The information in this preliminary pricing supplement is not complete and may be changed.

This preliminary pricing supplement is not an offer to sell these securities, and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to completion dated January 27, 2011.

Preliminary Pricing Supplement No. K143 To the Underlying Supplement dated June 24, 2010, Product Supplement No. AK-I dated November 25, 2009, Prospectus Supplement dated March 25, 2009 and Prospectus dated March 25, 2009 | Filed Pursuant to Rule 424(b)(2) Registration Statement No. 333-158199-10 January 27, 2011 |

Financial Products | $ Buffered Accelerated Return Equity Securities due February 27, 2015 Linked to the S&P 500® Index |

General

| • | The securities are designed for investors who seek a return linked to the performance of the S&P 500® Index. Investors should be willing to forgo interest payments and, if the Underlying declines by more than 10%, be willing to lose up to 90% of their investment. Any payment at maturity is subject to our ability to pay our obligations as they become due. |

| • | Senior unsecured obligations of Credit Suisse AG, acting through its Nassau Branch, maturing February 27, 2015.† |

| • | Minimum purchase of $10,000. Minimum denominations of $10,000 and integral multiples of $1,000 in excess thereof. |

| • | The securities are expected to price on or about February 18, 2011 (the “Trade Date”) and are expected to settle on or about February 28, 2011. Delivery of the securities in book-entry form only will be made through The Depository Trust Company. |

Key Terms

| Issuer: | Credit Suisse AG (“Credit Suisse”), acting through its Nassau Branch | ||||

| Underlying: | The S&P 500® Index. For more information on the Underlying, see “The Reference Indices—The S&P Indices—The S&P 500® Index” in the accompanying underlying supplement. | ||||

| Fixed Payment Percentage: | Expected to be between 18.00% and 22.00% (to be determined on the Trade Date). | ||||

| Redemption Amount: | At maturity, you will be entitled to receive a Redemption Amount in cash that will equal the principal amount of the securities you hold multiplied by the sum of 1 plus the Underlying Return, calculated as set forth below. Any payment at maturity is subject to our ability to pay our obligations as they become due. | ||||

| Underlying Return: | • | If the Final Level is greater than or equal to the Initial Level, the Underlying Return will equal the greater of (i) the Fixed Payment Percentage and (ii) an amount calculated as follows: | |||

(Final Level – Initial Level) Initial Level | |||||

| • | If the Final Level is less than the Initial Level by not more than the Buffer Amount, the Underlying Return will equal zero and the Redemption Amount will equal the principal amount of the securities. | ||||

| • | If the Final Level is less than the Initial Level by more than the Buffer Amount, the Underlying Return will be calculated as follows: | ||||

(Final Level – Initial Level) Initial Level | + Buffer Amount | ||||

If the Final Level is less than the Initial Level by more than the Buffer Amount, the Underlying Return will be negative and you will receive less than the principal amount of your securities at maturity. You could lose up to $900 per $1,000 principal amount. | |||||

| Buffer Amount: | 10% | ||||

| Initial Level:* | The closing level of the Underlying on the Trade Date. | ||||

| Final Level: | The closing level of the Underlying on the Valuation Date. | ||||

Valuation Date:† | February 20, 2015 | ||||

Maturity Date:† | February 27, 2015 | ||||

| Listing: | The securities will not be listed on any securities exchange. | ||||

| CUSIP: | 22546EU77 | ||||

* In the event that the closing level for the Underlying is not available on the Trade Date, the Initial Level for the Underlying will be determined on the immediately following trading day on which a closing level is available.

† The Valuation Date is subject to postponement if such date is not an underlying business day or as a result of a market disruption event and the Maturity Date is subject to postponement if such date is not a business day or if the Valuation Date is postponed, in each case as described in the accompanying product supplement under “Description of the Securities—Market disruption events.”

Investing in the securities involves a number of risks. See “Selected Risk Considerations” beginning on page 5 of this pricing supplement and “Risk Factors” beginning on page PS-3 of the accompanying product supplement.

You may revoke your offer to purchase the securities at any time prior to the time at which we accept such offer on the date the securities are priced. We reserve the right to change the terms of, or reject any offer to purchase the securities prior to their issuance. In the event of any changes to the terms of the securities, we will notify you and you will be asked to accept such changes in connection with your purchase. You may also choose to reject such changes in which case we may reject your offer to purchase.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities or passed upon the accuracy or the adequacy of this pricing supplement or the accompanying underlying supplement, the product supplement, the prospectus supplement and the prospectus. Any representation to the contrary is a criminal offense.

| Price to Public | Underwriting Discounts and Commissions(1) | Proceeds to Issuer | |

| Per security | $1,000.00 | $ | $ |

| Total | $ | $ | $ |

(1) We or one of our affiliates may pay discounts and commissions of $27.50 per $1,000 principal amount of securities in connection with the distribution of the securities. In addition, an affiliate of ours may pay referral fees of up to $5.00 per $1,000 principal amount of securities in connection with the distribution of the securities. For more detailed information, please see “Supplemental Plan of Distribution (Conflicts of Interest)” on the last page of this pricing supplement.

