| Preliminary Pricing Supplement ARN-97 (To the Prospectus dated June 30, 2017, the Prospectus Supplement dated June 30, 2017, and the Product Supplement EQUITY ARN-1 dated May 7, 2020) | Subject to Completion Preliminary Pricing Supplement dated May 8, 2020 | Filed Pursuant to Rule 424(b)(2) Registration Statement No. 333-218604-02 |

Units $10 principal amount per unit CUSIP No.  | Pricing Date* Settlement Date* Maturity Date* | May , 2020 June , 2020 July , 2021 |

| *Subject to change based on the actual date the notes are priced for initial sale to the public (the “pricing date”) | ||

Accelerated Return Notes®Linked to the VanEck Vectors® Gold Miners ETF

§ Maturity of approximately 14 months

§ 3-to-1 upside exposure to increases in the Underlying Fund, subject to a capped return of [44.00% to 54.00%]

§ 1-to-1 downside exposure to decreases in the Underlying Fund, with up to 100% of your principal at risk

§ All payments occur at maturity and are subject to the credit risk of Credit Suisse AG

§ No periodic interest payments

§ In addition to the underwriting discount set forth below, the notes include a hedging-related charge of $0.075 per unit. See “Structuring the Notes”.

§ Limited secondary market liquidity, with no exchange listing

§ The notes are senior unsecured debt securities and are not insured or guaranteed by the U.S. Federal Deposit Insurance Corporation or any other governmental agency of the United States, Switzerland or any other jurisdiction

|

The notes are being issued by Credit Suisse AG (“Credit Suisse”). There are important differences between the notes and a conventional debt security, including different investment risks and certain additional costs. See “Risk Factors” beginning on page TS-7 of this term sheet, “Additional Risk Factors” beginning on page TS-8 of this term sheet and “Risk Factors” beginning on page PS-6 of product supplement EQUITY ARN-1.

The initial estimated value of the notes as of the pricing date is expected to be between $9.40and $9.80 per unit, which is less than the public offering price listed below. See “Summary” on the following page, “Risk Factors” beginning on page TS-7 of this term sheet and “Structuring the Notes” on page TS-13 of this term sheet for additional information. The actual value of your notes at any time will reflect many factors and cannot be predicted with accuracy.

_________________________

None of the Securities and Exchange Commission (the “SEC”), any state securities commission, or any other regulatory body has approved or disapproved of these securities or determined if this Note Prospectus (as defined below) is truthful or complete. Any representation to the contrary is a criminal offense.

_________________________

| Per Unit | Total | |||||||

| Public offering price(1) | $ | 10.00 | $ | |||||

| Underwriting discount(1) | $ | 0.20 | $ | |||||

| Proceeds, before expenses, to Credit Suisse | $ | 9.80 | $ | |||||

| (1) | For any purchase of 500,000 units or more in a single transaction by an individual investor or in combined transactions with the investor’s household in this offering, the public offering price and the underwriting discount will be $9.95 per unit and $0.15 per unit, respectively. See “Supplement to the Plan of Distribution” below. |

The notes:

| Are Not FDIC Insured | Are Not Bank Guaranteed | May Lose Value |

BofA Securities

May , 2020

| Accelerated Return Notes® Linked to the VanEck Vectors® Gold Miners ETF, due July , 2021 |

Summary

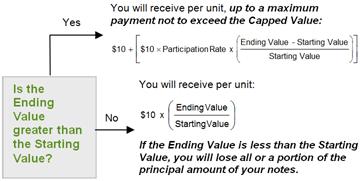

The Accelerated Return Notes®Linked to the VanEck Vectors® Gold Miners ETF, due July , 2021 (the “notes”) are our senior unsecured debt securities. The notes are not guaranteed or insured by the Federal Deposit Insurance Corporation or any other governmental agency of the United States, Switzerland or any other jurisdiction and are not secured by collateral.The notes will rank equally with all of our other unsecured and unsubordinated debt. Any payments due on the notes, including any repayment of principal, will be subject to the credit risk of Credit Suisse. The notes provide you a leveraged return, subject to a cap, if the Ending Value of the Market Measure, which is the VanEck Vectors® Gold Miners ETF (the “Underlying Fund”), is greater than the Starting Value. If the Ending Value is less than the Starting Value, you will lose all or a portion of the principal amount of your notes. Any payments on the notes, will be calculated based on the $10 principal amount per unit and will depend on the performance of the Underlying Fund, subject to our credit risk. See “Terms of the Notes” below.

The economic terms of the notes (including the Capped Value) are based on the rate we are currently paying to borrow funds through the issuance of market-linked notes (our “internal funding rate”) and the economic terms of certain related hedging arrangements. Our internal funding rate for market-linked notes is typically lower than a rate reflecting the yield on our conventional debt securities of similar maturity in the secondary market (our “secondary market credit rate”). This difference in borrowing rate, as well as the underwriting discount and the hedging related charge described below, will reduce the economic terms of the notes to you and the initial estimated value of the notes on the pricing date. These costs will be effectively borne by you as an investor in the notes, and will be retained by us and BofAS or any of our respective affiliates in connection with our structuring and offering of the notes. Due to these factors, the public offering price you pay to purchase the notes will be greater than the initial estimated value of the notes.

