Exhibit 99.2

Quarterly Supplemental Information

June 30, 2012

| | | | |

| Corporate Headquarters | | Institutional Analyst Contact | | Investor Relations |

| | |

| 11695 Johns Creek Parkway, Suite 350 | | Telephone: 770.418.8592 | | Telephone: 866.354.3485 |

| Johns Creek, GA 30097 | | research.analysts@piedmontreit.com | | investor.services@piedmontreit.com |

| Telephone: 770.418.8800 | | | | www.piedmontreit.com |

Piedmont Office Realty Trust, Inc.

Quarterly Supplemental Information

Index

| | |

| | | Page |

| |

Introduction | | |

Corporate Data | | 3 |

Investor Information | | 4 |

Financial Highlights | | 5-8 |

Key Performance Indicators | | 9 |

| |

Financials | | |

Balance Sheet | | 10 |

Income Statements | | 11-12 |

Funds From Operations / Adjusted Funds From Operations | | 13 |

Same Store Analysis | | 14-15 |

Capitalization Analysis | | 16 |

Debt Summary | | 17 |

Debt Detail | | 18 |

Debt Analysis | | 19 |

| |

Operational & Portfolio Information - Office Investments | | |

Tenant Diversification | | 20 |

Tenant Credit Rating & Lease Distribution Information | | 21 |

Leased Percentage Information | | 22 |

Rental Rate Roll Up / Roll Down Analysis | | 23 |

Lease Expiration Schedule | | 24 |

Quarterly Lease Expirations | | 25 |

Annual Lease Expirations | | 26 |

Capital Expenditures & Commitments | | 27 |

Contractual Tenant Improvements & Leasing Commissions | | 28 |

Geographic Diversification | | 29 |

Geographic Diversification by Location Type | | 30 |

Industry Diversification | | 31 |

Property Investment Activity | | 32 |

Value-Add Activity | | 33 |

| |

Other Investments | | |

Other Investments Detail | | 34 |

| |

Supporting Information | | |

Definitions | | 35-36 |

Research Coverage | | 37 |

Non-GAAP Reconciliations & Other Detail | | 38-41 |

Property Detail | | 42-43 |

Risks, Uncertainties and Limitations | | 44 |

Notice to Readers:

Please refer to page 44 for a discussion of important risks related to the business of Piedmont Office Realty Trust, Inc., as well as an investment in its securities, including risks that could cause actual results and events to differ materially from results and events referred to in the forward-looking information. Considering these risks, uncertainties, assumptions, and limitations, the forward-looking statements about leasing, financial operations, leasing prospects, etc. contained in this supplemental reporting package might not occur.

Certain prior period amounts have been reclassified to conform to the current period financial statement presentation. In addition, many of the schedules herein contain rounding to the nearest thousands or millions and, therefore, the schedules may not total due to this rounding convention. When the Company sells properties, it restates historical income statements with the financial results of the sold assets presented in discontinued operations.

Piedmont Office Realty Trust, Inc.

Corporate Data

Piedmont Office Realty Trust, Inc. (also referred to herein as “Piedmont” or the “Company”) (NYSE: PDM) is a fully-integrated and self-managed real estate investment trust (“REIT”) specializing in the acquisition, ownership, management, development and disposition of primarily high-quality Class A office buildings located predominantly in large U.S. office markets and leased principally to high-credit-quality tenants. Approximately 82% of our Annualized Lease Revenue (“ALR”)(1) is derived from our office properties located within the ten largest U.S. office markets, including Chicago, Washington, D.C., the New York metropolitan area, Boston and greater Los Angeles. Since its first acquisition in 1998, the Company has acquired $5.9 billion of office and industrial properties (inclusive of joint ventures) through June 30, 2012. Rated as an investment-grade company by Standard & Poor’s and Moody’s, Piedmont has maintained a low-leverage strategy while acquiring its properties.

This data supplements the information provided in our reports filed with the Securities and Exchange Commission and should be reviewed in conjunction with such filings.

| | | | | | | | | | |

| | | As of

June 30, 2012 | | | | | As of

December 31, 2011 | |

| | | |

Number of consolidated office properties (2) | | | 74 | | | | | | 79 | |

Rentable square footage (in thousands) (2) | | | 20,482 | | | | | | 20,942 | |

Percent leased (3) | | | 85.0% | | | | | | 86.5% | |

Percent leased - stabilized portfolio(4) | | | 88.1% | | | | | | 89.1% | |

Capitalization (in thousands): | | | | | | | | | | |

Total debt - principal amount outstanding | | | $1,400,525 | | | | | | $1,472,525 | |

Equity market capitalization(5) | | | $2,929,741 | | | | | | $2,941,611 | |

Total market capitalization(5) | | | $4,330,266 | | | | | | $4,414,136 | |

Total debt / Total market capitalization | | | 32.3% | | | | | | 33.4% | |

Total debt / Total gross assets | | | 26.7% | | | | | | 27.5% | |

Common stock data | | | | | | | | | | |

High closing price during quarter | | | $17.80 | | | | | | $17.50 | |

Low closing price during quarter | | | $16.19 | | | | | | $15.42 | |

Closing price of common stock at period end | | | $17.21 | | | | | | $17.04 | |

Weighted average fully diluted shares outstanding (in thousands) (6) | | | 172,520 | | | | | | 172,981 | |

Shares of common stock issued and outstanding (in thousands) | | | 170,235 | | | | | | 172,630 | |

Rating / outlook | | | | | | | | | | |

Standard & Poor’s | | | BBB / Stable | | | | | | BBB / Stable | |

Moody’s | | | Baa2 / Stable | | | | | | Baa2 / Stable | |

Employees | | | 118 | | | | | | 116 | |

| (1) | The definition for Annualized Lease Revenue can be found on page 35. |

| (2) | As of June 30, 2012, our consolidated office portfolio consisted of 74 properties (exclusive of our equity interests in five properties owned through unconsolidated joint ventures and our two industrial properties). During the first quarter of 2012, we sold our portfolio of assets in Portland, OR, comprised of four office properties totaling 326,000 square feet and developable land totaling 18.2 acres. During the second quarter of 2012, we sold 26200 Enterprise Way, a 145,000 square foot office building located in Lake Forest, CA, and we purchased approximately 2.0 acres of developable land in Atlanta, GA. For additional detail on asset transactions during 2012, please refer to page 32. |

| (3) | Calculated as leased square footage on June 30, 2012 plus square footage associated with executed new leases for currently vacant spaces divided by total rentable square footage (defined in note 2 above), expressed as a percentage. This measure is presented for our 74 consolidated office properties and excludes industrial and unconsolidated joint venture properties. Please refer to page 22 for additional analyses regarding Piedmont’s leased percentage. |

| (4) | Please refer to page 33 for information regarding value-add properties, data for which is removed from stabilized portfolio totals. The first six months of 2012 reflect the disposition of five well-leased properties totaling 470,000 square feet. Our dispositions of well-leased assets during the previous three quarters have resulted in a decrease in leased percentage; if those assets were not sold, our stabilized leased percentage would have been 88.9% as of June 30, 2012 as compared to 89.7% as of December 31, 2011. |

| (5) | Based on a share price of $17.21 as of June 29, 2012. |

| (6) | Weighted average fully diluted shares outstanding are presented on a year-to-date basis for each period. |

3

Piedmont Office Realty Trust, Inc.

Investor Information

Corporate

11695 Johns Creek Parkway, Suite 350, Johns Creek, Georgia 30097

770.418.8800

www.piedmontreit.com

Executive Management

| | | | |

| | |

| Donald A. Miller, CFA | | Robert E. Bowers | | Laura P. Moon |

Chief Executive Officer, President and Director | | Chief Financial Officer, Executive Vice President, Secretary, and Treasurer | | Chief Accounting Officer and Senior Vice President |

| | |

| Raymond L. Owens | | Carroll A. Reddic, IV | | |

Executive Vice President - Capital Markets | | Executive Vice President - Real Estate Operations, Assistant Secretary | | |

Board of Directors

| | | | |

| | |

| W. Wayne Woody | | Frank C. McDowell | | Donald A. Miller, CFA |

Director, Chairman of the Board of Directors and Chairman of Audit Committee | | Director and Vice Chairman of the Board of Directors | | Chief Executive Officer, President and Director |

| | |

| Michael R. Buchanan | | Wesley E. Cantrell | | Donald S. Moss |

Director and Chairman of Capital Committee | | Director and Chairman of Governance Committee | | Director and Chairman of Compensation Committee |

| | |

| William H. Keogler, Jr. | | Raymond G. Milnes, Jr. | | Jeffery L. Swope |

| Director | | Director | | Director |

| | | | |

Transfer Agent | | | | Corporate Counsel |

| | |

| Computershare | | | | King & Spalding |

P.O. Box 358010 Pittsburgh, PA 15252-8010 Phone: 866.354.3485 | | | | 1180 Peachtree Street, NE Atlanta, GA 30309 Phone: 404.572.4600 |

4

Piedmont Office Realty Trust, Inc.

