UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 6-K

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

July 24, 2008

Commission File Number 001-15244

CREDIT SUISSE GROUP AG

(Translation of registrant’s name into English)

Paradeplatz 8, P.O. Box 1, CH-8070 Zurich, Switzerland

(Address of principal executive office)

Commission File Number 001-33434

CREDIT SUISSE

(Translation of registrant’s name into English)

Paradeplatz 8, P.O. Box 1, CH-8070 Zurich, Switzerland

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F | Form 40-F |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Note: Regulation S-T Rule 101(b)(1) only permits the submission in paper of a Form 6-K if submitted solely to provide an attached annual report to security holders.

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Note: Regulation S-T Rule 101(b)(7) only permits the submission in paper of a Form 6-K if submitted to furnish a report or other document that the registrant foreign private issuer must furnish and make public under the laws of the jurisdiction in which the registrant is incorporated, domiciled or legally organized (the registrant’s “home country”), or under the rules of the home country exchange on which the registrant’s securities are traded, as long as the report or other document is not a press release, is not required to be and has not been distributed to the registrant’s security holders, and, if discussing a material event, has already been the subject of a Form 6-K submission or other Commission filing on EDGAR.

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes | No |

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): 82-.

| CREDIT SUISSE GROUP AG | |

Paradeplatz 8 P.O. Box CH-8070 Zurich Switzerland | Telephone +41 844 33 88 44 Fax +41 44 333 88 77 media.relations@credit-suisse.com

| |

Media Release

Credit Suisse Group reports net income of CHF 1.2 billion in the second quarter of 2008

All three divisions profitable; diluted earnings per share of CHF 1.12

Strong asset inflows in Private Banking: net new assets totaled CHF 17.4 billion

Solid operating performance in Investment Banking; net writedowns were immaterial at CHF 22 million

Continued significant reduction in risk exposures during 2Q08: risk exposures declined 31% in leveraged finance and 22% in commercial mortgages from the end of 1Q08, and 76% and 58% from the end of 3Q07, respectively

Strong BIS tier 1 ratio under Basel II of 10.2% as of June 30, 2008

Zurich, July 24, 2008 Credit Suisse Group reported net income of CHF 1,215 million in the second quarter of 2008, compared with net income of CHF 3,189 million in the second quarter of 2007. Core net revenues were CHF 7,830 million, up 159% from the first quarter of 2008 but down 33% from the second quarter of 2007. Diluted earnings per share in the second quarter of 2008 were CHF 1.12 compared with CHF 2.82 in the same period a year earlier.

Brady W. Dougan, Chief Executive Officer, said: “We are pleased with our second-quarter results, which reflect the resilience and earnings power of our integrated business model and our continued focus on risk and cost management. During the second quarter we saw strong momentum in our Wealth Management business and a solid operating performance in Investment Banking. We continued to reduce our risk positions, as we have done since the early stages of the credit crisis. At a time when the industry is undergoing fundamental change, our strength in the right mix of businesses provides us with excellent prospects to grow market share.”

He added: “Our conservative funding structure and our position as one of the world’s best capitalized banks remain competitive advantages. The quarter’s strong net new assets in Private Banking and other client flows across our franchise underscore the trust that clients are placing in Credit Suisse. We anticipate that the current challenging market conditions will persist over the near to medium term and we will continue to manage our business conservatively.”

| Media Release |

July 24, 2008 Page 2/6

|

Financial Highlights |

|

|

|

|

|

in CHF million | 2Q08 | 1Q08 | 2Q07 | Change in % | Change in % |

|

|

|

| vs 1Q08 | vs 2Q07 |

Net income/(loss) | 1,215 | (2,148) | 3,189 | - | (62) |

Diluted earnings per share (CHF) | 1.12 | (2.10) | 2.82 | - | (60) |

Return on equity | 13.2% | (20.8)% | 29.7% | - | - |

Basel II BIS tier 1 ratio (end of period) 1) | 10.2% | 9.8% | - | - | - |

Core results 2) |

|

|

|

|

|

Net revenues | 7,830 | 3,019 | 11,703 | 159 | (33) |

Provision for credit losses | 45 | 151 | (20) | (70) | - |

Total operating expenses | 6,214 | 5,440 | 7,637 | 14 | (19) |

Income/(loss) before taxes | 1,571 | (2,572) | 4,086 | - | (62) |

1) Under Basel II from January 1, 2008. Prior periods are reported under Basel I and are therefore not comparable. | |||||

2) Core results include the results of the three segments and the Corporate Center, excluding revenues and | |||||

expenses in respect of minority interests in which we do not have a significant economic interest. | |||||

Segment Results

Private Banking

Private Banking, which comprises the Wealth Management and Corporate & Retail Banking businesses, reported income before taxes of CHF 1,220 million in the second quarter of 2008, a decrease of 12% from the second quarter of 2007.

The Wealth Management business reported income before taxes of CHF 830 million in the second quarter of 2008, down 17% from the strong second quarter of 2007. Net revenues declined 4%, as an improvement in recurring revenues was more than offset by a decrease in transaction-based revenues. Total operating expenses rose 5%, primarily due to the ongoing strategic investment in expanding the global franchise. As part of that effort, Credit Suisse hired 120 relationship managers globally during the quarter, further strengthening its professional team. The pre-tax income margin was 36.4% in the second quarter of 2008 compared with 42.0% in the same period a year earlier.

The Corporate & Retail Banking business reported income before taxes of CHF 390 million in the second quarter of 2008, up 3% from the second quarter of 2007. Net revenues rose 2% from the same period a year earlier. Net releases of provision for credit losses were CHF 5 million compared with net releases of CHF 28 million in the second quarter of 2007, which benefited from the resolution of a single exposure. Total operating expenses were 2% lower than in the second quarter of 2007, as an increase in compensation and benefits was more than offset by lower general and administrative expenses and commission expenses. The pre-tax income margin was 39.5% in the second quarter of 2008 compared with 39.2% in the second quarter of 2007.

