UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

(Mark One)

| x | Quarterly Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the quarterly period ended March 31, 2007

or

| ¨ | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to

Commission file number 1-14760

RAIT FINANCIAL TRUST

(Exact name of registrant as specified in its charter)

| | |

| Maryland | | 23-2919819 |

State or other jurisdiction of incorporation or organization | | (I.R.S. Employer Identification No.) |

| | |

| 2929 Arch Street, 17th Floor, Philadelphia, PA | | 19104 |

| (Address of principal executive offices) | | (Zip Code) |

(215) 861-7900

Registrant’s telephone number

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act (Check one):

x Large Accelerated Filer ¨ Accelerated Filer ¨ Non-Accelerated Filer

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ Yes x No

A total of 63,685,413 common shares of beneficial interest, par value $0.01 per share, of the registrant were outstanding as of May 1, 2007.

RAIT FINANCIAL TRUST

TABLE OF CONTENTS

PART I - FINANCIAL INFORMATION

| Item 1. | - Financial Statements |

RAIT Financial Trust

Consolidated Balance Sheets

As of March 31, 2007 and December 31, 2006

(Unaudited and dollars in thousands, except share and per share information)

| | | | | | | | |

| | | March 31,

2007 | | | December 31,

2006 | |

| Assets | | | | | | | | |

Investments in securities | | | | | | | | |

Available-for-sale securities | | $ | 4,743,748 | | | $ | 3,978,999 | |

Security-related receivables | | | 1,378,843 | | | | 1,159,312 | |

| | | | | | | | |

Total investments in securities | | | 6,122,591 | | | | 5,138,311 | |

Investments in mortgages and loans, at amortized cost | | | | | | | | |

Residential mortgages and mortgage-related receivables | | | 4,495,796 | | | | 4,676,950 | |

Commercial mortgages, mezzanine loans and other loans | | | 1,864,727 | | | | 1,250,945 | |

Allowance for losses | | | (8,716 | ) | | | (5,345 | ) |

| | | | | | | | |

Total investments in mortgages and loans | | | 6,351,807 | | | | 5,922,550 | |

Investments in real estate interests | | | 163,866 | | | | 139,132 | |

Real estate interests held for sale | | | 13,254 | | | | — | |

Cash and cash equivalents | | | 169,681 | | | | 99,367 | |

Restricted cash | | | 209,463 | | | | 292,869 | |

Accrued interest receivable | | | 115,269 | | | | 111,238 | |

Warehouse deposits | | | 56,510 | | | | 44,618 | |

Other assets | | | 41,848 | | | | 42,274 | |

Deferred financing costs, net of accumulated amortization of $2,515 and $1,709, respectively | | | 25,445 | | | | 16,729 | |

Intangible assets, net of accumulated amortization of $17,464 and $3,175, respectively | | | 106,757 | | | | 121,046 | |

Goodwill | | | 129,611 | | | | 132,372 | |

| | | | | | | | |

Total assets | | $ | 13,506,102 | | | $ | 12,060,506 | |

| | | | | | | | |

| Liabilities and shareholders’ equity | | | | | | | | |

Indebtedness | | | | | | | | |

Repurchase agreements and other indebtedness | | $ | 1,983,123 | | | $ | 1,255,518 | |

Mortgage-backed securities issued | | | 3,568,889 | | | | 3,697,291 | |

Trust preferred obligations | | | 592,013 | | | | 643,639 | |

CDO notes payable | | | 5,373,447 | | | | 4,855,743 | |

| | | | | | | | |

Total indebtedness | | | 11,517,472 | | | | 10,452,191 | |

Accrued interest payable | | | 65,596 | | | | 67,393 | |

Accounts payable and accrued expenses | | | 19,785 | | | | 22,930 | |

Liabilities related to real estate interests held for sale | | | 250 | | | | — | |

Deferred taxes, borrowers’ escrows and other liabilities | | | 212,660 | | | | 158,197 | |

Distributions payable | | | 50,938 | | | | 39,118 | |

| | | | | | | | |

Total liabilities | | | 11,866,701 | | | | 10,739,829 | |

Minority interest | | | 123,517 | | | | 124,273 | |

Shareholders’ equity | | | | | | | | |

Preferred shares, $0.01 par value per share, 25,000,000 shares authorized; 7.75% Series A cumulative redeemable preferred shares, liquidation preference $25.00 per share, 2,760,000 shares issued and outstanding | | | 28 | | | | 28 | |

8.375% Series B cumulative redeemable preferred shares, liquidation preference $25.00 per share, 2,258,300 shares issued and outstanding | | | 23 | | | | 23 | |

Common shares, $0.01 par value per share, 200,000,000 shares authorized, 63,672,700 and 52,151,412 issued and outstanding, including 379,247 and 430,516 unvested restricted share awards, respectively | | | 632 | | | | 517 | |

Additional paid in capital | | | 1,589,631 | | | | 1,218,667 | |

Accumulated other comprehensive income (loss) | | | (24,094 | ) | | | (3,085 | ) |

Retained earnings (deficit) | | | (50,336 | ) | | | (19,746 | ) |

| | | | | | | | |

Total shareholders’ equity | | | 1,515,884 | | | | 1,196,404 | |

| | | | | | | | |

Total liabilities and shareholders’ equity | | $ | 13,506,102 | | | $ | 12,060,506 | |

| | | | | | | | |

The accompanying notes are an integral part of these consolidated financial statements.

1

RAIT Financial Trust

Consolidated Statements of Income

For the Three-Month Periods Ended March 31, 2007 and 2006

(Unaudited and dollars in thousands, except share and per share information)

| | | | | | | | |

| | | For the Three-Month Periods Ended March 31 | |

| | | 2007 | | | 2006 | |

| Revenue: | | | | | | | | |

Investment interest income | | $ | 202,679 | | | $ | 20,764 | |

Investment interest expense | | | (159,131 | ) | | | (5,375 | ) |

Provision for losses | | | (3,718 | ) | | | — | |

Change in fair value of free-standing derivatives | | | 3,196 | | | | — | |

| | | | | | | | |

Net investment income | | | 43,026 | | | | 15,389 | |

Rental income | | | 2,412 | | | | 3,553 | |

Fee and other income | | | 7,881 | | | | 5,661 | |

| | | | | | | | |

Total revenue | | | 53,319 | | | | 24,603 | |

| Expenses: | | | | | | | | |

Compensation expense | | | 8,376 | | | | 1,878 | |

Real estate operating expenses | | | 2,588 | | | | 1,966 | |

General and administrative | | | 6,283 | | | | 1,172 | |

Depreciation | | | 768 | | | | 304 | |

Amortization of intangible assets | | | 14,289 | | | | — | |

| | | | | | | | |

Total expenses | | | 32,304 | | | | 5,320 | |

| | | | | | | | |

Income before interest and other income (expense), minority interest, income taxes, and income from discontinued operations | | | 21,015 | | | | 19,283 | |

Interest and other income | | | 6,953 | | | | 349 | |

Unrealized gain on interest rate hedges | | | 88 | | | | — | |

Equity in loss of equity method investments | | | (4 | ) | | | — | |

Minority interest | | | (5,764 | ) | | | (4 | ) |

| | | | | | | | |

Income before taxes and discontinued operations | | | 22,288 | | | | 19,628 | |

Income tax benefit | | | 423 | | | | — | |

| | | | | | | | |

Income from continuing operations | | | 22,711 | | | | 19,628 | |

Income from discontinued operations | | | 156 | | | | 942 | |

| | | | | | | | |

Net income | | | 22,867 | | | | 20,570 | |

Income allocated to preferred shares | | | (2,519 | ) | | | (2,519 | ) |

| | | | | | | | |

Net income available to common shares | | $ | 20,348 | | | $ | 18,051 | |

| | | | | | | | |

Earnings per share—Basic: | | | | | | | | |

Continuing operations | | $ | 0.34 | | | $ | 0.62 | |

Discontinued operations | | | — | | | | 0.03 | |

| | | | | | | | |

Total earnings per share—Basic | | $ | 0.34 | | | $ | 0.65 | |

| | | | | | | | |

Weighted-average shares outstanding—Basic | | | 60,143,844 | | | | 27,900,276 | |

| | | | | | | | |

Earnings per share—Diluted: | | | | | | | | |

Continuing operations | | $ | 0.34 | | | $ | 0.61 | |

Discontinued operations | | | — | | | | 0.03 | |

| | | | | | | | |

Total earnings per share—Diluted | | $ | 0.34 | | | $ | 0.64 | |

| | | | | | | | |

Weighted-average shares outstanding—Diluted | | | 60,616,721 | | | | 28,121,735 | |

| | | | | | | | |

Distributions declared per common share | | $ | 0.80 | | | $ | 0.61 | |

| | | | | | | | |

The accompanying notes are an integral part of these consolidated financial statements.

