SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

(X) ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2011 |

| or |

( ) TRANSITION REPORT PURSUANT TO SECTION 13 or 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from ______ to ______ |

| |

Commission file number 0-23863 |

| |

| PEOPLES FINANCIAL SERVICES CORP. |

| (Exact name of registrant as specified in its charter) |

| PENNSYLVANIA | 23-2391852 |

| (State of incorporation) | (IRS Employer Identification No.) |

| | |

| 82 FRANKLIN AVENUE, HALLSTEAD, PA | 18822 |

| (Address of principal executive offices) | (Zip code) |

| |

| (570) 879-2175 |

| (Registrant’s telephone number including area code) |

| |

Securities registered pursuant to Section 12(b) of the Act: |

| Title of each class | Name of each exchange on which registered |

| None | None |

| Securities registered pursuant to Section 12(g) of the Act: |

| COMMON STOCK, par value, $2.00 per share |

| (Title of Class) |

| |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes __ No X |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes__ No X |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months or for such shorter period that the registrant was required to file such reports, and (2) has been subject to such filing requirements for the past 90 days. Yes X No__ |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months or for such shorter period that the registrant was required to submit and post such files. Yes X No__ |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. X |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company as defined in Rule 12b-2 of the Exchange Act. |

| Large accelerated filer ____ | Accelerated filer X | Non-accelerated filer _____ | Smaller reporting company _____ |

Indicate by check mark whether the registrant is a shell company as defined in Rule 12b-2 of the Exchange Act. Yes __ No X |

State the aggregate market value of the voting common stock held by non-affiliates based on the closing sale price as of the last business day of the registrant’s most recently completed second fiscal quarter: $79,909,920 at June 30, 2011 |

Indicate the number of shares outstanding of the registrant’s common stock, as of the latest practicable date: 3,117,606 at February 29, 2012. |

DOCUMENTS INCORPORATED BY REFERENCE |

| Portions of the registrant’s 2012 Proxy Statement are incorporated by reference in Part III of this Annual Report. |

Page 1 of 102 Exhibit Index on Page 101 |

PEOPLES FINANCIAL SERVICES CORP. FORM 10-K For the Year Ended December 31, 2011 TABLE OF CONTENTS |

| | | Page |

| Part I | | Number |

| Item 1. | Business | 3 |

| Item 1A. | Risk Factors | 12 |

| Item 1B. | Unresolved Staff Comments | 15 |

| Item 2. | Properties | 15 |

| Item 3. | Legal Proceedings | 15 |

| Item 4. | Mine Safety Disclosures | 15 |

| | | |

| Part II | | |

| Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 15 |

| Item 6. | Selected Financial Data | 18 |

| Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 19 |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 52 |

| Item 8. | Financial Statements and Supplementary Data | 53 |

Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 97 |

| Item 9A. | Controls and Procedures | 97 |

| Item 9B. | Other Information | 100 |

| | | |

| Part III | | |

| Item 10. | Directors, Executive Officers and Corporate Governance | 100 |

| Item 11. | Executive Compensation | 100 |

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 100 |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 100 |

| Item 14. | Principal Accountant Fees and Services | 100 |

| | | |

| Part IV | | |

Item 15. | Exhibits and Financial Statement Schedules | 101 |

| SIGNATURES | | 102 |

| | | |

PART I.

Item 1. Business

General

Peoples Financial Services Corp., a bank holding company incorporated in 1986 under the laws of Pennsylvania, provides a full range of financial services through its wholly-owned subsidiaries: Peoples Neighborhood Bank (“Peoples Bank”), including its subsidiaries, Peoples Advisors, LLC, Peoples Financial Leasing, LLC and Peoples Investment Holdings, LLC; and Peoples Financial Capital Corporation (collectively, the “Company”). The Company is headquartered in Hallstead, Pennsylvania and services its retail and commercial customers through eleven full-service community banking offices located within the Lackawanna, Susquehanna and Wyoming counties of Northern Pennsylvania and Broome county of Southern New York.

On December 13, 2010, Peoples Bank converted its charter to a state non-member bank under the jurisdiction of the Pennsylvania Department of Banking (“PADOB”) and the Federal Deposit Insurance Corporation (“FDIC”). Peoples Bank’s primary product is loans to small- and medium-sized businesses. Other lending products include one-to-four family residential mortgages and consumer loans. Peoples Bank primarily funds its loans by offering open time deposits to commercial enterprises and individuals. Other deposit product offerings include certificates of deposits and various demand deposit accounts.

Peoples Advisors, LLC, a member managed limited liability company, provides investment advisory services to individuals and small businesses. Peoples Financial Leasing, LLC, provides employee leasing services to Peoples Bank. Peoples Investment Holdings, LLC, incorporated under the laws of Delaware, maintains and manages the collection and distribution of income from certain investments of Peoples Bank.

Peoples Financial Capital Corporation, incorporated under the laws of Delaware, maintains and manages the collection and distribution of income from certain investments of the Company.

Peoples Advisors, LLC; Peoples Financial Leasing, LLC; Peoples Investment Holdings, LLC; and Peoples Financial Capital Corporation did not meet the quantitative thresholds for required segment disclosure in conformity with accounting principles generally accepted in the United States of America (“GAAP”). Peoples Bank’s eleven community banking offices, all similar with respect to economic characteristics, share a majority of the following aggregation criteria: (i) products and services; (ii) operating processes; (iii) customer bases; (iv) delivery systems; and (v) regulatory oversight. Accordingly, they were aggregated into a single operating segment.

As of December 31, 2011, the Company had 132 full-time equivalent employees. The Company and Peoples Bank are not parties to any collective bargaining agreement and employee relations are considered to be good.

Market Areas

Peoples Bank’s principal market area consists of Susquehanna, Wyoming and Lackawanna Counties of northeastern Pennsylvania and Broome County in the southern tier of New York. In addition, parts of Wayne and Bradford Counties in Pennsylvania that border Susquehanna and Wyoming Counties are also considered part of the market area.

Specifically, Peoples Bank’s market area is situated between:

| · | the city of Binghamton, Broome County, New York, located to the north; |

| · | the city of Scranton, Lackawanna County, Pennsylvania, to the south; and |

| · | Wilkes-Barre, Luzerne County, Pennsylvania, to the southwest. |

Most recently, the production of natural gas from the Marcellus Shale formation located in the heart of Peoples Bank’s market area has begun to provide economic benefits to the communities served and as a result to Peoples Bank itself. Natural gas producers have already invested more than $4 billion in Pennsylvania in lease and land acquisition, new well drilling, infrastructure development and community partnerships, with an even greater investment expected in the future. The growth of Peoples Bank’s deposits, and to a lesser extent, loan portfolio, has been influenced by natural gas drilling activities.

Products and Services

Lending Activities

Peoples Bank provides a full range of retail and commercial lending products designed to meet the borrowing needs of consumers and small and medium sized businesses in its market areas. A significant amount of Peoples Bank’s loans are to customers located within the defined market area. Peoples Bank has no foreign loans or highly leveraged transaction loans, as defined by the FRB. Although Peoples Bank participates in loans originated by other banks, the majority of loans in the portfolio have been originated by itself.

Retail lending products include the following types of loans, among others: (i) residential real estate; (ii) automobiles; (iii) manufactured housing; (iv) personal; (v) student; (vi) home equity and (vii) credit card. Commercial lending products include the following types of loans, among others: (i) commercial real estate; (ii) working capital; (iii) equipment and other commercial needs; (iv) construction; (v) Small Business Administration and (vi) agricultural and mineral rights. The terms offered on a loan vary depending primarily on the type of loan and credit-worthiness of the borrower.

