PRICING SUPPLEMENT No. VLS ETN-1 To the Prospectus Supplement dated March 25, 2009 and Prospectus dated March 25, 2009 | Filed Pursuant to Rule 424(b)(2) Registration Statement No. 333-158199-10 November 29, 2010 |

Issued by Credit Suisse AG

$100,000,000*VelocityShares Daily Inverse VIX Short Term ETN linked to the S&P 500 VIX Short-Term Futures™ Index due December 4, 2030

$100,000,000*VelocityShares Daily Inverse VIX Medium Term ETN linked to the S&P 500 VIX Mid-Term Futures™ Index due December 4, 2030

$100,000,000* VelocityShares VIX Short Term ETN linked to the S&P 500 VIX Short-Term Futures™ Index due December 4, 2030

$100,000,000*VelocityShares VIX Medium Term ETN linked to the S&P 500 VIX Mid-Term Futures™ Index due December 4, 2030

$100,000,000*VelocityShares Daily 2x VIX Short Term ETN linked to the S&P 500 VIX Short-Term Futures™ Index due December 4, 2030

$100,000,000*VelocityShares Daily 2x VIX Medium Term ETN linked to the S&P 500 VIX Mid-Term Futures™ Index due December 4, 2030

| ETNs | Leverage Amount | ETN Type | Exchange Ticker | Indicative Value Ticker | CUSIP | ISIN |

| Inverse VIX Short Term ETNs | -1 | “Inverse” | XIV | XIVIV | 22542D795 | US22542D7957 |

| Inverse VIX Medium Term ETNs | ZIV | ZIVIV | 22542D829 | US22542D8294 | ||

| Long VIX Short Term ETNs | 1 | “Long” | VIIX | VIIXIV | 22542D811 | US22542D8112 |

| Long VIX Medium Term ETNs | VIIZ | VIIZIV | 22542D787 | US22542D7874 | ||

| 2x Long VIX Short Term ETNs | 2 | “2x Long” or “Leveraged” | TVIX | TVIXIV | 22542D761 | US22542D7619 |

2x Long VIX Medium Term ETNs | TVIZ | TVIZIV | 22542D779 | US22542D7791 |

We are offering six separate series of exchange traded notes (collectively, the “ETNs”), the VelocityShares Daily Inverse VIX Short Term ETN linked to the S&P 500 VIX Short-Term Futures™ Index due December 4, 2030 (the “Inverse VIX Short Term ETNs”), the VelocityShares Daily Inverse VIX Medium Term ETN linked to the S&P 500 VIX Mid-Term Futures™ Index due December 4, 2030 (the “Inverse VIX Medium Term ETNs” and collectively with the Inverse VIX Short Term ETNs, the “Inverse ETNs”), the VelocityShares VIX Short Term ETN linked to the S&P 500 VIX Sho rt-Term Futures™ Index due December 4, 2030 (the “Long VIX Short Term ETNs”), the VelocityShares VIX Medium Term ETN linked to the S&P 500 VIX Mid-Term Futures™ Index due December 4, 2030 (the “Long VIX Medium Term ETNs” and collectively with the VIX Short Term ETNs, the “Long ETNs”), the VelocityShares Daily 2x VIX Short Term ETN linked to the S&P 500 VIX Short-Term Futures™ Index due December 4, 2030 (the “2x Long VIX Short Term ETNs”) and the VelocityShares Daily 2x VIX Medium Term ETN linked to the S&P 500 VIX Mid-Term Futures™ Index due December 4, 2030 (the “2x Long VIX Medium Term ETNs” and collectively with the Leveraged Short Term ETNs, the “2x Long ETNs”).

The ETNs, and in particular the 2x Long ETNs, are intended to be trading tools for sophisticated investors to manage daily trading risks. They are designed to achieve their stated investment objectives on a daily basis, but their performance over longer periods of time can differ significantly from their stated daily objectives. The ETNs are riskier than securities that have intermediate or long-term investment objectives, and may not be suitable for investors who plan to hold them for longer than one day. Accordingly, the ETNs should be purchased only by knowledgeable investors who understand the potential consequences of investing in volatility indices and of seeking inverse or leveraged investment results, as applicable. Investors should actively and frequently monitor thei r investments in the ETNs, even intra-day.

As explained in “Risk Factors” in this pricing supplement, because of the way in which the underlying Indices are calculated, the amount payable at maturity or upon redemption or acceleration is likely to be less than the initial principal amount of the ETNs, and you are likely to lose part or all of your initial investment. In almost any potential scenario the Closing Indicative Value (as defined below) of your ETNs is likely to be close to zero after 20 years and we do not intend or expect any investor to hold the ETNs from inception to maturity.

Investing in the ETNs involves a number of risks. See “Risk Factors” beginning on page PS-26 of this pricing supplement.

General

| · | The ETNs are designed for investors who seek exposure to the applicable underlying Index. The ETNs do not guarantee any return of principal at maturity and do not pay any interest during their term. For each ETN, investors will receive a cash payment at maturity, upon early redemption or upon acceleration by us that will be linked to the performance of the applicable underlying Index, plus a Daily Accrual and less a Daily Investor Fee (each as defined herein). Investors should be willing to forgo interest payments and, if the applicable underlying Index declines or increases, as applicable, be willing to lose up to 100% of their investment. Any payment on the ETNs is subject to our ability to pay our obligations as they become due. |

| · | The ETNs are senior medium-term notes of Credit Suisse AG, acting through its Nassau Branch, maturing December 4, 2030 (the “Maturity Date”).** |

| · | The denomination and stated principal amount of each ETN is $100. Any ETNs issued in the future may be issued at a price that is higher or lower than the stated principal amount, based on the most recent Closing Indicative Value of the ETNs of the applicable series at that time. |

| · | The initial issuance of ETNs of each series priced on November 29, 2010 (the “Inception Date”) and is expected to settle on December 2, 2010 (the “Initial Settlement Date”). Delivery of the ETNs in book-entry form only will be made through The Depository Trust Company (“DTC”). |

On the Inception Date, the issue price to the public per ETN is 100% of the principal amount of such ETN. We intend to sell a portion of the ETNs on the Inception Date at 100% of their stated principal amount. We expect to receive proceeds equal to 100% of the issue price to the public of the ETNs we issue and sell after the Inception Date.

VLS Securities, LLC (“VLS”) will receive all or a portion of the Daily Investor Fee in consideration for its role in marketing and placing the securities under the “VelocityShares” brand. See “Supplemental Plan of Distribution” in this pricing supplement for further information.

This pricing supplement provides specific pricing information in connection with the issuance of each series of the ETNs. Prospective investors should read this pricing supplement together with the prospectus supplement dated March 25, 2009 and the prospectus dated March 25, 2009 for a description of the specific terms and

(cover continued on next page)

(continued from previous page)

conditions of the ETNs. This pricing supplement amends and supersedes the accompanying prospectus supplement and prospectus to the extent that the information provided in this pricing supplement is different from the terms set forth in the prospectus supplement or the prospectus.

We may offer further issuances of ETNs of each series at offering prices based on the most recent Closing Indicative Value of the ETNs of the applicable series at that time. If there is a substantial demand for the ETNs, we may issue additional ETNs frequently. Any further issuances of ETNs of any series will form a single series with the offered ETNs of such series, will have the same CUSIP number and will trade interchangeably with the offered ETNs of such series upon settlement. Any further issuances will increase the outstanding aggregate principal amount of the applicable series of the ETNs. See “Supplemental Plan of Distribution” in this pricing supplement for further information.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined that this pricing supplement is truthful or complete. Any representation to the contrary is a criminal offense.

* The agent for this offering, Credit Suisse Securities (USA) LLC (“CSSU”), is our affiliate. We intend to sell $5,000,000 in principal amount of the Inverse VIX Short Term ETNs (50,000 Inverse VIX Short Term ETNs), $5,000,000 in principal amount of the Inverse VIX Medium Term ETNs (50,000 Inverse VIX Medium Term ETNs), $5,000,000 in principal amount of the Long VIX Short Term ETNs (50,000 Long VIX Short Term ETNs), $5,000,000 in principal amount of the Long VIX Medium Term ETNs (50,000 Long VIX Medium Term ETNs), $15,000,000 in principal amount of the 2x Long VIX Short Term ETNs (150,000 2x Long VIX Short Term ETNs) and $5,000,000 in principal amount of the 2x Long VIX Medium Term ETNs (50,000 2x Long VIX Medium Term ETNs), in each case on the initial settlemen t date through CSSU and through one or more dealers purchasing as principal through CSSU for $100.00 per each such ETN, which is the stated principal amount per ETN. Additional ETNs of each series may be offered and sold from time to time through CSSU and one or more dealers at a price that is higher or lower than the stated principal amount, based on the indicative value of the ETNs of such series at that time. We will receive proceeds equal to 100% of the offering price of the ETNs issued and sold after the initial settlement date. Delivery of the ETNs in book-entry form only will be made through The Depository Trust Company (“DTC”).

