Registration No. 333-218604-02

Dated October 2, 2018

Securities Act of 1933, Rule 424(b)(2)

UNDERLYING SUPPLEMENT TO THE PROSPECTUS SUPPLEMENT DATED JUNE 30, 2017

AND PROSPECTUS DATED JUNE 30, 2017

Credit Suisse AG

Medium-Term Notes

Underlying Supplement for

the Credit Suisse RavenPack AIS Balanced 5% ER Index

the Credit Suisse RavenPack Artificial Intelligence Sentiment Index

the Credit Suisse 10-Year U.S. Treasury Note Futures Index

the Credit Suisse 2-Year U.S. Treasury Note Futures Index

As part of our Medium-Term Notes program, Credit Suisse AG (“Credit Suisse”) from time to time may offer certain securities (the “securities”), linked to the performance of the Credit Suisse RavenPack AIS Balanced 5% ER Index, the Credit Suisse RavenPack Artificial Intelligence Sentiment Index, the Credit Suisse 10-Year U.S. Treasury Note Futures Index and the Credit Suisse 2-Year U.S. Treasury Note Futures Index. This prospectus supplement, which we refer to as an “underlying supplement,” describes each of these indices. The specific terms of each security offered will be described in the applicable pricing supplement and product supplement.

You should read this underlying supplement, the related prospectus and the related prospectus supplement both dated June 30, 2017, the applicable product supplement and pricing supplement, and any applicable free writing prospectus (each, an “offering document”) carefully before you invest. If the terms described in the applicable pricing supplement are different or inconsistent with those described herein (or with those described in the prospectus, prospectus supplement, any applicable product supplement or any applicable free writing prospectus), the terms described in the applicable pricing supplement will control.

The offering documents contain important risks and explanations relevant to the securities. For example, the titleartificial intelligence does not imply any form of actual intelligence, learning or comprehension.Similarly, the titlebalanced does not imply any risk adjusted diversified asset class allocation or actual balance among asset classes. Please refer to the “Selected Risk Considerations” section beginning on page 2, the “Risk Factors” section in the accompanying product supplement, the “Selected Risk Considerations” section in the applicable pricing supplement, “Foreign Currency Risks” on page 43 of the accompanying prospectus and the risk factors we describe in the most recent combined Annual Report on Form 20-F of Credit Suisse Group AG and Credit Suisse AG incorporated by reference herein for risks related to an investment in the securities, as applicable.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities or determined if this underlying supplement or any other offering document to which it relates is truthful or complete. Any representation to the contrary is a criminal offense.

Credit Suisse

The date of this underlying supplement is October 2, 2018.

table of contents

| THE SECURITIES | 1 |

| INDEX NAMES | 1 |

| SELECTED RISK CONSIDERATIONS | 2 |

| THE CREDIT SUISSE RAVENPACK AIS BALANCED 5% ER INDEX | 15 |

| THE CREDIT SUISSE RAVENPACK ARTIFICIAL INTELLIGENCE SENTIMENT INDEX | 29 |

| THE FIXED INCOME INDICES | 53 |

THE SECURITIES

We are responsible for the information contained and incorporated by reference in this underlying supplement. As of the date of this underlying supplement, we have not authorized anyone to provide you with different information, and we take no responsibility for any other information others may give you. We are not making an offer of these securities in any state where the offer is not permitted. You should not assume that the information in this document or other offering documents is accurate as of any date other than the date on the front of this document.

We are offering securities for sale in those jurisdictions in the United States where it is lawful to make such offers. The distribution of the offering documents and the offering of securities in some jurisdictions may be restricted by law. If you possess the offering documents, you should find out about and observe these restrictions. The offering documents are not an offer to sell the securities and are not soliciting an offer to buy the securities in any jurisdiction where the offer or sale is not permitted or where the person making the offer or sale is not qualified to do so or to any person to whom such offer or sale is not permitted. We refer you to the “Underwriting (Conflicts of Interest)” section of the applicable product supplement and the “Supplemental Plan of Distribution (Conflicts of Interest)” section of the applicable pricing supplement for additional information. If the terms described in the applicable pricing supplement are different or inconsistent with those described herein, the terms described in the applicable pricing supplement will control.

In the offering documents, unless otherwise specified or the context otherwise requires, references to “we,” “us” and “our” are to Credit Suisse and its consolidated subsidiaries, and references to “dollars” and “$” are to U.S. dollars.

INDEX NAMES

As used in this underlying supplement, we use the following defined terms for the following indices:

| · | The “Credit Suisse RavenPack AIS Balanced Index” means the Credit Suisse RavenPack AIS Balanced 5% ER Index. |

| · | The “Credit Suisse RavenPack AIS Index” means the Credit Suisse RavenPack Artificial Intelligence Sentiment Index. |

| · | The “Equity Index” means the excess return version of the Credit Suisse RavenPack AIS Index. |

| · | The “10Y Fixed Income Index” means the Credit Suisse 10-Year U.S. Treasury Note Futures Index. |

| · | The “2Y Fixed Income Index” means the Credit Suisse 2-Year U.S. Treasury Note Futures Index. |

| · | The “Fixed Income Indices” means the 10Y Fixed Income Index and the 2Y Fixed Income Index. |

| · | The “Component Indices” means the Equity Index and the Fixed Income Indices. |

1

SELECTED RISK CONSIDERATIONS

The following describes significant risks relating to the indices. We urge you to read the following information about these risks, together with the other information in the offering documents before investing in any securities related to the indices.

Selected Risk Factors Related to the Credit Suisse RavenPack AIS Balanced Index

The Credit Suisse RavenPack AIS Balanced Index is exposed to the Component Indices and thus the risks associated with the Component Indices. You should read the information set forth below concerning the Component Indices. Additionally, the Credit Suisse RavenPack AIS Balanced Index has its own index methodology that will affect the return on the securities. You should understand how the Credit Suisse RavenPack AIS Balanced Index is calculated, including the following risks related to the Credit Suisse RavenPack AIS Balanced Index.

The Credit Suisse RavenPack AIS Balanced Index Does Not Attempt to Achieve a Broad or “Balanced” Asset Class Diversification

The Credit Suisse RavenPack AIS Balanced Index is designed to provide exposure to a hypothetical “balanced” portfolio (consisting of the Equity Index and a momentum strategy-driven allocation of the Fixed Income Indices), while targeting a realized daily volatility of 5%. By “balanced” we mean the Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio may, under certain circumstances, include both equity exposure and fixed income exposure. “Balanced” is not meant to imply broad or balanced diversification across asset classes leading to risk mitigation because the Credit Suisse RavenPack AIS Balanced Index does not attempt to achieve a broad asset class diversification, and in some instances may have only equity exposure. You should not invest in securities that track the Credit Suisse RavenPack AIS Balanced Index if you are seeking asset class diversification of any kind.

The Credit Suisse RavenPack AIS Balanced Index Has Limited History and May Perform in Unexpected Ways

The Credit Suisse RavenPack AIS Balanced Index was launched on October 6, 2017. Therefore, the Credit Suisse RavenPack AIS Balanced Index has a limited performance history. Because the Credit Suisse RavenPack AIS Balanced Index is of recent origin with limited performance history, an investment linked to the Credit Suisse RavenPack AIS Balanced Index may involve a greater risk than an investment linked to one or more indices with an established record of performance. A longer history of actual performance through various economic and market conditions would have provided greater and more reliable information based on which an investor can assess the validity of the Credit Suisse RavenPack AIS Balanced Index’s investment thesis and index methodology. A longer history of actual performance would also have made the Credit Suisse RavenPack AIS Balanced Index more widely accepted in the market, and, consequently, less likely for the Index Sponsor to amend the Credit Suisse RavenPack AIS Balanced Index. However, any historical performance of the Credit Suisse RavenPack AIS Balanced Index is not an indication of how the Credit Suisse RavenPack AIS Balanced Index will perform in the future.