On the cover page of this term sheet, we have provided the initial estimated value range for the notes. This range of estimated values reflects terms that are not yet fixed and was determined based on our valuation of the theoretical components of the notes in accordance with our pricing models. These include a theoretical bond component valued using our internal funding rate, and theoretical individual option components valued using mid-market pricing. You will not have any interest in, or rights to, the theoretical components we use to determine the estimated value of the notes. The initial estimated value of the notes calculated on the pricing date will be set forth in the final term sheet made available to investors in the notes. For more information about the initial estimated value and the structuring of the notes, see “Structuring the Notes” on page TS-13.

| Terms of the Notes | Redemption Amount Determination | |

| Issuer: | Credit Suisse AG (“Credit Suisse”), acting through its London branch. | On the maturity date, you will receive a cash payment per unit determined as follows: |

| Principal Amount: | $10.00 per unit |  |

| Term: | Approximately 14 months | |

| Market Measure: | The VanEck Vectors® Gold Miners ETF (Bloomberg symbol: “GDX”) | |

| Starting Value: | The Closing Market Price of the Market Measure on the pricing date | |

| Ending Value: | The average of the Closing Market Prices of the Market Measure times the Price Multiplier on each calculation day occurring during the Maturity Valuation Period. The scheduled calculation days are subject to postponement in the event of Market Disruption Events, as described beginning on page PS-24 of product supplement EQUITY ARN-1. | |

| Participation Rate: | 300% | |

| Capped Value: | [$14.40 to $15.40] per unit, which represents a return of [44.00% to 54.00%] over the principal amount. The actual Capped Value will be determined on the pricing date. | |

| Maturity Valuation Period: | Five scheduled calculation days shortly before the maturity date. | |

| Price Multiplier: | 1, subject to adjustment for certain corporate events relating to the Market Measure, as described beginning on page PS-27 of product supplement EQUITY ARN-1. | |

| Fees and Charges: | The underwriting discount of $0.20 per unit listed on the cover page and the hedging related charge of $0.075 per unit described in “Structuring the Notes” on page TS-13. | |

| Joint Calculation Agents: | Credit Suisse International and BofA Securities, Inc. (“BofAS”), acting jointly. | |

| Accelerated Return Notes® | TS-2 |

| Accelerated Return Notes® Linked to the VanEck Vectors® Gold Miners ETF, due July , 2021 |

The terms and risks of the notes are contained in this term sheet and in the following:

| § | Product supplement EQUITY ARN-1 dated May 7, 2020: https://www.sec.gov/Archives/edgar/data/1053092/000095010320009208/dp127846_424b2-arn1.htm |

| § | Prospectus supplement and prospectus dated June 30, 2017: http://www.sec.gov/Archives/edgar/data/1053092/000104746917004364/a2232566z424b2.htm |

These documents (together, the “Note Prospectus”) have been filed as part of a registration statement with the SEC, which may, without cost, be accessed on the SEC website as indicated above or obtained from MLPF&S or BofAS by calling 1-800-294-1322. Before you invest, you should read the Note Prospectus, including this term sheet, for information about us and this offering. Any prior or contemporaneous oral statements and any other written materials you may have received are superseded by the Note Prospectus. Capitalized terms used but not defined in this term sheet have the meanings set forth in product supplement EQUITY ARN-1. Unless otherwise indicated or unless the context requires otherwise, all references in this document to “we,” “us,” “our,” or similar references are to Credit Suisse.

Investor Considerations

You may wish to consider an investment in the notes if:

| § | You anticipate that the Underlying Fund will increase moderately from the Starting Value to the Ending Value. |

| § | You are willing to risk a loss of principal and return if the Underlying Fund decreases from the Starting Value to the Ending Value. |

| § | You accept that the return on the notes will be capped. |

| § | You are willing to forgo the interest payments that are paid on traditional interest bearing debt securities. |

| § | You are willing to forgo dividends or other benefits of owning shares of the Underlying Fund or the securities held by the Underlying Fund. |

| § | You are willing to accept a limited or no market for sales prior to maturity, and understand that the market prices for the notes, if any, will be affected by various factors, including our actual and perceived creditworthiness, our internal funding rate and fees and charges on the notes. |

| § | You are willing to assume our credit risk, as issuer of the notes, for all payments under the notes, including the Redemption Amount. |

The notes may not be an appropriate investment for you if:

| § | You believe that the Underlying Fund will decrease from the Starting Value to the Ending Value or that it will not increase sufficiently over the term of the notes to provide you with your desired return. |

| § | You seek principal repayment or preservation of capital. |

| § | You seek an uncapped return on your investment. |

| § | You seek interest payments or other current income on your investment. |

| § | You want to receive dividends or other distributions paid on shares of the Underlying Fund or the securities held by the Underlying Fund. |

| § | You seek an investment for which there will be a liquid secondary market. |

| § | You are unwilling or are unable to take market risk on the notes or to take our credit risk as issuer of the notes. |

We urge you to consult your investment, legal, tax, accounting, and other advisors before you invest in the notes.

| Accelerated Return Notes® | TS-3 |

| Accelerated Return Notes® Linked to the VanEck Vectors® Gold Miners ETF, due July , 2021 |

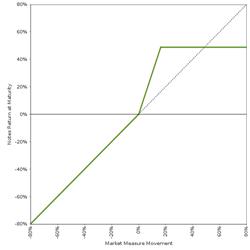

Hypothetical Payout Profile

The graph below is based onhypothetical numbers and values.

Accelerated Return Notes®

| This graph reflects the returns on the notes, based on the Participation Rate of 300% and a Capped Value of $14.90 per unit (the midpoint of the Capped Value range of [$14.40 to $15.40]). The green line reflects the returns on the notes, while the dotted gray line reflects the returns of a direct investment in the Underlying Fund, excluding dividends.

