UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the year ended December 31, 2005

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 000-25661

TenFold Corporation

(Exact name of registrant as specified in its charter)

| | |

| Delaware | | 83-0302610 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

698 West 10000 South

South Jordan, Utah 84095

(Address of principal executive offices, including zip code)

(801) 495-1010

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, par value $0.001 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. (Check one):

| | | | |

| Large Accelerated Filer ¨ | | Accelerated Filer ¨ | | Non-Accelerated Filer x |

Indicate by check mark whether the registrant is an accelerated filer (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

Market value of shares of Common Stock held by non-affiliates of the registrant, based on the closing price of the Common Stock on June 30, 2005 was approximately $8,002,000. Shares of Common Stock held by each current executive officer and director, and by each person who is known by the registrant to own 10 percent or more of the outstanding Common Stock, have been excluded from this computation in that such persons may be deemed to be affiliates of the Company. Share ownership information of certain persons known by the Company to own greater than 10 percent of the outstanding common stock for purposes of the preceding calculation is based solely on information known by the Company and is as of June 30, 2005. This determination of affiliate status is not a conclusive determination for other purposes.

As of February 28, 2006, there were 46,502,013 shares of the registrant’s Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the Registrant’s 2006 Annual Meeting of Stockholders are incorporated by reference into Part III of this Form 10-K.

TENFOLD CORPORATION

2005 FORM 10-K AND ANNUAL REPORT

TABLE OF CONTENTS

2

FORWARD-LOOKING STATEMENTS

In addition to historical information, this Annual Report on Form 10-K contains forward-looking statements that involve risks and uncertainties that could cause our actual results to differ materially from those contained in the forward-looking statements. Factors that might cause or contribute to such differences include, but are not limited to, those discussed in the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Factors That May Affect Future Results and the Market Price of Stock.” When used in this report, the words “expects,” “intends,” “anticipates,” “should,” “believes,” “will,” “plans,” “estimates,” “may,” “seeks,” “estimates” and similar expressions are generally intended to identify forward-looking statements. You should not place undue reliance on these forward-looking statements, which reflect our opinions only as of the date of this Annual Report. We undertake no obligation to publicly release any revisions to the forward-looking statements after the date of this document. You should carefully review the risk factors described in this Annual Report and in other documents we file from time to time with the Securities and Exchange Commission, including our Quarterly Reports on Form 10-Q.

3

PART I

Item 1. Business

Business Overview

TenFold provides services and technology for building complex, Service Oriented Architecture (“SOA”)-compliant, mission-critical applications in significantly less time and cost than it would otherwise take using traditional development technologies. We believe that with TenFold’s technology, EnterpriseTenFold™ (formerly “Universal Application”), customers will also experience significantly reduced ongoing applications maintenance and enhancement costs compared to what they generally experience with legacy applications.

At the end of 2005, we replaced our former Chief Executive Officer, with long-time TenFold director and shareholder, Robert W. Felton. Under his leadership, we have recently changed our business model to focus on selling larger consulting projects, instead of the smaller prototype application projects that we primarily sold in 2005. We believe that providing larger consulting projects (that include the full breadth of applications consulting from applications design through production implementation) will be a more successful model for both us and our customers. We believe that some of our customers would have been more successful with their projects with more consulting assistance than they chose to purchase under our prior business model. Although we hope to be more successful with this new business model, we have limited experience with it as we have introduced it only recently, and have not yet closed any sales under this model. As a result, it is unclear if or when we can expect to close significant sales to new or existing customers, and until we do so we are likely to continue to experience declining revenues and increasing losses.

EnterpriseTenFold automates most of what applications programmers typically do, and empowers small teams of business people and information technology (“IT”) professionals to design, build, test, deploy, and maintain complex, transaction and database-intensive applications, with significantly reduced demand on scarce IT resources as compared to other applications development approaches and technologies. Using a small team of business people supplemented with IT professionals for rapid applications development is a significant change from the industry-standard approach that relies on large teams of IT professionals who expend significant numbers of person years of effort to design, program, test, change, and deploy enterprise applications. We believe that with EnterpriseTenFold, customers get high-quality, complex enterprise applications into production faster and at significantly lower cost than with other applications development technologies.

We believe that in EnterpriseTenFold, TenFold has developed the first, complete service oriented technology. TenFold provides an applications development environment that enables corporations to custom-build and maintain complex, database, transactional, enterprise applications rapidly with high quality and functional richness.

We believe EnterpriseTenFold has two unique attributes that make building complex, database-intensive and transaction-intensive applications substantially cheaper, easier, and faster than traditional applications development methodologies and tools. First, EnterpriseTenFold is a model-driven architecture that renders modeled applications, which means that EnterpriseTenFold already includes most of what applications programmers typically do and automatically provides advanced applications functionality. Because of its model-driven architecture, we believe customers get more powerful, higher quality applications faster and at a fraction of the cost of traditional programming approaches. Second, since TenFold-powered applications development provides a tool and methodology that business people can effectively use, we believe it enables organizations to directly leverage their business experience and insight, and to adapt applications easily to meet changing business requirements. Thus we believe TenFold’s model-driven architecture lets a TenFold-trained team do Extremely Rapid Applications Development. As a result, a TenFold-trained team can build applications so quickly that customers experience both trying the application and improving the application in very short turnaround cycles to help ensure what is built is what the business really needs.

4

We believe EnterpriseTenFold offers three unique benefits:

| | 1. | Speed. EnterpriseTenFold lets a small, trained team of business people and IT professionals build and enhance high-quality, high-performance, powerful applications much faster than other technology because building or enhancing a TenFold-powered application using EnterpriseTenFold requires only describing applications features and functionality. Other applications development technologies also let you build and enhance applications, but most require large teams of programmers, take longer, and are risky for complex applications because those other technologies require detailed, complex, logic programming. The high failure rate of complex applications development projects suggests that other applications development technologies often lead to project cost and schedule overruns, applications quality problems, and sometimes project cancellations. |

| | 2. | Quality. EnterpriseTenFold includes the TenFold RenderingEngine, which renders an application from its description (or model). With EnterpriseTenFold, there is no need to write or test newly-written code in the building of an application. Thus, it is less likely for the application to have defects or quality problems. We believe that a TenFold-powered application works just as you describe it to work; it may not do what you want, but it does do what your description says for it to do. Because the code that every TenFold-powered application executes is the same well-tested code that TenFold provides before a project begins, we believe TenFold-powered applications are much higher quality than most other applications. |

| | 3. | Power. The TenFold RenderingEngine contains thousands of features that make any TenFold-powered application more functionally-rich than the same application that a programmer-staffed applications development team could pragmatically afford to program. TenFold-powered applications have clever, powerful features unavailable in most other applications. |

Our business model focuses on providing applications development services and our EnterpriseTenFold technology, support, and training, to customers who can use a TenFold team or their own business teams to build and maintain applications.

Business History

We founded TenFold in 1993. We spent the first several years primarily developing our patented EnterpriseTenFold technology. In 1996, we began using EnterpriseTenFold to build applications for customers.

