon when during the year the Company receives termination notices from tenants. During the three months ended June 30 2023, Piedmont recognized $0.2 million of termination income, as compared with $0.4 million during the same period in 2022. During the six months ended June 30, 2023, Piedmont recognized $0.4 million of termination income, as compared with $0.6 million during the same period in 2022. |

| (3) | Presented net of related operating expenses incurred to earn the revenue; therefore, the information presented on this line will not tie to the data presented on the income statements. |

| (4) | Figures presented on this line may not tie back to the relevant sources as some activity is attributable to property operations and is, therefore, presented in property net operating income. |

| (5) | Acquisitions includes 1180 Peachtree Street in Atlanta, GA, purchased in the third quarter of 2022. |

| (6) | Dispositions include Two Pierce Place in Itasca, IL and 225 and 235 Presidential Way in Woburn, MA, sold in the first quarter of 2022, and One Brattle Square and 1414 Massachusetts Avenue in Cambridge, MA, sold in the fourth quarter of 2022. |

| (7) | Other investments include active out-of-service redevelopment and development projects, land, and recently completed redevelopment and development projects. Additional information on our land holdings can be found on page 32. The operating results from 222 South Orange Avenue in Orlando, FL, are included in this line item. |

Piedmont Office Realty Trust, Inc.

Same Store Net Operating Income (Financial Components)

Unaudited (in thousands)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | |

| | Three Months Ended | | Six Months Ended |

| | 6/30/2023 | 6/30/2022 | Change ($) | Change (%) | | 6/30/2023 | 6/30/2022 | Change ($) | Change (%) |

| | | | | | | | | | |

| Revenue | | | | | | | | | |

| Cash rental income | $ | 100,259 | | $ | 101,158 | | $ | (899) | | (0.9) | % | | $ | 200,562 | | $ | 201,460 | | $ | (898) | | (0.4) | % |

| Tenant reimbursements (1) | 23,841 | | 21,341 | | 2,500 | | 11.7 | % | | 46,779 | | 42,818 | | 3,961 | | 9.3 | % |

| Straight line effects of lease revenue | 1,905 | | 2,974 | | (1,069) | | (35.9) | % | | 3,801 | | 5,473 | | (1,672) | | (30.5) | % |

| Amortization of lease-related intangibles | 2,026 | | 3,064 | | (1,038) | | (33.9) | % | | 4,336 | | 6,282 | | (1,946) | | (31.0) | % |

| Total rents | 128,031 | | 128,537 | | (506) | | (0.4) | % | | 255,478 | | 256,033 | | (555) | | (0.2) | % |

| | | | | | | | | | |

| Other property related income (2) | 4,487 | | 3,828 | | 659 | | 17.2 | % | | 9,097 | | 7,604 | | 1,493 | | 19.6 | % |

| Total revenue | 132,518 | | 132,365 | | 153 | | 0.1 | % | | 264,575 | | 263,637 | | 938 | | 0.4 | % |

| | | | | | | | | | |

Property operating expense (3) | 55,560 | | 52,459 | | (3,101) | | (5.9) | % | | 110,615 | | 104,480 | | (6,135) | | (5.9) | % |

| | | | | | | | | | |

| Property other income / (expense) | 215 | | 215 | | — | | — | % | | 431 | | 431 | | — | | — | % |

| | | | | | | | | | |

| Same store net operating income (accrual) | $ | 77,173 | | $ | 80,121 | | $ | (2,948) | | (3.7) | % | | $ | 154,391 | | $ | 159,588 | | $ | (5,197) | | (3.3) | % |

| | | | | | | | | | |

| Less: | | | | | | | | | |

| Straight line effects of lease revenue | (1,905) | | (2,974) | | 1,069 | | 35.9 | % | | (3,801) | | (5,473) | | 1,672 | | 30.5 | % |

| Amortization of lease-related intangibles | (2,026) | | (3,064) | | 1,038 | | 33.9 | % | | (4,336) | | (6,282) | | 1,946 | | 31.0 | % |

| Non-cash general reserve for uncollectible accounts | — | | (1,000) | | 1,000 | | 100.0 | % | | (400) | | (1,000) | | 600 | | 60.0 | % |

