PRICING SUPPLEMENT No. K1688 (To the Product Supplement No. I–C dated June 18, 2020, Prospectus Supplement dated June 18, 2020 and Prospectus dated June 18, 2020) Equity Fund Linked Securities |

Filed Pursuant to Rule 424(b)(2) | ||

Market Linked Securities—Leveraged Upside Participation Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023 |

n Linked to the iShares® Global Clean Energy ETF n Unlike ordinary debt securities, the securities do not pay interest or repay a fixed amount of principal at stated maturity. Instead, the securities provide for a maturity payment amount that may be greater than, equal to or less than the original offering price of the securities, depending on the performance of the Fund from the starting price to the ending price. The maturity payment amount will reflect the following terms: n If the ending price is greater than the starting price, you will receive the original offering price plus 200% participation in the upside performance of the Fund, subject to a maximum return at stated maturity of 33% of the original offering price. As a result of the maximum return, the maximum maturity payment amount is $1,330 n If the ending price is equal to or less than the starting price but equal to or greater than the threshold price, you will be repaid the original offering price n If the ending price is less than the threshold price, you will receive less than the original offering price and have 1-to-1 downside exposure to the decrease in the price of the Fund beyond the threshold price n The threshold price is equal to 82.50% of the starting price n You may lose up to 82.50% of the original offering price n All payments on the securities are subject to the credit risk of Credit Suisse; if Credit Suisse defaults on its obligations, you could lose some or all of your investment n No periodic interest payments or dividends n No exchange listing; you should be willing and able to hold your securities to stated maturity |

The securities have complex features and investing in the securities involves risks not associated with an investment in conventional debt securities. See “Selected Risk Considerations” beginning on page PRS-12 in this pricing supplement and “Risk Factors” beginning on page PS-3 of the accompanying product supplement.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities or passed upon the accuracy or the adequacy of this pricing supplement or any product supplement, the prospectus supplement and the prospectus. Any representation to the contrary is a criminal offense.

Original Offering Price | Agent Discount(1)(2) | Proceeds to Issuer | |

| Per Security | $1,000.00 | $29.75 | $970.25 |

| Total | $2,343,000 | $69,704.25 | $2,273,295.75 |

| (1) | Wells Fargo Securities, LLC (“WFS”) is the agent for the distribution of the securities. WFS will receive an agent discount of $29.75 per security. The agent may resell the securities to other securities dealers at the original offering price less a concession of $17.50 per security. Such securities dealers may include those using the trade name Wells Fargo Advisors (“WFA”) (the trade name of the retail brokerage business of WFS affiliates, Wells Fargo Clearing Services, LLC and Wells Fargo Advisors Financial Network, LLC). In addition to the selling concession allowed to WFA, the agent will pay $0.75 per security of the agent discount to WFA as a distribution expense fee for each security sold by WFA. See “Supplemental Plan of Distribution” in this pricing supplement for further information. |

| (2) | Credit Suisse will pay a fee of $1.00 per security to selected securities dealers in consideration for marketing and other services in connection with the distribution of the securities to other securities dealers. |

Credit Suisse AG (“Credit Suisse”) currently estimates the value of each $1,000 original offering price of the securities on the pricing date is $957 (as determined by reference to our pricing models and the rate we are currently paying to borrow funds through issuance of the securities (our “internal funding rate”)). See “Selected Risk Considerations” in this pricing supplement.

The securities are unsecured obligations of Credit Suisse, and all payments on the securities are subject to the credit risk of Credit Suisse.

The securities are not deposit liabilities and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency of the United States, Switzerland or any other jurisdiction.

Wells Fargo Securities

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

| Additional Information about the Issuer and the Securities |

You should read this pricing supplement together with the product supplement dated June 18, 2020, the prospectus supplement dated June 18, 2020 and the prospectus dated June 18, 2020, relating to our Medium-Term Notes of which these securities are a part. You may access these documents on the SEC website at www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC website):

| • | Product Supplement No. I–C dated June 18, 2020: |

https://www.sec.gov/Archives/edgar/data/1053092/000095010320011958/dp130587_424b2-ps1c.htm

| • | Prospectus Supplement and Prospectus dated June 18, 2020: |

https://www.sec.gov/Archives/edgar/data/1053092/000110465920074474/tm2019510-8_424b2.htm

In the event the terms of the securities described in this pricing supplement differ from, or are inconsistent with, the terms described in any accompanying product supplement, the prospectus supplement or prospectus, the terms described in this pricing supplement will control.

Our Central Index Key, or CIK, on the SEC website is 1053092. As used in this pricing supplement, “we,” “us,” or “our” refers to Credit Suisse.

This pricing supplement, together with the documents listed above, contains the terms of the securities and supersedes all other prior or contemporaneous oral statements as well as any other written materials including preliminary or indicative pricing terms, fact sheets, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. We may, without the consent of the registered holder of the securities and the owner of any beneficial interest in the securities, amend the securities to conform to its terms as set forth in this pricing supplement and the documents listed above, and the trustee is authorized to enter into any such amendment without any such consent. You should carefully consider, among other things, the matters set forth in “Selected Risk Considerations” in this pricing supplement and “Risk Factors” in any accompanying product supplement, “Foreign Currency Risks” in the accompanying prospectus, and any risk factors we describe in the combined Annual Report on Form 20-F of Credit Suisse Group AG and us incorporated by reference therein, and any additional risk factors we describe in future filings we make with the SEC under the Securities Exchange Act of 1934, as amended, as the securities involve risks not associated with conventional debt securities. You should consult your investment, legal, tax, accounting and other advisors before deciding to invest in the securities.

PRS-2

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

| Investor Considerations |

We have designed the securities for investors who:

| § | seek 200% leveraged exposure to the upside performance of the Fund if the ending price is greater than the starting price, subject to the maximum return at stated maturity of 33% of the original offering price; |

| § | desire to limit downside exposure to the Fund through the 17.50% buffer; |

| § | understand that if the ending price is less than the threshold price, they will receive less than the original offering price per security at stated maturity, and they may lose 82.50% of their investment; |

| § | are willing to forgo interest payments on the securities and dividends on shares of the Fund; and |

| § | are willing to hold the securities to stated maturity. |

The securities are not designed for, and may not be an appropriate investment for, investors who:

| § | seek a liquid investment or are unable or unwilling to hold the securities to stated maturity; |

| § | are unwilling to accept the risk that the ending price may be less than the threshold price; |

| § | seek uncapped exposure to the upside performance of the Fund; |

| § | seek full return of the original offering price of the securities at stated maturity; |

| § | are unwilling to purchase securities with an estimated value as of the pricing date that is lower than the original offering price, as set forth on the cover page; |

| § | seek current income; |

| § | are unwilling to accept the risk of exposure to companies included in the Fund; |

| § | seek exposure to the Fund but are unwilling to accept the risk/return trade-offs inherent in the maturity payment amount for the securities; |

| § | are unwilling to accept the credit risk of Credit Suisse to obtain exposure to the Fund generally, or to the exposure to the Fund that the securities provide specifically; or |

| § | prefer the lower risk of conventional fixed income investments with comparable maturities issued by companies with comparable credit ratings. |

