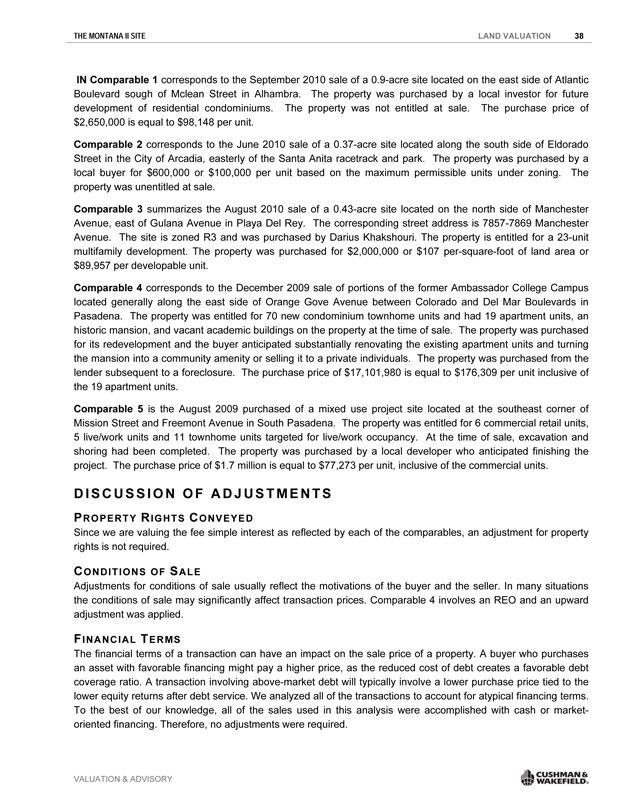

Exhibit (c)(9)

APPRAISAL OF REAL PROPERTY

The Montana II

380 Union Street Pasadena, Los Angeles County, CA 91101

Latitude: 34.146596 Longitude: -118.142479

IN A SELF-CONTAINED APPRAISAL REPORT

As of December 10, 2010

Prepared For:

Special Committee of the Board of Directors of Wesco Financial Corporation c/o

Skadden, Arps, Slate, Meagher & Flom LLP 300 South Grand Avenue, Suite 3200 Los Angeles, CA 90071

PHOTOGRAPH OF SUBJECT PROPERTY

Prepared By: Cushman & Wakefield Western, Inc.

Valuation & Advisory

601 South Figueroa Street, 47th Floor

Los Angeles, CA 90017-5752

C&W File ID: 10-38021-9027-3

CUSHMAN & WAKEFIELD® Global Real Estate Solution SM

As a matter of environmental responsibility. C&W has adopted a corporate-wide program to print our appraisal reports double-sided.

CUSHMAN & WAKEFIELD®

CUSHMAN & WAKEFIELD WESTERN, INC.

601 SOUTH FIGUEROA STREET, 47TH FLOOR

LOS ANGELES, CA 90017-5752

December 10, 2010

Special Committee of the Board of Directors of Wesco Financial Corporation c/o Brian McCarthy

Skadden, Arps, Slate, Meagher & Flom LLP

300 South Grand Avenue, Suite 3200 Los Angeles, CA 90071

Re: Appraisal of Real Property In a Self-Contained Report

The Montana II

380 Union Street Pasadena, Los Angeles County, CA 91101

C&W File ID: 10-38021-9027-3

Dear Mr. McCarthy:

In fulfillment of our agreement as outlined in the Letter of Engagement, we are pleased to transmit our appraisal presented in a self-contained report on the property referenced above. The date of the report is December 10, 2010. The effective date of value is December 10, 2010.

This report is addressed to Special Committee of the Board of Directors of Wesco Financial Corporation c/o Skadden, Arps, Slate, Meagher & Flom LLP and its affiliates. In conformance with your request, we have completed an appraisal of the above referenced property. The appraisal states our opinion of the property’s Market Value subject to various Assumptions and Limiting Conditions set forth in the accompanying report. The physical inspection and analysis that form the basis of the report have been conducted by Michele Kauffman and Michele Kauffman.

The accompanying report includes pertinent data secured in our investigation, exhibits and the details of the process used to arrive at our conclusion of value. The appraisal conforms to the Standards of Professional Practice and Code of Professional Ethics of Appraisal Institute, which incorporates the Uniform Standards of Professional Appraisal Practice (USPAP), of the Appraisal Foundation.

