UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

(MARK ONE) | ||||

o |

| Registration statement pursuant to Section 12(b) of the Securities Exchange Act of 1934 | ||

or |

|

|

| �� |

|

|

|

|

|

ý |

| Annual Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | ||

or |

| For the fiscal year ended: December 31, 2003 | ||

|

|

|

|

|

o |

| Transition Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | ||

|

| For the transition period from to |

|

|

|

|

|

|

|

Commission File Number: 333-07612 | ||||

BAYTEX ENERGY LTD.

(Exact name of Registrant as specified in its charter)

Alberta | 1311 | Not Applicable | ||

(Province or other jurisdiction of |

| (Primary standard industrial |

| (I.R.S. employer identification |

Suite 2200, 205 – 5th Avenue S.W. |

(Address and telephone number of registrant’s principle executive offices) |

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class: NONE

Securities registered or to be registered pursuant to Section 12(g) of the Act:

NONE

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

NONE

Indicate the number of outstanding shares of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

Common Shares: |

| 1 |

|

Exchangeable Shares |

| 3,724,649 |

|

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ý No o

Indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 ý Item 18 o

Contents |

|

|

|

| |

|

|

|

| ||

|

|

|

| ||

|

|

|

| ||

|

| |

|

| |

|

| |

|

| |

|

|

|

| ||

|

| |

|

| |

|

| |

|

| |

|

|

|

| ||

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

|

| ||

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

|

| ||

|

| |

|

| |

|

| |

|

|

|

| ||

|

| |

|

| |

|

|

|

| ||

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

2

| ||

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

|

| ||

|

|

|

| ||

|

|

|

|

| |

|

|

|

| ||

|

|

|

Material Modifications to the Rights of Security Holders and Use of Proceeds |

| |

|

|

|

| ||

|

|

|

| ||

|

|

|

| ||

|

|

|

| ||

|

|

|

| ||

|

|

|

| ||

|

|

|

Purchases of Equity Securities by the Issuer and Affiliated Purchases |

| |

|

|

|

PART III |

|

|

|

|

|

| ||

|

|

|

| ||

|

|

|

|

3

SPECIAL NOTE REGARDING FORWARD LOOKING STATEMENTS

Certain statements included or incorporated by reference in this annual report constitute “forward-looking statements” within the meaning of the United States Private Securities Legislation Act of 1995. Such forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by forward-looking statements. When used in this annual report or in documents incorporated by reference in this annual report, the words “believe,” “anticipate,” “estimate,” “project,” “intend,” “expect,” “may,” “will,” “plan,” “should,” “would,” “contemplate,” “possible,” “attempts,” “seeks” and similar expressions are intended to identify these forward-looking statements. These forward-looking statements were based on various factors and were derived utilizing numerous assumptions and other important factors that could cause actual results to differ materially from those in the forward-looking statements. Specific forward-looking statements contained in this annual report or in the documents incorporated by reference in this annual report include, among others, statements regarding:

• our expected financial performance in future periods;

• expected increases in revenues attributable to our exploration and production activities;

• our competitive advantages and ability to compete successfully;

• our intention to continue adding value through drilling;

• our plan to diversify our production mix by expanding our natural gas operations;

• our emphasis on having a low cost structure;

• our intention to match our exploration and development capital expenditures to our cash flow;

• our reserve estimates and our estimates of the present value of our future net cash flows;

• our methods of raising capital for exploration and development of reserves;

• the factors upon which we will decide whether or not to undertake an exploration or exploitation project;

• our plans to make acquisitions;

• our expectations regarding the exploration and production potential of our properties; and

With respect to forward-looking statements contained in this annual report or in the documents incorporated by reference in this annual report, we have made assumptions regarding, among other things:

• future oil and gas prices;

• the cost of expanding our property holdings;

• our ability to obtain equipment in a timely manner to meet our demand;

• our ability to market oil and gas successfully to current and new customers;

• the impact of increasing competition; and

• our ability to obtain financing on acceptable terms.

Some of the risks that could affect our future results and could cause results to differ materially from those expressed in our forward-looking statements include:

• the volatility of oil and gas prices, including the differential between the price of light and heavy oil;

• the uncertainty of estimates of oil and natural gas reserves;

• the impact of competition;

• difficulties encountered during the exploration for and production of oil and natural gas;

• the difficulties encountered in delivering oil and natural gas to commercial markets;

• changes in customer demand;

4

• any decrease in investor demand for trust units;

• foreign currency fluctuations;

• the uncertainty of our ability to attract capital;

• changes in, or the introduction of new, government regulations relating to the oil and natural gas business;

• costs associated with exploring for and producing oil and natural gas;

• compliance with environmental regulations;

• liabilities stemming from accidental damage to the environment;

• loss of the services of any of our executive officers; and

• adverse changes in the economy generally.

The information contained in this annual report and in the documents incorporated by reference in this annual report, including the information provided under the heading “Risk Factors,” identifies additional factors that could affect our operating results and performance. We urge you to carefully consider those factors.

All written or oral forward-looking statements attributable to us are expressly qualified in their entirety by the foregoing cautionary statement. You are cautioned not to rely on the forward-looking statements, which speak only as of the date of this annual report. We assume no obligation to update or to publicly announce the results of any revisions to any of the forward-looking statements to reflect actual results, future events or developments, changes in assumptions or changes in other factors affecting the forward-looking statements.

DEFINITIONS AND OTHER MATTERS

As used in this annual report, the following terms have the meaning indicated:

• “bbls” and “mbbls” mean barrels and thousand barrels, respectively;

• “mcf “, “mmcf” and “bcf” mean thousand cubic feet, million cubic feet and billion cubic feet, respectively;

• “boe” and “mboe” mean barrel of oil equivalent and thousand barrels of oil equivalent, respectively;

• “bbls/d”, “mcf/d” and “boe/d” mean barrels per day, thousand cubic feet per day and barrels of oil equivalent per day, respectively;

• “ngl” means natural gas liquids; and

Developed acreage means acreage on which we have a productive well. Undeveloped acreage means acreage on which we do not have a productive well and includes exploratory acreage. Proved reserves are those reserves estimated as recoverable under current technology and existing economic conditions under constant dollar economics, from that portion of a reservoir which can be reasonably evaluated as economically productive on the basis of analysis of drilling, geological, geophysical and engineering data, including the reserves to be obtained by enhanced recovery processes demonstrated to be economical and technically successful in the subject reservoir. Gross proved reserves or gross production are proved reserves or production attributable to our interest before deducting royalties; net proved reserves or net production are proved reserves or production after deducting royalties. Natural gas volumes are converted to barrels of oil equivalent using the ratio of 6 thousand cubic feet of natural gas to one barrel of oil. Natural gas volumes are stated at the official temperature and pressure bases of the area in which the reserves are located.

5

Item 1. Identity of Directors, Senior Management and Advisors

Not Applicable

Item 2. Offer Statistics and Expected Timetable

Not Applicable

Item 3. Key Information

A. Selected Financial Data

The financial data set forth below as at December 31, 2003 and 2002 and for each of the years in the three-year period ended December 31, 2003 have been derived from our audited consolidated financial statements included in Item 17 of this Form 20-F. Financial data at December 31, 2001, 2000 and 1999 and for each of the years in the three-year period ended December 31, 2000 have been derived from our previously published audited consolidated financial statements not included in this document.

The financial data as at December 31, 2003 and 2002 and for each of the years in the three-year period ended December 31, 2003 should be read in conjunction with, and are qualified in their entirety by reference to, our audited consolidated financial statements.

The financial data is derived from our financial statements which have been prepared in accordance with generally accepted accounting principles in Canada (“Canadian GAAP”), the application of which, in the case of Baytex Energy Ltd., conforms in all material respects for the periods presented with generally accepted accounting principles in the United States of America (“U.S. GAAP”), except as disclosed in footnotes to the consolidated financial statements.