CSSU is expected to charge normal commissions for the purchase of the ETNs. In exchange for providing certain services relating to the distribution of the ETNs, CSSU, a member of the Financial Industry Regulatory Authority (“FINRA”), may receive all or a portion of the investor fee. In addition, CSSU may charge investors a redemption charge of up to 0.05% of the stated principal amount of any ETN that is redeemed at the investor’s option. Please see “Supplemental Plan of Distribution (Conflicts of Interest)” in this pricing supplement for more information.

The securities are not deposit liabilities and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency of the United States, Switzerland or any other jurisdiction.

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities Offered | Maximum Aggregate Offering Price | Amount of Registration Fee |

| VelocityShares Daily Inverse VIX Short Term ETN linked to the S&P 500 VIX Short-Term Futures™ Index due December 4, 2030 | $5,000,000 | $356.50 |

| VelocityShares Daily Inverse VIX Medium Term ETN linked to the S&P 500 VIX Mid-Term Futures™ Index due December 4, 2030 | $5,000,000 | $356.50 |

| VelocityShares VIX Short Term ETN linked to the S&P 500 VIX Short-Term Futures™ Index due December 4, 2030 | $5,000,000 | $356.50 |

| VelocityShares VIX Medium Term ETN linked to the S&P 500 VIX Mid-Term Futures™ Index due December 4, 2030 | $5,000,000 | $356.50 |

| VelocityShares Daily 2x VIX Short Term ETN linked to the S&P 500 VIX Short-Term Futures™ Index due December 4, 2030 | $15,000,000 | $1069.50 |

| VelocityShares Daily 2x VIX Medium Term ETN linked to the S&P 500 VIX Mid-Term Futures™ Index due December 4, 2030 | $5,000,000 | $356.50 |

Credit Suisse

November 29, 2010

Key Terms

(continued from previous page)

Key Terms

| Issuer: | Credit Suisse AG (“Credit Suisse”), acting through its Nassau Branch |

| Index: | The return on the ETNs of any series will be based on the performance of the applicable underlying Index during the term of such ETNs. Each series of ETNs tracks the daily performance of either the S&P 500 VIX Short-Term Futures™ Index ER or S&P 500 VIX Mid-Term Futures™ Index ER (each such index, an “Index” and collectively the “Indices”). The Indices are designed to provide investors with exposure to one or more maturities of futures contracts on the CBOE Volatility Index® (the “VIX Index”), which reflect implied volatility of the S&P 500® Index at various points along the volatility forward curve. The calculation of the level of the VIX Index is based on prices of put and call options on the S&P 500® Index. Futures contracts on the VIX Index allow investors the ability to invest in forward volatility based on their view of the future direction of movement of the VIX Index. Each Index is intended to reflect the returns that are potentially available through an unleveraged investment in the relevant futures contract or contracts on the VIX Index. The S&P 500 VIX Short-Term Futures™ Index ER targets a constant weighted average futures contracts maturity of one mont h and the S&P 500 VIX Mid-Term Futures™ Index ER targets a constant weighted average futures contracts maturity of five months. The Indices were created by Standard & Poor’s Financial Services LLC (“S&P” or the “Index Sponsor”). The Index Sponsor calculates the level of the relevant Index daily when the Chicago Board Options Exchange, Incorporated (the “CBOE”) is open (excluding holidays and weekends) and publishes it on the Bloomberg pages specified below as soon as practicable thereafter. Each Index, or any successor index to such Index, may be modified, replaced or adjusted from time to time, as determined by t he Calculation Agents as set forth below. See “The Indices” in this pricing supplement for further information on the Indices. |

| ETNs | Underlying Index | Underlying Index Ticker |

Inverse VIX Short Term ETNs, Long VIX Short Term ETNs, 2x Long VIX Short Term ETNs | S&P 500 VIX Short-Term Futures™ Index ER | SPVXSP |

Inverse VIX Medium Term ETNs, Long VIX Medium Term ETNs, 2x LongVIX Medium Term ETNs | S&P 500 VIX Mid-Term Futures™ Index ER | SPVXMP |

| The Calculation Agents, may modify, replace or adjust the Indices under certain circumstances even if the Index Sponsor continues to publish the applicable Index without modification, replacement or adjustment. See “Specific Terms of the ETNs—Discontinuance or Modification of the Index” and “Risk Factors—The Calculation Agents may modify the applicable underlying Index” in this pricing supplement for further information. | |

| Payment at Maturity: | If your ETNs have not been previously redeemed or accelerated, on the Maturity Date you will receive for each $100 stated principal amount of your ETNs a cash payment equal to the applicable Closing Indicative Value on the Final Valuation Date (the “Final Indicative Value”), as calculated by the Calculation Agents. We refer to the amount of such payment as the “Maturity Redemption Amount.” If the Final Indicative Value is zero, the Maturity Redemption Amount will be zero. |

| Closing Indicative Value: | The Closing Indicative Value for any series of ETNs on the Inception Date will equal $100 (the “Initial Indicative Value”). The Closing Indicative Value on each calendar day following the Inception Date for each series of ETNs will be equal to (1)(a) the Closing Indicative Value for that series on the immediately preceding calendar day times (b) the Daily ETN Performance for that series on such calendar day minus (2) the Daily Investor Fee for that series on such calendar day. The Closing Indicative Value will never be less than zero. The Closing Indicative Value will be zero on and subsequent to any calendar day on which the Intraday Indicative Value equals zero at any time or Closing Indicative Value equals zero. If the ETNs undergo a split or reverse split, the Closing Indicative Value will be adjusted accordingly (see “Description of the ETNs—Split or Reverse Split of the ETNs” in this pricing supplement). VLS or its affiliate is responsible for computing and disseminating the Closing Indicative Value. |

| Daily ETN Performance: | The Daily ETN Performance for any series of ETNs on any Index Business Day will equal (1) the number one plus (2) the Daily Accrual plus (3)(a) the Daily Index Performance times (b) the Leverage Amount. The Daily ETN Performance is deemed to be one on any day that is not an Index Business Day. |

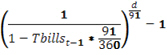

| Daily Accrual: | The Daily Accrual represents the rate of interest that could be earned on a notional capital reinvestment at the three month U.S. Treasury rate as reported on Bloomberg under ticker USB3MTA. The Daily Accrual for any series of ETNs on any Index Business Day will equal:  Where Tbillst-1 is the three month treasury rate reported on Bloomberg on the prior Index Business Day and d is the number of calendar days that have elapsed since the prior Index Business Day. The Daily Accrual is deemed to be zero on any day that is not an Index Business Day. |

| Daily Index Performance: | The Daily Index Performance for any series of ETNs on any Index Business Day will equal (1)(a) the closing level of the applicable underlying Index on such Index Business Day divided by (b) the closing level of the applicable underlying Index on the immediately preceding Index Business Day minus (2) the number one. If a Market Disruption Event occurs and continues on any Index Business Day, the Calculation Agents will determine the Daily Index Performance on such Index Business Day based on their assessment of the level of the applicable underlying Index that would have prevailed on such Index Business Day were it not for s uch Market Disruption Event. The Daily Index Performance is deemed to be zero on any day that is not an Index Business Day. |

| Leverage Amount: | The Leverage Amount for each series of ETNs is as follows: Inverse VIX Short Term ETNs: -1 Inverse VIX Medium Term ETNs: -1 Long VIX Short Term ETNs: 1 Long VIX Medium Term ETNs: 1 2x Long VIX Short Term ETNs: 2 2x Long VIX Medium Term ETNs: 2 |

