Table of Contents

FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16 of

the Securities Exchange Act of 1934

For the month of September 2005

CLP Holdings Limited

(Registrant’s name in English)

147 Argyle Street

Kowloon, Hong Kong

(Address of Registrant’s principal executive office)

Indicate by check mark whether the Registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F X Form 40-F

Indicate by check mark whether the Registrant by furnishing this information contained in this Form is also thereby furnishing information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes No X

If “Yes” is marked, indicate below the file number assigned to the Registrant in connection with Rule 12g3-2(b): 82-

Table of Contents

Registrant hereby incorporates by reference in the report on Form 6-K the following Exhibit:

Exhibit

The Interim Report 2005 which was despatched to shareholders on 13 September 2005.

2

Table of Contents

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| For and on behalf of | ||

CLP HOLDINGS LIMITED

| ||

By: | / s / April Chan | |

Name: | April Chan | |

Title: | Company Secretary | |

Date:17 October 2005

3

Table of Contents

HIGHLIGHTS

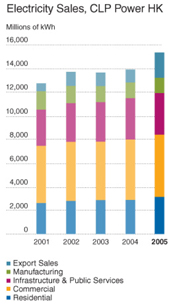

| • | Electricity sales in Hong Kong grew 3.1% to 13,193GWh; total sales (which include sales to the Chinese mainland) rose 10.5% to 15,338GWh. |

| • | Consolidated revenue rose 13.8% to HK$16,626 million; revenue from our electricity business in Hong Kong recorded a 8.6% growth to HK$13,638 million. |

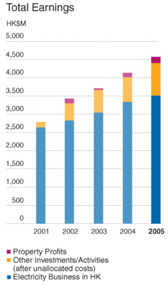

| • | Earnings from our electricity business in Hong Kong increased by 5.2% to HK$3,510 million; earnings from other activities grew by 27.7% to HK$1,010 million. |

| • | Total earnings up 10.6% to HK$4,577 million; operating earnings (which exclude Hok Un redevelopment profit) up 9.7% to HK$4,403 million. |

| • | Second interim dividend of HK$0.48 per share. |

Table of Contents

Page 1

| 6 months ended 30 June | Increase/ (Decrease) | | |||||||

| 2005

| 2004

| %

| |||||||

| Per share | |||||||||

Earnings per share, HK$ | |||||||||

Including Hok Un redevelopment profit | 1.90 | 1.72 | 10.6 | ||||||

Excluding Hok Un redevelopment profit | 1.83 | 1.67 | 9.7 | ||||||

Dividends per share, HK$ | |||||||||

First interim | 0.48 | 0.45 | |||||||

Second interim | 0.48 | 0.45 | |||||||

Total interim dividends | 0.96 | 0.90 | 6.7 | ||||||

| For the period | |||||||||

Revenue, HK$M | |||||||||

Hong Kong (HK) electricity business | 13,638 | 12,563 | 8.6 | ||||||

Total

| 16,626

| 14,615

| 13.8

| ||||||

Earnings, HK$M | |||||||||

Electricity business in HK | 3,510 | 3,337 | 5.2 | ||||||

Other investments / activities | |||||||||

Sales to Chinese mainland from HK | 63 | 30 | |||||||

Generating facilities in Chinese mainland serving HK 1 | 431 | 380 | |||||||

Other power projects in Chinese mainland | 95 | 43 | |||||||

Energy businesses in Asia-Pacific region | 425 | 404 | |||||||

Group non-energy activities | (4 | ) | (66 | ) | |||||

| 1,010

| 791

| 27.7

| |||||||

Unallocated net finance costs | (43 | ) | (39 | ) | |||||

Unallocated Group expenses | (74 | ) | (75 | ) | |||||

Total operating earnings | 4,403 | 4,014 | 9.7 | ||||||

Hok Un redevelopment profit | 174 | 124 | |||||||

Total earnings | 4,577 | 4,138 | 10.6 | ||||||

Electricity sales (CLP Power HK), millions of kWh | |||||||||

Residential | 3,114 | 2,875 | 8.3 | ||||||

Commercial | 5,259 | 5,093 | 3.3 | ||||||

Infrastructure & Public Services | 3,529 | 3,497 | 0.9 | ||||||

Manufacturing | 1,291 | 1,333 | (3.2 | ) | |||||

Total local sales | 13,193 | 12,798 | 3.1 | ||||||

Export sales | 2,145 | 1,085 | 97.7 | ||||||

Total electricity sales | 15,338 | 13,883 | 10.5 | ||||||

Interest cover2 , times | 10 | 9 | |||||||

| As at the balance sheet date | 30 June | 31 December | Increase | ||||||

| 2005 | 2004 | % | |||||||

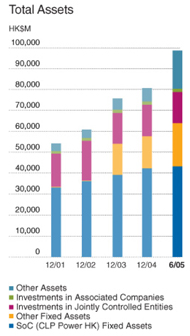

Total assets, HK$M | 98,738 | 80,799 | 22.2 | ||||||

Total borrowings, HK$M | 32,502 | 18,774 | 73.1 | ||||||

Shareholders’ funds, HK$M | 46,257 | 44,199 | 4.7 | ||||||

Total debt to total capital3, % | 41.3 | 29.8 | |||||||

| 1 | This represents earnings contribution from our investments in Guangdong Nuclear Power Joint Venture Company, Limited and Hong Kong Pumped Storage Development Company, Limited, whose generating facilities serve Hong Kong |

| 2 | Interest cover = Profit before taxation and interest / (interest charges + capitalised interest) |

| 3 | Total debt to total capital = debt / (shareholders’ funds + debt + minority interest) |

Table of Contents

Page 2

Table of Contents

Page 3

Dear Shareholders,

I am pleased to present our Interim Report for the half year ended 30 June 2005 and to record a strong performance by the CLP Group over this period.

Financial Results for the Six-month Period

Total operating earnings for the six months ended 30 June 2005 increased by 9.7% to HK$4,403 million, as compared with the corresponding period in 2004.

This growth in earnings came from across all our investments in the energy sector, whether these be our electricity business in Hong Kong or our interests in the electricity sector in the Mainland and elsewhere in the Asia-Pacific Region.

Further details of the Group’s financial performance are set out in the Management’s Discussion and Analysis which forms part of this Interim Report. In this Chairman’s Statement, I wish to focus on three aspects of our activities which have been of particular significance during the first half of 2005. These are:

| • | The Hong Kong Government’s public consultation on the development of the electricity market in Hong Kong after 2008; |

| • | The progress made by the Group in continuing to make good on its commitment to manage responsibly the environmental aspects of our activities; and |

| • | The completion of CLP’s acquisition of Singapore Power’s merchant energy business in Australia. |

Hong Kong Electricity Business

Stage I of the Hong Kong Government’s public consultation on the development of the electricity market in Hong Kong after 2008 concluded at the end of April. I wrote to shareholders in May to advise that, as promised, CLP has been an active, informed and authoritative participant in the public discussion todate. Our response to Stage I of the consultation, “A Balanced Deal - A Bright Future”, was submitted to Government on 26 April. In this, we emphasised that the keys to the excellence of Hong Kong’s electricity supply were found in a regulatory system which delivers practicality, service excellence, a fair deal for investors and clear accountability and responsibility.

In June, Government published its summary of the views received in response to Stage I of its consultation. These included 766 written submissions from many sectors of our community - ranging from businesses to individuals, from trade organisations to environmental groups, as well as 175 messages through the discussion forums on Government’s website. We welcome this wide participation in the debate on the future of our industry.

Table of Contents

Page 4

It has been noticeable that the majority of those who participated in the consultation consider reliability and the safety of electricity supply to be the most important objectives of the future regulation of Hong Kong’s electricity sectors - in line with the views which CLP itself has already expressed. We are also encouraged that most respondents consider our tariff to be reasonable and affordable.

Opinions were expressed that the post-2008 regulatory regime should provide for lowered returns for investors, and for that regime to be subject to a shortened review period. In these respects, CLP’s position is clear - returns must not be judged in isolation, nor should they be reset at unduly frequent intervals. The reliability of Hong Kong’s electricity supply has not happened by chance. It has stemmed from timely and adequate investment in Hong Kong’s electricity infrastructure. This, in turn, depends on a clear and stable regulatory system which offers reasonable returns to investors to facilitate such investment. After all, no other private industry in Hong Kong requires such continuous, large-scale and long-term investment as does the electricity sector.

We understand that Government is now taking into consideration the views collected during its Stage I consultation, so as to map out its proposals for the broad framework of development of the post-2008 electricity market, and that Stage II of the consultation will be launched later this year. CLP will continue its vigorous participation in this debate, and we will continue to report to shareholders on developments in this key issue for CLP’s future.

Environment

A number of respondents to the public consultation on Hong Kong’s electricity sector highlighted the importance of managing the environmental impact of electricity generation and of developing renewable energy sources.

I am pleased to report that CLP continues to move ahead on both these issues - in Hong Kong and elsewhere.