The following table presents a summary of our consolidated statement of operations derived from our financial statements for 2003, 2002, 2001, 2000 and 1999. All data presented below should be read in conjunction with the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements and accompanying notes included elsewhere in this Form 20-F.

Amounts in accordance with Canadian GAAP

(in thousands of Canadian $, except per share data)

|

| December 31, |

| ||||||||

|

| 2003 |

| 2002 |

| 2001 |

| 2000 |

| 1999 |

|

Petroleum and natural gas sales |

| 351,404 |

| 365,860 |

| 329,700 |

| 286,226 |

| 120,087 |

|

Income (loss) from operations |

| 19,539 |

| 92,808 |

| (237,306 | ) | 75,797 |

| 25,231 |

|

Net income (loss) |

| 21,376 |

| 45,136 |

| (137,107 | ) | 43,788 |

| 14,128 |

|

Net income (loss) per common share: |

|

|

|

|

|

|

|

|

|

|

|

basic |

| 0.60 |

| 0.86 |

| (2.77 | ) | 1.04 |

| 0.40 |

|

Net income (loss) per common share: |

|

|

|

|

|

|

|

|

|

|

|

diluted |

| 0.60 |

| 0.85 |

| (2.77 | ) | 1.01 |

| 0.39 |

|

Total assets |

| 864,991 |

| 997,760 |

| 967,046 |

| 829,414 |

| 418,426 |

|

Share capital |

| — |

| 398,176 |

| 394,734 |

| 326,767 |

| 210,426 |

|

Shareholders’ equity |

| (288,546 | ) | 359,687 |

| 311,109 |

| 379,322 |

| 230,264 |

|

Number of shares outstanding |

| — |

| 52,819 |

| 52,008 |

| 45,797 |

| 35,469 |

|

Dividends declared |

| Nil |

| Nil |

| Nil |

| Nil |

| Nil |

|

6

Amounts in accordance with U.S. GAAP

(in thousands of Canadian $, except per share data)

|

| December 31, |

| ||||||||

|

| 2003 |

| 2002 |

| 2001 |

| 2000 |

| 1999 |

|

Petroleum and natural gas sales |

| 351,404 |

| 365,860 |

| 329,700 |

| 286,226 |

| 120,087 |

|

Net income (loss) |

| (26,154 | ) | 22,889 |

| (124,936 | ) | 52,175 |

| 30,348 |

|

Net income (loss) per common share: |

|

|

|

|

|

|

|

|

|

|

|

basic |

| (0.73 | ) | 0.44 |

| (2.52 | ) | 1.24 |

| 0.86 |

|

Net income (loss) per common share: |

|

|

|

|

|

|

|

|

|

|

|

diluted |

| (0.73 | ) | 0.43 |

| (2.52 | ) | 1.20 |

| 0.84 |

|

Total assets |

| 719,078 |

| 855,719 |

| 829,027 |

| 707,352 |

| 315,183 |

|

Share capital |

| — |

| 412,118 |

| 408,676 |

| 340,709 |

| 224,368 |

|

Shareholders’ equity |

| (437,518 | ) | 286,129 |

| 259,799 |

| 317,134 |

| 155,026 |

|

Number of shares outstanding |

| — |

| 52,819 |

| 52,008 |

| 45,797 |

| 35,469 |

|

Dividends declared |

| Nil |

| Nil |

| Nil |

| Nil |

| Nil |

|

Exchange Rate Information

We publish our consolidated financial statements in Canadian dollars. In this annual report, except where otherwise indicated, all dollar amounts are stated in Canadian dollars. References to “$” or “Cdn.$” are to Canadian dollars and references to “US$” are to U.S. dollars. The following table sets forth for each period indicated the period end exchange rates for conversion of U.S. dollars to Canadian dollars, the average exchange rates on the last day of each month during such period and the high and low exchange rates during such period. These rates are based on the noon buying rate in New York City, expressed in U.S. dollars, for cable transfers in Canadian dollars as certified for customs purposes by the Federal Reserve Bank of New York. The exchange rates are presented as Canadian dollars per $1.00. On May 31, 2004, the noon buying rate was US$1.00 equals Cdn. $1.3634 and the inverse noon buying rate was Cdn.$1.00 equals US$0.7335.

U.S. Dollar/Canadian Dollar Exchange Rates for Five Most Recent Financial Years

Year Ended December 31, |

| 2003 |

| 2002 |

| 2001 |

| 2000 |

| 1999 |

|

End of period |

| 0.7738 |

| 0.6344 |

| 0.6285 |

| 0.6669 |

| 0.6918 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Average for the period |

| 0.7139 |

| 0.6372 |

| 0.6456 |

| 0.6732 |

| 0.6691 |

|

7

U.S. Dollar/Canadian Exchange Rates for Previous Six Months

|

| December |

| January |

| February |

| March |

| April |

| May |

|

High |

| 0.7747 |

| 0.7883 |

| 0.7650 |

| 0.7659 |

| 0.7638 |

| 0.7335 |

|

Low |

| 0.7447 |

| 0.7481 |

| 0.7398 |

| 0.7357 |

| 0.7301 |

| 0.7159 |

|

B. Capitalization and Indebtedness

Not Applicable

C. Reasons for the Offer and Use of Proceeds

Not Applicable

D. Risk Factors

Set out below are certain risk factors that could materially adversely affect our business and our cash flow, operating results and financial condition.

Oil and natural gas prices are volatile, and low prices will adversely affect our business.

Fluctuations in the prices of oil and natural gas will affect many aspects of our business, including:

• our revenues, cash flows and earnings;

• our ability to attract capital to finance our operations;

• our cost of capital;

• the amount we are allowed to borrow under our senior credit facilities; and

• the value of our oil and natural gas properties.

Both oil and natural gas prices are extremely volatile. Any material decline in prices will result in a reduction of our net production revenue, overall value and the economics of producing from some wells. Any material decline in prices would likely also result in a reduction in our oil and natural gas acquisition and development activities.

In addition, a material decline in oil and natural gas prices from historical average prices would reduce our borrowing base under our senior credit facilities, therefore reducing amounts available to us and possibly requiring that a portion of our senior credit facilities be repaid.

You should not unduly rely on reserve information because reserve information represents estimates and our actual reserves could be lower than the estimates.

Estimates of oil and natural gas reserves involve a great deal of uncertainty, because they depend in large part upon the reliability of available geologic and engineering data, which is inherently imprecise. Geologic and engineering data are used to determine the probability that a reservoir of oil and natural gas exists at a particular location, and whether oil and natural gas are recoverable from a reservoir.

The probability of the existence and recoverability of reserves is less than 100% and actual recoveries of proved reserves usually differ from estimates.

8

Estimates of oil and natural gas reserves also require numerous assumptions relating to operating conditions and economic factors, including, among others:

• the price at which recovered oil and natural gas can be sold;

• the costs associated with recovering oil and natural gas;

• the prevailing environmental conditions associated with drilling and production sites;

• the availability of enhanced recovery techniques;

• the ability to transport oil and natural gas to markets; and

• governmental and other regulatory factors, such as taxes and environmental laws.

A change in any one or more of these factors could result in known quantities of oil and natural gas previously estimated as proved reserves becoming unrecoverable and the present value of future net cash flows from estimated reserves being reduced.

In addition, estimates of reserves and future net cash flows expected from them prepared by different independent engineers or by the same engineers at different times, may vary substantially.

In addition, in accordance with Canadian GAAP, we could be required to write down the carrying value of our oil and natural gas properties if oil and natural gas prices become depressed for even a short period of time, or if there are substantial downward revisions to our quantities of proved reserves. A write down would result in a charge to earnings and a reduction of shareholders’ equity.

