Exhibit 99.1

The Supermarket REIT

www.equityone.net

April 2005

Forward Looking Statements

Certain matters discussed in this presentation constitute forward-looking statements within the meaning of the federal securities laws. Although Equity One believes that the expectations reflected in such forward-looking statements are based upon reasonable assumptions, it can give no assurance that these expectations will be achieved. Factors that could cause actual results to differ materially from current expectations include changes in macro-economic conditions and the demand for retail space in Florida, Texas, Georgia, Massachusetts and the other states in which Equity One owns properties; the continuing financial success of Equity One’s current and prospective tenants; continuing supply constraints in Equity One’s geographic markets; the availability of properties for acquisition; the success of Equity One’s efforts to lease up vacant properties; the effects of natural and other disasters; the ability of Equity One to successfully integrate the operations and systems of acquired companies and properties; and other risks, which are described in Equity One’s filings with the Securities and Exchange Commission.

Mission Statement

Equity One will be a dominant supermarket-anchored shopping center REIT in its target markets

3

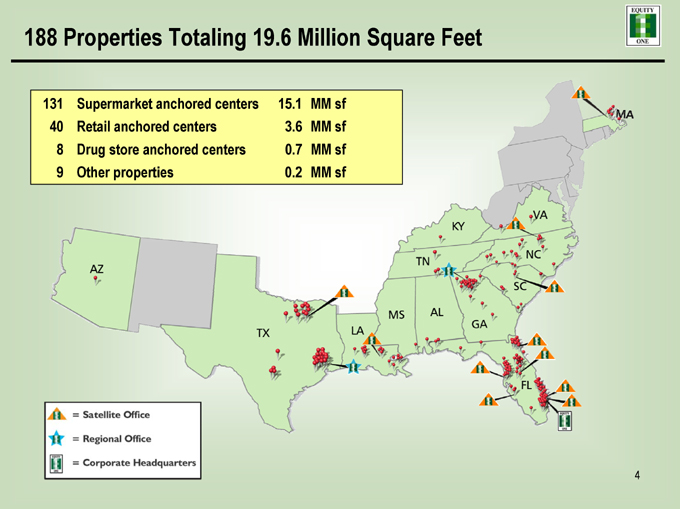

188 Properties Totaling 19.6 Million Square Feet

Satelite Office

Regional Office

Corporate Headquarters

131 Supermarket anchored centers 15.1 MM sf

40 Retail anchored centers 3.6 MM sf

8 Drug store anchored centers 0.7 MM sf

9 Other properties 0.2 MM sf

4

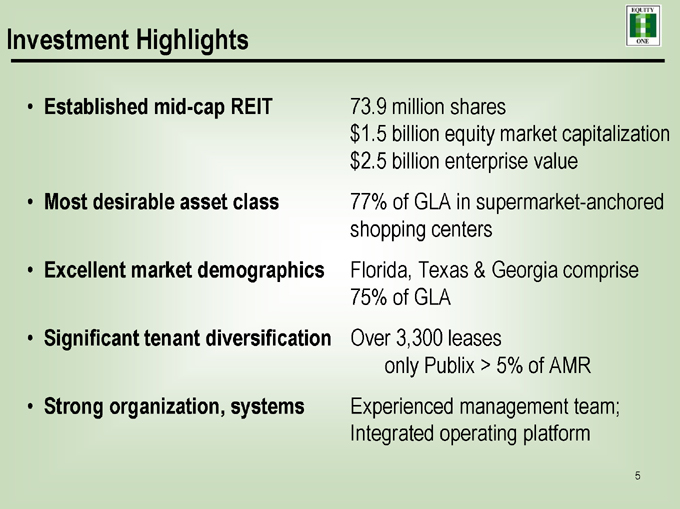

Investment Highlights

Established mid-cap REIT Most desirable asset class Excellent market demographics Significant tenant diversification Strong organization, systems

73.9 million shares $1.5 billion equity market capitalization $2.5 billion enterprise value 77% of GLA in supermarket-anchored shopping centers Florida, Texas & Georgia comprise 75% of GLA

Over 3,300 leases only Publix > 5% of AMR Experienced management team; Integrated operating platform

5

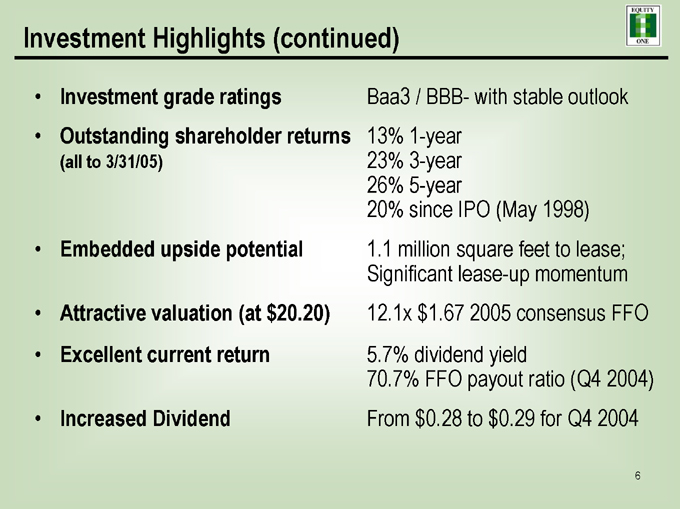

Investment Highlights (continued)