In Hong Kong, our proposals to retrofit flue gas desulphurisation (FGD) equipment at Castle Peak Power Station have now been approved by Government as part of the 2005-8 Financial Plan for our Hong Kong electricity business. This is a major project, and a challenging one - requiring substantial engineering works to be undertaken at the power station, whilst maintaining the availability of its essential generating capacity. Design and planning work is already underway.

The first half of 2005 also saw a significant step forward in our plans to develop the infrastructure needed to assure the availability of natural gas in Hong Kong for our electricity generation, with the start of the environmental review and approval procedures needed for site selection of the liquefied natural gas (LNG) receiving terminal which we will need in order to bring our LNG supply on stream early next decade.

As those shareholders who live in Hong Kong will know, local climatic, geographical and physical characteristics place significant constraints on the extent to which renewable energy can be developed in Hong Kong with existing technology. However, CLP remains keen to increase its participation in renewable energy projects - wherever these are economically, technically and environmentally feasible. In recent months, we have increased our investment in renewable energy projects in the Mainland, both wind and hydro. In addition, we are exploring new opportunities elsewhere, notably in Australia and India, where suitable natural resources are available. We aim to report further progress in this area by the end of 2005.

Table of Contents

Page 5

Australia

In April, a circular to shareholders advised you of the details of the proposed acquisition by CLP of Singapore Power’s merchant energy business in Australia.

This acquisition was completed, as targeted, on 31 May 2005. When coupled with CLP’s existing Yallourn Power Station, CLP is well on the way towards building a diversified and integrated energy business in Australia, focusing on electricity and gas retail, with a portfolio of physical assets in support of that retail business.

This business, which was rebranded as “TRUenergy” in June, constitutes the fifth largest energy retailer in Australia. The acquisition of the merchant energy business has also brought into the CLP Group a 1,280MW gas-fired power station at Torrens Island in South Australia - meaning that we have moved forward from reliance only on coal-fired generation at Yallourn. We believe that this diversified fuel mix promotes a better balance in our electricity generation activities in Australia, including from an environmental perspective.

Given that the acquisition of the merchant energy business was completed only at the end of May, considerable work is underway to integrate that business both with our existing investment at Yallourn and with the standards of operational excellence, financial control and corporate values of the CLP Group as a whole. I will report more fully to shareholders on the progress being made in this regard in our next Annual Report.

As in previous years, this Interim Report explains the wider environmental and social aspects of our activities, in addition to our financial and operational performance. 2005 has started well at the CLP Group - we are determined to carry this performance forward through the remainder of this year and beyond.

/ s / The Hon. Sir Michael Kadoorie

The Hon. Sir Michael Kadoorie

Hong Kong, 23 August 2005

Table of Contents

Page 6

Management’s Discussion And Analysis

This section describes CLP’s major activities in Hong Kong, the Chinese mainland and elsewhere in the Asia-Pacific region, as well as the Group’s financial results, funding and obligations during the first half of 2005.

CLP follows a clear, consistent and focused strategy to realise our vision of being a leading investor-operator in the Asia-Pacific electricity power sector. We aim continuously to enhance our core Hong Kong electricity business and to develop a portfolio of electricity businesses in the Chinese mainland and the Asia-Pacific region. An outline of our investments is set out below:

Hong Kong

| Investments | Equity Interest | Description | ||

CLP Power Hong Kong Limited (CLP Power Hong Kong) | 100% | CLP Power Hong Kong owns and operates the transmission and distribution system, covering a supply area of approximately 1,000 sq. km and which includes: • 554 km of 400kV lines; • 1,156 km of 132kV lines; • 296 km of 33kV lines; • 10,151 km of 11kV lines; • 55,631 MVA transformers; • 206 primary substations in operation; and • 12,327 secondary substations in operation.

| ||

Castle Peak Power Company Limited (CAPCO), 6,283 megawatts (MW) of installed generating capacity | 40% | CAPCO owns: Black Point Power Station (2,500MW, when completed) • Gas-fired power station (with distillate as back-up) comprising eight combined cycle turbines of 312.5MW each. • Units 1 to 6 in operation, Unit 7 commenced operation in August 2005 and Unit 8 to be commissioned in 2006.

Castle Peak Power Station (4,108MW) • Commissioned between 1982 and 1990. • One of the world’s largest coal-fired power station complexes, comprising eight units ranging from 350MW to 677MW. • Two of the 677MW units are capable of burning gas as backup fuel. All units can burn oil as a backup fuel.

Penny’s Bay Power Station (300MW) • Three diesel oil-fired units of 100MW each, commissioned in 1992.

|

| Note: | CLP Power Hong Kong operates CAPCO’s power stations and purchases its power from CAPCO and Guangdong Daya Bay Nuclear Power Station. These sources of power, together with CLP’s right to use 50% of the capacity of Phase 1 of the Guangzhou Pumped Storage Power Station, amount to a total installed capacity of 8,263MW. |

Table of Contents

Page 7

Chinese Mainland

Investments Gross/Equity MW | Equity Interest | Description | ||

Guangdong Nuclear Power Joint Venture Company, Limited (GNPJVC) 1,968/492MW | 25% | GNPJVC was established in 1985 to construct and operate Guangdong Daya Bay Nuclear Power Station (GNPS) at Daya Bay

| ||

Hong Kong Pumped Storage Development Company, Limited (PSDC) 1,200/600MW

| 49% | CLP has the right to use half of the 1,200MW pumped storage capacity of Phase I of the Guangzhou Pumped Storage Power Station until 2034. | ||

CLP Guohua Power Company Limited (CLP Guohua) 2,100/630MW

| 49% | CLP Guohua holds interests in three coal-fired power stations, namely Beijing Yire in Beijing , Panshan in Tianjin , Panshan in Tianjin , and Sanhe in Hebei , and Sanhe in Hebei , with a combined installed capacity of 2,100MW. , with a combined installed capacity of 2,100MW. | ||

CLP Guohua Shenmu Power Company Limited (Shenmu) 200/98MW

| 49% | Shenmu Power Station, in Shaanxi , has two 100MW coal-fired units. , has two 100MW coal-fired units. | ||

Guizhou CLP Power Company Limited (Guizhou CLP Power) 600/420MW

| 70% | Guizhou CLP Power owns and operates two 300MW coal-fired generating units which supply the Guizhou power grid and, indirectly, Guangdong Province power grid and, indirectly, Guangdong Province . . | ||

Shandong Zhonghua Power Company, Ltd. (SZPC) 3,000/882MW

| 29.4% | SZPC owns four coal-fired power stations, Shiheng I and II (totalling 1,200MW), Liaocheng (1,200MW) and Heze II (600MW), in Shandong Province . . | ||

Huaiji Power Project (Huaiji) 98/49MW

| 50% | Eight small hydro power stations in Huaiji County , Guangdong Province are in operation, with one under construction, amounting to a total of 98MW. , Guangdong Province are in operation, with one under construction, amounting to a total of 98MW. | ||

HNEEP-CLP Changdao Wind Power Co., Ltd. (Changdao Wind Power) 27/12MW

| 45% | Changdao Wind Power was established in 2004 to develop a 27MW wind power project on Changdao Island to supply power to Shandong Province. to supply power to Shandong Province. | ||

CLP Guangxi Fangchenggang Power Company Limited (Fangchenggang) 1,200/840MW

| 70% | Construction of a new power station with two 600MW coal-fired units at Fangchenggang , Guangxi , Guangxi is in progress and the project will be commissioned by end of 2007. is in progress and the project will be commissioned by end of 2007. |

. GNPS is equipped with two 984MW Pressurised Water Reactors for which the majority of the equipment was imported from France and the United Kingdom. 70% of electricity generated is supplied to Hong Kong, with the remaining 30% sold to Guangdong.

. GNPS is equipped with two 984MW Pressurised Water Reactors for which the majority of the equipment was imported from France and the United Kingdom. 70% of electricity generated is supplied to Hong Kong, with the remaining 30% sold to Guangdong.Table of Contents

Page 8

Asia-Pacific Region

Investments Gross/Equity MW | Equity Interest | Description | ||

Gujarat Paguthan Energy Corporation Private Limited (GPEC), India 655MW

| 100% | GPEC owns and operates a 655MW gas-fired combined cycle power station in Gujarat, India. | ||

Ho-Ping Power Company (Ho-Ping), Taiwan 1,320/528MW

| 40% | Ho-Ping owns a 1,320MW coal-fired power station at Ho-Ping, Taiwan, which started operations in 2002. Operation is by a separate joint venture, with the same shareholdings as Ho-Ping, but with CLP management leadership. | ||

Electricity Generating Public Company Limited (EGCO), Thailand 5,575/768MW

| 22.4% | EGCO owns and operates two gas-fired combined cycle power stations in Thailand (2,056MW). It has also invested in a number of small power projects operating in Thailand and the Philippines, totalling 958MW, and in 2,561MW of projects under construction in Thailand and Laos. | ||

BLCP Power Limited (BLCP), Thailand 1,434/717MW

| 50% | BLCP is the developer of a 1,434MW coal-fired power station now under construction at Map Ta Phut, Thailand. CLP is responsible for construction management and is the major shareholder in the operating company. | ||

TRUenergy, Australia 3,726MW | 100% | TRUenergy comprises the ownership and operation of a number of electricity and gas assets in Victoria and South Australia. These include: from 1 June 2005 • 1,480MW coal-fired Yallourn Power Station and mine • 1,280MW gas-fired Torrens Island Power Station • 966MW Ecogen long-term hedge agreement • Iona Gas Storage facility • Various long-term gas supply contracts • Over 1.1 million retail electricity and gas customer accounts from 29 August 2005 • 33% interest in SEAGas

|

Table of Contents

Page 9

Operational Performance and Outlook

Electricity Business in Hong Kong

Following a strong rebound in 2004, the momentum for economic growth slowed slightly but was still sustained at a moderately high pace in the first half of 2005. Electricity sales to local customers in the first half of 2005 rose by 3.1% compared to the corresponding period last year, mainly due to increase in sales to Residential and Commercial sectors.

