UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K /A

þ ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended February 28, 2009

o TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____ to _____

Commission file number 0-23561

___________________________

MEXORO MINERALS LTD.

(Exact name of registrant as specified in its charter)

Colorado |

| 84-1431797 | |

(State or other jurisdiction of incorporation) |

| (IRS Employer Identification Number) | |

|

| ||

C. General Retana #706 Col. San Felipe Chihuahua, Chih. Mexico |

31203 | ||

(Address of principal executive offices) | (Zip Code) | ||

Registrant’s telephone number, including area code: 52 (614) 426 5505

Securities registered under Section 12(b) of the Act:

Title of each class

N/A

Securities registered under Section 12(g) of the Act:

Title of Each Class Name of Each Exchange on Which Registered

Common Stock, no par value OTC Bulletin Board

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yeso Noþ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yeso Noþ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yesþ Noo

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendments to this Form 10-K. þ

1

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filero Accelerated filero

Non-accelerated filero (Do not check if a smaller reporting company) Smaller reporting companyþ

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yeso Noþ

The aggregate market value of voting Common Stock held by non-affiliates of the Registrant, based upon the average of the closing bid and asked price of Common Stock on the OTC Bulletin Board system on August 29, 2008 of $0.40 was approximately $10,936,555.

As of May 30, 2009, the Registrant had 34,845,493 shares of Common Stock issued and outstanding.

EXPLANATORY NOTE

Mexoro Minerals, Ltd. is filing this Amendment No. 1 on Form 10-K/A (this "Amendment") to its Annual Report on Form 10-K for the fiscal year ended February 28, 2009, which was filed with the Securities and Exchange Commission on June 15, 2009 (the "Original Filing"), to amend certain information primarily relating to Item 8 – Financial Statements and Supplementary Data, Item 9A(T) – Controls and Procedures, and Exhibit 31.1 - Certification.

This Amendment No. 1 on Form 10-K/A does not update other items or disclosures in the Original Filing. This Amendment No. 1 on Form 10-K/A does not reflect events occurring after the filing of the Original Filing or modify or update those disclosures, including any exhibits to the Original Filing affected by subsequent events. Information not affected by the changes described above is unchanged and reflects the disclosures made at the time of the Original Filing. Accordingly, this Amendment No. 1 on Form 10-K/A should be read in conjunction with our filings made with the Securities and Exchange Commission subsequent to the filing of the Original Filing, including any amendments to those filings.

PART I

ITEM 1. BUSINESS

Background

Mexoro Minerals Ltd. (formerly known as Sunburst Acquisitions IV, Inc.) (“the Company,” or “Mexoro”) was incorporated in the State of Colorado on August 27, 1997. We were formed to seek out and acquire business opportunities. Between 1997 and 2003, we engaged in two business acquisitions and one business opportunity, none of which generated a significant profit or created a sustainable business for us.

On May 3, 2004, we completed a “Share Exchange Agreement” with Sierra Minerals and Mining, Inc. (“Sierra Minerals”), a Nevada corporation, which caused Sierra Minerals to become our wholly owned subsidiary. At the time of the share exchange transaction, Sierra Minerals held, through a joint venture with Minera Rio Tinto, S.A. de C.V. (“MRT”), a company duly incorporated pursuant to the laws of the United Mexican States, mineral concessions and options to obtain certain mineral concessions on properties in Chihuahua, Mexico. Because Sierra Minerals was not a Mexican company, it was prohibited by Mexican law from owning the mineral concessions directly. The joint venture allowed Sierra Minerals to have rights to these concessions while maintaining compliance with Mexican law. MRT was controlled, and continues to be controlled, by Mario Ayub. Concurrently with the Share Exchange Agreement, Mr. Ayub became a director, and later Chief Operating Officer, of Mexoro. In August 2005, Mexoro cancelled the joint venture agreement in order to pursue the mineral exploration opportunity through a new wholly owned Mexican subsidiary. On January 20, 2006, Sierra Minerals was dissolved.

In August 2005, we created a wholly owned Mexican subsidiary corporation, Sunburst Mining de Mexico, S.A. de C.V. (“Sunburst Mining”). On August 25, 2005, Sunburst Mining, Mexoro and MRT entered into agreements in which MRT assigned to Sunburst Mining the right to explore and exploit two properties in Mexico. MRT had previously acquired property

2

rights from the owners, Corporativo Minero, S.A. de C.V. (“Corporativo Minero”), and Compañía Minera De Namiquipa, S. A. de C. V. (“Compañía Minera”), respectively. There is no relationship between either Corporativo Minero or Compañía Minera, their officers, directors and affiliates and Mexoro’s subsidiaries, officers, directors and affiliates. Concurrent with assigning to Sunburst Mining its rights to these two properties, MRT assigned to Sunburst Mining the option, but not the obligation, to purchase additional mineral concessions on a separate property, also located in Chihuahua, Mexico.

Through Sunburst Mining, we are engaged in the exploration of four gold and silver exploration properties, each made up of several mining concessions, located in the State of Chihuahua, Mexico. (“Mining Concessions” refers to an area of land for which the owner of the concession has the right to explore for and develop mineral deposits. The rights to and ownership of the minerals in the concessions were granted, in our case, originally by the Mexican Government to the former concession owners, and then to us from those owners. In Canada and the United States, the term is commonly referred to as “Mineral Rights” or “Mining Claims.”) These properties are generally referred to as the Cieneguita Property, the Guazapares Property, the Encino Gordo Property and the Sahuayacan Property. We will own 100% of the Cieneguita Property upon completion of a payment of $2,000,000 (of which $710,000 has been paid to date) to Corp orativo Minero and we have the option to purchase the Guazapares Property and Sahuayacan Property. In August 2005, we purchased two Encino Gordo mineral concessions for $100, and we have exercised our option to purchase three additional Encino Gordo mineral concessions from an unrelated third party, all of which now comprise the Encino Gordo Property.

In December 2005, Mexoro and Sunburst Mining entered into a new agreement with MRT (the “New Agreement”). In the New Agreement, Sunburst Mining exercised its option to purchase three additional mining concessions in the Encino Gordo region. The New Agreement required the Company to issue to MRT two million shares of Mexoro’s common stock within four months of the date of the signing of the New Agreement. These shares were issued on February 23, 2006. Under the terms of the New Agreement, MRT had the option to buy all of the outstanding shares of Sunburst Mining for $100 if the Company failed to transfer $1,500,000 to Sunburst Mining by April 30, 2006. However, in April 2006, the parties amended the New Agreement to delete both the required transfer of $1,500,000 to Sunburst Mining along with MRT’s option to purchase all of the shares of Sunburst Mining. The New Agreement also requires the Company to issue one million additional shares of common stock to MRT when, if ever, production of the Cieneguita Property reaches 85% of production capacity.

On October 24, 2006, we purchased exclusive exploration rights and an option to purchase several additional mineral concessions, collectively referred to as the Sahuayacan Property, in Chihuahua, Mexico, from Minera Emilio, S.A. de C.V., (“Minera Emilio”). There is no relationship between Minera Emilio, its officers, directors and affiliates and Mexoro‘s subsidiaries, officers, directors and affiliates. In order to maintain the right to explore the Sahuayacan Property, the Company paid $30,000 upon execution of the agreement and must pay $252,000 in monthly installments over a five year term. In order to purchase the Sahuayacan Property, Mexoro must pay $300,000 in cash or $500,000 in shares of the Company within the term of the option. The Company must also pay a royalty of 3% or 4% of “Net Revenues”. Net Revenue is calculated by subtracting smelting expenses, added value taxes and all other taxes on production sales from revenu e described in detail below.

On February 13, 2006, the shareholders of the Company approved a 1:50 reverse split of its issued and outstanding common stock with one new share issued for each 50 old shares. Prior to the reverse split, the Company had 189,994,324 shares of common stock issued and outstanding. Immediately following the reverse split, the Company had 3,799,887 shares issued and outstanding. All figures relating to shares of common stock or price of shares of common stock herein reflect the 1:50 reverse split unless otherwise indicated.

We changed our name to Mexoro Minerals Ltd. on February 15, 2006. As of the date of this report, we are considered to be an exploration stage corporation, as that term is defined in the U.S. Securities and Exchange Commission’s (“SEC”) Industry Guide 7, as we are engaged in the search for mineral deposits but not engaged in the preparation of an established commercially mineable deposit for extraction or in the exploitation of a mineral deposit.

