Ex99_1

JP Morgan

Gaming & Lodging Conference

March 18, 2004

Disclaimer

Certain matters discussed in this presentation may constitute forward-looking statements within the meaning of the federal securities law. Such statements are based on management’s beliefs, assumptions and expectations, which in turn are based on information currently available to management. Actual performance and results could differ from those expressed in or contemplated by the forward-looking statements due to a number of risks, uncertainties and other factors, many of which are beyond Choice’s ability to predict or control. For further information on factors that could impact Choice and the statements contained therein, we refer you to the filings made by Choice with the Securities and Exchange Commission, including its report on Form 10-K for the period ended December 31, 2003.

Additional corporate information may be found on the Choice Hotels’ Internet site, which may be accessed at www.choicehotels.com Choice Hotels, Choice Hotels International, Comfort Inn, Comfort Suites, Quality, Clarion, Sleep Inn, MainStay Suites, Econo Lodge, Rodeway Inn, 1-800-4CHOICE and The Power of Being There. Go. are proprietary trademarks and service marks of Choice Hotels International.

1

Company Overview

Company Profile

One of the Largest Hotel Companies in the World

4,810 hotels open worldwide representing 388,618 rooms

491 hotels under development representing 39,877 rooms

Our Brands Cover Many Segments

Limited Service

Full Service

Economy

Mid-Price

Upscale

Source: Choice Internal Data as of December 2003.

3

Company Profile (cont.)

Our Focus Is Solely on Hotel Franchising

Highest returning model in the industry (vs. management/ownership)

High margin, high cash flow with low capital requirements

Scaleable and predictable

Provides profitable growth opportunities

Highly skilled in this area

4

Investment Thesis

Strong, Stable and Growing System

4.4% increase in domestic rooms

470 new hotel contracts signed (up from 304)

20 year contracts, barriers to exit

Strong and Growing Earnings and Cash Flow

Cash flow from operations—$115 million (17% increase)

2003 EBITDA—$125 million (8% increase)

Adjusted Diluted EPS—$1.87 (23% increase)

5

Investment Thesis (cont.)

Management Focused on Creating Value

Share repurchases – 29.3 million repurchased at $17.54 per share

Dividends – Initiated quarterly cash dividend of $0.20/share in 2003

Equity Performance

5 year annualized return in excess of 20%

6

Strategy

Vision and Mission

Our Vision: To generate the highest return on investment of any hotel franchise

Our Mission: Deliver a franchise success system of strong brands, exceptional services, vast consumer reach, and size, scale and distribution that delivers guests and reduces costs for our hotel owners

Our Passion: Customer Profitability

8

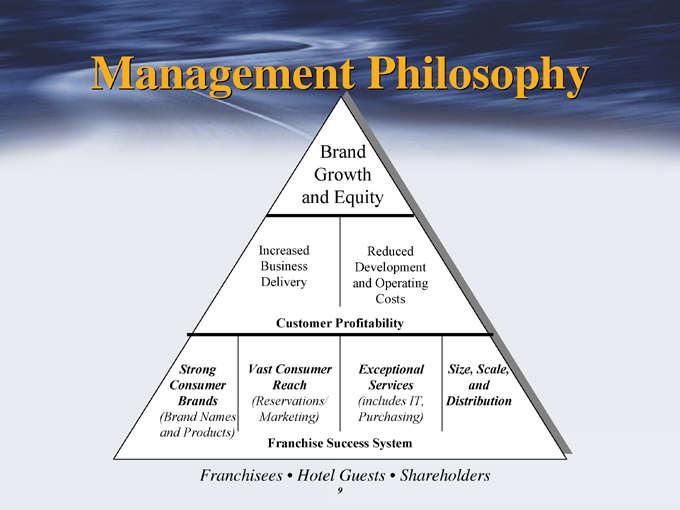

Management Philosophy

Brand

Growth

and Equity

Increased Reduced

Business Development

Delivery and Operating

Costs

Customer Profitability

Strong Vast Consumer Exceptional Size, Scale,

Consumer Reach Services and

Brands (Reservations/ (includes IT, Distribution

(Brand Names Marketing) Purchasing)

and Products)

Franchise Success System

Franchisees • Hotel Guests • Shareholders

9

Build Strong Brands

Among World’s Most Recognizable Hotel Brands

Improved Brand Consistency and Quality

Improved ROI for Owners

Significantly Enhanced Franchise Sales Capability

10

Vast Consumer Reach $50 Million Marketing and Advertising Plan

Creates brand awareness and loyalty

Drives traffic

Enhanced Loyalty Program

2.5 million members

$ 1 billion hotel program revenue to date

Strong Direct Sales Capability

$ 600 million in revenue

11

Vast Consumer Reach (cont.)

