High-Bandwidth Connectivity Solutions

AboveNet, Inc.

Second Quarter 2010

Earnings Conference Call

August 6, 2010

Bill LaPerch, President & CEO

Joe Ciavarella, SVP & CFO

2

Statements made in this presentation that are not historical in nature constitute forward-looking statements

within the meaning of the Safe Harbor Provisions of the Private Securities Litigation Reform Act of 1995.

We cannot assure you that the future results expressed or implied by the forward-looking statements will

be achieved. Such statements are based on the current expectations and beliefs of the management of

AboveNet, Inc. and are subject to a number of risks and uncertainties that could cause actual results to

differ materially from the future results expressed or implied by such forward-looking statements. These

risks and uncertainties include, but are not limited to, the Company's financial and operating prospects,

current economic trends, future opportunities, the Company's exposure to the financial services industry

and strength of competition and pricing. The Company's business could be materially adversely affected

and the trading price of the Company's common stock could decline if these risks and uncertainties

develop into actual events. The Company cautions you not to place undue reliance on these forward-

looking statements, which speak only as of their respective dates. The Company undertakes no obligation

to publicly update or revise forward-looking statements to reflect events or circumstances after the date of

this presentation or to reflect the occurrence of unanticipated events. A more detailed discussion of

factors that may affect the Company's business and future financial results is included in the Company’s

SEC filings, including, but not limited to, those described in “Risk Factors” and "Management's Discussion

and Analysis of Financial Condition and Results of Operations" in the Company's Annual Report on Form

10-K for the year ended December 31, 2009 and in the Company's subsequently filed Quarterly Report(s)

on Form 10-Q. We discuss certain non-GAAP financial measures in this presentation and provide the

GAAP financial measures that correspond to such non-GAAP measures, as well as the reconciliati

on between the two.

