UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

þ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended March 31, 2007

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _________ to _________

Commission file number 001-33192

www.bmhc.com

Building Materials Holding Corporation

Delaware | | 91-1834269 |

| (State of incorporation) | | (I.R.S. Employer Identification No.) |

Four Embarcadero Center, Suite 3200, San Francisco, CA 94111

(415) 627-9100

N/A

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer.

Large accelerated filer þ Accelerated filer ¨ Non-accelerated filer ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ¨ No þ

The number of shares outstanding of the registrant’s common stock as of May 4, 2007 was 29,387,326.

BUILDING MATERIALS HOLDING CORPORATION

FORM 10-Q

For the Period Ended March 31, 2007

INDEX

| | Page Number |

| | |

| 2 |

| | |

| 2 |

| | |

| 2 |

| | |

| 3 |

| | |

| 4 |

| | |

| 5 |

| | |

| 6 |

| | |

| 33 |

| | |

| 46 |

| | |

| 47 |

| | |

| 48 |

| | |

| 48 |

| | |

| 49 |

| |

| 53 |

| | |

| 54 |

| | |

| 55 |

| | |

| 56 |

| | |

| 57 |

| | |

| 58 |

Building Materials Holding Corporation

Consolidated Statements of Operations

(thousands, except per share data)

(unaudited)

| | | Three Months Ended March 31 | |

| | | 2007 | | 2006 | |

Sales | | | | | |

| Construction services | | $ | 319,008 | | $ | 549,058 | |

| Building products | | | 250,096 | | | 335,499 | |

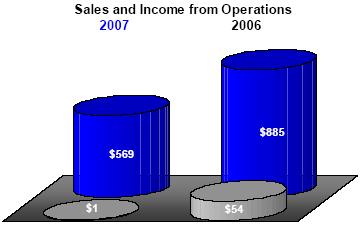

Total sales | | | 569,104 | | | 884,557 | |

| | | | | | | | |

Costs and operating expenses | | | | | | | |

| Cost of goods sold | | | | | | | |

| Construction services | | | 275,402 | | | 454,131 | |

| Building products | | | 181,078 | | | 247,226 | |

Selling, general and administrative expenses | | | 113,822 | | | 130,601 | |

| Other income, net | | | (2,158 | ) | | (1,787 | ) |

| Total costs and operating expenses | | | 568,144 | | | 830,171 | |

| | | | | | | | |

Income from operations | | | 960 | | | 54,386 | |

| | | | | | | | |

| Interest expense | | | 8,218 | | | 5,590 | |

| | | | | | | | |

(Loss) income before income taxes and minority interests | | | (7,258 | ) | | 48,796 | |

| | | | | | | | |

| Income tax benefit (expense) | | | 2,668 | | | (17,810 | ) |

| | | | | | | | |

| Minority interests income, net of income taxes | | | (376 | ) | | (2,917 | ) |

| | | | | | | | |

Net (loss) income | | | | ) | | $28,069 | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

Net (loss) income per share: | | | | | | | |

| Basic | | | $(0.17 | ) | | $0.98 | |

| Diluted | | | $(0.17 | ) | | | |

The accompanying notes are an integral part of these consolidated financial statements.

| | | March 31 | | | December 31 | | | | March 31 | | | December 31 |

| | | 2007 | | | 2006 | | | | 2007 | | | 2006 |

Assets | | | | | | | Liabilities, Minority Interests and Shareholders’ Equity | | | | | |

| Cash and cash equivalents | $ | 27,901 | | $ | 74,272 | | | | | | | |

| Marketable securities | | 5,806 | | | 4,337 | | Accounts payable | $ | 113,922 | | $ | 110,961 |

| Receivables, net of allowances | | | | | | | Accrued compensation | | 35,080 | | | 48,552 |

| of $4,948 and $4,487 | | 288,578 | | | 279,829 | | Insurance deductible reserves | | 26,731 | | | 24,931 |

| Inventory | | 144,361 | | | 144,366 | | Other accrued liabilities | | 28,140 | | | 103,402 |

| Unbilled receivables | | 57,331 | | | 43,527 | | Billings in excess of costs and estimated | | | | | |

| Deferred income taxes | | 7,097 | | | 8,914 | | earnings | | 27,221 | | | 27,622 |

| Prepaid expenses and other | | 18,541 | | | 11,166 | | Current portion of long-term debt | | 5,072 | | | 8,143 |

Current assets | | 549,615 | | | 566,411 | | Current liabilities | | 236,166 | | | 323,611 |

| | | | | | | | | | | | | |

| Property and equipment | | | | | | | Deferred income taxes | | 8,591 | | | 9,138 |

| Land | | 67,539 | | | 62,367 | | Insurance deductible reserves | | 27,139 | | | 25,841 |

| Buildings and improvements | | 143,410 | | | 139,602 | | Long-term debt | | 427,009 | | | 349,161 |

| Equipment | | 189,538 | | | 188,285 | | Other long-term liabilities | | 36,015 | | | 41,390 |

| Construction in progress | | 4,420 | | | 8,579 | | | | | | | |

| Accumulated depreciation | | (145,394) | | | (139,342) | | Minority interests | | 7,004 | | | 7,141 |

| Marketable securities | | 51,863 | | | 53,513 | | | | | | | |

| Deferred loan costs | | 5,200 | | | 5,481 | | Commitments and contingent liabilities | | — | | | — |

| Other long-term assets | | 30,539 | | | 27,223 | | | | | | | |

| Other intangibles, net | | 105,447 | | | 108,792 | | Shareholders’ equity | | | | | |

| Goodwill | | 306,479 | | | 308,000 | | Common shares, $0.001 par value: | | | | | |

| | $ | 1,308,656 | | $ | 1,328,911 | | authorized 50 million; issued and | | | | | |

| | | | | | | | outstanding 29.3 and 29.2 million | | | | | |

| | | | | | | | shares | | 29 | | | 29 |

| | | | | | | | Additional paid-in capital | | 156,794 | | | 154,405 |

| | | | | | | | Retained earnings | | 411,043 | | | 418,927 |

| | | | | | | | Accumulated other comprehensive loss, net | | (1,134) | | | (732) |

| | | | | | | | Shareholders’ equity | | 566,732 | | | 572,629 |

| | | | | | | | | $ | 1,308,656 | | $ | 1,328,911 |

The accompanying notes are an integral part of these consolidated financial statements.

| | | | | | | | | | | | | | | | Accumulated Other Comprehensive Income (Loss) | | | | |

| | | | | | | | | | | | | | | | Net Unrealized Gain (Loss) From | | | | |

| | | | Common Shares | | | Additional | | | | | | | | | Interest Rate | | | | | | | |

| | | | Shares | | | Amount | | | Paid-In Capital | | | Unearned Compensation | | | Retained Earnings | | | Swap Contracts | | | Marketable Securities | | | Total | |

Balance at December 31, 2005 | | | 28,759 | | $ | 29 | | $ | 143,780 | | $ | (2,698 | ) | $ | 328,463 | | $ | 736 | | $ | (249 | ) | $ | 470,061 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Net income | | | — | | | — | | | — | | | — | | | 28,069 | | | — | | | — | | | 28,069 | |

| Unrealized gain | | | — | | | — | | | — | | | — | | | — | | | 1,440 | | | — | | | 1,440 | |

| Taxes for unrealized gain | | | — | | | — | | | — | | | — | | | — | | | (554 | ) | | — | | | (554 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Unrealized loss | | | — | | | — | | | — | | | — | | | — | | | — | | | (103 | ) | | (103 | ) |

| Tax benefit for unrealized loss | | | — | | | — | | | — | | | — | | | — | | | — | | | 92 | | | 92 | |

Comprehensive income | | | | | | | | | | | | | | | | | | | | | | | | 28,944 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

Reclassify unearned compensation - restricted shares | | | — | | | — | | | (2,698 | ) | | 2,698 | | | — | | | — | | | — | | | — | |

| Earned compensation - options | | | — | | | — | | | 2,198 | | | — | | | — | | | — | | | — | | | 2,198 | |

| Earned compensation - restricted shares | | | — | | | — | | | 723 | | | — | | | — | | | — | | | — | | | 723 | |

| Issuance of restricted shares | | | 138 | | | — | | | — | | | — | | | — | | | — | | | — | | | — | |

| Share options exercised | | | 32 | | | — | | | 291 | | | — | | | — | | | — | | | — | | | 291 | |

| Tax benefit for share options exercised | | | — | | | — | | | 328 | | | — | | | — | | | — | | | — | | | 328 | |

| Shares issued from Employee Plan | | | 11 | | | — | | | 400 | | | — | | | — | | | — | | | — | | | 400 | |

| Cash dividends on common shares | | | — | | | — | | | — | | | — | | | (2,894 | ) | | — | | | — | | | (2,894 | ) |

