Exhibit 99.1

Getty Realty

Investor Presentation

Safe Harbor Statement

Certain statements in this Presentation constitute “forward-looking statements” within the meaning of the federal securities laws. Forward-looking statements are statements that relate to management’s expectations or beliefs, future plans and strategies, future financial performance and similar expressions concerning matters that are not historical facts. In some cases, you can identify forward-looking statements by the use of forward-looking terminology such as “may,” “will,” “should,” “expects,” “intends,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” or “potential.” Such forward-looking statements reflect current views with respect to the matters referred to and are based on certain assumptions and involve known and unknown risks, uncertainties and other important factors, many of which are beyond the Company’s control, that could cause the actual results, performance, or achievements of the Company to differ materially from any future results, performance, or achievement implied by such forward-looking statements.

While forward-looking statements reflect the Company’s good faith beliefs, assumptions and expectations, they are not guarantees of future performance. The Company does not undertake any obligation to publicly update or revise any forward-looking statements to reflect changes in underlying assumptions or factors, new information, data or methods, future events or other changes. Examples of forward-looking statements in this Presentation include, but are not limited to, statement(s): (a) relating to the Company’s Portfolio, Long-Term Leases and Rent Escalators, Tenant Base, Market Opportunity and Redevelopment Opportunities, (b) relating to Industry Fundamentals and (c) relating to the Company’s Balance Sheet, Dividend Growth and Investment Highlights. Other unknown or unpredictable factors could also have material adverse effects on our business, financial condition, liquidity, results of operations and prospects. For a further discussion of these and other factors that could cause the Company’s future results to differ materially from any forward-looking statements, see the Company’s Annual Report on Form 10-K for the year ended December 31, 2015 and the Company’s other filings with the SEC, including, in particular, the section entitled “Risk Factors” contained therein. In light of these risks, uncertainties, assumptions and factors, there can be no assurance that the results and events contemplated by the forward-looking statements contained in this Presentation will in fact transpire. Moreover, because the Company operates in a very competitive and rapidly changing environment, new risks are likely to emerge from time to time. Given these risks and uncertainties, potential investors are cautioned not to place undue reliance on these forward-looking statements as a prediction of future results.

Unless otherwise noted in this Presentation, all reported financial data is presented as of the year ended December 31, 2015, and all portfolio data is as of December 31, 2015. Except as required under the federal securities laws and the rules and regulations of the SEC, the Company does not undertake any obligation to release publicly any revisions to the forward-looking statements to reflect events or circumstances after the date of this Presentation or to reflect the occurrence of unanticipated events.

The information contained herein has been prepared from public and non-public sources believed to be reliable. However, the Company has not independently verified certain of the information contained herein, and does not make any representation or warranty as to the accuracy or completeness of the information contained in this Presentation.