Investment Banking

Investment Banking returned to profitability in the second quarter of 2008, reporting income before taxes of CHF 281 million, compared with the record CHF 2,502 million in the second quarter of 2007. Net revenues declined 50% from the second quarter of 2007, but rose substantially from the previous quarter. Despite the challenging market conditions, many businesses reported solid results. The year-on-year decline in revenues was due in large part to an industry-wide decline in origination activity, particularly in the structured products and leveraged finance businesses, compared with exceptionally high levels in the

| Media Release |

July 24, 2008 Page 3/6

|

second quarter of 2007. Net revenues in the second quarter of 2008 also reflected combined net writedowns of CHF 22 million in the leveraged finance and structured products businesses and a fair value loss of CHF 503 million on Credit Suisse debt due to narrower credit spreads.

Fixed income trading revenues were significantly lower in the second quarter of 2008 compared with the same period a year earlier, reflecting the above-mentioned net writedowns and lower levels of origination activity. Revenues from the global rates business also declined significantly. These declines were partly offset by increases in the residential mortgage-backed securities and European high grade businesses. Equity trading revenues decreased from the second quarter of 2007, primarily due to lower revenues in the equity proprietary trading and convertibles businesses than in the strong year-ago period. The decline was partially offset by a near-record performance in prime services and a strong performance in cash equities. Equity derivatives also posted solid results. Fixed income and equity trading were impacted by the fair value loss on Credit Suisse debt compared with significant gains in the first quarter of 2008. The underwriting and advisory businesses had lower revenues compared with the second quarter of 2007, in line with an industry-wide decline in market activity. Total operating expenses declined 32%, due primarily to a decrease in compensation and benefits, reflecting lower performance-related compensation on lower revenues.

Net valuation adjustments and exposures in Investment Banking

In the second quarter of 2008, combined net writedowns in the leveraged finance and structured products businesses were immaterial at CHF 22 million and exposures were significantly reduced compared with the previous quarters.

Net valuation adjustments |

| ||

in CHF million | 2Q08 | 1Q08 | 4Q07 |

Leveraged finance | (86) | (1’681) | (231) |

Commercial mortgage-backed securities (CMBS) | (477) | (848) | (384) |

Residential mortgage-backed securities (RMBS) | 33 | (96) | (480) |

Collateralized debt obligations (CDO) | 508 | (2’656) | (1’341) |

Total | (22) | (5’281) | (2’436) |

Risk exposures |

|

|

| ||

in CHF billion | End of | End of | End of | Change in % | Change in % |

| 2Q08 | 1Q08 | 4Q07 | vs. 1Q08 | vs. 4Q07 |

Leveraged finance | 14.3 | 20.8 | 35.1 | (31) | (59) |

Commercial mortgages | 15.0 | 19.3 | 25.9 | (22) | (42) |

Residential mortgages | 5.4 | 5.5 | 8.7 | (2) | (38) |

CDO US subprime | 1.1 | 1.9 | 4.6 | (42) | (76) |

Asset Management

Asset Management returned to profitability in the second quarter of 2008, reporting income before taxes of CHF 167 million, compared with income before taxes of CHF 299 million in the second quarter of 2007. Income before taxes declined as a valuation gain of CHF 79 million on securities purchased from Credit Suisse’s money market funds and semi-annual performance-based fees were more than offset by lower private equity and other investment-related gains and lower asset management and administrative revenues, reflecting a decline in average assets under management and higher funding costs. Compared with the second quarter of 2007, net revenues were down 13%, or 8% before the impact of the

| Media Release |

July 24, 2008 Page 4/6

|

securities purchased from Credit Suisse’s money market funds and private equity and other investment-related gains. Total operating expenses rose 3% from the second quarter of 2007, reflecting higher compensation and benefits and general and administrative expenses. In the second quarter of 2008, the pre-tax income margin was 22.6% compared with 35.1% in the second quarter of 2007, and was 13.3% before the impact of the securities purchased from Credit Suisse’s money market funds. The fair value of Credit Suisse’s balance sheet exposure from the purchased securities was CHF 1.5 billion at the end of the second quarter of 2008, down CHF 724 million from the first quarter of 2008.

Segment Results |

|

|

|

|

| |

in CHF million |

| 2Q08 | 1Q08 | 2Q07 | Change in % | Change in % |

|

|

|

|

| vs. 1Q08 | vs. 2Q07 |

Private | Net revenues | 3,265 | 3,355 | 3,353 | (3) | (3) |

Banking | Provision for credit losses | (5) | (5) | (29) | 0 | (83) |

| Total operating expenses | 2,050 | 2,036 | 2,001 | 1 | 2 |

| Income before taxes | 1,220 | 1,324 | 1,381 | (8) | (12) |

Investment | Net revenues | 3,740 | (489) | 7,538 | - | (50) |

Banking | Provision for credit losses | 50 | 156 | 9 | (68) | 456 |

| Total operating expenses | 3,409 | 2,815 | 5,027 | 21 | (32) |

| Income/(loss) before taxes | 281 | (3,460) | 2,502 | - | (89) |

Asset | Net revenues | 739 | 63 | 853 | - | (13) |

Management | Provision for credit losses | 0 | 0 | 0 | - | - |

| Total operating expenses | 572 | 531 | 554 | 8 | 3 |

| Income/(loss) before taxes | 167 | (468) | 299 | - | (44) |

Net New Assets

Private Banking recorded net new assets of CHF 17.4 billion in the second quarter of 2008, including net new assets of CHF 15.4 billion in the Wealth Management business, which represented a rolling four-quarter average growth rate of 5.9%. This result reflected good contributions from all regions, especially Europe, Middle East and Africa (EMEA) and Asia Pacific. Asset Management reported net new asset outflows of CHF 3.8 billion in the second quarter of 2008. The Group’s total assets under management were CHF 1,411.9 billion as of June 30, 2008, down 13.3% from June 30, 2007, primarily reflecting adverse foreign exchange-related and market movements.

Benefits of the integrated bank

In the second quarter of 2008, Credit Suisse generated CHF 1.3 billion in revenues from cross-divisional activities, bringing the 2008 year-to-date total to CHF 2.5 billion.