Balance at March 31, 2006 | | | 28,940 | | $ | 29 | | $ | 145,022 | | $ | — | | $ | 353,638 | | $ | 1,622 | | $ | (260 | ) | $ | 500,051 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

Balance at December 31, 2006 | | | 29,153 | | $ | 29 | | $ | 154,405 | | $ | — | | $ | 418,927 | | $ | (548 | ) | $ | (184 | ) | $ | 572,629 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Net loss | | | — | | | — | | | — | | | — | | | (4,966 | ) | | — | | | — | | | (4,966 | ) |

| Unrealized loss | | | — | | | — | | | — | | | — | | | — | | | (851 | ) | | — | | | (851 | ) |

| Tax benefit for unrealized loss | | | — | | | — | | | — | | | — | | | — | | | 321 | | | — | | | 321 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Unrealized gain | | | — | | | — | | | — | | | — | | | — | | | — | | | 193 | | | 193 | |

| Taxes for unrealized gain | | | — | | | — | | | — | | | — | | | — | | | — | | | (65 | ) | | (65 | ) |

Comprehensive loss | | | | | | | | | | | | | | | | | | | | | | | | (5,368 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Earned compensation - options | | | — | | | — | | | 1,254 | | | — | | | — | | | — | | | — | | | 1,254 | |

| Earned compensation - restricted shares | | | — | | | — | | | 796 | | | — | | | — | | | — | | | — | | | 796 | |

| Issuance of restricted shares | | | 110 | | | — | | | — | | | — | | | — | | | — | | | — | | | — | |

| Share options exercised | | | 5 | | | — | | | 35 | | | — | | | — | | | — | | | — | | | 35 | |

| Tax benefit for share options exercised | | | — | | | — | | | 28 | | | — | | | — | | | — | | | — | | | 28 | |

| Shares issued from Employee Plan | | | 13 | | | — | | | 276 | | | — | | | — | | | — | | | — | | | 276 | |

| Cash dividends on common shares | | | — | | | — | | | — | | | — | | | (2,918 | ) | | — | | | — | | | (2,918 | ) |

Balance at March 31, 2007 | | | 29,281 | | $ | 29 | | $ | 156,794 | | $ | — | | $ | 411,043 | | $ | (1,078 | ) | $ | (56 | ) | $ | 566,732 | |

The accompanying notes are an integral part of these consolidated financial statements.

Consolidated Statements of Cash Flows

(thousands)

| | | | Three Months Ended March 31 | |

Operating Activities | | | 2007 | | | 2006 | |

| Net (loss) income | | $ | (4,966 | ) | $ | 28,069 | |

| Items in net (loss) income not using (providing) cash: | | | | | | | |

| Minority interests, net | | | 376 | | | 2,917 | |

| Depreciation and amortization | | | 12,747 | | | 10,182 | |

| Deferred loan cost amortization | | | 281 | | | 208 | |

| Share-based compensation | | | 2,113 | | | 2,980 | |

| (Gain) loss on sale of assets, net | | | (363 | ) | | 27 | |

| Realized gain on marketable securities | | | (11 | ) | | — | |

| Deferred income taxes | | | 2,443 | | | (208 | ) |

| Changes in assets and liabilities, net of effects of acquisitions of business units: | | | | | | | |

| Receivables, net | | | (8,749 | ) | | (19,399 | ) |

| Inventory | | | 5 | | | (15,096 | ) |

| Unbilled receivables | | | (13,804 | ) | | (22,510 | ) |

| Prepaid expenses and other current assets | | | (7,386 | ) | | (2,257 | ) |

| Accounts payable | | | 15,831 | | | 35,094 | |

| Accrued compensation | | | (13,494 | ) | | (15,745 | ) |

| Insurance deductible reserves | | | 1,800 | | | 2,944 | |

| Other accrued liabilities | | | (14,675 | ) | | 16,019 | |

| Billings in excess of costs and estimated earnings | | | (401 | ) | | (4,425 | ) |

| Other long-term assets and liabilities | | | (10,057 | ) | | (4,068 | ) |

| Other, net | | | 256 | | | (370 | ) |

Cash flows (used) provided by operating activities | | | (38,054 | ) | | 14,362 | |

| | | | | | | | |

Investing Activities | | | | | | | |

| Purchases of property and equipment | | | (8,651 | ) | | (10,409 | ) |

| Acquisitions and investments in businesses, net of cash acquired | | | (61,596 | ) | | (80,005 | ) |

| Proceeds from dispositions of property and equipment | | | 1,187 | | | 425 | |

| Purchase of marketable securities | | | (8,739 | ) | | (834 | ) |

| Proceeds from sales of marketable securities | | | 9,150 | | | 581 | |

| Other, net | | | (463 | ) | | (1,777 | ) |

Cash flows used by investing activities | | | (69,112 | ) | | (92,019 | ) |

| | | | | | | | |

Financing Activities | | | | | | | |

| Net borrowings under revolver | | | 79,200 | | | 80,700 | |

| Principal payments on term notes | | | (875 | ) | | (313 | ) |

| Net payments on other notes | | | (3,548 | ) | | (688 | ) |

| (Decrease) increase in book overdrafts | | | (10,359 | ) | | 329 | |

| Proceeds from share options exercised | | | 35 | | | 291 | |

| Tax benefit for share options | | | 28 | | | 328 | |

| Dividends paid | | | (2,915 | ) | | (2,158 | ) |

| Distributions to minority interests | | | (1,003 | ) | | (245 | ) |

| Other, net | | | 232 | | | (395 | ) |

Cash flows provided by financing activities | | | 60,795 | | | 77,849 | |

| | | | | | | | |

(Decrease) Increase in Cash and Cash Equivalents | | | (46,371 | ) | | 192 | |

| | | | | | | | |

| Cash and cash equivalents, beginning of period | | | 74,272 | | | 30,078 | |

| Cash and cash equivalents, end of period | | $ | 27,901 | | $ | 30,270 | |

| | | | | | | | |

Supplemental Disclosure of Cash Flow Information | | | | | | | |

| Accrued but unpaid dividends | | $ | 2,918 | | $ | 2,894 | |

| Cash paid for interest | | $ | 7,819 | | $ | 4,923 | |

| Cash paid for income taxes | | $ | 1,820 | | $ | 13,146 | |

| | | | | | | | |

Supplemental Disclosure of Investing Activities | | | | | | | |

| Fair value of assets acquired | | $ | 715 | | $ | 131,312 | |

| Liabilities assumed | | $ | 100 | | $ | 62,637 | |

| Cash paid for acquisitions made this period | | $ | 615 | | $ | 68,675 | |

| Cash paid for acquisitions made in prior period | | $ | 60,981 | | $ | 11,330 | |

The accompanying notes are an integral part of these consolidated financial statements.

1. Summary of Significant Accounting Policies

Basis of Presentation

These consolidated financial statements have been prepared pursuant to the rules and regulations of the Securities and Exchange Commission. Certain information and disclosures normally included in financial statements prepared in accordance with accounting principles generally accepted in the United States have been condensed or omitted pursuant to those rules and regulations. These consolidated financial statements should be read in conjunction with the consolidated financial statements and the accompanying notes included in our most recent Annual Report on Form 10-K.

These consolidated financial statements have not been audited by independent registered public accountants. However, in the opinion of management, all adjustments necessary, including those of a normal and recurring nature, to present fairly the results for the periods have been included. The preparation of these consolidated financial statements required estimates and assumptions. Actual results may differ from those estimates.

Nature of Operations

Building Materials Holding Corporation (BMHC) provides construction services and building products to professional homebuilders and contractors in western and southern regions of the United States. We operate through two separately managed and reportable business segments: SelectBuild and BMC West. SelectBuild provides framing and other construction services to high-volume homebuilders in 16 of the top 25 single-family construction markets. BMC West distributes building materials, manufactures building components (millwork, floor and roof trusses and wall panels) and provides construction services to professional builders and contractors through a network of 41 distribution facilities and 60 manufacturing facilities.

Principles of Consolidation

The consolidated financial statements include the accounts of BMHC and its subsidiaries. All significant intercompany balances and transactions are eliminated.

Use of Estimates

The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and contingent assets and liabilities at the date of the financial statements as well as the reported amounts of sales and expenses during the reporting period. Actual amounts may differ materially from those estimates. The following critical accounting estimates require our subjective and complex judgment often as a result of the need to estimate matters that are inherently uncertain:

· Revenue Recognition for Construction Services

The percentage-of-completion method is used to recognize revenue for construction services. This method requires the use of various estimates, including among others, the extent of progress towards completion, contract revenues and contract completion costs. Periodic estimates of our progress towards completion are made based on a comparison of labor costs incurred to date with total estimated contract costs for labor. Contract revenues and contract costs to be recognized are dependent on the accuracy of estimates, including quantities of materials, labor productivity and other cost estimates. We have a history of making reasonable estimates of the extent of progress towards completion, contract revenues and contract completion costs. However, due to uncertainties inherent in the estimation process, it is possible that actual completion costs may vary from estimates. Revisions of contract revenues and cost estimates as well as provisions for estimated losses on uncompleted contracts are recognized in the period such revisions are known.