Our heavy oil production increases our susceptibility to low oil prices, because the price we receive for heavy oil is lower than for light oil.

The price we receive for heavy oil is lower than for light oil. In addition, seasonal fluctuation in demand for heavy oil affects the price differential between light and heavy oil. One of the main by-products from refining heavy oil is asphalt that is used in road paving. In general, municipal, state and provincial governments, particularly in Canada and the northern states of the United States, expend the majority of their budgets for road infrastructure improvements during the spring and summer months. Thus, the demand from the refineries to process heavy oil is the strongest during this period, which usually leads to higher prices for heavy oil in the spring and summer months. The effect of an increase in the price differential between light and heavy oil could adversely affect the profitability of heavy oil compared to light oil.

If we are unsuccessful in acquiring and developing oil and gas properties, we will be prevented from increasing our reserves and our business will be adversely affected because we will eventually run out of reserves.

The successful acquisition and development of oil and gas properties requires an assessment of:

• recoverable reserves;

• future oil and gas prices and operating costs;

• potential environmental and other liabilities; and

• productivity of new wells drilled.

These assessments are inexact and if they are made too inaccurately, we will not recover the purchase price of a property from the sale of production from the property, or will not recognize an acceptable return from properties we acquire.

In addition, the costs of exploitation and development could materially exceed initial estimates.

9

We will not be able to develop our reserves or make acquisitions if we are unable to generate sufficient cash flow or raise capital. If we are unable to increase our reserves, our business will be adversely affected because we will eventually run out of reserves.

We will be required to make substantial capital expenditures to develop our existing reserves, to discover new oil and gas reserves and to make acquisitions. We will be unable to accomplish these tasks if we are unable to generate sufficient cash flow or raise capital in the future.

Drilling activities are subject to many risks and any interruption or lack of success in our drilling activity will adversely affect our business because drilling is expensive and a lack of success will prevent us from increasing our reserves.

Drilling activities are subject to many risks, including the risk that no commercially productive and profitable reservoirs will be encountered and that we will not recover all or any portion of our investment. The cost of drilling, completing and operating wells is often uncertain. Our drilling operations could be curtailed, delayed or cancelled as a result of numerous factors, many of which are beyond our control, including:

• adverse weather conditions;

• compliance with governmental requirements; and

• shortages or delays in the delivery of equipment and services.

Our operations are affected by operating hazards and uninsured risks and a shutdown or slowdown of our operations will adversely affect our business.

There are many operating hazards in exploring for and producing oil and natural gas, including:

• our drilling operations could encounter unexpected formations or pressures that could cause damage to equipment or personal injury;

• we could experience blowouts, accidents, oil spills, fires or other damage to a well that could require us to redrill it or take other corrective action;

• we could experience equipment failure that curtails or stops production;

• our drilling and production operations, such as trucking of oil, are often interrupted by bad weather; and

• we would be unable to access our properties or conduct our operations due to surface conditions.

Any of these events could result in damage to or destruction of oil and natural gas wells, production facilities or other property, or injury to persons. In addition, any of the above events could result in environmental damage or personal injury for which we will be liable.

The occurrence of a significant event not fully insured or indemnified against could seriously harm our financial condition and operating results.

Our hedging activities could result in losses.

The nature of our operations results in exposure to fluctuations in commodity prices. We monitor and, when appropriate, utilize derivative financial instruments and physical delivery contracts to hedge our exposure to these risks. We are exposed to credit-related losses in the event of non-performance by counter-parties to the financial instruments. From time to time we enter into hedging activities in an effort to mitigate the potential impact of declines in oil and natural gas prices. You should also refer to Item 5 of this annual report entitled “Risk and Risk Management”.

If product prices increase above those levels specified in our various hedging agreements, the fixed price will limit us from receiving the full benefit of commodity price increases.

10

In addition, by entering into these hedging activities, we will suffer financial loss if:

• we are unable to produce oil or natural gas to fulfill our obligations;

• we are required to pay a margin call on a hedge contract; or

• we are required to pay royalties based on a market or reference price that is higher than our fixed or ceiling price.

In 2003, we incurred $33.8 million in losses due to hedging. In 2002, we incurred $8.3 million in losses due to hedging.

Complying with environmental and other government regulations could be costly and could negatively impact our production.

Our operations are governed by numerous Canadian laws and regulations at the provincial and federal level. These laws and regulations govern the operation and maintenance of our facilities, the discharge of materials into the environment and other environmental protection issues.

Under these laws and regulations, we could be liable for personal injury, clean-up costs, remedial measures and other environmental and property damages, as well as administrative, civil and criminal penalties. We do not believe that insurance coverage for the full potential liability of environmental damages is available at a reasonable cost, so we could be liable, or could be required to cease production on properties, if environmental damage occurs.

It is possible that the costs of complying with environmental laws and regulations in the future will have a material adverse effect on our financial condition or results of operations. Furthermore, future changes in environmental laws and regulations could result in materially increased costs for us, stricter standards and enforcement, larger fines and liability, and increased capital expenditures and operating costs, any of which could have a material adverse effect on our financial condition or results of operations.

Certain factors beyond our control can affect our ability to market production. Since we cannot fully protect ourselves from these factors, the impact of them, if serious, could adversely affect our business.

Our ability to market oil and gas from our wells depends upon numerous factors beyond our control. These factors include:

• the availability of capacity to refine heavy oil;

• the availability of natural gas processing capacity;

• the availability of pipeline capacity;

• the supply of and demand for oil and natural gas;

• the availability of alternative fuel sources;

• the availability of diluent to blend with heavy oil to enable transportation;

• the effects of inclement weather;

• Canadian federal and provincial regulation of oil and natural gas marketing; and

• Canadian federal regulation of natural gas sold or transported outside of the province of Alberta.

Because of these factors, we could be unable to market all of the oil or gas we produce. In addition, we could be unable to obtain favorable prices for the oil and gas we produce.

The oil and natural gas industry is highly competitive.

We compete for capital, acquisitions of reserves, undeveloped lands, skilled personnel, access to drilling rigs, service rigs and other equipment, access to processing facilities, pipeline and refining capacity and in many other respects with a substantial number of other organizations, many of which may have greater technical and

11

financial resources than we do. Some of these organizations not only explore for, develop and produce oil and natural gas but also carry on refining operations and market oil and other products on a worldwide basis. As a result of these complementary activities, some of our competitors may have greater and more diverse competitive resources to draw on than we do. Given the highly competitive nature of the oil and natural gas industry, this could adversely affect the market price of our trust units and distributions to unitholders.

Our current credit facilities and any replacement credit facilities may not provide sufficient liquidity.

Baytex has credit facilities in the amount of $165 million. Variations in interest rates and scheduled principal payments could result in significant changes in the amount required to be applied to debt service before payment of any amounts to the Trust. Although it is believed that the bank line of credit is sufficient, there can be no assurance that the amount will be adequate for the financial obligations of Baytex or that additional funds can be obtained.

The industry in which we operate exposes us to potential liabilities that may not be covered by insurance.

Our operations are subject to all of the risks associated with the operation and development of oil and natural gas properties, including the drilling of oil and natural gas wells, and the production and transportation of oil and natural gas. These risks include encountering unexpected formations or pressures, premature declines of reservoirs, blow-outs, equipment failures and other accidents, cratering, sour gas releases, uncontrollable flows of oil, natural gas or well fluids, adverse weather conditions, pollution, other environmental risks, fires and spills. A number of these risks could result in personal injury, loss of life, or environmental and other damage to our property or the property of others. We cannot fully protect against all of these risks, nor are all of these risks insurable. We may become liable for damages arising from these events against which we cannot insure or against which we may elect not to insure because of high premium costs or other reasons. Any costs incurred to repair these damages or pay these liabilities would reduce funds available for distribution to unitholders.

