UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark one) |

☒ | ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2016 |

OR |

☐ | TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to |

Commission file numbers: 000-24477

DIFFUSION PHARMACEUTICALS INC.

(Exact name of Registrants as specified in their Charter)

Delaware

(State or Other Jurisdiction of Incorporation or Organization) | 30-0645032

(I.R.S. Employer Identification Number) |

2020 Avon Court, #4

Charlottesville, Virginia

(Address of Principal Executive Offices) |

22902

(Zip Code)

|

(434) 220-0718

(Registrants’ telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Common Stock, par value $0.001 per share

(Title of each class)

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ☐ | Accelerated filer ☐ |

Non-accelerated filer (Do not check if a smaller reporting company) ☐ | Smaller reporting company ☒ |

Indicate by check mark whether registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the registrant’s common stock, excluding shares beneficially owned by affiliates, computed by reference to the closing sale price at which the common stock was last sold as of June 30, 2016 (the last business day of the registrant’s second fiscal quarter) as quoted by OTCQX on that date was approximately $72.7 million.

As of March 15, 2017, 10,345,637 shares of common stock of the registrant were outstanding.

Documents Incorporated by Reference

Part III of this annual report on Form 10-K incorporates by reference information (to the extent specific sections are referred to herein) from the registrant’s definitive proxy statement for its 2016 Annual Meeting of Stockholders or an amendment to this Annual Report on Form 10-K, in any case, to be filed within 120 days of the end of the period covered by this Annual Report.

TABLE OF CONTENTS

PART I | | 1 |

| | | |

ITEM 1. | BUSINESS | 1 |

| | | |

ITEM 1A. | RISK FACTORS | 24 |

| | | |

ITEM 1B. | UNRESOLVED STAFF COMMENTS | 56 |

| | | |

ITEM 2. | PROPERTIES | 56 |

| | | |

ITEM 3. | LEGAL PROCEEDINGS | 56 |

| | | |

ITEM 4. | MINE SAFETY DISCLOSURES | 57 |

| | | |

PART II | | 57 |

| | | |

ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES | 57 |

| | | |

ITEM 6. | SELECTED FINANCIAL DATA | 58 |

| | | |

ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 58 |

| | | |

ITEM 7A. | QUANTITATIVE AND QUALITATIVE DISCLOSURE ABOUT MARKET RISK | 65 |

| | | |

ITEM 8. | FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA | 65 |

| | | |

ITEM 9. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | 90 |

| | | |

ITEM 9A. | CONTROLS AND PROCEDURES | 90 |

| | | |

ITEM 9B. | OTHER INFORMATION | 91 |

| | | |

PART III | | 91 |

| | | |

ITEM 10. | DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE | 91 |

| | | |

ITEM 11. | EXECUTIVE COMPENSATION | 91 |

| | | |

ITEM 12. | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS | 91 |

| | | |

ITEM 13. | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE | 91 |

| | | |

ITEM 14. | PRINCIPAL ACCOUNTING FEES AND SERVICES | 92 |

| | | |

PART IV | | 93 |

| | | |

ITEM 15. | EXHIBITS, FINANCIAL STATEMENT SCHEDULES | 93 |

| | | |

| ITEM 16. | FORM 10-K SUMMARY | 93 |

This annual report on Form 10-K contains certain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are subject to the safe harbor created by those sections. For more information, see “Part I. Item 1. Business — Cautionary Note Regarding Forward-Looking Statements.”

As previously disclosed, on January 8, 2016, Diffusion Pharmaceuticals Inc. (f/k/a RestorGenex Corporation), a Delaware corporation (the “Company”), completed the merger (the “Merger”) of its wholly owned subsidiary, Arco Merger Sub, LLC (“Merger Sub”), with and into Diffusion Pharmaceuticals LLC, a Virginia limited liability company (“Diffusion LLC”), in accordance with the terms of the Agreement and Plan of Merger, dated as of December 15, 2015, among the Company, Merger Sub and Diffusion LLC (the “Merger Agreement”). As a result of the Merger, Diffusion LLC, the surviving company in the Merger, became a wholly owned subsidiary of the Company and, following the Merger, the Company changed its corporate name from RestorGenex Corporation to Diffusion Pharmaceuticals Inc.

For accounting purposes, the Merger is treated as a “reverse acquisition” under generally acceptable accounting principles in the United States (“U.S. GAAP”) and Diffusion LLC is considered the accounting acquirer. Accordingly, Diffusion LLC’s historical results of operations will have replaced the Company’s historical results of operations for all periods prior to the Merger.

Unless the context otherwise requires, references to “Diffusion,” the “Company,” “we,” “our” or “us” in this report refer to Diffusion Pharmaceuticals Inc. and its subsidiaries, following the completion of the Merger and Diffusion Pharmaceuticals LLC prior to the completion of the Merger, references to “RestorGenex” refer to the Company prior to the completion of the Merger and references to “Diffusion LLC” refer to Diffusion Pharmaceuticals LLC.

Except as otherwise noted, references to “common stock” in this report refer to common stock, par value $0.001 per share, of the Company.

This report contains the following trademarks, trade names and service marks of ours: RestorGenex and Diffusion. All other trade names, trademarks and service marks appearing in this Annual Report on Form 10-K are the property of their respective owners. We have assumed that the reader understands that all such terms are source-indicating. Accordingly, such terms appear without the trade name, trademark or service mark notice for convenience only and should not be construed as being used in a descriptive or generic sense.

PART I

We are a clinical stage biotechnology company focused on extending the life expectancy of cancer patients by improving the effectiveness of current standard-of-care treatments, including radiation therapy and chemotherapy. We are developing our lead product candidate,transcrocetinate sodium, also known astrans sodium crocetinate (“TSC”), for use in the many cancer types in which tumor oxygen deprivation (“hypoxia”) is known to diminish the effectiveness of current treatments. TSC is designed to target the cancer’s hypoxic micro-environment, re-oxygenating treatment-resistant tissue and making the cancer cells more susceptible to the therapeutic effects of standard-of-care radiation therapy and chemotherapy. Our lead development programs target TSC against cancers known to be inherently treatment-resistant, including brain cancers and pancreatic cancer. A Phase 1/2 clinical trial of TSC combined with first-line radiation and chemotherapy in patients newly diagnosed with primary brain cancer (“glioblastoma” or “GBM”) was completed in 2015. This trial provided evidence of efficacy and safety in extending overall survival without the addition of toxicity. Based on these results, an End-of-Phase 2 meeting was held with the U.S. Food and Drug Administration (“FDA”) in August 2015, resulting in guidelines for the design of a single 400 patient pivotal Phase 3 registration study which, if successful, would be sufficient to support approval. The Company is also exploring the possibility of focusing on the subset of inoperable patients in the GBM indication. Discussions with the FDA regarding extension of the TSC development program from first line GBM into first-line pancreatic cancer treatment are currently underway. TSC has been granted Orphan Drug designation for the treatment of both GBM and brain metastases.

In addition to cancer, TSC also has potential applications in other indications involving hypoxia, such as hemorrhagic shock, stroke, peripheral artery disease, respiratory diseases and neurodegenerative diseases. In this regard, the Company is exploring the feasibility of testing TSC as a novel stroke treatment in an emergency medicine/ambulance setting.

Summary of Current Product Candidate Pipeline

The following table summarizes the targeted clinical indications for Diffusion’s lead molecule,trans sodium crocetinate:

In addition to the TSC programs depicted in the table, we are exploring alternatives regarding how best to capitalize upon our product candidate, RES-529, a novel PI3K/Akt/mTOR pathway inhibitor which has completed two Phase I clinical trials for age-related macular degeneration and is in preclinical development in oncology, specifically GBM.