· Estimated Losses on Uncompleted Contracts and Changes in Contract Estimates

Estimated losses on uncompleted contracts and changes in contract estimates are established by assessing estimated costs to complete, change orders and claims for uncompleted contracts. Revisions of estimated losses are recognized in the period such revisions are known.

· Goodwill

Goodwill represents the excess of purchase price over the fair values of net tangible and identifiable intangible assets of acquired businesses. An annual assessment for impairment is completed in the fourth quarter and whenever events and circumstances indicate the carrying amount may not be recoverable. An impairment is recognized if the carrying amount is more than the estimated future operating cash flows as measured by fair value techniques.

· Insurance Deductible Reserves

The estimated cost of workers’ compensation, general liability and automobile claims is determined by actuarial methods. Claims in excess of insurance deductibles are insured with third-party insurance carriers. Reserves for deductible amounts are recognized based on the estimated costs of these claims as limited by the provisions of the applicable insurance policies. Revisions of estimated claims are recognized in the period such revisions are known.

· Warranties

The estimated cost of warranties for certain construction services is based on the nature and frequency of claims, anticipated claims and cost per claim. Claims in excess of insurance deductibles are insured with third-party insurance carriers. Estimated costs for warranties are recognized when the revenue associated with the service is recognized. Revisions of estimated warranties are recognized in the period such revisions are known.

· Share-based Compensation

Our estimates of the fair values of our share-based payment transactions are based on the modified Black-Scholes-Merton model. To meet the fair value measurement objective, we are required to develop estimates regarding expected exercise patterns, share price volatility, forfeiture rates, risk-free interest rate and dividend yield. These assumptions are based principally on historical experience. When circumstances indicate the availability of new or different information that would be useful in estimating these assumptions, revisions will be made and recognized in the period such revisions are known. Due to uncertainties inherent in these assumptions, it is possible that actual share-based compensation may vary from this estimate.

Cash and Cash Equivalents

Cash and cash equivalents consist of short-term investments that have a maturity of 3 months or less at the date of purchase. Cash and cash equivalents were $27.9 million at March 31, 2007 and $74.3 million at December 31, 2006.

Receivables

Receivables consist primarily of amounts due from customers and are net of an allowance for doubtful accounts. The allowance for doubtful accounts reflects our best estimate of probable losses inherent in the accounts receivable balance. We determine the allowance based on known troubled accounts, historical experience and other available evidence.

Inventory Valuation

Inventory consists principally of building materials purchased for resale and is valued at the lower of average cost or market. We participate in vendor rebate programs under which rebates are earned by attaining certain purchase volumes. Volume rebates are accrued as earned. These volume rebates are recorded as a reduction in inventory and recognized in cost of goods sold when the related product is sold.

Unbilled Receivables and Billings in Excess of Costs and Estimated Earnings

The percentage-of-completion method results in recognizing costs incurred and estimated revenues on uncompleted contracts. Unbilled receivables represent revenues recognized for construction services performed, however not yet billed. Billings in excess of costs and estimated earnings represent billings made in excess of estimated revenues recognized. These billings are deferred until the actual progress towards completion indicates recognition is appropriate. Costs include direct labor and materials as well as equipment costs related to contract performance.

Property and Equipment

Property and equipment are recorded at cost. Cost includes expenditures for major improvements and replacements that extend useful life. Certain costs of software are capitalized provided those costs are not research and development and certain other criteria are met. Capitalized interest was not significant. Expenditures for other maintenance and repairs are expensed as incurred. Gains and losses from sales and retirements are included in income as they occur. Depreciation is calculated using the straight-line method over the economic useful lives of the assets. The estimated useful lives of depreciable assets are generally:

· 10 to 30 years for buildings and improvements

· 7 to 10 years for machinery and fixtures

· 3 to 10 years for handling and delivery equipment

· 3 to 10 years for software development costs

In order to improve financial returns, we periodically evaluate our investments in property and equipment. As a result, property and equipment may be consolidated, leased or sold. We recognized a gain of $0.4 million for the period ended March 31, 2007, a loss of less than $0.1 million for the period ended March 31, 2006 and a loss of $0.2 million in 2006 from the sales of property and equipment.

In April 2007, BMC West sold certain real estate as a result of a relocation of our building materials operation in Austin, Texas. The sale is expected to result in a gain after tax of approximately $5.5 million in the second quarter.

Long-lived Assets

Long-lived assets such as property, equipment and intangibles with useful lives are evaluated for impairment whenever events or changes in circumstances indicate the carrying amount may not be recoverable. An impairment is recognized if the carrying amount exceeds its fair value and when the carrying amount is not recoverable based on the estimated future operating cash flows on an undiscounted basis.

Revenue Recognition

The percentage-of-completion method is used to recognize revenue for construction services. Revenues for building products are recognized when title to the goods and risk of loss pass to the buyer, which is at the time of delivery. Taxes assessed by governmental authorities that are directly imposed on our revenue-producing transactions are excluded from sales.

Shipping and Handling

Shipping and handling costs for manufactured building components and construction services are included as a component of cost of goods sold. Shipping and handling costs for building products are included as a component of selling, general and administrative expenses and were $17.7 million for the period ended March 31, 2007, $18.2 million for the period ended March 31, 2006 and $78.8 million in 2006.

Reclassifications

SelectBuild identified certain costs of sourcing materials and reclassified these costs to cost of goods sold from selling, general and administrative expenses. Costs reclassified to cost of goods sold from selling, general and administrative expenses were $6.3 million for the period ended March 31, 2006 and $29.1 million for 2006. These reclassifications, none of which affected previously reported consolidated results of operations, cash flows or shareholders’ equity, have been made to amounts reported in prior periods to conform to the current year presentation.

Recent Accounting Principles

In February 2007, the Financial Accounting Standards Board issued Statement of Financial Accounting Standards No. 159, The Fair Value Option for Financial Assets and Financial Liabilities - Including an Amendment of FASB Statement No. 115. This accounting principle expands the use of fair value accounting. Entities may elect to measure eligible items at fair value at specified election dates, however the fair value election is irrevocable and made on an instrument-by-instrument basis. Eligible items include financial assets and liabilities, firm commitments for financial instruments, loan commitments, nonfinancial insurance contracts and warranties (goods or services settled by a third party) and host financial instruments. Upon adoption, unrealized gains and losses for existing items measured at fair value are recorded as a cumulative adjustment to beginning retained earnings and subsequent changes are recognized in earnings at each reporting date. We elected to not adopt the fair value measurement option for eligible items. This accounting principle was adopted January 2007 and had no impact on consolidated financial position, results of operations or cash flows.

In September 2006, the Financial Accounting Standards Board issued Statement of Financial Accounting Standards No. 157, Fair Value Measurements. This accounting principle simplifies existing accounting literature by providing a single definition of fair value, a framework for measuring fair value and expanded disclosures about fair value. This accounting principle emphasized that fair value is a market-based measurement of the amount that would be received upon the sale of an asset or paid to transfer a liability (an exit price) and not the price that would be paid to acquire the asset or received to assume the liability (entry price). This accounting principle did not expand the use of fair value. This accounting principle was adopted January 2007 and had no impact on consolidated financial position, results of operations or cash flows.

In June 2006, the Financial Accounting Standards Board issued Interpretation No. 48, Accounting for Uncertainty in Income Taxes. This accounting principle provides specific guidance for measurement, recognition and disclosure of uncertain tax positions. This accounting principle was adopted January 2007 and had no impact on consolidated financial position, results of operations or cash flows.