Payment risk is a function of the economic climate in which Peoples Bank’s lending activities are conducted. Economic downturns in the economy generally or in a particular sector could cause cash flow problems for customers and make loan payments more difficult. Peoples Bank attempts to minimize this risk by not being exposed to loan concentrations of a single customer or a group of customers, the loss of any one or more of whom would have a materially adverse effect on its financial condition. Interest rate risk (“IRR”) would occur if Peoples Bank were to make loans at fixed rates in an environment in which rates were subject to rise thereby preventing it from making loans at higher prevailing rates. Peoples Bank attempts to mitigate this risk by making adjustable rate commercial loans and by limiting repricing terms to five years or less for customers requiring fixed rate loans. Finally, collateral risk can occur if Peoples Bank’s position in collateral taken as security for loan repayment is not adequate. Peoples Bank minimizes collateral risk by avoiding loan concentrations to particular borrowers, by perfecting liens on collateral and by obtaining appraisals on property prior to extending loans. Peoples Bank attempt to mitigate its exposure to these and other types of risks by stratifying authorization requirements by loan size and complexity.

Deposit Activities

Peoples Bank’s primary source of funds is the cash flow provided by its financing activities, mainly deposit gathering. Other sources of funds are provided by investing activities, including principal and interest payments on loans and investment securities, and operating activities, primarily net income. Peoples Bank offers a variety of deposit accounts with a range of interest rates and terms, including, among others: (i) money market accounts; (ii) NOW accounts; (iii) savings accounts; (iv) certificates of deposit; (v) individual retirement accounts and (vi) demand deposit accounts. These deposits are primarily obtained from areas surrounding People Bank’s branch offices. Peoples Bank relies primarily on marketing, product innovation, technology, service and long-standing relationships with customers to attract and retain these deposits. Other deposit related services include: (i) remote deposit capture; (ii) automatic clearing house transactions; (iii) cash management services; (iv) automated teller machines; (v) point of sale transactions; (vi) safe deposit boxes; (vii) night depository services; (viii) direct deposit and (ix) official check services.

Wealth Management Services

Peoples Wealth Management, a division of Peoples Advisors, LLC, provides a comprehensive array of wealth management products and services to individuals, small businesses and nonprofit entities. These products and services include the following, among others: (i) investment portfolio management; (ii) estate planning; (iii) annuities; (iv) business succession planning; (v) insurances; (vi) education funding strategies and (vii) tax planning.

Competition

Peoples Bank competes primarily with commercial banks, thrift institutions and credit unions, many of which are substantially larger in terms of assets and available resources. Certain of these institutions have significantly higher lending limits than Peoples Bank and may provide various services for their customers that are not presently available at Peoples Bank. In addition, Peoples Bank experiences competition for deposits from mutual funds and security brokers, while consumer discount, mortgage and insurance companies compete for various types of loans. Credit unions, finance companies and mortgage companies enjoy certain competitive advantages over Peoples Bank as they are not subject to the same regulatory restrictions and taxations as commercial banks. Principal methods of competing for bank products, permitted nonbanking services and financial activities include price, nature of product, quality of service and convenience of location.

Peoples Bank’s most significant competitive advantage originates from its business philosophy which includes offering direct access to senior management and other officers and providing friendly, informed and courteous service, local and timely decision making, flexible and reasonable operating procedures and consistently applied credit policies. In addition, Peoples Bank’s success has been, and will continue to be, a result of its emphasis on community involvement and customer relationships. With consolidation continuing in the financial industry, and particularly in Peoples Bank’s market area, smaller community banks such as Peoples Bank are gaining opportunities and market share as larger institutions reduce their emphasis on or exit the markets.

Seasonality

Generally, the operations of Peoples Bank are not seasonal in nature. However, Peoples Bank’s business activities have been somewhat influenced by the recent increase in activities related to natural gas drilling in its market area,

Supervision and Regulation

The Company and its subsidiaries are extensively regulated under federal and state laws. Generally, these laws and regulations are intended to protect consumers, not shareholders. The following is a summary description of certain provisions of law that affect the regulation of bank holding companies and banks. This discussion is qualified in its entirety by reference to applicable laws and regulations. Changes in law and regulation may have a material effect on the business and prospects of the Company.

The Company is a bank holding company within the meaning of the Bank Holding Company Act of 1956, as amended, and is subject to regulation, supervision, and examination by the Federal Reserve Board (“FRB”). The Company is required to file annual and quarterly reports with the FRB and to provide the FRB with such additional information as the FRB may require. The FRB also conducts examinations of the Company.

With certain limited exceptions, the Company is required to obtain prior approval from the FRB before acquiring direct or indirect ownership or control of more than 5% of any voting securities or substantially all of the assets of a bank or bank holding company, or before merging or consolidating with another bank holding company. Additionally, with certain exceptions, any person or entity proposing to acquire control through direct or indirect ownership of 25% or more of any voting securities of the Company is required to give 60 days written notice of the acquisition to the FRB, which may prohibit the transaction, and to publish notice to the public.

The Company’s banking subsidiary is regulated by the PADOB and the FDIC. The PADOB may prohibit an institution over which it has supervisory authority from engaging in activities or investments that the agency believes constitute unsafe or unsound banking practices. Federal banking regulators have extensive enforcement authority over the institutions they regulate to prohibit or correct activities that violate law, regulation or a regulatory agreement or which are deemed to constitute unsafe or unsound practices.

Enforcement actions may include:

| · | the appointment of a conservator or receiver; |

| · | the issuance of a cease and desist order; |

| · | the termination of deposit insurance, the imposition of civil money penalties on the institution, its directors, officers, employees and institution affiliated parties; |

| · | the issuance of directives to increase capital; |

| · | the issuance of formal and informal agreements; |

| · | the removal of or restrictions on directors, officers, employees and institution-affiliated parties; and |

| · | the enforcement of any such mechanisms through restraining orders or any other court actions. |

The Company is subject to the jurisdiction of the United States Securities and Exchange Commission (“SEC”) for matters relating to the offering and sale of securities. The Company is also subject to the SEC’s rules and regulations relating to periodic reporting, insider trading and proxy solicitation materials.

Limitations on Dividends and Other Payments

The Company’s current ability to pay dividends is largely dependent upon the receipt of dividends from Peoples Bank. Both federal and state laws impose restrictions on the ability of the Company and Peoples Bank to pay dividends. Under such restrictions, Peoples Bank may not, without prior approval, declare dividends in excess of the sum of its net profit for that year combined with its retained net profits of the preceding two calendar years. In addition to these specific restrictions, bank regulatory agencies, in general, also have the ability to prohibit proposed dividends by a financial institution that would otherwise be permitted under applicable regulations if the regulatory body determines that such distribution would constitute an unsafe or unsound practice.

Permitted Non-Banking Activities

Generally, a bank holding company may not engage in any activities other than banking, managing, or controlling its bank and other authorized subsidiaries, and providing service to those subsidiaries. With prior approval of the FRB, the Company may acquire more than 5% of the assets or outstanding shares of a company engaging in non-bank activities determined by the FRB to be closely related to the business of banking or of managing or controlling banks. The FRB provides expedited procedures for expansion into approved categories of non-bank activities.

Subsidiary banks of a bank holding company are subject to certain quantitative and qualitative restrictions: (i) on extensions of credit to the bank holding company or its subsidiaries; and (ii) on the use of their securities as collateral for loans to any borrower. These regulations and restrictions may limit the Company’s ability to obtain funds from Peoples Bank for its cash needs, including funds for the payment of dividends, interest and operating expenses. Further, subject to certain exceptions, a bank holding company and its subsidiaries are prohibited from engaging in certain tie-in arrangements in connection with any extension of credit, lease or sale of property or furnishing of services.