BRIAN MCCARTHY CUSHMAN & WAKEFIELD WESTERN, INC.

SKADDEN, ARPS, SLATE, MEAGHER & FLOM LLP DECEMBER 10, 2010 PAGE 2

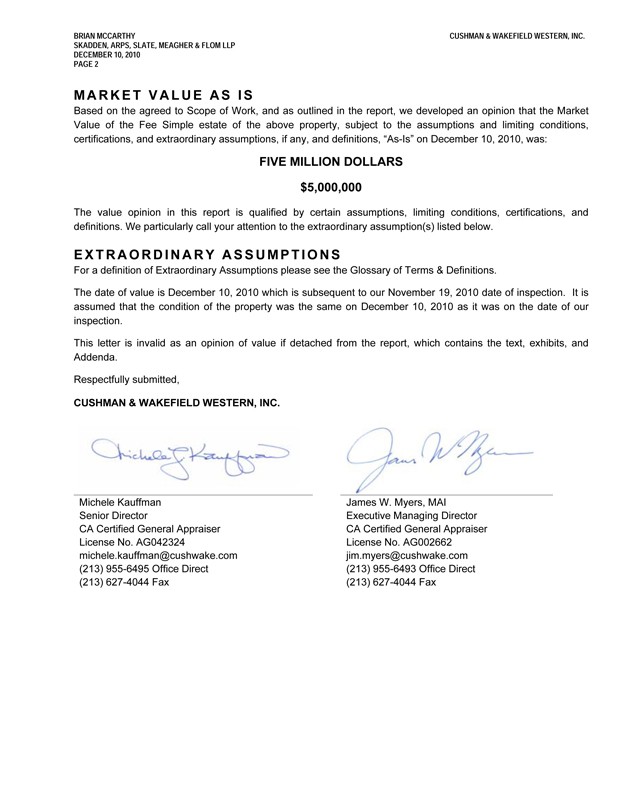

MARKET VALUE AS IS

Based on the agreed to Scope of Work, and as outlined in the report, we developed an opinion that the Market Value of the Fee Simple estate of the above property, subject to the assumptions and limiting conditions, certifications, and extraordinary assumptions, if any, and definitions, “As-Is” on December 10, 2010, was:

FIVE MILLION DOLLARS

$5,000,000

The value opinion in this report is qualified by certain assumptions, limiting conditions, certifications, and definitions. We particularly call your attention to the extraordinary assumption(s) listed below.

EXTRAORDINARY ASSUMPTIONS

For a definition of Extraordinary Assumptions please see the Glossary of Terms & Definitions.

The date of value is December 10, 2010 which is subsequent to our November 19, 2010 date of inspection. It is assumed that the condition of the property was the same on December 10, 2010 as it was on the date of our inspection.

This letter is invalid as an opinion of value if detached from the report, which contains the text, exhibits, and Addenda.

Respectfully submitted,

CUSHMAN & WAKEFIELD WESTERN, INC.