2. Net Income Per Share

Net income per share was determined using the following information (thousands, except per share data):

| | | | Three Months Ended March 31 | | | | |

| | | | 2007 | | | 2006 | | | 2006 | |

| | | | | | | | | | | |

| Net (loss) income | | $ | (4,966 | ) | $ | 28,069 | | $ | 102,074 | |

| Weighted average shares used to determine basic net income per share | | | 28,768 | | | 28,524 | | | 28,603 | |

| Net effect of dilutive stock options and restricted stock | | | — | | | 1,049 | | | 986 | |

Weighted average shares used to determine diluted net income per share | | | 28,768 | | | 29,573 | | | 29,589 | |

| | | | | | | | | | | |

| Net (loss) income per share: | | | | | | | | | | |

| Basic | | | | ) | | | | | $3.57 | |

| Diluted | | | $(0.17 | ) | | $0.95 | | | $3.45 | |

| | | | | | | | | | | |

| Cash dividends declared per share | | | $0.10 | | | $0.10 | | | $0.40 | |

Share options considered not dilutive are those with exercise prices greater than the average market value of the common shares in the periods presented. Share options that are not dilutive and therefore excluded from the computation of diluted net income per share were as follows:

| · | 819,098 shares for the period ended March 31, 2007, |

| · | 407,100 shares for the period ended March 31, 2006, and |

| · | 403,100 shares in 2006. |

3. Impairment of Assets

Long-lived assets such as property, equipment and intangibles are evaluated for impairment whenever events or changes in circumstances indicate the carrying amount may not be recoverable. An impairment for these assets is recognized if the carrying amount exceeds its fair value and when the carrying amount is not recoverable based on the estimated future operating cash flows on an undiscounted basis.

Similarly, goodwill is evaluated for impairment in the fourth quarter and whenever events and circumstances indicate the carrying amount may not be recoverable. An impairment for goodwill is recognized if the carrying amount is more than the estimated future operating cash flows as measured by fair value techniques.

As a result of changes in specific markets, SelectBuild recognized the following impairments during 2006:

| · | $1.8 million for the carrying amount of goodwill in the second quarter and |

| · | $0.4 million for the carrying amount of certain customer relationships in the second quarter. |

4. Acquisitions and Minority Interests

Acquisitions are accounted for under the purchase method of accounting. The purchase price is allocated to the assets acquired, including intangible assets, and liabilities assumed based on their estimated fair values at the date of acquisition. Subsequent to the initial allocation of purchase price, adjustments may be made to reflect the fair value of working capital and tangible assets. Any excess of the purchase price over the estimated fair value of the identifiable assets and liabilities acquired is recorded as goodwill. Operating results of acquired businesses are included in the consolidated statements of income from the date of acquisition.

| · | In March 2007, SelectBuild acquired the assets of a concrete services business in Fresno, California for approximately $0.7 million in cash of which $0.1 million has been retained for the settlement period. This purchase price is subject to working capital adjustment. Information required to complete the purchase price allocation is not yet available. Final allocation of the purchase price will be completed as soon as this information is available. |

| · | In December 2006, SelectBuild acquired a distribution services business in Southern California for approximately $1.6 million in cash of which $0.1 million has been retained for the settlement period. This purchase price is subject to working capital adjustment. Information required to complete the purchase price allocation is not yet available. Final allocation of the purchase price will be completed as soon as this information is available. |

| · | In August 2006, SelectBuild acquired a window installation business in Arizona for approximately $13.9 million in cash. |

| · | In July 2006, SelectBuild acquired a framing services business in Southern California for approximately $78.6 million in cash. Additional cash payments may be required based on operating performance through June 2009. |

| · | In June 2006, BMC West acquired a building materials distribution and truss manufacturing business in Eastern Idaho for approximately $5.1 million in cash. |

| · | In April 2006, SelectBuild acquired a concrete services business in Northern Arizona for approximately $1.5 million in cash. |

| · | In April 2006, SelectBuild acquired a wall panel and truss manufacturing business in Palm Springs, California for $6.7 million in cash. |

| · | In February 2006, BMC West acquired 3 facilities providing building materials distribution and millwork services in Houston, Texas for $20.6 million in cash. |

| · | In January 2006, SelectBuild acquired framing businesses in Palm Springs, California and Reno, Nevada for $57.1 million in cash. Additional cash payments may be required based on operating performance through December 2009. |

Minority interest reflects the other owners’ proportionate share in the assets and liabilities of business ventures as of the date of purchase, adjusted by the proportionate share of post-acquisition income or loss. As the operating results of entities with minority interest are consolidated, minority interests income represents the income or loss attributable to the other owners.

| · | In April 2007, SelectBuild acquired the remaining 27% interest in Riggs Plumbing for $10.5 million in cash. In July 2005, SelectBuild acquired an additional 13% interest for $1.4 million in cash and in April 2005, acquired an initial 60% interest for $17.8 million in cash. Information required to complete the purchase price allocation is not yet available. Final allocation of the purchase price will be completed as soon as this information is available. Riggs Plumbing provides plumbing services to high-volume production builders in the Phoenix and Tucson markets. |

| · | In November 2006, SelectBuild acquired the remaining 49% interest in BBP Companies for $22.8 million in cash. In July 2005, SelectBuild acquired an initial 51% interest for $9.4 million in cash and $1.0 million of our common shares. BBP Companies provide concrete services to high-volume production homebuilders in Arizona. |

| · | In January 2006, SelectBuild acquired the remaining 20% interest in WBC Construction, LLC for $36.0 million in cash. In August 2005, SelectBuild acquired an additional 20% interest for $24.8 million in cash and in January 2003, acquired an initial 60% interest for $22.9 million in cash and $1.0 million of our common shares. Information required to complete the purchase price allocation is not yet available. Final allocation of the purchase price will be completed as soon as this information is available. WBC provides concrete block masonry and concrete services to high-volume homebuilders in Florida. |

Assets and liabilities acquired in these acquisitions included (thousands):

| | | March 31 | | December 31 | | | | March 31 | | December 31 |

| | | 2007 | | 2006 | | | | 2007 | | 2006 |

| Cash and cash equivalents | | $ | — | | $ | — | | Accounts payable | | $ | — | | $ | 10,376 |

| Receivables | | | — | | | 44,683 | | Accrued compensation | | | — | | | 1,447 |

| Inventory | | | — | | | 19,957 | | Insurance deductible reserves | | | — | | | — |

| Unbilled receivables | | | — | | | 10,101 | | Other accrued liabilities | | | (60,587) | | | 50,340 |

| Deferred income taxes | | | — | | | — | | Billings in excess of | | | | | | |

| Prepaid expenses and other | | | 15 | | | 263 | | costs and estimated earnings | | | — | | | 23,557 |

| | | | | | | | | Current portion of long-term debt | | | — | | | — |

Current assets | | | 15 | | | 75,004 | | Current liabilities | | | (60,587) | | | 85,720 |

| | | | | | | | | | | | | | | |

| Property and equipment | | | 216 | | | 19,845 | | Deferred income taxes | | | (917) | | | 937 |

| Other long-term assets | | | — | | | 42 | | Long-term debt | | | — | | | — |

| Other intangibles, net | | | 1,382 | | | 68,692 | | Other long-term liabilities | | | — | | | 8,173 |

| Goodwill | | | (1,521) | | | 122,374 | | | | | | | | |

| | | | | | | | | Minority interests | | | — | | | (10,627) |

| | | $ | 92 | | $ | 285,957 | | | | $ | (61,504) | | $ | 84,203 |

The following summarizes pro forma results of operations assuming the acquisitions for 2007 and 2006 occurred as of the beginning of 2006. Due to uncertainties in these assumptions, the pro forma data does not purport to be indicative of the results of operations that would have resulted had the acquisitions been consummated at the beginning of the period presented, or that may occur in the future (thousands, except per share data):

| | | | Three Months Ended March 31 | | | | |

| | | | 2007 | | | 2006 | | | 2006 | |

| Sales - as reported | | $ | 569,104 | | $ | 884,557 | | $ | 3,245,169 | |

| Pro forma Sales | | $ | 569,868 | | $ | 931,467 | | $ | 3,325,314 | |

| | | | | | | | | | | |

| Net (loss) income - as reported | | $ | (4,966 | ) | $ | 28,069 | | $ | 102,074 | |

| Pro forma Net (loss) income | | $ | (3,976 | ) | $ | 30,061 | | $ | 102,017 | |

| | | | | | | | | | | |

| Net (loss) income per share: | | | | | | | | | | |

| Diluted - as reported | | | | ) | | $0.95 | | | $3.45 | |

| Pro forma Diluted | | | $(0.14 | ) | | | | | $3.45 | |

We have call rights and put obligations associated with the interests in RCI Construction, A-1 Truss and WBC Mid-Atlantic that we do not currently own. Under the purchase agreements, we have the right to purchase the other owners’ remaining portions during certain periods or if certain conditions are met. Likewise, the other owners have the option to require us to purchase their remaining portions during certain periods. The purchase price for the remaining portions will be based generally on a multiple of historical earnings. The following table summarizes the timing of these call and put obligations:

| | Call Options | | Put Options |

| RCI Construction | January 2008 through January 2012 | | January 2008 through January 2012 |

| A-1 Truss | September 2004 through August 2014 | | September 2009 through August 2014 |

| WBC Mid-Atlantic | October 2003 through September 2010 | | December 2006 through December 2008 |

5. Marketable Securities

Investments in marketable securities consist of debt securities held by our captive insurance subsidiary and are considered available-for-sale and recorded at fair value. Fair value is based on market quotes. Unrealized gains and losses, net of deferred taxes, are recorded as a component of accumulated other comprehensive (loss) income, net, a component of shareholders’ equity. There were no significant unrealized losses.