This graph has been prepared for purposes of illustration only.

|

Hypothetical Payments at Maturity

The following table and examples are for purposes of illustration only. They are based onhypothetical values and showhypothetical returns on the notes.The actual amount you receive and the resulting total rate of return will depend on the actual Starting Value, Ending Value, Capped Value and term of your investment.

The following table is based on a Starting Value of 100, the Participation Rate of 300% and a hypothetical Capped Value of $14.90 per unit. It illustrates the effect of a range of Ending Values on the Redemption Amount per unit of the notes and the total rate of return to holders of the notes. The following examples do not take into account any tax consequences from investing in the notes.

| Accelerated Return Notes® | TS-4 |

| Accelerated Return Notes® Linked to the VanEck Vectors® Gold Miners ETF, due July , 2021 |

Ending Value | Percentage Change from the Starting Value to the Ending Value | Redemption Amount per Unit | Total Rate of Return on the Notes |

| 0.00 | -100.00% | $0.00 | -100.00% |

| 50.00 | -50.00% | $5.00 | -50.00% |

| 60.00 | -40.00% | $6.00 | -40.00% |

| 70.00 | -30.00% | $7.00 | -30.00% |

| 80.00 | -20.00% | $8.00 | -20.00% |

| 90.00 | -10.00% | $9.00 | -10.00% |

| 100.00(1) | 0.00% | $10.00 | 0.00% |

| 103.00 | 3.00% | $10.90 | 9.00% |

| 105.00 | 5.00% | $11.50 | 15.00% |

| 110.00 | 10.00% | $13.00 | 30.00% |

| 116.34 | 16.34% | $14.90(2) | 49.00% |

| 120.00 | 20.00% | $14.90 | 49.00% |

| 130.00 | 30.00% | $14.90 | 49.00% |

| 140.00 | 40.00% | $14.90 | 49.00% |

| 150.00 | 50.00% | $14.90 | 49.00% |

| 160.00 | 60.00% | $14.90 | 49.00% |

| (1) | Thehypothetical Starting Value of 100 used in these examples has been chosen for illustrative purposes only, and does not represent a likely actual Starting Value for the Market Measure. |

| (2) | The Redemption Amount per unit cannot exceed thehypothetical Capped Value. |

For recent actual prices of the Market Measure, see “The Underlying Fund” section below. The Ending Value will not include any income generated by dividends paid on the Underlying Fund or the securities held by the Underlying Fund, which you would otherwise be entitled to receive if you invested in those securities directly. In addition, all payments on the notes are subject to issuer credit risk.

| Accelerated Return Notes® | TS-5 |

| Accelerated Return Notes® Linked to the VanEck Vectors® Gold Miners ETF, due July , 2021 |

Redemption Amount Calculation Examples

| Example 1 |

| The Ending Value is 80.00, or 80.00% of the Starting Value: |

| Starting Value: | 100.00 |

| Ending Value: | 80.00 |

| = $8.00 Redemption Amount per unit |

| Example 2 |

| The Ending Value is 104.00, or 104.00% of the Starting Value: |

| Starting Value: | 100.00 |

| Ending Value: | 104.00 |

| = $11.20 Redemption Amount per unit |

| Example 3 |

| The Ending Value is 130.00, or 130.00% of the Starting Value: |

| Starting Value: | 100.00 |

| Ending Value: | 130.00 |

| = $19.00, however, because the Redemption Amount for the notes cannot exceed the Capped Value, the Redemption Amount will be $14.90 per unit |

| Accelerated Return Notes® | TS-6 |

| Accelerated Return Notes® Linked to the VanEck Vectors® Gold Miners ETF, due July , 2021 |

Risk Factors

There are important differences between the notes and a conventional debt security. An investment in the notes involves significant risks, including those listed below. You should carefully review the more detailed explanation of risks relating to the notes in the “Risk Factors” sections beginning on page PS-6 of product supplement EQUITY ARN-1 identified above. We also urge you to consult your investment, legal, tax, accounting, and other advisors before you invest in the notes.

| § | Depending on the performance of the Underlying Fund as measured shortly before the maturity date, your investment may result in a loss; there is no guaranteed return of principal. |

| § | Your return on the notes may be less than the yield you could earn by owning a conventional fixed or floating rate debt security of comparable maturity. |

| § | Payments on the notes are subject to our credit risk, and actual or perceived changes in our creditworthiness are expected to affect the value of the notes. If we become insolvent or are unable to pay our obligations, you may lose your entire investment. |

| § | Your investment return is limited to the return represented by the Capped Value and may be less than a comparable investment directly in the Underlying Fund or the securities held by the Underlying Fund. |

| § | The initial estimated value of the notes is an estimate only, determined as of a particular point in time by reference to our proprietary pricing models. These pricing models consider certain factors, such as our internal funding rate on the pricing date, interest rates, volatility and time to maturity of the notes, and they rely in part on certain assumptions about future events, which may prove to be incorrect. Because our pricing models may differ from other issuers’ valuation models, and because funding rates taken into account by other issuers may vary materially from the rates used by us (even among issuers with similar creditworthiness), our estimated value may not be comparable to estimated values of similar notes of other issuers. |

| § | Our internal funding rate for market-linked notes is typically lower than our secondary market credit rates, as further described in “Structuring the Notes” on page TS-13. Because we use our internal funding rate to determine the value of the theoretical bond component, if on the pricing date our internal funding rate is lower than our secondary market credit rates, the initial estimated value of the notes will be greater than if we had used our secondary market credit rates in valuing the notes. |

| § | The public offering price you pay for the notes will exceed the initial estimated value. This is due to, among other transaction costs, the inclusion in the public offering price of the underwriting discount and the hedging related charge, as further described in “Structuring the Notes” on page TS-13. |