A steady increase in the number of residential customers and high temperatures in May helped sales to the Residential Sector. The Commercial Sector was supported by favourable business conditions and further improvement in the tourist industry. Growth in the Infrastructure & Public Services Sector was offset by the impact of energy conservation programmes within the Government. Sales to the Manufacturing Sector followed the past declining trend due to the reduction of production in Hong Kong.

A breakdown of the local sales growth by sector during the period is as follows:

| Increase/(Decrease) | Total Local Sales | |||

Residential | 8.3% | 23.6% | ||

Commercial | 3.3% | 39.9% | ||

Infrastructure & Public Services | 0.9% | 26.8% | ||

Manufacturing | (3.2%) | 9.7% | ||

Sales to the Chinese mainland recorded strong year-on-year growth of 97.7%. Demand from Shekou remained steady with a slight growth of 0.3%. With the contract with Guangdong Power Grid Corporation (GPG) renewed and continued shortage of electricity supply in Guangdong, significant growth in GPG sales was achieved.

Total unit sales, including both local sales and sales to the Chinese mainland, rose 10.5% in the first half of the year over the same period in 2004.

A new local maximum demand of 6,475MW was recorded in the evening on 18 July. This represented a growth of 2.3% over last year (6,329MW) and reduces our generation reserve margin to 27.6%.

CLP’s efforts towards improving productivity and keeping operating costs to a minimum have led to customers benefiting from an average net tariff that remains the lowest in Hong Kong. During 2004, we announced that tariffs would be frozen in 2005. There has now been no increase in tariff level since 1998.

To enhance supply quality and reliability, as well as provide for demand created by new towns and infrastructure development projects in our supply area, CLP incurred HK$1.8 billion of capital expenditure in the transmission and distribution networks during the period. Major projects included establishment of Mai Po, San Shek Wan, On Shum Street and Wan Po Road Substations. In addition, CLP also invested HK$0.7 billion in generation, customer services and other supporting facilities.

Table of Contents

Page 10

These investments will continue. In June 2005, the Executive Council approved the Financial Plan of our Hong Kong electricity business for the period from January 2005 to September 2008, submitted pursuant to the Scheme of Control Agreement. The approved Financial Plan provides for an estimated capital expenditure of HK$23.8 billion, the majority of which will be used to enhance the transmission and distribution systems.

We continue to strive to provide quality services to our customers, and to maintain a high level of satisfaction across all customer segments. Our 15 Customer Service Centres continue to be one of the popular service channels for the general public, visited by more and more customers. CLP’s commitment to quality customer service is reinforced by the Performance Pledges published annually.

Our performance in customer service is well recognised in the local industry. We won five awards at the Hong Kong Association for Customer Service Excellence Award 2004 in service counter, hotline and internal support services.

As an advocate of safe and efficient use of energy, CLP launched a series of promotional campaigns on electrical applications and appliances for business and residential customers. Electric cooking in particular has gained popularity. In a recent market survey, 58% of respondents are aware of induction cookers and 50% can easily recall the benefits.

To ensure ongoing improvements in business productivity, CLP continues to invest in information technology. Key projects include the Trouble Call and Outage Management System for supply reliability enhancement, a new field work handheld device system for improvement of customer service jobs, and a Plant Maintenance Optimisation System in order to better manage the generation assets.

CLP adopts innovative approaches with the aim of ongoing improvement in our work processes and environment. In March 2005, we won the Grand Award in the Green Innovative Practice Award for the Hong Kong Eco-Business Award 2004, based on our project on “Insulating Oil Regeneration Plant for Power Transformers” with an annual saving of HK$4 million.

Electricity Investments in the Chinese Mainland

The Guangdong Daya Bay Nuclear Power Station, in which CLP holds a 25% share, operated at a high capacity factor in the first six months. The station was awarded first places in Nuclear Safety, Industrial Safety and Radiation Protection in the 2004 Safety Challenge Competition, which included all the nuclear power stations in France and South Africa. Daya Bay also obtained its ISO 14001 re-accreditation, a recognition that Daya Bay has held since 1999.

Coal supply and tariff management for our joint ventures SZPC, CLP Guohua, Shenmu and Guizhou CLP Power continued to be a primary focus in 2005.

Despite the coal supply situation remaining tight, operation of the power stations has not been affected, except for Anshun II Power Station in Guizhou which experienced temporary restrictions in generation in February 2005 due to coal shortage.

Table of Contents

Page 11

The surge in coal prices which commenced in 2004 has not shown signs of abatement, and high coal prices are likely to prevail throughout 2005. To alleviate the financial pressure on power stations, the PRC authorities approved new tariffs which became effective in mid-2005. Most of the power stations under our joint ventures benefited from the increased tariffs. However, the increases are in general not sufficient to fully compensate for the significant rises in coal costs, resulting in various degrees of impact on profits of our joint ventures. The CLP Guohua and Shenmu power stations were least affected because of higher than projected operating hours. The impact on the Anshun II has been moderate, while that on the Shandong joint venture was substantial.

As regards new projects, satisfactory progress has been made on the 2 x 600MW greenfield project at Fangchenggang in Guangxi in which CLP has a 70% interest. Following the approval of the project by the National Development and Reform Commission and Ministry of Commerce, the joint venture was formally established in May 2005. Procurement of the major plant and auxiliary equipment was also completed. Construction has commenced and it is expected that the project will be commissioned by the end of 2007.

Electricity Investments in the Asia-Pacific Region

CLP acquired the TXU Merchant Energy Business (MEB) from Singapore Power on 31 May 2005. The acquisition was partly financed by CLP Group’s internal funds, with a new corporate finance facility used to finance the balance of the acquisition and re-finance existing facilities of Yallourn Energy Pty Limited (Yallourn Energy). An investment grade credit rating of “A-” was obtained from Standard & Poor’s.

Yallourn Energy and the MEB were combined to form TRUenergy which is the fifth largest energy retailer in Australia and sells gas and electricity to over 1.1 million customers across the eastern Australian states of Victoria, New South Wales, South Australia and Queensland. TRUenergy provides horizontal integration in generation and vertical integration into retail, and access to gas supply. Besides providing significant mitigation to electricity market risks, the integrated business with an investment grade credit rating also provides a strong platform for CLP’s future expansion in the Australian energy retail and generation sectors, including renewable energy.

Following obtaining all the necessary third party consents, CLP’s acquisition of Singapore Power’s 33% interest in SEAGas was completed on 29 August 2005.

Our wholly-owned power station GPEC, in India, continued to maintain high standards of reliability and safety. Following satisfactory implementation of the amended Power Purchase Agreement (PPA) with the Gujarat Electricity Board (GEB), there was significant improvement in overdue payments in 2004. Although some new challenges to the PPA terms in relation to matters such as incentive payments received when GPEC was available on naphtha fuel but not dispatched and calculations of interest on working capital re-emerged in early 2005, CLP has discussed these with GEB and Gujarat state authorities and is confident that these will be resolved amicably. Work on the 1,095MW expansion at the GPEC site has also been progressing, with tenders for the Engineering, Procurement and Construction contracts having been received and being evaluated. Discussions on power off-take and gas supply are also underway.

Table of Contents

Page 12

In Thailand, construction of the BLCP project has been progressing satisfactorily. The two 717MW coal-fired generating units are expected to commence commercial operation in 2006/07 as planned. Mobilisation of Operations and Maintenance (“O&M”) activities by an O&M company with CLP leadership also commenced. The current activities are focused on recruitment, installation of information technology systems, preparation of procedures and establishment of a comprehensive training program.

Details of the plans for the reform of the Thai electricity industry, privatisation of the Electricity Generating Authority of Thailand and the solicitation for new generation capacity are still being developed. In light of these developments, we continue to review our position in EGCO as well as our obligation under a Joint Development Agreement to divest half of our share in BLCP to EGCO.

In the first half of 2005, Ho-Ping Power Station in Taiwan continued to show significant improvements in operations, with high reliability recorded. However, on 18 July two of the three coal storage domes were damaged during the passage of Typhoon Haitang. The third dome had been damaged last year. Production and coal unloading were interrupted but resumed after a few days. In the meantime, claims under insurance policies and equipment warranties for the three domes are being pursued.