2

RAIT Financial Trust

Consolidated Statements of Other Comprehensive Income (Loss)

For the Three-Month Periods Ended March 31, 2007 and 2006

(Unaudited and dollars in thousands)

| | | | | | | |

| | | For the Three-Month Periods Ended March 31 |

| | | 2007 | | | 2006 |

Net income | | $ | 22,867 | | | $ | 20,570 |

Other comprehensive income (loss) | | | | | | | |

Change in the fair value of cash-flow hedges | | | (11,859 | ) | | | — |

Reclassification adjustments associated with unrealized gains from cash flow hedges included in net income | | | (88 | ) | | | — |

Realized (gain) loss on cash-flow hedges reclassified to earnings | | | (1,207 | ) | | | — |

Change in fair value of available-for-sale securities | | | 1,110 | | | | — |

| | | | | | | |

Total other comprehensive loss before minority interest allocation | | | (12,044 | ) | | | — |

Allocation to minority interest | | | (8,965 | ) | | | — |

| | | | | | | |

Total other comprehensive income (loss) | | | (21,009 | ) | | | — |

| | | | | | | |

Comprehensive income | | $ | 1,858 | | | $ | 20,570 |

| | | | | | | |

The accompanying notes are an integral part of these consolidated financial statements.

3

RAIT Financial Trust

Consolidated Statements of Cash Flows

For the Three-Month Periods Ended March 31, 2007 and 2006

(Unaudited and dollars in thousands)

| | | | | | | | |

| | | For the Three-Month Periods Ended March 31 | |

| | | 2007 | | | 2006 | |

| Operating activities: | | | | | | |

Net income | | $ | 22,867 | | | $ | 20,570 | |

Adjustments to reconcile net income to cash flow from operating activities: | | | | | | | | |

Minority interest | | | 5,764 | | | | 4 | |

Provision for losses | | | 3,718 | | | | — | |

Amortization of deferred compensation | | | 2,956 | | | | 38 | |

Equity in loss of equity method investments | | | 4 | | | | — | |

Depreciation and amortization | | | 15,057 | | | | 536 | |

Amortization of deferred financing costs | | | 6,739 | | | | 401 | |

Accretion of loan discounts | | | (2,762 | ) | | | (6 | ) |

Unrealized gain on interest rate hedges | | | (88 | ) | | | — | |

Foreign currency adjustment | | | (782 | ) | | | — | |

Changes in assets and liabilities: | | | | | | | | |

Accrued interest receivable | | | (4,031 | ) | | | (1,904 | ) |

Other assets | | | (13,755 | ) | | | (489 | ) |

Accrued interest payable | | | (1,797 | ) | | | 169 | |

Accounts payable and accrued expenses | | | (3,145 | ) | | | 1,183 | |

Deferred taxes, borrowers’ escrows and other liabilities | | | 25,303 | | | | 589 | |

| | | | | | | | |

Cash flow from operating activities | | | 56,048 | | | | 21,091 | |

Investing activities: | | | | | | | | |

Purchase and origination of investments in securities | | | (970,246 | ) | | | — | |

Purchase and origination of investments in loans | | | (678,886 | ) | | | (226,941 | ) |

Principal repayments on loans | | | 248,524 | | | | 89,645 | |

Investment in real estate interests | | | (37,992 | ) | | | (2,291 | ) |

Proceeds from dispositions of real estate interests | | | — | | | | 198 | |

Decrease in restricted cash | | | 104,829 | | | | — | |

Increase in warehouse deposits | | | (11,892 | ) | | | — | |

| | | | | | | | |

Cash flow from investing activities | | | (1,345,663 | ) | | | (139,389 | ) |

Financing activities: | | | | | | | | |

Repayments on repurchase agreements and other indebtedness | | | (68,854 | ) | | | (22,700 | ) |

Proceeds from repurchase agreements and other indebtedness | | | 795,903 | | | | 85,000 | |

Repayments on residential mortgage-backed securities | | | (132,148 | ) | | | — | |

Repayments on TruPS obligations | | | (47,962 | ) | | | — | |

Proceeds from issuance of CDO notes payable | | | 511,607 | | | | — | |

Acquisition of minority interest in CDOs | | | (8,685 | ) | | | — | |

Distributions to minority interest holders in CDOs | | | (6,800 | ) | | | — | |

Payments for deferred costs | | | (8,720 | ) | | | — | |

Common share issuance, net of costs incurred | | | 367,029 | | | | 145 | |

Distributions paid to preferred shares | | | (2,523 | ) | | | (2,519 | ) |

Distributions paid to common shares | | | (38,918 | ) | | | — | |

| | | | | | | | |

Cash flow from financing activities | | | 1,359,929 | | | | 59,926 | |

| | | | | | | | |

Net change in cash and cash equivalents | | | 70,314 | | | | (58,372 | ) |

Cash and cash equivalents at the beginning of the period | | | 99,367 | | | | 71,420 | |

| | | | | | | | |

Cash and cash equivalents at the end of the period | | $ | 169,681 | | | $ | 13,048 | |

| | | | | | | | |

Supplemental cash flow information: | | | | | | | | |

Cash paid for interest | | $ | 147,458 | | | $ | 7,465 | |

Cash paid for taxes | | | 1,426 | | | | — | |

Non-cash decrease in goodwill | | | (2,761 | ) | | | — | |

Stock issued under dividend reinvestment plan | | | 196 | | | | — | |

Distributions payable | | | 50,938 | | | | — | |

The accompanying notes are an integral part of these consolidated financial statements.

4

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of March 31, 2007

(Unaudited and dollars in thousands, except share and per share amounts)

NOTE 1: RAIT FINANCIAL TRUST

RAIT Financial Trust is a specialty finance company that provides a comprehensive set of debt financing options to the real estate industry. References to “RAIT”, “we”, “us”, and “our” refer to RAIT Financial Trust and its subsidiaries, unless the context otherwise requires. We originate and invest in real estate-related assets that are underwritten through our integrated investment process. We conduct our business through our subsidiaries, RAIT Partnership, L.P., or RAIT Partnership, and Taberna Realty Finance Trust, or Taberna, as well as through their respective subsidiaries. We and Taberna are self-managed and self-advised Maryland real estate investment trusts, or REITs. Our objective is to provide our shareholders with total returns over time, including quarterly distributions and capital appreciation, while seeking to manage the risks associated with our investment strategy.

NOTE 2: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

a. Basis of Presentation

The accompanying unaudited interim consolidated financial statements have been prepared by management in accordance with U.S. generally accepted accounting principles, or GAAP. Certain information and footnote disclosures normally included in annual consolidated financial statements prepared in accordance with GAAP have been condensed or omitted pursuant to such rules and regulations, although we believe that the included disclosures are adequate to make the information presented not misleading. The unaudited interim consolidated financial statements should be read in conjunction with our audited financial statements as of and for the year ended December 31, 2006 included in our Annual Report on Form 10-K. In the opinion of management, all adjustments, consisting only of normal recurring adjustments, necessary to present fairly our consolidated financial position and consolidated results of operations and cash flows are included. The results of operations for the interim periods presented are not necessarily indicative of the results for the full year. Certain prior period amounts have been reclassified to conform with the current period presentation.

b. Principles of Consolidation

The consolidated financial statements reflect our accounts and those accounts of our majority-owned and/or controlled subsidiaries. We also consolidate entities that are variable interest entities, or VIEs, where we have determined that we are the primary beneficiary of such entities. The portions of these entities that we do not own are presented as minority interest as of the dates and for the periods presented in the consolidated financial statements. All intercompany accounts and transactions have been eliminated in consolidation.

c. Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the reporting periods. Actual results could differ from those estimates.

d. Investments

We invest in debt securities, residential mortgages and mortgage-related receivables, commercial mortgages, mezzanine loans and other types of real estate-related assets. We account for our investments in securities under Statement of Financial Accounting Standards No. 115, “Accounting for Certain Investments in Debt and Equity Securities,” as amended and interpreted, or SFAS No. 115, and designate each investment as a trading security, an available-for-sale security, or a held-to-maturity security based on our intent at the time of acquisition. Under SFAS No. 115, trading securities are recorded at their fair value each reporting period with fluctuations in fair value reported as a component of earnings. Available-for-sale securities are recorded at fair value with changes in fair value reported as a component of other comprehensive income (loss). Fair value is based primarily on quoted market prices from independent

5

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of March 31, 2007

(Unaudited and dollars in thousands, except share and per share amounts)

pricing sources when available for actively traded securities or discounted cash flow analyses developed by management using current interest rates and other market data for securities without an active market. Our estimate of fair value is subject to a high degree of variability based upon market conditions and management assumptions. Upon the sale of an available-for-sale security, the realized gain or loss on the sale will be recorded as a component of earnings in the respective period. Held-to-maturity investments are carried at amortized cost at each reporting period.

