Exhibit 99.2

1Q 2015 Stockholder Supplement May 6, 2015

Safe Harbor Notice This news release and our public documents to which we refer contain or incorporate by reference certain forward-looking statements which are based on various assumptions (some of which are beyond our control) and may be identified by reference to a future period or periods or by the use of forward-looking terminology, such as "may," "will," "believe," "expect," "anticipate," "continue," or similar terms or variations on those terms or the negative of those terms. Actual results could differ materially from those set forth in forward-looking statements due to a variety of factors, including, but not limited to, changes in interest rates; changes in the yield curve; changes in prepayment rates; the availability of mortgage-backed securities and other securities for purchase; the availability of financing and, if available, the terms of any financings; changes in the market value of our assets; changes in business conditions and the general economy; our ability to grow the commercial mortgage business; credit risks related to our investments in commercial real estate assets and corporate debt; our ability to consummate any contemplated investment opportunities; changes in government regulations affecting our business; our ability to maintain our qualification as a REIT for federal income tax purposes; our ability to maintain our exemption from registration under the Investment Company Act of 1940, as amended; risks associated with the businesses of our subsidiaries, including the investment advisory business of a wholly-owned subsidiary and the broker-dealer business of a wholly-owned subsidiary. For a discussion of the risks and uncertainties which could cause actual results to differ from those contained in the forward-looking statements, see "Risk Factors" in our most recent Annual Report on Form 10-K and any subsequent Quarterly Reports on Form 10-Q. We do not undertake, and specifically disclaim any obligation, to publicly release the result of any revisions which may be made to any forward-looking statements to reflect the occurrence of anticipated or unanticipated events or circumstances after the date of such statements. 1

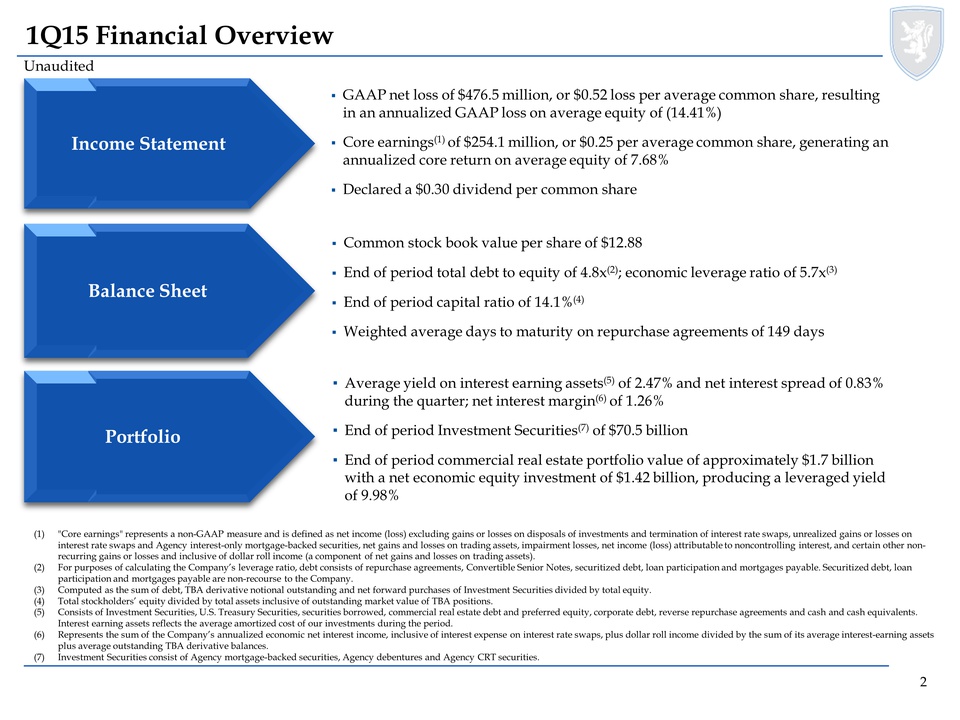

1Q15 Financial Overview Unaudited GAAP net loss of $476.5 million, or $0.52 loss per average common share, resulting in an annualized GAAP loss on average equity of (14.41%) Core earnings(1) of $254.1 million, or $0.25 per average common share, generating an annualized core return on average equity of 7.68% Declared a $0.30 dividend per common share Common stock book value per share of $12.88 End of period total debt to equity of 4.8x(2); economic leverage ratio of 5.7x(3) End of period capital ratio of 14.1%(4) Weighted average days to maturity on repurchase agreements of 149 days Average yield on interest earning assets(5) of 2.47% and net interest spread of 0.83% during the quarter; net interest margin(6) of 1.26% End of period Investment Securities(7) of $70.5 billion End of period commercial real estate portfolio value of approximately $1.7 billion with a net economic equity investment of $1.42 billion, producing a leveraged yield of 9.98% Income Statement Balance Sheet Portfolio (1) "Core earnings" represents a non-GAAP measure and is defined as net income (loss) excluding gains or losses on disposals of investments and termination of interest rate swaps, unrealized gains or losses on interest rate swaps and Agency interest-only mortgage-backed securities, net gains and losses on trading assets, impairment losses, net income (loss) attributable to noncontrolling interest, and certain other nonrecurring gains or losses and inclusive of dollar roll income (a component of net gains and losses on trading assets). (2) For purposes of calculating the Company’s leverage ratio, debt consists of repurchase agreements, Convertible Senior Notes, securitized debt, loan participation and mortgages payable. Securitized debt, loan participation and mortgages payable are non-recourse to the Company. (3) Computed as the sum of debt, TBA derivative notional outstanding and net forward purchases of Investment Securities divided by total equity. (4) Total stockholders’ equity divided by total assets inclusive of outstanding market value of TBA positions. (5) Consists of Investment Securities, U.S. Treasury Securities, securities borrowed, commercial real estate debt and preferred equity, corporate debt, reverse repurchase agreements and cash and cash equivalents. Interest earning assets reflects the average amortized cost of our investments during the period. (6) Represents the sum of the Company’s annualized economic net interest income, inclusive of interest expense on interest rate swaps, plus dollar roll income divided by the sum of its average interest-earning assets plus average outstanding TBA derivative balances. (7) Investment Securities consist of Agency mortgage-backed securities, Agency debentures and Agency CRT securities. 2

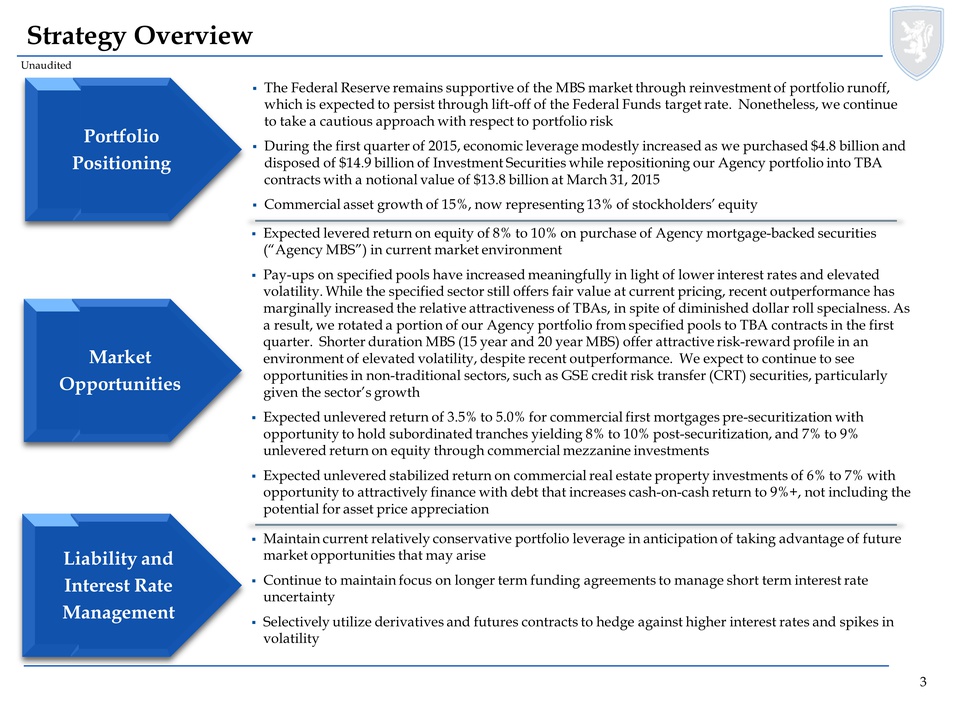

Strategy Overview Unaudited Portfolio Positioning Market Opportunities Liability and Interest Rate Management The Federal Reserve remains supportive of the MBS market through reinvestment of portfolio runoff, which is expected to persist through lift-off of the Federal Funds target rate. Nonetheless, we continue to take a cautious approach with respect to portfolio risk During the first quarter of 2015, economic leverage modestly increased as we purchased $4.8 billion and disposed of $14.9 billion of Investment Securities while repositioning our Agency portfolio into TBA contracts with a notional value of $13.8 billion at March 31, 2015 Commercial asset growth of 15%, now representing 13% of stockholders’ equity Expected levered return on equity of 8% to 10% on purchase of Agency mortgage-backed securities (“Agency MBS”) in current market environment Pay-ups on specified pools have increased meaningfully in light of lower interest rates and elevated volatility. While the specified sector still offers fair value at current pricing, recent outperformance has marginally increased the relative attractiveness of TBAs, in spite of diminished dollar roll specialness. As a result, we rotated a portion of our Agency portfolio from specified pools to TBA contracts in the first quarter. Shorter duration MBS (15 year and 20 year MBS) offer attractive risk-reward profile in an environment of elevated volatility, despite recent outperformance. We expect to continue to see opportunities in non-traditional sectors, such as GSE credit risk transfer (CRT) securities, particularly given the sector’s growth Expected unlevered return of 3.5% to 5.0% for commercial first mortgages pre-securitization with opportunity to hold subordinated tranches yielding 8% to 10% post-securitization, and 7% to 9% unlevered return on equity through commercial mezzanine investments Expected unlevered stabilized return on commercial real estate property investments of 6% to 7% with opportunity to attractively finance with debt that increases cash-on-cash return to 9%+, not including the potential for asset price appreciation Maintain current relatively conservative portfolio leverage in anticipation of taking advantage of future market opportunities that may arise Continue to maintain focus on longer term funding agreements to manage short term interest rate uncertainty Selectively utilize derivatives and futures contracts to hedge against higher interest rates and spikes in volatility 3