The fair value of these marketable securities were as follows (thousands):

| | | | | | | | |

| U.S. government and agencies | | $ | 22,159 | | $ | 25,661 | |

| Asset backed securities | | | 20,339 | | | 18,278 | |

| Corporate securities | | | 15,171 | | | 13,911 | |

| | | $ | 57,669 | | $ | 57,850 | |

Contractual maturities were as follows (thousands):

| | | | | | | | |

| Less than 1 year | | $ | 5,806 | | $ | 4,337 | |

| Due in 1 to 2 years | | | 15,453 | | | 16,648 | |

| Due in 2 to 5 years | | | 36,410 | | | 36,865 | |

| | | $ | 57,669 | | $ | 57,850 | |

6. Intangible Assets and Goodwill

Intangible assets represent the values assigned to customer relationships, covenants not to compete and trade names. Intangible assets are amortized on a straight-line basis over their expected useful lives. Customer relationships are amortized over 3 to 17 years, covenants not to compete over 2 to 5 years and trade names over 3 years. Amortization expense for intangible assets was $4.7 million for the period ended March 31, 2007, $3.1 million for the period ended March 31, 2006 and $14.7 million in 2006. Intangible assets consist of the following (thousands):

| | | | March 31, 2007 | |

| | | | Gross Carrying Amount | | | Accumulated Amortization | | | Net Carrying Amount | |

| Customer relationships | | $ | 123,845 | | $ | (25,771 | ) | $ | 98,074 | |

| Covenants not to compete | | | 12,095 | | | (5,308 | ) | | 6,787 | |

| Trade names | | | 204 | | | (176 | ) | | 28 | |

| Other | | | 657 | | | (99 | ) | | 558 | |

| | | $ | 136,801 | | $ | (31,354 | ) | $ | 105,447 | |

| | | | December 31, 2006 | |

| | | | Gross Carrying Amount | | | Accumulated Amortization | | | Net Carrying Amount | |

| Customer relationships | | $ | 122,498 | | $ | (22,125 | ) | $ | 100,373 | |

| Covenants not to compete | | | 13,094 | | | (4,802 | ) | | 8,292 | |

| Trade names | | | 204 | | | (159 | ) | | 45 | |

| Other | | | 146 | | | (64 | ) | | 82 | |

| | | $ | 135,942 | | $ | (27,150 | ) | $ | 108,792 | |

Estimated amortization expense for intangible assets is $12.9 million for the remainder of 2007, $15.6 million for 2008, $15.2 million for 2009, $14.3 million for 2010, $13.0 million for 2011 and $34.4 million thereafter.

Goodwill represents the excess of the purchase price over the fair value of net tangible and identifiable intangible assets of acquired businesses. Adjustments to amounts previously reported as goodwill occur as a result of completing the purchase price allocation to the assets acquired, including intangible assets, and liabilities assumed based on their estimated fair values at the date of acquisition.

An annual assessment for impairment is completed in the fourth quarter and whenever events and circumstances indicate the carrying amount may not be recoverable. An impairment is recognized at the reporting unit if the carrying amount is more than the estimated future operating cash flows as measured by fair value techniques.

Changes in the carrying amount of goodwill by business segment were as follows (thousands):

| | | | SelectBuild | | | BMC West | | | Total | |

Balance at December 31, 2006 | | $ | 287,123 | | $ | 20,877 | | $ | 308,000 | |

| Purchase Price Adjustment | | | (1,521 | ) | | — | | | (1,521 | ) |

Balance at March 31, 2007 | | $ | 285,602 | | $ | 20,877 | | $ | 306,479 | |

While goodwill is tested for impairment annually and not amortized for financial statement proposes, goodwill may be deductible for income tax purposes. Certain goodwill is non-deductible. Changes to non-deductible goodwill were as follows (thousands):

| | | | SelectBuild | | | BMC West | | | | |

Balance at December 31, 2006 | | $ | 33,939 | | $ | 7,423 | | $ | 41,362 | |

| Purchase Price Adjustment | | | 1,512 | | | — | | | 1,512 | |

Balance at March 31, 2007 | | $ | 35,451 | | $ | 7,423 | | $ | 42,874 | |

8. Debt

Long-term debt consists of the following (thousands):

| | | | | | | | | | Notional Amount | | | Effective Interest Rate | |

| As of March 31, 2007 | | | Balance | | | Stated Interest Rate | | | of Interest Rate Swaps | | | Average for Quarter | | | As of March 31 | |

| Revolver | | $ | 79,200 | | | LIBOR plus 1.25% or Prime plus 0.00% | | $ | — | | | 10.6 | % | | 8.3 | % |

| | | | | | | | | | | | | | | | | |

| Term note | | | 348,250 | | | LIBOR plus 2.50% or Prime plus 1.25% | | | 200,000 | | | 7.7 | % | | 7.7 | % |

| | | | | | | | | | | | | | | | | |

| Other | | | 4,631 | | | Various | | | — | | | | | | | |

| | | | 432,081 | | | | | $ | 200,000 | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Less: Current portion | | | 5,072 | | | | | | | | | | | | | |

| | | $ | 427,009 | | | | | | | | | | | | | |

| | | | | | | | | | Notional Amount of Interest | | | Effective Interest Rate | |

| As of December 31, 2006 | | | Balance | | | Stated Interest Rate | | | Rate Swaps | | | Average for Year | | | As of December 31 | |

| Revolver | | $ | — | | | LIBOR plus 1.25% or Prime plus 0.00% | | $ | ― | | | 6.5 | % | | n/a | |

| | | | | | | | | | | | | | | | | |

| Term note | | | 349,125 | | | LIBOR plus 2.50% or Prime plus 1.25% | | | 200,000 | | | 6.7 | % | | 7.0 | % |

| | | | | | | | | | | | | | | | | |

| Other | | | 8,179 | | | Various | | | — | | | — | | | — | |

| | | | 357,304 | | | | | $ | 200,000 | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Less: Current portion | | | 8,143 | | | | | | | | | | | | | |

| | | $ | 349,161 | | | | | | | | | | | | | |

Revolver

In November 2006, we entered into an amended $500 million revolver with a group of lenders. The revolver matures in November 2011. The revolver consists of both LIBOR and Prime based borrowings. These variable interest rates are subject to quarterly adjustment based on operating performance and range from LIBOR plus 1.00% to 2.00%, or Prime plus 0.00% to 0.75%. Interest is paid quarterly. As of March 31, 2007, $79.2 million was outstanding under the revolver.

Term Note

In November 2006, we entered into a $350 million term note with a group of lenders. The term note matures in November 2013 and is payable in quarterly installments for the first 7 years in amounts equal to 1% of the initial principal per year and the remaining principal due November 2013. The variable interest rate for the term note is LIBOR plus 2.50%, or Prime plus 1.25%. Interest is paid quarterly. As of March 31, 2007, $348.3 million was outstanding under this term note.

Other

Other long-term debt of $4.6 million consists of term notes, equipment notes and capital leases for equipment. Interest rates vary and dates of maturity are through March 2021.

Expansion of Credit Facility, Covenants and Maturities

The credit facility consists of the revolver and term note. The credit facility may be increased an aggregate amount of up to $250 million. The credit facility is collateralized by tangible and intangible property of our wholly-owned subsidiaries, except the assets of our captive insurance subsidiary. The credit facility contains covenants and conditions requiring the maintenance of certain financial ratios. At March 31, 2007, we were in compliance with these covenants and conditions.

Scheduled maturities of long-term debt are as follows (thousands):

| 2007 | | $ | 3,937 | |

| 2008 | | | 4,826 | |

| 2009 | | | 4,140 | |

| 2010 | | | 3,824 | |

| 2011 | | | 82,909 | |

| Thereafter | | | 332,445 | |

| | | $ | 432,081 | |

As of March 31, 2007 and December 31, 2006 there were $97.2 million of letters of credit outstanding that guaranteed performance or payment to third parties. These letters of credit reduce borrowing availability under the revolver.

Hedging Activities

Derivative and hedging activities are recorded on the balance sheet at their fair values. In November 2006, we entered into interest rate swap contracts that effectively convert $200 million of the variable rate borrowings of the $348.3 million term note to a fixed interest rate of 7.59% through November 2012, thus reducing the impact of increases in interest rates on future interest expense. Approximately 57% of the outstanding variable rate borrowings of the term note as of March 31, 2007 have been hedged through the designation of interest rate swap contracts accounted for as cash flow hedges. After giving effect to the interest rate swap contracts, total borrowings were 47% fixed and 53% variable.