Safe Harbor Statement

3

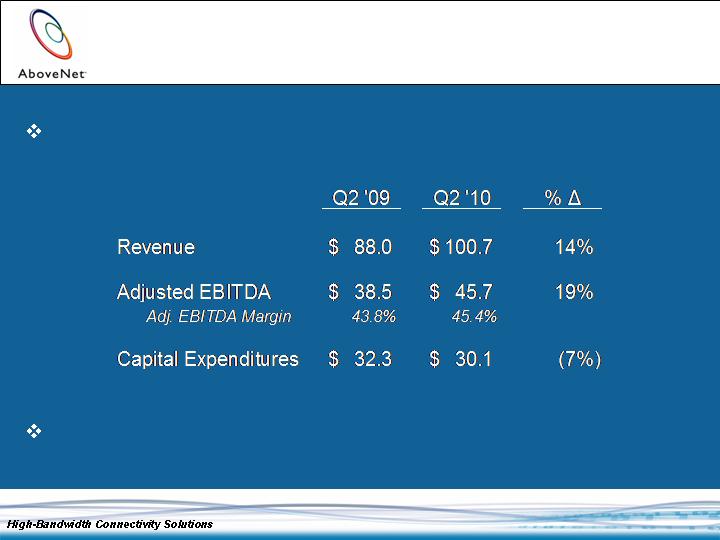

Q2 2010 Highlights

First $100 million revenue quarter

$/M

It was a great quarter

4

Q2 2010 Highlights

Company continues to execute

Customer demand remains steady, signed a few large WDM deals

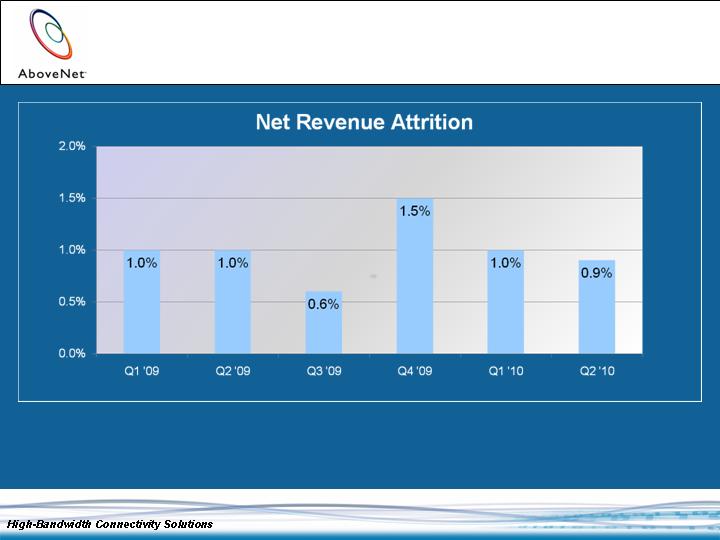

Net Revenue Attrition in line with business plan

Average MRR for new orders declined slightly

Customer deal provided catalyst to invest in previously inactive

Denver market. Expect to have Denver operational by year end

Launched Core Wave services in select markets

Metro optical core networks based at key data centers

Continued evolution of delivery methodology and service choice

Significant progress toward implementation of growth

initiatives

Capital expenditures will increase during the second half of year

5

Growth Initiatives – New Markets

Expect to be operational in Paris, Frankfurt, and Amsterdam by

year end

ROADM-based metro optical networks in London, Paris,

Frankfurt and Amsterdam

Scalable, next-generation European long haul network to connect

the markets together

Ability to offer services into 32 data centers in Europe

Sales effort to begin in the fourth quarter

Connected Miami to our domestic long haul network

Toronto – expect regulatory ruling by end of the third quarter

Net Revenue Attrition

6

Net Revenue Attrition: the reduction in monthly recurring revenue (MRR) for customers with net

decreases in MRR in the quarter (as a result of terminations, price declines and other decreases, which

are offset by any increases) divided by total revenue for the quarter (excluding contract termination

revenue).

7

Includes Contract Termination Revenue of $0.8, $1.0, $0.6, respectively

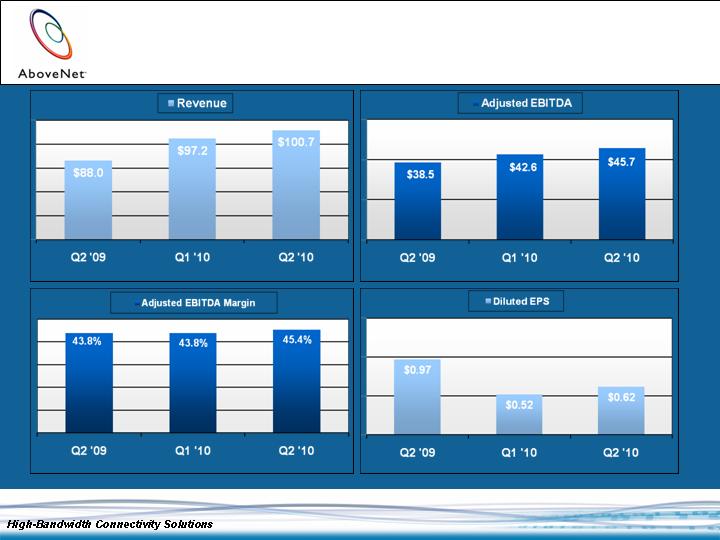

Q2 2010 Highlights

$/M

All periods adjusted for two-for-one stock split effective 09/03/09

$/M

Q1 and Q2 ’10 include income tax provisions that are

substantially non-cash.