Favourable adjustment in the energy charge rate at Ho-Ping has also been awarded in accordance with the mechanism under the PPA with Taiwan Power Company. This mitigated to a large extent previous increases in coal and transportation costs. Ho-Ping has obtained “twA+” long-term and “twA-2” short-term corporate credit ratings, with a stable long-term outlook, from Taiwan Ratings Corporation. This would assist Ho-Ping’s potential refinancing of its existing loans by the issue of an unsecured bond to reduce interest costs and interest rate exposure.

Electricity-Related Businesses

Property Business

CLP redevelops sites in Hong Kong which are no longer required for electricity purposes.

In recent years, our major project has been the residential redevelopment of the former power station at Hok Un, Kowloon. This 50/50 joint venture project, known as Laguna Verde, led by CLP and a wholly-owned subsidiary of Cheung Kong (Holdings) Ltd., comprises 4,735 flats, 1,692 parking spaces and 270,000 sq.ft. of commercial space. Over 99% of the residential units had been sold by the end of June 2005.

Following the completion of the Hok Un redevelopment and the sale of the site at 305 Castle Peak Road, as reported in our Annual Report 2004, we do not currently consider that there are other surplus sites in Hong Kong which would be made available for redevelopment on any significant scale.

Public Lighting and Engineering Services

CLP continues to offer contracting and consultancy services in power engineering, communications, building services, road lighting, facility management and energy services for customers in Hong Kong and neighbouring areas. Our energy services include energy audit, fuel switching, power quality improvement and chiller enhancement works. We also maintain electrical systems in the Passenger Terminal Building, the sea water pumping stations, fixed ground power installation and road lighting for the Airport Authority.

Table of Contents

Page 13

Human Resources

On 30 June 2005, the Group employed 5,672 staff (2004: 4,678), of whom 3,829 (2004: 3,897) were employed in the electricity business in Hong Kong and 1,536 (2004: 479) by CLP Power Asia, TRUenergy and GPEC. Total remuneration for the six months ended 30 June 2005 was HK$1,223 million (2004: HK$1,246 million), including retirement benefit costs of HK$91 million for Hong Kong-based employees. The reason for the reduction in total remuneration is that, in the comparable period in 2004, special provision was made by the electricity business in Hong Kong to buyout certain work related allowances and bonuses in order to facilitate the transition to a new incentive based remuneration system.

During the first half of 2005, we have undertaken a number of key human resources initiatives.

Group-wide, the 2005 Management Development and Succession Planning process was initiated. In addition to ensuring that we have successors in place for identified key positions and Senior Management, this annual process is designed to identify new talent systematically.

As a continued effort to develop talent, we nominate high potential staff to attend Leadership Development Programs organised by reputable business schools. In 2005, nine staff have completed the Leadership Development Program organised with the Richard Ivey School of Business.

We have also continued with the CLP Internship Programme which encourages students to join CLP during summer or for a 12-month placement. Each student is assigned a specific project and a CLP manager as mentor. The programme has an excellent reputation with local universities. There are 49 students participating in this year’s programme.

With the growth of our business in the Asia-Pacific region, we have been encouraging more staff mobility across the region in order to leverage our core skills and experience, and also provide development opportunities to staff.

Safety

Table of Contents

Page 14

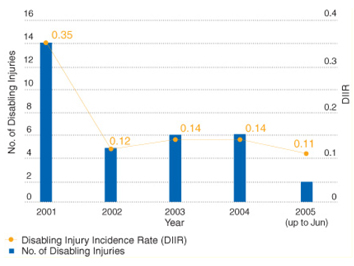

Two disabling injury incidents occurred in our Hong Kong electricity business in the first half of 2005, resulting in a disabling injury incidence rate of 0.09. On a rolling twelve months basis, the disabling injury incidence rate for the period to 30 June 2005 was 0.11, which compared favourably with that achieved for the calendar year 2004 (0.14).

During the period, significant efforts were placed on a number of safety enhancement and cultural improvement processes with the purpose of encouraging safer behaviour at work. We also continued the implementation of a Safety Incentive Scheme and a Behavior Safety Observation Scheme.

Environment

In the CLP Group’s “Manifesto on Air Quality and Climate Change” (the Manifesto) issued in December 2004, we committed to a series of initiatives in three key areas of responsible environmental management: climate change, air quality and energy conservation. We report below on our progress in each of these areas.

Climate Change

CLP undertook in the Manifesto to increase renewable energy sources to approximately 5% of the Group’s total generating capacity by 2010. In line with this commitment, CLP is investigating and investing in renewable energy projects outside of Hong Kong, focusing on wind farms and hydro schemes and with an immediate emphasis on China, Australia and India.

In June 2005, we increased our interest in the Huaiji hydro project in Guangdong, China, to 50%. A restructuring scheme is being implemented to resolve the issue of overdue electricity payment, to raise capital to complete a hydro plant being constructed and to improve the financing arrangements for the project. The scheme should put the project on a better financial standing and enable CLP to increase its ownership and exercise greater control over the project.

We have widened our partnership with a subsidiary of the China Huaneng Group on wind farm projects in China. Following our 45% investment in the 27MW wind farm at Changdao in Shandong Province, which is currently under construction, we have concluded commercial arrangements for taking a 45% interest in the 19.5MW greenfield wind project at Weihai in Shandong. Wind monitoring at various sites in Guangdong and Hainan Island is also being conducted. We are also reviewing wind farm opportunities in Australia and small hydro schemes in India.

In July 2004, CLP launched a commercial scale wind turbine pilot demonstration to investigate the economic, environmental and technical feasibility and practicality of wind energy applications in Hong Kong. This pilot study will take a commercial scale wind turbine through the full site selection and regulatory process to educate the industry and the community about wind energy applications in Hong Kong.

Through a structured site selection exercise and engagement of various stakeholders including the Government, green groups and community groups, two potential sites, namely Kau Sai Chau and Hei Ling Chau, were identified. A preferred site will be selected based on the results of the on-site wind resource measurement, engineering design and preliminary impact assessment to be conducted on both potential sites in the coming months.

Table of Contents

Page 15

The CLP-sponsored wind resource assessment for Hong Kong is nearing conclusion. This year CLP provided additional sponsorship to the same team at the Hong Kong University of Science and Technology for an assessment of the adjacent province of Guangdong.

Air Quality

We are committed to improving the environmental performance of our electricity generation activities in Hong Kong. A major environmental initiative we are planning to undertake is an Emissions Control Project at the Castle Peak B Power Station, which involves the retrofit of FGD equipment.

We have been proceeding with the necessary front-end engineering works. Technology option selection is nearing completion and we are preparing to undertake an Environmental Impact Assessment (EIA). A retrofit project such as this will involve a large amount of demolition, plant re-location, and construction works to be undertaken on an operating site. It is imperative that power generation is not disrupted throughout the project period. We are developing a project execution plan to ensure smooth and timely implementation of the project, while maintaining a reliable supply of electricity to our customers.

CLP is developing the infrastructure needed to assure the availability of LNG in Hong Kong. Preliminary site selection studies for the LNG receiving and storage terminal identified two sites which appear suitable, South Soko Island and adjacent to CAPCO’s Black Point Power Station. EIAs are underway for both sites, with anticipated completion in mid 2006.

Leading up to the EIA submission, an active public communication campaign has helped inform the public and various other stakeholders of the benefits of LNG, as well as the need for a receiving terminal and storage facility in Hong Kong. This campaign has included briefings with various stakeholders including green groups, community groups, and various government departments, advertisements, and a website. For more details, we invite you to visit our project website at www.clpgroup.com/environment/lng or phone our enquiry hotline at (852) 2678-8189.

CLP was the first company to sign the Clean Air Charter. This charter is led by the Business Coalition on the Environment, and aims to engage the business community in voluntary emissions reductions to clean up the air in Hong Kong and elsewhere in the Pearl River Delta.

Energy Conservation

In June 2005, we received our first certificate in the Hong Kong Energy Efficiency Registration Scheme for Buildings for our newly commissioned Sham Mong Road Substation. This will be adopted as the latest design standard for our future substations in Hong Kong.

CLP continued its effort in enhancing public awareness on energy savings through our school and community PowerWise outreach programmes. The PowerWise website, which passes on practical tips on wise use of energy in a fun and interactive way, has attracted about 60,000 visits from internet users.

During the first half of the year, more than 1,600 advisory services including energy audits were provided to our customers to help reduce their energy costs.

Table of Contents

Page 16

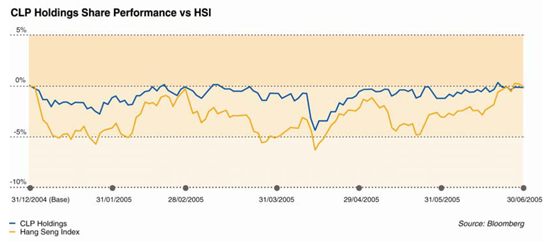

Shareholder value

During the first half of 2005, CLP’s share price was down 0.22%, whereas the Hang Seng Index (HSI) decreased by 0.20%.