In 1999, we completed our initial public offering. In 1999 and early 2000, we tested a new business model that caused us to face significant financial, legal, and operational issues. Starting in late 2000 we took steps to resolve the financial and legal liabilities that arose as a result of the interim business model and to restore the company to sound business health.

We raised capital twice during 2003. In February 2003, Robert W. Felton, a long-time TenFold director (who also recently became our Chairman, President, and Chief Executive Officer), made an investment of $700,000 in TenFold, by acquiring restricted TenFold common stock. In December 2003, we closed a $10 million private placement of restricted TenFold common stock.

During 2003 and 2004, we continued sales and marketing related initiatives including establishing alliance relationships with distributors such as VARs; prototyped a new sales model focusing on selling small, paid proof-of-concept projects; initiated internet access to TenFold technology; introduced TenFold Support SpeedPro, making expert consultants available for short-duration projects; and increased marketing and public relations efforts to broaden awareness of and interest in TenFold technology.

5

During 2004 and 2005, we enhanced EnterpriseTenFold adding substantial new functionality and features:

| | • | | SOA-compliance, including expanded web services standards support, authentication, single-sign-on and security integration, and enhanced integration tools |

| | • | | A new-generation browser user interface based on the XML and Ajax technologies |

| | • | | Multi-language support that includes Japanese and other multi-byte languages, and an auto-translation feature |

| | • | | The new generation of applications development environment – TenFoldTools – that we believe greatly improves developers’ productivity |

| | • | | User interface enhancements that allow developers to add graphical and web content to applications, and that we believe make our user interface more intuitive for untrained end-users |

| | • | | Support for new applications platforms including various types of the open-source Linux operating system, open-source databases MySQL and EnterpriseDB, and support for recent versions of Oracle and other platforms |

| | • | | Improvements in applications server stability, performance, and scalability |

During 2005, we continued to focus substantial effort on our marketing and public relations efforts to increase awareness of TenFold, TenFold technology, and to generate leads. We used a multi-faceted, integrated approach to marketing that included e-mail, direct mail, and telemarketing to support our TenFold Seminars as our principal approach to introducing people to TenFold and TenFold technology. We conducted numerous TenFold Seminars in various major metropolitan areas during 2005. Our lead generation increased substantially.

During 2005, we earned revenues from 45 customers. We continued to focus new-customer sales on selling small, proof-of-concept projects as part of our penetrate and radiate sales program. Once we completed an initial project, we attempted to radiate into the account by selling additional services and licenses. The financial impact of the new-account, or “penetrate”, transactions was immaterial to our overall financial performance. Some of these accounts radiated from proof-of-concept projects to purchase larger production licenses and additional services. However, they were not sufficiently large for us to achieve profitability or positive cash flow.

Some of our customers accounted for more than 10 percent of our annual revenues in 2005. XanGo accounted for 20 percent, JPMorgan Chase accounted for 18 percent, and DevonWay (a related party,see Management’s Discussion and Analysis of Financial Condition and Results of Operations – Related Party Transactions for more information) accounted for 11 percent of our revenues for the year ended December 31, 2005. XanGo completed its use of our consulting services for its application development project during the quarter ended December 31, 2005. XanGo has currently decided not to implement its TenFold-powered application into production. JPMorgan Chase substantially completed its application development project during the quarter ended March 31, 2005, and has its TenFold-powered application in production use. It continues to purchase support from us, and other services from time to time. DevonWay completed its application development project with us during the quarter ended December 31, 2005, is in the process of further enhancing and preparing its TenFold-powered application for production use, and continues to purchase support from us, and other services from time to time. In future periods, however, we do not expect the amount of revenue from these customers to be significant as they have completed their current projects with us. We have not sold new projects to replace these projects, and are not currently working on any significant consulting projects. SeeManagement’s Discussion and Analysis of Financial Condition and Results of Operations – 2005 as Compared to 2004 - Revenues for more information.

Cedars-Sinai Medical Center accounted for 50 percent, JPMorgan Chase accounted for 22 percent, and Sapient accounted for 15 percent of our revenues for the year ended December 31, 2004. Allstate accounted for 41 percent, JPMorgan Chase accounted for 25 percent, and Sapient accounted for 23 percent of our revenues for the year ended December 31, 2003.

6

Revenues from customers outside of North America were approximately 11 percent of total revenues for 2005, 20 percent of total revenues for 2004, and 29 percent of total revenues for 2003. Revenues from customers in the United Kingdom were 9 percent of total revenues for 2005, 19 percent of total revenues for 2004, and 29 percent of total revenues for 2003. Revenues from operations in Argentina were 2 percent of total revenues for 2005, 0.9 percent of total revenues for 2004, and 0.5 percent of total revenues for 2003. Our long-lived assets are deployed in the United States.

Customers with TenFold-powered applications in production today include, among others, Abbey National Bank, Allstate Insurance, Barclays Global Investors, Cedars-Sinai Medical Center, Deutsche Bank, Franklin Templeton, Guidant, Ingenix (a subsidiary of UnitedHealth Group), iplan networks, JPMorgan Chase, MedCath, Rand Technology, RCM Capital Management LLC, Trinity Health, and Vertex (a subsidiary of United Utilities).

Industry Challenge

Organizations worldwide face increasing pressure to replace their legacy enterprise applications and introduce new applications as they seek to increase productivity, cut costs, introduce new products and services, address changing regulatory and competitive demands, and access new technology. But, organizations face daunting odds of failure because traditional processes for building, integrating, and deploying complex applications are costly and risky. Consequently, many organizations continue to make substantial investments to maintain legacy applications that inadequately meet current needs and do not address new business requirements. To obtain new or replacement applications, companies choose between buying a packaged software application or building a custom software application.

Organizations generally turn to independent software vendors, such as Enterprise Resource Planning (“ERP”) vendors or vertical software vendors, when seeking packaged applications. In general, packaged applications promise predictable quality and relatively quick implementation. However, packaged applications frequently require that an organization adapt its business practices to the software. ERP systems generally fail to address specific industry problems, such as patient management or securities lending; often cost considerably more than planned to implement; and, once installed, are difficult to modify to adapt to changing business needs. In addition, when an organization chooses the costly and time-consuming path of customizing a packaged application, cost and risk rise rapidly and the organization is generally inhibited from future opportunities to upgrade the packaged application when subsequent new releases are available.

Alternatively, organizations can build custom applications, either internally or with third parties. This approach promises organizations the functionality, flexibility, and fit they seek, but custom applications development carries a high risk of failure, with projects often exceeding budgets and schedules, and with many projects being cancelled prior to implementation due to time delays, budget overruns, and functional or technical deficiencies. Companies often hire software integration or services firms to build and implement mission-critical applications. These firms generally engage a large number of consultants who may remain on the project for years, and may exceed budgets and schedules without producing significantly better results than internal development organizations. In addition, these firms typically do not offer ongoing product enhancements because they build custom solutions for a single customer.