The fair value of derivative instruments is based on pricing models using current market rates. The fair value of the interest rate swap contracts was a long-term liability of $1.7 million as of March 31, 2007. The effective portion was recorded in accumulated other comprehensive loss, net, a separate component of shareholders’ equity, and is subsequently reclassified into earnings in the same financial statement line item, interest expense, in the same period during which the hedged transaction is recognized in earnings. A corresponding deferred tax asset of $0.7 million was also recorded in accumulated other comprehensive loss, net for the income tax related to the estimated fair value of the interest rate swap contracts. The ineffective portion of the change in the value of the interest rate swap contracts is immediately recognized as a component of interest expense. Management may choose not to swap variable rates to fixed rates or may terminate a previously executed swap if the variable rate positions are more beneficial.

In June 2004, we entered into interest rate swap contracts that effectively converted $100 million of variable rate borrowings to a fixed interest rate. These swaps were settled in November 2006 and the $1.5 million gain recognized for this settlement was reclassified to other income, net from accumulated other comprehensive income, net.

9. Shareholders’ Equity

Preferred Shares

We are authorized to issue 2 million preferred shares, however none of these shares are issued. Under the terms of our Restated Certificate of Incorporation, the Board of Directors is authorized to determine or alter the rights, preferences, privileges and restrictions of the preferred shares.

Common Shares

Our common shares have a par value of $0.001. We have 50 million shares authorized of which approximately 29.3 million are issued and outstanding as of March 31, 2007.

Of the unissued shares, 322,928 shares were reserved for the following:

| Employee Stock Purchase Plan | | | 50,262 | |

| 2004 Incentive and Performance Plan | | | 272,666 | |

Shareholders’ Rights Plan

In September 1997, our Board of Directors adopted a shareholder rights plan. If a person acquires 15% or more of our common shares or makes a tender offer or other offer to do so without the approval of the Board of Directors, our shareholders would have the right to purchase our common shares or the shares of the acquiring company at a significant discount. The Board of Directors has the right to redeem these rights for a nominal amount, to extend the period before the rights may be exercised or to take other actions as defined. The plan is intended to encourage any person seeking to acquire us to negotiate with the Board of Directors. The plan expires in September 2007.

Dividends

Cash dividends per common share were as follows:

| | | | 2007 | | | 2006 | |

| First quarter | | | $0.10 | | | $0.10 | |

| Second quarter | | | — | | | 0.10 | |

| Third quarter | | | — | | | 0.10 | |

| Fourth quarter | | | — | | | 0.10 | |

| | | | $0.10 | | | | |

On May 1, 2007, our Board of Directors approved a 2007 second quarter cash dividend of $0.10 per common share. The dividend was payable to shareholders of record as of June 22, 2007 and will be paid on or about July 13, 2007.

Repurchase Program

In March 2007, our Board of Directors authorized the repurchase of up to $25 million of our common shares through March 2008. No common shares were repurchased in the period ended March 31, 2007.

| 10. | Employee Benefit Plans |

Retirement Plans

· Savings and Retirement Plan

We provide a savings and retirement plan for salaried and certain hourly employees whereby eligible employees may contribute a percentage of their earnings to a trust. Participants may defer 1% to 50% of their eligible compensation (base salary, annual incentive and long-term incentives) subject to the limitations imposed under the Internal Revenue Code. Vesting in matching contributions and related earnings/losses occurs at the rate of 20% per year of service or upon reaching age 65, death or disability.

Our matching contributions range from 50% of the first 6% to 25% of the first 4% of the participant’s contribution. Matching contributions are established at the discretion of the Compensation Committee of our Board of Directors in February. Matching contributions of $1.4 million for the period ended March 31, 2007, $1.5 million for the period ended March 31, 2006 and $4.5 million in 2006 were made to the trusts based on a percentage of the contributions made by participants.

Participants may direct their contributions and matching contributions through any of the investment options offered, including self-directed brokerage accounts. Investment options are reviewed and revised quarterly by an Investment Committee comprised of management and advised by consultants.

· Executive Deferred Compensation

We provide a deferred compensation plan for executives and key employees. The objective of the plan is to provide executives and key employees with an additional opportunity to save for their retirement. Participants may defer up to 80% of their eligible compensation (base salary, annual incentive and long-term incentives). Matching contributions mirror the savings and retirement plan matching contribution percentage. Matching contributions are established at the discretion of the Compensation Committee of our Board of Directors in February.

There are no minimum or guaranteed returns. Participants may elect distribution upon reaching a specific age, number of years or separation of service. Distributions may be a lump sum payment or monthly installment over 5 to 10 years.

Matching contributions mirror the savings and retirement plan matching contribution percentage. Matching contributions are established at the discretion of the Compensation Committee of our Board of Directors in February. Matching contributions of $0.2 million for the period ended March 31, 2007, $0.3 million for the period ended March 31, 2006 and $0.4 million for 2006 were made to the trust based on a percentage of the contributions made by participants.

Participants may direct their contributions and matching contributions through any of the investment options offered, including our common shares. Investment options are reviewed and revised quarterly by an Investment Committee comprised of management and advised by consultants.

· Supplemental Retirement

Additionally, there is a supplemental retirement plan for executives and key employees. The objective of the plan is to provide a meaningful supplemental retirement benefit that enables participants to retire at age 65 with 30 years of service at an income level of at least 60% of pre-retirement base salary after considering deferred compensation, predecessor retirement and social security benefits.

Active participants receive a guaranteed return of 7% and inactive participants receive a guaranteed return of 0% to 9% based on their years of service and payment elections. Contributions and the guaranteed return are established at the discretion of the Compensation Committee of our Board of Directors in February. Participants are immediately vested in the contribution.

In 2006, contributions were 3.6% of net income and were allocated proportionately to participants based on their base salaries. Contributions were $0.6 million for the period ended March 31, 2007, $1.8 million for the period ended March 31, 2006 and $7.5 million in 2006.

Contributions for the obligation are invested in company-owned life insurance policies. The cash surrender value of these policies approximates the obligation, however the guaranteed returns, if any, are not fully funded as these returns are dependent upon years of service and payment elections. These life insurance policies fund the obligation to the participants or their beneficiaries over a 5, 10 or 15-year period.

Employee Stock Purchase Plan

In September 2000, our Board of Directors adopted the Employee Stock Purchase Plan, which our shareholders approved in May 2001. The plan permits eligible employees to purchase common shares through payroll deductions of up to 10% of an employee’s compensation limited to $25,000 each year. The purchase price of the shares is 85% of the market price on the last day of each month. There were 400,000 common shares authorized under this plan and there were 50,262 shares available for future purchase as of March 31, 2007. Compensation expense recognized was $0.1 million for the period ended March 31, 2007, $0.1 million for the period ended March 31, 2006 and $0.3 million in 2006.

2004 Incentive and Performance Plan

In February 2004, our Board of Directors adopted the 2004 Incentive and Performance Plan, which our shareholders approved in May 2004. A total of 2.4 million shares are reserved for issuance under the plan. Employees and non-employee directors are eligible to receive awards at the discretion of the Compensation Committee. Options, appreciation rights, restricted shares, other share-based awards and non-discretionary awards may be granted under this plan.

Options

| · | Grants of options under the 2004 Incentive and Performance Plan vest ratably over 3 to 4 years from the date of grant and expire after 7 years if unexercised. Options were awarded with exercise prices equal to the fair value of the shares on the date of grant. |

| · | In February 2000, our Board of Directors adopted the 2000 Stock Incentive Plan which our shareholders approved in May 2000. Grants of options under the 2000 Stock Incentive Plan vest ratably through the end of the fourth year from the date of grant and expire after 10 years if unexercised. Options were awarded with exercise prices equal to the fair value of the shares on the date of grant. No further grants are made under this plan. |

With the adoption of Statement of Financial Accounting Standards No. 123 (Revised 2004), Share-Based Payment, in 2006, compensation expense is recognized over the requisite service period for all share-based awards granted after the date of adoption as well as awards unvested on the date of adoption. Prior periods are not revised for comparative purposes. Share-based compensation expense previously included restricted shares and share awards and will now include the fair value of share options.

Compensation expense is recognized over the requisite service period. The fair value of compensation expense recognized for options for the requisite service period was $1.3 million for the period ended March 31, 2007, $2.2 million for the period ended March 31, 2006 and $5.1 million, including $0.3 million for options vested due to early retirement eligibility, for 2006. Options are not included in the calculation of basic income per share, however options are included in the calculation of diluted income per share.