PRS-3

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

| Terms of the Securities | |

| Market Measure: | iShares® Global Clean Energy ETF (the “Fund”) |

| Pricing Date: | March 31, 2021 |

| Issue Date: | April 6, 2021 (T+4) |

| Original Offering Price: | $1,000 per security. References in this pricing supplement to a “security” are to a security with an original offering price of $1,000. |

| Calculation Day: | September 29, 2023. If such day is not a trading day, the calculation day will be postponed to the next succeeding trading day. The calculation day may also be postponed due to the occurrence of a market disruption event. See “Additional Terms of the Securities—Market Disruption Events” below. To the extent that we make any change to the expected issue date, the calculation day may also be changed in our discretion to ensure that the term of the securities remains the same. |

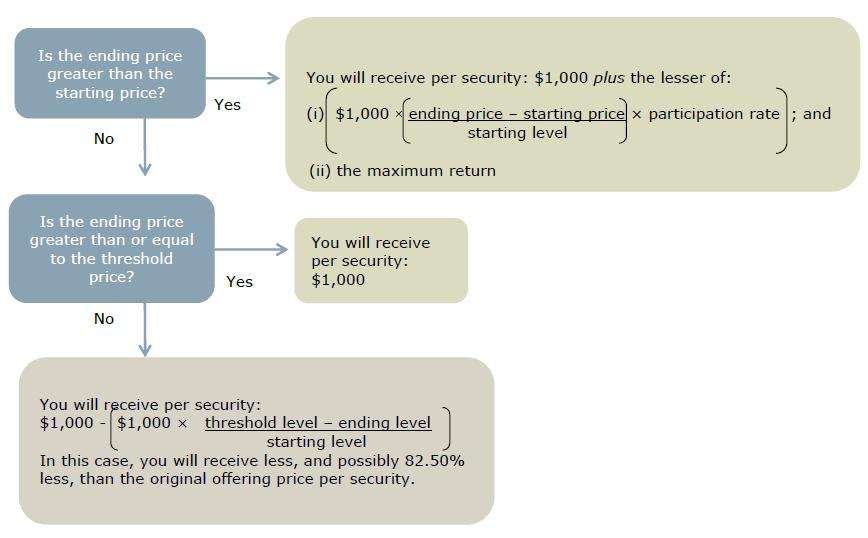

| Maturity Payment Amount: | The “maturity payment amount” per security will equal:

· if the ending price is greater than the starting price: $1,000 plus the lesser of:

(i)

(ii) the maximum return;

· if the ending price is less than or equal to the starting price, but greater than or equal to the threshold price: $1,000; or

· if the ending price is less than the threshold price:

If the ending price is less than the threshold price, you will receive less than the original offering price of your securities at stated maturity, and you may lose 82.50% of your investment.

All payments on the securities are subject to the credit risk of Credit Suisse; if Credit Suisse defaults on its obligations, you could lose some or all of your investment.

|

| Stated Maturity: | October 6, 2023. If the calculation day is postponed, the stated maturity will be the later of (i) October 6, 2023 and (ii) three business days after such calculation day as postponed. See “—Calculation Day” and “Additional Terms of the Securities—Market Disruption Events” below. To the extent that we make any change to the expected issue date, stated maturity may also be changed in our discretion to ensure that the term of the securities remains the same. If stated maturity is not a business day, the payment to be made at stated maturity will be made on the next succeeding business day with the same force and effect as if it had been made at stated maturity. The securities are not subject to redemption by Credit Suisse or repayment at the option of any holder of the securities prior to stated maturity. No interest or other payment will be payable hereon because of any such postponement of the stated maturity. |

, and

, andPRS-4

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

| Starting Price: | $24.30, which is the fund closing price on the pricing date.

In the event that the fund closing price is not available on the pricing date, the starting price will be determined on the immediately following trading day on which a fund closing price is available. |

| Ending Price: | The “ending price” will be the fund closing price of the Fund on the calculation day. |

| Fund Closing Price: | The “fund closing price” with respect to the Fund (or one unit of any other security for which a fund closing price must be determined) on any trading day means the product of (i) the closing price of one share of the Fund or such other security on such trading day and (ii) the adjustment factor applicable to the Fund on such trading day. |

| Closing Price: | The “closing price” with respect to a share of the Fund (or one unit of any other security for which a closing price must be determined) on any trading day means the price, at the scheduled weekday closing time, without regard to after hours or any other trading outside the regular trading session hours, of the share on the principal United States securities exchange registered under the Securities Exchange Act of 1934, as amended, on which the share (or any such other security) is listed or admitted to trading. |

| Threshold Price: | $20.0475, which is equal to 82.50% of the starting price. |

| Maximum Return: | The “maximum return” is 33% of the original offering price per security ($330 per security). As a result of the maximum return, the maximum maturity payment amount of the securities is $1,330 per security. |

| Participation Rate: | 200% |

| Adjustment Factor: | The “adjustment factor” means, with respect to a share of the Fund (or one unit of any other security for which a fund closing price must be determined), 1.0, subject to adjustment in the event of certain events affecting the shares of the Fund. See “Additional Terms of the Securities—Anti-dilution Adjustments Relating to the Fund; Alternate Calculation” below.

|

| Calculation Agent: | Credit Suisse International |

| No Listing: | The securities will not be listed on any securities exchange or automated quotation system |

| Material Tax Consequences: | For a discussion of the material U.S. federal income and certain estate tax consequences of the ownership and disposition of the securities, see “United States Federal Tax Considerations” herein. |

Supplemental

| Under the terms of the distributor accession confirmation with WFS dated as of August 1, 2016, WFS will act as agent for the securities and will receive an agent discount of $29.75 per security. The agent may resell the securities to other securities dealers at the original offering price of the securities less a concession of $17.50 per security. Such securities dealers may include WFA (the trade name of the retail brokerage business of WFS affiliates Wells Fargo Clearing Services, LLC and Wells Fargo Advisors Financial Network, LLC). WFS will pay $0.75 per security of the agent’s discount to WFA as a distribution expense fee for each security sold by WFA.

In addition, Credit Suisse will pay a fee of $1.00 per security to selected securities dealers in consideration for marketing and other services in connection with the distribution of the securities to other securities dealers.

We expect to deliver the securities against payment for the securities on the issue date indicated herein, which may be a date that is greater than two business days following the pricing date. Under Rule 15c6-1 of the Securities Exchange Act of 1934, as amended, trades in the secondary market generally are required to settle in two business days, unless the parties to a trade expressly agree otherwise. Accordingly, if the issue date is more than two business days after the pricing date, purchasers who wish to transact in the securities more than two business days prior to the issue date will be required to specify alternative settlement arrangements to prevent a failed settlement.

The securities and the related offer to purchase securities and sale of securities under the terms and conditions provided in this pricing supplement, product supplement, prospectus supplement and prospectus do not constitute

|

PRS-5

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

a public offering in any non-U.S. jurisdiction, and are being made available only to individually identified investors pursuant to a private offering as permitted in the relevant jurisdiction. The securities are not, and will not be, registered with any securities exchange or registry located outside of the United States and have not been registered with any non-U.S. securities or banking regulatory authority. The contents of this pricing supplement have not been reviewed or approved by any non-U.S. securities or banking regulatory authority. Any person who wishes to acquire the securities from outside the United States should seek the advice or legal counsel as to the relevant requirements to acquire these securities.