State-of-the-Art Reservations System – All Channels

$ 1.3 billion room revenue booked in 2003 – 29% delivery

Strong Synergies with Internet Distribution Channels

New Internet Channels Strengthen Franchise

• Increase distribution

• Improve placement

• Decrease complexity

• Lower cost

• Increase yield

12

Exceptional Services

Full Complement of Hands-On Services Improve Profitability and Create Loyalty

Brand

Complete Life-Cycle Service Offering 150 Field-Based Employees State-of-Art Training Capabilities

Operational and Yield Management Technology Purchasing Assistance

Generates $13 million revenue and lowers owner costs

13

Size, Scale, and Distribution

Lowers Costs and Increases Revenues for Owners

Enables Highly-Valued Capabilities

Brand awareness

National marketing

Reservations

Services

Technologies

Franchising Model is Difficult to Duplicate

Scale required to generate reasonable returns for shareholders

Capital required to generate scale

Scale is a barrier to entry

14

Performance

Business Focus

Profitably Grow

Improve brand performance – “ROI” to owners (business delivery, products, marketing, services)

Introduce new concepts (product design/innovation)

Increase distribution (franchise development)

Maximize Financial Returns and Create Value for Shareholders

Capital allocation – focus on returns

Capital structure – prudent leverage to maximize returns

Share repurchases Dividends

16

Profitably Grow

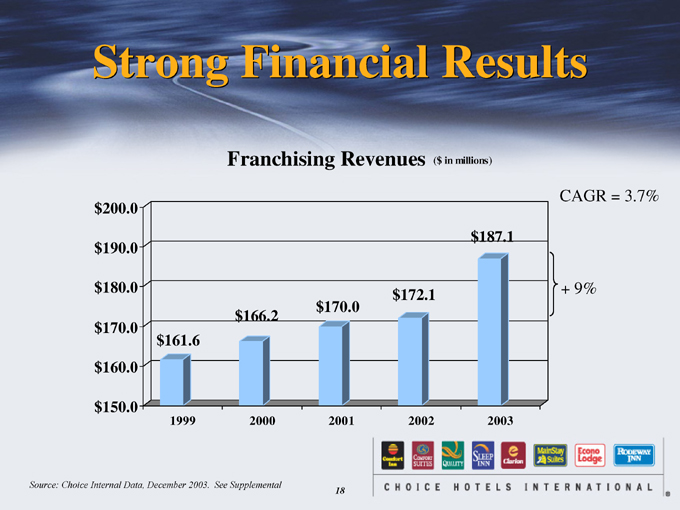

Strong Financial Results

Franchising Revenues ($ in millions)

CAGR = 3.7%

$ 200.0

$ 187.1

$ 190.0

$ 180.0 $ 172.1 + 9%

$ 170.0

$ 166.2

$ 170.0

$ 161.6

$ 160.0

$ 150.0

1999 2000 2001 2002 2003

Source: Choice Internal Data, December 2003. See Supplemental

18

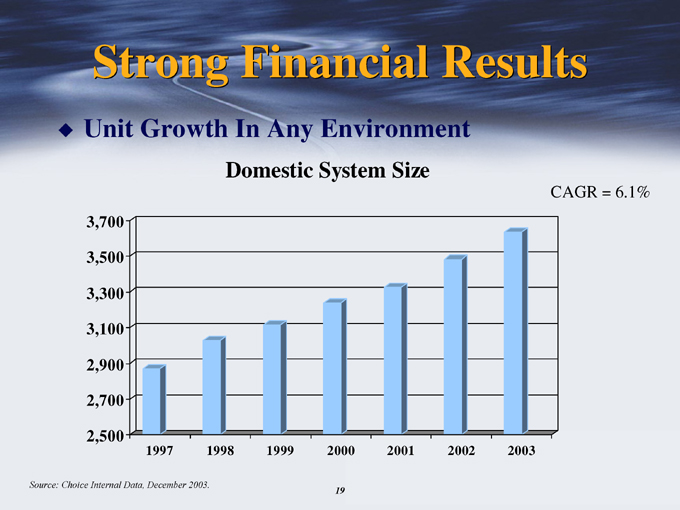

Strong Financial Results

Unit Growth In Any Environment

Domestic System Size

CAGR = 6.1%

3,700

3,500

3,300

3,100

2,900

2,700

2,500

1997 1998 1999 2000 2001 2002 2003

Source: Choice Internal Data, December 2003.