We account for our investments in subordinated debentures owned by trust VIEs that we consolidate as available-for-sale securities. These VIEs have no ability to sell, pledge, transfer or otherwise encumber the trust or the assets of the trust until such subordinated debenture’s maturity. We account for investments in securities where the transfer meets the criteria as a financing under Statement of Financial Accounting Standards No. 140, “Accounting for Transfers and Servicing of Financial Assets and Extinguishments of Liabilities”, or SFAS No. 140, at amortized cost. Our investments in security-related receivables represent securities that were transferred to issuers of collateralized debt obligations, or CDO, in which the transferors maintained some level of continuing involvement.

We account for our investments in residential mortgages and mortgage-related receivables, commercial mortgages, mezzanine loans and other loans at amortized cost. The carrying value of these investments is adjusted for origination discounts/premiums, nonrefundable fees and direct costs for originating loans which are amortized into income on a level yield basis over the terms of the loans. Mortgage-related receivables represent loan receivables secured by residential mortgages, the legal title to which is held by our trust subsidiaries. These residential mortgages were transferred to the trust subsidiaries in transactions accounted for as financings under SFAS No. 140. Mortgage-related receivables maintain all of the economic attributes of the underlying residential mortgages and all benefits or risks of that ownership inure to the trust subsidiary.

We use our judgment to determine whether an investment has sustained an other-than-temporary decline in value. If management determines that an investment has sustained an other-than-temporary decline in its value, the investment is written down to its fair value by a charge to earnings, and we establish a new cost basis for the investment. Our evaluation of an other-than-temporary decline is dependent on the specific facts and circumstances. Factors that we consider in determining whether an other-than-temporary decline in value has occurred include: the estimated fair value of the investment in relation to our cost basis; the financial condition of the related entity; and the intent and ability to retain the investment for a sufficient period of time to allow for recovery in the fair value of the investment.

We maintain an allowance for losses on our investments in residential mortgages and mortgage-related receivables, commercial mortgages, mezzanine loans and other loans. Our allowance for losses is based on management’s evaluation of known losses and inherent risks, for example, historical and industry loss experience, economic conditions and trends, estimated fair values, the quality of collateral and other relevant factors. Specific allowances for losses are established for impaired loans based on a comparison of the recorded carrying value of the loan to either the present value of the loan’s expected cash flow, the loan’s estimated market price or the estimated fair value of the underlying collateral. The allowance is increased by charges to operations and decreased by charge-offs (net of recoveries).

e. Transfers of Financial Assets

We account for transfers of financial assets under SFAS No. 140 as either sales or financings. Transfers of financial assets that result in sales accounting are those in which (1) the transfer legally isolates the transferred assets from the transferor, (2) the transferee has the right to pledge or exchange the transferred assets and no condition both constrains the transferee’s right to pledge or exchange the assets and provides more than a trivial benefit to the transferor, and (3) the transferor does not maintain effective control over the transferred assets. If the transfer does not meet these criteria, the transfer is accounted for as a financing. Financial assets that are treated as sales are removed from our accounts with any realized gain (loss) reflected in earnings during the period of sale. Financial assets that are treated as financings are maintained on the balance sheet with proceeds received from the legal transfer reflected as securitized borrowings.

6

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of March 31, 2007

(Unaudited and dollars in thousands, except share and per share amounts)

f. Revenue Recognition

| | 1) | Net investment income—We recognize interest income from investments in debt and other securities, residential mortgages, commercial mortgages and mezzanine loans on a yield to maturity basis. Upon the acquisition of a loan at a discount, we assess the portions of the discount that constitute accretable yields and non-accretable differences. The accretable yield represents the excess of our expected cash flows from the loan over the amount we paid for the loan. That amount, the accretable yield, is accreted to interest income over the remaining life of the loan. Many of our commercial mortgages and mezzanine loans provide for the accrual of interest at specified rates which differ from current payment terms. Interest income is recognized on such loans at the accrual rate subject to management’s determination that accrued interest and outstanding principal are ultimately collectible. Origination fees and direct loan origination costs are deferred and amortized to net investment income, using the effective interest method, over the contractual life of the underlying loan security or loan, in accordance with SFAS No. 91. We recognize interest income from interests in certain securitized financial assets on an estimated effective yield to maturity basis. Management estimates the current yield on the amortized cost of the investment based on estimated cash flows after considering prepayment and credit loss experience. |

| | 2) | Structuring fees—We receive structuring fees for services rendered in connection with the formation of CDO securitization entities. The structuring fee is a contractual fee paid when the related services are completed. The structuring fee is a negotiated fee with the investment bank acting as placement agent for the CDO securities and is capitalized by the CDO securitization entity as a deferred financing cost. We may decide to invest in the debt or equity securities issued by CDO securitization entities. We evaluate our investment in these entities under FIN 46R to determine whether the entity is a VIE, and, if so, whether or not we are the primary beneficiary. If we are determined to be the primary beneficiary, we will consolidate the accounts of the CDO securitization entity and upon consolidation, we eliminate intercompany transactions, specifically the structuring fees and deferred financing costs paid. Structuring fees totaling $5,625 were eliminated for the three month period ended March 31, 2007 upon the consolidation of Taberna Preferred Funding VIII. |

| | 3) | Fee and other income—we generate fee and other income, through our various subsidiaries, by providing (a) ongoing asset management services to CDO investment portfolios under cancelable management agreements, (b) providing or arranging to provide financing to our borrowers, and (c) providing financial consulting to our borrowers. We recognize revenue for these activities when the fees are fixed or determinable, evidenced by an arrangement, collection is reasonably assured and the services under the arrangement have been provided. CDO asset management fees are an administrative cost of a CDO entity and are paid by the CDO administrative trustee on behalf of its investors. These asset management fees are recognized when earned and are paid quarterly. Asset management fees from consolidated CDOs are eliminated in consolidation. During the three-month period ended March 31, 2007, we earned $5,650 of asset management fees, of which we eliminated $4,488 upon consolidation of CDOs of which we are the primary beneficiary. |

g. Off-Balance Sheet Arrangements

We maintain warehouse financing arrangements with various investment banks and engage in CDO securitizations. Prior to the completion of a CDO securitization, our warehouse providers acquire investments in accordance with the terms of the warehouse facilities. We are paid the difference between the interest earned on the investments and the interest charged by the warehouse providers from the dates on which the respective investments were acquired. We bear the first dollar risk of loss, up to our warehouse deposit amount, if (i) an investment funded through the warehouse facility becomes impaired or (ii) a CDO is not completed by the end of the warehouse period, and in either case, the warehouse provider

7

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of March 31, 2007

(Unaudited and dollars in thousands, except share and per share amounts)

is required to liquidate the securities at a loss. These off-balance sheet arrangements are not consolidated because our risk of loss is generally limited to the cash collateral held by the warehouse providers and our warehouse facilities are not special purpose vehicles. However, since we hold an implicit variable interest in many entities funded under our warehouse facilities, we often consolidate the Trust VIEs while the trust preferred securities, or TruPS, they issue are held on the warehouse lines. The economic return earned from these warehouse facilities is considered a non-hedge derivative and is recorded at fair value in our financial statements. Changes in fair value are reflected in earnings in the respective period.

h. Derivative Instruments

We may use derivative financial instruments to hedge all or a portion of the interest rate risk associated with our borrowings. Certain of the techniques used to hedge exposure to interest rate fluctuations may also be used to protect against declines in the market value of assets that result from general trends in debt markets. The principal objective of such agreements is to minimize the risks and/or costs associated with our operating and financial structure as well as to hedge specific anticipated transactions.