| § | Assuming no change in market conditions or other relevant factors after the pricing date, the market value of your notes may be lower than the price you paid for them and lower than the initial estimated value. This is due to, among other things, the inclusion in the public offering price of the underwriting discount and the hedging related charge and the internal funding rate we used in pricing the notes, as further described in “Structuring the Notes” on page TS-13. These factors, together with customary bid ask spreads, other transaction costs and various credit, market and economic factors over the term of the notes, including changes in the price of the Underlying Fund, are expected to reduce the price at which you may be able to sell the notes in any secondary market and will affect the value of the notes in complex and unpredictable ways. |

| § | A trading market is not expected to develop for the notes. None of us, MLPF&S or BofAS is obligated to make a market for, or to repurchase, the notes. The initial estimated value does not represent a minimum or maximum price at which we, MLPF&S, BofAS or any of our affiliates would be willing to purchase your notes in any secondary market (if any exists) at any time. BofAS has advised us that any repurchases by MLPF&S, BofAS or their affiliates will be made at prices determined by reference to their pricing models and at their discretion, and these prices will include MLPF&S’s and BofAS’s trading commissions and mark-ups. If you sell your notes to a dealer other than MLPF&S or BofAS in a secondary market transaction, the dealer may impose its own discount or commission. BofAS has also advised us that, at its discretion and for your benefit, assuming no changes in market conditions from the pricing date, MLPF&S or BofAS may offer to buy the notes in the secondary market at a price that may exceed the initial estimated value of the notes for a short initial period after the issuance of the notes. That higher price reflects costs that were included in the public offering price of the notes, and that higher price may also be initially used for account statements or otherwise. There is no assurance that any party will be willing to purchase your notes at any price in any secondary market. |

| § | Your return on the notes and the value of the notes may be affected by exchange rate movements and factors affecting the international securities markets. |

| § | Our business, hedging and trading activities, and those of MLPF&S, BofAS and our respective affiliates (including trading in shares of the Underlying Fund or the securities held by the Underlying Fund), and any hedging and trading activities we, MLPF&S, BofAS or our respective affiliates engage in for our clients’ accounts, may affect the market value and return of the notes and may create conflicts of interest with you. |

| § | The sponsor of the NYSE Arca Gold Miners Index (the “Underlying Index”) described below may adjust the Underlying Index in a way that affects its level, and has no obligation to consider your interests. |

| § | The sponsor and investment advisor of the Underlying Fund may adjust the Underlying Fund in a way that could adversely affect the value of the notes and the Redemption Amount, and these entities have no obligation to consider your interests. |

| Accelerated Return Notes® | TS-7 |

| Accelerated Return Notes® Linked to the VanEck Vectors® Gold Miners ETF, due July , 2021 |

| § | You will have no rights of a holder of shares of the Underlying Fund or the securities held by the Underlying Fund, and you will not be entitled to receive securities or dividends or other distributions by the issuers of those securities. |

| § | While we, MLPF&S, BofAS or our respective affiliates may from time to time own shares of the Underlying Fund or the securities held by the Underlying Fund, we, MLPF&S, BofAS and our respective affiliates do not control any company held by the Underlying Fund or included in the Underlying Index, and we have not verified any disclosure made by any other company. |

| § | There are liquidity and management risks associated with the Underlying Fund. |

| § | The performance of the Underlying Fund may not correlate with the performance of its Underlying Index as well as the net asset value per share of the Underlying Fund, especially during periods of market volatility when the liquidity and the market price of shares of the Underlying Fund and/or securities held by the Underlying Fund may be adversely affected, sometimes materially. |

| § | Risks associated with the Underlying Index or the underlying assets of the Underlying Fund will affect the share price of the Underlying Fund and hence, the value of the notes. |

| § | The payments on the notes will not be adjusted for all corporate events that could affect the Underlying Fund. See “Description of ARNs—Anti-Dilution and Discontinuance Adjustments Relating to Underlying Funds” beginning on page PS-27 of product supplement EQUITY ARN-1. |

| § | There may be potential conflicts of interest involving the calculation agents, one of which is our affiliate and one of which is BofAS. We have the right to appoint and remove the calculation agents. |

| § | As a Swiss bank, Credit Suisse is subject to regulation by governmental agencies, supervisory authorities and self-regulatory organizations in Switzerland. Such regulation is increasingly more extensive and complex and subjects Credit Suisse to risks. For example, pursuant to Swiss banking laws, FINMA has broad powers and discretion in the case of resolution proceedings, which include the power to convert debt instruments and other liabilities of Credit Suisse into equity and/or cancel such liabilities in whole or in part. |

| § | The U.S. federal tax consequences of an investment in the notes are unclear. There is no direct legal authority regarding the proper U.S. federal tax treatment of the notes, and we do not plan to request a ruling from the Internal Revenue Service (the “IRS”). Consequently, significant aspects of the tax treatment of the notes are uncertain, and the IRS or a court might not agree with the treatment of the notes as prepaid financial contracts that are treated as “open transactions.” If the IRS were successful in asserting an alternative treatment of the notes, the tax consequences of the ownership and disposition of the notes, including the timing and character of income recognized by U.S. investors and the withholding tax consequences to non-U.S. investors, might be materially and adversely affected. Even if the treatment of the notes described herein is respected, there is a substantial risk that a note will be treated as a “constructive ownership transaction,” with potentially adverse consequences described below under “United States Federal Tax Considerations.” Moreover, future legislation, Treasury regulations or IRS guidance could adversely affect the U.S. federal tax treatment of the notes, possibly retroactively. |

Additional Risk Factors

All of the securities held by the Underlying Fund are concentrated in one industry.