Strong capitalization

Credit Suisse Group’s capitalization remained strong, with a BIS tier 1 ratio of 10.2% under Basel II as of June 30, 2008. To achieve this, no dilutive equity capital was raised and the Group accrued a significant dividend during the quarter.

Information

Media Relations Credit Suisse, telephone +41 844 33 88 44, media.relations@credit-suisse.com

Investor Relations Credit Suisse, telephone +41 44 333 71 49, investor.relations@credit-suisse.com

| Media Release |

July 24, 2008 Page 5/6

|

Credit Suisse

As one of the world’s leading banks, Credit Suisse provides its clients with private banking, investment banking and asset management services worldwide. Credit Suisse offers advisory services, comprehensive solutions and innovative products to companies, institutional clients and high-net-worth private clients globally, as well as retail clients in Switzerland. Credit Suisse is active in over 50 countries and employs approximately 49,000 people. Credit Suisse is comprised of a number of legal entities around the world and is headquartered in Zurich. The registered shares (CSGN) of Credit Suisse’s parent company, Credit Suisse Group AG, are listed in Switzerland and, in the form of American Depositary Shares (CS), in New York. Further information about Credit Suisse can be found at www.credit-suisse.com.

Cautionary statement regarding forward-looking information and non-GAAP information

This press release contains statements that constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act. In addition, in the future we, and others on our behalf, may make statements that constitute forward-looking statements. Such forward-looking statements may include, without limitation, statements relating to the following:

• | our plans, objectives or goals; |

• | our future economic performance or prospects; |

• | the potential effect on our future performance of certain contingencies; and |

• | assumptions underlying any such statements. |

Words such as “believes,” “anticipates,” “expects,” “intends” and “plans” and similar expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements. We do not intend to update these forward-looking statements except as may be required by applicable securities laws. By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that predictions, forecasts, projections and other outcomes described or implied in forward-looking statements will not be achieved. We caution you that a number of important factors could cause results to differ materially from the plans, objectives, expectations, estimates and intentions expressed in such forward-looking statements. These factors include:

• | the ability to maintain sufficient liquidity and access capital markets; |

• | market and interest rate fluctuations; |

• | the strength of the global economy in general and the strength of the economies of the countries in which we conduct our operations, in particular the risk of a continued US or global economic downturn in 2008 and beyond; |

• | the direct and indirect impacts of continuing deterioration of subprime and other real estate markets; |

• | further adverse rating actions by credit rating agencies in respect of structured credit products or other credit-related exposures or of monoline insurers; |

• | the ability of counterparties to meet their obligations to us; |

• | the effects of, and changes in, fiscal, monetary, trade and tax policies, and currency fluctuations; |

• | political and social developments, including war, civil unrest or terrorist activity; |

• | the possibility of foreign exchange controls, expropriation, nationalization or confiscation of assets in countries in which we conduct our operations; |

• | operational factors such as systems failure, human error, or the failure to implement procedures properly; |

• | actions taken by regulators with respect to our business and practices in one or more of the countries in which we conduct our operations; |

• | the effects of changes in laws, regulations or accounting policies or practices; |

• | competition in geographic and business areas in which we conduct our operations; |

• | the ability to retain and recruit qualified personnel; |

• | the ability to maintain our reputation and promote our brand; |

• | the ability to increase market share and control expenses; |

• | technological changes; |

• | the timely development and acceptance of our new products and services and the perceived overall value of these products and services by users; |

• | acquisitions, including the ability to integrate acquired businesses successfully, and divestitures, including the ability to sell non-core assets; |

• | the adverse resolution of litigation and other contingencies; and |

• | our success at managing the risks involved in the foregoing. |

We caution you that the foregoing list of important factors is not exclusive. When evaluating forward-looking statements, you should carefully consider the foregoing factors and other uncertainties and events, as well as the information set forth in our Form 20-F Item 3 – Key Information – Risk Factors.

This press release contains non-GAAP financial information. Information needed to reconcile such non-GAAP financial information to the most directly comparable measures under GAAP can be found in the Credit Suisse Financial Report 2Q08.

| Media Release |

July 24, 2008 Page 6/6

|

Presentation of second-quarter 2008 results

Media conference

§ | Thursday, July 24, 2008 |

08:45 CEST / 07:45 GMT / 02:45 EST

Credit Suisse Forum St. Peter, Auditorium, St. Peterstrasse 19, Zurich

§ | Speakers |

Brady W. Dougan, Chief Executive Officer of Credit Suisse

Renato Fassbind, Chief Financial Officer of Credit Suisse

The presentations will be held in English.

Simultaneous interpreting: English – German, German – English

§ | Internet |

Live broadcast at: www.credit-suisse.com/results

Video playback available approximately 3 hours after the event

§ | Telephone |

Live audio dial-in on +41 44 580 40 01 (Switzerland), +44 1452 565 510 (Europe) and

+1 866 389 9771 (US); ask for “Credit Suisse Group quarterly results”.

Please dial in 10-15 minutes before the start of the presentation.

Telephone replay available approximately 1 hour after the event on +41 41 580 00 07 (Switzerland),

+44 1452 55 0000 (Europe) and +1 866 247 4222 (US); conference ID English - 50637155#, conference ID German – 50648562#.

Analyst conference

§ | Thursday, July 24, 2008 |

10:00 CEST / 09:00 GMT / 04:00 EST

Credit Suisse Forum St. Peter, Auditorium, St. Peterstrasse 19, Zurich

§ | Speakers |

Brady W. Dougan, Chief Executive Officer of Credit Suisse

Renato Fassbind, Chief Financial Officer of Credit Suisse

D. Wilson Ervin, Chief Risk Officer of Credit Suisse

The presentations will be held in English.

Simultaneous interpreting: English – German, German – English

§ | Internet |

Live broadcast at: www.credit-suisse.com/results

Video playback available approximately 3 hours after the event

§ | Telephone |

Live audio dial-in on +41 44 580 40 01 (Switzerland), +44 1452 565 510 (Europe) and

+1 866 389 9771 (US); ask for “Credit Suisse Group quarterly results”.

Please dial in 10-15 minutes before the start of the presentation.