1

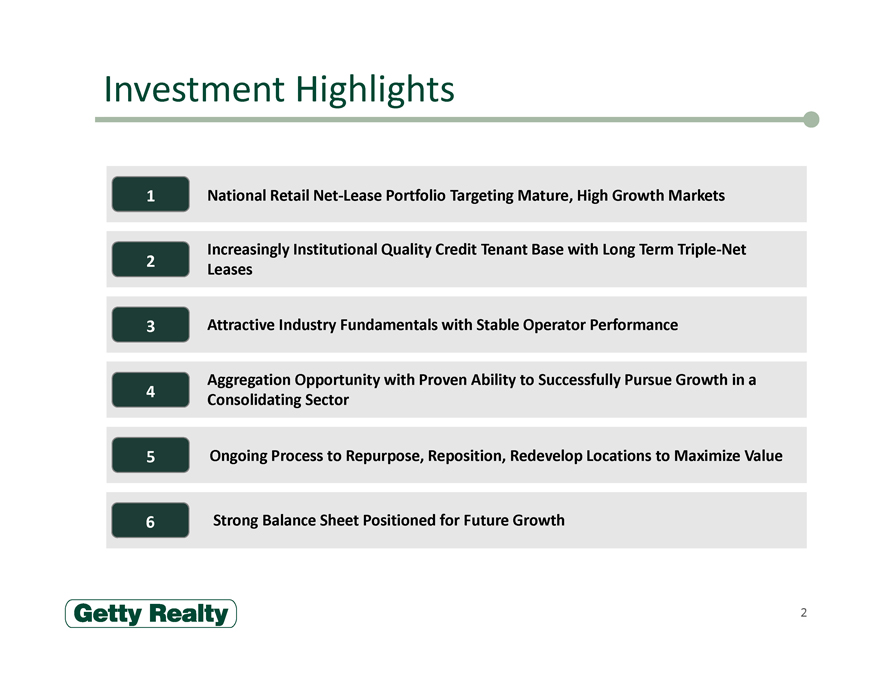

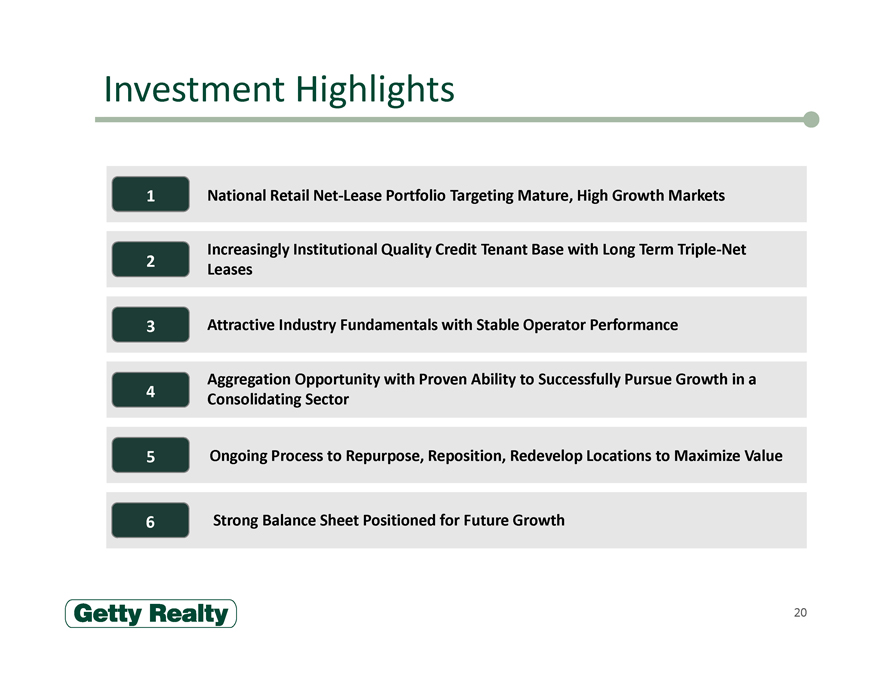

Investment Highlights

1 National Retail Net-Lease Portfolio Targeting Mature, High Growth Markets

Increasingly Institutional Quality Credit Tenant Base with Long Term Triple-Net

2 Leases

3 Attractive Industry Fundamentals with Stable Operator Performance

Aggregation Opportunity with Proven Ability to Successfully Pursue Growth in a

4 Consolidating Sector

5 Ongoing Process to Repurpose, Reposition, Redevelop Locations to Maximize Value

6 Strong Balance Sheet Positioned for Future Growth

2

Company Overview

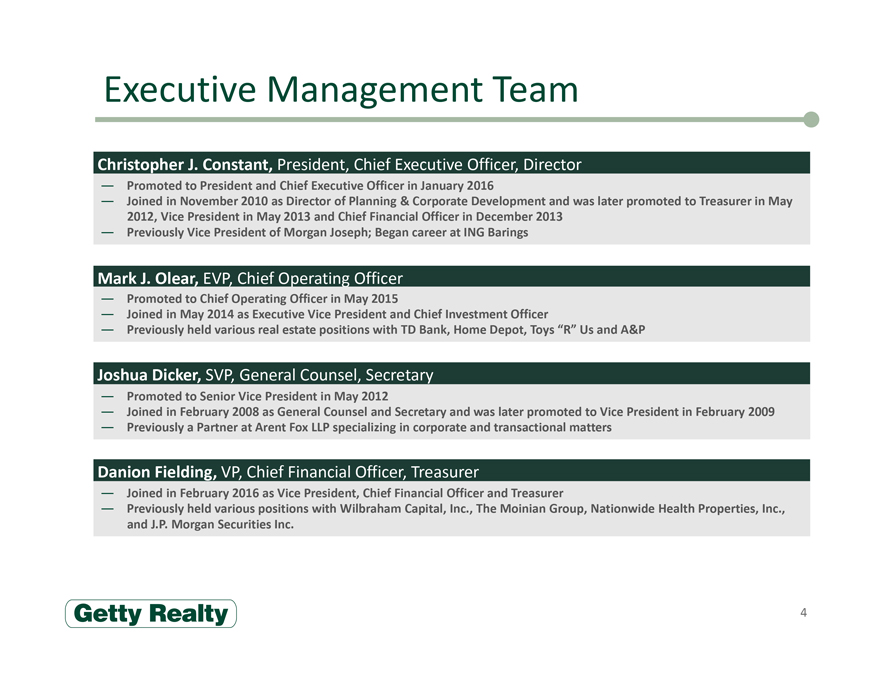

Executive Management Team

Christopher J. Constant, President, Chief Executive Officer, Director

Promoted to President and Chief Executive Officer in January 2016

Joined in November 2010 as Director of Planning & Corporate Development and was later promoted to Treasurer in May 2012, Vice

President in May 2013 and Chief Financial Officer in December 2013 Previously Vice President of Morgan Joseph; Began career at ING Barings

Mark J. Olear, EVP, Chief Operating Officer

Promoted to Chief Operating Officer in May 2015

Joined in May 2014 as Executive Vice President and Chief Investment Officer

Previously held various real estate positions with TD Bank, Home Depot, Toys “R” Us and A&P

Joshua Dicker, SVP, General Counsel, Secretary

Promoted to Senior Vice President in May 2012

Joined in February 2008 as General Counsel and Secretary and was later promoted to Vice President in February 2009 Previously a Partner at Arent Fox LLP specializing in corporate and transactional matters

Danion Fielding, VP, Chief Financial Officer, Treasurer

Joined in February 2016 as Vice President, Chief Financial Officer and Treasurer

Previously held various positions with Wilbraham Capital, Inc., The Moinian Group, Nationwide Health Properties, Inc., and J.P. Morgan Securities Inc.

