UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

FORM 10-K

(Mark One)

☑ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2018

OR

◻TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ___________ to ___________.

Commission File Number 000-23827

PC CONNECTION, INC.

(Exact name of registrant as specified in its charter)

Delaware | 02-0513618 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| |

730 Milford Road Merrimack, New Hampshire | 03054 (Zip Code) |

(Address of principal executive offices) | |

| | | |

| Registrant’s telephone number, including area code | (603) 683-2000 | |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | | Name of each exchange on which registered | |

| Common Stock, $.01 par value | | Nasdaq Global Select Market | |

Securities registered pursuant to Section 12(g) of the Act:

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

YES ☐ NO ☑

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

YES ☐ NO ☑

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

YES ☑ NO ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

YES ☑ NO ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ___ Accelerated filer Non-accelerated filer ___ Smaller reporting company ___ Emerging growth company ___

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

YES ☐ NO ☑

The aggregate market value of the registrant’s voting shares of common stock held by non-affiliates of the registrant on June 29, 2018, based on $33.20 per share, the last reported sale price on the Nasdaq Global Select Market on that date, was $380,230,570.

The number of shares outstanding of each of the registrant’s classes of common stock, as of February 4, 2019:

Class | | Number of Shares |

Common Stock, $.01 par value | | 26,395,683 |

The following documents are incorporated by reference into the Annual Report on Form 10-K: Portions of the registrant’s definitive Proxy Statement for its 2019 Annual Meeting of Stockholders are incorporated by reference into Part III of this Report.

FORWARD-LOOKING STATEMENTS

Statements contained or incorporated by reference in this Annual Report on Form 10‑K that are not based on historical fact are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Exchange Act. These forward-looking statements regarding future events and our future results are based on current expectations, estimates, forecasts, and projections and the beliefs and assumptions of management including, without limitation, our expectations with regard to the industry’s rapid technological change and exposure to inventory obsolescence, availability and allocations of goods, reliance on vendor support and relationships, competitive risks, pricing risks, and the overall level of economic activity and the level of business investment in information technology products. Forward-looking statements may be identified by the use of forward-looking terminology such as “may,” “could,” “expect,” “believe,” “estimate,” “anticipate,” “continue,” “seek,” “plan,” “intend,” or similar terms, variations of such terms, or the negative of those terms.

We cannot assure investors that our assumptions and expectations will prove to have been correct. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks, and changes in circumstances that are difficult to predict. These statements involve known and unknown risks, uncertainties, and other factors that may cause our actual results, performance, or achievements to be materially different from any future results, performance, or achievements expressed or implied by the forward-looking statements. We therefore caution you against undue reliance on any of these forward-looking statements. Important factors that could cause our actual results to differ materially from those indicated or implied by forward-looking statements include those discussed in Item 1A., “Risk Factors” of this Annual Report on Form 10-K. Any forward-looking statement made by us in this Annual Report on Form 10-K speaks only as of the date on which this Annual Report on Form 10-K was first filed. We undertake no intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise, except as may be required by law.

PART I

Item 1. Business

GENERAL

We are a national solutions provider of a wide range of information technology, or IT, solutions. We help our customers design, enable, manage, and service their IT environments. We provide IT products, including computer systems, data center solutions, software and peripheral equipment, networking communications, and other products and accessories that we purchase from manufacturers, distributors, and other suppliers. We also offer services involving design, configuration, and implementation of IT solutions. These services are performed by our personnel and by third-party providers. We have three operating segments, which serve primarily: (a) small- to medium-sized businesses, or SMBs, in our Business Solutions segment, through our PC Connection Sales subsidiary, (b) large enterprise customers, in our Enterprise Solutions segment, through our MoreDirect subsidiary, and (c) federal, state, and local government and educational institutions, in our Public Sector Solutions segment, through our GovConnection subsidiary. Financial results for each of our segments are included in the financial statements attached hereto. We generate sales through (i) outbound telemarketing and field sales contacts by sales representatives focused on the business, educational, healthcare, and government markets, (ii) our websites, and (iii) direct responses from customers responding to our advertising media. We offer a broad selection of over 425,000 products at competitive prices, including products from vendors like Apple, Cisco Systems, Dell, EMC, Hewlett-Packard, Lenovo, Microsoft, and VMWare, and we partner with more than 1,600 suppliers. We typically leverage our state-of-the art logistic capabilities to ship product to customers the same day the order is received.

Since our founding in 1982, we have consistently served our customers’ needs by providing innovative, reliable, and timely service and technical support, and by offering an extensive assortment of branded products through knowledgeable, well-trained sales and support teams. Our strategy’s effectiveness is reflected in the recognition we have received, including being named to the Fortune 1000 and the CRN Solution Provider 500 for eighteen straight years. Over the past few years, we have received numerous awards, including the Microsoft Excellence in Operations—Double Gold Level Award for delivering market-leading operational excellence, as well as being recently named to the CRN Tech Elite 250 for the third year. We believe that our ability to understand our customers’ needs and provide comprehensive and effective IT solutions has resulted in strong brand name recognition and a broad and loyal customer base. We also believe that through our strong vendor relationships we can provide an efficient supply chain and be an effective IT solution provider for our multiple customer segments.

We strive to identify the unique needs of our corporate, government, healthcare, educational, and small business customers, and have designed our business processes to enable our customers to effectively manage their IT systems. We provide value by offering our customers efficient design, integration, deployment, and support of their IT environments. As of December 31, 2018, we employed 823 sales representatives, whose average tenure exceeded six years. Sales representatives are responsible for managing enterprise, commercial, and public sector accounts, as specialization and a deep understanding of unique customer environments are more important than ever. These sales representatives focus on current and prospective customers and are supported by an increasing number of engineering, technical, and administrative staff. We believe that increasing our salesforce productivity is important to our future success, and we have increased our headcount and investments in this area accordingly.

In September 2016, we launched “Connection®,” uniting all of our subsidiaries into one cohesive brand, reflecting the promise of our trademark blue arc and our mission to connect people with technology that enhances growth, elevates productivity, and empowers innovation. MoreDirect, our enterprise team, became Connection® Enterprise Solutions; PC Connection Sales Corp, our SMB-focused team, became Connection® Business Solutions; and GovConnection, our public sector team, became Connection® Public Sector Solutions.

We market our products and services through our websites: www.connection.com, www.connection.com/enterprise, www.connection.com/publicsector, and www.macconnection.com. Our websites provide extensive product information, customized pricing, rich content, and a digital platform for online orders.

Additional financial information regarding our business segments and geographic data about our customers and assets is contained in Management’s Discussion and Analysis of Financial Condition and Results of Operations in Item 7 of Part II, and in Note 14 to our Consolidated Financial Statements included in Item 8 of Part II of this Annual Report on Form 10-K.

We are subject to the informational requirements of the Securities Exchange Act of 1934, as amended, or the Exchange Act, and accordingly, we file reports, proxy and information statements, and other information with the Securities and Exchange Commission, or the SEC. Information regarding the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. The SEC maintains a website (http://www.sec.gov) that contains such reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. We maintain a corporate website with the address www.connection.com. We are not including the information contained in our website as part of, or incorporating by reference into, this Annual Report on Form 10-K. We make available free of charge through our website our Annual Reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K, and amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act, as soon as reasonably practical after we electronically file these materials with, or otherwise furnish them to, the SEC.