Telephone replay available approximately 1 hour after the event on +41 41 580 00 07 (Switzerland),

+44 1452 55 0000 (Europe) and +1 866 247 4222 (US); conference ID English – 50637913#, conference ID German – 50624619#.

Second Quarter Results 2008

Zurich

July 24, 2008

Cautionary statement

Cautionary statement regarding forward-looking and non-GAAP information

This presentation contains forward-looking statements within the meaning of the Private

Securities Litigation Reform Act of 1995. Forward-looking statements involve inherent risks

and uncertainties, and we might not be able to achieve the predictions, forecasts,

projections and other outcomes we describe or imply in forward-looking statements.

A number of important factors could cause results to differ materially from the plans,

objectives, expectations, estimates and intentions we express in these forward-looking

statements, including those we identify in "Risk Factors" in our Annual Report on Form 20-

F for the fiscal year ended December 31, 2007 filed with the US Securities and Exchange

Commission, and in other public filings and press releases. We do not intend to update

these forward-looking statements except as may be required by applicable laws.

This presentation contains non-GAAP financial information. Information needed to reconcile

such non-GAAP financial information to the most directly comparable measures under

GAAP can be found in Credit Suisse Group's second quarter report 2008.

Second quarter 2008 results

Renato Fassbind, Chief Financial Officer

Risk management update

Wilson Ervin, Chief Risk Officer

Introduction

Brady W. Dougan, Chief Executive Officer

Summary

Brady W. Dougan, Chief Executive Officer

Key messages

Solid results with net income of CHF 1.2 bn; all three divisions profitable

Private Banking performed well with strong asset inflows of CHF 17.4 bn

Continued significant reduction in risk exposures

Solid operating performance in Investment Banking with

immaterial writedowns

Strong BIS tier 1 ratio of 10.2%

Second quarter 2008 results

Renato Fassbind, Chief Financial Officer

Risk management update

Wilson Ervin, Chief Risk Officer

Introduction

Brady W. Dougan, Chief Executive Officer

Summary

Brady W. Dougan, Chief Executive Officer

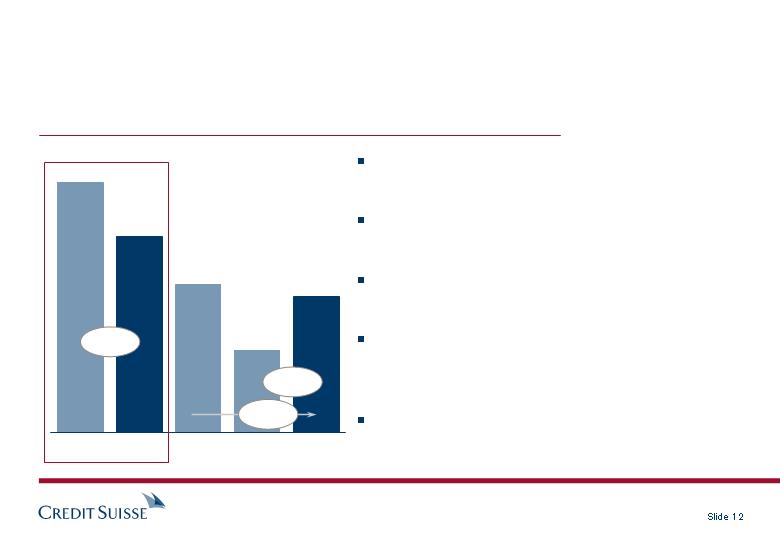

All divisions profitable

Asset Management

Pre-tax income in CHF m

Investment Banking

Private Banking

2,502

(3,460)

281

299

(468)

167

1,381

1,324

1,220

2Q07

1Q08

2Q08

Stable fee-based gross

margin

Strong inflows in alternative

investments

Reduced 'liftout' assets

1) Excluding a fair value adjustment on own debt of CHF (503) m and a net litigation credit of CHF 134 m

1)

Good results evidencing the

strength of business

Strong asset gathering and

hiring trends across all

regions

Continue to implement

international growth strategy

2Q08 operating earnings

of CHF 650 m

Most areas with good results

Immaterial net valuation

reductions of CHF 22 m

Significant progress in

reducing risk exposure

Results overview – solid profitability

2Q07

1Q08

2Q08

CHF bn, except where indicated

Note: Based on Core Results, i.e. excluding results from minority interests without significant interest

1) Under Basel I and as such not comparable

1)

Net revenues

7.8

3.0

11.7

Provisions for credit losses

0.0

0.2

0.0

Total operating expenses

6.2

5.4

7.6

Pre-tax income

1.6

(2.6)

4.1

Net income

1.2

(2.1)

3.2

Diluted earnings per share (in CHF)

1.12

(2.10)

2.82

Return on equity (in %)

13.2%

(20.8)%

29.7%

Basel II Tier 1 ratio (in %)