Technology Overview

Our proprietary technology is targeted at overcoming treatment-resistance in solid cancerous tumors by combining our lead product candidate, TSC, with standard-of-care radiation and chemotherapy regimens, thus effecting a better patient survival outcome without the addition of harmful side effects.

Under normally oxygenated cellular conditions, radiation and chemotherapy generally have a powerful killing effect upon cancerous tumor tissue. However, in many solid tumor types, cellular oxygen deprivation occurs as the result of rapid tumor growth, causing parts of the tumor to outgrow its blood supply. When tumor tissue becomes hypoxic, it is up to three times more resistant to the cancer-killing power of the standard therapies (radiation and chemotherapy) currently used in the treatment of the vast majority of cancer patients. Cancerous tumor cells are known to thrive under hypoxic conditions, as the resultant changes in the tumor microenvironment confer “treatment-resistance” to radiation and chemotherapy within the cell.

Many solid cancerous tumor types are hypoxic and therefore subject to this treatment-resistance. TSC safely re-oxygenates treatment-resistant hypoxic tumor tissue via a novel mechanism of action, without affecting the oxygenation of normal tissue, thereby increasing therapeutic effectiveness. To date, no addition of serious harmful side effects, or exacerbation of the known side effects of standard-of-care treatments, has been observed in our clinical studies.

TSC’s distinctive re-oxygenation capabilities derive from its mechanism of action, which promotes enhanced diffusion of oxygen through blood plasma and into the hypoxic tumor microenvironment. Disruption of the treatment-resistance syndrome by re-oxygenation promotes enhanced cancer-killing power from radiation and chemotherapy, thereby safely extending patient survival. Because of the characteristics of this novel mechanism, oxygen levels of normal tissue remain unaffected, thereby avoiding side effects related to the syndrome referred to as “oxygen toxicity.” We believe this avoidance of oxygen toxicity confers a significant advantage to TSC’s diffusion-based approach over previous attempts to diminish treatment-resistance based on enhancing the oxygen concentration levels of the blood.

Our clinical development plan targets TSC at radiation and chemotherapy sensitization of hypoxic tumor types, with an initial focus on primary brain cancer, pancreatic cancer, and brain metastases. We have been granted orphan drug designations by the FDA for the treatment of brain cancers based on the acknowledged unmet medical need and number of patients affected. Such orphan drug designations allow certain favorable treatments under FDA regulations in connection with exclusivity periods and the new drug approval process.

Tumor Hypoxia

We believe that our breakthrough small molecule approach to overcoming solid tumor treatment-resistance by the reduction of cellular hypoxia may have significant implications for the improved treatment of cancer. Hypoxia is a deficiency in the supply of oxygen. It is well known that tumors are especially susceptible to developing hypoxia, driven by a combination of rapid cellular growth, structural abnormalities of the tumor microvessels and disturbed circulation within the tumor. There are a number of known treatment-resistance consequences conferred by tumor hypoxia, including increases in:

| | ● | Resistance to ionizing radiation; |

| | ● | Clinically aggressive phenotype; |

| | ● | Potential for more invasive growth; and, |

| | ● | Regional and distal tumor spreading. |

The above-described phenomenon of hypoxia-related “treatment-resistance” has been known to the scientific and clinical communities for over half a century. The challenge has been to find an approach that can effectively mitigate treatment-resistance without the addition of toxic side effects or exacerbation of the side effects associated with radiation and chemotherapy treatments. We believe that TSC embodies such an approach.

Trans Sodium Crocetinate

Dr. John Gainer, our Chief Scientific Officer, one of our directors and Professor Emeritus of Chemical Engineering at the University of Virginia, was the first to propose the use of chemical compounds specifically to facilitate the diffusion of oxygen through blood plasma for the purpose of re-oxygenating hypoxic tissues. Dr. Gainer’s early laboratory work systematically examined various means to alter the diffusivity of oxygen through the use of small molecules that would affect the intermolecular forces existing in blood plasma. He originally identified crocetin, a natural carotenoid compound, as a molecule that could increase oxygen diffusion through the plasma, and crocetin was shown to be an effective treatment in a rabbit model of atherosclerosis and other indications. This work continued from the 1970s into the mid-1990s with various animal models, including radiation sensitization and hemorrhagic shock.

Because crocetin is an isomeric mixture, Dr. Gainer examined whether it was thetrans-isomer which was responsible for eliciting the therapeutic benefit. These experiments led to his development of a puretrans-isomer salt compound, which he namedtrans sodium crocetinate. (The USAN designated name istranscrocetinate sodium). TSC has been shown to be more effective than crocetin in a severe model of hemorrhagic shock in both rats and pigs. It also demonstrated safety and efficacy in animal models of stroke and myocardial infarction, as well as in enhancing the response of hypoxic tumors to the therapeutic effects of radiation and chemotherapy.

It is proposed that TSC works by altering the molecular arrangement of the water molecules in blood plasma (which is composed of 90% water), with the altered structure being less dense – and thus less resistant to oxygen diffusion – than untreated blood plasma. A water molecule is composed of two hydrogen atoms and one oxygen atom, with a net positive charge found on the hydrogen atoms and a net negative charge found on the oxygen atom. This results in the formation of hydrogen bonds, which are an attraction between the net-negatively charged oxygen of one water molecule and the net-positively charged hydrogen atoms of another water molecule. Theoretically, one water molecule can form four hydrogen bonds with neighboring water molecules. However, the literature on the subject indicates that a water molecule actually forms, on average, 2 to 3.6 hydrogen bonds. By promoting an increase in the average number of hydrogen bonds among the water molecules comprising the bulk of blood plasma, TSC enhances the ability of oxygen to diffuse more easily through the plasma and into hypoxic tissue.

In March 2017, we received a patent for bipolar trans carotenoid salts and their uses.This patent expands the coverage of the therapeutic use of TSC and other related compounds to five hypoxia-related conditions including congestive heart failure, chronic renal failure, acute lung injury (ALI), chronic obstructive pulmonary disease (COPD) and respiratory distress syndrome (RDS).

Trans Sodium Crocetinate Increases Oxygenation of Hypoxic Cancerous Tumors

While earlier studies focused on improved treatments for hemorrhagic shock, ischemia, and traumatic brain injury, the use of TSC as an agent to re-oxygenate hypoxic cancerous tumors became a central area of research for us following our founding in 2001. Because tumor hypoxia is a leading cause of solid tumor resistance to both radiation and chemotherapy, it was believed that an agent such as TSC – one that could safely increase the oxygenation of hypoxic tumor tissue – could prove effective in treatment-resistant cancers when combined with standard-of-care regimens of radiation and/or chemotherapy. This belief led to the development of preclinical and clinical development programs targeted against treatment-resistance in various cancers, with a focus on brain cancer types (both GBM and metastatic) and pancreatic cancer, all of which are known to be significantly hypoxic. The Company’s longer term goal is to use TSC against treatment-resistance in the entire range of hypoxic cancers now treated with radiation and chemotherapy.

Glioblastoma Program

Our lead program is targeted against newly diagnosed primary brain cancer, also known as glioblastoma (GBM). Glioblastoma is a grade IV brain tumor, characterized by a heterogeneous cell population, with a number of negative attributes. GBM cells are typically genetically unstable (and thus prone to mutation), highly infiltrative, angiogenic, and resistant to radiation and chemotherapy. The mutations typically found in GBM allow the tumor to grow and thrive in a hypoxic environment. GBM is classified into two major subclasses, primary or secondary, depending upon the clinical properties as well as the chromosomal and genetic alterations that are unique to each class. Primary GBM arisesde novo from normal glial cells and typically occurs in those over the age of 40, while secondary GBM arises from transformation of lower grade tumors and is usually seen in younger patients. Primary GBM is believed to account for approximately 95% of all GBM diagnoses.