The operation of oil and natural gas wells could subject us to environmental claims and liability.

The oil and natural gas industry is subject to extensive environmental regulation pursuant to local, provincial and federal legislation. A breach of that legislation may result in the imposition of fines or the issuance of “clean up” orders. Legislation regulating the oil and natural gas industry may be changed to impose higher standards and potentially more costly obligations. For example, the 1997 Kyoto Protocol to the United Nation’s Framework Convention on Climate Change, known as the Kyoto Protocol, was ratified by the Canadian government in December, 2002 and will require, among other things, significant reductions in greenhouse gases. The impact of the Kyoto Protocol on us is uncertain and may result in significant additional costs (future) for our operations. Although we record a provision in our financial statements relating to our estimated future environmental and reclamation obligations, we cannot guarantee that we will be able to satisfy our actual future environmental and reclamation obligations.

We are not fully insured against certain environmental risks, either because such insurance is not available or because of high premium costs. In particular, insurance against risks from environmental pollution occurring over time (as opposed to sudden and catastrophic damages) is not available on economically reasonable terms.

Accordingly, our properties may be subject to liability due to hazards that cannot be insured against, or that have not been insured against due to prohibitive premium costs or for other reasons. Any site reclamation or abandonment costs actually incurred in the ordinary course of business in a specific period will be funded out of cash flow and, therefore, will reduce the amounts available for distribution to unitholders. Should we be unable to fully fund the cost of remedying an environmental problem, we might be required to suspend operations or enter into interim compliance measures pending completion of the required remedy.

12

We may undertake acquisitions that could limit our ability to manage and maintain our business, result in adverse accounting treatment and are difficult to integrate into our business. Any of these events could result in a material change in our liquidity, impair our ability to pay dividends and could adversely affect the value of your investment.

A component of future growth will depend on the ability to identify, negotiate, and acquire additional companies and assets that complement or expand existing operations. However we may be unable to complete any acquisitions, or any acquisitions we may complete may not enhance our business. Any acquisitions could subject us to a number of risks, including:

• diversion of management’s attention;

• inability to retain the management, key personnel and other employees of the acquired business;

• inability to establish uniform standards, controls, procedures and policies;

• inability to retain the acquired company’s customers;

• exposure to legal claims for activities of the acquired business prior to acquisition; and inability to integrate the acquired company and its employees into our organization effectively.

Since we are a Canadian company and all of our assets and key personnel are located in Canada, you may not be able to enforce a U.S. judgment for claims you may bring against us, our assets, our key personnel or many of the experts named in this annual report. This may prevent you from receiving compensation to which you would otherwise be entitled.

We have been organized under the laws of Alberta, Canada and all of our assets are located outside the U.S. In addition, the members of our Board of Directors and our officers are residents of countries other than the U.S. As a result, it may be impossible for you to effect service of process upon us or these individuals within the U.S. or to enforce any judgments in civil and commercial matters, including judgments under U.S. federal securities laws. In addition, a Canadian court may not permit you to bring an original action in Canada or to enforce in Canada a judgment of a U.S. court based upon civil liability provisions of the U.S. federal securities laws.

Item 4. Information on the Company

A. History and Development of the Company

The head office of Baytex Energy Ltd. (“Baytex” or the “Company”) is located at Suite 2200, 205 - 5th Avenue S.W., Calgary, Alberta, T2P 2V7, telephone (403) 269-4828 and its registered office is located at Suite 1400, 350 – 7th Avenue S.W., Calgary, Alberta T2P 3N9, telephone (403) 260-0100.

Baytex was incorporated in Canada under the Business Corporations Act (Alberta) on June 3, 1993. On August 5, 1993, Baytex filed Articles of Amendment to delete the private company restrictions thereunder. On October 13, 1993, Articles of Amendment were filed to amend Baytex’s capital structure to create Class A Shares and Class B Non-Voting Shares. On October 21, 1997, Baytex filed Articles of Amalgamation to amalgamate with its wholly-owned subsidiary, Dorset Exploration Ltd. On May 28, 1999, Baytex filed Articles of Amendment to eliminate the Class B Shares and to change the designation of the Class A Shares in the share capital of Baytex from “Class A Shares” to “common shares”.

In May 2001, Baytex acquired all of the issued and outstanding shares of OGY Petroleums Ltd. (“OGY”), a public oil and gas company, the shares of which were listed on the TSX. The total consideration paid by Baytex for OGY was $50.7 million in cash and 1.2 million Baytex common shares. The operations of OGY concentrated on light oil and natural gas in central Alberta.

13

Also in May 2001, Baytex acquired all of the issued and outstanding shares of Triumph Energy Corporation (“Triumph”), a public oil and gas company, the shares of which were listed on the TSX. The total consideration paid for Triumph was $82.3 million in cash and 4.9 million Baytex common shares. The operations of Triumph were focused on the exploration and development of natural gas in Central Alberta and light oil and natural gas in East Central and Southern Alberta.

On January 1, 2002, Baytex filed Articles of Amalgamation to amalgamate with its wholly-owned subsidiaries, OGY and Triumph.

Additional heavy oil assets were acquired in the Cold Lake, Alberta and Carruthers, Saskatchewan areas in three separate property acquisitions in 2001 and 2002 for total cash consideration of $73.4 million.

In the fourth quarter of 2001 and first quarter of 2002, Baytex executed a plan to strengthen its balance sheet with the divestiture of certain oil and natural gas assets. This plan included the sale of light oil and natural gas assets for total proceeds of $101 million. This was later augmented in the first quarter of 2003 with the completion of the sale of natural gas assets in the Ferrier/O’Chiese area for proceeds of $133.3 million. Proceeds of the asset sales were applied to reduce outstanding indebtedness.

On September 2, 2003, Baytex completed a Plan of Arrangement (the “Arrangement”) whereby holders of common shares of Baytex elected or were deemed to have elected to receive either trust units (the “Trust Units”) of Baytex Energy Trust (the “Trust”) or exchangeable shares of Baytex (the “Exchangeable Shares”) for their common shares on the basis of one Trust Unit or Exchangeable Share, respectively, for each common share held. Coincident with the Arrangement becoming effective, certain of Baytex’s exploration assets were acquired by Crew Energy Inc. (“Crew”), and the common shares of Crew were distributed to the former holders of Baytex common shares on the basis of one-third of a common share of Crew for each such share held. The estimated fair market value at September 2, 2003 of the securities issued during the reorganization was $11.76 per Trust Unit and $0.55 per one-third of a common share of Crew.

On September 2, 2003, Baytex was amalgamated with Baytex Acquisition Corp. pursuant to the Arrangement.

We are an intermediate oil and gas company engaged in the exploration, development and production of oil and natural gas. We operate substantially all of our production in two core project areas in the provinces of Alberta and Saskatchewan, Canada. We have acquired our land holdings through government land sales, freehold acquisitions, drilling on farm-in lands and property and corporate acquisitions. We focus on building our asset base through land assembly, acquisitions of seismic data and exploratory and development drilling. Our drilling efforts are concentrated on properties that we believe will provide long lived reserves that will generate cash flow in the near term. We continually look for opportunities to enhance our position in our core areas and intend to pursue strategic acquisitions that are within the operating and financial parameters that we have established. See also Item 4 “Property, Plants and Equipment”.

The Trust is the holder of the common share of Baytex. Certain former shareholders of Baytex own Exchangeable Shares in accordance with the elections made by such shareholders under the Arrangement. Baytex continues to carry on an oil and natural gas business similar to that carried on by Baytex prior to the Arrangement becoming effective. Baytex owns, directly or indirectly, all of the assets that were owned by Baytex prior to the Arrangement becoming effective, other than certain oil and gas and exploration assets that were transferred to Crew in accordance with the Arrangement.