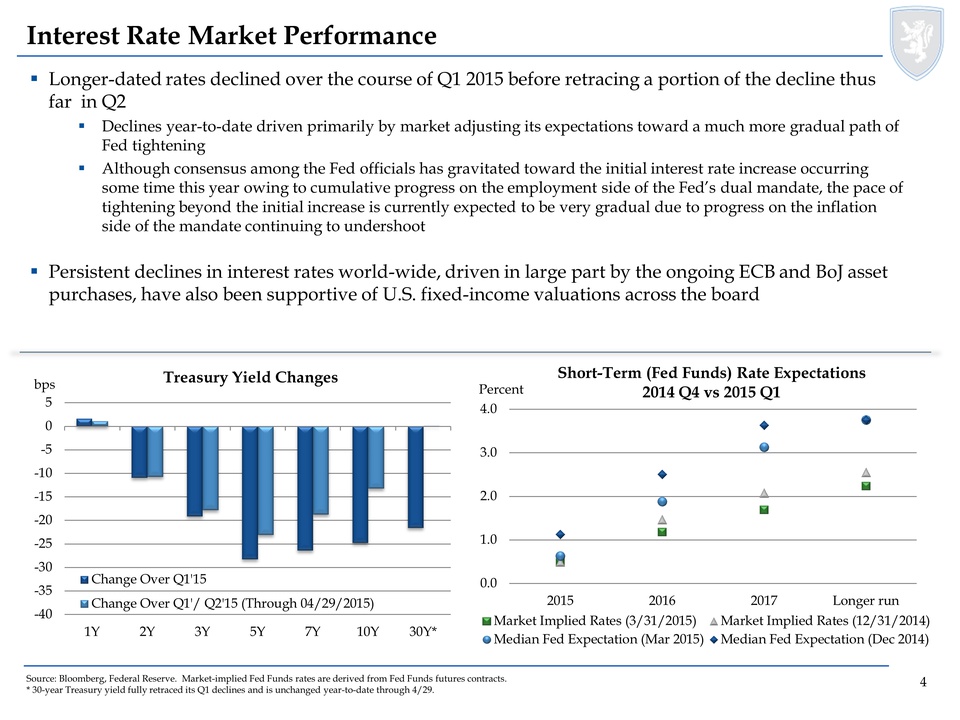

Interest Rate Market Performance Longer-dated rates declined over the course of Q1 2015 before retracing a portion of the decline thus far in Q2 Declines year-to-date driven primarily by market adjusting its expectations toward a much more gradual path of Fed tightening Although consensus among the Fed officials has gravitated toward the initial interest rate increase occurring some time this year owing to cumulative progress on the employment side of the Fed’s dual mandate, the pace of tightening beyond the initial increase is currently expected to be very gradual due to progress on the inflation side of the mandate continuing to undershoot Persistent declines in interest rates world-wide, driven in large part by the ongoing ECB and BoJ asset purchases, have also been supportive of U.S. fixed-income valuations across the board Treasury Yield Changes Short-Term (Fed Funds) Rate Expectations 2014 Q4 vs 2015 Q1 Source: Bloomberg, Federal Reserve. Market-implied Fed Funds rates are derived from Fed Funds futures contracts. * 30-year Treasury yield fully retraced its Q1 declines and is unchanged year-to-date through 4/29. 4

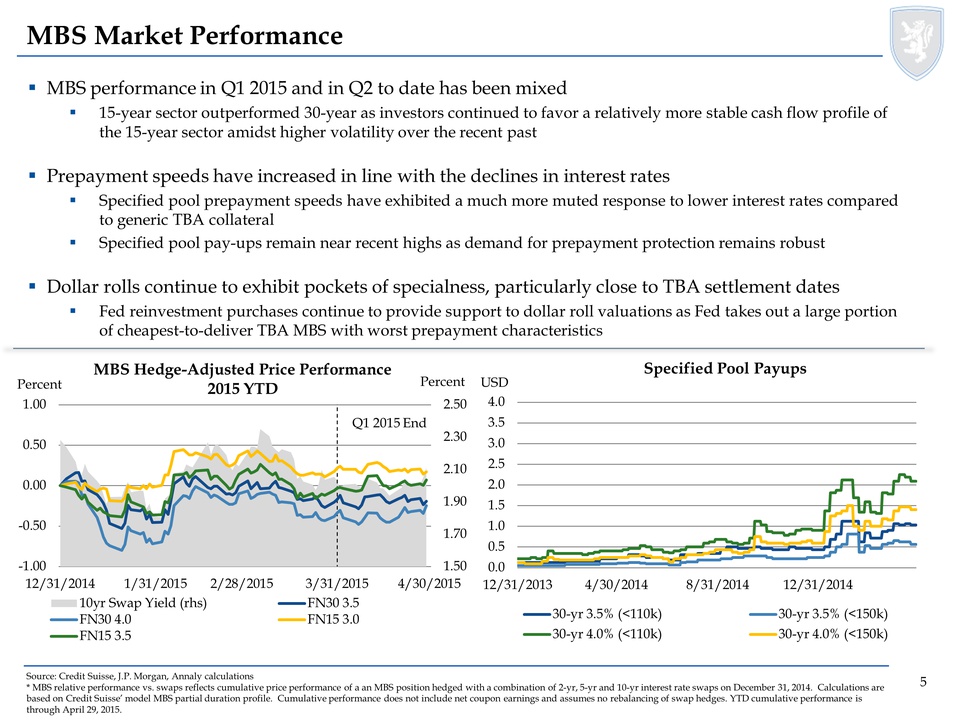

MBS Market Performance MBS performance in Q1 2015 and in Q2 to date has been mixed 15-year sector outperformed 30-year as investors continued to favor a relatively more stable cash flow profile of the 15-year sector amidst higher volatility over the recent past Prepayment speeds have increased in line with the declines in interest rates Specified pool prepayment speeds have exhibited a much more muted response to lower interest rates compared to generic TBA collateral Specified pool pay-ups remain near recent highs as demand for prepayment protection remains robust Dollar rolls continue to exhibit pockets of specialness, particularly close to TBA settlement dates Fed reinvestment purchases continue to provide support to dollar roll valuations as Fed takes out a large portion of cheapest-to-deliver TBA MBS with worst prepayment characteristics MBS Hedge-Adjusted Price Performance 2015 YTD Specified Pool Payups Source: Credit Suisse, J.P. Morgan, Annaly calculations * MBS relative performance vs. swaps reflects cumulative price performance of a an MBS position hedged with a combination of 2-yr, 5-yr and 10-yr interest rate swaps on December 31, 2014. Calculations are based on Credit Suisse’ model MBS partial duration profile. Cumulative performance does not include net coupon earnings and assumes no rebalancing of swap hedges. YTD cumulative performance is through April 29, 2015. 5

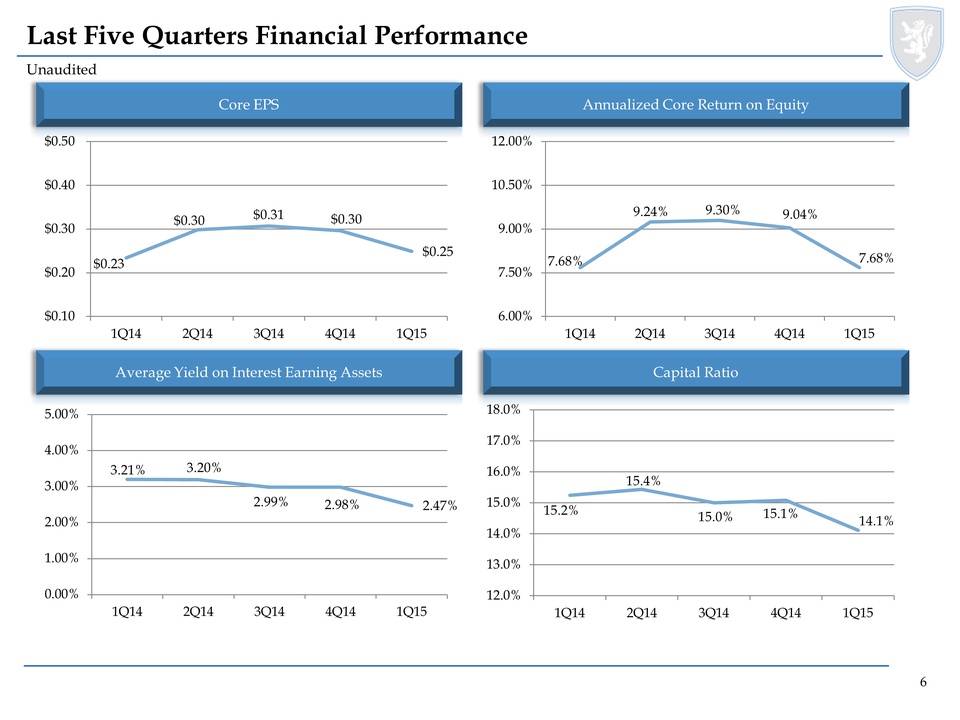

Last Five Quarters Financial Performance Unaudited Core EPS Annualized Core Return on Equity Average Yield on Interest Earning Assets Capital Ratio 6