MARKET AND COMPETITION

In the fiscal year ended December 31, 2018, we generated approximately 38% of our sales from small- to medium-sized customer accounts, 43% from medium-to-large corporate accounts (Fortune 1000), and 19% from government and educational institutions. The overall IT market that we serve is estimated to be approximately $200 billion.

The largest segment of this market is served by local and regional “value added resellers”, or VARs, many of whom we believe are transitioning from the hardware and software products business to higher-margin IT services. We have transitioned from an end-user or desktop-centric computing supplier to a network or enterprise-wide IT solutions supplier. We have also partnered with third-party technology and telecommunications service providers. We now offer our customers access to the same services and technical expertise as local and regional VARs, but with a more extensive product selection at generally lower prices.

Intense competition for customers has led manufacturers of our IT products to use all available channels, including solutions providers, to distribute their products. Certain of these manufacturers who have traditionally used resellers to distribute their products have, from time to time, established their own direct marketing operations, including sales through the Internet. Nonetheless, we believe that these manufacturers will continue to provide us and other third-party solutions providers favorable product allocations and marketing support.

We believe new entrants to the IT Solutions channel must overcome a number of obstacles, including:

| · | | the substantial time and resources required to build a customer base of meaningful size and profitability for cost-effective operation; |

| · | | the high costs of developing the information systems and operating infrastructure required to successfully compete as a national solutions provider; |

| · | | the advantages enjoyed by larger and more established competitors in terms of purchasing and operating efficiencies; |

| · | | the difficulty of building relationships with vendors to achieve favorable product allocations and attractive pricing terms; and |

| · | | the difficulty of identifying and recruiting management personnel with significant direct marketing experience in the industry. |

BUSINESS STRATEGIES

We believe we become our customers’ IT provider of choice by providing innovative IT solutions which meet their needs of increased productivity, mobility, virtualization, and security in a continually evolving IT environment. We provide enhanced value by assisting them in cost-effectively maximizing business opportunities provided by new technologies and advanced service solutions. The key elements of our business strategies include:

| · | | Providing consistent customer service before, during, and after the sale. We believe that we have earned a reputation for providing superior customer service by consistently focusing on our customers’ needs. We have dedicated our resources to developing strong, long-term relationships with our customers by accurately assessing their IT needs, and providing scalable, high-quality solutions and services through our knowledgeable, well-trained personnel. Through operational excellence, we have efficient delivery programs that provide a quality buying experience for our customers with reasonable return policies. |

| · | | Offering a broad product selection at competitive prices. We offer a broad range of IT products and solutions, including personal computers and related peripheral products, servers, storage, managed services, and networking infrastructure, at costs that allow our customers to be more productive while maximizing their IT budgets. Our advanced solution offerings include network, server, storage, and mission-critical onsite installation and support using proprietary cloud-based service management software. We offer products and enhanced service capabilities with aggressive price and performance standards, all with the convenience of one-stop shopping for technology solutions. |

| · | | Simplifying technology product procurement for corporate customers. We offer Internet-based procurement options to eliminate complexity and enhance customer value, as well as lower the cost of procurement for our customers. We specialize in Internet-based solutions and provide electronic integration between our customers and suppliers. |

| · | | Offering targeted IT solutions. Our customers seek solutions to increasingly complex IT infrastructure demands. To better address their business needs, we have focused our solution service capabilities on seven practice areas—Converged Data Center, Networking, Mobility, Security, Cloud Solutions, Lifecycle, and Software. These IT practice groups are responsible for understanding the infrastructure needs of our customers, and for designing cost-effective technology solutions to address them. We have also partnered with third-party providers to make available a range of IT support services, including asset assessment, implementation, maintenance, and disposal services. We believe we can leverage these seven practice groups to transform our company into a recognized IT solution provider, which will enable us to capture a greater share of the IT expenditures of our customers. |

| · | | Maintaining a strong brand name and customer awareness. Since our founding in 1982, we have built a strong brand name and customer awareness. We have been named to the Fortune 1000 and the CRN Solution Provider 500 for each of the last eighteen years. We actively work with our existing customers to become their IT provider of choice for products and enhanced solution services, while seeking to ensure our reputation of high-quality customer service, tailored marketing programs, and competitive pricing lead the way to expanding our share of the overall IT market. |

| · | | Maintaining long-standing vendor relationships. We have a history of strong relationships with vendors, and were among the first national solutions providers qualified by manufacturers to market computer systems to end users. By working closely with our vendors to provide an efficient channel for the advertising and distribution of their products and solutions, we expect to expand market share and generate opportunities for optimizing partner incentive programs. |

GROWTH STRATEGIES

Our growth strategies are designed to increase revenues by maximizing operational efficiencies while offering innovative products and value added service offerings, increasing penetration of our existing customers, and expanding our customer base. Our six key elements of growth are:

| · | | Expanding hardware and software offerings. We offer our customers an extensive range of IT hardware and software products, and in response to customer demand, we continually evaluate and add new products as they become available. We work closely with vendors to identify and source first-to-market product offerings at aggressive prices. |

| · | | Expanding IT solution services offerings. We strive to accelerate solution and service growth by providing creative solutions to the increasingly complex hardware and software needs of our customers. Our Converged Data Center, Networking, Mobility, Security, Cloud Solutions, Lifecycle, and Software services practice groups consist of industry-certified and product-certified engineers, as well as highly specialized third-party providers. Our investment in these seven practice areas is expected to increase our share of our customers’ annual IT expenditures by broadening the range of products and services they purchase from us. |

| · | | Targeting customer segments. Through increased targeted marketing, we seek to expand the number of our active customers and generate additional sales to existing customers by providing more value-added services and solutions. We have developed specialty catalogs featuring product offerings designed to address the needs of specific customer populations, including new product inserts targeted to purchasers of graphics, server, and networking products. We also utilize Internet marketing campaigns that focus on select markets, such as healthcare. |

| · | | Increasing productivity of our sales representatives. We believe that higher sales productivity is the key to leveraging our expense structure and driving future profitability improvements. We invest significant resources in training new sales representatives and providing ongoing training to experienced personnel. Our training and evaluation programs are focused towards assisting our sales personnel in understanding and anticipating clients’ IT needs, with the goal of fostering loyal customer relationships. We also provide our sales representatives with technical support on more complex sales opportunities through our expanding group of technical solution specialists. |

| · | | Migrating to cloud-based solutions for our customers. Cloud computing is a key driver of new IT spending as our customers seek scalable, cost-effective solutions. We plan to expand our cloud-based solution sales and assist our customers in navigating the complex and growing field of cloud-solution offerings. |

| · | | Pursuing strategic acquisitions and alliances. We seek acquisitions and alliances that add new customers, strengthen our product and solution offerings, add management talent, and produce operating results which are accretive to our core business earnings. |

SERVICE AND SUPPORT

Since our founding in 1982, our primary objective has been to provide products and services that meet the demands and needs of customers and to supplement those products with up-to-date product information and excellent customer service and support. We believe that offering our customers superior value, through a combination of product knowledge, consistent and reliable service and support, and leading products at competitive prices, differentiates us from other national solutions providers and provides the foundation for developing a broad and loyal customer base.

We invest in training programs for our service and support personnel, with an emphasis on putting customer needs and service first. Product support technicians assist customers with questions concerning compatibility, installation, and more difficult questions relating to product use. The product support technicians authorize customers to return defective or incompatible products to either the manufacturer or to us for warranty service. In-house technicians perform both warranty and non-warranty repair on most major systems and hardware products.