All of the securities held by the Underlying Fund are issued by companies in the gold and silver mining industry. As a result, the securities that will determine the performance of the notes are concentrated in one industry. Although an investment in the notes will not give holders any ownership or other direct interests in the securities held by the Underlying Fund, the return on an investment in the notes will be subject to certain risks similar to those associated with direct equity investments in the gold and silver mining industry. Accordingly, by investing in the notes, you will not benefit from the diversification which could result from an investment linked to companies that operate in multiple sectors.

A limited number of securities may affect the level of the Underlying Index, and the Underlying Index is not necessarily representative of the gold and silver mining industry.

As May 4, 2020, the top two securities included in the Underlying Index constituted 30.66% of the total weight of the Underlying Index and the top six securities included in the Underlying Index constituted 53.90% of the total weight of the Underlying Index. Because the Underlying Fund attempts to track the performance of the Underlying Index, any reduction in the market price of those securities is likely to have a substantial adverse impact on the price of the Underlying Fund and the value of the notes.

While the securities included in the Underlying Index are common stocks, American Depositary Receipts (“ADRs”) or global depositary receipts (“GDRs”) of companies generally considered to be involved in various segments of the gold and silver mining industry, the securities included in the Underlying Index may not follow the price movements of the entire gold and silver mining industry generally. If the securities included in the Underlying Index (and, accordingly, the securities held by the Underlying Fund) decline in value, the Underlying Fund will decline in value even if security prices in the gold and silver mining industry generally increase in value.

There is no direct correlation between the value of the notes or the price of the Underlying Fund, on the one hand, and gold and silver prices, on the other hand.

Although the price of gold or silver is one factor that may influence the performance of the securities held by the Underlying Fund, the notes are not linked to the gold or silver spot prices or to gold or silver futures. There is no direct linkage between the price of the Underlying Fund and the prices of gold and silver. While gold and silver prices may be one factor that could affect the prices of the securities included in the Underlying Index and, consequently, the price of the Underlying Fund and the Redemption Amount are not

| Accelerated Return Notes® | TS-8 |

| Accelerated Return Notes® Linked to the VanEck Vectors® Gold Miners ETF, due July , 2021 |

directly linked to the movement of gold and silver prices and may be affected by factors unrelated to those movements. Investing in the notes is not the same as investing in gold or silver, and you should not invest in the notes if you wish to invest in a product that is linked directly to the price of gold or silver.

NYSE Arca, Inc. (“NYSE Arca”) the sponsor and compiler of the Underlying Index, retains significant control and discretionary decision-making over the Underlying Index and is responsible for decisions regarding the interpretation of and amendments to the Underlying Index rules, which may have an adverse effect on the price of the Underlying Fund, the market value of the notes and the Redemption Amount.

NYSE Arca is the compiler of the Underlying Index and, as such, is responsible for the day-to-day management of the Underlying Index and for decisions regarding the interpretation of the rules governing the Underlying Index. NYSE Arca has the discretion to make operational adjustments to the Underlying Index and to the Underlying Index components, including discretion to exclude companies that otherwise meet the minimum criteria for inclusion in the Underlying Index. In addition, NYSE Arca retains the power to supplement, amend in whole or in part, revise or withdraw the Underlying Index rules at any time, any of which may lead to changes in the way the Underlying Index is compiled or calculated or adversely affect the Underlying Index in another way. Any of these adjustments to the Underlying Index or the Underlying Index rules may adversely affect the composition of the Underlying Index, the price of the Underlying Fund, the market value of the notes and the Redemption Amount. The Underlying Index sponsor has no obligation to take the needs of any buyer, seller or holder of the notes into consideration at any time.

The performance of the Underlying Fund may be influenced by gold and silver prices.

To the extent the price of gold or silver has a limited effect, if any, on the prices of the securities held by the Underlying Fund, gold prices and silver prices are subject to volatile price movements over short periods of time, represent trading in commodities markets, which are substantially different from equities markets, and are affected by numerous factors. These include economic factors, including the structure of and confidence in the global monetary system, expectations of the future rate of inflation, the relative strength of, and confidence in, the U.S. dollar (the currency in which the prices of gold and silver are generally quoted), interest rates and gold and silver borrowing and lending rates, and global or regional economic, financial, political, regulatory, judicial, or other events.

Gold prices and silver prices may also be affected by industry factors such as industrial and jewelry demand, lending, sales and purchases of gold and silver by the official sector, including central banks and other governmental agencies and multilateral institutions which hold gold and silver, levels of gold and silver production and production costs, and short-term changes in supply and demand because of trading activities in the gold and silver markets. It is not possible to predict the aggregate effects of all or any combination of these factors. Any negative developments with respect to these factors may have an adverse effect on gold and silver prices and, as a result, on the prices of the securities held by the Underlying Fund and the price of the Underlying Fund.

| Accelerated Return Notes® | TS-9 |

| Accelerated Return Notes® Linked to the VanEck Vectors® Gold Miners ETF, due July , 2021 |

The Underlying Fund

All disclosures contained in this term sheet regarding the Underlying Fund and the Underlying Index, including, without limitation, their make up, method of calculation, and changes in its components, have been derived from publicly available sources. The information reflects the policies of, and is subject to change by, Van Eck Associates Corporation (“Van Eck”). VanEck Vectors Gold Miners ETF is an exchange-traded fund incorporated in the U.S. The Underlying Fund tracks the performance of the NYSE Arca Gold Miners Index. The Underlying Fund or the Underlying Index may be discontinued at any time. The consequences of such discontinuance are discussed in the section entitled “Description of ARNs—Anti-Dilution and Discontinuance Adjustments Relating to Underlying Funds” beginning on page PS-27 of product supplement EQUITY ARN-1. None of us, the calculation agents, MLPF&S or BofAS accepts any responsibility for the calculation, maintenance or publication of the Underlying Fund, the Underlying Index, or any successor fund or index.