The Index Fee Will Adversely Affect Index Performance

An index fee of 0.50% per annum is deducted in the calculation of the Credit Suisse RavenPack AIS Balanced Index. The index fee will place a drag on the performance of the Credit Suisse RavenPack AIS Balanced Index, offsetting any appreciation of its portfolio, exacerbating any depreciation of its portfolio and causing the level of the Credit Suisse RavenPack AIS Balanced Index to decline steadily if the value of its portfolio remains relatively constant. The Credit Suisse RavenPack AIS Balanced Index will not participate in any appreciation of its portfolio unless it is sufficiently great to offset the negative effects of the index fee, and then only to the extent that the favorable performance of its portfolio is greater than the index fee (and subject to the volatility-targeting feature). As a result of this deduction, the level of the Credit Suisse RavenPack AIS Balanced Index may decline even if its portfolio appreciates.

2

The Credit Suisse RavenPack AIS Balanced Index May Fail to Maintain Its Volatility Target and May Experience Large Declines as a Result

The Credit Suisse RavenPack AIS Balanced Index adjusts its exposure to the portfolio of Component Indices as often as each Index Calculation Day in an attempt to maintain a target realized volatility of 5%. If the volatility of the portfolio of Component Indices increases, the Credit Suisse RavenPack AIS Balanced Index will reduce its exposure to the portfolio of Component Indices to the extent necessary to maintain a target realized volatility of 5%. However, because this exposure adjustment is backward-looking based on realized volatility over a prior period, because past volatility may not be predictive of future volatility and because there is a time lag between when volatility occurs and when the Credit Suisse RavenPack AIS Balanced Index rebalances its portfolio, there may be a time lag before a sudden increase in the volatility of the portfolio of Component Indices is sufficiently reflected in the exposure to the portfolio of Component Indices to result in a meaningful reduction in realized volatility. In the meantime, the Credit Suisse RavenPack AIS Balanced Index may experience significantly more than 5% volatility and, if the increase in volatility is accompanied by a decline in the value of the portfolio of Component Indices, the Credit Suisse RavenPack AIS Balanced Index may incur significant losses.

Furthermore, because the notional exposure to the portfolio cannot exceed 150% on each Index Calculation Day, the Credit Suisse RavenPack AIS Balanced Index may not be able to achieve or maintain the target volatility of 5%. If the realized volatility of the portfolio is less than 3.33%, the Credit Suisse RavenPack AIS Balanced Index will not achieve its target volatility of 5% even with 150% exposure to the portfolio.

The Volatility-Targeting Feature May Cause the Credit Suisse RavenPack AIS Balanced Index to Perform Poorly in Temporary Market Crashes

A temporary market crash is an event in which the volatility of the Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio spikes suddenly and the Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio declines sharply in value over a short period of time, but the decline is short-lived and the Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio soon recovers its losses. In this circumstance, although the value of the Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio after the recovery may return to its value before the crash, the level of the Credit Suisse RavenPack AIS Balanced Index may not fully recover its losses. This is because of the time lag that results from using historical realized volatility as the basis for the Credit Suisse RavenPack AIS Balanced Index’s volatility-targeting feature. Because of the time lag, the Credit Suisse RavenPack AIS Balanced Index may not meaningfully reduce its exposure to the Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio until the crash has already occurred, and by the time the reduced exposure does take effect, the recovery may have already begun. For example, if the Credit Suisse RavenPack AIS Balanced Index has 50% exposure to the decline in the Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio, and then reduces its exposure so that it has only 20% exposure to the recovery, the Credit Suisse RavenPack AIS Balanced Index will end up significantly lower after the crash and recovery than it was before the crash.

The Credit Suisse RavenPack AIS Balanced Index’s Volatility Target Is Arbitrary

Realized volatility is an historical measure of volatility and does not reflect volatility going forward. Realized volatility is not the same as implied volatility, which is an estimation of future volatility and may better reflect market volatility expectation. The Credit Suisse RavenPack AIS Balanced Index’s target realized volatility of 5% is one of many volatility targets that Credit Suisse could have selected and may not be the optimal target volatility for the Credit Suisse RavenPack AIS Balanced Index.

There are measurements that the Credit Suisse RavenPack AIS Balanced Index will deem to be meaningful to the index methodology that would not be deemed meaningful if a different volatility target were chosen. Alternatively, the Credit Suisse RavenPack AIS Balanced Index may be overly restrictive and treat as not meaningful changes in volatility that in fact contain meaningful information. Any fixed rule for measuring the volatility of the Credit Suisse RavenPack AIS Balanced Index will necessarily be a blunt tool and, accordingly, may have a high rate of inaccuracy. The particular ways in which the Credit Suisse RavenPack AIS Balanced Index operates may produce a lower return than other rules that could have been adopted for the volatility target. Thus, target realized volatility of 5% may not be the best measure for controlling the volatility of the Credit Suisse RavenPack AIS Balanced Index. Even if the Credit Suisse RavenPack AIS Balanced Index maintains its volatility target, the Credit Suisse RavenPack AIS Balanced Index may still incur significant losses.

3

The Credit Suisse RavenPack AIS Balanced Index’s Decay Factors Are Arbitrary

The Credit Suisse RavenPack AIS Balanced Index calculates two exponential moving averages of the variance of the Credit Suisse RavenPack AIS Index using a decay factor of 0.93 or 0.97. Approximately 99% of the weight included in an exponential moving average is derived (i) from the previous 64 trading days if the decay factor is 0.93 and (ii) from the previous 152 trading days if the decay factor is 0.97. However, these two decay factors were chosen arbitrarily by Credit Suisse out of many decay factors that Credit Suisse could have selected, and may not be the optimal decay factors to use for the Credit Suisse RavenPack AIS Balanced Index. The Credit Suisse RavenPack AIS Balanced Index may perform worse than if Credit Suisse had chosen different decay factors.

Calculating the Preliminary Weight of the Equity Index in the Credit Suisse RavenPack AIS Balanced Index’s Portfolio Based on the Arithmetic Average of the Short-Term and Long-Term Realized Volatilities of the Credit Suisse RavenPack AIS Index Is Arbitrary

We refer to the realized volatility (the square root of the applicable variance) calculated using the decay factor of 0.93 as the “short-term realized volatility” and the realized volatility calculated using the decay factor of 0.97 as the “long-term realized volatility,” calculated on an annualized basis. In calculating the preliminary weight of the Equity Index in the Credit Suisse RavenPack AIS Balanced Index’s portfolio, the Credit Suisse RavenPack AIS Balanced Index uses the average of these two different methods to calculate the historical realized volatility of the Credit Suisse RavenPack AIS Index to average out the risk that the long-term realized volatility is meaningfully different from the short-term realized volatility. For the purpose of determining the asset allocation of the portfolio, the historical realized volatility of the Credit Suisse RavenPack AIS Index on each day is equal to the arithmetic average of the short-term and long-term realized volatilities of the Credit Suisse RavenPack AIS Index on such day. However, this averaging of short-term realized volatility and long-term realized volatility is arbitrary and may dampen or heighten the calculated realized volatility of the Credit Suisse RavenPack AIS Index compared to other methods of calculating volatility such as implied volatility, which is an estimation of future volatility and may better reflect market volatility expectation.

There are measurements that the Credit Suisse RavenPack AIS Balanced Index will deem to be meaningful to the index methodology that would not be deemed meaningful if the Credit Suisse RavenPack AIS Balanced Index used a different method of calculating volatility. Alternatively, the Credit Suisse RavenPack AIS Balanced Index may be overly restrictive and treat as meaningful changes in volatility that in fact contain meaningful information. In this latter case, the Credit Suisse RavenPack AIS Balanced Index may retain exposure to the Equity Index after other methods would have dictated allocating exposure to the Fixed Income Indices. Any fixed rule for determining a change to the portfolio of the Credit Suisse RavenPack AIS Balanced Index will necessarily be a blunt tool and, accordingly, may have a high rate of inaccuracy. The particular ways in which the Credit Suisse RavenPack AIS Balanced Index operates may produce a lower return than other rules that could have been adopted for the identification of the volatility of the Equity Index. There is nothing inherent in the particular methodology used by the Credit Suisse RavenPack AIS Balanced Index that makes it a more or less accurate predictor of the volatility of the Equity Index. It is possible that the rules used by the Credit Suisse RavenPack AIS Balanced Index may not identify the volatility of the Equity Index as effectively as other rules that might have been adopted, or at all.

