Exhibit B.3(c): Management’s discussion and analysis excerpted from pages 1-86 of CIBC’s 2014 Annual Report

|

Management’s discussion and analysis |

Management’s discussion and analysis

Management’s discussion and analysis (MD&A) is provided to enable readers to assess CIBC’s financial condition and results of operations as at and for the year ended October 31, 2014, compared with prior years. The MD&A should be read in conjunction with the audited consolidated financial statements. Unless otherwise indicated, all financial information in this MD&A has been prepared in accordance with International Financial Reporting Standards (IFRS or GAAP) and all amounts are expressed in Canadian dollars. This MD&A is current as of December 3, 2014. Additional information relating to CIBC is available on SEDAR at www.sedar.com and on the U.S. Securities and Exchange Commission’s (SEC) website at www.sec.gov. No information on CIBC’s website (www.cibc.com) should be considered incorporated herein by reference. A glossary of terms used in the MD&A and the audited consolidated financial statements is provided on pages 168 to 172 of this Annual Report.

| | |

| 2 | | External reporting changes |

| 3 | | Overview |

| 3 | | Vision, mission and values |

| 3 | | CIBC’s strategy |

| 3 | | Performance against

objectives |

| 4 | | Economic and market environment |

| |

| 5 | | Financial performance overview |

| 5 | | Financial highlights |

| 6 | | 2014 Financial results |

| 6 | | Net interest income and margin |

| | |

| 7 | | Non-interest income |

| 7 | | Trading activities (TEB) |

| 8 | | Provision for credit losses |

| 8 | | Non-interest expenses |

| 8 | | Taxes |

| 9 | | Foreign exchange |

| 9 | | Significant events |

| 10 | | Fourth quarter review |

| 11 | | Quarterly trend analysis |

| 11 | | Review of 2013 financial performance |

| 12 | | Outlook for calendar year 2015 |

| |

| 13 | | Non-GAAP measures |

| | |

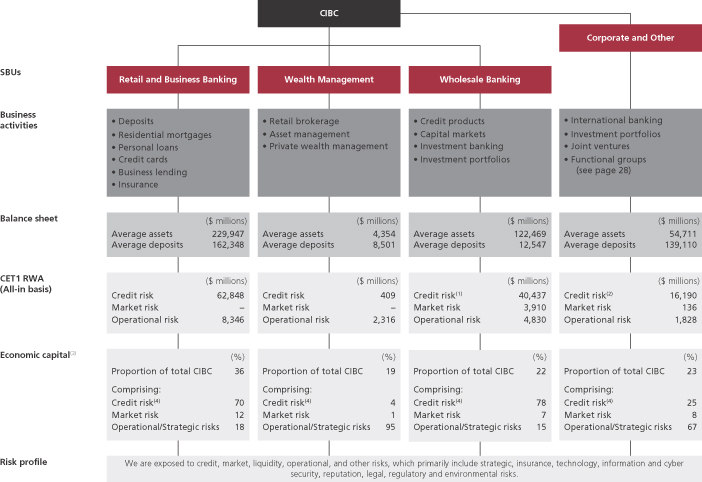

| 16 | | Strategic business units overview |

| 17 | | Retail and Business Banking |

| 20 | | Wealth Management |

| 23 | | Wholesale Banking |

| 28 | | Corporate and Other |

| |

| 29 | | Financial condition |

| 29 | | Review of consolidated balance sheet |

| 30 | | Capital resources |

| 38 | | Off-balance sheet arrangements |

| |

| 40 | | Management of risk |

| | |

| 73 | | Accounting and control matters |

| 73 | | Critical accounting policies and estimates |

| 77 | | Financial instruments |

| 77 | | Accounting developments |

| 77 | | Regulatory developments |

| 78 | | Related-party transactions |

| 78 | | Policy on the Scope of Services of the Shareholders’ Auditors |

| 78 | | Controls and procedures |

| |

| 79 | | Supplementary annual financial information |

A NOTE ABOUT FORWARD-LOOKING STATEMENTS: From time to time, we make written or oral forward-looking statements within the meaning of certain securities laws, including in this Annual Report, in other filings with Canadian securities regulators or the U.S. Securities and Exchange Commission and in other communications. All such statements are made pursuant to the “safe harbour” provisions of, and are intended to be forward-looking statements under, applicable Canadian and U.S. securities legislation, including the U.S. Private Securities Litigation Reform Act of 1995. These statements include, but are not limited to, statements made in the “Message from the President and Chief Executive Officer”, “Overview – Performance against objectives”, “Financial performance overview – Taxes”, “Financial performance overview – Significant events”, “Financial performance overview – Outlook for calendar year 2015”, “Strategic business units overview – Retail and Business Banking”, “Strategic business units overview – Wealth Management”, “Strategic business units overview – Wholesale Banking”, “Financial condition – Capital resources”, “Financial condition – Off-balance sheet arrangements”, “Management of risk – Risk overview”, “Management of risk – Top and emerging risks”, “Management of risk – Credit risk”, “Management of risk – Market risk”, “Management of risk – Liquidity risk”, “Accounting and control matters – Critical accounting policies and estimates”, “Accounting and control matters – Financial instruments” and “Accounting and control matters – Controls and procedures” sections of this report and other statements about our operations, business lines, financial condition, risk management, priorities, targets, ongoing objectives, strategies and outlook for calendar year 2015 and subsequent periods. Forward-looking statements are typically identified by the words “believe”, “expect”, “anticipate”, “intend”, “estimate”, “forecast”, “target”, “objective” and other similar expressions or future or conditional verbs such as “will”, “should”, “would” and “could”. By their nature, these statements require us to make assumptions, including the economic assumptions set out in the “Financial performance overview – Outlook for calendar year 2015” section of this report, and are subject to inherent risks and uncertainties that may be general or specific. A variety of factors, many of which are beyond our control, affect our operations, performance and results, and could cause actual results to differ materially from the expectations expressed in any of our forward-looking statements. These factors include: credit, market, liquidity, strategic, insurance, operational, reputation and legal, regulatory and environmental risk; the effectiveness and adequacy of our risk management and valuation models and processes; legislative or regulatory developments in the jurisdictions where we operate, including the Dodd-Frank Wall Street Reform and Consumer Protection Act and the regulations issued and to be issued thereunder, the U.S. Foreign Account Tax Compliance Act and regulatory reforms in the United Kingdom and Europe, the Basel Committee on Banking Supervision’s global standards for capital and liquidity reform, and those relating to the payments system in Canada; amendments to, and interpretations of, risk-based capital guidelines and reporting instructions, and interest rate and liquidity regulatory guidance; the resolution of legal and regulatory proceedings and related matters; the effect of changes to accounting standards, rules and interpretations; changes in our estimates of reserves and allowances; changes in tax laws; changes to our credit ratings; political conditions and developments; the possible effect on our business of international conflicts and the war on terror; natural disasters, public health emergencies, disruptions to public infrastructure and other catastrophic events; reliance on third parties to provide components of our business infrastructure; potential disruptions to our information technology systems and services, including the evolving risk of cyber attack; social media risk; losses incurred as a result of internal or external fraud; the accuracy and completeness of information provided to us concerning clients and counterparties; the failure of third parties to comply with their obligations to us and our affiliates; intensifying competition from established competitors and new entrants in the financial services industry including through internet and mobile banking; technological change; global capital market activity; changes in monetary and economic policy; currency value and interest rate fluctuations; general business and economic conditions worldwide, as well as in Canada, the U.S. and other countries where we have operations, including increasing Canadian household debt levels and the high U.S. fiscal deficit; our success in developing and introducing new products and services, expanding existing distribution channels, developing new distribution channels and realizing increased revenue from these channels; changes in client spending and saving habits; our ability to attract and retain key employees and executives; our ability to successfully execute our strategies and complete and integrate acquisitions and joint ventures; and our ability to anticipate and manage the risks associated with these factors. This list is not exhaustive of the factors that may affect any of our forward-looking statements. These and other factors should be considered carefully and readers should not place undue reliance on our forward-looking statements. We do not undertake to update any forward-looking statement that is contained in this report or in other communications except as required by law.

|

Management’s discussion and analysis |

External reporting changes

The following external reporting changes were made in 2014. Prior period amounts were restated accordingly.

Amendments to IAS 19 “Employee Benefits”

We adopted amendments to IAS 19 “Employee Benefits” commencing November 1, 2011, which require us to recognize: (i) actuarial gains and losses in Other comprehensive income (OCI) in the period in which they arise; (ii) interest income on plan assets in net income using the same rate as that used to discount the defined benefit obligation; and (iii) all past service costs (gains) in net income in the period in which they arise.

Adoption of IFRS 10 “Consolidated Financial Statements”

We adopted IFRS 10 “Consolidated Financial Statements” commencing November 1, 2012, which replaces IAS 27 “Consolidated and Separate Financial Statements” and Standard Interpretations Committee (SIC) – 12 “Consolidated – Special Purpose Entities”. The adoption of IFRS 10 required us to deconsolidate CIBC Capital Trust from the consolidated financial statements, which resulted in a replacement of Capital Trust securities issued by CIBC Capital Trust with Business and government deposits for the senior deposit notes issued by us to CIBC Capital Trust.