Investment grade ratings Outstanding shareholder returns

(all to 3/31/05)

Embedded upside potential

Attractive valuation (at $20.20) Excellent current return

Increased Dividend

Baa3 / BBB- with stable outlook 13% 1-year 23% 3-year 26% 5-year 20% since IPO (May 1998) 1.1 million square feet to lease; Significant lease-up momentum 12.1x $1.67 2005 consensus FFO 5.7% dividend yield 70.7% FFO payout ratio (Q4 2004) From $0.28 to $0.29 for Q4 2004

6

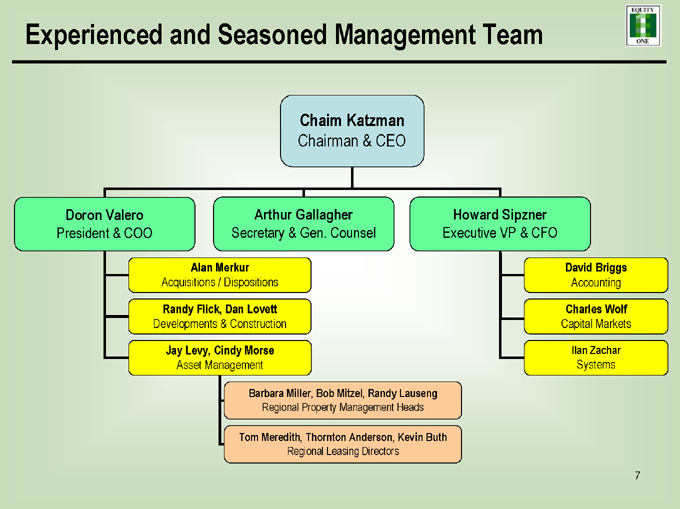

Experienced and Seasoned Management Team

Chaim Katzman

Chairman & CEO

Doron Valero

President & COO

Arthur Gallagher

Secretary & Gen. Counsel

Howard Sipzner

Executive VP & CFO

Alan Merkur

Acquisitions / Dispositions

Randy Flick, Dan Lovett

Developments & Construction

Jay Levy, Cindy Morse

Asset Management

David Briggs

Accounting

Charles Wolf

Capital Markets

IIan Zachar

Systems

Barbara Miller, Bob Mitzel, Randy Lauseng

Regional Property Management Heads

Tom Meredith, Thornton Anderson, Kevin Buth

Regional Leasing Directors

7

Company Timeline

Indexed Total Return

450 400 350 300 250 200 150 100 50

244.0% Cumulative Total Return (IPO to Present) $120MM Boston Portfolio Purchase $200MM Unsecured 5-YR Bond Sale

3MM Share Equity Offering

3MM Share Equity Offering

9.7% Equity Stake in CDR

$763MM IRT Acquisition

3.45MM Share Equity Offering $281MM CEFUS

Acquisition $148MM UIRT Acquisition

4.7MM Share IPO

Nov-04

May-04

Nov-03

May-03

Nov-02

May-02

Nov-01

May-01

Nov-00

May-00

Nov-99

May- 99

Nov-98

May-98

Note: Data is through March 31, 2005.