10.2 %

9.8%

13.0%

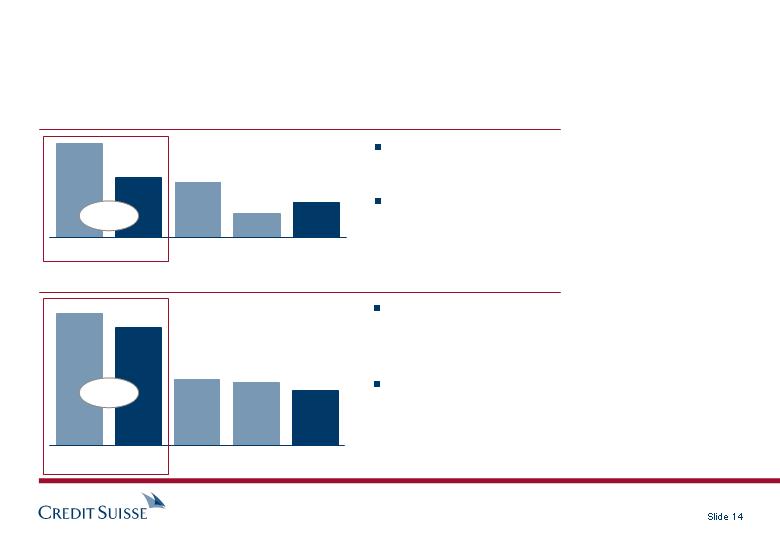

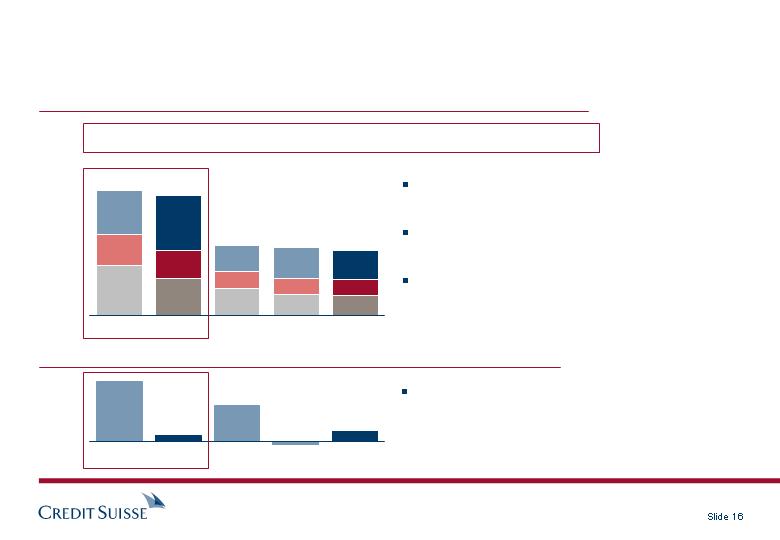

Wealth Management maintains strong gross margins

Net revenues

CHF m

4,763

4,591

2,384

2,313

2,278

6M07

6M08

2Q07

1Q08

2Q08

Gross margin on assets under management

116

117

113

117

116

6M07

6M08

2Q07

1Q08

2Q08

39

31

38

32

30

77

86

75

85

86

basis points (bp)

+7%

(27%)

+7%

(24%)

(4%)

(4%)

Transaction-based

Recurring

Transaction-based

Recurring

Strong net new asset growth in Wealth Management

Net new assets (NNA)

CHF bn

6M08

28.9

EMEA

Asia Pacific

Americas

Switzerland

7.8

6.6

5.7

8.8

1Q08

2Q07

3Q07

4Q07

2Q08

13.5

15.2

9.7

12.0

15.4

5.9%

rolling 4 qtr

NNA growth

rate

8.2%

annualized 2Q08

NNA growth

rate

13.3

1Q07

5.7

4.1

2.1

3.5

2,540

3,140

4,100

3,370

Wealth Management with continued investments in international

growth platform

Relationship managers (RMs)

2004

2007

6M08

at period-end

+200 p.a.

+230 in

6M08

Goal 2010

+330 p.a.

goal

450 new RMs in last 12 months

Entered 4 new local markets and opened 14

new offices globally (since 2007)

Approximately 40% of current net new assets

from hires made over last three years

Investments into international growth of above

CHF 350 m annually

Continued efficiency measures elsewhere, but

dilution of profitability ratios in downturn

markets should be expected as we maintain

long-term focus

120 new

RMs in 2Q08

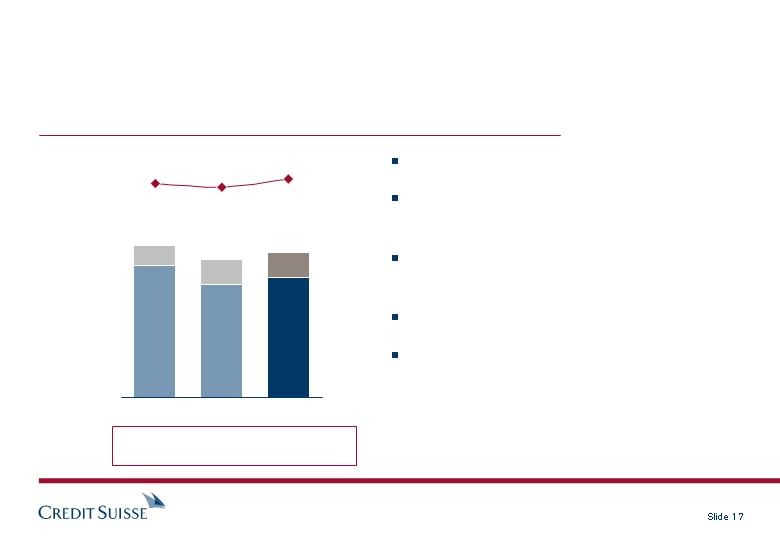

Fixed income trading with reduced writedowns, but market

conditions remain difficult

Investment Banking fixed income trading net revenues

CHF m

6M07

6M08

2Q07

1Q08

2Q08

6,054

3,282

(1,576)

320

(1,256)

Increased revenues in RMBS, Europe high

grade and life finance

2Q08 revenues benefit from substantial

reductions in writedowns

Reported revenues of CHF 320 m include

writedowns of CHF 391 m 1) and a fair

value reduction on own debt of CHF 453 m

1) Does not include offsetting gains of CHF 369 m reported in debt underwriting and other revenues