Under FRB policy, a bank holding company is expected to act as a source of financial strength to its subsidiary banks and to make capital injections into a troubled subsidiary bank, and the FRB may charge the bank holding company with engaging in unsafe and unsound practices for failure to commit resources to a subsidiary bank when required. A required capital injection may be called for at a time when the holding company does not have the resources to provide it. In addition, depository institutions insured by the FDIC can be held liable for any losses incurred by, or reasonably anticipated to be incurred by, the FDIC in connection with the default of or assistance provided to, a commonly controlled FDIC-insured depository institution. Accordingly, in the event that any insured subsidiary of a bank holding company causes a loss to the FDIC, other insured subsidiaries of a bank holding company could be required to compensate the FDIC by reimbursing it for the estimated amount of such loss. Such cross guarantee liabilities generally are superior in priority to the obligation of the depository institutions to its stockholders due solely to their status as stockholders and obligations to other affiliates.

Pennsylvania Law

As a Pennsylvania bank holding company, the Company is subject to various restrictions on its activities as set forth in Pennsylvania law. This is in addition to those restrictions set forth in federal law. Under Pennsylvania law, a bank holding company that desires to acquire a bank or bank holding company that has its principal place of business in Pennsylvania must obtain permission from the PADOB.

Interstate Banking Legislation

The Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994 provides that, among other things, substantially all state law barriers to the acquisition of banks by out-of-state bank holding companies were eliminated. The law also permits interstate branching by banks, subject to the ability of states to opt-out completely or to set an earlier effective date.

Financial Institution Reform, Recovery, and Enforcement Act (“FIRREA”)

FIRREA was enacted into law in order to address the financial condition of the Federal Savings and Loan Insurance Corporation, to restructure the regulation of the thrift industry, and to enhance the supervisory and enforcement powers of the federal bank and thrift regulatory agencies. As the primary federal regulator of Peoples Bank, the FDIC, in conjunction with the State is responsible its supervision. When dealing with capital requirements, those regulatory bodies have the flexibility to impose supervisory agreements on institutions that fail to comply with regulatory requirements. The imposition of a capital plan, termination of deposit insurance, and removal or temporary suspension of an officer, director or other institution-affiliated person may cause enforcement actions.

There are three levels of civil penalties under FIRREA.

| · | The first tier provides for civil penalties of up to $5 thousand per day for any violation of law or regulation |

| · | The second tier provides for civil penalties of up to $25 thousand per day if more than a minimal loss or a pattern is involved. |

| · | Finally, civil penalties of up to $1 million per day may be assessed for knowingly or recklessly causing a substantial loss to an institution or taking action that results in a substantial pecuniary gain or other benefit. |

Criminal penalties are increased to $1 million per violation and may be up to $5 million for continuing violations or for the actual amount of gain or loss. These penalties may be combined with prison sentences of up to five years.

Federal Deposit Insurance Corporation Improvement Act of 1991 (“FDICIA”)

FDICIA provides for, among other things:

| · | publicly available annual financial condition and management reports for financial institutions, including audits by independent accountants; |

| · | the establishment of uniform accounting standards by federal banking agencies; |

| · | the establishment of a “prompt corrective action” system of regulatory supervision and intervention, based on capitalization levels, with more scrutiny and restrictions placed on depository institutions with lower levels of capital; |

| · | additional grounds for the appointment of a conservator or receiver; and |

| · | restrictions or prohibitions on accepting brokered deposits, except for institutions which significantly exceed minimum capital requirements. |

FDICIA also provides for increased funding of the FDIC insurance funds and the implementation of risk-based premiums.

A central feature of FDICIA is the requirement that the federal banking agencies take “prompt corrective action” with respect to depository institutions that do not meet minimum capital requirements. Pursuant to FDICIA, the federal bank regulatory authorities have adopted regulations setting forth a five-tiered system for measuring the capital adequacy of the depository institutions that they supervise. Under these regulations, a depository institution is classified in one of the following capital categories:

| · | "adequately capitalized"; |

| · | "significantly undercapitalized"; and |

| · | "critically undercapitalized". |

FDICIA generally prohibits a depository institution from making any capital distribution including payment of a cash dividend or paying any management fees to its holding company, if the depository institution would thereafter be undercapitalized. Undercapitalized depository institutions are subject to growth limitations and are required to submit capital restoration plans. If a depository fails to submit an acceptable plan, it is treated as if it is “significantly undercapitalized”. Significantly undercapitalized depository institutions may be subject to a number of other requirements and restrictions, including orders to sell sufficient voting stock to become adequately capitalized, requirements to reduce total assets and stop accepting deposits from correspondent banks. Critically undercapitalized institutions are subject to the appointment of a receiver or conservator; generally within 90 days of the date such institution is determined to be critically undercapitalized.

FDICIA provides the federal banking agencies with significantly expanded powers to take enforcement action against institutions that fail to comply with capital or other standards. Such actions may include the termination of deposit insurance by the FDIC or the appointment of a receiver or conservator for the institution. FDICIA also limits the circumstances under which the FDIC is permitted to provide financial assistance to an insured institution before appointment of a conservator or receiver.

Under FDICIA, each federal banking agency is required to prescribe, by regulation, non-capital safety and soundness standards for institutions under its authority. The federal banking agencies, including the FDIC, have adopted standards covering:

| · | information systems and internal audit systems; |

| · | interest rate exposure; |

| · | compensation fees and benefits. |

Any institution that fails to meet these standards may be required to develop an acceptable plan, specifying the steps that the institutions will take to meet the standards. Failure to submit or implement such a plan may subject the institution to regulatory sanctions. The Company believes that it meets substantially all the standards that have been adopted. FDICIA also imposed new capital standards on insured depository institutions. Before establishing new branch offices, Peoples Bank must meet certain minimum capital stock and surplus requirements and must obtain State approval.

Risk-Based Capital Requirements

The federal banking regulators have adopted certain risk-based capital guidelines to assist in the assessing capital adequacy of a banking organization’s operations for both transactions reported on the balance sheet as assets and transactions, such as letters of credit, and recourse agreements, which are recorded as off-balance sheet items. Under these guidelines, nominal dollar amounts of assets and credit-equivalent amounts of off-balance sheet items are multiplied by one of several risk adjustment percentages, which range from 0% for assets with low credit risk, such as certain US Treasury securities, to 100% for assets with relatively high credit risk, such as business loans.

A banking organization’s risk-based capital ratios are obtained by dividing its qualifying capital by its total risk adjusted assets. The regulators measure risk-adjusted assets, which include off-balance-sheet items, against both total qualifying capital, the sum of Tier 1 capital and limited amounts of Tier 2 capital, and Tier 1 capital.

| · | "Tier 1", or core capital, includes common equity, perpetual preferred stock and minority interest in equity accounts of consolidated subsidiaries, less goodwill and other intangibles, subject to certain exceptions. |

| · | "Tier 2", or supplementary capital, includes, among other things, limited life preferred stock, hybrid capital instruments, mandatory convertible securities, qualifying subordinated debt, and the allowance for loan and lease losses, subject to certain limitations and less restricted deductions. The inclusion of elements of Tier 2 capital is subject to certain other requirements and limitations of the federal banking agencies. |

Banks and bank holding companies subject to the risk-based capital guidelines are required to maintain a ratio of Tier 1 capital to risk-weighted assets of at least 4% and a ratio of total capital to risk-weighted assets of at least 8%. The appropriate regulatory authority may set higher capital requirements when particular circumstances warrant. As of December 31, 2011, At December 31, 2011. The Company met both requirements with Tier 1 and Total capital ratios of 11.57% and 12.69%. In addition to risk-based capital, banks and bank holding companies are required to maintain a minimum amount of Tier 1 capital to total assets, referred to as the leverage capital ratio, of at least 4.00%. At December 31, 2011, the Company’s leverage ratio was 9.42%.