The final dividends for 2004, comprising HK$0.73 per share by way of ordinary dividend and HK$0.15 per share as special dividend, were paid to Shareholders on 29 April 2005. The first interim dividend for 2005 of HK$0.48 per share was paid on 15 June 2005 and the second interim dividend of HK$0.48 per share will be paid on 15 September 2005.

Table of Contents

Page 17

The financial results for the six months ended 30 June 2005, which are unaudited but have been reviewed by the Audit Committee and our external Auditors, incorporate the following two significant changes from the corresponding period in 2004 and from the financial year ended 31 December 2004:

| 1. | The adoption of a number of new and revised Hong Kong Financial Reporting Standards (HKFRSs) and Hong Kong Accounting Standards (HKASs) issued by the Hong Kong Institute of Certified Public Accountants which become effective for accounting periods beginning on or after 1 January 2005; and |

| 2. | The consolidation of the MEB in Australia following completion of the acquisition on 31 May 2005. |

The adoption of the new accounting standards does not have material impact on earnings, but requires changes to the presentation of the profit and loss account (refer to page 27 of this Interim Report). HKAS 1 “Presentation of Financial Statements” prohibits presentation of any items of income and expense as extraordinary items and hence, the following reclassifications have been made:

| (a) | Profit from Hok Un redevelopment, previously shown as a separate line on the profit and loss account, has been grouped as part of the share of results from jointly controlled entities; |

| (b) | The transfers under the Scheme of Control (SoC) arrangement have been reclassified, namely (i) transfers from or to the Development Fund reclassified as revenue and (ii) the transfer to Rate Reduction Reserve (i.e. 8% interest on the average Development Fund balance) reclassified as finance costs. |

For the balance sheet (refer to page 28 of this Report), the major changes are:

| (a) | Leasehold land is now shown separately from fixed assets; |

| (b) | Negative goodwill of HK$1,046 million recognised to 2004 has been credited to the opening balance of retained profits; |

| (c) | Mark-to-market value of all derivative and energy trading instruments, which previously were not allowed for recognition, are now recognised; and |

| (d) | GPEC’s discounted bills with recourse, which were previously treated as contingent liabilities, have been accounted for as a collateralised borrowing starting 2005. The Group has no material contingent liabilities as at 30 June 2005. |

As the acquisition of the MEB was only completed on 31 May 2005, the one-month post-acquisition profit of HK$6 million, which was affected by seasonal factors in Australia and non-recurring expenses associated with the acquisition and re-branding exercise, did not make a significant contribution to earnings. However, the consolidation of the MEB’s net assets did have a significant impact on the consolidated balance sheet. These are described in more details under the “Group’s Financial Position” section.

Table of Contents

Page 18

Consolidated Financial Results

Revenue

During the six-month period to 30 June 2005, our revenue registered a 13.8% increase to HK$16,626 million (2004: HK$14,615 million). Our businesses in Hong Kong and Australia contributed to this growth.

Revenue from our electricity business in Hong Kong recorded a 8.6% growth to HK$13,638 million (2004: HK$12,563 million). The increase was mainly due to higher unit sales and increased fuel clause revenue. The transfer from the Development Fund, which is an adjustment under the SoC, has now been reclassified as revenue which amounted to HK$338 million (2004: HK$693 million, including HK$96 million transferred from the special provision account).

Revenue from our energy businesses outside Hong Kong amounted to HK$2,922 million (2004: HK$1,966 million), with the increase mainly resulting from the incorporation of the MEB’s revenue of HK$935 million for the one-month post-acquisition period.

Group Earnings

Total operating earnings were HK$4,403 million, which was HK$389 million higher than the corresponding period last year, representing an increase of 9.7%. Total earnings, which include Hok Un redevelopment profit, increased by 10.6% to HK$4,577 million.

Our electricity business in Hong Kong continues to provide stable earnings growth, with earnings increasing by 5.2% to HK$3,510 million. This resulted from the combined effect of ongoing investments in fixed assets to meet new customer demands and to improve quality of services.

Earnings from other energy businesses and investments rose 27.7% to HK$1,010 million, reflecting improved contributions from our overseas businesses and investments in the energy sector and reduction in losses from non-energy activities particularly after the withdrawal from telecommunication business in 2004.

Earnings from investments in GNPJVC and PSDC increased from HK$380 million to HK$431 million due to increased generation from continuous high performance of the nuclear plant. Earnings from other investments in the Chinese mainland continued to be adversely affected by high coal costs, and were lower than last year when the write-off of financing charges related to the Shandong project loans was excluded.

Our energy businesses in the Asia-Pacific region recorded an earnings growth of 5.2% to HK$425 million, with contributions mainly coming from GPEC, India. Contributions from our Australian business during the six-month period to 30 June 2005 had been affected by the one-off swap breakage cost associated with the refinancing of Yallourn Energy’s loans. With the progressive integration of Yallourn Energy and MEB, we expect to have a meaningful contribution from this segment in the second half of the year.

Table of Contents

Page 19

The contribution of each major activity to the Group earnings is analysed as follows:

| 6 months ended 30 June | ||||||||||||||

| 2005 | 2004 | Increase | ||||||||||||

| HK$M | HK$M | HK$M | HK$M | % | ||||||||||

Earnings from electricity business in Hong Kong | 3,510 | 3,337 | 5.2 | |||||||||||

Electricity sales to Chinese mainland from Hong Kong | 63 | 30 | ||||||||||||

Generating facilities in Chinese mainland serving Hong Kong (GNPJVC & PSDC) | 431 | 380 | ||||||||||||

Other power projects in Chinese mainland | 95 | 43 | ||||||||||||

Energy businesses in Asia-Pacific region | 425 | 404 | ||||||||||||

Group non-energy activities | (4 | ) | (66 | ) | ||||||||||

Earnings from other investments / activities | 1,010 | 791 | 27.7 | |||||||||||

Unallocated net finance costs | (43 | ) | (39 | ) | ||||||||||

Unallocated Group expenses | (74 | ) | (75 | ) | ||||||||||

Total operating earnings | 4,403 | 4,014 | 9.7 | |||||||||||

Hok Un redevelopment profit | 174 | 124 | ||||||||||||

Group earnings attributable to shareholders | 4,577 | 4,138 | 10.6 | |||||||||||

Weighted average number of shares in issue, million shares | 2,408.25 | 2,408.25 | ||||||||||||

Earnings per share, HK$ | ||||||||||||||

Including Hok Un redevelopment profit | 1.90 | 1.72 | 10.6 | |||||||||||

Excluding Hok Un redevelopment profit | 1.83 | 1.67 | 9.7 | |||||||||||

Earnings per share increased by 10.6% when compared to the corresponding period in 2004. Excluding the Hok Un redevelopment profit, earnings per share increased by 9.7%.

Group’s Financial Position

The Group has a strong balance sheet, with total assets as at 30 June 2005 amounting to HK$98,738 million (December 2004: HK$80,799 million). The increase of HK$17,939 million was mainly due to the consolidation of the newly acquired MEB. The acquisition gave rise to a significant increase on items such as fixed assets, derivative instruments, and trade and other receivables and reduction of deferred tax assets after offsetting by the assumed deferred tax liabilities. Goodwill and other intangible assets arising from this acquisition totalled HK$6,974 million. As the acquisition was completed only one month prior to the balance sheet date, the fair values assigned to the identifiable assets and liabilities are provisional only. Further work will be carried out in the coming months before the end of 2005 to refine the fair value allocation and therefore may result in a corresponding adjustment to goodwill.

Table of Contents

Page 20

Our total assets, which comprise primarily fixed and intangible assets as well as investments in jointly controlled entities and associated companies, analysed by principal activities, are as follows:

| 30 June 2005 | 31 December 2004 | |||||||

HK$M

| %

| HK$M

| %

| |||||

Energy businesses / investments in | ||||||||

Hong Kong | 53,057 | 53 | 50,710 | 63 | ||||

Asia-Pacific region | 38,251 | 39 | 22,468 | 28 | ||||

Chinese mainland | 6,722 | 7 | 6,858 | 8 | ||||

| 98,030 | 99 | 80,036 | 99 | |||||

Property and other businesses | 708 | 1 | 763 | 1 | ||||

| 98,738 | 100 | 80,799 | 100 | |||||

Total bank loans and other borrowings, which excluded the obligations under finance leases, increased from HK$18,774 million to HK$30,967 million. Details of the Group’s borrowings are provided in the “Financing” section.

Business Acquisitions and Developments

On 31 May 2005, we completed the acquisition of the MEB (except for the interest on SEAGas partnership) in Australia for a purchase consideration of HK$11,916 million. The acquisition was funded from internal resources as well as new financing facilities which are discussed further in the “Financing” section. With respect to the acquisition of Singapore Power’s interest in SEAGas partnership, all necessary third party consents were obtained and the acquisition was completed on 29 August 2005. The consideration for this acquisition was A$195 million, of which a deposit of A$75 million (approximately HK$448 million) was paid prior to 30 June 2005.

Pursuant to the Equity Contribution Agreement and its amendment agreement relating to the BLCP power project of Thailand, we are required to make further equity contributions of US$148 million by 2007.