Using our customized information system, we transmit our customer orders either to our distribution center or to our drop‑ship suppliers, depending on product availability, for processing immediately after a customer receives credit approval. At our distribution center, we also perform custom configuration services, which typically includes custom imaging, the installation and integration of additional components, and other technology enhancements. Our customers may select the method of delivery that best meets their needs and is most cost effective, ranging from expedited overnight delivery for urgently needed items to ground freight.

Our inventory stocking strategy is based on economics and the general availability of the product. We will stock product where there is an economic advantage to do so, or the product is in constrained supply. We also will stock product to support customer rollouts, including product that is running through our configuration and integration services prior to shipment.

MARKETING AND SALES

We sell our products through our direct marketing channels to (i) SMBs including small office/home office customers, (ii) government and educational institutions, and (iii) medium-to-large corporate accounts. We strive to be the primary supplier of IT products and solutions to our existing and prospective customers by providing exemplary customer service. We use multiple marketing approaches to reach existing and prospective customers, including:

| · | | outbound telemarketing and field sales; |

| · | | digital, web, and print media advertising; and |

| · | | targeted marketing programs to specific customer populations. |

All of our marketing approaches emphasize our broad product and service offerings, fast delivery, customer support, competitive pricing, and our wide range of service solutions.

Sales Channels. We believe that our ability to establish and maintain long-term customer relationships and to encourage repeat purchases is largely dependent on the strength of our sales personnel and programs. Because our customers’ primary contact with us is through our sales representatives, we are committed to maintaining a qualified, knowledgeable, and motivated sales staff with its principal focus on customer service.

Outbound Telemarketing and Field Sales. We seek to build loyal relationships with potential high-volume customers by assigning them to individual account managers. We believe that customers respond favorably to one-on-one relationships with personalized, well-trained account managers. Once established, these one-on-one relationships are maintained and enhanced through frequent telecommunications and targeted electronic communications, as well as other marketing materials designed to meet each customer’s specific IT needs. We pay most of our account managers a base annual salary plus incentive compensation. Incentive compensation is tied generally to gross profit dollars produced by the individual account manager. Account managers historically have significantly increased productivity after approximately twelve months of training and experience.

E-commerce Sales. (www.connection.com, www.connection.com/enterprise, www.connection.com/publicsector, and www.macconnection.com) We provide product descriptions and prices for generally all products online. Our Connection website also provides updated information for more than 425,000 items. We offer, and continuously update, selected product offerings and other special buys. We believe our websites are important sales sources and communication tools for improving customer service.

Our MoreDirect subsidiary’s business process and operations are primarily Web-based. Most of its corporate customers utilize a customized Web page to quickly search, source, and track IT products. MoreDirect’s website (www.connection.com/enterprise) aggregates the current available inventories of its largest IT suppliers into a single online source for its corporate customers. Its custom designed Internet-based system, TRAXX®, provides corporate buyers with comparative pricing from several suppliers as well as special pricing arranged through the manufacturer.

The Internet supports three key business initiatives for us:

| · | | Customer choice — We have built our business on the premise that our customers should be able to choose how they interact with us--be it by telephone, or by means of their desktop or mobile device via email or the Internet. |

| · | | Lowering transactions costs — Our website tools include robust product search features and Internet Business Accounts (customized Web pages), which allow customers to quickly and easily find information about products of interest to them. If customers still have questions, they may call our account managers. Such phone calls are typically shorter and have higher close rates than calls from customers who have not first visited our websites. |

| · | | Leveraging the time of experienced sales representatives — Our investments in technology-based sales and service programs allow our sales representatives more time to build and maintain relationships with our customers and help them to solve their business problems. |

Business Segments. We conduct our business operations through three business segments: Business Solutions, Enterprise Solutions, and Public Sector Solutions.

Business Solutions Segment. Our principal target markets in this segment are small-to-medium-sized business customers. We use a combination of outbound telemarketing, including some on-site sales solicitation by business development managers, and Internet sales through customized Internet Business Accounts, to reach these customers.

Enterprise Solutions Segment. Through our custom designed Web-based system, we are able to offer our larger corporate customers an efficient and effective method of sourcing, evaluating, purchasing, and tracking a wide variety of IT products and services. Our strategy is to be the primary single source procurement portal for our large corporate customers.

Public Sector Solutions Segment. We use a combination of outbound telemarketing, including some on-site sales solicitation by business development managers, and Internet sales through customized Internet Business Accounts, to reach these customers. We target each of the four distinct market sectors within this segment—federal government, higher educational institutions, school grades K-12, and state and local governments.

The following table sets forth the relative distribution of net sales by business segment:

| | | | | | | |

| | Years Ended December 31, | |

| | 2018 | | 2017 | | 2016 | |

Sales Segment | | | | | | | |

Enterprise Solutions | | 43 | % | 39 | % | 38 | % |

Business Solutions | | 38 | | 40 | | 40 | |

Public Sector Solutions | | 19 | | 21 | | 22 | |

Total | | 100 | % | 100 | % | 100 | % |

Our brand, and each of Connection’s business segments, is supported by targeted marketing campaigns across a variety of media:

Digital. We utilize a series of digital programs, in conjunction with advanced data analytics, to identify prospective customers and generate new leads within our existing customer base. These programs include website, email, blog, social media, electronic catalogs, webinars, and video/multimedia promotions.

Print. Connection produces a variety of print media, including direct mail pieces and Connected, a quarterly publication that provides informative articles on the latest technologies and industry trends. We distribute specialty catalogs to education, healthcare, and government customers and prospective customers on a periodic basis. The

Company’s MacConnection® brand publishes an eponymous catalog for the Apple market. These publications showcase the depth of our in-house expertise in the marketplace and extend Connection’s brand to a wide audience of IT decision makers.

Specialty Marketing. In addition to our digital and print marketing efforts, Connection maintains a strong presence at industry tradeshows and conventions across the country, including a number of healthcare and education IT conferences. Connection also hosts a series of Technology Summits each year, with a focus on building stronger relationships with our customers and reinforcing our reputation as a trusted source of expertise.

Customers. We maintain an extensive database of customers and prospects. However, no single customer accounted for more than 3% of our consolidated revenue in 2018. While no single agency of the federal government comprised more than 3% of total sales, aggregate sales to the federal government were 5.4% 7.8%, and 7.5% in 2018, 2017, and 2016, respectively. The loss of any single customer would not have a material adverse effect on any of our business segments. In addition, we do not have individual orders in our backlog that are material to our business, as we typically ship products within hours of receipt of orders.