4

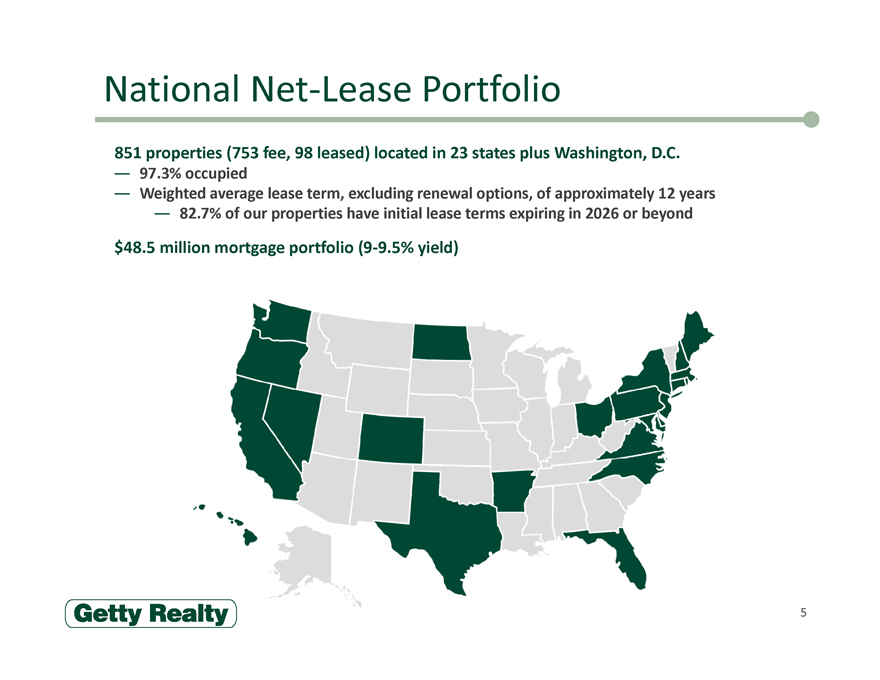

National Net-Lease Portfolio

851 properties (753 fee, 98 leased) located in 23 states plus Washington, D.C.

97.3% occupied

Weighted average lease term, excluding renewal options, of approximately 12 years

82.7% of our properties have initial lease terms expiring in 2026 or beyond

$48.5 million mortgage portfolio (9-9.5% yield)

5

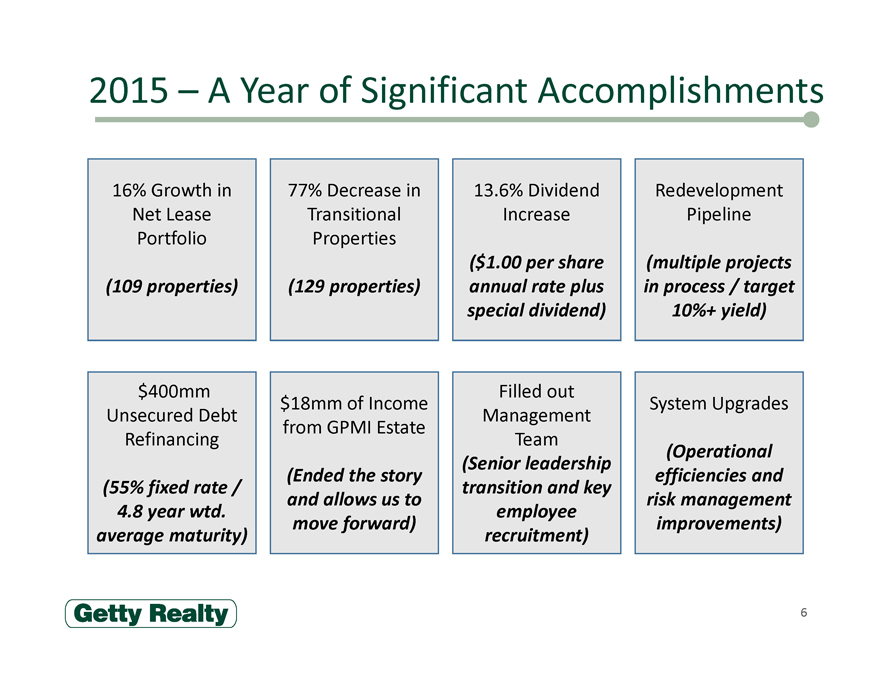

2015 – A Year of Significant Accomplishments

16% Growth in Net Lease Portfolio

(109 properties)

77% Decrease in Transitional Properties

(129 properties)

13.6% Dividend Increase

($1.00 per share annual rate plus special dividend)

Redevelopment Pipeline

(multiple projects in process / target 10%+ yield)

$400mm Unsecured Debt Refinancing

(55% fixed rate / 4.8 year wtd. average maturity)

$18mm of Income from GPMI Estate

(Ended the story and allows us to move forward)

Filled out Management Team

(Senior leadership transition and key employee recruitment)

System Upgrades

(Operational efficiencies and risk management improvements)