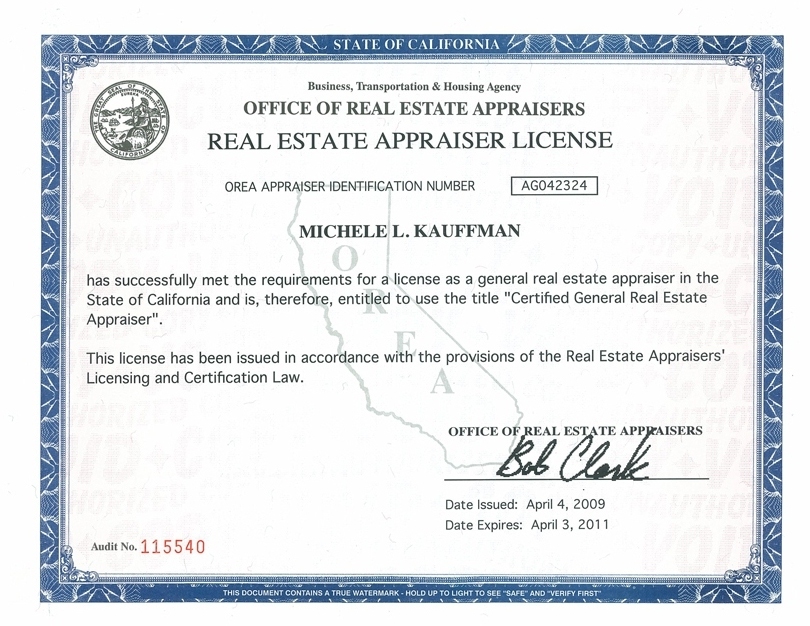

Michele Kauffman

Senior Director

CA Certified General Appraiser

License No. AG042324

michele.kauffman@cushwake.com

(213) 955-6495 Office Direct

(213) 627-4044 Fax

James W. Myers, MAI Executive Managing Director CA Certified General Appraiser License No. AG002662 jim.myers@cushwake.com

(213) 955-6493 Office Direct

(213) 627-4044 Fax

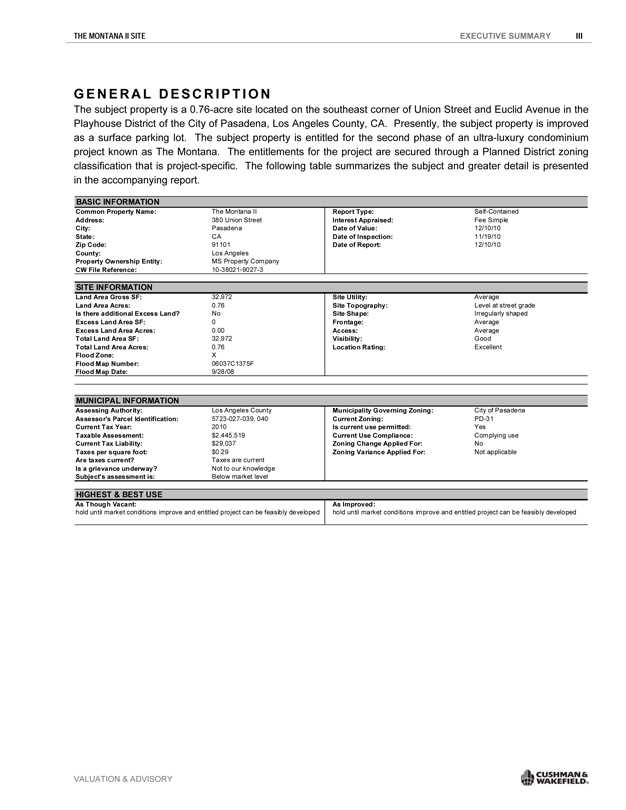

THE MONTANA II SITE EXECUTIVE SUMMARY III

GENERAL DESCRIPTION

The subject property is a 0.76-acre site located on the southeast corner of Union Street and Euclid Avenue in the Playhouse District of the City of Pasadena, Los Angeles County, CA. Presently, the subject property is improved as a surface parking lot. The subject property is entitled for the second phase of an ultra-luxury condominium project known as The Montana. The entitlements for the project are secured through a Planned District zoning classification that is project-specific. The following table summarizes the subject and greater detail is presented in the accompanying report.

BASIC INFORMATION

Common Property Name: The Montana II Report Type: Self-Contained

Address: 380 Union Street Interest Appraised: Fee Simple

City: Pasadena Date of Value: 12/10/10

State: CA Date of Inspection: 11/19/10

Zip Code: 91101 Date of Report: 12/10/10

County: Los Angeles

Property Ownership Entity: MS Property Company

CW File Reference: 10-38021-9027-3

SITE INFORMATION

Land Area Gross SF: Land Area Acres: Is there additional Excess Land? Excess Land Area SF: Excess Land Area Acres: Total Land Area SF: Total Land Area Acres: Flood Zone: Flood Map Number: Flood Map Date: 32,972 0.76 No 0 0.00 32,972 0.76 X 06037C1375F 9/28/08 Site Utility: Site Topography: Site Shape: Frontage: Access: Visibility: Location Rating: Average Level at street grade Irregularly shaped Average Average Good Excellent

MUNICIPAL INFORMATION

Assessing Authority: Assessor’s Parcel Identification: Current Tax Year: Taxable Assessment: Current Tax Liability: Taxes per square foot: Are taxes current? Is a grievance underway? Subject’s assessment is: Los Angeles County 5723-027-039, 040 2010 $2,445,519 $29,037 $0.29 Taxes are current Not to our knowledge Below market level Municipality Governing Zoning: Current Zoning: Is current use permitted: Current Use Compliance: Zoning Change Applied For: Zoning Variance Applied For: City of Pasadena PD-31 Yes Complying use No Not applicable