PRODUCTS AND MERCHANDISING

We continuously focus on expanding the breadth of our product and service offerings. We currently offer our customers over 425,000 information technology products designed for business applications from more than 1,600 vendors, including hardware and peripherals, accessories, networking products, and software. We select the products we sell based upon their technology and effectiveness, market demand, product features, quality, price, margins, and warranties. The following table sets forth our percentage of net sales (in dollars) for major product categories:

| | | | | | | |

| | PERCENTAGE OF | |

| | NET SALES | |

| | Years Ended December 31, | |

| | 2018 (1) | | 2017 (2) | | 2016 (2) | |

Notebooks/Mobility | | 26 | % | 22 | % | 23 | % |

Accessories | | 13 | | 10 | | 11 | |

Software | | 12 | | 23 | | 20 | |

Desktops | | 11 | | 11 | | 10 | |

Servers/Storage | | 11 | | 9 | | 10 | |

Displays and sound | | 9 | | 8 | | 8 | |

Net/Com Product | | 8 | | 7 | | 8 | |

Other Hardware/Services | | 10 | | 10 | | 10 | |

Total | | 100 | % | 100 | % | 100 | % |

| (1) | | The Company adopted ASC 606 in 2018 using the modified retrospective approach, which primarily resulted in certain software sales being reported on a net basis where they would have otherwise been reported on a gross basis under the previous revenue recognition guidance. As a result, certain revenue figures reported in the current year may not be comparable with prior-year disclosures. |

| (2) | | Product categories were separated into additional categories in 2018. Certain prior-year balances have been reclassified to conform to 2018 presentation. |

We offer a 30-day right of return generally limited to defective merchandise. Returns of non-defective products are subject to restocking fees. Substantially all of the products marketed by us are warranted by the manufacturer. We generally accept returns directly from the customer and then either credit the customer’s account or ship the customer a replacement or similar product from our inventory.

PURCHASING AND VENDOR RELATIONS

Product purchases from Ingram Micro, Inc., or Ingram, our largest supplier, accounted for approximately 22% of our total product purchases in both 2018 and 2017 and 21% in 2016. Purchases from Synnex Corporation, or Synnex, comprised 12%, 12%, and 13% of our total product purchases in 2018, 2017, and 2016, respectively. Purchases from Tech Data comprised of 10%, 11% and 8% in 2018, 2017, and 2016, respectively. Purchases from Hewlett-Packard

Company, or HP, accounted for approximately 7% of our total product purchases in 2018, 11% in 2017, and 9% in 2016. No other vendor supplied more than 10% of our total product purchases in 2018, 2017, or 2016. We believe that, while we may experience some short-term disruption if products from Ingram, Synnex, HP and/or Tech Data become unavailable to us, alternative sources for products obtained directly from Ingram, Synnex, HP and Tech Data are available.

Products manufactured by HP represented approximately 18% of our net sales in 2018 and approximately 20% in both 2017 and 2016. We believe that in the event we experience either a short-term or permanent disruption of supply of HP products, such disruption would likely have a material adverse effect on our results of operations and cash flows.

Many product suppliers reimburse us for advertisements or other cooperative marketing programs in our catalogs and other marketing vehicles. Reimbursements may be in the form of discounts, advertising allowances, and/or rebates. We also receive allowances from certain vendors based upon the volume of our purchases or sales of the vendors’ products by us. Some of our vendors offer limited price protection in the form of rebates or credits against future purchases. We may also participate in end-of-life product and other special purchases which may not be eligible for price protection.

We believe that we have excellent relationships with our vendors. We generally pay vendors within stated terms, or earlier when favorable cash discounts are offered. We believe our high volume of purchases enables us to obtain product pricing and terms that are competitive with those available to other national IT solutions providers. Although brand names and individual product offerings are important to our business, we believe that competitive products are available in substantially all of the merchandise categories offered by us.

DISTRIBUTION

We fulfill orders from customers both from products we hold in inventory and through drop shipping arrangements with manufacturers and distributors. At our 283,000 square foot technology integration and distribution complex in Wilmington, Ohio, we receive and ship inventory, configure and integrate technology solutions, provide depot maintenance and services, and process returned products.

We also place product orders directly with manufacturers and/or distribution companies for drop shipment directly to our customers. Order status with distributors is tracked online, and in all circumstances, a confirmation of shipment from manufacturers and/or distribution companies is received prior to initial recording of the transaction. At the end of each financial reporting period, revenue is adjusted to reflect the anticipated receipt of products by the customers in the period. Products drop shipped by suppliers were 80%, 77%, and 75%, of net sales in 2018, 2017, and 2016, respectively. In future years, we expect that products drop shipped from suppliers may increase, both in dollars and as a percentage of net sales, as we seek to lower our overall inventory and distribution costs while maintaining excellent customer service.

Certain of our larger customers occasionally request special staged delivery arrangements under which either we or our distribution partners set aside and temporarily hold inventory on our customer’s behalf. Such orders are firm delivery orders, and customers generally pay under normal credit terms, regardless of delivery. Revenue on such transactions is not recorded until shipment to their final destination as requested by the customer. Inventory held for such staged delivery requests aggregated $46.1 million and $32.0 million at December 31, 2018 and 2017, respectively.

MANAGEMENT INFORMATION SYSTEMS

Our subsidiaries utilize management information systems which have been significantly customized for our use. These systems permit centralized management of key functions, including order taking and processing, inventory and accounts receivable management, purchasing, sales, and distribution, and the preparation of daily operating control reports on key aspects of the business. We also operate advanced telecommunications equipment to support our sales and customer service operations. Key elements of the telecommunications systems are integrated with our computer systems to provide timely customer information to sales and service representatives, and to facilitate the preparation of operating and performance data.

Our success is dependent in large part on the accuracy and proper use of our information systems, including our telephone systems, to manage our inventory and accounts receivable collections, to purchase, sell, and ship our products efficiently and on a timely basis, and to maintain cost-efficient operations. We expect to continue upgrading our information systems in the future to more effectively manage our operations and customer database.

Our investments in IT systems and infrastructure are designed to enable us to operate more efficiently and to provide our customers enhanced functionality. In October 2017, we began a multi-year initiative to upgrade our IT infrastructure, and have incurred $16.3 million of capital expenditures through December 31, 2018. We expect additional related capital expenditures to range from $6.0 to $7.0 million over the next six to nine months, when we expect to have completed the initiative. For further discussion see “Liquidity and Capital Resources” of Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” of this Annual Report on Form 10-K.

COMPETITION

The direct marketing and sale of IT-related products is highly competitive. We compete with other national solutions providers of IT products, including CDW Corporation and Insight Enterprises, Inc., who are the current leaders in the space. We also compete with:

| · | | certain product manufacturers that sell directly to customers as well as some of our own suppliers, such as Apple, Dell, HP, and Lenovo; |

| · | | software publishers, such as Microsoft, VMware, Adobe, and Symantec; |

| · | | distributors that sell directly to certain customers; |

| · | | local and regional VARs; |

| · | | various franchisers, office supply superstores, and national computer retailers; and |

| · | | e-tailers, such as Amazon Web Services, with more extensive commercial online networks. |

Additional competition may arise if other new methods of distribution emerge in the future. We compete not only for customers, but also for favorable product allocations and cooperative advertising support from product manufacturers. Several of our competitors are larger than we are and have substantially greater financial resources. These and other factors related to our competitive position are discussed more fully in the “Overview” of Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” of this Annual Report on Form 10-K.

We believe that price, product selection and availability, solutions capabilities, and service and support are the most important competitive factors in our industry.

INTELLECTUAL PROPERTY RIGHTS

Our trademarks include, among others, Connection®, PC Connection®, GovConnection®, MacConnection®, we solve IT®, Everything Overnight®, The Connection™, HealthConnectionTM, Mobile Connection®, Cloud Connection®, ServiceConnectionTM, ProConnection™, Education Connection®, MoreDirect A PC Connection Company®, TRAXX®, WebSPOC®, Softmart®, GlobalServeTM, Raccoon CharacterTM, and their related logos and all iterations thereof. We intend to use and protect these and our other marks, as we deem necessary. We believe our trademarks have significant value and are an important factor in the marketing of our products. We do not maintain a traditional research and development group, but we work closely with computer product manufacturers and other technology developers to stay abreast of the latest developments in computer technology, with respect to the products we both sell and use.