19

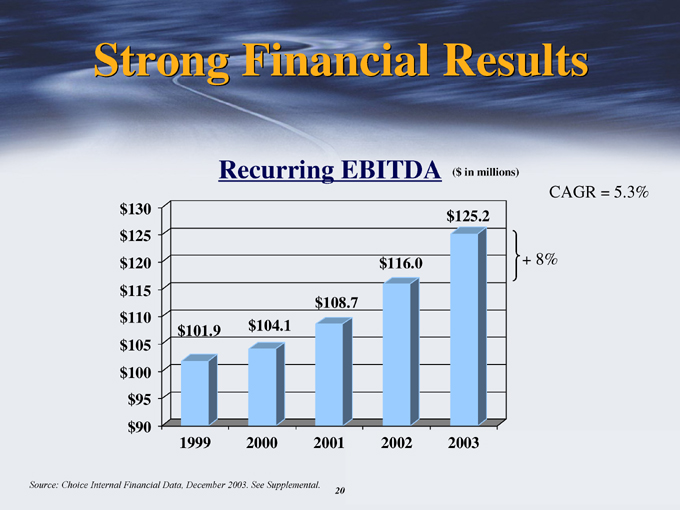

Strong Financial Results

Recurring EBITDA ($ in millions)

CAGR = 5.3%

$ 130 $ 125.2

$ 125

$ 120 $ 116.0 + 8%

$ 115

$ 108.7

$ 110

$101.9 $104.1

$ 105

$ 100

$ 95

$ 90

1999 2000 2001 2002 2003

Source: Choice Internal Financial Data, December 2003. See Supplemental.

20

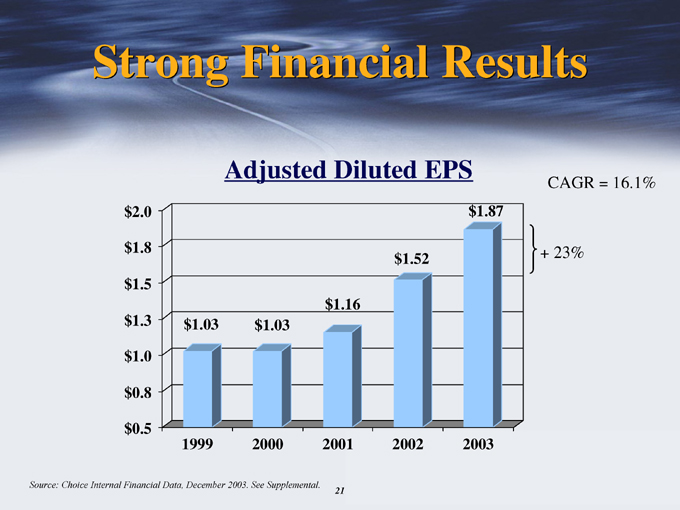

Strong Financial Results

Adjusted Diluted EPS

CAGR = 16.1%

$ 2.0 $ 1.87

$ 1.8 + 23%

$ 1.52

$ 1.5

$ 1.16

$ 1.3 $ 1.03 $ 1.03

$ 1.0

$ 0.8

$ 0.5

1999 2000 2001 2002 2003

Source: Choice Internal Financial Data, December 2003. See Supplemental.

