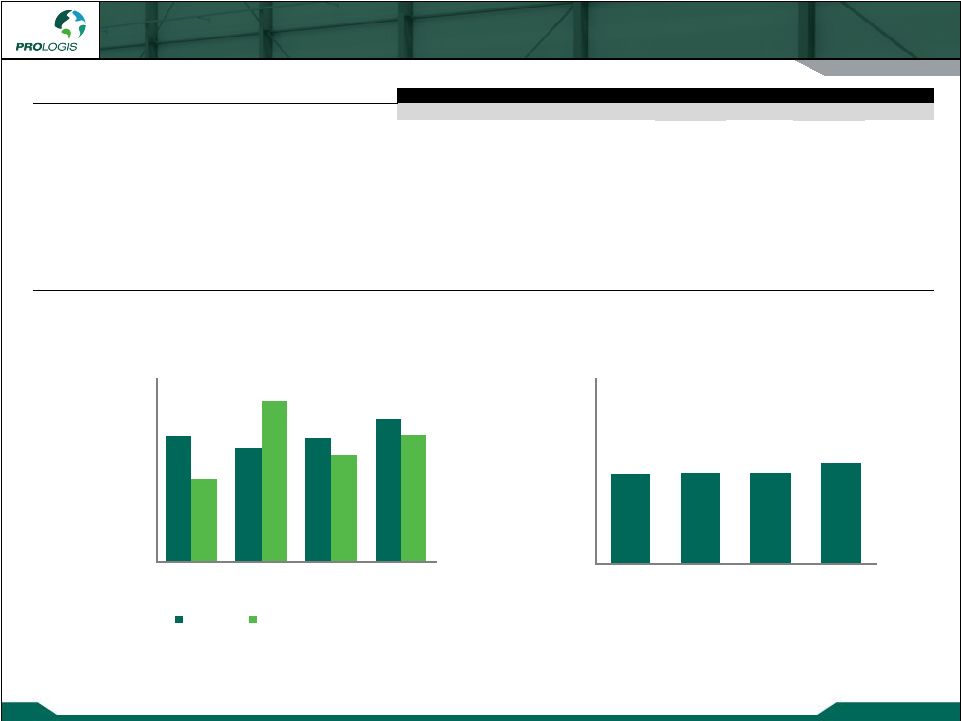

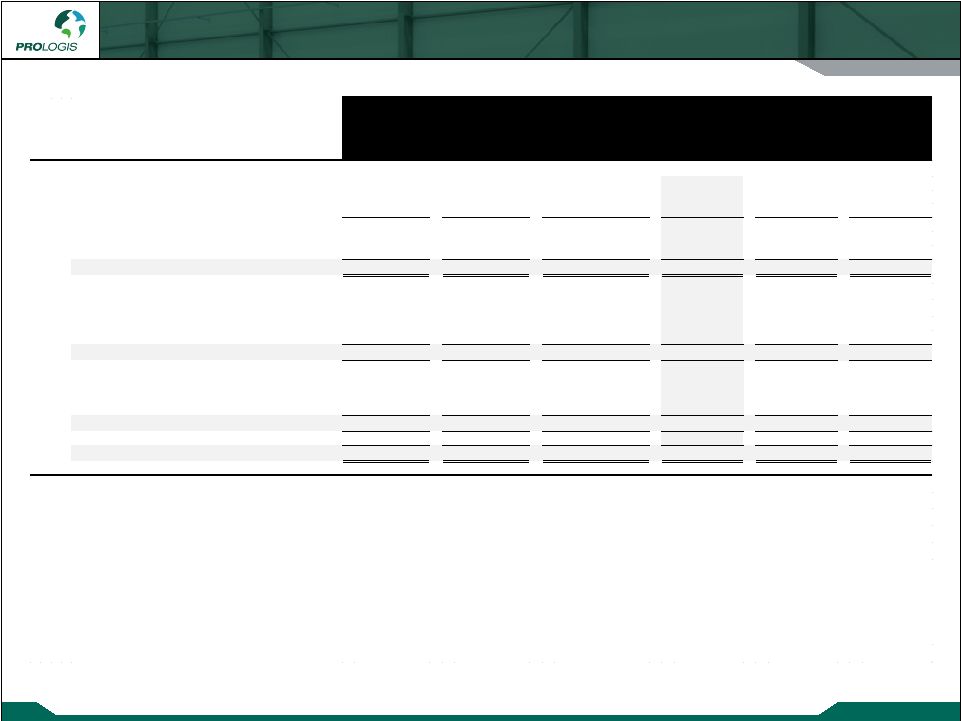

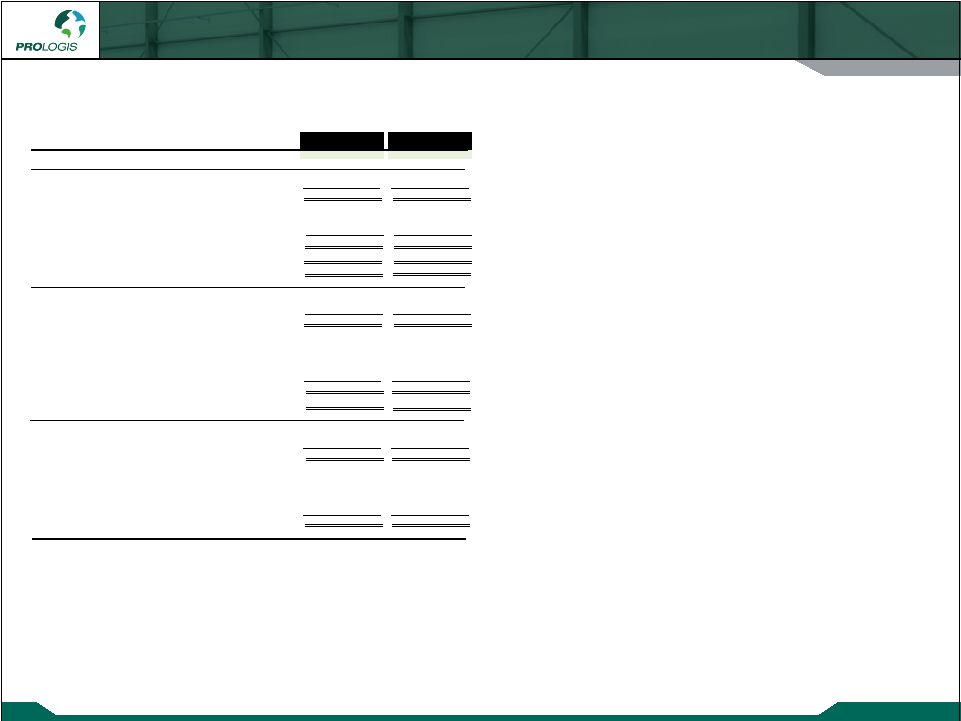

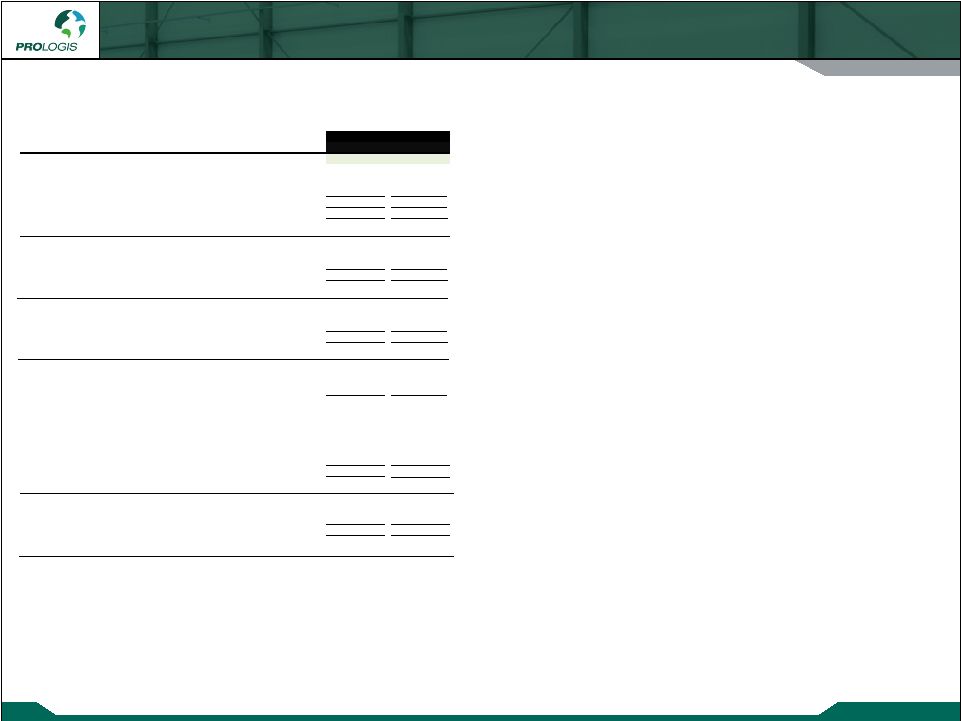

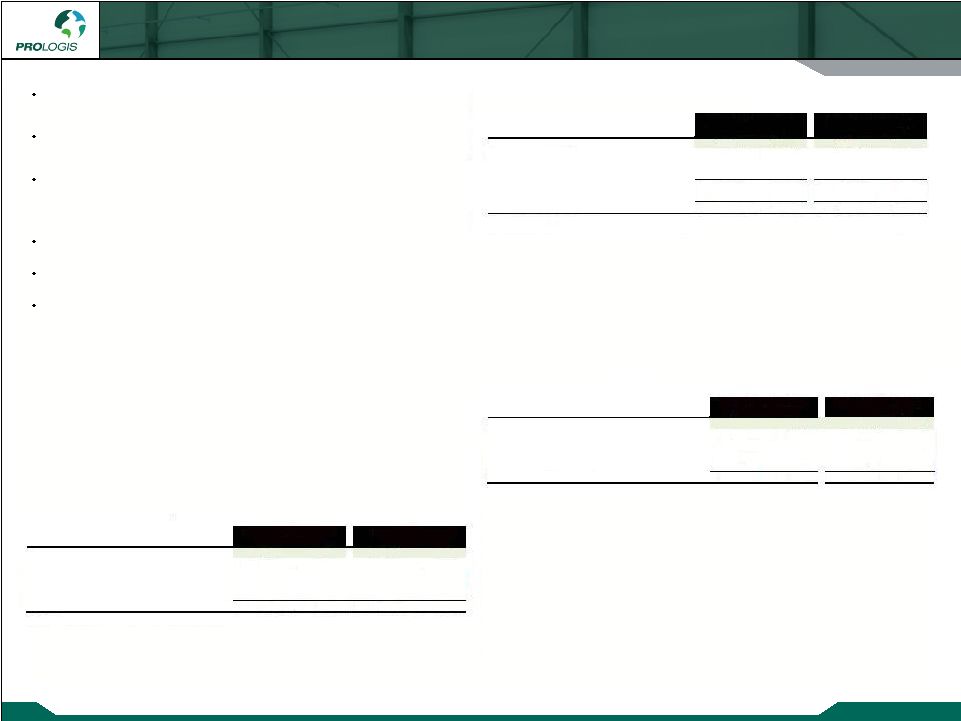

Copyright © 2012 Prologis Third Quarter 2012 Report Notes and Definitions 34 We use our FFO measures as supplemental financial measures of operating performance. We do not use our FFO measures as, nor should they be considered to be, alternatives to net earnings computed under GAAP, as indicators of our operating performance, as alternatives to cash from operating activities computed under GAAP or as indicators of our ability to fund our cash needs. FFO, as defined by Prologis To arrive at FFO, as defined by Prologis, we adjust the NAREIT defined FFO measure to exclude: (i) deferred income tax benefits and deferred income tax expenses recognized by our subsidiaries; (ii) current income tax expense related to acquired tax liabilities that were recorded as deferred tax liabilities in an acquisition, to the extent the expense is offset with a deferred income tax benefit in GAAP earnings that is excluded from our defined FFO measure; (iii) foreign currency exchange gains and losses resulting from debt transactions between us and our foreign consolidated subsidiaries and our foreign unconsolidated entities; (iv) foreign currency exchange gains and losses from the remeasurement (based on current foreign currency exchange rates) of certain third party debt of our foreign consolidated subsidiaries and our foreign unconsolidated entities; and (v) mark-to-market adjustments associated with derivative financial instruments. We calculate FFO, as defined by Prologis for our unconsolidated entities on the same basis as we calculate our FFO, as defined by Prologis. We believe investors are best served if the information that is made available to them allows them to align their analysis and evaluation of our operating results along the same lines that our management uses in planning and executing our business strategy. Core FFO In addition to FFO, as defined by Prologis, we