Financial Highlights

As of June 30, 2012

|

Financial Results(1) |

- Funds from operations (FFO) for the quarter ended June 30, 2012 was $60.3 million, or $0.35 per share (diluted), compared to $65.1 million, or $0.38 per share (diluted), for the same quarter in 2011. FFO for the six months ended June 30, 2012 was $120.3 million, or $0.70 per share (diluted), compared to $136.4 million, or $0.79 per share (diluted), for the same period in 2011. The decrease in FFO for both the three months and the six months ended June 30, 2012 as compared to the same periods in 2011 was principally related to the following factors: 1) decreased operating income due to the disposition of certain assets with meaningful operating income contributions, notably 35 West Wacker Drive, offset somewhat by operating income contributions from newly acquired assets, 2) lower overall occupancy in 2012 as compared to 2011, and 3) reduced termination fee income of $1.3 million and $4.5 million, respectively, for the three and six months ended June 30, 2012 as compared to 2011. The reduction in FFO in 2012 as compared to 2011 was also offset somewhat by reduced General & Administrative expenses, related primarily to lower legal expense and lower deferred stock compensation expense, and reduced interest expense attributable to decreased total debt outstanding due to the repayment of several loans during the last twelve months. - Core funds from operations (Core FFO) for the quarter ended June 30, 2012 was $60.4 million, or $0.35 per share (diluted), compared to $65.8 million, or $0.38 per share (diluted), for the same quarter in 2011. Core FFO for the six months ended June 30, 2012 was $120.4 million, or $0.70 per share (diluted), compared to $137.1 million, or $0.79 per share (diluted), for the same period in 2011. The decrease in Core FFO for the three months and the six months ended June 30, 2012 as compared to the same periods in 2011 was principally related to the items described for changes in FFO above. - Adjusted funds from operations (AFFO) for the quarter ended June 30, 2012 was $36.2 million, or $0.21 per share (diluted), compared to $50.6 million, or $0.29 per share (diluted), for the same quarter in 2011. AFFO for the six months ended June 30, 2012 was $86.3 million, or $0.50 per share (diluted), compared to $106.9 million, or $0.62 per share (diluted), for the same period in 2011. The decrease in AFFO for the three months ended June 30, 2012 as compared to the same period in 2011 was primarily related to the items described above for the FFO variance, as well as increased rental abatements associated with newly commenced leases in 2012 as compared to 2011, and an increase in non-incremental capital expenditures in 2012 as compared to 2011. The decrease in AFFO for the six months ended June 30, 2012 as compared to the same period in 2011 was primarily related to the items described above for the FFO variance, as well as increased rental abatements associated with newly commenced leases in 2012 as compared to 2011, offset somewhat by a decrease in non-incremental capital expenditures in 2012 as compared to 2011. - During the quarter ended June 30, 2012, the Company paid to shareholders a quarterly dividend in the amount of $0.20 per share for its common stock. The Company’s dividend payout percentage for the six months ended June 30, 2012 was 57.3% of Core FFO and 79.9% of AFFO. |

|

Operations |

- On a square footage leased basis, our total office portfolio was 85.0% leased as of June 30, 2012, as compared to 86.5% as of December 31, 2011 and 84.4% as of March 31, 2012. On a stabilized square footage leased basis, our portfolio was 88.1% leased as of June 30, 2012. The stabilized leased percentage excludes the impact of value-add acquisitions completed in 2010 and 2011 (see page 33) that have not yet reached stabilization, including 500 West Monroe Street in Chicago, IL, The Medici in Atlanta, GA, Suwanee Gateway One in Suwanee, GA, and 400 TownPark in Lake Mary, FL. During the last year, our same store stabilized leased percentage declined from 88.5% at June 30, 2011 to 87.9% at June 30, 2012. The primary reason for the decline in the leased rate for our same store stabilized assets during that period is negative net absorption associated with several recent lease expirations (after taking into account leases signed to backfill the affected spaces), including space at 200 Bridgewater Crossing in Bridgewater, NJ associated with the sanofi-aventis lease expiration and at Aon Center in Chicago, IL associated with the Kirkland & Ellis lease expiration. Please refer to page 22 for additional leased percentage information. - The weighted average remaining lease term of our portfolio was 6.5 years(2) as of June 30, 2012 as compared to 6.4 years at December 31, 2011. - During the three months ended June 30, 2012, the Company completed 595,000 square feet of total leasing. Of the total office leasing activity during the quarter, we signed renewal leases for 234,000 square feet and new tenant leases for 362,000 square feet. No leases were signed for our industrial or joint venture assets during the quarter. During the first half of the year, we completed 1,041,000 square feet of leasing for our consolidated office properties and 1,414,000 square feet of leasing inclusive of activity associated with our industrial and unconsolidated joint venture assets. The average committed capital cost for leases signed during the first half of the year at our consolidated office properties was $4.75 per square foot per year of lease term. Average committed capital cost per square foot per year of lease term for renewal leases signed during the six months ended June 30, 2012 was $2.48 and average committed capital cost per square foot per year of lease term for new leases signed during the same time period was $5.83 (see page 28). |

(1) FFO, Core FFO and AFFO are supplemental non-GAAP financial measures. See pages 35-36 for definitions of non-GAAP financial measures. See pages 13 and 38 for reconciliations of FFO, Core FFO and AFFO to Net Income. (2) Remaining lease term (after taking into account leases for vacant spaces which had been executed but not commenced as of June 30, 2012) is weighted based on Annualized Lease Revenue, as defined on page 35. |

5

Piedmont Office Realty Trust, Inc.

Financial Highlights

As of June 30, 2012

| | - | During the three months ended June 30, 2012, we executed six leases greater than 20,000 square feet. Please see information on those leases listed below. |

| | | | | | | | | | | | |

| Tenant Name | | Property | | Property Location | | Square Feet

Leased | | | | Expiration Year | | Lease Type |

| Piper Jaffray & Co. | | US Bancorp Center | | Minneapolis, MN | | 123,882 | | | | 2025 | | New (former sub-tenant) |

Brother International Corporation | | 200 Bridgewater Crossing | | Bridgewater, NJ | | 101,724 | | | | 2023 | | New |

HD Vest | | Las Colinas Corporate Center I | | Irving, TX | | 81,069 | | | | 2023 | | Renewal |

| Dendreon Corporation | | 200 Bridgewater Crossing | | Bridgewater, NJ | | 39,937 | | | | 2023 | | New |

Global Knowledge Training, LLC | | Windy Point I | | Schaumburg, IL | | 22,028 | | | | 2020 | | Renewal / Expansion |

Comptroller of the Currency | | 400 Virginia Avenue | | Washington, DC | | 21,042 | | | | 2017 | | Renewal |

Leasing Update

| | - | As of March 31, 2012, there were three tenants whose leases contributed greater than 1% to our Annualized Lease Revenue and were scheduled to expire during the second quarter of 2012 or the eighteen month period following the end of the second quarter of 2012. Information regarding the leasing status of the spaces associated with those tenants’ leases is presented below. |

| | | | | | | | | | | | |

| Tenant Name | | Property | | Property Location | | Square

Footage (1) | | Percentage of Current

Quarter Annualized Lease

Revenue (%) | | Expiration (2) | | Current Leasing Status |

United States of America (National Park Service) | | 1201 Eye Street | | Washington, D.C. | | 219,750 | | 1.9% | | Q3 2012 | | The Company is awaiting the release of the Congressionally-approved solicitation for offers from the GSA, a key component of the Government’s space acquisition process. National Park Service is now in holdover status. The Company anticipates that the National Park Service will remain in holdover in its existing space while the GSA negotiates the National Park Service’s future lease. |

| Comptroller of the Currency | | One

Independence

Square | | Washington, D.C. | | 333,815 | | 3.7% | | Q1 2013 | | The tenant is expected to vacate at lease expiration. The Company is actively marketing the space for lease. |

| BP | | Aon Center | | Chicago, IL | | 776,359 | | 5.9% | | Q4 2013 | | Lease negotiations with the primary sublessee, Aon Corporation, are near completion. Aon is expected to lease approximately 400,000 square feet on a direct basis with no downtime between the expiration of the BP lease and the commencement of the Aon lease. Additionally, long-term leases comprising approximately 37% of the square footage leased by BP have been entered into with: Thoughtworks, Integrys Energy Group, and Federal Home Loan Bank. After the execution of the Aon lease, leases comprising approximately 88% of the square footage leased by BP will have been signed. |

(1)Square footage represents the total square footage leased by the tenant at the building expiring during the expiration quarter.

(2)The lease expiration date presented is that of the majority of the space leased to the tenant at the building.

6

Piedmont Office Realty Trust, Inc.

Financial Highlights

As of June 30, 2012

| | - | Piedmont typically signs leases several months in advance of their anticipated lease commencement dates. Presented below is a schedule of uncommenced leases greater than 50,000 square feet and their anticipated commencement dates. Lease renewals are excluded from this schedule. |

| | | | | | | | | | | | | | |

| Tenant Name | | Property | | Property Location | | Square Feet

Leased | | | | Space Status | | Estimated

Commencement Date | | New / Expansion |

| KPMG | | Aon Center | | Chicago, IL | | 239,189 | | | | Vacant | | Q3 2012 | | New |

United Healthcare Services, Inc. | | Aon Center | | Chicago, IL | | 55,059 | | | | Vacant | | Q3 2012 | | New |

GE(1) | | 500 West Monroe Street | | Chicago, IL | | 86,028 | | | | Vacant | | Q4 2012 - Q4 2014 | | Expansion |

| Brother International Corporation | | 200 Bridgewater Crossing | | Bridgewater, NJ | | 101,724 | | | | Vacant | | Q1 2013 | | New |

Thoughtworks, Inc. | | Aon Center | | Chicago, IL | | 52,529 | | | | Not Vacant | | Q4 2013 | | New |

Federal Home Loan Bank of Chicago | | Aon Center | | Chicago, IL | | 79,054 | | | | Not Vacant | | Q4 2013 | | New |

Integrys Business Support, LLC | | Aon Center | | Chicago, IL | | 159,432 | | | | Not Vacant | | Q2 2014 | | New |

Piper Jaffray & Co. | | US Bancorp Center | | Minneapolis, MN | | 123,882 | | | | Not Vacant | | Q2 2014 | | New |

(1) The square footage presented includes the 19th floor premises, which is leased through fourth quarter 2012. GE is required to lease that space one year after the commencement of the renewal term.

Occupancy versus NOI Analysis

| | - | Piedmont has been in a period of high lease rollover since 2010. This high lease rollover has resulted in a decrease in leased percentage and economic leased percentage. This, in turn, has effected a lower Same Store NOI than might otherwise be anticipated given the overall leased percentage and the historical relationship between leased percentage and Same Store NOI. The decreased economic leased percentage is attributable to two factors: |

1) leases which have been contractually entered into for currently vacant space which have not commenced (amounting to approximately 600,000 square feet of leases as of June 30, 2012, or 2.8% of the office portfolio); and

2) leases which have commenced but the tenants have not commenced paying full rent due to rental abatements (amounting to 1.3 million square feet of leases as of June 30, 2012, or a 4.7% impact to leased percentage on an economic basis).

As the executed but not commenced leases become effective and as the rental abatement periods expire, there will be greater Same Store NOI growth than might otherwise be expected based on changes in overall leased percentage alone during that time period.