21

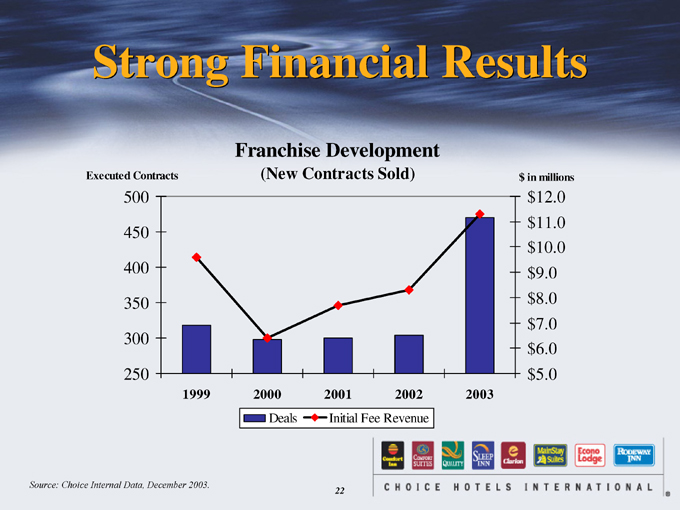

Strong Financial Results

Franchise Development

Executed Contracts (New Contracts Sold) $ in millions

500 $ 12.0

$ 11.0

450

$ 10.0

400 $ 9.0

350 $ 8.0

$ 7.0

300

$ 6.0

250 $ 5.0

1999 2000 2001 2002 2003

Deals Initial Fee Revenue

Source: Choice Internal Data, December 2003.

22

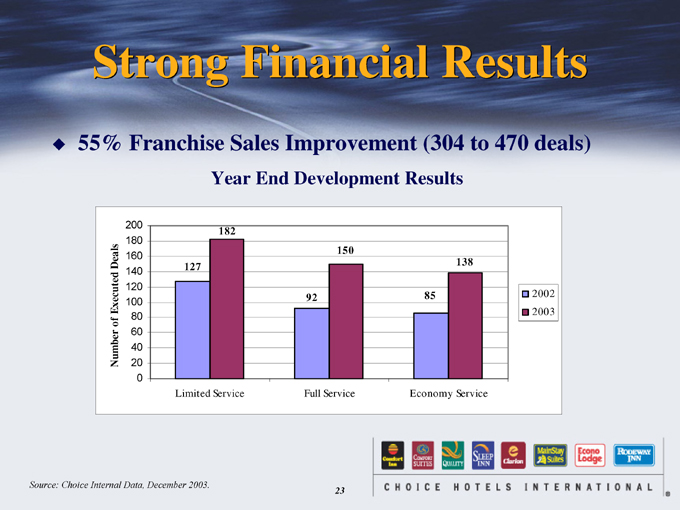

Strong Financial Results

55% Franchise Sales Improvement (304 to 470 deals)

Year End Development Results

200

180 182

150

160

Deals 127 138

Executed 140

of 120

Number 100 92 85 2002

80 2003

60

40

20

0

Limited Service Full Service Economy Service

Source: Choice Internal Data, December 2003.