The Volatility-Targeting Feature Could Cause the Credit Suisse RavenPack AIS Balanced Index to Significantly Underperform Its Portfolio in Rising Equity Markets

The performance of the Credit Suisse RavenPack AIS Balanced Index will be based on the performance of the Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio, but only to the extent that the Credit Suisse RavenPack AIS Balanced Index has exposure to the Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio. The Credit Suisse RavenPack AIS Balanced Index will have less than 100% exposure to the Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio at any time when realized volatility of the Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio is greater than the Credit Suisse RavenPack AIS Balanced Index’s volatility target of 5%. An exposure of less than 100% would mean that the Credit Suisse RavenPack AIS Balanced Index will participate in less than the full performance of the Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio, and the difference between 100% and that exposure would be hypothetically allocated to non-remunerating cash, on which no interest or other return will accrue. For example, if the realized volatility of the Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio 10%, then the Credit Suisse RavenPack AIS Balanced Index would have 50% exposure to the performance of the Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio (the 5% volatility target divided by the 10% realized volatility). An

4

exposure of 50% would mean that the Credit Suisse RavenPack AIS Balanced Index would participate in only 50% of the performance of the Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio. In this example, if the Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio were to appreciate by 2%, the Credit Suisse RavenPack AIS Balanced Index would only appreciate by 1% (which is 50% of 2%), minus the index fee. This limited exposure to the performance of the Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio means that the Credit Suisse RavenPack AIS Balanced Index is likely to underperform the Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio in rising equity markets. The index fee will exacerbate this underperformance.

A Significant Portion of the Credit Suisse RavenPack AIS Balanced Index May Be Hypothetically Allocated to Non-remunerating Cash, Which May Dampen Returns

At any time when the Credit Suisse RavenPack AIS Balanced Index has less than 100% exposure to the Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio, a portion of the Credit Suisse RavenPack AIS Balanced Index (corresponding to the difference between the exposure to the Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio and 100%) will be hypothetically allocated to non-remunerating cash and will not accrue any interest or other return. In the example in the previous risk factor, where the Credit Suisse RavenPack AIS Balanced Index has 50% exposure to the Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio, the remaining 50% of the Credit Suisse RavenPack AIS Balanced Index would be hypothetically allocated to non-remunerating cash. A significant hypothetical allocation to cash will significantly reduce the Credit Suisse RavenPack AIS Balanced Index’s potential for gains. In addition, the index fee will be deducted from the entire Credit Suisse RavenPack AIS Balanced Index, including the portion hypothetically allocated to non-remunerating cash. As a result, after taking into account the deduction of the index fee, any portion of the Credit Suisse RavenPack AIS Balanced Index that is hypothetically allocated to non-remunerating cash will experience a net decline at a rate equal to the index fee.

The Credit Suisse RavenPack AIS Balanced Index Is Exposed to Risks Related to the Component Indices

The Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio may include exposure to both the Credit Suisse RavenPack AIS Index and the Fixed Income Indices. The Credit Suisse RavenPack AIS Balanced Index’s performance will be directly affected by the performance of the Component Indices and the risks related to the Component Indices.

The Credit Suisse RavenPack AIS Balanced Index’s Allocation Methodology May Not Be Successful If the Equity Component and the Fixed Income Components Decline at the Same Time

The Credit Suisse RavenPack AIS Balanced Index’s allocation methodology is premised on the Equity Index and the Fixed Income Indices being either uncorrelated or inversely correlated. The thesis underlying the Credit Suisse RavenPack AIS Balanced Index’s allocation methodology is that, if the Credit Suisse RavenPack AIS Balanced Index determines that the Equity Index is likely to decline, the Credit Suisse RavenPack AIS Balanced Index may avoid losses and even potentially generate positive returns by allocating exposure to the Fixed Income Indices instead of the Equity Index. If, however, the Fixed Income Indices also decline, then the Credit Suisse RavenPack AIS Balanced Index will decline regardless of whether its exposure is allocated to the Equity Index or the Fixed Income Indices. It is also possible that the Fixed Income Indices decline at a greater rate than the Equity Index. If the Equity Index and the Fixed Income Indices tend to decline at the same time—in other words, if they prove to be positively correlated—the Credit Suisse RavenPack AIS Balanced Index’s allocation methodology will not be successful, and the Credit Suisse RavenPack AIS Balanced Index may experience significant declines.

The Credit Suisse RavenPack AIS Balanced Index May Have Significant Exposure to the Fixed Income Indices, Which Have Limited Return Potential and Significant Downside Potential, Particularly in Times of Rising Interest Rates

The Fixed Income Indices offer only limited return potential, which in turn limits the return potential of the Credit Suisse RavenPack AIS Balanced Index. The U.S. Treasury note futures contracts included in the Fixed Income Indices track the value of futures contracts on U.S. Treasury notes, which may be subject to significant fluctuations and declines. In particular, the value of a futures contract on a U.S. Treasury note is likely to decline if there is a general rise in interest rates. To the extent the Credit Suisse RavenPack AIS Balanced Index is allocated to the Fixed Income Indices, you could suffer a loss in such market conditions.

5

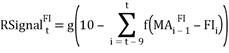

The ten-year U.S. Treasury note futures contracts may perform negatively from time to time. The Credit Suisse RavenPack AIS Balanced Index uses a “Risk Signal” to capture the presence of a downward trend in the performance of the 10Y Fixed Income Index. If the Risk Signal is off, the Credit Suisse RavenPack AIS Balanced Index will allocate all of the Fixed Income Exposure (as defined herein) to the 10Y Fixed Income Index. The Risk Signal is turned on if the performance of the 10Y Fixed Income Index over the previous ten Index Calculation Days (as defined herein) is lower than its historical moving average, indicating that the risk of future negative performance in ten-year U.S. Treasury note futures contracts is rising. In this scenario, the Credit Suisse RavenPack AIS Balanced Index will allocate half of the Fixed Income Exposure to the 10Y Fixed Income Index and the remaining half to the 2Y Fixed Income Index, which generally has a lower volatility than the 10Y Fixed Income Index. However, if both Fixed Income Indices perform negatively, this allocation strategy may adversely affect the performance of the Credit Suisse RavenPack AIS Balanced Index. Additionally, the 2Y Fixed Income Index may perform worse than the 10Y Fixed Income Index in certain market conditions (e.g., at a time of negative interest rates); in these conditions, the Credit Suisse RavenPack AIS Balanced Index may perform worse than if the Fixed Income Exposure was only allocated to the 10Y Fixed Income Index.

Selected Risk Factors Related to the Credit Suisse RavenPack AIS Index

The Credit Suisse RavenPack AIS Index is a Component Index of the Credit Suisse RavenPack AIS Balanced Index. However, the Credit Suisse RavenPack AIS Balanced Index has its own index methodology. You should understand how the Credit Suisse RavenPack AIS Index is calculated, including the following risks related to the Credit Suisse RavenPack AIS Index.

The Credit Suisse RavenPack AIS Index Is Called “Artificial Intelligence” Only in the Limited Sense that It Is Based on a Static Algorithm

RavenPack has developed an algorithm, licensed by CSI for use by the Credit Suisse RavenPack AIS Index, that is designed to assign scores to news items that discuss companies (the “RPNA Algorithm”). Because the RPNA Algorithm does not aim to comprehend news items, it cannot necessarily predict human or the market classification or sentiment of a particular news item. For example, the RPNA Algorithm might not process enthusiasm, nuance, sarcasm, satire or other types of writing that a human could understand. The RPNA Algorithm also does not learn from news items it processes or adapt to its environment and, as a static algorithm, will continue to use the same mathematical rules to process news items, even as news develops over time. The RPNA Algorithm is called “artificial intelligence” only in the limited sense that it applies static algorithmic rules to language to produce a mathematical result that might indicate relevance, novelty or a given sentiment about a company. You will not benefit from an algorithm that has the capability to learn, grow or adapt to new information.