Financing and Capital Activity

| | - | As of June 30, 2012, our ratio of debt to total gross assets was 26.7%, our ratio of debt to gross real estate assets was 30.7%, and our ratio of debt to total market capitalization was 32.3%. These debt ratios are based on total principal amount outstanding for our various loans at June 30, 2012. |

| | - | On May 31, 2012, Piedmont completed the sale of 26200 Enterprise Way, a 144,906 square foot office building located in Lake Forest, CA. The property was sold for $28.25 million, or $195 per square foot. Piedmont recorded a gain on the sale of the asset of approximately $10 million. The sale allowed the Company to divest a two-story property that was not deemed to be consistent with its long-term strategic objectives for location and building quality. |

| | - | On June 28, 2012, Piedmont completed the purchase of approximately 2.0 acres of land adjacent to The Medici, one of the Company’s recent value-add acquisitions, in Atlanta, GA. The site is commonly referred to as Gavitello by brokers. Located within the Buckhead area of Atlanta, the site is part of a mixed-use, high-end office and residential complex. The site is zoned for office development and will accommodate a building consisting of approximately 250,000 square feet. The acquisition adds to the Company’s developable land holdings and allows the Company to control a site that is directly competitive to The Medici. |

| | - | On May 1, 2012, Piedmont repaid a $45 million loan secured by 4250 North Fairfax Drive in Arlington, VA. The loan was open to prepayment without any yield maintenance requirements. The repayment of the loan allowed Piedmont to further its strategic objective of decreasing its secured debt borrowings in relation to its total borrowings. |

| | - | On May 2, 2012, the Board of Directors of Piedmont declared dividends for the second quarter of 2012 in the amount of $0.20 per common share outstanding to stockholders of record as of the close of business on June 1, 2012. The dividends were paid on June 22, 2012. |

7

Piedmont Office Realty Trust, Inc.

Financial Highlights

As of June 30, 2012

| | - | During the second quarter of 2012, the Company repurchased approximately 2.6 million shares of common stock at an average purchase price of $16.66 per share, or approximately $42.8 million in aggregate (before consideration of transaction costs). Since the stock repurchase program’s inception last fall, the Company has repurchased a total of 2.8 million shares at an average price of $16.62 per share, or approximately $46.1 million in aggregate (before consideration of transaction costs). Any future repurchases of the Company’s common stock will be made at the discretion of the Company. As of quarter end, there was Board-approved capacity for additional repurchases totaling approximately $250 million under the stock repurchase plan. |

| | - | The ongoing shareholder litigation is awaiting the judge’s ruling on our motion to dismiss the one remaining item in the case. Piedmont believes that the case is without merit and intends to continue to vigorously defend. See Piedmont’s Form 10-Q dated as of June 30, 2012 for further disclosure. |

Subsequent Events

| | - | Piedmont is close to finalizing a new $500 million unsecured revolving credit facility. The terms of the facility will be provided after the transaction has closed. The Company’s current revolver will be terminated prior to the effectiveness of the transaction. |

| | - | On August 1, 2012, the Board of Directors of Piedmont declared dividends for the third quarter of 2012 in the amount of $0.20 per common share outstanding to stockholders of record as of the close of business on August 31, 2012. The dividends are to be paid on September 21, 2012. |

Guidance for 2012

| | - | The following financial guidance for calendar year 2012 remains unchanged and is based on management’s expectations at this time: |

| | |

| | | Low High |

Core Funds from Operations | | $234 - $250 million |

Core Funds from Operations per diluted share | | $1.35 - $1.45 |

These estimates reflect management’s view of current market conditions and incorporate certain economic and operational assumptions and projections, including the disposition of 35 West Wacker Drive which contributed approximately $0.13 per share of funds from operations in 2011. Actual results could differ from these estimates. Note that individual quarters may fluctuate on both a cash and an accrual basis due to the timing of lease commencements and expirations, repairs and maintenance, capital expenditures, capital markets activities and one-time revenue or expense events. In addition, the Company’s guidance is based on information available to management as of the date of this supplemental report.

8

Piedmont Office Realty Trust, Inc.

Key Performance Indicators

Unaudited (in thousands except for per share data)

This section of our supplemental report includes non-GAAP financial measures, including, but not limited to, Core Earnings Before Interest, Taxes, Depreciation, and Amortization (Core EBITDA), Funds from Operations (FFO), Core Funds from Operations (Core FFO), and Adjusted Funds from Operations (AFFO). Definitions of these non-GAAP measures are provided on pages 35-36 and reconciliations are provided on pages 38-40.

| | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended | |

Selected Operating Data | | 6/30/2012 | | | 3/31/2012 | | | 12/31/2011 | | | 9/30/2011 | | | 6/30/2011 | |

| | | | | |

Percent leased (1) | | | 85.0% | | | | 84.4% | | | | 86.5% | | | | 86.4% | | | | 86.5% | |

| | | | | |

Percent leased - stabilized portfolio (1) (2) | | | 88.1% | | | | 87.5% | | | | 89.1% | | | | 88.8% | | | | 89.0% | |

| | | | | |

Rental income | | | $105,992 | | | | $105,282 | | | | $105,982 | | | | $104,460 | | | | $103,205 | |

| | | | | |

Total revenues | | | $133,716 | | | | $132,697 | | | | $135,992 | | | | $132,805 | | | | $135,555 | |

| | | | | |

Total operating expenses | | | $97,840 | | | | $98,111 | | | | $103,509 | | | | $96,386 | | | | $100,034 | |

| | | | | |

Real estate operating income | | | $35,876 | | | | $34,586 | | | | $32,483 | | | | $36,419 | | | | $35,521 | |

| | | | | |

Core EBITDA | | | $76,327 | | | | $76,680 | | | | $82,523 | | | | $86,941 | | | | $84,729 | |

| | | | | |

Core FFO | | | $60,356 | | | | $60,043 | | | | $65,270 | | | | $69,203 | | | | $65,843 | |

| | | | | |

Core FFO per share - diluted | | | $0.35 | | | | $0.35 | | | | $0.38 | | | | $0.40 | | | | $0.38 | |

| | | | | |

AFFO | | | $36,216 | | | | $50,113 | | | | $44,728 | | | | $50,988 | | | | $50,578 | |

| | | | | |

AFFO per share - diluted | | | $0.21 | | | | $0.29 | | | | $0.26 | | | | $0.29 | | | | $0.29 | |

| | | | | |

Gross dividends | | | $34,418 | | | | $34,526 | | | | $54,441 | | | | $54,441 | | | | $54,440 | |

| | | | | |

Dividends per share | | | $0.200 | | | | $0.200 | | | | $0.315 | | | | $0.315 | | | | $0.315 | |

| | | | | |

Selected Balance Sheet Data | | | | | | | | | | | | | | | |

| | | | | |

Total real estate assets | | | $3,638,101 | | | | $3,657,677 | | | | $3,704,051 | | | | $3,926,638 | | | | $3,899,639 | |

| | | | | |

Total gross real estate assets | | | $4,558,128 | | | | $4,590,544 | | | | $4,615,812 | | | | $4,875,854 | | | | $4,828,700 | |

| | | | | |

Total assets | | | $4,328,308 | | | | $4,326,698 | | | | $4,447,834 | | | | $4,613,118 | | | | $4,560,206 | |

| | | | | |

Net debt (3) | | | $1,325,610 | | | | $1,298,738 | | | | $1,323,796 | | | | $1,600,650 | | | | $1,583,812 | |

| | | | | |

Total liabilities | | | $1,601,568 | | | | $1,550,040 | | | | $1,674,406 | | | | $1,896,195 | | | | $1,838,983 | |

| | | | | |

Ratios | | | | | | | | | | | | | | | |

| | | | | |

Core EBITDA margin(4) | | | 56.9% | | | | 57.1% | | | | 55.8% | | | | 59.8% | | | | 56.1% | |

| | | | | |

Fixed charge coverage ratio(5) | | | 4.8 x | | | | 4.6 x | | | | 4.7 x | | | | 4.9 x | | | | 4.4 x | |

| | | | | |

Net debt to core EBITDA (6) (7) | | | 4.3 x | | | | 4.2 x | | | | 4.0 x | | | | 4.6 x | | | | 4.7 x | |

(1) Please refer to page 22 for additional leased percentage information.

(2) Please refer to page 33 for additional information on value-add properties, data for which is removed from stabilized portfolio totals.

(3)Net debt is calculated as the total principal amount of debt outstanding minus cash and cash equivalents and escrow deposits and restricted cash. The decrease in net debt during the fourth quarter of 2011 was primarily attributable to the application of proceeds from the sale of 35 West Wacker Drive.

(4)Core EBITDA margin is calculated as Core EBITDA divided by total revenues (including revenues associated with discontinued operations).

(5) The fixed charge coverage ratio is calculated as Core EBITDA divided by the sum of interest expense, principal amortization, capitalized interest and preferred dividends. The Company had no capitalized interest, principal amortization or preferred dividends during any of the periods presented.

(6) The Company’s net debt declined during the fourth quarter of 2011 with the application of the proceeds from the sale of 35 West Wacker Drive, thereby positively affecting the net debt to core EBITDA ratios.

(7)Core EBITDA is annualized for the purposes of this calculation.

9

Piedmont Office Realty Trust, Inc.