The agent for this offering, Credit Suisse Securities (USA) LLC (“CSSU”), is our affiliate. For more information, see “Supplemental Plan of Distribution (Conflicts of Interest)” on the last page of this pricing supplement.

The securities are not deposit liabilities and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency of the United States, Switzerland or any other jurisdiction.

Credit Suisse

February , 2011

Additional Terms Specific to the Securities

You should read this pricing supplement together with the underlying supplement dated June 24, 2010, the product supplement dated November 25, 2009, the prospectus supplement dated March 25, 2009 and the prospectus dated March 25, 2009, relating to our Medium-Term Notes of which these securities are a part. You may access these documents on the SEC website at www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC website):

| • | Underlying supplement dated June 24, 2010: |

| • | Product supplement No. AK-I dated November 25, 2009: |

| • | Prospectus supplement dated March 25, 2009: |

| • | Prospectus dated March 25, 2009: |

Our Central Index Key, or CIK, on the SEC website is 1053092. As used in this pricing supplement, the “Company,” “we,” “us,” or “our” refers to Credit Suisse.

This pricing supplement, together with the documents listed above, contains the terms of the securities and supersedes all other prior or contemporaneous oral statements as well as any other written materials including preliminary or indicative pricing terms, fact sheets, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. You should carefully consider, among other things, the matters set forth in “Selected Risk Considerations” in this pricing supplement and “Risk Factors” in the accompanying product supplement, as the securities involve risks not associated with conventional debt securities. You should consult your investment, legal, tax, accounting and other advisors before deciding to invest in the securities.

1

Hypothetical Redemption Amounts at Maturity

The table and scenarios below illustrate hypothetical Redemption Amounts per $1,000 principal amount of securities for a range of hypothetical scenarios assuming an Initial Level of 1290 and a Fixed Payment Percentage of 20.00% (the midpoint of the expected range set forth on the cover page of this pricing supplement). The actual Initial Level and Fixed Payment Percentage will be determined on the Trade Date. The hypothetical Redemption Amounts set forth below are for illustrative purposes only. The actual Redemption Amount applicable to a purchaser of the securities will be based on the Final Level determined on the Valuation Date. Any payment at maturity is subject to our ability to pay our obligations as they become due. The numbers appearing in the table and scenarios below have been rounded for ease of analysis.

Final Level | Percentage Change in Underlying Level | Underlying Return | Redemption Amount |

| 2580.00 | 100.00% | 100.00% | $2,000.00 |

| 2257.50 | 75.00% | 75.00% | $1,750.00 |

| 1935.00 | 50.00% | 50.00% | $1,500.00 |

| 1806.00 | 40.00% | 40.00% | $1,400.00 |

| 1677.00 | 30.00% | 30.00% | $1,300.00 |

| 1548.00 | 20.00% | 20.00% | $1,200.00 |

| 1483.50 | 15.00% | 20.00% | $1,200.00 |

| 1419.00 | 10.00% | 20.00% | $1,200.00 |

| 1354.50 | 5.00% | 20.00% | $1,200.00 |

| 1322.25 | 2.50% | 20.00% | $1,200.00 |

| 1302.90 | 1.00% | 20.00% | $1,200.00 |

| 1290.00 | 0.00% | 20.00% | $1,200.00 |

| 1225.50 | −5.00% | 0.00% | $1,000.00 |

| 1161.00 | −10.00% | 0.00% | $1,000.00 |

| 1096.50 | −15.00% | −5.00% | $950.00 |

| 1032.00 | −20.00% | −10.00% | $900.00 |

| 903.00 | −30.00% | −20.00% | $800.00 |

| 774.00 | −40.00% | −30.00% | $700.00 |

| 645.00 | −50.00% | −40.00% | $600.00 |

| 516.00 | −60.00% | −50.00% | $500.00 |

| 387.00 | −70.00% | −60.00% | $400.00 |

| 258.00 | −80.00% | −70.00% | $300.00 |

| 129.00 | −90.00% | −80.00% | $200.00 |

| 0.00 | −100.00% | −90.00% | $100.00 |

2

The following scenarios illustrate how the Redemption Amount is calculated.