While GBM is the most common form of primary brain tumor involving glial cells it is still relatively rare, as approximately 12,000 people in the United States were diagnosed with GBM in 2014. The median age of GBM diagnosis is approximately 65 years, with the incidence of GBM in those over 65 increasing rapidly as shown by a doubling in incidence from 5.1 per 100,000 in the 1970s to 10.6 per 100,000 in the 1990s. Those diagnosed with the disease have a grim prognosis, with the median survival time of untreated patients being 4.5 months. Current standard-of-care treatment only provides 14-16 months of survival time after diagnosis.

Current Treatments for GBM

The standard-of-care for GBM tumors generally begins with surgical resection, unless the tumor is deemed inoperable due to its location near vital centers of the brain. This surgery is performed both to alleviate the symptoms associated with the disease as well as to facilitate treatment of residual tumor cells. Even with advances in surgical technique, complete removal of the tumor with clean margins is difficult to achieve, as the tumors are highly infiltrative and typically extend into the normal brain parenchyma. Due to this, almost all GBM patients have recurrence of the tumor, with 90% of such recurrence occurring at the primary site.

Due to the invasive nature of the tumors, surgical resection is promptly followed by radiotherapy coupled with the use of chemotherapeutic agents. Radiotherapy involves the administration of irradiation to the whole brain. While nitrosoureas were historically a commonly used chemotherapeutic agent, temozolomide (“TMZ”) was approved in 2005 and is now a mainstay of the standard-of-care. This is based on a clinical trial that showed the addition of TMZ to surgery and radiation increased median survival in newly diagnosed GBM patients to 14.6 months compared to 12.1 months for the surgery and radiation only group.

Most chemotherapeutic drugs have a limited ability to cross the blood brain barrier, thus a strategy to attempt to circumvent this was the development of Gliadel®, dissolvable chemotherapy wafers that could be placed in the tumor bed following surgical resection. Gliadel® contains the nitrosourea chemotherapeutic agent carmustine that is released for several weeks, in contrast to systemically administered carmustine that has a very short half-life. While Gliadel® wafers were shown to be safe, the drugs’ addition to radiation and TMZ did not result in a statistically significant increase in survival.

GBM tumors show increased expression of vascular endothelial growth factor (“VEGF”), and the anti-angiogenesis drug bevacizumab has been approved by the FDA for the treatment of recurrent GBM. A Phase 2 study found that bevacizumab treatment in patients with recurrent GBM increased six-month progression-free survival from a historical 9-15% to 25% with overall six-month survival of 54%. Another Phase 2 study showed that recurrent GBM patients treated with bevacizumab at a lower dose but a higher frequency had even higher six-month progression-free survival of 42.6%.

While bevacizumab has shown success in recurrent GBM, it is not utilized in newly diagnosed patients, our target patient population, as two separate clinical trials showed no difference in overall survival in patients treated with radiation, TMZ, and bevacizumab compared to patients treated with only radiation and TMZ. Bevacizumab treatment did result in an increase in progression free survival in both studies; however, the reason why this increase in progression free survival did not translate to an increase in overall survival is unclear. In addition, certain studies have reported that patients treated with bevacizumab had an increased symptom burden, a worse quality of life, and a decline in neurocognitive function.

GBM Therapies Under Development

There are a number of companies developing GBM therapies. For example, a search on the website www.clinicaltrials.gov yields over 300 results for “glioblastoma multiforme” and “open trials.” Most of these trials focus on the recurrent patient population, whereas our target population is newly diagnosed patients. In addition to the therapeutics previously mentioned, current GBM trials include Northwest Therapeutics’ DCVax®-L, Bristol-Myers Squibb’s Nivolumab/Ipilimumab and AbbVie’s Veliparib. In addition, the medical device company Novocure has been developing a novel approach called Tumor Treating Fields (“TTFields”) using low intensity, alternating electric fields within the intermediate frequency range. TTFields are believed to disrupt cell division through physical interactions with key molecules during mitosis. This medical device approach has shown some success in the recurrent GBM patient population and more recently as an initial treatment.

GBM is an Orphan Disease

GBM is diagnosed in approximately 12,000 individuals every year, making it an “orphan disease.” The Orphan Drug Act of 1983 was designed to provide financial incentives for, and to reduce the costs associated with, developing drugs for rare diseases and disorders. A “rare disease or disorder” is defined by the Orphan Drug Act of 1983 as affecting fewer than 200,000 Americans at the time of designation or one for which “there is no reasonable expectation that the cost of developing and making available in the United States…will be recovered from sales in the United States.” A sponsor must request that the FDA designate a drug currently under development for a “rare disease or condition” as an orphan drug, and if the FDA agrees that the drug and indication meet the criteria set forth in the Orphan Drug Act of 1983, certain financial and marketing incentives become available.

In July 2011, we announced that TSC was granted Orphan Drug Designation by the FDA for the treatment of GBM.

Trans Sodium Crocetinate Phase 1/2 Clinical Trial in GBM

We have evaluated TSC in 148 human subjects in various Phase 1 and Phase 2 clinical trials to date, with no serious adverse events attributable to TSC. Our Phase 1/2 clinical trial of TSC in patients with newly diagnosed GBM completed in 2015 is described in more detail below. TSC is targeted for testing against newly diagnosed GBM in an upcoming Phase 3 clinical trial that, assuming the availability of funding resources and the completion of certain manufacturing and animal toxicology guidelines mandated by the FDA guidance, could begin within the next twelve (12) months.

Our Phase 1/2 clinical trial in GBM enrolled 59 newly diagnosed patients who received TSC in conjunction with radiation and TMZ. In the Phase I portion of the trial, TSC was initially administered three times per week at half-dose to three patients prior to radiation. Subsequently, six additional patients received full-dose TSC for six weeks in combination with radiation. No dose-limiting toxicities were identified in the nine patients during the Phase I portion of the trial, nor were any serious adverse events relating to the drug observed. Fifty additional patients were enrolled in the Phase II trial and received full-dose TSC in combination with TMZ and radiation therapy. Four weeks after completion of radiation therapy, all patients underwent chemotherapy with higher doses of TMZ for five (5) days every four weeks, but no further TSC was administered.

We presented initial results from the trial at the 2015 American Society of Clinical Oncology (“ASCO”) Annual Meeting in June 2015, which discussed data from the 18 trial sites covering the first twenty-one months. Final results were published in the Journal of Neurosurgery online in May 2016. We compared results in relation to a historical control group from a 2005 study which showed that the addition of TMZ to standard-of-care (surgery plus radiation) increased overall survival from 12.1 months to 14.6 months. We reported that:

| | ● | TSC plus radiation and TMZ increased the patients’ chance of survival at two years by 37% compared to the historical control group. The overall survival at two years was 36.3% in the TSC group compared to 26.5% in the historical control group. |

| | ● | In the subgroup of patients considered inoperable, the chance of survival at two years for those who received TSC was increased by 380%, (40% alive at two years for TSC group versus 10% for control). |

| | ● | 71% of those treated with TSC were alive at one year compared to 61% of those in the historical control group. In 11 of 56 patients, tumors regressed to undetectable. |

| | ● | No serious safety findings attributed to TSC were observed in the TSC study and adverse events were consistent with those seen in previous trials of GBM featuring radiation and TMZ. |