(continued from previous page)

| Daily Investor Fee: | On any calendar day (the “calculation day”), the Daily Investor Fee for any series of ETNs will be equal to (1) the Closing Indicative Value for that series on the immediately preceding calendar day times (2) the Daily ETN Performance for that series on the calculation day times (3)(a) the Daily Investor Fee Factor for that series divided by (b) 365. The “Daily Investor Fee Factor” will be equal to (i) 0.0089 for each of the Long ETNs, (ii) 0.0135 for each of the Inverse ETNs and (iii) 0.0165 for each of the 2x Long ETNs. If the level of the Index decreases or does not increase sufficiently in the case of the Long ETNs or 2x Long ETNs or if it increases or does not decrease sufficiently in the case of the Inverse ETNs (in each case in addition to the Daily Accrual) to offset the sum of the Daily Investor Fees (and in the case of Early Redemption, the Early Redemption Charge) over the term of the ETNs, you will receive less than the principal amount of your investment at maturity or upon early redemption or acceleration of the ETNs. See “Risk Factors — Even if the closing level of the Index on the applicable Valuation Date exceeds (or is less than in the case of the Inverse ETNs) the initial closing level of the applicable underlying Index on the date of your investment, you may receive less than the principal amount of your ETNs” and “Hypothetical Examples” in this pricing supplement for additional information on how the Daily Investor Fee affects the overall value of the ETNs. |

| Intraday Indicative Value: | The Intraday Indicative Value of the ETNs will be calculated every 15 seconds on each Index Business Day during the period when a Market Disruption Event has not occurred or is not continuing and disseminated over the Consolidated Tape, or other major market data vendor. The Intraday Indicative Value at any time is based on the most recent intraday level of the underlying Index. The Intraday Indicative Value will be calculated using the Daily Investor Fee and the Daily Accrual on the immediately preceding calendar day, so the Intraday Indicative Value published at any time during a given Index Business Day will not reflect any Daily Investor Fee or Daily Accrual for the current Index Business Day or any part thereof. If the Intraday Indicative Value is equal to or less than zero at any time, the Closing In dicative Value on that day, and all future days, will be zero. See “Description of the ETNs—Intraday Indicative Value” in this pricing supplement. VLS or its affiliate is responsible for computing and disseminating the Intraday Indicative Value. |

| Valuation Dates: | November 30, 2030 or, if such date is not an Index Business Day, the next following Index Business Day (the “Final Valuation Date”), any Early Redemption Valuation Date and the Accelerated Valuation Date. |

| Secondary Market: | We intend to list each series of the ETNs on the NYSE Arca under the ticker symbols as set forth in the table above. However, there is no assurance that our application will be approved. If an active secondary market in the ETNs develops, we expect that investors will purchase and sell the ETNs primarily in this secondary market. We have no obligation to maintain any listing on NYSE Arca or any other exchange. |

| Early Redemption: | Prior to maturity, you may, subject to certain restrictions described below, offer the applicable minimum number of your ETNs to us for redemption on an Early Redemption Date during the term of the ETNs until November 28, 2030. If you elect to offer your ETNs for redemption, and the requirements for acceptance by us are met, you will receive a cash payment per ETN on the Early Redemption Date equal to the Early Redemption Amount. You must offer for redemption at least 25,000 ETNs, or an integral multiple of 25,000 ETNs in excess thereof, at one time in order to exercise your right to cause us to redeem your ETNs on any Early Redemption Date (the “Minimum Redemption Amount”); provided that we or Credit Suisse International (“CSI”) as one of the Calculation Agents, may from time to time reduce, in part or in whole, the Minimum Redemption Amount. Any such reduction will be applied on a consistent basis for all holders of the relevant series of ETNs at the time the reduction becomes effective. If the ETNs undergo a split or reverse split, the minimum number of ETNs needed to exercise your right to redeem will remain the same. |

| Early Redemption Mechanics: | You may exercise your early redemption right by causing your broker or other person with whom you hold your ETNs to deliver a Redemption Notice (as defined herein) to the Redemption Agent (as defined herein). If your Redemption Notice is delivered prior to 4:00 p.m., New York City time, on any Business Day, the immediately following Index Business Day will be the applicable “Early Redemption Valuation Date”. Otherwise, the second following Index Business Day will be the applicable Early Redemption Valuation Date. See “Specific Terms of the ETNs—Redemption Procedures” in this pricing supplement. |

| Early Redemption Date: | The third Business Day following an Early Redemption Valuation Date.** |

| Early Redemption Amount: | A cash payment per ETN equal to the greater of (A) zero and (B) (1) the Closing Indicative Value on the Early Redemption Valuation Date minus (2) the Early Redemption Charge. |

| Early Redemption Charge: | The Early Redemption Charge will be equal to 0.05% times the Closing Indicative Value on the Early Redemption Valuation Date. |

| Acceleration at Our Option or Upon Acceleration Event: | We will have the right to accelerate the ETNs of any series in whole but not in part on any Business Day occurring on or after the Inception Date (an “Optional Acceleration”). In addition, if an Acceleration Event (as defined herein) occurs at any time with respect to any series of the ETNs, we will have the right, and under certain circumstances as described herein the obligation, to accelerate all of the outstanding ETNs of such series (an “Event Acceleration”). In either case, upon acceleration you will receive a cash payment in an amount (the “Accelerated Redemption Amount”) equal to the Closing Indicative Value on the Accelerated Valuation Date. In the case of an Optional Acceleration, the “Accelerated Valuation Date” shall be an Index Business Day specified in our notice of Optional Acceleration, which Index Business Day shall be at least 5 Business Days after the date on which we give you notice of such Optional Acceleration. In the case of an Event Acceleration, the Accelerated Valuation Date shall be the day on which we give notice of such Event Acceleration (or, if such day is not an Index Business Day, the next following Index Business Day). The Accelerated Redemption Amount will be payable on the third Business Day following the Accelerated Valuation Date (such third Business Day the “Acceleration Date”).*** We will give you notice of any acceleration of the ETNs through customary channels used to deliver notices to holders of exchange traded notes. |

| Acceleration Event: | As discussed in more detail under “Specific Terms of the ETNs—Acceleration at Our Option or Upon an Acceleration Event” in this pricing supplement, an Acceleration Event includes any event that adversely affects our ability to hedge or our rights in connection with the ETNs, including, but not limited to, if the Intraday Indicative Value is equal to or less than 20% of the prior day’s Closing Indicative Value. |

| Business Day: | Any day that is not (a) a Saturday or Sunday or (b) a day on which banking institutions generally are authorized or obligated by law or executive order to close in New York. |

| Index Business Day: | An Index Business Day, with respect to the applicable underlying Index, is a day on which (i) trading is generally conducted on the CBOE, (ii) the applicable underlying Index is published by S&P and (iii) trading is generally conducted on NYSE Arca, in each case as determined by VLS, as one of the Calculation Agents. |

| Calculation Agents: | CSI and VLS. See “Specific Terms of the ETNs—Role of Calculation Agents” in this pricing supplement. |

** An Early Redemption Date will be postponed if a Market Disruption Event occurs and is continuing on the applicable Early Redemption Valuation Date. No interest or additional payment will accrue or be payable as a result of any postponement of any Early Redemption Date. See “Specific Terms of the ETNs—Market Disruption Events”.

*** The Acceleration Date will be postponed if a Market Disruption Event occurs and is continuing on the Accelerated Valuation Date. No interest or additional payment will accrue or be payable as a result of any postponement of the Acceleration Date. See “Specific Terms of the ETNs—Market Disruption Events”.

TABLE OF CONTENTS

Page | |

SUMMARY | PS-1 |

HYPOTHETICAL EXAMPLES | PS-12 |

RISK FACTORS | PS-26 |

THE INDICES | PS-39 |

DESCRIPTION OF THE ETNS | PS-47 |

SPECIFIC TERMS OF THE ETNS | PS-49 |

CLEARANCE AND SETTLEMENT | PS-56 |

USE OF PROCEEDS AND HEDGING | PS-56 |

CERTAIN U.S. FEDERAL INCOME TAX CONSIDERATIONS | PS-57 |

SUPPLEMENTAL PLAN OF DISTRIBUTION (CONFLICTS OF INTEREST) | PS-62 |

BENEFIT PLAN INVESTOR CONSIDERATIONS | PS-63 |

ANNEX A | A-1 |

You should read this pricing supplement together with the accompanying prospectus supplement dated March 25, 2009 and the prospectus dated March 25, 2009, relating to our Medium-Term Notes of which these ETNs are a part. You may access these documents on the SEC website at www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC website):

| · | Prospectus supplement dated March 25, 2009: |

| · | Prospectus dated March 25, 2009: |

Our Central Index Key, or CIK, on the SEC website is 1053092.

This pricing supplement, together with the documents listed above, contains the terms of the ETNs of any series and supersedes all other prior or contemporaneous oral statements as well as any other written materials including preliminary or indicative pricing terms, fact sheets, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. You should carefully consider, among other things, the matters set forth in “Risk Factors” in this pricing supplement and the accompanying prospectus supplement and prospectus, as the ETNs of any series involve risks not associated with conventional debt securities. You should consult your investment, legal, tax, accounting and other advisers before deciding to invest in the ETNs of any series. You sho uld rely only on the information contained in this document or in any documents to which we have referred you. We have not authorized anyone to provide you with information that is different. This document may only be used where it is legal to sell these ETNs. The information in this document may only be accurate on the date of this document.

The distribution of this pricing supplement and the accompanying prospectus supplement and prospectus and the offering of the ETNs of any series in some jurisdictions may be restricted by law. If you possess this pricing supplement, you should find out about and observe these restrictions.