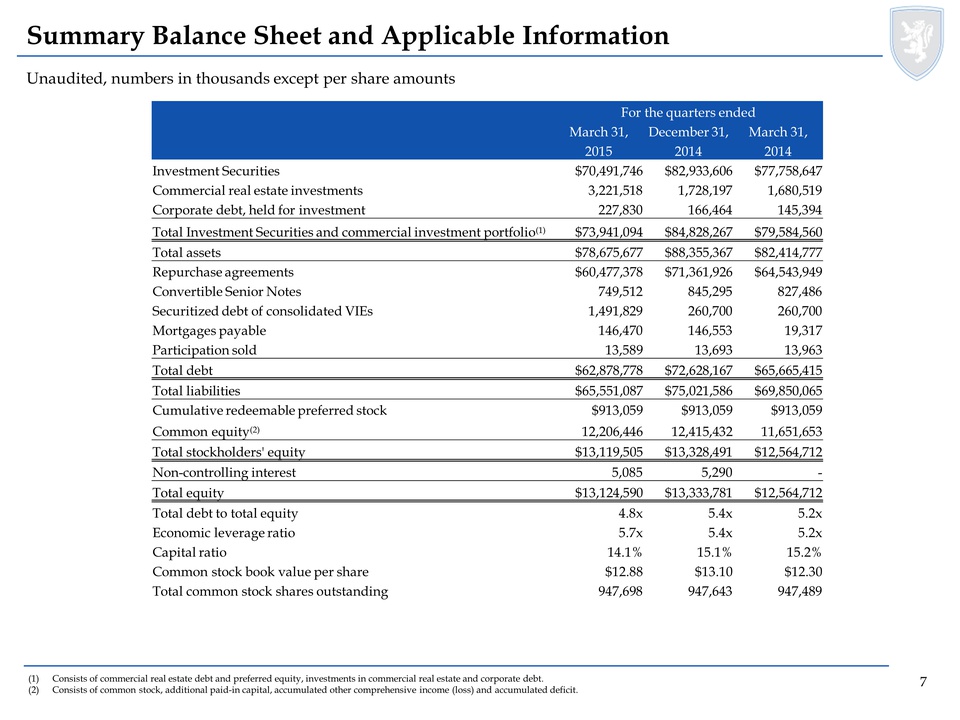

Summary Balance Sheet and Applicable Information Unaudited, numbers in thousands except per share amounts For the quarters ended March 31, December 31, March 31, 2015 2014 2014 Investment Securities $70,491,746 $82,933,606 $77,758,647 Commercial real estate investments 3,221,518 1,728,197 1,680,519 Corporate debt, held for investment 227,830 166,464 145,394 Total Investment Securities and commercial investment portfolio(1) $73,941,094 $84,828,267 $79,584,560 Total assets $78,675,677 $88,355,367 $82,414,777 Repurchase agreements $60,477,378 $71,361,926 $64,543,949 Convertible Senior Notes 749,512 845,295 827,486 Securitized debt of consolidated VIEs 1,491,829 260,700 260,700 Mortgages payable 146,470 146,553 19,317 Participation sold 13,589 13,693 13,963 Total debt $62,878,778 $72,628,167 $65,665,415 Total liabilities $65,551,087 $75,021,586 $69,850,065 Cumulative redeemable preferred stock $913,059 $913,059 $913,059 Common equity(2) 12,206,446 12,415,432 11,651,653 Total stockholders' equity $13,119,505 $13,328,491 $12,564,712 Non-controlling interest 5,085 5,290 - Total equity $13,124,590 $13,333,781 $12,564,712 Total debt to total equity 4.8x 5.4x 5.2x Economic leverage ratio 5.7x 5.4x 5.2x Capital ratio 14.1% 15.1% 15.2% Common stock book value per share $12.88 $13.10 $12.30 Total common stock shares outstanding 947,698 947,643 947,489 (1) Consists of commercial real estate debt and preferred equity, investments in commercial real estate and corporate debt. (2) Consists of common stock, additional paid-in capital, accumulated other comprehensive income (loss) and accumulated deficit. 7

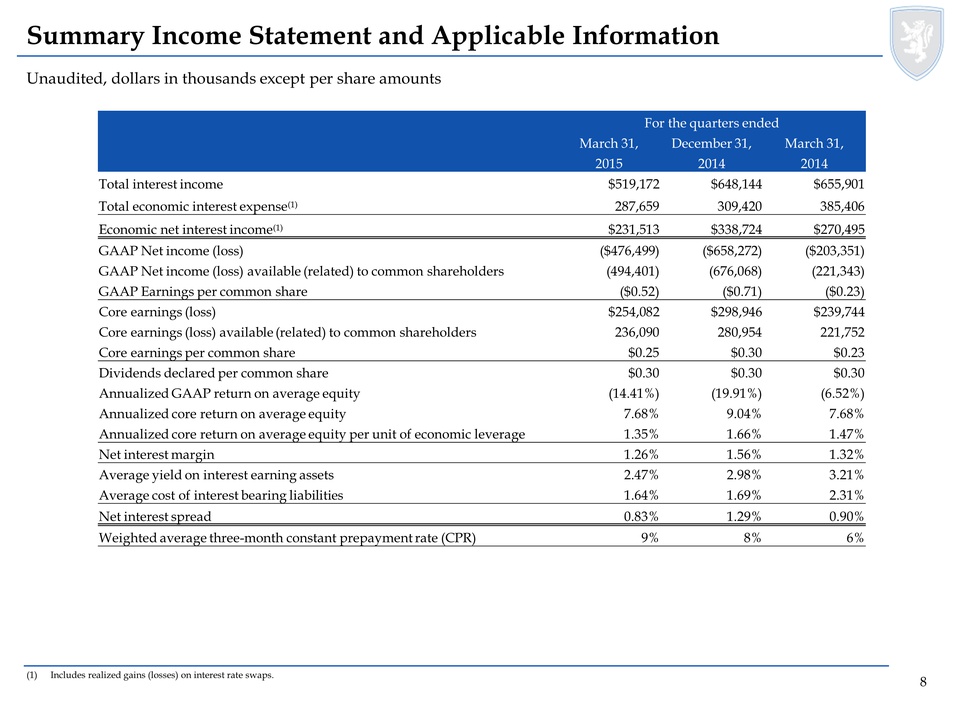

Summary Income Statement and Applicable Information Unaudited, dollars in thousands except per share amounts For the quarters ended March 31, December 31, March 31, 2015 2014 2014 Total interest income $519,172 $648,144 $655,901 Total economic interest expense(1) 287,659 309,420 385,406 Economic net interest income(1) $231,513 $338,724 $270,495 GAAP Net income (loss) ($476,499) ($658,272) ($203,351) GAAP Net income (loss) available (related) to common shareholders (494,401) (676,068) (221,343) GAAP Earnings per common share ($0.52) ($0.71) ($0.23) Core earnings (loss) $254,082 $298,946 $239,744 Core earnings (loss) available (related) to common shareholders 236,090 280,954 221,752 Core earnings per common share $0.25 $0.30 $0.23 Dividends declared per common share $0.30 $0.30 $0.30 Annualized GAAP return on average equity (14.41%) (19.91%) (6.52%) Annualized core return on average equity 7.68% 9.04% 7.68% Annualized core return on average equity per unit of economic leverage 1.35% 1.66% 1.47% Net interest margin 1.26% 1.56% 1.32% Average yield on interest earning assets 2.47% 2.98% 3.21% Average cost of interest bearing liabilities 1.64% 1.69% 2.31% Net interest spread 0.83% 1.29% 0.90% Weighted average three-month constant prepayment rate (CPR) 9% 8% 6% (1) Includes realized gains (losses) on interest rate swaps. 8

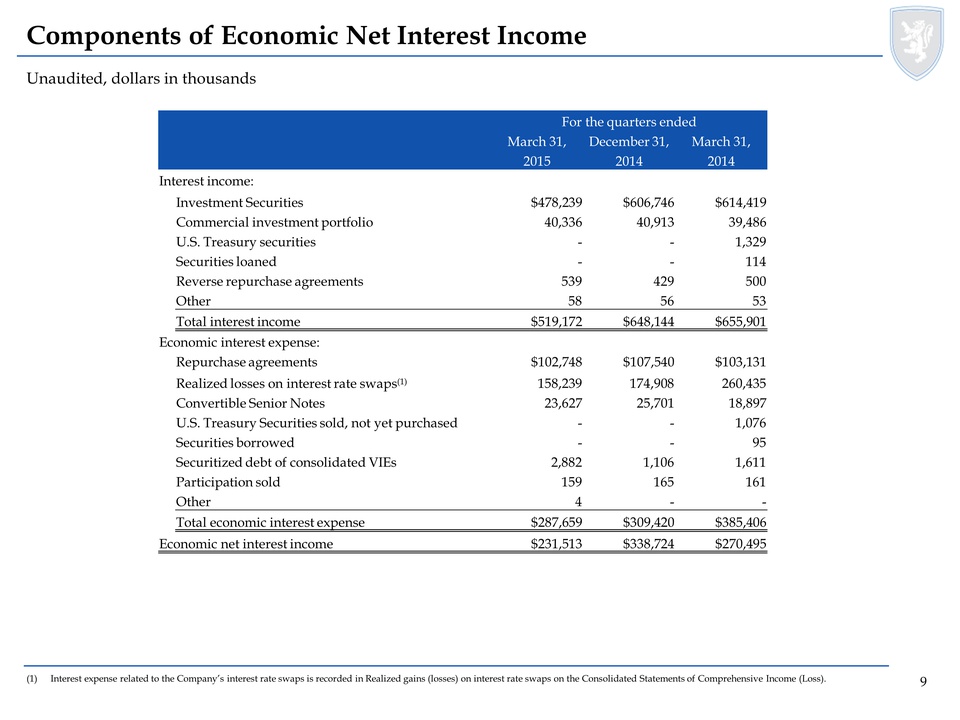

Components of Economic Net Interest Income Unaudited, dollars in thousands For the quarters ended March 31, December 31, March 31, 2015 2014 2014 Interest income: Investment Securities $478,239 $606,746 $614,419 Commercial investment portfolio 40,336 40,913 39,486 U.S. Treasury securities - - 1,329 Securities loaned - - 114 Reverse repurchase agreements 539 429 500 Other 58 56 53 Total interest income $519,172 $648,144 $655,901 Economic interest expense: Repurchase agreements $102,748 $107,540 $103,131 Realized losses on interest rate swaps(1) 158,239 174,908 260,435 Convertible Senior Notes 23,627 25,701 18,897 U.S. Treasury Securities sold, not yet purchased - - 1,076 Securities borrowed - - 95 Securitized debt of consolidated VIEs 2,882 1,106 1,611 Participation sold 159 165 161 Other 4 - - Total economic interest expense $287,659 $309,420 $385,406 Economic net interest income $231,513 $338,724 $270,495 (1) Interest expense related to the Company’s interest rate swaps is recorded in Realized gains (losses) on interest rate swaps on the Consolidated Statements of Comprehensive Income (Loss). 9