End-of-Phase 2 FDA Meeting and Plans for TSC Phase 3 GBM Clinical Trial

Following the announcement of the results of the 2015 Phase 1/2 clinical trial in GBM, we held an end of Phase 2 meeting with the FDA in August 2015 to discuss planning for a Phase 3 clinical trial. At the meeting, guidance was received on a trial design for the Phase 3 study, including:

| | ● | A single, randomized trial of the agreed upon design, if successful, can serve as the basis for an application for approval. |

| | ● | The trial will consist of 400 newly diagnosed GBM patients with half given TSC in conjunction with standard-of-care radiation and TMZ and half receiving standard-of-care radiation and TMZ only. |

| | ● | Based on the Phase 1/2 safety results with supporting toxicology, TSC’s dosing exposure will be substantially increased, which means that TSC can now be used for both the radiation + chemotherapy and subsequent TMZ chemotherapy-only phase of GBM treatment, extending the TSC treatment duration from 6 weeks to 30 weeks. |

| | ● | Diffusion will provide certain expanded information on animal toxicology, pharmacokinetics and manufacturing practices to the FDA before initiating the trial. |

One of the major differences between the Phase 3 trial and the Phase 1/2 trial is the addition of TSC doses after the completion of the radiation/chemotherapy phase of treatment into the chemotherapy only phase. In the Phase 1/2 trial, TSC was only given prior to radiation (18 doses total over 6 weeks). In the Phase 3 study, we are planning to give the patients 36 total doses of TSC, 18 in conjunction with radiation/chemotherapy and 18 in conjunction with chemotherapy alone for a total TSC treatment duration of 30 weeks. The following figure gives a graphical representation of our planned Phase 3 trial, which, assuming the availability of financial resources and the completion of certain manufacturing and animal toxicology guidelines mandated by the FDA guidelines, we intend to commence enrollment in 2017, complete enrollment and potentially receive interim data in 2019 and complete conduct (enrollment and dosing) of the study in 2020. Data collection, analysis and regulatory interaction are projected to occur over the following 12 to 18 months.

Pancreatic Cancer Program

One of the most hypoxic of all the solid cancers, and therefore one of the most treatment-resistant, is pancreatic cancer. According to the American Cancer Society, pancreatic cancer is responsible for 7% of all cancer deaths in both men and women, making it the fourth leading cause of cancer death in the U.S. Estimates are that 40% of pancreatic cancer cases are sporadic in nature, 30% are related to smoking and 20% may be associated with dietary factors, with only 5-10% of cases hereditary in nature.

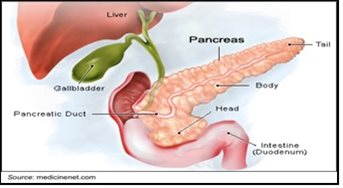

Pancreatic cancer is difficult to diagnose in early stages because initial symptoms are often nonspecific and subtle in nature, and include anorexia, malaise, nausea, fatigue, and back pain. Approximately 75% of all pancreatic carcinomas occur within the head or neck of the pancreas, 15-20% occur in the body of the pancreas, and 5-10% occur in the tail.

The only potential curative therapy for pancreatic cancer is complete surgical resection. Unfortunately, this is only possible for approximately 20% of cases, and even of those patients whose cancer is surgically resected, 80% will develop metastatic disease within two to three years following surgery. Patients with unresectable pancreatic cancer have a median overall survival of 10 to 14 months while patients diagnosed with Stage IV disease (indicative of metastases) have a 5-year overall survival of just 1%.

Multiple studies have confirmed that pancreatic cancers are highly hypoxic. A study reporting the direct measurement of oxygenation in human pancreatic tumors prior to surgery showed dramatic differences between tumors and normal tissue. The partial pressure of oxygen (“pO2”) ranged between 0-5.3 mmHg in tumors but in adjacent normal tissue it ranged from 9.3-92.7 mmHg. Hypoxic areas are also frequently found when examining tissue from mouse models of pancreatic cancer.

Current Treatment Options for Pancreatic Cancer

Surgery remains the primary mode of treatment for patients with pancreatic cancer. However, there is an important role for chemotherapy and/or radiation in an adjuvant setting (given to prevent recurrence) or neoadjuvant setting (given before surgery to shrink the tumor to make complete resection more probable), as well as in patients with unresectable disease.

Since its approval in 1996, gemcitabine has been partnered with approximately 30 different agents in late-stage clinical trials in an attempt to improve upon the effectiveness of gemcitabine alone in treating patients with metastatic pancreatic cancer. Only two of these trials have demonstrated improved efficacy, leading to FDA approvals – erlotinib (Tarceva®) and nab-paclitaxel (Abraxane®).

In patients with metastatic disease, the use of erlotinib with gemcitabine led to a significantly higher one-year survival rate than with the use of gemcitabine alone (23% vs. 17%,P= 0.023) as well as an increased median overall survival (6.24 months vs. 5.91 months,P = 0.038). A more recent study showed that the addition of nanoparticle albumin-bound (nab)-paclitaxel to gemcitabine significantly improved overall survival in treatment naïve patients with metastatic cancer, as overall survival was approximately two (2) months longer in patients treated with combination therapy (8.5 vs. 6.7 months).

The Folfirinox (leucovorin + 5-fluorouracil + oxaliplatin + irinotecan) regimen was shown to significantly improve overall survival compared to treatment with gemcitabine (11.1 months vs. 6.8 months). While dramatically improving overall survival, the Folfirinox treatment was accompanied by serious adverse events and thus is only recommended for patients with good performance status.

Other combinations of gemcitabine with cisplatin, oxaliplatin, irinotecan or docetaxel tested in Phase 3 trials have not been of superior benefit to gemcitabine alone. The combination therapy nab-Paclitaxel and gemcitabine was recently approved by the FDA as an additional standard-of-care for the treatment of patients with untreated pancreatic adenocarcinoma. However, the improvements were modest, and treatment of pancreatic cancer remains an area of intense research, with 92 products in all stages of clinical development with 14 of them in Phase 3 at this time according to clinicaltrials.gov.

Just recently, the FDA approved Onivyde® (irinotecan liposome injection) in combination with fluorouracil and leucovorin, to treat patients with metastatic pancreatic cancer who were previously treated with gemcitabine-based chemotherapy. In the pivotal clinical trial, patients treated with Onivyde® plus fluorouracil/leucovorin lived an average of 6.1 months, compared to 4.2 months for those treated with only fluorouracil/leucovorin.

Pancreatic Cancer Market Analysis

It is estimated that every year approximately 49,000 people are diagnosed with pancreatic cancer in the United States. More than half of these patients will be diagnosed with metastatic disease. The five-year survival rates for patients with pancreatic cancer are dismal (<14%) and are particularly bad for those with metastatic disease (~1%).

The current standard-of-care for patients with metastatic pancreatic cancer includes gemcitabine combined with either erlotinib or nab-paclitaxel. Gemzar® (gemcitabine) is now available as a generic, however prior to losing patent protection the drug generated peak revenues of approximately $700 million in the United States for Eli Lilly. Tarceva®(erlotinib), which is approved for the treatment of metastatic non-small cell lung cancer and metastatic pancreatic cancer, is marketed by Roche and Astellas and sales of the drug generated $1.2 billion in revenue in 2015. Abraxane® (nab-paclitaxel), which was approved for the treatment of breast cancer in 2005 and non-small cell lung cancer in 2012, was approved by the FDA in 2013 for the treatment of metastatic pancreatic cancer. Sales of Abraxane® totaled $848 million in 2014 for all indications.

TSC in Pancreatic Cancer

We believe that targeting hypoxia in pancreatic cancer with TSC, especially in combination with standard-of-care therapies involving gemcitabine and nab-paclitaxel, may be beneficial in the treatment of pancreatic cancer. Pancreatic cancer is one of the most hypoxic malignant tumors, making it one of the most resistant tumors to therapy. Patients with advanced pancreatic cancer of exocrine origin have few therapeutic options and, for patients with advanced cancers, the overall survival rate of all stages is less than 1% at 5 years, with most patients dying within 1 year. Gemcitabine remains to-date, the backbone of treatment of pancreatic cancer.