In this pricing supplement and the accompanying prospectus supplement and prospectus, unless otherwise specified or the context otherwise requires, references to “Credit Suisse”, the “Company”, “we”, “us” and “our” are to Credit Suisse AG, acting through its Nassau Branch, and references to “dollars” and “$” are to United States dollars.

i

SUMMARY

The following is a summary of terms of the ETNs, as well as a discussion of risks and other considerations you should take into account when deciding whether to invest in any of the series of the ETNs. References to the “prospectus” mean our accompanying prospectus, dated March 25, 2009 and references to the “prospectus supplement” mean our accompanying prospectus supplement, dated March 25, 2009.

We may, without providing you notice or obtaining your consent, create and issue ETNs of each series in addition to those offered by this pricing supplement having the same terms and conditions as the ETNs of such series. We may consolidate the additional ETNs to form a single class with the outstanding ETNs of such series.

What are the ETNs and how do they work?

The ETNs are medium-term notes of Credit Suisse AG (“Credit Suisse”), the return on which is linked to the performance of either the S&P 500 VIX Short-Term Futures™ Index ER or the S&P 500 VIX Mid-Term Futures™ Index ER (each such index, an “Index” and collectively the “Indices”).

We will not pay you interest during the term of the ETNs. The ETNs do not have a minimum redemption or acceleration amount and are fully exposed to any decline or increase, as applicable, in the applicable underlying Index.

If you invest in the Long ETNs or the 2x Long ETNs, depreciation of the applicable underlying Index will reduce your payment at maturity, upon redemption or acceleration, and you could lose your entire investment.

If you invest in the Inverse ETNs, appreciation of the applicable underlying Index will reduce your payment at maturity, upon redemption or acceleration, and you could lose your entire investment.

The ETNs, and in particular the 2x Long ETNs, are intended to be trading tools for sophisticated investors to manage daily trading risks. They are designed to achieve their stated investment objectives on a daily basis, but their performance over longer periods of time can differ significantly from their stated daily objectives. The ETNs are riskier than securities that have intermediate or long-term investment objectives, and may not be suitable for investors who plan to hold them for longer than one day. Accordingly, the ETNs should be purchased only by knowledgeable investors who understand the potential consequences of investing in volatility indices and of seeking inverse or leveraged investment results, as applicable. Investors should actively and frequently monitor their investments in t he ETNs, even intra-day.

As explained in “Risk Factors” in this pricing supplement, because of the way in which the Closing Indicative Value of the ETNs and the underlying Indices are calculated, the amount payable at maturity or upon redemption or acceleration is likely to be less than the initial principal amount of the ETNs, and you are likely to lose part or all of your initial investment. In almost any potential scenario the Closing Indicative Value (as defined below) of your ETNs is likely to be close to zero after 20 years and we do not intend or expect any investor to hold the ETNs from inception to maturity.

For a description of how the payment at maturity, upon redemption or upon acceleration is calculated, please refer to the “Specific Terms of the ETNs—Payment at Maturity,” “—Payment Upon Early Redemption” and “—Acceleration at Our Option or Upon an Acceleration Event” sections herein.

The denomination and stated principal amount of each ETN is $100. Any ETNs issued in the future may be issued at a price higher or lower than the stated principal amount, based on the most recent Closing Indicative Value of the ETNs of the applicable series at that time. You will not have the right to receive physical certificates evidencing your ownership except under limited circumstances. Instead, we will issue the ETNs in the form of a global certificate, which will be held by DTC or its nominee. Direct and indirect participants in DTC will record beneficial ownership of the ETNs by individual investors. Accountholders in the Euroclear or Clearstream Banking clearance systems may hold beneficial interests in the ETNs through the accounts those systems maintain with DTC. 0;You should refer to the section “Description of Notes—Book-Entry, Delivery and Form” in the accompanying

PS-1

prospectus supplement and the section “Description of Debt Securities—Book-Entry System” in the accompanying prospectus.

What are the Indices and who publishes the level of the Indices?

The Indices are designed to provide investors with exposure to one or more maturities of futures contracts on the CBOE Volatility Index® (the “VIX Index”), which reflect implied volatility of the S&P 500® Index at various points along the volatility forward curve. The calculation of the level of the VIX Index is based on prices of put and call options on the S&P 500® Index. Futures contracts on the VIX Index allow investors the ability to invest in forward volatility based on their view of the future direction of movement of the VIX Index. Each Index is intended to reflect the returns that are potentially available through an unleveraged investment in the relevant futures contract or contracts on the VIX Index. The S&P 500 VIX Short-Term Futures™ Index ER targets a constant weighted average futures maturity of one month and the S&P 500 VIX Mid-Term Futures™ Index ER targets a constant weighted average futures maturity of five months.

The Indices were created by Standard & Poor’s Financial Services LLC (“S&P” or the “Index Sponsor”). The Index Sponsor calculates the level of the relevant Index daily when the Chicago Board Options Exchange, Incorporated (the “CBOE”) is open (excluding holidays and weekends) and publishes it on the Bloomberg pages specified herein as soon as practicable thereafter. Each Index, or any successor index to such Index, may be modified, replaced or adjusted from time to time, as determined by the Calculation Agents as set forth below. See “The Indices” in this pricing supplement for f urther information on the Indices.

| ETNs | Underlying Index | Underlying Index Ticker |

Inverse VIX Short Term, Long VIX Short Term, 2x VIX Short Term | S&P 500 VIX Short-Term Futures™ Index ER | SPVXSP |

Inverse VIX Medium-Term, Long VIX Medium Term, 2xVIX Medium Term | S&P 500 VIX Medium-Term Futures™ Index ER | SPVXMP |

The Calculation Agents, may modify, replace or adjust the Indices under certain circumstances even if the Index Sponsor continues to publish the applicable Index without modification, replacement or adjustment. See “Specific Terms of the ETNs—Discontinuation or Modification of the Index” and “Risk Factors—The Calculation Agents may modify the Indices” in this pricing supplement for further information.

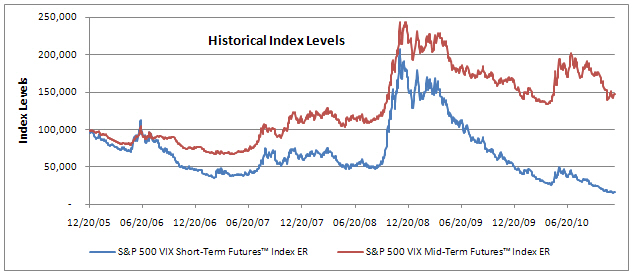

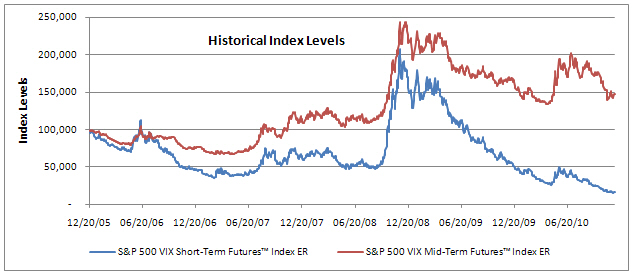

How have the Indices performed historically?

The inception date for the Indices is January 22, 2009 at the market close. The Indices were not in existence prior to that date. The chart below shows the closing level of each Index since the base date, December 20, 2005 through November 29, 2010. The historical performance is presented from January 22, 2009 through November 29, 2010. The closing levels from the base date of December 22, 2005 through January 22, 2009 represents hypothetical values determined by S&P, as the Index Sponsor, as if the relevant Index had been established on December 20, 2005 each with a base value of 100,000 on such date and calculated according to the methodology described below since that date. The closing levels from January 22, 2009 thro ugh November 29, 2010 represent the actual closing levels of the Indices as calculated on such dates. We obtained the levels below from Bloomberg, without independent verification. We have derived all information regarding each of the Indices contained in this pricing supplement, including, without limitation, their make-up, method of calculation and changes to their components, from publicly available information, and we have not participated in the preparation of, or verified, such publicly available information. We make no representation or warranty as to the accuracy or completeness of this publicly available information. Such information reflects the policies of, and is subject to change by the Index Sponsor. We and our affiliates make no representation or warranty as to, and assume no responsibility for, the accuracy or completeness of such information. The hypothetical and historical Inde x performance should not be taken as an indication of future performance, and no assurance can be given as to

PS-2

the level of either Index on any given date. See “The Indices” in this pricing supplement for more information on the Indices.

Will I receive interest on the ETNs?

You will not receive any interest payments on your ETNs. The ETNs are not designed for investors who are looking for periodic cash payments. Instead, the ETNs are designed for investors who are willing to forgo cash payments and, if the applicable underlying Index declines or does not increase enough (or increases or does not decline enough in the case of the Inverse ETNs) to offset the effect of the Daily Investor Fee as described below, are willing to lose some or all of the their principal.