23

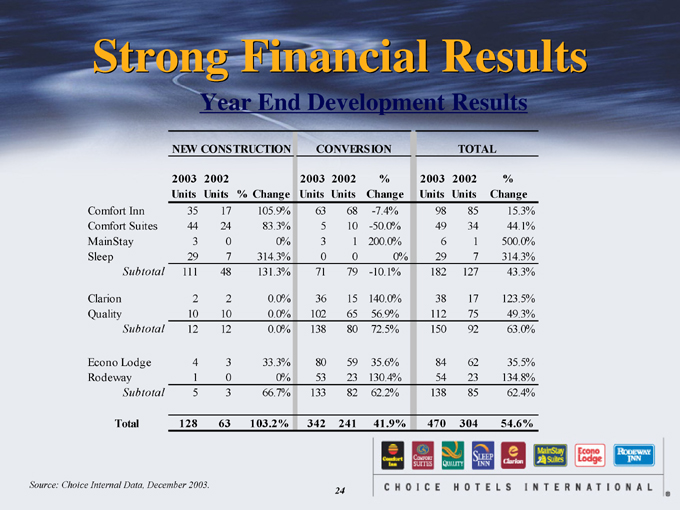

Strong Financial Results

Year End Development Results

NEW CONSTRUCTION CONVERSION TOTAL

2003 2002 2003 2002 % 2003 2002 %

Units Units % Change Units Units Change Units Units Change

Comfort Inn 35 17 105.9% 63 68 -7.4% 98 85 15.3%

Comfort Suites 44 24 83.3% 5 10 -50.0% 49 34 44.1%

MainStay 3 0 0% 3 1 200.0% 6 1 500.0%

Sleep 29 7 314.3% 0 0 0% 29 7 314.3%

Subtotal 111 48 131.3% 71 79 -10.1% 182 127 43.3%

Clarion 2 2 0.0% 36 15 140.0% 38 17 123.5%

Quality 10 10 0.0% 102 65 56.9% 112 75 49.3%

Subtotal 12 12 0.0% 138 80 72.5% 150 92 63.0%

Econo Lodge 4 3 33.3% 80 59 35.6% 84 62 35.5%

Rodeway 1 0 0% 53 23 130.4% 54 23 134.8%

Subtotal 5 3 66.7% 133 82 62.2% 138 85 62.4%

Total 128 63 103.2% 342 241 41.9% 470 304 54.6%

Source: Choice Internal Data, December 2003.

24

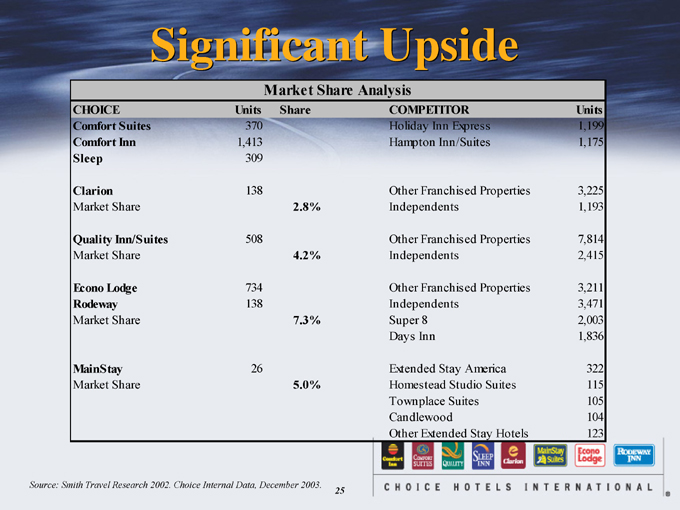

Significant Upside

Market Share Analysis

CHOICE Units Share COMPETITOR Units

Comfort Suites 370 Holiday Inn Express 1,199

Comfort Inn 1,413 Hampton Inn/Suites 1,175

Sleep 309

Clarion 138 Other Franchised Properties 3,225

Market Share 2.8% Independents 1,193

Quality Inn/Suites 508 Other Franchised Properties 7,814

Market Share 4.2% Independents 2,415

Econo Lodge 734 Other Franchised Properties 3,211

Rodeway 138 Independents 3,471

Market Share 7.3% Super 8 2,003

Days Inn 1,836

MainStay 26 Extended Stay America 322

Market Share 5.0% Homestead Studio Suites 115

Townplace Suites 105

Candlewood 104

Other Extended Stay Hotels 123

Source: Smith Travel Research 2002. Choice Internal Data, December 2003.

25

Maximize Returns

Maximize Returns

High Margins, After-Tax Free Cash Flow, and Returns on Capital

Year Ended December 31,

($ in millions) 2002 2003 Percentage

Franchising Margins 67.2% 66.4% (1.2%)

Cash Flow From Operations $ 99.0 $ 115.5 16.7%

CAPEX $ 12.2 $8.5 (30.3%)

After-Tax Free Cash Flow $ 86.5 $99.3 14.8%

ROIC (Net Income over Debt + Equity) 35.8% 35.6% (20 bps)

Source: Choice Internal Financial Data, December 2003. See Supplemental.