6

Investment Overview

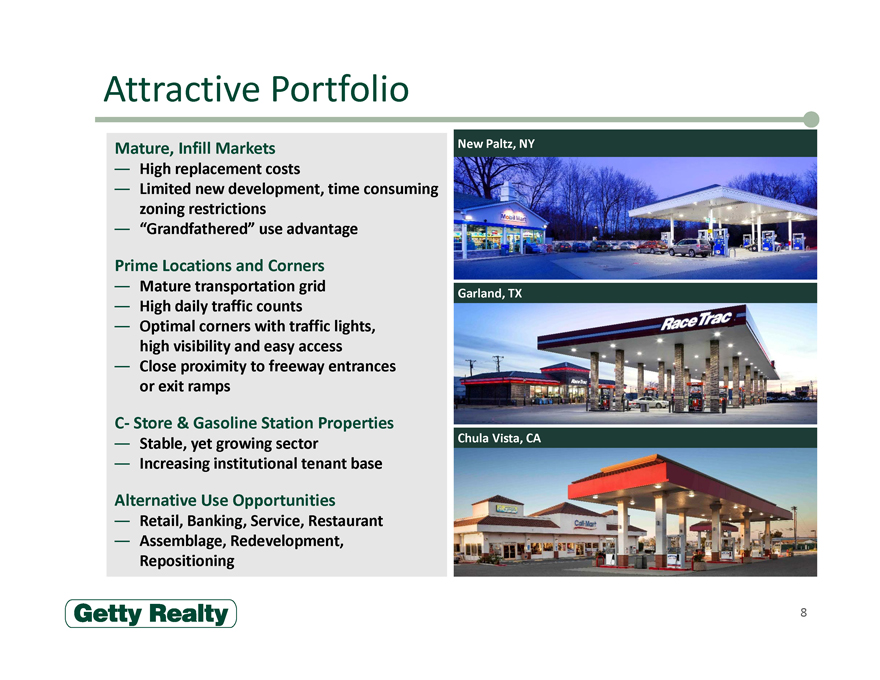

Attractive Portfolio

Mature, Infill Markets

High replacement costs

Limited new development, time consuming

zoning restrictions

“Grandfathered” use advantage

Prime Locations and Corners

Mature transportation grid

High daily traffic counts

Optimal corners with traffic lights,

high visibility and easy access

Close proximity to freeway entrances

or exit ramps

C- Store & Gasoline Station Properties

Stable, yet growing sector

Increasing institutional tenant base

Alternative Use Opportunities

Retail, Banking, Service, Restaurant

Assemblage, Redevelopment,

Repositioning

New Paltz, NY

Garland, TX

Chula Vista, CA

8

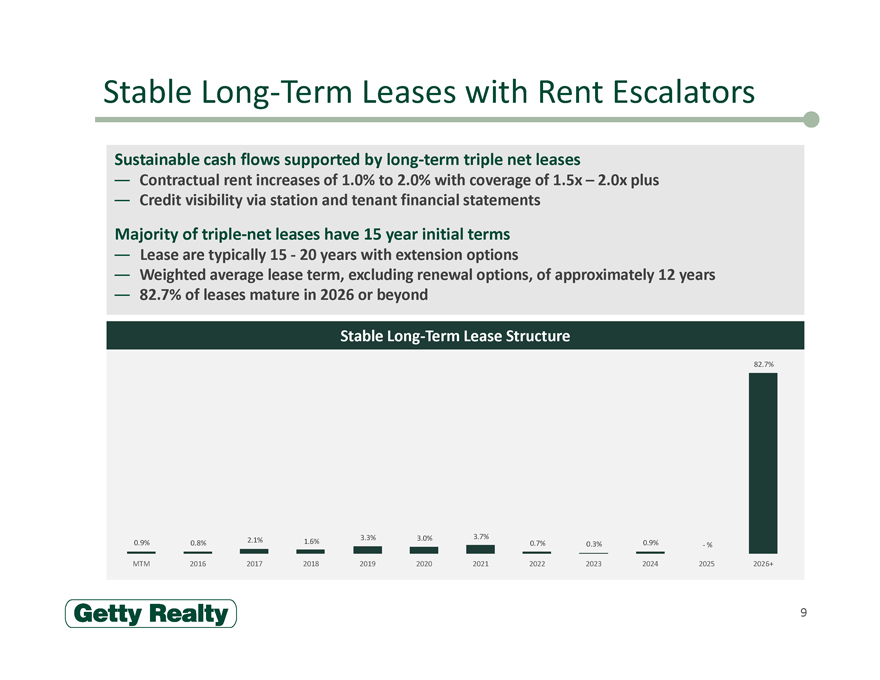

Stable Long-Term Leases with Rent Escalators

Sustainable cash flows supported by long-term triple net leases

Contractual rent increases of 1.0% to 2.0% with coverage of 1.5x – 2.0x plus

Credit visibility via station and tenant financial statements

Majority of triple-net leases have 15 year initial terms

Lease are typically 15 - 20 years with extension options

Weighted average lease term, excluding renewal options, of approximately 12 years