14

Inter-Corporate Relationships

The following table provides the name, the percentage of voting securities owned by Baytex and the jurisdiction of incorporation, continuance or formation of these subsidiaries either, direct and indirect, as at the date hereof.

|

| Percentage of voting securities |

| Jurisdiction of |

|

Baytex Energy (USA) Inc. |

| 100 | % | Delaware |

|

Baytex Marketing Ltd. |

| 100 | % | Alberta |

|

D. Property, Plants and Equipment

The following is a description of Baytex’s principal oil and natural gas properties on production or under development as at January 1, 2004. The term “net”, when used to describe Baytex’s share of production, means the total of Baytex’s working interest share before deduction of royalties owned by others. Reserve amounts are stated, before deduction of royalties, at January 1, 2004, based on forecast cost and price assumptions (gross) as evaluated in the independent reserve evaluators (see “ Reserves and Present Value Summary”). Unless otherwise specified, gross and net acres and well count information are as at January 1, 2004. Information in respect of current production is average production, net to Baytex, for the year ended December 31, 2003, except where otherwise indicated. Information related to land holdings is at December 31, 2003.

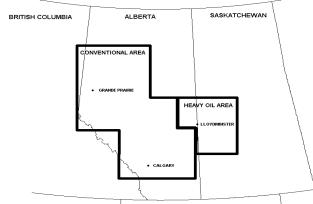

The crude oil and natural gas properties in which Baytex has an interest are within two districts in Alberta and Saskatchewan. Each district constitutes a well-balanced portfolio of operated properties and development prospects with considerable upside potential.

15

Heavy Oil District

The Heavy Oil District accounts for approximately two-thirds of Baytex’s current production and approximately three-quarters of reserves. Heavy oil operations consist largely of cold conventional production from wells with multi-zone potential. Production is generated primarily from vertical, slant and horizontal wells using progressive cavity pump technology to generate large volumes of heavy oil combined with gas, water and sand. Production from these wells usually averages between 40 and 100 Bbls/d of low gravity crude ranging from 11 to 18 API. Once produced, the oil is trucked or pipelined to markets in both Canada and the United States for upgrading into lighter grades of crude or refined into petroleum products such as fuel oil, lubricants and asphalt.

During 2003, production in the Heavy Oil District averaged 25,676 Boe/d made up of 23,911 Bbls/d of heavy oil and 10.6 Mmcf/d of natural gas. Baytex drilled 174 gross (165.2 net) wells in the district, resulting in 159 gross (150.2 net) oil wells, four gas wells, four service wells, and seven dry and abandoned wells for a success rate of 96 percent.

Baytex possesses a vast inventory of development projects in the west central Saskatchewan heavy oil region and the Cold Lake, Ardmore and Seal areas of north central Alberta. The ability to generate replacement production through conventional drilling methods allows Baytex to better control the cost and timing of its capital investments.

Baytex will continue to build value through internal property development and selective acquisitions. Future heavy oil activity will focus on the development of the Seal and Ardmore Properties along with continued infill drilling at adjacent Cold Lake and throughout the Saskatchewan Properties.

Ardmore: Ardmore is one of the key heavy oil development and production areas for Baytex. Acquired in 2002, this year-round access area generated approximately 3,100 Bbls/d of oil in 2003, with current production in excess of 4,500 Bbls/d. Since acquiring this property, Baytex has applied leading-edge heavy oil drilling and production technology to improve production and reduce cost. Wells in the area are 100 percent owned and operated by Baytex and they are able to produce up to 300 Bbls/d of 11 to 13 API heavy crude oil primarily from the McLaren and Sparky formations. Baytex drilled 48 gross (47.6 net) oil wells in the area during 2003, resulting in 47 gross (46.6 net) oil wells and one service well. Baytex holds approximately 32,000 net acres of 100 percent working interest undeveloped land in this area.

Cold Lake: Baytex acquired the Cold Lake heavy oil property in 2001. This year-round drilling area is located on Cold Lake First Nations Land with heavy oil production generated largely from the Colony formation. Average production was 935 Bbls/d during 2003. Baytex drilled 15 gross (13.5 net) operated oil wells in the Cold Lake area during 2003 and holds 19,500 net acres of undeveloped land.

16

Seal: The Seal property is a highly prospective heavy oil area for Baytex. The property is located in the Peace River oilsands area of northwest Alberta. Baytex holds 100 percent working interests in approximately 58 sections of land of which 44 sections were acquired in 2003. The Seal oil deposits can be produced through horizontal wells using primary production technology without the use of capital intensive steam injection methods. Baytex completed a seven-well test program during the first quarter of 2004. A development plan for a pilot production is being designed for the second half of 2004 and the winter of 2005.

Tangleflags: Baytex acquired the Tangleflags property through the acquisition of Bellator Exploration Inc. in 2000. Tangleflags is characterized by multiple-zone reservoirs with production from the Colony, McLaren, Waseca, Sparky, General Petroleum and Lloydminster formations. Provincial government regulations generally prohibit production from more than one formation at a time. As such, this property possesses long-term development potential with a considerable number of up-hole completion opportunities. Average production during 2003 was 4,940 Bbls/d of heavy oil and 1.6 Mmcf/d of natural gas.

Carruthers: The Carruthers property was obtained by Baytex in 1997 through the merger with Dorset Exploration Ltd. The property consists of two separate pools in the Cummings formation. During 2003, average production was 3,300 Bbls/d of heavy oil and 0.6 Mmcf/d of natural gas. Baytex drilled 35 gross (29.75 net) oil wells in the Carruthers area during 2003, resulting in 33 gross (27.75 net) oil wells and 2 dry holes for an overall drilling success rate of 94 percent. Baytex has continued to develop the southern pool since 1999, with 15 to 20 locations planned for 2004.

Marsden/Silverdale: The Marsden/Silverdale area of Saskatchewan is characterized by quality oil of 13 to 18 API and production averaging 100 Bbls/d per well. The lighter gravity oil allows production to be flow-lined to treating and disposal facilities thereby reducing trucking costs. Lower trucking costs, combined with characteristically low sand production, result in lower overall operating costs. Production averaged 3,400 Bbls/d of oil and 1.1 Mmcf/d of natural gas during 2003. Baytex drilled 9 oil wells in the area during 2003, with 100 percent success. Baytex has approximately 12,000 net acres of undeveloped land in the Marsden/Silverdale area.

Conventional Oil and Gas District

The Conventional Oil and Gas District includes Properties located in Alberta producing light and medium gravity crude oil, natural gas and related liquids. Production in this district averaged 11,010 Boe/d for the year ended December 31, 2003, consisting of 2,273 Bbls/d of oil and natural gas liquids and 52.4 Mmcf/d of natural gas.

Excluding production from the Ferrier area, which was sold in March 2003, and production from the properties which were transferred to Crew pursuant to the Arrangement, production in this district averaged 1,860 Bbls/d of oil and natural gas liquids and 45.2 Mmcf/d of natural gas, or 9,400 Boe/d during 2003.

Leahurst: Baytex began operations in the Leahurst area in 1993. Production in the area is primarily natural gas from the Belly River and lower Mannville formations. Baytex holds approximately 19,000 net acres of land in the area, interests in two gas plants and a 100-km gathering system. In 2003, Baytex drilled 7.8 net successful natural gas wells. The Leahurst area has year-round access, which allows Baytex to conduct continuous development activities. Baytex’s average production for 2003 was 7.3 Mmcf/d of natural gas in this area.

Red Earth/Goodfish: Baytex commenced operations in this area through the merger with Dorset Exploration Ltd. in 1997. Production includes light oil from the Slave Point and Granite Wash formations and natural gas from the Bluesky formation. In 2003, Baytex drilled 10.2 net wells in the area resulting in 5 net oil wells and 5

17

net natural gas wells. Baytex holds approximately 58,000 net acres of undeveloped land in this area. Baytex’s average production in 2003 was 1,000 Bbls/d of light oil and 9.8 Mmcf/d of natural gas.