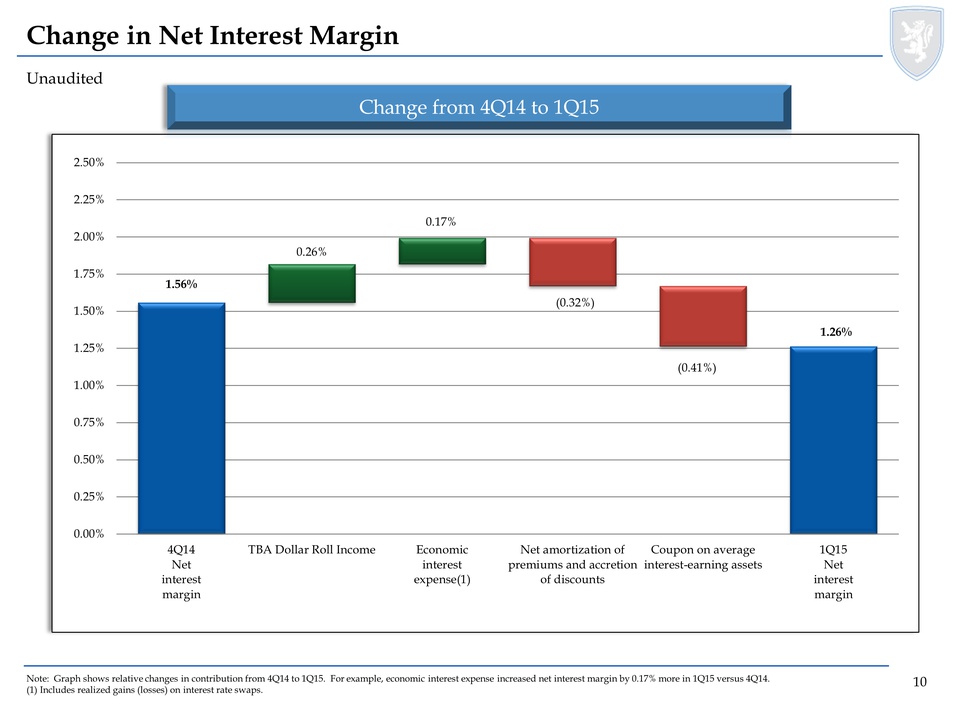

Change in Net Interest Margin Unaudited Change from 4Q14 to 1Q15 1.26% 1.56% 4Q14 Net interest margin TBA Dollar Roll Income Economic interest expense(1) Net amortization of premiums and accretion of discounts Coupon on average interest-earning assets 1Q15 Net interest margin (0.32%) (0.41%) 0.17% 0.26% Note: Graph shows relative changes in contribution from 4Q14 to 1Q15. For example, economic interest expense increased net interest margin by 0.17% more in 1Q15 versus 4Q14. (1) Includes realized gains (losses) on interest rate swaps. 10

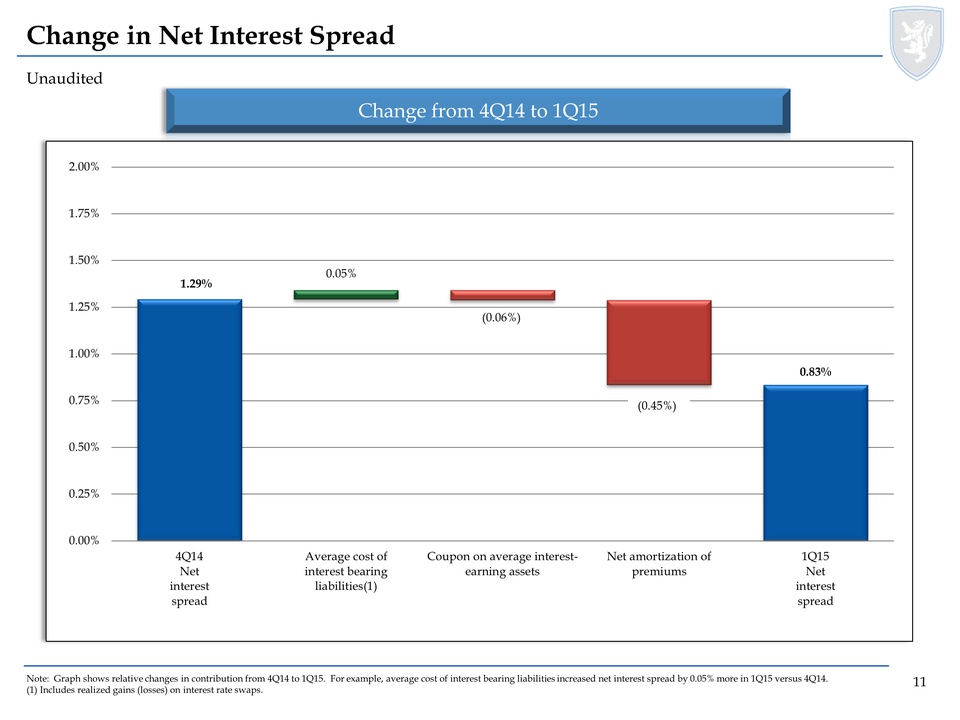

Change in Net Interest Spread Unaudited Change from 4Q14 to 1Q15 0.83% 1.29% 4Q14 Net interest spread Average cost of interest bearing liabilities(1) Coupon on average interest-earning assets Net amortization of premiums 1Q15 Net interest spread 0.05% (0.06%) (0.45%) Note: Graph shows relative changes in contribution from 4Q14 to 1Q15. For example, average cost of interest bearing liabilities increased net interest spread by 0.05% more in 1Q15 versus 4Q14. (1) Includes realized gains (losses) on interest rate swaps. 11

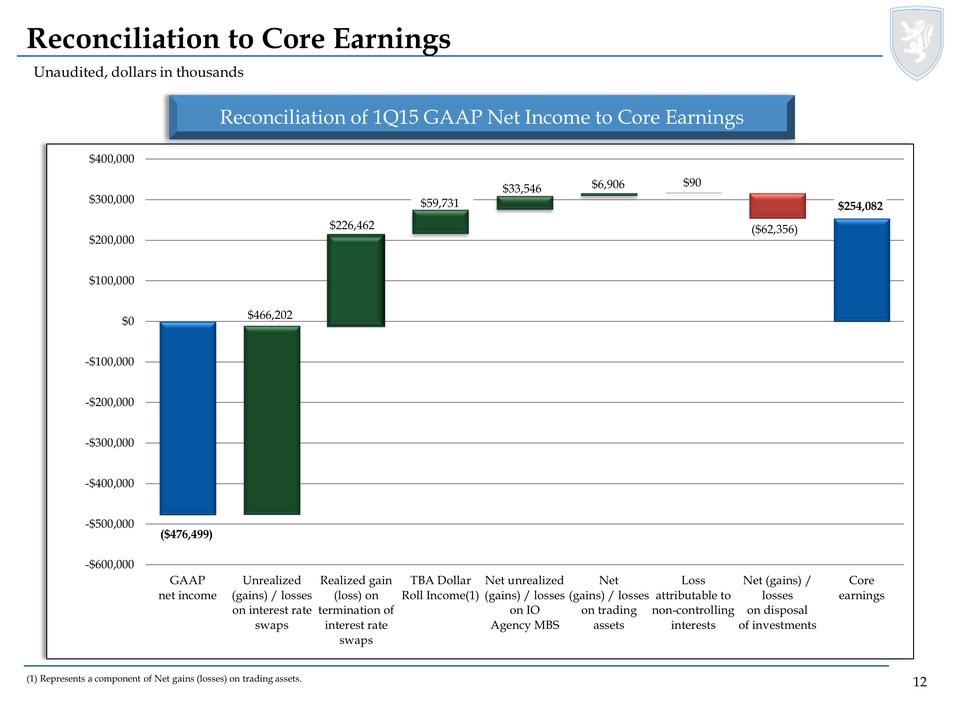

Reconciliation to Core Earnings Unaudited, dollars in thousands Reconciliation of 1Q15 GAAP Net Income to Core Earnings $254,082 ($476,499) GAAP net income Unrealized (gains) / losses on interest rate swaps Realized gain (loss) on termination of interest rate swaps TBA Dollar Roll Income(1) Net unrealized (gains) / losses on IO Agency MBS Net (gains) / losses on trading assets Loss attributable to non-controlling interests Net (gains) / losses on disposal of investments Core earnings $33,546 $6,906 $466,202 $59,731 $90 $226,462 ($62,356) (1) Represents a component of Net gains (losses) on trading assets. 12

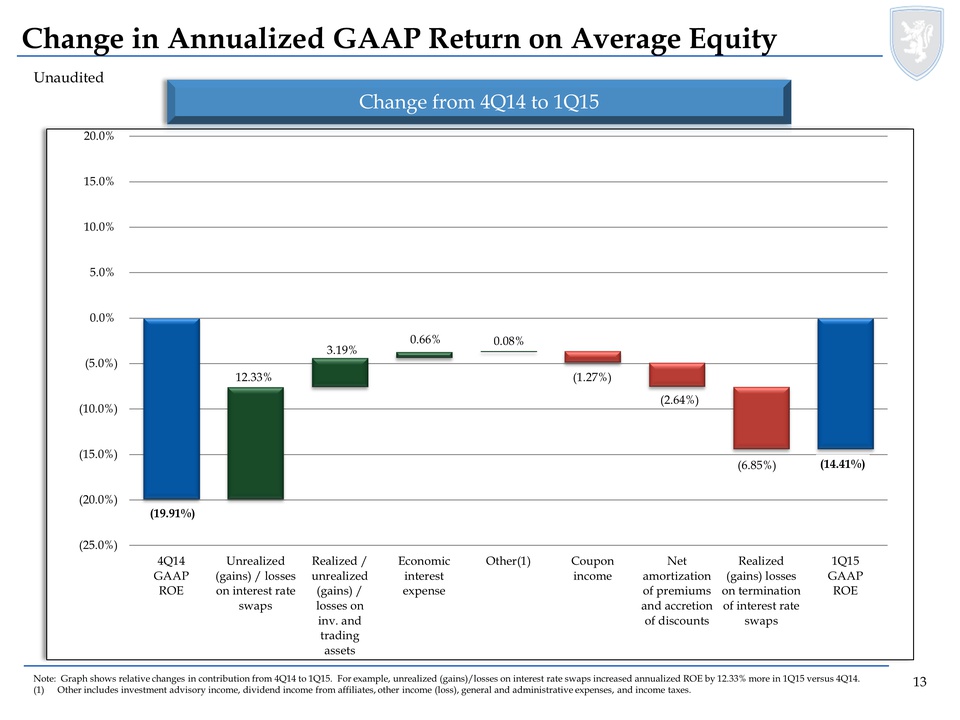

Change in Annualized GAAP Return on Average Equity Unaudited Change from 4Q14 to 1Q15 (14.41%) (19.91%) 4Q14 GAAP ROE Unrealized (gains) / losses on interest rate swaps Realized / unrealized (gains) / losses on inv. and trading assets Economic interest expense Other(1) Coupon income Net amortization of premiums and accretion of discounts Realized (gains) losses on termination of interest rate swaps 1Q15 GAAP ROE (1.27%) 0.66% 0.08% 3.19% 12.33% (6.85%) (2.64%) Note: Graph shows relative changes in contribution from 4Q14 to 1Q15. For example, unrealized (gains)/losses on interest rate swaps increased annualized ROE by 12.33% more in 1Q15 versus 4Q14. (1) Other includes investment advisory income, dividend income from affiliates, other income (loss), general and administrative expenses, and income taxes. 13

