1 CEDC Central European Distribution Corporation CEDC Investor Presentation November 2007 Exhibit 99.1 |

2 Forward Looking Statements This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements involve known and unknown risks and uncertainties, including, without limitation, economic and vodka consumption trends in Poland or other markets CEDC serves, risks arising from exchange rate and interest rate movements, CEDC’s ability to make and integrate acquisitions and CEDC’s ability to implement its business plan, that may cause the actual results, performance or achievements of CEDC to be materially different from any future results, performance or achievements, expressed or implied, by forward-looking statements. Forward looking statements are based on Management’s current expectations and assessments of market and other conditions. Investors are cautioned that forward-looking statements are not guarantees of future performance and that undue reliance should not be placed on such statements. CEDC undertakes no obligation to publicly update or revise any forward-looking statements or to make any other forward-looking statements, whether as a result of new information, future events or otherwise unless required to do so by the securities laws. Investors are referred to the full discussion of risks and uncertainties included in CEDC’s Form 10-K and prospectus for the fiscal year ended December 31, 2006, and in other periodic and current reports filed by CEDC with the Securities and Exchange Commission. |

3 Current Business Overview Ongoing, strong economic trends in Poland continue to drive the premiumization of the wine and spirits market • Imported spirit market has grown year to date over 20% in 2007 • Polish vodka market is up 7% in value year to date 2007 CEDC business objectives continue to be executed leading to a strong base for 2008 • Strong organic growth of core business (22% organic sales growth in Q3 2007–12 % excluding currency) • Successful launch of new flavored vodka brand – Zlota Gorzka • Numerous packaging changes driving positive volume development • Zubrowka new export packaging starting to roll out • Rectification project completed – significant savings on spirit pricing • Expanding business operations to Russia |

4 CEDC Core Brands in Poland • Our four core brands (Bols, Zubrowka, Soplica and Absolwent) delivering double digit growth year to date 2007 • Bols Vodka up 18% after price adjustment in February 2007 • New labeling of Zubrowka package in Poland has sparked strong sales growth, with an increase in value over 15% since redesign in April 2007 • Imports continue to see strong growth, with Carlo Rossi up 47% in volume year to date (Carlo Rossi is now the #1 wine brand in Poland) |

5 Launch of Zlota Gorzka • August 1st 2007 launched new flavored vodka • Competitor for Zolakowa Gorzka from Lublin • Price at similar point as ZG from Lublin • Mint flavor to be launched this month • Our objective is to take 30% of the Gorzka segment by 2009 (600,000 9L cases) |

6 Export Forging Ahead • In Q3 2007 first shipments of Zubrowka in the new export packaging began to U.S., U.K. as well as other export markets • Launch in the US supported by new marketing campaign • Creative focuses on the uniqueness of the product, with special emphasis on the bison grass. Campaign “Play on Words” uses double entendre to bring together grass and seduction…. - “SEDUCTIVE BY NATURE” |

7 Zubrowka U.S. Marketing Campaign |

8 Rectification Completed • Both rectification plants in Bols and Polmos Bialystok completed and operational • Final investments for both facilities are approximately $15 million with projected annual cost savings of approximately $4.0 million (based upon 36 million liters of 100% spirit) • Financial impact of rectification to begin Q4 2007 |

9 Other Polish Acquisition Opportunities V&S process provides an acquisition opportunity for CEDC in Poland to acquire Polmos Zielona Gora, a leading local producer • CEDC will be taking an active role in the process to bid for this business. The process is expected to close Q1-Q2 2008 • Polmos Zielona Gora, owned by V&S, has a market share of approximately 7% in Poland through the Polska and Luksusowa brands • Luksusowa brand is a potato vodka which will provide a complimentary product to our grain based vodka portfolio • Combined portfolio would leave CEDC with an approximate 37% market share, which is below the typical Polish anti trust limits of 40% Still looking at other wholesalers that would fill distribution gaps Evaluating niche brands that are still State owned in Poland that would provide a good fit with our portfolio |

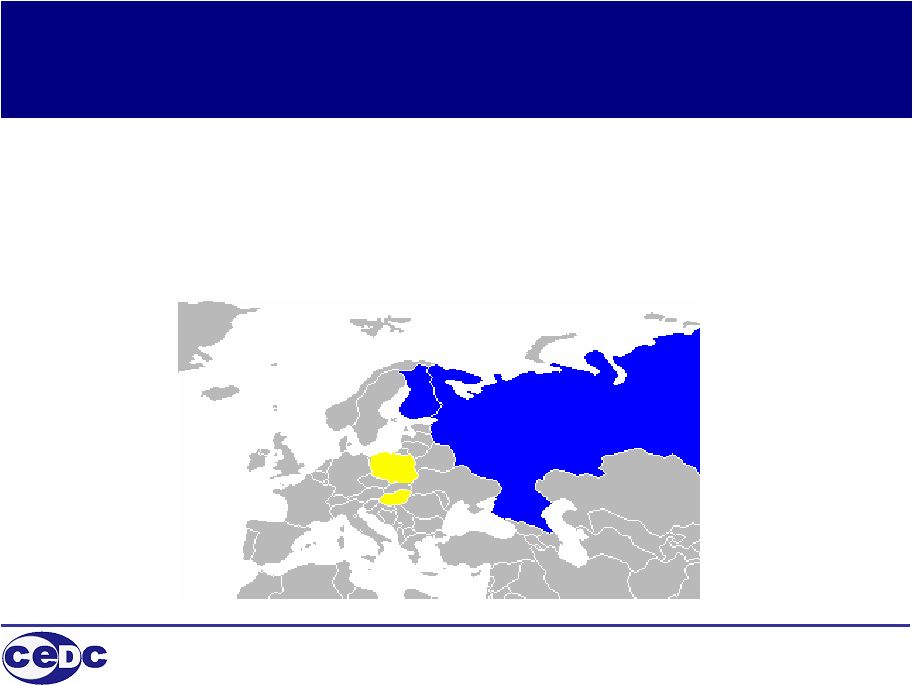

10 Russian Expansion Strategy • We are looking to expand our business model into new growth markets – with a focus on Russia • CEDC has recently entered into a binding Letter of Intent to acquire the Parliament business in Russia (#1 premium vodka in Russia) |

11 Russia and Ukraine – The Time is Right Take leading role in the consolidation of a fragmented spirit market Acquire leading brands with a national sales platform Target import brands to add to local portfolio Premiumization trends taking place in the region Cost and sales synergies through expansion Strong economic growth in the region Leverage our regional know how to execute acquisitions |

12 Russian Market • Russia is the largest vodka market in the world and the 2 nd largest alcohol market in the world • Rapidly growing economy (GDP growth of 6.5% YTD 2007) which in turn is driving consumer spending for premium branded products (both imported and domestic) • Russian market is very fragmented with no producer having over a 7% market share • The Russian Government is focused on reducing “grey zone” vodka with tighter controls over spirit production and distribution -> expected that legalized spirits will grow from 50%-60% of current market share to 75%- 80% by 2011 Source: Renaissance Capital Report, August 2007 |

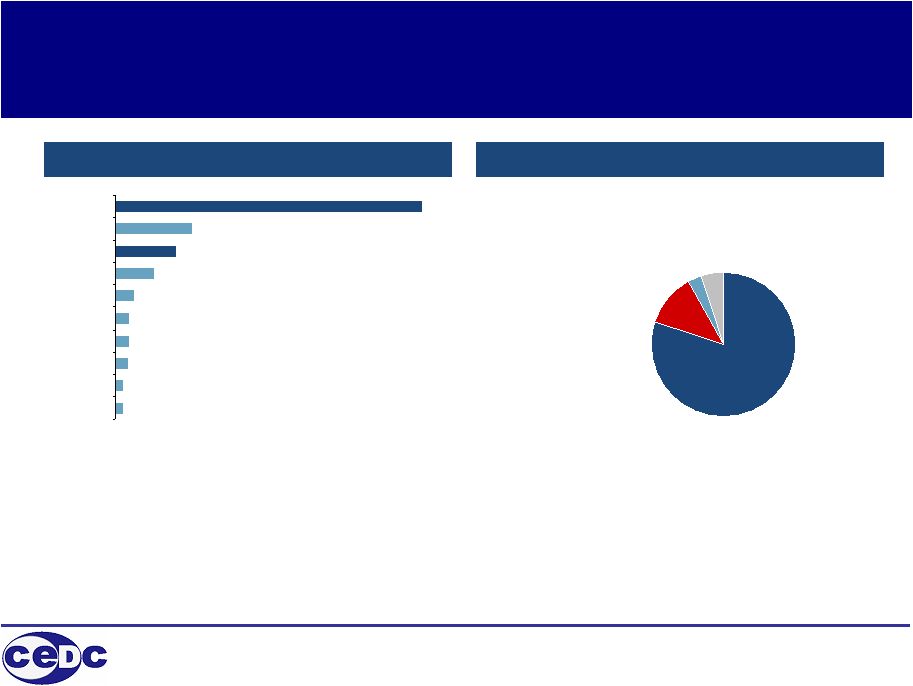

13 Russian Market Global vodka market, by volume (2006) Russian spirits market, by value (2006) • Russia is by far the world’s largest vodka market in volume terms • The vodka market in Russia in volume terms is nearly four times bigger than in the United States Source: Euromonitor Vodka 80% Whiskey 3% Other spirits 5% Cognac and Brandy 12% . 4 5 7 8 8 11 22 34 44 176 Germany Brazil Belarus Uzbekistan United Kingdom Kazakhstan Poland Ukraine USA Russia mln. decalitres |

14 Russian Market Russian vodka market by production • Although in volume terms the market has been in decline, the value branded segment of the market is growing rapidly – premium segment of Parliament is fastest growing segment • Economic sector vodka is being replaced by more expensive branded vodka • Currently mainstream and premium segments make up approximately 40% of the market, and this is expected to increase to 60% by 2011 276.4 275 272.2 253.1 246.8 239.4 237.5 231 224.1 217.1 210.1 9.3 9.6 10.8 12.9 14.2 15.1 16.5 17.6 18.6 19.6 20.5 0 50 100 150 200 250 300 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 - 5 10 15 20 25 30 Vodka market volume (mn dl) Vodka market value ($bn) Source: Renaissance Capital Estimates |

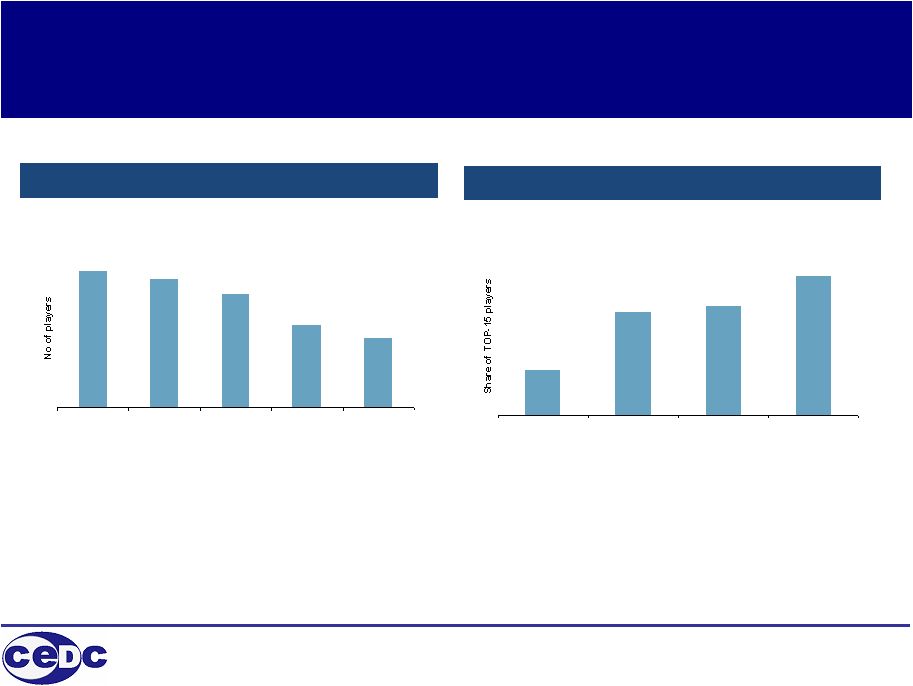

15 Russian Market Market Share of the Top-5 leaders (2006) Number of players on the market 344 324 286 209 175 2003 2004 2005 2006 2007E 26% 58% 61% 78% Russia USA Ukraine Poland • The Russian vodka market is undergoing consolidation and the number of players has halved in the last five years • However, compared to other developed consumer markets, the level of consolidation is still comparatively low Source: Management, Business Analytica Data as of January 2007 |

16 Parliament, #1 Market Share in the Premium Sector • Forecasted 2007 sales of approximately 25 million liters – 5 year CAGR of 37% • Distributed in over 60,000 outlets across Russia • 53% brand awareness – second only to Russian Standard • 115-240 RUR price segment (Parliament 170 RUR) is the fastest growing vodka segment • Over 200 sales staff serving Russia • Currently not distributing any 3 rd party agency brands (represents a big potential) • Nearly 60% lower excise tax in Russia as compared to Poland, with similar retail price, translating into higher margins for producers Source: CEDC Management Estimates, Renaissance Capital Estimates |

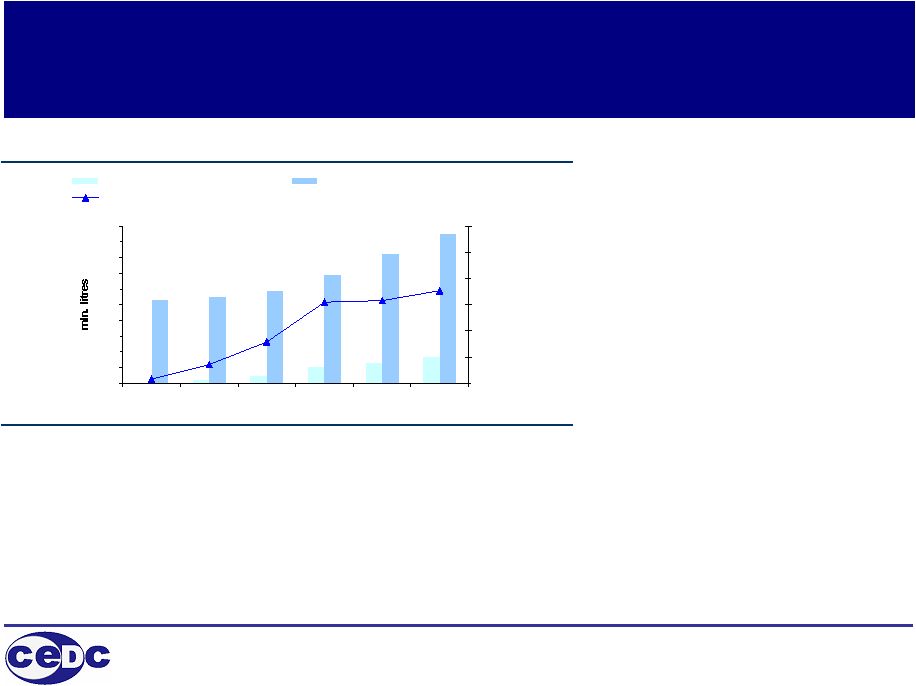

17 Parliament The Group’s market share in the sub-premium segment (total market) 0 2 5 11 13 17 53 55 59 69 82 95 1% 4% 8% 15% 16% 18% 0 10 20 30 40 50 60 70 80 90 100 2001 2002 2003 2004 2005 2006E 0% 5% 10% 15% 20% 25% 30% Parliament Sub-premium segment Market share of sub-premium segment Source: Management, Business Analytica data as of January 2006 Strong brand growth driven primarily by core brand Parliament Classic split almost 50/50 in 0.5 liter and 0.7 liter Also sold is a range of flavored vodka’s • Black current • Mandarin • Pepper |

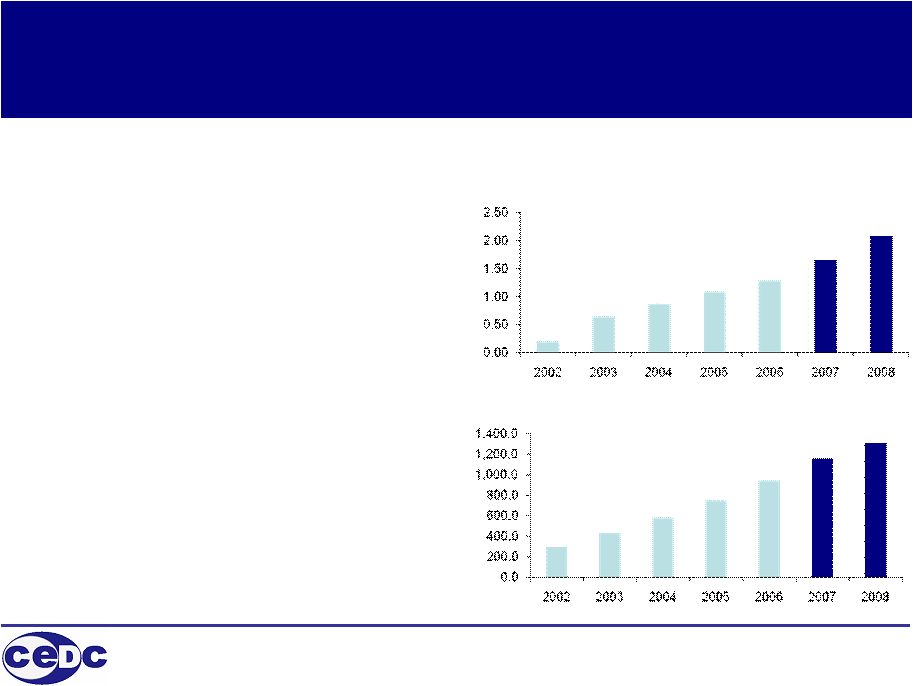

18 2007 and 2008 Guidance • 2007 Comparable EPS of $1.65 to $1.79 per fully diluted share • 2008 Comparable EPS of $2.03 to $2.13 per fully diluted share • 2007 revenue projection of $1.17 billion to $1.20 billion, an increase of approximately 25% as compared to 2006 • 2008 revenue projection of $1.26 billion to $1.36 billion • Above guidance does not factor in the impact of any future acquisitions, including Parliament EPS on a comparable basis (US$) Net sales (US$000’s) GAAP information for the relevant periods, and reconciling information, is set forth on page 21 and 22 |

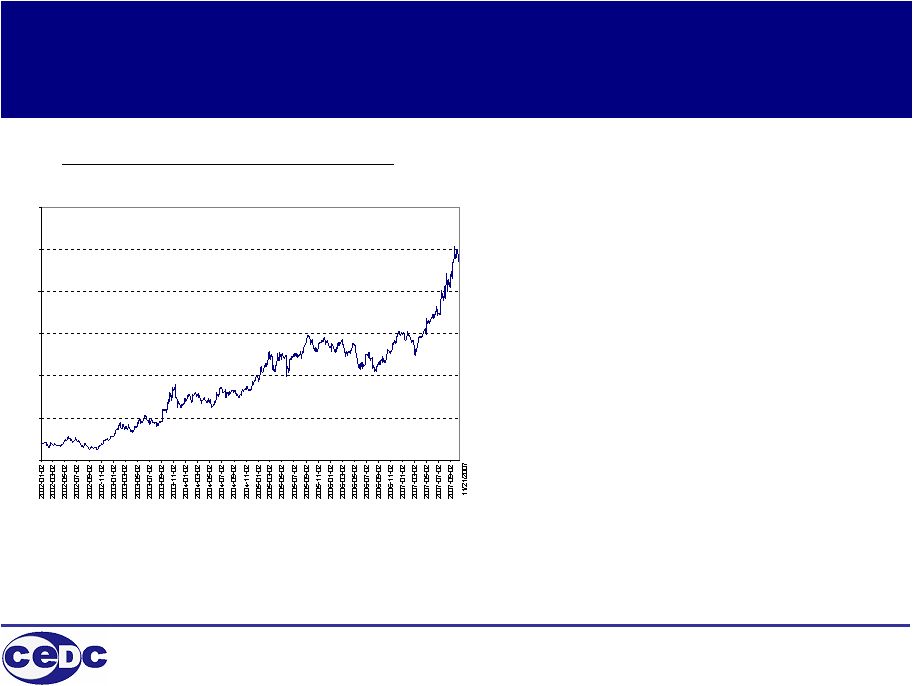

19 Increased Distribution and Liquidity • Average trading volume increased from approximately 350,000 to over 450,000 shares a day over the last 3 months • Shares dually traded on Nasdaq and WSE •Diversified investor base with 74% of our shares held by institutions (60% a year ago) • 54% U.S. Investors • 7% Polish Investors • 13% Other non U.S. Investors • Market capitalization approximately $2 billion CEDC closing price on Nasdaq 0 10 20 30 40 50 60 |

20 Summary GROWTH in emerging markets will continue to fuel increasing consumer demand for BRANDS CEDC is well positioned to EXPAND and GROW with these trends |

21 UNAUDITED RECONCILIATION OF NON-GAAP MEASURES CEDC has reported net income and diluted net income per share in accordance with GAAP and on a non-GAAP basis, referred to in this docment as comparable non-GAAP net income. CEDC’s management believes that the non-GAAP reporting giving effect to the adjustments shown in the attached reconciliation provides meaningful information and an alternative presentation useful to investors' understanding of CEDC’s core operating results and trends. CEDC discusses results on a comparable basis in order to give investors better insight into underlying business trends from continuing operations. CEDC’s calculation of this measure may not be the same as similarly named measures presented by other companies. This measure is not presented as an alternative to net income computed in accordance with GAAP as a performance measure, and you should not place undue reliance on such measures. Our full year guidance is forward-looking information. See “Forward Looking Statements” at the beginning of this presentation. Note: for periods prior to 2005 there is no difference between GAAP and comparable non-GAAP net income in this presentation A) Represents the net after tax impact of the foreign currency revaluation related to our Senior Secured Notes and mark to market revaluation of financing related hedges. CEDC closed a EURO 325 million Senior Secured Notes offering on July 25, 2005 in order to fund the acquisitions of Polmos Bialystok and Bols. B) Due to various delays in receiving final approval from the Polish Anti-Monopoly office, the acquisitions were not completed until August 17, 2005, in the case of Bols, and October 12, 2005, in the case of Polmos Bialystok. These amounts represent the proportional share of interest accrued (net of interest earned in escrow) on our senior secured noted prior to completion of the acquisitions. In addition, the CEDC incurred additional debt to support the deposit payment made to the State Treasury as pa rt of the Polmos Bialystok acquisition. The costs relating to this additional financing are also represented in this calculation. C) Represents other miscellaneous costs incurred in 2005, directly related to the acquisitions of Bols and Polmos Bialystok and 2006 costs related to the tender for additional shares of Polmos Bialystok. D) Represents cost incurred with the potential acquisition of Polmos Lublin which was not completed and has since been acquired by another company. E) On January 1, 2006, the Company adopted SFAS 123(R) and began to expense stock options. This amount represents the net after tax impact of the expensing of stock options. 12 Months Ended December 31, 2005 2006 GAAP net income/(loss) 20,268 55,450 A. Foreign exchange impact and hedge revaluation 6,832 (11,810) B. Pre-acquisition financing costs 3,907 - C. Other acquisition costs 317 423 D. Impact of Polmos Lublin acquistion costs write-off 469 E. Impact of expensing stock options 1,548 Range for Comparable non-GAAP Fully Diluted Earnings per 31,324 46,080 Comparable net income per share of common stock, basic 1.11 1.29 Comparable net income per share of common stock, diluted 1.09 1.28 GAAP net income per share of common stock, basic 0.72 1.55 GAAP net income per share of common stock, diluted 0.70 1.53 Share base for fully diluted earnings per share calculation 28,820 36,137 |

22 UNAUDITED RECONCILIATION OF NON-GAAP MEASURES Note: Although changes in foreign exchange have had a significant impact on EPS in prior periods, it is not possible to estimate this for 2008; therefore, no adjustment is provided. A) Represents the net after tax impact of the foreign currency revaluation related to our Senior Secured Notes and mark to market revaluation of financing related hedges as of September 30, 2007. The impact of foreign exchange revaluation will change which may have a material effect on our financial results. B) Represents other miscellaneous costs incurred in 2007, directly related to the tender for additional shares of Polmos Bialystok and other acquisitions. C) Represents the net after tax impact associated with the early retirement of 20% of CEDC’s outstanding Senior Secured Notes, including an 8% one-time redemption premium payment to the Noteholders and write-off of prepaid financing costs. D) On January 1, 2006 CEDC adopted SFAS 123(R) and began to expense stock options. This amount represents the net after tax impact of the expensing of stock options. E) Represents one time charge for early retirement incentive program and cost incurred with the potential acquisition of Polmos Lublin, which was not completed in 2006. Full Year Guidance, 12 Months Ending December 31, 2007 2008 1.44 $ 1.99 1.58 $ 2.09 A. Foreign exchange impact and hedge revaluation (0.10) - B. Other acquisition related costs 0.03 - C. Cost associated with early retirement of debt 0.23 - D. Impact of expensing stock options 0.04 0.04 E. Other non recurring costs 0.01 - 1.65 $ 2.03 1.79 $ 2.13 Range for Comparable non-GAAP Fully Diluted Earnings per Share Range for GAAP Fully Diluted Earnings per Share |