Applications development projects fail because the process of designing, programming, and testing complex applications with conventional tools and approaches is very complex and labor intensive. Designing, programming, testing, integrating, and deploying complex applications can be difficult, take a long time, be expensive, and tie up scarce IT resources. This high cost and high risk is in stark contrast to the business need for new applications that address current business practices and can be adapted quickly and easily to meet the evolving business requirements of a dynamic, highly competitive business environment.

7

TenFold Technology and Products

We believe TenFold’s patented EnterpriseTenFold presents a significantly new approach to applications development. We believe that this approach reduces applications development and maintenance cost and time in two ways: first, by automating tedious, time-consuming, error-prone tasks that programmers would generally do; and, second, by providing an applications development tool and methodology that lets business people actively participate in applications development. We believe that EnterpriseTenFold enables organizations to directly leverage their business experience and insight and to adapt applications easily to meet changing business requirements.

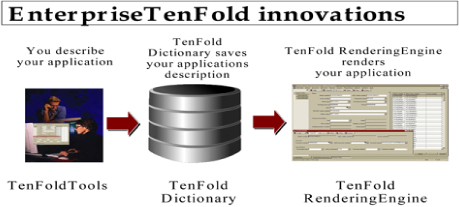

EnterpriseTenFold has three key innovations that make designing, building, testing, deploying, and maintaining an application completely different from traditional programming-oriented technologies:

| | |

Innovation | | Description |

| TenFold Tools | | • Can be used by non-technical business people with relatively little training and some help from an experienced TenFoldTools consultant. • Provides a sophisticated applications developer environment that is convenient for describing applications requirements. • Is itself a set of easy-to-use applications with security, concurrency control, audit trails, et cetera. • Is a set of TenFold-powered applications, so an applications developer has the same intuitive user interface, benefits from the same Quality and Power as other applications end-users. |

| |

TenFold Dictionary | | • Saves the applications description in an RDBMS to make changing the description easy and fast. • Secures and manages the applications description just as an RDBMS does for any applications database data such as invoices or insurance policies. |

| |

| TenFold Rendering-Engine | | • Reads the applications description and renders the application. • Supports using and changing an application as you describe it. • Scales to support tens of thousands of simultaneous end-users. |

These EnterpriseTenFold innovations work together to automate tedious, repetitive, and error-prone tasks like writing SQL, Java, C++, or VisualBasic code. We believe that automating tedious programming tasks lets applications developers focus their intellect and energy on solving the business problem instead of fighting technology problems.

8

We believe this revolutionary EnterpriseTenFold approach has important implications:

| | |

Implication | | Description |

| Requirements are easier, faster, and more rewarding | | • Accelerates the difficult, time-consuming, resource intensive, traditional first step in applications development, Requirements. • Lets applications developers describe and unambiguously record requirements with TenFoldTools. • Lets applications developers see a running application as they describe requirements. • Lets applications developers build and modify their application quickly, so they can evolve requirements in concert with developing and trying their application. |

| |

| Power features make applications functionally richer | | • Built-in TenFold RenderingEngine features make applications automatically powerful with a slick Windows user-interface, a slick browser interface that includes Ajax behavior, powerful database features like TimeRelation, AuditTrail, and more. |

| |

| The meaning and purpose of Testing changes to everyone’s benefit | | • TenFold RenderingEngine renders a working application, so testing becomes ‘an exercise to verify the business solution,’ instead of ‘figure out where it blows up and fix it.’ • With portions of the application running almost at the very start of the project, users can demonstrate it to business people and get feedback throughout the project, not just at the end when the project should be complete. • Automated regression testing tools let users capture what they want to automatically test and help them ensure that ongoing applications changes do not impact things that work as they wish. |

| |

| Change is fast, responsive, and significantly lower cost | | • Since changing an application involves only changing its description, change is much faster and less costly than alternative reprogramming strategies that are prevalent with traditional technologies and inherent in legacy systems. • Automated regression testing tools make it possible to fully test a new applications version quickly and verify that new features work and that existing features still work as before. • Built-in change management tools automate most of the work in promoting new applications versions into production. |

The EnterpriseTenFold value proposition provides three major benefits – Speed, Quality, and Power – to its customers.Speed. EnterpriseTenFold makes building complex applications faster than other technologies so projects can be finished in months, not years.Quality. EnterpriseTenFold addresses eleven key attributes of quality applications. Since TenFold RenderingEngine renders an application from its description, tedious, error-prone, programming-like tasks are avoided in building or enhancing a TenFold-powered application. Thus, we believe the quality of the application is excellent.Power. EnterpriseTenFold renders an application from its description and automatically includes considerable, rich built-in functionality in the application. Interestingly, complex feature requirements, which traditionally generate complexity and a high likelihood of project failure, add little incremental cost to TenFold applications development, just as a spreadsheet requiring more-complex formulas is not significantly more costly to build than one with only simple formulas.

EnterpriseTenFold has been in development for more than 13 years, contains more than 3.3 million lines of C and C++ code, and is covered by three issued United States patents. We believe that with EnterpriseTenFold, business people or applications developers with little or no traditional programming skills can collaborate with IT professionals to build and maintain an application by describing the application without needing to program in C, C++, Java, HTML, Structured Query Language (“SQL”) or other programming languages and without the need to do other programming-like tasks such as designing screens and writing technical designs.

9

We believe EnterpriseTenFold delivers these benefits:

| | • | | Faster development of complex applications because EnterpriseTenFold automates tasks that programmers would otherwise have to do such as coding SQL, coding logic functions, managing computer-to-computer communications, and coding user interface screens; |

| | • | | Longer-lived applications that can survive changes in underlying technologies without requiring applications rewrites, because EnterpriseTenFold insulates applications from many technical changes such as new operating system and database software releases; |

| | • | | Relatively easy development of web services as a customer can expose any part of a TenFold-powered application as an industry-standard web service; |

| | • | | Reduced maintenance costs because there is little or no code to maintain; |

| | • | | Improved quality because EnterpriseTenFold replaces individually-coded logic with already-existing, thoroughly-tested algorithms that provide both basic and sophisticated applications behavior such as security, menus, transaction behavior, and powerful windows and browser user interface features; |

| | • | | Greater consistency to look, feel and operation across the entire application, by replacing individually-built screen designs and transactions with a systematic, optimal, standard design and by eliminating the details of screen layout and repetitive transaction behavior from the application developer’s task list; |

| | • | | Demonstrated scalability as customers add simultaneous end-users and computing capacity; and |

| | • | | Typically sub-second response-time on properly configured hardware for most applications actions, because EnterpriseTenFold is carefully optimized to provide good performance. |

In addition to the above benefits, EnterpriseTenFold has many distinguishing advanced features. The following is a partial listing of these features:

| | • | | Portability across popular databases such as Oracle, DB2, SQL Server, Sybase, EnterpriseDB, and MySQL; |

| | • | | Generation of all SQL statements for accessing and updating data, each highly optimized for each relational database; |

| | • | | Automatic screen layout to ensure consistency and quality in both web and desktop environments; |

| | • | | Automatic creation of both a Windows and web browser user interface; |

| | • | | Built-in support for query and update of time-varying data such as effective-dated employee or insurance policy records; |

| | • | | Real-time, server-supplied screen refresh of detail and summary information as underlying data changes; |

| | • | | Simplified business rule definition and optimized rule execution for workflow, posting, access control, and other sophisticated rule types; |

| | • | | Formal rule abstractions for validation, propagation, population, without requiring application developers to master complex event models; |

| | • | | Shared middle-tier caching, deferred query execution, and optimistic concurrency control to minimize database server load; |

| | • | | Codeless integration with third-party applications via real-time messages, APIs, or files based on a simple interface description including support for many different messaging layers such as Tibco, TCP/IP, MQSeries, and Pipes; and |

| | • | | Application-level data synchronization between central servers and intermittently connected laptops. |

10

EnterpriseTenFold is composed of components for developing, executing, integrating, and configuring applications.