Scenario 1:

Scenario 1 assumes the Final Level is 1935, an increase of 50.00% from the Initial Level. The determination of the Redemption Amount when the Final Level is greater than the Initial Level is as follows:

| Underlying Return | = | the greater of (i) the Fixed Payment Percentage and (ii) (Final Level - Initial Level) / Initial Level |

| = | the greater of (i) the Fixed Payment Percentage and (ii) (1935 – 1290) / 1290 | |

| = | the greater of (i) 20.00% and (ii) 50.00% | |

| = | 50.00% | |

| Redemption Amount | = | Principal × (1 + Underlying Return) |

| = | $1,000 × 1.50 | |

| = | $1,500 |

In this scenario, at maturity you would be entitled to receive a Redemption Amount equal to $1,500 per $1,000 principal amount of securities based on a return linked to the appreciation in the level of the Underlying.

Scenario 2:

Scenario 2 assumes the Final Level is 1322.25, an increase of 2.50% from the Initial Level. The determination of the Redemption Amount when the Final Level is greater than the Initial Level is as follows:

| Underlying Return | = | the greater of (i) the Fixed Payment Percentage and (ii) (Final Level - Initial Level) / Initial Level |

| = | the greater of (i) the Fixed Payment Percentage and (ii) (1322.25 – 1290) / 1290 | |

| = | the greater of (i) 20.00% and (ii) 2.50% | |

| = | 20.00% | |

| Redemption Amount | = | Principal × (1 + Underlying Return) |

| = | $1,000 × 1.20 | |

| = | $1,200 |

In this scenario, at maturity you would be entitled to receive a Redemption Amount equal to the principal amount of your securities plus the Fixed Payment Percentage, or $1,200.00 per $1,000 principal amount of securities. Because the Final Level is greater than the Initial Level by less than the Fixed Payment Percentage, the Underlying Return is equal to the Fixed Payment Percentage. In this scenario you will receive more than the appreciation in the level of the Underlying during the term of the securities.

Scenario 3:

Scenario 3 assumes the Final Level is 1290, equal to the Initial Level. The determination of the Redemption Amount when the Final Level is greater than or equal to the Initial Level is as follows:

| Underlying Return | = | the greater of (i) the Fixed Payment Percentage and (ii) (Final Level - Initial Level) / Initial Level |

| = | the greater of (i) the Fixed Payment Percentage and (ii) (1290 – 1290) / 1290 | |

| = | the greater of (i) 20.00% and (ii) 0.00% | |

| = | 20.00% | |

| Redemption Amount | = | Principal × (1 + Underlying Return) |

| = | $1,000 × 1.20 | |

| = | $1,200 |

3

In this scenario, at maturity you would be entitled to receive a Redemption Amount equal to the principal amount of your securities plus the Fixed Payment Percentage, or $1,200.00 per $1,000 principal amount of securities. Because the Final Level is equal to the Initial Level, the Underlying Return equal to the Fixed Payment Percentage. In this scenario you would be entitled to receive a return of 20.00% even though the Underlying did not appreciate from its Initial Level.

Scenario 4:

Scenario 4 assumes the Final Level is 1225.50, a decrease of 5% from the Initial Level. Because the Final Level is less than the Initial Level by not more than the Buffer Amount of 10%, at maturity you would be entitled to receive a Redemption Amount equal to $1,000 per $1,000 principal amount of securities.

Scenario 5:

Scenario 5 assumes the Final Level is 645, a decrease of 50% from the Initial Level. The determination of the Redemption Amount when the Final Level is less than the Initial Level by more than the Buffer Amount of 10% is as follows:

| Underlying Return | = | [(Final Level - Initial Level)/Initial Level] + Buffer Amount |

| = | [(645 - 1290)/1290] + 10% | |

| = | −40% | |

| Redemption Amount | = | Principal × (1 + Underlying Return) |

| = | $1,000 × 0.60 | |

| = | $600 |

In this scenario, at maturity you would be entitled to receive a Redemption Amount equal to $600 per $1,000 principal amount of securities because the Final Level is less than the Initial Level by more than the Buffer Amount and you will participate in any depreciation in the level of the Underlying beyond the Buffer Amount.