For our investments in the Chinese mainland, we made capital contributions of RMB27 million (approximately HK$25 million) to a wind power project in Changdao and advances of RMB131 million (approximately HK$123 million) to a coal-fired power project in Fangchenggang during the first half of 2005. Further equity contributions of RMB18 million and RMB966 million are expected to be made by the end of this year for the Changdao project and by 2007 for the Fangchenggang project respectively. We also entered into a joint venture to develop another wind project in Weihai and are required to make an equity contribution of RMB30 million by 2006. We increased our shareholding in the hydro power stations in Huaiji, Guangdong, through an acquisition of the interest held by Sun Hung Kai China Development Fund Limited. The acquisition, at a consideration of HK$53 million, was completed on 30 June 2005.

Table of Contents

Page 21

Fixed Assets and Capital Expenditure

Fixed assets and leasehold land of the Group totalled HK$63,976 million as at 30 June 2005, comprising mainly the investments in the transmission and distribution network for our core Hong Kong electricity business of HK$43,296 million (December 2004: HK$42,415 million) and in the generating facilities of overseas subsidiaries of HK$20,502 million (December 2004: HK$15,147 million). During the six-month period, we invested HK$2,179 million (2004: HK$2,637 million), of which HK$1,911 million (2004: HK$2,313 million) was made by CLP Power Hong Kong, in various fixed assets (including payments for lease premium for land). Capital expenditure by CAPCO for the six months was HK$619 million (2004: HK$829 million).

Capital expenditure contracted, but not provided for in the accounts, as at 30 June 2005 amounted to HK$2,300 million (December 2004: HK$2,207 million). Other than HK$377 million (December 2004: HK$240 million) which was for our overseas subsidiaries, these contracted amounts are primarily for enhancing our transmission and distribution systems in Hong Kong.

Liquidity and Capital Resources

As at 30 June 2005, we had liquid funds of HK$1,932 million (December 2004: HK$2,520 million), of which 94% was denominated in foreign currency mainly held by overseas subsidiaries in India and Australia. The remainder was in Hong Kong dollars.

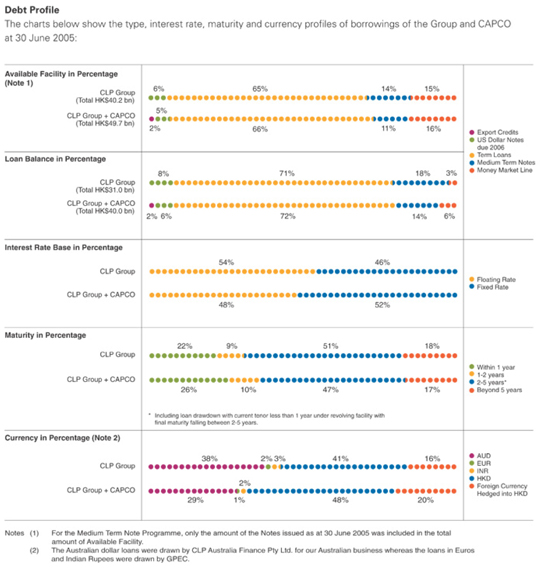

We strive to maintain an appropriate mix of committed and uncommitted facilities and solicit our facilities from a pool of financial institutions with strong credit standing. As at 30 June 2005, financing facilities totalling HK$40.2 billion were available to the Group, including HK$15.6 billion for overseas subsidiaries. Of the available facilities, HK$31.0 billion had been drawn down, of which HK$13.2 billion was by overseas subsidiaries. Facilities totalling HK$9.5 billion were available to CAPCO, of which HK$9.0 billion had been drawn down. The debts of overseas subsidiaries are without recourse to CLP Holdings. Of these borrowings, HK$716 million as at 30 June 2005 are secured by fixed and floating charges over the assets of GPEC.

Our total debt to total capital as at 30 June 2005 was 41.3% and interest cover for the six months ended 30 June 2005 was 10 times.

Financing

The Group engaged in new financing activities in the first half of 2005 to support the continuous expansion of electricity business in Hong Kong and acquisition of the MEB in Australia. We continue to adopt a prudent approach to all our financial arrangements, while at the same time aiming to achieve cost effective funding.

In April 2005, CLP Holdings completed a HK$6 billion self-arranged medium term loan facility with 15 international banks. CLP Holdings increased the limit of this loan arrangement to HK$6 billion from the original target of HK$4 billion upon favourable responses from the financial market, and utilised a HK$2 billion commitment amount to replace a higher-priced tranche of its existing loan facility. A portion of the financing was also used to fund part of the equity contribution related to the acquisition of the MEB. The new loan facility should provide CLP Holdings with ample liquidity to meet its investment needs over the next few years.

Table of Contents

Page 22

CLP Australia Finance Pty Ltd. (CLP Australia Finance), a wholly-owned subsidiary in Australia, completed a A$2.2 billion unsecured corporate loan facility and a A$250 million working capital facility in May 2005. The facilities were used to fund the balance of the purchase consideration payable upon the acquisition of the MEB, refinance the existing Yallourn Energy’s project finance facilities, and fund the working capital requirements for our business in Australia. The loans are non-recourse to CLP Holdings and Standard & Poor’s (S&P) has assigned its “A-” credit rating to the A$2.2 billion unsecured debt facilities with stable outlook.

In January and June 2005, CLP Power Hong Kong issued two tranches of fixed rate notes due 2015 of HK$500 million each, with coupon rates at 4.35% and 4.15% respectively, through its wholly-owned subsidiary CLP Power Hong Kong Financing Limited. These issues were made under the Medium Term Note (MTN) Programme set up by CLP Power Hong Kong Financing Limited in 2002. Under the MTN Programme, notes in an aggregate amount of up to US$1.5 billion may be issued and will be unconditionally and irrevocably guaranteed by CLP Power Hong Kong. As at 30 June 2005, nominal value of about HK$5,340 million notes have been issued under the MTN Programme.

Table of Contents

Page 23

Credit Rating

In May 2005, S&P lowered the foreign currency and local currency corporate credit rating of CLP Holdings to “A” from “A+”. S&P’s downgrade of CLP Holdings’ rating reflects its view of CLP Holdings’ increasing business risk as a result of our international diversification efforts over the past few years and the increased level of debt following the acquisition of the MEB in Australia. At the same time, S&P affirmed its “A+” foreign currency and local currency credit rating on CLP Power Hong Kong. S&P noted that although the SoC was likely to be renegotiated with a potential lower rate of return, it expected that CLP Power Hong Kong’s market position and financial performance would remain strong.

In addition to CLP Holdings and CLP Power Hong Kong, S&P also assigned its “A-” long-term credit rating to two of our Australian subsidiaries, namely CLP Australia Holdings Pty Ltd. and TRUenergy Pty Ltd. in May 2005. The outlook for all ratings is stable.

Moody’s re-affirmed the foreign currency rating of CLP Holdings and CLP Power Hong Kong unchanged at “A1” in May 2005 and at the same time revised downward the local currency issuer rating of CLP Holdings and CLP Power Hong Kong to “A1” and “Aa3” from “Aa2” and “Aa1” respectively. This puts CLP Power Hong Kong on par with the HKSAR’s local currency rating of “Aa3”. The outlook for the ratings is stable. Moody’s downgrade reflected its view of the increased overall business risk profile and financial leverage of CLP Holdings after the acquisition of the Australian MEB. At the same time, Moody’s continued to recognise the key credit strengths of strong and highly predictable cash flow generated from CLP Power Hong Kong, management’s gradual approach to overseas expansion, and CLP Group’s strong access to bank and capital markets. Both Moody’s and S&P consider CLP Power Hong Kong to be an integral part of CLP Holdings with both ratings closely linked.

In July 2005, Moody’s upgraded the foreign currency bond rating of CLP Power Hong Kong to “Aa3” from “A1” based on the view that foreign currency bonds subject to international law are less likely to be subject to a debt moratorium than foreign currency obligations subject to local law and hence the differential in the ratings on foreign currency bond and foreign currency issuer ratings.

Separately, Fitch affirmed its self-initiated foreign currency and local currency ratings of CLP Holdings and CLP Power Hong Kong at “A+” with stable outlook in March 2005.

The credit ratings of major companies within the Group as at 30 June 2005 are summarised below. All ratings remain at investment grade which can facilitate and enhance our position in local and overseas business activities, including fund raising, investment and new business opportunities.

| CLP Holdings | CLP Power Hong Kong | CLP Australia Holdings | HKSAR Government 1 | |||||||||||

S&P

| Moody’s

| S&P

| Moody’s

| S&P

| S&P

| Moody’s

| ||||||||

| Long-term Rating | ||||||||||||||

Foreign Currency | A | A1 | A+ | A1 | A- | AA- | A1 | |||||||

Outlook | Stable | Stable | Stable | Stable | Stable | Stable | Stable | |||||||

Local Currency | A | A1 | A+ | Aa3 | A- | AA- | Aa3 | |||||||

Outlook | Stable | Stable | Stable | Stable | Stable | Stable | Stable | |||||||

| Short-term Rating | ||||||||||||||

Foreign Currency | A-1 | P-1 | A-1 | P-1 | — | A-1+ | P-1 | |||||||

Local Currency | A-1 | — | A-1 | — | — | A-1+ | — | |||||||

| 1 | rating updated as at 20 July 2005 |

Table of Contents

Page 24

Risk Management

The Group’s investments and operations have resulted in exposures to foreign currency risks, interest rate risks, credit risks and price risks associated with the sales and purchases of electricity in Australia. We actively manage such risks by using different derivative instruments with an objective to minimise the impact of exchange rate, interest rate and electricity price fluctuations on earnings, reserves and tariff charges to customers and monitor our risk exposures with the assistance of “Value-at-Risk” (VaR) methodology. VaR is a risk measurement that probabilistically calculates the market risk of a portfolio using historical volatility over a defined holding period. Other than certain electricity trading activities engaged by our Australian business, all derivative instruments are employed solely for hedging purposes.