8

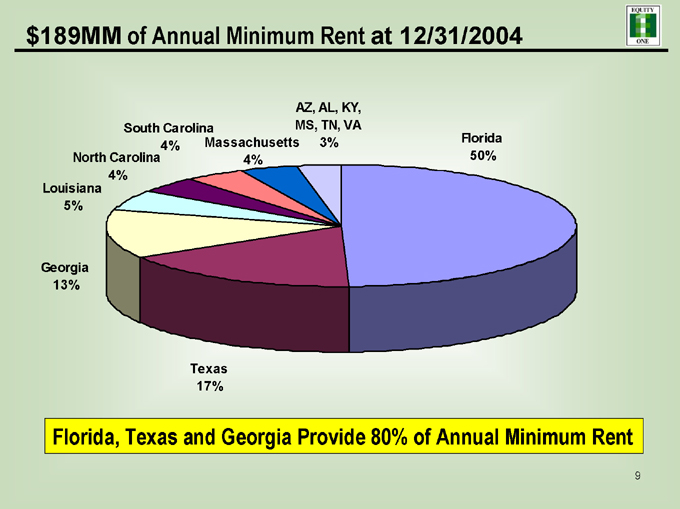

$189MM of Annual Minimum Rent at 12/31/2004

AZ, AL, KY, South Carolina MS, TN, VA

Massachusetts 3% Florida 4% North Carolina 4% 50% 4% Louisiana 5%

Georgia 13%

Texas 17%

Florida, Texas and Georgia Provide 80% of Annual Minimum Rent

9

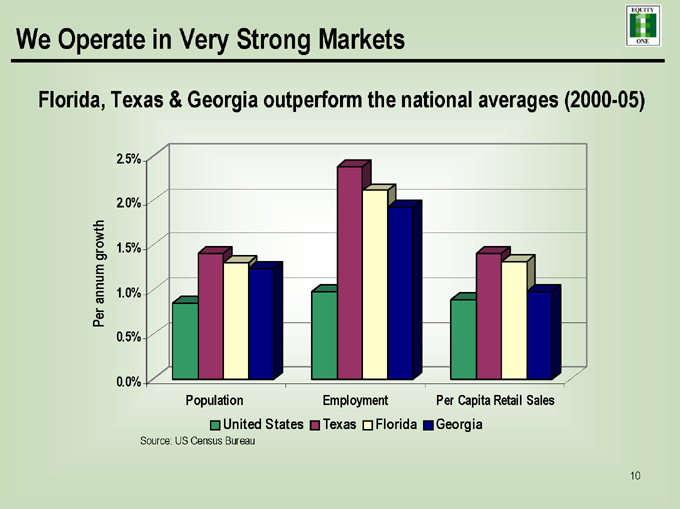

We Operate in Very Strong Markets

Florida, Texas & Georgia outperform the national averages (2000-05)

2.5%

2.0%

1.5%

Per annum growth 1.0% 0.5%

0.0%

Population Employment Per Capita Retail Sales

United States Texas Florida Georgia

Source: US Census Bureau

10

Our Supermarkets are Top Performers

Sales AMR AMR /

PSF AMR PSF Sales(1)

$511 $15.7MM $7.20 1.4%

$337 $8.0MM $8.31 2.3%

$433 $6.6MM $19.62 4.2%

$266 $5.1MM $6.93 2.6%

$681 $2.8MM $10.83 1.8%

$284 $2.0MM $6.66 2.5%

$366 $1.4MM $7.19 2.0%

$308 $1.0MM $4.53 2.2%

(1) Data is limited to stores that provide sales data.

Note: Kash n’ Karry data also includes Food Lion figures; both companies are owned by Delhaize Group.

11

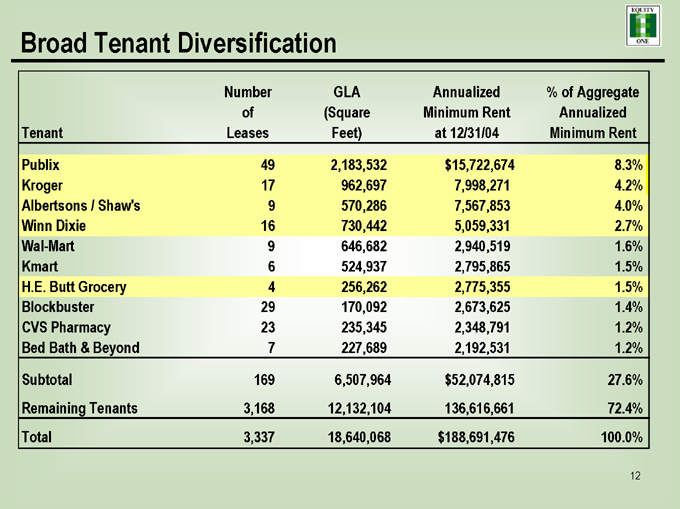

Broad Tenant Diversification

Number GLA Annualized % of Aggregate

of (Square Minimum Rent Annualized

Tenant Leases Feet) at 12/31/04 Minimum Rent

Publix 49 2,183,532 $15,722,674 8.3%

Kroger 17 962,697 7,998,271 4.2%

Albertsons / Shaw’s 9 570,286 7,567,853 4.0%

Winn Dixie 16 730,442 5,059,331 2.7%

Wal-Mart 9 646,682 2,940,519 1.6%

Kmart 6 524,937 2,795,865 1.5%

H.E. Butt Grocery 4 256,262 2,775,355 1.5%

Blockbuster 29 170,092 2,673,625 1.4%

CVS Pharmacy 23 235,345 2,348,791 1.2%

Bed Bath & Beyond 7 227,689 2,192,531 1.2%

Subtotal 169 6,507,964 $52,074,815 27.6%

Remaining Tenants 3,168 12,132,104 136,616,661 72.4%

Total 3,337 18,640,068 $188,691,476 100.0%

12

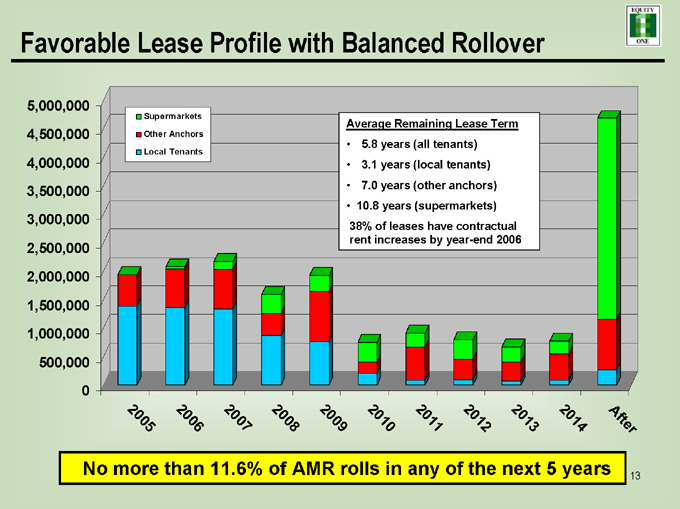

Favorable Lease Profile with Balanced Rollover

5,000,000 4,500,000 4,000,000 3,500,000 3,000,000 2,500,000 2,000,000 1,500,000 1,000,000 500,000 0