4

Selected Risk Considerations

An investment in the securities involves significant risks. Investing in the securities is not equivalent to investing directly in the Underlying. These risks are explained in more detail in the “Risk Factors” section of the accompanying product supplement.

| • | YOUR INVESTMENT IN THE SECURITIES MAY RESULT IN A LOSS – The securities do not guarantee any return of your principal amount in excess of $100 per $1,000 principal amount. You could lose up to $900 per $1,000 principal amount of securities. If the Final Level is less than the Initial Level by more than the Buffer Amount of 10%, you will lose 1% of your principal for each 1% decline in the Final Level as compared to the Initial Level beyond the Buffer Amount. Any payment at maturity is subject to our ability to pay our obligations as they become due. |

| • | THE SECURITIES ARE SUBJECT TO THE CREDIT RISK OF CREDIT SUISSE – Although the return on the securities will be based on the performance of the Underlying, the payment of any amount due on the securities is subject to the credit risk of Credit Suisse. Investors are dependent on our ability to pay all amounts due on the securities and, therefore, investors are subject to our credit risk. In addition, any decline in our credit ratings, any adverse changes in the market’s view of our creditworthiness or any increase in our credit spreads is likely to adversely affect the value of the securities prior to maturity. |

| • | CERTAIN BUILT-IN COSTS ARE LIKELY TO ADVERSELY AFFECT THE VALUE OF THE SECURITIES PRIOR TO MATURITY – While the payment at maturity described in this pricing supplement is based on the full principal amount of your securities, the original issue price of the securities includes the agent’s commission and the cost of hedging our obligations under the securities through one or more of our affiliates. As a result, the price, if any, at which Credit Suisse (or its affiliates), will be willing to purchase securities from you in secondary market transactions, if at all, will likely be lower than the original issue price, and any sale prior to the Maturity Date could result in a substantial loss to you. The securities are not designed to be short-term trading instruments. Accordingly, you should be able and willing to hold your securities to maturity. |

| • | NO VOTING RIGHTS OR DIVIDEND PAYMENTS – As a holder of the securities, you will not have voting rights or rights to receive cash dividends or other distributions or other rights with respect to the stocks that comprise the Underlying. |

| • | NO INTEREST PAYMENTS – As a holder of the securities, you will not receive interest payments. |

| • | LACK OF LIQUIDITY – The securities will not be listed on any securities exchange. Credit Suisse (or its affiliates) intends to offer to purchase the securities in the secondary market but is not required to do so. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the securities when you wish to do so. Because other dealers are not likely to make a secondary market for the securities, the price at which you may be able to trade your securities is likely to depend on the price, if any, at which Credit Suisse (or its affiliates) is willing to buy the securities. If you have to sell your securities prior to maturity, you may not be able to do so or you may have to sell them at a substantial loss. |

| • | POTENTIAL CONFLICTS – We and our affiliates play a variety of roles in connection with the issuance of the securities, including acting as calculation agent and hedging our obligations under the securities. In performing these duties, the economic interests of the calculation agent and other affiliates of ours are potentially adverse to your interests as an investor in the securities. |

5

| • | MANY ECONOMIC AND MARKET FACTORS WILL AFFECT THE VALUE OF THE SECURITIES – In addition to the level of the Underlying on any day, the value of the securities will be affected by a number of economic and market factors that may either offset or magnify each other, including: |

| o | the expected volatility of the Underlying; |

| o | the time to maturity of the securities; |

| o | the dividend rate on the stocks comprising the Underlying; |

| o | interest and yield rates in the market generally; |

| o | geopolitical conditions and a variety of economic, financial, political, regulatory or judicial events that affect the stocks comprising the Underlying or markets generally and which may affect the level of the Underlying; and |

| o | our creditworthiness, including actual or anticipated downgrades in our credit ratings. |

Some or all of these factors may influence the price that you will receive if you choose to sell your securities prior to maturity. The impact of any of the factors set forth above may enhance or offset some or all of any change resulting from another factor or factors.

Supplemental Use of Proceeds and Hedging

We intend to use the proceeds of this offering for our general corporate purposes, which may include the refinancing of existing debt outside Switzerland. Some or all of the proceeds we receive from the sale of the securities may be used in connection with hedging our obligations under the securities through one or more of our affiliates. Such hedging or trading activities on or prior to the Trade Date and during the term of the securities (including on the Valuation Date) could adversely affect the value of the Underlying and, as a result, could decrease the amount you may receive on the securities at maturity. For further information, please refer to “Use of Proceeds and Hedging” in the accompanying product supplement.