Failure to meet applicable capital guidelines could subject a banking organization to a variety of enforcement actions including:

| · | limitations on its ability to pay dividends; |

| · | the issuance by the applicable regulatory authority of a capital directive to increase capital, and in the case of depository institutions, the termination of deposit insurance by the FDIC, as well as to the measures described under FDICIA as applicable to undercapitalized institutions. |

In addition, future changes in regulations or practices could further reduce the amount of capital recognized for purposes of capital adequacy. Such a change could affect the ability of Peoples Bank to grow and could restrict the amount of profits, if any, available for the payment of dividends to the Company.

Interest Rate Risk

Regulatory agencies include, in their evaluations of a bank’s capital adequacy, an assessment of the bank’s IRR exposure. The standards for measuring the adequacy and effectiveness of a banking organization’s IRR management includes a measurement of Board of Directors and senior management oversight, and a determination of whether a banking organization’s procedures for comprehensive risk management are appropriate to the circumstances of the specific banking organization. Peoples Bank utilizes internal IRR models to measure and monitor IRR. In addition, Peoples Bank employs an independent consultant to provide a quarterly assessment of its IRR. Finally, regulatory agencies, as part of the scope of their periodic examinations, evaluate Peoples Bank’s IRR management. For these reasons, the Company does not expect the IRR evaluation in the agencies’ capital guidelines to result in significant changes in its capital requirements.

FDIC Insurance Assessments

As a FDIC member institution, Peoples Bank’s deposits are insured to a maximum of $250 thousand per depositor through the Bank Insurance Fund (“BIF”) that is administered by the FDIC and each institution is required to pay deposit insurance premium assessments to the FDIC. The Deposit Insurance Funds Act of 1996 recapitalized the Savings Association Insurance Fund (“SAIF”) and provided that BIF deposits would be subject to one-fifth of the assessment to which SAIF deposits are subject for FICO bond payments. Beginning in 2000, BIF deposits and SAIF deposits were subject to the same assessment for FICO bonds. The FICO assessment for Peoples Bank for 2011 was $0.0084 for each $100 of BIF deposits.

The FDIC adopted a risk-based deposit insurance assessment system that required all FDIC-insured institutions to pay quarterly premiums beginning in 2007. The Bank paid insurance premiums at levels stated for well-capitalized banks. The FDIC assessment for Peoples Bank for 2011 was $0.11 for each $100 of BIF deposits. Most recent assessment information from the FDIC indicate that annual premiums will range from 5 and 9 basis points of average total assets less average tangible equity for Risk Category 1 banks with the highest examination ratings to 35 basis points for Risk Category 4 banks with the lowest examination ratings. The Company anticipates being assessed deposit insurance premiums of between 5 and 9 basis points.

On November 12, 2009, the FDIC adopted a final rule that required all insured depository institutions to prepay their estimated quarterly risk-based assessments for the fourth quarter of 2009 and for all of 2010, 2011 and 2012. The FDIC also adopted a uniform increase in assessment rates of $0.03 per $100 of assessable deposits effective on January 1, 2011. The remaining prepaid assessment was $929 thousand at December 31, 2011.

Community Reinvestment Act

The Community Reinvestment Act of 1977, (“CRA”) is designed to create a system for bank regulatory agencies to evaluate a depository institution’s record in meeting the credit needs of its community. The CRA regulations were completely revised as of July 1, 1995, to establish performance-based standards for use in examining for compliance. The Bank had its last CRA compliance examination in 2008 and received a “satisfactory” rating.

USA Patriot Act of 2001

The Patriot Act contains anti-money laundering and financial transparency laws and imposes various regulations, including standards for verifying client identification at account opening, and rules to promote cooperation among financial institutions, regulators and law enforcement entities in identifying parties that may be involved in terrorism or money laundering.

Sarbanes-Oxley Act of 2002

The goals of the Sarbanes-Oxley Act (“SOX”) are to increase corporate responsibility, to provide for enhanced penalties for accounting and auditing improprieties at publicly traded companies and to protect investors by improving the accuracy and reliability of corporate disclosures pursuant to the securities laws.

Regulation W

Certain transactions, including loans and credit extensions, between the Company and its affiliates and subsidiaries are subject to quantitative and qualitative limitations, collateral requirements, and other restrictions imposed by statute and FRB regulation. Transactions subject to these restrictions are generally required to be made on an arms-length basis. These restrictions generally do not apply to transactions between the Company and its direct wholly-owned subsidiaries.

Overdraft Fee Regulation

On November 12, 2009, the FRB issued a final rule amending Regulation E, Electronic Funds Transfers. Effective July 1, 2010, banks may not charge fees for paying overdrafts on ATM and debit card transactions unless the customer gives consent, or opts in, to the payment of overdrafts for these transactions. Additional federal legislation has been introduced which would limit the number and amount of overdraft fees which banks can charge, prohibit ordering the posting transactions to cause customers to incur higher fees, prohibit insufficient funds fees on ATM or debit card transactions and require banks to provide a customer notice and opportunity to cancel transactions that would trigger an overdraft.

Dodd-Frank Act

On July 21, 2010, the Dodd-Frank Act became law. The Dodd-Frank Act has had a broad impact on the financial services industry, including significant regulatory and compliance changes.

The Dodd-Frank Act makes permanent the $250 thousand deposit insurance limit for insured deposits. Amendments to the FDICIA also revise the assessment base against which an insured depository institution’s deposit insurance premiums paid to the FDIC’s Deposit Insurance Fund (“DIF”) will be calculated. Under the amendments, the FDIC assessment base will no longer be the institution’s deposit base, but rather its average consolidated total assets less its average equity. The Dodd-Frank Act also changes the minimum designated reserve ratio of the DIF, increasing the minimum from 1.15% to 1.35% of the estimated amount of total insured deposits, and eliminating the requirement that the FDIC pay dividends to depository institutions to ensure that the DIF will reach 1.35% by September 30, 2020. Several of these provisions may increase the FDIC deposit insurance premiums Peoples Bank pays.

The Dodd-Frank Act also provided that, effective one year after the date of its enactment; depository institutions could begin to pay interest on commercial demand deposits. This change in regulations has had little impact on the Company.

The Dodd-Frank Act addresses many corporate governance and executive compensation matters that will affect most U.S. publicly traded companies, including the Company. The Dodd-Frank Act: grants shareholders of U.S. publicly traded companies an advisory vote on executive compensation and requires companies listed on national securities exchanges to adopt clawback policies for incentive-based compensation plans applicable to executive officers.

Many of the requirements the Dodd-Frank Act authorized will be implemented over time. The Company continues to assess the impact of the changes. Given the uncertainty associated with the timing and the manner in which the requirements will be implemented, the full extent of impact is unclear. These changes may require the Company to invest significant management attention and resources to make any necessary changes to comply with the requirements. While the Company cannot predict the final impact, its present assessment of the changes indicates that it will not have a material effect.

Item 1A. Risk Factors

Changes in interest rates could reduce income, cash flows and asset values.

The Company’s income and cash flows and the value of assets depend to a great extent on the difference between the interest rates earned on interest-earning assets, such as loans and investment securities, and the interest rates paid on interest-bearing liabilities such as deposits and borrowings. These rates are highly sensitive to many factors which are beyond the Company’s control, including general economic conditions and policies of various governmental and regulatory agencies and, in particular, the FRB. Changes in monetary policy, including changes in interest rates, will influence not only the interest received on loans and investment securities and the amount of interest paid on deposits and borrowings, but will also affect the Company’s ability to originate loans and obtain deposits and the value of its investment portfolio. If the rate of interest paid on deposits and other borrowings increases more than the rate of interest earned on loans and other investments, net interest income, and therefore earnings, could be adversely affected. The Company’s earnings also could be adversely affected if the rates on its loans and other investments fall more quickly than those on its deposits and other borrowings.

Economic conditions either nationally or locally in areas in which the Company’s operations are concentrated may adversely affect its business.