RavenPack Exercised Discretion in Developing the RPNA Algorithm

The mathematical rules used by the RPNA Algorithm were created by RavenPack in its sole discretion. Consequently, the way the RPNA Algorithm processes news items reflects decisions RavenPack made about the RPNA Algorithm’s construction. For example, prior to assigning a news item an Event Score, the RPNA Algorithm attempts to identify the event category and event discussed in the news item by algorithmically processing words in that news item. RavenPack, in its discretion, created these event categories and events and designed the methods by which different default Event Scores were applied to each event. A news item’s Event Score is based on the event assigned to it by the RPNA Algorithm and how the specific words within that news item alters the default Event Score.

RavenPack created 27 events relating to revenues and 65 events relating to earnings, and assigned default Event Scores to each event in one of two ways. First, RavenPack included some events in surveys given to Event Assessors (the “Survey Events”) and then used the survey results to assign default Event Scores to the Survey Events. Second, because RavenPack regarded each remaining event (the “Non-Survey Events”) as similar a Survey Event (regardless of whether that Survey Event was included in the “REVENUES” or “EARNINGS” event categories), RavenPack used its discretion to model each Non-Survey Event to have the same default Event Score as the relevant Survey Event and assigned the Non-Survey Event the same default Event Score as that Survey Event. As a result, certain Non-Survey Events in the “REVENUES” and “EARNINGS” event categories are treated by the RPNA Algorithm as identical to Survey Events both within and outside of the “REVENUES” and “EARNINGS” event categories.

6

This approach to categorization, which forms the framework under which the RPNA Algorithm produces Event Scores, may not yield the same result as human or the market categorization of a particular event. For example, RavenPack assigned the event “same-store-sales” the same default Event Score as the event “revenues.” However, when evaluating a particular company, news about same store sales may be more significant than news about revenues (e.g., changes in revenue as a result of an acquisition may not be as significant as changes in same store sales).

The rules RavenPack created for the RPNA Algorithm may not be the optimal rules for determining the sentiment of news items. Discretionary judgments by RavenPack in the development of the RPNA Algorithm, of which the foregoing are only examples thereof, may cause the RPNA Algorithm to overestimate, underestimate or misjudge the impact of news items on the performance of a Component Stock, which may adversely affect the performance of the Credit Suisse RavenPack AIS Index, and therefore the value of your securities.

The Event Assessors Had Limited Expertise

The Event Scores assigned to new items are based in part on surveys completed by the Event Assessors, who were selected by RavenPack to give opinions based on RavenPack’s view of their expertise in finance and/or economics. The Event Assessors might not have expertise in other industries that may relate to news items, such as biomedicine, engineering or technology. As a result, the Event Assessors may have lacked the requisite expertise or foresight to accurately judge the impact of events on the performance of Component Stocks in specialized industries, which may be reflected in the RPNA Algorithm’s treatment of news items. The Event Assessors may also not have been diverse and may have shared similar professional backgrounds, which may have caused them to be biased in how they interpret events. The biases and limitations present in the data provided by the Event Assessors may cause the RPNA Algorithm to overestimate, underestimate or misjudge the impact of news items on the performance of a Component Stock, which may adversely affect the performance of the Credit Suisse RavenPack AIS Index, and therefore the value of your securities.

News Items Used to Calculate the Credit Suisse RavenPack AIS Index May Be Incomplete, Biased or Inaccurate

The Credit Suisse RavenPack AIS Index and related sector weightings are calculated based on RPNA Algorithm scores assigned to a limited number of news items. Any news items used to calculate the Credit Suisse RavenPack AIS Index and related sector weightings may contain misstatements, inaccuracies or omissions, which may be material to the performance of the relevant issuer. Furthermore, any news items used to calculate the Credit Suisse RavenPack AIS Index and related sector weightings may include derivative coverage of primary releases by corporate issuers or public agencies (in lieu of such primary releases), as well as articles written by opinion journalists, which may lack objectivity. Inaccurate or biased reporting, as well as the omission of news items produced by alternative news sources, may impact the quarterly weightings of the S&P Sector TR Indices. Any of these limitations could adversely affect the performance of the Credit Suisse RavenPack AIS Index, and therefore the value of your securities.

The Scoring and Classification of News Items May Be Materially Inaccurate

The scoring and classification of news items about individual companies (or their affiliates) by the RPNA Algorithm may not accurately reflect the impact such news items have on the performance of an S&P Sector TR Index as a whole, which may adversely affect the performance of the Credit Suisse RavenPack AIS Index, and therefore the value of your securities. Because the RPNA Algorithm does not aim to comprehend news items, it cannot necessarily predict human or the market classification or sentiment of a particular news item. The RPNA Algorithm also does not learn from news items it processes or adapt to its environment and, as a static algorithm, will continue to use the same mathematical rules to process news items, even as news develops over time.

In particular, the RPNA Algorithm may produce inaccurate results by (1) categorizing a news item within an event category that a human or the market generally would assign to a different category or (2) assigning a Relevance Score, Novelty Score or Sentiment Score to a news item that either over- or under-estimates the relevance, novelty or sentiment that a human or the market generally would associate with such news item. It is important to understand the RPNA Algorithm categorizes news items and produces Relevance Scores, Novelty Scores and Event Scores based solely on static, algorithmic rules applied to the text of news items without comprehension. We highlight below some of those risks associated with this classification and scoring system.

7

Misclassification of News Items

While many different types of news items may be relevant to the performance of the S&P Sector TR Indices, the Credit Suisse RavenPack AIS Index only considers news items the RPNA Algorithm has algorithmically mapped to the “REVENUES” or “EARNINGS” event categories. These event categories were created by RavenPack. The RPNA Algorithm may classify a news item to an event category that is different than what a human or the market generally would have chosen. For example, a news item discussing a particular product of a Component Stock’s issuer may be mapped as “REVENUES” because the news item might discuss how that product has historically impacted revenues. Similarly, a news item discussing how a Component Stock’s issuer exceeded earnings expectations by a wide margin may not be classified as “EARNINGS” because the news item focused on the financial restructuring of that Component Stock’s issuer’s affiliate or the market generally. Any inaccuracies or shortcomings in the manner in which the RPNA Algorithm classifies news items may adversely affect the performance of the Credit Suisse RavenPack AIS Index, and therefore the value of your securities.

Inaccurate Relevance Scores, Novelty Scores and Event Scores

The RPNA Algorithm will assign each news item it processes a Relevance Score, a Novelty Score and an Event Score. The scores the RPNA Algorithm assigns to news items will impact the composition of the Credit Suisse RavenPack AIS Index. The RPNA Algorithm may over- or under-emphasize the relevance of a particular news item or its overall sentiment in a way that could be materially inaccurate relative to how the market reacts to that news item. Various algorithmic factors, such as word choice, syntax and morphology may produce counter-intuitive, inaccurate or simply wrong results, all of which may materially and adversely affect the performance of the Credit Suisse RavenPack AIS Index. By way of example only, some ways the RPNA Algorithm may produce inaccurate results include:

| · | Producing Event Scores that over- or under-emphasize market sentiment because of the idiosyncratic word choice, placement or syntax in a given news item; |

| · | Producing materially different Event Scores for news items that the market may regard as similar (see, e.g., the examples in “The Credit Suisse RavenPack Artificial Intelligence Sentiment Index—Overview—Event Score—Examples of Event Scores”); |

| · | Assigning a Relevance Score of 100 based on a news item relating to a minor affiliate of a Component Stock’s issuer; |

| · | Failing to assign a Relevance Score of 100 where a news item reports on news that is highly relevant to a particular Component Stock’s issuer’s business or financial results; or |

| · | Producing Event Scores that attempt to match actual earnings or revenue figures with figures estimated by market participants. |

The foregoing examples are not meant to be exhaustive. They illustrate the risks of the RPNA Algorithm applying a static, rules-based methodology as a proxy for market comprehension and sentiment. Any of the RPNA Algorithm’s shortcomings may cause the RPNA Algorithm to overestimate, underestimate or misjudge the impact of news items on the performance of an S&P Sector TR Index as a whole, which may adversely affect the performance of the Credit Suisse RavenPack AIS Index, and therefore the value of your securities.