Developing an Application. TenFoldTools provides a sophisticated user interface that lets applications developers describe an application without traditional programming activities. Business people or other applications developers describe the database that the application uses and manages, transactions that business end-users use to do each end-user activity, and rules that control transaction behavior. TenFoldTools is itself a TenFold-powered application, that applications developers use to describe their application. TenFold AutoTest, a portion of TenFoldTools, uses patented techniques to simplify and automate functional and regression testing. TenFold Reporter and TenFoldAnalyzer, each a portion of TenFoldTools, let business people define their own reports and real-time data analysis. TenFoldTools store the description of their applications objects in a relational database called TenFold Dictionary.

Executing an Application. TenFold RenderingEngine is an executable program, generally deployed in various configurations on multiple client and server computers, that reads an applications description from TenFold Dictionary and runs as that application. TenFold RenderingEngine has these four major components:

| | |

Component | | Description |

TenFold Client | | The TenFoldClient part of the TenFold RenderingEngine typically runs on a client computer and interacts with you as you use a TenFold-powered application. TenFoldClient is a feature-rich, secure, portable, and graphical, transaction-execution environment that implements transaction requirements that applications developers describe in the TenFold Dictionary. TenFoldClient includes TenFold Browser UI Library, TenFold Windows UI Library, TenFold TransactionManager, TenFold FrameComposer, TenFold FrameManager, TenFold GraphicInterface Library, TenFold TransactionEngine, and TenFold GraphicInterface standard. |

| |

TenFold Server | | The TenFoldServer part of the TenFold Rendering Engine typically runs on a server computer and provides non-visible applications services. TenFoldServer provides an open-to-industry-standards messaging layer, applications server technologies, and standard business engines, and distributes data-intensive and computing-intensive processing across multiple server computers and multiple distributed databases. TenFoldServer includes TenFold Security Library, TenFold Server Manager, TenFold FastConnect, TenFold Messages Library, TenFold Scheduler, TenFold Network Library, TenFold BusinessEngines, and TenFold Messages standard. |

| |

| LogicXpress | | The LogicXpress part of the TenFold RenderingEngine includes TenFold Language for describing complex applications logic, reports, and processes, and technologies to compile, distribute, and efficiently run that logic portably across the various client and server computers on which you deploy an application. LogicXpress includes TenFold Compiler, TenFold Interpreter, TenFold MetaFile Library, TenFold Language, and TenFold MetaFile standards. |

| |

TenFold Kernel | | The TenFoldKernel part of the TenFold RenderingEngine provides rich, portable, data-related functionality and powerful, standard, basic-applications functions to other TenFold RenderingEngine components. TenFoldKernel provides a dictionary-driven, read-write set interface to supported relational databases, and provides optimal performance, guaranteed portability, low development cost, low maintenance cost, and rich functionality to both applications and EnterpriseTenFold. TenFoldKernel includes TenFold Database Library, TenFold OptionsFile Library, TenFold Validation Library, TenFold Knobs&Dials Library, TenFold Error Library, TenFold CommonRoutines Library, and TenFold OperatingSystem Library. |

11

Integrating an Application. TenFoldTools contains integration tools, called TenFoldConnect, that connect a TenFold-powered application to other applications, both within a company and at its customers and suppliers. Whether exchanging files, directly accessing another database, or using real-time messaging, applications developers codelessly describe the path that data follows to interface with typically-inflexible legacy or third party applications. Applications developers can convert and cleanse data during its passage to or from a TenFold-powered application.

Configuring an Application. EnterpriseTenFold supports leading relational databases, server operating systems, client operating systems, web servers and browsers, and communications systems. EnterpriseTenFold is highly configurable so that it can distribute components of the TenFold RenderingEngine across many computers to provide n-tier processing or run on a single computer. Configuration options let customers tune performance and scalability by configuring EnterpriseTenFold to match the underlying hardware and software environment. The EnterpriseTenFold architectural design simplifies adding support for additional technologies to respond to customer needs and emerging new technology market changes.

TenFold ComponentWare

TenFold ComponentWare is a family of pre-written applications components that easily plug into EnterpriseTenFold to extend its functionality without programming. For example, PowerBilling provides a robust suite of billing transactions, engines, and features. PowerAccounting makes it easy to include accounting-system integration to application descriptions.

TenFold Services

We offer consulting services that provide end-to-end custom applications development solutions and systems integration; basic and advanced applications development training; EnterpriseTenFold maintenance training; and customer support.

Training

TenFold University offers training so that customers can learn how to successfully build, implement, operate, maintain, and enhance their applications. Available training services include classroom instruction (with detailed courseware) offered at TenFold locations on a published schedule or at customer locations scheduled on demand, and on-site, on-the-job training working alongside TenFold expert consultants.

Consulting Services

Our consulting services offer expertise in using EnterpriseTenFold to provide end-to-end custom applications development solutions and systems integration. Our consultants help customers design, develop, test, integrate, deploy, operate and maintain their applications.

12

Implementation services include converting and cleansing legacy data, systems integration, running parallel application testing, and managing the implementation project. We use TenFold technology to leverage open standards, such as web services to build, connect, and streamline business processes.

Our consulting services provide technology transfer, which helps customer staff become self-sufficient with TenFold technology and tools.

Customer Support and SpeedPro Consulting

We provide customers who buy support services with new releases of EnterpriseTenFold as new releases become available, telephone technical support for EnterpriseTenFold, and, optionally, telephone applications support for their TenFold-powered application. We make SpeedPro consulting available to customers who maintain a support relationship with TenFold. SpeedPro offers customers a way to obtain the services of a TenFold expert at a moment’s notice for immediate help or for short projects.

Competition

The competitive landscape for new and legacy-replacement enterprise applications is split among the options available to corporations today. These options are:

| | • | | Buy a packaged application (with or without modification); and |

| | • | | Build a new application using internal IT resources or third-party consulting and software integration firms. |

Status quo

TenFold’s largest competitor is “status quo.” Corporations continually wrestle with the issue of when to take on the challenge of building strategic new applications or attempting to retire and replace “legacy” applications. In recent years, most companies chose to invest large amounts of money to maintain legacy applications rather than replace them. Remaining with the status quo results in: continuously increasing costs as maintenance on top of maintenance gets harder; acceptance of barely adequate applications; limitations on lowering costs; limitations to embracing new technologies; and, difficulty in adding products or expanding markets. Status quo postpones the inevitable replacement of the application.