| | | | | | | | | | |

| Same store net operating income (cash) | $ | 73,242 | | $ | 73,083 | | $ | 159 | | 0.2 | % | | $ | 145,854 | | $ | 146,833 | | $ | (979) | | (0.7) | % |

| | | | | | | | | | |

| | | | | |

| (1) | The increase in tenant reimbursements for the three months and the six months ended June 30, 2023 as compared to the same periods in 2022 was primarily the result of an increase in recoverable operating expenses in 2023 in comparison to 2022 due to the increased physical utilization of our buildings. |

| (2) | The increase in other property related income for the three months and the six months ended June 30, 2023 as compared to the same periods in 2022 was primarily related to increased parking demand across the portfolio as a result of post-pandemic increased business activity. |

| (3) | The increase in property operating expense for the three months and the six months ended June 30, 2023 as compared to the same periods in 2022 was primarily associated with increased variable operating costs as a result of increasing physical office space utilization by tenants across our portfolio. |

Piedmont Office Realty Trust, Inc.

Capitalization Analysis

Unaudited (in thousands except for per share data and ratios)

| | | | | | | | | | | |

| | | |

| As of | | As of |

| June 30, 2023 | | December 31, 2022 |

| | | |

| Market Capitalization | | | |

| Common stock price | $7.27 | | $9.17 |

| Total shares outstanding | 123,692 | | 123,440 |

Equity market capitalization (1) | $899,238 | | $1,131,941 |

| Total debt - GAAP | $2,049,236 | | $1,983,681 |

| Total principal amount of debt outstanding (excludes premiums, discounts, and deferred financing costs) | $2,062,000 | | $1,997,000 |

Total market capitalization (1) | $2,961,238 | | $3,128,941 |

Total principal amount of debt / Total market capitalization (1) | 69.6 | % | | 63.8 | % |

| Ratios & Information for Debt Holders | | | |

Total gross assets (2) | $5,367,236 | | $5,312,960 |

Total principal amount of debt / Total gross assets (2) | 38.4 | % | | 37.6 | % |

Average net principal amount of debt to Core EBITDA - quarterly (3) | 6.4 x | | 6.4 x |

Average net principal amount of debt to Core EBITDA - trailing twelve months (4) | 6.3 x | | 6.0 x |

| | | | | |

| (1) | Reflects common stock closing price, shares outstanding, and principal amount of debt outstanding as of the end of the reporting period, as appropriate. |

| (2) | Total gross assets is defined as total assets with the add-back of accumulated depreciation and accumulated amortization related to real estate assets and accumulated amortization related to deferred lease costs. |

| (3) | For the purposes of this calculation, we annualize the Core EBITDA for the quarter and use the average daily principal balance of debt outstanding during the quarter, less cash and cash equivalents and escrow deposits and restricted cash as of the end of each month of the quarter. |

| (4) | For the purposes of this calculation, we use the sum of Core EBITDA for the trailing four quarters and the average daily principal balance of debt outstanding for the trailing four quarters, less the average of cash and cash equivalents and escrow deposits and restricted cash as of the end of each month in the trailing four quarter period. |

Piedmont Office Realty Trust, Inc.

Debt Summary

As of June 30, 2023

Unaudited ($ in thousands)

| | | | | | | | | | | | | | | |

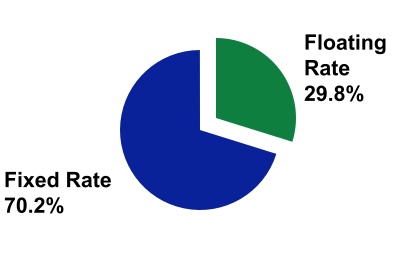

| Floating Rate & Fixed Rate Debt | | | | |

Debt (1) | Principal Amount Outstanding | Weighted Average Stated Interest Rate (2) | Weighted Average Maturity |