WORK FORCE

As of December 31, 2018, we employed 2,513 persons (full-time equivalent), of whom 1,153 (including 330 management and support personnel) were engaged in sales-related activities, 556 were engaged in providing IT services and customer service and support, 526 were engaged in purchasing, marketing, and distribution-related activities, 82 were engaged in the operation and development of management information systems, and 196 were engaged in administrative and finance functions. We consider our employee relations to be good. Our employees are not represented by a labor union, and we have never experienced a labor related work stoppage.

Item 1A. Risk Factors

We cannot assure investors that our assumptions and expectations will prove to have been correct. Important factors could cause our actual results to differ materially from those indicated or implied by forward-looking statements. Such factors that could cause or contribute to such differences include those factors discussed below. We undertake no intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. If any of the following risks actually occur, our business, financial condition, or results of operations would likely suffer.

Instability in economic conditions in the financial markets may adversely affect our business and reduce our operating results.

Our business has been affected by changes in economic conditions that are outside of our control, including reductions in business investment, loss of consumer confidence, and fiscal uncertainty at both federal and state government levels. Reductions in federal government spending may result in significant reductions in program funding. Uncertainty also exists regarding expected economic conditions both globally and in the United States, and future delays or reductions in IT spending could have a material adverse effect on demand for our products and consequently on our financial results.

Despite the recent increase in general economic optimism, there is always a risk that heightened economic expectations may not be realized. Economic instability may arise, and it is difficult to predict to what extent our business may be adversely affected. However, if IT spending should again decline, we are likely to experience an adverse impact, which may be material on our business and our results of operations.

We have experienced variability in sales and may not be able to maintain profitable operations.

Several factors have caused our results of operations to fluctuate and we expect some of these fluctuations to continue. Causes of these fluctuations include:

| · | | shifts in customer demand that affect our distribution models, including demand for total solutions; |

| · | | loss of customers to competitors; |

| · | | industry shipments of new products or upgrades; |

| · | | changes in overall demand and timing of product shipments related to economic markets and to government spending; |

| · | | changes in vendor distribution of products; |

| · | | changes in our product offerings and in merchandise returns; |

| · | | changes in distribution models as a result of cloud and software-as-a-service, or SaaS; |

| · | | adverse weather conditions that affect response, distribution, or shipping; and |

Our results also may vary based on our ability to manage personnel levels in response to fluctuations in revenue. We base personnel levels and other operating expenditures on sales forecasts. If our revenues do not meet anticipated levels in the future, we may not be able to reduce our staffing levels and operating expenses in a timely manner to avoid significant losses from operations.

Substantial competition could reduce our market share and may negatively affect our business.

The direct marketing industry and the computer products retail business, in particular, are highly competitive. We compete with other national solutions providers of hardware and software and computer related products, including CDW Corporation and Insight Enterprises, Inc., who are the current leaders in the space. Certain hardware and software vendors, such as Apple, Dell, Lenovo, and HP, who provide products to us, also sell their products directly to end users through their own catalogs, stores, and via the Internet. We also compete with computer retail stores and websites, who are increasingly selling to business customers and may become a significant competitor. We compete not only for customers, but also for advertising support from IT product manufacturers. Some of our competitors have larger customer bases and greater financial, marketing, and other resources than we do. In addition, some of our competitors offer a wider range of products and services than we do and may be able to respond more quickly to new or changing opportunities, technologies, and customer requirements. Many current and potential competitors also have greater name recognition, engage in more extensive promotional activities, and adopt pricing policies that are more aggressive than ours. We expect competition to increase as retailers and solution providers who have not traditionally sold computers and related products enter the industry.

In addition, product resellers and national solutions providers are combining operations or acquiring or merging with other resellers and national solutions providers to increase efficiency. Moreover, current and potential competitors have established or may establish cooperative relationships among themselves or with third parties to enhance their products and services. Accordingly, it is possible that new competitors or alliances among competitors may emerge and acquire significant market share. We may not be able to continue to compete effectively against our current or future competitors. If we encounter new competition or fail to compete effectively against our competitors, our business may be harmed.

We face and will continue to face significant price competition.

Generally, pricing is very aggressive in our industry, and we expect pricing pressures to escalate should economic conditions deteriorate. An increase in price competition could result in a reduction of our profit margins. We may not be able to offset the effects of price reductions with an increase in the number of customers, higher sales, cost reductions, or otherwise. Such pricing pressures could result in an erosion of our market share, reduced sales, and reduced operating margins, any of which could have a material adverse effect on our business.

Virtualization of IT resources and applications, including networks, servers, applications, and data storage may disrupt or alter our traditional distribution models.

Our customers can access, through a cloud-based platform, business-critical solutions without the significant initial capital investment required for dedicated infrastructure. Growing demand for the development of cloud-based solutions may reduce demand for some of our existing hardware products. If the transition to an environment characterized by cloud-based computing and software being delivered as a service progresses, we will likely increase investments in this area before knowing whether our sales forecasts will accurately reflect customer demand for these products, services, and solutions. We may not be able to effectively compete using these virtual distribution models. Our inability to compete effectively with current or future virtual distribution model competitors, or adapt to a cloud-based environment, could have a material adverse effect on our business.

We may experience a reduction in the incentive programs offered to us by our vendors.

Some product manufacturers and distributors provide us with incentives such as supplier reimbursements, payment discounts, price protection, rebates, and other similar arrangements. The increasingly competitive technology reseller market has already resulted in the following:

| · | | reduction or elimination of some of these incentive programs; |

| · | | more restrictive price protection and other terms; and |

| · | | reduced advertising allowances and incentives. |

Many product suppliers provide us with advertising allowances, and in exchange, we feature their products on our website, and in our catalogs and other marketing vehicles. These vendor allowances, to the extent that they represent specific reimbursements of incremental and identifiable costs, are offset against SG&A expenses. Advertising allowances that cannot be associated with a specific program funded by an individual vendor or that exceed the fair value of advertising expense associated with that program are classified as offsets to cost of sales or inventory. In the past, we have experienced a decrease in the level of vendor consideration available to us from certain manufacturers. The level of such consideration we receive from some manufacturers may decline in the future. Such a decline could decrease our gross profit and have a material adverse effect on our earnings and cash flows.

Our business could be materially adversely affected by system failures, interruption, integration issues, or security lapses of our information technology systems or those of our third-party providers.

Our ability to effectively manage our business depends significantly on our information systems and infrastructure as well as, in certain instances those of our business partners and third-party providers. The failure of our current systems to operate effectively or to integrate with other systems, including integration of upgrades to better meet the changing needs of our customers, could result in transaction errors, processing inefficiencies, and the loss of sales and customers. In addition, cybersecurity threats are evolving and include, but are not limited to, malicious software, attempts to gain unauthorized access to company or customer data, denial of service attacks, the processing of fraudulent transactions, and other electronic security breaches that could lead to disruptions in critical systems, unauthorized release of confidential or otherwise protected information, and corruption of data. In our case, these attacks and attempted attacks have generally been in the form of active intrusion attempts from the internet, passive vulnerability mapping from the internet, and internal malware and or phishing attempts delivered through user actions. Although we have in place various processes, procedures, and controls to monitor and mitigate these threats, these measures may not be sufficient to prevent a material security threat or mitigate these risks for our customers. If any of these events were to materialize, they could lead to disruption of our operations or loss of sensitive information as well as subject us to regulatory actions, litigation, or damage to our reputation, and could have a material adverse effect on our financial position, results of operations, and cash flows. Similar risks exist with respect to our business partners and third-party providers. As a result, we are subject to the risk that the activities of our business partners and third-party providers may adversely affect our business even if an attack or breach does not directly impact our systems.