Prior Acquisitions

In August 1999, we invested $1,000,000 in Prologic Management Systems, Inc. (“Prologic”), which was engaged in the business of providing systems integration services, networking services, software development and applications software for the commercial market. The investment in Prologic was made in anticipation of a business combination with that company. As part of that transaction, we acquired 3,459,972 shares of Prologic. However, the agreement to complete a business combination was terminated prior to its consummation and in March 2000 we charged off our investment to operations.

3

In January 2001, we entered into an agreement with Prologic to recover a portion of our investment. Pursuant to that agreement, on February 16, 2001, we completed the sale of 2,859,972 shares of stock in Prologic to Prologic, or its designees, for a total sales price of $400,000. Of the sale price, $325,000 was paid in cash at closing and $75,000 through Prologic’s execution of a promissory note. The promissory note bore interest at the rate of 10% per annum and required payments of $25,000 principal, plus accrued interest, on each of April 12, 2001, July 12, 2001 and October 12, 2001, none of which were ever received by us. Subsequently, Prologic declared bankruptcy and we wrote the promissory note off as uncollectible.

We retained ownership of a total of 600,000 shares of Prologic, which we subsequently sold. Such shares were “restricted securities” as defined in Rule 144 under the Securities Act of 1933. The shares were sold in accordance with the provisions of Rule 144.

On December 4, 2000, the Company completed an agreement for share exchange between itself and HollywoodBroadcasting.com, Inc. (“HBC”), a Nevada corporation. As a result of that closing, HBC became a wholly-owned subsidiary of the Company.

HBC was a development stage company formed for the purpose of developing and producing original entertainment and information programming for various media including domestic and foreign broadcast, cable and satellite television, home video, DVD sales and rentals and the Internet. The Company was not able to generate significant revenues from any of the sources it relied upon in establishing its business model.

On September 28, 2001, the Company completed the sale of its wholly-owned subsidiary HBC for $1,000 in cash.

Prior Business Activities

On February 27, 2002, we were assigned a sub-distributorship agreement pursuant to a contract between 1357784 Ontario Ltd. and Romlight International, Inc. (“Romlight International”), a company based in Toronto, Ontario, Canada. There was no affiliation between 1357784 Ontario Ltd. and Romlight International and Prologic, HBC, Sierra Minerals, Mexoro, their officers, directors or affiliates. Pursuant to the sub-distributorship agreement, we became the exclusive worldwide distributor to the hydroponics industry of digital electronic lighting ballasts. This sub-distributorship agreement was assigned to our wholly owned subsidiary, Sunburst Digital, Inc. (“Sunburst Digital”), a Canadian corporation. In January 2003, the contract between 1357784 Ontario Ltd. and Romlight International and our sub-distributorship agreement were cancelled. On April 2, 2003, Sunburst Digital signed an agreement directly with Romlight International containing terms and conditions substantially identical to the terms of the sub-distributorship agreement.

We paid Romlight International a deposit of $183,454 for the sub-distributorship. Due to quality control issues, the ballasts were never sold, and we wrote off our entire deposit and ceased to operate Sunburst Digital. Sunburst Digital was administratively dissolved on March 31, 2006. We had no operations between the cessation of these activities and the acquisition of Sierra Minerals.

Current Operations

On May 3, 2004, we entered into a Share Exchange Agreement with the shareholders of Sierra Minerals, which was incorporated in Nevada on March 19, 2004. As a result of this transaction, Sierra Minerals became our wholly owned subsidiary. Pursuant to the Share Exchange Agreement, we agreed to loan to MRT, on behalf of Sierra Minerals, $147,500 to be evidenced by an 8% promissory note signed by MRT. In addition, and as a result of the closing of this Share Exchange Agreement, we paid a finders’ fee to two corporate entities whereby we issued an aggregate of 120,000 five year options to purchase shares of our common stock, at a price of $0.50 per share, as follows: 60,000 were issued to T.R. Winston & Company, LLC and 60,000 were issued to Liberty Management, LLC. T.R. Winston & Company, LLC, Liberty Management, LLC, and their officers, directors and affiliates are not affiliates of Mexoro, Sierra Minerals, MRT or their officers, directors, and affiliates.

Sierra Minerals had no operations between its date of incorporation and April 26, 2005. Sierra Minerals was a party to a joint venture agreement dated April 26, 2004 and amended on June 1, 2004, by and between Sierra Minerals and MRT. MRT had the right to acquire certain mineral concessions, the Cieneguita Property and Guazapares Property, as explained below. Under the terms of the joint venture, MRT and Sierra Minerals planned to form a Mexican corporation, of which Sierra Minerals would own 60% and MRT would own 40%. Sierra Minerals was required to invest $1,000,000 in this corporation within 30 days of the signing of the joint venture agreement and to secure an additional $2,000,000 line of credit for the new company. In exchange, MRT would transfer its rights in the mineral concessions to the new corporation. MRT was appointed

4

as the operator of the Cieneguita Property. Sierra Minerals advanced $167,500 to MRT, pursuant to the joint venture agreement, to pay for costs associated with the rights. However, Sierra Minerals did not meet the deadline of investing $1,000,000 into the new corporation. MRT retained the $167,500 as liquidated damages under the joint venture agreement; Sierra Minerals was not required to pay any additional damages.

The board of directors decided that it wanted to hold these mineral concessions and options for mineral concessions directly instead of through a joint venture agreement due to its belief that holding the title directly is a stronger legal position for the Company. Consequently, the joint venture agreement was cancelled and a new subsidiary formed. Once the joint venture agreement was cancelled, Sierra Minerals no longer had any rights to the mineral concessions.

On August 25, 2005, we entered into a new arrangement with MRT. Instead of a joint venture, we formed a wholly owned subsidiary, Sunburst Mining, which was incorporated in Mexico. Because Sunburst Mining is a Mexican corporation, this restructuring allowed us to take title to the properties directly in the name of Sunburst Mining rather than holding the interests in a joint venture. We entered into agreements with MRT, which gave Sunburst Mining options to purchase the mineral concessions of the Cieneguita and Guazapares Properties and the right of first refusal on two Encino Gordo Properties. The parties also entered into an operating agreement (which has subsequently been cancelled) that gave MRT the sole and exclusive right and authority to manage the Cieneguita Property. (This right had also been granted to MRT under the joint venture agreement with Sierra Minerals.)

The material provisions of the Company’s property agreements are as follows:

(1) | MRT assigned to Sunburst Mining, with the permission of Corporativo Minero (the “Cieneguita Owner”), all of MRT’s rights and obligations acquired under a previous agreement, the “Cieneguita Option Agreement”, including the exclusive option to acquire the Cieneguita concessions for a price of $2,000,000. The Cieneguita Option Agreement states that the Company is to make yearly payments on May 6 of each year in the amount of $120,000 for the next 13 years and a final payment of the outstanding balance owed on the $2,000,000 in the 14th year to the Cieneguita Owner to keep the option in good standing. The Company renegotiated the payment due May 6, 2007, to $60,000 payable on November 6, 2007, which was paid and the balance of $60,000 was paid on December 20, 2007. Once the full $2,000,000 payment has been made, we will own the concessions. Yearly payments will need to be made from working capital. We d o not have the capital at this time to fund the ongoing payments. We will need to raise the funds through the sale of debt or equity. We do not have any sources for such capital at this time. In the alternative, if Cieneguita is put into production, of which there is no guarantee, we must pay the Cieneguita Owner $20 per ounce of gold produced, if any, from the Cieneguita concessions up to the total $2,000,000 due. In the event that the price of gold is above $400 per ounce, the property payments payable to the Cieneguita Owners from production will be increased by $0.10 for each dollar increment the spot price of gold trades over $400 per ounce. The total payment of $2,000,000 does not change with fluctuations in the price of gold. Non-payment of any portion of the $2,000,000 total payment will constitute a default. In such case, the Cieneguita Owners will retain ownership of the concessions, but we will not incur any additional default penalty. MRT retained no interest in the Cieneguita Property. |

(2) | MRT assigned Sunburst Mining, with the consent of Compañía Minera (the “Guazapares Owner”) MRT’s rights and obligations concerning the Guazapares Property, including the exclusive option under the “Guazapares Option Agreement”, for a term of four years, to purchase seven of the Guazapares concessions upon payment of $910,000. In return, Sunburst Mining granted MRT a 2.5% Net Smelter Royalty (“NSR”) and the right to extract from the Guazapares concessions up to 5,000 tons per month of rock material; this right will terminate on exercise of the option to purchase the concessions. MRT retained no interest in the Guazapares Property. |