The antitumor efficacy of gemcitabine is known to be hindered by a number of hypoxia-related factors including, but not limited to:

| | ● | Limited Delivery of Gemcitabine to Intracellular Tumor Microenvironment. Hypoxia has been associated with resistance to nucleoside analogs such as gemcitabine by decreasing the expression of the human cross-cell membrane equilibrative nucleoside transporter 1 (hENT1), thereby decreasing transport of gemcitabine and other nucleoside analogues into tumor cells. |

| | ● | Gemcitabine Intratumor Cell Inhibition of Ribonucleotide Reductase Compromised. Hypoxia has been associated with a decrease in intracellular tumor ribonucleotide reductase, an enzyme required for the antitumor effect of gemcitabine. Indeed, this decrease leads to cell cycle arrest in G1 or G2 phase, thereby allowing DNA repair before progression to S or M phase. |

| | ● | Increased Breakdown of Gemcitabine. It has been also observed that under hypoxic conditions, intratumor cell levels of cytidine deaminase are substantially increased. Cytidine Deaminase is the main enzyme responsible for the breakdown of gemcitabine and similar nucleosides. As a result of this, the gemcitabine antitumor effect is substantially decreased under hypoxic conditions. |

| | ● | Nab-paclitaxel Potentiates Gemcitabine by Decreasing Cytidine Deaminase. One of the ways nab-paclitaxel decreases cytidine deaminase has been observed to be through increasing reactive oxygen species (“ROSs”) which has been shown to deactivate cytidine deaminase. |

Taken together, the four factors above are believed to explain, at least in part, the limitations of gemcitabine in hypoxic conditions and the efficacy observed with the gemcitabine plus nab-paclitaxel combination regimen for the treatment of pancreatic cancer. They also suggest that correction of hypoxia with an anti-hypoxia agent such as TSC may significantly improve the efficacy of the gemcitabine plus nab-paclitaxel combination regimen for the treatment of pancreatic cancer, including for the following reasons:

| | ● | TSC has been shown to improve the cytotoxic effect of gemcitabine in a pre-clinical rat model. |

| | ● | By correcting hypoxia, TSC may improve delivery of gemcitabine to intracellular tumor microenvironment by increasing levels of hENT-1. |

| | ● | By reversing hypoxia-induced cell cycle arrest via reactivation of ribonucleotide reductase, TSC may restore gemcitabine’s antitumor effect. |

| | ● | By reversing the hypoxia-induced increase of cytidine deaminase, TSC may increase intratumoral gemcitabine levels. Addition of TSC to the gemcitabine plus nab-paclitaxel regimen could further improve the efficacy of the combination by further decreasing cytidine deaminase. Of note, hypoxia has also been implicated in conferring tumor resistance to taxane-based therapies. |

Proposed Plans for TSC Phase 2 Clinical Trial in Pancreatic Cancer

The planned Phase 2 clinical trial for TSC in pancreatic cancer is based on preclinical safety and efficacy data, and findings from the Phase 1/2 clinical trial in GBM, as well as the facts noted above. Global experts in the field agree that pancreatic cancer is an appropriate target for expansion of the use of TSC, and a clinical advisory committee of these key opinion leaders has been assembled to facilitate our pancreatic cancer clinical development program. We are currently in discussions with recognized pancreatic cancer experts and the FDA regarding trial design, end-points, and patient numbers. Assuming the availability of financial resources, we anticipate beginning enrollment in this trial during 2017 and completing conduct of the study (enrollment and dosing) in 2019. Data collection, analysis and regulatory interaction are projected to occur over the following 9 to 12 months.

Brain Metastases Program

In contrast to the relative rarity of primary brain cancers, life-threatening cancers that metastasize to the brain are much more common and represent a serious complication in the treatment of many cancer types. Up to 30% of adult cancer patients will suffer from brain metastases. There are approximately 170,000 cases of metastatic brain cancer every year in the United States. Incidence of brain metastases varies depending upon the primary tumor type, although lung cancer appears to carry the greatest risk. The prognosis for patients with brain metastases is very grim, with current treatment options only resulting in median overall survival times of less than one year.

Treatment for brain metastases involves both controlling the symptoms associated with the condition as well as attacking the cancer directly. Brain metastases typically result in edema that can be controlled with the use of steroids; however, long-term use of steroids typically results in side effects that diminish a patient’s quality of life. Approximately 25-45% of patients will experience seizures and require the use of anti-epileptic drugs. Surgery is only utilized in patients with a solitary brain metastatic lesion. Radiation therapy remains the standard-of-care for the vast majority of patients with brain metastases. There is very limited evidence for the use of chemotherapy, as few clinical trials have been conducted. There are no medications currently approved for the treatment of brain metastases.

Plans for TSC Phase 2/3 Clinical Trial in Metastatic Brain Cancer

We are planning to conduct a Phase 2/3 clinical trial in metastatic brain cancer after further discussions with experts and the FDA regarding trial design, end-points, and patient numbers.

In December 2012, the FDA granted us Orphan Drug Designation for the use of TSC in brain metastases.

Description of Other Indications/Products

We have rights to and own technologies and potential products beyond those described above, including analog molecules as backups to TSC. It is our strategy to focus at the current time on our TSC for oncology, specifically GBM and pancreatic cancer, as described herein. Beyond those described herein, we also intend to continue to review our technologies and potential products on a regular basis and consider internal development in the future and the potential to out-license portions of our technology and potential products to other biopharmaceutical companies with greater focus and resources than ours, or potentially in-license late stage products which are in or ready for human clinical trials.

As a result of the Merger, we acquired product candidates for ophthalmology, oncology and dermatology. One such product candidate is RES-529, a novel PI3K/Akt/mTOR pathway inhibitor which has completed two Phase I clinical trials for age-related macular degeneration and is in preclinical development in oncology, specifically GBM. The novel inhibition of the PI3K/Akt/mTOR pathway and targeting of the androgen receptor have also shown potential in a number of additional indications.

We are exploring partnering opportunities for our product candidates, such as strategic partnerships, alliances or licensing arrangements.

Competition

Our industry is highly competitive and subject to rapid and significant change. Potential competitors in the United States are numerous and include major pharmaceutical and specialty pharmaceutical companies, universities and other institutions. We generally divide our competition in the pharmaceutical industry into four categories: (1) corporations with large research and developmental departments that develop and market products in many therapeutic areas; (2) companies that have moderate research and development capabilities and focus their product strategy on a small number of therapeutic areas; (3) small companies with limited development capabilities and only a few product offerings; and (4) university and other research institutions. Many of our competitors have longer operating histories, greater name recognition, substantially greater financial resources and larger research and development staffs than we do, as well as substantially greater experience than us in developing products, obtaining regulatory approvals, and manufacturing and marketing pharmaceutical products. A significant amount of research is carried out at academic and government institutions. These institutions are aware of the commercial value of their findings and are aggressive in pursuing patent protection and negotiating licensing arrangements to collect royalties for use of technology that they have developed.

There are several firms currently marketing or developing products that may be competitive with our products, including therapeutics and devices. We believe TSC is a first-in-class novel small molecule that re-oxygenates hypoxic tissue, enhancing efficacy of radiation and chemotherapy without harmful side effects.