We could experience Internet and other system failures which would interfere with our ability to process orders.

We depend on the accuracy and proper use of our management information systems, including our telephone system. Many of our key functions depend on the quality and effective utilization of the information generated by our management information systems, including:

| · | | our ability to purchase, sell, and ship products efficiently and on a timely basis; |

| · | | our ability to manage inventory and accounts receivable collection; and |

| · | | our ability to maintain operations. |

Our management information systems require continual upgrades to most effectively manage our operations and customer database. Although we maintain some redundant systems, with full data backup, a significant component of our computer and telecommunications hardware is located in a single facility in New Hampshire, and a substantial interruption in our management information systems or in our telephone communication systems, including those resulting from extreme weather and natural disasters, as well as power loss, telecommunications failure, or similar events, would substantially hinder our ability to process customer orders and thus could have a material adverse effect on our business.

Should our financial performance not meet expectations, we may be required to record a significant charge to earnings for impairment of goodwill and other intangibles.

We test goodwill for impairment each year and more frequently if potential impairment indicators arise. Although the fair value of our Business Solutions and Enterprise Solutions reporting units substantially exceeded their carrying value at our annual impairment test, should the financial performance of a reporting unit not meet expectations due to the economy or otherwise, we would likely adjust downward expected future operating results and cash flows. Such adjustment may result in a determination that the carrying value of goodwill and other intangibles for a reporting unit exceeds its fair value. This determination may in turn require that we record a significant non-cash charge to earnings to reduce the $73.6 million aggregate carrying amount of goodwill held by our Business Solutions and Enterprise Solutions reporting units, resulting in a negative effect on our results of operations.

The failure to comply with our public sector contracts could result in, among other things, fines or liabilities.

Revenues from the Public Sector Solutions segment are derived from sales to federal, state, and local government departments and agencies, as well as to educational institutions, through various contracts and open market sales. Government contracting is a highly regulated area. Noncompliance with government procurement regulations or contract provisions could result in civil, criminal, and administrative liability, including substantial monetary fines or damages, termination of government contracts, and suspension, debarment, or ineligibility from doing business with the government. Our current arrangements with these government agencies allow them to cancel orders with little or no notice and do not require them to purchase products from us in the future. The effect of any of these possible actions by any government department or agency could adversely affect our financial position, results of operations, and cash flows.

We acquire a majority of our products for resale from a limited number of vendors. The loss of any one of these vendors could have a material adverse effect on our business.

We acquire products for resale both directly from manufacturers and increasingly indirectly through distributors and other sources. The five vendors supplying the greatest amount of goods to us constituted 59% of our total product purchases in the year ended December 31, 2018 and 61% and 59% in 2017 and 2016, respectively. Among these five suppliers, product purchases from Ingram, our largest supplier, accounted for approximately 22% of our total product purchases in both 2018 and 2017 and 21% in 2016. Purchases from Synnex comprised 12%, 12%, and 13% of our total product purchases in 2018, 2017, and 2016, respectively. Purchases from Tech Data comprised of 10% of our total product purchases in 2018 and 11% and 8% in 2017 and 2016, respectively. Purchases from HP accounted for approximately 7% of our total product purchases in 2018 and 11% and 9% in 2017 and 2016, respectively. No other vendor supplied more than 10% of our total product purchases in 2018, 2017, or 2016. If we were unable to acquire products from Ingram, Synnex, HP or Tech Data, we could experience a short-term disruption in the availability of products, and such disruption could have a material adverse effect on our results of operations and cash flows.

Products manufactured by HP represented approximately 18% of our net sales in 2018 and approximately 20% in both 2017 and 2016. We believe that in the event we experience either a short-term or permanent disruption of supply of HP products, such disruption would likely have a material adverse effect on our results of operations and cash flows.

Substantially all of our contracts and arrangements with our vendors that supply significant quantities of products are terminable by such vendors or us without notice or upon short notice. Most of our product vendors provide us with trade credit, of which the net amount outstanding at December 31, 2018 was $201.6 million. Termination, interruption,

or contraction of relationships with our vendors, including a reduction in the level of trade credit provided to us, could have a material adverse effect on our financial position.

Some product manufacturers either do not permit us to sell the full line of their products or limit the number of product units available to national solutions providers such as us. An element of our business strategy is to continue increasing our participation in first-to-market purchase opportunities. The availability of certain desired products, especially in the direct marketing channel, has been constrained in the past. We could experience a material adverse effect to our business if we are unable to source first-to-market purchases or similar opportunities, or if significant availability constraints reoccur.

We are exposed to inventory obsolescence due to the rapid technological changes occurring in the IT industry.

The market for IT products is characterized by rapid technological change and the frequent introduction of new products and product enhancements. Our success depends in large part on our ability to identify and market products that meet the needs of customers in that marketplace. In order to satisfy customer demand and to obtain favorable purchasing discounts, we have and may continue to carry increased inventory levels of certain products. By so doing, we are subject to the increased risk of inventory obsolescence. Also, in order to implement our business strategy, we intend to continue, among other things, placing larger than typical inventory stocking orders of selected products and increasing our participation in first-to-market purchase opportunities. We may also, from time to time, make large inventory purchases of certain end‑of‑life products, which would increase the risk of inventory obsolescence. In addition, we sometimes acquire special purchase products without return privileges. For these and other reasons, we may not be able to avoid losses related to obsolete inventory. Manufacturers have limited return rights and have taken steps to reduce their inventory exposure by supporting “configure‑to-order” programs authorizing distributors and resellers to assemble computer hardware under the manufacturers’ brands. These actions reduce the costs to manufacturers and shift the burden of inventory risk to resellers like us, which could negatively impact our business.

We are dependent on key personnel.

Our future performance will depend to a significant extent upon the efforts and abilities of our senior executives and other key management personnel. The current environment for qualified management personnel in the computer products industry is very competitive, and the loss of service of one or more of these persons could have an adverse effect on our business. Our success and plans for future growth will also depend on our ability to hire, train, and retain skilled personnel in all areas of our business, especially sales representatives and technical support personnel. We may not be able to attract, train, and retain sufficient qualified personnel to achieve our business objectives.

The methods of distributing IT products are changing, and such changes may negatively impact us and our business.

The manner in which IT hardware and software is distributed and sold is changing, and new methods of distribution and sale have emerged, including distribution through cloud-based and SaaS solutions. In addition, hardware and software manufacturers have sold, and may intensify their efforts to sell, their products directly to end users. From time to time, certain manufacturers have instituted programs for the direct sales of large order quantities of hardware and software to certain major corporate accounts. These types of programs may continue to be developed and used by various manufacturers. Some of our vendors, including Apple, Dell, HP, and Lenovo, currently sell some of their products directly to end users and have stated their intentions to increase the level of such direct sales. In addition, manufacturers may attempt to increase the volume of software products distributed electronically to end users. An increase in the volume of products sold through or used by consumers of any of these competitive programs, or our inability to effectively adapt our business to increased electronic distribution of products and services to end users could have a material adverse effect on our results of operations.