Supermarkets Other Anchors Local Tenants

Average Remaining Lease Term

5.8 years (all tenants) 3.1 years (local tenants) 7.0 years (other anchors) 10.8 years (supermarkets)

38% of leases have contractual rent increases by year-end 2006

After

2014

2013

2012

2011

2010

2009

2008

2007

2006

2005

No more than 11.6% of AMR rolls in any of the next 5 years 13

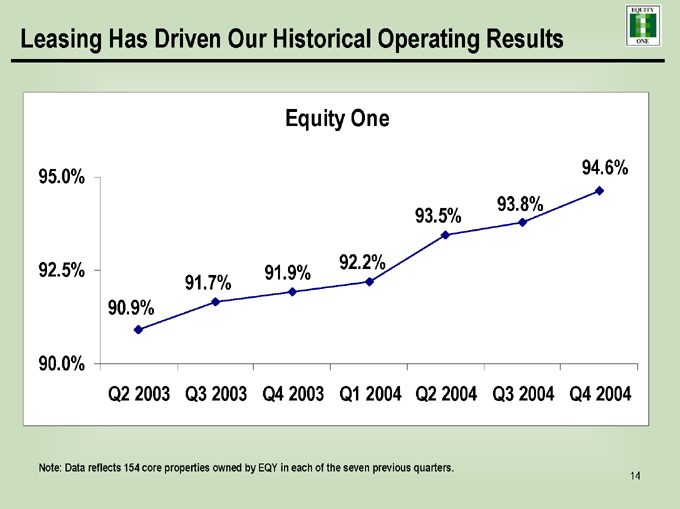

Leasing Has Driven Our Historical Operating Results

Equity One

95.0% 92.5% 90.0%

90.9%

91.7%

91.9%

92.2%

93.5%

93.8%

94.6%

Q2 2003 Q3 2003 Q4 2003 Q1 2004 Q2 2004 Q3 2004 Q4 2004

Note: Data reflects 154 core properties owned by EQY in each of the seven previous quarters.

14

15

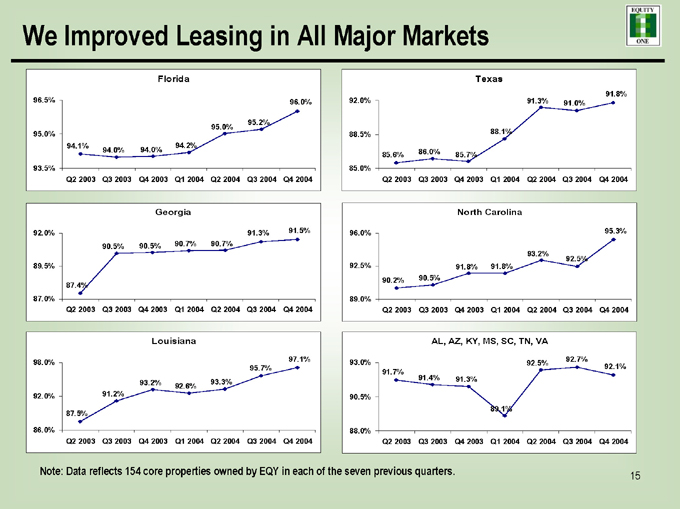

We Improved Leasing in All Major Markets

Florida

96.5% 96.0%

95.2% 95.0% 95.0% 94.1% 94.2% 94.0% 94.0%

93.5%

Q2 2003 Q3 2003 Q4 2003 Q1 2004 Q2 2004 Q3 2004 Q4 2004

Georgia

92.0% 91.3% 91.5% 90.5% 90.5% 90.7% 90.7%

89.5%

87.4% 87.0%

Q2 2003 Q3 2003 Q4 2003 Q1 2004 Q2 2004 Q3 2004 Q4 2004

Louisiana

98.0% 97.1% 95.7% 93.2% 93.3% 92.6% 92.0% 91.2% 87.5%

86.0%

Q2 2003 Q3 2003 Q4 2003 Q1 2004 Q2 2004 Q3 2004 Q4 2004

Texas

91.8% 92.0% 91.3% 91.0%

88.5% 88.1% 85.6% 86.0% 85.7% 85.0%

Q2 2003 Q3 2003 Q4 2003 Q1 2004 Q2 2004 Q3 2004 Q4 2004

North Carolina

96.0% 95.3%

93.2%

92.5% 92.5% 91.8% 91.8% 90.2% 90.5%

89.0%

Q2 2003 Q3 2003 Q4 2003 Q1 2004 Q2 2004 Q3 2004 Q4 2004

AL, AZ, KY, MS, SC, TN, VA

93.0% 92.7% 92.5%

92.1% 91.7% 91.4% 91.3% 90.5% 89.1%

88.0%

Q2 2003 Q3 2003 Q4 2003 Q1 2004 Q2 2004 Q3 2004 Q4 2004

Note: Data reflects 154 core properties owned by EQY in each of the seven previous quarters.