Deterioration in local, regional, national or global economic conditions could cause the Company to experience a reduction in deposits and new loans, an increase in the number of borrowers who default on their loans and a reduction in the value of the collateral securing their loans, all of which could adversely affect performance and financial condition. Unlike larger banks that are more geographically diversified, the Company provides banking and financial services locally. Therefore, it is particularly vulnerable to adverse local economic conditions.

The financial condition and results of operations would be adversely affected if the allowance for loan losses is not sufficient to absorb actual losses or if the Company is required to increase its allowance.

Despite the Company’s underwriting criteria, it may experience loan delinquencies and losses. In order to absorb losses associated with nonperforming loans, the Company maintains an allowance for loan losses based on, among other things, historical experience, an evaluation of economic conditions, and regular reviews of delinquencies and loan portfolio quality. Determination of the allowance inherently involves a high degree of subjectivity and requires the Company to make significant estimates of current credit risks and future trends, all of which may undergo material changes. At any time, there are likely to be loans in the portfolio that will result in losses but that have not been identified as nonperforming or potential problem credits. The Company cannot be sure that it will be able to identify deteriorating credits before they become nonperforming assets or that it will be able to limit losses on those loans that are identified. The Company may be required to increase its allowance for loan losses for any of several reasons. Regulators, in reviewing the loan portfolio as part of a regulatory examination, may request that the Company increase its allowance for loan losses. Changes in economic conditions affects borrowers, new information regarding existing loans, identification of additional problem loans and other factors, both within and outside of the Company’s control, may require an increase in its allowance. In addition, if charge-offs in future periods exceed the allowance for loan losses; the Company will need additional increases in its allowance for loan losses. Any increase in the allowance for loan losses will result in a decrease in net income and capital and may materially affect the results of operations in the period in which the allowance is increased.

Competition may decrease growth or profits.

The Company faces substantial competition in all phases of its operations from a variety of different competitors, including commercial banks, credit unions, consumer finance companies, insurance companies and money market funds. There is very strong competition among financial services providers in the Company’s principal service area. Competitors may have greater resources, higher lending limits or larger branch systems than does the Company. Accordingly, they may be able to offer a broader range of products and services as well as better pricing for those products and services than the Company can. In addition, some of the financial services organizations with which the Company competes are not subject to the same degree of regulation as is imposed on federally insured financial institutions. As a result, those non-bank competitors may be able to access funding and provide various services more easily or at less cost than the Company, adversely affecting its ability to compete effectively.

The Company may be adversely affected by government regulation.

The banking industry is heavily regulated. Banking regulations are primarily intended to protect the federal deposit insurance funds and consumers, not shareholders. Changes in the laws, regulations, and regulatory practices affecting the banking industry may increase the Company’s cost of doing business or otherwise adversely affect it and create competitive advantages for others. Regulations affecting banks and financial services companies undergo continuous change, and the Company cannot predict the ultimate effect of these changes, which could have a material adverse effect on its profitability or financial condition.

The Company relies on its management and other key personnel, and the loss of any of them may adversely affect its operations.

The Company is, and will continue to be, dependent upon the services of its management team. The unexpected loss of services of any key management personnel could have an adverse effect on its business and financial condition because of their skills, knowledge of the Company’s market, years of industry experience and the difficulty of promptly finding qualified replacement personnel.

Environmental liability associated with lending activities could result in losses.

In the course of normal business, the Company may foreclose on and take title to properties securing its loans. If hazardous substances were discovered on any of these properties, it could be liable to governmental entities or third parties for the costs of remediation of the hazard, as well as for personal injury and property damage. Many environmental laws can impose liability regardless of whether the Company knew of, or were responsible for, the contamination. In addition, if the Company arranges for the disposal of hazardous or toxic substances at another site, it may be liable for the costs of cleaning up and removing those substances from the site even if it neither owns nor operates the disposal site. Environmental laws may require it to incur substantial expenses and may materially limit use of properties the Company acquires through foreclosure, reduce their value or limit its ability to sell them in the event of a default on the loans they secure. In addition, future laws or more stringent interpretations or enforcement policies with respect to existing laws may increase its exposure to environmental liability.

Failure to implement new technologies in operations may adversely affect growth or profits.

The market for financial services, including banking services and consumer finance services, is increasingly affected by advances in technology, including developments in telecommunications, data processing, computers, automation, internet-based banking and telebanking. The Company’s ability to compete successfully in its markets may depend on the extent to which it is able to exploit such technological changes. However, the Company can provide no assurance that it will be able to properly or timely anticipate or implement such technologies or properly train its staff to use such technologies. Any failure to adapt to new technologies could adversely affect its business, financial condition or operating results.

An investment in the Company’s common stock is not an insured deposit. The Company’s stock price is subject to market forces that could have an adverse affect to its stocks market value.

The Company’s common stock is not a bank deposit and, therefore, is not insured against loss by the FDIC, or any other deposit insurance fund or by any other public or private entity. Investment in the Company’s common stock is subject to the same market forces that affect the price of common stock in any company.

The Company’s legal lending limits are relatively low and this may restrict its ability to compete for larger customers.

At December 31, 2011, the Company’s lending limit per borrower was approximately $8.5 million or approximately 15% of its unimpaired capital. Accordingly, the size of loans that the Company can offer to potential borrowers, without participation by other lenders, is less than the size of loans that many of its competitors with larger capitalization are able to offer. The Company’s legal lending limit also impacts the efficiency of its lending operation because it tends to lower its average loan size, which means it has to generate a higher number of transactions to achieve the same portfolio volume. The Company may engage in loan participations with other banks for loans in excess of its legal lending limits. However, there can be no assurance that such participations will be available at all or on terms which are favorable to the Company and its customers.

The Company’s information systems may experience an interruption or breach in security.

The Company relies heavily on communications and information systems to conduct its business. Any failure, interruption or breach in security of these systems could result in failures or disruptions in the Company’s customer relationship management, general ledger, deposit, loan and other systems. Although the Company has policies and procedures designed to prevent or limit the effect of the failure, interruption or security breach of these information systems, there can be no assurance that any such failures, interruptions or security breaches will not occur or, if they do occur, that they will be adequately addressed. The occurrence of any failures, interruptions or security breaches of the Company’s information systems could damage its reputation, result in a loss of customer business, subject it to additional regulatory scrutiny, or expose it to civil litigation and possible financial liability, any of which could have a material adverse effect on the Company’s financial condition and results of operations.

Rapid growth could require the Company to raise additional capital.

The Company is required by federal and state regulatory authorities to maintain adequate levels of capital to support its operations. As a financial holding company, the Company seeks to maintain capital sufficient to meet the “well-capitalized” standard set by regulators. The Company anticipates that its current capital resources will satisfy its capital requirements for the foreseeable future. The Company may at some point, however, need to raise additional capital to support continued growth, whether such growth occurs internally or through acquisitions. The Company’s ability to raise additional capital, if needed, will depend on conditions in the capital markets at that time, which are outside of the Company’s control, and on the Company’s financial performance. Accordingly, there can be no assurance of the Company’s ability to expand its operations through internal growth and acquisitions could be materially impaired. As such, the Company may be forced to delay raising capital, issue shorter term securities than desired or bear an unattractive cost of capital, which could decrease profitability and significantly reduce financial flexibility. In the event current sources of liquidity, including internal sources, do not satisfy the Company’s needs, the Company would be required to seek additional financing. The availability of additional financing will depend on a variety of factors such as market conditions, the general availability of credit, the overall availability of credit to the financial services industry, the Company’s credit ratings and credit capacity, as well as the possibility that lenders could develop a negative perception of the Company’s long- or short-term financial prospects if the Company incurs large credit losses or if the level of business activity decreases due to economic conditions.

Market conditions may adversely affect fee based investment business.