8

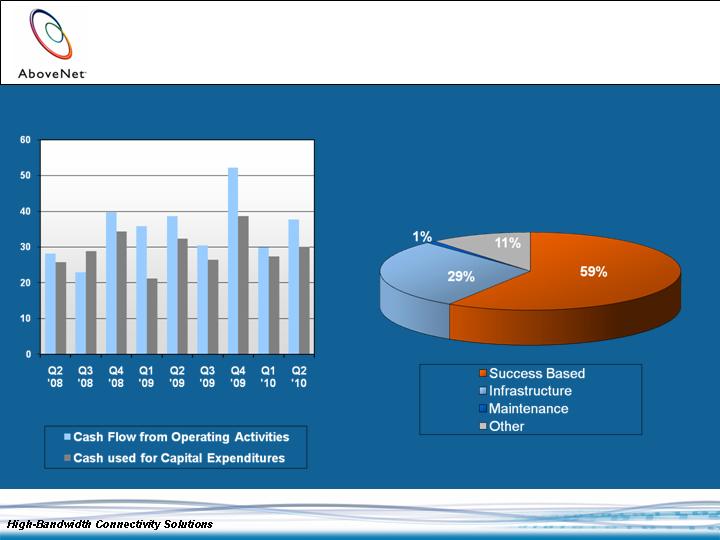

Cash Flow from Operating Activities and Capex

$/M

Capital Expenditure Components

June 30, 2010 YTD

High-Bandwidth Connectivity Solutions

Financial Review

10

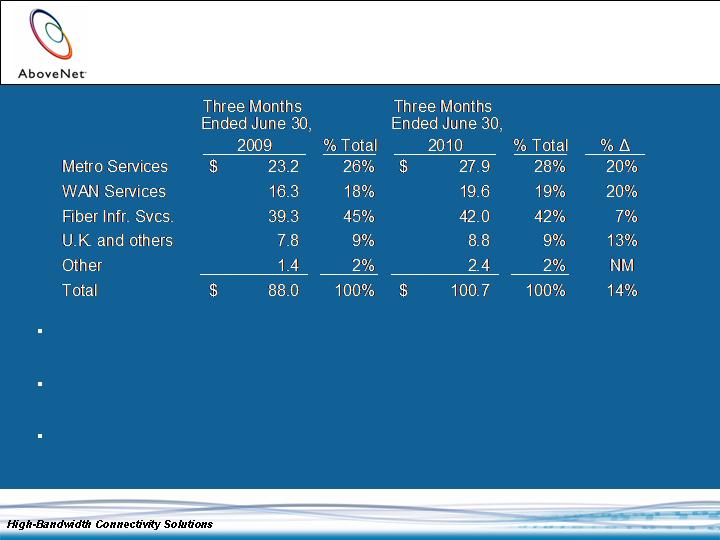

Q2 2010 Revenue –

Year-over-Year Comparison

$/M

Domestic Metro and WAN revenue increased from 44% to 47% of total revenue

between Q2 2009 and Q2 2010

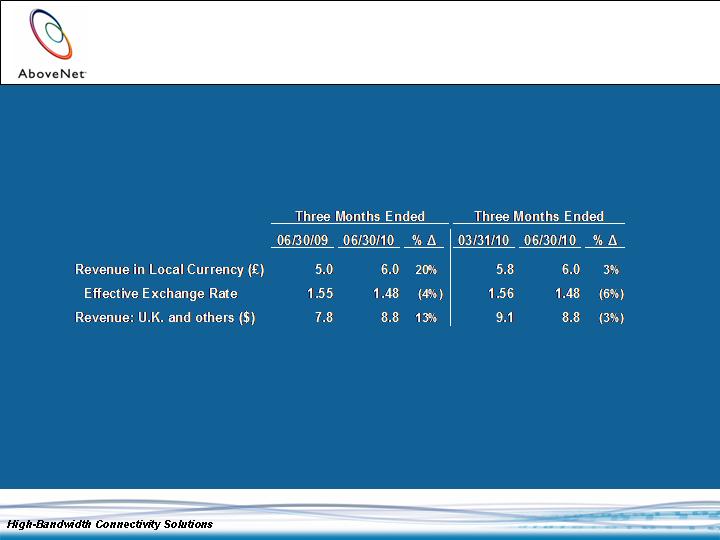

Revenue from U.K. operations increased 20% in local currency, which was offset

by a 4% impact due to weakening of the British Pound

Contract Termination Revenue was $0.8M in Q2 2009 vs. $0.6M in Q2 2010.