HIGHEST & BEST USE

As Though Vacant: As Improved:

hold until market conditions improve and entitled project can be feasibly developed hold until market conditions improve and entitled project can be feasibly developed

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE EXECUTIVE SUMMARY IV

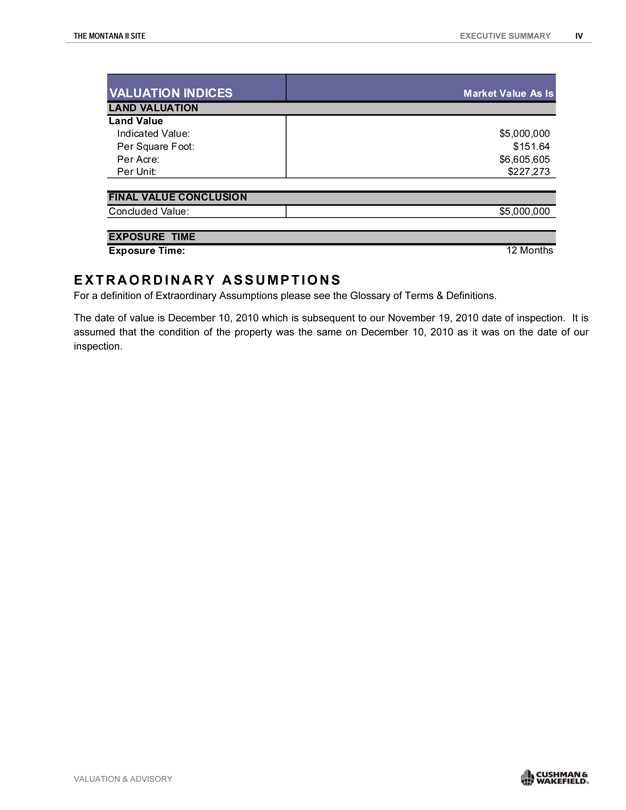

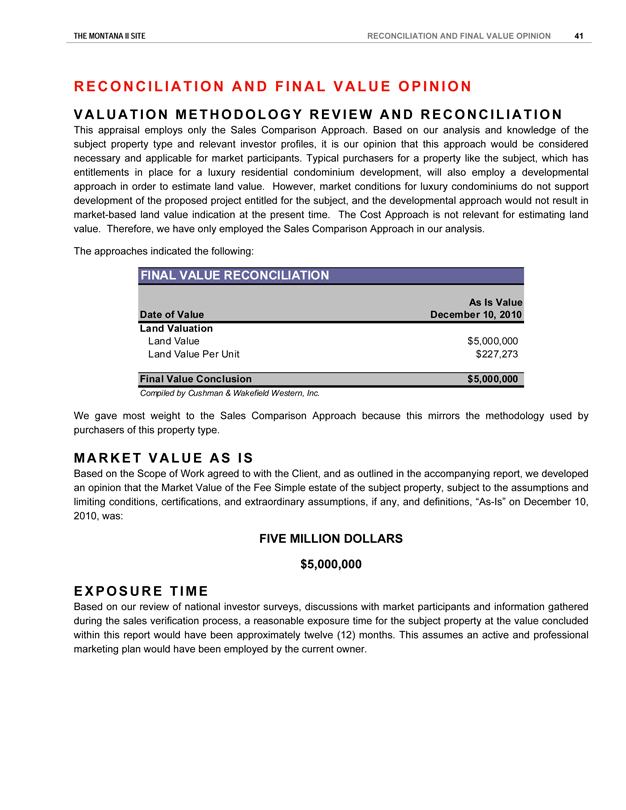

VALUATION INDICES Market Value As Is

LAND VALUATION

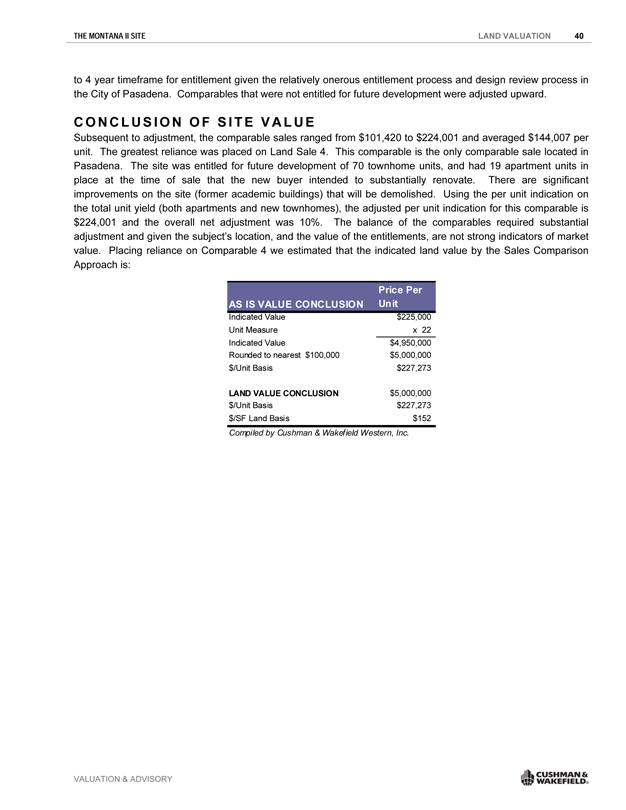

Land Value Indicated Value: Per Square Foot: Per Acre: Per Unit: $5,000,000

$151.64

$6,605,605

$227,273

FINAL VALUE CONCLUSION

Concluded Value: $5,000,000

EXPOSURE TIME

Exposure Time: 12 Months

EXTRAORDINARY ASSUMPTIONS

For a definition of Extraordinary Assumptions please see the Glossary of Terms & Definitions.

The date of value is December 10, 2010 which is subsequent to our November 19, 2010 date of inspection. It is assumed that the condition of the property was the same on December 10, 2010 as it was on the date of our inspection.