6

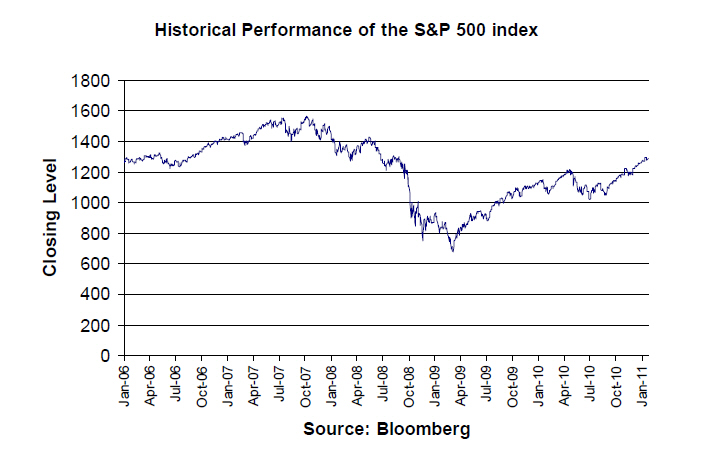

Historical Information

The following graph sets forth the historical performance of the S&P 500 Index based on the closing levels of the Underlying from January 1, 2006 through January 25, 2011. The closing level of the Underlying on January 25, 2011 was 1291.18. We obtained the closing levels below from Bloomberg, without independent verification. We make no representation or warranty as to the accuracy or completeness of the information obtained from Bloomberg.

The historical levels of the Underlying should not be taken as an indication of future performance, and no assurance can be given as to the closing level of the Underlying on any trading day during the term of the securities, including on the Valuation Date. We cannot give you assurance that the performance of the Underlying will result in any return of your investment beyond the Buffer Amount. Any payment at maturity is subject to our ability to pay our obligations as they become due.

For further information on the S&P 500 Index, see “The Reference Indices—The S&P Indices—The S&P 500® Index” in the accompanying underlying supplement.

7

Certain United States Federal Income Tax Considerations

The following discussion summarizes certain U.S. federal income tax consequences of owning and disposing of securities that may be relevant to holders of securities that acquire their securities from us as part of the original issuance of the securities. This discussion applies only to holders that hold their securities as capital assets within the meaning of the Internal Revenue Code of 1986, as amended (the “Code”). Further, this discussion does not address all of the U.S. federal income tax consequences that may be relevant to you in light of your individual circumstances or if you are subject to special rules, such as if you are:

| · | a financial institution, |

| · | a mutual fund, |

| · | a tax-exempt organization, |

| · | a grantor trust, |

| · | certain U.S. expatriates, |

| · | an insurance company, |

| · | a dealer or trader in securities or foreign currencies, |

| · | a person (including traders in securities) using a mark-to-market method of accounting, |

| · | a person who holds securities as a hedge or as part of a straddle with another position, constructive sale, conversion transaction or other integrated transaction, or |

| · | an entity that is treated as a partnership for U.S. federal income tax purposes. |

The discussion is based upon the Code, law, regulations, rulings and decisions, in each case, as available and in effect as of the date hereof, all of which are subject to change, possibly with retroactive effect. Tax consequences under state, local and foreign laws are not addressed herein. No ruling from the U.S. Internal Revenue Service (the “IRS”) has been or will be sought as to the U.S. federal income tax consequences of the ownership and disposition of securities, and the following discussion is not binding on the IRS.

You should consult your tax advisor as to the specific tax consequences to you of owning and disposing of securities, including the application of federal, state, local and foreign income and other tax laws based on your particular facts and circumstances.

IRS CIRCULAR 230 REQUIRES THAT WE INFORM YOU THAT ANY TAX STATEMENT HEREIN REGARDING ANY U.S. FEDERAL TAX IS NOT INTENDED OR WRITTEN TO BE USED, AND CANNOT BE USED, BY ANY TAXPAYER FOR THE PURPOSE OF AVOIDING ANY PENALTIES. ANY SUCH STATEMENT HEREIN WAS WRITTEN TO SUPPORT THE MARKETING OR PROMOTION OF THE TRANSACTION(S) OR MATTER(S) TO WHICH THE STATEMENT RELATES. A PROSPECTIVE INVESTOR (INCLUDING A TAX-EXEMPT INVESTOR) IN THE SECURITIES SHOULD CONSULT ITS OWN TAX ADVISOR IN DETERMINING THE TAX CONSEQUENCES OF AN INVESTMENT IN THE SECURITIES, INCLUDING THE APPLICATION OF STATE, LOCAL OR OTHER TAX LAWS AND THE POSSIBLE EFFECTS OF CHANGES IN FEDERAL OR OTHER TAX LAWS.