In accordance with Statement of Financial Accounting Standards No. 133, “Accounting for Derivative Instruments and Hedging Activities,” as amended and interpreted, or SFAS No. 133, we measure each derivative instrument (including certain derivative instruments embedded in other contracts) at fair value and record such amounts in its consolidated balance sheet as either an asset or liability. For derivatives designated as fair value hedges or for derivatives not designated as hedges, the changes in fair value of both the derivative instrument and the hedged item are recorded in earnings. For derivatives designated as cash flow hedges, the changes in the fair value of the effective portions of the derivative are reported in other comprehensive income. Changes in the ineffective portions of cash flow hedges are recognized in earnings.

i. Income Taxes

RAIT and Taberna have each elected to be taxed as a REIT and to comply with the related provisions of the Internal Revenue Code of 1986, as amended or, the Internal Revenue Code. Accordingly, we generally will not be subject to U.S. federal income tax to the extent of our distributions to shareholders and as long as certain asset, income and share ownership tests are met. If we were to fail to meet these requirements, we would be subject to U.S. federal income tax, which could have a material adverse impact on our results of operations and amounts available for distributions to our shareholders. Management believes that all of the criteria to maintain RAIT’s and Taberna’s REIT qualification have been met for the applicable periods, but, there can be no assurances that these criteria will continue to be met in subsequent periods.

We maintain various taxable REIT subsidiaries, or TRSs, which may be subject to U.S. federal, state and local income taxes. From time to time, these TRSs generate taxable income from intercompany transactions. The TRS entities generate taxable revenue from fees for services provided to CDO entities. Some of these fees paid to the TRS entities are capitalized as deferred financing costs by the CDO entities. Certain CDO entities may be consolidated in our financial statements pursuant to FIN 46R. In consolidation, these fees are eliminated when the CDO entity is included in the consolidated group. Nonetheless, all income taxes are accrued by the TRSs in the year in which the taxable revenue is received. These income taxes are not eliminated when the related revenue is eliminated in consolidation.

j. Goodwill and Intangible assets

On December 11, 2006, we acquired all of the outstanding common shares of Taberna Realty Finance Trust. Refer to our Annual Report on Form 10-K for additional information regarding this acquisition. As part of purchase accounting, we allocated the purchase price consideration to the net assets acquired, including identifiable intangible assets. As of December 31, 2006, we were finalizing the

8

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of March 31, 2007

(Unaudited and dollars in thousands, except share and per share amounts)

purchase price accounting allocation and were in the process of obtaining appraisals from third party valuation specialists. During the three month period ended March 31, 2007, we reallocated approximately $2,761 of the original purchase price amongst Taberna’s investments in securities and goodwill. Ultimately, these reallocations caused a reduction in goodwill and an increased amortized cost basis of the investment in securities by $2,761.

k. Recent Accounting Pronouncements

In February 2006, the FASB issued SFAS No. 155,Accounting for Certain Hybrid Financial Instruments, or SFAS No. 155. Key provisions of SFAS No. 155 include: (1) a broad fair value measurement option for certain hybrid financial instruments that contain an embedded derivative that would otherwise require bifurcation; (2) clarification that only the simplest separations of interest payments and principal payments qualify for the exception afforded to interest-only strips and principal-only strips from derivative accounting under paragraph 14 of SFAS No. 133,Accounting for Derivative Instruments and Hedging Activities, thereby narrowing such exception; (3) a requirement that beneficial interests in securitized financial assets be analyzed to determine whether they are freestanding derivatives or whether they are hybrid instruments that contain embedded derivatives requiring bifurcation; (4) clarification that concentrations of credit risk in the form of subordination are not embedded derivatives; and (5) elimination of the prohibition on a qualified special purpose entity, or QSPE, holding passive derivative financial instruments that pertain to beneficial interests that are or contain a derivative financial instrument. In general, these changes will reduce the operational complexity associated with bifurcating embedded derivatives, and increase the number of beneficial interests in securitization transactions, including interest-only strips and principal-only strips, required to be accounted for in accordance with SFAS No. 133. We adopted SFAS No. 155 in the first quarter of 2007 and the adoption of SFAS No. 155 did not have a material effect on our consolidated financial statements.

In September 2006, the FASB issued Interpretation No. 48,Accounting for Uncertainty in Income Taxes—an interpretation of FASB Statement No. 109 , or FIN 48. FIN 48 clarifies the accounting for uncertainty in income taxes recognized in an enterprise’s financial statements in accordance with FASB Statement No. 109,Accounting for Income Taxes. FIN 48 prescribes a recognition threshold and measurement attribute for the financial statement recognition and measurement of a tax position taken or expected to be taken in a tax return. We adopted FIN 48 in the first quarter of 2007 and the adoption of FIN 48 did not have an effect on our consolidated financial statements as we do not maintain any uncertain tax contingencies.

In September 2006, the FASB issued SFAS No. 157,Fair Value Measurements, or SFAS 157. SFAS 157 defines fair value, establishes a framework for measuring fair value in GAAP, and requires enhanced disclosures about fair value measurements. SFAS 157 applies when other accounting pronouncements require or permit fair value measurements; it does not require new fair value measurements. SFAS 157 is effective for financial statements issued for fiscal years beginning after November 15, 2007, and interim periods within those years. Management is currently evaluating the impact that this statement may have on our financial statements.

In February 2007, the FASB issued SFAS No. 159,The Fair Value Option for Financial Assets and Financial Liabilities. This statement provides entities with an irrevocable option to report most financial assets and liabilities at fair value, with subsequent changes in fair value reported in earnings. The election can be applied on an instrument-by-instrument basis. The statement establishes presentation and measurement attributes for similar types of assets and liabilities. The statement is effective for fiscal years beginning after November 15, 2007. Management is currently evaluating the impact that this statement may have on our financial statements.

9

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of March 31, 2007

(Unaudited and dollars in thousands, except share and per share amounts)

NOTE 3: INVESTMENTS IN SECURITIES

The following table summarizes our investments in available-for-sale securities as of March 31, 2007:

| | | | | | | | | | | | | | | | | | |

Investment Description | | Amortized Cost | | Gross Unrealized Gains | | Gross Unrealized

Losses | | | Estimated Fair Value | | Weighted

Average

Coupon | | | Weighted

Average

Years to

Maturity |

TruPS and subordinated debentures | | $ | 4,083,942 | | $ | 1,167 | | $ | (28,510 | ) | | $ | 4,056,599 | | 7.9 | % | | 28.0 |

Other securities | | | 693,383 | | | 198 | | | (6,432 | ) | | | 687,149 | | 6.1 | % | | 28.4 |

| | | | | | | | | | | | | | | | | | |

Total available-for-sale securities | | $ | 4,777,325 | | $ | 1,365 | | $ | (34,942 | ) | | $ | 4,743,748 | | 7.6 | % | | 28.1 |

| | | | | | | | | | | | | | | | | | |

TruPS included above as available-for-sale securities include (a) investments in TruPS issued by VIEs of which we are not the primary beneficiary and which we do not consolidate and (b) transfers of investments in TruPS securities to us that were accounted for as a sale pursuant to SFAS No. 140. Subordinated debentures included above represent the primary assets of VIEs that we consolidate pursuant to FIN 46R. Management believes that none of these securities are other than temporarily impaired at March 31, 2007.

The following table summarizes our investments in security-related receivables, as of March 31, 2007:

| | | | | | | | | | | |

Investment Description | | Amortized Cost | | Weighted

Average

Coupon | | | Weighted

Average Years to

Maturity | | Estimated Fair Value |

TruPS and subordinated debenture receivables | | $ | 770,876 | | 8.0 | % | | 25.4 | | $ | 784,991 |

Unsecured REIT note receivables | | | 393,766 | | 5.6 | % | | 10.1 | | | 390,584 |

CMBS receivables(1) | | | 214,201 | | 5.6 | % | | 35.5 | | | 208,898 |

| | | | | | | | | | | |

Total | | $ | 1,378,843 | | 6.9 | % | | 22.6 | | $ | 1,384,473 |

| | | | | | | | | | | |

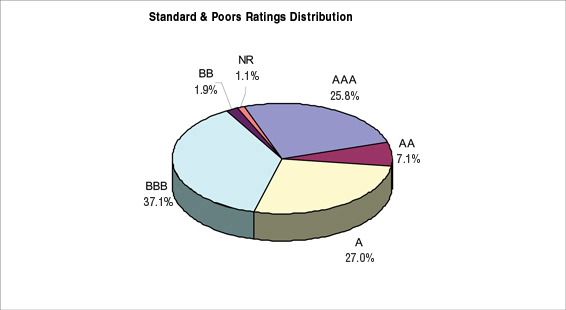

| (1) | Commercial mortgage-backed securities, or CMBS, receivables include securities with a fair value totaling $180,237 that are rated “BBB+” and “BBB-” by Standard & Poor’s and securities with a fair value totaling $28,661 that are rated between “AA” and “A-” by Standard & Poor’s. |

Our investments in security-related receivables represent securities owned by CDO entities that we account for as financings under SFAS No. 140.