Consolidated Balance Sheets

Unaudited (in thousands)

| | | | | | | | | | | | | | | | | | | | |

| | | June 30, 2012 | | | March 31, 2012 | | | December 31, 2011 | | | September 30, 2011 | | | June 30, 2011 | |

Assets: | | | | | | | | | | | | | | | | | | | | |

Real estate, at cost: | | | | | | | | | | | | | | | | | | | | |

Land assets | | $ | 629,476 | | | $ | 631,745 | | | $ | 640,196 | | | $ | 693,229 | | | $ | 693,962 | |

Buildings and improvements | | | 3,754,954 | | | | 3,750,475 | | | | 3,759,596 | | | | 3,930,126 | | | | 3,894,258 | |

Buildings and improvements, accumulated depreciation | | | (837,285) | | | | (813,679) | | | | (792,342) | | | | (807,917) | | | | (792,881) | |

Intangible lease asset | | | 149,544 | | | | 191,599 | | | | 198,667 | | | | 232,973 | | | | 225,182 | |

Intangible lease asset, accumulated amortization | | | (82,742) | | | | (119,188) | | | | (119,419) | | | | (141,299) | | | | (136,180) | |

Construction in progress | | | 24,154 | | | | 16,725 | | | | 17,353 | | | | 19,526 | | | | 15,298 | |

| | | | | | | | | | | | | | | | | | | | |

Total real estate assets | | | 3,638,101 | | | | 3,657,677 | | | | 3,704,051 | | | | 3,926,638 | | | | 3,899,639 | |

Investment in unconsolidated joint ventures | | | 37,580 | | | | 37,901 | | | | 38,181 | | | | 38,391 | | | | 41,271 | |

Cash and cash equivalents | | | 26,869 | | | | 28,679 | | | | 139,690 | | | | 16,128 | | | | 21,404 | |

Tenant receivables, net of allowance for doubtful accounts | | | 22,884 | | | | 24,932 | | | | 24,722 | | | | 32,066 | | | | 31,143 | |

Straight line rent receivable | | | 111,731 | | | | 106,723 | | | | 104,801 | | | | 110,818 | | | | 107,463 | |

Notes receivable | | | 19,000 | | | | 19,000 | | | | - | | | | - | | | | - | |

Due from unconsolidated joint ventures | | | 569 | | | | 449 | | | | 788 | | | | 643 | | | | 537 | |

Escrow deposits and restricted cash | | | 48,046 | | | | 25,108 | | | | 9,039 | | | | 47,747 | | | | 32,309 | |

Prepaid expenses and other assets | | | 7,385 | | | | 12,477 | | | | 9,911 | | | | 13,978 | | | | 14,577 | |

Goodwill | | | 180,097 | | | | 180,097 | | | | 180,097 | | | | 180,097 | | | | 180,097 | |

Deferred financing costs, less accumulated amortization | | | 4,597 | | | | 5,187 | | | | 5,977 | | | | 4,788 | | | | 4,396 | |

Deferred lease costs, less accumulated amortization | | | 231,449 | | | | 228,468 | | | | 230,577 | | | | 241,824 | | | | 227,370 | |

| | | | | | | | | | | | | | | | | | | | |

Total assets | | $ | 4,328,308 | | | $ | 4,326,698 | | | $ | 4,447,834 | | | $ | 4,613,118 | | | $ | 4,560,206 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Liabilities: | | | | | | | | | | | | | | | | | | | | |

Line of credit and notes payable | | $ | 1,400,525 | | | $ | 1,352,525 | | | $ | 1,472,525 | | | $ | 1,664,525 | | | $ | 1,637,054 | |

Accounts payable, accrued expenses, and accrued capital expenditures | | | 126,207 | | | | 116,292 | | | | 122,986 | | | | 143,106 | | | | 126,111 | |

Deferred income | | | 23,668 | | | | 32,031 | | | | 27,321 | | | | 32,514 | | | | 32,161 | |

Intangible lease liabilities, less accumulated amortization | | | 44,246 | | | | 46,640 | | | | 49,037 | | | | 56,050 | | | | 43,657 | |

Interest rate swap | | | 6,922 | | | | 2,552 | | | | 2,537 | | | | - | | | | - | |

| | | | | | | | | | | | | | | | | | | | |

Total liabilities | | | 1,601,568 | | | | 1,550,040 | | | | 1,674,406 | | | | 1,896,195 | | | | 1,838,983 | |

| | | | | |

Stockholders’ equity: | | | | | | | | | | | | | | | | | | | | |

Common stock | | | 1,702 | | | | 1,726 | | | | 1,726 | | | | 1,728 | | | | 1,728 | |

Additional paid in capital | | | 3,665,284 | | | | 3,664,202 | | | | 3,663,662 | | | | 3,663,155 | | | | 3,662,522 | |

Cumulative distributions in excess of earnings | | | (934,933) | | | | (888,331) | | | | (891,032) | | | | (952,370) | | | | (948,956) | |

Other comprehensive loss | | | (6,922) | | | | (2,552) | | | | (2,537) | | | | - | | | | (44) | |

| | | | | | | | | | | | | | | | | | | | |

Piedmont stockholders’ equity | | | 2,725,131 | | | | 2,775,045 | | | | 2,771,819 | | | | 2,712,513 | | | | 2,715,250 | |

Non-controlling interest | | | 1,609 | | | | 1,613 | | | | 1,609 | | | | 4,410 | | | | 5,973 | |

| | | | | | | | | | | | | | | | | | | | |

Total stockholders’ equity | | | 2,726,740 | | | | 2,776,658 | | | | 2,773,428 | | | | 2,716,923 | | | | 2,721,223 | |

| | | | | | | | | | | | | | | | | | | | |

Total liabilities, redeemable common stock and stockholders’ equity | | $ | 4,328,308 | | | $ | 4,326,698 | | | $ | 4,447,834 | | | $ | 4,613,118 | | | $ | 4,560,206 | |

| | | | | | | | | | | | | | | | | | | | |

Common stock outstanding at end of period | | | 170,235 | | | | 172,630 | | | | 172,630 | | | | 172,827 | | | | 172,827 | |

10

Piedmont Office Realty Trust, Inc.

Consolidated Statements of Income

Unaudited (in thousands except for per share data)

| | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended | |

| | | | |

| | | 6/30/2012 | | | 3/31/2012 | | | 12/31/2011 | | | 9/30/2011 | | | 6/30/2011 | |

| | | | |

| | | | | |

Revenues: | | | | | | | | | | | | | | | | | | | | |

Rental income | | $ | 105,992 | | | $ | 105,282 | | | $ | 105,982 | | | $ | 104,460 | | | $ | 103,205 | |

Tenant reimbursements | | | 27,010 | | | | 26,718 | | | | 29,409 | | | | 28,268 | | | | 30,640 | |

Property management fee revenue | | | 626 | | | | 574 | | | | 281 | | | | 110 | | | | 363 | |

Other rental income | | | 88 | | | | 123 | | | | 320 | | | | (33) | | | | 1,347 | |

| | | | |

Total revenues | | | 133,716 | | | | 132,697 | | | | 135,992 | | | | 132,805 | | | | 135,555 | |

| | | | | |

Operating expenses: | | | | | | | | | | | | | | | | | | | | |

Property operating costs | | | 53,699 | | | | 52,743 | | | | 55,107 | | | | 50,814 | | | | 52,950 | |

Depreciation | | | 27,798 | | | | 27,368 | | | | 26,794 | | | | 26,071 | | | | 25,702 | |

Amortization | | | 11,478 | | | | 12,743 | | | | 15,403 | | | | 14,824 | | | | 14,040 | |

Impairment loss | | | - | | | | - | | | | - | | | | - | | | | - | |

General and administrative | | | 4,865 | | | | 5,257 | | | | 6,205 | | | | 4,677 | | | | 7,342 | |

| | | | |

Total operating expenses | | | 97,840 | | | | 98,111 | | | | 103,509 | | | | 96,386 | | | | 100,034 | |

| |

| | | | |

Real estate operating income | | | 35,876 | | | | 34,586 | | | | 32,483 | | | | 36,419 | | | | 35,521 | |

| | | | | |

Other income (expense): | | | | | | | | | | | | | | | | | | | | |

Interest expense | | | (15,943) | | | | (16,537) | | | | (16,179) | | | | (16,236) | | | | (17,762) | |

Interest and other income (expense) | | | 285 | | | | 97 | | | | (357) | | | | (91) | | | | (238) | |

Equity in income of unconsolidated joint ventures | | | 246 | | | | 170 | | | | 587 | | | | 485 | | | | 338 | |

Gain / (loss) on consolidation of variable interest entity | | | - | | | | - | | | | - | | | | - | | | | (388) | |

Gain / (loss) on extinguishment of debt | | | - | | | | - | | | | 1,039 | | | | - | | | | - | |

| | | | |

Total other income (expense) | | | (15,412) | | | | (16,270) | | | | (14,910) | | | | (15,842) | | | | (18,050) | |

| |

| | | | |

Income from continuing operations | | | 20,464 | | | | 18,316 | | | | 17,573 | | | | 20,577 | | | | 17,471 | |

| | | | | |

Discontinued operations: | | | | | | | | | | | | | | | | | | | | |

Operating income, excluding impairment loss | | | 240 | | | | 1,085 | | | | 5,550 | | | | 3,697 | | | | 3,560 | |

Gain / (loss) on sale of properties | | | 10,008 | | | | 17,830 | | | | 95,901 | | | | 26,756 | | | | - | |

| | | | |

Income / (loss) from discontinued operations(1) | | | 10,248 | | | | 18,915 | | | | 101,451 | | | | 30,453 | | | | 3,560 | |

| |

| | | | |

Net income | | | 30,712 | | | | 37,231 | | | | 119,024 | | | | 51,030 | | | | 21,031 | |

| | | | | |

Less: Net income attributable to noncontrolling interest | | | (4) | | | | (4) | | | | (4) | | | | (4) | | | | (4) | |

| | | | |

| | | | | |

Net income attributable to Piedmont | | $ | 30,708 | | | $ | 37,227 | | | $ | 119,020 | | | $ | 51,026 | | | $ | 21,027 | |

| | | | |

| | | | | |

Weighted average common shares outstanding - diluted | | | 172,209 | | | | 172,874 | | | | 173,036 | | | | 173,045 | | | | 172,986 | |

| | | | | |

Net income per share available to common stockholders - diluted | | $ | 0.18 | | | $ | 0.22 | | | $ | 0.69 | | | $ | 0.29 | | | $ | 0.12 | |

| | | | |

(1) Reflects operating results for Eastpointe Corporate Center in Issaquah, WA, which was sold on July 1, 2011; 5000 Corporate Court in Holtsville, NY, which was sold on August 31, 2011; 35 West Wacker Drive in Chicago, IL, which was sold on December 15, 2011; Deschutes, Rhein, Rogue, Willamette, and Portland Land Parcels in Beaverton, OR, which were all sold on March 19, 2012; and 26200 Enterprise Way in Lake Forest, CA, which was sold on May 31, 2012.

11

Piedmont Office Realty Trust, Inc.