Characterization of the Securities

There are no statutory provisions, regulations, published rulings, or judicial decisions addressing the characterization for U.S. federal income tax purposes of securities with terms that are substantially the same as those of your securities. Thus, we intend to treat the securities, for U.S. federal income tax purposes, as a prepaid financial contract, with respect to the Underlying that is eligible for open transaction treatment. In the absence of an administrative or judicial ruling to the contrary, we and, by acceptance of the securities, you, agree to treat your securities for all tax purposes in accordance with such characterization. In light of the fact that we agree to treat the securities as a prepaid financial contract, the balance of this discussion assumes that the securities will be s o treated.

8

You should be aware that the characterization of the securities as described above is not certain, nor is it binding on the IRS or the courts. Thus, it is possible that the IRS would seek to characterize your securities in a manner that results in tax consequences to you that are different from those described above. For example, the IRS might assert that the securities constitute debt instruments that are “contingent payment debt instruments” that are subject to special tax rules under the applicable Treasury regulations governing the recognition of income over the term of your securities. If the securities were to be treated as contingent payment debt instruments (one of the requirements of which is that the instruments have a term of more than one year), you would be required to inc lude in income on an economic accrual basis over the term of the securities an amount of interest that is based upon the yield at which we would issue a non-contingent fixed-rate debt instrument with other terms and conditions similar to your securities, or the comparable yield. The characterization of securities as contingent payment debt instruments under these rules is likely to be adverse. However, if the securities had a term of one year or less, the rules for short-term debt obligations would apply rather than the rules for contingent payment debt instruments. Under Treasury regulations, a short-term debt obligation is treated as issued at a discount equal to the difference between all payments on the obligation and the obligation’s issue price. A cash method U.S. Holder that does not elect to accrue the discount in income currently should include the payments attributable to interest on the security as income upon receipt. Under these rules, any contingent payment would be taxable upon receipt by a cash basis taxpayer as ordinary interest income. You should consult your tax advisor regarding the possible tax consequences of characterization of the securities as contingent payment debt instruments or short-term debt obligations.

It is also possible that the IRS would seek to characterize your securities as Code section 1256 contracts in the event that they are listed on a securities exchange. In such case, the securities would be marked to market at the end of the year and 40% of any gain or loss would be treated as short-term capital gain or loss, and the remaining 60% of any gain or loss would be treated as long-term capital gain or loss. We are not responsible for any adverse consequences that you may experience as a result of any alternative characterization of the securities for U.S. federal income tax or other tax purposes.

You should consult your tax advisor as to the tax consequences of such characterization and any possible alternative characterizations of your securities for U.S. federal income tax purposes.

U.S. Holders

For purposes of this discussion, the term “U.S. Holder,” for U.S. federal income tax purposes, means a beneficial owner of securities that is (1) a citizen or resident of the United States, (2) a corporation (or an entity treated as a corporation for U.S. federal income tax purposes) created or organized in or under the laws of the United States or any state thereof or the District of Columbia, (3) an estate, the income of which is subject to U.S. federal income taxation regardless of its source, or (4) a trust, if (a) a court within the United States is able to exercise primary supervision over the administration of such trust and one or more U.S. persons have the authority to control all substantial decisions of the trust or (b) such trust has in effect a valid election to be treated as a domestic trust for U.S. fed eral income tax purposes. If a partnership (or an entity treated as a partnership for U.S. federal income tax purposes) holds securities, the U.S. federal income tax treatment of such partnership and a partner in such partnership will generally depend upon the status of the partner and the activities of the partnership. If you are a partnership, or a partner of a partnership, holding securities, you should consult your tax advisor regarding the tax consequences to you from the partnership's purchase, ownership and disposition of the securities.

In accordance with the agreed-upon tax treatment described above, upon receipt of the redemption amount of the securities from us, a U.S. Holder will recognize gain or loss equal to the difference between the amount of cash received from us and the U.S. Holder’s tax basis in the security at that time. For securities with a term of more than one year, such gain or loss will be long-term capital gain or loss if the U.S. Holder has held the security for more than one year at maturity. For securities with a term of one year or less, such gain or loss will be short-term capital gain or loss.

Upon the sale or other taxable disposition of a security, a U.S. Holder generally will recognize capital gain or loss equal to the difference between the amount realized on the sale or other taxable disposition and the U.S. Holder’s tax basis in the security (generally its cost). For securities with a term of more than one year, such gain or loss will be long-term capital gain or loss if the U.S. Holder has held the security for more than one year at the time of disposition. For securities with a term of one year or less, such gain or loss will be short-term capital gain or loss.