(3) | Sunburst Mining purchased two of the Encino Gordo concessions from MRT for a price of 1,000 pesos (approximately US$90), and MRT assigned to Sunburst Mining a first right of refusal to acquire three additional Encino Gordo concessions. The Company has the option to acquire 100% of the additional three Encino Gordo concessions subject to a 2.5% NSR and the obligation to make the scheduled property payments totaling $500,000. |

5

(4) | MRT assigned to Sunburst Mining, for a term of 60 months, commencing from June 25, 2004 (the “Option Period”), with the consent of Minera Rachasa, S.A. de C. V. (the “San Francisco Concessions Owner”), MRT’s rights and obligations acquired under the “San Francisco Option Agreement”, including the option to purchase the San Francisco concession for a price of $250,000 (the “Purchase Price”). MRT and the San Francisco Concessions Owner reserved a combined 2.5% NSR. MRT reserved no other rights in the San Francisco concessions. To maintain the option, Sunburst Mining assumed the obligation to pay to the San Francisco Concessions Owner cumulative annual payments totaling $90,000; if the option is exercised prior to the expiration of the Option Period by payment of the Purchase Price, the obligation to pay the annual payments will be terminated. |

(5) | MRT assigned to Sunburst Mining, with the consent of the Rafael Fernando Astorga Hernández (“San Antonio Concessions Owner”), MRT’s rights and obligations acquired under the San Antonio Option Agreement, including the option to purchase the San Antonio concessions for a price of $500,000 (the “Purchase Price”) commencing from January 15, 2004, the date of signing of the “San Antonio Option Agreement” (the “Option Period”). MRT and the San Antonio Concessions Owner reserved a combined 2.5% NSR to be paid to them. MRT reserved no other rights in the San Antonio concessions. To maintain the option, Sunburst Mining assumed the obligation to pay to the San Antonio Concessions Owner cumulative annual payments totaling $150,000; if the option is exercised prior to the expiration of the Option Period by payment of the Purchase Price, the obligation to pay the annual payments will be terminated. The San Antonio Concessions Owner reserved the right to extract from the San Antonio concessions up to 50 tonnes per day of rock material; this right will terminate on the date of the exercise of the option. |

Also on August 25, 2005, the parties signed an operator’s agreement (which has subsequently been cancelled, as discussed below) pursuant to which Sunburst Mining engaged MRT as the operator of the Cieneguita Property. MRT was to be paid an operator’s fee based on the functions performed and an operator’s bonus equal to 10% of the net proceeds of production if operating cash costs did not exceed $230 per ounce of gold produced from the Cieneguita Property. The operator’s fee was to be: (a) with respect to programs: (i) 2% for each individual contract which expressly includes an overhead charge by the party contracted; (ii) 5% for each individual contract which exceeds $50,000; (iii) 15% of all other costs not included; (b) with respect to construction: 2 % of all other such costs; (c) 3.5% of operating costs after the completion of construction on Cieneguita. MRT’s duties were to (a) comply with the provisions of all agreements or instruments of title under which the Cieneguita Property or assets were held; (b) pay all costs properly incurred promptly as and when due; (c) keep the Cieneguita Property and assets free of all liens and encumbrances arising out of the mining operations and, in the event of any lien being filed as aforesaid, proceed with diligence to contest or discharge the same; (d) perform such assessment work or make payments in lieu thereof and pay such rentals, taxes or other payments and do all such other things as may be necessary to maintain the Cieneguita Property in good standing, (e) maintain books of account in accordance with generally accepted accounting principles provided that the judgment of the operator, as to matters related to the accounting, shall govern if the operator’s accounting practices are in accordance with accounting principles generally accepted in the mining industry in Canada; (f) perform its duties and obligations in accordance with sound mining and engineering practices and other p ractices customary in the Canadian mining industry, and in substantial compliance with all applicable federal, state and municipal laws of Mexico; and (g) prepare and deliver reports.

The parties also signed a share option agreement pursuant to which Sunburst Mining granted to MRT the exclusive option to acquire up to 100% of all outstanding shares of Sunburst Mining if Mexoro did not (a) comply with the terms of the underlying Cieneguita Option Agreement, the San Antonio Option Agreement, the San Francisco Option Agreement and the Guazapares Option Agreement and (b) loan to Sunburst Mining the amounts of $1,000,000 by December 31, 2005 and $1,000,000 by April 30, 2006. If the option to purchase 100% of the shares of the capital of Sunburst Mining were exercised by MRT, MRT was obligated to return to the Company for cancellation all of the shares of the capital of Mexoro issued by the Company to MRT and Mario Ayub. No finder’s fees were paid in these agreements.

On December 8, 2005, Mexoro and Sunburst Mining entered into a new agreement with MRT (the “New Agreement’) to exercise their option under the August 18, 2005 “Sale and Purchase of Mining Concessions Agreement” to obtain two mining concessions in the Encino Gordo region. The New Agreement modified the Company’s property agreements, as discussed below. The following are additional material terms of the New Agreement:

(1) | The share option agreement with MRT was cancelled. |

6

(2) | The Company granted MRT the option to buy all of the outstanding shares of Sunburst Mining for $100 if the Company failed to transfer $1,500,000 to Sunburst Mining by April 30, 2006. On April 6, 2006, MRT agreed to waive its option to purchase the shares of Sunburst Mining and also waived Mexoro’s obligation to transfer $1,500,000 to Sunburst Mining. |

(3) | The property agreements were modified to change the NSR to a maximum of 2.5% for all properties covered by the Agreements. The property agreements contained NSRs ranging from 0.5% to 7%. |

(4) | The Company agreed to issue 2,000,000 shares of the Company to MRT within four months of the date of the signing of the New Agreement. These shares were issued to MRT and its assignee, Etson, Inc., on February 23, 2006. This issuance fulfilled the Company’s payment obligations under the previous property agreements. |

(5) | The Company agreed to issue 1,000,000 additional shares of the Company’s common stock to MRT when the Cieneguita Property is put into production, if ever, and it reaches 85% of production capacity over a 90-day period, as defined in the New Agreement. |

(6) | The New Agreement gave Sunburst Mining the option to obtain three additional concessions in the Encino Gordo region. |

(7) | The operator’s agreement with MRT was cancelled. |

Unless explicitly superseded or terminated by the New Agreement, as discussed above, the terms of the Company’s existing property agreements remain in effect. Under the New Agreement, MRT has assigned to Sunburst Mining rights it acquired in a contract with Corporativo Minero. MRT entered into an agreement with Corporativo Minero on January 12, 2004 by which it acquired the right to explore and exploit the Cieneguita Property and purchase it for $2,000,000. MRT paid $150,000 upon execution of the agreement and two months later paid $200,000. This agreement gave MRT the exclusive right and option, but not the obligation, to purchase, during the term of the mining concessions of the property, an undivided 100% title to the mining concessions and the exclusive right to carry out mining activities on any portion of the mining concessions. Under our agreements with MRT, MRT has assigned this agreement and all of its rights and obligations there under, to us. As of the date of this annual report, $710,000 of the $2,000,000 has been paid to Corporativo Minero by MRT ($350,000 paid) and Sunburst Mining ($360,000 paid in “no production” penalty fees). Sunburst Mining had the obligation of bringing the property to production on or prior to May 6, 2006. The Cieneguita Property was not in production as of May 6, 2006 and, therefore, Sunburst Mining had the obligation to pay $120,000 to Corporativo Minero on May 6, 2006 to extend the contract. Through discussions with Mexoro, Corporativo Minero agreed to reduce the obligation to $60,000, of which $10,000 was paid in April 2006. Sunburst Mining was then required to pay the remaining $50,000 by May 6, 2006. We made this payment to Corporativo Minero and the contract was extended. The Company renegotiated the payment due May 6, 2007, to $60,000 payable on November 6, 2007, which was paid and the balance of $60,000, which was paid on December 20, 2007. Payment of $60,000 on the $120,000 that was due to the co ncession holders was made in May 2008 with the balance of the payment due to be paid in June 2008. We have the obligation to pay a further $120,000 per year on May 6 of each year, until the total of $2,000,000 is paid. We are currently not in default on our payments.

If the property is put into production, of which there is no assurance, then the contract calls for the remaining payments to be paid from the sale of gold, up to a total of $2,000,000. The payments, if the property should go into production, would be as follows: Any remaining amount of the $2,000,000 payment would be paid out of production from the Cieneguita Property at a rate of $20 dollars per ounce of gold sold. However, in the event that the price of gold exceeds $400, then Sunburst Mining would be required to pay an additional $0.10 per each ounce for every dollar the spot price of gold trades over $400. For example, at $900 per ounce gold price, the royalty payment would be $70 per ounce of gold produced. Once $2,000,000 is paid, there is no further obligation to Corporativo Minero. Non-payment of any portion of the $2,000,000 total payment will constitute a default. In such case, Corporativo Minero would retain ownership of the concessions, but we will not incur any additional default penalty. Corporativo Minero has the obligation to pay, from the funds they receive from us, any royalties that may be outstanding on the properties from prior periods. Corporativo Minero has informed us that there were royalties of up to 7% NSR owned by various former owners of the Cieneguita Property. They have informed us that the corporations holding those royalties have been dissolved and that there is no further legal requirement to make these royalty payments. We can make no assurance that we will not ultimately be responsible to pay all or some of the 7% NSR to these former royalty holders if the property was ever put into production and Corporativo Minero did not make the payments to the royalty holders. MRT no longer has any ownership interest or payment obligations with respect to any of the Cieneguita concessions.

7

On May 15, 2006, Sunburst Mining entered into an exploration contract with Jose Maria Rascon Rascon and Sabino Amador Rascon Polanco and with Rene Muro Lugo (all three representatives constitute the “Concessionaires”) for the Segundo Santo Nino concession on the Sahuayacan Property. Each concession representative owns 33.3% of the total Segundo Santo Nino title. The Company must pay the Concessionaires a total of $255,000 for this concession. The total payments to acquire 100% of this concession are as follows: all payments up to November 15, 2008 totaling $85,000 have been paid, May 15, 2009 - $20,000 ($3,333 paid, balance to be paid in June 2009), November 15, 2009 - $30,000 and May 15, 2010 - $120,000.

On June 21, 2006, Sunburst Mining entered into an Exploration and Sale Option Agreement of Mining Concessions (the “Exploration Agreement”) with Minera Emilio for mineral concessions in Chihuahua, Mexico on the Sahuayacan Property. Minera Emilio owns 100% of the Sahuayacan Property. There is no affiliation between Minera Emilio and the Company or its officers, directors or affiliates.

Under the Exploration Agreement, Minera Emilio granted the Company the exclusive right to conduct exploration on the Sahuayacan Property. The Company must pay Minera Emilio $282,000 in the following manner: (i) $30,000 payable at the execution of the Agreement (paid); (ii) $2,500 per month as of August 21, 2006, and so on for each month elapsed for twelve months, on the 21st day of each month (these amounts have been paid); (iii) $3,500 per month as of the beginning of the second yearly term, that is, as of August 21, 2007, and every month, on the 21st day of each month, for the whole second yearly term (these amounts have been paid); and (iv) $5,000 monthly, during the third, fourth, and fifth yearly term, on the 21st. day of each month (we have yet to pay the March, April and May 2009 payments, which we are negotiating for extension). The term of the Exploration Agreement is five years from the date of execution by Minera Emilio, which is June 22, 2011. While Minera Emilio signed the agreement on June 22, 2006, further negotiations occurred and the Company signed the agreement on October 24, 2006. Non-payment of any of the payments owed would constitute a default under the Exploration Agreement. As of the date of this annual report, we have not been given notice of any default. In the event we were given notice and default was not cured in a timely manner, the Company would lose the right to explore on the Sahuayacan Property and would lose the option to purchase the mineral concessions.

Minera Emilio also granted the Company the option to purchase the mineral claim. The option shall expire on June 22, 2011. The Company must provide Minera Emilio with 30 days written notice before exercising the option. The purchase price of the mineral claim is $300,000 or the equivalent of $500,000 in restricted shares of common stock of Mexoro based upon the market value of such shares during the 30 days preceding notice of the intent to exercise the option. The Company must complete a feasibility survey within three years from the date the option is exercised.

After exercising the option, the Company must pay Minera Emilio royalties on any mineral ore that is sold from the mineral claim. The rate of the royalties due varies based on the price of gold on the London Metal Exchange (the “Price”). If the Price is less than or equal to $600 per ounce, the royalty due is 3% of Net Revenue. If the Price is higher than $600 per ounce, the royalty due is 4% of the Net Revenue. Net Revenue is calculated by subtracting smelting expenses, added value taxes, and all other taxes on production sales from revenue.

On January 25 2008, Sunburst Mining entered into an exploration and option agreement with Maria Luisa Wong Madrigal for mineral concessions under the “La Maravilla” project on the Sahuayacan Property. The Company must pay Maria Luisa Wong Madrigal $600,000 in the following manner: (i) $33,000 – January 25, 2008 (paid); (ii) $33,000 – July 25, 2008 (paid); (iii) $34,000 – January 25, 2009 (outstanding, negotiating for extension); (iv) $500,000 – at the option to purchase the concession or in 36 months – January 25, 2010.

The La Maravilla project concessions are subject to royalties of 2.0% over net liquidations, which may be acquired by Sunburst Mining for $400,000 before commercial production is initiated. This exploration and option agreement has yet to be filed before the Mining Public Records Office as of the date of this report.

In addition, we intend to identify and obtain options on additional gold and silver properties within the Chihuahua region, if possible. We will utilize our management’s contacts in the Mexican mining community in order to find potential properties that may be available. There can be no assurance that we will be able to obtain any additional property on acceptable terms or at all.

On September 19, 2007, Sunburst Mining, MRT and Mexoro entered into an agreement to defer Guazapares Property payments. This agreement modifies the agreement entered into by MRT and Sunburst Mining on August 18, 2005 in regard to the Guazapares concessions in Mexico. Under the original agreement entered into by the parties on August 18, 2005, Sunburst Mining was obligated to pay MRT US$60,000 on August 2, 2006 as part of the payments required for the purchase of eight mineral concessions in the Guazapares area of Mexico. On July 18, 2006 the parties agreed to extend the due date

8

for ninety days until October 31, 2006. MRT agreed to re-extend the due date for such payment by 120 days until February 28, 2007 and then again to May 31, 2007. An oral agreement extended the due date to August 31, 2007. Pursuant to the same agreement entered into by the parties on August 18, 2005, Sunburst Mining was obligated to pay MRT a further amount of US$140,000 on August 2, 2007 to purchase the Guazapares concessions.

Under the September 17, 2007 agreement, Sunburst Mining, MRT and Mexoro agree that:

● | Any and all property payments regarding Guazapares, then owing to MRT or which would otherwise become due by December 31, 2007, will be deferred until such time as Sunburst Mining and Mexoro have sufficient funds to make the payments, in the opinion of the disinterested directors of Mexoro and, |

● | Mexoro issued 250,000 shares to MRT and/or assignees, in consideration for the deferral of any and all Guazapares property payments then outstanding or those arising on or before December 31, 2007. |

On May 5, 2008, we signed a letter of intent (Paramount “LOI”) to enter into a strategic alliance with Paramount Gold and Silver Corp. (“Paramount”) to combine mining and exploration expertise, along with efficient use of personnel, drill rigs and current mining concessions to improve efficiencies and potentially reduce costs for both companies. We believed that the alignment of interest between the two companies created synergy, especially as the two companies’ Guazapares projects are contiguous and create a large land position located in the state of Chihuahua, Mexico.

The Paramount LOI called for Paramount to invest a minimum of $4 million and maximum of $6 million into the Company, at a fixed price of $0.50 per unit by June 23, 2008. This date was extended until July 21, 2008 and then to August 5, 2008. Paramount was unable to complete the minimum investment on August 5, 2008 and as such the strategic alliance with Paramount was terminated on August 6, 2008. Prior to the termination, we issued three debentures to Paramount.

On May 9, 2008, we issued a secured convertible debenture (the “Debenture”) with a one-year term in the amount of $500,000. In connection with the issuance of the Debenture, we entered into a “Security Agreement” with Paramount that secures our assets until there has been full compliance with the terms of the Debenture. Paramount may convert all or a portion of the principal amount of the Debenture into units consisting of one share of our common stock and half a warrant to purchase one share of our common stock. Subject to certain adjustments upon the occurrence of various capital reorganizations and other events, the units are convertible at $0.50 per unit for a total of up to 1,000,000 shares of common stock and up to 500,000 warrants at $0.75 to purchase shares of common stock (the “Warrants”). The Warrants have a term of four years from the date that Paramount converts the Debenture or the portion of the Debenture cover ing those warrants. A holder of the Warrants may exercise those Warrants at $0.75 (subject to adjustments upon the occurrence of certain events like stock splits).

On June 23, 2008, we signed an addendum to the strategic alliance granting Paramount an extension for the closing of the transaction until July 21, 2008. As such, Paramount invested an additional $70,000 on June 10, 2008 and $300,000 on June 23, 2008 into the Company under the same terms as the original secured convertible debenture. This debenture is convertible into 740,000 shares of our common stock and up to 370,000 warrants, which are exercisable into shares of our common stock at $0.75 per share.

On July 16, 2008, we received an additional payment from Paramount in the amount of $500,000 pursuant to the strategic alliance. This additional advance allowed Mexoro to continue its ongoing drill program on both the Cieneguita and Guazapares projects. The funds are advanced by way of a secured convertible debenture which bears interest at a rate of 8% per annum for a term of one year. Paramount had the option to convert the debt into units. Along with this additional advance, Mexoro agreed to extend the closing deadline of the strategic alliance transaction until August 5, 2008 with Paramount's continued commitment to fund Mexoro's operating expenses.

On August 6, 2008, the strategic alliance between Mexoro and Paramount was terminated, including Paramount’s right of first refusal on financings. As a result of Paramount holding convertible debentures in the amount of $1,370,000 resulting from advances made to Mexoro Minerals to fund exploration, they agreed to defer interest payments on the advances until September 10, 2008. The September 10, 2008 interest payment date was subsequently extended again to November 10, 2008. All interest payments were brought up to date by December 30, 2008 and we are now current with all of our interest payments to Paramount Gold and Silver Corp.

Subsequent to the year ended February 28, 2009, in March, 2009, we entered into an agreement with Paramount Gold and Silver Corp. (“Paramount”) restructuring our payment terms on the three outstanding secured convertible debentures held by Paramount. Under the terms of the agreement we paid Paramount $1,000,000 to cancel two debentures held by them,

9

the first debenture issued May 9, 2008 for $500,000 and the third debenture issued to them July 11, 2009 for $500,000. We also amended the second debenture that we issued to them in June 18, 2009 in the face amount of $370,000. The amount of that debenture was increased to $521,047.37 which, among other things, includes interest accrued to March 31, 2009. We are obligated to make a payment on March 31, 2009 on this debenture in the amount of $393,547.37 (of which $300,000 was paid on March 31, 2009) and the balance of $127,500 is to be re-paid on April 30, 2009. This remaining amount of $127,500 is interest free as long as the debenture remains in good standing. As part of a restructuring fee, we issued to Paramount 150,000 shares of our common stock. As we were granted an extension for the balance of the March 31, 2009 payment, we have issued an additional 100,000 shares to Paramount as an extension fee. As part of the agreemen t, Paramount has released its security interest on our Cieneguita properties. The other security as described in the original security agreement issued with the original debentures remains in place until the amended debenture has been repaid in full.

Subsequent to the year ended February 28, 2009, in May , 2009 we entered into a letter of agreement to sell our Guazapares project located in southwestern Chihuahua, Mexico to Paramount Gold de Mexico, SA de C.V., the Mexican subsidiary of Paramount Gold and Silver Corp. (“Paramount”) for a total consideration of up to $5.3 million USD. The sale is subject to the signing of a definitive agreement by June 2, 2009 and to the satisfaction of various conditions precedent prior to closing. Closing is scheduled prior to the end of June 2009 and a 5.7% commission is payable on the closing of the sale.

Mexoro’s Guazapares project comprises 12 claims close to Paramount’s San Miguel discovery. The purchase price is to be paid in two stages. The first payment of $3.7 million will be deposited into escrow at closing, and will be released from escrow to Mexoro when the transfer of the 12 claims to Paramount is finalized. An additional payment of $1.6 million is due to Mexoro if, within 36 months following execution of the letter of agreement, either (i) Paramount Gold de Mexico SA de C.V. is sold by Paramount, either through a stock sale or a sale of substantially all of its assets, or (ii) Paramount’s San Miguel project is put into commercial production. As such, the final repayment of the outstanding loan with Paramount has been deferred until the closing of the sale of the Guazapares properties. Interest will accrue on the outstanding amount at 8% per annum and the final payment will be deducted from the first $3.7 million purchase price payable to us.

On February 12, 2009 we entered into a definitive agreement for development of Cieneguita project with Minera Rio Tinto, a private Mexican corporation whose president was a former president of our Company. The definitive agreement covers project financing of up to USD $9,000,000. The major points of the agreement are as follows:

1.

Minera Rio Tinto (“MRT”) and/or its investors will subscribe for up to USD$1 million of a secured convertible debenture at 8% interest (payable in stock or cash). The debenture is convertible into units at $0.60 per unit. Each unit comprises 2 common shares and 1 warrant. Each warrant is exercisable at $0.50 per share for a period of 3 years. The placement will be used for continued exploration of our properties and general working capital. As of May 15, 2009 MRT had contributed the $1 million.

2.

MRT is to provide the necessary working capital to begin and maintain mining operations estimated to be $3,000,000 used for the purpose of putting the Cieneguita property into production. MRT will spend 100% of the money to earn 75% of the net cash flow from production. The agreement will limit the mining to the mineralized material that is available from surface to a depth of 15 meters or approximately 10% of the mineralized material found to date. It is anticipated that production at the rate of 750 tonnes per day will commence by July 2009.

3.

MRT will spend up to USD $5 million to take the Cieneguita property through the feasibility stage. In doing so, MRT will earn a 60% interest in Mexoro’s rights to the property. After the expenditure of the $5 million all costs will be shared on a ratio of 60% to MRT and 40% to Mexoro Minerals. If we elect not to pay our portion of costs after the $5 million has been spent, our position shall revert to a 25% carried interest on the property.

4.

Portions of the joint venture agreement require we obtain consent from Paramount Gold and Silver Corporation, our secured convertible debenture holder or we repay the debenture held by Paramount Gold and Silver Corporation. Those portions of the agreement that need consent will not be undertaken until such consent is obtained or extinguished by repayment. Subsequently, we repaid approximately $1,300,000 of the debenture owed to Paramount Gold and Silver Corp and in doing so, Paramount agreed to release the Cieneguita property as part of its security under the debenture. Therefore, we no longer need the consent of Paramount to begin extraction of mineralized material at Cieneguita.

5.

The Spanish version of this agreement is the governing agreement in case of dispute between the English version and the Spanish versions.

Principal Products

10

Our principal product is the exploration for, and, if warranted, the mining and sale of precious minerals. Because our properties are in the exploration stage, there is no guarantee that any ore body will be found.

Francisco Quiroz, the Company’s President and chief operating officer, has been able to discuss and obtain information on additional potential mining properties. A potential mining property is identified first by a visit to the property by a geologist. If the property has potential, based upon the geologist’s findings, another visit is made to gather more information by taking surface samples and mapping the property. Also, geophysical work (in this case mineral exploration techniques using electromagnetic instruments to measure the conductivity of the rocks underground) may be performed before entering into the negotiation process for a particular property. To date we have not entered into any agreements to acquire additional potential mining properties and no assurance may be given that such agreements will ever be entered into.

Glossary of Certain Mining Terms

ASSAY -- A chemical test performed on a sample of ores or minerals to determine the amount of valuable metals contained.

AURIFEROUS ZONE -- An area of gold bearing rock.

BRECCIA -- A rock in which angular fragments are surrounded by a mass of fine-grained minerals.

BROWNFILEDS EXPLORATION -- While loosely defined, the general meaning of brownfields exploration is that which is conducted within geological terranes within close proximity to known ore deposits.

COLUMN TEST -- The process of putting sample ore in a PVC pipe 500 centimeters in diameter and 2-3 meters high and applying lime and a cyanide solution. The purpose of a column leach test is to collect kinetic information on the ore being evaluated so that scale-up equations can be validated which will allow the projection of the commercial heap leach operation's performance under different operating scenarios.

DEVELOPMENT DRILLING -- Drilling to establish accurate estimates of mineral reserves.

DILUTION (mining) -- Rock that is, by necessity, removed along with the mineralized ore in the mining process, subsequently lowering the grade of the ore.

EPITHERMAL DEPOSIT -- A mineral deposit consisting of veins and replacement bodies, usually in volcanic or sedimentary rocks, containing precious metals, or, more rarely, base metals.

EXPLORATION -- Work involved in searching for ore, usually by sampling rocks, drilling or driving a drift.

HEAP LEACHING -- A process involving the percolation of a cyanide solution through crushed ore heaped on an impervious pad or base to dissolve minerals or metals out of the ore.

HIGH GRADE -- Rich ore. As a verb, it refers to selective mining of the best ore in a deposit.

HYDROTHERMAL -- An adjective applied to heated or hot magmatic emanations rich in water, to the processes in which they are concerned, and to the rocks, ore deposits, alteration products and springs produced by them.

INDICATED MINERAL RESOURCE -- An ‘Indicated Mineral Resource’ is that part of a mineral resource for which quantity, grade or quality, densities, shape and physical characteristics, can be estimated with a level of confidence sufficient to allow the appropriate application of technical and economic parameters, to support mine planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes that are spaced closely enough for geological and grade continuity to be reasonably assumed. Under SEC standards this term is not a recognized term in Industry Guide 7.

INFERRED MINERAL RESOURCE -- An ‘Inferred Mineral Resource’ is that part of a mineral resource for which quantity and grade or quality can be estimated on the basis of geological evidence and limited sampling and reasonably assumed,

11

but not verified, geological and grade continuity. The estimate is based on limited information and sampling gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes. Under SEC standards this term is not a recognized term in Industry Guide 7.

LEACHABILITY -- The ability for cyanide solution in a heap leach operation to leach the desirable minerals from the host rock and allow for recovery at an economic level.

MINERAL -- A naturally occurring homogeneous substance having definite physical properties and chemical composition and, if formed under favorable conditions, a definite crystal form.

MINERAL RESERVE -- A mineral reserve is the economically mineable part of a measured or indicated mineral resource demonstrated by at least a preliminary feasibility study. This study must include adequate information on mining, processing, metallurgical, economic and other relevant factors that demonstrate, at the time of reporting, that economic extraction can be justified. A mineral reserve includes diluting materials and allowances for losses that may occur when the material is mined.

MINERAL RESOURCE -- A mineral resource is a concentration or occurrence of diamonds, natural solid inorganic material, or natural solid fossilized organic material including base and precious metals, coal, and industrial minerals in or on the earth’s crust in such form and quantity and of such a grade or quality that it has reasonable prospects for economic extraction. The location, quantity, grade, geological characteristics and continuity of a mineral resource are known, estimated or interpreted from specific geological evidence and knowledge.

MINERALIZATION -- The act or process of mineralizing.

MINERALIZED MATERIAL OR DEPOSIT -- A mineralized body which has been delineated by appropriate drilling and/or underground sampling to support a sufficient tonnage and average grade of metal(s). Under SEC standards, such a deposit does not qualify as a reserve until a comprehensive evaluation, based upon unit cost, grade, recoveries, and other factors, concludes economic feasibility.

MINING CONCESSION -- A term used to describe an area of land for which the owner of the concession has the right to explore for and develop mineral deposits. The rights to and ownership of the minerals in the concession are granted, in our case, by the Mexican Government to the former owners who then either transferred or optioned them to us. In Canada and the United States, the term is commonly referred to as a Mineral Right or Mining Claim.

NET SMELTER RETURN (“NSR”) -- A share of the net revenues generated from the sale of metal produced by a mine.

ORE -- Mineralized material that can be mined and processed at a positive cash flow.

OREBODY -- A natural concentration of valuable material that can be extracted and sold at a profit.

PRELIMINARY FEASIBILITY STUDY -- A preliminary feasibility study is a comprehensive study of the viability of a mineral project that has advanced to a stage where the mining method, in the case of underground mining, or the pit configuration, in the case of an open pit, has been established and an effective method of mineral processing has been determined, and includes a financial analysis based on reasonable assumptions of technical, engineering, legal, operating, economic, social, and environmental factors and the evaluation of other relevant factors which are sufficient for a qualified person, acting reasonably, to determine if all or part of the mineral resource may be classified as a mineral reserve.

QUALIFIED PERSON -- An individual who is an engineer or geoscientist with at least five years of experience in mineral exploration, mine development or operation or mineral project assessment, or any combination of these; has experience relevant to the subject matter of the mineral project and the technical report; and is a member or licensee in good standing of a professional association. Under SEC standards this term is not a recognized term in Industry Guide 7 but is more commonly used in Canadian National Instrument 43-101.

RECLAMATION -- The restoration of a site after mining or exploration activity is completed.

ROYALTY -- An amount of money paid at regular intervals by the lessee or operator of an exploration or mining property to the owner of the ground. The royalty, generally, is based on a certain amount per ton or a percentage of the total production or profits. Also, the fee paid for the right to use a patented process.

12

SILVER PAN AMALGAMATION MILL -- The raw ore is wet crushed with stamps, the crushed ore is separated from the slurry in a settling tank and then the crushed ore is charged with mercury (approximately 10% of the weight of the ore) in the amalgamation pan. The amalgam is separated from the slurry and the silver and gold is separated from the amalgam with a retort.

STRIKE LENGTH -- The actual or estimated length, generally measured in meters, of a mineralized structure.

VEIN -- A mineralized zone having a more or less regular development in length, width and depth, which clearly separates it from neighboring rock.

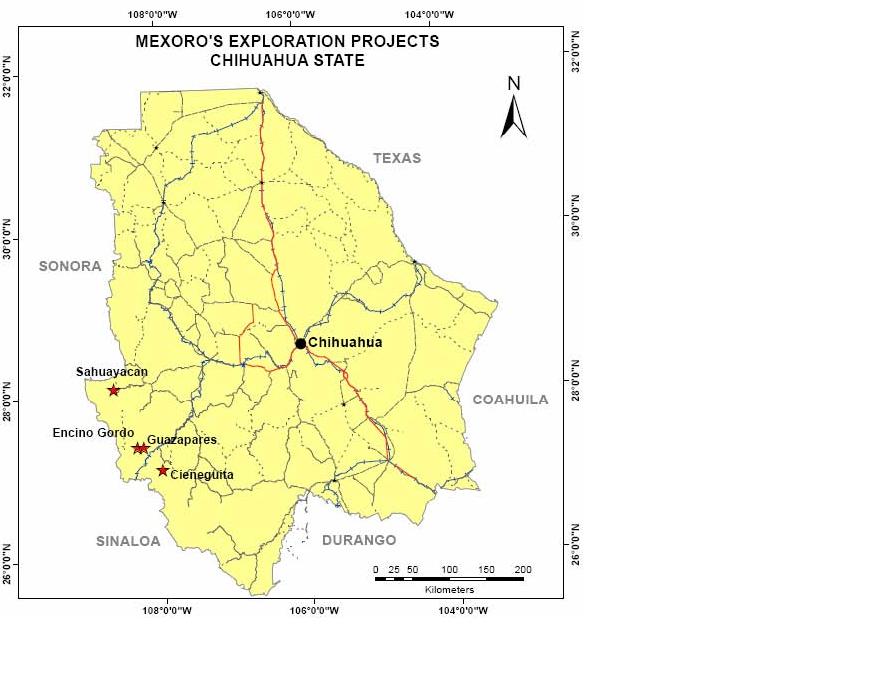

ITEM 2. PROPERTIES

All of the properties discussed below are located in the State of Chihuahua, Mexico. The following map illustrates the locations of Chihuahua and of the properties:

Location of Cieneguita, Encino Gordo and Guazapares Properties in Chihuahua, Mexico

13

Cieneguita Property

Property Location

The Cieneguita Property is located in the Baja Tarahumara in Cieneguita Lluvia De Oro, an area of canyons in the Municipality of Urique, in southwest Chihuahua, Mexico. The property is located within one half mile of the small village of Cieneguita Lluvia de Oro. Access to the property is by an all weather dirt road. There is available electrical power for the property generated by diesel generators at Cieneguita Lluvia de Oro.

Claim Status and Licensing

The Cieneguita Property is currently owned by Corporativo Minero. Sunburst Mining has the option of purchasing the concessions under the payment plan discussed below. The concessions of this project cover a total area of 822 hectares (approximately 2,031 acres). The following table is a summary of the concessions on the Cieneguita Property:

Lot Name | Title Number | Area (Ha) | Term of Validity(2) | Royalties and Payments |

|

|

|

|

|

Aurifero | 196356 | 492.00 | 7/16/1993 to 7/15/2043 | (1) |

|

|

|

|

|

Aurifero Norte | 196153 | 60.00 | 7/16/1993 to 7/15/2043 | (1) |

|

|

|

|

|

Aquilon Uno | 208339 | 222.1077 | 9/23/1998 to 9/22/2048 | (1) |

|

|

|

|

|

La Maravilla | 190479 | 48.00 | 4/29/1991 to 4/24/2041 | (1) |

|

|

|

|

|

|

|

|

|

|

(1) The Cieneguita concessions are all under an option to purchase for $2,000,000 of which $710,000 has been paid. MRT paid $150,000 upon execution of the agreement with Corporativo Minero and two months later paid $200,000. Because the Cieneguita property was not in production by May 6, 2006, Sunburst Mining was required to pay $120,000 to Corporativo Minero to extend the contract. Through discussions with Mexoro, Corporativo Minero agreed to reduce the obligation to $60,000, of which $10,000 was paid in April 2006. Sunburst Mining was then required to pay the remaining $50,000 by May 6, 2006. We made this payment to Corporativo Minero so the contract has been extended. The Company renegotiated the payment due May 6, 2007, to $60,000 payable on November 6, 2007, which was paid and the balance of $60,000 was paid on December 20, 2007. We paid $60,000 on May 12, 2008 of the $120,000 due on May 6, 2008, and the balance was paid in June 2008. We paid $30,000 on May 22, 2009 of the $120,000 payment due on May 6, 2009. We’ve verbally negotiated to pay the balance of $90,000 in three equal monthly payments from June 2009 to August, 2009. We are not in default on our payments. We have the obligation to pay a further $120,000 per year for the next 13 years and the balance of payments in the 14th year, until the total of $2,000,000 is paid. If the property is put into production, of which there is no assurance, then the contract calls for the remaining payments to be paid from the sale of gold, to avoid termination of the agreement.

The payments, if the property should go into production, would be as follows: The remainder of the $2,000,000 payment will be paid out of production from the Cieneguita Property at a rate of $20 dollars per ounce of gold sold. However, in the event that the price of gold is in excess of $400, then Sunburst Mining is required to accelerate payments by an additional $0.10 per each ounce for every dollar of gold priced over $400. The total payment we are liable for is $2,000,000. Once that amount is paid, we have no further obligation to Corporativo Minero. Corporativo Minero has the obligation to pay, from the funds they receive from us, any royalties that may be outstanding on the properties from prior periods. Corporativo Minero has informed us that there were royalties up to 7% NSR owned by various former owners of the property. They have informed us that the corporations holding those royalties have been dissolved and t hat there is no further legal requirement to make these royalty payments. We can make no assurances that we will not ultimately be responsible to pay all or some of the 7% NSR to these former royalty holders if the property were ever put into production and Corporativo Minero did not make the payments to the royalty holders. However, we do not see this potential for additional royalty payments as a material risk to us.

(2) Amendments to the Mexican mining laws took effect with the publication on December 21, 2005, including certain amendments to the Ley Federal de Derechos, the act that sets forth the mining taxes' rates. Effective January 1, 2006, this legislation has converted all of the former exploration and exploitive concessions in Mexico, which carried maximum lives of six years, and 25 years, respectively, into general concessions with a 50 year life from their date of registration with the Mining Registry. The concessions are automatically registered as soon as the concession mining rights are paid and no further paper work is required. Our claims are currently in good standing and held by Sunburst Mining. There will be no special documents sent to us to reflect the change.

In April 2006, we applied to the Mexican government for a change of use of land permit for 30 hectares of the La Maravilla concession. La Maravilla is the concession that contains the mineralized rock that is the main interest of our exploration on the Cieneguita Property. As described in our joint venture agreement below, we are currently extracting mineralized material from La Maravilla as well as continuing our exploration program. The purpose of the change of use permit is to allow us to

14

extract the rock from this concession for the purposes of processing to extract the precious metals that may be contained therein. We made the application in advance of any known reserves being discovered on the Cieneguita Property. We cannot assure that we will have sufficient ore reserves, if any, to continue extraction as per our agreement with MRT. This permit required negotiations with the government and municipality concerning such things as the removal of timber, building and maintaining roads and reclamation. We paid the required amount of approximately $67,000 (726,000 Mexican pesos) in November 2006 and the government agency issued the change of use permit in January 2007. The permit is valid until December 31, 2011.

In July 2006, we submitted an environmental impact study and a risk analysis study to the Mexican government for a permit to build a heap leach mining operation on the Aurifero concession of the Cieneguita Property. The purpose of this permit is to allow us to construct an ore processing facility through heap leach mining methods. We do not have any ore reserves on the Cieneguita Property and applied for permits in advance of any conclusive results. In January 2007, the necessary permits to allow for the building and operation of a heap leach operation were granted to the Company. If we are unable to extract and process our discoveries, if any, then there is no need to continue exploration.

On February 12, 2009 we entered into a Definitive Agreement For Development Of “Cieneguita” Project with Minera Rio Tinto, a private Mexican corporation whose president was a former president of our Company. The definitive agreement covers project financing of up to USD $9,000,000. The major points of the agreement are as follows:

1.

Minera Rio Tinto (“MRT”) and/or its investors will subscribe for up to USD$1 million of a secured convertible debenture at 8% interest (payable in stock or cash). The debenture is convertible into units at $0.60 per unit. Each unit comprises 2 common shares and 1 warrant. Each warrant is exercisable at $0.50 per share for a period of 3 years. The placement will be used for continued exploration of our properties and general working capital. As of May 15, 2009, MRT has contributed the $1 million.

2.

MRT is to provide the necessary working capital to begin and maintain mining operations estimated to be $3,000,000 used for the purpose of putting the Cieneguita property into production. MRT will spend 100% of the money to earn 75% of the net cash flow from production. The agreement will limit the mining to the mineralized material that is available from surface to a depth of 15 meters or approximately 10% of the mineralized material found to date.

3.

MRT will spend up to USD $5 million to take the Cieneguita property through the feasibility stage. In doing so, MRT will earn a 60% interest in Mexoro’s rights to the property. After the expenditure of the $5 million all costs will be shared on a ratio of 60% to MRT and 40% to Mexoro Minerals. If we elect not to pay our portion of costs after the $5 million has been spent, our position shall revert to a 25% carried interest on the property.

4.

Portions of the joint venture agreement require we obtain consent from Paramount Gold and Silver Corporation, our secured convertible debenture holder or we repay the debenture held by Paramount Gold and Silver Corporation. Those portions of the agreement that need consent will not be undertaken until such consent is obtained or extinguished by repayment. Subsequently, we repaid approximately $1,300,000 of the debenture owed to Paramount Gold and Silver Corp and in doing so, Paramount agreed to release the Cieneguita property as part of its security under the debenture. As a result of this partial repayment we no longer need the consent of Paramount to begin extraction of mineralized material at Cieneguita.

5.

The Spanish version of this agreement is the governing agreement in case of dispute between the English version and the Spanish versions.

History

The Cieneguita mine was in limited production in the 1990s. Over a four-year period, the Cieneguita mine was operated by Mineral Glamis La Cieneguita S. de R.L. de C.V. (“Glamis”), a subsidiary of the Canadian company Glamis Gold Ltd. (“Glamis Gold”). Glamis was recently acquired by Goldcorp Inc. According to Glamis’ records, Glamis mined and processed 198,000 tonnes of mineralized rock grading 2.2 g/t gold on the property in 1995, ceasing production shortly thereafter. At that time, Corporativo Minero, the operator of the mine for Glamis, acquired the property. MRT entered into an agreement with Corporativo Minero on January 12, 2004 pursuant to which MRT acquired all of the mineral rights from Corporativo Minero to explore and exploit the Cieneguita concessions and to purchase them for $2,000,000. Under our agreements with MRT, MRT has assigned this agreement to us. As of the date of this annual report, $710,000 of the $2,000,0 00 has been paid to Corporativo Minero. MRT paid $150,000 upon execution of this agreement and two months later paid $200,000. We are obligated to make yearly payments on these concessions to Corporativo Minero until the $2,000,000 has been paid.

15

Also, the agreement calls for the balance of the purchase price remaining to be paid out of production, if any, on Cieneguita at a rate of $20 per ounce of gold sold. However, in the event that the price of gold were to exceed $400, then Sunburst Mining would be required to pay an additional $0.10 per each ounce for every dollar gold trades over $400.

If Cieneguita is never put into production, we are still obligated to pay the $120,000 per year until the $2,000,000 is paid. Sunburst Mining made payments to the property owners of $10,000 in April 2006 and $50,000 in May 2006 in lieu of its obligation of bringing the property to production on or prior to May 6, 2006. Sunburst Mining has the obligation to pay $120,000 per year for the years subsequent to May 6, 2006 until the $2,000,000 is paid or the mine is put into production, if ever, in which case the remaining amount owed would be paid out of any production of the property, to avoid termination of the agreement. The Company renegotiated the payment due May 6, 2007, to $60,000 payable on November 6, 2007, which was paid, and the balance of $60,000 which was paid on December 20, 2007. The Company paid $60,000 of the $120,000 due on May 6, 2008, and the balance was paid on June 20, 2008. We paid $30,000 on May 22, 2009 of the $120,000 payment due on May 6, 2009. We’ve verbally negotiated to pay the balance of $90,000 in three equal monthly payments from June 2009 to August, 2009. We are not in default on our payments. On termination of the agreement, there would be no further obligations by Mexoro to any parties other than assuming responsibility for any reclamation work that may need to be done as a result of exploration or mining activity if any should occur.

Geology

The Cieneguita Property is located in the mid-Tertiary domain of the Sierra Madre Occidental of Chihuahua State, Mexico. This region is dominated by felsic ignimbrites and reportedly represents the largest field of felsic volcanics in the world (Jones, 2006).

Based on the work of Jones (2006), who spent approximately two weeks on the Cieneguita Property in mid-November of 2006, the Cieneguita Property appears to lie along the eastern margin of a well-defined but previously unidentified collapse caldera named the ‘Cieneguita Caldera’. The Cieneguita Caldera appears to be part of a larger caldera complex which exhibits a rough north-south trend, which may, at its southern end, include the El Sauzal project (a producing mine). As suggested by Jones (2006), this north-south trending caldera complex may have developed along a broad north-south arc related to post-Laramide collapse and extension which occurred throughout western North America. The identification of this nested caldera is considered important as the mineralization on the Cieneguita Property appears to be controlled by volcano-structural features related to the Cieneguita Caldera and the caldera complex in which it lies (Jones, 2006).

Field mapping by Jones (2006) has indicated that the Cieneguita Caldera is approximately 15 kilometers in width and possibly up to 32 kilometers in length. This mapping also identified a number of diagnostic features of calderas. These include:

·

Significant thicknesses of horizontally stratified tuff – interpreted as intracaldera deposits.

·

Morphologic/topographic break between ponded and outflow ignimbrites – interpreted as the topographic caldera wall.

·

Ring structure (based on satellite imagery).

·

Landslide deposits of caldera wallrocks that have been engulfed by intra-caldera tuffs in the form of megabreccias.

Jones (2006) has suggested that the Cieneguita deposit lies along the (eastern) topographic rim of the Cieneguita Caldera. This interpretation is based on an important litho-structural break between outward (easterly) dipping outflow tuffs and horizontally stratified intra-caldera tuffs. Furthermore, erosion appears to have reduced the rim to the level of the ring-fracture zone. This is based on a number of well-defined north-south striking faults and shears in the caldera wall (Jones, 2006).

Lithotypes

A number of lithologies have been identified on the Cieneguita Property and have been summarized by Jones (2006) below.

The extra-caldera (caldera wall) lithologies include (from oldest to youngest) a lower rhyolite tuff, an andesite vitrophyre, an upper rhyolite tuff and basaltic dykes.

Field observations indicate that the lower two units and portions of the third were deposited prior to caldera formation. Landslide blocks of andesite vitrophyre and portions of the upper rhyolite can be found engulfed by intra-caldera tuffs.

16

These units show relatively conformable dips in sequential beds demonstrating that they were deposited on the margins of the volcanic edifice and predate caldera formation.

Lower rhyolite tuff: The lower rhyolite unit includes at least two welded tuff sequences that are nearly indistinguishable from the upper rhyolite sequence. The rhyolites contain a low percentage but consistent amount of lithic fragments. The unit’s thickness is unknown.

Andesite vitrophyre: This unit is a basaltic to andesitic flow which is exposed for nearly two kilometers along the strike of the caldera wall. It is strongly vitric to the north, moderately vitric in the centre and largely devitrified at the project area and to the south. The unit contains an even abundance of relatively calcic plagioclase crystals while the mafic component is predominately hornblende with minor pyroxene and biotite. This unit acts as the most important marker horizon in the caldera wall with an estimated thickness of 65-80 meters.

Upper rhyolite tuff: The base of this unit is defined by locally well graded basal surge deposits that grade upwards into tuffs with a very high percentage of lithic fragments including blocks up to several metres in diameter. The unit grades upward into a high lithic load welded tuff which marks the lowest of at least three welded tuff packages. The base of this unit occurs as landslide blocks on the Cieneguita Property indicating that it at least partially predates the Cieneguita Caldera. The three overlying welded tuff packages may be correlative with the Cieneguita Caldera itself

Basalt dykes: A single 6 meter wide basaltic dyke has been mapped cutting the upper rhyolite tuff sequence. This dyke cuts the upper caldera fill facies of the upper rhyolite sequence and is therefore considered to be post-Cieneguita Caldera formation.

The intra caldera lithologies are found within the Cieneguita Caldera and include a megabreccia sequence and caldera infill sequence.

Megabreccia Sequence: This unit is characterized by large blocks of caldera wall that collapsed into the caldera during caldera collapse. At Cieneguita, a portion of the caldera wall, consisting of both the andesite vitrophyre and the basal units of the upper rhyolite sequence, slid into the caldera and were engulfed and injected by intra caldera ash flow deposits. Within one of the larger blocks contained in the megabreccia, the contact between the andesite vitrophyre unit and the upper rhyolite tuffs strikes through the center of the formally mined area of Pit 1. This contact is thought to have had an important control on the emplacement and localization of the gold mineralization.

Caldera Infill Sequence: This unit includes rocks that were formed by volcaniclastics that were vented and deposited during caldera formation. This unit can be subdivided into two groups; basal surge deposits and lithic rhyolite tuffs.

i) | Basal surge deposits exhibit dune-like forms consisting of moderately to well sorted beds of well rounded grains of siliceous volcanic rocks. They are thought to be shock deposits formed from the air blast of the initial caldera explosion. |

ii) | Lithic rhyolite tuffs overlying the basal surge deposits consist of horizontally stratified pyroclastics that were deposited into the Cieneguita Caldera. The tuffs include a variable, heterogeneous lithic load of pre-existing volcanic rocks and megabreccia. The unit varies from grey (when unconsolidated) to purple-salmon colored where they are more indurated and welded. |

Intrusives: The youngest rocks found at Cieneguita are the intrusives, which cut the caldera infill sequences. They occur as dykes and sills ranging in width from one to eight meters. The three types of intrusives that have been identified are felsites, composite basalt-rhyolite vent breccias, and basalts.

i) | Felsite dykes can be observed along the south ridge of Cieneguita as two dykes with an east-northeast strike dipping moderately to steeply to the northwest. They clearly crosscut the intra-caldera tuffs and are nowhere brecciated, altered or veined. They are characteristically fine grained and siliceous with sanidine and bi-pyramidal quartz phenocrysts. |

ii) | The composite basalt-rhyolite vent breccias/dykes commonly contain a high percentage of lithic and pumice clasts, compositional banding and spherulites. Quartz veining, specularite and heavy hematite dustings are locally quite intense within and adjacent to these intrusions suggesting they may be mineralized. They are thought to have formed by the commingling of actively erupting basaltic and rhyolitic melt. |

17

iii) | Basalt is present as dykes and irregular intrusions exhibiting a chocolate brown color and fine-grained homogenous texture. They show no signs of deformation or alteration and are thought to be post-mineralization. |

Structure