The unrealized losses on our securities are primarily the result of market interest rate factors rather than credit impairment, and we believe that the carrying values are fully realizable over the securities’ expected holding period.

Some of our investments in securities collateralize debt issued through CDO entities. Our TruPS CDO entities are static pools and prohibit, in most cases, the sale of such securities until the mandatory auction call period, typically 10 years from the CDO entity’s inception. At and subsequent to the mandatory auction call date, remaining securities will be offered in the general market and the proceeds

10

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of March 31, 2007

(Unaudited and dollars in thousands, except share and per share amounts)

from sales of such securities will be used to repay outstanding indebtedness and liquidate the CDO entity. The assets of our consolidated CDOs collateralize the debt of such entities and are not available to our creditors. As of March 31, 2007, CDO notes payable related to investment in securities were collateralized by $4,251,400 of principal amount of TruPS and subordinated debentures and $609,013 of principal amount of unsecured REIT note receivables and CMBS receivables. Some of these investments were eliminated upon the consolidation of various VIEs that we consolidate and the corresponding subordinated debentures of the VIEs are included as assets in our consolidated balance sheet.

11

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of March 31, 2007

(Unaudited and dollars in thousands, except share and per share amounts)

NOTE 4: INVESTMENTS IN LOANS

Our investments in mortgages and loans are accounted for at amortized cost.

(a) Investments in residential mortgages and mortgage- related receivables:

The following tables summarize our investments in residential mortgages and mortgage-related receivables as of March 31, 2007:

| | | | | | | | | | | | | | | | | |

| | | Unpaid

Principal

Balance | | Unamortized

(Discount) | | | Carrying

Amount | | Number of Loans

and Mortgage-

Related

Receivables | | Average

Interest

Rate | | | Average

Contractual

Maturity date |

3/1 Adjustable rate | | $ | 136,215 | | $ | (2,071 | ) | | $ | 134,144 | | 345 | | 5.6 | % | | August 2035 |

5/1 Adjustable rate | | | 3,725,239 | | | (20,010 | ) | | | 3,705,229 | | 7,604 | | 5.6 | % | | September 2035 |

7/1 Adjustable rate | | | 594,210 | | | (4,819 | ) | | | 589,391 | | 1,295 | | 5.7 | % | | July 2035 |

10/1 Adjustable rate | | | 67,723 | | | (691 | ) | | | 67,032 | | 75 | | 5.7 | % | | June 2035 |

| | | | | | | | | | | | | | | | | |

Total | | $ | 4,523,387 | | $ | (27,591 | ) | | $ | 4,495,796 | | 9,319 | | 5.6 | % | | |

| | | | | | | | | | | | | | | | | |

As of March 31, 2007, approximately 44% of our residential mortgage loans were in the state of California.

As of March 31, 2007, $3,825,177 of our residential mortgages and mortgage-related receivables were pledged as collateral with mortgage securitizations. These mortgage securitizations have issued mortgage backed securities with a principal balance outstanding of $3,610,231.

(b) Investments in commercial mortgages, mezzanine loans, and other loans:

The following tables summarize our investments in commercial mortgages, mezzanine loans and other loans as of March 31, 2007:

| | | | | | | | | | | | | | | | | | | |

| | | Unpaid Principal Balance | | | Unamortized (Discounts) Premiums | | | Carrying Amount | | | Number of Loans | | Weighted Average Interest Rate | | | Range of Maturity Dates |

Commercial mortgages | | $ | 1,179,677 | | | $ | — | | | $ | 1,179,677 | | | 80 | | 8.2 | % | | Apr. 2007 to

Nov. 2015 |

Mezzanine loans | | | 532,322 | | | | (3,386 | ) | | | 528,936 | | | 163 | | 10.7 | % | | Apr. 2007 to

Aug. 2021 |

Other loans | | | 168,614 | | | | 1,316 | | | | 169,930 | | | 9 | | 7.5 | % | | May 2010

to Oct. 2016 |

| | | | | | | | | | | | | | | | | | | |

Total | | | 1,880,613 | | | | (2,070 | ) | | | 1,878,543 | | | 252 | | 8.9 | % | | |

| | | | | | | | | | | | | | | | | | | |

Unearned fees | | | (13,816 | ) | | | — | | | | (13,816 | ) | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

Total | | $ | 1,866,797 | | | $ | (2,070 | ) | | $ | 1,864,727 | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

(c) Allowance for losses:

We maintain an allowance for losses on our investments in residential mortgages and mortgage-related receivables, commercial mortgages, mezzanine loans and other real estate related assets. Specific allowances for losses are established for impaired loans based on a comparison of the recorded carrying value of the loan to either the present value of the loan’s expected cash flow, the loan’s estimated market price or the estimated fair value of the underlying collateral. The allowance is increased by charges to

12

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of March 31, 2007

(Unaudited and dollars in thousands, except share and per share amounts)

operations and decreased by charge-offs (net of recoveries). Management’s periodic evaluation of the adequacy of the allowance is based upon expected and inherent risks in the portfolio, historical trends in adjustable rate residential mortgages (if applicable), the estimated value of underlying collateral, and current and expected future economic conditions. As of March 31, 2007, our allowance for losses was $8,716, net of charge-offs of $338 during the three months ended March 31, 2007.

NOTE 5: INDEBTEDNESS

We maintain various forms of short-term and long-term financing arrangements. Generally, these financing agreements are collateralized by assets within CDOs or mortgage securitizations. The following table summarizes our indebtedness as of March 31, 2007:

| | | | | | | | | | | | | | | | |

Description | | Principal | | Unamortized

Premium

(Discount) | | | Carrying

Amount | | Interest Rate

Terms | | Current

Weighted-

Average

Interest Rate | | Contractual

Maturity |

Repurchase agreements and other indebtedness | | $ | 1,983,123 | | $ | — | | | $ | 1,983,123 | | 5.4% to

7.7% | | 5.9% | | Apr. 2007

to 2037 (1) |

Mortgage-backed securities issued(2) | | | 3,610,231 | | | (41,342 | ) | | | 3,568,889 | | 4.6% to 5.5%(3) | | 5.0% | | 2035 |

Trust preferred obligations | | | 592,013 | | | — | | | | 592,013 | | 6.8% to 9.1% | | 7.3% | | 2036 |

CDO notes payable(2) | | | 5,493,107 | | | (119,660 | ) | | | 5,373,447 | | 4.7% to 10.4% | | 6.2% | | 2035 to 2046 |

| | | | | | | | | | | | | | | | |

Total indebtedness | | $ | 11,678,474 | | $ | (161,002 | ) | | $ | 11,517,472 | | | | | | |

| | | | | | | | | | | | | | | | |

| (1) | We intend to re-negotiate and extend our repurchase agreements as they mature. |

| (2) | Excludes mortgage-backed securities and CDO notes payable purchased by us which are eliminated in consolidation. |

| (3) | Rates generally follow the terms of the underlying mortgages, which are fixed for a period of time and variable thereafter. |

Financing arrangements we entered into during the three months ended March 31, 2007 were as follows:

| | (a) | Repurchase agreements and other indebtedness: |

On February 12, 2007, we formed Taberna Funding Capital Trust I which issued $25,000 of trust preferred securities to investors and $100 of common securities to us. The combined proceeds were used by Taberna Funding Capital Trust I to purchase $25,100 of junior subordinated notes issued by us. The junior subordinated notes are the sole assets of Taberna Capital Trust I and mature on April 30, 2037, but are callable on or after April 30, 2012. Interest on the junior subordinated notes is payable quarterly at a fixed rate of 7.69% through April 2012 and thereafter at a floating rate equal to three-month LIBOR plus 2.50%.

On February 15, 2007, we entered into a repurchase agreement with an investment bank to provide up to $750,000 of financing to accumulate commercial loan investments in commercial mortgages and mezzanine loans on a short-term basis pending a CDO issuance. The agreement terminates on February 14, 2008 and bears interest at various rates over LIBOR ranging from 0.30% to 1.35%, depending on the types and ratings of assets financed. As of March 31, 2007, this repurchase agreement had $307,677 outstanding collateralized by commercial mortgage and mezzanine loans with a principal amount of $354,354.