Equity trading with strong performance in most businesses

Investment Banking equity trading net revenues

CHF m

Prime services generated near-record revenues

with growing client balances and new mandates

Near-record revenues in equity derivatives,

driven by strength in all regions and products

Strong result in the global cash business, driven

by increased client flows and growth in AES

Proprietary trading gains in 2Q08 were lower

than in 2Q07 but an improvement from the loss

in 1Q08

2Q08 fair value reduction on own debt

of CHF 50 m

6M07

6M08

2Q07

1Q08

2Q08

4,646

2,475

1,379

2,255

3,634

(9)%

(22)%

+64%

AES = Advanced Execution Services, our electronic trading platform

Underwriting fees still adversely affected by market conditions

Underwriting fees

CHF m

6M07

6M08

2Q07

1Q08

2Q08

1,438

713

136

216

352

Advisory and other fees

CHF m

6M07

6M08

2Q07

1Q08

2Q08

1,143

632

396

364

760

724

417

413

172

245

Debt underwriting

Equity underwriting

Disciplined cost management in Investment Banking

Compensation expenses in CHF m

Other operating expenses in CHF m

6M07

6M08

2Q07

1Q08

2Q08

Increased compensation from 1Q08 reflecting

improved results

Hires in prime services and equity derivatives

partly offset headcount reductions in fixed

income and banking

6M07

6M08

2Q07

1Q08

2Q08

2,286

2,044

1,145

1,097

947

7,272

4,180

1,718

2,462

3,882

Other operating expenses1) decreased CHF

108 m, or 5%, from 6M07, CHF 16 m from

1Q08 and CHF 64 m from 2Q07

This reflects higher average headcount

compared to 6M07, offset by cost reduction

efforts, a stronger Swiss franc and, in 2Q08,

lower commission spend

1) Excluding net litigation credit of CHF 134 m in 2Q08

(11)%

(43)%

Asset Management with good inflows in higher margin

businesses

Assets under management

CHF bn

Asset

Management

Division

Multi-asset

class solutions

(MACS)

Global

investors (GI)

Alternative

investment

strategies (AI)

Net new assets

7.5

(9.3)

(3.8)

Gross margin by asset class

Before gains/losses from money market funds and

private equity in 2Q08

(2.0)

CHF bn in 2Q08

605

273

164

168

1) Including CHF 10.0 bn outflows from institutional pension advisory business

1)

1)

40

26

36

64

Improved gross margin from last year

Private equity and other investment-related gains

CHF m

Asset management and administrative fees

CHF m

6M07

6M08

2Q07

1Q08

2Q08

MACS and GI with decline in fees due to lower

assets under management

AI with higher performance fees, offset in part

by higher funding costs

Gross margin on AuM maintained at 40 bp

Gains from energy-related companies

6M07

6M08

2Q07

1Q08

2Q08

1,312

1,258

664

648

AI

MACS

GI

1) before private equity and other investment-related gains and securities

purchased from our money market funds

610

317

31

(19)

50

189

1)

1)

37

40

36

40

40

Gross margin on AuM in bp

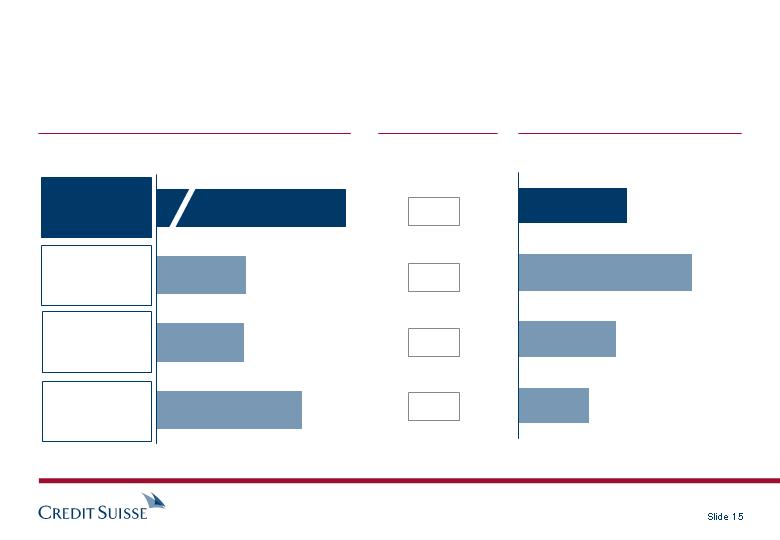

Maintained strong Basel II capital position

4Q07

1Q08

2Q08

Strong tier 1 capital ratio at 10.2%

High quality composition, with 85% from

core capital

Maintained capital strength without raising

dilutive equity capital

Includes accrual for significant dividend

Strong capital base and conservative

funding as competitive advantage

Tier 1 capital and tier 1 capital ratio (CHF bn and %)

32.2

29.4

30.8

Core tier 1

capital

Hybrid tier 1

capital

10.0%

9.8%

10.2%

Tier 1

capital ratio

Risk-weighted assets in CHF bn

324

301

302

2nd quarter 2008 results

Renato Fassbind, Chief Financial Officer

Risk management update

Wilson Ervin, Chief Risk Officer

Introduction

Brady W. Dougan, Chief Executive Officer

Summary

Brady W. Dougan, Chief Executive Officer

Investment Banking: Overview of key sectors

Business area (in CHF bn)

Change

Exposures

1) All non-agency business, including higher quality Residential Mortgage segments (Alt-A and prime); global total

2) Positions relate to US subprime; long positions are CHF 5.2 bn and short positions of CHF 4.1bn; total net subprime exposure in IB is CHF 1.9 bn in residential mortgages

and CDO trading. See CDO supplemental page for details on exposure methodology refinement

3) Index hedges held in the above focus areas that reference non-investment grade, crossover credit and mortgage indices only; excludes other indices (e.g. investment grade)

and single name hedges; trading hedges embedded in US subprime residential mortgages & CDO trading are included in the net exposures shown above and not included in the

total for Index hedges

2Q08

Origination-

based

(exposures

shown gross)

Trading-

based

(exposures

shown net)

1Q08

Net (writedowns)/

writebacks

2Q08

1Q08

1)

2)

3)

Leveraged finance

14.3

20.8

(31%)

(0.1)

(1.7)

Commercial mortgages

15.0

19.3

(22%)

(0.5)

(0.8)

Residential mortgage

5.4

5.5

(2%)

+0.0

(0.1)

of which US subprime

0.8

1.1

(27%)

CDO Trading

1.1

1.9

(42%)

+0.5

(2.7)

Total

(0.0)

(5.3)

Index hedges

(6.6)

(20.9)

59.2

35.1

14.3

20.8

Leveraged finance

All positions are fair valued (no “accrual”

book); weighted price below 80% of par

Portfolio has become more concentrated as

sales effort has progressed

High proportion (76%) of exposure is

senior secured lending; no exposure to

auto, home building or retail industries

Term financing used only in a small

proportion of sales (total of CHF 2.8 bn)