27

Create Value

Create Value

Management Focused on Creating Value

Share repurchases – 29.3 million repurchased at $17.54 per share

Dividends – Initiated quarterly cash dividend of $0.20/share in 2003

Equity Performance

5 year annualized return in excess of 20%

29

Closing Comments

Strong Earnings Per Share, EBITDA, and Cash Flow Growth

Proven Earnings Stability Even through Industry/ Economic Downturns

Pure-Play Franchise Focus, Highest Returning “Model” in the Industry

High Operating Margins

Significant and Growing Free Cash Flow

Experienced Management Team Focused on Shareholder Value

30

Supplemental

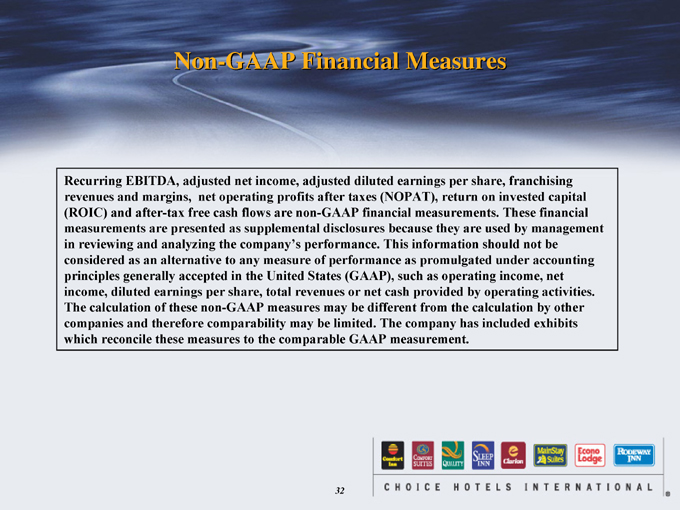

Non-GAAP Financial Measures

Recurring EBITDA, adjusted net income, adjusted diluted earnings per share, franchising revenues and margins, net operating profits after taxes (NOPAT), return on invested capital (ROIC) and after-tax free cash flows are non-GAAP financial measurements. These financial measurements are presented as supplemental disclosures because they are used by management in reviewing and analyzing the company’s performance. This information should not be considered as an alternative to any measure of performance as promulgated under accounting principles generally accepted in the United States (GAAP), such as operating income, net income, diluted earnings per share, total revenues or net cash provided by operating activities. The calculation of these non-GAAP measures may be different from the calculation by other companies and therefore comparability may be limited. The company has included exhibits which reconcile these measures to the comparable GAAP measurement.

32

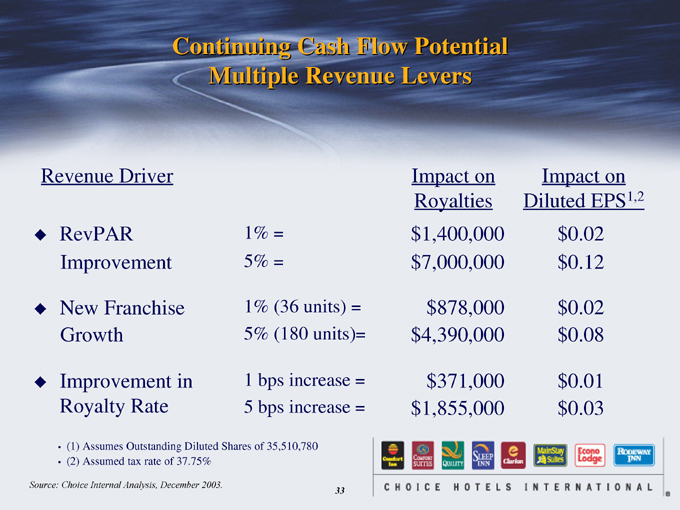

Continuing Cash Flow Potential Multiple Revenue Levers

Revenue Driver Impact on Impact on

Royalties Diluted EPS1,2

RevPAR 1% = $ 1,400,000 $ 0.02

Improvement 5% = $ 7,000,000 $ 0.12

New Franchise 1% (36 units) = $ 878,000 $ 0.02

Growth 5% (180 units)= $ 4,390,000 $ 0.08

Improvement in 1 bps increase = $ 371,000 $ 0.01

Royalty Rate 5 bps increase = $ 1,855,000 $ 0.03

• (1) Assumes Outstanding Diluted Shares of 35,510,780

• (2) Assumed tax rate of 37.75%

Source: Choice Internal Analysis, December 2003.

33

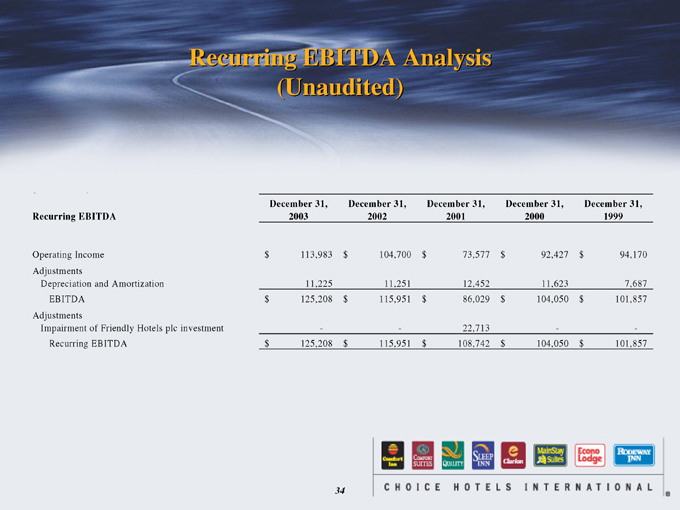

Recurring EBITDA Analysis (Unaudited)