82.7% of leases mature in 2026 or beyond

Stable Long-Term Lease Structure

82.7%

2.1% 3.3% 3.0% 3.7%

0.9% 0.8% 1.6% 0.7% 0.3% 0.9% - %

MTM 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026+

9

High Quality Tenant Base

55% of Getty’s rental income comes from high-quality, credit worthy tenant base

Tenant Credit Rating

Tenant Rank Status / Parent Company (Moody’s / S&P / Fitch) % of Total

1st NYSE: GLP B1 / B+ / NA 19.0%

Fortress Portfolio

2nd NA / NA / BBB 15.2%

Company

Parent Co., Crossamerica

5th Ba2 / BB / NA 7.5%

NYSE: CAPL

Parent Co.: GPM

6th Petroleum NA 6.6%

IPO Filed

8th NYSE: BP A2 / A- / A 2.8%

Parent Co.: Sunoco LP

9th Ba2 / BB / BB 2.2%

NYSE: SUN

World’s largest C-store

11th Baa1 / AA- / NA 1.4%

chain

10

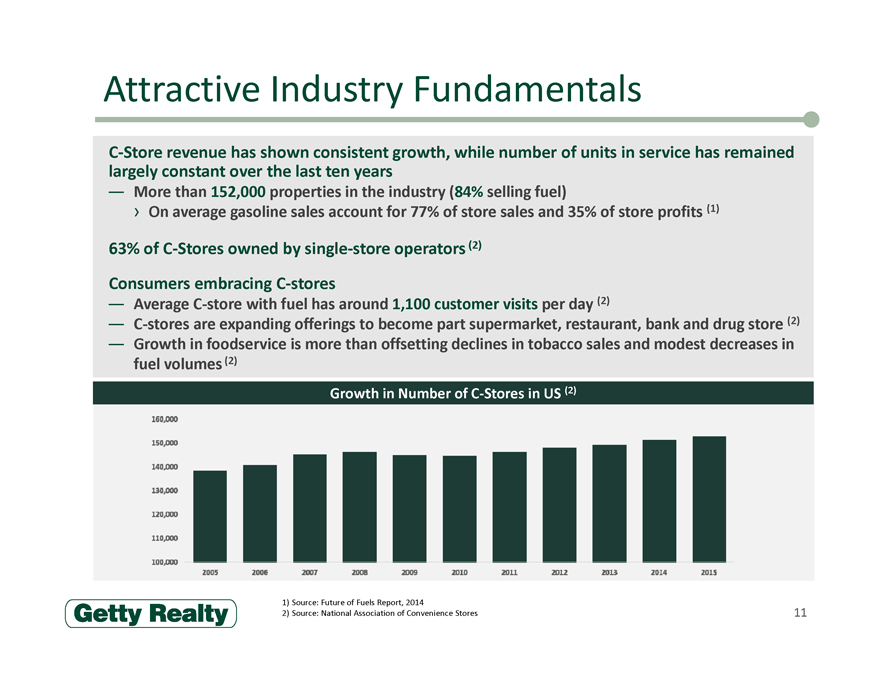

Attractive Industry Fundamentals

C-Store revenue has shown consistent growth, while number of units in service has remained

largely constant over the last ten years

More than 152,000 properties in the industry (84% selling fuel)

On average gasoline sales account for 77% of store sales and 35% of store profits (1)

63% of C-Stores owned by single-store operators (2)

Consumers embracing C-stores

Average C-store with fuel has around 1,100 customer visits per day (2)

C-stores are expanding offerings to become part supermarket, restaurant, bank and drug store (2)

Growth in foodservice is more than offsetting declines in tobacco sales and modest decreases in

fuel volumes (2)

Growth in Number of C-Stores in US (2)

1) Source: Future of Fuels Report, 2014

2) Source: National Association of Convenience Stores

11

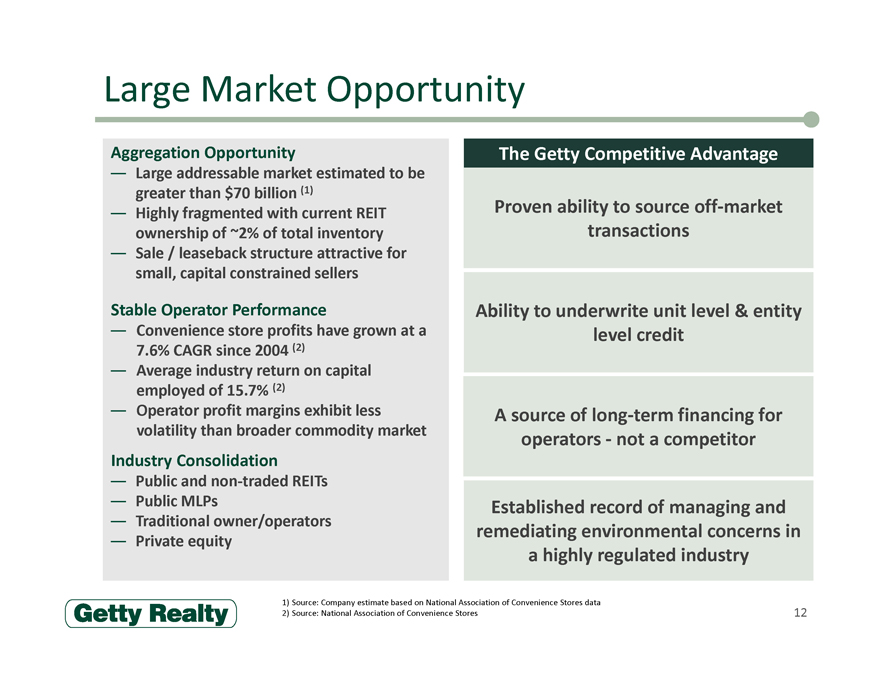

Large Market Opportunity

Aggregation Opportunity

Large addressable market estimated to be

greater than $70 billion (1)