Added CHF 1.1 bn of new exposures in

2Q08; remain active in pursuing and

executing quality business

3Q07

4Q07

1Q08

2Q08

(76)%

Total exposure

CHF m

35.9

25.9

15.0

19.3

Commercial mortgage (CMBS)

All positions carried at fair value

Portfolio breakdown similar to 1Q08 with

average loan-to-value (LTV) of 70%

Majority of portfolio is secured by high quality,

income-producing real estate; office properties

as largest segment

Development loans are less than 5% of our

portfolio with an average LTV of 54%

Continental Europe 50% of the portfolio;

exposures primarily in Northern Europe,

particularly Germany

1) Includes both loans in the warehouse as well as securities still in syndication

3Q07

4Q07

1Q08

2Q08

(58)%

Total exposure

CHF m

1)

CDO trading

1) Positions related to US subprime, and includes refinement to methodology (see supplement)

Net gain in 2Q08 mainly reflects

i) ongoing trading (i.e. excludes run-off book)

performed well despite volatile markets

ii) run-off portfolio benefited from some

normalization of 1Q08 basis risk stress levels,

as well as good hedging execution

Solid progress in reducing overall sizing and

reducing “basis risks” between longs and shorts

Sample sensitivities to possible adverse market

developments shown at lower left (details of

vintage and rating are shown in supplement)

Going forward, both active and run-off CDO

portfolios will be managed and reported in

RMBS area

Exposure (CHF bn)

1)

Long

Short

Net

2Q08

1Q08

CDO Trading: subprime sensitivities (CHF m)

(CHF bn)

1Q08

9.3

(7.4)

1.9

2Q08

5.2

(4.1)

1.1

Net (writedowns)/writebacks

0.5

(2.7)

of which runoff

0.2

(2.9)

Potential scenario

Estimated loss

20% drop in ABS subprime

(0.2)

10% wider cash/CDS basis

(0.3)

2006 vintage outperforms by 10%

(0.1)

AAA underperforms by 10%

(0.1)

Asset Management: money market 'liftout' portfolio

Gross exposure (CHF bn)

2Q08

Securities transferred to bank balance sheet

Roll-forward of exposure (CHF bn)

1Q08

2Q08

1Q08

No new liftouts during 2Q08; money market

funds operated normally during the period

Portfolio reduced by 32% in 2Q08 largely

due to sales and maturities

Small net writebacks in 2Q08, mainly from

hedging gains; small writedowns on 'liftout'

portfolio

Positions now carried at a weighted

average value of approx. 60% to par

We continue to focus on reducing positions

while maximizing value

(CHF bn)

Structured Inv. Vehicles (SIVs)

1.1

1.5

Asset Backed Securities (ABS)

0.2

0.5

Corporates

0.2

0.2

Total

1.5

2.2

of which subprime-related

0.2

0.2

Exposure 1Q08

2.2

Sales, maturities, writedowns and FX

(0.7)

Exposure 2Q08

1.5

Net (writedowns)/writebacks

0.1

(0.6)

Other industry focus areas

Monolines

Auction Rate

Securities

We do not rely on monolines in our subprime hedging

Our inventory in monoline-wrapped paper is more than offset

by CDS and other forms of protection

SIVs

Credit Suisse does not sponsor any SIVs

US Agencies

Exposure to subordinated debt and preferred classes is limited

Credit Suisse has not been an active underwriter in auction rate

securities

Summary

Good reduction in risk exposure continued in 2Q08

Risk now re-sized to a level appropriate for current market conditions

Net investment banking writedowns immaterial in 2Q08 as we benefited from

consistent reduction strategy and mark-to-market disciplines

Asset Management 'liftout' portfolio reduced by 32% in 2Q08 with a small net

writeback

Expect market conditions to remain volatile; Credit Suisse portfolio is well

positioned for such an environment

Second quarter 2008 results

Renato Fassbind, Chief Financial Officer

Risk management update

Wilson Ervin, Chief Risk Officer

Introduction

Brady W. Dougan, Chief Executive Officer

Summary

Brady W. Dougan, Chief Executive Officer

Supplemental slides

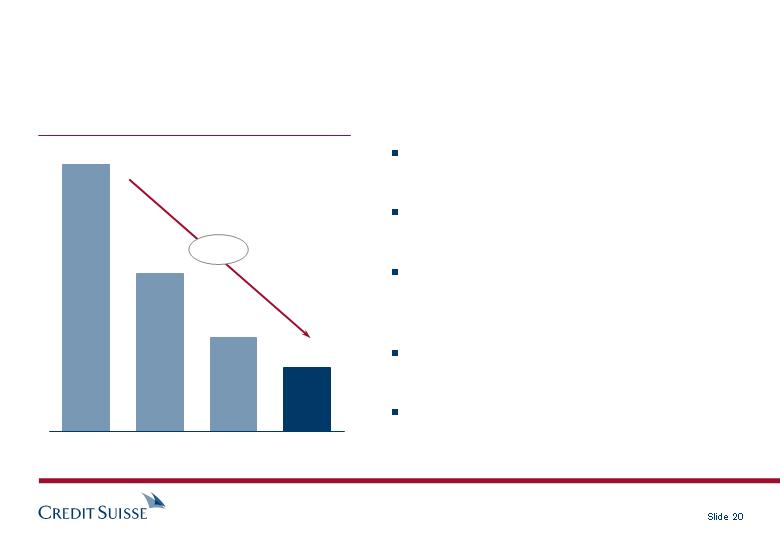

Leveraged finance exposures

Total exposure down 31% to CHF 14.3 bn

during 2Q08, driven primarily by continued

sales activity offset somewhat by new

originations

Gross exposure (CHF bn)

Roll-forward (CHF bn)

1) Non-investment grade exposures, at fair value

2) Figures exclude term financing to support certain sales transactions. This increased to CHF 2.8

bn in 2Q08 from CHF 2.2 bn in 1Q08

2Q08

1Q08

Unfunded

Funded

2Q08

1Q08

(CHF m)

1)

2)

Unfunded commitments

11.0

13.0

Funded positions

3.0

7.5

Equity bridges

0.3

0.3

Total gross exposure

14.3

20.8

Net writedowns

(0.1)