Foreign Currency Risks

The Group’s foreign currency exposures primarily arise from CLP Power Hong Kong’s significant foreign currency obligations related to its U.S. dollar-denominated debt, nuclear power purchase off-take commitments, fuel and other purchase-related payments and CLP Power Asia’s investments abroad.

In order to mitigate the potential impact of foreign currency movement on electricity tariff in Hong Kong, CLP Power Hong Kong continues to hedge a significant portion of its U.S. dollar obligations, provided that the hedging can be accomplished at rates below the Government’s target peg rate of 7.80. We will review this policy periodically in light of changing market conditions to optimise benefits.

For investments overseas, we do not hedge translation exposure arising from consolidation of the Group’s net assets outside Hong Kong because the investments are long-term and effective hedging instruments are either limited or costly. The translation gains or losses do not affect the Group’s cash flow or earnings until an investment is sold. Our primary foreign exchange risk is at the individual project company level where non-functional currency exposures, if not managed properly, can lead to significant financial distress. Therefore, our primary risk mitigation is to ensure that project-level debt financings are implemented on a local currency basis to the maximum extent possible. Certain investments have incorporated direct and indirect indexation in their project agreements to reduce earnings impact from foreign exchange fluctuation.

Interest Rate Risks

The Group utilises fixed rate borrowings and interest rate swaps to mitigate the impact of interest rate volatility on current and future corporate profitability.

CLP Power Hong Kong conducts annual reviews to determine a preferred fixed/floating interest rate mix appropriate for its business profile. For the Group’s overseas investments, each project company has developed its own hedging program taking into consideration project debt service sensitivities to interest rate movements, lender requirements, tax and accounting implications.

In May 2005, Yallourn Energy closed out all its interest rate swaps upon completion of its project debt refinancing by new credit facilities at CLP Australia Finance. To mitigate its interest rate exposure arising from the new borrowings, CLP Australia Finance entered into interest rate swaps with notional amount totalled A$1.2 billion to convert part of its floating interest rate obligations into fixed rate.

Table of Contents

Page 25

Credit Risks

All finance-related hedging transactions and deposits of CLP Holdings and its principal subsidiaries are made with counter-parties with acceptable credit rating to minimise credit exposure. The Group assigns limits to its counter-parties and monitors potential exposures to each counter-party utilising the VaR methodology. All derivative transactions are entered into at the sole credit of the respective subsidiaries and affiliates and the counter-parties have no recourse to CLP Holdings for any change in the market value of derivatives.

Electricity Sales and Purchases Risks

There are risks in the Australian energy sector resulting from price volatility and the possibility of continuing low pool prices in Australia’s National Electricity Market (NEM). Our operating companies in Australia have entered into energy contracts, including forward electricity pricing contracts, swaps and options contracts to help reduce the impact on earnings of the volatility of NEM pool prices. They have engaged in energy trading activities and all trading and marketing activities are conducted within a clear and appropriate risk management framework.

The successful acquisition of the MEB in May 2005 takes the Group from ownership of a single electricity generating asset towards a broader-based vertically integrated Australian energy business with significant access to the retail gas and electricity market. The resulting combination of generation and retail should provide a natural hedge that can significantly reduce the potential impacts of volatile and cyclical wholesale pool prices.

Derivative Instruments

As at 30 June 2005, the Group had gross outstanding derivative instruments amounting to HK$71.6 billion. The fair value of these derivative instruments was at a net surplus of HK$90 million, which represents the net amount we would receive if these contracts were closed out on 30 June 2005. The significant change in fair value from net deficit of HK$1,199 million as at 31 December 2004 is primarily attributed to the strengthening of U.S. dollar in the forward currency markets in the first half of 2005.

The breakdown by type and maturity profile of the Group’s derivative instruments are shown below:

Type | ||||||||||

| Notional Amount | Fair Value Gain/(Loss) 1 | |||||||||

| 30 June 2005 | 31 December 2004 | 30 June 2005 | | 31 December 2004 | | |||||

| HK$M | HK$M | HK$M | HK$M | |||||||

CLP Group | ||||||||||

Forward Foreign Exchange Contracts | 42,593 | 44,961 | (231 | ) | (1,192 | ) | ||||

Interest Rate Swaps | 9,509 | 16,295 | (105 | ) | (358 | ) | ||||

Currency Swaps & Collars | 4,681 | 4,680 | 187 | 255 | ||||||

Energy Hedging & Trading Options | 1,131 | 48 | (2 | ) | — | |||||

Energy Hedging & Trading Swap Contracts | 13,669 | 2,330 | 241 | 96 | ||||||

| 71,583 | 68,314 | 90 | (1,199 | ) | ||||||

CAPCO | ||||||||||

Interest Rate Swaps | 4,293 | 4,378 | (85 | ) | (253 | ) | ||||

Total | 75,876 | 72,692 | 5 | (1,452 | ) | |||||

| 1 | 2004 comparative figures are not provided in the condensed consolidated interim accounts as HKAS 39 “Financial Instruments: Recognition and Measurement” prescribes the recognition of derivatives at fair value in the balance sheet to take effect prospectively from 1 January 2005. |

Table of Contents

Page 26

Maturity Profile

With the adoption of HKAS 39 “Financial Instruments: Recognition and Measurement” in 2005, all derivatives are required to be recognised in the balance sheet at their fair value. The fair value of derivatives as at 31 December 2004 had been recognised as assets or liabilities on 1 January 2005. Subsequent changes in fair value of the derivatives will have no impact on the Group’s cash flow until settlement as these are non-cash items.

Table of Contents

Page 27

Condensed Consolidated Profit And Loss Account

| (Unaudited) 6 months ended 30 June | | |||||||

| Note | 2005 HK$M | | 2004 HK$M | | ||||

| (Restated) | ||||||||

Revenue | 5,6 | 16,626 | 14,615 | |||||

Expenses | ||||||||

Purchases of electricity and gas | 27 | 8,613 | 7,630 | |||||

Staff expenses | 665 | 648 | ||||||

Fuel and other operating costs | 1,976 | 1,493 | ||||||

Depreciation and amortisation | 1,359 | 1,219 | ||||||

| 12,613 | 10,990 | |||||||

Operating profit | 6,7 | 4,013 | 3,625 | |||||

Finance costs | 8 | (725 | ) | (595 | ) | |||

Finance income | 8 | 63 | 23 | |||||

Share of results, net of tax | ||||||||

jointly controlled entities | 9, 16 | 1,614 | 1,541 | |||||

associated companies | 9, 17 | 79 | 116 | |||||

Profit before taxation | 5,044 | 4,710 | ||||||

Taxation | 10 | (467 | ) | (572 | ) | |||

Earnings attributable to shareholders | 11 | 4,577 | 4,138 | |||||

Dividends | 12 | |||||||

First interim paid | 1,156 | 1,084 | ||||||

Second interim proposed | 1,156 | 1,084 | ||||||

| 2,312 | 2,168 | |||||||

Earnings per share | 13 | HK$1.90 | HK$1.72 | |||||

Table of Contents

Page 28

Condensed Consolidated Balance Sheet

| (Unaudited) 30 June 2005 | | (Restated) 31 December 2004 | | |||||

| Note | HK$M | HK$M | ||||||

Non-current assets | ||||||||

Fixed assets | 14 | 61,758 | 55,508 | |||||

Leasehold land | 14 | 2,218 | 2,240 | |||||

Goodwill and other intangible assets | 15 | 6,961 | (1,022 | ) | ||||

Investments in jointly controlled entities | 16 | 14,886 | 14,998 | |||||

Investments in associated companies | 17 | 1,596 | 1,640 | |||||

Deferred tax assets | 368 | 1,043 | ||||||

Derivative instruments | 18 | 472 | — | |||||

Other non-current assets | 459 | 9 | ||||||

| 88,718 | 74,416 | |||||||

Current assets | ||||||||

Inventories – stores and fuel | 659 | 299 | ||||||

Trade and other receivables | 19 | 6,559 | 3,564 | |||||

Derivative instruments | 18 | 870 | — | |||||

Bank balances, cash and other liquid funds | 20 | 1,932 | 2,520 | |||||

| 10,020 | 6,383 | |||||||

Current liabilities | ||||||||

Customers’ deposits | (3,223 | ) | (3,119 | ) | ||||

Fuel clause account | (460 | ) | (762 | ) | ||||

Trade and other payables | 21 | (4,915 | ) | (4,216 | ) | |||

Taxation payable | (662 | ) | (403 | ) | ||||

Short-term loans and current portion of long-term borrowings | 22 | (7,023 | ) | (1,178 | ) | |||