also use Core FFO. To arrive at Core FFO, we adjust FFO, as defined by Prologis, to exclude the following recurring and non-recurring items that we recognized directly or our share recognized by our unconsolidated entities to the extent they are included in FFO, as defined by Prologis: (i) gains or losses from acquisition, contribution or sale of land or development properties; (ii) income tax expense related to the sale of investments in real estate; (iii) impairment charges recognized related to our investments in real estate (either directly or through our investments in unconsolidated entities) generally as a result of our change in intent to contribute or sell these properties; (iv) impairment charges of goodwill and other assets; (v) gains or losses from the early extinguishment of debt; (vi) merger, acquisition and other integration expenses; and (vii) expenses related to natural disasters We believe it is appropriate to further adjust our FFO, as defined by Prologis for certain recurring items as they were driven by transactional activity and factors relating to the financial and real estate markets, rather than factors specific to the on-going operating performance of our properties or investments. The impairment charges we recognized were primarily based on valuations of real estate, which had declined due to market conditions, that we no longer expected to hold for long-term investment. We currently have and have had over the past several years a stated priority to strengthen our financial position. We expect to accomplish this by reducing our debt, our investment in certain low yielding assets, such as land that we decide not to develop and our exposure to foreign currency exchange fluctuations. As a result, we have sold to third parties or contributed to unconsolidated entities real estate properties that, depending on market conditions, might result in a gain or loss. The impairment charges related to goodwill and other assets that we have recognized were similarly caused by the decline in the real estate markets. Also in connection with our stated priority