The Company receives fee based revenues from commissions on the sale of securities and investment advisory fees. In the event of decreased stock market activity, the volume of trading executed by its Wealth Management subsidiary will in all likelihood decrease resulting in decreased commission revenue on purchases and sales of securities. In addition, investment advisory fees, which are generally based on a percentage of the total value of an investment portfolio, will decrease in the event of decreases in the values of the investment portfolios as a result of overall market declines.

Available Information

The Company files reports, proxy and information statements and other information electronically with the SEC. You may read and copy any materials that the Company files with the SEC at the SEC’s Public Reference Room located at 100 F. Street, N.E., Washington, DC 20549 on official business days between the hours of 10:00am and 3:00pm EST. You can obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site that contains reports, proxy and information statements and other information regarding issuers that file electronically. The SEC’s website address is http://www.sec.gov. Copies of the Company’s Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed with the SEC may be obtained without charge by writing to Peoples Financial Services Corp., 82 Franklin Avenue, Hallstead, PA 18822, Attn: Investor Relations or through the Company’s website at http://www.peoplesnatbank.com.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

The Company’s corporate headquarters is located at 82 Franklin Avenue, Hallstead, Susquehanna County, Pennsylvania. The Company owns the facility which has approximately 9,800 square feet.

In addition to the above location, at December 31, 2011, the Company owned 10 and leased one retail community banking offices. The Company also owns an office building located at 241 Main Street, Hallstead, Susquehanna County, Pennsylvania, which serves as its Bank Secrecy Act facility. The Company considers its properties to be suitable and adequate for its current and immediate future purposes.

Item 3. Legal Proceedings

The Company, Peoples Bank and their subsidiaries are not parties to any legal proceedings that could have a material effect on the financial condition or operating results of the Company. In addition, the Company, Peoples Bank and their subsidiaries are not parties to any legal proceedings under federal and state environmental laws.

Item 4. Mine Safety Disclosures

Not Applicable

PART II.

Item 5. Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

The Company had 1,077 stockholders of record, including individual participants in security position listings, and 3,117,606 shares of common stock, par value of $2.00 per share, the only authorized class of stock outstanding as of February 29, 2012. The Company’s common stock trades on the Over-the-Counter-Bulletin-Board under the symbol “PFIS.” The Company has paid cash dividends since its incorporation in 1986. The payment of future dividends must necessarily depend upon earnings, financial position, appropriate restrictions under applicable laws and other factors relevant at the time the Board of Directors considers any declaration of dividends. For information on dividend restrictions on the Company and Peoples Bank, refer to the consolidated financial statements and notes to these statements filed at Item 8 to this report and incorporated in their entirety by reference under this Item 5.

The high and low closing sale prices and dividends per share of the Company’s common stock for the four quarters of 2011 and 2010 are summarized in the following table:

| | | 2011 | | | 2010 | |

| | | Low | | | High | | | Dividends Declared | | | Low | | | High | | | Dividends Declared | |

| First Quarter | | $ | 26.31 | | | $ | 28.00 | | | $ | 0.20 | | | $ | 18.05 | | | $ | 22.75 | | | $ | 0.19 | |

| Second Quarter | | | 25.50 | | | | 27.50 | | | | 0.20 | | | | 21.65 | | | | 29.00 | | | | 0.20 | |

| Third Quarter | | | 26.90 | | | | 28.25 | | | | 0.20 | | | | 26.00 | | | | 28.00 | | | | 0.20 | |

| Fourth Quarter | | $ | 27.05 | | | $ | 28.25 | | | $ | 0.20 | | | $ | 26.60 | | | $ | 28.00 | | | $ | 0.20 | |

The following table discloses the number of outstanding options, warrants and rights granted by the Company to participants in equity compensation plans, as well as the number of securities remaining available for future issuance under these plans. Securities for future issuance are reserved and issued at the discretion of the Board of Directors on an annual basis. The table provides this information separately for equity compensation plans that have and have not been approved by security holders.

| | | Number of securities to be issued upon exercise of outstanding options, warrants and rights | | | Weighted-average exercise price of outstanding options, warrants and rights | | | Number of securities remaining available for future issuance under equity compensation plans | |

| Equity compensation plans approved | | | 13,399 | | | $ | 26.59 | | | | 35,451 | |

| Equity compensation plans not approved | | | | | | | | | | | | |

| Total | | | 13,399 | | | $ | 26.59 | | | | 35,451 | |

The following table presents information with respect to purchases made by or on behalf of the Company or any “affiliated purchaser,” as defined in the Exchange Act Rule 10b-18(a)(3), of the Company’s common stock during each of the three months ended December 31, 2011:

| Month Ending | | Total Number of Shares Purchased | | | Average Price Paid Per Share | | | Total Number of Shares Purchased as Part of Publicly Announced Programs(1) | | | Maximum Number of Shares that may yet be Purchased Under the Programs(1) | |

| October 31, 2011 | | | 8,000 | | | | 27.35 | | | | 8,000 | | | | 37,651 | |

| November 30, 2011 | | | | | | | | | | | | | | | 37,651 | |

| December 31, 2011 | | | 2,200 | | | | 27.80 | | | | 2,200 | | | | 35,451 | |

| Total | | | 10,200 | | | | 27.45 | | | | 10,200 | | | | | |

(1) On July 2, 2001, the Board of Directors authorized the purchase of 158,931 shares of the Company’s common stock. As of December 31, 2011, there were 35,451 shares available for repurchase under this Program. The 2001 Stock Repurchases Program has no expiration date.

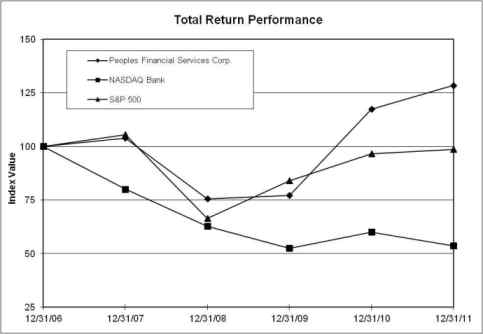

The following line graph compares the cumulative total stockholder return on the Company’s common stock, based on the market price change and assumes reinvestment of dividends, with the cumulative total return of the index for The NASDAQ Bank Stocks and the index for the Standards and Poor 500 Stocks during the five-year period ended December 31, 2011. The stockholder return shown on the graph and table below is not necessarily indicative of future performance.

Comparison of Five-Year Cumulative Total Returns

Performance Graph of

PEOPLES FINANCIAL SERVICES CORP.

| | | Period Ending | |

| Index | | 12/31/06 | | | 12/31/07 | | | 12/31/08 | | | 12/31/09 | | | 12/31/10 | | | 12/31/11 | |

| Peoples Financial Services Corp. | | $ | 100.00 | | | $ | 104.01 | | | $ | 75.66 | | | $ | 77.18 | | | $ | 117.50 | | | $ | 128.54 | |

| NASDAQ Bank | | | 100.00 | | | | 80.09 | | | | 62.84 | | | | 52.60 | | | | 60.04 | | | | 53.74 | |

| S&P 500 | | $ | 100.00 | | | $ | 105.49 | | | $ | 66.46 | | | $ | 84.05 | | | $ | 96.71 | | | $ | 98.76 | |

(Dollars in thousands, except per share data)

| Year Ended December 31 | | 2011 | | | 2010 | | | 2009 | | | 2008 | | | 2007 | |

| Condensed statements of financial performance: | | | | | | | | | | | | | | | |

| Interest income | | $ | 27,350 | | | $ | 25,577 | | | $ | 24,273 | | | $ | 25,479 | | | $ | 24,611 | |

| Interest expense | | | 5,639 | | | | 6,498 | | | | 7,258 | | | | 9,154 | | | | 11,105 | |

| Net interest income | | | 21,711 | | | | 19,079 | | | | 17,015 | | | | 16,325 | | | | 13,506 | |