Sale of Aeroplan portfolio

On December 27, 2013, we sold approximately 50% of our Aerogold VISA portfolio, consisting primarily of credit card only customers, to The Toronto-Dominion Bank (TD). Accordingly, the revenue related to the sold credit card portfolio was moved from Personal banking to the Other line of business within Retail and Business Banking.

Allocation of Treasury activities

Treasury-related transfer pricing continues to be charged or credited to each line of business within our strategic business units (SBUs). We changed our approach to allocating the residual financial impact of Treasury activities. Certain fees are charged directly to the lines of business, and the residual net revenue is retained in Corporate and Other.

Income statement presentation

We reclassified certain amounts associated with our self-managed credit card portfolio from Non-interest expenses to Non-interest income. There was no impact on consolidated net income due to this reclassification.

|

Management’s discussion and analysis |

Overview

CIBC is a leading Canadian-based global financial institution with a market capitalization of $41 billion and a Basel III Common Equity Tier 1 (CET1) ratio of 10.3%. Through our three main businesses, Retail and Business Banking, Wealth Management, and Wholesale Banking, CIBC provides a full range of financial products and services to 11 million individual, small business, commercial, corporate and institutional clients in Canada and around the world. We have more than 44,000 employees dedicated to helping our clients achieve what matters to them; delivering consistent and sustainable earnings for our shareholders; and giving back to our communities.

Vision, mission and values

CIBC’s vision is to be the leader in client relationships.

Our mission is to fulfill the commitments we have made to each of our stakeholders:

| • | | Help our clients achieve what matters to them |

| • | | Create an environment where all employees can excel |

| • | | Make a real difference in our communities |

| • | | Generate strong total returns for our shareholders |

Our vision and mission are driven by an organizational culture based on core values of Trust, Teamwork and Accountability.

CIBC’s strategy

CIBC aspires to be the leading bank for our clients. We have a client-focused strategy that creates value for all our stakeholders. We have four corporate objectives:

| 1. | Deep, long-lasting client relationships |

| 2. | Strategic growth where we have, or can build, competitive capabilities |

| 4. | Consistent, sustainable earnings |

To deliver on our corporate objectives, we are further strengthening our business in Canada, as well as expanding in key global centres to serve our clients.

Performance against objectives

For many years, CIBC has reported a scorecard of financial measures that we use to measure and report on our progress to external stakeholders. These measures can be categorized into four key areas of shareholder value – earnings growth, return on common shareholders’ equity (ROE), total shareholder return (TSR) and balance sheet strength. We have set targets for each of these measures over the medium term, which we define as three to five years.

Earnings growth

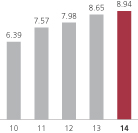

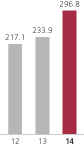

To assess our earnings growth, we monitor our earnings per share (EPS). CIBC has an EPS growth target of 5% to 10% on average annually. In 2014, we reported adjusted diluted EPS(1) of $8.94, up 3% from $8.65 in 2013. As a result of the impact of the Aeroplan transactions noted in the Significant Events section, we did not meet our EPS growth target of 5% to 10%. We are maintaining our 5% to 10% average annual EPS growth target over the medium term.

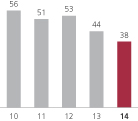

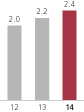

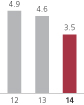

In support of our EPS target, we also have objectives to maintain a loan loss ratio of less than 60 basis points through the cycle and to maintain our adjusted efficiency ratio(1) at the median position among our industry peers.

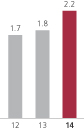

Our loan loss ratio is defined as the provision for credit losses on impaired loans to average loans and acceptances, net of allowance for credit losses. In 2014, our loan loss ratio was 38 basis points, down from the 44 basis points we reported in 2013, and well within our target. We are maintaining our loan loss ratio target of less than 60 basis points.

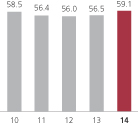

Our adjusted efficiency ratio(1) was 59.1% in 2014, up from 56.5% in 2013 as a result of the Aeroplan sale noted above, as well as higher spending on strategic initiatives. Based on the most recent publicly reported results of our industry peer group, CIBC did not meet its industry median efficiency ratio target in 2014. We are maintaining our industry median target going forward.

| | | | |

Adjusted diluted EPS(1)(2)(3) ($) | | Loan loss ratio(2) (basis points) | | Adjusted efficiency ratio(1)(2)(3) (%) |

| |  | |  |

| (1) | For additional information, see the “Non-GAAP measures” section. |

| (2) | Beginning in fiscal year 2011, these measures are under IFRS; prior fiscal years are under Canadian GAAP. |

| (3) | Information for 2013 and 2012 has been restated to reflect the changes in accounting policies stated in Note 1 to the consolidated financial statements and to conform to the presentation in the current year. |

|

Management’s discussion and analysis |

| | |

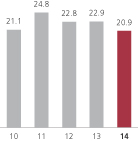

Adjusted return on common shareholders’ equity (1) Adjusted ROE is another key measure of shareholder value. CIBC’s target is to achieve adjusted ROE of 20% through the cycle. In 2014, adjusted ROE of 20.9% was above this target, but below the 22.9% in 2013. We are maintaining our minimum adjusted ROE target of 20%. | | Adjusted return on common shareholders’ equity(1)(2)(3) (%)

|

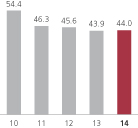

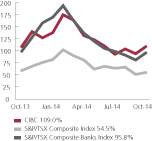

Total shareholder return One of CIBC’s priorities is to fulfill the commitments we have made to each of our stakeholders, which includes generating a strong level of TSR. We have two targets that support this priority: 1. Consistent with prior years, we target on a long-term, average basis, between 40% and 50% of our earnings in the form of dividends to our common shareholders. In 2014, our adjusted dividend payout ratio(1) was within this target range. Our key criteria for considering dividend increases are our current level of payout relative to our target and our view on the sustainability of our current earnings level through the cycle. Our confidence in our ability to generate consistent, sustainable returns allowed us to increase our quarterly dividend by $0.04 to $1.00 per share in 2014. This year we also announced a new share buyback program to purchase for cancellation up to a maximum of 8.0 million outstanding common shares. In 2014, we repurchased 3,369,000 CIBC shares for cancellation. The share buyback program was renewed for another 12 months effective September 16, 2014. 2. We also have an objective to deliver a TSR that exceeds the industry average, which we have defined as the Standard & Poor’s (S&P)/TSX Composite Banks Index, over a rolling five-year period. For the five years ended October 31, 2014, CIBC delivered a TSR of 109.0%, above the Index return of 95.8%. Going forward, we are maintaining our objectives to deliver an adjusted dividend payout ratio between 40% and 50% of our earnings and a rolling five-year TSR above the industry average. | | Adjusted dividend payout ratio(1)(2)(3) (%)

Rolling five-year total shareholder return (%)

|

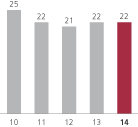

Balance sheet strength Maintaining a strong balance sheet is foundational to our long-term sustainability. Capital levels are a key component of balance sheet strength. We have set a target for our Basel III CET1 ratio to exceed the regulatory target set by the Office of the Superintendent of Financial Institutions (OSFI). At the end of 2014, our Basel III CET1 ratio on an all-in basis was 10.3%, well above the regulatory target set by OSFI. How we deploy our capital is also important. Our target is to limit the proportion of the economic capital allocated to Wholesale Banking to a maximum of 25% of CIBC’s total economic capital. At the end of 2014, the economic capital allocated to Wholesale Banking was 22%. In addition to our capital and business mix objectives, we remain focused on asset quality and a strong funding profile as key underpinnings of a strong balance sheet. | | Business mix (Wholesale Banking economic capital)(1)(4) (%)

|

| (1) | For additional information, see the “Non-GAAP measures” section. |

| (2) | Beginning in fiscal year 2011, these measures are under IFRS; prior fiscal years are under Canadian GAAP. |

| (3) | Information for 2013 and 2012 has been restated to reflect the changes in accounting policies stated in Note 1 to the consolidated financial statements and to conform to the presentation in the current year. |

| (4) | Information for prior years has been restated to conform to the presentation in the current year. |

Economic and market environment

CIBC operated in an environment of moderate economic growth in 2014. Canadian economic activity was held back by a deceleration in global growth that slowed capital spending, although exports accelerated as U.S. demand improved through the year. Home building remained brisk, at levels comparable with the prior year, and rising house prices continued to support modest growth in mortgage demand. Household consumption maintained its prior year pace, as Canadians pared back on savings to supplement spending power in the face of only moderate employment gains and limited use of non-auto consumer credit. Slightly lower unemployment rates and low interest rates kept household insolvencies and arrears at very low levels. Profit gains and solid balance sheets also kept Canadian business bankruptcies in check. Low interest rates encouraged growth in lending for both commercial and corporate banking and strong investor appetite for spread product supported corporate bond issuance, although at lower volumes in Canada than last year. Governments continued to have elevated borrowing needs, but issuance in Canada was down somewhat from the prior year. Canadian and global equity markets were strong through much of the year, supporting wealth management and an upturn in equity issuance and investment banking.

|

Management’s discussion and analysis |

Financial performance overview

Financial highlights

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | IFRS | | | | | Canadian GAAP | |

| As at or for the year ended October 31 | | | | 2014 | | | 2013 (1) | | | 2012 (1) | | | 2011 | | | | | 2010 | |