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

|

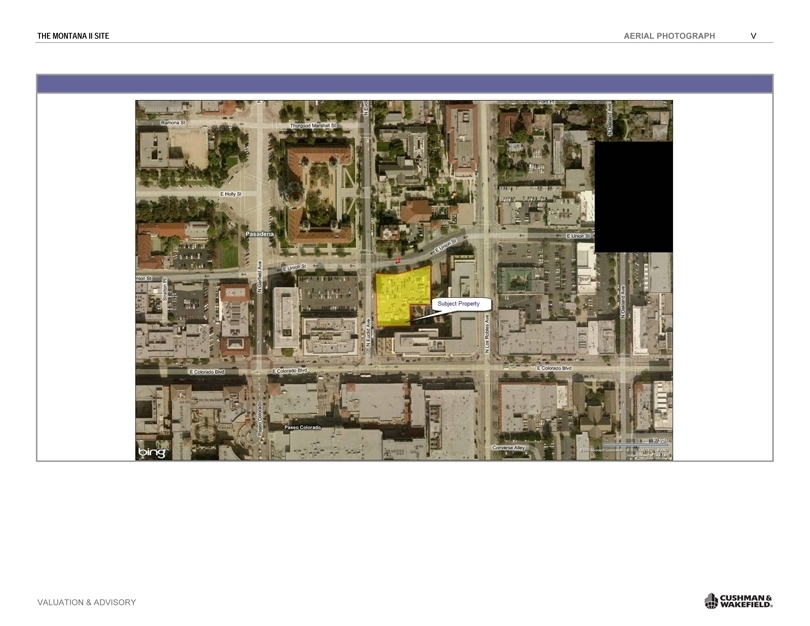

THE MONTANA II SITE AERIAL PHOTOGRAPH V

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

|

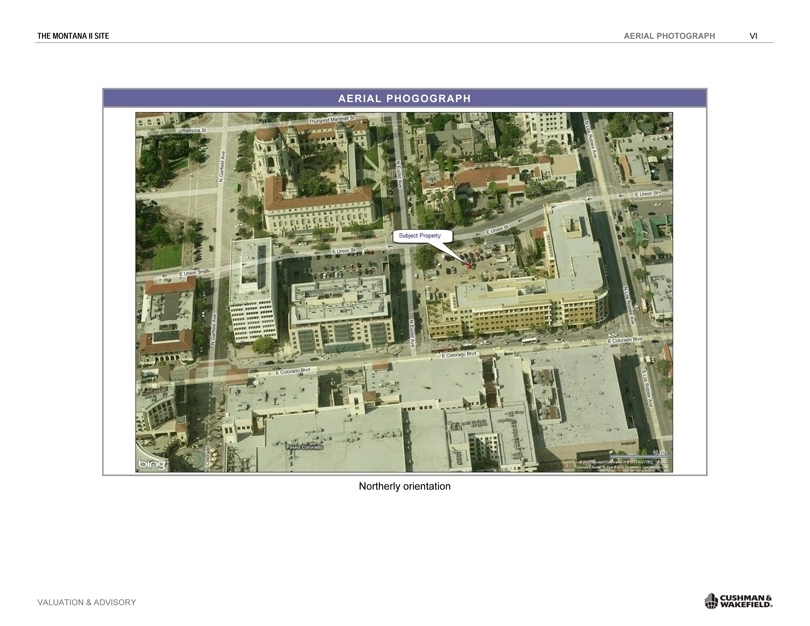

THE MONTANA II SITE AERIAL PHOTOGRAPH VI

AERIAL PHOGOGRAPH

Northerly orientation

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

|

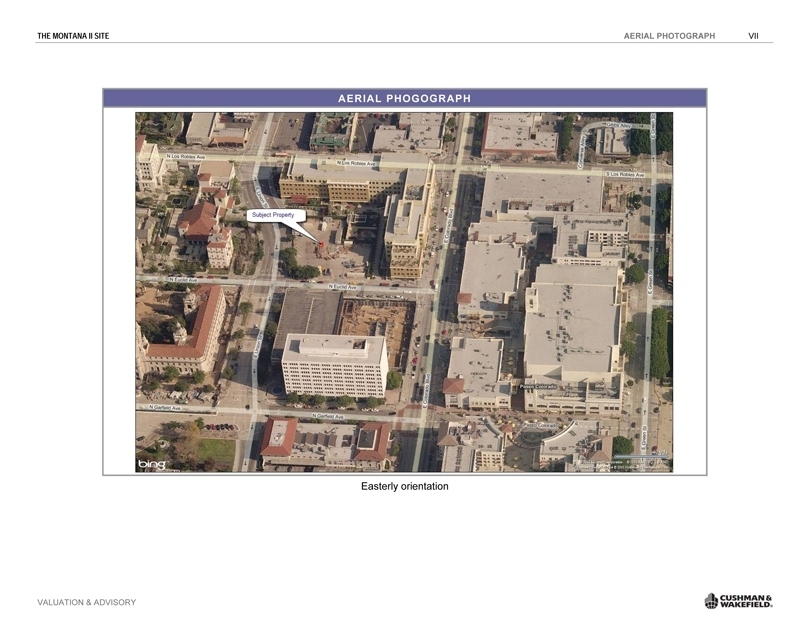

THE MONTANA II SITE AERIAL PHOTOGRAPH VII

AERIAL PHOGOGRAPH

Easterly orientation

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

|

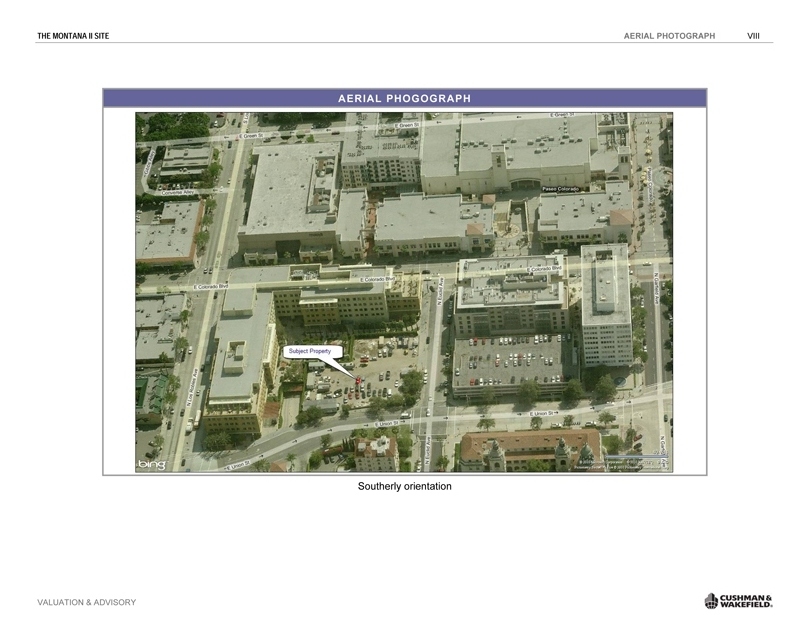

THE MONTANA II SITE AERIAL PHOTOGRAPH VIII

AERIAL PHOGOGRAPH

Southerly orientation

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

|

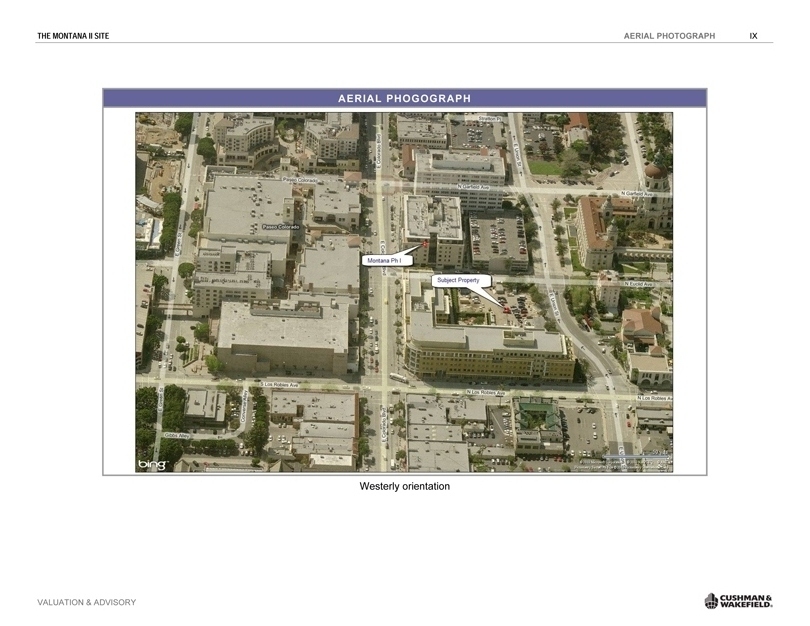

THE MONTANA II SITE AERIAL PHOTOGRAPH IX

AERIAL PHOGOGRAPH

Westerly orientation

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

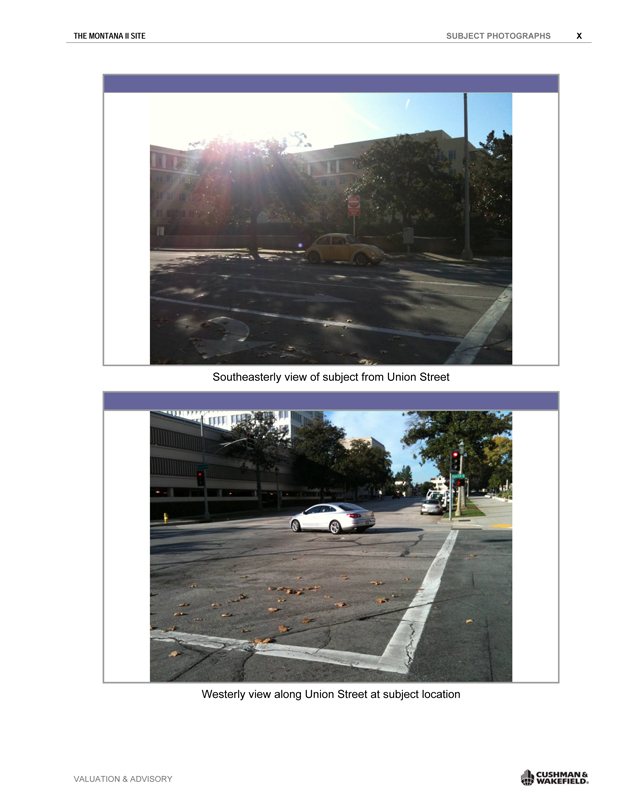

THE MONTANA II SITE SUBJECT PHOTOGRAPHS X