| Provision for loan losses | | | 1,794 | | | | 2,202 | | | | 1,735 | | | | 713 | | | | 280 | |

| Net interest income after provision for loan losses | | | 19,917 | | | | 16,877 | | | | 15,280 | | | | 15,612 | | | | 13,226 | |

| Noninterest income (loss) | | | 5,567 | | | | 4,290 | | | | 3,082 | | | | (1,809 | ) | | | 3,308 | |

| Noninterest expense | | | 15,310 | | | | 13,245 | | | | 12,390 | | | | 10,677 | | | | 10,566 | |

| Income before income taxes | | | 10,174 | | | | 7,922 | | | | 5,972 | | | | 3,126 | | | | 5,968 | |

| Provision for income tax expense | | | 2,357 | | | | 1,437 | | | | 923 | | | | 87 | | | | 1,097 | |

| Net income | | $ | 7,817 | | | $ | 6,485 | | | $ | 5,049 | | | $ | 3,039 | | | $ | 4,871 | |

| | | | | | | | | | | | | | | | | | | | | |

| Condensed statements of financial position: | | | | | | | | | | | | | | | | | | | | |

| Investment securities | | $ | 139,899 | | | $ | 121,772 | | | $ | 130,506 | | | $ | 107,589 | | | $ | 109,471 | |

| Net loans | | | 439,754 | | | | 386,672 | | | | 332,196 | | | | 313,606 | | | | 288,524 | |

| Other assets | | | 41,751 | | | | 50,143 | | | | 53,781 | | | | 51,181 | | | | 36,439 | |

| Total assets | | $ | 621,404 | | | $ | 558,587 | | | $ | 516,483 | | | $ | 472,376 | | | $ | 434,434 | |

| | | | | | | | | | | | | | | | | | | | | |

| Deposits | | $ | 494,283 | | | $ | 438,734 | | | $ | 410,038 | | | $ | 371,268 | | | $ | 327,430 | |

| Short-term borrowings | | | 43,791 | | | | 38,724 | | | | 20,439 | | | | 18,432 | | | | 22,848 | |

| Long-term debt | | | 18,927 | | | | 27,336 | | | | 38,750 | | | | 39,691 | | | | 38,534 | |

| Other liabilities | | | 4,790 | | | | 3,277 | | | | 2,286 | | | | 3,265 | | | | 2,817 | |

| Stockholders’ equity | | | 59,613 | | | | 50,516 | | | | 44,970 | | | | 39,720 | | | | 42,805 | |

| Total liabilities and stockholders’ equity | | $ | 621,404 | | | $ | 558,587 | | | $ | 516,483 | | | $ | 472,376 | | | $ | 434,434 | |

| | | | | | | | | | | | | | | | | | | | | |

| Per share data: | | | | | | | | | | | | | | | | | | | | |

| Net income | | $ | 2.49 | | | $ | 2.07 | | | $ | 1.61 | | | $ | 0.97 | | | $ | 1.55 | |

| Cash dividends declared | | | 0.80 | | | | 0.79 | | | | 0.76 | | | | 0.76 | | | | 0.76 | |

| Stockholders’ equity | | $ | 19.11 | | | $ | 16.07 | | | $ | 14.34 | | | $ | 12.69 | | | $ | 13.64 | |

| Cash dividends declared as a percentage of net income | | | 32.28 | % | | | 38.24 | % | | | 47.15 | % | | | 79.53 | % | | | 48.92 | % |

| Average common shares outstanding | | | 3,136,663 | | | | 3,139,606 | | | | 3,133,518 | | | | 3,128,170 | | | | 3,135,889 | |

| | | | | | | | | | | | | | | | | | | | | |

| Selected ratios (based on average balances): | | | | | | | | | | | | | | | | | | | | |

| Net income as a percentage of total assets | | | 1.33 | % | | | 1.18 | % | | | 1.07 | % | | | 0.68 | % | | | 1.17 | % |

| Net income as a percentage of stockholders’ equity | | | 14.80 | | | | 13.87 | | | | 12.62 | | | | 7.53 | | | | 11.85 | |

| Stockholders’ equity as a percentage of total assets | | | 8.99 | | | | 8.53 | | | | 8.50 | | | | 9.01 | | | | 9.86 | |

| Tier I capital as a percentage of adjusted total assets | | | 9.42 | | | | 9.19 | | | | 9.92 | | | | 9.31 | | | | 10.14 | |

| Net interest income as a percentage of earning assets | | | 4.18 | | | | 4.00 | | | | 4.23 | | | | 4.25 | | | | 3.82 | |

| Loans, net, as a percentage of deposits | | | 89.70 | % | | | 84.67 | % | | | 87.33 | % | | | 86.38 | % | | | 86.13 | % |

| | | | | | | | | | | | | | | | | | | | | |

| Selected ratios and data (based on period end balances): | | | | | | | | | | | | | | | | | | | | |

| Tier I capital as a percentage of risk-weighted assets | | | 11.57 | % | | | 11.72 | % | | | 12.30 | % | | | 12.26 | % | | | 13.64 | % |

| Total capital as a percentage of risk-weighted assets | | | 12.69 | | | | 12.68 | | | | 13.18 | | | | 13.10 | | | | 14.42 | |

| Allowance for loan losses as a percentage of loans, net | | | 1.20 | | | | 1.05 | | | | 0.99 | | | | 0.95 | | | | 0.84 | |

| Nonperforming loans as a percentage of loans, net | | | 2.30 | % | | | 1.77 | % | | | 0.99 | % | | | 1.63 | % | | | 0.17 | % |

Note: Average balances were calculated using average daily balances. Average balances for loans include nonaccrual loans. Tax-equivalent adjustments were calculated using the prevailing statutory rate of 34.0 percent.

Peoples Financial Services Corp.

Item 7. Management’s Discussion and Analysis

(Dollars in thousands, except per share data)

Management’s Discussion and Analysis appearing on the following pages should be read in conjunction with the Consolidated Financial Statements contained in this Annual Report.

Forward-Looking Discussion:

This report on Form 10-K and the documents into which it may be incorporated by reference may contain and, from time to time, may make, certain statements that constitute forward-looking statements. Words such as “expects,” “anticipates,” “believes,” “estimates” and other similar expressions or future or conditional verbs such as “will,” “should,” “would” and “could” are intended to identify such forward-looking statements. These statements are not historical facts, but instead represent the current expectations, plans or forecasts of Peoples Financial Services Corp. and its subsidiaries regarding its future operating results, financial position, asset quality, credit reserves, credit losses, capital levels, dividends, liquidity, service charges, cost savings, effective tax rate, impact of changes in fair value of financial assets and liabilities, impact of new accounting and regulatory guidance, legal proceedings and other matters relating to us and the securities that we may offer from time to time. These statements are not guarantees of future results or performance and involve certain risks, uncertainties and assumptions that are difficult to predict, change over time and are often beyond our control. Actual outcomes and results may differ materially from those expressed in, or implied by, forward-looking statements.

You should not place undue reliance on any forward-looking statement and should consider the uncertainties and risks discussed in Part I Item 1A entitled “Risk Factors,” in this Annual Report, among others, and in any of our subsequent Securities and Exchange Commission (“SEC”) filings. Forward-looking statements speak only as of the date they are made, and we undertake no obligation to update any forward-looking statement to reflect the impact of circumstances or events that arise after the date the forward-looking statement was made. Notes to the Consolidated Financial Statements referred to in the Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) are incorporated by reference into the MD&A. Certain prior period amounts have been reclassified to conform with the current year’s presentation.

Critical Accounting Policies:

Our financial statements are prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”). The preparation of financial statements in conformity with GAAP requires us to establish critical accounting policies and make accounting estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements, as well as the reported amounts of revenues and expenses during those reporting periods.