On March 29, 2007, we closed Taberna Preferred Funding VIII, Ltd., a $772,000 CDO transaction that provides financing for investments consisting of TruPS issued by REITs and real estate operating companies, senior and subordinated notes issued by real estate entities, commercial mortgage-backed securities, other real estate interests, senior loans and CDOs issued by special purpose issuers that own a portfolio of commercial real estate loans. The investments that are owned by Taberna Preferred Funding VIII are pledged as collateral to secure its debt and, as a result, are not available to us, our creditors or our shareholders. Taberna Preferred Funding VIII issued a total of $471,000 of notes at par to investors. In addition, we retained $111,000 of the senior notes, $50,000 of the junior notes and $60,000 of the preference shares. The notes issued to investors bear interest at rates ranging from LIBOR plus 0.34% to

13

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of March 31, 2007

(Unaudited and dollars in thousands, except share and per share amounts)

LIBOR plus 4.90%. All of the notes mature in 2037, although Taberna Preferred Funding VIII may call the notes at par at any time after May 2017. The senior notes retained by us bear interest at rates ranging from LIBOR plus 0.34% to LIBOR plus 0.53% and the junior notes retained by us bear interest at rates ranging from LIBOR plus 2.85% to LIBOR plus 4.90%. We financed our investment in the senior notes through $103,710 of borrowings under our existing repurchase agreements bearing interest at rates ranging from LIBOR plus 0.05% to LIBOR plus 0.10%.

The assets of our consolidated CDOs collateralize the debt of such entities and are not available to our creditors. As of March 31, 2007, the CDO notes payable are collateralized by $4,251,400 of principal amount of TruPS and subordinated debentures, $609,013 of principal amount of unsecured REIT note receivables and CMBS receivables and $1,098,683 in principal amount of commercial mortgages, mezzanine loans and other loans. A portion of the TruPS that collateralize CDO notes payable are eliminated upon the consolidation of various Trust VIE entities that we consolidate. The corresponding subordinated debentures of the Trust VIE entities are included as investments in securities in our consolidated balance sheet.

NOTE 6: DERIVATIVE FINANCIAL INSTRUMENTS

Cash Flow Hedges

We have entered into various interest rate swap contracts to hedge interest rate exposure on CDO notes payable and repurchase agreements.

We designate interest rate hedge agreements at inception and determine whether or not the interest rate hedge agreement is highly effective in offsetting interest rate fluctuations associated with the identified indebtedness. At designation, certain of these interest rate swaps had a fair value not equal to zero. However, we concluded, at designation, that these hedging arrangements were highly effective during their term using regression analysis and determined that the hypothetical derivative method would be used in measuring any ineffectiveness. At each reporting period, we update our regression analysis and, as of March 31, 2007, we concluded that these hedging arrangements were highly effective during their remaining term and used the hypothetical derivative method in measuring the ineffective portions of these hedging arrangements.

14

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of March 31, 2007

(Unaudited and dollars in thousands, except share and per share amounts)

The interest rate hedge agreements are summarized as of March 31, 2007:

| | | | | | | | | | | | | | | | | | | | | |

Hedge Product | | Hedged Item | | Aggregate

Notional | | Strike | | Maturity | | Fair Value

as of

March 31,

2007 | | | Amounts

Reclassified

to Earnings

for

Effective

Hedges—

Gains

(Losses) | | | Amounts

Reclassified

to Earnings

for

Ineffective

Hedges—

Gains

(Losses) | |

Interest rate swaps | | CDO notes payable | | $ | 653,750 | | 3.9% to 5.2% | | Aug. 2010 to Nov. 2015 | | $ | 11,218 | | | $ | (718 | ) | | $ | 519 | |

Interest rate swaps | | CDO notes payable | | | 450,500 | | 4.6% to 5.6% | | Nov. 2010 to Nov. 2015 | | | 3,446 | | | | (151 | ) | | | 27 | |

Interest rate and basis swaps | | CDO notes payable | | | 396,625 | | 4.9% to 5.6% | | February 2016 | | | (4,364 | ) | | | 42 | | | | (143 | ) |

Interest rate swaps | | CDO notes payable | | | 300,000 | | 5.1% to 5.3% | | Feb. 2011 to Feb. 2016 | | | (2,323 | ) | | | 76 | | | | (28 | ) |

Interest rate swaps | | CDO notes payable | | | 502,860 | | 5.1% to 5.9% | | Oct. 2011 to Oct. 2016 | | | (14,905 | ) | | | 598 | | | | (11 | ) |

Interest rate swaps | | CDO notes payable | | | 480,000 | | 5.4% to 5.9% | | July 2016 to Aug. 2016 | | | (9,761 | ) | | | 415 | | | | (141 | ) |

Interest rate cap | | CDO notes payable | | | 15,000 | | 8.5% | | August 2031 | | | 191 | | | | — | | | | (47 | ) |

Interest rate swaps | | CDO notes payable | | | 346,000 | | 5.0% | | August 2017 | | | 2,323 | | | | 59 | | | | — | |

Interest rate swaps | | CDO notes payable | | | 768,722 | | 4.8% to 5.3% | | Jan. 2010 to June 2016 | | | (6,249 | ) | | | 34 | | | | — | |

Interest rate swap | | Repurchase agreements | | | 733,570 | | 5.3% | | July 2011 | | | (8,862 | ) | | | 877 | | | | (146 | ) |

Interest rate swaps | | Repurchase agreements | | | 94,478 | | 4.6% to 4.9% | | Oct. 2010 to Dec. 2012 | | | 584 | | | | (47 | ) | | | 44 | |

Interest rate swaps | | Other indebtedness | | | 121,833 | | 5.0% | | Nov. 2011 to Dec. 2011 | | | (642 | ) | | | 25 | | | | — | |

Interest rate swaps | | Other indebtedness | | | 31,450 | | 5.2% to 5.3% | | Feb. 2009 to Feb. 2017 | | | (332 | ) | | | (3 | ) | | | (36 | ) |

Currency option | | EUR-USD exchange rate | | | 8,633 | | 1.2633

EUR-USD | | May 2007 to May 2009 | | | 50 | | | | — | | | | 50 | |

| | | | | | | | | | | | | | | | | | | | | |

Total Portfolio/ Weighted Average | | | | $ | 4,903,421 | | | | | | $ | (29,626 | ) | | $ | 1,207 | | | $ | 88 | |

| | | | | | | | | | | | | | | | | | | | | |

Amounts reclassified to earnings associated with effective cash flow hedges are reported in investment interest expense and the fair value of these hedge agreements is included in other assets and liabilities.

Free-Standing Derivatives

We maintain arrangements with various investment banks regarding CDO securitizations and warehouse facilities. Prior to the completion of a CDO securitization, investments are acquired by the warehouse providers in accordance with the warehouse facilities. Pursuant to the terms of the warehouse agreements, we receive the difference between the interest earned on the investments under the warehouse facilities and the interest charged by the warehouse facilities from the dates on which the respective securities are acquired. Under the warehouse agreements, we are required to deposit cash collateral with the warehouse provider and as a result, we bear the first dollar risk of loss, and in some cases share the first dollar risk of loss, up to our warehouse deposit, if (i) an investment funded through the warehouse facility becomes impaired or (ii) a CDO is not completed by the end of the warehouse period, and in either case, if the warehouse facility is required to liquidate the securities at a loss. Upon the completion of a CDO securitization, the cash collateral held by the warehouse provider is returned to us. The terms of the warehouse facilities are generally at least nine months. As of March 31, 2007, we had approximately $56,510 of cash collateral held by warehouse providers pursuant to warehouse facilities. These arrangements are deemed to be derivative financial instruments and are recorded at fair value each accounting period with the change in fair value recorded in earnings.

A summary of these arrangements is as follows:

| | | | | | | | | | | |

Warehouse Facility | | Warehouse

Availability | | Funding as of

March 31,

2007 | | Remaining

Availability | | Maturity |

Merrill Lynch International | | $ | 700,053 | | $ | 400,419 | | $ | 299,634 | | June 2007 to February 2008 |

Bear, Stearns & Co. Inc. | | | 700,000 | | | 395,188 | | | 304,812 | | September 2007 to March 2008 |

| | | | | | | | | | | |

Total | | $ | 1,400,053 | | $ | 795,607 | | $ | 604,446 | | |

| | | | | | | | | | | |

15

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of March 31, 2007

(Unaudited and dollars in thousands, except share and per share amounts)

The financing costs of these warehouse facilities are based on one-month LIBOR plus 50 basis points.