(1.7)

Exposures 1Q08

13.0

7.5

New exposures

1.1

–

Fundings

(1.3)

1.3

Sales, terminations,

writedowns & FX

(1.8)

(5.8)

Exposures 2Q08

11.0

3.0

Leveraged finance portfolio analysis

US bias reflects market leadership with

financial sponsors / LBO deals

The largest 5 commitments now

represent 80% of the portfolio; increase

in concentration is a natural result of

shrinking total exposure

Total exposure by geography

Asia

1%

Europe

9%

US

90%

Exposure by industry sector

Specialty

chemicals

50%

Gaming & Hotel 6%

Other 19%

Publishing

& Printing 5%

Home Furnishings 4%

Broadcast

services 16%

Commercial mortgage (CMBS) exposures

Gross exposure reduced by 22% to

CHF 15.0 bn during 2Q08

Positions carried at fair value, taking into

consideration prices for cash trading and

relevant indices (e.g. CMBX), as well as

specific asset fundamentals

Some new loan originations, largely outside

Europe and US

(CHF bn)

2Q08

1Q08

Roll-forward of exposure (CHF bn)

Net writedowns

1Q08

1) Includes both loans in the warehouse as well as securities still in syndication

(CHF bn)

2Q08

(0.8)

(0.5)

1)

Warehouse exposure

15.0

19.3

Exposure 1Q08

19.3

New loan originations

0.4

Sales, terminations,

writedowns and FX

(4.7)

Exposure 2Q08

15.0

Commercial mortgage (CMBS) portfolio analysis

Total exposure by geography

Asia

18%

Germany

27%

US

29%

Exposure by loan type

Office 40%

Retail 19%

Hotel 15%

Other 7%

Healthcare 8%

Multifamily 10%

Industrial 1%

Weighted average loan-to-value (LTV) ratio

Europe

US

Asia

Total

74

61

71

70

%

Portfolio is well-diversified with solid LTV

origination ratios

Exposure to continental Europe is now 50%

of the portfolio, with the largest contribution

from Germany

UK

3%

Other

Continental

Europe 23%

Residential mortgage (RMBS) exposure and portfolio analysis

Small net valuation gain in 2Q08; good

positioning in face of volatile markets

Exposures are fair valued based on market

levels

Overall exposures unchanged versus 1Q08

and relatively modest in overall scale

Gross positions are fairly similar to net

positions

(i.e. short positions are less than CHF 1 bn)

2Q08

1Q08

Net exposure (CHF bn)

2Q08

1Q08

1) All non-agency business, including higher quality segments

(CHF bn)

1)

Net (writedowns)/writebacks

0.0

(0.1)

US subprime

0.8

1.1

US Alt-A

1.1

1.1

US prime

0.7

0.8

Europe/Asia

2.8

2.5

Total net exposure

5.4

5.5

CDO trading: Vintage / rating analysis & methodology detail

1) Positions related to US subprime

Some exposure to basis risks if values shift among

vintage / rating buckets, but buckets are relatively

well-balanced

Methodology changes include two elements:

A) ‘Former methodology’ derived from spread

sensitivity and duration data while the ‘new

methodology’ uses a price-based method, which

is more appropriate when spreads become

extremely wide

B) In the ‘new methodology’, we net down gross

longs and shorts where a short is identical to a

matching long position while the “former

methodology” showed this gross if such

positions were with different counterparties; this

change should give a better view of market

sensitivity to basis risk between longs and shorts

Methodology changes impact risk exposure reporting

but do not affect valuation, which is done based on

market movements

Net exposures by vintage and rating

Exposure (CHF bn)

Long

Short

Net

(CHF bn)

1)

1)

(former methodology)

(new methodology)

(new methodology)

Vintage

Pre 2006

2006

2007

AAA

0.4

(0.3)

0.9

AA

0.3

(0.3)

–

A

0.2

–

(0.1)

BBB and below

0.3

(0.2)

1Q08

12.7

(12.0)

0.7

1Q08

9.3

(7.4)

1.9

2Q08

5.2

(4.1)

1.1

12.2

11.5

13.6

12.4

11.1

11.0

Risk measures – recent trends

Reported figures have grown over recent quarters,

largely due to volatile data from recent market

conditions and methodology changes

Adjusted for these factors, trading risk declined

since 1Q08

VaR not used for crisis planning because of

inherent sensitivity to market conditions

ERC trend (position risk)

VaR trend (Investment Banking trading only)

CHF bn

CHF bn

ERC is a broad measure of Credit Suisse

exposure, covering credit, market and investment

risks

ERC is down 19% vs. peak in 3Q07

Reduction is largely driven by reduced exposures

in leverage finance and CMBS

Dataset /

methodology changes

Positioning

2Q08

1Q08

4Q07

3Q07

2Q07

1Q07

2Q08

1Q08

4Q07

3Q07

2Q07

1Q07

193

194

176

95

110

78

Additional information

Valuation gains/(reductions) on structured products businesses and leveraged loan

commitments are included in Investment Banking net revenues as follows:

2Q08

1Q08

6M08

2007

Net revenues

(22)

(5,281)

(5,304)

(3,187)

of which

Fixed income trading

(391)

(4,523)

(4,915)

(2,283)

Net value gains/(reductions) from

structured products and leveraged

finance

Debt underwriting

61

(49)

12

(349)

Net value gains/(reductions) from

structured products and fee revenues/

(losses) from leveraged finance

Other revenues

308

(709)

(401)

(555)

Net value gains/(reductions) from

leveraged finance

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

|

| CREDIT SUISSE GROUP AG and CREDIT SUISSE |

|

| (Registrant) |

|

|

|

| By: | /s/ Urs Rohner |

|

| (Signature)* |

|

| General Counsel |

|

| Credit Suisse Group AG and Credit Suisse |

Date: July 24, 2008 |

|

|

|

| /s/ Charles Naylor |

|

| Head of Corporate Communications |

*Print the name and title under the signature of the signing officer. |

| Credit Suisse Group AG and Credit Suisse |