The Credit Suisse RavenPack AIS Index Is Calculated Based on Third-Party Data, Which May Become Unavailable

The Credit Suisse RavenPack AIS Index is calculated based on scores assigned to news items by the RPNA Algorithm. The RPNA Algorithm is owned and operated by RavenPack, which is not affiliated with Credit Suisse. The scores assigned to news items by the RPNA Algorithm may become temporarily unavailable due to data outages resulting from external factors or technical malfunctions in the RPNA Algorithm’s software, which may prevent the RPNA Algorithm from producing such scores in a timely manner and, thus, may prevent Credit Suisse from calculating the Credit Suisse RavenPack AIS Index as anticipated. The temporary unavailability of data produced by the RPNA Algorithm may result in Credit Suisse International postponing publication of the Credit Suisse RavenPack AIS Index or Credit Suisse International exercising its discretion, as Index Calculation Agent, to determine the level of the Credit Suisse RavenPack AIS Index, and any such postponement or exercise of discretion by the Index Calculation Agent may be adverse to your interests as a holder of the securities. Furthermore, such scores may become permanently unavailable if, for instance, the sources that publish news items used to calculate the Credit Suisse RavenPack AIS Index are discontinued or if our annual license to use data produced by the RPNA

8

Algorithm is not renewed, in which case the method of calculating the Credit Suisse RavenPack AIS Index could be materially altered in the Index Calculation Agent’s sole discretion and/or the calculation of the Credit Suisse RavenPack AIS Index could be suspended. Any such loss of Credit Suisse’s ability to use RPNA Algorithm scores in calculating the Credit Suisse RavenPack AIS Index, whether on a temporary or permanent basis, could adversely affect the performance of the Credit Suisse RavenPack AIS Index, and therefore the value of your securities.

You Will Not Benefit from Any Updates to the RPNA Algorithm

From time to time, RavenPack may publish new versions of the RPNA Algorithm for analyzing and scoring news items, which may contain improvements or refinements to the last version of the RPNA Algorithm. However, Credit Suisse will continue to calculate and publish the Credit Suisse RavenPack AIS Index based on scoring for news items using Version 4.0 of the RPNA Algorithm, as described in this underlying supplement. Accordingly, any improvements or refinements to the RPNA Algorithm that are published after Version 4.0 will not be reflected in the Credit Suisse RavenPack AIS Index. The Credit Suisse RavenPack AIS Index will continue to be published using Version 4.0 of the RPNA Algorithm notwithstanding any subsequent updates to the RPNA Algorithm, which may adversely affect the performance of the Credit Suisse RavenPack AIS Index, and therefore the value of your securities.

Use of RavenPack Data by Third Parties May Adversely Affect the Performance of the Credit Suisse RavenPack AIS Index

The scores produced by the RPNA Algorithm that are used in calculating the Credit Suisse RavenPack AIS Index, as well as the methodology for analyzing news items and producing such data, are proprietary to RavenPack and confidential. RavenPack sells rights to use RPNA Algorithm data to third parties, and Credit Suisse has no control over the actions of any such third parties. Other users of RPNA Algorithm data may initiate trades in, or in instruments linked or related to, the Component Stocks based on such data. Such trades may be executed in advance of any consequent adjustment or rebalancing of the Credit Suisse RavenPack AIS Index, and may adversely affect the performance of the Credit Suisse RavenPack AIS Index. Furthermore, the RPNA Algorithm methodology is described in this underlying supplement, which is publicly available. Any loss of confidentiality of RavenPack data or proprietary technology resulting from this public disclosure or otherwise may result in third parties executing trading strategies based on such data or similar data, which may adversely affect the performance of the Credit Suisse RavenPack AIS Index, and therefore the value of your securities.

Because of Arbitrary Methodological Rules, the Credit Suisse RavenPack AIS Index Excludes News Items that May Be Significant to the Performance of Companies in the S&P Sector TR Indices

The Credit Suisse RavenPack AIS Index is designed to maintain exposure to a hypothetical portfolio of at least four S&P Sector TR Indices. The Credit Suisse RavenPack AIS Index selects these S&P Sector TR Indices based on scores assigned to news items about companies in the S&P Sector TR Indices, as calculated by the RPNA Algorithm. However, due to arbitrary methodological rules, the news items considered by the Credit Suisse RavenPack AIS Index may not include all news items that are relevant to the performance of companies in the S&P Sector TR Indices. For example, an event that is not detected in the headline of a news item by the RPNA Algorithm will not be considered by the Credit Suisse RavenPack AIS Index, even if such event is covered in the body of such news item. The methodological limitations imposed by the Credit Suisse RavenPack AIS Index on the RPNA Algorithm exclude news items:

| · | not produced by Dow Jones Newswires, The Wall Street Journal, Barron’s or MarketWatch; |

| · | with a Relevance Score less than 100; |

| · | with a Novelty Score less than 100; |

| · | not mapped by the RPNA Algorithm to either the “REVENUES” or “EARNINGS” event category; or |

| · | with a Modified EScore greater than -0.6 but below 0.6. |

Any one of these rules (or combination of rules) could cause the Credit Suisse RavenPack AIS Index to fail to consider news items that the market generally considers significant to the performance of companies in the S&P Sector TR Indices. For example, the news item discussed in “The Credit Suisse RavenPack Artificial Intelligence Sentiment Index—Overview—Event Score—Examples of Event Scores” herein with the headline “MW Company Q4 revenue $20.20 bln vs. $18.11 bln; Service consensus $20.08 bln” would receive a Modified EScore of 0.02, calculated as follows: 0.02 x 51 – 1 = 0.02. Because this Modified EScore is greater than -0.6 but below 0.6, this

9

news item should be excluded from the calculation of the Average EScore for this component stock, even if the market generally considered this news item significant to the performance of this company.

There is nothing inherent in the particular methodology used by the Credit Suisse RavenPack AIS Index that makes it a more or less accurate selector of news items that are relevant to the performance of companies in the S&P Sector TR Indices. It is possible that the rules used by the Credit Suisse RavenPack AIS Index may not identify significant news items as effectively as other rules that might have been adopted. The Credit Suisse RavenPack AIS Index will perform differently, and possibly worse, than if Credit Suisse has chosen different rules relating to the selection of news items.

The Credit Suisse RavenPack AIS Index Has Limited History and May Perform in Unexpected Ways

The Credit Suisse RavenPack AIS Index was launched on September 29, 2017. Therefore, the Credit Suisse RavenPack AIS Index has a limited performance history. Because the Credit Suisse RavenPack AIS Index is of recent origin with limited performance history, an investment linked to the Credit Suisse RavenPack AIS Index may involve a greater risk than an investment linked to one or more indices with an established record of performance. A longer history of actual performance through various economic and market conditions would have provided greater and more reliable information based on which an investor can assess the validity of the Credit Suisse RavenPack AIS Index’s investment thesis and index methodology. A longer history of actual performance would also have made the Credit Suisse RavenPack AIS Index more widely accepted in the market, and, consequently, less likely for the Index Sponsor to amend the Credit Suisse RavenPack AIS Index. However, any historical performance of the Credit Suisse RavenPack AIS Index is not an indication of how the Credit Suisse RavenPack AIS Index will perform in the future.