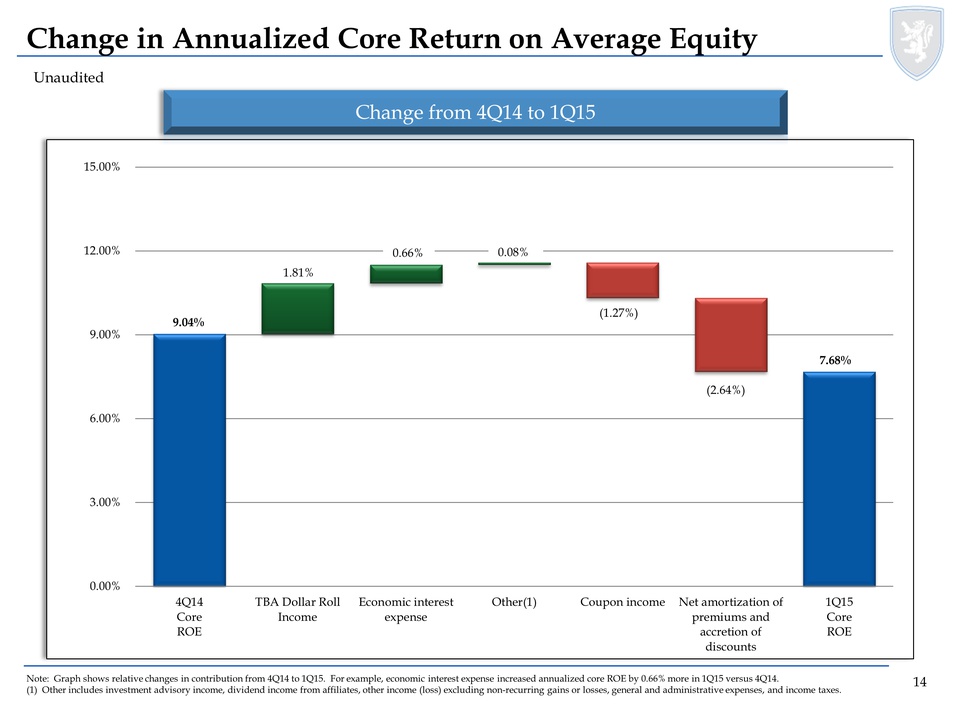

Change in Annualized Core Return on Average Equity Unaudited Change from 4Q14 to 1Q15 7.68% 9.04% 4Q14 Core ROE TBA Dollar Roll Income Economic interest expense Other(1) Coupon income Net amortization of premiums and accretion of discounts 1Q15 Core ROE 0.66% (2.64%) (1.27%) 0.08% 1.81% Note: Graph shows relative changes in contribution from 4Q14 to 1Q15. For example, economic interest expense increased annualized core ROE by 0.66% more in 1Q15 versus 4Q14. (1) Other includes investment advisory income, dividend income from affiliates, other income (loss) excluding non-recurring gains or losses, general and administrative expenses, and income taxes. 14

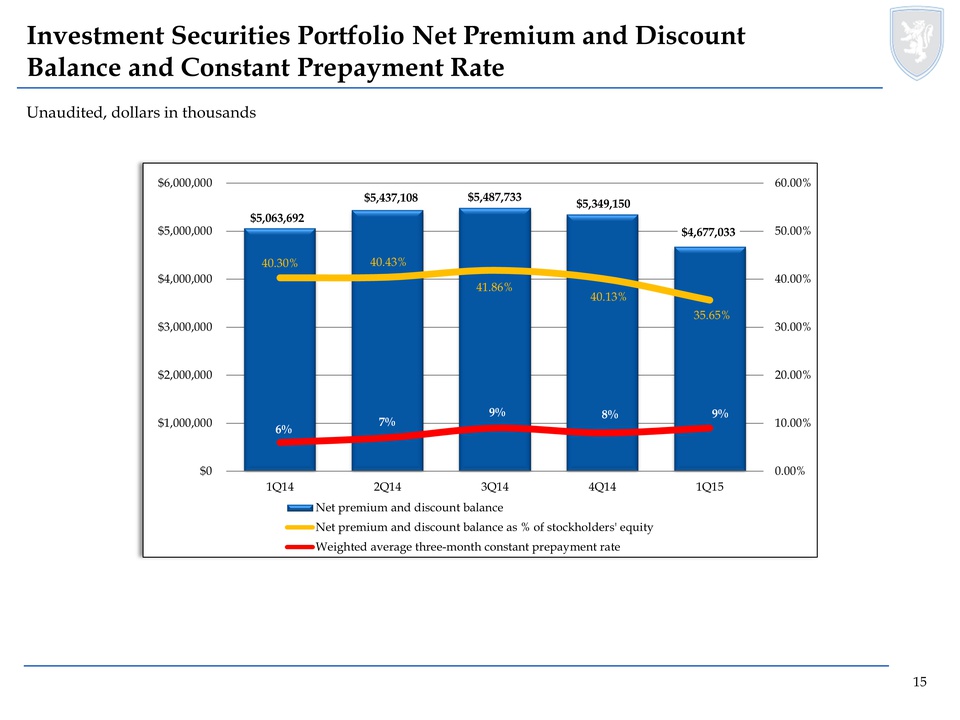

Investment Securities Portfolio Net Premium and Discount Balance and Constant Prepayment Rate Unaudited, dollars in thousands $5,063,692 $5,437,108 $5,487,733 $5,349,150 $4,677,033 40.30% 40.43% 41.86% 40.13% 35.65% 6% 7% 9% 8% 9% Net premium and discount balance Net premium and discount balance as % of stockholders' equity Weighted average three-month constant prepayment rate 15

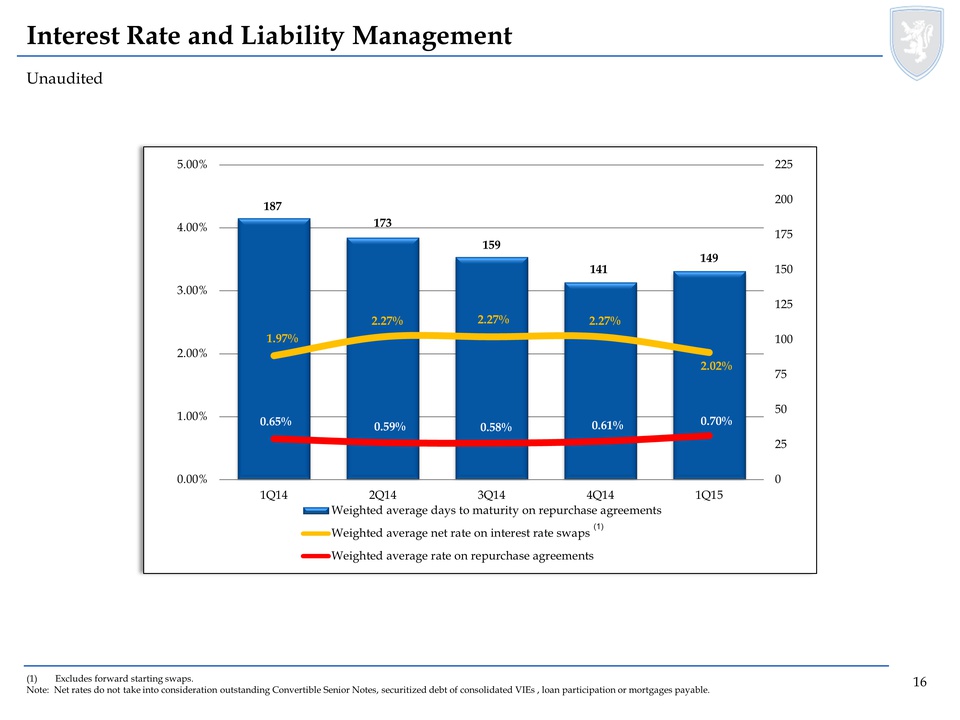

Interest Rate and Liability Management Unaudited 187 173 159 141 149 1.97% 2.27% 2.27% 2.27% 2.02% 0.65% 0.59% 0.58% 0.61% 0.70% Weighted average days to maturity on repurchase agreements Weighted average net rate on interest rate swaps Weighted average rate on repurchase agreements (1) Excludes forward starting swaps. Note: Net rates do not take into consideration outstanding Convertible Senior Notes, securitized debt of consolidated VIEs , loan participation or mortgages payable. 16