to reduce debt and extend debt maturities, we have purchased portions of our debt securities. As a result, we recognized net gains or losses on the early extinguishment of certain debt due to the financial market conditions at that time. We have also adjusted for some non-recurring items. The merger, acquisition and other integration expenses include costs we incurred in 2011 and that we expect to incur in 2012 associated with the Merger and PEPR Acquisition and the integration of our systems and processes. We have not adjusted for the acquisition costs that we have incurred as a result of routine acquisitions but only the costs associated with significant business combinations that we would expect to be infrequent in nature. Similarly, the expenses related to the natural disaster in Japan that we recognized in 2011 are a rare occurrence but we may incur similar expenses again in the future. We analyze our operating performance primarily by the rental income of our real estate and the revenue driven by our private capital business, net of operating, administrative and financing expenses. This income stream is not directly impacted by fluctuations in the market value of our investments in real estate or debt securities. As a result, although these items have had a material impact on our operations and are reflected in our financial statements, the removal of the effects of these items allows us to better understand the core operating performance of our properties over the long-term. We use Core FFO, including by segment and region, to: (i) evaluate our performance and the performance of our properties in comparison to expected results and results of previous periods, relative to resource allocation decisions; (ii) evaluate the performance of our management; (iii) budget and forecast future results to assist in the allocation of resources; (iv) provide guidance to the financial markets to understand our expected operating performance; (v) assess our operating performance as compared to similar real estate companies and the industry in general; and (vi) evaluate how