Buy a Packaged Application (with or without modification)

Many corporations prefer to obtain an off-the-shelf application from ERP or vertical packaged software vendors. Corporations license software packages to limit the risks associated with new software development projects. However, packaged applications force corporations to conform their business problems to the packaged solution, often with a poor fit. Corporations can modify a packaged application to solve their business problems, but such blended solutions are expensive, slow to implement, and suffer from poor integration.

We believe buying packaged applications is not a viable solution for replacing many legacy applications for most customers in most industries, as reasonable-fit packaged applications do not exist.

Build New Applications

When companies contemplate building their own applications on their own or with help, TenFold competes primarily with suppliers of traditional programming technologies and development tools. Internal IT organizations and third party consulting firms frequently use tools from Oracle, IBM, Microsoft, BEA, Computer Associates, and others.

Programming languages such as COBOL, C, and C++ perform well and scale well, but require extraordinarily large project teams to spend multiple years to complete projects. Such projects generally run

13

over budget in time and dollars and frequently fail. Visual Basic, SmallTalk, and other personal computer technologies support rapid applications development and improved productivity for smaller projects, but do not scale to support large numbers of end-users.

Today’s typical technologies include Java, J2EE, .NET, and other component-enabling technologies intending to make Java and Java-like languages viable for complex applications. Such technologies, all of which rely on programmers, have not significantly reduced the time and cost of large applications development at this time. Using such technologies for very large, complex applications development projects is likely to result in continued high failure rates for applications build projects since longer projects and large numbers of programmers on a project increase risk of failure exponentially according to most industry pundits.

Patents, Intellectual Property Rights and Licensing

We rely primarily on a combination of patent, copyright, trade secret and trademark laws, and nondisclosure and other contractual restrictions on copying and distribution to protect our proprietary technology. We have received three separate patents in the United States. The first patent (US Patent # 6016394) relates to EnterpriseTenFold. The second (US Patent # 6016643) relates to TenFold AutoTest, our automated testing technology. The third patent (US Patent # 6301701) relates to our computer-assisted testing of software application components. We have these patents issued and pending in other countries. Our trademark portfolio contains a variety of U.S. and international trademark registrations and pending trademark applications.

In addition, as part of our confidentiality procedures, we enter into nondisclosure agreements with our employees, customers, consultants, and corporate partners, and limit access to and distribution of our software, documentation, and other proprietary information. We retain ownership of EnterpriseTenFold. Under our prior business model we generally retained ownership of the applications products that we developed for customers; however, we allowed a small number of customers to own rights to the applications we developed for them. In some cases, our contracts obligate us to pay royalties on future sales of specific applications, or prohibit us from licensing applications for specified periods of time or to specified third parties.

For information concerning risks associated with intellectual property rights, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Factors that May Affect Future Results and Market Price of Stock.”

Research and Development

Our technology development organization consists of teams of development engineers and product managers. These teams use a “documentation-centric” development process that includes planning and documenting deliverables in advance, adhering to coding standards, and performing nightly regression tests of all technology. We continuously monitor quality, analyze the root-cause of defects, report daily and weekly status, and regularly communicate individual and team performance and adherence to schedule and functionality requirements.

Our development infrastructure and processes produce documentation, quality assurance, platform certification, release management, and delivery capabilities (in addition to design and implementation functions) for our technology and products. Developers use TenFold AutoTest – our patented integrated testing technology – to perform nightly regression tests on all products, components, and technologies under development or modification. Developers use DocuManage, our web-based documentation management and reference system, to access and maintain product documentation.

Our development organization regularly produces new versions and releases of our EnterpriseTenFold technology. Our latest major release of EnterpriseTenFold includes many new features that we believe, make building enterprise applications faster, production deployment more robust, and production management more cost-effective.

14

Research and development expenses were $3.5 million for the year ended December 31, 2005, $3.7 million for the year ended December 31, 2004, and $3.5 million in 2003. As of December 31, 2005, we had 21 staff engaged in research and development activities. We intend to continue to make investments in research and development to maintain and enhance our technology.

Employees

As of December 31, 2005, we had 47 employees, including 9 in consulting, training and support, 21 in research and development, 7 in sales and marketing, and 10 in finance, administrative, and information technology support functions. During the year ended December 31, 2005, our average headcount was 62. None of our employees is represented by a labor union or a collective bargaining agreement and all are at-will employees.

15

Executive Officers

The executive officers of TenFold are as follows:

| | | | |

Name | | Age | | Position(s) |

| Robert Felton | | 67 | | Chairman of the Board of Directors, Chief Executive Officer, and President |

| | |

| Alexei Chadovich | | 46 | | Senior Vice President, Research and Development |

| | |

| Samer Diab | | 37 | | Vice President, Customer Services |

| | |

| Robert Hughes | | 46 | | Chief Financial Officer, Chief of Staff |

| | |

| Robert Trounce | | 35 | | Vice President, Consulting |

| | |

| Jeffrey Walker | | 63 | | Executive Vice President, Chief Technology Officer |

| | |

| Sally White | | 45 | | Vice President, Business Development |

Robert Feltonjoined TenFold as an executive officer in November 2005, and has served as Chairman of the Board of Directors, Chief Executive Officer, and President since that time. Mr. Felton has also served as a member of TenFold’s Board of Directors since March 1997. Mr. Felton is the founder and Chairman of DevonWay, a software applications company, which he founded in May 2005, and a customer of TenFold. Mr. Felton was the founder and served as a member of the Board of Directors of Indus International, Inc., a software applications company, since its inception in 1988 until 2002, at which point he retired. From 1988 to January 1999, Mr. Felton also served as Indus’s Chairman, President, and Chief Executive Officer. Mr. Felton holds a BS in mechanical engineering from Cornell University and an MS in nuclear engineering from the University of Washington.

Alexei Chadovich joined TenFold in October 1997, and has served as Senior Vice President of Research & Development since February 2002. Prior to that, Mr. Chadovich held various technical and development management roles at TenFold including Director, Development, Vice President of Universal Application Client, Director of Universal Application Core, Senior Developer, and Architect for Universal Application Client. Prior to joining TenFold, Mr. Chadovich served from 1996 to 1997 as software architect and developer with Corel Corporation, a business and graphics software development company. From 1990 to 1996, Mr. Chadovich served in various software development and architect positions with WordPerfect Corp., a business software development company, and after its merger with Novell Inc. in 1994, a business and networking software development company. Prior to joining WordPerfect, Mr. Chadovich held various software development management positions with Kurchatov Atomic Energy Institute in Russia, a physics research institute. Mr. Chadovich holds MS in Computer Science from Moscow Institute of Electronic Technology, Russia.