Mergers and acquisitions in the pharmaceutical and biotechnology industries may result in even more resources being concentrated among a smaller number of our competitors. Our commercial opportunity could be reduced or eliminated if our competitors develop or market products or other novel therapies that are more effective, safer or less costly than our current or future product candidates, or obtain regulatory approval for their products more rapidly than we may obtain approval for our product candidates. In addition, the first product to reach the market in a therapeutic or preventative area is often at a significant competitive advantage relative to later entrants in the market and may result in certain marketing exclusivity as per federal legislation. Acceptance by physicians and other health care providers, including managed care groups, also is critical to the success of a product versus competitor products. Our success will be based in part on our ability to identify, develop and manage a portfolio of product candidates that are safer and more effective than competing products.

Research and Product Development

We incurred approximately $7.2 million in 2016 and $3.9 million in 2015 on research and product development activities that related primarily to activities associated with the synthesis and formulations of our products then in development, additional preclinical studies and planning for Phase I/Phase II studies. We anticipate that our research and development expenses during 2017 will increase compared to 2016 and will consist primarily of expenses associated with the initiation of our glioblastoma and pancreatic cancer human clinical trials.

Intellectual Property

Our success depends and will continue to depend in part upon our ability to maintain proprietary protection for our products and technologies, to preserve our proprietary information, trademarks and trade secrets and to operate without infringing the proprietary rights of others. Our policy is to attempt to protect our technology by, among other things, filing patent applications on inventions that are important to the development and conduct of our business with the U.S. Patent and Trademark Office (“USPTO”), and its foreign counterparts or obtaining license rights for technology that we consider important to the development of our business.

As of December 31, 2016, we owned approximately 14 issued U.S. patents and 46 issued foreign patents, which include granted European, Japanese, Chinese and Indian patent rights, and over 50 pending patent applications worldwide, covering the product candidates we currently intend to develop. Our current patents expire between 2026 and 2031. TSC has been granted Orphan Drug Designation for the treatment of both GBM and metastatic brain cancer and an application is pending for pancreatic cancer. A formulation patent provides protection for the TSC oral drug product until 2031 with extensions possible.

Patents extend for varying periods according to the date of patent filing or grant and the legal term of patents in various countries where patent protection is obtained. The actual protection afforded by a patent, which can vary from country to country, depends on the type of patent, the scope of its coverage and the availability of legal remedies in the country.

In addition to patents, we use other forms of protection, such as trademark, copyright and trade secret protection, to protect our intellectual property, particularly where we do not believe patent protection is appropriate or obtainable. We aim to take advantage of all of the intellectual property rights that are available to us and believe that this comprehensive approach will provide us with proprietary positions for our product candidates, where available.

We also protect our proprietary information by requiring our employees, consultants, contractors and other advisors to execute nondisclosure and assignment of invention agreements upon commencement of their respective employment or engagement. Agreements with our employees also prevent them from bringing the proprietary rights of third parties to us. In addition, we also require confidentiality or service agreements from third parties that receive our confidential information or materials.

Government Regulation

FDA Drug Approval Process

In the United States, pharmaceutical products are subject to extensive regulation by the FDA. The Federal Food, Drug, and Cosmetic Act (the “FDC Act”) and other federal and state statutes and regulations, govern, among other things, the research, development, testing, manufacture, storage, recordkeeping, approval, labeling, promotion and marketing, distribution, post-approval monitoring and reporting, sampling and import and export of pharmaceutical products. Failure to comply with applicable U.S. requirements may subject a company to a variety of administrative or judicial sanctions, such as FDA refusal to approve pending new drug applications (“NDAs”), warning or untitled letters, product recalls, product seizures, total or partial suspension of production or distribution, injunctions, fines, civil penalties and criminal prosecution.

Pharmaceutical product development for a new product or certain changes to an approved product in the United States typically involves preclinical laboratory and animal tests, the submission to the FDA of an investigational new drug application (“IND”) which must become effective before clinical testing may commence, and adequate and well-controlled clinical trials to establish the safety and effectiveness of the drug for each indication for which FDA approval is sought. Satisfaction of FDA pre-market approval requirements typically takes many years and the actual time required may vary substantially based upon the type, complexity and novelty of the product or disease.

Preclinical tests include laboratory evaluation of product chemistry, formulation and toxicity, as well as animal trials to assess the characteristics and potential safety and efficacy of the product. The conduct of the preclinical tests must comply with federal regulations and requirements, including good laboratory practices. The results of preclinical testing are submitted to the FDA as part of an IND, along with other information, including information about product chemistry, manufacturing and controls and a proposed clinical trial protocol. Long term preclinical tests, such as animal tests of reproductive toxicity and carcinogenicity, may continue after the IND is submitted.

A 30-day waiting period after the submission of each IND is required prior to the commencement of clinical testing in humans. If the FDA has neither commented on nor questioned the IND within this 30-day period, the clinical trial proposed in the IND may begin.

Clinical trials involve the administration of the investigational new drug to healthy volunteers or patients under the supervision of a qualified investigator. Clinical trials must be conducted: (1) in compliance with federal regulations; (2) in compliance with good clinical practice (“GCP”) an international standard meant to protect the rights and health of patients and to define the roles of clinical trial sponsors, administrators and monitors; and (3) under protocols detailing the objectives of the trial, the parameters to be used in monitoring safety and the effectiveness criteria to be evaluated. Each protocol involving testing on U.S. patients and subsequent protocol amendments must be submitted to the FDA as part of the IND.

The FDA may order the temporary or permanent discontinuation of a clinical trial at any time, or impose other sanctions, if it believes that the clinical trial either is not being conducted in accordance with FDA requirements or presents an unacceptable risk to the clinical trial patients. The study protocol and informed consent information for patients in clinical trials must also be submitted to an institutional review board (“IRB”) for approval at each site at which the clinical trial will be conducted. An IRB may also require the clinical trial at the site to be halted, either temporarily or permanently, for failure to comply with the IRB’s requirements, or may impose other conditions.

Clinical trials to support NDAs for marketing approval are typically conducted in three sequential phases, but the phases may overlap, especially in cancer indications. In Phase 1, the initial introduction of the drug into healthy human subjects or patients, the drug is tested to assess pharmacological actions, side effects associated with increasing doses and, if possible, early evidence on effectiveness. Phase 2 usually involves trials in a limited patient population to determine metabolism, pharmacokinetics, the effectiveness of the drug for a particular indication, dosage tolerance and optimum dosage, and to identify common adverse effects and safety risks. If a compound demonstrates evidence of effectiveness and an acceptable safety profile in Phase 2 evaluations, Phase 3 clinical trials are undertaken to obtain the additional information about clinical efficacy and safety in a larger number of patients, typically at geographically dispersed clinical trial sites, to permit the FDA to evaluate the overall benefit-risk relationship of the drug and to provide adequate information for the labeling of the drug. In most cases the FDA requires two adequate and well-controlled Phase 3 clinical trials with statistically significant results to demonstrate the efficacy of the drug. With suitable FDA agreement, a single Phase 3 clinical trial with other confirmatory evidence may be sufficient. In those instances, the study is usually a large multicenter trial demonstrating internal consistency and a statistically persuasive finding of an effect on mortality, irreversible morbidity or prevention of a disease with a potentially serious outcome and confirmation of the result in a second trial would be practically or ethically impossible.

After completion of the required clinical testing, an NDA is prepared and submitted to the FDA. FDA approval of the NDA is required before marketing of the product may begin in the United States. The NDA must include the results of all preclinical, clinical and other testing and a compilation of data relating to the product’s pharmacology, chemistry, manufacture and controls. The cost of preparing and submitting an NDA is substantial. The submission of most NDAs is additionally subject to a substantial application user fee, and the manufacturer and sponsor under an approved new drug application are also subject to annual product and establishment user fees. These fees are typically increased annually.