a specific potential investment will impact our future results. Because we make decisions with regard to our performance with a long-term outlook, we believe it is appropriate to remove the effects of items that we do not expect to affect the underlying long-term performance of the properties we own. As noted above, we believe the long-term performance of our properties is principally driven by rental income. We believe investors are best served if the information that is made available to them allows them to align their analysis and evaluation of our operating results along the same lines that our management uses in planning and executing our business strategy. AFFO To arrive at AFFO, we adjust Core FFO to further exclude; (i) straight-line rents; (ii) amortization of above- and below-market lease intangibles; (iii) recurring capital expenditures; (iv) amortization of management contracts; (v) amortization of debt premiums and discounts, net of amounts capitalized, and; (vi) stock compensation expense. We believe AFFO provides a meaningful indicator of our ability to fund cash needs, including cash distributions to our stockholders. Limitations on Use of our FFO Measures While we believe our defined FFO measures are important supplemental measures, neither NAREIT’s nor our measures of FFO should be used alone because they exclude significant economic components of net earnings computed under GAAP and are, therefore, limited as an analytical tool. Accordingly, they are two of many measures we use when analyzing our business. Some of these limitations are: The current income tax expenses that are excluded from our defined FFO measures represent the taxes that are payable. Depreciation and amortization of real estate assets are economic costs that are excluded from FFO. FFO is limited, as it does not reflect the cash requirements that may be necessary for future replacements of the real estate assets. Further, the amortization of capital expenditures and leasing costs necessary to maintain the operating performance of industrial properties are not reflected in FFO. |