Nina/Darwin: Baytex began operations in the Darwin area in 1998, targeting natural gas from the Bluesky formation. Production from Nina commenced in March 2001. Baytex holds approximately 34,000 net acres of land in the area. Average production in this area in 2003 was 4.9 Mmcf/d of natural gas.

Bon Accord: The Bon Accord natural gas property was acquired by Baytex in 1997 through the merger with Dorset Exploration Ltd. Baytex utilizes 3-D seismic technology to identify gas-producing zones in the Mannville, Nisku and Sparky formations. Baytex drilled 8 wells in the Bon Accord area during 2003, resulting in 5 natural gas wells and 1 oil well. Average production was 8.4 Mmcf/d of natural gas and 360 Bbls/d of oil and natural gas liquids. Baytex has approximately 13,000 net acres of land in this area.

Hamburg/Chinchaga: Baytex constructed a natural gas processing plant in this area during 2003 with processing capacity of 8.0 Mmcf/d. Baytex’s production in the area averaged approximately 5 Mmcf/d during 2003, leaving approximately 3 Mmcf/d of plant capacity for third-party processing which is expected to be filled by the end of the first quarter of 2004. Baytex has had success targeting natural gas in the Slave Point, Bluesky and Gilwood formations. Drilling activity in 2003 resulted in two successful natural gas wells. Net landholdings in the area total 17,500 acres as at December 31, 2003.

Reserves and Present Value Summary

Baytex is required to comply with the National Instrument 51-101, (“NI 51-101”) issued by the Canadian Securities Administrators, in all its reserves related disclosures. NI 51-101 came into effect on September 30, 2003 and is applicable for financial years ended on or after December 31, 2003. The purpose of NI 51-101 is to enhance the quality, consistency, timeliness and comparability of oil and gas activities by reporting issuers and elevate reserves reporting to a higher level of accountability. NI 51-101 brought about significant changes in which Canadian reporting issuers manage and publicly disclose information relating to their oil and gas reserves, mandates annual disclosure requirements and prescribes new reserve definitions as follows:

NI 51-101 requires a higher degree of confidence in the assignment of oil and gas reserves. Under NI 51-101, proved reserves are defined to have a 90% probability that the actual reserves recovered will equal or exceed the assigned estimates compared to the previous definition of “reasonable certainty” as stipulated by National Policy 2-B (“NP 2-B”). Also, under NI 51-101, probable reserves are defined to have a 50% probability that the actual reserves recovered will equal or exceed the assigned estimates compared to the previous definition of “likelihood of existence” in NP 2-B. Because of the more stringent requirements under NI 51-101, the industry has adopted the interpretation that the new proved plus probable (P-50) reserves represent the most “realistic” estimates of remaining recoverable reserves. The following reserves information also adopts the general industry practice of comparing the new P-50 reserves to the previous proved plus risk adjusted (50%) probable reserves, commonly referred to as “established reserves”, under NP 2-B.

In the United States, registrants [other than foreign private issuers] are required to disclose reserves using the standards contained in U.S. Regulation S-X, and the standardized measure of discounted future net cash flows relating to proved oil and gas reserves determined in accordance with United States Statement of Financial Accounting Standards No.69 “Disclosures About Oil and Gas Producing Activities’’ (“FAS 69’’). As a foreign private issuer, Baytex is permitted to comply with the disclosure requirements contained in NI 51-101 for the purposes of its U.S. regulatory filings. Unless otherwise indicated, all of the reserves and production information disclosure in this Form 20-F is in compliance with NI 51-101.

The primary differences between the U.S. requirements and the NI 51-101 requirements are that (i)the U.S. standards require disclosure only of proved reserves, whereas NI 51-101 requires disclosure of proved and probable reserves, and (ii) the U.S. standards require that the reserves and related future net revenue be

18

estimated under existing economic and operating conditions, i.e., prices and costs as of the date the estimate is made, whereas NI 51-101 requires disclosure of proved reserves and the related future net revenue estimated using constant prices and costs as at the last day of the financial year, and of proved and probable reserves and related future net revenue using forecast prices and costs. The definitions of proved reserves also differ, but according to the Canadian Oil and Gas Evaluation Handbook (the reference source for the definition of proved reserves under NI 51-101), differences in the estimated proved reserve quantities based on constant prices should not be material. Baytex believes that the definition and measurement of proved reserves under NI 51-101 will be more conservative than proved reserves under U.S. standards.

In this Form 20-F, certain natural gas volumes have been converted to barrels of oil equivalent (“BOEs’’) on the basis of six thousand cubic feet to one barrel. BOEs may be misleading, particularly if used in isolation. A BOE conversion ratio of six Mcf to one bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent equivalency at the well head.

Reserve volumes and values at January 1, 2004 are based on Baytex’s interest in its total proved and probable reserves prior to royalties as defined in NI 51-101. Reserve volumes and values for previous years are based on “established” (proved plus 50% probable) reserves prior to deduction of royalties. Under those definitions, probable reserves were discounted by an arbitrary risk factor of 50% in reporting established reserves. Under NI 51-101 reserves definitions, estimates are prepared such that the full proved and probable reserves are estimated to be recoverable (proved plus probable reserves are effectively a “most likely case”). As such, the probable reserves now reported are already “risked”.

Baytex has its reserves evaluated by independent engineers every year. Baytex’s 2003 reserves were independently evaluated as at January 1, 2004 by Sproule Associates Limited (“Sproule”) for all its properties.

The following table shows our oil and natural gas proved reserves based on constant prices. All of the oil and natural gas proved reserves are located in Canada. Oil reserves are expressed in millions of barrels and natural gas reserves in billions of cubic feet.

|

| January 1, |

| December 31, |

| ||||||||

2002 |

| 2001 | |||||||||||

|

| Oil |

| Gas |

| Oil |

| Gas |

| Oil |

| Gas |

|

Net proved reserves |

| 56.6 |

| 66.3 |

| 95.5 |

| 120.1 |

| 95.1 |

| 105.8 |

|

Net proved developed reserves |

| 39.4 |

| 63.1 |

| 61.4 |

| 105.1 |

| 59.1 |

| 96.6 |

|

Long-term Supply Contract

In October 2002, we entered into a long-term crude oil supply contract with a third party that requires the delivery of up to 20,000 barrels per day of Lloydminster Blend crude oil at a price fixed at 71% of NYMEX WTI oil price. The contract is for an initial term of five years commencing January 1, 2003. The contract volumes increased from 9,000 barrels per day in January 2003 to 20,000 barrels per day in October 2003 and thereafter.

Production

The following table summarizes Baytex’s working interest production during the periods indicated:

|

| Years Ended December 31, |

| ||||

|

| 2003 |

| 2002 |

| 2001 |

|

Oil and NGL (bbls/d) |

| 26,184 |

| 27,121 |

| 31,685 |

|

Natural gas (mmcf/d) |

| 63.0 |

| 72.6 |

| 70.8 |

|

Total (BOE/d) |

| 36,686 |

| 39,214 |

| 43,488 |

|

19

Industry Conditions

General

The oil and natural gas industry is subject to extensive controls and regulations governing its operations (including land tenure, exploration, development, production, refining, transportation and marketing) imposed by legislation enacted by various levels of government and with respect to pricing and taxation of oil and natural gas by agreements among the governments of Canada, Alberta, British Columbia and Saskatchewan, all of which should be carefully considered by investors in the oil and gas industry. It is not expected that any of these controls or regulations will affect the operations of the Company in a manner materially different than they would affect other oil and gas companies of similar size. All current legislation is a matter of public record and the Company unable to predict what additional legislation or amendments may be enacted. Outlined below are some of the principal aspects of legislation, regulations and agreements governing the oil and gas industry.