Southeasterly view of subject from Union Street

Westerly view along Union Street at subject location

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

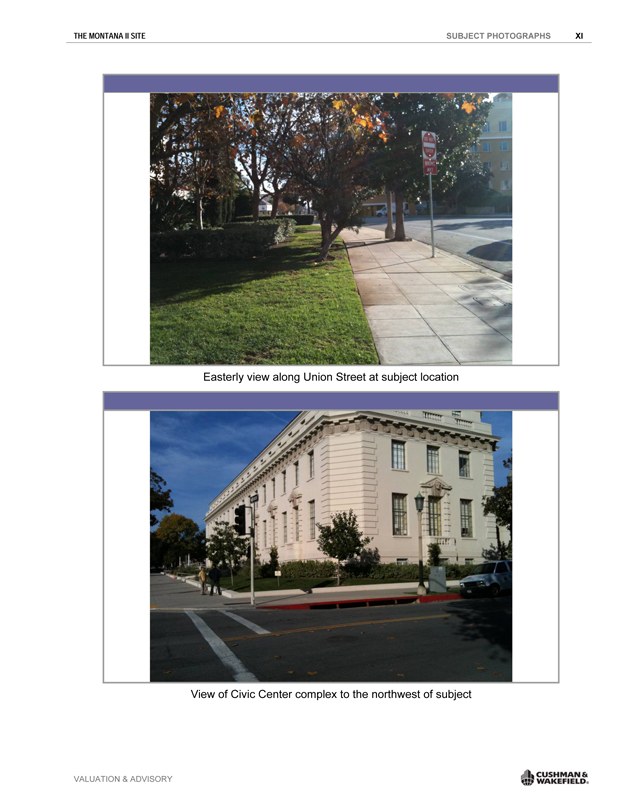

THE MONTANA II SITE SUBJECT PHOTOGRAPHS XI

Easterly view along Union Street at subject location

View of Civic Center complex to the northwest of subject

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE TABLE OF CONTENTS

TABLE OF CONTENTS

INTRODUCTION 1

REGIONAL MAP 4

LOS ANGELES REGIONAL ANALYSIS 5

LOCAL AREA MAP 16

LOCAL AREA ANALYSIS17

SITE DESCRIPTION 26

REAL PROPERTY TAXES AND ASSESSMENTS 29

ZONING30

HIGHEST AND BEST USE 32

VALUATION PROCESS 33

LAND VALUATION 34

RECONCILIATION AND FINAL VALUE OPINION 41

ASSUMPTIONS AND LIMITING CONDITIONS 42

CERTIFICATION OF APPRAISAL 44

GLOSSARY OF TERMS & DEFINITIONS 45

ADDENDA CONTENTS 48

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE INTRODUCTION 1

INTRODUCTION

SCOPE OF WORK