Highly fragmented with current REIT

ownership of ~2% of total inventory

Sale / leaseback structure attractive for

small, capital constrained sellers

Stable Operator Performance

Convenience store profits have grown at a

7.6% CAGR since 2004 (2)

Average industry return on capital

employed of 15.7% (2)

Operator profit margins exhibit less

volatility than broader commodity market

Industry Consolidation

Public and non-traded REITs

Public MLPs

Traditional owner/operators

Private equity

The Getty Competitive Advantage

Proven ability to source off-market transactions

Ability to underwrite unit level & entity level credit

A source of long-term financing for operators -not a competitor

Established record of managing and remediating environmental concerns in a highly regulated industry

1) Source: Company estimate based on National Association of Convenience Stores data

2) Source: National Association of Convenience Stores

12

Acquisition – United Oil

$214.5 million Acquisition of 77 Properties in June 2015

Financed with a combination of long-term fixed rate

debt and credit facility borrowings

Tenant is United Oil, a leading regional convenience

store and gas station operator

› Operates ~400 locations in the Western United States

and Colorado

› Fortress Investment Group portfolio company

20 yr. triple-net lease with three 5-year renewal options

Attractive Sites in High Growth Markets

Site located across California, Colorado, Nevada, Oregon

and Washington State

Recognized brands including 7-Eleven, 76, Circle K,

Conoco and My Goods Market

Credit Enhancement

Properties supplied with fuel by Philips 66 under a long-

term supply agreement

Agreement contains credit enhancement consignment

features

13

Redevelopment – Unlocking Value in Our Assets

Getty’s unique network of assets are located on irreplaceable corners in attractive

neighborhoods which provides numerous opportunities for value enhancement

Funding of upgrades to convenience stores

NNN single tenant retail development

Multi-use urban building leases

Sources of opportunities for redevelopment include:

Transitional properties

Recapturing properties from unitary leases within Net-Lease portfolio

Supporting tenants as they convert to a full service convenience store model

Acquiring adjacent properties for development

Creating value through asset repositioning

Capital investment with attractive returns

Significant economic upside through incremental NOI

Diversifies tenant base

Improves tenant credit quality and coverage ratios

14

Case Study – MattressFIRM

Salem, New Hampshire

Property acquired in 1986 and previously

leased to Getty Petroleum Marketing, Inc.

Re-leased in 2012

Vacant as of 2015

Property Attributes

Well located retail location at traffic corner

Several large shopping centers with major

retailers adjacent to the site

Surrounded by other single tenant net-

lease retail stores

Redevelopment Project

$1.1 million invested in a build to suit

Corporate guarantee with Mattress Firm

Holding Corp. (NASDAQ:MFRM,

Moody’s B1)

Rent commencement February 2016

13% return on invested capital

Before

After

15

Financial Overview

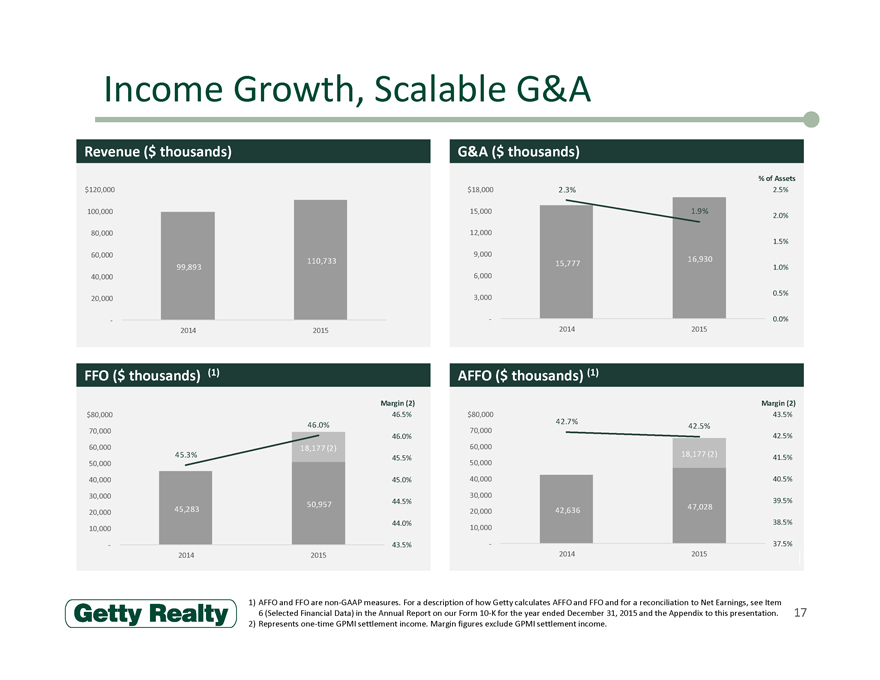

Income Growth, Scalable G&A

Revenue ($ thousands) G&A ($ thousands)