We depend heavily on third-party shippers to deliver our products to customers.

Many of our customers elect to have their purchases shipped by an interstate common carrier, such as UPS or FedEx Corporation. A strike or other interruption in service by these shippers could adversely affect our ability to market or deliver products to customers on a timely basis.

Natural disasters, terrorism, and other circumstances could materially adversely affect our business.

Natural disasters, terrorism, and other business interruptions have caused and could cause damage or disruption to international commerce and the global economy, and thus could have a negative effect on the Company, its suppliers, logistics providers, manufacturing vendors, and customers. Our business operations are subject to interruption by natural disasters, fire, power shortages, nuclear power plant accidents, terrorist attacks, and other hostile acts, and other events beyond our control. Such events could decrease demand for our products, make it difficult or impossible for us to deliver services or products to our customers, or to receive products from our suppliers, and create delays and inefficiencies in our supply chain. In the event of a natural disaster or other business interruption, significant recovery time and substantial expenditures could be required to resume operations and our financial condition, results of operations, and cash flows could be materially adversely affected.

We may experience increases in shipping and postage costs, which may adversely affect our business if we are not able to pass such increases on to our customers.

Shipping costs are a significant expense in the operation of our business. Increases in postal or shipping rates could significantly impact the cost of shipping customer orders and mailing our catalogs. Postage prices and shipping rates increase periodically, and we have no control over future increases. We have a long-term contract with UPS, and believe that we have negotiated favorable shipping rates with our carriers. While we generally invoice customers for shipping and handling charges, we may not be able to pass on to our customers the full cost, including any future increases in the cost, of commercial delivery services, which would adversely affect our business.

We rely on the continued development of electronic commerce and Internet infrastructure development.

We continue to have increasing levels of sales made through our e-commerce sites. The on-line experience for our clients continues to improve, but the competitive nature of the e-commerce channel also continues to increase. Growth of our overall sales is dependent on customers continuing to expand their on-line purchases in addition to traditional channels to purchase products and services. We cannot accurately predict the rate at which on-line purchases will expand.

Our success in growing our Internet business will depend in large part upon our development of an increasingly sophisticated e-commerce experience and infrastructure. Increasing customer sophistication requires that we provide additional website features and functionality in order to be competitive in the marketplace and maintain market share. We will continue to iterate our website features, but we cannot predict future trends and required functionality or our adoption rate for customer preferences. As the number of on-line users continues to grow, such growth may impact the performance of our existing Internet infrastructure.

We face uncertainties relating to unclaimed property and the collection of state sales and use tax.

We collect and remit sales and use taxes in states in which we have either voluntarily registered or have a physical presence. Various states have sought to impose on direct marketers the burden of collecting state sales and use taxes on the sales of products shipped to their residents. Many states have adopted rules that require companies and their affiliates to register in those states as a condition of doing business with those state agencies. Our three sales companies are registered in substantially all states, however, if a state were to determine that our earlier contacts with that state exceeded the constitutionally permitted contacts, the state could assess a tax liability relating to our prior year sales. Various states have from time-to-time initiated unclaimed property audits of our company escheatment practices. A multi-state unclaimed property audit continues to be in process, and total accruals for unclaimed property aggregated $1.0 million at December 31, 2018.

Privacy concerns with respect to list development and maintenance may materially adversely affect our business.

We mail catalogs and other promotional materials to names in our customer database and to potential customers whose names we obtain from rented or exchanged mailing lists. Public concern regarding the protection of personal information has subjected the rental and use of customer mailing lists and other customer information to increased scrutiny. Legislation enacted limiting or prohibiting the use of rented or exchanged mailing lists could negatively affect our business.

We are controlled by two principal stockholders.

Patricia Gallup and David Hall, our two principal stockholders, beneficially own or control, in the aggregate, approximately 56% of the outstanding shares of our common stock as of December 31, 2018. Because of their beneficial stock ownership, these stockholders can continue to elect the members of the Board of Directors and decide all matters requiring stockholder approval at a meeting or by a written consent in lieu of a meeting. Similarly, such stockholders can control decisions to adopt, amend, or repeal our charter and our bylaws, or take other actions requiring the vote or consent of our stockholders and prevent a takeover of us by one or more third parties, or sell or otherwise transfer their stock to a third party, which could deprive our stockholders of a control premium that might otherwise be realized by them in connection with an acquisition of our Company. Such control may result in decisions that are not in the best interest of our public stockholders. In connection with our initial public offering, the principal stockholders placed substantially all shares of common stock beneficially owned by them into a voting trust, pursuant to which they are required to agree as to the manner of voting such shares in order for the shares to be voted. Such provisions could discourage bids for our common stock at a premium as well as have a negative impact on the market price of our common stock.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

We lease our corporate headquarters located at 730 Milford Road, Merrimack, New Hampshire 03054-4631, from an affiliated company, G&H Post, which is related to us through common ownership. The lease term ended in November 2018, and the Company is currently in the process of negotiating an amendment to extend the lease term. We expect that an extension to the lease will be available at market terms. In addition to the rent payable under the facility lease, we are required to pay real estate taxes, insurance, and common area maintenance charges. The lease has been recorded as an operating lease in the financial statements.

We also lease an office facility adjacent to our corporate headquarters from the same affiliated company, G&H Post. The lease term ended in July 2018, but the Company is currently in the process of negotiating an amendment to extend the lease term. We expect that an extension to the lease will be available at market terms. The lease requires us to pay our proportionate share of real estate taxes and common area maintenance charges as either additional rent or directly to third parties and also to pay insurance premiums for the leased property. The lease has been recorded as an operating lease in the financial statements.

In August 2014, we entered into a ten-year lease for a facility in Wilmington, Ohio, which houses our distribution and order fulfillment operations. We also operate sales and support offices throughout the United States and lease facilities at these locations. Leasehold improvements associated with these properties are amortized over the terms of the leases or their useful lives, whichever is shorter. We believe that our physical properties will be sufficient to support our anticipated needs through the next twelve months and beyond.

Item 3. Legal Proceedings

We are subject to audits by states on sales and income taxes, unclaimed property, employment matters, and other assessments. While management believes that known and estimated liabilities have been adequately provided for, it is too early to determine the ultimate outcome of such audits, as formal assessments have not been finalized. Additional liabilities for this and other audits could be assessed, and such outcomes could have a material, negative impact on our financial position, results of operations, and cash flows.

We are subject to various legal proceedings and claims, including patent infringement claims, which have arisen during the ordinary course of business. In the opinion of management, the outcome of such matters is not expected to have a material effect on our business, financial position, results of operations, or cash flows.

In December 2018, we executed a favorable $3.0 million cash resolution of a contract dispute that arose in 2017. The cash payment was received on January 4, 2019, and the gain, net of costs incurred of $0.7 million, is included in “Other Income” in the consolidated statements of income for the year ended December 31, 2018. The cash received is unrelated to the existing contract. We included the $3.0 million owed to us in “Other Assets” as of December 31, 2018.

Item 4. Mine Safety Disclosures

Not applicable.