| | | | |

| Floating Rate | $615,000 | (3) | 6.14% | 30.0 months |

| | | | |

| Fixed Rate | 1,447,000 | | | 3.80% | 54.1 months |

| | | | |

| Total | $2,062,000 | | 4.49% | 46.9 months |

| | | | |

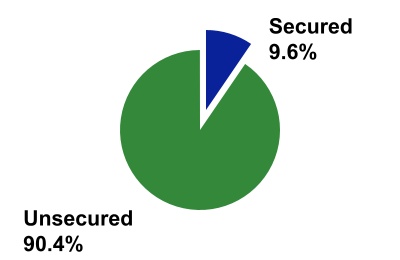

| | | | | | | | | | | | | | | |

| Unsecured & Secured Debt | |

Debt (1) | Principal Amount Outstanding | Weighted Average Stated Interest Rate (2) | Weighted Average Maturity |

| | | | |

| Unsecured | $1,865,000 | | 4.54% | 45.2 months |

| Secured | 197,000 | | | 4.10% | 63.1 months |

| | | | |

| Total | $2,062,000 | | 4.49% | 46.9 months |

| | | | |

| | | | | | | | | | | | | | | | | | | | | | | | |

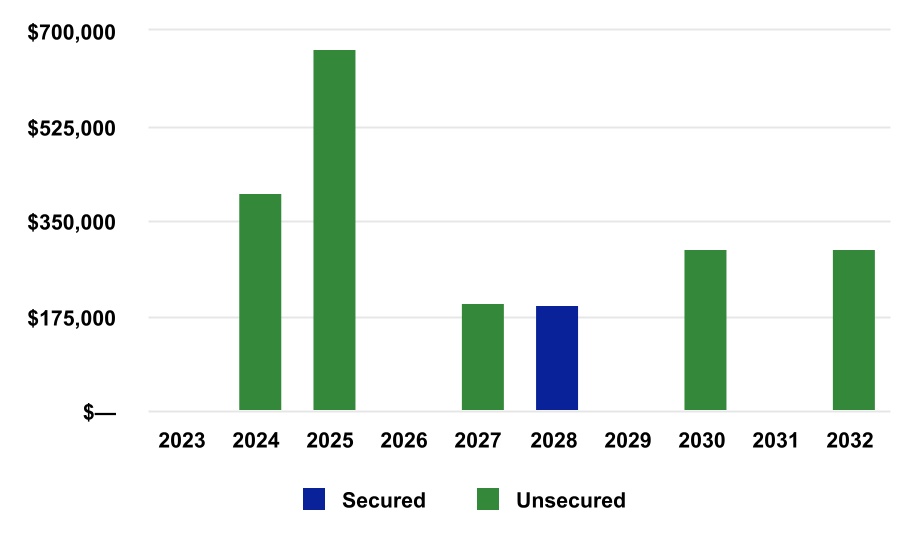

Debt Maturities (4) | |

| Maturity Year | Secured Debt - Principal Amount Outstanding (1) | Unsecured Debt - Principal Amount Outstanding (1) | Weighted Average Stated Interest Rate (2) | Percentage of Total |

| | | | | | | |

| 2023 | $— | | | $— | | | N/A | | —% |

| 2024 | — | | | 400,000 | | | 4.45% | | 19.4% |

| 2025 | — | | | 665,000 | | | 5.58% | | 32.3% |

| 2026 | — | | | — | | | N/A | | —% |

| 2027 | — | | | 200,000 | | | 6.00% | | 9.7% |

| 2028 | 197,000 | | | — | | | 4.10% | | 9.6% |

| 2029 | — | | | — | | | N/A | | —% |

| 2030 | — | | | 300,000 | | | 3.15% | | 14.5% |

| 2031 | — | | | — | | | N/A | | —% |

| 2032 | — | | | 300,000 | | | 2.75% | | 14.5% |

| | | | | | | |

| Total | $197,000 | | $1,865,000 | | 4.49% | | 100.0% |

| | | | | | | |

| | | | | | | |

| | | | | |

| (1) | All of Piedmont's outstanding debt as of June 30, 2023, was interest-only debt or in an interest-only payment period. |

| (2) | Weighted average stated interest rate is calculated based upon the principal amounts outstanding. |

| (3) | The amount of floating rate debt is comprised of the $200 million outstanding balance as of June 30, 2023 on the $600 million unsecured revolving credit facility, the entire principal balance of the $200 million unsecured term loan that closed in 2022, and the entire principal balance of the $215 million unsecured term loan that closed in 2023. |

| (4) | For loans which provide extension options that are conditional solely upon the Company providing proper notice to the loan's administrative agent and the payment of an extension fee, the final extended maturity date is reflected herein. |

Piedmont Office Realty Trust, Inc.