Financial results ($ millions) | | | | | | | | | | | | | | | | | | | | | | | | |

Net interest income | | | | $ | 7,459 | | | $ | 7,453 | | | $ | 7,326 | | | $ | 7,062 | | | | | $ | 6,204 | |

Non-interest income | | | | | 5,917 | | | | 5,265 | | | | 5,159 | | | | 5,373 | | | | | | 5,881 | |

Total revenue | | | | | 13,376 | | | | 12,718 | | | | 12,485 | | | | 12,435 | | | | | | 12,085 | |

Provision for credit losses | | | | | 937 | | | | 1,121 | | | | 1,291 | | | | 1,144 | | | | | | 1,046 | |

Non-interest expenses | | | | | 8,525 | | | | 7,621 | | | | 7,202 | | | | 7,486 | | | | | | 7,027 | |

Income before taxes | | | | | 3,914 | | | | 3,976 | | | | 3,992 | | | | 3,805 | | | | | | 4,012 | |

Income taxes | | | | | 699 | | | | 626 | | | | 689 | | | | 927 | | | | | | 1,533 | |

Non-controlling interests | | | | | – | | | | – | | | | – | | | | – | | | | | | 27 | |

Net income | | | | $ | 3,215 | | | $ | 3,350 | | | $ | 3,303 | | | $ | 2,878 | | | | | $ | 2,452 | |

Net income (loss) attributable to non-controlling interests | | | (3 | ) | | | (2 | ) | | | 9 | | | | 11 | | | | | | – | |

Preferred shareholders | | | | | 87 | | | | 99 | | | | 158 | | | | 177 | | | | | | 169 | |

Common shareholders | | | | | 3,131 | | | | 3,253 | | | | 3,136 | | | | 2,690 | | | | | | 2,283 | |

Net income attributable to equity shareholders | | $ | 3,218 | | | $ | 3,352 | | | $ | 3,294 | | | $ | 2,867 | | | | | $ | 2,452 | |

Financial measures | | | | | | | | | | | | | | | | | | | | | | | | |

Reported efficiency ratio | | | | | 63.7 | % | | | 59.9 | % | | | 57.7 | % | | | 60.2 | % | | | | | 58.1 | % |

Adjusted efficiency ratio (2) | | | | | 59.1 | % | | | 56.5 | % | | | 56.0 | % | | | 56.4 | % | | | | | 58.5 | % |

Loan loss ratio | | | | | 0.38 | % | | | 0.44 | % | | | 0.53 | % | | | 0.51 | % | | | | | 0.56 | % (2) |

Reported return on common shareholders’ equity | | | 18.3 | % | | | 21.4 | % | | | 22.2 | % | | | 22.2 | % | | | | | 19.4 | % |

Adjusted return on common shareholders’ equity (2) | | | 20.9 | % | | | 22.9 | % | | | 22.8 | % | | | 24.8 | % | | | | | 21.1 | % |

Net interest margin | | | | | 1.81 | % | | | 1.85 | % | | | 1.84 | % | | | 1.79 | % | | | | | 1.79 | % |

Net interest margin on average interest-earning assets | | | 2.05 | % | | | 2.12 | % | | | 2.15 | % | | | 2.03 | % | | | | | 2.11 | % |

Return on average assets | | | | | 0.78 | % | | | 0.83 | % | | | 0.83 | % | | | 0.73 | % | | | | | 0.71 | % |

Return on average interest-earning assets | | | 0.89 | % | | | 0.95 | % | | | 0.97 | % | | | 0.83 | % | | | | | 0.83 | % |

Total shareholder return | | | | | 20.87 | % | | | 18.41 | % | | | 9.82 | % | | | 0.43 | % | | | | | 32.38 | % |

Reported effective tax rate | | | | | 17.9 | % | | | 15.8 | % | | | 17.3 | % | | | 24.4 | % | | | | | 38.2 | % |

Adjusted effective tax rate (2) | | | | | 15.4 | % | | | 16.5 | % | | | 18.0 | % | | | 23.0 | % | | | | | 27.2 | % |

Common share information | | | | | | | | | | | | | | | | | | | | | | | | |

Per share ($) | | – basic earnings | | $ | 7.87 | | | $ | 8.11 | | | $ | 7.77 | | | $ | 6.79 | | | | | $ | 5.89 | |

| | – reported diluted earnings | | | 7.86 | | | | 8.11 | | | | 7.76 | | | | 6.71 | | | | | | 5.87 | |

| | – adjusted diluted earnings (2) | | | 8.94 | | | | 8.65 | | | | 7.98 | | | | 7.57 | | | | | | 6.39 | |

| | – dividends | | | 3.94 | | | | 3.80 | | | | 3.64 | | | | 3.51 | | | | | | 3.48 | |

| | – book value | | | 44.30 | | | | 40.36 | | | | 35.83 | | | | 32.88 | | | | | | 32.17 | |

Share price ($) | | – high | | | 107.01 | | | | 88.70 | | | | 78.56 | | | | 85.49 | | | | | | 79.50 | |

| | – low | | | 85.49 | | | | 74.10 | | | | 68.43 | | | | 67.84 | | | | | | 61.96 | |

| | – closing | | | 102.89 | | | | 88.70 | | | | 78.56 | | | | 75.10 | | | | | | 78.23 | |

Shares outstanding (thousands) | | – weighted average basic | | | 397,620 | | | | 400,880 | | | | 403,685 | | | | 396,233 | | | | | | 387,802 | |

| | – weighted average diluted | | | 398,420 | | | | 401,261 | | | | 404,145 | | | | 406,696 | | | | | | 388,807 | |

| | – end of period | | | 397,021 | | | | 399,250 | | | | 404,485 | | | | 400,534 | | | | | | 392,739 | |

Market capitalization ($ millions) | | | | $ | 40,850 | | | $ | 35,413 | | | $ | 31,776 | | | $ | 30,080 | | | | | $ | 30,724 | |

Value measures | | | | | | | | | | | | | | | | | | | | | | | | |

Dividend yield (based on closing share price) | | | 3.8 | % | | | 4.3 | % | | | 4.6 | % | | | 4.7 | % | | | | | 4.4 | % |

Reported dividend payout ratio | | | | | 50.0 | % | | | 46.8 | % | | | 46.9 | % | | | 51.7 | % | | | | | 59.1 | % |

Adjusted dividend payout ratio (2) | | | | | 44.0 | % | | | 43.9 | % | | | 45.6 | % | | | 46.3 | % | | | | | 54.4 | % |

Market value to book value ratio | | | | | 2.32 | | | | 2.20 | | | | 2.19 | | | | 2.28 | | | | | | 2.43 | |

On- and off-balance sheet information ($ millions) | | | | | | | | | | | | | | | | | | | | | | |

Cash, deposits with banks and securities | | | | $ | 73,089 | | | $ | 78,363 | | | $ | 70,061 | | | $ | 65,437 | | | | | $ | 89,660 | |

Loans and acceptances, net of allowance | | | | | 268,240 | | | | 256,380 | | | | 252,732 | | | | 248,409 | | | | | | 184,576 | |

Total assets | | | | | 414,903 | | | | 398,006 | | | | 393,119 | | | | 383,758 | | | | | | 352,040 | |

Deposits | | | | | 325,393 | | | | 315,164 | | | | 300,344 | | | | 289,220 | | | | | | 246,671 | |

Common shareholders’ equity | | | | | 17,588 | | | | 16,113 | | | | 14,491 | | | | 13,171 | | | | | | 12,634 | |

Average assets | | | | | 411,481 | | | | 403,546 | | | | 397,155 | | | | 394,527 | | | | | | 345,943 | |

Average interest-earning assets | | | | | 362,997 | | | | 351,687 | | | | 341,053 | | | | 347,634 | | | | | | 294,428 | |

Average common shareholders’ equity | | | | | 17,067 | | | | 15,167 | | | | 14,116 | | | | 12,145 | | | | | | 11,772 | |

Assets under administration (3) | | | | | 1,717,563 | | | | 1,513,126 | | | | 1,445,870 | | | | 1,317,799 | | | | | | 1,260,989 | |

Balance sheet quality measures (4) | | | | | | | | | | | | | | | | | | | | | | | | |

Basel III – All-in basis | | | | | | | | | | | | | | | | | | | | | | | | |

CET1 capital risk-weighted assets (RWA) ($ billions) | | $ | 141,250 | | | $ | 136,747 | | | | n/a | | | | n/a | | | | | | n/a | |

Tier 1 capital RWA | | | | | 141,446 | | | | 136,747 | | | | n/a | | | | n/a | | | | | | n/a | |

Total capital RWA | | | | | 141,739 | | | | 136,747 | | | | n/a | | | | n/a | | | | | | n/a | |

CET1 ratio | | | | | 10.3 | % | | | 9.4 | % | | | n/a | | | | n/a | | | | | | n/a | |

Tier 1 capital ratio | | | | | 12.2 | % | | | 11.6 | % | | | n/a | | | | n/a | | | | | | n/a | |

Total capital ratio | | | | | 15.5 | % | | | 14.6 | % | | | n/a | | | �� | n/a | | | | | | n/a | |

Basel II (5) | | | | | | | | | | | | | | | | | | | | | | | | |

RWA ($ millions) | | | | | n/a | | | | n/a | | | $ | 115,229 | | | $ | 109,968 | | | | | $ | 106,663 | |

Tier 1 capital ratio | | | | | n/a | | | | n/a | | | | 13.8 | % | | | 14.7 | % | | | | | 13.9 | % |

Total capital ratio | | | | | n/a | | | | n/a | | | | 17.3 | % | | | 18.4 | % | | | | | 17.8 | % |

Other information | | | | | | | | | | | | | | | | | | | | | | | | |

Full-time equivalent employees | | | | | 44,424 | | | | 43,039 | | | | 42,595 | | | | 42,239 | | | | | | 42,354 | |

| (1) | Certain information has been restated to reflect the changes in accounting policies stated in Note 1 to the consolidated financial statements and to conform to the presentation in the current year. |

| (2) | For additional information, see the “Non-GAAP measures” section. |

| (3) | Includes the full contract amount of assets under administration or custody under a 50/50 joint venture between CIBC and The Bank of New York Mellon. |

| (4) | Capital measures for fiscal years 2014 and 2013 are based on Basel III whereas measures for prior years are based on Basel II. |

| (5) | Capital measures for fiscal year 2011 are under Canadian GAAP and have not been restated for IFRS. |

|

Management’s discussion and analysis |

2014 Financial results

Reported net income for the year was $3,215 million, compared with $3,350 million in 2013.