Notice to Prospective Investors in Argentina

The securities are not and will not be marketed in Argentina by means of a public offering, as such term is defined under Section 2 of Law Number 26,831, as amended. No application has been or will be made with the Argentine Comisión Nacional de Valores, the Argentine securities governmental authority, to offer the securities in Argentina. The contents of this pricing supplement have not been reviewed by the Argentine Comisión Nacional de Valores.

Notice to Prospective Investors in Brazil

The securities have not been and will not be issued nor publicly placed, distributed, offered or negotiated in the Brazilian capital markets and, as a result, have not been and will not be registered with the Comissão de Valores Mobiliáros (“CVM”). Any public offering or distribution, as defined under Brazilian laws and regulations, of the securities in Brazil is not legal without prior registration under Law 6,385/76, and CVM applicable regulation. Documents relating to the offering of the securities, as well as information contained therein, may not be supplied to the public in Brazil (as the offering of the securities is not a public offering of securities in Brazil), nor be used in connection with any offer for subscription or sale of the securities to the public in Brazil. Persons wishing to offer or acquire the securities within Brazil should consult with their own counsel as to the applicability of registration requirements or any exemption therefrom.

Notice to Prospective Investors in the British Virgin Islands

The securities have not been, and will not be, registered under the laws and regulations of the British Virgin Islands, nor has any regulatory authority in the British Virgin Islands passed comment upon or approved the accuracy or adequacy of this pricing supplement. This pricing supplement shall not constitute an offer, invitation or solicitation to any member of the public in the British Virgin Islands for the purposes of the Securities and Investment Business Act, 2010, of the British Virgin Islands.

Notice to Prospective Investors in Chile

Neither the issuer nor the securities have been registered with the Comisión Para el Mercado Financiero pursuant to Law No. 18.045, the Ley de Mercado de Valores and regulations thereunder, so they cannot be publicly offered in Chile. This pricing supplement does not constitute an offer of, or an invitation to subscribe for or purchase, the securities in the republic of Chile, other than to individually identified buyers pursuant to a private offering within the meaning of Article 4 of the Ley de Mercado de Valores (an offer that is not addressed to the public at large or to a certain sector or specific group of the public).

Notice to Prospective Investors in Mexico

The securities have not been registered with the National Registry of Securities maintained by the Mexican National Banking and Securities Commission and may not be offered or sold publicly in Mexico. This pricing supplement, product supplement, prospectus supplement and prospectus may not be publicly distributed in Mexico. The securities may only be offered in a private offering pursuant to Article 8 of the Securities Market Law.

|

PRS-6

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

Notice to Prospective Investors in Panama

The securities have not been and will not be registered with the Superintendency of Securities Market of the Republic of Panama under Decree Law N°1 of July 8, 1999 (the “Panamanian Securities Act”) and may not be publicly offered or sold within Panama, except in certain limited transactions exempt from the registration requirements of the Panamanian Securities Act, including the private placement rule based on number 2 of Article 83 of Law Decree 1 of July 8, 1999 (or number 2 of Article 129 of the Unified Text of Law Decree 1 of July 8, 1999). The securities do not benefit from the tax incentives provided by the Panamanian Securities Act and are not subject to regulation or supervision by the Superintendency of Securities Market of the Republic of Panama.

Notice to Prospective Investors in Paraguay

The sale of the securities qualifies as a private placement pursuant to Law No. 5810/17 “Stock Market”. The securities must not be offered or sold to the public in Paraguay, except under circumstances which do not constitute a public offering in accordance with Paraguayan regulations. The securities are not and will not be registered before the Paraguayan securities supervisory body Comisión Nacional de Valores (“CNV”) the Paraguayan private stock exchange Bolsa de Valores y Productos de Asunción (“BVPASA”). The issuer is also not registered before the CNV or the BVPASA.

In no case may securities not registered before the CNV be offered to the general public via mass media such as press, radio, television, or internet when such media are publicly accessible in the Republic of Paraguay, regardless of the location from where they are issued.

The privately placed securities are not registered with the National Securities Commission, and therefore do not have tax benefits and are not negotiable through the BVPASA. Privately placed securities may have less liquidity, making it difficult to sell such securities in the secondary market, which could also affect the sale price. Private securities of issuers not registered before the CNV may not have periodic financial information or audited financial statements, which could generate greater risk to the investor due to the asymmetry of information. It is the responsibility of the investor to ascertain and assess the risk assumed in the acquisition of the security.

Notice to Prospective Investors in Peru

The securities have not been and will not be registered with the Capital Markets Public Registry of the Capital Markets Superintendence (“SMV”) nor the Lima Stock Exchange Registry (“RBVL”) for their public offering in Peru under the Peruvian Capital Markets Law (Law No. 861/ Supreme Decree No. 093-2002) and the decrees and regulations thereunder. Consequently, the securities may not be offered or sold, directly or indirectly, nor may this pricing supplement or any other offering material relating to the securities be distributed or caused to be distributed in Peru to the general public. The securities may only be offered in a private offering under Peruvian regulation and without using mass marketing, which is defined as a marketing strategy utilizing mass distribution and mass media to offer, negotiate or distribute securities to the whole market. Mass media includes newspapers, magazines, radio, television, mail, meetings, social networks, Internet servers located in Peru, and other media or technology platforms.

Notice to Prospective Investors in Taiwan

The securities may be made available outside Taiwan for purchase by Taiwan residents outside Taiwan but may not be offered or sold in Taiwan.

Notice to Prospective Investors in Uruguay

|

PRS-7

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

| The sale of the securities qualifies as a private placement pursuant to section 2 of Uruguayan law 18,627. The securities must not be offered or sold to the public in Uruguay, except in circumstances which do not constitute a public S-31 offering or distribution under Uruguayan laws and regulations. The securities are not and will not be registered with the Financial Services Superintendency of the Central Bank of Uruguay. | |

| Denominations: | $1,000 and any integral multiple of $1,000. |

| Events of Default: | With respect to these securities, the first bullet of the first sentence of “Description of Debt Securities— Events of Default” in the accompanying prospectus is amended to read in its entirety as follows:

· a default in payment of the principal or any premium on any debt security of that series when due, and such default continues for 30 days;

|

| CUSIP: | 22552XDH3 |

PRS-8

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

| Supplemental Terms of the Securities |

For purposes of the securities offered by this pricing supplement, all references to each of the following terms used in any product supplement will be deemed to refer to the corresponding term used in this pricing supplement, as set forth in the table below:

Product Supplement Term | Pricing Supplement Term |

| Underlying | Fund |

| Trade date | Pricing date |

| Principal amount | Original offering price |

| Valuation date | Calculation day |

| Maturity date | Stated maturity |

| Closing level | Fund closing price |

| Initial level | Starting price |

| Final level | Ending price |

| Knock-in level | Threshold price |

PRS-9

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

| Determining Maturity Payment Amount |

On the stated maturity date, you will receive a cash payment per security (the maturity payment amount) calculated as follows:

PRS-10

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

| Hypothetical Payout Profile |

The following profile is based on a maximum return of 33% or $330 per security, a participation rate of 200% and a threshold price equal to 82.50% of the starting price. This graph has been prepared for purposes of illustration only. Your actual return will depend on the actual ending price and whether you hold your securities to maturity.

|

PRS-11

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

| Selected Risk Considerations |

The securities have complex features and investing in the securities will involve risks not associated with an investment in conventional debt securities. You should carefully consider the risk factors set forth below as well as the other information contained in this pricing supplement, any product supplement, prospectus supplement and prospectus, including the documents they incorporate by reference. An investment in the securities involves significant risks. This section describes material risks relating to an investment in the securities.