Consolidated Statements of Income

Unaudited (in thousands except for per share data)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended | | | Six Months Ended | |

| | | 6/30/2012 | | | 6/30/2011 | | | Change | | | Change | | | 6/30/2012 | | | 6/30/2011 | | | Change | | | Change | |

Revenues: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Rental income | | $ | 105,992 | | | $ | 103,205 | | | $ | 2,787 | | | | 2.7% | | | $ | 211,275 | | | $ | 203,035 | | | $ | 8,240 | | | | 4.1% | |

Tenant reimbursements | | | 27,010 | | | | 30,640 | | | | (3,630) | | | | -11.8% | | | | 53,728 | | | | 57,520 | | | | (3,792) | | | | -6.6% | |

Property management fee revenue | | | 626 | | | | 363 | | | | 263 | | | | 72.5% | | | | 1,199 | | | | 1,193 | | | | 6 | | | | 0.5% | |

Other rental income | | | 88 | | | | 1,347 | | | | (1,259) | | | | -93.5% | | | | 212 | | | | 4,751 | | | | (4,539) | | | | -95.5% | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total revenues | | | 133,716 | | | | 135,555 | | | | (1,839) | | | | -1.4% | | | | 266,414 | | | | 266,499 | | | | (85) | | | | 0.0% | |

| | | | | | | | |

Operating expenses: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Property operating costs | | | 53,699 | | | | 52,950 | | | | (749) | | | | -1.4% | | | | 106,442 | | | | 101,743 | | | | (4,699) | | | | -4.6% | |

Depreciation | | | 27,798 | | | | 25,702 | | | | (2,096) | | | | -8.2% | | | | 55,167 | | | | 50,663 | | | | (4,504) | | | | -8.9% | |

Amortization | | | 11,478 | | | | 14,040 | | | | 2,562 | | | | 18.2% | | | | 24,221 | | | | 24,314 | | | | 93 | | | | 0.4% | |

Impairment loss | | | - | | | | - | | | | - | | | | 0.0% | | | | - | | | | - | | | | - | | | | 0.0% | |

General and administrative | | | 4,865 | | | | 7,342 | | | | 2,477 | | | | 33.7% | | | | 10,122 | | | | 13,954 | | | | 3,832 | | | | 27.5% | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total operating expenses | | | 97,840 | | | | 100,034 | | | | 2,194 | | | | 2.2% | | | | 195,952 | | | | 190,674 | | | | (5,278) | | | | -2.8% | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

Real estate operating income | | | 35,876 | | | | 35,521 | | | | 355 | | | | 1.0% | | | | 70,462 | | | | 75,825 | | | | (5,363) | | | | -7.1% | |

| | | | | | | | |

Other income (expense): | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Interest expense | | | (15,943) | | | | (17,762) | | | | 1,819 | | | | 10.2% | | | | (32,480) | | | | (33,402) | | | | 922 | | | | 2.8% | |

Interest and other income (expense) | | | 285 | | | | (238) | | | | 523 | | | | 219.7% | | | | 382 | | | | 3,221 | | | | (2,839) | | | | -88.1% | |

Equity in income of unconsolidated joint ventures | | | 246 | | | | 338 | | | | (92) | | | | -27.2% | | | | 416 | | | | 547 | | | | (131) | | | | -23.9% | |

Gain / (loss) on consolidation of variable interest entity | | | - | | | | (388) | | | | 388 | | | | 100.0% | | | | - | | | | 1,532 | | | | (1,532) | | | | -100.0% | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total other income (expense) | | | (15,412) | | | | (18,050) | | | | 2,638 | | | | 14.6% | | | | (31,682) | | | | (28,102) | | | | (3,580) | | | | -12.7% | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

Income from continuing operations | | | 20,464 | | | | 17,471 | | | | 2,993 | | | | 17.1% | | | | 38,780 | | | | 47,723 | | | | (8,943) | | | | -18.7% | |

| | | | | | | | |

Discontinued operations: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Operating income, excluding impairment loss | | | 240 | | | | 3,560 | | | | (3,320) | | | | -93.3% | | | | 1,325 | | | | 7,279 | | | | (5,954) | | | | -81.8% | |

Gain / (loss) on sale of properties | | | 10,008 | | | | - | | | | 10,008 | | | | 0.0% | | | | 27,838 | | | | - | | | | 27,838 | | | | 0.0% | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Income / (loss) from discontinued operations(1) | | | 10,248 | | | | 3,560 | | | | 6,688 | | | | 187.9% | | | | 29,163 | | | | 7,279 | | | | 21,884 | | | | 300.6% | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

Net income | | | 30,712 | | | | 21,031 | | | | 9,681 | | | | 46.0% | | | | 67,943 | | | | 55,002 | | | | 12,941 | | | | 23.5% | |

| | | | | | | | |

Less: Net income attributable to noncontrolling interest | | | (4) | | | | (4) | | | | - | | | | 0.0% | | | | (8) | | | | (8) | | | | - | | | | 0.0% | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

Net income attributable to Piedmont | | $ | 30,708 | | | $ | 21,027 | | | $ | 9,681 | | | | 46.0% | | | $ | 67,935 | | | $ | 54,994 | | | $ | 12,941 | | | | 23.5% | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

Weighted average common shares outstanding - diluted | | | 172,209 | | | | 172,986 | | | | | | | | | | | | 172,520 | | | | 172,908 | | | | | | | | | |

| | | | | | | | |

Net income per share available to common stockholders - diluted | | $ | 0.18 | | | $ | 0.12 | | | | | | | | | | | $ | 0.39 | | | $ | 0.32 | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

(1) Reflects operating results for Eastpointe Corporate Center in Issaquah, WA, which was sold on July 1, 2011; 5000 Corporate Court in Holtsville, NY, which was sold on August 31, 2011; 35 West Wacker Drive in Chicago, IL, which was sold on December 15, 2011; Deschutes, Rhein, Rogue, Willamette, and Portland Land Parcels in Beaverton, OR, which were all sold on March 19, 2012; and 26200 Enterprise Way in Lake Forest, CA, which was sold on May 31, 2012.

12

Piedmont Office Realty Trust, Inc.

Funds From Operations, Core Funds From Operations and Adjusted Funds From Operations

Unaudited (in thousands except for per share data)

| | | | | | | | | | | | | | | | |

| | | Three Months Ended | | | Six Months Ended | |

| | | 6/30/2012 | | | 6/30/2011 | | | 6/30/2012 | | | 6/30/2011 | |

Net income attributable to Piedmont | | $ | 30,708 | | | $ | 21,027 | | | $ | 67,935 | | | $ | 54,994 | |

| | | | |

Depreciation (1) (2) | | | 28,033 | | | | 27,879 | | | | 55,842 | | | | 55,033 | |

Amortization (1) | | | 11,539 | | | | 15,878 | | | | 24,379 | | | | 27,984 | |

Impairment loss(1) | | | - | | | | - | | | | - | | | | - | |

(Gain) / loss on sale of properties (1) | | | (10,008) | | | | (45) | | | | (27,838) | | | | (45) | |

(Gain) / loss on consolidation of VIE | | | - | | | | 388 | | | | - | | | | (1,532) | |

| | | | | | | | | | | | | | | | |

Funds from operations | | | 60,272 | | | | 65,127 | | | | 120,318 | | | | 136,434 | |

| | | | |

Acquisition costs | | | 84 | | | | 716 | | | | 81 | | | | 690 | |

| | | | | | | | | | | | | | | | |

Core funds from operations | | | 60,356 | | | | 65,843 | | | | 120,399 | | | �� | 137,124 | |

| | | | |

Depreciation of non real estate assets | | | 108 | | | | 168 | | | | 201 | | | | 338 | |

Stock-based and other non-cash compensation expense | | | 289 | | | | 896 | | | | 623 | | | | 1,864 | |

Deferred financing cost amortization(1) | | | 590 | | | | 1,060 | | | | 1,392 | | | | 1,667 | |

Amortization of fair market adjustments on notes payable | | | - | | | | 942 | | | | - | | | | 942 | |

Straight-line effects of lease revenue (1) | | | (5,477) | | | | (2,596) | | | | (7,042) | | | | (359) | |

Amortization of lease-related intangibles (1) | | | (1,785) | | | | (1,670) | | | | (3,316) | | | | (3,033) | |

Income from amortization of discount on purchase of mezzanine loans | | | - | | | | - | | | | - | | | | (484) | |

Acquisition costs | | | (84) | | | | (716) | | | | (81) | | | | (690) | |

Non-incremental capital expenditures(3) | | | (17,781) | | | | (13,349) | | | | (25,847) | | | | (30,480) | |

| | | | | | | | | | | | | | | | |

Adjusted funds from operations | | $ | 36,216 | | | $ | 50,578 | | | $ | 86,329 | | | $ | 106,889 | |

| | | | | | | | | | | | | | | | |

| | | | |

Weighted average common shares outstanding - diluted | | | 172,209 | | | | 172,986 | | | | 172,520 | | | | 172,908 | |

| | | | |

Funds from operations per share (diluted) | | $ | 0.35 | | | $ | 0.38 | | | $ | 0.70 | | | $ | 0.79 | |

Core funds from operations per share (diluted) | | $ | 0.35 | | | $ | 0.38 | | | $ | 0.70 | | | $ | 0.79 | |

Adjusted funds from operations per share (diluted) | | $ | 0.21 | | | $ | 0.29 | | | $ | 0.50 | | | $ | 0.62 | |

| (1) | Includes adjustments for consolidated properties, including discontinued operations, and for our proportionate ownership in unconsolidated joint ventures. |

| (2) | Excludes depreciation of non real estate assets. |

| (3) | Non-incremental capital expenditures are defined on page 36. |

13

Piedmont Office Realty Trust, Inc.