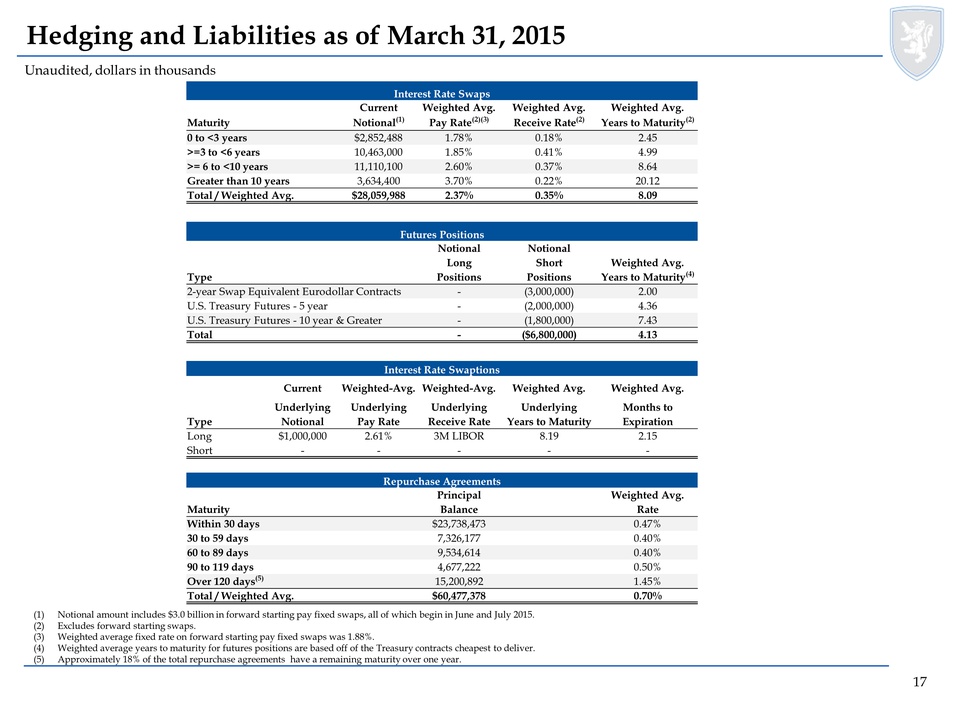

Hedging and Liabilities as of March 31, 2015 Unaudited, dollars in thousands Interest Rate Swaps Current Weighted Avg. Weighted Avg. Weighted Avg. Maturity Notional(1) Pay Rate(2)(3) Receive Rate(2) Years to Maturity(2) 0 to <3 years $2,852,488 1.78% 0.18% 2.45 >=3 to <6 years 10,463,000 1.85% 0.41% 4.99 >= 6 to <10 years 11,110,100 2.60% 0.37% 8.64 Greater than 10 years 3,634,400 3.70% 0.22% 20.12 Total / Weighted Avg. $28,059,988 2.37% 0.35% 8.09 Futures Positions Notional Notional Long Short Weighted Avg. Type Positions Positions Years to Maturity(4) 2-year Swap Equivalent Eurodollar Contracts - (3,000,000) 2.00 U.S. Treasury Futures - 5 year - (2,000,000) 4.36 U.S. Treasury Futures - 10 year & Greater - (1,800,000) 7.43 Total - ($6,800,000) 4.13 Interest Rate Swaptions Current Weighted-Avg. Weighted-Avg. Weighted Avg. Weighted Avg. Underlying Underlying Underlying Underlying Months to Type Notional Pay Rate Receive Rate Years to Maturity Expiration Long $1,000,000 2.61% 3M LIBOR 8.19 2.15 Short - - - - - Repurchase Agreements Principal Weighted Avg. Maturity Balance Rate Within 30 days $23,738,473 0.47% 30 to 59 days 7,326,177 0.40% 60 to 89 days 9,534,614 0.40% 90 to 119 days 4,677,222 0.50% Over 120 days(5) 15,200,892 1.45% Total / Weighted Avg. $60,477,378 0.70% (1) Notional amount includes $3.0 billion in forward starting pay fixed swaps, all of which begin in June and July 2015. (2) Excludes forward starting swaps. (3) Weighted average fixed rate on forward starting pay fixed swaps was 1.88%. (4) Weighted average years to maturity for futures positions are based off of the Treasury contracts cheapest to deliver. (5) Approximately 18% of the total repurchase agreements have a remaining maturity over one year. 17

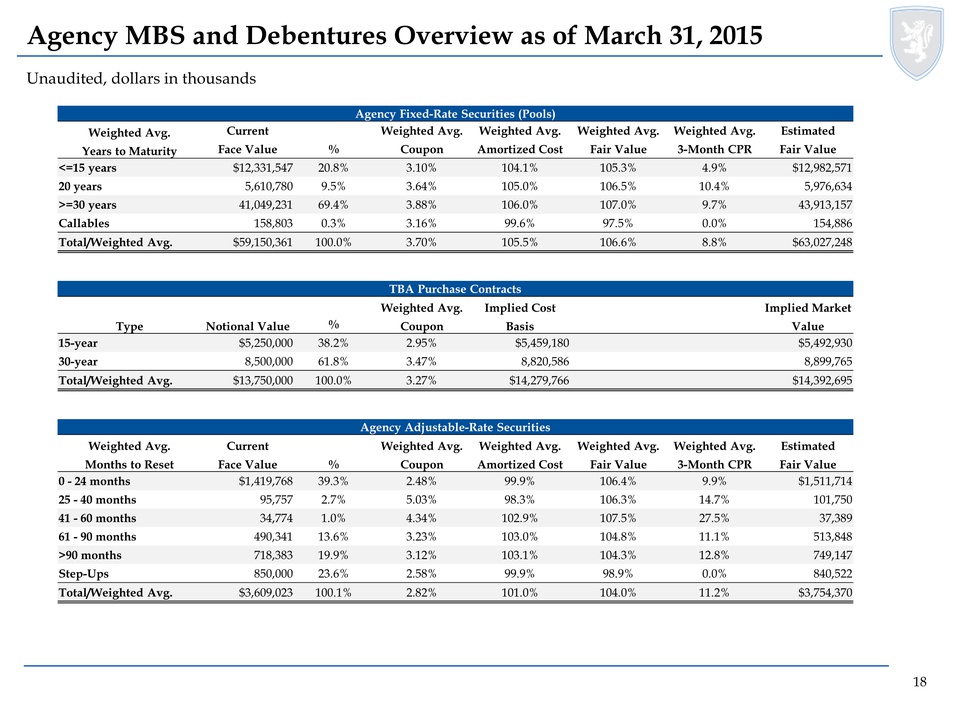

Agency MBS and Debentures Overview as of March 31, 2015 Unaudited, dollars in thousands Agency Fixed-Rate Securities (Pools) Weighted Avg. Current Weighted Avg. Weighted Avg. Weighted Avg. Weighted Avg. Estimated Years to Maturity Face Value % Coupon Amortized Cost Fair Value 3-Month CPR Fair Value <=15 years $12,331,547 20.8% 3.10% 104.1% 105.3% 4.9% $12,982,571 20 years 5,610,780 9.5% 3.64% 105.0% 106.5% 10.4% 5,976,634 >=30 years 41,049,231 69.4% 3.88% 106.0% 107.0% 9.7% 43,913,157 Callables 158,803 0.3% 3.16% 99.6% 97.5% 0.0% 154,886 Total/Weighted Avg. $59,150,361 100.0% 3.70% 105.5% 106.6% 8.8% $63,027,248 TBA Purchase Contracts Weighted Avg. Implied Cost Implied Market Type Notional Value % Coupon Basis Value 15-year $5,250,000 38.2% 2.95% $5,459,180 $5,492,930 30-year 8,500,000 61.8% 3.47% 8,820,586 8,899,765 Total/Weighted Avg. $13,750,000 100.0% 3.27% $14,279,766 $14,392,695 Agency Adjustable-Rate Securities Weighted Avg. Current Weighted Avg. Weighted Avg. Weighted Avg. Weighted Avg. Estimated Months to Reset Face Value % Coupon Amortized Cost Fair Value 3-Month CPR Fair Value 0 - 24 months $1,419,768 39.3% 2.48% 99.9% 106.4% 9.9% $1,511,714 25 - 40 months 95,757 2.7% 5.03% 98.3% 106.3% 14.7% 101,750 41 - 60 months 34,774 1.0% 4.34% 102.9% 107.5% 27.5% 37,389 61 - 90 months 490,341 13.6% 3.23% 103.0% 104.8% 11.1% 513,848 >90 months 718,383 19.9% 3.12% 103.1% 104.3% 12.8% 749,147 Step-Ups 850,000 23.6% 2.58% 99.9% 98.9% 0.0% 840,522 Total/Weighted Avg. $3,609,023 100.1% 2.82% 101.0% 104.0% 11.2% $3,754,370 18

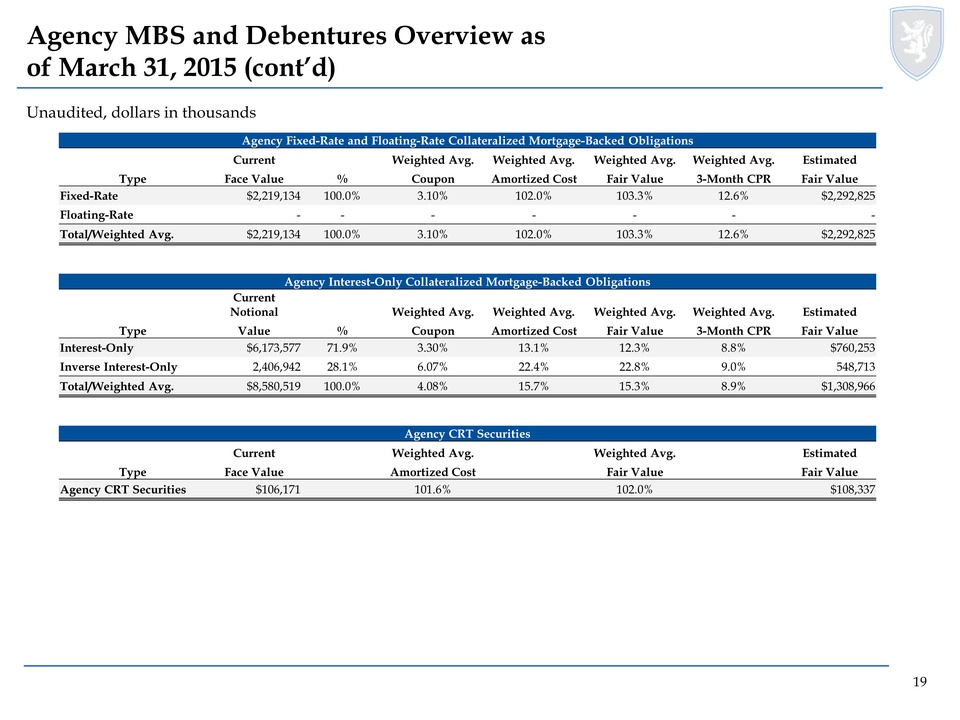

Agency MBS and Debentures Overview as of March 31, 2015 (cont’d) Unaudited, dollars in thousands Agency Fixed-Rate and Floating-Rate Collateralized Mortgage-Backed Obligations Current Weighted Avg. Weighted Avg. Weighted Avg. Weighted Avg. Estimated Type Face Value % Coupon Amortized Cost Fair Value 3-Month CPR Fair Value Fixed-Rate $2,219,134 100.0% 3.10% 102.0% 103.3% 12.6% $2,292,825 Floating-Rate - - - - - - - Total/Weighted Avg. $2,219,134 100.0% 3.10% 102.0% 103.3% 12.6% $2,292,825 Agency Interest-Only Collateralized Mortgage-Backed Obligations Current Notional Weighted Avg. Weighted Avg. Weighted Avg. Weighted Avg. Estimated Type Value % Coupon Amortized Cost Fair Value 3-Month CPR Fair Value Interest-Only $6,173,577 71.9% 3.30% 13.1% 12.3% 8.8% $760,253 Inverse Interest-Only 2,406,942 28.1% 6.07% 22.4% 22.8% 9.0% 548,713 Total/Weighted Avg. $8,580,519 100.0% 4.08% 15.7% 15.3% 8.9% $1,308,966 Agency CRT Securities Current Weighted Avg. Weighted Avg. Estimated Type Face Value Amortized Cost Fair Value Fair Value Agency CRT Securities $106,171 101.6% 102.0% $108,337 19