Risks Relating to the Securities Generally

You May Receive Less Than The Original Offering Price Of Your Securities At Stated Maturity.

If the ending price is less than the threshold price, the maturity payment amount that you receive at stated maturity will be reduced by an amount equal to the decline in the price of the Fund to the extent it is below the threshold price (expressed as a percentage of the starting price). The threshold price is 82.50% of the starting price. As a result, you may receive less than the original offering price per security at stated maturity, and you may lose 82.50% of your investment, even if the value of the Fund is greater than or equal to the starting price or the threshold price at certain times during the term of the securities.

Regardless Of The Amount Of Any Payment You Receive On The Securities, Your Actual Yield May Be Different In Real Value Terms.

Inflation may cause the real value of any payment you receive on the securities to be less at stated maturity than it is at the time you invest. An investment in the securities also represents a forgone opportunity to invest in an alternative asset that generates a higher real return. You should carefully consider whether an investment that may result in a return that is lower than the return on alternative investments is appropriate for you.

The Potential Return On The Securities Is Limited To The Maximum Return.

The appreciation potential of the securities will be limited to the maximum return, regardless of any appreciation of the Fund, which may be significant. The Fund may appreciate by significantly more than the percentage represented by the maximum return, in which case an investment in the securities will underperform a hypothetical alternative investment providing a 1-to-1 return based on the performance of the Fund. Furthermore, the effect of the participation rate will be progressively reduced for all ending levels exceeding the ending level at which the maximum return is reached.

No Periodic Interest Will Be Paid On The Securities.

We will not pay interest on the securities. You may receive less at stated maturity than you could have earned on ordinary interest bearing debt securities with similar maturities, including other of our debt securities, since the maturity payment amount is based on the appreciation or depreciation of the Fund.

Stated Maturity May Be Postponed If The Calculation Day Is Postponed.

The calculation day will be postponed if the originally scheduled calculation day is not a trading day or if the calculation agent determines that a market disruption event has occurred or is continuing on the calculation day. If such a postponement occurs, stated maturity will be the later of (i) the initial stated maturity and (ii) three business days after the postponed calculation day.

The Probability That The Ending Price Will Be Less Than The Threshold Price Will Depend On The Volatility Of The Fund.

“Volatility” refers to the frequency and magnitude of changes in the price of the Fund. The greater the expected volatility with respect to the Fund on the pricing date, the higher the expectation as of the pricing date that the ending price could be less than the threshold price, indicating a higher expected risk of loss on the securities. The terms of the securities are set, in part, based on expectations about the volatility of the Fund as of the pricing date. The volatility of the Fund can change significantly over the term of the securities. The price of the Fund could fall sharply, which could result in a loss of 82.50% of the original offering price of the securities. You should be willing to accept the downside market risk of the Fund and the potential to lose a significant portion of the original offering price per security at stated maturity.

The U.S. Federal Tax Consequences Of An Investment In The Securities Are Unclear.

There is no direct legal authority regarding the proper U.S. federal tax treatment of the securities, and we do not plan to request a ruling from the Internal Revenue Service (the “IRS”). Consequently, significant aspects of the tax treatment of the securities are uncertain, and the IRS or a court might not agree with the treatment of the securities as prepaid financial contracts that are treated as “open transactions.” If the IRS were successful in asserting an alternative treatment of the securities, the tax consequences of the ownership and disposition of the securities, including the timing and character of income recognized by U.S. investors and the withholding tax consequences to non-U.S. investors, might

PRS-12

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

be materially and adversely affected. Even if the treatment of the securities described herein is respected, there is a substantial risk that a security will be treated as a “constructive ownership transaction,” with potentially adverse consequences described below under “United States Federal Tax Considerations.” Moreover, future legislation, Treasury regulations or IRS guidance could adversely affect the U.S. federal tax treatment of the securities, possibly retroactively.

Risks Relating to the Fund

Historical Performance Of The Fund Is Not Indicative Of Future Performance.

The future performance of the Fund cannot be predicted based on its historical performance. We cannot guarantee that the fund closing price or ending price will be at a price that would result in a positive return on your overall investment in the securities.

We Cannot Control The Actions Of Any Issuers Whose Equity Securities Are Included In Or Held By The Fund.

We cannot control the actions of any issuers of the equity securities included in or held by the Fund. Actions by such issuers may have an adverse effect on the price of the Fund and, consequently, on the value of the securities.

There Are Risks Associated With The Fund.

Although shares of the Fund are listed for trading on a national securities exchange and a number of similar products have been traded on various national securities exchanges for varying periods of time, there is no assurance that an active trading market will continue for the shares of the Fund or that there will be liquidity in the trading market. The Fund is subject to management risk, which is the risk that a Fund’s investment strategy, the implementation of which is subject to a number of constraints, may not produce the intended results. Pursuant to the Fund’s investment strategy or otherwise, its investment advisor may add, delete or substitute the assets held by the Fund. Any of these actions could adversely affect the price of the shares of the Fund and consequently the value of the securities. For additional information on the Fund, see “The iShares® Global Clean Energy ETF” herein.

The Performance And Market Value Of The Fund, Particularly During Periods Of Market Volatility, May Not Correlate To The Performance Of The Tracked Index.

The Fund will generally invest in all of the equity securities included in the index tracked by the Fund (the “tracked index”), but may not fully replicate such tracked index. There may be instances where the Fund’s investment advisor may choose to overweight another stock in the Fund’s tracked index, purchase securities not included in the Fund’s tracked index that the investment advisor believes are appropriate to substitute for a security included in the tracked index or utilize various combinations of other available investment techniques. In addition, the performance of the Fund will reflect additional transaction costs and fees that are not included in the calculation of the Fund’s tracked index. Finally, because the shares of the Fund are traded on a national securities exchange and are subject to market supply and investor demand, the market value of one share of the Fund may differ from the net asset value per share of the Fund.

During periods of market volatility, securities held by the Fund may be unavailable in the secondary market, market participants may be unable to calculate accurately the net asset value per share of the Fund and the liquidity of the Fund may be adversely affected. This kind of market volatility may also disrupt the ability of market participants to create and redeem shares of the Fund. Further, market volatility may adversely affect, sometimes materially, the prices at which market participants are willing to buy and sell shares of the Fund. As a result, under these circumstances, the market value of shares of the Fund may vary substantially from the net asset value per share of the Fund. For all the foregoing reasons, the performance of the Fund may not correlate with the performance of the tracked index. For additional information on the Fund, see “The iShares® Global Clean Energy ETF” herein.