Same Store Net Operating Income (Cash Basis)

Unaudited (in thousands)

| | | | | | | | | | | | | | | | |

| | | Three Months Ended | | | Six Months Ended | |

| | | 6/30/2012 | | | 6/30/2011 | | | 6/30/2012 | | | 6/30/2011 | |

Net income attributable to Piedmont | | $ | 30,708 | | | $ | 21,027 | | | $ | 67,935 | | | $ | 54,994 | |

| | | | |

Net income attributable to noncontrolling interest | | | 4 | | | | 121 | | | | 8 | | | | 243 | |

Interest expense | | | 15,943 | | | | 19,313 | | | | 32,480 | | | | 36,487 | |

Depreciation(1) | | | 28,141 | | | | 28,047 | | | | 56,043 | | | | 55,371 | |

Amortization(1) | | | 11,539 | | | | 15,878 | | | | 24,379 | | | | 27,984 | |

Impairment loss(1) | | | - | | | | - | | | | - | | | | - | |

(Gain) / loss on sale of properties(1) | | | (10,008) | | | | (45) | | | | (27,838) | | | | (45) | |

(Gain) / loss on consolidation of VIE | | | - | | | | 388 | | | | - | | | | (1,532) | |

| | | | | | | | | | | | | | | | |

Core EBITDA | | | 76,327 | | | | 84,729 | | | | 153,007 | | | | 173,502 | |

| | | | |

General & administrative expenses(1) | | | 4,866 | | | | 7,392 | | | | 10,184 | | | | 14,096 | |

Management fee revenue | | | (626) | | | | (363) | | | | (1,199) | | | | (1,193) | |

Interest and other income(1) | | | (305) | | | | 253 | | | | (403) | | | | (3,206) | |

Lease termination income | | | (88) | | | | (1,347) | | | | (212) | | | | (4,751) | |

Lease termination expense - straight line rent & acquisition intangibles write-offs | | | 165 | | | | 43 | | | | 264 | | | | 479 | |

Straight-line effects of lease revenue(1) | | | (5,642) | | | | (2,639) | | | | (7,306) | | | | (667) | |

Net effect of amortization of above/(below) market in-place lease intangibles(1) | | | (1,785) | | | | (1,670) | | | | (3,316) | | | | (3,204) | |

| | | | | | | | | | | | | | | | |

Core net operating income - cash basis | | | 72,912 | | | | 86,398 | | | | 151,019 | | | | 175,056 | |

| | | | |

Net operating income from: | | | | | | | | | | | | | | | | |

Acquisitions(2) | | | (3,886) | | | | (3,446) | | | | (7,036) | | | | (3,444) | |

Dispositions(3) | | | (296) | | | | (7,376) | | | | (1,692) | | | | (14,873) | |

Industrial properties | | | (245) | | | | (242) | | | | (487) | | | | (479) | |

Unconsolidated joint ventures | | | (598) | | | | (696) | | | | (1,188) | | | | (1,354) | |

| | | | | | | | | | | | | | | | |

Same Store NOI - Cash Basis | | $ | 67,887 | | | $ | 74,638 | | | $ | 140,616 | | | $ | 154,906 | |

| | | | | | | | | | | | | | | | |

Change period over period | | | -9.0% | | | | N/A | | | | -9.2% | | | | N/A | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

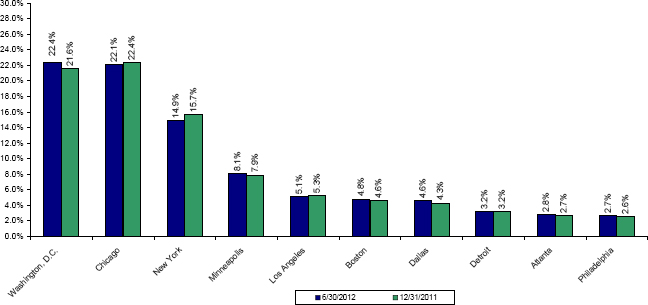

| | | Same Store Net Operating Income Top Seven Markets | | | |

| | | | | Three Months Ended | | | Six Months Ended | | | |

| | | | | 6/30/2012 | | | 6/30/2011 | | | 6/30/2012 | | | 6/30/2011 | | | |

| | | | | $ | | | % | | | $ | | | % | | | $ | | | % | | | $ | | | % | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | Washington, D.C. (4) | | $ | 17,996 | | | | 26.5 | | | $ | 17,731 | | | | 23.7 | | | $ | 37,046 | | | | 26.3 | | | $ | 35,753 | | | | 23.1 | | | |

| | | New York(5) | | | 11,111 | | | | 16.4 | | | | 14,093 | | | | 18.9 | | | | 23,429 | | | | 16.7 | | | | 27,678 | | | | 17.9 | | | |

| | | Chicago (6) | | | 9,573 | | | | 14.1 | | | | 12,815 | | | | 17.2 | | | | 18,999 | | | | 13.5 | | | | 25,208 | | | | 16.3 | | | |

| | | Minneapolis | | | 5,277 | | | | 7.8 | | | | 4,937 | | | | 6.6 | | | | 10,270 | | | | 7.3 | | | | 9,980 | | | | 6.4 | | | |

| | | Dallas | | | 3,529 | | | | 5.2 | | | | 3,390 | | | | 4.5 | | | | 7,334 | | | | 5.2 | | | | 7,203 | | | | 4.6 | | | |

| | | Los Angeles(7) | | | 3,232 | | | | 4.7 | | | | 3,858 | | | | 5.2 | | | | 6,408 | | | | 4.6 | | | | 7,459 | | | | 4.8 | | | |

| | | Boston(8) | | | 2,696 | | | | 4.0 | | | | 2,598 | | | | 3.5 | | | | 5,240 | | | | 3.7 | | | | 6,469 | | | | 4.2 | | | |

| | | Other(9) | | | 14,473 | | | | 21.3 | | | | 15,216 | | | | 20.4 | | | | 31,890 | | | | 22.7 | | | | 35,156 | | | | 22.7 | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | Total | | $ | 67,887 | | | | 100.0 | | | $ | 74,638 | | | | 100.0 | | | $ | 140,616 | | | | 100.0 | | | $ | 154,906 | | | | 100.0 | | | |

| | | | | | | | | | | | | | | | | | | | | |

(1) Includes amounts attributable to consolidated properties, including discontinued operations, and our proportionate share of amounts attributable to unconsolidated joint ventures.

(2)Acquisitions consist of 1200 Enclave Parkway in Houston, TX, purchased on March 30, 2011; 500 West Monroe Street in Chicago, IL, acquired on March 31, 2011; The Dupree in Atlanta, GA, purchased on April 29, 2011; The Medici in Atlanta, GA, purchased on June 7, 2011; 225 and 235 Presidential Way in Woburn, MA, purchased on September 13, 2011; 400 TownPark in Lake Mary, FL purchased on November 10, 2011; and Gavitello Land Parcels in Atlanta, GA, purchased on June 28, 2012.

(3)Dispositions consist of Eastpointe Corporate Center in Issaquah, WA, sold on July 1, 2011; 5000 Corporate Court in Holtsville, NY, sold on August 31, 2011; 35 West Wacker Drive in Chicago, IL, sold on December 15, 2011; Deschutes, Rhein, Rogue, Willamette, and Portland Land Parcels in Beaverton, OR, sold on March 19, 2012; and 26200 Enterprise Way in Lake Forest, CA, sold on May 31, 2012.

(4) The increase in Washington, D.C. Same Store Net Operating Income for the six months ended June 30, 2012 as compared to the same period in 2011 was primarily related to increased rental revenue due to a rental rate increase associated with the lease extension of the Comptroller of the Currency at One Independence Square in Washington, D.C.

(5) The decrease in New York Same Store Net Operating Income for the three months and the six months ended June 30, 2012 as compared to the same periods in 2011 was primarily related to the lease expirations of and the downtime and rental abatements associated with newly signed leases to backfill the spaces formerly occupied by sanofi-aventis at 200 & 400 Bridgewater Crossing in Bridgewater, NJ.

(6) The decrease in Chicago Same Store Net Operating Income for the three months and the six months ended June 30, 2012 as compared to the same periods in 2011 was primarily related to the expiration of the Zurich American Insurance Company lease at Windy Point II in Schaumburg, IL in August 2011, as well as the expiration of the Kirkland & Ellis lease at Aon Center in Chicago, IL in December 2011. The loss of the Zurich and Kirkland & Ellis leases reduced rental revenues by approximately $5.2 million and $10.4 million, respectively, for the three months and the six months ended June 30, 2012; these amounts are offset partially by incremental operating expense savings due to the vacancy of those tenants. Additionally, the negative contributions are offset somewhat by the commencement of several new leases during the last year (although there are several replacement leases that are in abatement or have yet to commence).

(7) The decrease in Los Angeles Same Store Net Operating Income for the three months and the six months ended June 30, 2012 as compared to the same periods in 2011 was primarily related to a net lease expiration of approximately 65,000 square feet at 1055 East Colorado Boulevard in Pasadena, CA.

(8) The decrease in Boston Same Store Net Operating Income for the six months ended June 30, 2012 as compared to the same period in 2011 was primarily due to a rental abatement concession associated with a long-term lease renewal with State Street Bank at 1200 Crown Colony Drive in Quincy, MA. The renewal period for the State Street Bank lease commenced in April 2011.

(9) The decrease in Other Same Store Net Operating Income for the three months ended June 30, 2012 as compared to the same period in 2011 was primarily related to a rental abatement concession in 2012 associated with a new lease with Grand Canyon Education at Desert Canyon 300 in Phoenix, AZ. The decrease in Other Same Store Net Operating Income for the six months ended June 30, 2012 as compared to the same period in 2011 was primarily attributable to four factors: 1) the rental abatement concession described above at Desert Canyon 300 in Phoenix, AZ, 2) a rental abatement concession in 2012 associated with a new lease with Chrysler Group, LLC at 1075 West Entrance Drive in Auburn Hills, MI, 3) a decrease in rental revenue associated with a lower lease renewal rental rate at 5601 Headquarters Drive in Plano, TX, and 4) a decrease in rental revenue associated with lease expirations in 2011 at Las Colinas Corporate Center II in Irving, TX.

14

Piedmont Office Realty Trust, Inc.