Adjusted net income(1) for the year was $3,657 million, compared with $3,569 million in 2013.

Reported diluted EPS for the year was $7.86, compared with $8.11 in 2013.

Adjusted diluted EPS(1) for the year was $8.94, compared with $8.65 in 2013.

2014

Net income was affected by the following items of note:

| • | | $543 million ($543 million after-tax) of charges relating to FirstCaribbean International Bank Limited (CIBC FirstCaribbean), comprising a goodwill impairment charge of $420 million ($420 million after-tax) and loan losses of $123 million ($123 million after-tax), reflecting revised expectations on the extent and timing of the anticipated economic recovery in the Caribbean region (Corporate and Other); |

| • | | $190 million ($147 million after-tax) gain in respect of the Aeroplan transactions with Aimia Canada Inc. (Aimia) and TD, net of costs relating to the development of our enhanced travel rewards program ($87 million after-tax in Retail and Business Banking, and $60 million after-tax in Corporate and Other); |

| • | | $112 million ($82 million after-tax) charge relating to the incorporation of funding valuation adjustments (FVA) into the valuation of our uncollateralized derivatives (Wholesale Banking); |

| • | | $78 million ($57 million after-tax) gain, net of associated expenses, on the sale of an equity investment in our exited European leveraged finance portfolio (Wholesale Banking); |

| • | | $52 million ($30 million after-tax) gain within an equity-accounted investment in our merchant banking portfolio (Wholesale Banking); |

| • | | $36 million ($28 million after-tax) amortization of intangible assets(2) ($4 million after-tax in Retail and Business Banking, $15 million after-tax in Wealth Management, and $9 million after-tax in Corporate and Other); |

| • | | $26 million ($19 million after-tax) reduction in the portion of the collective allowance recognized in Corporate and Other(3), including lower estimated credit losses relating to the Alberta floods (Corporate and Other); |

| • | | $26 million ($19 million after-tax) charge resulting from operational changes in the processing of write-offs in Retail and Business Banking; |

| • | | $22 million ($12 million after-tax) loan losses in our exited U.S. leveraged finance portfolio (Wholesale Banking); and |

| • | | $15 million ($11 million after-tax) loss from the structured credit run-off business (Wholesale Banking). |

The above items of note increased revenue by $276 million, provision for credit losses by $145 million, non-interest expenses by $539 million, and income tax expense by $34 million. In aggregate, these items of note decreased net income by $442 million.

2013

Net income was affected by the following items of note:

| • | | $114 million ($84 million after-tax) loss from the structured credit run-off business, including the charge in respect of a settlement of the U.S. Bankruptcy Court adversary proceeding brought by the Estate of Lehman Brothers Holdings, Inc. (Wholesale Banking); |

| • | | $39 million ($37 million after-tax) restructuring charge relating to CIBC FirstCaribbean (Corporate and Other); |

| • | | $38 million ($28 million after-tax) increase in the portion of the collective allowance recognized in Corporate and Other(3), including $56 million of estimated credit losses relating to the Alberta floods; |

| • | | $35 million ($19 million after-tax) impairment of an equity position associated with our exited U.S. leveraged finance portfolio (Wholesale Banking); |

| • | | $24 million ($18 million after-tax) costs relating to the development of our enhanced travel rewards program and to the Aeroplan transactions with Aimia and TD (Retail and Business Banking); |

| • | | $23 million ($19 million after-tax) amortization of intangible assets(2) ($5 million after-tax in Retail and Business Banking, $4 million after-tax in Wealth Management, and $10 million after-tax in Corporate and Other); |

| • | | $21 million ($15 million after-tax) loan losses in our exited European leveraged finance portfolio (Wholesale Banking); |

| • | | $20 million ($15 million after-tax) charge resulting from a revision of estimated loss parameters on our unsecured lending portfolios (Retail and Business Banking); and |

| • | | $16 million ($16 million after-tax) gain, net of associated expenses, on the sale of our Hong Kong and Singapore-based private wealth management business (Corporate and Other). |

The above items of note increased revenue by $30 million, provision for credit losses by $79 million and non-interest expenses by $249 million, and decreased income tax expense by $79 million. In aggregate, these items of note decreased net income by $219 million.

Net interest income and margin

| | | | | | | | | | | | |

| $ millions, for the year ended October 31 | | 2014 | | | 2013 (4) | | | 2012 | |

Average interest-earning assets | | | $ 362,997 | | | | $ 351,687 | | | | $ 341,053 | |

Net interest income | | | 7,459 | | | | 7,453 | | | | 7,326 | |

Net interest margin on average interest-earning assets | | | 2.05 | % | | | 2.12 | % | | | 2.15 | % |

Net interest income was comparable with 2013 as volume growth across most retail products and higher revenue from corporate banking was offset by lower card revenue, as a result of the Aeroplan transactions noted above, and lower treasury revenue.

Net interest margin on average interest-earning assets was down 7 basis points primarily due to the Aeroplan transactions.

Additional information on net interest income and margin is provided in the “Supplementary annual financial information” section.

| (1) | For additional information, see the “Non-GAAP measures” section. |

| (2) | Beginning in the fourth quarter of 2013, also includes amortization of intangible assets for equity-accounted associates. |

| (3) | Relates to collective allowance, except for (i) residential mortgages greater than 90 days delinquent; (ii) personal loans and scored small business loans greater than 30 days delinquent, and (iii) net write-offs for the cards portfolio, which are all reported in the respective SBUs. |

| (4) | Certain information has been restated to reflect the changes in accounting policies stated in Note 1 to the consolidated financial statements and to conform to the presentation in the current year. |

|

Management’s discussion and analysis |

Non-interest income

| | | | | | | | | | | | |

| $ millions, for the year ended October 31 | | 2014 | | | 2013 (1) | | | 2012 (1) | |

Underwriting and advisory fees | | $ | 444 | | | $ | 389 | | | $ | 438 | |

Deposit and payment fees | | | 848 | | | | 824 | | | | 775 | |

Credit fees | | | 478 | | | | 462 | | | | 418 | |

Card fees | | | 414 | | | | 535 | | | | 560 | |

Investment management and custodial fees | | | 677 | | | | 474 | | | | 424 | |

Mutual fund fees | | | 1,236 | | | | 1,014 | | | | 880 | |

Insurance fees, net of claims | | | 369 | | | | 358 | | | | 335 | |

Commissions on securities transactions | | | 408 | | | | 412 | | | | 402 | |

Trading income (loss) | | | (176 | ) | | | 27 | | | | 53 | |

Available-for-sale (AFS) securities gains, net | | | 201 | | | | 212 | | | | 264 | |

Designated at fair value (FVO) gains (losses), net | | | (15 | ) | | | 5 | | | | (32 | ) |

Foreign exchange other than trading | | | 43 | | | | 44 | | | | 91 | |

Income from equity-accounted associates and joint ventures | | | 226 | | | | 140 | | | | 155 | |

Other | | | 764 | | | | 369 | | | | 396 | |

| | | $ | 5,917 | | | $ | 5,265 | | | $ | 5,159 | |

| (1) | Certain information has been restated to reflect the changes in accounting policies stated in Note 1 to the consolidated financial statements and to conform to the presentation in the current year. |

Non-interest income was up $652 million or 12% from 2013.

Underwriting and advisory fees were up $55 million or 14%, primarily due to higher equity issuance revenue and advisory activity.

Card fees were down $121 million or 23%, as a result of the Aeroplan transactions noted above.

Investment management and custodial fees were up $203 million or 43%, primarily due to the acquisition of Atlantic Trust Private Wealth Management (Atlantic Trust) and growth in client balances.

Mutual fund fees were up $222 million or 22%, primarily due to higher net sales of long-term mutual funds and market appreciation.

Trading incomewas down $203 million. See the “Trading activities (TEB)” section which follows for further details.

Income from equity-accounted associates and joint ventureswas up $86 million or 61%, primarily due to the gain within an equity-accounted investment in our merchant banking portfolio, shown as an item of note, and a higher contribution from American Century Investments (ACI).