Debt Detail

Unaudited ($ in thousands) | | | | | | | | | | | | | | | | | |

Facility (1) | Property | Stated Rate | Maturity | Principal Amount Outstanding as of June 30, 2023 |

| | | | | |

| Secured | | | | | |

| $197.0 Million Fixed-Rate Mortgage | 1180 Peachtree Street | 4.10 | % | (2) | 10/1/2028 | $ | 197,000 | |

Subtotal / Weighted Average (3) | | 4.10 | % | | | $ | 197,000 | |

| | | | | |

| Unsecured | | | | | |

| $400.0 Million Unsecured 2014 Senior Notes | N/A | 4.45 | % | (4) | 3/15/2024 | 400,000 | |

$215.0 Million Unsecured 2023 Term Loan (5) | N/A | 6.20 | % | (6) | 1/31/2025 | 215,000 | |

| $250.0 Million Unsecured 2018 Term Loan | N/A | 4.54 | % | (7) | 3/31/2025 | 250,000 | |

$200.0 Million Unsecured 2022 Term Loan (8) | N/A | 6.20 | % | (9) | 6/18/2025 | 200,000 | |

$600.0 Million Unsecured Line of Credit (10) | N/A | 6.00 | % | (11) | 6/30/2027 | 200,000 | |

| $300.0 Million Unsecured 2020 Senior Notes | N/A | 3.15 | % | (12) | 8/15/2030 | 300,000 | |

| $300.0 Million Unsecured 2021 Senior Notes | N/A | 2.75 | % | (13) | 4/1/2032 | 300,000 | |

Subtotal / Weighted Average (3) | | 4.54 | % | | | $ | 1,865,000 | |

| | | | | |

Total Debt - Principal Amount Outstanding / Weighted Average Stated Rate (3) | 4.49 | % | | | $ | 2,062,000 | |

GAAP Accounting Adjustments (14) | | | | | (12,764) | |

| Total Debt - GAAP Amount Outstanding | | | | $ | 2,049,236 | |

| | | | | |

| (1) | All of Piedmont’s outstanding debt as of June 30, 2023, was interest-only debt or in an interest-only payment period. |

| (2) | Upon acquiring the property, Piedmont assumed the mortgage. The stated interest rate of the loan was estimated to be an at-market rate as of the date of closing. The loan is interest-only through September 2023; effective October 1, 2023, the loan will begin amortizing based on a 30-year amortization schedule. |

| (3) | Weighted average is based on the principal amounts outstanding and interest rates at June 30, 2023. |

| (4) | The $400 million unsecured senior notes were offered for sale at 99.791% of the principal amount. The resulting effective cost of the financing is approximately 4.48% before the consideration of transaction costs and proceeds from interest rate hedges. After the application of proceeds from interest rate hedges, the effective cost of the financing is approximately 4.10%. |

| (5) | The $215 million unsecured term loan has an initial maturity date of January 31, 2024. There is a one-year extension option available under the facility for a final maturity of January 31, 2025. The final extended maturity date is presented on this schedule. |

| (6) | The $215 million unsecured term loan has a variable interest rate. Piedmont may select from multiple interest rate options, including the prime rate and various SOFR rates. The all-in interest rate associated with each SOFR interest period selection is comprised of the relevant adjusted SOFR rate (comprised of the relevant base SOFR interest rate plus a fixed adjustment of 0.10%) plus a credit spread (1.05% as of June 30, 2023) based on Piedmont's then current credit rating. |

| (7) | The $250 million unsecured term loan has a stated variable interest rate; however, Piedmont entered into various interest rate swap agreements in a total notional amount equal to the size of the facility which effectively fix the interest rate for the term loan (at 4.54% as of June 30, 2023; this rate can change only with a credit rating change for the Company) through the loan's maturity date of March 31, 2025. |