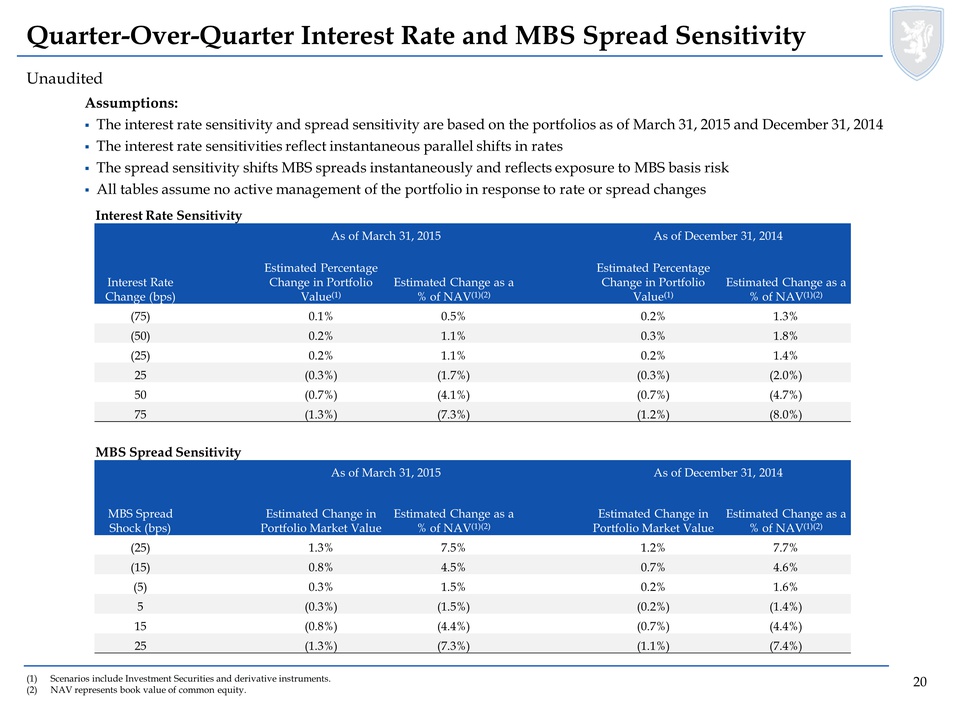

Quarter-Over-Quarter Interest Rate and MBS Spread Sensitivity Unaudited Assumptions: The interest rate sensitivity and spread sensitivity are based on the portfolios as of March 31, 2015 and December 31, 2014 The interest rate sensitivities reflect instantaneous parallel shifts in rates The spread sensitivity shifts MBS spreads instantaneously and reflects exposure to MBS basis risk All tables assume no active management of the portfolio in response to rate or spread changes Interest Rate Sensitivity As of March 31, 2015 As of December 31, 2014 Interest Rate Change (bps) Estimated Percentage Change in Portfolio Value(1) Estimated Change as a % of NAV(1)(2) Estimated Percentage Change in Portfolio Value(1) Estimated Change as a % of NAV(1)(2) (75) 0.1% 0.5% 0.2% 1.3% (50) 0.2% 1.1% 0.3% 1.8% (25) 0.2% 1.1% 0.2% 1.4% 25 (0.3%) (1.7%) (0.3%) (2.0%) 50 (0.7%) (4.1%) (0.7%) (4.7%) 75 (1.3%) (7.3%) (1.2%) (8.0%) MBS Spread Sensitivity As of March 31, 2015 As of December 31, 2014 MBS Spread Shock (bps) Estimated Change in Portfolio Market Value Estimated Change as a % of NAV(1)(2) Estimated Change in Portfolio Market Value Estimated Change as a % of NAV(1)(2) (25) 1.3% 7.5% 1.2% 7.7% (15) 0.8% 4.5% 0.7% 4.6% (5) 0.3% 1.5% 0.2% 1.6% 5 (0.3%) (1.5%) (0.2%) (1.4%) 15 (0.8%) (4.4%) (0.7%) (4.4%) 25 (1.3%) (7.3%) (1.1%) (7.4%) (1) Scenarios include Investment Securities and derivative instruments. (2) NAV represents book value of common equity. 20

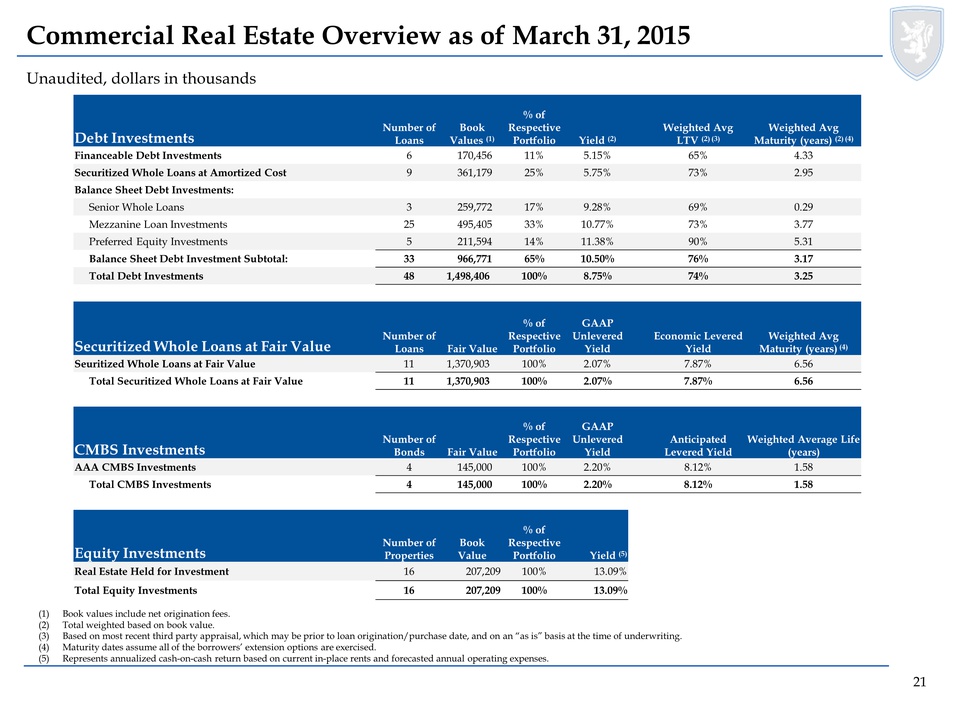

Commercial Real Estate Overview as of March 31, 2015 Unaudited, dollars in thousands Debt Investments Number of Loans Book Values (1) % of Respective Portfolio Yield (2) Weighted Avg LTV (2) (3) Weighted Avg Maturity (years) (2) (4) Financeable Debt Investments 6 170,456 11% 5.15% 65% 4.33 Securitized Whole Loans at Amortized Cost 9 361,179 25% 5.75% 73% 2.95 Balance Sheet Debt Investments: Senior Whole Loans 3 259,772 17% 9.28% 69% 0.29 Mezzanine Loan Investments 25 495,405 33% 10.77% 73% 3.77 Preferred Equity Investments 5 211,594 14% 11.38% 90% 5.31 Balance Sheet Debt Investment Subtotal: 33 966,771 65% 10.50% 76% 3.17 Total Debt Investments 48 1,498,406 100% 8.75% 74% 3.25 Securitized Whole Loans at Fair Value Number of Loans Fair Value % of Respective Portfolio GAAP Unlevered Yield Economic Levered Yield Weighted Avg Maturity (years) (4) Seuritized Whole Loans at Fair Value 11 1,370,903 100% 2.07% 7.87% 6.56 Total Securitized Whole Loans at Fair Value 11 1,370,903 100% 2.07% 7.87% 6.56 CMBS Investments Number of Bonds Fair Value % of Respective Portfolio GAAP Unlevered Yield Anticipated Levered Yield Weighted Average Life (years) AAA CMBS Investments 4 145,000 100% 2.20% 8.12% 1.58 Total CMBS Investments 4 145,000 100% 2.20% 8.12% 1.58 Equity Investments Number of Properties Book Value % of Respective Portfolio Yield (5) Real Estate Held for Investment 16 207,209 100% 13.09% Total Equity Investments 16 207,209 100% 13.09% (1) Book values include net origination fees. (2) Total weighted based on book value. (3) Based on most recent third party appraisal, which may be prior to loan origination/purchase date, and on an “as is” basis at the time of underwriting. (4) Maturity dates assume all of the borrowers’ extension options are exercised. (5) Represents annualized cash-on-cash return based on current in-place rents and forecasted annual operating expenses. 21

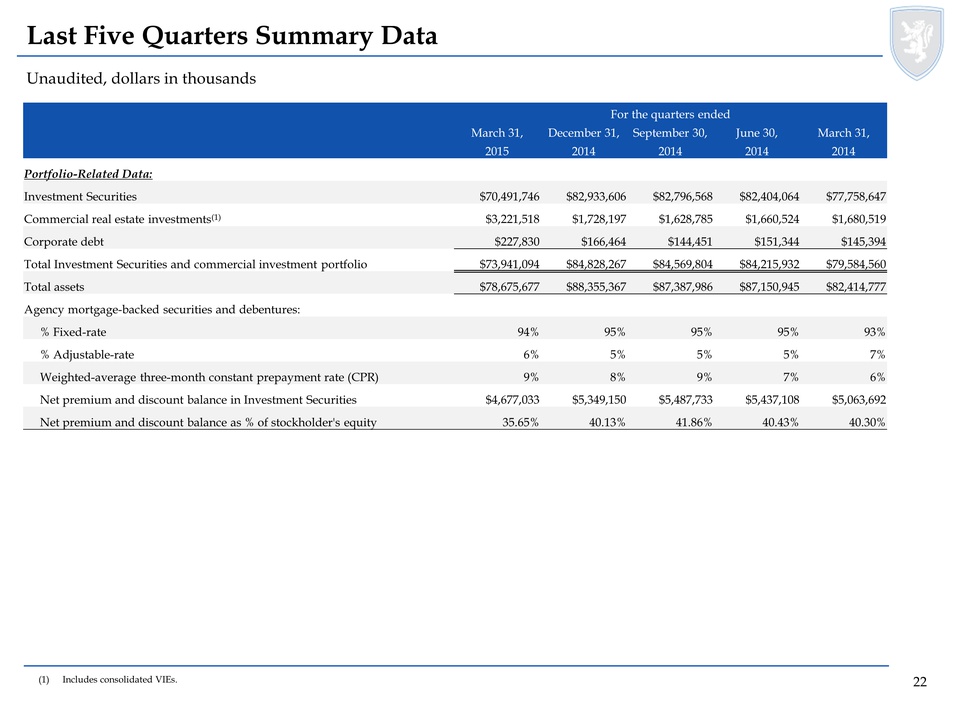

Last Five Quarters Summary Data Unaudited, dollars in thousands For the quarters ended March 31, December 31, September 30, June 30, March 31, 2015 2014 2014 2014 2014 Portfolio-Related Data: Investment Securities $70,491,746 $82,933,606 $82,796,568 $82,404,064 $77,758,647 Commercial real estate investments(1) $3,221,518 $1,728,197 $1,628,785 $1,660,524 $1,680,519 Corporate debt $227,830 $166,464 $144,451 $151,344 $145,394 Total Investment Securities and commercial investment portfolio $73,941,094 $84,828,267 $84,569,804 $84,215,932 $79,584,560 Total assets $78,675,677 $88,355,367 $87,387,986 $87,150,945 $82,414,777 Agency mortgage-backed securities and debentures: % Fixed-rate 94% 95% 95% 95% 93% % Adjustable-rate 6% 5% 5% 5% 7% Weighted-average three-month constant prepayment rate (CPR) 9% 8% 9% 7% 6% Net premium and discount balance in Investment Securities $4,677,033 $5,349,150 $5,487,733 $5,437,108 $5,063,692 Net premium and discount balance as % of stockholder's equity 35.65% 40.13% 41.86% 40.43% 40.30% (1) Includes consolidated VIEs. 22