Otherwas up $395 million or 107%, primarily due to gains relating to the Aeroplan transactions and the sale of an equity investment in our exited European leveraged finance portfolio, both shown as items of note.

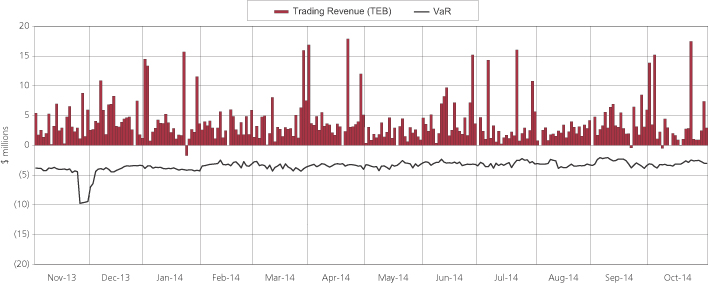

Trading activities (TEB)

| | | | | | | | | | | | |

| $ millions, for the year ended October 31 | | 2014 | | | 2013 (1) | | | 2012 (1) | |

Trading income (loss) consists of: | | | | | | | | | | | | |

Net interest income(2) | | $ | 1,049 | | | $ | 969 | | | $ | 762 | |

Non-interest income | | | (176 | ) | | | 27 | | | | 53 | |

| | | $ | 873 | | | $ | 996 | | | $ | 815 | |

Trading income (loss) by product line: | | | | | | | | | | | | |

Interest rates | | $ | (20 | ) | | $ | 135 | | | $ | 146 | |

Foreign exchange | | | 392 | | | | 344 | | | | 323 | |

Equities | | | 369 | | | | 333 | | | | 235 | |

Commodities | | | 48 | | | | 55 | | | | 52 | |

Structured credit | | | 35 | | | | 77 | | | | 7 | |

Other | | | 49 | | | | 52 | | | | 52 | |

| | | $ | 873 | | | $ | 996 | | | $ | 815 | |

| (1) | Certain information has been restated to reflect the changes in accounting policies stated in Note 1 to the consolidated financial statements and to conform to the presentation in the current year. |

| (2) | Includes taxable equivalent basis (TEB) adjustment of $421 million (2013: $356 million; 2012: $280 million) reported within Wholesale Banking. See “Strategic business units overview” section for further details. |

Net interest income comprises interest and dividends relating to financial assets and liabilities associated with trading activities, net of interest expense and interest income associated with funding these assets and liabilities. Non-interest income includes realized and unrealized gains and losses on securities held-for-trading and income relating to changes in fair value of derivative financial instruments. Trading activities and related risk management strategies can periodically shift income between net interest income and non-interest income. Therefore, we view total trading revenue as the most appropriate measure of trading performance.

Trading income was down $123 million or 12% from 2013, primarily due to the charge relating to FVA in the current year, shown as an item of note. Lower income in the structured credit run-off business and lower interest rate trading income was partially offset by higher client-driven equity trading income.

|

Management’s discussion and analysis |

Provision for credit losses

| | | | | | | | | | | | |

| $ millions, for the year ended October 31 | | 2014 | | | 2013 | | | 2012 | |

Retail and Business Banking | | $ | 731 | | | $ | 930 | | | $ | 1,080 | |

Wealth Management | | | – | | | | 1 | | | | – | |

Wholesale Banking | | | 43 | | | | 44 | | | | 142 | |

Corporate and Other | | | 163 | | | | 146 | | | | 69 | |

| | | $ | 937 | | | $ | 1,121 | | | $ | 1,291 | |

Provision for credit losses was down $184 million or 16% from 2013.

In Retail and Business Banking, the provision was down mainly due to lower write-offs and bankruptcies in the card portfolio which reflect credit improvements, as well as the impact of an initiative to enhance account management practices, and the sold Aeroplan portfolio. The current year also had lower losses in the business lending portfolio. The current year included a charge resulting from operational changes in the processing of write-offs, and the prior year included a charge resulting from a revision of estimated loss parameters on our unsecured lending portfolios, both shown as items of note.

In Wholesale Banking, the provision was comparable with the prior year. The current year had losses in our exited U.S. leveraged finance portfolio, while the prior year had losses in our exited European leveraged finance portfolio, both shown as items of note.

In Corporate and Other, the provision was up primarily due to the loan losses in the current year relating to CIBC FirstCaribbean, shown as an item of note, partially offset by a decrease in the collective allowance. The prior year included estimated credit losses related to the Alberta floods, shown as an item of note, a portion of which was estimated to not be required and therefore reversed in the current year.

Non-interest expenses

| | | | | | | | | | | | |

| $ millions, for the year ended October 31 | | 2014 | | | 2013 (1) | | | 2012 (1) | |

Employee compensation and benefits | | | | | | | | | | | | |

Salaries | | $ | 2,502 | | | $ | 2,397 | | | $ | 2,285 | |

Performance-based compensation | | | 1,483 | | | | 1,299 | | | | 1,236 | |

Benefits | | | 651 | | | | 628 | | | | 569 | |

| | | 4,636 | | | | 4,324 | | | | 4,090 | |

Occupancy costs | | | 736 | | | | 700 | | | | 697 | |

Computer, software and office equipment | | | 1,200 | | | | 1,052 | | | | 1,022 | |

Communications | | | 312 | | | | 307 | | | | 304 | |

Advertising and business development | | | 285 | | | | 236 | | | | 233 | |

Professional fees | | | 201 | | | | 179 | | | | 174 | |

Business and capital taxes | | | 59 | | | | 62 | | | | 50 | |

Other | | | 1,096 | | | | 761 | | | | 632 | |

| | | $ | 8,525 | | | $ | 7,621 | | | $ | 7,202 | |

| (1) | Certain information has been restated to reflect the changes in accounting policies stated in Note 1 to the consolidated financial statements and to conform to the presentation adopted in the current year. |

Non-interest expenses increased by $904 million or 12% from 2013.

Employee compensation and benefits increased by $312 million or 7%, primarily due to higher performance-based compensation and salaries. The prior year included a restructuring charge relating to CIBC FirstCaribbean, shown as an item of note.

Computer, software and office equipmentincreased by $148 million or 14%, andAdvertising and business development increased by $49 million or 21%, primarily due to higher spending on strategic initiatives and the costs relating to the development of our enhanced travel rewards program.

Other increased by $335 million or 44%. The goodwill impairment charge relating to CIBC FirstCaribbean was included in the current year, while the settlement charge in the structured credit run-off business was included in the prior year, both shown as items of note.

Taxes

| | | | | | | | | | | | |

| $ millions, for the year ended October 31 | | 2014 | | | 2013 (1) | | | 2012 (1) | |

Income tax expense | | $ | 699 | | | $ | 626 | | | $ | 689 | |

Indirect taxes (2) | | | | | | | | | | | | |

Goods and services tax (GST), harmonized sales tax (HST) and sales taxes | | | 330 | | | | 324 | | | | 321 | |

Payroll taxes | | | 216 | | | | 204 | | | | 192 | |

Capital taxes | | | 34 | | | | 40 | | | | 33 | |

Property and business taxes | | | 59 | | | | 55 | | | | 50 | |

Total indirect taxes | | | 639 | | | | 623 | | | | 596 | |

Total taxes | | $ | 1,338 | | | $ | 1,249 | | | $ | 1,285 | |

Reported effective tax rate | | | 17.9 | % | | | 15.8 | % | | | 17.3 | % |

Total taxes as a percentage of net income before deduction of total taxes | | | 29.4 | % | | | 27.2 | % | | | 28.0 | % |

| (1) | Certain information has been restated to reflect the changes in accounting policies stated in Note 1 to the consolidated financial statements and to conform to the presentation in the current year. |

| (2) | Certain amounts are based on a paid or payable basis and do not factor in capitalization and subsequent amortization. |

Income taxes include those imposed on CIBC as a Canadian legal entity, as well as on our domestic and foreign subsidiaries. Indirect taxes comprise GST, HST, and sales, payroll, capital, property and business taxes. Indirect taxes are included in non-interest expenses.

Total income and indirect taxes were up $89 million from 2013.

Income tax expense was $699 million, compared with $626 million in 2013. Income tax expense was higher, notwithstanding lower income in the current year, primarily due to no tax recovery being booked in the current year in respect of the CIBC FirstCaribbean goodwill impairment charge and loan losses, partially offset by the impact of higher tax-exempt income.

|

Management’s discussion and analysis |

Indirect taxes were up by $16 million, mainly due to higher payroll taxes. Payroll taxes increased due to higher rates and compensation.

In prior years, the Canada Revenue Agency issued reassessments disallowing the deduction of approximately $3 billion of the 2005 Enron settlement payments and related legal expenses. The matter is currently in litigation. The Tax Court of Canada trial on the deductibility of the Enron payments is scheduled to commence in October 2015.

Should we successfully defend our tax filing position in its entirety, we would recognize an additional accounting tax benefit of $214 million and taxable refund interest of approximately $207 million. Should we fail to defend our position in its entirety, we would incur an additional tax expense of approximately $866 million and non-deductible interest of approximately $124 million.

The statutory income tax rate applicable to CIBC as a legal entity was 26.4% in 2014. The rate will remain the same in future years.