For a discussion of the recent Accounting Standards Updates (“ASU”) issued by the Financial Accounting Standards Board (“FASB”) refer to Note 1 entitled “Summary of significant accounting policies — Recent accounting standards,” in the Notes to Consolidated Financial Statements to this Annual Report.

An accounting estimate requires assumptions about uncertain matters that could have a material effect on the financial statements if a different amount within a range of estimates were used or if estimates changed from period to period. Readers of this report should understand that estimates are made considering facts and circumstances at a point in time, and changes in those facts and circumstances could produce results that differ from when those estimates were made. Significant estimates that are particularly susceptible to material change within the near term relate to the determination of allowance for loan losses, the determination of other-than-temporary impairment, the fair value of financial instruments, the valuations of real estate acquired in connection with foreclosures or satisfaction of loans and the valuation of loans deferred tax assets and liabilities. Actual amounts could differ from those estimates.

We maintain the allowance for loan losses at a level we believe adequate to absorb probable credit losses related to individually evaluated loans, as well as probable incurred losses inherent in the remainder of the loan portfolio as of the balance sheet date. The balance in the allowance for loan losses account is based on past events and current economic conditions.

Peoples Financial Services Corp.

Management’s Discussion and Analysis

(Dollars in thousands, except per share data)

The allowance for loan losses account consists of an allocated element and an unallocated element. The allocated element consists of a specific portion for the impairment of loans individually evaluated and a formula portion for loss contingencies on those loans collectively evaluated. The unallocated element, if any, is used to cover inherent losses that exist as of the evaluation date, but which have not been identified as part of the allocated allowance using our impairment evaluation methodology due to limitations in the process.

We monitor the adequacy of the allocated portion of the allowance quarterly and adjusts the allowance for any deficiencies through normal operations. This ongoing evaluation reduces potential differences between estimates and actual observed losses. The determination of the level of the allowance for loan losses is inherently subjective as it requires estimates that are susceptible to significant revision as more information becomes available. Accordingly, management cannot ensure that charge-offs in future periods will not exceed the allowance for loan losses or that additional increases in the allowance for loan losses will not be required, resulting in an adverse impact on operating results.

In determining the requirement to record an other-than-temporary impairment on securities owned by us, four main characteristics are considered including: (i) the length of time and the extent to which the fair value has been less than amortized cost; (ii) the financial condition and near-term prospects of the issuer; (iii) whether the market decline was affected by macroeconomic conditions and (iv) whether the entity has the intent to sell the debt security or more likely than not will be required to sell the debt security before its anticipated recovery. The assessment of whether an other-than-temporary impairment exists involves a high degree of subjectivity and judgment and is based on information available to us at a point in time.

Fair values of financial instruments, in cases where quoted market prices are not available, are based on estimates using present value or other valuation techniques which are subject to change.

Real estate acquired in connection with foreclosures or in satisfaction of loans is adjusted to fair value based upon current estimates derived through independent appraisals less cost to sell. However, proceeds realized from sales may ultimately be higher or lower than those estimates.

Deferred tax assets and liabilities are recognized for the estimated future tax effects of temporary differences by applying enacted statutory tax rates to differences between the financial statement carrying amounts and the tax bases of existing assets and liabilities. The amount of deferred tax assets is reduced, if necessary, to the amount that, based on available evidence, will more likely than not be realized. As changes in tax laws or rates are enacted, deferred tax assets and liabilities are adjusted through the provision for income taxes.

For a further discussion of our critical accounting policies, refer to Note 1 entitled, “Summary of significant accounting policies,” in the Notes to Consolidated Financial Statements to this Annual Report. This note lists the significant accounting policies used by us in the development and presentation of the financial statements. This MD&A, the Notes to Consolidated Financial Statements and other financial statement disclosures identify and address key variables and other qualitative and quantitative factors that are necessary for the understanding and evaluation of our financial position, results of operations and cash flows.

Operating Environment:

The United States economy continued to expand moderately in 2011, as the gross domestic product (“GDP”), the value of all goods and services produced in the Nation, increased at an annual rate of 2.8 percent in the fourth quarter of 2011, compared to 1.8 percent in the third quarter of 2011. The fourth quarter increase reflected positive contributions from private inventory investment, personal consumption expenditures (“PCE”), exports, and residential and nonresidential fixed investment which were partially offset by negative impacts from federal, state and local government spending, and an increase in imported goods.

Peoples Financial Services Corp.

Management’s Discussion and Analysis

(Dollars in thousands, except per share data)

As a result of the tepid economic growth in 2011, the Federal Open Market Committee (“FOMC”) maintained the federal funds target range of 0 to 25 basis points throughout the year and further signaled that they intend to keep short-term rates at extraordinarily low levels through at least late 2014. Despite the apparent recovery in 2011, many areas of the economy such as employment conditions and the housing market remained weak. Given these weaknesses, the FOMC decided that this extraordinary monetary policy stance was necessary to support the recovery. At their most recent meeting in January, 2012, the FOMC indicated that economic conditions will continue to warrant policy accommodation for an extended period. The committee directed that the program of quantitative easing, which began in September 2011, be continued. The Federal Reserve will purchase an additional $400 billion in Treasury securities with remaining maturities of approximately 6 to 30 years and in turn sell $400 billion in Treasuries with remaining maturities of 3 years or less by the end of June 2012. This action should contribute to a flatter yield curve and keep long-term rates low, with the intention of spurring business investment.

The PCE increased 2.0 percent in the fourth quarter up from 1.7 percent in the third quarter of 2011. The main contributor to the growth in PCE was durable goods which increased 14.8 percent and 5.7 percent, respectively. Nonresidential fixed investment increased 1.7 percent in the fourth quarter of 2011 and 15.7 percent in the third quarter of 2011. Exports of goods and services were up 4.7 percent in the third and fourth quarters of 2011. In contrast to these increases, federal government consumption expenditures decreased 7.3 percent in the fourth quarter of 2011 while the third quarter reflected an increase of 2.1 percent. State and local governments scaled back consumption expenditures by 2.6 percent and 1.6 percent in the fourth and third quarters of 2011.

Employment conditions improved moderately in 2011. The civilian labor force increased 274 thousand, while the number of people employed increased 1.6 million for the same period. As a result, the unemployment rate for the Nation fell to 8.5 percent in December 2011 from 9.4 percent in December 2010. All sectors of employment, with the exception of the government sector, reported employment gains from the end of 2010.

National, Pennsylvania, New York and our market area’s seasonally-adjusted unemployment rates at December 31, 2011 and 2010, are summarized as follows:

| December 31 | | 2011 | | | 2010 | |

| United States | | | 8.5 | % | | | 9.4 | % |

| Pennsylvania | | | 7.2 | % | | | 8.1 | % |

| New York | | | 8.0 | % | | | 8.0 | % |

| Lackawanna County | | | 8.1 | % | | | 8.8 | % |

| Susquehanna County | | | 7.0 | % | | | 7.8 | % |

| Wyoming County | | | 8.2 | % | | | 9.9 | % |

| Broome County | | | 8.2 | % | | | 8.7 | % |

Employment conditions improved for the Commonwealth of Pennsylvania, as the unemployment rate fell to 7.2 percent by year-end 2011 from 8.1 percent at the end of 2010. The unemployment rate for New York State remained at 8.0 percent at year-end 2011 and 2010. With respect to the markets we serve, the unemployment rate decreased for all four counties in northeastern Pennsylvania and Broome County in the southern tier of New York. Jobs related to natural gas drilling and exploration in Susquehanna and Wyoming counties in Pennsylvania have contributed to the turnaround in the employment situation in those counties, as well as to the improving employment situation in the neighboring counties of Lackawanna, Pennsylvania and Broome, New York.

Peoples Financial Services Corp.

Management’s Discussion and Analysis

(Dollars in thousands, except per share data)