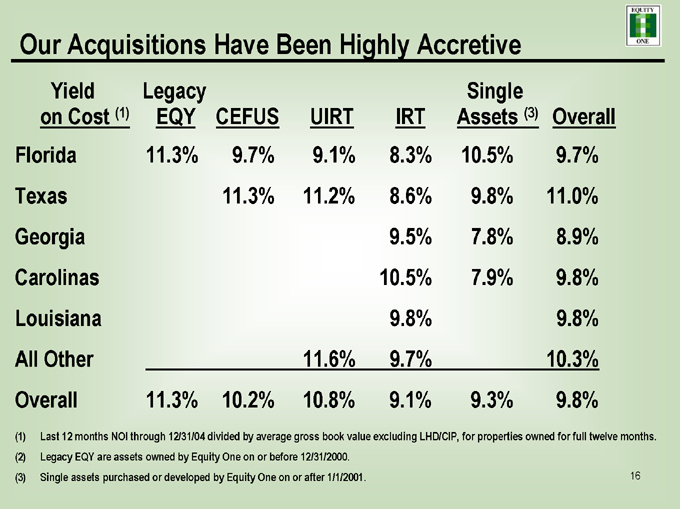

(1) Last 12 months NOI through 12/31/04 divided by average gross book value excluding LHD/CIP, for properties owned for full twelve months. (2) Legacy EQY are assets owned by Equity One on or before 12/31/2000.

(3) Single assets purchased or developed by Equity One on or after 1/1/2001. 16

Our Acquisitions Have Been Highly Accretive

Yield Legacy Single

on Cost (1) EQY CEFUS UIRT IRT Assets (3) Overall

Florida 11.3% 9.7% 9.1% 8.3% 10.5% 9.7%

Texas 11.3% 11.2% 8.6% 9.8% 11.0%

Georgia 9.5% 7.8% 8.9%

Carolinas 10.5% 7.9% 9.8%

Louisiana 9.8% 9.8%

All Other 11.6% 9.7% 10.3%

Overall 11.3% 10.2% 10.8% 9.1% 9.3% 9.8%

17

Completed Ground-up Developments

Miami, Florida Completed Q4 2003 96.1% leased @ 12/31/04

11.0% yield based on 2005 budget

PLAZA ALEGRE

Atlanta, Georgia Completed Q4 2003 98.5% leased @ 12/31/04 9.2% yield based on 2005 budget

SHOPS OF HUNTCREST

18

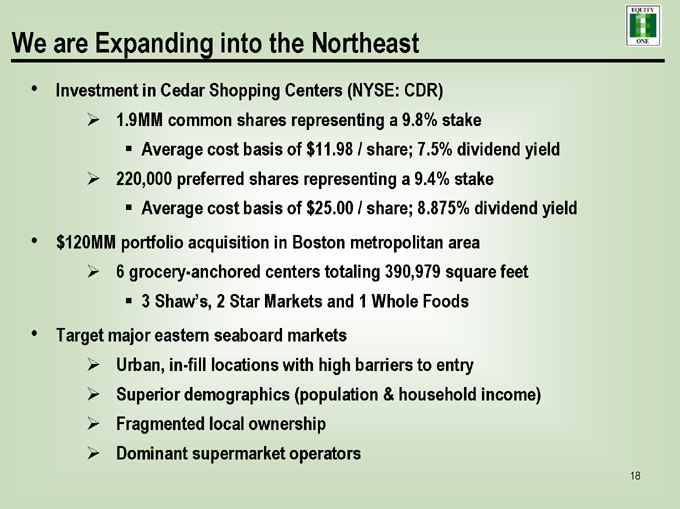

We are Expanding into the Northeast

Investment in Cedar Shopping Centers (NYSE: CDR)

1.9MM common shares representing a 9.8% stake

Average cost basis of $11.98 / share; 7.5% dividend yield

220,000 preferred shares representing a 9.4% stake

Average cost basis of $25.00 / share; 8.875% dividend yield $120MM portfolio acquisition in Boston metropolitan area

6 grocery-anchored centers totaling 390,979 square feet

3 Shaw’s, 2 Star Markets and 1 Whole Foods

Target major eastern seaboard markets

Urban, in-fill locations with high barriers to entry

Superior demographics (population & household income) Fragmented local ownership Dominant supermarket operators