The Underlying Fund invests in materials stocks of all capitalization sizes across the globe. Its largest allocation is in North American companies, principally those domiciled in Canada. The Underlying Fund weights the holdings using a market capitalization methodology.

VanEck Vectors ETF Trust is a registered investment company that consists of numerous separate investment portfolios, including the Underlying Fund. Information filed by VanEck Vectors ETF Trust with the SEC under the Securities Exchange Act of 1934 and the Investment Company Act of 1940 can be found by reference to its SEC file numbers: 333-123257 and 811-10325 through the SEC’s website at http://www.sec.gov.

This term sheet relates only to the notes and does not relate to the Underlying Fund or to any securities included in the Underlying Index. None of us, MLPF&S, BofAS or any of our respective affiliates has participated or will participate in the preparation of the publicly available documents described below. None of us, MLPF&S, BofAS or any of our respective affiliates has made any due diligence inquiry with respect to the Underlying Fund in connection with the offering of the notes. None of us, MLPF&S, BofAS or any of our respective affiliates makes any representation that the publicly available documents or any other publicly available information regarding the Underlying Fund are accurate or complete. Furthermore, there can be no assurance that all events occurring prior to the date of this term sheet, including events that would affect the accuracy or completeness of these publicly available documents that would affect the trading price of the Underlying Fund, have been or will be publicly disclosed. Subsequent disclosure of any events or the disclosure of or failure to disclose material future events concerning the Underlying Fund could affect the price of the Underlying Fund and therefore could affect your return on the notes. The selection of the Underlying Fund is not a recommendation to buy or sell the Underlying Fund or any securities held by the Underlying Fund.

The Underlying Fund trades on the NYSE Arca under the symbol “GDX.”

| Accelerated Return Notes® | TS-10 |

| Accelerated Return Notes® Linked to the VanEck Vectors® Gold Miners ETF, due July , 2021 |

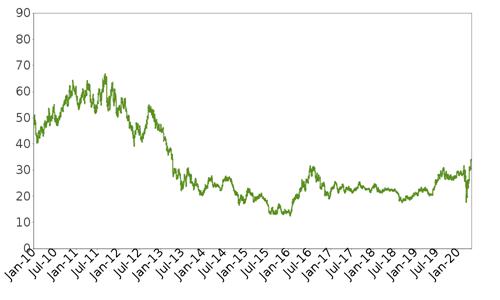

The following graph shows the daily historical performance of the Underlying Fund on its primary exchange in the period from January 1, 2010 through May 6, 2020. We obtained this historical data from Bloomberg L.P. We have not independently verified the accuracy or completeness of the information obtained from Bloomberg L.P. On May 6, 2020 the Closing Market Price of the Underlying Fund was $33.70. The graph below may have been adjusted to reflect certain corporate actions such as stock splits and reverse stock splits.

Historical Performance of the Underlying Fund

This historical data on the Underlying Fund is not necessarily indicative of the future performance of the Underlying Fund or what the value of the notes may be. Any historical upward or downward trend in the price per share of the Underlying Fund during any period set forth above is not an indication that the price per share of the Underlying Fund is more or less likely to increase or decrease at any time over the term of the notes.

Before investing in the notes, you should consult publicly available sources for the prices and trading pattern of the Underlying Fund.

| Accelerated Return Notes® | TS-11 |

| Accelerated Return Notes® Linked to the VanEck Vectors® Gold Miners ETF, due July , 2021 |

Supplement to the Plan of Distribution

Under our distribution agreement with BofAS, BofAS will purchase the notes from us as principal at the public offering price indicated on the cover of this term sheet, less the indicated underwriting discount.

BofAS has informed us that MLPF&S will purchase the notes from BofAS for resale, and will receive a selling concession in connection with the sale of the notes in an amount up to the full amount of underwriting discount set forth on the cover of this term sheet.

We may deliver the notes against payment therefor in New York, New York on a date that is greater than two business days following the pricing date. Under Rule 15c6-1 of the Securities Exchange Act of 1934, trades in the secondary market generally are required to settle in two business days, unless the parties to any such trade expressly agree otherwise. Accordingly, if the initial settlement of the notes occurs more than two business days from the pricing date, purchasers who wish to trade the notes more than two business days prior to the original issue date will be required to specify alternative settlement arrangements to prevent a failed settlement.

The notes will not be listed on any securities exchange. In the original offering of the notes, the notes will be sold in minimum investment amounts of 100 units. If you place an order to purchase the notes, you are consenting to MLPF&S and/or one of its affiliates acting as a principal in effecting the transaction for your account.

BofAS has advised us as follows: MLPF&S, BofAS or their affiliates may repurchase and resell the notes, with repurchases and resales being made at prices related to then-prevailing market prices or at negotiated prices determined by reference to their pricing models and at their discretion, and these prices will include MLPF&S’s and BofAS’s trading commissions and mark-ups or mark-downs. MLPF&S and BofAS may act as principal or agent in these market-making transactions; however, neither is obligated to engage in any such transactions. BofAS has informed us that at MLPF&S’s and BofAS’s discretion and for your benefit, assuming no changes in market conditions from the pricing date, MLPF&S and BofAS may offer to buy the notes in the secondary market at a price that may exceed the initial estimated value of the notes for a short initial period after the issuance of the notes. Any price offered by MLPF&S or BofAS for the notes will be based on then-prevailing market conditions and other considerations, including the performance of the Underlying Fund and the remaining term of the notes. However, none of us, MLPF&S, BofAS or any of our respective affiliates is obligated to purchase your notes at any price or at any time, and we cannot assure you that we, MLPF&S, BofAS or any of our respective affiliates will purchase your notes at a price that equals or exceeds the initial estimated value of the notes.