Emerging Markets Risk.

The Fund and the tracked index are exposed to the political and economic risks of an emerging market country. In recent years, some emerging markets have undergone significant political, economic and social upheaval. Such far-reaching changes have resulted in constitutional and social tensions and, in some cases, instability and reaction against market reforms has occurred. With respect to any emerging market nation, there is the possibility of nationalization, expropriation or confiscation, political changes, government regulation and social instability. There can be no assurance that future political changes will not adversely affect the economic conditions of an emerging market nation. Political or economic instability could have an adverse effect on the performance of the securities.

Currency Exchange Risk.

Because some of the prices of the equity securities included in the Fund are converted into U.S. dollars for purposes of calculating the fund closing price of the Fund, investors will be exposed to currency exchange rate risk with respect to each of the currencies in which the non-U.S. equity securities included in the Fund trade. Currency exchange rates may be highly volatile, particularly in relation to emerging nations’ currencies. Significant changes in currency exchange rates, including changes in liquidity and prices, can occur within very short periods of

PRS-13

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

time. Currency exchange rate risks include, but are not limited to, convertibility risk, market volatility and potential interference by foreign governments through regulation of local markets, foreign investment or particular transactions in foreign currency. These factors may adversely affect the values of the non-U.S. equity securities included in the Fund, the fund closing price of the Fund and the value of the securities.

Risks Associated With Investments In Securities Linked To The Performance of Foreign Equity Securities.

The Fund includes the stocks of foreign companies and you should be aware that investments in securities linked to the value of foreign equity securities involve particular risks. Foreign securities markets may have less liquidity and may be more volatile than the U.S. securities markets, and market developments may affect foreign markets differently than U.S. securities markets. Direct or indirect government intervention to stabilize a foreign securities market, as well as cross-shareholdings in foreign companies, may affect trading prices and volumes in those markets. Also, there is generally less publicly available information about non-U.S. companies that are not subject to the reporting requirements of the Securities and Exchange Commission, and non-U.S. companies are subject to accounting, auditing and financial reporting standards and requirements that differ from those applicable to U.S. reporting companies.

The prices and performance of securities of non-U.S. companies are subject to political, economic, financial, military and social factors which could negatively affect foreign securities markets, including the possibility of recent or future changes in a foreign government’s economic, monetary and fiscal policies, the possible imposition of, or changes in, currency exchange laws or other laws or restrictions applicable to foreign companies or investments in foreign equity securities, the possibility of imposition of withholding taxes on dividend income, the possibility of fluctuations in the rate of exchange between currencies, the possibility of outbreaks of hostility or political instability and the possibility of natural disaster or adverse public health developments. Moreover, the relevant non-U.S. economies may differ favorably or unfavorably from the U.S. economy in important respects, such as growth of gross national product, rate of inflation, trade surpluses or deficits, capital reinvestment, resources and self-sufficiency.

The securities included in the Fund may be listed on a foreign stock exchange. A foreign stock exchange may impose trading limitations intended to prevent extreme fluctuations in individual security prices and may suspend trading in certain circumstances. These actions could limit variations in the fund closing price of the Fund which could, in turn, adversely affect the value of the securities.

The Stocks Included In The Fund Are Concentrated In One Particular Sector.

All of the stocks included in the Fund are issued by companies in a single sector. As a result, the stocks that will determine the performance of the Fund are concentrated in a single sector. Although an investment in the securities will not give holders any ownership or other direct interests in the stocks held by the Fund, the return on an investment in the securities will be subject to certain risks associated with a direct equity investment in companies in a single sector. Accordingly, by investing in the securities, you will not benefit from the diversification which could result from an investment linked to companies that operate in a broader range of sectors.

No Ownership Rights Relating To The Fund.

Your return on the securities will not reflect the return you would realize if you actually owned shares of the Fund or the assets that comprise the Fund. The return on your investment is not the same as the total return you would receive based on a purchase of shares of the Fund or the assets that comprise the Fund.

No Dividend Payments Or Voting Rights.

As a holder of the securities, you will not have voting rights or rights to receive cash dividends or other distributions or other rights with respect to shares of the Fund or the assets that comprise the Fund.

Anti-Dilution Protection Is Limited.

The calculation agent will make anti-dilution adjustments for certain events affecting the Fund. However, an adjustment will not be required in response to all events that could affect the Fund. If an event occurs that does not require the calculation agent to make an adjustment, or if an adjustment is made but such adjustment does not fully reflect the economics of such event, the value of the securities may be materially and adversely affected. See “Additional Terms of the Securities—Anti-dilution Adjustments Relating to the Fund; Alternate Calculation” herein.

Risks Relating to the Issuer

The Securities Are Subject To The Credit Risk Of Credit Suisse.

Investors are dependent on our ability to pay all amounts due on the securities and, therefore, if we were to default on our obligations, you may not receive any amounts owed to you under the securities. In addition, any decline in our credit ratings, any adverse changes in the

PRS-14

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

market’s view of our creditworthiness or any increase in our credit spreads is likely to adversely affect the value of the securities prior to stated maturity.

Credit Suisse Is Subject To Swiss Regulation.

As a Swiss bank, Credit Suisse is subject to regulation by governmental agencies, supervisory authorities and self-regulatory organizations in Switzerland. Such regulation is increasingly more extensive and complex and subjects Credit Suisse to risks. For example, pursuant to Swiss banking laws, the Swiss Financial Market Supervisory Authority (“FINMA”) may open resolution proceedings if there are justified concerns that Credit Suisse is over-indebted, has serious liquidity problems or no longer fulfills capital adequacy requirements. FINMA has broad powers and discretion in the case of resolution proceedings, which include the power to convert debt instruments and other liabilities of Credit Suisse into equity and/or cancel such liabilities in whole or in part. If one or more of these measures were imposed, such measures may adversely affect the terms and market value of the securities and/or the ability of Credit Suisse to make payments thereunder and you may not receive any amounts owed to you under the securities.

Risks Relating to Conflicts of Interest

Hedging And Trading Activity Could Adversely Affect Our Payment To You At Stated Maturity.

Credit Suisse (or any of its affiliates) or WFS (or any of its affiliates) may carry out hedging activities related to the securities, including in the Fund or instruments related to the Fund. Credit Suisse (or any of its affiliates) or WFS (or any of its affiliates) may also trade in the Fund or instruments related to the Fund from time to time. Any of these hedging or trading activities on or prior to the pricing date and during the term of the securities could adversely affect our payment to you at stated maturity.

Our Economic Interests Are Potentially Adverse To Your Interests.

We and our affiliates play a variety of roles in connection with the issuance of the securities, including acting as calculation agent for the offering of the securities, hedging our obligations under the securities and determining their estimated value. In performing these duties, the economic interests of us and our affiliates are potentially adverse to your interests as an investor in the securities. Further, hedging activities may adversely affect any payment on or the value of the securities. Any profit in connection with such hedging activities will be in addition to any other compensation that we and our affiliates receive for the sale of the securities, which creates an additional incentive to sell the securities to you.

Risks Relating to the Estimated Value and Secondary Market Prices of the Securities

Unpredictable Economic And Market Factors Will Affect The Value Of The Securities.