Adjusting for Contract Termination Revenue, increase was 15%

11

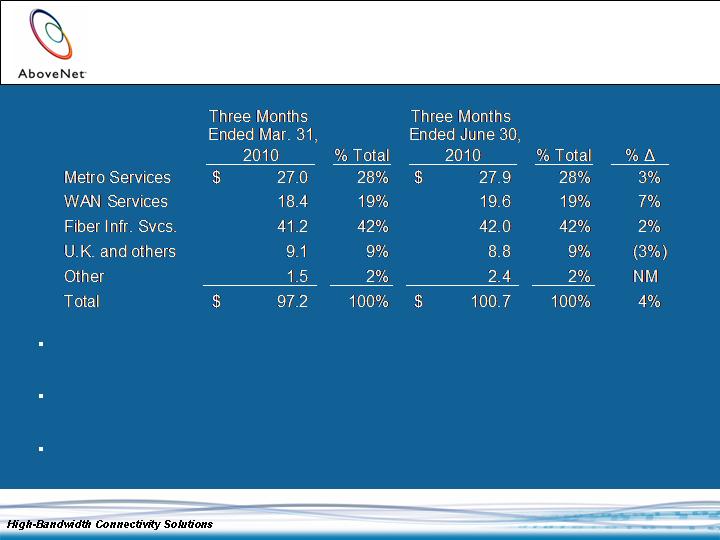

$/M

Domestic Metro and WAN Services accounted for majority of revenue increase

over Q1 2010

Revenue from U.K. operations increased 3% in local currency, which was offset

by a 6% impact due to weakening of the British Pound

Contract Termination Revenue was $1.0M in Q1 2010 vs. $0.6M in Q2 2010

Q2 2010 Revenue –

Sequential Quarter Comparison

12

Q2 2010 Highlights

Costs of Revenue increased over Q2 2009 primarily a result of increased co-location and expenses associated with

re-billable equipment sales to customers

Net Income and Diluted EPS for Q2 2009, Q1 2010 and Q2 2010 include income tax provisions of $0.2M, $9.6M and

$11.1M, respectively. In Q1 and Q2 2010, these income tax provisions are substantially non-cash

* Diluted EPS adjusted for two-for-one stock split effective 09/03/09

$/M, except EPS

13

Future Scheduled Secured Credit

Facility Repayments (as of 6/30/10)

$53.6 million term loan outstanding

$27 million revolver ($26 million available)

2008 2009 2010

Cash/cash equivalents $87.1 $165.3 $173.0

Debt(1)

$37.6 $58.6 $54.9

$/M (for period ended)

$/M (at period ended)

$/M

(1)

Includes capital lease obligation and senior secured credit

facility

Financial Strength

Secured Credit Facility

Cash Flow

Balance Sheet

2010 2011 2012 2013

$ 3.9 $ 7.6 $ 9.4 $32.7

2008 2009 2010

CF from Operating Act. $116.1 $157.2 $67.7

Capital Expenditures (2) $117.2 $118.7 $57.5

CF from Financing Act. $42.6 $38.9 ($2.2)

(2)

Per Consolidated Statements of Cash Flows

December 31,

December 31,

June 30,

June 30,

14

Business continues to perform well

Revenue guidance raised to $400M - $410M from $395M - $400M

Macroeconomic conditions remain uncertain; keeping Net Revenue

Attrition assumption at 1%

Revised revenue guidance includes Contract Termination Revenue for

full year

FY 2010 Adjusted EBITDA Margin expectations:

Roughly in line, to slightly above, 2009 actual Adjusted EBITDA margin

2010 Capital Expenditures forecast of $150M to $160M unchanged

Growth initiatives contribute to increased second half capital spend

2010 Outlook

High-Bandwidth Connectivity Solutions

Thank You

High-Bandwidth Connectivity Solutions

Appendix

17

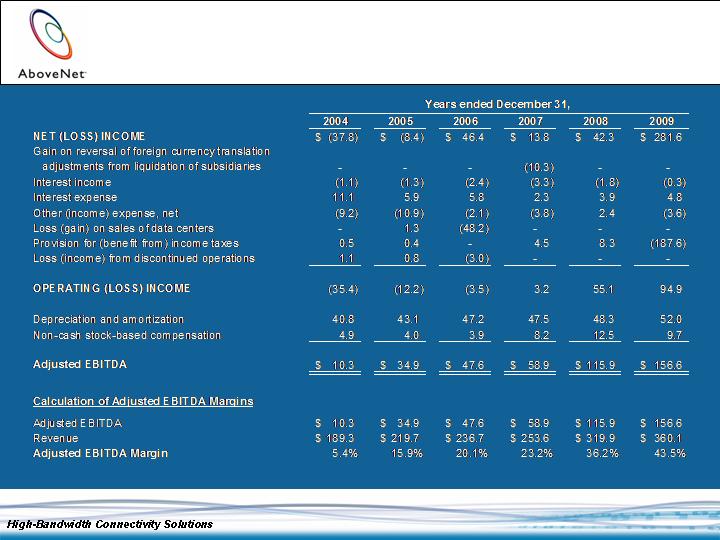

Adjusted EBITDA is defined as net income before provision for

(benefit from) income taxes, other income/expense, interest

income/expense, gain on reversal of foreign currency translation

adjustments from liquidation of subsidiaries, income/loss from

discontinued operations, gain/loss on asset dispositions,

depreciation and amortization, and non-cash stock-based

compensation

Adjusted EBITDA Margin is defined as Adjusted EBITDA divided by

revenue

Revenue, Net of Contract Termination Revenue is defined as

Revenue minus Contract Termination Revenue

Revenue in Local Currency is defined as Revenue from U.K. and

others in the respective functional currency. This amount is

multiplied by the period average exchange rate between such local

functional currency and our functional currency, the U.S. dollar, to

derive Revenue: UK and others ($)

Reconciliation of Non-GAAP

Financial Measures

18

Reconciliation of Non-GAAP

Financial Measures (Cont’d)

19

Reconciliation of Non-GAAP

Financial Measures (Cont’d)

$/M

20

Reconciliation of Non-GAAP

Financial Measures (Cont’d)

$/M

21

Reconciliation of Non-GAAP

Financial Measures (Cont’d)

(in millions)

Note: The percentage changes are calculated based on the detailed amounts and may differ slightly from

percentages calculated based on rounded amounts in the table above.

Reconciliation of Non-GAAP

Financial Measures (Cont’d)

AboveNet’s management believes that adjusted or modified EBITDA and its related margin are measures of

operating performance that are commonly reported and widely used by analysts, investors, and other interested

parties in the telecommunications industry because they eliminate many differences in financial, capitalization,

and tax structures, as well as certain non-cash and non-operating charges to earnings. AboveNet’s

management currently uses Adjusted EBITDA and Adjusted EBITDA Margin for these purposes. AboveNet’s

management believes that Adjusted EBITDA and Adjusted EBITDA Margin trends can be used as indicators of

whether the Company’s operations are able to produce sufficient operating cash flow to fund working capital

needs, service debt obligations and fund capital expenditures.

Adjusted EBITDA is also used by the Company for other purposes, including, management’s assessment of

ongoing operations and as a measure for performance-based compensation. However, the definition of

adjusted EBITDA for other purposes may differ from the definition of Adjusted EBITDA used herein. For

example, for 2009 and 2010 the definition of adjusted EBITDA in the Company’s incentive cash bonus plan

excludes certain customer termination fees. Additionally, Adjusted EBITDA as used in this press release may

not be calculated identically to similarly titled measures reported by other companies.

The Company also reviews revenue, net of contract termination revenue as well as revenue in local currency.

Revenue, net of contract termination revenue shows the change in the Company’s recurring revenue from

period to period excluding the impact of non-recurring contract termination revenue. Revenue in local currency

shows the changes of foreign subsidiary revenue without the impact of currency fluctuations. Management

believes these non-GAAP metrics provide helpful insight into revenue trends.

22