The fair value of each option is estimated on the date of grant using the modified Black-Scholes-Merton model. Significant awards of options and their key assumptions are as follows:

Grant Year | | Grant Month | | Grant Date Fair Value of Options | |

Exercise Price | |

Risk Free Interest Rate | | Expected Volatility | | Expected Dividend Yield | | Expected Term (years) | |

| 2007 | | March | | | $8.21 | | $18.28 | | | 4.53 | % | | 54.53 | % | | 2.03 | % | | 5.19 | |

| 2006 | | September | | | $12.74 | | $28.01 | | | 4.51 | % | | 55.58 | % | | 1.59 | % | | 4.72 | |

| 2006 | | January | | | $17.59 | | $37.93 | | | 3.77 | % | | 48.58 | % | | 0.70 | % | | 5.60 | |

| 2005 | | May | | | $15.79 | | $28.36 | | | 4.29 | % | | 54.16 | % | | 0.68 | % | | 7.00 | |

| 2005 | | February | | | $12.31 | | $22.77 | | | 4.10 | % | | 54.16 | % | | 0.84 | % | | 6.84 | |

| 2004 | | May | | | $4.39 | | $8.50 | | | 4.56 | % | | 54.25 | % | | 1.45 | % | | 7.00 | |

| 2004 | | February | | | $4.16 | | $7.88 | | | 4.09 | % | | 54.68 | % | | 1.45 | % | | 7.50 | |

These assumptions are based principally on historical experience. When circumstances indicate the availability of new or different information that would be useful in estimating these assumptions, revisions will be made and reflected in the period such revisions are determined. Due to uncertainties inherent in these assumptions, it is possible that actual share-based compensation may vary from the estimate of the fair value of these options.

Activity for option awards was as follows (thousands, except per share data):

| | | | Three Months Ended March 31 2007 | | | Three Months Ended March 31 2006 | | | 2006 | |

| | | Shares | | | Weighted Average Exercise Price | | | Weighted Average Remaining Contractual Term (years) | | | Intrinsic Value | | | Shares | | | Weighted Average Exercise Price | | | Shares | | | Weighted Average Exercise Price | |

| Outstanding at beginning of the period | | | 2,521 | | | | | | 5.1 | | | | | | 2,300 | | | | | | 2,300 | | | $9.73 | |

| Granted | | | 354 | | | $18.28 | | | | | | | | | 407 | | | $37.93 | | | 409 | | | $37.88 | |

| Exercised | | | (5 | ) | | $6.97 | | | | | | | | | (31 | ) | | $9.22 | | | (176 | ) | | $7.34 | |

| Forfeited | | | (1 | ) | | $6.25 | | | | | | | | | (7 | ) | | $14.33 | | | (12 | ) | | $21.98 | |

| Outstanding at end of the period | | | 2,869 | | | $14.90 | | | 5.1 | | | | | | 2,669 | | | $14.03 | | | 2,521 | | | $14.41 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Exercisable at end of the period | | | 1,924 | | | $11.27 | | | 4.6 | | | | | | 1,535 | | | $8.09 | | | 1,658 | | | $8.20 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| In-the-money: | | | | | | | | | | | | | | | | | | | | | | | | | |

| Outstanding | | | 1,696 | | | $6.76 | | | | | $ | 19,244 | | | 2,662 | | | $9.72 | | | 2,108 | | | $9.84 | |

| Exercisable | | | 1,518 | | | $6.56 | | | | | $ | 17,530 | | | 1,525 | | | $7.74 | | | 1,656 | | | $7.85 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Weighted average fair value of options granted at fair value | | | | | | $8.21 | | | | | | | | | | | | $17.59 | | | | | | $17.56 | |

The intrinsic value or the difference between our share price and the exercise price, for in-the-money options represents the value that would have been received by option holders had they exercised their options. These values change based on the fair market value of our shares. The intrinsic value was:

· $19.2 million for options outstanding

· $17.5 million for options exercisable (vested)

The intrinsic value for options exercised was $0.1 million for the period ended March 31, 2007, $0.9 million for the period ended March 31, 2006 and $3.8 million in 2006.

As of March 31, 2007, option awards outstanding and exercisable were as follows (thousands, except per share data):

| | | | Options Outstanding | | | Options Exercisable | |

Range of Exercise Prices | | | Options Outstanding | | | Weighted Average Remaining Contractual Life (years) | | | Weighted Average Exercise Price | | | Shares Exercisable | | | Weighted Average Exercise Price | |

| $4.84 to $5.97 | | | 555 | | | 3.2 | | | | | | 555 | | | $4.94 | |

| $6.19 to $6.97 | | | 336 | | | 5.9 | | | $6.96 | | | 336 | | | $6.96 | |

| $7.00 to $7.88 | | | 467 | | | 5.7 | | | $7.38 | | | 415 | | | $7.31 | |

| $8.70 | | | 338 | | | 4.1 | | | $8.70 | | | 212 | | | $8.70 | |

| $18.28 | | | 354 | | | 7.0 | | | $18.28 | | | 15 | | | $18.28 | |

| $22.77 to $28.36 | | | 416 | | | 4.9 | | | $22.90 | | | 272 | | | $22.83 | |

| $37.93 to $38.16 | | | 403 | | | 5.8 | | | $37.93 | | | 146 | | | $37.93 | |

| $4.84 to $38.16 | | | 2,869 | | | 5.1 | | | $14.90 | | | 1,951 | | | $11.27 | |

As of March 31, 2007, there was $8.9 million of unrecognized compensation expense related to these options. This is recognized as the requisite services are rendered and is expected to be recognized ratably through March 2011. The total fair value of options vested and unexercised was $4.0 million for the period ended March 2007, $1.7 million for the period ended March 2006 and $2.7 million in 2006.

Restricted Shares

Grants of restricted shares vest 3 years from the date of grant. Under certain circumstances some or all of the restricted shares may vest earlier. Compensation expense is recognized over the vesting period. Compensation expense recognized was $0.8 million for the period ended March 31, 2007, $0.7 million for the period ended March 31, 2006 and $3.1 million in 2006.

Activity for nonvested restricted share awards was as follows (thousands, except per share data):

| | | | Three Months Ended March 31 2007 | | | Three Months Ended March 31 2006 | | | 2006 | |

| | | | Shares | | | Weighted Average Grant Date Fair Value | | | Shares | | | Weighted Average Grant Date Fair Value | | | Shares | | | Weighted Average Grant Date Fair Value | |

| Nonvested at beginning of the period | | | 396 | | | | | | 258 | | | | | | 258 | | | $16.46 | |

| Granted | | | 109 | | | $18.28 | | | 138 | | | $37.88 | | | 139 | | | $37.83 | |

| Vested | | | — | | | — | | | — | | | — | | | — | | | — | |

| Forfeited | | | — | | | — | | | — | | | — | | | (1 | ) | | $37.93 | |

| Nonvested at end of the period | | | 505 | | | $22.69 | | | 396 | | | $23.95 | | | 396 | | | $23.91 | |

As of March 31, 2007, there was $0.6 million of unrecognized compensation expense related to these restricted shares. This is recognized as the requisite services are rendered and is expected to be recognized ratably through March 2010. Restricted shares are not included in the calculation of basic income per share, however restricted shares are included in the calculation of diluted income per share.

Shares

We issue shares to non-employee directors of our Board of Directors for their services. These shares vest immediately, however trading is restricted for 1 year from the date of grant. We issued 12,000 shares in May 2006 and 14,000 shares in May 2005 and recognized compensation expense of $0.1 million for the period ended March 31, 2007, $0.1 million for the period ended March 31, 2006 and $0.4 million in 2006.

The following table summarizes equity compensation information as of March 31, 2007 (thousands, except per share data):

| | | Number of Securities to be Issued Upon Exercise of Outstanding Options, Warrants and Rights | | Weighted Average Exercise Price of Outstanding Options, Warrants and Rights | | Number of Securities Remaining Available for Future Issuance Under Equity Compensation Plans | |

Equity compensation plans approved by security holders | | | 3,374 | | | | | | 273 | |

Equity compensation plans not approved by security holders | | | — | | | — | | | — | |

| Total | | | 3,374 | | | $12.67 | | | 273 | |

Share-based compensation expense is included in selling, general and administrative expenses since it is incentive compensation issued primarily to our executives and senior management. Share-based compensation expense for options, restricted shares and share awards was $2.1 million for the period ended March 31, 2007, $3.0 million for the period ended March 31, 2006 and $8.5 million for 2006.

11. Income Taxes

The asset and liability method is used to account for income taxes. Under this method, deferred tax assets and liabilities are recognized for tax credits and for the future tax consequences attributable to differences between the financial statement carrying amounts of existing assets and liabilities and their tax bases. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. A valuation allowance is recorded to reduce the carrying amounts of deferred tax assets unless it is more likely than not that such assets will be realized.

Our income tax compliance is periodically examined by various taxing authorities. Our tax returns for 2006 through 2002 are either under examination or open for future examination. We believe the ultimate results of examinations, if any, will not have an adverse affect on our financial condition, results of operations or cash flows. Revisions of estimated tax liabilities are reflected in the period such revisions are known.