| (8) | The $200 million unsecured term loan has an initial maturity date of December 16, 2024. There is a six-month extension option available under the facility for a final maturity of June 18, 2025. The final extended maturity date is presented on this schedule. |

| (9) | The $200 million unsecured term loan has a variable interest rate. Piedmont may select from multiple interest rate options, including the prime rate and various term SOFR rates. The all-in interest rate associated with each SOFR interest period selection is comprised of the relevant adjusted SOFR rate (comprised of the relevant base SOFR interest rate plus a fixed adjustment of 0.10%) plus a credit spread (1.00% as of June 30, 2023) based on Piedmont's then current credit rating. |

| (10) | All of Piedmont’s outstanding debt as of June 30, 2023 was term debt with the exception of the $200 million balance on our unsecured revolving credit facility. The $600 million unsecured revolving credit facility has an initial maturity date of June 30, 2026; however, there are two, six-month extension options available under the facility providing for a total extension of up to one year to June 30, 2027. The final extended maturity date is presented on this schedule. |

| (11) | The interest rate presented for the $600 million unsecured revolving credit facility is the weighted average interest rate for all outstanding draws as of June 30, 2023. Piedmont may select from multiple interest rate options with each draw under the facility, including the prime rate and various SOFR rates. The all-in interest rate associated with each SOFR interest period selection is comprised of the relevant adjusted SOFR rate (comprised of the relevant base SOFR interest rate plus a fixed adjustment of 0.10%) plus a credit spread (0.85% as of June 30, 2023) based on Piedmont's then current credit rating. |

| (12) | The $300 million unsecured senior notes were offered for sale at 99.236% of the principal amount. The resulting effective cost of the financing is approximately 3.24% before the consideration of transaction costs and the impact of interest rate hedges. After incorporating the results of the related interest rate hedging activity, the effective cost of the financing is approximately 3.90%. |

| (13) | The $300 million unsecured senior notes were offered for sale at 99.510% of the principal amount. The resulting effective cost of the financing is approximately 2.80% before the consideration of transaction costs and the impact of interest rate hedges. After incorporating the results of the related interest rate hedging activity, the effective cost of the financing is approximately 2.78%. |

| (14) | The GAAP accounting adjustments relate to original issue discounts, third-party fees, and lender fees resulting from the procurement processes for our various debt facilities. The original issue discounts and fees are amortized to interest expense over the contractual term of the related debt. |

Piedmont Office Realty Trust, Inc.

Debt Covenant & Ratio Analysis (for Debt Holders)

As of June 30, 2023

Unaudited

| | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended |

Bank Debt Covenant Compliance (1) | Required | 6/30/2023 | 3/31/2023 | 12/31/2022 | 9/30/2022 | 6/30/2022 |

| | | | | | |

| Maximum leverage ratio | 0.60 | 0.37 | 0.38 | 0.39 | 0.40 | 0.35 |

Minimum fixed charge coverage ratio (2) | 1.50 | 3.52 | 3.91 | 4.36 | 4.82 | 5.21 |

| Maximum secured indebtedness ratio | 0.40 | 0.04 | 0.04 | 0.04 | 0.04 | — |

| Minimum unencumbered leverage ratio | 1.60 | 2.66 | 2.64 | 2.56 | 2.46 | 2.87 |

Minimum unencumbered interest coverage ratio (3) | 1.75 | 3.67 | 4.10 | 4.55 | 4.93 | 5.26 |

| | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended |

Bond Covenant Compliance (4) | Required | 6/30/2023 | 3/31/2023 | 12/31/2022 | 9/30/2022 | 6/30/2022 |

| | | | | | |

| Total debt to total assets | 60% or less | 44.8% | 47.1% | 44.0% | 46.8% | 40.9% |

| Secured debt to total assets | 40% or less | 4.3% | 4.2% | 4.3% | 4.3% | —% |

| Ratio of consolidated EBITDA to interest expense | 1.50 or greater | 3.97 | 4.44 | 4.95 | 5.49 | 5.92 |

| Unencumbered assets to unsecured debt | 150% or greater | 223% | 211% | 227% | 212% | 245% |

| | | | | | |

| | | | | | | | | | | | | |

| Three Months Ended | | Six Months Ended | Twelve Months Ended | |

| Other Debt Coverage Ratios for Debt Holders | June 30, 2023 | | June 30, 2023 | December 31, 2022 | |

| | | | | |

Average net principal amount of debt to core EBITDA (5) | 6.4 x | | 6.3 x | 6.0 x | |

