Fourth - Quarter 2018 Results February 28, 2019

2 Forward - Looking Statements Statements in this presentation that are not historical facts are forward - looking statements, which involve risks and uncertaint ies that could cause actual events or results to differ materially from those expressed or implied by the statements. Important factors that ma y cause actual results to differ materially from those in the forward - looking statements include, among other factors, the loss or bankruptcy o f a major customer; the costs and timing of facility closures, business realignment or similar actions; a significant change in commerc ial vehicle, automotive, agricultural and off - highway vehicle production; our ability to achieve cost reductions that offset or exceed custom er - mandated selling price reductions; a significant change in general economic conditions in any of the various countries in which Stoner idg e operates; labor disruptions at Stoneridge’s facilities or at any of Stoneridge’s significant customers or suppliers; the ability of sup pli ers to supply Stoneridge with parts and components at competitive prices on a timely basis; the amount of Stoneridge’s indebtedness and the re strictive covenants contained in the agreements governing its indebtedness, including its revolving credit facility; customer acceptanc e o f new products; capital availability or costs, including changes in interest rates or market perceptions; the failure to achieve su cce ssful integration of any acquired company or business; the occurrence or non - occurrence of circumstances beyond Stoneridge’s control; and the items described in “Risk Factors” and other uncertainties or risks discussed in Stoneridge’s periodic and current reports filed wit h t he Securities and Exchange Commission. Important factors that could cause the performance of the commercial vehicle and automotive industry to differ materially fro m t hose in the forward - looking statements include factors such as (1) continued economic instability or poor economic conditions in the United States and global markets, (2) changes in economic conditions, housing prices, foreign currency exchange rates, commodity prices, includ ing shortages of and increases or volatility in the price of oil, (3) changes in laws and regulations, (4) the state of the credit markets, (5 ) political stability, (6) international conflicts and (7) the occurrence of force majeure events. These factors should not be construed as exhaustive and should be considered with the other cautionary statements in Stonerid ge’ s filings with the Securities and Exchange Commission. Forward - looking statements are not guarantees of future performance; Stoneridge’s actual results of operations, financial condit ion and liquidity, and the development of the industry in which Stoneridge operates may differ materially from those described in or sug gested by the forward - looking statements contained in this presentation. In addition, even if Stoneridge’s results of operations, financial co ndition and liquidity, and the development of the industry in which Stoneridge operates are consistent with the forward - looking statements c ontained in this presentation, those results or developments may not be indicative of results or developments in subsequent periods. This presentation contains time - sensitive information that reflects management’s best analysis only as of the date of this prese ntation. Any forward - looking statements in this presentation speak only as of the date of this presentation, and Stoneridge undertakes no obl igation to update such statements. Comparisons of results for current and any prior periods are not intended to express any future tren ds or indications of future performance, unless expressed as such, and should only be viewed as historical data. Stoneridge does not undertake any obligation to publicly update or revise any forward - looking statement as a result of new infor mation, future events or otherwise, except as otherwise required by law. Rounding Disclosure: There may be slight immaterial differences between figures represented in our public filings compared t o w hat is shown in this presentation. The differences are the a result of rounding due to the representation of values in millions rat her than thousands in public filings.

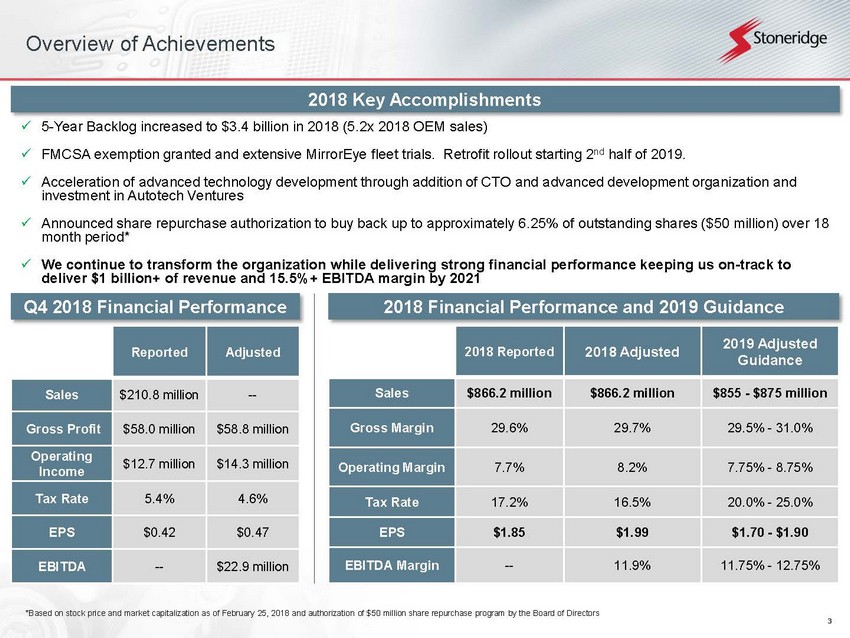

3 Overview of Achievements x 5 - Year Backlog increased to $3.4 billion in 2018 (5.2x 2018 OEM sales) x FMCSA exemption granted and extensive MirrorEye fleet trials. Retrofit rollout starting 2 nd half of 2019. x Acceleration of advanced technology development through addition of CTO and advanced development organization and investment in Autotech Ventures x Announced share repurchase authorization to buy back up to approximately 6.25% of outstanding shares ($50 million) over 18 month period* x We continue to transform the organization while delivering strong financial performance keeping us on - track to deliver $1 billion+ of revenue and 15.5%+ EBITDA margin by 2021 2018 Key Accomplishments *Based on stock price and market capitalization as of February 25, 2018 and authorization of $50 million share repurchase pro gra m by the Board of Directors Q 4 2018 Financial Performance 2018 Financial Performance and 2019 Guidance 2018 Reported 2018 Adjusted 2019 Adjusted Guidance Sales $866.2 million $866.2 million $855 - $875 million Gross Margin 29.6% 29.7% 29.5% - 31.0% Operating Margin 7.7% 8.2% 7.75% - 8.75% Tax Rate 17.2% 16.5% 20.0% - 25.0% EPS $1.85 $1.99 $1.70 - $1.90 EBITDA Margin -- 11.9% 11.75% - 12.75% Reported Adjusted Sales $210.8 million -- Gross Profit $58.0 million $58.8 million Operating Income $12.7 million $14.3 million Tax Rate 5.4% 4.6% EPS $0.42 $0.47 EBITDA -- $22.9 million

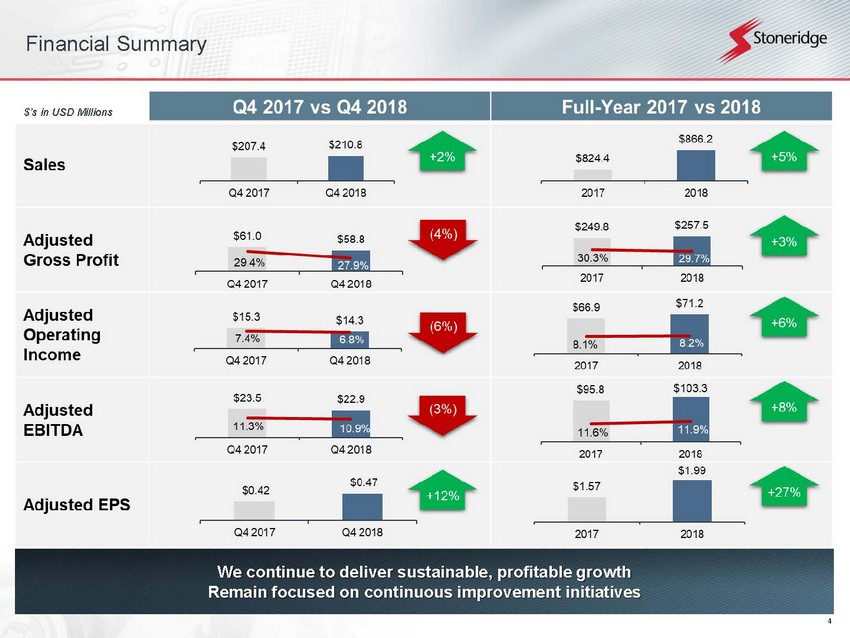

4 Financial Summary We continue to deliver sustainable, profitable growth Remain focused on continuous improvement initiatives $’s in USD Millions