For a reconciliation of our income taxes in the consolidated statement of income with the combined Canadian federal and provincial income tax rate, see Note 20 to the consolidated financial statements.

Foreign exchange

The estimated impact of U.S. dollar translation on key lines of our consolidated statement of income, as a result of changes in average exchange rates, is as follows:

| | | | | | | | | | | | |

| $ millions, for the year ended October 31 | | 2014 vs. 2013 | | | 2013 vs. 2012 | | | 2012 vs. 2011 | |

Estimated increase in: | | | | | | | | | | | | |

Total revenue | | $ | 131 | | | $ | 34 | | | $ | 27 | |

Provision for credit losses | | | 17 | | | | 3 | | | | 5 | |

Non-interest expense | | | 83 | | | | 14 | | | | 12 | |

Income taxes | | | 5 | | | | 1 | | | | – | |

Net income | | | 26 | | | | 16 | | | | 10 | |

Average US$ appreciation relative to C$ | | | 6.9 | % | | | 2.0 | % | | | 1.8 | % |

Significant events

Goodwill impairment

During the year, we recognized a goodwill impairment charge of $420 million relating to CIBC FirstCaribbean. This impairment reflects revised expectations on the extent and timing of the anticipated economic recovery in the Caribbean region. For additional information, see the Accounting and control matters section and Note 8 to our consolidated financial statements.

Aeroplan Agreements and enhancements to CIBC travel rewards program

On December 27, 2013, CIBC completed the transactions contemplated by the tri-party agreements with Aimia and TD.

CIBC sold to TD approximately 50% of its existing Aerogold VISA credit card portfolio, consisting primarily of credit card only customers. Consistent with its strategy to invest in and deepen client relationships, CIBC retained the Aerogold VISA credit card accounts held by clients with broader banking relationships at CIBC.

The portfolio divested by CIBC consisted of $3.3 billion of credit card receivables. Upon closing, CIBC received a cash payment from TD equal to the credit card receivables outstanding being acquired by TD.

CIBC also received upon closing, in aggregate, $200 million in upfront payments from TD and Aimia.

In addition to these amounts, CIBC released $81 million of allowance for credit losses related to the sold portfolio, and incurred $3 million in direct costs related to the transaction in the quarter ended January 31, 2014. The net gain on sale of the sold portfolio recognized in the quarter ended January 31, 2014, which included the upfront payments, release of allowance for credit losses and costs related to the transaction, was $278 million ($211 million after-tax).

Under the terms of the agreements:

| • | | CIBC continues to have rights to market the Aeroplan program and originate new Aerogold cardholders through its CIBC branded channels. |

| • | | The parties have agreed to certain provisions to compensate for the risk of cardholder migration from one party to another. There is potential for payments of up to $400 million by TD/Aimia or CIBC for net cardholder migration over a period of five years (Migration Payments). |

| • | | CIBC receives annual commercial subsidy payments from TD expected to be approximately $38 million per year in each of the three years after closing. |

| • | | The CIBC and Aimia agreement includes an option for either party to terminate the agreement after the third year and provides for penalty payments due from CIBC to Aimia if holders of Aeroplan credit cards from CIBC’s retained portfolio switch to other CIBC credit cards above certain thresholds. |

In conjunction with the completion of the Aeroplan transaction, CIBC has fully released Aimia and TD from any potential claims in connection with TD becoming Aeroplan’s primary financial credit card partner.

Separate from the tri-party agreements, CIBC continues with its plan to provide enhancements to our proprietary travel rewards program, delivering on our commitment to give our clients access to a market leading travel rewards program. The enhanced program is built on extensive research and feedback from our clients and from Canadians about what they want from their travel rewards card.

For the year ended October 31, 2014, CIBC incurred incremental costs of $88 million ($64 million after-tax) relating to the development of our enhanced travel rewards programs and in respect of supporting the tri-party agreements. Amounts recognized in respect of Migration Payments in the year ended October 31, 2014 were not significant.

Acquisition of Atlantic Trust Private Wealth Management

On December 31, 2013, CIBC completed the acquisition of Atlantic Trust from its parent company, Invesco Ltd., for $224 million (US$210 million) plus working capital and other adjustments. Atlantic Trust provides integrated wealth management solutions for high net worth individuals, families, foundations and endowments in the United States. The results of the acquired business have been consolidated from the date of close and are included in the Wealth Management SBU. For additional information, see Note 3 to our consolidated financial statements.

|

Management’s discussion and analysis |

Voluntary agreement on the reduction of credit card interchange fees

In recent years, the Canadian federal government has held discussions with various stakeholders on the fees paid by merchants to accept credit card payments from their customers, including fees set by payment networks known as interchange fees.

On November 4, 2014, an agreement was announced between the Canadian federal government, VISA and MasterCard for the voluntary reduction of interchange fee rates to an average effective rate of 1.50% for the next five years.

CIBC is evaluating the details of the agreement to assess the impact on CIBC, clients and other stakeholders.

Sale of equity investment

On November 29, 2013, CIBC sold an equity investment that was previously acquired through a loan restructuring in CIBC’s exited European leveraged finance business. The transaction resulted in an after-tax gain, net of associated expenses, of $57 million in the quarter ended January 31, 2014.

Fourth quarter review

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| $ millions, except per share amounts, for the three months ended | | | | | | | | | 2014 | | | 2013 (1) | |

| | | | | Oct. 31 | | | Jul. 31 | | | Apr. 30 | | | Jan. 31 | | | Oct. 31 | | | Jul. 31 | | | Apr. 30 | | | Jan. 31 | |

Revenue | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Retail and Business Banking | | $ | 2,050 | | | $ | 2,032 | | | $ | 1,939 | | | $ | 2,255 | | | $ | 2,087 | | | $ | 2,067 | | | $ | 1,985 | | | $ | 2,010 | |

Wealth Management | | | 584 | | | | 568 | | | | 548 | | | | 502 | | | | 470 | | | | 458 | | | | 443 | | | | 432 | |

Wholesale Banking (2) | | | 468 | | | | 670 | | | | 606 | | | | 680 | | | | 520 | | | | 589 | | | | 574 | | | | 557 | |

Corporate and Other (2) | | | 115 | | | | 88 | | | | 74 | | | | 197 | | | | 103 | | | | 135 | | | | 122 | | | | 166 | |

Total revenue | | $ | 3,217 | | | $ | 3,358 | | | $ | 3,167 | | | $ | 3,634 | | | $ | 3,180 | | | $ | 3,249 | | | $ | 3,124 | | | $ | 3,165 | |

Net interest income | | $ | 1,881 | | | $ | 1,875 | | | $ | 1,798 | | | $ | 1,905 | | | $ | 1,893 | | | $ | 1,883 | | | $ | 1,822 | | | $ | 1,855 | |

Non-interest income | | | 1,336 | | | | 1,483 | | | | 1,369 | | | | 1,729 | | | | 1,287 | | | | 1,366 | | | | 1,302 | | | | 1,310 | |

Total revenue | | | 3,217 | | | | 3,358 | | | | 3,167 | | | | 3,634 | | | | 3,180 | | | | 3,249 | | | | 3,124 | | | | 3,165 | |

Provision for credit losses | | | 194 | | | | 195 | | | | 330 | | | | 218 | | | | 271 | | | | 320 | | | | 265 | | | | 265 | |

Non-interest expenses | | | 2,087 | | | | 2,047 | | | | 2,412 | | | | 1,979 | | | | 1,930 | | | | 1,878 | | | | 1,825 | | | | 1,988 | |

Income before taxes | | | 936 | | | | 1,116 | | | | 425 | | | | 1,437 | | | | 979 | | | | 1,051 | | | | 1,034 | | | | 912 | |

Income taxes | | | 125 | | | | 195 | | | | 119 | | | | 260 | | | | 154 | | | | 173 | | | | 172 | | | | 127 | |

Net income | | $ | 811 | | | $ | 921 | | | $ | 306 | | | $ | 1,177 | | | $ | 825 | | | $ | 878 | | | $ | 862 | | | $ | 785 | |

Net income (loss) attributable to: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Non-controlling interests | | $ | 2 | | | $ | 3 | | | $ | (11 | ) | | $ | 3 | | | $ | (7 | ) | | $ | 1 | | | $ | 2 | | | $ | 2 | |

Equity shareholders | | | 809 | | | | 918 | | | | 317 | | | | 1,174 | | | | 832 | | | | 877 | | | | 860 | | | | 783 | |

EPS | | - basic | | $ | 1.99 | | | $ | 2.26 | | | $ | 0.73 | | | $ | 2.88 | | | $ | 2.02 | | | $ | 2.13 | | | $ | 2.09 | | | $ | 1.88 | |

| | | - diluted | | $ | 1.98 | | | $ | 2.26 | | | $ | 0.73 | | | $ | 2.88 | | | $ | 2.02 | | | $ | 2.13 | | | $ | 2.09 | | | $ | 1.88 | |

| (1) | Certain information has been restated to reflect the changes in accounting policies stated in Note 1 to the consolidated financial statements and to conform to the presentation in the current period. |

| (2) | Wholesale Banking revenue and income taxes are reported on a TEB basis with an equivalent offset in the revenue and income taxes of Corporate and Other. |

Compared with Q4/13

Net income for the quarter was $811 million, down $14 million or 2% from the fourth quarter of 2013.