In November 2006, SelectBuild acquired the remaining 49% interest in BBP Companies. Prior to the acquisition, income taxes associated with the other owner’s proportionate interest were $0.8 million for the period ended March 31, 2006 and $1.7 million in 2006. We were required to recognize income taxes for all of the earnings due to its C Corporation status. While these income taxes were recognized in income tax expense, the portion of income taxes associated with the other owner’s proportionate share of earnings was eliminated through minority interest.

The tax benefit associated with options exercised by employees under the various share plans reduced taxes payable an insignificant amount for the period ended March 31, 2007, $0.3 million for the period ended March 31, 2006 and $1.5 million in 2006. These tax benefits are recognized in additional paid-in capital, a component of shareholders’ equity.

12. Financial Instruments

The estimated fair values of cash and cash equivalents, receivables, unbilled receivables, accounts payable and accruals are the same as their carrying amounts due to their short-term nature. After giving effect to the interest rate swap contracts, the interest for our debt is 47% fixed and 53% variable. The estimated market value of our debt, based on current interest rates for similar obligations with like maturities, was:

| · | $0.9 million more than the amount of debt reported on the consolidated balance sheet at March 31, 2007 and |

| · | $0.2 million less than the amount of debt reported on the consolidated balance sheet at December 31, 2006. |

Changes in interest rates expose us to financial market risk. We currently utilize interest rate swap contracts to hedge interest exposure on our term note. The interest rate swap contracts effectively convert $200 million of the term note to a fixed interest rate of 7.59% through November 2012. Changes in the fair value of the interest rate swap contracts are recorded as accumulated other comprehensive loss, net, a separate component of shareholders’ equity, and are subsequently reclassified into interest expense as interest expense is recognized on the term note.

Derivative financial instruments are not utilized to hedge other risks or for speculative or trading purposes.

13. Commitments and Contingencies

Warranties

We provide limited warranties for certain construction services. Specific terms and conditions for warranties vary from 1 year to 10 years and are based on geographic market and state regulations. Factors for determining estimates of warranties include the nature and frequency of claims, anticipated claims and cost per claim. Estimated costs for warranties are recognized when the revenue associated with the service is recognized. Revisions of estimated warranties are reflected in the period such revisions are determined. Warranty activity is as follows (thousands):

| | | | Three Month Ended March 31 | | | | |

| | | | 2007 | | | 2006 | | | 2006 | |

| Balance at beginning of the period | | $ | 7,155 | | $ | 5,404 | | $ | 5,404 | |

| Provision for warranties | | | 113 | | | 1,438 | | | 3,009 | |

| Provision for warranties from acquisitions | | | — | | | 95 | | | 117 | |

| Warranty charges | | | (201 | ) | | (119 | ) | | (1,375 | ) |

| Balance at end of the period | | $ | 7,067 | | $ | 6,818 | | $ | 7,155 | |

Legal Proceedings

We are involved in litigation and other legal matters arising in the normal course of business. In the opinion of management, the recovery or liability, if any, under any of these matters will not have a material effect on our financial position, results of operations or cash flows.

14. Segment Information

The consolidated financial statements include operations from our two reportable segments, SelectBuild and BMC West. These segments represent businesses that are managed separately. Each of these businesses requires distinct marketing and operating strategies. Management reviews financial performance based on these operating segments.

SelectBuild

SelectBuild provides construction services to high-volume homebuilders. These services include wood framing or concrete block masonry, concrete services, plumbing and other services. Construction services include managing labor and construction schedules as well as sourcing materials.

BMC West

BMC West markets and sells building products, manufactures building components and provides construction services. Products include structural lumber and building materials purchased from other manufacturers as well as manufactured building components including millwork, trusses and wall panels. Construction services include framing and installation of miscellaneous building products. Building products and construction services are sold principally to professional builders and contractors.

Corporate

Corporate represents expenses to support the operations of our business segments, SelectBuild and BMC West. These costs include administrative functions for information systems, reporting, accounts payable and human resources, professional fees for regulatory compliance, executive and senior management, certain incentive compensation as well as actuarial adjustments for insurance and medical claims. These costs are not allocated to our business segments.

The financial performance for these reporting segments is based on income from operations before interest expense, income taxes and minority interests. These segments follow the accounting principles described in the Summary of Significant Accounting Policies included in our most recent Annual Report on Form 10-K. Sales between segments are recognized at market prices and no single customer accounts for more than 10% of sales.

Selected financial information by segment is as follows (thousands):

| | | | Sales | | | Income (Loss) Before Taxes and | | | Depreciation | | | | | | | |

| | | | Total | | | Inter- Segment | | | Trade | | | Minority Interests | | | and Amortization | | | Capital (1) Expenditures | | | Assets | |

| | | | | | | | | | | | | | | | | | | | | | | |

Three Months Ended March 31, 2007 | | | | | | | |

| SelectBuild | | $ | 282,531 | | $ | (60 | ) | $ | 282,471 | | $ | 2,586 | | $ | 8,626 | | $ | 5,893 | | $ | 730,724 | |

| BMC West | | | 286,755 | | | (122 | ) | | 286,633 | | | 11,431 | | | 3,155 | | | 1,971 | | | 444,465 | |

| Corporate | | | — | | | — | | | — | | | (13,057 | ) | | 966 | | | 1,003 | | | 133,467 | |

| | | $ | 569,286 | | $ | (182 | ) | $ | 569,104 | | | 960 | | $ | 12,747 | | $ | 8,867 | | $ | 1,308,656 | |

| Interest Expense | | | | | | | | | | | | 8,218 | | | | | | | | | | |

| | | | | | | | | | | | $ | (7,258 | ) | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended March 31, 2006 | | | | |

| SelectBuild | | $ | 498,330 | | $ | (32 | ) | $ | 498,298 | | $ | 46,075 | | $ | 6,627 | | $ | 14,232 | | $ | 770,685 | |

| BMC West | | | 386,876 | | | (617 | ) | | 386,259 | | | 30,546 | | | 2,895 | | | 4,123 | | | 493,042 | |

| Corporate | | | — | | | — | | | — | | | (22,235 | ) | | 660 | | | 660 | | | 86,572 | |

| | | $ | 885,206 | | $ | (649 | ) | $ | 884,557 | | | 54,386 | | $ | 10,182 | | $ | 19,015 | | $ | 1,350,299 | |

| Interest Expense | | | | | | | | | | | | 5,590 | | | | | | | | | | |

| | | | | | | | | | | | $ | 48,796 | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| Year Ended December 31, 2006 | | | | | | | |

| SelectBuild | | $ | 1,744,092 | | $ | (12,278 | ) | $ | 1,731,814 | | $ | 148,416 | | $ | 30,002 | | $ | 33,409 | | $ | 722,328 | |

| BMC West | | | 1,515,121 | | | (1,766 | ) | | 1,513,355 | | | 124,523 | | | 12,178 | | | 33,135 | | | 487,703 | |

| Corporate | | | — | | | — | | | — | | | (75,484 | ) | | 3,104 | | | 6,174 | | | 118,880 | |

| | | $ | 3,259,213 | | $ | (14,044 | ) | $ | 3,245,169 | | | 197,455 | | $ | 45,284 | | $ | 72,718 | | $ | 1,328,911 | |

| Interest Expense | | | | | | | | | | | | 29,082 | | | | | | | | | | |

| | | | | | | | | | | | $ | 168,373 | | | | | | | | | | |

(1) Property and equipment from acquisitions are included as capital expenditures.

15. Quarterly Results of Operations

Operating results by quarter for 2007 and 2006 were as follows (thousands, except per share data):

| | | First | | Second | | Third | | Fourth | |

2007 | | | | | | | | | |

| Sales | | $ | 569,104 | | | — | | | — | | | — | |

| Income from operations | | $ | 960 | | | — | | | — | | | — | |

| Net loss | | $ | (4,966 | | | — | | | — | | | — | |

| | | | | | | | | | | | | | |

| Net income per diluted common share | | | $(0.17 | | | — | | | — | | | — | |

| Common share prices: | | | | | | | | | | | | | |

High | | | $24.93 | | | — | | | — | | | — | |

Low | | | $18.11 | | | — | | | — | | | — | |

| | | | | | | | | | | | | | |

2006 | | | | | | | | | | | | | |

| Sales | | $ | 884,557 | | $ | 921,992 | | $ | 830,599 | | $ | 608,021 | |

| Income from operations | | $ | 54,386 | | $ | 64,317 | | $ | 64,271 | | $ | 14,481 | |

| Net income | | $ | 28,069 | | $ | 34,175 | (1) | $ | 35,348 | | $ | 4,482 | |

| | | | | | | | | | | | | | |