The payout on the securities can be replicated using a combination of the components described in “The Estimated Value Of The Securities On The Pricing Date Is Less Than The Original Offering Price.” Therefore, in addition to the fund closing price of the Fund, the terms of the securities at issuance and the value of the securities prior to stated maturity may be influenced by factors that impact the value of fixed income securities and options in general such as:

| o | the expected and actual volatility of the Fund; |

| o | the time to stated maturity of the securities; |

| o | the dividend rate on the equity securities included in the Fund; |

| o | interest and yield rates in the market generally; |

| o | investors’ expectations with respect to the rate of inflation; |

| o | events affecting companies engaged in the industries tracked by the Fund; |

| o | geopolitical conditions and economic, financial, political, regulatory, judicial or other events that affect the components included in the Fund or markets generally and which may affect the price of the Fund; and |

| o | our creditworthiness, including actual or anticipated downgrades in our credit ratings. |

Some or all of these factors may influence the price that you will receive if you choose to sell your securities prior to stated maturity. The impact of any of the factors set forth above may enhance or offset some or all of any change resulting from another factor or factors.

PRS-15

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

The Estimated Value Of The Securities On The Pricing Date Is Less Than The Original Offering Price.

The initial estimated value of your securities on the pricing date (as determined by reference to our pricing models and our internal funding rate) is less than the original offering price. The original offering price of the securities includes any discounts or commissions as well as transaction costs such as expenses incurred to create, document and market the securities and the cost of hedging our risks as issuer of the securities through one or more of our affiliates (which includes a projected profit). These costs will be effectively borne by you as an investor in the securities. These amounts will be retained by Credit Suisse or our affiliates in connection with our structuring and offering of the securities (except to the extent discounts or commissions are reallowed to other broker-dealers or any costs are paid to third parties).

On the pricing date, we value the components of the securities in accordance with our pricing models. These include a fixed income component valued using our internal funding rate, and individual option components valued using proprietary pricing models dependent on inputs such as volatility, correlation, dividend rates, interest rates and other factors, including assumptions about future market events and/or environments. These inputs may be market-observable or may be based on assumptions made by us in our discretionary judgment As such, the payout on the securities can be replicated using a combination of these components and the value of these components, as determined by us using our pricing models, will impact the terms of the securities at issuance. Our option valuation models are proprietary. Our pricing models take into account factors such as interest rates, volatility and time to stated maturity of the securities, and they rely in part on certain assumptions about future events, which may prove to be incorrect.

Because Credit Suisse’s pricing models may differ from other issuers’ valuation models, and because funding rates taken into account by other issuers may vary materially from the rates used by Credit Suisse (even among issuers with similar creditworthiness), our estimated value at any time may not be comparable to estimated values of similar securities of other issuers.

Effect Of Interest Rate Used In Structuring The Securities.

The internal funding rate we use in structuring notes such as these securities is typically lower than the interest rate that is reflected in the yield on our conventional debt securities of similar maturity in the secondary market (our “secondary market credit spreads”). If on the pricing date our internal funding rate is lower than our secondary market credit spreads, we expect that the economic terms of the securities will generally be less favorable to you than they would have been if our secondary market credit spread had been used in structuring the securities. We will also use our internal funding rate to determine the price of the securities if we post a bid to repurchase your securities in secondary market transactions. See “The Estimated Value Of The Securities Is Not An Indication Of The Price, If Any, At Which Credit Suisse Or Any Other Person May Be Willing To Buy The Securities From You In The Secondary Market” below.

The Estimated Value Of The Securities Is Not An Indication Of The Price, If Any, At Which Credit Suisse Or Any Other Person May Be Willing To Buy The Securities From You In The Secondary Market.

If Credit Suisse (or any of its affiliates) or WFS (or any of its affiliates) bid for your securities in secondary market transactions, the secondary market price (and the value used for account statements or otherwise) may be higher or lower than the original offering price and the estimated value of the securities on the pricing date. Neither Credit Suisse (or any of its affiliates) nor WFS (or any of its affiliates) is obligated to make a secondary market. The estimated value of the securities on the cover of this pricing supplement does not represent a minimum price at which Credit Suisse or WFS would be willing to buy the securities in the secondary market (if any exists) at any time. The secondary market price of your securities at any time cannot be predicted and will reflect the then-current estimated value determined by reference to our pricing models, the related inputs and other factors, including our internal funding rate, customary bid and ask spreads and other transaction costs, changes in market conditions and deterioration or improvement in our creditworthiness. In circumstances where our internal funding rate is higher than our secondary market credit spreads, our secondary market bid for your securities could be less favorable than what other dealers might bid because, assuming all else equal, we use the higher internal funding rate to price the securities and other dealers might use the lower secondary market credit spread to price them. Furthermore, assuming no change in market conditions from the pricing date, the secondary market price of your securities will be lower than the original offering price because it will not include any discounts or commissions and hedging and other transaction costs. If you sell your securities to a dealer in a secondary market transaction, the dealer may impose an additional discount or commission, and as a result the price you receive on your securities may be lower than the price at which we may repurchase the securities from such dealer.

Credit Suisse (or any of its affiliates) or WFS (or any of its affiliates) may initially post a bid to repurchase the securities from you at a price that will exceed the then-current estimated value of the securities. That higher price reflects our projected profit and costs, which may include discounts and commissions that were included in the original offering price, and that higher price may also be initially used for account statements or otherwise. Credit Suisse (or any of its affiliates) or WFS (or any of its affiliates) may offer to pay this higher price, for your benefit, but the amount of any excess over the then-current estimated value will be temporary and is expected to decline over a period of approximately three months.

PRS-16

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

The securities are not designed to be short-term trading instruments and any sale prior to stated maturity could result in a substantial loss to you. You should be willing and able to hold your securities to stated maturity.

The Securities Will Not Be Listed On Any Securities Exchange And A Trading Market For The Securities May Not Develop.

The securities will not be listed on any securities exchange. Credit Suisse (or its affiliates) intends to offer to purchase the securities in the secondary market but is not required to do so. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the securities when you wish to do so. Because other dealers are not likely to make a secondary market for the securities, the price at which you may be able to trade your securities is likely to depend on the price, if any, at which Credit Suisse (or its affiliates) is willing to buy the securities. If you have to sell your securities prior to stated maturity, you may not be able to do so or you may have to sell them at a substantial loss.

PRS-17

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

| Supplemental Use of Proceeds and Hedging |

We intend to use the proceeds of this offering for our general corporate purposes, which may include the refinancing of existing debt outside Switzerland. Some or all of the proceeds we receive from the sale of the securities may be used in connection with hedging our obligations under the securities through one or more of our affiliates. Such hedging or trading activities on or prior to the pricing date and during the term of the securities (including on the calculation day) could adversely affect the price of the Fund and, as a result, could decrease the amount you may receive on the securities at stated maturity. For additional information, see “Supplemental Use of Proceeds and Hedging” in the accompanying product supplement.