Selected Risk Factors Related to the Fixed Income Indices

The Fixed Income Indices are Component Indices of the Credit Suisse RavenPack AIS Balanced Index. However, the Fixed Income Indices have their own index methodology that will affect the return on the securities independently of the Credit Suisse RavenPack AIS Balanced Index. You should understand how the Fixed Income Indices are calculated, including the following risks related to the Fixed Income Indices.

The Securities Do Not Offer Direct Exposure to the Spot Prices of U.S. Treasury Notes

The Fixed Income Indices are linked to U.S. Treasury note futures contracts, not the underlying U.S. Treasury notes (nor their respective spot prices). The price of a U.S. Treasury note futures contract reflects the expected value of the underlying U.S. Treasury note upon delivery in the future, whereas the spot price of a U.S. Treasury note reflects the immediate delivery value of the U.S. Treasury note.

A variety of factors can lead to a disparity between the expected future price of an underlying asset and the spot price at a given point in time, such as expectations concerning supply and demand for the underlying asset. The price movements of a futures contract are typically correlated with the movements of the spot price of the underlying asset, but the correlation is generally imperfect and price movements in the spot market may not be reflected in the futures market (and vice versa). Accordingly, the securities may underperform a similar investment that is linked to the spot prices or current levels, as applicable, of the underlying assets upon which the U.S. Treasury note futures contracts included in the Fixed Income Indices are based.

The Level of the Fixed Income Indices May Be Calculated and Published at Different Times than the Prices of the U.S. Treasury Note Futures Contracts

The level of a Fixed Income Index may not correspond to the price of the relevant U.S. Treasury note futures contracts due to differences in timing. The prices of U.S. Treasury Note Futures Contracts may be calculated and published at times when the levels of the Fixed Income Indices are not calculated and published. Consequently, there could be market developments or other events that cause or exacerbate the difference between the price of the relevant U.S. Treasury note futures contracts and the level of the Fixed Income Indices.

10

Higher Future Prices of U.S. Treasury Notes Relative to Their Current Prices, or “Contango,” May Lead to a Decrease in the Level of the Fixed Income Indices and the Amount Payable on the Securities

The Fixed Income Indices are composed of index components, each of which consists of or includes futures contracts. As these futures contracts come to expiration, they are replaced by contracts that have a later expiration. For example, a contract purchased and held in June may specify a September expiration. As time passes, the contract expiring in September is replaced by a contract for delivery in December. This is accomplished by selling the September contract and purchasing the December contract. This process is referred to as “rolling.” Excluding other considerations, if the market for these contracts is in “contango,” where the prices are higher in the distant delivery months than in the nearer delivery months, the sale of the September contract would take place at a price that is lower than the price of the December contract, thereby creating a negative “carry” or “roll yield,” as the case may be. By contrast, if the market for these contracts is in “backwardation,” where the prices are lower in the distant delivery months than in the nearer delivery months, the sale of the September contract would take place at a price that is higher than the price of the December contract, thereby creating a positive “carry” or “roll yield,” as the case may be. The remaining time to expiration may also be a factor. For example, a U.S. Treasury note futures contract with a remaining term of one month may have a higher negative roll yield as compared to a futures contract with a remaining term of six months. Finally, some futures contracts may be in contango whereas other futures contracts on the same commodity may be in backwardation. Any of these circumstances could cause a decline in the level of a Fixed Income Index and therefore the value of and return on your securities.

The U.S. Treasury notes underlying the U.S. Treasury note futures contracts have at times in the past traded in contango and may do so in the future. Because carry and roll yields are considered in the calculation of the index components and the Fixed Income Indices, the presence of contango in the futures markets could result in negative “carry” or “roll yields,” as the case may be, which could adversely affect the level of the index components to which the Fixed Income Indices have exposure, and accordingly, the level of the Fixed Income Indices and amount payable upon repurchase or at maturity of the securities.

The Securities Are Subject to Interest Rate Risk

The level of each U.S. Treasury note futures contract is affected by the market prices of the underlying U.S. Treasury notes, which may be volatile and are significantly influenced by a number of factors, particularly the yields on the underlying sovereign bonds as compared to current market interest rates. Interest rates are subject to volatility due to a variety of factors, including performance of capital markets.

Fluctuations in interest rates could affect the level of the U.S. Treasury Note futures contracts, the levels of the Fixed Income Indices and the value of and amount payable upon repurchase or at maturity of the securities.

General Risks Related to the Indices

The following risks relate to the Credit Suisse RavenPack AIS Balanced Index, the Credit Suisse RavenPack AIS Index and the Fixed Income Indices.

Past Performance of the Indices Is No Guide to Future Performance and There Is No Assurance that the Strategies on Which the Indices Are Based Will Be Successful

The actual performance of the indices over the term of the securities, as well as the amount payable upon early redemption or at maturity, may bear little relation to the historical values of the indices, or to the hypothetical return examples set forth elsewhere in the applicable pricing supplement. We cannot predict the future performance of the indices, and there is no assurance that the strategies on which the indices are based will be successful in producing positive returns.

There Can Be No Assurance that the Performance of the Indices over Time Will Approximate the Return of the Relevant Strategy or Any Other Strategy

The indices are each designed to pursue a particular strategy. The composition of the indices at any time is determined by the allocation methodology described in this underlying supplement, and is not actively managed by the Index Sponsor. There can be no assurance that the performance of the indices over time will approximate the return of the relevant strategy or any other strategy.

11

You Will Not Have Any Rights in Any Stocks or U.S. Treasury Note Futures Contracts Included in the Indices

As an owner of the securities, you will not have rights that holders of any stocks or U.S. Treasury note futures contracts included in the indices may have. The securities will be paid in cash, and you will have no right to receive any payment or delivery in respect of any stocks or U.S. Treasury note futures contracts.

Owning the Securities Is Not the Same as Directly Owning the Stocks or U.S. Treasury Note Futures Contracts Included in the Indices

Your return on the securities will not reflect the return you would have realized on a direct investment in the stocks or U.S. Treasury note futures contracts, as applicable, included in any index. For example, as an investor in the securities, you will not have rights to receive dividends or other distributions or any other rights, including voting rights, with respect to any stocks included in any index. The calculation agent will calculate the amount payable to you at maturity by reference to the level of the applicable index on the relevant valuation date(s), and will not include the amount of any such dividend payments or other distributions. Therefore, the return on your investment, which will be determined as set forth in the applicable pricing supplement, is not the same as the total return based on the purchase of any stocks or U.S. Treasury note futures contracts, as applicable, included in any index.

Suspension or Disruptions of Market Trading in Stocks or Futures Contracts May Adversely Affect the Value of the Securities

Stock markets and futures markets are subject to temporary distortions or other disruptions due to various factors, including the lack of liquidity in the markets, the participation of speculators, and government regulation and intervention. In addition, futures markets may have regulations that limit the amount of fluctuation in some futures contract prices that may occur during a single business day. These limits are generally referred to as “daily price fluctuation limits” and the maximum or minimum price of a contract on any given day as a result of these limits is referred to as a “limit price.” Once the limit price has been reached in a particular contract, no trades may be made at a price beyond the limit, or trading may be limited for a set period of time. Limit prices have the effect of precluding trading in a particular contract or forcing the liquidation of contracts at potentially disadvantageous times or prices. These circumstances could affect the level of the index components and therefore could adversely affect the level of the indices and the value of the securities.

We and Our Affiliates May Have Economic Interests Adverse to Those of the Holders of the Securities

Because our affiliates are acting as the calculation agent for the securities, the Index Calculation Agent and the Index Sponsor, potential conflicts of interest may exist between our affiliates and you, including with respect to certain determinations and judgments that they must make in determining amounts due to you, either at maturity or upon early redemption of the securities or the composition or methodology of the indices.

For example, the Index Sponsor may adjust the method of calculating any index if it reasonably determines that the publication of such index is discontinued and there is no successor index. The Index Sponsor may also adjust the method of calculating any index if it reasonably determines that such index or the method of calculating such index has been changed at any time in any significant respect.