Fixed charge coverage ratio (6) | 3.2 x | | 3.3 x | 4.5 x | |

Interest coverage ratio (7) | 3.2 x | | 3.3 x | 4.5 x | |

| | | | | |

| (1) | Bank debt covenant compliance calculations relate to the most restrictive of the specific calculations detailed in the relevant credit agreements. Please refer to such agreements for relevant defined terms. |

| (2) | Defined as EBITDA for the trailing four quarters (including the Company's share of EBITDA from unconsolidated interests), excluding one-time or non-recurring gains or losses, less a $0.15 per square foot capital reserve, and excluding the impact of straight line rent leveling adjustments and amortization of intangibles divided by the Company's share of fixed charges, as more particularly described in the credit agreements. This definition of fixed charge coverage ratio as prescribed by our credit agreements is different from the fixed charge coverage ratio definition employed elsewhere within this report. |

| (3) | Defined as net operating income for the trailing four quarters for unencumbered assets (including the Company's share of net operating income from partially-owned entities and subsidiaries that are deemed to be unencumbered) less a $0.15 per square foot capital reserve divided by the Company's share of interest expense associated with unsecured financings only, as more particularly described in the credit agreements. |

| (4) | Bond covenant compliance calculations relate to specific calculations prescribed in the relevant debt agreements. Please refer to the Indenture dated May 9, 2013, the Indenture and the First Supplemental Indenture dated March 6, 2014, the Second Supplemental Indenture dated August 12, 2020, and the Third Supplemental Indenture dated September 20, 2021 for defined terms and detailed information about the calculations. |

| (5) | For the purposes of this calculation, we use the average daily principal balance of debt outstanding during the identified period, less the average of cash and cash equivalents and escrow deposits and restricted cash as of the end of each month in the relevant period. |

| (6) | Fixed charge coverage ratio is calculated as Core EBITDA divided by the sum of interest expense, principal amortization (none during periods presented), capitalized interest and preferred dividends (none during periods presented). The Company had capitalized interest of $1.4 million for the three months ended June 30, 2023, $2.6 million for the six months ended June 30, 2023, and $4.2 million for the twelve months ended December 31, 2022. |

| (7) | Interest coverage ratio is calculated as Core EBITDA divided by the sum of interest expense and capitalized interest. The Company had capitalized interest of $1.4 million for the three months ended June 30, 2023, $2.6 million for the six months ended June 30, 2023, and $4.2 million for the twelve months ended December 31, 2022. |

Piedmont Office Realty Trust, Inc.

Tenant Diversification (1)

As of June 30, 2023

(in thousands except for number of properties)

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Tenant | Credit Rating (2) | Number of

Properties | Lease Term Remaining (3) | Annualized Lease

Revenue | Percentage of

Annualized Lease

Revenue (%) | Leased

Square Footage | Percentage of

Leased

Square Footage (%) |

| US Bancorp | A / A3 | 3 | 0.9 | | $28,092 | 5.0 | | 787 | 5.5 |

| State of New York | AA+ / Aa1 | 1 | 13.3 | | 25,564 | 4.5 | | 482 | 3.4 |

| Amazon | AA / A1 | 4 | 1.5 | | 16,474 | 2.9 | | 337 | 2.3 |

| City of New York | AA / Aa2 | 1 | 2.9 | | 15,513 | 2.7 | | 313 | 2.2 |

| Microsoft | AAA / Aaa | 2 | 7.9 | | 13,475 | 2.4 | | 355 | 2.5 |

| King & Spalding | No Rating Available | 1 | 7.7 | | 12,628 | 2.2 | | 272 | 1.9 |