How will payment at maturity, at redemption or upon acceleration be determined for the ETNs?

Unless your ETNs have been previously redeemed or accelerated, the ETNs will mature on December 4, 2030 (the “Maturity Date”).

Payment at Maturity

If your ETNs have not been previously redeemed or accelerated, on the Maturity Date you will receive a cash payment per ETN equal to the applicable Closing Indicative Value on the Final Valuation Date (the “Final Indicative Value”), as calculated by the Calculation Agents. We refer to the amount of such payment as the “Maturity Redemption Amount.” If the scheduled Maturity Date is not a Business Day, the Maturity Date will be postponed to the first Business Day following the scheduled Maturity Date. If the scheduled Final Valuation Date is not an Index Business Day, the Final Valuation Date will be postponed to the next following Index Business Day, in which case the Matu rity Date will be postponed to the third Business Day following the Final Valuation Date as so postponed. No interest or additional payment will accrue or be payable as a result of any postponement of the Maturity Date.

If the Final Indicative Value is zero, the Maturity Redemption Amount will be zero.

The “Closing Indicative Value” for any given series of ETNs on any given calendar day will be calculated in the following manner: The Closing Indicative Value on the Inception Date will equal $100 (the “Initial Indicative Value”). The Closing Indicative Value on each calendar day following the Inception Date for each series of ETNs will be equal to (1)(a) the Closing Indicative Value for that series on the immediately preceding calendar day times (b) the Daily ETN Performance for that series on such calendar day minus (2) the Daily Investor Fee for that series on such calendar day. The Closing Indicative Value will never be less than zero. The Closing Indicative Value will be zero on and subsequent to any calendar day on which the Intraday Indicative Value

PS-3

equals zero at any time or Closing Indicative Value equals zero. If the ETNs undergo a split or reverse split, the Closing Indicative Value will be adjusted accordingly (see “Description of ETNs—Split or Reverse Split of the ETNs” herein). VLS Securities, LLC (“VLS”) or its affiliate is responsible for computing and disseminating the Closing Indicative Value.

The “Daily ETN Performance” for any series of ETNs on any Index Business Day will equal (1) the number one plus (2) the Daily Accrual plus (3) the multiple of (a) the Daily Index Performance and (b) the Leverage Amount. The Daily ETN Performance is deemed to be one on any day that is not an Index Business Day.

An “Index Business Day”, with respect to the applicable underlying Index, is a day on which (i) trading is generally conducted on the CBOE, (ii) the applicable underlying Index is published by S&P and (iii) trading is generally conducted on NYSE Arca, in each case as determined by VLS, as one of the Calculation Agents.

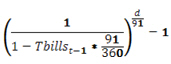

The “Daily Accrual” represents the rate of interest that could be earned on a notional capital reinvestment at the three month U.S. Treasury rate as reported on Bloomberg under ticker USB3MTA. The Daily Accrual for any series of ETNs on any Index Business Day will equal:

Where Tbillst-1 is the three month treasury rate reported on Bloomberg on the prior Index Business Day and d is the number of calendar days which have elapsed since the prior Index Business Day. The Daily Accrual is deemed to be zero on any day which is not an Index Business Day.

The “Daily Index Performance” for any series of ETNs on any Index Business Day will equal (1)(a) the closing level of the applicable underlying Index for that series on such Index Business Day divided by (b) the closing level of the applicable underlying Index for that series on the immediately preceding Index Business Day minus (2) the number one. If a Market Disruption Event occurs and continues on any Index Business Day, the Calculation Agents will determine the Daily Index Performance on such Index Business Day based on their assessment of the level of the applicable underlying Index that would have prevailed on such Index Business Day were it not for such Market Disruption Event. The Daily Index Performance is deemed to be zero on any day that is not an Index Business Day.

The “Leverage Amount” for each series of ETNs is as follows:

Daily Inverse VIX Short Term ETN: -1

Daily Inverse VIX Medium Term ETN: -1

VIX Short Term ETN: 1

VIX Medium Term ETN: 1

Daily 2x VIX Short Term ETN: 2

Daily 2x VIX Medium Term ETN: 2

With respect to any calendar day (the “calculation day”), the “Daily Investor Fee” is equal to the product of (1) the Closing Indicative Value for that series on the immediately preceding calendar day multiplied by (2) the Daily ETN Performance for that series on the calculation day times (3)(a) the Daily Investor Fee Factor for that series divided by (b) 365.

The “Daily Investor Fee Factor” will be equal to (i) 0.0089 for each of the Long ETNs, (ii) 0.0135 for each of the Inverse ETNs and (iii) 0.0165 for each of the 2x Long ETNs.

If the level of the applicable underlying Index decreases or does not increase sufficiently in the case of the Long or 2x Long ETNs or if it increases or does not decrease sufficiently in the case of the Inverse ETNs (in each case in addition to Daily Accrual) to offset the sum of the Daily Investor Fees (and in the case of Early Redemption, the Early Redemption Charge) over the term of the ETNs, you will receive less than the

PS-4

principal amount of your investment at maturity, upon early redemption or acceleration of the ETNs. See “Risk Factors—Even if the closing level of the Index on the applicable Valuation Date exceeds (or is less than in the case of the Inverse ETNs) the initial closing level of the Index on the date of your investment, you may receive less than the principal amount of your ETNs” and “Hypothetical Examples” in this pricing supplement for additional information on how the Daily Investor Fee affects the overall value of the ETNs.

The closing level of the applicable underlying Index on any Index Business Day will be the closing level reported by the Index Sponsor on the applicable Bloomberg page as set forth in the table below or any successor page on Bloomberg or any successor service, as applicable, as determined by the Calculation Agents, provided that in the event a Market Disruption Event is continuing on an Index Business Day, the Calculation Agents will determine the closing level of the applicable underlying Index for such Index Business Day according to the methodology described below in “Specific Terms of the ETNs—Market Disruption Events.”

| Index | Bloomberg Page Ticker |

| S&P 500 VIX Short-Term Futures™ Index ER | SPVXSP |

| S&P 500 VIX Mid-Term Futures™ Index ER | SPVXMP |

Any payment you will be entitled to receive is subject to our ability to pay our obligations as they become due.

For a further description of how your payment at maturity will be calculated, see “Hypothetical Examples” and “Specific Terms of the ETNs” in this pricing supplement.

Payment Upon Early Redemption

Prior to maturity, you may, subject to certain restrictions described below, offer the applicable Minimum Redemption Amount or more of your ETNs to us for redemption on an Early Redemption Date during the term of the ETNs until November 28, 2030. If you elect to offer your ETNs for redemption, and the requirements for acceptance by us are met, you will receive a cash payment per ETN on the Early Redemption Date equal to the Early Redemption Amount.

You may exercise your early redemption right by causing your broker or other person with whom you hold your ETNs to deliver a Redemption Notice (as defined herein) to the Redemption Agent (as defined herein). If your Redemption Notice is delivered prior to 4:00 p.m., New York City time, on any Business Day, the immediately following Index Business Day will be the applicable “Early Redemption Valuation Date”. Otherwise, the second following Index Business Day will be the applicable Early Redemption Valuation Date. See “Specific Terms of the ETNs—Redemption Procedures” in this pricing supplement.

You must offer for redemption at least 25,000 ETNs, or an integral multiple of 25,000 ETNs in excess thereof, at one time in order to exercise your right to cause us to redeem your ETNs on any Early Redemption Date (the “Minimum Redemption Amount”); provided that we or CSI as one of the Calculation Agents may from time to time reduce, in part or in whole, the Minimum Redemption Amount. Any such reduction will be applied on a consistent basis for all holders of the relevant series of ETNs at the time the reduction becomes effective. If the ETNs undergo a split or reverse split, the minimum number of ETNs needed to exercise your right to redeem will remain the same.

The “Early Redemption Date” is the third Business Day following an Early Redemption Valuation Date.*

The “Early Redemption Charge” is equal to 0.05% times the Closing Indicative Value on the Early Redemption Valuation Date.

* An Early Redemption Date will be postponed if a Market Disruption Event occurs and is continuing on the applicable Early Redemption Valuation Date. No interest or additional payment will accrue or be payable as a result of any postponement of any Early Redemption Date. See “Specific Terms of the ETNs—Market Disruption Events”.

PS-5

The “Early Redemption Amount” is a cash payment per ETN equal to the greater of (A) zero and (B) (1) the Closing Indicative Value on the Early Redemption Valuation Date minus (2) the Early Redemption Charge and will be calculated by the Calculation Agents.