Samer Diab joined TenFold in June 1994 and has served as Vice President, Customer Services since April 2004. From September 2002 to April 2004, Mr. Diab served as TenFold’s Operations Chief of Staff, and from October 1999 to September 2002, he served as a Vice President of Applications Development for TenFold and a prior wholly owned subsidiary. From June 1994 to October 1999, Mr. Diab served in various technical and management roles in TenFold’s development and consulting organizations. Prior to joining TenFold, Mr. Diab served from 1989 to 1994 in various technical, architectural, and managerial roles in the Applications Division of Oracle Corporation, a large database and applications software company. Mr. Diab holds a BS in Electrical Engineering from the California Institute of Technology.

Robert Hughesjoined TenFold in February 1995, and has served as Chief Financial Officer since January 2006 and as Chief of Staff since November 2005. Mr. Hughes has also served as Senior Vice President Finance since December 2000 and Chief Accounting Officer since May 2003. From September 2000 until December 2000, Mr. Hughes served as Chief Financial Officer of a TenFold subsidiary. From February 1995 until August 2000, Mr. Hughes served as TenFold’s Chief Financial Officer. Prior to joining TenFold, Mr. Hughes served in various finance and administrative capacities at Oracle Corporation, a large database and applications software company, from 1989 to 1995. Prior to joining Oracle, from 1982 to 1989, Mr. Hughes served in various audit positions for KPMG LLP, a public accounting firm. Mr. Hughes holds a BA in business administration from the Haas School of Business, University of California, Berkeley, and is a Certified Public Accountant.

16

Robert Trouncejoined TenFold in February 1998 and has served as Vice President, Consulting since October 2005. From May 2005 to October 2005, Mr. Trounce served as Client Services Executive. From February 1998 to May 2005, Mr. Trounce served in various technical, account management and project management roles in TenFold’s applications development and consulting organizations. Prior to joining TenFold, Mr. Trounce served as an Associate Systems Engineer at Electronic Data Systems, an information technology and business process outsourcing services company. Mr. Trounce holds a BS in Business Management with an emphasis in Management Information Systems from the Marriott School of Management, Brigham Young University.

Jeffrey Walkerfounded TenFold in February 1993 and has served as Executive Vice President, and Chief Technology Officer since October 1996. He served as its Chairman from TenFold’s inception to November 2005. From TenFold’s inception to October 1996, Mr. Walker served as TenFold’s President, Chief Executive Officer, and Chief Technology Officer. Prior to founding TenFold, from 1991 to 1993, Mr. Walker was an independent consultant. From 1985 to 1991, Mr. Walker held several management positions at Oracle Corporation, a large database and applications software company, including Executive Vice President from 1987 to 1991, General Manager Applications Division from 1985 to 1991, Chief Financial Officer from 1987 to 1991, and Senior Vice President of Marketing during 1986. Prior to joining Oracle, Mr. Walker founded and served as Chief Executive Officer of Walker Interactive Products, an application software company, from 1980 to 1985. Mr. Walker holds a BA in mathematics from Brown University.

Sally White joined TenFold in May 2000 and has served as Vice President, Business Development since February 2002. From May 2000 to February 2002, Ms. White served as TenFold’s Training Sales Director. Prior to joining TenFold, Ms. White held several management positions with Provant, Inc., a performance improvement training services organization, including Director of Business Development from 1997 to 1999 and Vice President of Sales Strategies from 1999 to 2000. From 1988 to 1997, Ms. White was Vice President of Sales and Marketing for Innovations, a leadership seminar company. From 1982 to 1988, Ms. White served as the Director of Marketing, then Vice President of Sales and Marketing for Mrs. Fields Cookies, Inc. a global chain of premier cookie shops. Ms. White holds BS in communications from Westminster College and an MBA from Alameda College.

Available Information

Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to reports filed or furnished pursuant to Sections 13(a) and 15(d) of the Securities Exchange Act of 1934, as amended, are available free of charge from links on our website at www.tenfold.com as soon as reasonably practicable after such reports are electronically filed with, or furnished to, the Securities and Exchange Commission. Registration statements and amendments thereto filed pursuant to the Securities Act of 1933, as amended, are similarly available from our website. The information posted on our web site is not incorporated into this Annual Report.

You may read and copy all or any portion of reports, statements or other information we file with the SEC at the public reference facility maintained by the SEC at 100 F Street, N.E., Washington, DC 20549.

Please call the SEC at 1-800-SEC-0330 for more information on the public reference room. You can also find our SEC filings at the SEC’s website at http://www.sec.gov.

17

Item 1A. Risk Factors

We operate in a rapidly changing environment that involves numerous risks, some of which are beyond our control. The following discussion elaborates on some of these risks.

If we are unable to generate sufficient cash flow from operations, or secure additional sources of financing in the future, we will be unable to continue operations as a going concern

While our financial statements have been prepared under the assumption that we will continue as a going concern, the independent accounting firm’s report on our December 31, 2005 financial statements, prepared by Tanner LC, included an explanatory paragraph relating to their substantial doubt as to our ability to continue as a going concern. Our business model relies upon generating new sales to existing and new customers. On March 30, 2006 we completed a capital raising transaction for gross proceeds of approximately $6.3 million (before expenses and repayment of $1.1 million of interim financing obligations). We believe that with the proceeds of this capital transaction, and new sales that we believe that we can close during 2006, we will have sufficient liquidity for our operations during 2006. However, if we do not close sufficient new sales to existing and new customers, we would be required to pursue one or a combination of the following remedies: seek additional sources of financing, further reduce operating expenses, sell part or all of our assets, or terminate operations. There can be no assurance that we will be successful achieving sufficient cash flow.

We continue to experience difficulty in securing customer revenue

We have experienced difficulty closing substantial new sales, and it is unclear when or if we can expect to predictably close material sales to new or existing customers. Our recent strategy of selling small, proof-of-concept initial “penetrate” projects, and then seeking to “radiate” into the account by selling additional services and licenses was not successful in generating sufficient sales to achieve profitability or positive cash flow. Under the leadership of our new Chief Executive Officer, Robert W. Felton, we have recently changed our business model to focus on selling larger consulting projects but we have not yet closed any sales under this model. Furthermore, our uncertain future may make it less likely for customers to want to do business with us. As a result, there is no assurance that we will be able to convince existing customers or future prospective customers to purchase products or services from us or that any customer revenue that is achieved can be sustained. If we are unable to obtain future customer revenue or outside financing, our operations, financial condition, liquidity, and prospects will be materially and adversely affected, and we would be required to pursue one or a combination of the following remedies: seek additional sources of financing, further reduce operating expenses, sell part or all of our assets, or terminate operations.

Our sales cycle can be lengthy and subject to delays and these delays could cause our operating results to suffer

We believe that a customer’s decision to purchase significant products or services from us can involve a significant commitment of resources and be influenced by customer budget cycles. To successfully sell our products and services, we generally must educate our potential customers regarding the use and benefit of our products and services. Getting new customers to purchase significant licenses or services can require significant time and resources. Consequently, the period between initial contact and the purchase of our products or services can be long and subject to delays associated with the lengthy budgeting, approval, and competitive evaluation processes that typically accompany significant capital expenditures. Sales delays could cause our operating results to vary widely. There can be no assurance that we will not experience sales delays in the future. In addition, we face a challenging sales environment and there can be no assurance that we will have sales in the future.