NOTE 7: SHAREHOLDERS’ EQUITY

On January 23, 2007, our board of trustees awarded 408,517 phantom units, valued at $14,997 using our closing stock price of $36.71, to various employees and trustees. The awards generally vest over four year periods.

On January 23, 2007, our board of trustees declared a first quarter 2007 cash dividend of $0.484375 per share on our 7.75% Series A Cumulative Redeemable Preferred Shares and $0.5234375 per share on our 8.375% Series B Cumulative Redeemable Preferred Shares. The dividends were paid on April 2, 2007 to holders of record on March 1, 2007 and totaled $2,519.

On January 24, 2007, 6,010 of our phantom unit awards were redeemed for our common shares. These phantom units were fully vested at the time of redemption.

On January 24, 2007, we issued 11,500,000 common shares in a public offering at an offering price of $34.00 per share. After deducting offering costs, including the underwriter’s discount, and expenses of approximately $24,070, we received approximately $366,894 of net proceeds.

On March 15, 2007, our board of trustees declared a quarterly distribution of $0.80 per common share totaling $50,938 that was paid on April 13, 2007 to shareholders of record as of March 29, 2007.

16

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of March 31, 2007

(Unaudited and dollars in thousands, except share and per share amounts)

NOTE 8: EARNINGS PER SHARE

The following table presents a reconciliation of basic and diluted earnings per share for the three month periods ended March 31, 2007 and 2006:

| | | | | | | | |

| | | For the three month periods ended March 31 | |

| | | 2007 | | | 2006 | |

Income from continuing operations | | $ | 22,711 | | | $ | 19,628 | |

Income allocated to preferred shares | | | (2,519 | ) | | | (2,519 | ) |

| | | | | | | | |

Income from continuing operations available to common shares | | | 20,192 | | | | 17,109 | |

Income from discontinued operations | | | 156 | | | | 942 | |

| | | | | | | | |

Net income available to common shares | | $ | 20,348 | | | $ | 18,051 | |

| | | | | | | | |

Weighted-average shares outstanding—Basic | | | 60,143,844 | | | | 27,900,276 | |

Dilutive securities under the treasury stock method | | | 472,877 | | | | 221,459 | |

| | | | | | | | |

Weighted-average shares outstanding—Diluted | | | 60,616,721 | | | | 28,121,735 | |

| | | | | | | | |

Earnings per share—Basic: | | | | | | | | |

Continuing operations | | $ | 0.34 | | | $ | 0.62 | |

Discontinued operations | | | — | | | | 0.03 | |

| | | | | | | | |

Total earnings per share—Basic | | $ | 0.34 | | | $ | 0.65 | |

| | | | | | | | |

Earnings per share—Diluted: | | | | | | | | |

Continuing operations | | $ | 0.34 | | | $ | 0.61 | |

Discontinued operations | | | — | | | | 0.03 | |

| | | | | | | | |

Total earnings per share—Diluted | | $ | 0.34 | | | $ | 0.64 | |

| | | | | | | | |

NOTE 9: RELATED PARTY TRANSACTIONS

In the ordinary course of our business operations, we have ongoing relationships and have engaged in transactions with several related entities described below. All of these relationships and transactions were approved or ratified by a majority of our independent board of trustees as being on terms comparable to those available on an arm’s-length basis from an unaffiliated third party or otherwise not creating a conflict of interest.

Our Chief Executive Officer, Daniel G. Cohen, holds controlling positions in various companies with which the Company conducts business. Daniel G. Cohen is the majority member of Cohen Brothers LLC d/b/a Cohen & Company, or Cohen & Company, a registered broker-dealer. Each transaction with Cohen & Company is described below:

a).Shared Services—we share office space and related resources with Cohen & Company. For services relating to structuring and managing our investments in CMBS and RMBS, we pay an annual fee ranging from 2 to 20 basis points on the amount of the investments, based on the rating of the security. For investments in residential whole loans, we pay an annual fee of 1.5 basis points on the amount of the investments. In respect of other administrative services, we pay an amount equal to the cost of providing those services plus 10% of such cost. During the three-month period ended March 31, 2007, we incurred total shared service expenses of approximately $300, which has been included in general and administrative expense in the accompanying statement of income.

b).OfficeLease—We maintain a separate five-year sub-lease agreement for shared office space and facilities commencing April 1, 2006 and expiring March 31, 2011. Rent expense during the three-month period ended March 31, 2007 relating to this lease was $17 and has been included in general and administrative expense in the accompanying statement of income. Future minimum lease payments due over the remaining term of the lease is approximately $290.

17

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of March 31, 2007

(Unaudited and dollars in thousands, except share and per share amounts)

c).Origination Fees—during the three-month period ended March 31, 2007, Cohen & Company provided origination services for our investments and placement services for certain debt and equity securities issued by our CDO securitizations. For these services, Cohen & Company received approximately $390 in origination fees and $1,500 in placement fees. In February 2007, we engaged an affiliate of Cohen & Company for the placement of debt securities to be issued by a future CDO transaction. Fees to be paid are 50 basis points of the total expected final collateral balance of the CDO.

d).Non-Competition Agreement—As part of the spin-off of Taberna from Cohen & Company, Taberna and Cohen & Company entered into a three-year non-competition agreement ending in April 2008. As part of this agreement, Cohen & Company agreed not to engage in purchasing from, or acting as a placement agent for, issuers of TruPS or other preferred equity securities of real estate investment trusts and other real estate operating companies. Cohen & Company agreed to refrain from acting as asset manager for any such securities. As part of our acquisition of Taberna, we valued this non-competition agreement as an amortizing intangible asset. As of March 31, 2007, the balance of the intangible asset, net of accumulated amortization, was $11,706.

e).Strategos Capital Management—Strategos Capital Management, or Strategos, is an affiliate of Cohen & Company. In October 2006, Taberna engaged Strategos to create and manage a $1.0 billion high-grade asset backed CDO. For its services, Strategos, upon completion of the CDO, will receive an upfront structuring fee of 15 basis points, or approximately $1,500 and ongoing management fees of 10 basis points, or $1,000 per year.

The Bancorp, Inc.—Betsy Z. Cohen, our Chairman, is the Chairman of the Board and Chief Executive Officer of The Bancorp Bank (“Bancorp”), a commercial bank. Daniel G. Cohen, our Chief Executive Officer and Trustee is the Vice-Chairman of the Board of Bancorp. We maintain checking and demand deposit accounts at Bancorp. As of March 31, 2007 and December 31, 2006, we had $88,819 and $117,123, respectively, on deposit. During the three-month periods ended March 31, 2007 and 2006, we received $267 and $311, respectively, of interest income from Bancorp. During the three-month periods ended March 31, 2007 and 2006, we paid fees of $20 and $15, respectively, to Bancorp for information system technical support services. We sublease a portion of our downtown Philadelphia office space from Bancorp at an annual rental expense based upon the amount of square footage occupied. The sub-lease expires in August 2010 and there are two five-year renewal options. Rent paid to Bancorp Inc. was approximately $124 and $84 for the three-month periods ended March 31, 2007 and 2006, respectively.

We have a $3,369 first mortgage loan secured by Pennsview Apartments that has junior lien against it that is held by an entity controlled by Daniel Cohen. Our loan bears interest at a fixed rate of 8%, matures on March 29, 2008 and is paying in accordance with its terms.

Eton Park Fund, L.P. and its affiliates—Eton Park Fund, L.P., or Eton Park, owns approximately 6.4% of our common shares based on the most recent Form 13-G they filed with the SEC. In connection with the Taberna Euro CDO I we sponsored, we paid Eton Park a standby equity commitment fee of $1,000. In exchange for this fee, they agreed to purchase up to €5,500 of the Class F subordinated notes issued by Taberna Euro CDO I.

Mercury Real Estate Advisors LLC—Mercury Real Estate Advisors LLC, or Mercury, and its affiliates own approximately 6.9% of our common shares based on the most recent form 13-G they filed with the SEC. In March 2007, we purchased approximately $9,000 in par amount of preference shares issued by various CDOs sponsored by Taberna from Mercury for a purchase price of approximately $8,685.