9

Legislation Affecting Securities Held Through Foreign Accounts

Under the “Hiring Incentives to Restore Employment Act” (the “Act”), a 30% withholding tax is imposed on “withholdable payments” made to foreign financial institutions (and their more than 50% affiliates) unless the payee foreign financial institution agrees, among other things, to disclose the identity of any U.S. individual with an account at the institution (or the institution’s affiliates) and to annually report certain information about such account. “Withholdable payments” include payments of interest (including original issue discount), dividends, and other items of fixed or determinable annual or periodical gains, profits, and income (“FDAP”), in each case, from sources within the United States, as well as gross proceeds from the sale of any prop erty of a type which can produce interest or dividends from sources within the United States. The Act also requires withholding agents making withholdable payments to certain foreign entities that do not disclose the name, address, and taxpayer identification number of any substantial U.S. owners (or certify that they do not have any substantial United States owners) to withhold tax at a rate of 30%. We will treat payments on the securities as withholdable payments for these purposes.

Withholding under the Act will apply to all withholdable payments without regard to whether the beneficial owner of the payment is a U.S. person, or would otherwise be entitled to an exemption from the imposition of withholding tax pursuant to an applicable tax treaty with the United States or pursuant to U.S. domestic law. Unless a foreign financial institution is the beneficial owner of a payment, it will be subject to refund or credit in accordance with the same procedures and limitations applicable to other taxes withheld on FDAP payments provided that the beneficial owner of the payment furnishes such information as the IRS determines is necessary to determine whether such beneficial owner is a United States owned foreign entity and the identity of any substantial United States owners of such entity. Ge nerally, the Act’s withholding and reporting regime will apply to payments made after December 31, 2012. Thus, if you hold your securities through a foreign financial institution or foreign corporation or trust, a portion of any of your payments made after December 31, 2012 may be subject to 30% withholding.

Non-U.S. Holders Generally

In the case of a holder of the securities that is not a U.S. Holder and has no connection with the United States other than holding its securities (a “Non-U.S. Holder��), payments made with respect to the securities will not be subject to U.S. withholding tax, provided that such Non-U.S. Holder complies with applicable certification requirements. Any gain realized upon the sale or other disposition of the securities by a Non-U.S. Holder generally will not be subject to U.S. federal income tax unless (1) such gain is effectively connected with a U.S. trade or business of such Non-U.S. Holder or (2) in the case of an individual, such individual is present in the United States for 183 days or more in the taxable year of the sale or other disposition and certain other conditions are met. Non-U.S. Hold ers should consult their tax advisors regarding the possibility that any portion of the return with respect to the securities could be characterized as dividend income and be subject to U.S. withholding tax.

Non-U.S. Holders that are subject to U.S. federal income taxation on a net income basis with respect to their investment in the securities should refer to the discussion above relating to U.S. Holders.

Legislation Affecting Substitute Dividend and Dividend Equivalent Payments

The Act treats a “dividend equivalent” payment as a dividend from sources within the United States. Under the Act, unless reduced by an applicable tax treaty with the United States, such payments generally would be subject to U.S. withholding tax. A “dividend equivalent” payment is (i) a substitute dividend payment made pursuant to a securities lending or a sale-repurchase transaction that (directly or indirectly) is contingent upon, or determined by reference to, the payment of a dividend from sources within the United States, (ii) a payment made pursuant to a “specified notional principal contract” that (directly or indirectly) is contingent upon, or determined by reference to, the payment of a dividend from sources within the United States, and (iii) any other payment d etermined by the IRS to be substantially similar to a payment described in the preceding clauses (i) and (ii). In the case of payments made after March 18, 2012, a dividend equivalent payment includes a payment made pursuant to any notional principal contract unless otherwise exempted by the IRS. Where the securities reference an interest in a fixed basket of securities or an index, such fixed basket or index will be treated as a single security. Where the securities reference an interest in a basket of securities or an index that may provide for the payment of dividends from sources within the United States, absent guidance from the IRS, it is uncertain whether the IRS would determine that payments under the securities are substantially similar to a dividend. If the IRS determines that a payment is substantially similar to a dividend, it may be subject to U.S. withholding tax, unless reduced by an applicable tax treaty.

10

U.S. Federal Estate Tax Treatment of Non-U.S. Holders

The securities may be subject to U.S. federal estate tax if an individual Non-U.S. Holder holds the securities at the time of his or her death. The gross estate of a Non-U.S. Holder domiciled outside the United States includes only property situated in the United States. Individual Non-U.S. Holders should consult their tax advisors regarding the U.S. federal estate tax consequences of holding the securities at death.