BofAS has informed us that, as of the date of this term sheet, it expects that if you hold your notes in a BofAS account, the value of the notes shown on your account statement will be based on BofAS’s estimate of the value of the notes if BofAS or another of its affiliates were to make a market in the notes, which it is not obligated to do; and that estimate will be based upon the price that BofAS may pay for the notes in light of then-prevailing market conditions, and other considerations, as mentioned above, and will include transaction costs. Any such price may be higher than or lower than the initial estimated value of the notes.

The distribution of the Note Prospectus in connection with these offers or sales will be solely for the purpose of providing investors with the description of the terms of the notes that was made available to investors in connection with their initial offering. Secondary market investors should not, and will not be authorized to, rely on the Note Prospectus for information regarding Credit Suisse or for any purpose other than that described in the immediately preceding sentence.

An investor’s household, as referenced on the cover of this term sheet, will generally include accounts held by any of the following, as determined by MLPF&S in its discretion and acting in good faith based upon information then available to MLPF&S:

| · | the investor’s spouse (including a domestic partner), siblings, parents, grandparents, spouse’s parents, children and grandchildren, but excluding accounts held by aunts, uncles, cousins, nieces, nephews or any other family relationship not directly above or below the individual investor; |

| · | a family investment vehicle, including foundations, limited partnerships and personal holding companies, but only if the beneficial owners of the vehicle consist solely of the investor or members of the investor’s household as described above; and |

| · | a trust where the grantors and/or beneficiaries of the trust consist solely of the investor or members of the investor’s household as described above; provided that, purchases of the notes by a trust generally cannot be aggregated together with any purchases made by a trustee’s personal account. |

Purchases in retirement accounts will not be considered part of the same household as an individual investor’s personal or other non-retirement account, except for individual retirement accounts (“IRAs”), simplified employee pension plans (“SEPs”), savings incentive match plan for employees (“SIMPLEs”), and single-participant or owners only accounts (i.e., retirement accounts held by self-employed individuals, business owners or partners with no employees other than their spouses).

Please contact your Merrill financial advisor if you have any questions about the application of these provisions to your specific circumstances or think you are eligible.

| Accelerated Return Notes® | TS-12 |

| Accelerated Return Notes® Linked to the VanEck Vectors® Gold Miners ETF, due July , 2021 |

Structuring the Notes

The notes are our debt securities, the return on which is linked to the performance of the Underlying Fund. As is the case for all of our debt securities, including our market-linked notes, the economic terms of the notes reflect our actual or perceived creditworthiness at the time of pricing. In addition, because market-linked notes result in increased operational, funding and liability management costs to us, the internal funding rate we use in pricing market-linked notes is typically lower than a rate reflecting the yield on our conventional debt securities of similar maturity in the secondary market. Because we use our internal funding rate to determine the value of the theoretical bond component, if on the pricing date our internal funding rate is lower than our secondary market credit rates, the initial estimated value of the notes will be higher than if the initial estimated value was based our secondary market credit rates.

Payments on the notes, including the amount you receive at maturity, will be calculated based on the $10 principal amount per unit and will depend on the performance of the Underlying Fund. In order to meet these payment obligations, at the time we issue the notes, we may choose to enter into certain hedging arrangements (which may include call options, put options or other derivatives) with BofAS or one of its affiliates. The terms of these hedging arrangements are determined by seeking bids from market participants, including BofAS and its affiliates, and take into account a number of factors, including our creditworthiness, interest rate movements, the volatility of the Underlying Fund, the tenor of the notes and the tenor of the hedging arrangements. The economic terms of the notes and their initial estimated value depend in part on the terms of these hedging arrangements.

BofAS has advised us that the hedging arrangements will include a hedging related charge of approximately $0.075 per unit, reflecting an estimated profit to be credited to BofAS from these transactions. Since hedging entails risk and may be influenced by unpredictable market forces, additional profits and losses from these hedging arrangements may be realized by BofAS or any third party hedge providers.

For further information, see “Risk Factors—General Risks Relating to ARNs” beginning on page PS-6 and “Supplemental Use of Proceeds and Hedging” on page PS-20 of product supplement EQUITY ARN-1.

| Accelerated Return Notes® | TS-13 |

| Accelerated Return Notes® Linked to the VanEck Vectors® Gold Miners ETF, due July , 2021 |

United States Federal Tax Considerations

This discussion supplements and, to the extent inconsistent therewith, supersedes the discussion in the accompanying product supplement under “United States Federal Tax Considerations.”

There are no statutory, judicial or administrative authorities that address the U.S. federal income tax treatment of the notes or instruments that are similar to the notes. In the opinion of our counsel, Davis Polk & Wardwell LLP, a note should be treated as a prepaid financial contract that is an “open transaction” for U.S. federal income tax purposes. However, there is uncertainty regarding this treatment. Moreover, our counsel’s opinion is based on market conditions as of the date of this preliminary pricing supplement and is subject to confirmation on the pricing date.