19

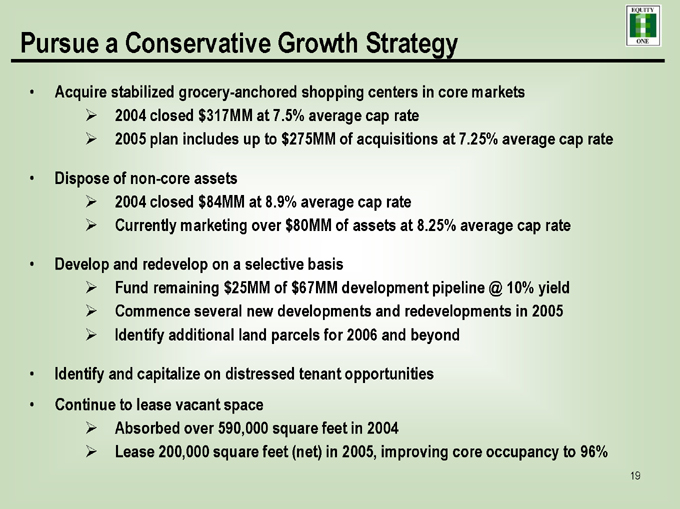

Pursue a Conservative Growth Strategy

Acquire stabilized grocery-anchored shopping centers in core markets

2004 closed $317MM at 7.5% average cap rate

2005 plan includes up to $275MM of acquisitions at 7.25% average cap rate

Dispose of non-core assets

2004 closed $84MM at 8.9% average cap rate

Currently marketing over $80MM of assets at 8.25% average cap rate

Develop and redevelop on a selective basis

Fund remaining $25MM of $67MM development pipeline @ 10% yield Commence several new developments and redevelopments in 2005 Identify additional land parcels for 2006 and beyond

Identify and capitalize on distressed tenant opportunities Continue to lease vacant space