Brandywine Construction & Management, Inc., or Brandywine is an affiliate of the spouse of Betsy Z. Cohen, our Chairman, and father of Daniel G. Cohen, our Chief Executive Officer. Brandywine provided real estate management services to three and six properties underlying our real estate interests as of March 31, 2007 and 2006, respectively. Management fees of $37 and $164 were paid to Brandywine for the three-month periods ended March 31, 2007 and 2006, respectively, relating to those interests.

18

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of March 31, 2007

(Unaudited and dollars in thousands, except share and per share amounts)

NOTE 10: DISCONTINUED OPERATIONS

The following table summarizes the single asset held for sale and the liabilities related to the asset held for sale as of March 31, 2007:

| | | |

Investment in real estate, net of accumulated depreciation | | $ | 12,720 |

Prepaids and other assets | | | 534 |

| | | |

Total assets held for sale | | | 13,254 |

| | | |

Accounts payable and accrued expenses | | $ | 250 |

| | | |

Total liabilities related to assets held for sale | | $ | 250 |

| | | |

The following table summarizes revenue and expense information for the four properties sold since January 1, 2006 and the one property held for sale as of March 31, 2007:

| | | | | | |

| | | For the three month period ended March 31 |

| | | 2007 | | 2006 |

Rental income | | $ | 483 | | $ | 4,444 |

Expenses: | | | | | | |

Real estate operating expenses | | | 276 | | | 3,271 |

Depreciation | | | 51 | | | 231 |

| | | | | | |

Total expenses | | | 327 | | | 3,502 |

| | | | | | |

Income from discontinued operations | | $ | 156 | | $ | 942 |

| | | | | | |

Discontinued operations have not been segregated in the consolidated statements of cash flows. Therefore, amounts for certain captions will not agree with respective data in the consolidated statements of operations.

NOTE 11: SUBSEQUENT EVENTS

On April 16, 2007, we terminated our $335,000 secured line of credit led by KeyBanc Capital Markets, as syndication agent. As of March 31, 2007, we had $20,000 outstanding under this facility and all amounts were repaid prior to April 16, 2007. We expensed $2,985 of deferred financing costs associated with the line of credit upon termination.

On April 18, 2007, we issued and sold in a private offering to qualified institutional buyers, $425,000 aggregate principal amount of 6.875% convertible senior notes due 2027. After deducting the initial purchaser’s discount and the estimated offering expenses, we received approximately $414,250 of net proceeds. Interest on the notes is paid semi-annually and the notes mature on April 15, 2027. In April 2007, our board of trustees authorized the repurchase of approximately $106,250 of our common shares. We used a portion of the net proceeds from the offering to repurchase 2,717,600 of our common shares at a price of $27.34 per share (the closing price on April 12, 2007, the date we entered into the purchase agreement relating to the offering) for an aggregate purchase price, including commission costs, of $74,381.

Prior to April 20, 2012, the notes will not be redeemable at RAIT’s option, except to preserve RAIT’s status as a REIT. On or after April 20, 2012, RAIT may redeem all or a portion of the notes at a

19

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of March 31, 2007

(Unaudited and dollars in thousands, except share and per share amounts)

redemption price equal to the principal amount plus accrued and unpaid interest (including additional interest), if any. Note holders may require RAIT to repurchase all or a portion of the notes at a purchase price equal to the principal amount plus accrued and unpaid interest (including additional interest), if any, on the notes on April 15, 2012, April 15, 2017, and April 15, 2022, or upon the occurrence of certain change in control transactions prior to April 20, 2012.

Prior to April 15, 2026, upon the occurrence of specified events, the notes will be convertible at the option of the holder at an initial conversion rate of 28.6874 shares per $1,000 principal amount of notes. The initial conversion price of $34.86 represents a 27.5% premium to the per share closing price of $27.34 on the date the offering was priced. Upon conversion of notes by a holder, the holder will receive cash up to the principal amount of such notes and, with respect to the remainder, if any, of the conversion value in excess of such principal amount, at the option of RAIT in cash or RAIT’s common shares. The initial conversion rate is subject to adjustment in certain circumstances.

20

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

Board of Trustees and Shareholders RAIT Financial Trust

We have reviewed the accompanying consolidated balance sheet of RAIT Financial Trust and subsidiaries as of March 31, 2007 and the related consolidated statements of income, comprehensive income and cash flows for the three-month periods ended March 31, 2007 and 2006. These interim financial statements are the responsibility of the Company’s management.

We conducted our review in accordance with standards of the Public Company Accounting Oversight Board (United States). A review of interim financial information consists principally of applying analytical procedures and making inquiries of persons responsible for financial and accounting matters. It is substantially less in scope than an audit conducted in accordance with generally accepted auditing standards, the objective of which is the expression of an opinion regarding the financial statements taken as a whole. Accordingly, we do not express such an opinion.

Based on our review, we are not aware of any material modifications that should be made to the accompanying financial statements for them to be in conformity with accounting principles generally accepted in the United States of America.

We have previously audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States), the consolidated balance sheet as of December 31, 2006, and the related consolidated statements of income, comprehensive income, changes in shareholders’ equity and cash flows for the year then ended (not presented herein); and in our report dated February 28, 2007 (which contains an explanatory paragraph relating to the initial adoption of financial accounting Board Statement No. 123RStock Based Compensation as discussed in note 11 to the consolidated financial statements) we expressed an unqualified opinion on those consolidated financial statements. In our opinion, the information set forth in the accompanying consolidated balance sheet as of December 31, 2006 is fairly stated, in all material respects, in relation to the consolidated balance sheet from which it has been derived.

/s/ Grant Thornton LLP

Philadelphia, Pennsylvania

May 3, 2007

21

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

Forward-Looking Statements

In addition to historical information, this discussion and analysis contains forward-looking statements. These statements can be identified by the use of forward-looking terminology including “may,” “believe,” “will,” “expect,” “anticipate,” “estimate,” “continue” or similar words. These forward-looking statements are subject to risks and uncertainties, as more particularly set forth in our filings with the Securities and Exchange Commission, including those described in the “Risk Factors” section of our Annual Report on Form 10-K for the year ended December 31, 2006, that could cause actual results to differ materially from those projected in the forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements, which reflect management’s analysis only as of the date hereof. We undertake no obligation to publicly revise or update these forward-looking statements to reflect events or circumstances that arise after the date of this report, except as may be required by applicable law.

Overview

We are a diversified real estate finance company that provides a comprehensive set of financing options to the real estate industry. We originate and invest in real estate-related assets that are underwritten through an integrated investment process. We conduct our business through our subsidiaries, RAIT Partnership and Taberna, as well as through their respective subsidiaries. RAIT and Taberna are self-managed and self-advised Maryland REITs. Our objective is to provide our shareholders with total returns over time, including quarterly distributions and capital appreciation, while seeking to manage the risks associated with our investment strategy.

In the three months ended March 31, 2007, we generated income for distribution to our shareholders primarily from a combination of the interest and dividend income from our investment portfolio and the fees from originating, structuring and managing the assets collateralizing CDOs we sponsored. We provide financing in the form of TruPS and subordinated debentures to real estate and real estate finance companies in the United States and Europe and commercial mortgages and mezzanine loans to real estate operators throughout the United States.

We continued to increase our investment in our targeted asset classes during the three months ended March 31, 2007. Our net increase in investments in this period was $1.5 billion.

We focus on maximizing the net spread we can generate on our match-funded portfolios financed primarily by CDOs. The difference, or net spread, between the yield on our investment portfolio and the cost to finance our investment portfolio generates our net investment income. In the three months ended March 31, 2007, our net investment income was $43.0 million. We also generated substantial fees in the three months ended March 31, 2007, primarily through our taxable REIT subsidiaries.

Commercial mortgages, mezzanine loans and TruPS and subordinated debentures are our primary asset classes. We expect these asset classes to be the primary sources for growth in returns generated by our investment portfolio. In the quarter ended March 31, 2007, we completed two CDOs – our eighth domestic CDO primarily collateralized by $750 million of TruPS and subordinated debentures from domestic real estate companies and our first European CDO collateralized primarily by approximately €600 million of subordinated debt to European real estate companies. We completed an equity offering in January 2007 and a convertible notes offering in April 2007 which we believe provide us additional liquidity to invest in our pipeline of opportunities and support our continued growth.

During the three months ended March 31, 2007, we developed certain financial and operating measures relating to our performance. Those measures are adjusted earnings, total fees generated and assets under management, or AUM. The following defines these measures and describes their relevence to our financial and operating performance: