UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-08495

NATIONWIDE MUTUAL FUNDS

(Exact name of registrant as specified in charter)

1000 CONTINENTAL DRIVE, SUITE 400, KING OF PRUSSIA, PENNSYLVANIA 19406-2850

(Address of principal executive offices) (Zip code)

Eric E. Miller, Esq.

1000 Continental Drive

Suite 400

King of Prussia, Pennsylvania 19406-2850

(Name and address of agent for service)

Registrant’s telephone number, including area code: (610) 230-2839

Date of fiscal year end: July 31, 2014

Date of reporting period: August 1, 2013 through January 31, 2014

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than ten (10) days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR § 270.30e-1). The Commission may use the information provided on Form N-CSR in the Commission’s regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, D. C. 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

Include a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR § 270.30e-1).

Semiannual Report

January 31, 2014

Nationwide Mutual Funds

Equity Funds

Nationwide Bailard Cognitive Value Fund

Nationwide Bailard International Equities Fund

Nationwide Bailard Technology & Science Fund

Nationwide Geneva Mid Cap Growth Fund

Nationwide Geneva Small Cap Growth Fund

Nationwide HighMark Balanced Fund

Nationwide HighMark Large Cap Core Equity Fund

Nationwide HighMark Large Cap Growth Fund

Nationwide HighMark Small Cap Core Fund

Nationwide HighMark Value Fund

Nationwide Ziegler Equity Income Fund

Nationwide Ziegler NYSE Arca Tech 100 Index Fund

| Nationwide Funds® |

Commentary in this report is provided by the portfolio manager(s) of each Fund as of the date of this report and is subject to change at any time based on market or other conditions.

Third-party information has been obtained from sources that Nationwide Fund Advisors (NFA), the investment adviser to the Funds, deems reliable. This report and the holdings provided are for informational purposes only and are not intended to be relied on as investment advice. Portfolio composition is accurate as of the date of this report and is subject to change at any time and without notice. NFA, one of its affiliated advisers or its employees may hold a position in the securities in this report.

Statement Regarding Availability of Quarterly Portfolio Holdings.

The Trust files complete schedules of portfolio holdings for each Fund with the Securities and Exchange Commission (SEC) for the first and third quarters of each fiscal year on Form N-Q. Additionally, the Trust files a schedule of portfolio holdings monthly for the Nationwide Money Market Fund on Form N-MFP. Forms N-Q and Forms N-MFP are available on the SEC’s website at http://www.sec.gov. Forms N-Q and Forms N-MFP may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling 800-SEC-0330. The Trust also makes this information available to shareholders on nationwide.com/mutualfunds or upon request without charge.

Statement Regarding Availability of Proxy Voting Record.

Information regarding how the Funds voted proxies relating to portfolio securities held during the most recent 12-month period ended June 30 is available without charge, upon request, by calling 800-848-0920, and on the SEC’s website at http://www.sec.gov.

| Nationwide Funds® Semiannual Report |

Nationwide Funds®

January 31, 2014

Dear Shareholder,

I am pleased to write this message to you for the mutual fund reports covering the six-month period ended January 31, 2014. Perhaps you recently became a Nationwide Funds shareholder through our 2013 acquisition of 17 HighMark Funds. Or maybe you have been a Nationwide Funds shareholder for a long time and are now invested in one of our newer solutions. Either way, we sincerely value your business. You can be assured that we are dedicated to your success and look forward to providing you and your advisor with timely information and service.

This is an exciting time to be a Nationwide Funds shareholder. The HighMark acquisition expanded the breadth of our fund lineup by adding exposure to eight new asset classes, giving us the ability to offer our shareholders more diverse investment options.

As a Nationwide Funds shareholder you understand that planning and preparation are essential steps to reaching future goals. When I think about smart planning I think about Abraham Lincoln, who said “Give me six hours to chop down a tree and I will spend the first four sharpening the ax.” By working with your advisor and taking a considered, disciplined, long-term approach to investing, you are taking the time to sharpen your ax. Doing so can enable you to be well positioned, even during periods of market volatility and economic downturns.

After several years of tepid economic recovery, many investors are casting a wary eye toward the future. While we have seen progress across economic indicators quarter to quarter, we understand that for many Americans it still does not feel like things are getting better. Domestically, economic progress has been evident as the unemployment rate, gross domestic product (GDP) and the housing market showed modest indications of improvement throughout the six months of the reporting period. Broad U.S. stock market performance increased for the reporting period, with gains for the S&P 500® Index at 6.85%. Still, many investors’ portfolio returns were tempered during the reporting period by low-yielding fixed-income investments, as evidenced by the Barclays U.S. Aggregate Bond Index, which returned 1.78%. More market mending is still needed.

Yet, with preparation, poise and a patient forward-looking perspective, you may confidently pursue your goals no matter what the current economic or market climate. Nationwide has the wisdom and perspective that come from a long history of caring for our customers. For more than 80 years, we have nurtured our customers’ assets through all phases of market cycles. We are honored to now work with you.

Thank you for investing with Nationwide Funds.

Sincerely,

Michael S. Spangler

President & CEO

Nationwide Funds

1

| Economic Review |

During the six-month reporting period ended January 31, 2014, the level of investment return in the markets varied greatly by asset class. U.S. equities experienced a broad-based rally, with the S&P 500® Index delivering a 6.85% return, and nearly all sectors and capitalization ranges showing strong performance for the reporting period. International equities results were mixed, with positive developed market performance offset by negative returns in emerging markets. Fixed-income returns were positive, primarily in the long-term and credit-sensitive segments.

In the United States, investment performance during the reporting period was affected by news from Washington and reports of uncertainty regarding emerging market economies. Equity market returns and bond yields reacted to actions by the Federal Reserve Board to decrease (taper) the asset purchase program, also known as Quantitative Easing (QE).

The S&P 500 Index registered negative performance in the first and last months of the reporting period (August 2013 and January 2014), but delivered strong performance from September through December 2013.

The best-performing sectors for the S&P 500 Index during the reporting period were technology, up 13.2%; industrials, up 11.7%; and health care, up 10.7%. Technology and industrials benefited from a strong earnings environment, while health care rallied in reaction to excitement surrounding new products. The weakest sectors during the reporting period were telecommunications, with -2.6%; consumer staples, with -0.2%; and utilities, with 1.1%. These three sectors were affected by investors’ move away from dividend-focused sectors as rates rose and cyclical exposure was preferred.

The strong performance in U.S. equities was broad based during the reporting period, with small-capitalization stocks outperforming large-cap stocks, and growth outperforming value.

U.S. economic activity was strong during the reporting period; third-quarter 2013 gross domestic product (GDP) growth of 4.1% was the second-highest quarterly result since March 2006. GDP growth decelerated to 3.2% in the fourth quarter of 2013 but remained above average in relation to other post-recession quarters. Inflation remained well controlled throughout the reporting period, with the U.S. Consumer Price Index (CPI) and the core CPI (excluding the volatile food and energy categories) remaining below 2%. Despite job-creation levels coming in lower than during many past recoveries, the unemployment rate continued to decline during the reporting period, falling from 7.2% to 6.6%.

Throughout the reporting period, the performance of international stocks continued to be positive, but weaker relative to U.S. stocks. Europe was reminded of the fragile state of the banking systems of its weaker members, this time with Cyprus. Continued political tensions in Greece, sluggish European economic growth and worries about a U.S. tapering depressed relative returns through mid-2013 before the market rallied in response to the stabilization of political and banking system risk. Returns in Asia were mixed, with relative strength exhibited in Japan due to the prospect of renewed stimulus by Japan’s central bank and a beneficial exchange rate offset by weakness in the developing economies. Emerging market stocks were weak on concerns about slowing economic growth in China, political tensions in Brazil, Turkey, North Korea and the Middle East, and steadily declining commodity prices.

2

| Economic Review (con’t.) |

Performance in the fixed-income markets was driven by stabilization in interest rates during the reporting period. Long-term Treasury yields rose from 1.63% to 2.71% in the three months prior to the reporting period (May 1 through August 1), but showed little volatility during the reporting period, ending at 2.65%. Fixed-income returns were positive, as investors absorbed the news that the Fed will begin to taper the QE program. Long-term and credit-sensitive bonds delivered the strongest performance during the reporting period.

| Index | Six-Month Total Return (as of 1/31/14) | |||

| Barclays Emerging Markets USD Aggregate Bond | 1.16% | |||

| Barclays Municipal Bond | 2.99% | |||

| Barclays U.S. 1-3 Year Government/Credit Bond | 0.55% | |||

| Barclays U.S. 10-20 Year Treasury Bond | 1.69% | |||

| Barclays U.S. Aggregate Bond | 1.78% | |||

| Barclays U.S. Corporate High Yield | 4.70% | |||

| MSCI Emerging Markets® | -0.33% | |||

| MSCI World ex USA | 6.44% | |||

| Russell 1000® Growth | 10.15% | |||

| Russell 1000® Value | 4.63% | |||

| Russell 2000® | 8.88% | |||

| S&P 500® | 6.85% | |||

3

| Fund Commentary | Nationwide Bailard Cognitive Value Fund |

For the semiannual period ended January 31, 2014, the Nationwide Bailard Cognitive Value Fund (Class M at NAV) returned 3.69%* versus 9.44% for its benchmark, the S&P SmallCap 600 Value Index. For broader comparison, the median return for the Fund’s closest Lipper peer category of Small-Cap Value Funds (consisting of 319 funds as of January 31, 2014) was 6.86% for the same time period.

*Performance prior to the Fund’s inception on September 16, 2013, is based on the performance of the Fund’s predecessor fund.

The subadvisor utilizes a proprietary multifactor model, the Behavioral Ranking Model (BRM), to aid in portfolio construction. There are two primary determinants of the Fund’s relative performance. One is how the subadviser’s BRM performs relative to the benchmark, and the other is how successfully the BRM’s signals are translated into Fund performance.

For the reporting period, the BRM outperformed the Fund’s benchmark index. However, the positive model performance did not translate in actual Fund performance. The underperformance of the Fund versus the model and the benchmark was the result of delayed implementation of model changes into the actual Fund. Once implemented, changes to the Fund had a positive impact on relative performance, but were insufficient to offset the underperformance from the early part of the reporting period.

The Fund’s strategy seeks to minimize relative sector and subsector weights versus the benchmark, as we believe that stock selection holds greater potential for excess return. As a result, the Fund’s tracking error tends to max out at about 4.5%, below the typical small-cap value managers’ 6.5% tracking error. When sector weights do diverge from the benchmark, it is a result of stock selection and the abundance or scarcity of high BRM scores in the sector rather than an active portfolio decision.

For the reporting period, overweights in the industrials sector and underweights in the energy sector were the largest contributors to Fund performance versus the benchmark index. Kimball

International and Universal Insurance were the largest individual stock performance contributors for the Fund during the reporting period. In Kimball’s case this was due to positive earnings surprises, and in Universal’s case due to a lack of hurricane activity.

For the reporting period, an overweight in telecommunication services and an underweight in health care were the largest detractors from Fund performance versus the benchmark index, though in health care’s case the detraction was minimal. Renewable Energy Group and Gain Capital were the largest detractors from Fund performance involving individual stocks during the reporting period. In Renewable’s case this was due to unfavorable legislation. In Gain’s case this was due to earnings dilution.

Subadviser:

Bailard, Inc.

Portfolio Manager:

Thomas J. Mudge III

The Fund is subject to the risks of investing in equity securities and risks associated with investing in stocks of smaller companies. Value funds may underperform other funds that use different investing styles. The Fund may invest in more-aggressive investments such as derivatives (many of which create investment leverage and are highly volatile), exchange-traded funds (ETFs) (shareholders will bear additional costs) and foreign securities (which are volatile, harder to price and less liquid than U.S. securities). Please refer to the summary prospectus for a more detailed explanation of the Fund’s principal risks.

A description of the benchmarks can be found on the Market Index Definitions page at the back of this book.

4

| Fund Overview (Unaudited) | Nationwide Bailard Cognitive Value Fund |

Objective

The Fund seeks long-term capital appreciation.

Highlights

| Ÿ | For the six-month period ended January 31, 2014, the Fund (Class M at NAV) returned 3.69%, underperforming the benchmark by 5.75% and the Lipper peer category by 3.17%. |

| Ÿ | Overweights in the industrials sector and underweights in the energy sector were the largest contributors to Fund performance versus the benchmark index during the reporting period. |

| Ÿ | An overweight in telecommunication services and an underweight in health care were the largest detractors from Fund performance versus the benchmark index during the reporting period. |

Asset Allocation†

| Common Stocks | 95.1% | |||

| Exchange Traded Funds | 3.8% | |||

| Mutual Fund | 1.0% | |||

| Other assets in excess of liabilities | 0.1% | |||

| 100.0% |

Top Industries††

| Commercial Banks | 9.0% | |||

| Insurance | 7.1% | |||

| Aerospace & Defense | 4.7% | |||

| Real Estate Investment Trusts (REITs) | 4.6% | |||

| Electrical Equipment | 4.6% | |||

| Commercial Services & Supplies | 4.2% | |||

| Oil, Gas & Consumable Fuels | 3.8% | |||

| Electronic Equipment, Instruments & Components | 3.6% | |||

| Health Care Providers & Services | 3.5% | |||

| Semiconductors & Semiconductor Equipment | 3.0% | |||

| Other Industries | 51.9% | |||

| 100.0% |

Top Holdings††

| Kimball International, Inc., Class B | 3.2% | |||

| EnerSys, Inc. | 3.0% | |||

| Carriage Services, Inc. | 2.9% | |||

| Schweitzer-Mauduit International, Inc. | 2.8% | |||

| Exelis, Inc. | 2.7% | |||

| Insteel Industries, Inc. | 2.7% | |||

| Electronics For Imaging, Inc. | 2.7% | |||

| Blucora, Inc. | 2.4% | |||

| FutureFuel Corp. | 2.3% | |||

| Hanover Insurance Group, Inc. (The) | 2.1% | |||

| Other Holdings | 73.2% | |||

| 100.0% |

| † | Percentages indicated are based upon net assets as of January 31, 2014. |

| †† | Percentages indicated are based upon total investments as of January 31, 2014. |

5

| Fund Performance | Nationwide Bailard Cognitive Value Fund |

Average Annual Total Return

(For periods ended January 31, 2014)

| Six Months* | 1 Yr. | 5 Yr. | 10 Yr. | |||||||||||||||

| Class A | w/o SC1 | 3.52% | 17.13% | 19.51% | 7.33% | |||||||||||||

| w/SC2 | -2.17% | 10.69% | 18.17% | 6.73% | ||||||||||||||

| Class C | w/o SC1 | 3.20% | 16.40% | 18.80% | 6.69% | |||||||||||||

| w/SC3 | 2.20% | 15.40% | 18.80% | 6.69% | ||||||||||||||

| Class M4 | w/o SC | 3.69% | 17.53% | 19.99% | 7.77% | |||||||||||||

| Institutional Service Class4,5 | w/o SC | 3.61% | 17.43% | 19.89% | 7.67% | |||||||||||||

| Institutional Class4 | w/o SC | 3.55% | 6 | — | — | — | ||||||||||||

All figures showing the effect of a sales charge (SC) reflect the maximum charge possible, because it has the most significant effect on performance data.

| * | Not annualized. |

| 1 | These returns do not reflect the effects of SCs. |

| 2 | For the period from September 16, 2013 through January 31, 2014 a front-end sales charge of 5.75% was deducted. Prior to September 16, 2013, a front-end sales charge of 5.50% was deducted. |

| 3 | A 1.00% CDSC was deducted from the one year return because it is charged when you sell Class C shares within the first year after purchase. |

| 4 | Not subject to any SCs. |

| 5 | Effective September 16, 2013 Fiduciary Shares were renamed Institutional Service Class Shares. |

| 6 | Since inception date of September 18, 2013. Not Annualized. |

Expense Ratios

| Gross Expense Ratio* | Net Expense Ratio* | |||||

| Class A | 1.54% | 1.48% | ||||

| Class C | 2.04% | 2.04% | ||||

| Class M | 1.04% | 1.04% | ||||

| Institutional Service Class | 1.29% | 1.23% | ||||

| Institutional Class | 1.04% | 1.04% | ||||

| * | Current effective prospectus dated September 16, 2013. The difference between gross and net operating expenses reflects contractual waivers in place through November 30, 2015. Please see the Fund’s most recent prospectus for details. |

6

| Fund Performance | Nationwide Bailard Cognitive Value Fund |

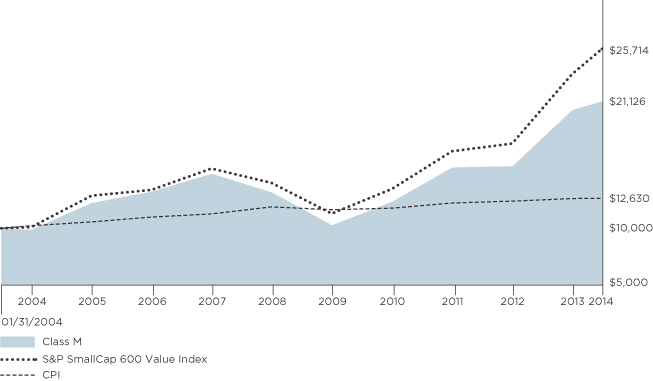

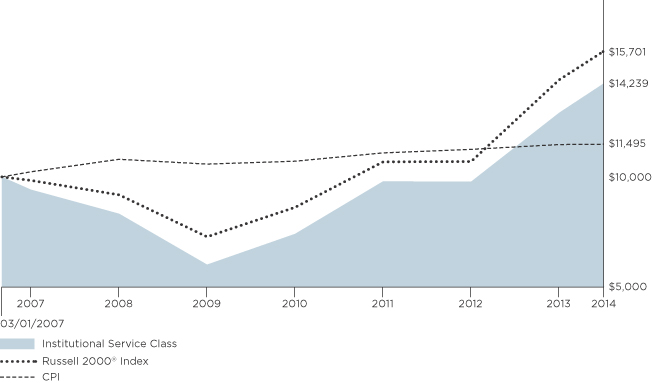

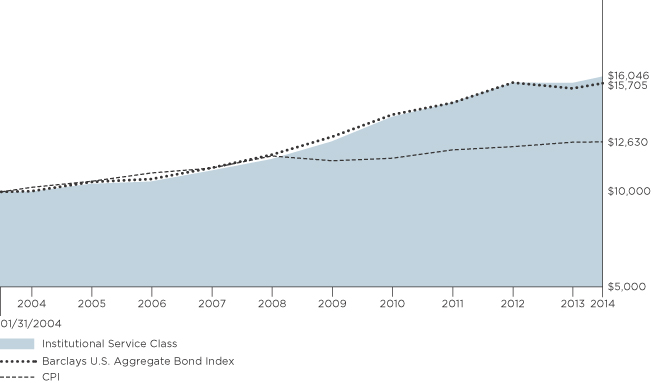

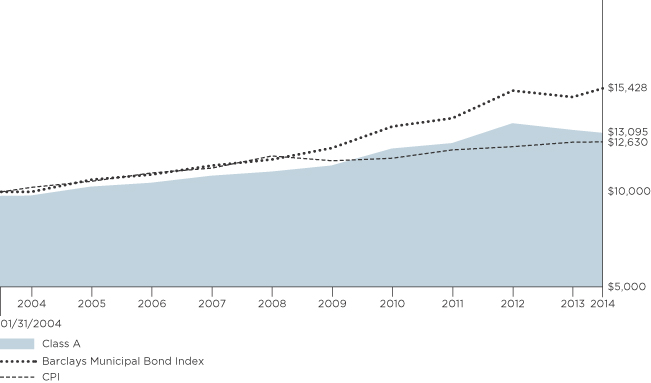

Performance of a $10,000 Investment

Investment return and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions.

Comparative performance of $10,000 invested in Class M shares of the Nationwide Bailard Cognitive Value Fund versus the S&P SmallCap 600 Value Index and the Consumer Price Index (CPI) over the 10-year period ended 1/31/14. Unlike the Fund, the performance for these unmanaged indexes does not reflect any fees, expenses, or sales charges. One cannot invest directly in a market index. A description of the benchmarks can be found on the Market Index Definitions page at the back of this book.

7

| Shareholder Expense Example | Nationwide Bailard Cognitive Value Fund |

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) paid on purchase payments and redemption fees; and (2) ongoing costs, including investment advisory fees, administration fees, distribution fees and other Fund expenses. The examples below are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. Per Securities and Exchange Commission (“SEC”) requirements, the examples assume that you had a $1,000 investment in the Class at the beginning of the reporting period (August 1, 2013) and continued to hold your shares at the end of the reporting period (January 31, 2014).

Actual Expenses

For each Class of the Fund in the table below, the first line provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid from August 1, 2013 through January 31, 2014. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line of each Class under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Expenses for Comparison Purposes

The second line of each Class in the table below provides information about hypothetical account values and hypothetical expenses based on the Class’ actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Class’ actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period from August 1, 2013 through January 31, 2014. You may use this information to compare the ongoing costs of investing in the Class of the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as sales charges (loads) or redemption fees. If these transaction costs were included, your costs would have been higher. Therefore, the second line for each Class in the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. The examples also assume all dividends and distributions are reinvested.

Schedule of Shareholder Expenses

Expense Analysis of a $1,000 Investment

Nationwide Bailard Cognitive January 31, 2014 | Beginning Account Value ($) 08/01/13 | Ending Account Value ($) 01/31/14 | Expenses Paid During Period ($) 08/01/13 - 01/31/14 | Expense Ratio During Period (%) 08/01/13 - 01/31/14 | ||||||||

| Class A Shares | Actual | a | 1,000.00 | 1,035.20 | 7.44 | 1.45 | ||||||

| Hypothetical | a,b | 1,000.00 | 1,017.90 | 7.38 | 1.45 | |||||||

| Class C Shares | Actual | a | 1,000.00 | 1,032.00 | 10.14 | 1.98 | ||||||

| Hypothetical | a,b | 1,000.00 | 1,015.22 | 10.06 | 1.98 | |||||||

| Class M Shares | Actual | a | 1,000.00 | 1,036.90 | 5.19 | 1.01 | ||||||

| Hypothetical | a,b | 1,000.00 | 1,020.11 | 5.14 | 1.01 | |||||||

| Institutional Service Class Sharesc | Actual | a | 1,000.00 | 1,036.10 | 6.16 | 1.20 | ||||||

| Hypothetical | a,b | 1,000.00 | 1,019.16 | 6.11 | 1.20 | |||||||

| Institutional Class Shares | Actual | d | 1,000.00 | 1,035.50 | 3.73 | 0.99 | ||||||

| Hypothetical | a,b | 1,000.00 | 1,020.21 | 5.04 | 0.99 | |||||||

| a | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value from August 1, 2013 through January 31, 2014 multiplied to reflect one-half year period. The expense ratio presented represents a six-month, annualized ratio in accordance with Securities and Exchange Commission guidelines. |

| b | Represents the hypothetical 5% return before expenses. |

| c | Effective September 16, 2013, Fiduciary Shares were renamed Institutional Service Class Shares. |

| d | Actual expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value from September 19, 2013 through January 31, 2014 to reflect the period from commencement of operations. |

8

Statement of Investments

January 31, 2014 (Unaudited)

Nationwide Bailard Cognitive Value Fund

| Common Stocks 95.1% | ||||||||||

| Shares | Market Value | |||||||||

| ||||||||||

Aerospace & Defense 4.7% | ||||||||||

Alliant Techsystems, Inc. | 4,000 | $ | 574,800 | |||||||

Engility Holdings, Inc.* | 39,800 | 1,524,738 | ||||||||

Exelis, Inc. | 146,000 | 2,860,140 | ||||||||

|

| |||||||||

| 4,959,678 | ||||||||||

|

| |||||||||

| ||||||||||

Automobiles 0.3% |

| |||||||||

Thor Industries, Inc. | 6,200 | 318,494 | ||||||||

|

| |||||||||

| ||||||||||

Building Products 2.7% |

| |||||||||

Insteel Industries, Inc. | 152,500 | 2,841,075 | ||||||||

|

| |||||||||

| ||||||||||

Capital Markets 1.2% |

| |||||||||

FBR & Co.* | 54,200 | 1,314,892 | ||||||||

|

| |||||||||

| ||||||||||

Chemicals 2.6% |

| |||||||||

Chase Corp. | 9,000 | 284,580 | ||||||||

FutureFuel Corp. | 150,400 | 2,460,544 | ||||||||

|

| |||||||||

| 2,745,124 | ||||||||||

|

| |||||||||

| ||||||||||

Commercial Banks 9.0% |

| |||||||||

1st Source Corp. | 11,900 | 350,693 | ||||||||

American National Bankshares, Inc. | 11,469 | 266,654 | ||||||||

Center Bancorp, Inc. | 8,201 | 145,568 | ||||||||

Central Pacific Financial Corp. | 65,400 | 1,200,090 | ||||||||

Financial Institutions, Inc. | 5,007 | 104,546 | ||||||||

First Interstate BancSystem, Inc. | 79,321 | 2,035,377 | ||||||||

German American Bancorp, Inc. | 16,400 | 442,144 | ||||||||

Independent Bank Corp.* | 123,500 | 1,636,375 | ||||||||

MainSource Financial Group, Inc. | 70,613 | 1,151,698 | ||||||||

Metro Bancorp, Inc.* | 35,200 | 699,424 | ||||||||

MidWestOne Financial Group, Inc. | 9,100 | 223,678 | ||||||||

Northrim BanCorp, Inc. | 50,375 | 1,210,008 | ||||||||

|

| |||||||||

| 9,466,255 | ||||||||||

|

| |||||||||

| ||||||||||

Commercial Services & Supplies 4.2% |

| |||||||||

Courier Corp. | 41,865 | 661,048 | ||||||||

Kimball International, Inc., Class B | 225,218 | 3,348,992 | ||||||||

UniFirst Corp. | 3,900 | 412,620 | ||||||||

|

| |||||||||

| 4,422,660 | ||||||||||

|

| |||||||||

| ||||||||||

Computers & Peripherals 2.7% | ||||||||||

Electronics For Imaging, Inc.* | 66,300 | 2,809,131 | ||||||||

|

| |||||||||

| ||||||||||

Construction & Engineering 1.7% |

| |||||||||

Comfort Systems USA, Inc. | 37,400 | 637,296 | ||||||||

Furmanite Corp.* | 102,300 | 1,194,864 | ||||||||

|

| |||||||||

| 1,832,160 | ||||||||||

|

| |||||||||

| ||||||||||

Consumer Finance 2.9% | ||||||||||

Nelnet, Inc., Class A | 25,000 | 931,250 | ||||||||

Nicholas Financial, Inc. | 64,650 | 1,020,177 | ||||||||

World Acceptance Corp.* | 11,600 | 1,110,004 | ||||||||

|

| |||||||||

| 3,061,431 | ||||||||||

|

| |||||||||

| Common Stocks (continued) | ||||||||||

| Shares | Market Value | |||||||||

| ||||||||||

Containers & Packaging 1.6% | ||||||||||

Myers Industries, Inc. | 90,400 | $ | 1,731,160 | |||||||

|

| |||||||||

| ||||||||||

Distributors 0.6% |

| |||||||||

Weyco Group, Inc. | 23,600 | 623,512 | ||||||||

|

| |||||||||

| ||||||||||

Diversified Consumer Services 2.9% |

| |||||||||

Carriage Services, Inc. | 140,717 | 3,011,344 | ||||||||

|

| |||||||||

| ||||||||||

Electric Utilities 2.3% |

| |||||||||

Great Plains Energy, Inc. | 22,500 | 555,300 | ||||||||

PNM Resources, Inc. | 45,500 | 1,121,575 | ||||||||

Portland General Electric Co. | 23,200 | 700,176 | ||||||||

|

| |||||||||

| 2,377,051 | ||||||||||

|

| |||||||||

| ||||||||||

Electrical Equipment 4.6% |

| |||||||||

EnerSys, Inc. | 46,400 | 3,157,984 | ||||||||

Espey Manufacturing & Electronics Corp. | 8,300 | 259,375 | ||||||||

Lihua International, Inc.* | 38,400 | 209,664 | ||||||||

Powell Industries, Inc. | 7,100 | 436,011 | ||||||||

SL Industries, Inc.* | 29,203 | 759,862 | ||||||||

|

| |||||||||

| 4,822,896 | ||||||||||

|

| |||||||||

| ||||||||||

Electronic Equipment, Instruments & Components 3.6% |

| |||||||||

Benchmark Electronics, Inc.* | 24,800 | 563,704 | ||||||||

Hollysys Automation Technologies Ltd.* | 60,911 | 1,027,569 | ||||||||

PC Connection, Inc. | 63,157 | 1,292,192 | ||||||||

Sanmina Corp.* | 32,322 | 540,424 | ||||||||

Vishay Intertechnology, Inc.* | 30,300 | 411,474 | ||||||||

|

| |||||||||

| 3,835,363 | ||||||||||

|

| |||||||||

| ||||||||||

Energy Equipment & Services 2.0% |

| |||||||||

Matrix Service Co.* | 80,100 | 2,105,028 | ||||||||

|

| |||||||||

| ||||||||||

Food & Staples Retailing 0.8% |

| |||||||||

Andersons, Inc. (The) | 9,700 | 802,578 | ||||||||

|

| |||||||||

| ||||||||||

Food Products 0.6% |

| |||||||||

John B. Sanfilippo & Son, Inc. | 4,777 | 110,588 | ||||||||

Sanderson Farms, Inc. | 7,600 | 565,060 | ||||||||

|

| |||||||||

| 675,648 | ||||||||||

|

| |||||||||

| ||||||||||

Gas Utilities 0.5% |

| |||||||||

Gas Natural, Inc. | 52,700 | 483,259 | ||||||||

|

| |||||||||

| ||||||||||

Health Care Equipment & Supplies 0.4% |

| |||||||||

Kewaunee Scientific Corp. | 9,725 | 161,435 | ||||||||

Span-America Medical Systems, Inc. | 11,000 | 218,240 | ||||||||

|

| |||||||||

| 379,675 | ||||||||||

|

| |||||||||

| ||||||||||

Health Care Providers & Services 3.5% |

| |||||||||

Addus HomeCare Corp.* | 76,000 | 1,796,640 | ||||||||

PharMerica Corp.* | 7,100 | 172,814 | ||||||||

Triple-S Management Corp., Class B* | 93,734 | 1,672,215 | ||||||||

|

| |||||||||

| 3,641,669 | ||||||||||

|

| |||||||||

9

Statement of Investments (Continued)

January 31, 2014 (Unaudited)

Nationwide Bailard Cognitive Value Fund (Continued)

| Common Stocks (continued) | ||||||||||

| Shares | Market Value | |||||||||

| ||||||||||

Hotels, Restaurants & Leisure 0.3% | ||||||||||

Rick’s Cabaret International, Inc.* | 28,800 | $ | 325,152 | |||||||

|

| |||||||||

| ||||||||||

Household Durables 0.5% |

| |||||||||

La-Z-Boy, Inc. | 18,900 | 508,788 | ||||||||

|

| |||||||||

| ||||||||||

Household Products 0.9% |

| |||||||||

Oil-Dri Corp. of America | 27,800 | 954,930 | ||||||||

|

| |||||||||

| ||||||||||

Information Technology Services 0.2% |

| |||||||||

Global Cash Access Holdings, Inc.* | 29,100 | 246,768 | ||||||||

NCI, Inc., Class A* | 200 | 1,330 | ||||||||

|

| |||||||||

| 248,098 | ||||||||||

|

| |||||||||

| ||||||||||

Insurance 7.1% |

| |||||||||

Allied World Assurance Co. Holdings AG | 5,900 | 607,228 | ||||||||

Aspen Insurance Holdings Ltd. | 23,550 | 916,095 | ||||||||

FBL Financial Group, Inc., Class A | 10,600 | 409,478 | ||||||||

Hanover Insurance Group, Inc. (The) | 39,038 | 2,167,780 | ||||||||

HCI Group, Inc. | 21,238 | 903,252 | ||||||||

Safety Insurance Group, Inc. | 6,907 | 373,531 | ||||||||

United Insurance Holdings Corp. | 33,800 | 444,808 | ||||||||

Universal Insurance Holdings, Inc. | 145,430 | 1,621,544 | ||||||||

|

| |||||||||

| 7,443,716 | ||||||||||

|

| |||||||||

| ||||||||||

Internet Software & Services 2.5% |

| |||||||||

Blucora, Inc.* | 97,400 | 2,494,414 | ||||||||

XO Group, Inc.* | 15,500 | 188,015 | ||||||||

|

| |||||||||

| 2,682,429 | ||||||||||

|

| |||||||||

| ||||||||||

Life Sciences Tools & Services 0.5% |

| |||||||||

Nordion, Inc.* | 56,400 | 539,184 | ||||||||

|

| |||||||||

| ||||||||||

Machinery 1.6% |

| |||||||||

CIRCOR International, Inc. | 10,800 | 777,816 | ||||||||

Greenbrier Cos., Inc. (The)* | 10,400 | 381,576 | ||||||||

NN, Inc. | 28,100 | 497,089 | ||||||||

|

| |||||||||

| 1,656,481 | ||||||||||

|

| |||||||||

| ||||||||||

Marine 1.5% |

| |||||||||

Safe Bulkers, Inc. | 163,751 | 1,603,122 | ||||||||

|

| |||||||||

| ||||||||||

Media 0.1% |

| |||||||||

Insignia Systems, Inc.* | 31,220 | 85,543 | ||||||||

|

| |||||||||

| ||||||||||

Multi-Utilities 0.6% |

| |||||||||

Avista Corp. | 21,500 | 619,845 | ||||||||

|

| |||||||||

| ||||||||||

Oil, Gas & Consumable Fuels 3.8% |

| |||||||||

Adams Resources & Energy, Inc. | 7,500 | 498,900 | ||||||||

Delek US Holdings, Inc. | 28,100 | 851,430 | ||||||||

Gran Tierra Energy, Inc.* | 125,598 | 948,265 | ||||||||

TransGlobe Energy Corp.* | 237,684 | �� | 1,730,339 | |||||||

|

| |||||||||

| 4,028,934 | ||||||||||

|

| |||||||||

| Common Stocks (continued) | ||||||||||

| Shares | Market Value | |||||||||

| ||||||||||

Paper & Forest Products 2.8% |

| |||||||||

Schweitzer-Mauduit International, Inc. | 63,796 | $ | 2,942,909 | |||||||

|

| |||||||||

| ||||||||||

Professional Services 1.0% |

| |||||||||

VSE Corp. | 24,129 | 1,064,330 | ||||||||

|

| |||||||||

| ||||||||||

Real Estate Investment Trusts (REITs) 4.6% |

| |||||||||

DuPont Fabros Technology, Inc. | 28,600 | 743,314 | ||||||||

Franklin Street Properties Corp. | 64,400 | 772,156 | ||||||||

Medical Properties Trust, Inc. | 22,700 | 301,229 | ||||||||

One Liberty Properties, Inc. | 46,000 | 959,560 | ||||||||

Pennsylvania Real Estate Investment Trust | 15,100 | 281,615 | ||||||||

Post Properties, Inc. | 16,400 | 769,652 | ||||||||

Urstadt Biddle Properties, Inc., Class A | 7,095 | 133,102 | ||||||||

Winthrop Realty Trust | 81,103 | 931,063 | ||||||||

|

| |||||||||

| 4,891,691 | ||||||||||

|

| |||||||||

| ||||||||||

Semiconductors & Semiconductor Equipment 3.0% |

| |||||||||

Cascade Microtech, Inc.* | 90,182 | 928,874 | ||||||||

Silicon Motion Technology Corp., ADR-TW | 6,100 | 102,663 | ||||||||

Supertex, Inc.* | 78,088 | 2,084,950 | ||||||||

|

| |||||||||

| 3,116,487 | ||||||||||

|

| |||||||||

|

|

|

|

| ||||||

Software 2.0% |

| |||||||||

Perfect World Co., Ltd., ADR-CN | 109,000 | 2,109,150 | ||||||||

|

| |||||||||

| ||||||||||

Specialty Retail 1.4% |

| |||||||||

Haverty Furniture Cos., Inc. | 15,939 | 443,423 | ||||||||

Kirkland’s, Inc.* | 11,100 | 209,013 | ||||||||

Trans World Entertainment Corp.* | 222,049 | 879,314 | ||||||||

|

| |||||||||

| 1,531,750 | ||||||||||

|

| |||||||||

| ||||||||||

Textiles, Apparel & Luxury Goods 1.0% |

| |||||||||

Crown Crafts, Inc. | 130,166 | 1,041,328 | ||||||||

|

| |||||||||

| ||||||||||

Thrifts & Mortgage Finance 1.8% |

| |||||||||

First Defiance Financial Corp. | 34,100 | 877,052 | ||||||||

WSFS Financial Corp. | 14,040 | 1,008,072 | ||||||||

|

| |||||||||

| 1,885,124 | ||||||||||

|

| |||||||||

| ||||||||||

Trading Companies & Distributors 1.2% |

| |||||||||

Aceto Corp. | 60,648 | 1,293,015 | ||||||||

|

| |||||||||

| ||||||||||

Wireless Telecommunication Services 1.3% |

| |||||||||

USA Mobility, Inc. | 93,800 | 1,337,588 | ||||||||

|

| |||||||||

Total Common Stocks |

| 100,169,677 | ||||||||

|

| |||||||||

10

Statement of Investments (Continued)

January 31, 2014 (Unaudited)

Nationwide Bailard Cognitive Value Fund (Continued)

| Exchange Traded Funds 3.8% | ||||||||||

| Shares | Market Value | |||||||||

| ||||||||||

Equity Funds 3.8% | ||||||||||

iShares Russell 2000 Value ETF | 21,000 | $ | 2,008,440 | |||||||

Vanguard Small-Cap Value ETF | 21,000 | 1,987,860 | ||||||||

|

| |||||||||

| 3,996,300 | ||||||||||

|

| |||||||||

Total Exchange Traded Funds |

| 3,996,300 | ||||||||

|

| |||||||||

| Mutual Fund 1.0% | ||||||||||

Money Market Fund 1.0% | ||||||||||

Fidelity Institutional Money Market Fund — Institutional Class, 0.08% (a) | 1,078,490 | 1,078,490 | ||||||||

|

| |||||||||

Total Mutual Fund (cost $1,078,490) |

| 1,078,490 | ||||||||

|

| |||||||||

Total Investments |

| 105,244,467 | ||||||||

Other assets in excess of liabilities — 0.1% |

| 83,134 | ||||||||

|

| |||||||||

NET ASSETS — 100.0% |

| $ | 105,327,601 | |||||||

|

| |||||||||

| * | Denotes a non-income producing security. |

| (a) | Represents 7-day effective yield as of January 31, 2014. |

| (b) | See notes to financial statements for tax cost and unrealized appreciation/(depreciation) of securities. |

| ADR | American Depositary Receipt |

| AG | Stock Corporation |

| CN | China |

| ETF | Exchange Traded Fund |

| Ltd. | Limited |

| REIT | Real Estate Investment Trust |

| TW | Taiwan |

The accompanying notes are an integral part of these financial statements.

11

Statement of Assets and Liabilities

January 31, 2014 (Unaudited)

| Nationwide Bailard Cognitive Value Fund | ||||||

Assets: | ||||||

Investments, at value (cost $99,480,793) | $ | 105,244,467 | ||||

Dividends receivable | 39,224 | |||||

Receivable for investments sold | 1,996,265 | |||||

Receivable for capital shares issued | 1,394,080 | |||||

Prepaid expenses | 17,874 | |||||

|

| |||||

Total Assets | 108,691,910 | |||||

|

| |||||

Liabilities: | ||||||

Payable for investments purchased | 3,213,006 | |||||

Payable for capital shares redeemed | 27,495 | |||||

Cash overdraft (Note 2) | 12 | |||||

Accrued expenses and other payables: | ||||||

Investment advisory fees | 69,324 | |||||

Fund administration fees | 6,325 | |||||

Distribution fees | 11,993 | |||||

Administrative servicing fees | 1,502 | |||||

Accounting and transfer agent fees | 4,350 | |||||

Trustee fees | 1,172 | |||||

Deferred compensation (Note 2) | 6,254 | |||||

Custodian fees | 585 | |||||

Compliance program costs (Note 3) | 1,528 | |||||

Professional fees | 14,034 | |||||

Printing fees | 4,432 | |||||

Other | 2,297 | |||||

|

| |||||

Total Liabilities | 3,364,309 | |||||

|

| |||||

Net Assets | $ | 105,327,601 | ||||

|

| |||||

Represented by: | ||||||

Capital | $ | 98,775,896 | ||||

Accumulated distributions in excess of net investment income | (312,991 | ) | ||||

Accumulated net realized gains from investment transactions | 1,101,022 | |||||

Net unrealized appreciation/(depreciation) from investments | 5,763,674 | |||||

|

| |||||

Net Assets | $ | 105,327,601 | ||||

|

| |||||

Net Assets: | ||||||

Class A Shares | $ | 1,166,369 | ||||

Class C Shares | 13,197,488 | |||||

Class M Shares | 89,803,168 | |||||

Institutional Service Class Shares | 1,150,222 | |||||

Institutional Class Shares | 10,354 | |||||

|

| |||||

Total | $ | 105,327,601 | ||||

|

| |||||

Shares Outstanding (unlimited number of shares authorized): | ||||||

Class A Shares | 93,617 | |||||

Class C Shares | 1,104,431 | |||||

Class M Shares | 7,233,599 | |||||

Institutional Service Class Shares | 92,538 | |||||

Institutional Class Shares | 834 | |||||

|

| |||||

Total | 8,525,019 | |||||

|

| |||||

12

Statement of Assets and Liabilities (Continued)

January 31, 2014 (Unaudited)

| Nationwide Bailard Cognitive Value Fund | ||||||

Net asset value and redemption price per share (Net assets by class divided by shares outstanding by class, respectively): | ||||||

Class A Shares (a) | $ | 12.46 | ||||

Class C Shares (b) | $ | 11.95 | ||||

Class M Shares | $ | 12.41 | ||||

Institutional Service Class Shares | $ | 12.43 | ||||

Institutional Class Shares | $ | 12.41 | ||||

Maximum offering price per share (100%/(100%-maximum sales charge) of net asset value adjusted to the nearest cent): | ||||||

Class A Shares | $ | 13.22 | ||||

|

| |||||

Maximum Sales Charge: | ||||||

Class A Shares | 5.75 | % | ||||

|

| |||||

| (a) | For Class A Shares, the redemption price per share is reduced by 1.00% on sales of shares of original purchases of $1,000,000 or more or that were not subject to a front-end sales charge made with 18 months of the purchase date. |

| (b) | For Class C Shares, the redemption price per share is reduced by 1.00% for shares held less than 1 year. |

The accompanying notes are an integral part of these financial statements.

13

Statement of Operations

For the Six Months Ended January 31, 2014 (Unaudited)

| Nationwide Bailard Cognitive Value Fund | ||||||

INVESTMENT INCOME: | ||||||

Dividend income | $ | 998,230 | ||||

Interest income | 39 | |||||

Foreign tax withholding | (2,728 | ) | ||||

|

| |||||

Total Income | 995,541 | |||||

|

| |||||

EXPENSES: | ||||||

Investment advisory fees | 391,450 | |||||

Fund administration fees | 65,492 | |||||

Distribution fees Class A | 1,436 | |||||

Distribution fees Class C | 39,338 | |||||

Administrative servicing fees Class A | 1,219 | |||||

Administrative servicing fees Institutional Service Class (a) | 1,736 | |||||

Registration and filing fees | 25,167 | |||||

Professional fees | 16,399 | |||||

Printing fees | 9,108 | |||||

Trustee fees | 1,891 | |||||

Custodian fees | 2,223 | |||||

Accounting and transfer agent fees | 7,969 | |||||

Compliance program costs (Note 3) | 1,748 | |||||

Other | 8,790 | |||||

|

| |||||

Total expenses before earnings credit, fees waived, and expenses reimbursed | 573,966 | |||||

|

| |||||

Earnings credit (Note 5) | (41 | ) | ||||

Administrative servicing fees voluntarily waived — Class A (Note 3) | (141 | ) | ||||

Administrative servicing fees voluntarily waived — Institutional Service Class (a) (Note 3) | (235 | ) | ||||

Expenses reimbursed by adviser (Note 3) | (3,943 | ) | ||||

|

| |||||

Net Expenses | 569,606 | |||||

|

| |||||

NET INVESTMENT INCOME | 425,935 | |||||

|

| |||||

REALIZED/UNREALIZED GAINS (LOSSES) FROM INVESTMENTS: | ||||||

Net realized gains from investment transactions | 3,834,901 | |||||

Net change in unrealized appreciation/(depreciation) from investments | (614,020 | ) | ||||

|

| |||||

Net realized/unrealized gains from investments | 3,220,881 | |||||

|

| |||||

CHANGE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 3,646,816 | ||||

|

| |||||

| (a) | Effective September 16, 2013, Fiduciary Shares were renamed Institutional Service Class Shares. |

The accompanying notes are an integral part of these financial statements.

14

Statements of Changes in Net Assets

| Nationwide Bailard Cognitive Value Fund | ||||||||||||

| Six Months Ended January 31, 2014 (Unaudited) | Year Ended July 31, 2013 | |||||||||||

Operations: | ||||||||||||

Net investment income | $ | 425,935 | $ | 1,330,136 | ||||||||

Net realized gains from investment transactions | 3,834,901 | 22,104,698 | ||||||||||

Net change in unrealized appreciation/(depreciation) from investments | (614,020 | ) | 1,516,351 | |||||||||

|

|

|

| |||||||||

Change in net assets resulting from operations | 3,646,816 | 24,951,185 | ||||||||||

|

|

|

| |||||||||

Distributions to Shareholders From: | ||||||||||||

Net investment income: | ||||||||||||

Class A | (8,779 | ) | (5,466 | ) | ||||||||

Class C | (142,234 | ) | (1,418 | ) | ||||||||

Class M | (1,084,904 | ) | (975,185 | ) | ||||||||

Institutional Service Class (a) | (12,511 | ) | (35,776 | ) | ||||||||

Institutional Class | (120 | )(b) | – | |||||||||

Net realized gains: | ||||||||||||

Class A | (204,658 | ) | – | |||||||||

Class C | (2,644,093 | ) | – | |||||||||

Class M | (17,530,044 | ) | – | |||||||||

Institutional Service Class (a) | (246,368 | ) | – | |||||||||

Institutional Class | (1,945 | )(b) | – | |||||||||

|

|

|

| |||||||||

Change in net assets from shareholder distributions | (21,875,656 | ) | (1,017,845 | ) | ||||||||

|

|

|

| |||||||||

Change in net assets from capital transactions | 26,774,861 | (9,217,565 | ) | |||||||||

|

|

|

| |||||||||

Change in net assets | 8,546,021 | 14,715,775 | ||||||||||

|

|

|

| |||||||||

Net Assets: | ||||||||||||

Beginning of period | 96,781,580 | 82,065,805 | ||||||||||

|

|

|

| |||||||||

End of period | $ | 105,327,601 | $ | 96,781,580 | ||||||||

|

|

|

| |||||||||

Accumulated undistributed (distributions in excess of) net investment income at end of period | $ | (312,991 | ) | $ | 509,622 | |||||||

|

|

|

| |||||||||

CAPITAL TRANSACTIONS: | ||||||||||||

Class A Shares | ||||||||||||

Proceeds from shares issued | $ | 213,764 | $ | 493,322 | (c) | |||||||

Dividends reinvested | 187,155 | 4,699 | ||||||||||

Cost of shares redeemed | (179,896 | ) | (205,914 | ) | ||||||||

|

|

|

| |||||||||

Total Class A Shares | 221,023 | 292,107 | ||||||||||

|

|

|

| |||||||||

Class C Shares | ||||||||||||

Proceeds from shares issued | 14,406,228 | 125,270 | (c) | |||||||||

Dividends reinvested | 2,776,516 | 1,190 | ||||||||||

Cost of shares redeemed | (1,814,130 | ) | (102,342 | ) | ||||||||

|

|

|

| |||||||||

Total Class C Shares | 15,368,614 | 24,118 | ||||||||||

|

|

|

| |||||||||

| (a) | Effective September 16, 2013, Fiduciary Shares were renamed Institutional Service Class Shares. |

| (b) | For the period from September 19, 2013 (commencement of operations) through January 31, 2014. |

| (c) | Includes redemption fees. See Note 4 for further information. |

15

Statements of Changes in Net Assets (Continued)

| Nationwide Bailard Cognitive Value Fund | ||||||||||||

| Six Months Ended January 31, 2014 (Unaudited) | Year Ended July 31, 2013 | |||||||||||

CAPITAL TRANSACTIONS: (continued) | ||||||||||||

Class M Shares | ||||||||||||

Proceeds from shares issued | $ | 4,337,002 | $ | 6,055,974 | (c) | |||||||

Dividends reinvested | 16,825,543 | 866,070 | ||||||||||

Cost of shares redeemed | (9,391,980 | ) | (12,514,797 | ) | ||||||||

|

|

|

| |||||||||

Total Class M Shares | 11,770,565 | (5,592,753 | ) | |||||||||

|

|

|

| |||||||||

Institutional Service Class Shares (a) | ||||||||||||

Proceeds from shares issued | 10,984 | 1,303,454 | (c) | |||||||||

Dividends reinvested | 233,874 | 30,635 | ||||||||||

Cost of shares redeemed | (842,264 | ) | (5,275,126 | ) | ||||||||

|

|

|

| |||||||||

Total Institutional Service Class Shares | (597,406 | ) | (3,941,037 | ) | ||||||||

|

|

|

| |||||||||

Institutional Class Shares | ||||||||||||

Proceeds from shares issued | 10,000 | (b) | – | |||||||||

Dividends reinvested | 2,065 | (b) | – | |||||||||

Cost of shares redeemed | – | (b) | – | |||||||||

|

|

|

| |||||||||

Total Institutional Class Shares | 12,065 | (b) | – | |||||||||

|

|

|

| |||||||||

Change in net assets from capital transactions | $ | 26,774,861 | $ | (9,217,565 | ) | |||||||

|

|

|

| |||||||||

SHARE TRANSACTIONS: | ||||||||||||

Class A Shares | ||||||||||||

Issued | 15,523 | 36,204 | ||||||||||

Reinvested | 15,020 | 383 | ||||||||||

Redeemed | (11,893 | ) | (15,249 | ) | ||||||||

|

|

|

| |||||||||

Total Class A Shares | 18,650 | 21,338 | ||||||||||

|

|

|

| |||||||||

Class C Shares | ||||||||||||

Issued | 967,299 | 9,595 | ||||||||||

Reinvested | 232,150 | 100 | ||||||||||

Redeemed | (133,506 | ) | (7,810 | ) | ||||||||

|

|

|

| |||||||||

Total Class C Shares | 1,065,943 | 1,885 | ||||||||||

|

|

|

| |||||||||

Class M Shares | ||||||||||||

Issued | 308,343 | 455,168 | ||||||||||

Reinvested | 1,355,805 | 70,873 | ||||||||||

Redeemed | (662,285 | ) | (922,037 | ) | ||||||||

|

|

|

| |||||||||

Total Class M Shares | 1,001,863 | (395,996 | ) | |||||||||

|

|

|

| |||||||||

Institutional Service Class Shares (a) | ||||||||||||

Issued | 838 | 98,683 | ||||||||||

Reinvested | 18,815 | 2,507 | ||||||||||

Redeemed | (56,690 | ) | (412,288 | ) | ||||||||

|

|

|

| |||||||||

Total Institutional Service Class Shares | (37,037 | ) | (311,098 | ) | ||||||||

|

|

|

| |||||||||

| (a) | Effective September 16, 2013, Fiduciary Shares were renamed Institutional Service Class Shares. |

| (b) | For the period from September 19, 2013 (commencement of operations) through January 31, 2014. |

| (c) | Includes redemption fees. See Note 4 for further information. |

16

Statements of Changes in Net Assets (Continued)

| Nationwide Bailard Cognitive Value Fund | ||||||||||||

| Six Months Ended January 31, 2014 (Unaudited) | Year Ended July 31, 2013 | |||||||||||

SHARE TRANSACTIONS: (continued) | ||||||||||||

Institutional Class Shares | ||||||||||||

Issued | 668 | (b) | – | |||||||||

Reinvested | 166 | (b) | – | |||||||||

Redeemed | – | (b) | – | |||||||||

|

|

|

| |||||||||

Total Institutional Class Shares | 834 | (b) | – | |||||||||

|

|

|

| |||||||||

Total change in shares | 2,050,253 | (683,871 | ) | |||||||||

|

|

|

| |||||||||

Amounts designated as “–” are zero or have been rounded to zero.

| (b) | For the period from September 19, 2013 (commencement of operations) through January 31, 2014. |

The accompanying notes are an integral part of these financial statements.

17

Financial Highlights

Selected data for each share of capital outstanding throughout the periods indicated

Nationwide Bailard Cognitive Value Fund

| Operations | Distributions | Ratios/Supplemental Data | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net Asset Value, Beginning of Period | Net Investment Income (Loss) | Net Realized and Unrealized Gains (Losses) from Investments | Total from Operations | Net Investment Income | Net Realized Gains | Total Distributions | Redemption Fees | Net Asset Value, End of Period | Total Return (a)(b) | Net Assets at End of Period | Ratio of Expenses to Average Net Assets (c) | Ratio of Net Investment Income (Loss) to Average Net Assets (c) | Ratio of Expenses (Prior to Reimbursements) to Average Net Assets (c)(d) | Portfolio Turnover (e) | ||||||||||||||||||||||||||||||||||||||||||||||

| Class A Shares | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Six Months Ended January 31, 2014 (f) | $ | 14.97 | 0.03 | 0.49 | 0.52 | (0.12 | ) | (2.91 | ) | (3.03 | ) | – | $ | 12.46 | 3.52% | $ | 1,166,369 | 1.45% | 0.44 | % | 1.48% | 174.67% | ||||||||||||||||||||||||||||||||||||||

Year Ended July 31, 2013 (f) | $ | 11.48 | 0.14 | 3.45 | 3.59 | (0.10 | ) | – | (0.10 | ) | – | $ | 14.97 | 31.48% | $ | 1,122,377 | 1.47% | 1.09 | % | 1.58% | 339.00% | |||||||||||||||||||||||||||||||||||||||

Year Ended July 31, 2012 (f) | $ | 11.51 | 0.03 | (0.01 | ) | 0.02 | (0.05 | ) | – | (0.05 | ) | – | $ | 11.48 | 0.21% | $ | 615,772 | 1.47% | 0.23 | % | 1.60% | 268.00% | ||||||||||||||||||||||||||||||||||||||

Year Ended July 31, 2011 (f) | $ | 9.37 | 0.07 | 2.19 | 2.26 | (0.12 | ) | – | (0.12 | ) | – | $ | 11.51 | 24.05% | $ | 961,056 | 1.47% | 0.60 | % | 1.58% | 216.00% | |||||||||||||||||||||||||||||||||||||||

Year Ended July 31, 2010 (f) | $ | 7.89 | 0.03 | 1.50 | 1.53 | (g) | (0.05 | ) | – | (0.05 | ) | – | $ | 9.37 | 19.60% | (g) | $ | 654,681 | 1.45% | 0.34 | % | 1.58% | 152.00% | |||||||||||||||||||||||||||||||||||||

Year Ended July 31, 2009 (f) | $ | 10.19 | 0.06 | (2.34 | ) | (2.28 | ) | (0.02 | ) | – | (0.02 | ) | – | $ | 7.89 | (22.40% | ) | $ | 332,812 | 1.40% | 0.74 | % | 1.59% | 141.00% | ||||||||||||||||||||||||||||||||||||

| Class C Shares | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Six Months Ended January 31, 2014 (f) | $ | 14.55 | (0.01 | ) | 0.48 | 0.47 | (0.16 | ) | (2.91 | ) | (3.07 | ) | – | $ | 11.95 | 3.20% | $ | 13,197,488 | 1.98% | (0.08 | %) | 1.98% | 174.67% | |||||||||||||||||||||||||||||||||||||

Year Ended July 31, 2013 (f) | $ | 11.17 | 0.06 | 3.36 | 3.42 | (0.04 | ) | – | (0.04 | ) | – | $ | 14.55 | 30.67% | $ | 559,903 | 2.07% | 0.49 | % | 2.08% | 339.00% | |||||||||||||||||||||||||||||||||||||||

Year Ended July 31, 2012 (f) | $ | 11.20 | (0.04 | ) | 0.01 | (0.03 | ) | – | – | – | – | $ | 11.17 | (0.27% | ) | $ | 408,689 | 2.07% | (0.37 | %) | 2.10% | 268.00% | ||||||||||||||||||||||||||||||||||||||

Year Ended July 31, 2011 (f) | $ | 9.11 | – | 2.12 | 2.12 | (0.03 | ) | – | (0.03 | ) | – | $ | 11.20 | 23.30% | $ | 567,831 | 2.07% | – | 2.08% | 216.00% | ||||||||||||||||||||||||||||||||||||||||

Year Ended July 31, 2010 (f) | $ | 7.68 | (0.02 | ) | 1.47 | 1.45 | (g) | (0.02 | ) | – | (0.02 | ) | – | $ | 9.11 | 18.92% | (g) | $ | 520,057 | 2.05% | (0.26 | %) | 2.08% | 152.00% | ||||||||||||||||||||||||||||||||||||

Year Ended July 31, 2009 (f) | $ | 10.04 | 0.01 | (2.32 | ) | (2.31 | ) | (0.05 | ) | – | (0.05 | ) | – | $ | 7.68 | (22.92% | ) | $ | 413,389 | 2.02% | 0.12 | % | 2.09% | 141.00% | ||||||||||||||||||||||||||||||||||||

| Class M Shares | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Six Months Ended January 31, 2014 (f) | $ | 14.95 | 0.07 | 0.48 | 0.55 | (0.18 | ) | (2.91 | ) | (3.09 | ) | – | $ | 12.41 | 3.69% | $ | 89,803,168 | 1.01% | 0.90 | % | 1.02% | 174.67% | ||||||||||||||||||||||||||||||||||||||

Year Ended July 31, 2013 (f) | $ | 11.47 | 0.19 | 3.44 | 3.63 | (0.15 | ) | – | (0.15 | ) | – | $ | 14.95 | 31.94% | $ | 93,162,527 | 1.07% | 1.49 | % | 1.08% | 339.00% | |||||||||||||||||||||||||||||||||||||||

Year Ended July 31, 2012 (f) | $ | 11.51 | 0.07 | – | 0.07 | (0.11 | ) | – | (0.11 | ) | – | $ | 11.47 | 0.71% | $ | 75,990,508 | 1.07% | 0.63 | % | 1.10% | 268.00% | |||||||||||||||||||||||||||||||||||||||

Year Ended July 31, 2011 (f) | $ | 9.37 | 0.11 | 2.18 | 2.29 | (0.15 | ) | – | (0.15 | ) | – | $ | 11.51 | 24.54% | $ | 87,921,410 | 1.07% | 1.00 | % | 1.08% | 216.00% | |||||||||||||||||||||||||||||||||||||||

Year Ended July 31, 2010 (f) | $ | 7.87 | 0.06 | 1.51 | 1.57 | (g) | (0.07 | ) | – | (0.07 | ) | – | $ | 9.37 | 20.08% | (g) | $ | 70,390,248 | �� | 1.05% | 0.74 | % | 1.08% | 152.00% | ||||||||||||||||||||||||||||||||||||

Year Ended July 31, 2009 (f) | $ | 10.22 | 0.08 | (2.34 | ) | (2.26 | ) | (0.09 | ) | – | (0.09 | ) | – | $ | 7.87 | (22.02% | ) | $ | 67,710,862 | 1.02% | 1.12 | % | 1.09% | 141.00% | ||||||||||||||||||||||||||||||||||||

| Institutional Service Class Shares (h) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Six Months Ended January 31, 2014 (f) | $ | 14.95 | 0.06 | 0.48 | 0.54 | (0.15 | ) | (2.91 | ) | (3.06 | ) | – | $ | 12.43 | 3.61% | $ | 1,150,222 | 1.20% | 0.75 | % | 1.24% | 174.67% | ||||||||||||||||||||||||||||||||||||||

Year Ended July 31, 2013 (f) | $ | 11.46 | 0.18 | 3.45 | 3.63 | (0.14 | ) | – | (0.14 | ) | – | $ | 14.95 | 31.93% | $ | 1,936,773 | 1.14% | 1.42 | % | 1.33% | 339.00% | |||||||||||||||||||||||||||||||||||||||

Year Ended July 31, 2012 (f) | $ | 11.50 | 0.06 | – | 0.06 | (0.10 | ) | – | (0.10 | ) | – | $ | 11.46 | 0.60% | $ | 5,050,836 | 1.16% | 0.54 | % | 1.35% | 268.00% | |||||||||||||||||||||||||||||||||||||||

Year Ended July 31, 2011 (f) | $ | 9.36 | 0.09 | 2.19 | 2.28 | (0.14 | ) | – | (0.14 | ) | – | $ | 11.50 | 24.32% | $ | 5,075,223 | 1.21% | 0.86 | % | 1.33% | 216.00% | |||||||||||||||||||||||||||||||||||||||

Year Ended July 31, 2010 (f) | $ | 7.87 | 0.06 | 1.50 | 1.56 | (g) | (0.07 | ) | – | (0.07 | ) | – | $ | 9.36 | 20.06% | (g) | $ | 2,230,226 | 1.13% | 0.66 | % | 1.33% | 152.00% | |||||||||||||||||||||||||||||||||||||

Year Ended July 31, 2009 (f) | $ | 10.23 | 0.08 | (2.35 | ) | (2.27 | ) | (0.09 | ) | – | (0.09 | ) | – | $ | 7.87 | (22.10% | ) | $ | 1,837,049 | 1.03% | 1.11 | % | 1.34% | 141.00% | ||||||||||||||||||||||||||||||||||||

| Institutional Class Shares | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Period Ended January 31, 2014 (f)(i) | $ | 14.97 | 0.04 | 0.49 | 0.53 | (0.18 | ) | (2.91 | ) | (3.09 | ) | – | $ | 12.41 | 3.55% | $ | 10,354 | 0.99% | 0.70 | % | 0.99% | 174.67% | ||||||||||||||||||||||||||||||||||||||

Amounts designated as “–” are zero or have been rounded to zero.

| (a) | Excludes sales charge. |

| (b) | Not annualized for periods less than one year. |

| (c) | Annualized for periods less than one year. |

| (d) | During the period, certain fees may have been waived and/or reimbursed. If such waivers/reimbursements had not occurred, the ratios would have been as indicated. |

| (e) | Portfolio turnover is calculated on the basis of the Fund as a whole without distinguishing among the classes of shares. |

| (f) | Per share calculations were performed using average shares method. |

| (g) | Includes payment by affiliates of $0.001 per share. The effects of such pauments did not affect the amount shown as total return for the period. |

| (h) | Effective September 16, 2013, Fiduciary Shares were renamed Institutional Service Class Shares. |

| (i) | For the period from September 19, 2013 (commencement of operations) through January 31, 2014. Total return is calculated based on inception date of September 18, 2013 through January 31, 2014. |

The accompanying notes are an integral part of these financial statements.

18

| Fund Commentary | Nationwide Bailard International Equities Fund |

For the semiannual period ended January 31, 2014, the Nationwide Bailard International Equities Fund (Class M at NAV) returned 10.34%* versus 5.48% for its benchmark, the MSCI ACWI ex USA. For broader comparison, the median return for the Fund’s closest Lipper peer category of International Multi-Cap Core Funds (consisting of 165 funds as of January 31, 2014) was 6.21% for the same time period.

| * | Performance prior to the Fund’s inception on September 16, 2013, is based on the performance of the Fund’s predecessor fund. |

The Fund operates from the top down, with a strategy that focuses first on country selection, followed by stock selection within each individual market. During the reporting period, both country and stock selection were positive contributors to Fund performance versus the primary benchmark. Broadly speaking, added value on the country selection side came from overweighting the better-performing markets of developed Europe and underweighting a number of poor-performing emerging markets. The six months of the reporting period saw a wide divergence in returns between developed markets, particularly in Europe (the MSCI Europe ex-UK Index rose more than 10%), and emerging markets (the MSCI Emerging Markets® Index posted a small loss). In Europe, positive gross domestic product (GDP) growth readings in Spain and Italy, along with a revised economic outlook from the Organization for Economic Cooperation and Development (OECD), provided evidence of the Continent’s emergence from recession. Meanwhile, the anticipation and start of bond purchase tapering (gradual reduction in monetary easing) by the U.S. Federal Reserve had widely negative effects on sentiment toward emerging market stocks and currencies.

Country choices that proved beneficial for Fund performance during the reporting period included overweight positions in Finland, Germany and Spain, zero-weight positions in laggards Canada and Singapore, and underweight or zero-weight positions in troubled emerging markets Brazil, Indonesia, Thailand, South Africa and Turkey. Also helpful for Fund performance was an overweight in Egypt, a top performer among all markets. A large overweight in Japan, combined with a

sizable currency hedge, formed a “long local market, short yen” position that proved beneficial to the Fund as the yen weakened from 98 to 102 per dollar during the reporting period.

Results on the stock selection side were strongest for the Fund during the reporting period in Japan and across much of developed Europe (France, Switzerland, the U.K., Spain, Germany and the Netherlands), where portfolio holdings far outperformed the respective MSCI country indexes. Within each market, the Fund’s sector weights are generally held in line with the country index, and sector selection is not pursued as an investment strategy. Notable individual stock outperformers included Fund holdings in printer and watch maker Seiko Epson in Japan, computer peripheral company Logitech International in Switzerland, banks Credit Agricole in France and Bankinter in Spain, retailer W.H. Smith in the U.K., travel services firm TUI in Germany and temporary staffing company Randstad in the Netherlands.

Country selection decisions that did not help Fund results during the reporting period included a couple of “misses” in high-flying developed Europe (zero weights in Italy and Denmark) as well as overweight exposures to disappointing emerging markets Hungary and Russia (positions still held at the end of the reporting period) and the typhoon-struck Philippines (position sold at the end of 2013).

Points of weakness for stock selection within the Fund during the reporting period were Belgium and Finland, where Fund holdings failed to keep up with the respective MSCI country indexes. Results for the emerging markets as a whole were negative, due to slippage in China, Russia, the Czech Republic and Egypt, standing in stark contrast to the very strong developed market results; fortunately, the impact from this on overall Fund performance was minimal as the Fund’s average weight in emerging markets was less than 10%. The most notable individual stock detractor was a name not held by the Fund, Nokia in Finland, which rose mightily on a generous bid by Microsoft for its handset business.

19

| Fund Commentary (cont’d) | Nationwide Bailard International Equities Fund |

The Fund entered into financial futures contracts (“futures contracts”) to enable the Fund to more closely approximate the performance of its benchmark indices or for tactical hedging purposes. The Fund entered into forward foreign currency contracts in connection with planned purchases or sales of securities denominated in a foreign currency and/or to hedge the U.S. dollar value of portfolio securities denominated in a foreign currency.

Subadviser:

Bailard, Inc.

Portfolio Managers:

Anthony Craddock; Peter M. Hill; and Eric P. Leve

The Fund is subject to the risks of investing in equity securities and risks associated with investing in foreign securities, such as currency fluctuation, political risk, differences in accounting and limited availability of information, all of which are magnified in emerging markets. The Fund may invest in more-aggressive investments such as derivatives (many of which create investment leverage and are highly volatile) and exchange-traded funds (ETFs) (shareholders will bear additional costs). Please refer to the summary prospectus for a more detailed explanation of the Fund’s principal risks.

A description of the benchmarks can be found on the Market Index Definitions page at the back of this book.

20

| Fund Overview (Unaudited) | Nationwide Bailard International Equities Fund |

Objective

The Fund seeks long-term capital appreciation.

Highlights

| Ÿ | For the semiannual period ended January 31, 2014, the Fund (Class M at NAV) returned 10.34%, outperforming the benchmark by 4.86% and the Lipper peer category by 4.13%. |

| Ÿ | Country choices that proved beneficial for Fund performance during the reporting period included overweight positions in Finland, Germany and Spain, zero-weight positions in laggards Canada and Singapore, and underweight or zero-weight positions in troubled emerging markets Brazil, Indonesia, Thailand, South Africa and Turkey. |

| Ÿ | Country selection detracted from Fund performance during the reporting period in developed Europe (zero weights in Italy and Denmark) as well as overweight exposures to disappointing emerging markets Hungary, Russia and the Philippines. |

Asset Allocation†

| Common Stocks | 95.5% | |||

| Mutual Fund | 3.4% | |||

| Exchange Traded Funds | 2.0% | |||

| Liabilities in excess of other assets | (0.9)% | |||

| 100.0% |

Top Industries††

| Commercial Banks | 10.3% | |||

| Pharmaceuticals | 7.9% | |||

| Insurance | 6.6% | |||

| Oil, Gas & Consumable Fuels | 5.1% | |||

| Auto Components | �� | 4.4% | ||

| Hotels, Restaurants & Leisure | 4.3% | |||

| Diversified Telecommunication Services | 3.0% | |||

| Food Products | 3.0% | |||

| Information Technology Services | 2.5% | |||

| Construction & Engineering | 2.4% | |||

| Other Industries | 50.5% | |||

| 100.0% |

Top Holdings††

| Fidelity Institutional Money Market Fund —Institutional Class | 3.4% | |||

| Roche Holding AG | 2.7% | |||

| Sumitomo Mitsui Financial Group, Inc. | 2.1% | |||

| Market Vectors ETF Trust | 1.5% | |||

| Bankinter SA | 1.5% | |||

| Credit Agricole SA | 1.4% | |||

| Vinci SA | 1.3% | |||

| Seiko Epson Corp. | 1.3% | |||

| Cie Generale des Etablissements Michelin | 1.3% | |||

| Bayer AG | 1.2% | |||

| Other Holdings | 82.3% | |||

| 100.0% |

Top Countries†

| Japan | 20.5% | |||

| United Kingdom | 12.9% | |||

| France | 11.6% | |||

| Switzerland | 11.1% | |||

| Germany | 8.1% | |||

| United States | 5.4% | |||

| Netherlands | 5.1% | |||

| Spain | 4.2% | |||

| Finland | 3.8% | |||

| Australia | 3.5% | |||

| Other Countries | 13.8% | |||

| 100.0% |

| † | Percentages indicated are based upon net assets as of January 31, 2014. |

| †† | Percentages indicated are based upon total investments as of January 31, 2014. |

21

| Fund Performance | Nationwide Bailard International Equities Fund |

Average Annual Total Return

(For periods ended January 31, 2014)

| Six Months* | 1 Yr. | 5 Yr. | 10 Yr. | |||||||||||||||

| Class A | w/o SC1 | 10.00% | 11.20% | 13.89% | 7.18% | |||||||||||||

| w/SC2 | 3.96% | 5.04% | 12.60% | 6.57% | ||||||||||||||

| Class C | w/o SC1 | 9.62% | 10.52% | 13.10% | 6.47% | |||||||||||||

| w/SC3 | 8.62% | 9.52% | 13.10% | 6.47% | ||||||||||||||

| Class M4 | w/o SC | 10.34% | 11.85% | 14.28% | 7.55% | |||||||||||||

| Institutional Service Class4,5 | w/o SC | 10.05% | 11.41% | 14.07% | 7.39% | |||||||||||||

| Institutional Class4 | w/o SC | 3.09% | 6 | — | — | — | ||||||||||||

All figures showing the effect of a sales charge (SC) reflect the maximum charge possible, because it has the most significant effect on performance data.

| * | Not annualized. |

| 1 | These returns do not reflect the effects of SCs. |

| 2 | For the period from September 16, 2013 through January 31, 2014 a front-end sales charge of 5.75% was deducted. Prior to September 16, 2013, a front-end sales charge of 5.50% was deducted. |

| 3 | A 1.00% CDSC was deducted from the one year return because it is charged when you sell Class C shares within the first year after purchase. |

| 4 | Not subject to any SCs. |

| 5 | Effective September 16, 2013 Fiduciary Shares were renamed Institutional Service Class Shares. |

| 6 | Since inception date of September 18, 2013. Not Annualized. |

Expense Ratios

| Expense Ratio* | ||

| Class A | 1.42% | |

| Class C | 1.92% | |

| Class M | 0.92% | |

| Institutional Service Class | 1.17% | |

| Institutional Class | 0.92% |

| * | Current effective prospectus dated September 16, 2013. Please see the Fund’s most recent prospectus for details. |

22

| Fund Performance | Nationwide Bailard International Equities Fund |

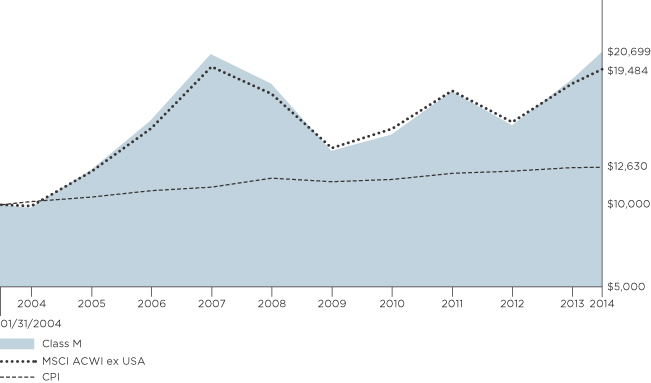

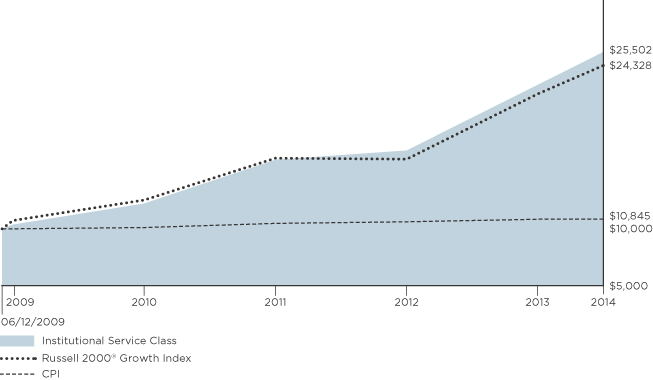

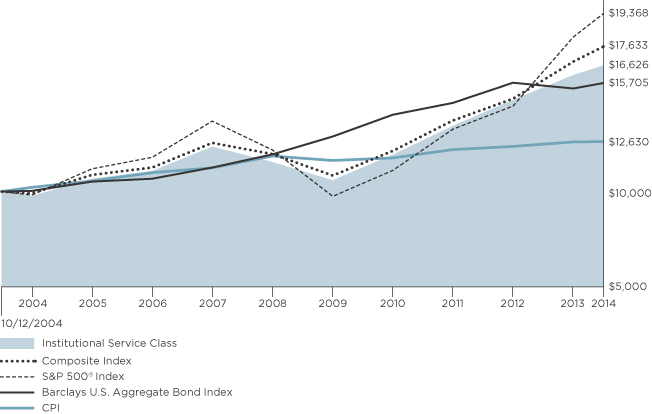

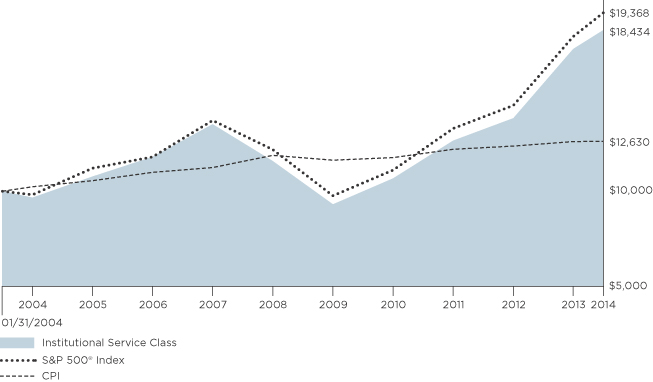

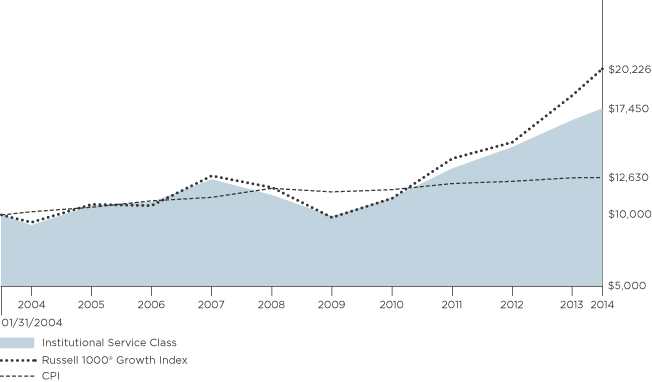

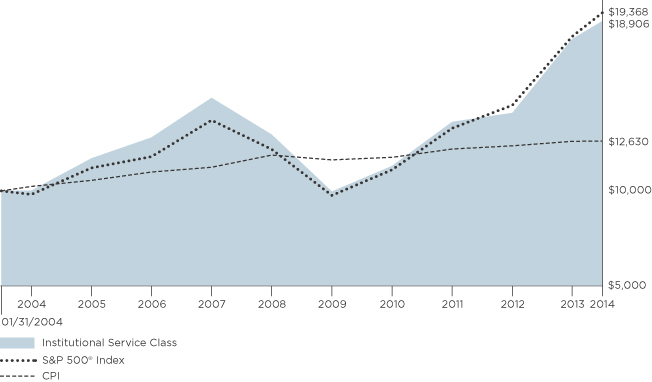

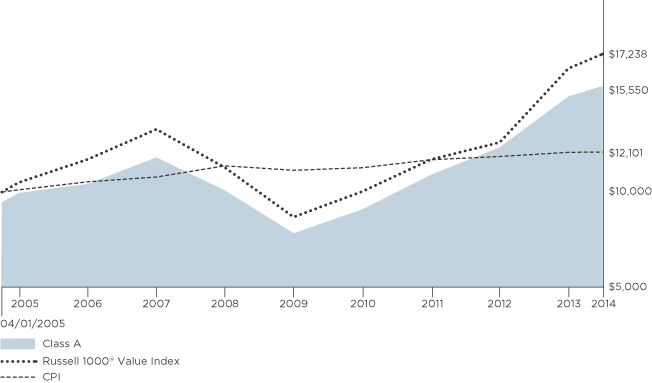

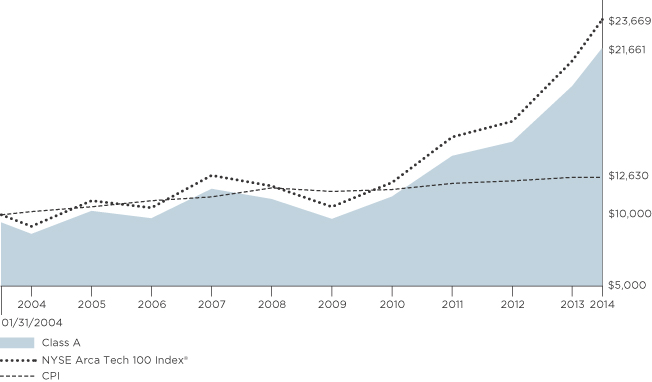

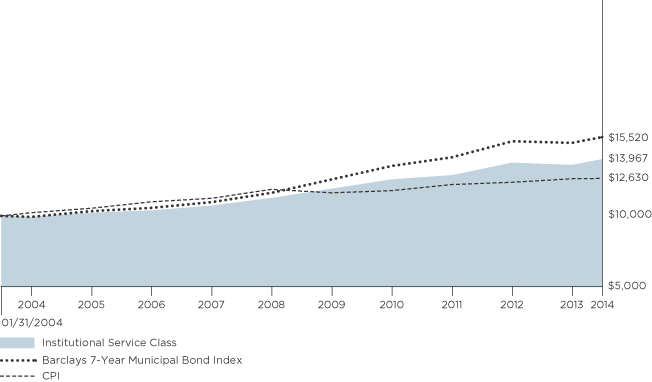

Performance of a $10,000 Investment

Investment return and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions.

Comparative performance of $10,000 invested in Class M shares of the Nationwide Bailard International Equities Fund versus the MSCI ACWI ex USA and the Consumer Price Index (CPI) over the 10-year period ended 1/31/14. Fund performance prior to the Fund’s inception on 9/16/13 is based on the Fund’s predecessor Fund. Unlike the Fund, the performance for these unmanaged indexes does not reflect any fees, expenses, or sales charges. One cannot invest directly in a market index. A description of the benchmarks can be found on the Market Index Definitions page at the back of this book.

23

| Shareholder Expense Example | Nationwide Bailard International Equities Fund |

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) paid on purchase payments and redemption fees; and (2) ongoing costs, including investment advisory fees, administration fees, distribution fees and other Fund expenses. The examples below are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. Per Securities and Exchange Commission (“SEC”) requirements, the examples assume that you had a $1,000 investment in the Class at the beginning of the reporting period (August 1, 2013) and continued to hold your shares at the end of the reporting period (January 31, 2014).

Actual Expenses

For each Class of the Fund in the table below, the first line provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid from August 1, 2013 through January 31, 2014. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line of each Class under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Expenses for Comparison Purposes

The second line of each Class in the table below provides information about hypothetical account values and hypothetical expenses based on the Class’ actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Class’ actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period from August 1, 2013 through January 31, 2014. You may use this information to compare the ongoing costs of investing in the Class of the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as sales charges (loads) or redemption fees. If these transaction costs were included, your costs would have been higher. Therefore, the second line for each Class in the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. The examples also assume all dividends and distributions are reinvested.

Schedule of Shareholder Expenses

Expense Analysis of a $1,000 Investment

Nationwide Bailard International January 31, 2014 | Beginning Account Value ($) 08/01/13 | Ending Account Value ($) 01/31/14 | Expenses Paid During Period ($) 08/01/13 - 01/31/14 | Expense Ratio During Period (%) 08/01/13 - 01/31/14 | ||||||||

| Class A Shares | Actual | a | 1,000.00 | 1,100.00 | 7.36 | 1.39 | ||||||

| Hypothetical | a,b | 1,000.00 | 1,018.20 | 7.07 | 1.39 | |||||||

| Class C Shares | Actual | a | 1,000.00 | 1,096.20 | 10.20 | 1.93 | ||||||

| Hypothetical | a,b | 1,000.00 | 1,015.48 | 9.80 | 1.93 | |||||||

| Class M Shares | Actual | a | 1,000.00 | 1,103.40 | 4.93 | 0.93 | ||||||

| Hypothetical | a,b | 1,000.00 | 1,020.52 | 4.74 | 0.93 | |||||||

| Institutional Service Class Sharesc | Actual | a | 1,000.00 | 1,100.50 | 6.14 | 1.16 | ||||||

| Hypothetical | a,b | 1,000.00 | 1,019.36 | 5.90 | 1.16 | |||||||

| Institutional Class Shares | Actual | d | 1,000.00 | 1,030.90 | 3.31 | 0.88 | ||||||

| Hypothetical | a,b | 1,000.00 | 1,020.77 | 4.48 | 0.88 | |||||||

| a | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value from August 1, 2013 through January 31, 2014 multiplied to reflect one-half year period. The expense ratio presented represents a six-month, annualized ratio in accordance with Securities and Exchange Commission guidelines. |

| b | Represents the hypothetical 5% return before expenses. |

| c | Effective September 16, 2013, Fiduciary Shares were renamed Institutional Service Class Shares. |

| d | Actual expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value from September 19, 2013 through January 31, 2014 to reflect the period from commencement of operations. |

24

Statement of Investments

January 31, 2014 (Unaudited)

Nationwide Bailard International Equities Fund

| Common Stocks 95.5% | ||||||||||

| Shares | Market Value | |||||||||

| ||||||||||

AUSTRALIA 3.5% |

| |||||||||

Capital Markets 0.3% |

| |||||||||

Perpetual Ltd. | 20,000 | $ | 823,134 | |||||||

|

| |||||||||

Construction & Engineering 0.3% |

| |||||||||

Leighton Holdings Ltd. | 50,000 | 718,607 | ||||||||

|

| |||||||||

Containers & Packaging 0.5% |

| |||||||||

Amcor Ltd. | 120,000 | 1,125,638 | ||||||||

Orora Ltd.* | 120,000 | 134,423 | ||||||||

|

| |||||||||

| 1,260,061 | ||||||||||

| �� |

|

| ||||||||

Diversified Financial Services 0.4% |

| |||||||||