Same Store Net Operating Income (Accrual Basis)

Unaudited (in thousands)

| | | | | | | | | | | | | | | | |

| | | Three Months Ended | | | Six Months Ended | |

| | | 6/30/2012 | | | 6/30/2011 | | | 6/30/2012 | | | 6/30/2011 | |

Net income attributable to Piedmont | | $ | 30,708 | | | $ | 21,027 | | | $ | 67,935 | | | $ | 54,994 | |

| | | | |

Net income attributable to noncontrolling interest | | | 4 | | | | 121 | | | | 8 | | | | 243 | |

Interest expense | | | 15,943 | | | | 19,313 | | | | 32,480 | | | | 36,487 | |

Depreciation(1) | | | 28,141 | | | | 28,047 | | | | 56,043 | | | | 55,371 | |

Amortization(1) | | | 11,539 | | | | 15,878 | | | | 24,379 | | | | 27,984 | |

Impairment loss(1) | | | - | | | | - | | | | - | | | | - | |

(Gain) / loss on sale of properties(1) | | | (10,008) | | | | (45) | | | | (27,838) | | | | (45) | |

(Gain) / loss on consolidation of VIE | | | - | | | | 388 | | | | - | | | | (1,532) | |

| | | | | | | | | | | | | | | | |

Core EBITDA | | | 76,327 | | | | 84,729 | | | | 153,007 | | | | 173,502 | |

| | | | |

General & administrative expenses(1) | | | 4,866 | | | | 7,392 | | | | 10,184 | | | | 14,096 | |

Management fee revenue | | | (626) | | | | (363) | | | | (1,199) | | | | (1,193) | |

Interest and other income(1) | | | (305) | | | | 253 | | | | (403) | | | | (3,206) | |

Lease termination income | | | (88) | | | | (1,347) | | | | (212) | | | | (4,751) | |

Lease termination expense - straight line rent & acquisition intangibles write-offs | | | 165 | | | | 43 | | | | 264 | | | | 479 | |

| | | | | | | | | | | | | | | | |

Core net operating income - accrual basis | | | 80,339 | | | | 90,707 | | | | 161,641 | | | | 178,927 | |

| | | | |

Net operating income from: | | | | | | | | | | | | | | | | |

Acquisitions(2) | | | (5,120) | | | | (3,591) | | | | (9,309) | | | | (3,590) | |

Dispositions (3) | | | (308) | | | | (8,958) | | | | (1,690) | | | | (17,961) | |

Industrial properties | | | (496) | | | | (257) | | | | (749) | | | | (513) | |

Unconsolidated joint ventures | | | (563) | | | | (653) | | | | (1,127) | | | | (1,269) | |

| | | | | | | | | | | | | | | | |

Same Store NOI - Accrual Basis | | $ | 73,852 | | | $ | 77,248 | | | $ | 148,766 | | | $ | 155,594 | |

| | | | | | | | | | | | | | | | |

Change period over period | | | -4.4% | | | | N/A | | | | -4.4% | | | | N/A | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Same Store Net Operating Income Top Seven Markets | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended | | | Six Months Ended | | | |

| | | | | 6/30/2012 | | | 6/30/2011 | | | 6/30/2012 | | | 6/30/2011 | | | |

| | | | | $ | | | % | | | $ | | | % | | | $ | | | % | | | $ | | | % | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | Washington, D.C.(4) | | $ | 19,437 | | | | 26.3 | | | $ | 18,228 | | | | 23.6 | | | $ | 39,893 | | | | 26.8 | | | $ | 36,305 | | | | 23.3 | | | |

| | | New York(5) | | | 11,988 | | | | 16.2 | | | | 13,688 | | | | 17.7 | | | | 24,587 | | | | 16.5 | | | | 27,317 | | | | 17.5 | | | |

| | | Chicago(6) | | | 9,177 | | | | 12.4 | | | | 12,308 | | | | 15.9 | | | | 18,306 | | | | 12.3 | | | | 24,401 | | | | 15.7 | | | |

| | | Minneapolis(7) | | | 5,552 | | | | 7.5 | | | | 5,911 | | | | 7.6 | | | | 10,888 | | | | 7.3 | | | | 11,920 | | | | 7.7 | | | |

| | | Dallas | | | 3,883 | | | | 5.3 | | | | 3,601 | | | | 4.7 | | | | 7,811 | | | | 5.3 | | | | 7,635 | | | | 4.9 | | | |

| | | Los Angeles(8) | | | 3,101 | | | | 4.2 | | | | 3,699 | | | | 4.8 | | | | 6,436 | | | | 4.3 | | | | 7,109 | | | | 4.6 | | | |

| | | Boston | | | 2,989 | | | | 4.1 | | | | 2,831 | | | | 3.7 | | | | 5,856 | | | | 4.0 | | | | 6,354 | | | | 4.1 | | | |

| | | Other(9) | | | 17,725 | | | | 24.0 | | | | 16,982 | | | | 22.0 | | | | 34,989 | | | | 23.5 | | | | 34,553 | | | | 22.2 | | | |

| | | | | | | | | | | | | | | | | | | |

| | | Total | | $ | 73,852 | | | | 100.0 | | | $ | 77,248 | | | | 100.0 | | | $ | 148,766 | | | | 100.0 | | �� | $ | 155,594 | | | | 100.0 | | | |

| | | | | | | | | | | | | | | | | | | |

(1) Includes amounts attributable to consolidated properties, including discontinued operations, and our proportionate share of amounts attributable to unconsolidated joint ventures.

(2)Acquisitions consist of 1200 Enclave Parkway in Houston, TX, purchased on March 30, 2011; 500 West Monroe Street in Chicago, IL, acquired on March 31, 2011; The Dupree in Atlanta, GA, purchased on April 29, 2011; The Medici in Atlanta, GA, purchased on June 7, 2011; 225 and 235 Presidential Way in Woburn, MA, purchased on September 13, 2011; 400 TownPark in Lake Mary, FL purchased on November 10, 2011; and Gavitello Land Parcels in Atlanta, GA, purchased on June 28, 2012.

(3)Dispositions consist of Eastpointe Corporate Center in Issaquah, WA, sold on July 1, 2011; 5000 Corporate Court in Holtsville, NY, sold on August 31, 2011; 35 West Wacker Drive in Chicago, IL, sold on December 15, 2011; Deschutes, Rhein, Rogue, Willamette, and Portland Land Parcels in Beaverton, OR, sold on March 19, 2012; and 26200 Enterprise Way in Lake Forest, CA, sold on May 31, 2012.

(4) The increase in Washington, D.C. Same Store Net Operating Income for the three months and the six months ended June 30, 2012 as compared to the same periods in 2011 was primarily attributable to two factors: 1) an increase in revenue due to a rental rate increase associated with the lease extension of the Comptroller of the Currency at One Independence Square in Washington, D.C., and 2) increased rental revenue as a result of the commencement of several new leases at Piedmont Pointe I and II in Bethesda, MD.

(5) The decrease in New York Same Store Net Operating Income for the three months and the six months ended June 30, 2012 as compared to the same periods in 2011 was primarily related to the lease expirations of and the downtime associated with newly signed leases to backfill the spaces formerly occupied by sanofi-aventis at 200 & 400 Bridgewater Crossing in Bridgewater, NJ.

(6) The decrease in Chicago Same Store Net Operating Income for the three months and the six months ended June 30, 2012 as compared to the same periods in 2011 was primarily related to the expiration of the Zurich American Insurance Company lease at Windy Point II in Schaumburg, IL in August 2011, as well as the expiration of the Kirkland & Ellis lease at Aon Center in Chicago, IL in December 2011. The loss of the Zurich and Kirkland & Ellis leases reduced rental revenues by approximately $4.6 million and $9.2 million, respectively, for the three months and the six months ended June 30, 2012; these amounts are offset partially by incremental operating expense savings due to the vacancy of those tenants. Additionally, the negative contributions are offset somewhat by the commencement of several new leases during the last year.

(7)The decrease in Minneapolis Same Store Net Operating Income for the three months and the six months ended June 30, 2012 as compared to the same periods in 2011 was primarily related to the net loss of approximately 76,000 leased square feet associated with the expiration of the HSBC Card Services lease at Crescent Ridge II in Minnetonka, MN.

(8) The decrease in Los Angeles Same Store Net Operating Income for the three months ended June 30, 2012 as compared to the same period in 2011 was primarily related to a net lease expiration of approximately 65,000 square feet at 1055 East Colorado Boulevard in Pasadena, CA.

(9) The increase in Other Same Store Net Operating Income for the three months ended June 30, 2012 as compared to the same period in 2011 was primarily related to three factors: 1) an increase in rental revenue due to downtime between the EDS and Chrysler Group leases in 2011 at 1075 West Entrance Drive in Auburn Hills, MI, 2) an increase in rental revenue due to the commencement of the US Foods lease at River Corporate Center in Tempe, AZ, and 3) an increase in rental revenue due to the commencement of several new leases at Glenridge Highlands II in Atlanta, GA.

15

Piedmont Office Realty Trust, Inc.

Capitalization Analysis

Unaudited ($ and shares in thousands)

| | | | | | | | |

| | | As of

June 30, 2012 | | | As of

December 31, 2011 | |

Common stock price(1) | | | $17.21 | | | | $17.04 | |

Total shares outstanding | | | 170,235 | | | | 172,630 | |

Equity market capitalization(1) | | | $2,929,741 | | | | $2,941,611 | |

Total debt - principal amount outstanding | | | $1,400,525 | | | | $1,472,525 | |

Total market capitalization(1) | | | $4,330,266 | | | | $4,414,136 | |

Total debt / Total market capitalization | | | 32.3% | | | | 33.4% | |

Total gross real estate assets | | | $4,558,128 | | | | $4,615,812 | |

Total debt / Total gross real estate assets (2) | | | 30.7% | | | | 31.9% | |

Total debt / Total gross assets (3) | | | 26.7% | | | | 27.5% | |

(1)Reflects common stock closing price as of the end of the reporting period.

(2)Total debt to total gross real estate assets ratio is defined as total debt divided by gross real estate assets. Gross real estate assets is defined as total real estate assets with the add back of accumulated depreciation and accumulated amortization related to real estate assets.

(3)Total debt to total gross assets ratio is defined as total debt divided by gross assets. Gross assets is defined as total assets with the add back of accumulated depreciation and accumulated amortization related to real estate assets.

16

Piedmont Office Realty Trust, Inc.