We are substantially dependent on a small number of customers and the loss of one or more of these customers may cause revenues and cash flow to decline

We have derived, and over the near term we expect to continue to derive, a significant portion of our revenues and cash flow from a limited number of customers. For example, three customers accounted for a

18

total of 49 percent of our total revenues for the year ended December 31, 2005 (individually 20 percent, 18 percent, and 11 percent, respectively). For the year ended December 31, 2004, three customers accounted for a total of 87 percent of total revenue (individually 50 percent, 22 percent and 15 percent, respectively). Significant reductions in the amount of business major customers conduct with us has previously and may in the future, materially and adversely affect our business, results of operations, financial position and liquidity. Replacing the loss of a major customer is unpredictable, and we have not been successful in doing so in the past. Revenues and cash flows from a single customer or a few major customers may constitute a significant portion of our total revenues and cash inflows in a particular period, then decline as the volume of work performed for specific customers decreases as they complete projects. A major customer in one period may not continue to purchase significant licenses or services from us in a subsequent period.

The customer accounting for 20 percent of our total revenues for the year ended December 31, 2005, completed its use of our time-and-materials consulting services for its application development project during the quarter ended December 31, 3005. The customer accounting for 18 percent of our total revenues for the year ended December 31, 2005, substantially completed its application development project during the quarter ended March 31, 2005. The customer accounting for 11 percent of our total revenues for the year ending December 31, 2005, DevonWay, is a related party. See Note 18 of Notes to Financial Statements for more information. In future periods, we do not expect the amount of revenue from these customers to be significant as they have completed their current projects. We have not sold new projects to replace these projects, and are not currently working on any significant consulting projects (which have been our primary source of revenue in recent years).

Our growth and success depends on our ability to successfully implement our new business model; however, we have limited experience with the new model

Under the leadership of our new Chief Executive Officer, Robert W. Felton, we have recently changed our business model to focus on selling larger consulting projects, instead of the smaller prototype application projects that we primarily sold in 2005. Although we hope to be more successful with this new model, we have limited experience with the new model as we have introduced it only recently, and have not yet closed any sales under this model. Under this new model, we expect to take on larger, more difficult and complex consulting projects than we typically have in recent years. Under our original fixed-price project business model that we discontinued several years ago, we received customer complaints and lawsuits concerning some of our projects. Although we have substantially changed our business model, including no longer offering to do such projects on a fixed-price basis or providing a money-back guarantee, we cannot be certain that we will not receive customer complaints in the future. Such complaints would likely adversely affect our ability to sell to other customers. If our new strategy for selling and delivering our services and products is unsuccessful, or if we are unable to close significant new business within the time frames anticipated, our revenues and operating results will continue to suffer.

Our historical quarterly operating results have varied significantly and our future operating results could vary

Historically, our quarterly operating results have varied significantly. For example, during some years, we have had quarterly profits followed by losses in subsequent quarters. Our future operating results may vary significantly in the future as well. Until we achieve and sustain material sales to new or existing customers, we expect to continue to experience declining revenues and losses.

Our future prospects are difficult to evaluate

In light of our operating results for recent periods and the continued difficult sales environment we face and in the technology sector in general, it is difficult to evaluate our future prospects. There can be no assurance that we will be able to successfully complete current or new projects. Additionally, our failure to successfully complete any current or new projects may have a material adverse impact on our financial position and results of operations. We cannot be certain that our business strategy will succeed.

19

Our failure to attract and retain highly skilled employees, particularly consultants, project managers and other senior technical personnel, could impair our ability to complete projects and expand our business

Our services business is labor intensive. We currently have only a small number of consultants in our consulting organization. We expect to supplement them on projects with members of our Development organization for projects in the near term. Longer term, our success will depend in large part upon our ability to attract, retain, train, and motivate highly skilled employees, particularly consultants, project managers and other senior technical personnel. Any failure on our part to do so would impair our ability to adequately manage and complete existing projects, bid for and obtain new projects, and expand business. There exists significant competition for employees with the skills required to perform the services we offer. Qualified consultants, project managers and senior technical staff are in great demand and are likely to remain a limited resource for the foreseeable future. Our current financial condition, and our prior restructurings and related headcount reductions, may make it more difficult for us to retain and compete for such employees. There can be no assurance that we will be successful in retaining, training, and motivating our employees or in attracting new, highly skilled employees. If we are unsuccessful in this effort or if our employees are unable to achieve expected performance levels, our business will be harmed.

A loss of Robert W. Felton, Jeffrey L. Walker, or any other key employee could impair our business

Our industry is competitive and we are substantially dependent upon the continued service of our existing executive personnel, especially Robert W. Felton, Chairman, President, and Chief Executive Officer. Furthermore, our products and technologies are complex and we are substantially dependent upon the continued service of our senior technical staff, including Jeffrey L. Walker, Executive Vice President, and Chief Technology Officer. If a key employee resigns to join a competitor or to form a competing company, the loss of the employee and any resulting loss of existing or potential customers to the competing company would harm our business. We do not carry key-man life insurance on any of our employees. We have not entered into employment agreements with our executives. In the event of the loss of key personnel, there can be no assurance that we would be able to prevent their unauthorized disclosure or use of our technical knowledge, practices, or procedures.

If we fail to adequately anticipate employee and resource utilization rates, our operating results could suffer

A high percentage of our operating expenses, particularly personnel and rent, are relatively fixed in advance of any particular quarter. As a result, unanticipated variations in the number, or progress toward completion, of our projects or in employee utilization rates did and may continue to cause significant variations in operating results in any particular quarter and could result in quarterly losses. Time-and-materials consulting arrangements can typically be terminated by a customer on short notice. An unanticipated termination of a major project, the delay of a project, or the completion during a quarter of several projects has in the past and may continue to result in under-utilized employees and could, therefore, cause us to suffer quarterly losses or cause adverse results of operations.

Our errors and omissions coverage may not cover contractual disputes

While we maintain errors and omissions insurance coverage for claims related to customer contract disputes within the coverage scope and term, given the nature and complexity of the factors affecting the estimated liabilities, actual liabilities may exceed or be outside the scope of our current errors and omissions coverage. We can give no assurance that our insurance carrier will extend coverage to future claims. In addition, no assurance can be given that we will not be subject to material additional liabilities and significant additional litigation relating to errors and omissions arising from future claims.

Our errors and omissions insurance policy is in the form of an industry standard software errors and omissions policy. As such, it only covers software errors and omissions that occur after the delivery of software and excludes contractual disputes such as service commitments and cost and time related guarantees. We have previously had contractual disputes related to our guarantees. While we have substantially changed our business model and no longer offer a money-back guarantee, no assurance can

20

be given that we will not be subject to these types of claims in the future. In the event that liabilities from claims are not covered by or exceed our errors and omissions coverage, our business, results of operations, financial position, or liquidity could be materially and adversely affected.