Therefore, potential conflicts of interest may exist between our affiliates and you, including with respect to certain determinations and judgments that they must make in determining amounts due to you, either at maturity or upon redemption of the securities or the composition or methodology of the indices.

In addition, Credit Suisse and other affiliates of ours expect to engage in trading activities related to the index components or futures contracts referenced by the index components, futures or options on the index components or the indices, or other derivative instruments with returns linked to the performance of index components or the indices, for their accounts and for other accounts under their management. Credit Suisse and these affiliates may also issue or underwrite or assist unaffiliated entities in the issuance or underwriting of other securities or financial instruments linked or related to the performance of the indices or the index components. By introducing competing products into the marketplace in this manner, we or one or more of our affiliates could adversely affect the value of the securities. To the extent that we or one of our affiliates serves as issuer, agent or underwriter for such securities or financial instruments, our or their interests with respect to such products may be adverse to those of the holders of

12

the securities. Any of these trading activities could potentially affect the level of the indices and, accordingly, could affect the value of the securities and the amount payable to you at maturity or upon early redemption, as applicable.

We or our affiliates may currently or from time to time engage in business with the issuers of the index components, including extending loans to, making equity investments in, or providing advisory services to them, including merger and acquisition advisory services. In the course of this business, we or our affiliates may acquire nonpublic information about the companies, and we will not disclose any such information to you. In addition, we or one or more of our affiliates may publish research reports or otherwise express views or provide recommendations about the issuers of the index components. Any such views or recommendations may be inconsistent with purchasing or holding the securities. Any prospective purchaser of securities should undertake such independent investigation of each company whose stock is included as an index component as in its judgment is appropriate to make an informed decision with respect to an investment in the securities.

With respect to any of the activities described herein, neither Credit Suisse nor its affiliates have any obligation to take the needs of any buyer, seller or holder of the securities into consideration at any time.

Adjustments to the Indices or to the Index Components Could Adversely Affect the Securities

The Index Sponsor is responsible for calculating and maintaining the indices. The Index Sponsor can make methodological changes that could change the level of the indices at any time. The Index Sponsor may discontinue or suspend calculation or dissemination of the indices.

If one or more of these events occurs, the calculation of the amount payable at maturity or upon repurchase could be adjusted to reflect such event or events. Consequently, any of these actions could adversely affect the amount payable at maturity or repurchase and/or the market value of the securities. All determinations and adjustments to be made by the Index Calculation Agent with respect to the level of the indices may be made in the Index Calculation Agent’s reasonable discretion. The Index Calculation Agent will make all determinations and adjustments such that, to the greatest extent possible in the Index Calculation Agent’s reasonable discretion, the fundamental economic terms of the indices are equivalent to those immediately prior to the event requiring or permitting such determinations or adjustments.

See “—We and Our Affiliates May Have Economic Interests Adverse to Those of the Holders of the Securities” herein for a discussion of certain conflicts of interest that may arise between CSI in its capacity as Index Sponsor and you.

You Will Have No Rights Against the Entities with Discretion over the Indices or the Index Components

As an owner of the securities, you will have no rights against the Index Sponsor or the Index Calculation Agent even though the amount you receive at maturity or upon repurchase of your securities by Credit Suisse will depend on the level of the indices. By investing in the securities, you will not acquire any interest in any stock or bond futures component. Your securities will be paid in cash, and you will have no right to receive delivery in respect of any stocks, bond futures components or any underlying asset upon which such bond futures components are based.

Adjustments to the Indices Could Adversely Affect the Performance of the Indices

At any time, the Index Calculation Agent can make methodological changes that could change the present and past levels of the Indices. Any action taken by the Index Calculation Agent could adversely affect performance of the Indices. For example, in the event that the level of the Credit Suisse RavenPack AIS Index published by the Index Calculation Agent on an Index Calculation Day is amended after it is initially published, but prior to the publication of the level of the Credit Suisse RavenPack AIS Index on the following Index Calculation Day, the amended level of the Credit Suisse RavenPack AIS Index will be deemed to be the official fixing level and will be used in all applicable calculations. All determinations and adjustments made by the Index Calculation Agent may be made in the Index Calculation Agent’s sole discretion, and the Index Calculation Agent has no obligation to take your interests into account.

13

The Indices Will Be Calculated Pursuant to a Set of Fixed Rules and Will Not Be Actively Managed. If the Indices Perform Poorly, the Index Sponsor Will Not Change the Rules in an Attempt to Improve Performance

The indices will not be actively managed. If the relevant rules-based investment methodology tracked by an index performs poorly, the Index Sponsor will not change the rules in an attempt to improve performance. Accordingly, an investment in securities linked to an index is not like an investment in a mutual fund. Unlike a mutual fund, which could be actively managed by the fund manager in an attempt to maximize returns in changing market conditions, the index rules will remain unchanged, even if those rules might prove to be ill-suited to future market conditions.

14

THE CREDIT SUISSE RAVENPACK AIS BALANCED 5% ER INDEX

All disclosure contained in this underlying supplement regarding the Credit Suisse RavenPack AIS Balanced 5% ER Index (the “Credit Suisse RavenPack AIS Balanced Index”), including, without limitation, its make-up, method of calculation and changes to its components, has been derived from information prepared by Credit Suisse International (“CSI”). CSI, as the sponsor of the Credit Suisse RavenPack AIS Balanced Index (in such capacity, the “Index Sponsor”), controls the policies of the Credit Suisse RavenPack AIS Balanced Index. The Index Sponsor also acts as the administrator of the Credit Suisse RavenPack AIS Balanced Index for the purposes of the Benchmark Regulation (Regulation (EU) 2016/1011) (the “BMR”) (the “Index Administrator”). CSI, as the calculation agent for the Credit Suisse RavenPack AIS Balanced Index (in such capacity, the “Index Calculation Agent”), is responsible for calculating the Credit Suisse RavenPack AIS Balanced Index. However, CSI may delegate to a third party some or all of their functions in respect of the Credit Suisse RavenPack AIS Balanced Index. A committee whose membership comprises personnel from CS (the “Index Committee”) governs the Credit Suisse RavenPack AIS Balanced Index. The Index Committee is responsible for approving certain actions in calculating and maintaining the Credit Suisse RavenPack AIS Balanced Index as described herein. The Index Calculation Agent will consult the Index Committee as necessary on matters of interpretation in calculating the Credit Suisse RavenPack AIS Balanced Index. Neither CSI nor the Index Committee has any obligation to take the needs of any investor in the securities, CSI or any of their clients into consideration in determining, composing, calculating or publishing the Credit Suisse RavenPack AIS Balanced Index or any of the components of the Credit Suisse RavenPack AIS Balanced Index.

Overview

The Credit Suisse RavenPack AIS Balanced Index is designed to provide exposure to a hypothetical “balanced” portfolio (consisting of the Equity Index and a momentum strategy-driven allocation of the Fixed Income Indices), while targeting a realized daily volatility of 5%. By “balanced” we mean the Credit Suisse RavenPack AIS Balanced Index’s hypothetical portfolio may, under certain circumstances, include both:

| · | equity exposure, in the form of large-cap U.S. equities included in an excess return version of the Credit Suisse RavenPack Artificial Intelligence Sentiment Index (the “Credit Suisse RavenPack AIS Index”); and |

| · | fixed income exposure, in the form of U.S. Treasury note futures contracts tracked by the Credit Suisse 10-Year U.S. Treasury Note Futures Index (the “10Y Fixed Income Index”) and the Credit Suisse 2-Year U.S. Treasury Note Futures Index (the “2Y Fixed Income Index”) (each, a “Fixed Income Index,” and together, the “Fixed Income Indices”). |

“Balanced” does not imply any risk adjusted diversified asset class allocation or actual balance among asset classes. See “Selected Risk Considerations—Selected Risk Factors Related to the Credit Suisse RavenPack AIS Balanced Index—The Credit Suisse RavenPack AIS Balanced Index Does Not Attempt to Achieve a Broad or “Balanced” Asset Class Diversification.”