December 31, December 31, December 31, December 31, December 31,

Recurring EBITDA 2003 2002 2001 2000 1999

Adjustments Depreciation and Amortization 11,225 11,251 12,452 11,623 7,687

EBITDA $ 125,208 $ 115,951 $ 86,029 $ 104,050 $ 101,857

Adjustments Impairment of Friendly Hotels plc investment - - 22,713 - -

Recurring EBITDA $ 125,208 $ 115,951 $ 108,742 $ 104,050 $ 101,857

34

Calculation of Adjusted Net Income and Adjusted Diluted Earnings Per Share (EPS) (Unaudited)

December 31, December 31, December 31, December 31, December 31,

2003 2002 2001 2000 1999

Net Income $ 71,863 $ 60,844 $ 14,327 $ 42,445 $ 57,155

Adjustments:

Loss(Gain) on Sunburst Note Transactions (3,383) - - 4,721 -

Impairment of and Equity Losses in Friendly Hotels

PLC Investment - - 37,166 7,532 -

Adjusted Net Income $ 68,480 $ 60,844 $ 51,493 $ 54,698 $ 57,155

Weighted Average Shares Outstanding-Diluted 36,674 40,057 44,572 53,253 55,667

Diluted Earnings Per Share $ 1.96 $ 1.52 $ 0.32 $ 0.80 $ 1.03

Adjustments:

Loss(Gain) on Sunburst Note Transactions (0.09) - - 0.09 -

Impairment of and Equity Losses in Friendly Hotels

PLC Investment - - 0.83 0.14 -

Adjusted Diluted Earnings Per Share (EPS) $ 1.87 $ 1.52 $ 1.16 $ 1.03 $ 1.03

35

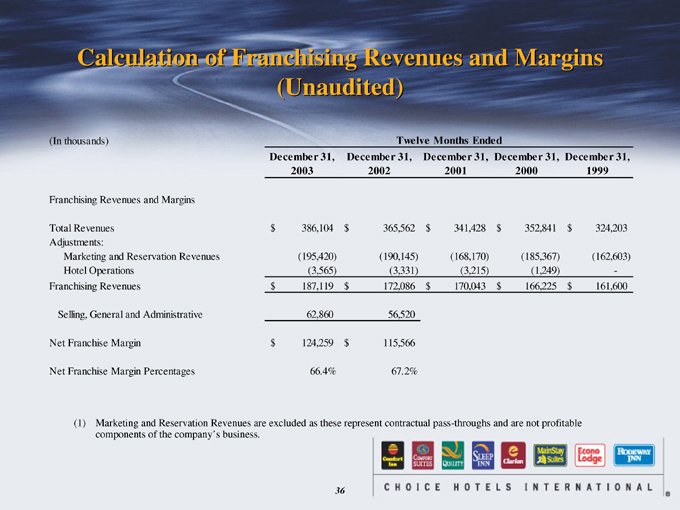

Calculation of Franchising Revenues and Margins (Unaudited)

(In thousands) Twelve Months Ended

December 31, December 31, December 31, December 31, December 31,

2003 2002 2001 2000 1999

Franchising Revenues and Margins

Total Revenues $ 386,104 $ 365,562 $ 341,428 $ 352,841 $ 324,203

Adjustments:

Marketing and Reservation Revenues (195,420) (190,145) (168,170) (185,367) (162,603)

Hotel Operations (3,565) (3,331) (3,215) (1,249) -

Franchising Revenues $ 187,119 $ 172,086 $ 170,043 $ 166,225 $ 161,600

Selling, General and Administrative 62,860 56,520

Net Franchise Margin $ 124,259 $ 115,566

Net Franchise Margin Percentages 66.4% 67.2%

(1) Marketing and Reservation Revenues are excluded as these represent contractual pass-throughs and are not profitable components of the company’s business.