% of Assets

$120,000 $18,000 2.3% 2.5%

100,000 15,000 1.9% 2.0%

80,000 12,000

1.5%

60,000 9,000

110,733 15,777 16,930

99,893 1.0%

40,000 6,000

0.5%

20,000 3,000

- - 0.0%

2014 2015 2014 2015

FFO ($ thousands) (1) AFFO ($ thousands) (1)

Margin (2) Margin (2)

$80,000 46.5% $80,000 43.5%

42.7%

46.0% 42.5%

70,000 70,000

46.0% 42.5%

60,000 18,177 (2) 60,000

45.3% 45.5% 18,177 (2) 41.5%

50,000 50,000

40,000 45.0% 40,000 40.5%

30,000 30,000

44.5% 39.5%

50,957 47,028

20,000 45,283 20,000 42,636

44.0% 38.5%

10,000 10,000

- 43.5% - 37.5%

2014 2015 2014 2015

1) AFFO and FFO are non-GAAP measures. For a description of how Getty calculates AFFO and FFO and for a reconciliation to Net

Earnings, see Item

6 (Selected Financial Data) in the Annual Report on our Form 10-K for the year ended December 31, 2015 and the Appendix to this

presentation.

2) Represents one-time GPMI settlement income. Margin figures exclude GPMI settlement income.

17

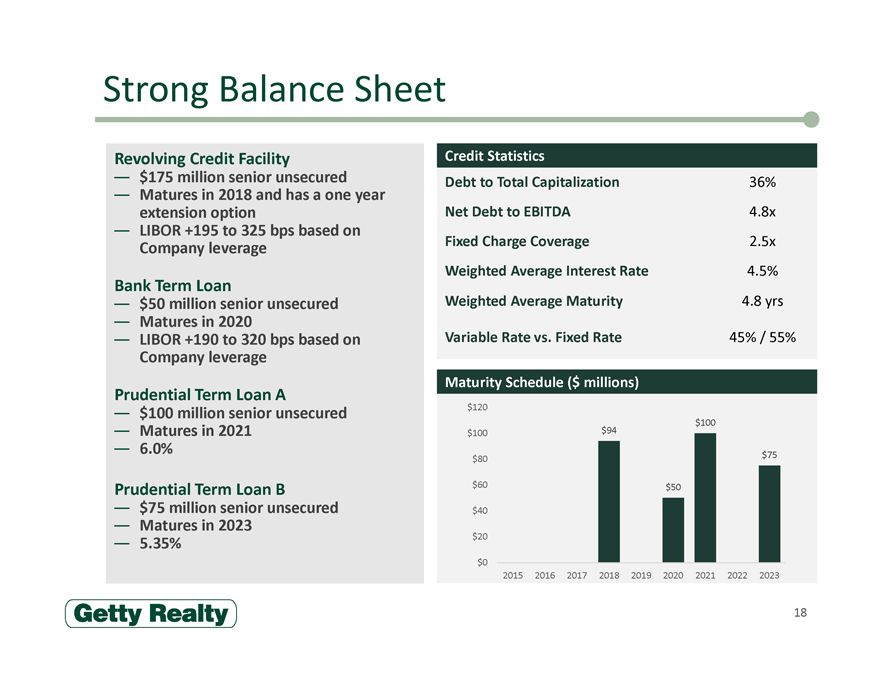

Strong Balance Sheet

Revolving Credit Facility

$175 million senior unsecured

Matures in 2018 and has a one year

extension option

LIBOR +195 to 325 bps based on

Company leverage

Bank Term Loan

$50 million senior unsecured

Matures in 2020

LIBOR +190 to 320 bps based on

Company leverage

Prudential Term Loan A

$100 million senior unsecured

Matures in 2021

6.0%

Prudential Term Loan B

$75 million senior unsecured

Matures in 2023

5.35%

Credit Statistics

Debt to Total Capitalization 36% Net Debt to EBITDA 4.8x Fixed Charge Coverage 2.5x Weighted Average Interest Rate 4.5% Weighted Average Maturity 4.8 yrs

Variable Rate vs. Fixed Rate 45% / 55%

Maturity Schedule ($ millions)