| Transocean | CCC / Caa1 | 1 | 12.8 | | 11,392 | 2.0 | | 301 | 2.1 |

| Ryan | No Rating Available | 1 | 2.6 | | 9,344 | 1.6 | | 178 | 1.2 |

| VMware, Inc. | BBB- / Baa3 | 1 | 4.1 | | 8,786 | 1.6 | | 215 | 1.5 |

| Schlumberger Technology | A / A2 | 1 | 5.5 | | 8,106 | 1.4 | | 254 | 1.8 |

| Gartner | BB+ / Ba1 | 2 | 11.0 | | 7,761 | 1.4 | | 207 | 1.4 |

| Salesforce.com | A+ / A2 | 1 | 6.1 | | 7,465 | 1.3 | | 182 | 1.3 |

| Fiserv | BBB / Baa2 | 1 | 4.1 | | 7,373 | 1.3 | | 195 | 1.4 |

| Epsilon Data Management / subsidiary of Publicis | BBB+ / Baa1 | 1 | 3.0 | | 6,905 | 1.2 | | 222 | 1.5 |

| Applied Predictive Technologies / subsidiary of MasterCard | A+ / Aa3 | 1 | 4.9 | | 6,783 | 1.2 | | 133 | 0.9 |

| Eversheds Sutherland | No Rating Available | 1 | 2.8 | | 6,567 | 1.2 | | 180 | 1.2 |

| International Food Policy Research Institute | No Rating Available | 1 | 5.8 | | 6,479 | 1.1 | | 102 | 0.7 |

| Cargill | A / A2 | 1 | 0.5 | | 5,625 | 1.0 | | 268 | 1.9 |

| | | | | | | | | |

| | | | | | | | | |

| | | | | | | | | |

| | | | | | | | | |

| | | | | | | | | |

| Other | | | Various | | 363,232 | 64.0 | | 9,382 | 65.3 |

| Total | | | | | $567,564 | 100.0 | | 14,365 | 100.0 |

| | | | | |

| (1) | This schedule presents all tenants contributing 1.0% or more to Annualized Lease Revenue. |

| (2) | Credit rating may reflect the credit rating of the parent or a guarantor. When available, both the Standard & Poor's credit rating and the Moody's credit rating are provided. The absence of a credit rating for a tenant is not an indication of the creditworthiness of the tenant; in most cases, the lack of a credit rating reflects that the tenant has not sought such a rating. |

| (3) | The metrics presented are the weighted average lease terms remaining in years weighted by Annualized Lease Revenue. |

| |

| |

Piedmont Office Realty Trust, Inc.

Tenant Credit Rating & Lease Distribution Information

As of June 30, 2023

Tenant Credit Rating (1)

| | | | | | | | |

| Rating Level | Annualized

Lease Revenue

(in thousands) | Percentage of

Annualized Lease

Revenue (%) |

| | |

| AAA / Aaa | $22,300 | 3.9 |

| AA / Aa | 71,201 | 12.5 |

| A / A | 76,894 | 13.6 |

| BBB / Baa | 55,063 | 9.7 |

| BB / Ba | 19,400 | 3.4 |

| B / B | 9,290 | 1.6 |

| Below | 18,425 | | 3.3 |

Not rated (2) | 294,991 | 52.0 |

| Total | $567,564 | 100.0 |

| | |

Lease Distribution

| | | | | | | | | | | | | | | | | | | | |

| Lease Size | Number of Leases | Percentage of

Leases (%) | Annualized

Lease Revenue

(in thousands) | Percentage of

Annualized Lease

Revenue (%) | Leased

Square Footage

(in thousands) | Percentage of

Leased

Square Footage (%) |

| | | | | | |

| 2,500 or Less | 360 | 36.9 | $24,746 | 4.4 | 245 | | 1.7 |

| 2,501 - 10,000 | 348 | 35.6 | 69,711 | 12.3 | 1,797 | | 12.5 |

| 10,001 - 20,000 | 102 | 10.4 | 53,096 | 9.3 | 1,396 | | 9.7 |

| 20,001 - 40,000 | 90 | 9.2 | 94,480 | 16.6 | 2,438 | | 17.0 |

| 40,001 - 100,000 | 48 | 4.9 | 116,292 | 20.5 | 2,963 | | 20.6 |

| Greater than 100,000 | 29 | 3.0 | 209,239 | 36.9 | 5,526 | | 38.5 |

| Total | 977 | 100.0 | $567,564 | 100.0 | 14,365 | | 100.0 |

| | | | | | |

| | | | | |

| (1) | Credit rating may reflect the credit rating of the parent or a guarantor. Where differences exist between the Standard & Poor's credit rating for a tenant and the Moody's credit rating for a tenant, the higher credit rating is selected for this analysis. |

| (2) | The classification of a tenant as "not rated" is not an indication of the creditworthiness of the tenant; in most cases, the lack of a credit rating reflects that the tenant has not sought such a rating. Included in this category are such tenants as Piper Sandler, Ernst & Young, KPMG, BDO, and RaceTrac Petroleum. |