Assuming this treatment of the notes is respected and subject to the discussion in “United States Federal Tax Considerations” in the accompanying product supplement, the following U.S. federal income tax consequences should result:

| · | You should not recognize taxable income over the term of the notes prior to maturity, other than pursuant to a sale or other disposition. |

| · | Upon a sale or other disposition (including retirement) of a note, you should recognize gain or loss equal to the difference between the amount realized and your tax basis in the note. Subject to the discussion below concerning the potential application of the “constructive ownership” rules under Section 1260 of the Internal Revenue Code of 1986, as amended (the “Code”), such gain or loss should be long-term capital gain or loss if you held the note for more than one year. |

Even if the treatment of the notes as described herein is respected, there is a substantial risk that your purchase of a note will be treated as entry into a “constructive ownership transaction,” within the meaning of Section 1260 of the Code. In that case, all or a portion of any long-term capital gain you would otherwise recognize in respect of your notes would be recharacterized as ordinary income to the extent such gain exceeded the “net underlying long-term capital gain.” Any long-term capital gain recharacterized as ordinary income under Section 1260 would be treated as accruing at a constant rate over the period you held your notes, and you would be subject to an interest charge in respect of the deemed tax liability on the income treated as accruing in prior tax years. Due to the lack of governing authority under Section 1260, our counsel is not able to opine as to whether or how Section 1260 applies to the notes. You should read the section entitled “United States Federal Tax Considerations—Tax Consequences to U.S. Holders—Potential Application of Section 1260 of the Code” in the accompanying product supplement for additional information and consult your tax advisor regarding the potential application of the “constructive ownership” rule.

We do not plan to request a ruling from the IRS regarding the treatment of the notes, and the IRS or a court might not agree with the treatment described herein. In particular, the IRS could treat the notes as contingent payment debt instruments, in which case the tax consequences of ownership and disposition of the notes, including the timing and character of income recognized, could be materially and adversely affected. Moreover, the U.S. Treasury Department and the IRS have requested comments on various issues regarding the U.S. federal income tax treatment of “prepaid forward contracts” and similar financial instruments and have indicated that such transactions may be the subject of future regulations or other guidance. In addition, members of Congress have proposed legislative changes to the tax treatment of derivative contracts. Any legislation, Treasury regulations or other guidance promulgated after consideration of these issues could materially and adversely affect the tax consequences of an investment in the notes, possibly with retroactive effect. You should consult your tax advisor regarding possible alternative tax treatments of the notes and potential changes in applicable law.

Non-U.S. Holders.Subject to the discussions in the next paragraph and in “United States Federal Tax Considerations” in the accompanying product supplement, if you are a Non-U.S. Holder (as defined in the accompanying product supplement) of the notes, you generally should not be subject to U.S. federal withholding or income tax in respect of any amount paid to you with respect to the notes, provided that (i) income in respect of the notes is not effectively connected with your conduct of a trade or business in the United States, and (ii) you comply with the applicable certification requirements.

As discussed under “United States Federal Tax Considerations—Tax Consequences to Non-U.S. Holders—Possible Withholding under Section 871(m) of the Code” in the accompanying product supplement, Section 871(m) of the Code generally imposes a 30% withholding tax on “dividend equivalents” paid or deemed paid to Non-U.S. Holders with respect to certain financial instruments linked to U.S. equities or indices that include U.S. equities. Treasury regulations under Section 871(m), as modified by an IRS notice, exclude from their scope financial instruments issued prior to January 1, 2023 that do not have a “delta” of one with respect to any U.S. equity. Based on the terms of the notes and representations provided by us as of the date of this preliminary pricing supplement, our counsel is of the opinion that the notes should not be treated as transactions that have a “delta” of one within the meaning of the regulations with respect to any U.S. equity and, therefore, should not be subject to withholding tax under Section 871(m). However, the final determination regarding the treatment of the notes under Section 871(m) will be made as of the pricing date for the notes and it is possible that the notes will be subject to withholding tax under Section 871(m) based on circumstances on that date.

A determination that the notes are not subject to Section 871(m) is not binding on the IRS, and the IRS may disagree with this determination. Moreover, Section 871(m) is complex and its application may depend on your particular circumstances, including your other transactions. You should consult your tax advisor regarding the potential application of Section 871(m) to the notes.

If withholding tax applies to the notes, we will not be required to pay any additional amounts with respect to amounts withheld.

| Accelerated Return Notes® | TS-14 |

| Accelerated Return Notes® Linked to the VanEck Vectors® Gold Miners ETF, due July , 2021 |

You should read the section entitled “United States Federal Tax Considerations” in the accompanying product supplement. The preceding discussion, when read in combination with that section, constitutes the full opinion of Davis Polk & Wardwell LLP regarding the material U.S. federal tax consequences of owning and disposing of the notes.

You should also consult your tax advisor regarding all aspects of the U.S. federal income and estate tax consequences of an investment in the notes and any tax consequences arising under the laws of any state, local or non-U.S. taxing jurisdiction.

Where You Can Find More Information

We have filed a registration statement (including a product supplement, a prospectus supplement, and a prospectus) with the SEC for the offering to which this term sheet relates. Before you invest, you should read the Note Prospectus, including this term sheet, and the other documents that we have filed with the SEC, for more complete information about us and this offering. You may get these documents without cost by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, we, any agent, or any dealer participating in this offering will arrange to send you these documents if you so request by calling MLPF&S or BofAS toll-free at 1-800-294-1322.

“Accelerated Return Notes®” and “ARNs®” are registered service marks of Bank of America Corporation, the parent company of MLPF&S and BofAS.

| Accelerated Return Notes® | TS-15 |