Payment Upon Acceleration

We will have the right to accelerate the ETNs of any series in whole but not in part on any Business Day occurring on or after the Inception Date (an “Optional Acceleration”). In addition, if an Acceleration Event (as defined herein) occurs at any time with respect to any series of the ETNs, we will have the right, and under certain circumstances as described herein the obligation, to accelerate all of the outstanding ETNs of such series (an “Event Acceleration”). In either case, upon acceleration you will receive a cash payment in an amount (the “Accelerated Redemption Amount”) equal to the Closing Indicative Value on the Accelerated Valuation Date. In the case of an Optional Acceleration, the “Accelerated Valuation Date” shall be an Index Business Day specified in our notice of Optional Acceleration, which Index Business Day shall be at least 5 Business Days after the date on which we give you notice of such Optional Acceleration. In the case of an Event Acceleration, the Accelerated Valuation Date shall be the day on which we give notice of such Event Acceleration (or, if such day is not an Index Business Day, the next following Index Business Day). The Accelerated Redemption Amount will be payable on the third Business Day following the Accelerated Valuation Date (such third Business Day the “Acceleration Date”).* We will give you notice of any acceleration of the ETNs through customary channels used to deliver notices to holders of exchange traded notes. See “Specific Terms of the ETNs—Acceleration at Our Option or Upon an Acceleration Event” in this pricing supplement.

Any ETNs previously redeemed by us at your or our option or accelerated following an Acceleration Event will be cancelled on the Early Redemption Date or the Acceleration Date, as applicable. Consequently, as of such Early Redemption Date or the Acceleration Date, as applicable, the redeemed ETNs will no longer be considered outstanding.

Any payment you will be entitled to receive is subject to our ability to pay our obligations as they become due.

For a further description of how your payment at maturity, on redemption or upon acceleration will be calculated, see “Hypothetical Examples” and “Specific Terms of the ETNs” in this pricing supplement.

What will be the Intraday Indicative Value of the ETNs?

The “Intraday Indicative Value” of the ETNs will be calculated every 15 seconds on each Index Business Day during the period when a Market Disruption Event has not occurred or is not continuing and disseminated over the Consolidated Tape, or other major market data vendor. The Intraday Indicative Value at any time is based on the most recent intraday level of the underlying Index. The Intraday Indicative Value will be calculated using the Daily Investor Fee and the Daily Accrual on the immediately preceding calendar day, so the Intraday Indicative Value published at any time during a given Index Business Day will not reflect any Daily Investor Fee or Daily Accrual for the current Index Business Day or any part thereof. If the Intraday Ind icative Value is equal to or less than zero at any time, the Closing Indicative Value on that day, and all future days, will be zero. See “Description of the ETNs—Intraday Indicative Value” in this pricing supplement. VLS or its affiliate is responsible for computing and disseminating the Intraday Indicative Value.

How do you sell your ETNs?

We intend to list each series of the ETNs on the NYSE Arca under the ticker symbols as set forth in the table above. However, there is no assurance that our application will be approved. If an active secondary market in the ETNs develops, we expect that investors will purchase and sell the ETNs primarily in this secondary market. We have no obligation to maintain any listing on NYSE Arca or any other exchange.

* The Acceleration Date will be postponed if a Market Disruption Event occurs and is continuing on the Accelerated Valuation Date. No interest or additional payment will accrue or be payable as a result of any postponement of the Acceleration Date. See “Specific Terms of the ETNs—Market Disruption Events”.

PS-6

How do you offer your ETNs for redemption by Credit Suisse?

If you wish to offer your ETNs to Credit Suisse for redemption, your broker must follow the following procedures:

| · | Deliver a notice of redemption, in substantially the form as Annex A (the “Redemption Notice”), to VLS (the “Redemption Agent”) via email or other electronic delivery (including, without limitation, the Redemption Agent’s proprietary technology system, TENZING) as requested by the Redemption Agent. If your Redemption Notice is delivered prior to 4:00 p.m., New York City time, on any Business Day, the immediately following Index Business Day will be the applicable “Early Redemption Valuation Date”. Otherwise, the second following Index Business Day will be the applicable Early Redemption Valuation Date. If the R edemption Agent receives your Redemption Notice no later than 4:00 p.m., New York City time, on any Business Day, the Redemption Agent will respond by sending your broker an acknowledgment of the Redemption Notice accepting your redemption request by 7:30 p.m., New York City time, on the Business Day prior to the applicable Early Redemption Valuation Date. The Redemption Agent or its affiliate must acknowledge to your broker acceptance of the Redemption Notice in order for your redemption request to be effective; |

| · | Cause your DTC custodian to book a delivery vs. payment trade with respect to the ETNs on the applicable Early Redemption Valuation Date at a price equal to the applicable Early Redemption Amount, facing us; and |

| · | Cause your DTC custodian to deliver the trade as booked for settlement via DTC at or prior to 10:00 a.m. New York City time, on the applicable Early Redemption Date (the third Business Day following the Early Redemption Valuation Date). |

You are responsible for (i) instructing or otherwise causing your broker to provide the Redemption Notice and (ii) your broker satisfying the additional requirements as set forth in the second and third bullet above in order for the redemption to be effected. Different brokerage firms may have different deadlines for accepting instructions from their customers. Accordingly, you should consult the brokerage firm through which you own your interest in the ETNs in respect of such deadlines. If the Redemption Agent does not (i) receive the Redemption Notice from your broker by 4:00 p.m. and (ii) deliver an acknowledgment of such Redemption Notice to your broker accepting your redemption request by 7:30 p.m., on the Business Day prior to the applicable Early Redemption Valuation Date, such notice will not be effective fo r such Business Day and the Redemption Agent will treat such Redemption Notice as if it was received on the next Business Day. Any redemption instructions for which the Redemption Agent receives a valid confirmation in accordance with the procedures described above will be irrevocable.

What are some of the risks of the ETNs?

An investment in the ETNs involves risks. Some of these risks are summarized here, but we urge you to read the more detailed explanation of risks in “Risk Factors” in this pricing supplement.

| · | Uncertain Principal Repayment—The ETNs are designed for investors who seek exposure to the applicable underlying Index. The ETNs do not guarantee any return of principal at maturity. For each ETN, investors will receive a cash payment at maturity, upon early redemption or upon acceleration by us that will be linked to the performance of the applicable underlying Index, plus a Daily Accrual and less a Daily Investor Fee. If the applicable underlying Index declines or increases, as applicable, investors should be willing to lose up to 100% of their investment. Any payment on the ETNs is subject to our ability to pay our obligations as they become due. As explained in “Risk Factors&# 8221; in this pricing supplement, because of the way in which the underlying Indices are calculated, the amount payable at maturity or upon redemption or acceleration is likely to be less than the initial principal amount of the ETNs, and you are likely to lose part or all of your initial investment. In almost any potential scenario the Closing Indicative Value (as defined below) of |

PS-7

| your ETNs is likely to be close to zero after 20 years and we do not intend or expect that any investor to hold the ETNs from inception to maturity. |

| · | Credit Risk of the Issuer—Any payments you are entitled to receive on your ETNs are subject to the ability of Credit Suisse to pay its obligations as they come due. |

| · | Market and Volatility Risk—The return on each series of ETNs is linked to the performance of an applicable underlying Index which, in turn is linked to the performance of one or more futures contracts on the VIX Index. The VIX Index measures the 30-day forward volatility of the S&P 500® Index as calculated based on the prices of certain put and call options on the S&P 500® Index. The level of the S&P 500® Index, the prices of options on the S&P 500® Index, and the level of the VIX Index may change unpredictably, affecting the value of futures contracts on the VIX Index and, consequently, the level of each Index and the value of your ETNs in unforseeable ways. |

| · | No Interest Payments—You will not receive any periodic interest payments on the ETNs. |

| · | Long Holding Period Risk—The ETNs, and in particular the 2x Long ETNs, are intended to be trading tools for sophisticated investors to manage daily trading risks. They are designed to achieve their stated investment objectives on a daily basis, but their performance over longer periods of time can differ significantly from their stated daily objectives. The ETNs are riskier than securities that have intermediate or long-term investment objectives, and may not be suitable for investors who plan to hold them for longer than one day. Accordingly, the ETNs should be purchased only by knowledgeable investors who understand the potential consequences of investing in volatility indices and of seeking inverse or leveraged investment results, as applicable. &# 160;Investors should actively and frequently monitor their investments in the ETNs, even intra-day. |

| · | A Trading Market for the ETNs May Not Develop—Although we intend to list the ETNs on NYSE Arca, a trading market for your ETNs may not develop. We are not required to maintain any listing of the ETNs on NYSE Arca or any other exchange. |

| · | Requirements on Redemption by Credit Suisse—You must offer at least the applicable Minimum Redemption Amount to Credit Suisse and satisfy the other requirements described herein for your offer for redemption to be considered. |

| · | Your Offer for Redemption Is Irrevocable—You will not be able to rescind your offer for redemption after it is received by the Redemption Agent, so you will be exposed to market risk in the event market conditions change after the Redemption Agent receives your offer. |

| · | Uncertain Tax Treatment—No ruling is being requested from the Internal Revenue Service (“IRS”) with respect to the tax consequences of the ETNs. There is no direct authority dealing with securities such as the ETNs, and there can be no assurance that the IRS will accept, or that a court will uphold, the tax treatment described in this pricing supplement. In addition, you should note that the IRS and the U.S. Treasury Department have announced a review of the tax treatment of prepaid forward contracts. Accordingly, no assurance can be given that future tax legislation, regulations or other guidance may not change the tax treatment of the ETNs. ;Potential investors should consult their tax advisors regarding the U.S. federal income tax consequences of an investment in the ETNs, including possible alternative treatments. |

| · | Acceleration Feature—Your ETNs may be accelerated by us at any time on or after the Inception Date or accelerated by us at any time if an Acceleration Event occurs, and upon any such acceleration you may receive less, and possibly significantly less, than your original investment in the ETNs. |

PS-8

Is this the right investment for you?