Absorbed over 590,000 square feet in 2004

Lease 200,000 square feet (net) in 2005, improving core occupancy to 96%

20

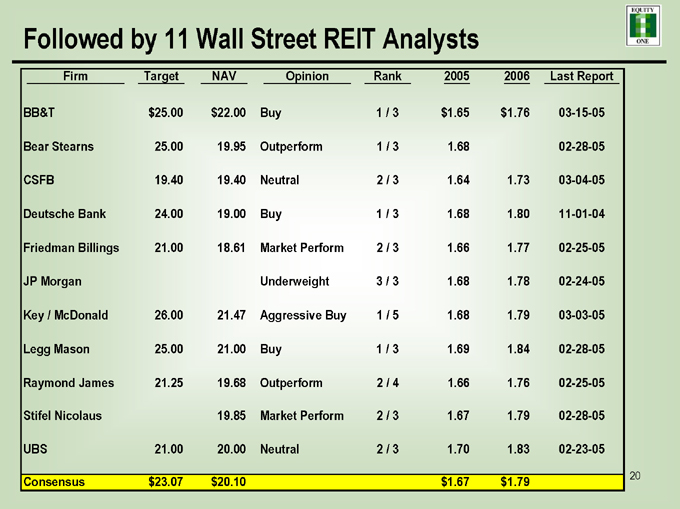

Followed by 11 Wall Street REIT Analysts

Firm Target NAV Opinion Rank 2005 2006 Last Report

BB&T $25.00 $22.00 Buy 1 / 3 $1.65 $1.76 03-15-05

Bear Stearns 25.00 19.95 Outperform 1 / 3 1.68 02-28-05

CSFB 19.40 19.40 Neutral 2 / 3 1.64 1.73 03-04-05

Deutsche Bank 24.00 19.00 Buy 1 / 3 1.68 1.80 11-01-04

Friedman Billings 21.00 18.61 Market Perform 2 / 3 1.66 1.77 02-25-05

JP Morgan Underweight 3 / 3 1.68 1.78 02-24-05

Key / McDonald 26.00 21.47 Aggressive Buy 1 / 5 1.68 1.79 03-03-05

Legg Mason 25.00 21.00 Buy 1 / 3 1.69 1.84 02-28-05

Raymond James 21.25 19.68 Outperform 2 / 4 1.66 1.76 02-25-05

Stifel Nicolaus 19.85 Market Perform 2 / 3 1.67 1.79 02-28-05

UBS 21.00 20.00 Neutral 2 / 3 1.70 1.83 02-23-05

Consensus $23.07 $20.10 $1.67 $1.79

21

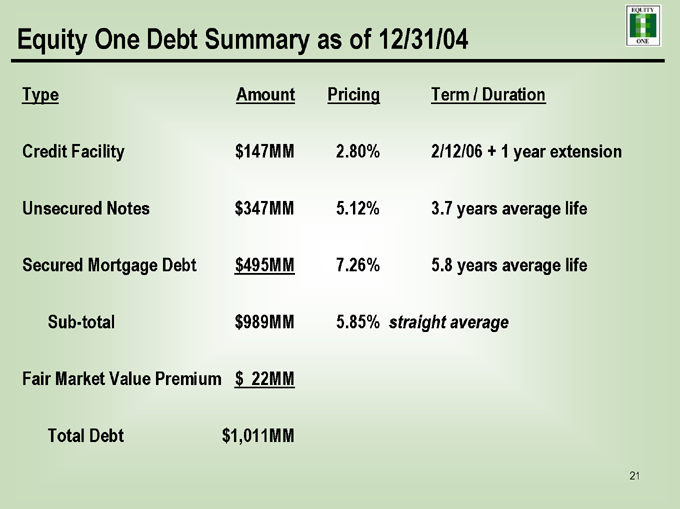

Equity One Debt Summary as of 12/31/04

Type Amount Pricing Term / Duration

Credit Facility $147MM 2.80% 2/12/06 + 1 year extension

Unsecured Notes $347MM 5.12% 3.7 years average life

Secured Mortgage Debt $495MM 7.26% 5.8 years average life

Sub-total $989MM 5.85% straight average

Fair Market Value Premium $22MM

Total Debt $1,011MM

Credit Facilities Unsecured Notes Balloon Amortization

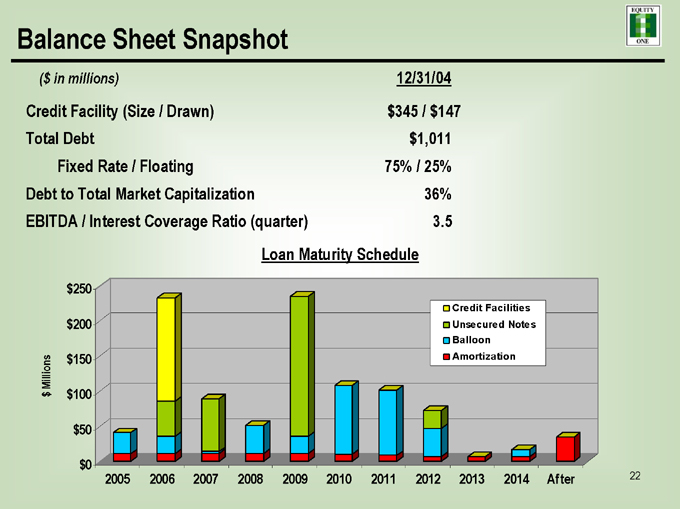

Balance Sheet Snapshot

($in millions) 12/31/04

Credit Facility (Size / Drawn) $345 / $147

Total Debt $1,011

Fixed Rate / Floating 75% / 25%

Debt to Total Market Capitalization 36%

EBITDA / Interest Coverage Ratio (quarter) 3.5

Loan Maturity Schedule $250 $200 $150 $100 $50 $0 $Millions

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 After

22

23

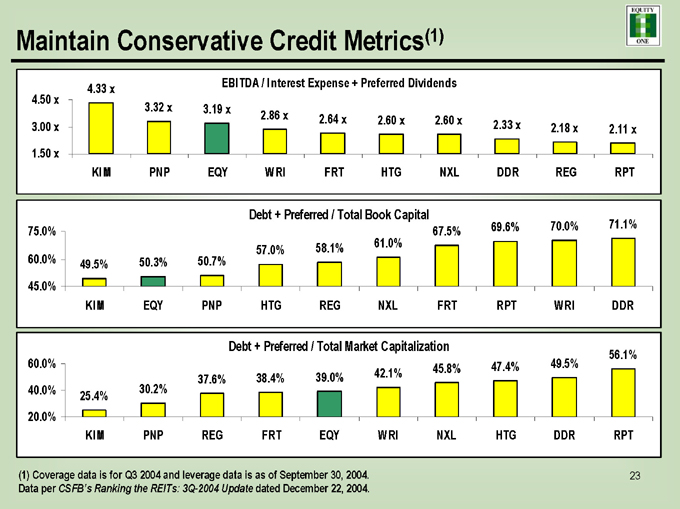

Maintain Conservative Credit Metrics(1)

4.33x EBITDA / Interest Expense + Preferred Dividends 4.50x 3.32x 3.19x 2.86x 2.64x 2.60x 2.60x

3.00x 2.33x 2.18x 2.11x 1.50x KIM PNP EQY WRI FRT HTG NXL DDR REG RPT

Debt + Preferred / Total Book Capital

69.6% 70.0% 71.1% 75.0% 67.5% 58.1% 61.0% 57.0% 60.0% 49.5% 50.3% 50.7% 45.0% KIM EQY PNP HTG REG NXL FRT RPT WRI DDR

Debt + Preferred / Total Market Capitalization

56.1% 60.0% 45.8% 47.4% 49.5% 37.6% 38.4% 39.0% 42.1% 40.0% 30.2% 25.4% 20.0% KIM PNP REG FRT EQY WRI NXL HTG DDR RPT

(1) Coverage data is for Q3 2004 and leverage data is as of September 30, 2004. Data per CSFB’s Ranking the REITs: 3Q-2004 Update dated December 22, 2004.