If our software contains defects or other limitations, we could face product liability exposure

Because of our limited operating history and our small number of customers, we have completed a limited number of projects that are now in production. As a result, there may be undiscovered material defects in our products or technology. Furthermore, complex software products often contain errors or defects, particularly when first introduced or when new versions or enhancements are released. Despite internal testing and testing by current and potential customers, our current and future products may contain serious defects. Serious defects or errors could result in lost revenues or a delay in market acceptance, which would damage our reputation and business.

Because our customers may use our products for mission-critical applications, errors, defects, or other performance problems could result in financial or other damages to customers. Our customers could seek damages for these losses. Any successful claims for these losses, to the extent not covered by insurance, could result in our being obligated to pay substantial damages, which would cause operating results to suffer. Although our license agreements typically contain provisions designed to limit our liability, existing or future laws or unfavorable judicial decisions could negate these limitations of liability provisions. A product liability claim brought against us, even if not successful, would likely be time consuming and costly.

We are involved in one litigation matter and in settlement discussions with our prior CEO, and may in the future be involved in further litigation or disputes that may be costly and time-consuming, and if we suffer adverse outcomes, our operating results could suffer

We are involved in a class action suit against more than 300 issuers involving the underwriters of those issuers’ initial public offerings. Although we currently expect to resolve this matter without significant cost to TenFold, we may in the future face other litigation or disputes with customers, employees, business partners, stockholders, or other third parties. Such litigation or disputes could result in substantial costs and diversion of resources that would harm our business. An unfavorable outcome of this matter may have a material adverse impact on our business, results of operations, financial position, or liquidity.

For the year ended December 31, 2005, we recognized estimated severance related charges related to the departure of our prior CEO totaling $670,000, including an estimated option modification charge of $157,000; which represents our best estimate as the separation terms have not been finalized. The parties are in settlement discussions but a settlement has not been reached. An unfavorable outcome of this matter could have a material adverse impact on our business, results of operations, financial position, or liquidity.

See Note 9 “Legal Proceedings and Contingencies” of Notes to Financial Statements for more information concerning our litigation and disputes.

Our settlements with Perot Systems and Cedars-Sinai Medical Center require that if we do not meet certain obligations their claims may be re-instated or re-asserted, and if this were to happen and we suffer adverse judgments, our operating results could suffer

Although we have settled prior disputes with Perot Systems and Cedars-Sinai Medical Center, and during 2004 entered into revised agreements with Cedars that confirm our completion of the earlier project and provide for mutual releases from prior related claims, our agreements still require that we perform and meet certain obligations. If we are unable to or do not perform or meet these obligations, Perot Systems and Cedars may re-instate or re-assert their respective prior claims against us. If either Perot Systems or Cedars were to re-instate or re-assert their respective claims, an unfavorable outcome of the matter may have a material adverse impact on our business, results of operations, financial position, or liquidity.

If we cannot protect or enforce our intellectual property rights, our competitive position would be impaired and we may become involved in costly and time-consuming litigation

Our success is dependent, in large part, upon our proprietary EnterpriseTenFold technology and other intellectual property rights. If we are unable to protect and enforce these intellectual property rights, our competitors will have the ability to introduce competing products that are similar to ours, and our revenues, market share, and operating results will suffer. To date, we have relied primarily on a combination of patent, copyright, trade secret, and trademark laws, and nondisclosure and other

21

contractual restrictions on copying and distribution to protect our proprietary technology. We have been issued three patents in the United States and intend to continue to seek patents on our technology when appropriate. There can be no assurance that the steps we have taken in this regard will be adequate to deter misappropriation of our proprietary information or that we will be able to detect unauthorized use and take appropriate steps to enforce our intellectual property rights. The laws of some countries may not protect our intellectual property rights to the same extent as do the laws of the United States. Furthermore, litigation may be necessary to enforce our intellectual property rights, to protect our trade secrets, to determine the validity and scope of the proprietary rights of others, or to defend against claims of infringement or invalidity. This litigation could result in substantial costs and diversion of resources that would harm our business.

To date, we have not been notified that our products infringe the proprietary rights of third parties, but there can be no assurance that third parties will not claim infringement by us with respect to current or future products. We expect software developers will increasingly be subject to infringement claims as the number of products and competitors in our industry segment grows and the functionality of products in different industry segments overlaps. Any of these claims, with or without merit, could be time-consuming to defend, result in costly litigation, divert management’s attention and resources, cause product shipment delays, or require us to enter into royalty or licensing agreements. These royalty or licensing agreements, if required, may not be available on terms acceptable to us, or at all. A successful claim against us of product infringement and our failure or inability to license the infringed or similar technology on favorable terms would harm our business.

If we fail to successfully compete, our revenues and market share will be adversely affected

The market for our products and services is highly competitive, and if we are not successful in competing in this market, our revenues and market share will suffer. Many of our competitors have significantly greater financial, technical and marketing resources, generate greater revenues, and have greater name recognition than we do. In addition, there are relatively low barriers to entry into our markets and we have faced, and expect to continue to face, additional competition from new entrants into our markets.

International political and economic uncertainty could have an adverse impact on our business and on our operating results

Revenues from customers outside of North America were approximately 11 percent of total revenues for 2005, and approximately 20 percent of total revenues for 2004. The international political and economic uncertainty caused by the ongoing war on terrorism and other international political developments may adversely impact our ability to continue existing relationships with our foreign customers and to develop new business abroad.

Our stock price may continue to be volatile

Our stock price has fluctuated widely in the past and could continue to do so in the future. Your investment in our stock could lose value. Some of the factors that could significantly affect the market price of our stock, in addition to those mentioned in this section, include: further decreases in our cash resources, changes in our revenue; changes in our customer base including the loss of a major customer; changes in management; variations in our quarterly financial results; problems implementing our business model; reports or earnings estimates published by financial analysts; changes in political, economic and market conditions either generally or specifically to particular industries; and fluctuations in stock prices generally, particularly with respect to the stock prices for other technology companies. A significant drop in our stock price could expose us to the risk of securities class action lawsuits. Defending against such lawsuits could result in substantial costs and divert management’s attention and resources. An unfavorable outcome of such a matter may have a material adverse impact on our business, results of operations, financial position, or liquidity.

22

No corporate actions requiring stockholder approval can take place without the approval of our controlling stockholders

The executive officers, directors, and entities affiliated with them, in the aggregate, beneficially own approximately 70 percent of our voting stock (as calculated using the SEC’s conventions). These stockholders acting together or with others would be able to decide or significantly influence all matters requiring approval by our stockholders, including the election of directors and the approval of mergers or other business combination transactions. This concentration of ownership may have the effect of delaying or preventing a merger or other business combination transaction, even if the transaction would be beneficial to our other stockholders.

The anti-takeover provisions in our charter documents and/or under Delaware law could discourage a takeover that stockholders may consider favorable