Piedmont Office Realty Trust, Inc.

Leased Percentage Information

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended | | Three Months Ended | |

| | June 30, 2023 | | June 30, 2022 | |

| | Leased Square Footage | Rentable Square Footage | Percent Leased (1) | | Leased Square Footage | Rentable Square Footage | Percent Leased (1) | |

| As of March 31, 20xx | 14,352 | | 16,674 | | 86.1 | % | | 14,026 | | 16,126 | | 87.0 | % | |

| | | | | | | | | |

| | | | | | | | | |

| Leases signed during the period | 581 | | | | | 724 | | | | |

| Less: | | | | | | | | |

| Lease renewals signed during period | (345) | | | | | (491) | | | | |

| New leases signed during period for currently occupied space | (64) | | | | | (36) | | | | |

| Leases expired during period and other | (159) | | (2) | | | | (194) | | 3 | | | |

| Subtotal | 14,365 | | 16,672 | | 86.2 | % | | 14,029 | | 16,129 | | 87.0 | % | |

| Acquisitions and properties placed in service during period (2) | — | | — | | | | — | | — | | | |

| Dispositions and properties taken out of service during period (2) | — | | — | | | | — | | — | | | |

| As of June 30, 20xx | 14,365 | | 16,672 | | 86.2 | % | | 14,029 | | 16,129 | | 87.0 | % | |

| | | | | | | | | |

| | | | | | | | | |

| | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | |

| | Six Months Ended | | Six Months Ended | |

| | June 30, 2023 | | June 30, 2022 | |

| | Leased Square Footage | Rentable Square Footage | Percent Leased (1) | | Leased Square Footage | Rentable Square Footage | Percent Leased (1) | |

| As of December 31, 20xx | 14,440 | | 16,658 | | 86.7 | % | | 14,583 | | 17,051 | | 85.5 | % | |

| | | | | | | | | |

| | | | | | | | | |

| Leases signed during the period | 1,125 | | | | | 1,276 | | | | |

| Less: | | | | | | | | |

| Lease renewals signed during period | (619) | | | | | (800) | | | | |

| New leases signed during period for currently occupied space | (110) | | | | | (56) | | | | |

| Leases expired during period and other | (471) | | 14 | | | | (368) | | 3 | | | |

| Subtotal | 14,365 | | 16,672 | | 86.2 | % | | 14,635 | | 17,054 | | 85.8 | % | |

| Acquisitions and properties placed in service during period (2) | — | | — | | | | — | | — | | | |

| Dispositions and properties taken out of service during period (2) | — | | — | | | | (606) | | (925) | | | |

| As of June 30, 20xx | 14,365 | | 16,672 | | 86.2 | % | | 14,029 | | 16,129 | | 87.0 | % | |

| | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Same Store Analysis | | | | | | | | |

| Less acquisitions / dispositions after June 30, 2022 and developments / out-of-service redevelopments (2) (3) | (664) | | (691) | | 96.1 | % | | (170) | | (174) | | 97.7 | % | |

| Same Store Leased Percentage | 13,701 | | 15,981 | | 85.7 | % | | 13,859 | | 15,955 | | 86.9 | % | |

| | | | | | | | | |

| | | | | |

| (1) | Calculated as square footage associated with commenced leases as of period end with the addition of square footage associated with uncommenced leases for spaces vacant as of period end at our in-service properties, divided by total rentable in-service square footage as of period end, expressed as a percentage. |

| (2) | For additional information on acquisitions and dispositions completed during the last year and current developments and out-of-service redevelopments, please refer to pages 31 and 32, respectively. |