PRS-18

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

| Hypothetical Returns |

The following table illustrates, for a maximum return of 33% or $330 per security and a range of hypothetical percentage changes from the starting price to the hypothetical ending price of the Fund:

| • | the hypothetical maturity payment amount payable per security; and |

| • | the hypothetical total rate of return. |

Hypothetical percentage change from the starting price to the hypothetical ending price | Hypothetical maturity payment amount payable per security | Hypothetical total rate of return |

| 75.00% | $1,330 | 33.00% |

| 50.00% | $1,330 | 33.00% |

| 40.00% | $1,330 | 33.00% |

| 30.00% | $1,330 | 33.00% |

| 20.00% | $1,330 | 33.00% |

| 16.50% | $1,330 | 33.00% |

| 10.00% | $1,200 | 20.00% |

| 5.00% | $1,100 | 10.00% |

| 0.00% | $1,000 | 0.00% |

| -5.00% | $1,000 | 0.00% |

| -10.00% | $1,000 | 0.00% |

| -17.50% | $1,000 | 0.00% |

| -18.50% | $990 | -1.00% |

| -20.00% | $975 | -2.50% |

| -30.00% | $875 | -12.50% |

| -40.00% | $775 | -22.50% |

| -50.00% | $675 | -32.50% |

| -75.00% | $425 | -57.50% |

| -100.00% | $175 | -82.50% |

The above figures are for purposes of illustration only and may have been rounded for ease of analysis. The actual amount you receive at stated maturity and the resulting rate of return will depend on the actual ending price.

PRS-19

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

| Hypothetical Maturity Payment Amounts |

Set forth below are four examples of maturity payment amount calculations, reflecting a maximum return of 33% or $330 per security and a hypothetical threshold price of $82.50. The terms used for purposes of these hypothetical examples do not represent the actual starting price or ending price. The hypothetical starting price of $100 has been chosen for illustrative purposes only and does not represent the actual starting price. The actual starting price is set forth under “Terms of the Securities” above. For historical data regarding the actual closing prices of the Fund, see the historical information set forth herein. These examples are for purposes of illustration only and the values used in the examples may have been rounded for ease of analysis.

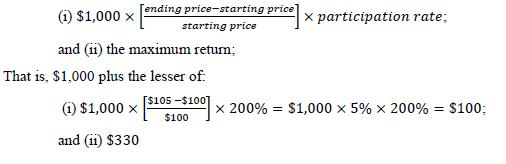

Example 1. The price of the Fund increases by 5% from the starting price to the ending price. The maturity payment amount is greater than the original offering price but less than the maximum return:

Hypothetical starting price: $100

Hypothetical ending price: $105

Since the hypothetical ending price is greater than the hypothetical starting price, the maturity payment amount would equal $1,000 plus the lesser of:

At stated maturity you would receive $1,100 per security.

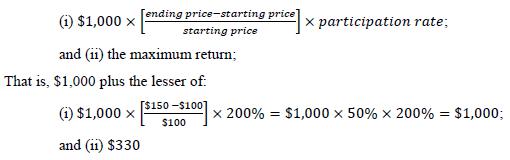

Example 2. The price of the Fund increases by 50% from the starting price to the ending price. The maturity payment is equal to the maximum return:

Hypothetical starting price: $100

Hypothetical ending price: $150

Since the hypothetical ending price is greater than the hypothetical starting price, the maturity payment amount would equal $1,000 plus the lesser of:

At stated maturity you would receive $1,330 per security.

In addition to limiting your return on the securities, the maximum return limits the positive effect of the participation rate. If the ending price is greater than the starting price, you will participate in the performance of the Fund at a rate of 200% up to a certain point. However, the effect of the participation rate will be progressively reduced for ending prices that are greater than 116.50% of the starting price (assuming a maximum return of 33% or $330 per security) since your return on the securities for any ending price greater than 116.50% of the starting

PRS-20

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

price will be limited to the maximum return. In this example, because your return on the securities is $1,330 per security and the price of the Fund increases by 50% from the starting price to the ending price, your effective participation rate is 66% (50% × 66% = 33% return per security over the original offering price).

Example 3. The price of the Fund decreases by 5% from the starting price to the ending price. The maturity payment amount is equal to the original offering price:

Hypothetical starting price: $100

Hypothetical ending price: $95

Hypothetical threshold price: $82.50, which is 82.50% of the hypothetical starting price

Since the hypothetical ending price is less than the hypothetical starting price, but not less than the hypothetical threshold price, you would not lose any of the original offering price of your securities.

At stated maturity you would receive $1,000 per security.

Example 4. The price of the Fund decreases by 60% from the starting price to the ending price. The maturity payment amount is less than the original offering price:

Hypothetical starting price: $100

Hypothetical ending price: $40

Hypothetical threshold price: $82.50, which is 82.50% of the hypothetical starting price

Since the hypothetical ending price is less than the hypothetical threshold price, you would lose a portion of the original offering price of your securities and receive the maturity payment amount equal to:

That is:

At stated maturity you would receive $575 per security.

To the extent that the starting price, ending price and threshold price differ from the values assumed above, the results indicated above would be different.

PRS-21

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

| Additional Terms of the Securities |

The securities are senior unsecured Medium-Term Notes issued by Credit Suisse. In the event the terms of the securities described in this pricing supplement differ from, or are inconsistent with, the terms described in any product supplement, prospectus supplement or prospectus, the terms described in this pricing supplement will control.

Certain Definitions

A “trading day” means a day, as determined by the calculation agent, on which the relevant stock exchange and each related futures or options exchange with respect to the Fund or other relevant security for which a closing price must be determined or any successor thereto, if applicable, are scheduled to be open for trading for their respective regular trading sessions.

The “relevant stock exchange” for the Fund means the primary exchange or quotation system on which shares (or other applicable securities) of the Fund are traded, as determined by the calculation agent.

The “related futures or options exchange” for the Fund means each exchange or quotation system where trading has a material effect (as determined by the calculation agent) on the overall market for futures or options contracts (or other applicable securities) relating to the Fund.

Calculation Agent

Credit Suisse International, one of our subsidiaries, will act as calculation agent for the securities and may appoint agents to assist it in the performance of its duties. Pursuant to a calculation agent agreement, we may appoint a different calculation agent without your consent and without notifying you.

The calculation agent will determine the maturity payment amount. In addition, the calculation agent will, among other things:

| • | determine whether a market disruption event has occurred; | ||

| • | determine the fund closing price of the Fund under certain circumstances; | ||

| • | determine if adjustments are required to the fund closing price of the Fund under various circumstances; and | ||

| • | if the Fund undergoes a liquidation event, select a successor fund (as defined below) or, if no successor fund is available, determine the fund closing price. |

All determinations made by the calculation agent will be at the sole discretion of the calculation agent and, in the absence of manifest error, will be conclusive for all purposes and binding on us and you. The calculation agent will have no liability for its determinations.