Debt Summary

As of June 30, 2012

Unaudited ($ in thousands)

| | | | | | | | |

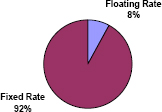

Floating Rate & Fixed Rate Debt |

| Debt(1) | | Principal Amount

Outstanding | | Weighted Average

Stated Interest Rate | | Weighted Average

Maturity | |

|

| |

Floating Rate | | $113,000(2) | | 0.73% | | 2.0 months | |

Fixed Rate | | 1,287,525 | | 4.59% | | 38.3 months | |

| |

Total | | $1,400,525 | | 4.28% | | 35.4 months | |

| |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

Unsecured & Secured Debt |

| Debt(1) | | Principal Amount

Outstanding | | Weighted Average

Stated Interest Rate | | Weighted Average

Maturity | |

|

| |

Unsecured | | $413,000 | | 2.15%(3) | | 38.9 months | |

Secured | | 987,525 | | 5.17% | | 33.9 months | |

| |

Total | | $1,400,525 | | 4.28% | | 35.4 months | |

| |

| | | | | | | |

| | | | | | | �� |

| | | | | | | |

| | | | | | | | | | | | | | |

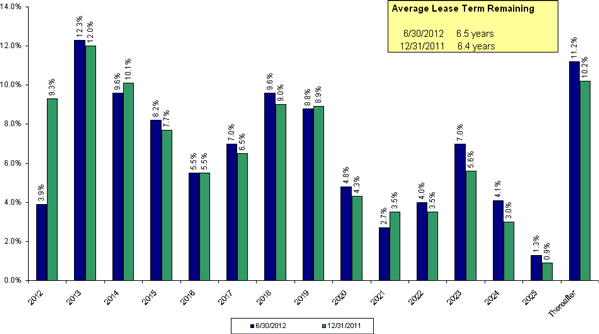

Debt Maturities |

| Maturity Year | | Secured Debt -

Principal Amount

Outstanding (1) | | | | Unsecured Debt -

Principal Amount

Outstanding (1) | | | | Weighted Average

Stated Interest

Rate | | Percentage

of Total | | |

| |

2012 | | $0 | | | | $113,000 | | | | 0.73% | | 8.1% | |

2013 | | 0 | | | | 0 | | | | N/A | | 0.0% | |

2014 | | 575,000 | | | | 0 | | | | 4.89% | | 41.0% | |

2015 | | 105,000 | | | | 0 | | | | 5.29% | | 7.5% | |

2016 | | 167,525 | | | | 300,000 | | | | 3.71% | | 33.4% | |

2017 | | 140,000 | | | | 0 | | | | 5.76% | | 10.0% | |

| |

Total | | $987,525 | | | | $413,000 | | | | 4.28% | | 100.0% | |

| |

(1) All of Piedmont’s outstanding debt as of June 30, 2012 was interest-only debt.

(2) Amount represents the outstanding balance as of June 30, 2012, on the $500 million unsecured line of credit.

(3) The weighted average interest rate is a weighted average rate for amounts outstanding under our $500 million unsecured line of credit and our $300 million unsecured term loan. The $300 million unsecured term loan has a stated variable rate; however, Piedmont entered into interest rate swap agreements which effectively fix the interest rate on this loan at 2.69% through its maturity date of November 22, 2016, assuming no credit rating change for the Company.

17

Piedmont Office Realty Trust, Inc.

Debt Detail

Unaudited ($ in thousands)

| | | | | | | | | | | | |

| Facility | | Property | | Rate(1) | | Maturity | | | Principal Amount

Outstanding as of

June 30, 2012 | |

| |

| | | | |

Secured | | | | | | | | | | | | |

$200.0 Million Fixed-Rate Loan | | Aon Center | | 4.87% | | | 5/1/2014 | | | | $200,000 | |

$25.0 Million Fixed-Rate Loan | | Aon Center | | 5.70% | | | 5/1/2014 | | | | 25,000 | |

$350.0 Million Secured Pooled Facility | | Nine Property Collateralized Pool(2) | | 4.84% | | | 6/7/2014 | | | | 350,000 | |

$105.0 Million Fixed-Rate Loan | | US Bancorp Center | | 5.29% | | | 5/11/2015 | | | | 105,000 | |

$125.0 Million Fixed-Rate Loan | | Four Property Collateralized Pool(3) | | 5.50% | | | 4/1/2016 | | | | 125,000 | |

$42.5 Million Fixed-Rate Loan | | Las Colinas Corporate Center I & II | | 5.70% | | | 10/11/2016 | | | | 42,525 | |

$140.0 Million WDC Fixed-Rate Loans | | 1201 & 1225 Eye Street | | 5.76% | | | 11/1/2017 | | | | 140,000 | |

| |

| | | | |

Subtotal / Weighted Average(4) | | | | 5.17% | | | | | | | $987,525 | |

| | | | |

Unsecured | | | | | | | | | | | | |

$500.0 Million Unsecured Facility(5) | | N/A | | 0.73%(6) | | | 8/30/2012 | | | | $113,000 | |

$300.0 Million Unsecured Term Loan | | N/A | | 2.69%(7) | | | 11/22/2016 | | | | 300,000 | |

| |

| | | | |

Subtotal / Weighted Average(4) | | | | 2.15% | | | | | | | $413,000 | |

|

| |

Total Debt - Principal Amount Outstanding / Weighted Average Stated Rate(4) | | 4.28% | | | | | | | $1,400,525 | |

| |

(1) All of Piedmont’s outstanding debt as of June 30, 2012, was interest-only debt.

(2) The nine property collateralized pool includes 1200 Crown Colony Drive, Braker Pointe III, 2 Gatehall Drive, One and Two Independence Square, 2120 West End Avenue, 200 and 400 Bridgewater Crossing, and Fairway Center II.

(3) The four property collateralized pool includes 1430 Enclave Parkway, Windy Point I and II, and 1055 East Colorado Boulevard.

(4) Weighted average is based on the total balance outstanding and interest rate at June 30, 2012.

(5) All of Piedmont’s outstanding debt as of June 30, 2012, was term debt with the exception of $113 million outstanding on our unsecured line of credit. Piedmont is close to finalizing a new $500 million unsecured revolving credit facility. The terms of the facility will be provided after the transaction has closed. The Company’s current revolver will be terminated prior to the effectiveness of the transaction.

(6)The interest rate on the $500 million unsecured line of credit is equal to the weighted average interest rate on all outstanding draws as of June 30, 2012. Piedmont may select from multiple interest rate options with each draw under this facility, including the prime rate and various length LIBOR locks. All LIBOR selections are subject to an additional spread (0.475% as of June 30, 2012) over the selected rate based on Piedmont’s current credit rating.

(7) The $300 million unsecured term loan has a stated variable rate; however, Piedmont entered into interest rate swap agreements which effectively fix the interest rate on this loan at 2.69% through its maturity date of November 22, 2016, assuming no credit rating change for the Company.

18

Piedmont Office Realty Trust, Inc.

Debt Analysis

As of June 30, 2012

Unaudited

| | | | | | | | |

| Debt Covenant Compliance(1) | | Required | | | Actual | |

Maximum Leverage Ratio | | | 0.60 | | | | 0.35 | |

Minimum Fixed Charge Coverage Ratio (2) | | | 1.50 | | | | 4.62 | |

Maximum Secured Indebtedness Ratio | | | 0.40 | | | | 0.25 | |

Minimum Unencumbered Leverage Ratio | | | 1.60 | | | | 4.81 | |

Minimum Unencumbered Interest Coverage Ratio(3) | | | 1.75 | | | | 19.68 | |

Maximum Certain Permitted Investments Ratio(4) | | | 0.35 | | | | 0.01 | |

(1) Debt covenant compliance calculations relate to specific calculations detailed in our line of credit agreement. (2) Defined as EBITDA for the trailing four quarters (including the company’s share of EBITDA from unconsolidated interests), less one-time or non-recurring gains or losses, less a $0.15 per square foot capital reserve, and excluding the impact of straight line rent leveling adjustments and amortization of intangibles divided by the company’s share of fixed charges, as more particularly described in the credit agreements. This definition of fixed charge coverage ratio as prescribed by our credit agreements is different from the fixed charge coverage ratio definition employed elsewhere within this report. (3) Defined as net operating income for the trailing four quarters for unencumbered assets (including the company’s share of net operating income from unconsolidated interests that are unencumbered) less a $0.15 per square foot capital reserve divided by the company’s share of interest expense associated with unsecured financings only, as more particularly described in the credit agreements. (4) Permitted investments are defined as unconsolidated interests, debt investments, unimproved land, and development projects. Investments in permitted investments shall not exceed 35% of total asset value. | |

| | |

| | | | | | |

| Other Debt Coverage Ratios | | Three months ended

June 30, 2012 | | Six months ended

June 30, 2012 | | Year ended

December 31, 2011 |

Net debt to core EBITDA | | 4.3 x | | 4.3 x | | 3.9 x |

Fixed charge coverage ratio (5) | | 4.8 x | | 4.7 x | | 4.8 x |

Interest coverage ratio(6) | | 4.8 x | | 4.7 x | | 4.8 x |

(5) Fixed charge coverage is calculated as Core EBITDA divided by the sum of interest expense, principal amortization, capitalized interest and preferred dividends. We had no capitalized interest, principal amortization or preferred dividends during the periods ended June 30, 2012 and December 31, 2011. (6) Interest coverage ratio is calculated as Core EBITDA divided by the sum of interest expense and capitalized interest. We had no capitalized interest during the periods ended June 30, 2012 and December 31, 2011. |

19

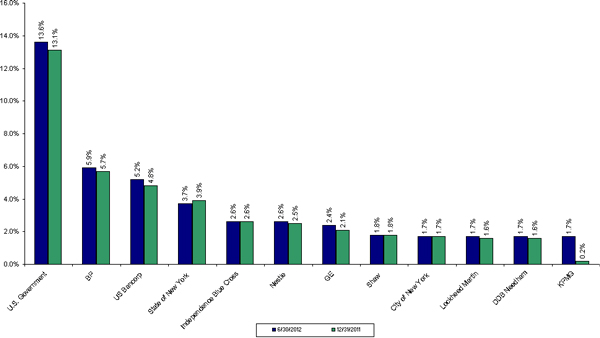

Piedmont Office Realty Trust, Inc.

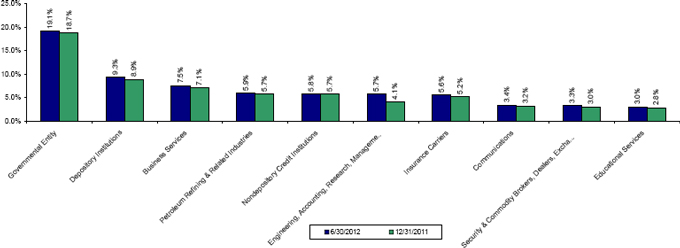

Tenant Diversification(1)

As of June 30, 2012

(in thousands except for number of properties)

| | | | | | | | | | | | | | |

| | | Credit Rating (2) | | Number of

Properties | | Lease

Expiration(s) (3) | | Annualized Lease

Revenue | | Percentage of

Annualized Lease

Revenue (%) | | Leased Square

Footage | | Percentage of

Leased Square

Footage (%) |

U.S. Government | | AA+ / Aaa | | 9 | | (4) | | $73,357 | | 13.6 | | 1,596 | | 9.2 |

BP(5) | | A / A2 | | 1 | | 2013 | | 31,749 | | 5.9 | | 776 | | 4.5 |