We refer to each of the excess return version of the Credit Suisse RavenPack AIS Index (the “Equity Index”) and the Fixed Income Indices a “Component Index,” and together, the “Component Indices.”

The Credit Suisse RavenPack AIS Index is composed of at least four of the eleven industry-specific sub-indices of the S&P 500® Index. The Credit Suisse RavenPack AIS Index selects these sub-indices for inclusion based on a quarterly measurement of the “sentiment” relating to earnings and revenues toward each of the eleven sub-indices. “Sentiment” is measured by an algorithm developed by RavenPack that is designed to assign scores to news items. While the algorithm assigns many different types of scores to news items, the Credit Suisse RavenPack AIS Index uses three of these scores that are on a scale from zero to 100 that are meant to reflect the “relevance,” “novelty” and “sentiment” of the news items in relation to the companies discussed in such news item. Using these scores, the Credit Suisse RavenPack AIS Index selects the most relevant and most novel news items with significant positive or negative “sentiment” in relation to earnings or revenues of the companies in a particular sector and calculates the “sentiment” for such sector based on the “sentiment” scores given to the selected news items. Because the algorithm does not aim to comprehend news items, it cannot necessarily predict human or the market classification or sentiment of a particular news item. For example, the algorithm might not process enthusiasm, nuance, sarcasm,

15

satire or other types of writing that a human could understand. The algorithm also does not learn from news items it processes or adapt to its environment and, as a static algorithm, will continue to use the same mathematical rules to process news items, even as news develops over time. The algorithm is called “artificial intelligence” only in the limited sense that it applies static algorithmic rules to language to produce a mathematical result that might indicate relevance, novelty or a given sentiment about a company. See “Selected Risk Considerations—Selected Risk Factors Related to the Credit Suisse RavenPack AIS Index—The Credit Suisse RavenPack AIS Index Is Called “Artificial Intelligence” Only in the Limited Sense that It Is Based on a Static Algorithm” herein. The Credit Suisse RavenPack AIS Index is described in greater detail in “The Credit Suisse RavenPack Artificial Intelligence Sentiment Index” herein.

The Equity Index is an excess return version of the Credit Suisse RavenPack AIS Index, reflecting the performance of the Credit Suisse RavenPack AIS Index less a deemed borrowing cost calculated based on 3-month USD LIBOR. Calculation of the Equity Index is described in greater detail herein under “The Equity Index.”

Depending on market conditions, the Credit Suisse RavenPack AIS Balanced Index may allocate exposure to one or both Fixed Income Indices that track the performance of notional long investments in two- and ten-year U.S. Treasury note futures contracts. U.S. Treasury notes are United States government debt securities issued by the United States Treasury. These indices are described in greater detail in “The Fixed Income Indices” herein.

The Index Calculation Agent deducts an index fee in the calculation of the Credit Suisse RavenPack AIS Balanced Index. The index fee is deducted from the daily performance of the Credit Suisse RavenPack AIS Balanced Index at a rate of 0.50% per annum. The annualized index fee reduces the level of the Credit Suisse RavenPack AIS Balanced Index.

Asset Allocation

The Credit Suisse RavenPack AIS Balanced Index varies its allocation between the Equity Index and the Fixed Income Indices over time. The Credit Suisse RavenPack AIS Balanced Index allocates (i) all of its exposure to the Equity Index during potential “lower risk” periods and (ii) part of its exposure to the Equity Index and the remainder of its exposure to one or both Fixed Income Indices during potential “higher risk” periods. Thus, the Credit Suisse RavenPack AIS Balanced Index diversifies its exposure to include the lower risk Fixed Income Indices when there is more volatility in U.S. equity markets.

“Volatility” refers to the annualized standard deviation of the daily performance of an asset. The greater the historical volatility with respect to the asset on a given date, the higher the historical variation of their daily performance and thus the greater the range of potential negative (or positive) performance of the asset (if expected volatility is in line with historical volatility). It is important to note that the historical realized volatility is an historical measure of realized volatility and it does not necessarily reflect volatility going forward. Historical realized volatility is not the same as implied volatility, which is an estimation of future volatility and may better reflect market expectations.

Lower historical realized volatility of the Credit Suisse RavenPack AIS Index is deemed herein as a proxy for “less risky” markets. Conversely, higher historical realized volatility of the Credit Suisse RavenPack AIS Index is deemed herein as a proxy for “more risky” markets. To measure the historical realized volatility of the Credit Suisse RavenPack AIS Index, the Credit Suisse RavenPack AIS Balanced Index first calculates the exponential moving average of the variance of the Credit Suisse RavenPack AIS Index. Variance is the square of volatility and is used in certain products in the over-the-counter derivatives market in place of volatility due to mathematical properties that make it more convenient for financial institutions to value and hedge those products. The variance of the Credit Suisse RavenPack AIS Index on each day is calculated using the exponential moving average of the variance of the Credit Suisse RavenPack AIS Index. A simple moving average is the unweighted average of a previous fixed subset of data points, such as index closing levels. When a new data point is included in the average, the then oldest data point is excluded. An exponential moving average includes all of the data points from a fixed starting point and applies a decay factor to exponentially decrease the weights given to older data points. The exponential moving averages used by the Credit Suisse RavenPack AIS Balanced Index thus give the most weight to the most recent variance. The Credit Suisse RavenPack AIS Balanced Index calculates two exponential moving averages of the variance of the Credit Suisse RavenPack AIS Index using a decay factor of 0.93 or 0.97. Approximately 99% of the weight included in an exponential moving average is derived (i) from the previous 64 trading days if the decay factor is 0.93 and (ii) from the previous 152 trading days if the decay factor is 0.97. We refer to the realized

16

volatility (the square root of the applicable variance) calculated using the decay factor of 0.93 as the “short-term realized volatility” and the realized volatility calculated using the decay factor of 0.97 as the “long-term realized volatility,” calculated on an annualized basis. The Credit Suisse RavenPack AIS Balanced Index uses the average of these two different methods to calculate the historical realized volatility of the Credit Suisse RavenPack AIS Index to average out the risk that the long-term realized volatility is meaningfully different from the short-term realized volatility. For the purpose of determining the asset allocation of the portfolio, the historical realized volatility of the Credit Suisse RavenPack AIS Index on each day is equal to the arithmetic average of the short-term and long-term realized volatilities of the Credit Suisse RavenPack AIS Index on such day. However, this averaging of short-term realized volatility and long-term realized volatility is arbitrary and may dampen or heighten the calculated volatility of the Credit Suisse RavenPack AIS Index compared to other methods of calculating volatility such as implied volatility, which is an estimation of future volatility and may better reflect market volatility expectation.

There are measurements that the Credit Suisse RavenPack AIS Balanced Index will deem to be meaningful to the index methodology that would not be deemed meaningful if the Credit Suisse RavenPack AIS Balanced Index used a different method of calculating volatility. Alternatively, the Credit Suisse RavenPack AIS Balanced Index may be overly restrictive and treat as not meaningful changes in volatility that in fact contain meaningful information. In this latter case, the Credit Suisse RavenPack AIS Balanced Index may retain exposure to the Equity Index after other methods would have dictated allocating exposure to the Fixed Income Indices. Any fixed rule for determining a change to the portfolio of the Credit Suisse RavenPack AIS Balanced Index will necessarily be a blunt tool and, accordingly, may have a high rate of inaccuracy. The particular ways in which the Credit Suisse RavenPack AIS Balanced Index operates may produce a lower return than other rules that could have been adopted for the identification of the volatility of the Equity Index. There is nothing inherent in the particular methodology used by the Credit Suisse RavenPack AIS Balanced Index that makes it a more or less accurate predictor of the volatility of the Equity Index. It is possible that the rules used by the Credit Suisse RavenPack AIS Balanced Index may not identify the volatility of the Equity Index as effectively as other rules that might have been adopted, or at all.