$120

$100

$100 $94

$80 $75

$60 $50

$40

$20

$0

2015 2016 2017 2018 2019 2020 2021 2022 2023

18

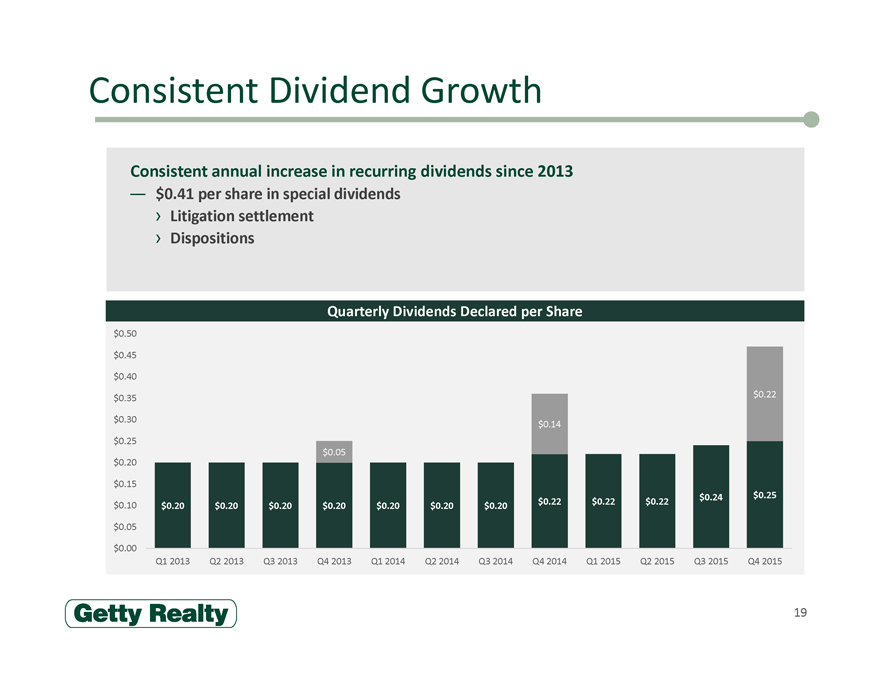

Consistent Dividend Growth

$0.41 per share in special dividends

Consistent annual increase in recurring dividends since 2013

Litigation settlement Dispositions

Quarterly Dividends Declared per Share

$0.50

$0.45

$0.40

$0.35 $ 0.22

$0.30 $ 0.14

$0.25

$ 0.05

$0.20

$0.15

$ 0.24 $ 0.25

$0.10 $ 0.20 $ 0.20 $ 0.20 $ 0.20 $ 0.20 $ 0.20 $ 0.20 $ 0.22 $ 0.22 $ 0.22

$0.05

$0.00

Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015

19

Investment Highlights

1 National Retail Net-Lease Portfolio Targeting Mature, High Growth Markets

Increasingly Institutional Quality Credit Tenant Base with Long Term Triple-Net

2 Leases

3 Attractive Industry Fundamentals with Stable Operator Performance

Aggregation Opportunity with Proven Ability to Successfully Pursue Growth in a

4 Consolidating Sector

5 Ongoing Process to Repurpose, Reposition, Redevelop Locations to Maximize Value

6 Strong Balance Sheet Positioned for Future Growth

20

Appendix

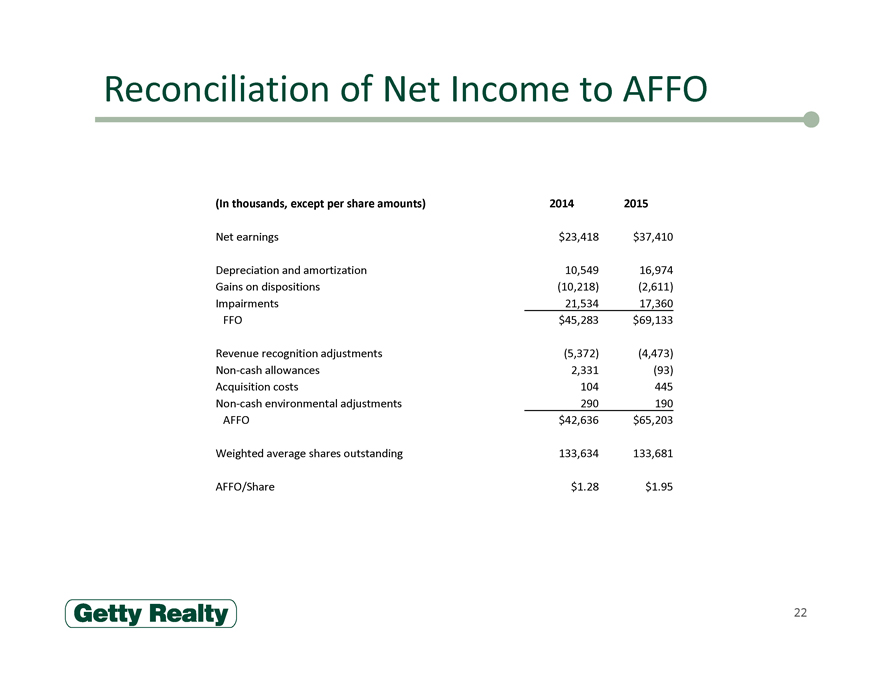

Reconciliation of Net Income to AFFO

(In thousands, except per share amounts) 2014 2015

Net earnings $23,418 $37,410

Depreciation and amortization 10,549 16,974

Gains on dispositions (10,218) (2,611)

Impairments 21,534 17,360

FFO $45,283 $69,133

Revenue recognition adjustments (5,372) (4,473)

Non-cash allowances 2,331 (93)

Acquisition costs 104 445

Non-cash environmental adjustments 290 190

AFFO $42,636 $65,203

Weighted average shares outstanding 133,634 133,681

AFFO/Share $1.28 $1.95

22