The ETNs may be a suitable investment for you if:

| · | You seek an investment with a return linked to the performance of the applicable underlying Index. |

| · | You are willing to accept the risk of fluctuations in volatility in general and in the level of the applicable underlying Index in particular. |

| · | You are a sophisticated investor seeking to manage daily trading risk using a short-term investment, and are knowledgeable and understand the potential consequences of investing in volatility indices and of seeking inverse or leveraged investment results, as applicable. |

| · | You believe the level of the applicable underlying Index will increase (if you invest in the Long ETNs or 2x Long ETNs) or decline (if you invest in the Inverse ETNs) by an amount, and at a time or times, sufficient to offset the sum of the Daily Investor Fees (and in the case of Early Redemption, the Early Redemption Charge) over your intended holding period of the ETNs and to provide you with a satisfactory return on your investment during the time you hold the ETNs. |

| · | You do not seek current income from this investment. |

| · | You do not seek a guaranteed return of principal. |

| · | You are a sophisticated investor using the ETNs to manage daily trading risks and you understand that the ETNs are designed to achieve their stated investment objectives on a daily basis, but their performance over longer periods of time can differ significantly from their stated daily objectives. |

| · | You understand that the Daily Investor Fees and the Early Redemption Charge, if applicable, will reduce your return (or increase your loss, as applicable) on your investment. |

The ETNs may not be a suitable investment for you if:

| · | You are not willing to be exposed to fluctuations in volatility in general and in the level of the applicable underlying Index in particular. |

| · | You seek a guaranteed return of principal. |

| · | You seek a long-term investment objective. |

| · | You believe the level of the applicable underlying Index will decrease (if you invest in the Long ETNs or 2x Long ETNs) or increase (if you invest in the Inverse ETNs) or will not increase (if you invest in the Long ETNs or 2x Long ETNs) or decrease (if you invest in the Inverse ETNs) by an amount, and at a time or times, sufficient to offset the sum of the Daily Investor Fees (and in the case of Early Redemption, the Early Redemption Charge) over your intended holding period of the ETNs and to provide you with a satisfactory return on your investment during the time you hold the ETNs. |

| · | You prefer the lower risk and therefore accept the potentially lower returns of fixed income investments with comparable maturities and credit ratings. |

| · | You seek current income from your investment. |

| · | You are not a sophisticated investor and you seek an investment for other purposes than managing daily trading risks. |

PS-9

| · | You seek an investment with a longer duration than a daily basis. |

| · | You do not want to pay Daily Investor Fees and the Early Redemption Charge, if applicable, which are charged on the ETNs and which will reduce your return (or increase your loss, as applicable) on your investment. |

Will the ETNs be distributed by our affiliates?

Our affiliate, Credit Suisse Securities (USA) LLC (“CSSU”), a member of the Financial Industry Regulatory Authority (“FINRA”) will participate in the initial distribution of the ETNs on the initial settlement date and will likely participate in any future distribution of the ETNs. CSSU is expected to charge normal commissions for the purchase of any ETNs and may also receive all or a portion of the investor fee. Any offering in which CSSU participates will be conducted in compliance with the requirements of NASD Rule 2720 of FINRA regarding a FINRA member firm’s distribution of the securities of an affiliate and related conflicts of interest. In accordance with NASD Rule 2720, CSSU may n ot make sales in offerings of the ETNs to any of its discretionary accounts without the prior written approval of the customer. Please see the section entitled “Supplemental Plan of Distribution (Conflicts of Interest)” in this pricing supplement.

What is the U.S. Federal income tax treatment of an investment in the ETNs?

Please refer to “Certain U.S. Federal Income Tax Considerations” on page PS-56 for a discussion of certain U.S. federal income tax considerations for making an investment in the ETNs.

What is the role of our affiliates?

Our affiliate, CSSU, is the underwriter for the offering and sale of the ETNs of each series. After the initial offering, CSSU and/or other of our affiliated dealers currently intend, but are not obligated, to buy and sell the ETNs of any series to create a secondary market for holders of the ETNs of any such series, and may engage in other activities described in the section “Supplemental Plan of Distribution” in this pricing supplement, the accompanying prospectus supplement and prospectus. However, neither CSSU nor any of these affiliates will be obligated to engage in any market-making activities, or continue those activities once it has started them.

CSI will also act as one of the Calculation Agents for the ETNs. In addition, we may in the future become a minority investor in an affiliate of VLS, and may in connection with such investment obtain customary rights to nominate a director of such affiliate. As Calculation Agents CSI and VLS will make determinations with respect to the ETNs. The determinations may be adverse to you. You should refer to “Risk Factors—There Are Potential Conflicts of Interest Between You and the Calculation Agents” in this pricing supplement for more information.

Can you tell me more about the effect of Credit Suisse’s hedging activity?

We expect to hedge our obligations under the ETNs through one or more of our affiliates. This hedging activity will likely involve purchases or sales of equity securities underlying the S&P 500® Index and/or trading in instruments, such as options, swaps or futures, related to the VIX Index (including the VIX futures contracts which are used to calculate the Indices), the S&P 500® Index (including the put and call options used to calculate the level of the VIX Index) and the equity securities underlying the S&P 500® Index. The costs of maintaining or adjust ing this hedging activity could affect the value of the Index, and accordingly the value of the ETNs. Moreover, this hedging activity may result in our or our affiliates’ receipt of a profit, even if the market value of the ETNs declines. You should refer to “Risk Factors—Trading and other transactions by us, our affiliates or third parties with whom we transact, in securities or financial instruments related to the applicable underlying Index may impair the market value of the ETNs” and “Risk Factors—There may be conflicts of interest between you, us, the Redemption Agent, and the Calculation Agents” and “Use of Proceeds and Hedging” in this pricing supplement.

PS-10

Does ERISA Impose Any Limitations on Purchases of the ETNs?

Employee benefit plans subject to ERISA, entities the assets of which are deemed to constitute the assets of such plans, governmental or other plans subject to laws substantially similar to ERISA and retirement accounts (including Keogh, SEP and SIMPLE plans, individual retirement accounts and individual retirement annuities) are permitted to purchase the ETNs as long as either (A) (1) no CSSU affiliate or employee is a fiduciary to such plan or retirement account that has or exercises any discretionary authority or control with respect to the assets of such plan or retirement account used to purchase the ETNs or renders investment advice with respect to those assets, and (2) such plan or retirement account is paying no more than adequate consideration for the ETNs or (B) its acquisition and holding of the ETNs is not prohibited by any such provisions or laws or is exempt from any such prohibition. However, individual retirement accounts, individual retirement annuities and Keogh plans, as well as employee benefit plans that permit participants to direct the investment of their accounts, will not be permitted to purchase or hold the ETNs if the account, plan or annuity is for the benefit of an employee of CSSU or a family member and the employee receives any compensation (such as, for example, an addition to bonus) based on the purchase of ETNs by the account, plan or annuity. Please refer to the section “ERISA Matters” in this pricing supplement for further information.

PS-11

HYPOTHETICAL EXAMPLES

Hypothetical Examples

The following examples show how the ETNs would perform in hypothetical circumstances. These hypothetical examples are meant to illustrate the effect that different factors may have on the Maturity Redemption Amount. These factors include fees, compounding of returns, underlying futures volatility, and underlying T-Bill rates. Many other factors may affect the value of your ETNs, and these figures are provided for purposes of illustration only. They should not be taken as an indication or prediction of future investment results and are intended merely to illustrate a few of the potential possible Closing Indicative Values for the ETNs. The figures in these examples have been rounded for convenience.