Pricing and Marketing Oil and Natural Gas

The producers of oil are entitled to negotiate sales contracts directly with oil purchasers, with the result that the market determines the price of oil. Such price depends in part on oil quality, prices of competing oils, distance to market, the value of refined products and the supply/demand balance. Oil exporters are also entitled to enter into export contracts with terms not exceeding one year in the case of light crude oil and two years in the case of heavy crude oil, provided that an order approving such export has been obtained from the National Energy Board of Canada (the “NEB”). Any oil export to be made pursuant to a contract of longer duration (to a maximum of 25 years) requires an exporter to obtain an export licence from the NEB and the issuance of such licence requires the approval of the Governor in Council.

The price of natural gas is determined by negotiation between buyers and sellers. Natural gas exported from Canada is subject to regulation by the NEB and the Government of Canada. Exporters are free to negotiate prices with purchasers, provided that the export contracts must continue to meet certain other criteria prescribed by the NEB and the Government of Canada. Natural gas exports for a term of less than 2 years or for a term of 2 to 20 years (in quantities of not more than 30,000 m3/day), must be made pursuant to an NEB order. Any natural gas export to be made pursuant to a contract of longer duration (to a maximum of 25 years) or a larger quantity requires an exporter to obtain an export licence from the NEB and the issuance of such licence requires the approval of the Governor in Council.

The governments of Alberta, British Columbia and Saskatchewan also regulate the volume of natural gas which may be removed from those provinces for consumption elsewhere based on such factors as reserve ability, transportation arrangements and market considerations.

The lack of firm pipeline capacity continues to limit the ability to produce and market natural gas production although pipeline expansions are ongoing. In addition, the prorationing of capacity on the interprovincial pipeline systems continues to limit oil exports.

The North American Free Trade Agreement

The North American Free Trade Agreement (“NAFTA”) among the governments of Canada, United States of America and Mexico became effective on January 1, 1994. NAFTA carries forward most of the material energy terms that are contained in the Canada United States Free Trade Agreement. Canada continues to remain free to determine whether exports of energy resources to the United States or Mexico will be allowed, provided that any export restrictions do not: (i) reduce the proportion of energy resources exported relative to domestic use (based upon the proportion prevailing in the most recent 36 month period); (ii) impose an export

20

price higher than the domestic price; or (iii) disrupt normal channels of supply. All three countries are prohibited from imposing minimum export or import price requirements.

NAFTA contemplates the reduction of Mexican restrictive trade practices in the energy sector and prohibits discriminatory border restrictions and export taxes. The agreement also contemplates clearer disciplines on regulators to ensure fair implementation of any regulatory changes and to minimize disruption of contractual arrangements, which is important for Canadian natural gas exports.

Provincial Royalties and Incentives

In addition to federal regulation, each province has legislation and regulations which govern land tenure, royalties, production rates, environmental protection and other matters. The royalty regime is a significant factor in the profitability of crude oil, natural gas liquids, sulphur and natural gas production. Royalties payable on production from lands other than Crown lands are determined by negotiations between the mineral owner and the lessee, although production from such lands is subject to certain provincial taxes and royalties. Crown royalties are determined by governmental regulation and are generally calculated as a percentage of the value of the gross production. The rate of royalties payable generally depends in part on prescribed reference prices, well productivity, geographical location, field discovery date and the type or quality of the petroleum product produced.

From time to time the governments of the western Canadian provinces create incentive programs for exploration and development. Such programs often provide for royalty rate reductions, royalty holidays and tax credits, and are generally introduced when commodity prices are low. The programs are designed to encourage exploration and development activity by improving earnings and cash flow within the industry.

In the Province of Alberta, a producer of oil or natural gas is entitled to a credit against the royalties payable to the Crown by virtue of the Alberta royalty tax credit (“ARTC”) program. The ARTC rate is based on a price sensitive formula and the ARTC rate varies between 75% at prices at and below $100 per m3 and 25% at prices at and above $210 per m3. The ARTC rate is applied to a maximum of $2,000,000 of Alberta Crown royalties payable for each producer or associated group of producers. Crown royalties on production from producing properties acquired from a corporation claiming maximum entitlement to ARTC will generally not be eligible for ARTC. The rate will be established quarterly based on the average “par price”, as determined by the Alberta Department of Energy for the previous quarterly period.

Crude oil and natural gas royalty programs for specific wells and royalty reductions reduce the amount of Crown royalties paid by the Trust’s operating subsidiaries to the provincial governments. In general, the ARTC program provides a rebate on Alberta Crown royalties paid in respect of eligible producing properties.

Land Tenure

Crude oil and natural gas located in the western provinces is owned predominantly by the respective provincial governments. Provincial governments grant rights to explore for and produce oil and natural gas pursuant to leases, licences and permits for varying terms from two years and on conditions set forth in provincial legislation including requirements to perform specific work or make payments. Oil and natural gas located in such provinces can also be privately owned and rights to explore for and produce such oil and natural gas are granted by lease on such terms and conditions as may be negotiated.

Environmental Regulation

The oil and natural gas industry is currently subject to environmental regulations pursuant to a variety of provincial and federal legislation. Such legislation provides for restrictions and prohibitions on the release or emission of various substances produced in association with certain oil and gas industry operations. In addition, such legislation requires that well and facility sites be abandoned and reclaimed to the satisfaction of

21

provincial authorities. Compliance with such legislation can require significant expenditures and a breach of such requirements may result in suspension or revocation of necessary licenses and authorizations, civil liability for pollution damage and the imposition of material fines and penalties.

Environmental legislation in the Province of Alberta has been consolidated into the Alberta Environmental Protection and Enhancement Act (the “APEA”), which came into force on September 1, 1993. The APEA imposes stricter environmental standards, requires more stringent compliance, reporting and monitoring obligations and significantly increases penalties. The Trust is committed to meeting its responsibilities to protect the environment wherever it operates and anticipates making increased expenditures of both a capital and an expense nature as a result of the increasingly stringent laws relating to the protection of the environment and will be taking such steps as required to ensure compliance with the APEA and similar legislation in other jurisdictions in which it operates. The Company believes that it is in material compliance with applicable environmental laws and regulations. The Company also believes that it is reasonably likely that the trend towards stricter standards in environmental legislation and regulation will continue.

In December 2002 the Government of Canada ratified the Kyoto Protocol. This protocol calls for Canada to reduce its greenhouse gas emissions to 6 percent below 1990 levels during the period between 2008 and 2012. The protocol will only become legally binding when it is ratified by at least 55 countries, covering at least 55 percent of the emissions addressed by the protocol. If the protocol becomes legally binding, it is expected to affect the operation of all industries in Canada, including the oil and gas industry. As details of the implementation of this protocol have yet to be announced, the effect on the Company cannot be determined at this time.

Item 5: Operating and Financial Review and Prospects

Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis, dated June 29, 2004, should be read in conjunction with Baytex’ audited consolidated financial statements for the fiscal years ended December 31, 2003 and 2002. Per barrel of oil equivalent (“boe”) amounts have been calculated using a conversion rate of six thousand cubic feet of natural gas to one barrel of oil.

The financial results of the Company for 2003 were impacted by the Arrangement. The net loss for the year ended December 31, 2003 included $18.9 million of costs related to the reorganization under the Arrangement. The loss for the year also included $44.8 million of costs related to redemption and exchange of notes. These items were offset by a foreign exchange gain of $52.1 million on our U.S. denominated debt.