IRS Notice on Certain Financial Transactions

On December 7, 2007, the IRS and the Treasury Department issued Notice 2008-2, in which they stated they are considering issuing new regulations or other guidance on whether holders of an instrument such as the securities should be required to accrue income during the term of the instrument. The IRS and Treasury Department also requested taxpayer comments on (a) the appropriate method for accruing income or expense (e.g., a mark-to-market methodology or a method resembling the noncontingent bond method), (b) whether income and gain on such an instrument should be ordinary or capital, and (c) whether foreign holders should be subject to withholding tax on any deemed income accrual.

Accordingly, it is possible that regulations or other guidance may be issued that require holders of the securities to recognize income in respect of the securities prior to receipt of any payments thereunder or sale thereof. Any regulations or other guidance that may be issued could result in income and gain (either at maturity or upon sale) in respect of the securities being treated as ordinary income. It is also possible that a Non-U.S. Holder of the securities could be subject to U.S. withholding tax in respect of the securities under such regulations or other guidance. It is not possible to determine whether such regulations or other guidance will apply to your securities (possibly on a retroactive basis). You are urged to consult your tax advisor regarding Notice 2008-2 and its possible impact o n you.

Information Reporting Regarding Specified Foreign Financial Assets

The Act requires individual U.S. Holders with an interest in any “specified foreign financial asset” to file a report with the IRS with information relating to the asset, including the maximum value thereof, for any taxable year in which the aggregate value of all such assets is greater than $50,000 (or such higher dollar amount as prescribed by Treasury regulations). Specified foreign financial assets include any depository or custodial account held at a foreign financial institution; any debt or equity interest in a foreign financial institution if such interest is not regularly traded on an established securities market; and, if not held at a financial institution, (i) any stock or security issued by a non-U.S. person, (ii) any financial instrument or contract held for investment where the issuer or coun terparty is a non-U.S. person, and (iii) any interest in an entity which is a non-U.S. person. Depending on the aggregate value of your investment in specified foreign financial assets, you may be obligated to file an annual report under this provision. The requirement to file a report is effective for taxable years beginning after March 18, 2010. Penalties apply to any failure to file a required report. Additionally, in the event a U.S. Holder does not file the information report relating to disclosure of specified foreign financial assets, the statute of limitations on the assessment and collection of U.S. federal income taxes of such U.S. Holder for the related tax year may not close before such information is filed. You should consult your own tax advisor as to the possible application to you of this information reporting requirement and related statute of limitations tolling provision.

Backup Withholding and Information Reporting

A holder of the securities (whether a U.S. Holder or a Non-U.S. Holder) may be subject to information reporting requirements and to backup withholding with respect to certain amounts paid to such holder unless it provides a correct taxpayer identification number, complies with certain certification procedures establishing that it is not a U.S. Holder or establishes proof of another applicable exemption, and otherwise complies with applicable requirements of the backup withholding rules.

11

Supplemental Plan of Distribution (Conflicts of Interest)

Under the terms and subject to the conditions contained in a distribution agreement dated May 7, 2007, as amended, which we refer to as the distribution agreement, we have agreed to sell the securities to CSSU.

The distribution agreement provides that CSSU is obligated to purchase all of the securities if any are purchased.

CSSU proposes to offer the securities at the offering price set forth on the cover page of this pricing supplement and may receive underwriting discounts and commissions of $27.50 per $1,000 principal amount of securities. CSSU may re-allow some or all of the discount on the principal amount per security on sales of such securities by other brokers or dealers. If all of the securities are not sold at the initial offering price, CSSU may change the public offering price and other selling terms.

In addition, Credit Suisse International, an affiliate of Credit Suisse, may pay referral fees to some broker dealers of up to $5.00 per $1,000 principal amount of securities in connection with the distribution of the securities. An affiliate of Credit Suisse has paid or may pay in the future a fixed amount to broker dealers in connection with the costs of implementing systems to support these securities.

The agent for this offering, CSSU, is our affiliate. In accordance with FINRA Rule 5121, CSSU may not make sales in this offering to any of its discretionary accounts without the prior written approval of the customer. A portion of the net proceeds from the sale of the securities will be used by CSSU or one of its affiliates in connection with hedging our obligations under the securities.

We expect that delivery of the securities will be made against payment for the securities on or about February 28, 2011, which will be the fifth business day following the Trade Date for the securities (this settlement cycle being referred to as T+5). Under Rule 15c6-1 under the Securities Exchange Act of 1934, as amended, trades in the secondary market generally are required to settle in three business days, unless the parties to that trade expressly agree otherwise. Accordingly, purchasers who wish to trade the securities on the Trade Date or the following business day will be required to specify an alternate settlement cycle at the time of any such trade to prevent a failed settlement and should consult their own advisors.

For further information, please refer to “Underwriting (Conflicts of Interest)” in the accompanying product supplement.

12

Credit Suisse