Derivative instruments | 18 | (586 | ) | — | ||||

| (16,869 | ) | (9,678 | ) | |||||

Net current liabilities | (6,849 | ) | (3,295 | ) | ||||

Total assets less current liabilities | 81,869 | 71,121 | ||||||

Table of Contents

Page 29

Condensed Consolidated Balance Sheet (continued)

| (Unaudited) 30 June 2005 | (Restated) 31 December 2004 | |||||

| Note | HK$M | HK$M | ||||

Financed by: | ||||||

Equity | ||||||

Share capital | 23 | 12,041 | 12,041 | |||

Share premium | 1,164 | 1,164 | ||||

Reserves | ||||||

Proposed dividends | 1,156 | 2,119 | ||||

Others | 31,896 | 28,875 | ||||

Shareholders’ funds | 46,257 | 44,199 | ||||

Non-current liabilities | ||||||

Long-term borrowings | 22 | 25,479 | 17,596 | |||

Deferred tax liabilities | 5,115 | 5,084 | ||||

Derivative instruments | 18 | 666 | — | |||

Scheme of Control (SoC) reserve accounts | 24 | 3,338 | 3,720 | |||

Other non-current liabilities | 1,014 | 522 | ||||

| 35,612 | 26,922 | |||||

Equity and non-current liabilities | 81,869 | 71,121 | ||||

/s/ W. E. Mocatta | /s/ Andrew Brandler | /s/ Peter P. W. Tse | ||

W. E. Mocatta Vice Chairman | Andrew Brandler Group Managing Director & Chief Executive Officer | Peter P. W. Tse Group Executive Director & Chief Financial Officer | ||

| Hong Kong, 23 August 2005 | ||||

Table of Contents

Page 30

Condensed Consolidated Statement of Changes in Equity

(Unaudited) | Share Capital | Share Premium | Capital Redemption Reserve | Other Reserves | | Retained Profits | | Total | |||||||

| HK$M | HK$M | HK$M | HK$M | HK$M | HK$M | ||||||||||

Balance as at 1 January 2005, as previously reported | 12,041 | 1,164 | 2,482 | 830 | 27,682 | 44,199 | |||||||||

Adjustments for adoption of new HKFRSs | |||||||||||||||

Negative goodwill (HKFRS 3) (Notes 3,15) | — | — | — | — | 1,046 | 1,046 | |||||||||

Derivative instruments (HKAS 39) (Note 3) | — | — | — | (99 | ) | 83 | (16 | ) | |||||||

Balance as at 1 January 2005, as restated | 12,041 | 1,164 | 2,482 | 731 | 28,811 | 45,229 | |||||||||

Exchange differences on translation of: | |||||||||||||||

subsidiaries | — | — | — | (200 | ) | — | (200 | ) | |||||||

jointly controlled entities | — | — | — | (6 | ) | — | (6 | ) | |||||||

associated companies | — | — | — | (98 | ) | — | (98 | ) | |||||||

designated hedges | — | — | — | (6 | ) | — | (6 | ) | |||||||

Net losses not recognised in the profit and loss account | — | — | — | (310 | ) | — | (310 | ) | |||||||

Cash flow hedges, net of tax | — | — | — | 65 | — | 65 | |||||||||

Earnings for the period | — | — | — | — | 4,577 | 4,577 | |||||||||

Dividends paid | |||||||||||||||

2004 finals | — | — | — | — | (2,119 | ) | (2,119 | ) | |||||||

2005 interim | — | — | — | — | (1,156 | ) | (1,156 | ) | |||||||

Capital redemption by a subsidiary | — | — | — | 417 | (417 | ) | — | ||||||||

Share of movements in reserves of | |||||||||||||||

jointly controlled entities | — | — | — | (9 | ) | (14 | ) | (23 | ) | ||||||

associated company | — | — | — | (6 | ) | — | (6 | ) | |||||||

Balance as at 30 June 2005 | 12,041 | 1,164 | 2,482 | 888 | 29,682 | (a) | 46,257 | ||||||||

Company and subsidiaries | 12,041 | 1,164 | 2,482 | 846 | 25,821 | 42,354 | |||||||||

Jointly controlled entities | — | — | — | 35 | 3,233 | 3,268 | |||||||||

Associated companies | — | — | — | 7 | 628 | 635 | |||||||||

Balance as at 30 June 2005 | 12,041 | 1,164 | 2,482 | 888 | 29,682 | 46,257 | |||||||||

Balance as at 1 January 2004 | 12,041 | 1,164 | 2,482 | 387 | 24,167 | 40,241 | |||||||||

Exchange differences on translation of: | |||||||||||||||

subsidiaries | — | — | — | (341 | ) | — | (341 | ) | |||||||

jointly controlled entities | — | — | — | 49 | — | 49 | |||||||||

associated company | — | — | — | (49 | ) | — | (49 | ) | |||||||

designated hedges | — | — | — | 279 | — | 279 | |||||||||

Net losses not recognised in the profit and loss account | — | — | — | (62 | ) | — | (62 | ) | |||||||

Earnings for the period | — | — | — | — | 4,138 | 4,138 | |||||||||

Dividends paid | |||||||||||||||

2003 finals | — | — | — | — | (1,806 | ) | (1,806 | ) | |||||||

2004 interim | — | — | — | — | (1,084 | ) | (1,084 | ) | |||||||

| Share of movements in reserves of | |||||||||||||||

jointly controlled entities | — | — | — | 20 | (19 | ) | 1 | ||||||||

associated company | — | — | — | (25 | ) | — | (25 | ) | |||||||

Balance as at 30 June 2004 | 12,041 | 1,164 | 2,482 | 320 | 25,396 | (b) | 41,403 | ||||||||

Company and subsidiaries | 12,041 | 1,164 | 2,482 | 238 | 21,943 | 37,868 | |||||||||

Jointly controlled entities | — | — | — | 62 | 2,956 | 3,018 | |||||||||

Associated company | — | — | — | 20 | 497 | 517 | |||||||||

Balance as at 30 June 2004 | 12,041 | 1,164 | 2,482 | 320 | 25,396 | 41,403 | |||||||||

Notes:

| (a) | The proposed interim dividend as at 30 June 2005 and balance of retained profits after the proposed interim dividend were HK$1,156 million and HK$28,526 million respectively. |

| (b) | The proposed interim dividend as at 30 June 2004 and balance of retained profits after the proposed interim dividend were HK$1,084 million and HK$24,312 million respectively. |

Table of Contents

Page 31

Condensed Consolidated Cash Flow Statement

(Unaudited) 6 months ended 30 June | ||||||||||||||

| 2005 | 2004 | |||||||||||||

| Note | HK$M | HK$M | HK$M | HK$M | ||||||||||

Operating activities | ||||||||||||||

Net cash inflow from operations | 25 | 3,933 | 3,826 | |||||||||||

Operating interest paid | (408 | ) | (405 | ) | ||||||||||

Interest received | 64 | 19 | ||||||||||||

Profits tax paid | (170 | ) | (139 | ) | ||||||||||

Net cash inflow from operating activities | 3,419 | 3,301 | ||||||||||||

Investing activities | ||||||||||||||

Capital expenditure | (2,617 | ) | (2,825 | ) | ||||||||||

Capitalised interest paid | (143 | ) | (150 | ) | ||||||||||

Proceeds from disposal of fixed assets | 4 | 10 | ||||||||||||

Proceeds from disposal of other investments | — | 31 | ||||||||||||

Net cash outflow for acquisition of a subsidiary | (11,318 | ) | — | |||||||||||

Acquisition of remaining interest in a subsidiary | — | (376 | ) | |||||||||||

Net cash inflow on settlement of forward contracts for investment hedging | — | 86 | ||||||||||||

Investments in and advances to jointly controlled entities | (42 | ) | (220 | ) | ||||||||||

Dividends received from investments | ||||||||||||||

- jointly controlled entities | 1,639 | 1,855 | ||||||||||||

- associated company | 31 | 30 | ||||||||||||

Net cash outflow from investing activities | (12,446 | ) | (1,559 | ) | ||||||||||

Net cash (outflow)/inflow before financing activities | (9,027 | ) | 1,742 | |||||||||||

Financing activities | ||||||||||||||

Proceeds from long-term borrowings | 14,181 | 2,200 | ||||||||||||

Repayment of long-term borrowings | (6,103 | ) | (1,692 | ) | ||||||||||

Increase in short-term borrowings | 3,644 | 1,127 | ||||||||||||

Dividends paid | (3,275 | ) | (2,890 | ) | ||||||||||

Net cash inflow/(outflow) from financing activities | 8,447 | (1,255 | ) | |||||||||||

Net (decrease)/increase in cash and cash equivalents | (580 | ) | 487 | |||||||||||