Net interest income was down $12 million or 1%, primarily due to lower card revenue as a result of the Aeroplan transactions noted above, and lower treasury revenue, partially offset by volume growth across most retail products.

Non-interest income was up $49 million or 4%, primarily due to higher fee-based revenue, partially offset by the charge relating to FVA, shown as an item of note. The same quarter last year included an impairment of an equity position, shown as an item of note.

Provision for credit losses was down $77 million or 28%. In Retail and Business Banking, the provision was down due to lower write-offs and bankruptcies in the card portfolio which reflect credit improvements, as well as the impact of an initiative to enhance account management practices, and the sold Aeroplan portfolio, and lower losses in the business lending portfolio. In Wholesale Banking, the provision was up primarily due to higher losses in the U.S. real estate finance portfolio. In Corporate and Other, the provision was down primarily due to lower losses in CIBC FirstCaribbean.

Non-interest expenses were up $157 million or 8%, primarily due to higher employee-related compensation and computer, software and office expenses. The same quarter last year included the restructuring charge relating to CIBC FirstCaribbean.

Income tax expense was down $29 million or 19%, primarily due to an increase in the relative proportion of income earned in low tax jurisdictions, and lower income.

Compared with Q3/14

Net income for the quarter was $811 million, down $110 million or 12% from the prior quarter.

Net interest income was comparable with the prior quarter as volume growth across most retail products was largely offset by lower trading income.

Non-interest income was down $147 million or 10%, primarily due to the charge relating to FVA noted above. In addition, the prior quarter included a gain within an equity-accounted investment in our merchant banking portfolio, shown as an item of note.

Provision for credit losses was comparable with the prior quarter. In Retail and Business Banking, the provision was down due to lower write-offs and bankruptcies in the card portfolio which reflect credit improvements, as well as the impact of an initiative to enhance account management practices. In Wholesale Banking, the provision was up due to higher losses in the U.S. real estate finance portfolio. In Corporate and Other, the provision was down primarily due to lower losses in CIBC FirstCaribbean.

Non-interest expenses were up $40 million or 2%, primarily due to higher professional fees and computer software and office equipment expenses.

Income tax expense was down $70 million or 36%, primarily due to lower income.

| | |

| 10 | | CIBC2014 ANNUAL REPORT |

|

Management’s discussion and analysis |

Quarterly trend analysis

Our quarterly results are modestly affected by seasonal factors. The second quarter has fewer days as compared with the other quarters, generally leading to lower earnings. The summer months (July – third quarter and August – fourth quarter) typically experience lower levels of capital markets activity, which affects our brokerage, investment management, and wholesale banking activities.

Revenue

Retail and Business Banking revenue has benefitted from volume growth across most retail products, largely offset by the impact of the sold Aeroplan portfolio from the first quarter of 2014, the continued low interest rate environment, and attrition in our exited FirstLine mortgage broker business. The first quarter of 2014 also included the gain relating to the Aeroplan transactions with Aimia and TD.

Wealth Management revenue has benefitted from the impact of the acquisition of Atlantic Trust from the first quarter of 2014, higher average assets under management (AUM), higher contribution from our investment in ACI, and strong net sales of long-term mutual funds.

Wholesale Banking revenue is influenced, to a large extent, by capital markets conditions, and includes the TEB adjustment. Revenue has also been impacted by the volatility in the structured credit run-off business. The fourth quarter of 2014 included the charge related to FVA, while the third quarter and the first quarter of 2014 included gains within an equity-accounted investment in our merchant banking portfolio and on the sale of an equity investment in our exited European leveraged finance portfolio, respectively. The fourth quarter of 2013 included the impairment of an equity position in our exited U.S. leveraged finance portfolio.

Corporate and Other includes the offset related to the TEB adjustment noted above. The first quarter of 2014 included the gain relating to the Aeroplan transactions noted above and the first quarter of 2013 included the gain on sale of the private wealth management (Asia) business.

Provision for credit losses

Provision for credit losses is dependent upon the credit cycle in general and on the credit performance of the loan portfolios. In Retail and Business Banking, losses in the card portfolio have been trending lower since 2013 and have declined further in 2014 due to credit improvements, as well as the impact of an initiative to enhance account management practices, and the sold Aeroplan portfolio. A charge resulting from operational changes in the processing of write-offs was included in the first quarter of 2014, and a charge resulting from a revision of estimated loss parameters on our unsecured lending portfolios was included in the third quarter of 2013. In Wholesale Banking, the second quarter of 2014 included losses in the exited U.S. leveraged finance portfolio. The second and third quarters of 2013 had higher losses in the exited European leveraged finance portfolio. In Corporate and Other, the second quarter of 2014 had loan losses relating to CIBC FirstCaribbean. The third quarter of 2013 had an increase in the collective allowance, which included estimated credit losses relating to the Alberta floods, while the first and third quarters of 2014 included a decrease in collective allowance, including partial reversal of the credit losses relating to the Alberta floods.

Non-interest expenses

Non-interest expenses have fluctuated over the period largely due to changes in employee-related compensation and benefits, including pension expense, as well as higher spending on strategic initiatives. The second quarter of 2014 had a goodwill impairment charge and the fourth quarter of 2013 had a restructuring charge relating to CIBC FirstCaribbean. The first half of 2014 and the fourth quarter of 2013 had expenses relating to the development of our enhanced travel rewards program, and to the Aeroplan transactions with Aimia and TD. The first quarter of 2013 also had higher expenses in the structured credit run-off business.

Income taxes

Income taxes vary with changes in income subject to tax, and the jurisdictions in which the income is earned. Taxes can also be affected by the impact of significant items, and the level of tax-exempt income. No tax recovery was booked in the second quarter of 2014 in respect of the CIBC FirstCaribbean goodwill impairment charge and loan losses.

Review of 2013 financial performance

| | | | | | | | | | | | | | | | | | | | | | |

| $ millions, for the year ended October 31 | | Retail and Business Banking | | | Wealth Management | | | Wholesale Banking (1) | | | Corporate and Other (1) | | | CIBC Total | |

2013 (2) | | Net interest income | | $ | 5,656 | | | $ | 186 | | | $ | 1,403 | | | $ | 208 | | | $ | 7,453 | |

| | Non-interest income | | | 2,155 | | | | 1,960 | | | | 832 | | | | 318 | | | | 5,265 | |

| | | Intersegment revenue | | | 338 | | | | (343 | ) | | | 5 | | | | – | | | | – | |

| | Total revenue | | | 8,149 | | | | 1,803 | | | | 2,240 | | | | 526 | | | | 12,718 | |

| | Provision for credit losses | | | 930 | | | | 1 | | | | 44 | | | | 146 | | | | 1,121 | |

| | | Non-interest expenses | | | 4,051 | | | | 1,301 | | | | 1,317 | | | | 952 | | | | 7,621 | |

| | Income (loss) before taxes | | | 3,168 | | | | 501 | | | | 879 | | | | (572 | ) | | | 3,976 | |

| | | Income taxes | | | 791 | | | | 116 | | | | 180 | | | | (461 | ) | | | 626 | |

| | | Net income (loss) | | $ | 2,377 | | | $ | 385 | | | $ | 699 | | | $ | (111 | ) | | $ | 3,350 | |

| | Net income (loss) attributable to: | | | | | | | | | | | | | | | | | | | | |

| | Non-controlling interests | | $ | – | | | $ | – | | | $ | – | | | $ | (2 | ) | | $ | (2 | ) |

| | | Equity shareholders | | | 2,377 | | | | 385 | | | | 699 | | | | (109 | ) | | | 3,352 | |

2012 (2) | | Net interest income | | $ | 5,518 | | | $ | 187 | | | $ | 1,113 | | | $ | 508 | | | $ | 7,326 | |

| | Non-interest income | | | 2,098 | | | | 1,783 | | | | 912 | | | | 366 | | | | 5,159 | |

| | | Intersegment revenue | | | 294 | | | | (296 | ) | | | 2 | | | | – | | | | – | |

| | Total revenue | | | 7,910 | | | | 1,674 | | | | 2,027 | | | | 874 | | | | 12,485 | |

| | Provision for credit losses | | | 1,080 | | | | – | | | | 142 | | | | 69 | | | | 1,291 | |

| | | Non-interest expenses | | | 3,950 | | | | 1,238 | | | | 1,109 | | | | 905 | | | | 7,202 | |

| | Income (loss) before taxes | | | 2,880 | | | | 436 | | | | 776 | | | | (100 | ) | | | 3,992 | |

| | | Income taxes | | | 724 | | | | 101 | | | | 187 | | | | (323 | ) | | | 689 | |

| | | Net income | | $ | 2,156 | | | $ | 335 | | | $ | 589 | | | $ | 223 | | | $ | 3,303 | |

| | Net income attributable to: | | | | | | | | | | | | | | | | | | | | |

| | Non-controlling interests | | $ | – | | | $ | – | | | $ | – | | | $ | 9 | | | $ | 9 | |

| | | Equity shareholders | | | 2,156 | | | | 335 | | | | 589 | | | | 214 | | | | 3,294 | |

| (1) | Wholesale Banking revenue and income taxes are reported on a TEB basis with an equivalent offset in the revenue and income taxes of Corporate and Other. |

| (2) | Certain information has been restated to reflect the changes in accounting policies stated in Note 1 to the consolidated financial statements and to conform to the presentation in the current year. |

| | | | |

| CIBC2014 ANNUAL REPORT | | | 11 | |

|

Management’s discussion and analysis |

The following discussion provides a comparison of our results of operations for the years ended October 31, 2013 and 2012.