The FDA has sixty (60) days from its receipt of an NDA to determine whether the application will be accepted for filing based on the agency’s threshold determination that it is sufficiently complete to permit substantive review. Once the submission is accepted for filing, the FDA begins an in-depth review. The FDA has agreed to certain performance goals in the review of new drug applications. Priority review can be applied to drugs that the FDA determines offer major advances in treatment, or provide a treatment where no adequate therapy exists. For certain drugs, priority review is further limited only for drugs intended to treat a serious or life-threatening disease relative to the currently approved products. The review process for both standard and priority review may be extended by the FDA for three (3) additional months to consider certain late-submitted information, or information intended to clarify information already provided in the submission.

The FDA may also refer applications for novel drug products, or drug products that present difficult questions of safety or efficacy, to an advisory committee, typically a panel that includes clinicians and other experts, for review, evaluation and a recommendation as to whether the application should be approved. The FDA is not bound by the recommendation of an advisory committee, but it generally follows such recommendations. Before approving an NDA, the FDA will typically inspect one or more clinical sites to assure compliance with GCP. Additionally, the FDA will inspect the facility or the facilities at which the drug is manufactured. The FDA will not approve the product unless compliance with current good manufacturing practice (“cGMP”) is satisfactory and the NDA contains data that provide substantial evidence that the drug is safe and effective in the indication studied.

After the FDA evaluates the NDA and the manufacturing facilities, it issues either an approval letter or a complete response letter. A complete response letter generally outlines the deficiencies in the submission and may require substantial additional testing, or information, in order for the FDA to reconsider the application. If, or when, those deficiencies have been addressed to the FDA’s satisfaction in a resubmission of the NDA, the FDA will issue an approval letter. The FDA has committed to reviewing such resubmissions in two or six (6) months depending on the type of information included.

An approval letter authorizes commercial marketing of the drug with specific prescribing information for specific indications. As a condition of NDA approval, the FDA may require a risk evaluation and mitigation strategy (“REMS”) to help ensure that the benefits of the drug outweigh the potential risks. REMS can include medication guides, communication plans for healthcare professionals and elements to assure safe use (“ETASU”). ETASU can include, but are not limited to, special training or certification for prescribing or dispensing, dispensing only under certain circumstances, special monitoring and the use of patient registries. The requirement for a REMS can materially affect the potential market and profitability of the drug. Moreover, product approval may require substantial post-approval testing and surveillance to monitor the drug’s safety or efficacy. Once granted, product approvals may be withdrawn if compliance with regulatory standards is not maintained or problems are identified following initial marketing.

Changes to some of the conditions established in an approved application, including changes in indications, labeling, or manufacturing processes or facilities, require submission and FDA approval of a new NDA or NDA supplement before the change can be implemented. An NDA supplement for a new indication typically requires clinical data similar to that in the original application, and the FDA uses the same procedures and actions in reviewing NDA supplements as it does in reviewing NDAs.

The Hatch-Waxman Act

Orange Book Listing

In seeking approval for a drug through an NDA, applicants are required to list with the FDA each patent whose claims cover the applicant’s product. Upon approval of a drug, each of the patents listed in the application for the drug is then published in the FDA’s Approved Drug Products with Therapeutic Equivalence Evaluations, commonly known as the Orange Book. Drugs listed in the Orange Book can, in turn, be cited by potential generic competitors in support of approval of an abbreviated new drug application (“ANDA”). An ANDA provides for marketing of a drug product that has the same active ingredients in the same strengths and dosage form as the listed drug and has been shown through bioequivalence testing to be therapeutically equivalent to the listed drug. Other than the requirement for bioequivalence testing, ANDA applicants are not required to conduct, or submit results of, preclinical or clinical tests to prove the safety or effectiveness of their drug product. Drugs approved in this way are commonly referred to as “generic equivalents” to the listed drug, and can often be substituted by pharmacists under prescriptions written for the original listed drug.

The ANDA applicant is required to certify to the FDA concerning any patents listed for the approved product in the FDA’s Orange Book. Specifically, the applicant must certify that: (1) the required patent information has not been filed; (2) the listed patent has expired; (3) the listed patent has not expired, but will expire on a particular date and approval is sought after patent expiration; or (4) the listed patent is invalid or will not be infringed by the new product. The ANDA applicant may also elect to submit a section viii statement certifying that its proposed ANDA label does not contain (or carves out) any language regarding the patented method-of-use rather than certify to a listed method-of-use patent. If the applicant does not challenge the listed patents, the ANDA will not be approved until all the listed patents claiming the referenced product have expired.

A certification that the new product will not infringe the already approved product’s listed patents, or that such patents are invalid, is called a Paragraph IV certification. If the ANDA applicant has provided a Paragraph IV certification to the FDA, the applicant must also send notice of the Paragraph IV certification to the NDA and patent holders once the ANDA has been accepted for filing by the FDA. The NDA and patent holders may then commence a patent infringement lawsuit in response to the notice of the Paragraph IV certification. The filing of a patent infringement lawsuit within forty-five (45) days of the receipt of a Paragraph IV certification automatically prevents the FDA from approving the ANDA until the earlier of thirty (30) months, expiration of the patent, settlement of the lawsuit, or a decision in the infringement case that is favorable to the ANDA applicant.

The ANDA also will not be approved until any applicable non-patent exclusivity listed in the Orange Book for the referenced product has expired.

Exclusivity

Upon NDA approval of a new chemical entity (“NCE”) which is a drug that contains no active moiety that has been approved by the FDA in any other NDA, that drug receives five years of marketing exclusivity during which the FDA cannot receive any ANDA seeking approval of a generic version of that drug. Certain changes to a drug, such as the addition of a new indication to the package insert, are associated with a three-year period of exclusivity during which the FDA cannot approve an ANDA for a generic drug that includes the change.

An ANDA may be submitted one year before NCE exclusivity expires if a Paragraph IV certification is filed. If there is no listed patent in the Orange Book, there may not be a Paragraph IV certification and, thus, no ANDA may be filed before the expiration of the exclusivity period.

REMS

The FDA has the authority to require a REMS to ensure the safe use of the drug. In determining whether a REMS is necessary, the FDA must consider the size of the population likely to use the drug, the seriousness of the disease or condition to be treated, the expected benefit of the drug, the duration of treatment, the seriousness of known or potential adverse events, and whether the drug is a new molecular entity. If the FDA determines a REMS is necessary, the drug sponsor must agree to the REMS plan at the time of approval. A REMS may be required to include various elements, such as a medication guide or patient package insert, a communication plan to educate healthcare providers of the drug’s risks, limitations on who may prescribe or dispense the drug, or other measures that the FDA deems necessary to assure the safe use of the drug. REMS can include medication guides, communication plans for healthcare professionals, and ETASU. ETASU can include, but are not limited to, special training or certification for prescribing or dispensing, dispensing only under certain circumstances, special monitoring, and the use of patient registries. In addition, the REMS must include a timetable to periodically assess the strategy. The FDA may also impose a REMS requirement on a drug already on the market if the FDA determines, based on new safety information, that a REMS is necessary to ensure that the drug’s benefits outweigh its risks. The requirement for a REMS can materially affect the potential market and profitability of a drug.

Patent Term Extension

After NDA approval, owners of relevant drug patents may apply for up to a five-year patent extension. The allowable patent term extension is calculated as half of the drug’s testing phase, the time between IND application and NDA submission, and all of the review phase, the time between NDA submission and approval, up to a maximum of five years. The time can be shortened if the FDA determines that the applicant did not pursue approval with due diligence. The total patent term after the extension may not exceed 14 years.