36

Calculation of NOPAT and ROIC

(Unaudited)

(In thousands) Twelve Months Ended

December 31, December 31,

2003 2002

Pre-Tax Income $ 112,407 $ 95,818

Depreciation Expense 11,225 11,251

Interest Expense 11,597 13,136

Other Income and Expenses (10,021) (4,254)

EBITDA 125,208 115,951

Less: Depreciation Expense 11,225 11,251

Net $ 113,983 $ 104,700

Cash Paid For Income Taxes $ 49,559 $ 14,674

Interest Expense (Tax Shield Add-Back) @ 38% 4,407 4,992

$ 53,966 $ 19,666

Cash Tax Rate 48.0% 20.5%

(1) NOPAT $ 59,261 $ 83,211

37

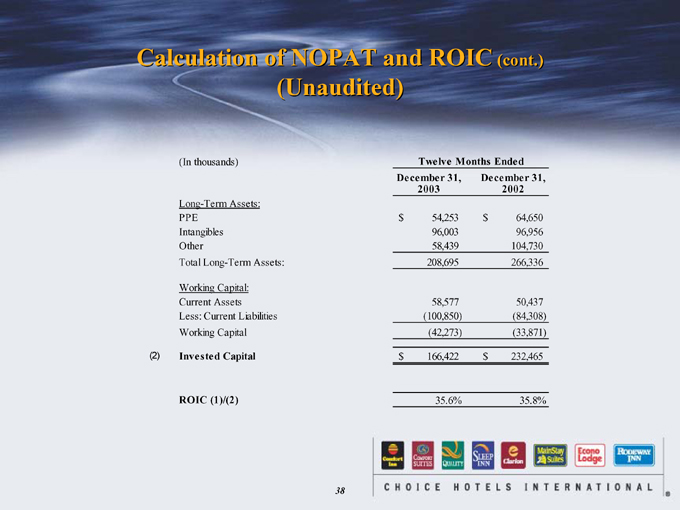

Calculation of NOPAT and ROIC (cont.) (Unaudited)

(In thousands) Twelve Months Ended

December 31, December 31,

2003 2002

Long-Term Assets:

PPE $ 54,253 $ 64,650

Intangibles 96,003 96,956

Other 58,439 104,730

Total Long-Term Assets: 208,695 266,336

Working Capital:

Current Assets 58,577 50,437

Less: Current Liabilities (100,850) (84,308)

Working Capital (42,273) (33,871)

(2) Invested Capital $ 166,422 $ 232,465

ROIC (1)/(2) 35.6% 35.8%

38

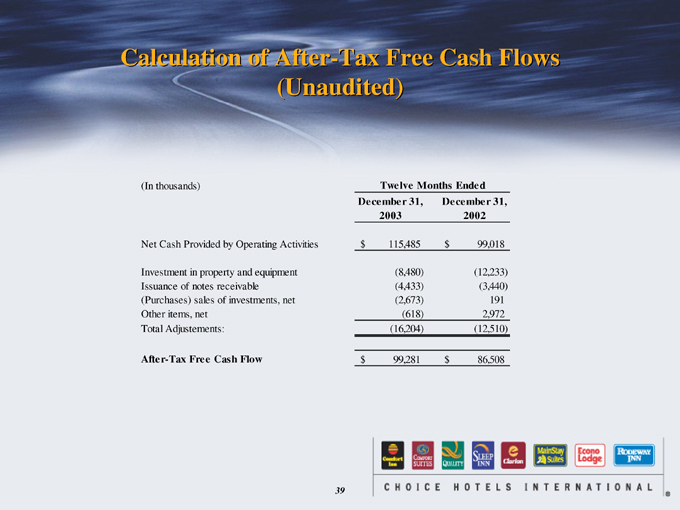

Calculation of After-Tax Free Cash Flows (Unaudited)

(In thousands) Twelve Months Ended

December 31, December 31,

2003 2002

Net Cash Provided by Operating Activities $ 115,485 $ 99,018

Investment in property and equipment (8,480) (12,233)

Issuance of notes receivable (4,433) (3,440)

(Purchases) sales of investments, net (2,673) 191

Other items, net (618) 2,972

Total Adjustements: (16,204) (12,510)

After-Tax Free Cash Flow $ 99,281 $ 86,508

39