Crude oil prices remained strong in 2003 as supply and demand fundamentals supported higher prices. Instability in the Middle East, growing demand and low inventory levels kept average WTI at US$31.04/bbl. The oil price received by Baytex averaged $26.36 per barrel for 2003. Natural gas prices received averaged $6.07 per mcf for 2003. The overall higher prices offset lower oil and gas production during 2003. Production was lower during 2003 as certain properties were transferred to Crew under the Arrangement.

The strengthening Canadian dollar relative to the U.S. dollar impacted our net income, as revenues and realized commodity prices, referenced in U.S. dollars, were lower when translated to Canadian dollars. However, we benefit as our fixed-rate debt is denominated in U.S. dollars so this debt is reduced with a strengthening Canadian dollar.

Baytex evaluates performance based on net income and cash flow from operations. Cash flow from operations is not a measure based on generally accepted accounting principles, but is a financial term commonly used in the oil and gas industry. It represents cash generated from operating activities before changes in non-cash working capital, deferred charges and other assets and deferred credits. Baytex considers it a key measure of performance as it demonstrates the ability of the Company to generate the cash flow necessary to fund future distributions to unitholders and capital investments.

Results of Operations 2003 compared to 2002

Production Baytex’s average production for fiscal 2003 decreased by six percent to 36,686 boe per day from 39,214 boe per day for fiscal 2002. This decrease was the result of property dispositions that occurred at the end of the first quarter of 2003 and the transfer of the petroleum and natural gas assets to Crew under the Plan of Arrangement effective September 2, 2003.

Light oil production decreased 28 percent to 2,273 barrels per day during 2003 from 3,154 barrels per day in 2002. Heavy oil production during 2003 was 23,911 barrels per day, consistent with production of 23,967 barrels per day during fiscal 2002. Natural gas production for 2003 decreased by 13 percent to 63.0 million cubic feet per day compared to 72.6 million cubic feet per day for the prior year.

22

Production by Area |

| Light Oil |

| Heavy Oil |

| Natural Gas |

| Barrels of Oil |

|

|

| (bbls/d) |

| (bbls/d) |

| (mmcf/d) |

| (boe/d) |

|

2003 |

|

|

|

|

|

|

|

|

|

Heavy Oil District |

| — |

| 23,911 |

| 10.6 |

| 25,676 |

|

Conventional Oil and Gas District |

| 2,273 |

| — |

| 52.4 |

| 11,010 |

|

Total Production |

| 2,273 |

| 23,911 |

| 63.0 |

| 36,686 |

|

|

|

|

|

|

|

|

|

|

|

2002 |

|

|

|

|

|

|

|

|

|

Heavy Oil District |

| — |

| 23,967 |

| 10.5 |

| 25,710 |

|

Conventional Oil and Gas District |

| 3,154 |

| — |

| 62.1 |

| 13,504 |

|

Total Production |

| 3,154 |

| 23,967 |

| 72.6 |

| 39,214 |

|

Revenue Petroleum and natural gas sales for 2003 decreased by four percent to $351.4 million from $365.9 million for fiscal 2002. Benchmark WTI crude oil averaged US$31.04 per barrel for 2003, representing a 19 percent increase over the US$26.08 per barrel for 2002. Correspondingly, the Trust’s light oil and NGLs price increased to $39.04 per barrel from $33.86 per barrel in 2002. The heavy oil price decreased five percent to $25.12 per barrel in 2003 from $26.39 per barrel in 2002, principally due to the increase in heavy oil differentials. Natural gas prices were 54 percent higher in 2003, averaging $6.07 per thousand cubic feet compared to $3.94 per thousand cubic feet during the previous year. Overall, after accounting for financial derivative contracts, the Trust averaged $26.72 per boe for 2003, a 4 percent increase from $25.56 per boe received in the prior year. For the per-sales-unit calculations, heavy oil sales for 2003 were 650 barrels per day lower than the production for the year due to inventory in transit under the Frontier supply agreement.

For 2003, light oil revenue decreased 17 percent over 2002, as the 15 percent increase in wellhead prices were offset by a 28 percent decrease in production. Revenue from heavy oil decreased eight percent due to a five percent decrease in wellhead prices and a three percent decrease in sales volumes. Natural gas revenue increased 34 percent as the 13 percent production decreased was offset by a 54 percent increase in wellhead prices.

Gross Revenue Analysis |

| 2003 |

| 2002 |

| ||||

|

| $ thousands |

| $/Unit (1) |

| $ thousands |

| $/Unit (1) |

|

Light oil |

| 32,393 |

| 39.04 |

| 38,985 |

| 33.86 |

|

Heavy oil |

| 213,297 |

| 25.12 |

| 230,874 |

| 26.39 |

|

Derivative contract loss |

| (33,777 | ) | (3.62 | ) | (10,622 | ) | (1.07 | ) |

Total oil revenue |

| 211,913 |

| 22.74 |

| 259,237 |

| 26.19 |

|

|

|

|

|

|

|

|

|

|

|

Natural gas revenue |

| 139,491 |

| 6.07 |

| 104,284 |

| 3.94 |

|

Derivative contract gain |

| — |

| — |

| 2,339 |

| 0.09 |

|

Total natural gas revenue |

| 139,491 |

| 6.07 |

| 106,623 |

| 4.03 |

|

|

|

|

|

|

|

|

|

|

|

Total revenue (boe @ 6:1) |

| 351,404 |

| 26.72 |

| 365,860 |

| 25.56 |

|

(1) Per-unit oil revenue is in $/bbl; per unit natural gas revenue is in $/mcf.

Royalties For the year ended December 31, 2003, royalties decreased eight percent to $54.2 million from $58.9 million last year and were 15.4 percent of sales compared to 15.7 percent of sales in 2002. A portion of the royalties paid during 2003 were reimbursed by the Trust, resulting in a lower royalty rate. Before the reimbursement by the Trust, royalties for 2003 were 17.8 percent of sales for light oil, 13.8 percent for heavy

23

oil and 22.9 percent for natural gas. These rates compared to 16.7 percent, 13.9 percent and 19.5 percent, respectively, for 2002.

Operating Expenses Operating expenses for the year 2003 increased 14 percent to $86.0 million from $75.2 million for 2002. This increase is attributable to the disposition of properties with lower operating costs and a general increase in field operating costs. Operating expenses were $6.54 per boe for 2003 compared to $5.26 per boe for the prior year. Operating expenses were $8.32 per barrel of light oil, $7.34 per barrel of heavy oil and $0.73 per thousand cubic feet of natural gas for 2003 versus $5.83, $5.99 and $0.61, respectively, for 2002.

General and Administrative Expenses General and administrative expenses for 2003 were $8.9 million, compared to $6.7 million a year ago. On a sales-unit basis, these expenses increased to $0.67 per boe from $0.47 per boe. In accordance with the full-cost accounting policy, $4.4 million of expenses were capitalized in 2003, compared with $6.7 million capitalized in 2002. The amount of capitalized expenses has been reduced due to lower exploration activity since the effective date of the Arrangement.

Stock-based Compensation Baytex accounts for compensation expense based on the fair value of rights granted to its employees under the Trust’s unit-based compensation plan. As the Trust is unable to determine the fair value of the rights granted, compensation expense has been determined based on the intrinsic value of the rights at the exercise date or at the date of the consolidated financial statements for unexercised rights. Compensation expense of $0.22 million was recorded as compensation expense for all trust unit rights granted on or after January 1, 2003.

Compensation expense was also calculated on the stock options outstanding prior to the Plan of Arrangement. Compensation expense of $0.52 million was recorded as compensation expense for all stock options granted on or after January 1, 2003. All outstanding stock options were cancelled or exercised effective September 2, 2003.

Interest Expense For 2003, interest expenses on long-term debt were $23.5 million compared to $25.2 million for 2002. The decrease is due to the redemption of the senior secured term notes and the impact of the stronger Canadian dollar on U.S dollar based interest expenses. Interest on intercompany notes for 2003 was $21.5 million.