Market Disruption Events

A “market disruption event” means any of the following events as determined by the calculation agent in its sole discretion:

| (A) | The occurrence or existence of a material suspension of or limitation imposed on trading by the relevant stock exchange or otherwise relating to the shares (or other applicable securities) of the Fund or any successor fund on the relevant stock exchange at any time during the one-hour period that ends at the close of trading on such day, whether by reason of movements in price exceeding limits permitted by such relevant stock exchange or otherwise. | |

| (B) | The occurrence or existence of a material suspension of or limitation imposed on trading by any related futures or options exchange or otherwise in futures or options contracts relating to the shares (or other applicable securities) of the Fund or any successor fund on any related futures or options exchange at any time during the one-hour period that ends at the close of trading on that day, whether by reason of movements in price exceeding limits permitted by the related futures or options exchange or otherwise. | |

| (C) | The occurrence or existence of any event, other than an early closure, that materially disrupts or impairs the ability of market participants in general to effect transactions in, or obtain market values for, shares (or other applicable securities) of the Fund or any successor fund on the relevant stock exchange at any time during the one-hour period that ends at the close of trading on that day. | |

| (D) | The occurrence or existence of any event, other than an early closure, that materially disrupts or impairs the ability of market participants in general to effect transactions in, or obtain market values for, futures or options contracts relating to shares (or other applicable securities) of the Fund or any successor fund on any related futures or options exchange at any time during the one-hour period that ends at the close of trading on that day. | |

| (E) | The closure of the relevant stock exchange or any related futures or options exchange with respect to the Fund or any successor fund prior to its scheduled closing time unless the earlier closing time is announced by the relevant stock exchange or related futures or options exchange, as applicable, at least one hour prior to the earlier of (1) the actual closing time for the regular trading session on such relevant stock exchange or related futures or options exchange, as applicable, and (2) the submission deadline for orders to be entered into the relevant stock exchange or related futures or options exchange, as applicable, system for execution at the close of trading on that day. | |

PRS-22

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

| (F) | The relevant stock exchange or any related futures or options exchange with respect to the Fund or any successor fund fails to open for trading during its regular trading session.

|

For purposes of determining whether a market disruption event has occurred:

| (1) | “close of trading” means the scheduled closing time of the relevant stock exchange with respect to the Fund or any successor fund; and | |

| (2) | the “scheduled closing time” of the relevant stock exchange or any related futures or options exchange on any trading day for the Fund or any successor fund means the scheduled weekday closing time of such relevant stock exchange or related futures or options exchange on such trading day, without regard to after hours or any other trading outside the regular trading session hours. | |

If a market disruption event occurs or is continuing on the calculation day, then the calculation day will be postponed to the first succeeding trading day on which a market disruption event has not occurred and is not continuing; however, if such first succeeding trading day has not occurred as of the eighth trading day after the originally scheduled calculation day, that eighth trading day shall be deemed to be the calculation day. If the calculation day has been postponed eight trading days after the originally scheduled calculation day and a market disruption event occurs or is continuing with respect to the Fund on such eighth trading day, the calculation agent will determine the fund closing price of the Fund on such eighth trading day based on its good faith estimate of the value of the shares (or other applicable securities) of the Fund as of the close of trading on such eighth trading day.

Anti-dilution Adjustments Relating to the Fund; Alternate Calculation

Anti-dilution Adjustments

The calculation agent will adjust the adjustment factor as specified below if any of the events specified below occurs with respect to the Fund and the effective date or ex-dividend date, as applicable, for such event is after the pricing date and on or prior to the calculation day.

The adjustments specified below do not cover all events that could affect the Fund, and there may be other events that could affect the Fund for which the calculation agent will not make any such adjustments, including, without limitation, an ordinary cash dividend. Nevertheless, the calculation agent may, in its sole discretion, make additional adjustments to any terms of the securities upon the occurrence of other events that affect or could potentially affect the market price of, or shareholder rights in, the Fund, with a view to offsetting, to the extent practical, any such change, and preserving the relative investment risks of the securities. In addition, the calculation agent may, in its sole discretion, make adjustments or a series of adjustments that differ from those described herein if the calculation agent determines that such adjustments do not properly reflect the economic consequences of the events specified in this pricing supplement or would not preserve the relative investment risks of the securities. All determinations made by the calculation agent in making any adjustments to the terms of the securities, including adjustments that are in addition to, or that differ from, those described in this pricing supplement, will be made in good faith and a commercially reasonable manner, with the aim of ensuring an equitable result. In determining whether to make any adjustment to the terms of the securities, the calculation agent may consider any adjustment made by the Options Clearing Corporation or any other equity derivatives clearing organization on options contracts on the Fund.

For any event described below, the calculation agent will not be required to adjust the adjustment factor unless the adjustment would result in a change to the adjustment factor then in effect of at least 0.10%. The adjustment factor resulting from any adjustment will be rounded up or down, as appropriate, to the nearest one-hundred thousandth.

| (A) | Stock Splits and Reverse Stock Splits |

If a stock split or reverse stock split has occurred, then once such split has become effective, the adjustment factor will be adjusted to equal the product of the prior adjustment factor and the number of securities which a holder of one share (or other applicable security) of the Fund before the effective date of such stock split or reverse stock split would have owned or been entitled to receive immediately following the applicable effective date.

| (B) | Stock Dividends |

If a dividend or distribution of shares (or other applicable securities) to which the securities are linked has been made by the Fund ratably to all holders of record of such shares (or other applicable security), then the adjustment factor will be adjusted on the ex-dividend date to equal the prior adjustment factor plus the product of the prior adjustment factor and the number of shares (or other applicable security) of the Fund which a holder of one share (or other applicable security) of the Fund before the ex-dividend date would have owned or been entitled to receive immediately following that date; provided, however, that no adjustment will be made for a distribution for which the number of securities of the Fund paid or distributed is based on a fixed cash equivalent value.

| (C) | Extraordinary Dividends |

If an extraordinary dividend (as defined below) has occurred, then the adjustment factor will be adjusted on the ex-dividend date to equal the product of the prior adjustment factor and a fraction, the numerator of which is the closing price per share (or other applicable security) of the

PRS-23

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the iShares® Global Clean Energy ETF due October 6, 2023

Fund on the trading day preceding the ex-dividend date, and the denominator of which is the amount by which the closing price per share (or other applicable security) of the Fund on the trading day preceding the ex-dividend date exceeds the extraordinary dividend amount (as defined below).

For purposes of determining whether an extraordinary dividend has occurred:

| (1) | “extraordinary dividend” means any cash dividend or distribution (or portion thereof) that the calculation agent determines, in its sole discretion, is extraordinary or special; and | |

| (2) | “extraordinary dividend amount” with respect to an extraordinary dividend for the securities of the Fund will equal the amount per share (or other applicable security) of the Fund of the applicable cash dividend or distribution that is attributable to the extraordinary dividend, as determined by the calculation agent in its sole discretion. | |

A distribution on the securities of the Fund described below under the section entitled “—Reorganization Events” below that also constitutes an extraordinary dividend will only cause an adjustment pursuant to that “—Reorganization Events” section.

| (D) | Other Distributions |

If the Fund declares or makes a distribution to all holders of the shares (or other applicable security) of the Fund of any non-cash assets, excluding dividends or distributions described under the section entitled “—Stock Dividends” above, then the calculation agent may, in its sole discretion, make such adjustment (if any) to the adjustment factor as it deems appropriate in the circumstances. If the calculation agent determines to make an adjustment pursuant to this paragraph, it will do so with a view to offsetting, to the extent practical, any change in the economic position of a holder of the securities that results solely from the applicable event.

| (E) | Reorganization Events |