The information in the tables reflects hypothetical rates of return on the ETNs assuming that they are purchased on the Inception Date at the Closing Indicative Value and disposed of on the Maturity Date for the Maturity Redemption Amount. We have not considered early redemption or acceleration for simplicity. Your ETNs may be accelerated early under certain circumstances. Although your payment upon redemption or acceleration would be based on the Closing Indicative Value of the ETNs, which is calculated in the manner illustrated in the examples below, your payment upon early redemption would be subject to the Early Redemption Charge.

Any rate of return you may earn on an investment in the ETNs may be lower than that which you could earn on a comparable investment in the underlying futures. The examples below assume no Market Disruption Event occurs. Also, the hypothetical rates of return shown below do not take into account the effects of applicable taxes. Because of the U.S. tax treatment applicable to your ETN, tax liabilities could affect the after-tax rate of return on your ETNs to a comparatively greater extent than the after-tax return on the underlying futures.

The prices of the futures contracts underlying the Indices have been highly volatile in the past and the performance of the Indices cannot be predicted for any future period. The actual performance of the Indices over the life of the ETNs, as well as the amount payable at the relevant Early Redemption Date, Acceleration Date or the Maturity Date, as applicable, may bear little relation to the hypothetical return examples set forth below or to the hypothetical historical closing levels of the Index set forth elsewhere in this pricing supplement. The examples included below are broken into sections to highlight some of the most significant factors that may affect the return on your ETNs. Each section is based upon numerous assumptions related to interest rate levels, interest rate volatilities, interest rat e spreads, underlying futures returns, underlying futures volatilities, and underlying futures funding and borrow costs. No single example can easily capture all the possible influences on the value of your ETNs, and each example is a simplified hypothetical example intended purely to illustrate the effect of various key factors which can influence the value of your ETNs. Many of the factors will primarily affect the value of your ETNs by affecting the level of the Index. These factors include, among others, interest rate levels, interest rate volatilities, interest rate spreads, underlying futures returns, underlying futures volatilities, and underlying futures funding and borrow costs.

Two of the most important factors that will affect the value of your ETNs are the directional change in the in the level of the applicable underlying Index (either up or down) and the annualized volatility of the applicable underlying Index itself. The annualized volatility of each underlying Index is a measure of the magnitude and frequency of changes in the underlying Index closing level, and is equal to the standard deviation of the underlying Index’s daily returns over twenty years, annualized by multiplying by the square root of 252. When we refer to “volatility in the daily change in Index levels” we mean that the annualized volatility of the daily closing levels of the applicable underlying Index over the relevant term. We therefore provide four examples below that reflect four di fferent scenarios related to these two factors. The hypothetical examples highlight the negative impact of higher annualized volatility of the applicable underlying Index on the rate of return on your ETNs. In Example 1 we show increasing Index levels with 10.21% annualized volatility in the daily change in Index levels over the relevant term. In example 2 we show decreasing Index levels with 10.10% annualized volatility in the daily change in Index levels over the relevant term. In example 3 we show increasing Index levels with 60.53% annualized volatility in the daily change in Index levels over the relevant term. In Example 4 we show decreasing Index levels with 49.69% annualized volatility in the daily change in Index levels over the relevant term. Because the Investor Fee is

PS-12

calculated on a daily basis, its effect on the value of your ETNs is dependent upon the path the applicable underlying Index takes rather than just the endpoint of the applicable underlying Index. Each of these four examples is a random possibility generated by a computer among an infinite number of possible outcomes. Your return may be materially worse. As explained in “Risk Factors—The ETNs do not pay interest nor guarantee return of principal and you may lose all or a significant part of your investment in the ETNs” in this pricing supplement, in almost any potential scenario the Closing Indicative Value of your ETNs is likely to be close to zero after 20 years and we do not intend or expect any investor to hold the ETNs from inception to maturity.

Any payment you will be entitled to receive is subject to our ability to pay our obligations as they become due.

PS-13

Example 1. This example assumes the index increases by 478% with 10.21% annualized volatility in the daily change in Index levels over the relevant term.

Inverse ETNs:

| A | B | C | D | E | F | G | H | I |

| Year | Index Level | Daily Accrual | Daily Index Factor | Daily ETN Performance | Daily Investor Fee | Closing Indicative Value | Annualized Index Return | Annualized ETN Return |

| Total for year | Total for year | Total for year | Total for year | At year end | Total for year | Total for year | ||

| 00 | 100.00 | 0.00% | 0.00% | 0.00% | $0.00 | $100.00 | 0.00% | 0.00% |

| 01 | 109.74 | 5.01% | 9.74% | -5.22% | $1.25 | $93.51 | 9.74% | -6.49% |

| 02 | 104.37 | 5.48% | -4.89% | 9.87% | $1.30 | $101.30 | -4.89% | 8.33% |

| 03 | 122.23 | 5.63% | 17.11% | -11.73% | $1.31 | $89.25 | 17.11% | -11.90% |

| 04 | 138.52 | 4.80% | 13.32% | -8.49% | $1.19 | $80.71 | 13.32% | -9.57% |

| 05 | 155.58 | 4.57% | 12.32% | -7.72% | $1.07 | $73.47 | 12.32% | -9.00% |

| 06 | 189.37 | 4.77% | 21.72% | -15.75% | $0.95 | $61.80 | 21.72% | -16.08% |

| 07 | 253.09 | 5.50% | 33.64% | -22.99% | $0.75 | $47.73 | 33.64% | -23.78% |

| 08 | 280.79 | 5.02% | 10.95% | -5.93% | $0.63 | $44.12 | 10.95% | -7.55% |

| 09 | 270.35 | 5.06% | -3.72% | 8.07% | $0.63 | $47.05 | -3.72% | 5.07% |

| 10 | 295.24 | 5.60% | 9.21% | -3.62% | $0.59 | $44.40 | 9.21% | -5.63% |

| 11 | 304.69 | 5.62% | 3.20% | 0.54% | $0.64 | $44.36 | 3.20% | -0.09% |

| 12 | 331.19 | 5.40% | 8.70% | -5.35% | $0.58 | $42.06 | 8.70% | -5.73% |

| 13 | 317.61 | 4.50% | -4.10% | 7.83% | $0.56 | $44.78 | -4.10% | 6.46% |

| 14 | 387.27 | 4.73% | 21.93% | -16.04% | $0.57 | $37.58 | 21.93% | -16.08% |

| 15 | 491.85 | 4.98% | 27.00% | -18.92% | $0.46 | $30.36 | 27.00% | -19.20% |

| 16 | 514.06 | 4.68% | 4.52% | -1.69% | $0.40 | $29.69 | 4.52% | -2.23% |

| 17 | 471.37 | 4.42% | -8.30% | 12.00% | $0.43 | $33.05 | -8.30% | 11.32% |

| 18 | 448.43 | 4.53% | -4.87% | 8.22% | $0.46 | $35.42 | -4.87% | 7.81% |

| 19 | 499.34 | 5.07% | 11.35% | -6.15% | $0.48 | $32.67 | 11.35% | -7.77% |

| 20 | 577.98 | 4.61% | 15.75% | -9.95% | $0.42 | $28.90 | 15.75% | -11.56% |

| Total Return | 477.98% | -71.10% |

PS-14

Long ETNs:

| A | B | C | D | E | F | G | H | I |

| Year | Index Level | Daily Accrual | Daily Index Factor | Daily ETN Performance | Daily Investor Fee | Closing Indicative Value | Annualized Index Return | Annualized ETN Return |

| Total for year | Total for year | Total for year | Total for year | At year end | Total for year | Total for year | ||

| 00 | 100.00 | 0.00% | 0.00% | 0.00% | $0.00 | $100.00 | 0.00% | 0.00% |

| 01 | 109.74 | 5.01% | 9.74% | 15.37% | $0.99 | $114.36 | 9.74% | 14.36% |

| 02 | 104.37 | 5.48% | -4.89% | 0.49% | $1.02 | $113.87 | -4.89% | -0.42% |

| 03 | 122.23 | 5.63% | 17.11% | 25.35% | $1.11 | $139.83 | 17.11% | 22.79% |

| 04 | 138.52 | 4.80% | 13.32% | 19.12% | $1.30 | $164.78 | 13.32% | 17.84% |

| 05 | 155.58 | 4.57% | 12.32% | 17.57% | $1.57 | $192.00 | 12.32% | 16.54% |

| 06 | 189.37 | 4.77% | 21.72% | 29.24% | $1.87 | $242.81 | 21.72% | 26.83% |

| 07 | 253.09 | 5.50% | 33.64% | 43.64% | $2.51 | $339.80 | 33.64% | 41.85% |

| 08 | 280.79 | 5.02% | 10.95% | 16.31% | $3.20 | $392.87 | 10.95% | 15.62% |

| 09 | 270.35 | 5.06% | -3.72% | 1.27% | $3.42 | $394.33 | -3.72% | 1.85% |