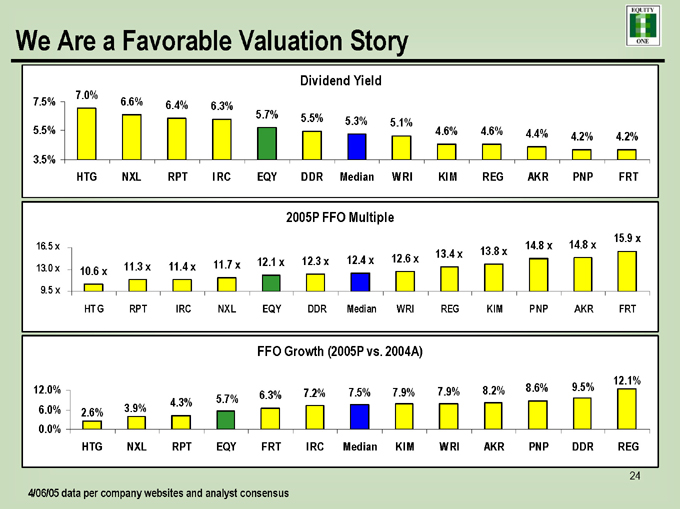

4/06/05 data per company websites and analyst consensus

We Are a Favorable Valuation Story

Dividend Yield

7.0%

7.5% 6.6% 6.4% 6.3%

5.7% 5.5%

5.3% 5.1%

5.5% 4.6% 4.6% 4.4%

4.2% 4.2% 3.5% HTG NXL RPT IRC EQY DDR Median WRI KIM REG AKR PNP FRT

2005P FFO Multiple

15.9x 16.5x 14.8x 14.8x 13.4x 13.8x 12.1x 12.3x 12.4x 12.6x 13.0x 11.3x 11.4x 11.7x 10.6x

9.5x

HTG RPT IRC NXL EQY DDR Median WRI REG KIM PNP AKR FRT

FFO Growth (2005P vs. 2004A)

12.1% 12.0% 7.5% 7.9% 7.9% 8.2% 8.6% 9.5% 5.7% 6.3% 7.2% 3.9% 4.3% 6.0% 2.6% 0.0% HTG NXL RPT EQY FRT IRC Median KIM WRI AKR PNP DDR REG

24

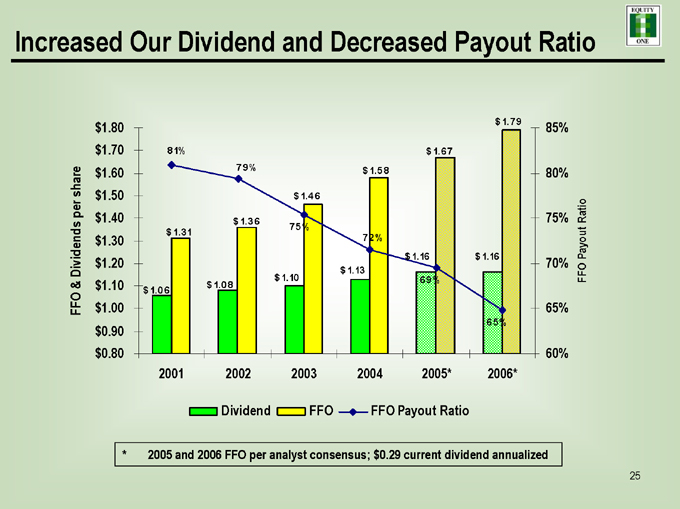

FFO & Dividends per share

Increased Our Dividend and Decreased Payout Ratio $1.80 $1.70 $1.60 $1.50 $1.40 $1.30 $1.20 $1.10 $1.00 $0.90 $0.80 $1.79 85% 81% $1.67 79% $1.58 80% $1.46 $1.36 75% Ratio 75%

$1.31 Payout

72% $1.16 $1.16 70% $1.13 $1.10 69% FFO $1.08 $1.06

65%

65%

60% 2001 2002 2003 2004 2005* 2006*

Dividend FFO FFO Payout Ratio

* 2005 and 2006 FFO per analyst consensus; $0.29 current dividend annualized

25

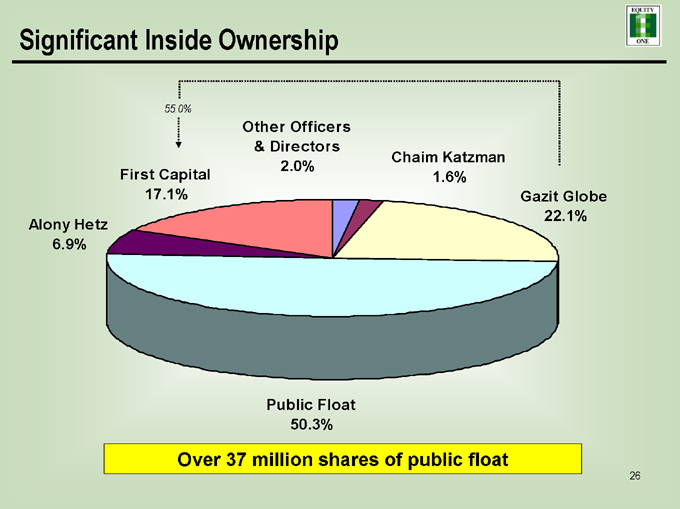

Significant Inside Ownership

55.0%

Other Officers & Directors

Chaim Katzman 2.0% First Capital 1.6%

17.1% Gazit Globe 22.1% Alony Hetz 6.9%

Public Float 50.3%

Over 37 million shares of public float

26

Why Equity One?

Established mid-cap REIT Experienced management team Most desirable asset class Excellent market demographics

Significant tenant diversification with balanced lease rollover Proven growth strategy Conservative and flexible balance sheet Favorable valuation metrics Attractive dividend and yield characteristics

27