Overview

Net income for 2013 was $3,350 million, compared with $3,303 million in 2012. The increase in net income of $47 million was due to higher revenue, a lower provision for credit losses, and lower income taxes, partially offset by higher non-interest expenses.

Revenue by segments

Retail and Business Banking

Revenue was up $239 million or 3% from 2012, primarily due to volume growth across most retail products, wider retail spreads and higher fees, partially offset by lower revenue from our exited FirstLine mortgage broker business.

Wealth Management

Revenue was up $129 million or 8% from 2012, primarily due to higher fee-based revenue in retail brokerage, higher assets under management, strong net sales of long-term mutual funds and higher contribution from our investment in ACI.

Wholesale Banking

Revenue was up $213 million or 11% from 2012, primarily due to higher revenue from corporate banking and investment portfolio gains within corporate and investment banking and higher capital markets revenue.

Corporate and Other

Revenue was down $348 million or 40% from 2012, mainly due to lower treasury revenue and a higher TEB adjustment.

Consolidated CIBC

Net interest income

Net interest income was up $127 million or 2% from 2012, primarily due to higher trading income, wider retail spreads, volume growth across most retail products and higher revenue from corporate banking, partially offset by lower treasury revenue.

Non-interest income

Non-interest income was up $106 million or 2% from 2012, primarily due to higher client assets under management driven by market appreciation and net sales of long-term mutual funds, and higher fees due to growth in our corporate lending business. This was partially offset by losses from our exited U.S. leveraged finance portfolio and higher losses on economic hedging activities.

Provision for credit losses

Provision for credit losses was down $170 million or 13% from 2012. In Retail and Business Banking, the provision was down due to lower write-offs and bankruptcies in the cards portfolio and lower losses in the personal lending portfolio, partially offset by a charge resulting from a revision of estimated loss parameters on our unsecured lending portfolios, shown as an item of note. In Wholesale Banking, the provision was down mainly due to lower losses in the U.S. real estate finance portfolio. 2012 included losses in the exited U.S. leveraged finance portfolio and 2013 included losses in the exited European leveraged finance portfolio, both shown as items of note. In Corporate and Other, the provision was up due to higher losses in CIBC FirstCaribbean. In addition, the collective allowance reported in this segment increased, which included $56 million of estimated credit losses relating to the Alberta floods, shown as an item of note. The increase in the collective allowance relating to the personal lending portfolio was largely offset by a decrease to the collective allowance relating to the commercial lending portfolio.

Non-interest expenses

Non-interest expenses increased by $419 million or 6% from 2012, primarily due to higher employee compensation and benefits which included a restructuring charge relating to CIBC FirstCaribbean, shown as an item of note, and higher expenses in the structured credit run-off business which included the Lehman-related settlement charge shown as an item of note.

Income taxes

Income tax expense was $626 million, compared with $689 million in 2012. This change was primarily due to higher tax-exempt income in 2013.

Outlook for calendar year 2015

Global growth is on track to be only marginally stronger in 2015, as an easing pace in China and recession risks in Russia, coupled with still sluggish gains in Europe, offset an expected acceleration in North America. The U.S. appears to be gathering momentum from improved credit access for households and the income gains associated with healthy job growth, which is expected to set the stage for nearly 3% real GDP growth in 2015. Canada’s growth rate should run in the 2.5% to 3.0% range, with exports lifted by improved U.S. demand and a weaker Canadian dollar, and federal tax cuts underpinning moderate growth in consumption, countering reduced activity in housing construction. The U.S. Federal Reserve is likely to begin lifting interest rates moderately in the first half of the year, with the Bank of Canada waiting until later in 2015 before following suit, given its higher starting point for rates, but long-term yields could rise early in the year in both countries in anticipation of that policy tightening.

Retail and Business Banking could see a moderation in already temperate growth in mortgage credit if house price inflation eases on rising mortgage rates, but non-auto consumer credit is unlikely to decelerate from its already modest pace. Demand for business credit should continue to grow at a healthy pace, with tighter capacity use and a more competitive exchange rate supporting business capital spending. A further drop in the unemployment rate and rising profits should support credit quality, but business and household insolvency rates are unlikely to dip from what are already very low levels.

Equity markets might see somewhat slower gains and moderating new issuance volumes after a strong 2014, but growing pools of household savings will support demand for wealth management.

Wholesale Banking should benefit as business capital spending picks up somewhat from very low levels, supporting the demand for corporate financing. Provincial governments will continue to have elevated financing needs, including those tied to ongoing infrastructure projects.

| | |

| 12 | | CIBC2014 ANNUAL REPORT |

|

Management’s discussion and analysis |

Non-GAAP measures

We use a number of financial measures to assess the performance of our business lines as described below. Some measures are calculated in accordance with GAAP (IFRS), while other measures do not have a standardized meaning under GAAP, and accordingly, these measures may not be comparable to similar measures used by other companies. Investors may find these non-GAAP measures useful in analyzing financial performance.

Adjusted measures

Management assesses results on a reported and adjusted basis and considers both as useful measures of performance. Adjusted results remove items of note from reported results and are used to calculate our adjusted measures noted below. Items of note include the results of our structured credit run-off business, the amortization of intangibles and certain items of significance that arise from time to time which management believes are not reflective of underlying business performance. We believe that adjusted measures provide the reader with a better understanding of how management assesses underlying business performance and facilitate a more informed analysis of trends. While we believe that adjusted measures may facilitate comparisons between our results and those of some of our Canadian peer banks which make similar adjustments in their public disclosure, it should be noted that there is no standardized meaning for adjusted measures under GAAP.

We also adjust our results to gross up tax-exempt revenue on certain securities to a TEB basis, being the amount of fully taxable revenue, which, were it to have incurred tax at the statutory income tax rate, would yield the same after-tax revenue.

Adjusted diluted EPS

We adjust our reported diluted EPS to remove the impact of items of note, net of taxes, and any other item specified in the table on the following page to calculate the adjusted EPS.

Adjusted efficiency ratio

We adjust our reported revenue and non-interest expenses to remove the impact of items of note and gross up tax-exempt revenue to bring it to a TEB basis, as applicable.

Adjusted dividend payout ratio

We adjust our reported net income attributable to common shareholders to remove the impact of items of note, net of taxes, to calculate the adjusted dividend payout ratio.

Adjusted return on common shareholders’ equity

We adjust our reported net income attributable to common shareholders to remove the impact of items of note, net of taxes, to calculate the adjusted ROE.

Adjusted effective tax rate

We adjust our reported income before income taxes and reported income taxes to remove the impact of items of note to calculate the adjusted effective tax rate.

Economic capital

Economic capital provides a framework to evaluate the returns of each SBU, commensurate with risk assumed. The economic capital measure is based upon an estimate of equity capital required by the businesses to absorb unexpected losses consistent with our targeted risk rating over a one-year horizon. Economic capital comprises primarily credit, market, operational and strategic risk capital. The difference between our total equity capital and economic capital is held in Corporate and Other.

There is no comparable GAAP measure for economic capital.

Economic profit

Net income attributable to equity shareholders, adjusted for a charge on economic capital, determines economic profit. This measures the return generated by each SBU in excess of our cost of capital, thus enabling users of our financial information to identify relative contributions to shareholder value.

Segmented return on equity

We use ROE on a segmented basis as one of the measures for performance evaluation and resource allocation decisions. While ROE for total CIBC provides a measure of return on common equity, ROE on a segmented basis provides a similar metric relating to the economic capital allocated to the segments. As a result, segmented ROE is a non-GAAP measure.

Managed loans and acceptances

Under Canadian GAAP, securitized loans were removed from the consolidated balance sheet upon sale. Loans on a managed basis included securitization inventory as well as loans and securities sold. We used this measure to evaluate the credit performance and the overall financial performance of the underlying loans.

| | | | |

| CIBC2014 ANNUAL REPORT | | | 13 | |

|

Management’s discussion and analysis |

The following table provides a reconciliation of non-GAAP to GAAP measures related to CIBC on a consolidated basis.

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | IFRS | | | | | Canadian GAAP | |

| $ millions, as at or for the year ended October 31 | | 2014 | | | 2013 (1) | | | 2012 (1) | | | 2011 | | | | | 2010 | |

Reported and adjusted diluted EPS | | | | | | | | | | | | | | | | | | | | | | | | |

Reported net income attributable to diluted common shareholders | | A | | $ | 3,131 | | | $ | 3,253 | | | $ | 3,136 | | | $ | 2,728 | | | | | $ | 2,283 | |

After-tax impact of items of note (2) | | | | | 442 | | | | 219 | | | | 88 | | | | 316 | | | | | | 200 | |

After-tax impact of items of note on non-controlling interests | | | | | (10 | ) | | | – | | | | – | | | | – | | | | | | – | |

Dividends on convertible preferred shares (3) | | | | | – | | | | – | | | | – | | | | (38 | ) | | | | | – | |