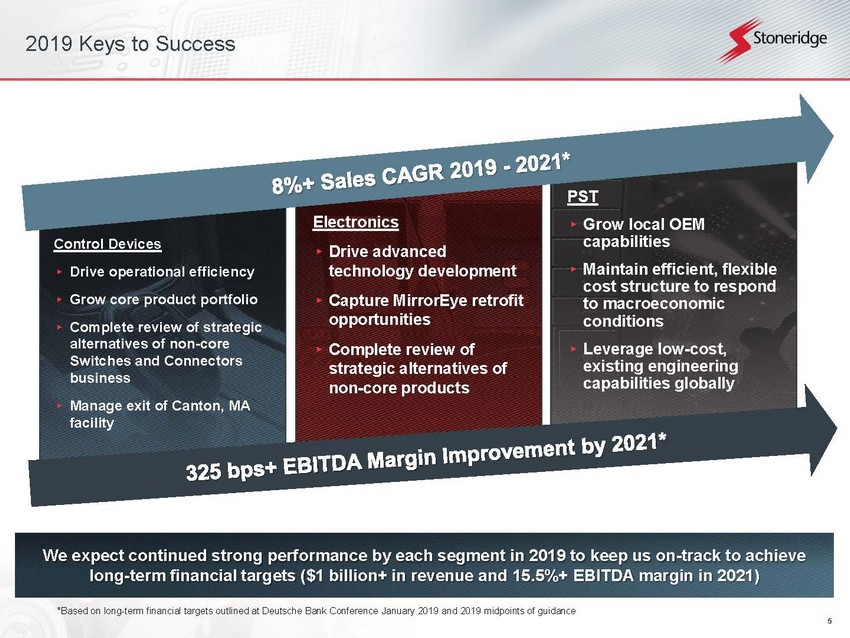

5 2019 Keys to Success *Based on long - term financial targets outlined at Deutsche Bank Conference January 2019 and 2019 midpoints of guidance We expect continued strong performance by each segment in 2019 to keep us on - track to achieve long - term financial targets ($1 billion+ in revenue and 15.5%+ EBITDA margin in 2021) Control Devices ▸ Drive operational efficiency ▸ Grow core product portfolio ▸ Complete review of strategic alternatives of non - core Switches and Connectors business ▸ Manage exit of Canton, MA facility Electronics ▸ Drive advanced technology development ▸ Capture MirrorEye retrofit opportunities ▸ Complete review of strategic alternatives of non - core products PST ▸ Grow local OEM capabilities ▸ Maintain efficient, flexible cost structure to respond to macroeconomic conditions ▸ Leverage low - cost, existing engineering capabilities globally

6 Leveraging Our Existing Technology Portfolio We are investing in current and future technologies that will enable system - based solutions by combining vision systems, connectivity capabilities and driver information systems Our telematics and tachograph units provide a gateway for vehicles to connect to other vehicles, fleet management tools and the environment around them Connectivity Our vision products create safer vehicles and enable advanced active safety applications when combined with other sensors and powertrain applications Vision and Safety Our driver information systems are the primary interface between a driver and the vehicle and will enable additional driver features and vehicle / driver interaction Driver Information Systems

7 Summary 2018 Summary ▸ We continue to transform the organization while delivering consistent financial performance improvement keeping us on - track to deliver $1 billion+ of revenue and 15.5%+ EBITDA margin in 2021 ▸ MirrorEye remains on - track • Significant fleet trials paving the way for 2019 retrofit roll - out • FMCSA exemption in late - 2018 means that MirrorEye is the only product in North America that allows for the removal of traditional mirrors on commercial vehicles ▸ Acceleration of advanced technology development through addition of CTO, advanced development team and investment in Autotech Ventures 2019 Outlook ▸ Continued focus on operational performance improvement ▸ Continued investment in engineering to drive technology platforms - $5 million incremental to 2018 ▸ Continued progress on Stoneridge 2020 initiatives • Review strategic alternatives for non - core Control Devices and Electronics products • Exit Canton, MA facility • Fully utilize global capabilities • OEM program development at PST • Global engineering footprint Driving shareholder value through strong financial performance and a well defined long - term strategy

8 Financial Update

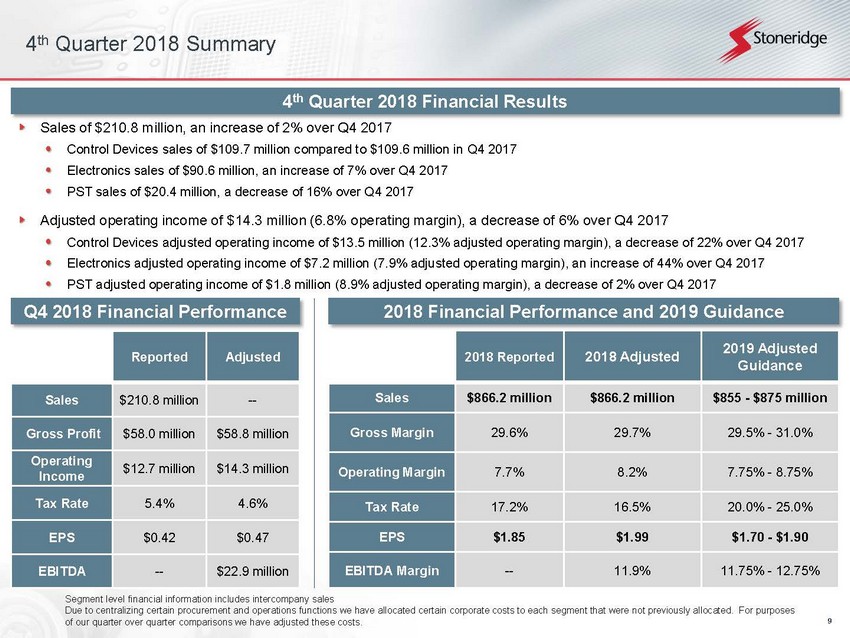

9 4 th Quarter 2018 Summary 4 th Quarter 2018 Financial Results Sales of $210.8 million, an increase of 2% over Q4 2017 Control Devices sales of $109.7 million compared to $109.6 million in Q4 2017 Electronics sales of $90.6 million, an increase of 7% over Q4 2017 PST sales of $20.4 million, a decrease of 16% over Q4 2017 Adjusted operating income of $14.3 million (6.8% operating margin), a decrease of 6% over Q4 2017 Control Devices adjusted operating income of $13.5 million (12.3% adjusted operating margin), a decrease of 22% over Q4 2017 Electronics adjusted operating income of $7.2 million (7.9% adjusted operating margin), an increase of 44% over Q4 2017 PST adjusted operating income of $1.8 million (8.9% adjusted operating margin), a decrease of 2% over Q4 2017 Segment level financial information includes intercompany sales Due to centralizing certain procurement and operations functions we have allocated certain corporate costs to each segment th at were not previously allocated. For purposes of our quarter over quarter comparisons we have adjusted these costs. Q 4 2018 Financial Performance 2018 Financial Performance and 2019 Guidance 2018 Reported 2018 Adjusted 2019 Adjusted Guidance Sales $866.2 million $866.2 million $855 - $875 million Gross Margin 29.6% 29.7% 29.5% - 31.0% Operating Margin 7.7% 8.2% 7.75% - 8.75% Tax Rate 17.2% 16.5% 20.0% - 25.0% EPS $1.85 $1.99 $1.70 - $1.90 EBITDA Margin -- 11.9% 11.75% - 12.75% Reported Adjusted Sales $210.8 million -- Gross Profit $58.0 million $58.8 million Operating Income $12.7 million $14.3 million Tax Rate 5.4% 4.6% EPS $0.42 $0.47 EBITDA -- $22.9 million

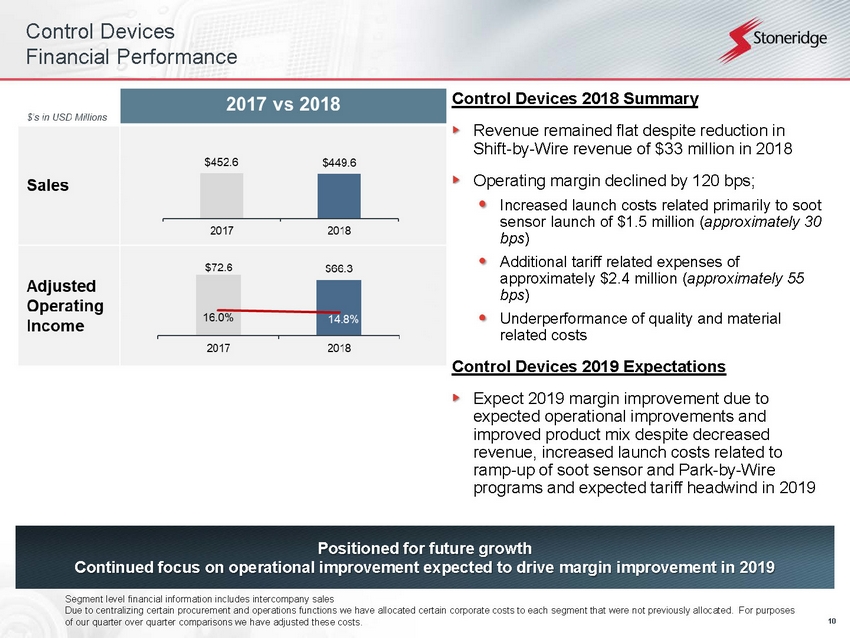

10 Control Devices Financial Performance Control Devices 2018 Summary Shift-by-Wire revenue of $33 million in 2018 sensor launch of $1.5 million (approximately 30bps) approximately $2.4 million (approximately 55 bps) related costs Control Devices 2019 Expectations expected operational improvements and improved product mix despite decreased revenue, increased launch costs related to ramp-up of soot sensor and Park-by-Wire programs and expected tariff headwind in 2019 Positioned for future growth Continued focus on operational improvement expected to drive margin improvement in 2019 Segment level financial information includes intercompany sales Due to centralizing certain procurement and operations functions we have allocated certain corporate costs to each segment that were not previously allocated. For purposes of our quarter over quarter comparisons we have adjusted these costs.

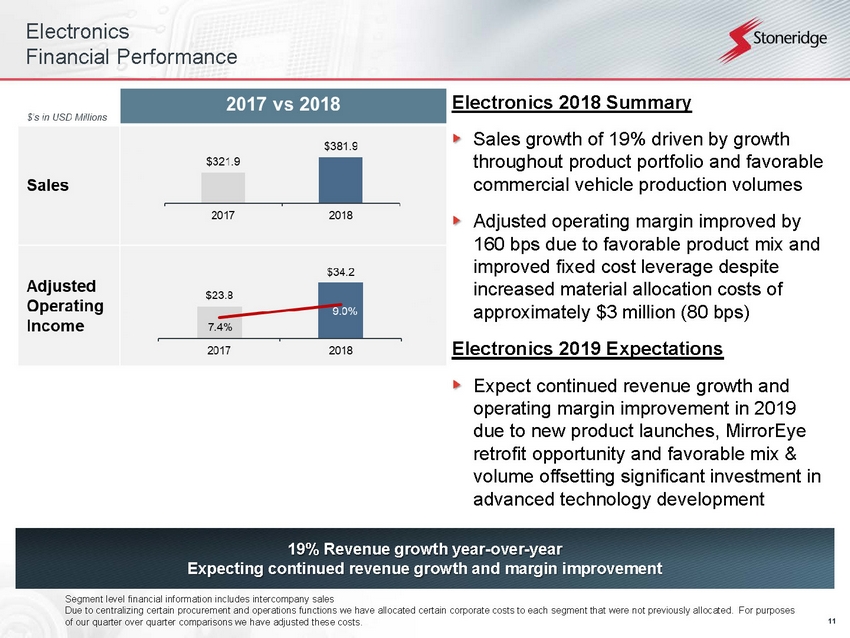

11 Electronics Financial Performance 19% Revenue growth year-over-year Expecting continued revenue growth and margin improvement Electronics 2018 Summary Sales growth of 19% driven by growth throughout product portfolio and favorable commercial vehicle production volumes Adjusted operating margin improved by 160 bps due to favorable product mix and improved fixed cost leverage despite increased material allocation costs of approximately $3 million (80 bps) Electronics 2019 Expectations Expect continued revenue growth and operating margin improvement in 2019 due to new product launches, MirrorEye retrofit opportunity and favorable mix & volume offsetting significant investment in advanced technology development Segment level financial information includes intercompany sales Due to centralizing certain procurement and operations functions we have allocated certain corporate costs to each segment that were not previously allocated. For purposes of our quarter over quarter comparisons we have adjusted these costs.

12 PST Financial Performance Continued operating margin improvement despite significant currency headwinds 2019 Expected to be relatively flat PST 2018 Summary Excluding impact of currency, sales declined by approximately $3 million (3%) Currency headwind of approximately $12 million Continued adjusted operating margin expansion in 2018 due to favorable product mix and a fully optimized cost structure PST 2019 Expectations Expect flat 2019 sales and operating margin as a result of forecasted macroeconomic stability and continued operational improvements offset by continued currency headwinds Segment level financial information includes intercompany sales Due to centralizing certain procurement and operations functions we have allocated certain corporate costs to each segment that were not previously allocated. For purposes of our quarter over quarter comparisons we have adjusted these costs.

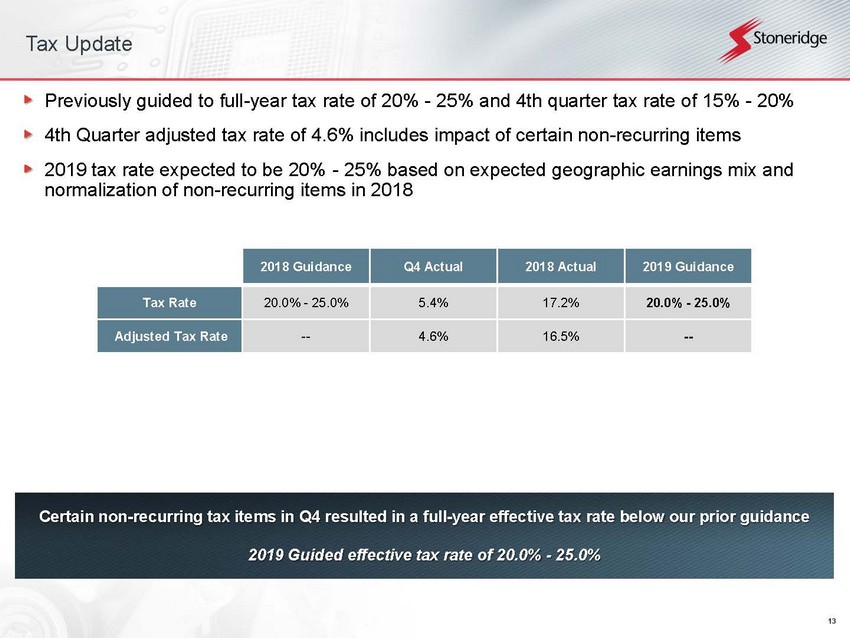

13 Tax Update Previously guided to full - year tax rate of 20% - 25% and 4th quarter tax rate of 15% - 20% 4th Quarter adjusted tax rate of 4.6% includes impact of certain non - recurring items 2019 tax rate expected to be 20% - 25% based on expected geographic earnings mix and normalization of non - recurring items in 2018 Certain non - recurring tax items in Q4 resulted in a full - year effective tax rate below our prior guidance 2019 Guided effective tax rate of 20.0% - 25.0% 2018 Guidance Q4 Actual 2018 Actual 2019 Guidance Tax Rate 20.0% - 25.0% 5.4% 17.2% 20.0% - 25.0% Adjusted Tax Rate -- 4.6% 16.5% --

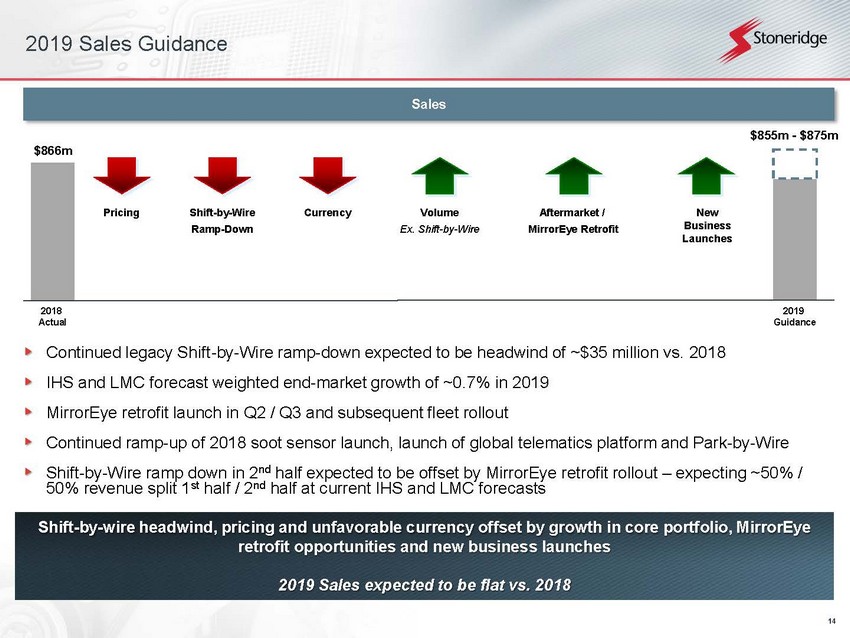

14 2019 Sales Guidance 2018 Actual Sales New Business Launches Aftermarket / MirrorEye Retrofit Pricing $866m Shift - by - Wire Ramp - Down Currency Volume Ex. Shift - by - Wire $855m - $875m 2019 Guidance Shift - by - wire headwind, pricing and unfavorable currency offset by growth in core portfolio, MirrorEye retrofit opportunities and new business launches 2019 Sales expected to be flat vs. 2018 Continued legacy Shift - by - Wire ramp - down expected to be headwind of ~$35 million vs. 2018 IHS and LMC forecast weighted end - market growth of ~0.7% in 2019 MirrorEye retrofit launch in Q2 / Q3 and subsequent fleet rollout Continued ramp - up of 2018 soot sensor launch, launch of global telematics platform and Park - by - Wire Shift - by - Wire ramp down in 2 nd half expected to be offset by MirrorEye retrofit rollout – expecting ~50% / 50% revenue split 1 st half / 2 nd half at current IHS and LMC forecasts

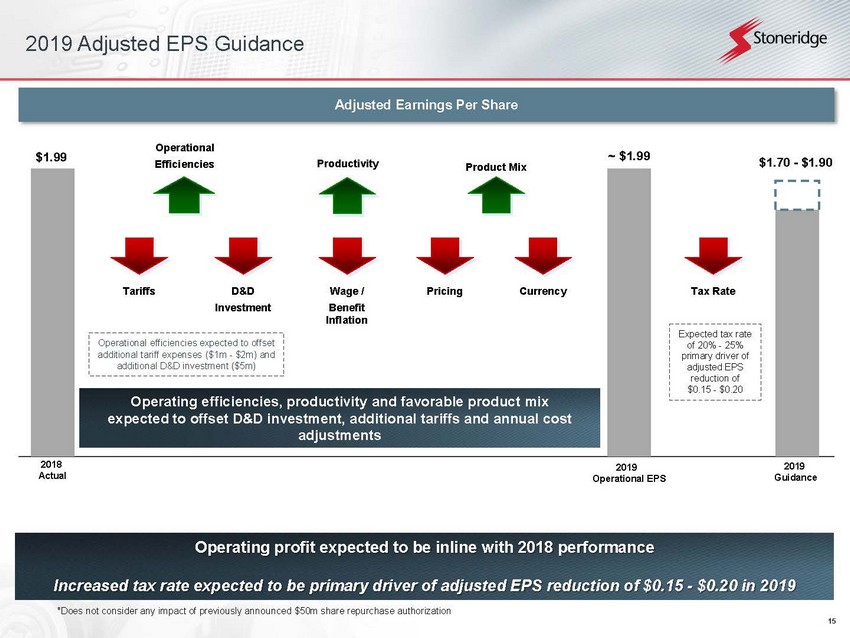

15 2019 Adjusted EPS Guidance Adjusted Earnings Per Share Wage / Benefit Inflation 2018 Actual $1.99 Tax Rate Tariffs D&D Investment Product Mix Operational Efficiencies $1.70 - $1.90 ~ $1.99 Expected tax rate of 20% - 25% primary driver of adjusted EPS reduction of $0.15 - $0.20 *Does not consider any impact of previously announced $50m share repurchase authorization 2019 Operational EPS 2019 Guidance Productivity Pricing Currency Operating profit expected to be inline with 2018 performance Increased tax rate expected to be primary driver of adjusted EPS reduction of $0.15 - $0.20 in 2019 Operational efficiencies expected to offset additional tariff expenses ($1m - $2m) and additional D&D investment ($5m) Operating efficiencies, productivity and favorable product mix expected to offset D&D investment, additional tariffs and annual cost adjustments

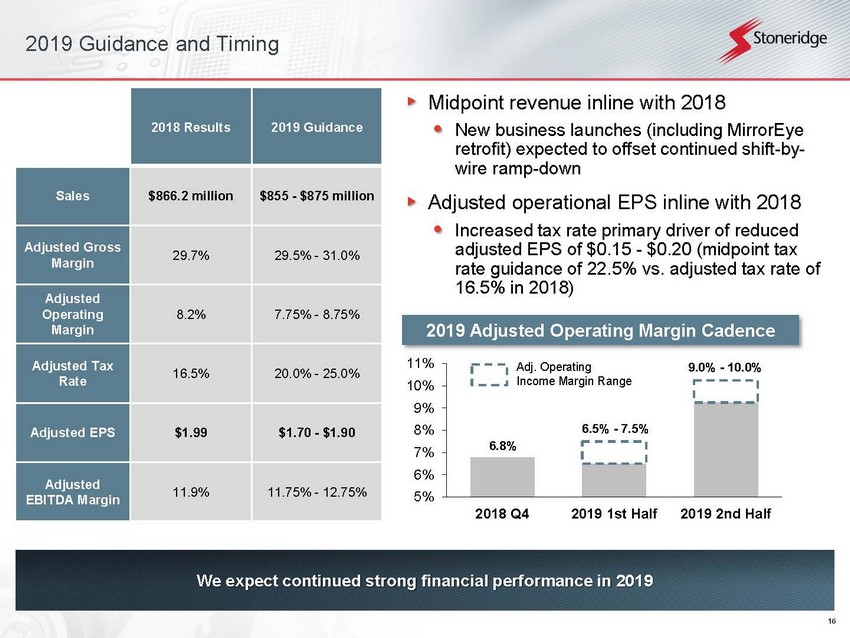

16 5% 6% 7% 8% 9% 10% 11% 2018 Q4 2019 1st Half 2019 2nd Half 2019 Guidance and Timing 2018 Results 2019 Guidance Sales $866.2 million $855 - $875 million Adjusted Gross Margin 29.7% 29.5% - 31.0% Adjusted Operating Margin 8.2% 7.75% - 8.75% Adjusted Tax Rate 16.5% 20.0% - 25.0% Adjusted EPS $1.99 $1.70 - $1.90 Adjusted EBITDA Margin 11.9% 11.75% - 12.75% We expect continued strong financial performance in 2019 2019 Adjusted Operating Margin Cadence Midpoint revenue inline with 2018 New business launches (including MirrorEye retrofit) expected to offset continued shift - by - wire ramp - down Adjusted operational EPS inline with 2018 Increased tax rate primary driver of reduced adjusted EPS of $0.15 - $0.20 (midpoint tax rate guidance of 22.5% vs. adjusted tax rate of 16.5% in 2018) 9.0% - 10.0% 6.5% - 7.5% Adj. Operating Income Margin Range 6.8%

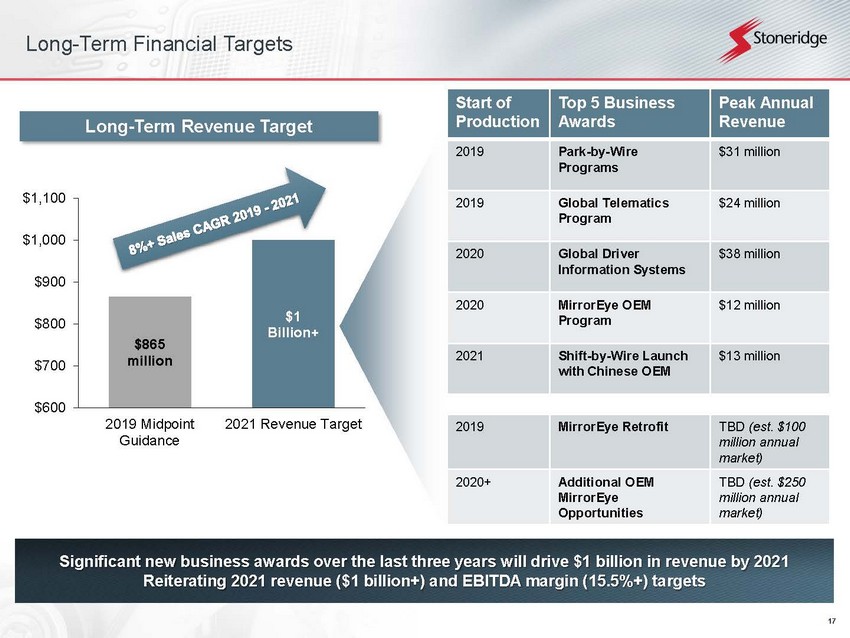

17 Long - Term Financial Targets Significant new business awards over the last three years will drive $1 billion in revenue by 2021 Reiterating 2021 revenue ($1 billion+) and EBITDA margin (15.5%+) targets Start of Production Top 5 Business Awards Peak Annual Revenue 2019 Park - by - Wire Programs $31 million 2019 Global Telematics Program $24 million 2020 Global Driver Information Systems $38 million 2020 MirrorEye OEM Program $12 million 2021 Shift - by - Wire Launch with Chinese OEM $13 million 2019 MirrorEye Retrofit TBD (est. $100 million annual market) 2020+ Additional OEM MirrorEye Opportunities TBD (est. $250 million annual market) $865 million $1 Billion+ $600 $700 $800 $900 $1,000 $1,100 2019 Midpoint Guidance 2021 Revenue Target Long - Term Revenue Target

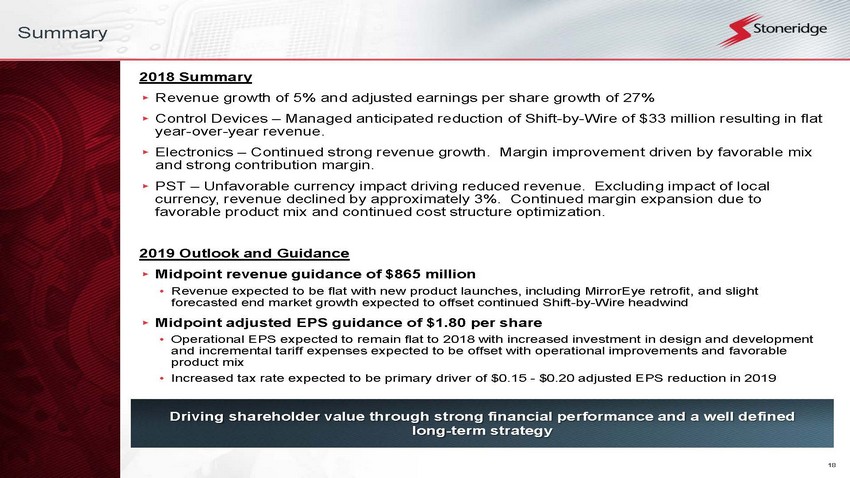

18 Summary 2018 Summary ▸ Revenue growth of 5% and adjusted earnings per share growth of 27% ▸ Control Devices – Managed anticipated reduction of Shift - by - Wire of $33 million resulting in flat year - over - year revenue. ▸ Electronics – Continued strong revenue growth. Margin improvement driven by favorable mix and strong contribution margin. ▸ PST – Unfavorable currency impact driving reduced revenue. Excluding impact of local currency, revenue declined by approximately 3%. Continued margin expansion due to favorable product mix and continued cost structure optimization. 2019 Outlook and Guidance ▸ Midpoint revenue guidance of $865 million • Revenue expected to be flat with new product launches, including MirrorEye retrofit, and slight forecasted end market growth expected to offset continued Shift - by - Wire headwind ▸ Midpoint adjusted EPS guidance of $1.80 per share • Operational EPS expected to remain flat to 2018 with increased investment in design and development and incremental tariff expenses expected to be offset with operational improvements and favorable product mix • Increased tax rate expected to be primary driver of $0.15 - $0.20 adjusted EPS reduction in 2019 Driving shareholder value through strong financial performance and a well defined long - term strategy

19 Appendix

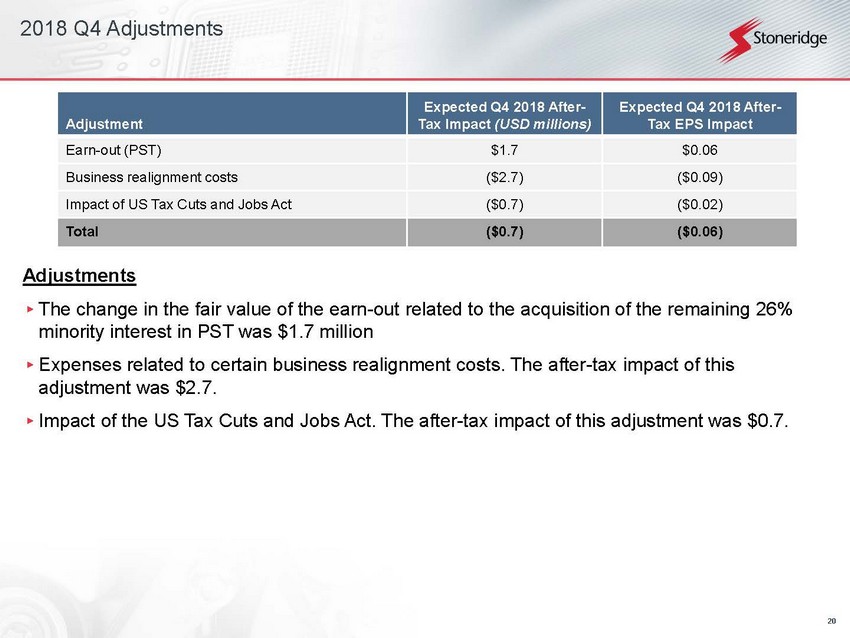

20 2018 Q4 Adjustments Adjustments ▸ The change in the fair value of the earn - out related to the acquisition of the remaining 26% minority interest in PST was $1.7 million ▸ Expenses related to certain business realignment costs. The after - tax impact of this adjustment was $2.7. ▸ Impact of the US Tax Cuts and Jobs Act. The after - tax impact of this adjustment was $0.7. Adjustment Expected Q4 2018 After - Tax Impact (USD millions) Expected Q4 2018 After - Tax EPS Impact Earn - out (PST) $1.7 $0.06 Business realignment costs ($2.7) ($0.09) Impact of US Tax Cuts and Jobs Act ($0.7) ($0.02) Total ($0.7) ($0.06)

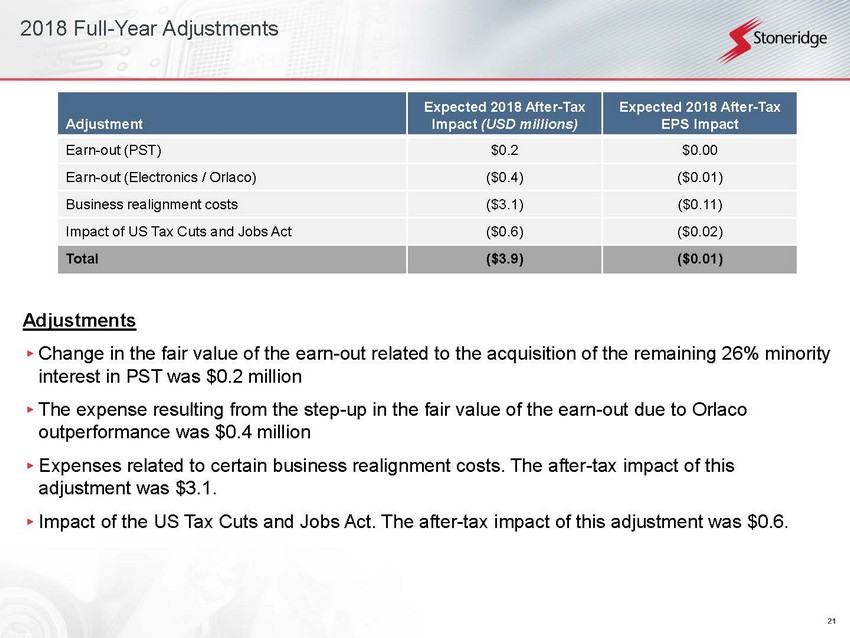

21 2018 Full - Year Adjustments Adjustments ▸ Change in the fair value of the earn - out related to the acquisition of the remaining 26% minority interest in PST was $0.2 million ▸ The expense resulting from the step - up in the fair value of the earn - out due to Orlaco outperformance was $0.4 million ▸ Expenses related to certain business realignment costs. The after - tax impact of this adjustment was $3.1. ▸ Impact of the US Tax Cuts and Jobs Act. The after - tax impact of this adjustment was $0.6. Adjustment Expected 2018 After - Tax Impact (USD millions) Expected 2018 After - Tax EPS Impact Earn - out (PST) $0.2 $0.00 Earn - out (Electronics / Orlaco) ($0.4) ($0.01) Business realignment costs ($3.1) ($0.11) Impact of US Tax Cuts and Jobs Act ($0.6) ($0.02) Total ($3.9) ($0.01)

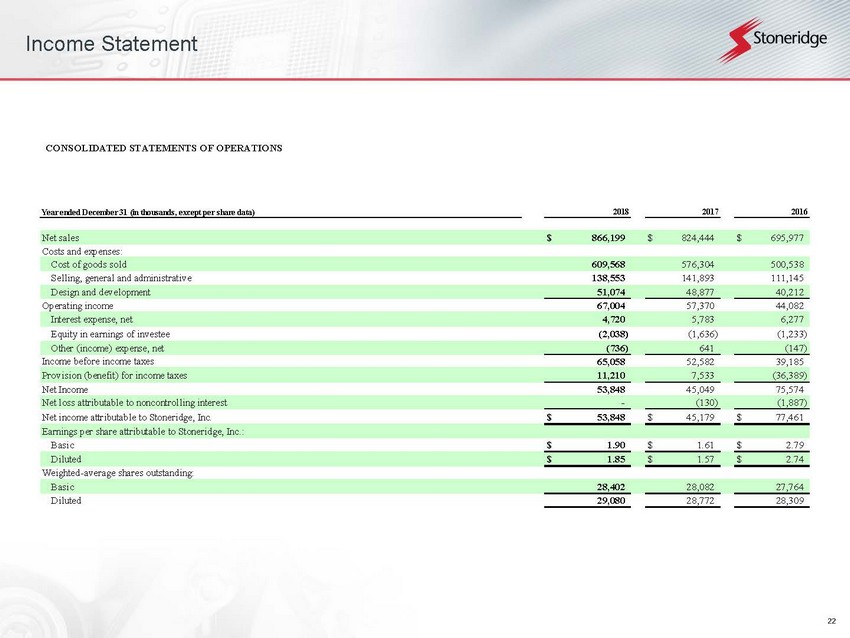

22 Income Statement Year ended December 31 (in thousands, except per share data) Net sales $ 866,199 $ 824,444 $ 695,977 Costs and expenses: Cost of goods sold 609,568 576,304 500,538 Selling, general and administrative 138,553 141,893 111,145 Design and development 51,074 48,877 40,212 Operating income 67,004 57,370 44,082 Interest expense, net 4,720 5,783 6,277 Equity in earnings of investee (2,038) (1,636) (1,233) Other (income) expense, net (736) 641 (147) 65,058 52,582 39,185 11,210 7,533 (36,389) Net Income 53,848 45,049 75,574 Net loss attributable to noncontrolling interest - (130) (1,887) Net income attributable to Stoneridge, Inc. $ 53,848 $ 45,179 $ 77,461 Earnings per share attributable to Stoneridge, Inc.: Basic $ 1.90 $ 1.61 $ 2.79 Diluted $ 1.85 $ 1.57 $ 2.74 Weighted-average shares outstanding: Basic 28,402 28,082 27,764 Diluted 29,080 28,772 28,309 2016 CONSOLIDATED STATEMENTS OF OPERATIONS Income before income taxes Provision (benefit) for income taxes 2018 2017

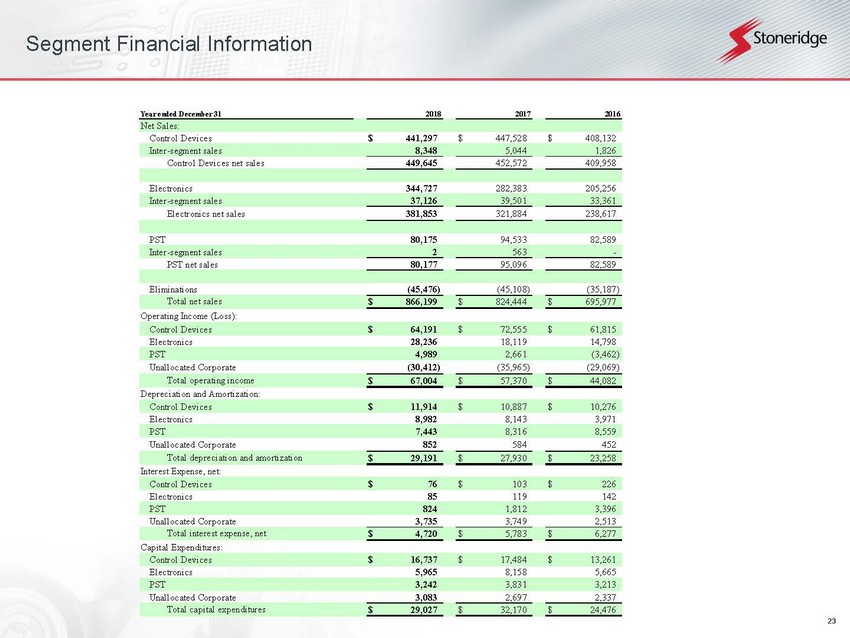

23 Segment Financial Information Year ended December 31 Net Sales: Control Devices $ 441,297 $ 447,528 $ 408,132 Inter-segment sales 8,348 5,044 1,826 Control Devices net sales 449,645 452,572 409,958 Electronics 344,727 282,383 205,256 Inter-segment sales 37,126 39,501 33,361 Electronics net sales 381,853 321,884 238,617 PST 80,175 94,533 82,589 Inter-segment sales 2 563 - PST net sales 80,177 95,096 82,589 Eliminations (45,476) (45,108) (35,187) Total net sales $ 866,199 $ 824,444 $ 695,977 Operating Income (Loss): Control Devices $ 64,191 $ 72,555 $ 61,815 Electronics 28,236 18,119 14,798 PST 4,989 2,661 (3,462) Unallocated Corporate (30,412) (35,965) (29,069) Total operating income $ 67,004 $ 57,370 $ 44,082 Depreciation and Amortization: Control Devices $ 11,914 $ 10,887 $ 10,276 Electronics 8,982 8,143 3,971 PST 7,443 8,316 8,559 Unallocated Corporate 852 584 452 Total depreciation and amortization $ 29,191 $ 27,930 $ 23,258 Interest Expense, net: Control Devices $ 76 $ 103 $ 226 Electronics 85 119 142 PST 824 1,812 3,396 Unallocated Corporate 3,735 3,749 2,513 Total interest expense, net $ 4,720 $ 5,783 $ 6,277 Capital Expenditures: Control Devices $ 16,737 $ 17,484 $ 13,261 Electronics 5,965 8,158 5,665 PST 3,242 3,831 3,213 Unallocated Corporate 3,083 2,697 2,337 Total capital expenditures $ 29,027 $ 32,170 $ 24,476 20162018 2017

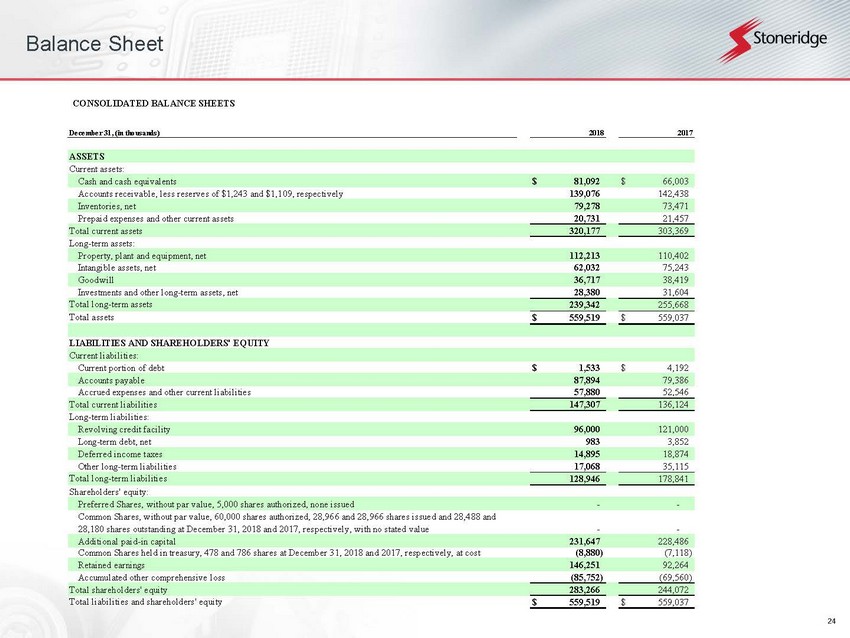

24 Balance Sheet CONSOLIDATED BALANCE SHEETS December 31, (in thousands) ASSETS Current assets: Cash and cash equivalents $ 81,092 $ 66,003 Accounts receivable, less reserves of $1,243 and $1,109, respectively 139,076 142,438 Inventories, net 79,278 73,471 Prepaid expenses and other current assets 20,731 21,457 Total current assets 320,177 303,369 Long-term assets: Property, plant and equipment, net 112,213 110,402 Intangible assets, net 62,032 75,243 Goodwill 36,717 38,419 Investments and other long-term assets, net 28,380 31,604 Total long-term assets 239,342 255,668 Total assets $ 559,519 $ 559,037 LIABILITIES AND SHAREHOLDERS' EQUITY Current liabilities: Current portion of debt $ 1,533 $ 4,192 Accounts payable 87,894 79,386 Accrued expenses and other current liabilities 57,880 52,546 Total current liabilities 147,307 136,124 Long-term liabilities: Revolving credit facility 96,000 121,000 Long-term debt, net 983 3,852 Deferred income taxes 14,895 18,874 Other long-term liabilities 17,068 35,115 Total long-term liabilities 128,946 178,841 Shareholders' equity: Preferred Shares, without par value, 5,000 shares authorized, none issued - - Common Shares, without par value, 60,000 shares authorized, 28,966 and 28,966 shares issued and 28,488 and 28,180 shares outstanding at December 31, 2018 and 2017, respectively, with no stated value - - Additional paid-in capital 231,647 228,486 Common Shares held in treasury, 478 and 786 shares at December 31, 2018 and 2017, respectively, at cost (8,880) (7,118) Retained earnings 146,251 92,264 Accumulated other comprehensive loss (85,752) (69,560) Total shareholders' equity 283,266 244,072 Total liabilities and shareholders' equity $ 559,519 $ 559,037 2017 2018

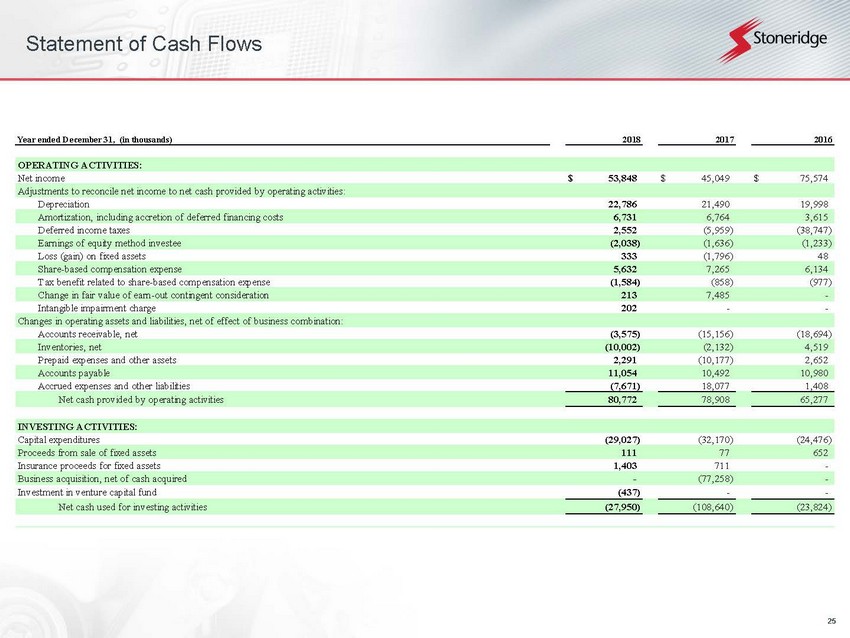

25 Statement of Cash Flows Year ended December 31, (in thousands) OPERATING ACTIVITIES: Net income $ 53,848 $ 45,049 $ 75,574 Adjustments to reconcile net income to net cash provided by operating activities: Depreciation 22,786 21,490 19,998 Amortization, including accretion of deferred financing costs 6,731 6,764 3,615 Deferred income taxes 2,552 (5,959) (38,747) Earnings of equity method investee (2,038) (1,636) (1,233) Loss (gain) on fixed assets 333 (1,796) 48 Share-based compensation expense 5,632 7,265 6,134 Tax benefit related to share-based compensation expense (1,584) (858) (977) Change in fair value of earn-out contingent consideration 213 7,485 - Intangible impairment charge 202 - - Changes in operating assets and liabilities, net of effect of business combination: Accounts receivable, net (3,575) (15,156) (18,694) Inventories, net (10,002) (2,132) 4,519 Prepaid expenses and other assets 2,291 (10,177) 2,652 Accounts payable 11,054 10,492 10,980 Accrued expenses and other liabilities (7,671) 18,077 1,408 Net cash provided by operating activities 80,772 78,908 65,277 INVESTING ACTIVITIES: Capital expenditures (29,027) (32,170) (24,476) Proceeds from sale of fixed assets 111 77 652 Insurance proceeds for fixed assets 1,403 711 - Business acquisition, net of cash acquired - (77,258) - Investment in venture capital fund (437) - - Net cash used for investing activities (27,950) (108,640) (23,824) 20162018 2017

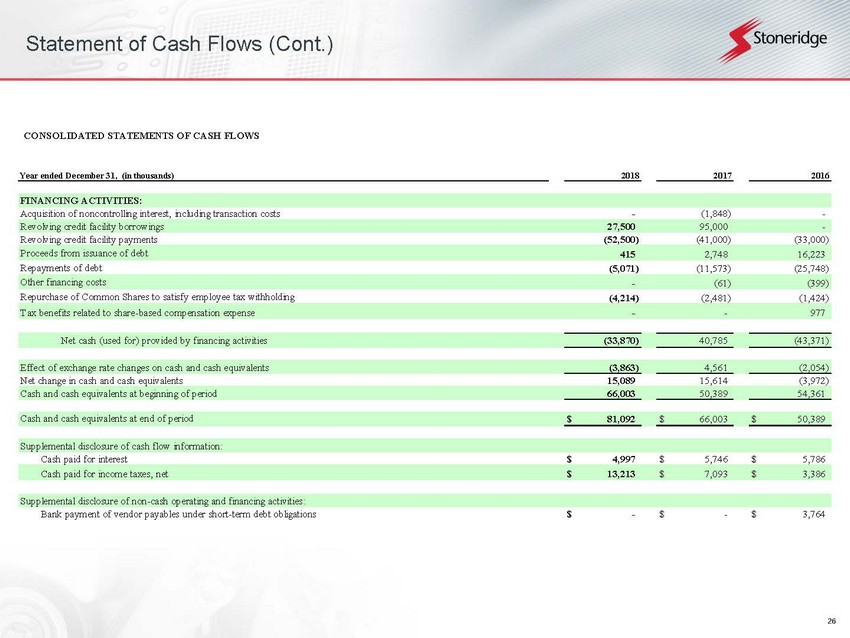

26 Statement of Cash Flows (Cont.) CONSOLIDATED STATEMENTS OF CASH FLOWS Year ended December 31, (in thousands) FINANCING ACTIVITIES: Acquisition of noncontrolling interest, including transaction costs - (1,848) - Revolving credit facility borrowings 27,500 95,000 - Revolving credit facility payments (52,500) (41,000) (33,000) Proceeds from issuance of debt 415 2,748 16,223 Repayments of debt (5,071) (11,573) (25,748) Other financing costs - (61) (399) Repurchase of Common Shares to satisfy employee tax withholding (4,214) (2,481) (1,424) Tax benefits related to share-based compensation expense - - 977 Net cash (used for) provided by financing activities (33,870) 40,785 (43,371) Effect of exchange rate changes on cash and cash equivalents (3,863) 4,561 (2,054) Net change in cash and cash equivalents 15,089 15,614 (3,972) Cash and cash equivalents at beginning of period 66,003 50,389 54,361 Cash and cash equivalents at end of period $ 81,092 $ 66,003 $ 50,389 Supplemental disclosure of cash flow information: Cash paid for interest $ 4,997 $ 5,746 $ 5,786 Cash paid for income taxes, net $ 13,213 $ 7,093 $ 3,386 Supplemental disclosure of non-cash operating and financing activities: Bank payment of vendor payables under short-term debt obligations $ - $ - $ 3,764 2018 2017 2016

27 Reconciliations to US GAAP

28 Reconciliations to US GAAP This document contains information about Stoneridge's financial results which is not presented in accordance with accounting principles generally accepted in the United States ("GAAP"). Such non - GAAP financial measures are reconciled to their closest GAAP financial measures in the appendix of this document. The provision of these non - GAAP financial measures is not intended to indicate that Stoneridge is explicitly or implicitly providing projections on those non - GAAP financial measures, and actual results for such measures are likely to vary from those presented. The reconciliations include all information reasonably available to the Company at the date of this document and the adjustments that management can reasonably predict.

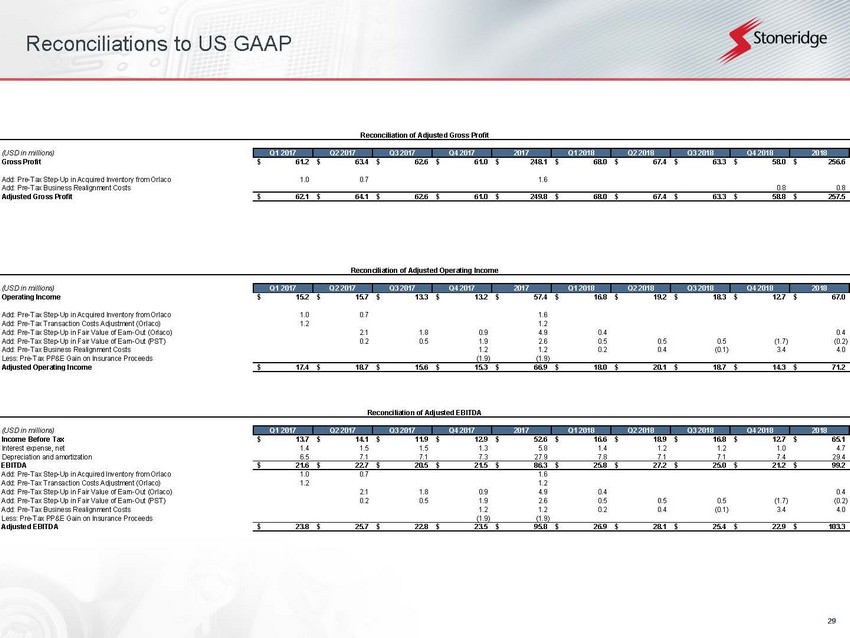

29 Reconciliations to US GAAP (USD in millions) Q1 2017 Q2 2017 Q3 2017 Q4 2017 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 2018 Gross Profit 61.2$ 63.4$ 62.6$ 61.0$ 248.1$ 68.0$ 67.4$ 63.3$ 58.0$ 256.6$ Add: Pre-Tax Step-Up in Acquired Inventory from Orlaco 1.0 0.7 1.6 Add: Pre-Tax Business Realignment Costs 0.8 0.8 Adjusted Gross Profit 62.1$ 64.1$ 62.6$ 61.0$ 249.8$ 68.0$ 67.4$ 63.3$ 58.8$ 257.5$ Reconciliation of Adjusted Gross Profit (USD in millions) Q1 2017 Q2 2017 Q3 2017 Q4 2017 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 2018 Operating Income 15.2$ 15.7$ 13.3$ 13.2$ 57.4$ 16.8$ 19.2$ 18.3$ 12.7$ 67.0$ Add: Pre-Tax Step-Up in Acquired Inventory from Orlaco 1.0 0.7 1.6 Add: Pre-Tax Transaction Costs Adjustment (Orlaco) 1.2 1.2 Add: Pre-Tax Step-Up in Fair Value of Earn-Out (Orlaco) 2.1 1.8 0.9 4.9 0.4 0.4 Add: Pre-Tax Step-Up in Fair Value of Earn-Out (PST) 0.2 0.5 1.9 2.6 0.5 0.5 0.5 (1.7) (0.2) Add: Pre-Tax Business Realignment Costs 1.2 1.2 0.2 0.4 (0.1) 3.4 4.0 Less: Pre-Tax PP&E Gain on Insurance Proceeds (1.9) (1.9) Adjusted Operating Income 17.4$ 18.7$ 15.6$ 15.3$ 66.9$ 18.0$ 20.1$ 18.7$ 14.3$ 71.2$ Reconciliation of Adjusted Operating Income (USD in millions) Q1 2017 Q2 2017 Q3 2017 Q4 2017 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 2018 Income Before Tax 13.7$ 14.1$ 11.9$ 12.9$ 52.6$ 16.6$ 18.9$ 16.8$ 12.7$ 65.1$ Interest expense, net 1.4 1.5 1.5 1.3 5.8 1.4 1.2 1.2 1.0 4.7 Depreciation and amortization 6.5 7.1 7.1 7.3 27.9 7.8 7.1 7.1 7.4 29.4 EBITDA 21.6$ 22.7$ 20.5$ 21.5$ 86.3$ 25.8$ 27.2$ 25.0$ 21.2$ 99.2$ Add: Pre-Tax Step-Up in Acquired Inventory from Orlaco 1.0 0.7 1.6 Add: Pre-Tax Transaction Costs Adjustment (Orlaco) 1.2 1.2 Add: Pre-Tax Step-Up in Fair Value of Earn-Out (Orlaco) 2.1 1.8 0.9 4.9 0.4 0.4 Add: Pre-Tax Step-Up in Fair Value of Earn-Out (PST) 0.2 0.5 1.9 2.6 0.5 0.5 0.5 (1.7) (0.2) Add: Pre-Tax Business Realignment Costs 1.2 1.2 0.2 0.4 (0.1) 3.4 4.0 Less: Pre-Tax PP&E Gain on Insurance Proceeds (1.9) (1.9) Adjusted EBITDA 23.8$ 25.7$ 22.8$ 23.5$ 95.8$ 26.9$ 28.1$ 25.4$ 22.9$ 103.3$ Reconciliation of Adjusted EBITDA

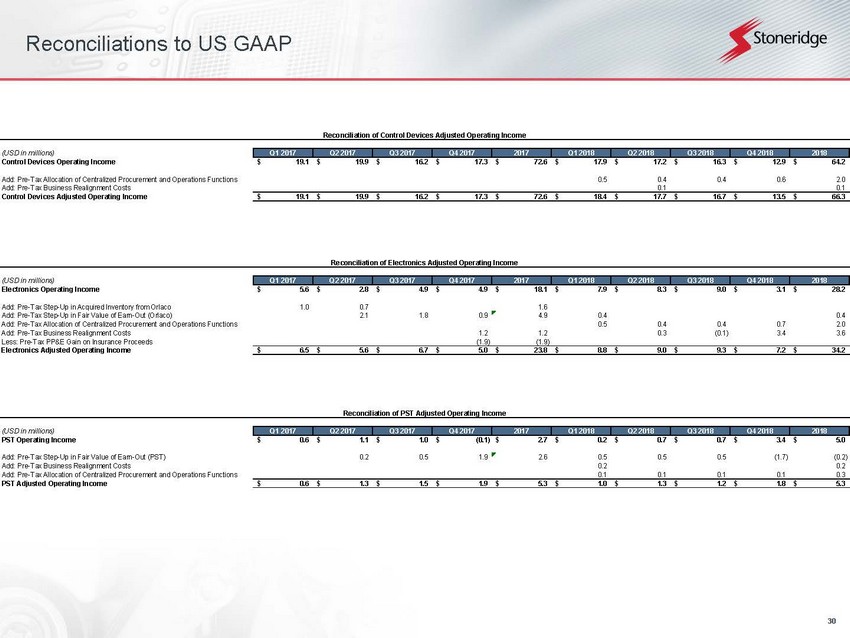

30 Reconciliations to US GAAP (USD in millions) Q1 2017 Q2 2017 Q3 2017 Q4 2017 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 2018 Control Devices Operating Income 19.1$ 19.9$ 16.2$ 17.3$ 72.6$ 17.9$ 17.2$ 16.3$ 12.9$ 64.2$ Add: Pre-Tax Allocation of Centralized Procurement and Operations Functions 0.5 0.4 0.4 0.6 2.0 Add: Pre-Tax Business Realignment Costs 0.1 0.1 Control Devices Adjusted Operating Income 19.1$ 19.9$ 16.2$ 17.3$ 72.6$ 18.4$ 17.7$ 16.7$ 13.5$ 66.3$ Reconciliation of Control Devices Adjusted Operating Income (USD in millions) Q1 2017 Q2 2017 Q3 2017 Q4 2017 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 2018 Electronics Operating Income 5.6$ 2.8$ 4.9$ 4.9$ 18.1$ 7.9$ 8.3$ 9.0$ 3.1$ 28.2$ Add: Pre-Tax Step-Up in Acquired Inventory from Orlaco 1.0 0.7 1.6 Add: Pre-Tax Step-Up in Fair Value of Earn-Out (Orlaco) 2.1 1.8 0.9 4.9 0.4 0.4 Add: Pre-Tax Allocation of Centralized Procurement and Operations Functions 0.5 0.4 0.4 0.7 2.0 Add: Pre-Tax Business Realignment Costs 1.2 1.2 0.3 (0.1) 3.4 3.6 Less: Pre-Tax PP&E Gain on Insurance Proceeds (1.9) (1.9) Electronics Adjusted Operating Income 6.5$ 5.6$ 6.7$ 5.0$ 23.8$ 8.8$ 9.0$ 9.3$ 7.2$ 34.2$ Reconciliation of Electronics Adjusted Operating Income (USD in millions) Q1 2017 Q2 2017 Q3 2017 Q4 2017 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 2018 PST Operating Income 0.6$ 1.1$ 1.0$ (0.1)$ 2.7$ 0.2$ 0.7$ 0.7$ 3.4$ 5.0$ Add: Pre-Tax Step-Up in Fair Value of Earn-Out (PST) 0.2 0.5 1.9 2.6 0.5 0.5 0.5 (1.7) (0.2) Add: Pre-Tax Business Realignment Costs 0.2 0.2 Add: Pre-Tax Allocation of Centralized Procurement and Operations Functions 0.1 0.1 0.1 0.1 0.3 PST Adjusted Operating Income 0.6$ 1.3$ 1.5$ 1.9$ 5.3$ 1.0$ 1.3$ 1.2$ 1.8$ 5.3$ Reconciliation of PST Adjusted Operating Income

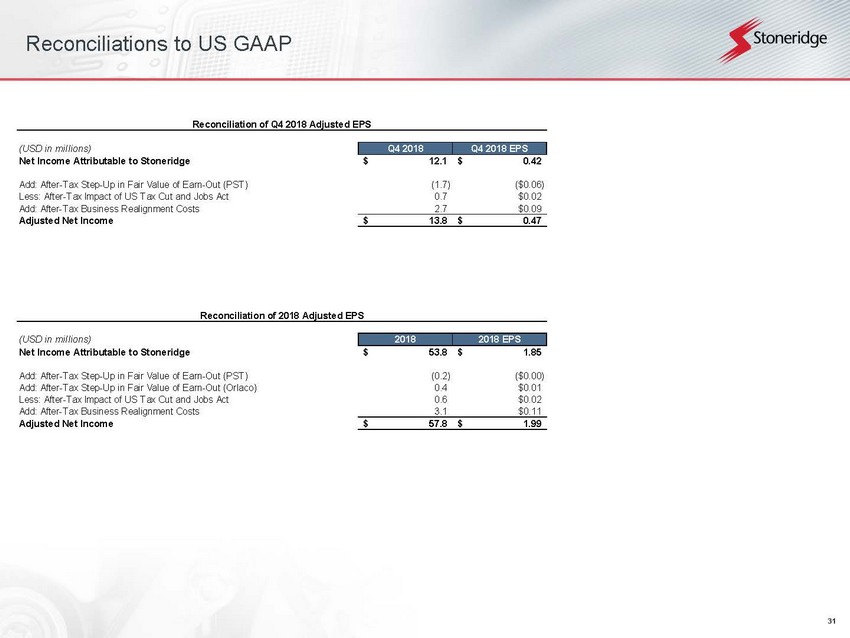

31 Reconciliations to US GAAP (USD in millions) Q4 2018 Q4 2018 EPS Net Income Attributable to Stoneridge 12.1$ 0.42$ Add: After-Tax Step-Up in Fair Value of Earn-Out (PST) (1.7) ($0.06) Less: After-Tax Impact of US Tax Cut and Jobs Act 0.7 $0.02 Add: After-Tax Business Realignment Costs 2.7 $0.09 Adjusted Net Income 13.8$ 0.47$ Reconciliation of Q4 2018 Adjusted EPS (USD in millions) 2018 2018 EPS Net Income Attributable to Stoneridge 53.8$ 1.85$ Add: After-Tax Step-Up in Fair Value of Earn-Out (PST) (0.2) ($0.00) Add: After-Tax Step-Up in Fair Value of Earn-Out (Orlaco) 0.4 $0.01 Less: After-Tax Impact of US Tax Cut and Jobs Act 0.6 $0.02 Add: After-Tax Business Realignment Costs 3.1 $0.11 Adjusted Net Income 57.8$ 1.99$ Reconciliation of 2018 Adjusted EPS

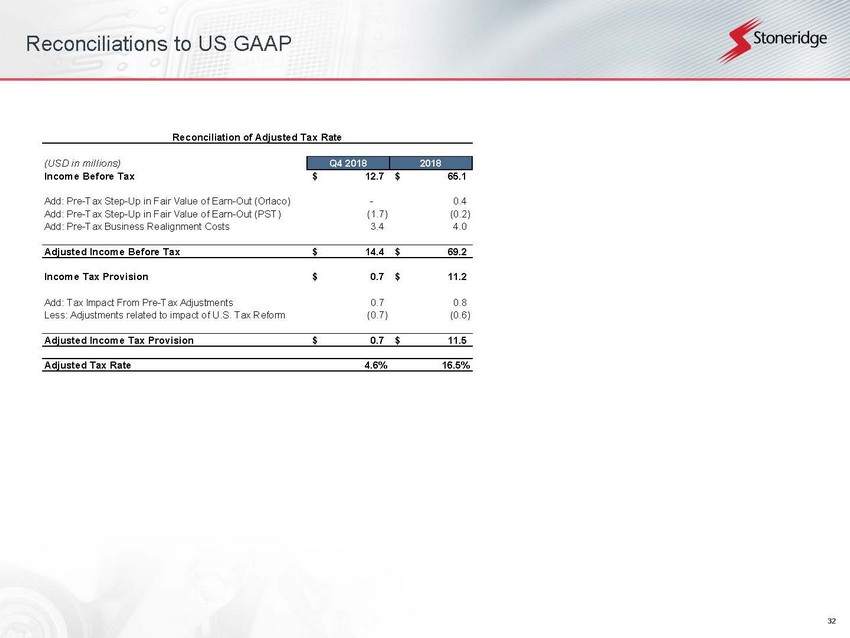

32 Reconciliations to US GAAP (USD in millions) Q4 2018 2018 Income Before Tax 12.7$ 65.1$ Add: Pre-Tax Step-Up in Fair Value of Earn-Out (Orlaco) - 0.4 Add: Pre-Tax Step-Up in Fair Value of Earn-Out (PST) (1.7) (0.2) Add: Pre-Tax Business Realignment Costs 3.4 4.0 Adjusted Income Before Tax 14.4$ 69.2$ Income Tax Provision 0.7$ 11.2$ Add: Tax Impact From Pre-Tax Adjustments 0.7 0.8 Less: Adjustments related to impact of U.S. Tax Reform (0.7) (0.6) Adjusted Income Tax Provision 0.7$ 11.5$ Adjusted Tax Rate 4.6% 16.5% Reconciliation of Adjusted Tax Rate