Executive Officers of PC Connection

Our executive officers and their ages as of February 7, 2019 are as follows:

| | | | |

Name | | Age | | Position |

Patricia Gallup | | 64 | | Chair and Chief Administrative Officer |

Timothy McGrath | | 60 | | President and Chief Executive Officer |

Stephen Sarno | | 51 | | Senior Vice President, Chief Financial Officer and Treasurer |

Patricia Gallup is our co-founder and has served as Chair of our Board of Directors since September 1994, and as Chief Administrative Officer since August 2011. Ms. Gallup has served as a member of our executive management team since 1982.

Timothy McGrath has served as our Chief Executive Officer since August 2011, and as President since May 2010. Mr. McGrath has served as a member of our executive management team since he joined the Company in 2005.

Stephen Sarno has served as our Chief Financial Officer and as a member of our executive management team since he joined the Company in the spring of 2018. Prior to joining Connection, Mr. Sarno served as Chief Financial Officer of Wyless, Inc., a privately held international provider of wireless data communication services, beginning in January 2015, and as Chief Accounting Officer of Exa Corporation, a publicly-traded global developer and distributor of computer-aided engineering software, beginning in October 2012.

PART II

Item 5. Market for the Registrant’s Common Equity, Related Stockholder Matters, and Issuer Purchases of Equity Securities

Market Information

Our common stock commenced trading on March 3, 1998, on the Nasdaq Global Select Market and trades today under the symbol “CNXN”. As of February 4, 2019, there were 26,395,683 shares of our common stock outstanding, held by approximately 47 stockholders of record. This figure does not include an estimate of the number of beneficial holders whose shares are held of record by brokerage firms.

In 2018, we declared a special cash dividend of $0.32 per share. The total cash payment of $8.5 million was made on January 11, 2019 to stockholders of record at the close of business on December 28, 2018. In 2017, we declared a special cash dividend of $0.34 per share. The total cash payment of $9.1 million was made on January 12, 2018 to stockholders of record at the close of business on December 29, 2017. We have no current plans to pay additional cash dividends on our common stock in the foreseeable future, and declaration of any future cash dividends will depend upon our financial position, strategic plans, and general business conditions.

Share Repurchase Authorization

In 2001, our Board of Directors authorized the spending of up to $15.0 million to repurchase shares of our common stock. In 2014, our Board approved a new share repurchase program authorizing up to an additional $15.0 million in share repurchases, for a total authorized repurchase amount of $30.0 million. We consider block repurchases directly from larger stockholders, as well as open market purchases, in carrying out our ongoing stock repurchase program.

In 2018, we repurchased 0.5 million shares for $15.4 million under the Board-approved repurchase programs. As of December 31, 2018, we have repurchased an aggregate of 2.2 million shares for $27.6 million under our Board-approved repurchase programs.

On December 17, 2018, our Board approved a new share repurchase program authorizing up to $25.0 million in additional share repurchases. There is no fixed termination date for this repurchase program. Purchases may be made in open-market transactions, block transactions on or off an exchange, or in privately negotiated transactions. We intend to complete the remaining 2001 and 2014 repurchase programs before repurchasing shares under the new program. The timing and amount of any share repurchases will be based on market conditions and other factors. At December 31, 2018, the maximum approximate dollar value of shares that may yet be purchased under Board-authorized programs is $27.4 million.

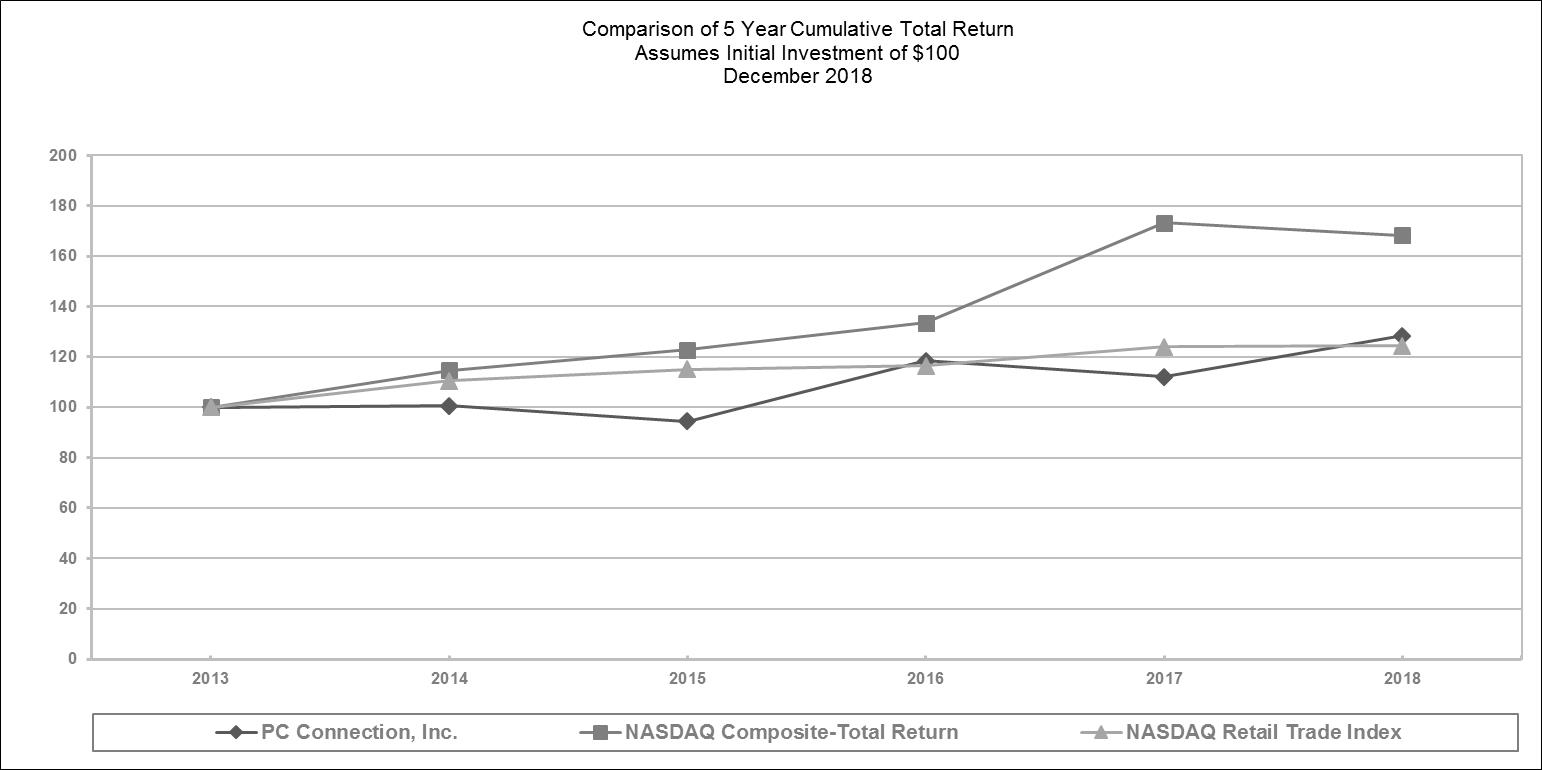

Stock Performance Graph

The following performance graph and related information shall not be deemed “soliciting material” or to be “filed” with the SEC, nor shall such information be incorporated by reference into any future filing under the Securities Act of 1933 or the Exchange Act, each as amended, except to the extent that we specifically incorporate it by reference into such filing.