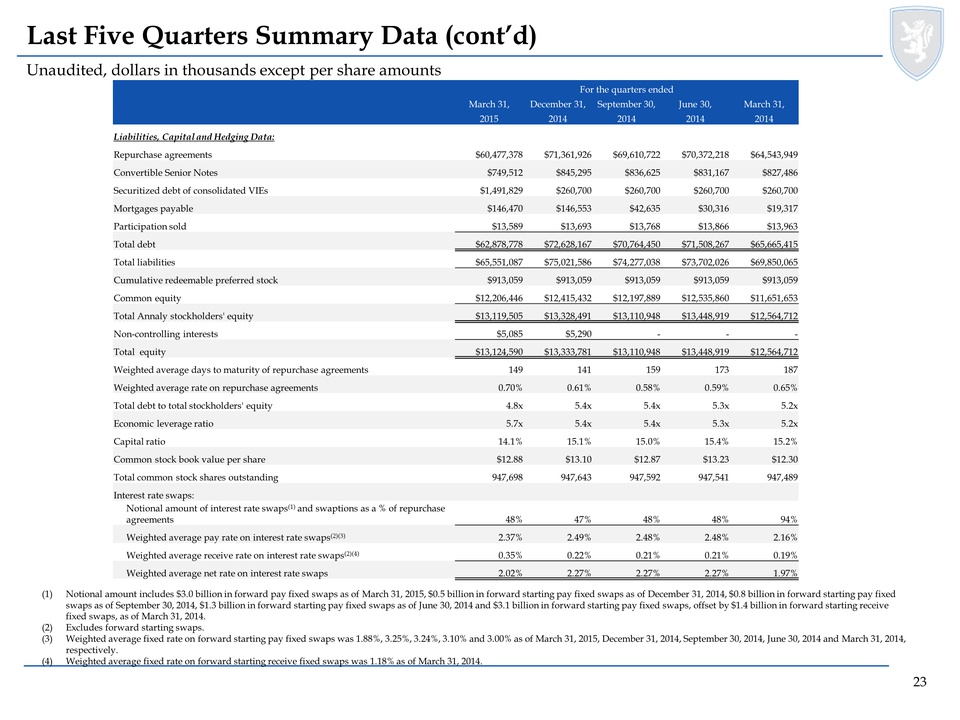

Last Five Quarters Summary Data (cont’d) Unaudited, dollars in thousands except per share amounts For the quarters ended March 31, December 31, September 30, June 30, March 31, 2015 2014 2014 2014 2014 Liabilities, Capital and Hedging Data: Repurchase agreements $60,477,378 $71,361,926 $69,610,722 $70,372,218 $64,543,949 Convertible Senior Notes $749,512 $845,295 $836,625 $831,167 $827,486 Securitized debt of consolidated VIEs $1,491,829 $260,700 $260,700 $260,700 $260,700 Mortgages payable $146,470 $146,553 $42,635 $30,316 $19,317 Participation sold $13,589 $13,693 $13,768 $13,866 $13,963 Total debt $62,878,778 $72,628,167 $70,764,450 $71,508,267 $65,665,415 Total liabilities $65,551,087 $75,021,586 $74,277,038 $73,702,026 $69,850,065 Cumulative redeemable preferred stock $913,059 $913,059 $913,059 $913,059 $913,059 Common equity $12,206,446 $12,415,432 $12,197,889 $12,535,860 $11,651,653 Total Annaly stockholders' equity $13,119,505 $13,328,491 $13,110,948 $13,448,919 $12,564,712 Non-controlling interests $5,085 $5,290 - - - Total equity $13,124,590 $13,333,781 $13,110,948 $13,448,919 $12,564,712 Weighted average days to maturity of repurchase agreements 149 141 159 173 187 Weighted average rate on repurchase agreements 0.70% 0.61% 0.58% 0.59% 0.65% Total debt to total stockholders' equity 4.8x 5.4x 5.4x 5.3x 5.2x Economic leverage ratio 5.7x 5.4x 5.4x 5.3x 5.2x Capital ratio 14.1% 15.1% 15.0% 15.4% 15.2% Common stock book value per share $12.88 $13.10 $12.87 $13.23 $12.30 Total common stock shares outstanding 947,698 947,643 947,592 947,541 947,489 Interest rate swaps: Notional amount of interest rate swaps(1) and swaptions as a % of repurchase agreements 48% 47% 48% 48% 94% Weighted average pay rate on interest rate swaps(2)(3) 2.37% 2.49% 2.48% 2.48% 2.16% Weighted average receive rate on interest rate swaps(2)(4) 0.35% 0.22% 0.21% 0.21% 0.19% Weighted average net rate on interest rate swaps 2.02% 2.27% 2.27% 2.27% 1.97% (1) Notional amount includes $3.0 billion in forward pay fixed swaps as of March 31, 2015, $0.5 billion in forward starting pay fixed swaps as of December 31, 2014, $0.8 billion in forward starting pay fixed swaps as of September 30, 2014, $1.3 billion in forward starting pay fixed swaps as of June 30, 2014 and $3.1 billion in forward starting pay fixed swaps, offset by $1.4 billion in forward starting receive fixed swaps, as of March 31, 2014. (2) Excludes forward starting swaps. (3) Weighted average fixed rate on forward starting pay fixed swaps was 1.88%, 3.25%, 3.24%, 3.10% and 3.00% as of March 31, 2015, December 31, 2014, September 30, 2014, June 30, 2014 and March 31, 2014, respectively. (4) Weighted average fixed rate on forward starting receive fixed swaps was 1.18% as of March 31, 2014. 23

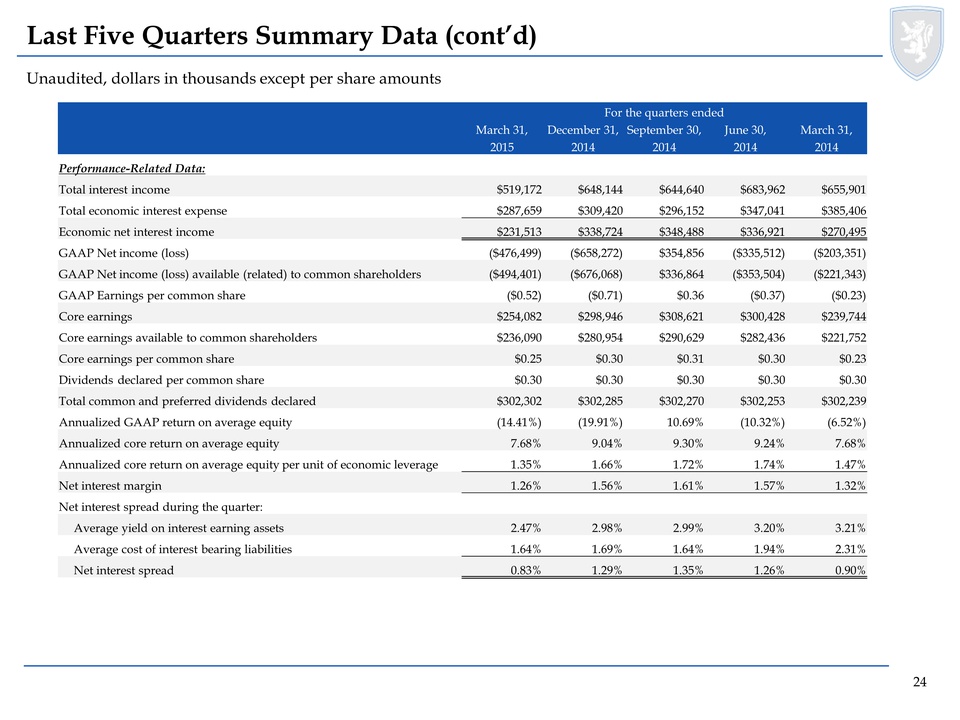

Last Five Quarters Summary Data (cont’d) Unaudited, dollars in thousands except per share amounts For the quarters ended March 31, December 31, September 30, June 30, March 31, 2015 2014 2014 2014 2014 Performance-Related Data: Total interest income $519,172 $648,144 $644,640 $683,962 $655,901 Total economic interest expense $287,659 $309,420 $296,152 $347,041 $385,406 Economic net interest income $231,513 $338,724 $348,488 $336,921 $270,495 GAAP Net income (loss) ($476,499) ($658,272) $354,856 ($335,512) ($203,351) GAAP Net income (loss) available (related) to common shareholders ($494,401) ($676,068) $336,864 ($353,504) ($221,343) GAAP Earnings per common share ($0.52) ($0.71) $0.36 ($0.37) ($0.23) Core earnings $254,082 $298,946 $308,621 $300,428 $239,744 Core earnings available to common shareholders $236,090 $280,954 $290,629 $282,436 $221,752 Core earnings per common share $0.25 $0.30 $0.31 $0.30 $0.23 Dividends declared per common share $0.30 $0.30 $0.30 $0.30 $0.30 Total common and preferred dividends declared $302,302 $302,285 $302,270 $302,253 $302,239 Annualized GAAP return on average equity (14.41%) (19.91%) 10.69% (10.32%) (6.52%) Annualized core return on average equity 7.68% 9.04% 9.30% 9.24% 7.68% Annualized core return on average equity per unit of economic leverage 1.35% 1.66% 1.72% 1.74% 1.47% Net interest margin 1.26% 1.56% 1.61% 1.57% 1.32% Net interest spread during the quarter: Average yield on interest earning assets 2.47% 2.98% 2.99% 3.20% 3.21% Average cost of interest bearing liabilities 1.64% 1.69% 1.64% 1.94% 2.31% Net interest spread 0.83% 1.29% 1.35% 1.26% 0.90% 24