For patents that might expire during the application phase, the patent owner may request an interim patent extension. An interim patent extension increases the patent term by one year and may be renewed up to four times. For each interim patent extension granted, the post-approval patent extension is reduced by one year. The director of the USPTO must determine that approval of the drug covered by the patent for which a patent extension is being sought is likely. Interim patent extensions are not available for a drug for which an NDA has not been submitted.

Post-Approval Requirements

Once an NDA is approved, a product will be subject to certain post-approval requirements. For instance, the FDA closely regulates the post-approval marketing and promotion of drugs, including standards and regulations for direct-to-consumer advertising, off-label promotion, industry-sponsored scientific and educational activities and promotional activities involving the internet. Drugs may be marketed only for the approved indications and in accordance with the provisions of the approved labeling.

Adverse event reporting and submission of periodic reports is required following FDA approval of an NDA. The FDA also may require post-marketing testing, known as Phase 4 testing, REMS, and surveillance to monitor the effects of an approved product, or the FDA may place conditions on an approval that could restrict the distribution or use of the product. In addition, quality-control, drug manufacture, packaging and labeling procedures must continue to conform to cGMPs after approval. Drug manufacturers and certain of their subcontractors are required to register their establishments with the FDA and certain state agencies. Registration with the FDA subjects entities to periodic unannounced inspections by the FDA, during which the agency inspects manufacturing facilities to assess compliance with cGMPs. Accordingly, manufacturers must continue to expend time, money and effort in the areas of production and quality-control to maintain compliance with cGMPs. Regulatory authorities may withdraw product approvals or request product recalls if a company fails to comply with regulatory standards, if it encounters problems following initial marketing, or if previously unrecognized problems are subsequently discovered.

Pediatric Information

Under the Pediatric Research Equity Act, NDAs or supplements to NDAs must contain data to assess the safety and effectiveness of the drug for the claimed indications in all relevant pediatric subpopulations and to support dosing and administration for each pediatric subpopulation for which the drug is safe and effective. The FDA may grant full or partial waivers, or deferrals, for submission of data.

The Best Pharmaceuticals for Children Act (“BPCA”) provides NDA holders a six-month extension of any exclusivity, patent or non-patent, for a drug if certain conditions are met. Conditions for exclusivity include the FDA’s determination that information relating to the use of a new drug in the pediatric population may produce health benefits in that population, the FDA making a written request for pediatric studies and the applicant agreeing to perform, and reporting on, the requested studies within the statutory timeframe. Applications under the BPCA are treated as priority applications, with all of the benefits that designation confers.

The Orphan Drug Act of 1983

The Orphan Drug Act of 1983 was designed to provide financial incentives for, and to reduce the costs associated with, developing drugs for rare diseases and disorders. A “rare disease or disorder” is defined by the Orphan Drug Act of 1983 as affecting fewer than 200,000 Americans at the time of designation or one for which “there is no reasonable expectation that the cost of developing and making available in the United States…will be recovered from sales in the United States.” A sponsor must request that the FDA designate a drug currently under development for a “rare disease or condition” as an orphan drug, and if the FDA agrees that the drug and indication meet the criteria set forth in the Orphan Drug Act of 1983, certain financial and marketing incentives become available. As mentioned previously, we have received Orphan Drug designations for GBM and metastatic brain cancer.

Disclosure of Clinical Trial Information

Sponsors of clinical trials of FDA-regulated products, including drugs, are required to register and disclose certain clinical trial information. Information related to the product, patient population, phase of investigation, study sites and investigators and other aspects of the clinical trial is then made public as part of the registration. Sponsors are also obligated to discuss the results of their clinical trials after completion. Disclosure of the results of these trials can be delayed until the new product or new indication being studied has been approved. Competitors may use this publicly-available information to gain knowledge regarding the progress of development programs.

Regulation Outside of the United States

In addition to regulations in the United States, we will be subject to regulations of other countries governing any clinical trials and commercial sales and distribution of our product candidates. Whether or not we obtain FDA approval for a product, we must obtain approval by the comparable regulatory authorities of countries outside of the United States before we can commence clinical trials in such countries and approval of the regulators of such countries or economic areas, such as the European Union, before we may market products in those countries or areas. Certain countries outside of the United States have a process similar to the FDA’s that requires the submission of a clinical trial application (“CTA”) much like the IND prior to the commencement of human clinical trials. In the European Union, for example, a CTA must be submitted to each country’s national health authority and an independent ethics committee, much like the FDA and IRB, respectively. Once the CTA is approved in accordance with a country’s requirements, clinical trial development may proceed. The approval process and requirements governing the conduct of clinical trials, product licensing, pricing and reimbursement vary greatly from place to place, and the time may be longer or shorter than that required for FDA approval.

Under European Union regulatory systems, a company may submit marketing authorization applications either under a centralized or decentralized procedure. The centralized procedure, which is compulsory for medicines produced by biotechnology or those medicines intended to treat AIDS, cancer, neurodegenerative disorders or diabetes and is optional for those medicines which are highly innovative, provides for the grant of a single marketing authorization that is valid for all European Union member states. The decentralized procedure provides for mutual recognition of national approval decisions. Under this procedure, the holder of a national marketing authorization may submit an application to the remaining member states. Within ninety (90) days of receiving the applications and assessments report, each member state must decide whether to recognize approval. If a member state does not recognize the marketing authorization, the disputed points are eventually referred to the European Commission, whose decision is binding on all member states.

Anti-Kickback and False Claims Laws

In addition to FDA restrictions on marketing of pharmaceutical products, several other types of state and federal laws have been applied to restrict certain marketing practices in the pharmaceutical industry. These laws include, among others, anti-kickback statutes, false claims statutes and other statutes pertaining to healthcare fraud and abuse. The federal healthcare program anti-kickback statute prohibits, among other things, knowingly and willfully offering, paying, soliciting or receiving remuneration to induce, or in return for, purchasing, leasing, ordering or arranging for the purchase, lease or order of any healthcare item or service reimbursable under Medicare, Medicaid or other federally financed healthcare programs. The Patient Protection and Affordable Care Act, as amended by the Health Care and Education Affordability Reconciliation Act of 2010, collectively referred to as the Affordable Care Act amended the intent element of the federal anti-kickback statute so that a person or entity no longer needs to have actual knowledge of the statute or specific intent to violate it. This statute has been interpreted to apply to arrangements between pharmaceutical manufacturers on the one hand and prescribers, purchasers and formulary managers on the other. Although there are a number of statutory exceptions and regulatory safe harbors protecting certain common activities from prosecution or other regulatory sanctions, the exceptions and safe harbors are drawn narrowly, and practices that involve remuneration intended to induce prescribing, purchases or recommendations may be subject to scrutiny if they do not qualify for an exception or safe harbor.

Federal false claims laws prohibit any person or entity from, among other things, knowingly presenting, or causing to be presented, a false claim for payment to the federal government, or knowingly making, or causing to be made, a false statement to have a false claim paid. This includes claims made to programs where the federal government reimburses, such as Medicaid, as well as programs where the federal government is a direct purchaser, such as when it purchases off the Federal Supply Schedule. Pharmaceutical and other healthcare companies have been prosecuted under these laws for, among other things, allegedly inflating drug prices they report to pricing services, which in turn were used by the government to set Medicare and Medicaid reimbursement rates, and for allegedly providing free product to customers with the expectation that the customers would bill federal programs for the product. In addition, certain marketing practices, including off-label promotion, may also violate federal false claims laws. Additionally, Affordable Care Act amended the federal healthcare program anti-kickback statute such that a violation of that statute can serve as a basis for liability under certain federal false claims laws.

The majority of states also have statutes or regulations similar to the federal anti-kickback law and false claims laws, which apply to items and services reimbursed under Medicaid and other state programs, or, in several states, apply regardless of the payor.