This appraisal, presented in a self-contained report, is intended to comply with the reporting requirements outlined under the USPAP for a self-contained appraisal report. The report was also prepared to comply with the requirements of the Code of Professional Ethics of the Appraisal Institute.

Cushman & Wakefield Western, Inc. has an internal Quality Control Oversight Program. This Program mandates a “second read” of all appraisals. Assignments prepared and signed solely by designated members (MAIs) are read by another MAI who is not participating in the assignment. Assignments prepared, in whole or in part, by non-designated appraisers require MAI participation, Quality Control Oversight, and signature.

For this assignment, Quality Control Oversight was provided by James W. Myers, MAI. In addition to a qualitative assessment of the appraisal report, James W. Myers, MAI is a signatory to the appraisal report and concurs in the value estimate(s) set forth herein.

The scope of this appraisal required collecting primary and secondary data relevant to the subject property. Vacant land and improved sales were researched in the subject’s market, rental data was analyzed, and the input of buyers, sellers, brokers, property developers and public officials was considered. A physical inspection of the property was made. In addition, the general regional economy as well as the specifics of the subject’s local area was investigated.

The data have been thoroughly analyzed and confirmed with sources believed to be reliable, leading to the value conclusions in this report. The valuation process used generally accepted market-derived methods and procedures appropriate to the assignment.

This appraisal employs only the Sales Comparison Approach. Based on our analysis and knowledge of the subject property type and relevant investor profiles, it is our opinion that this approach would be considered necessary and applicable for market participants. Typical purchasers for a property like the subject, which has entitlements in place for a luxury residential condominium development, will also employ a developmental approach in order to estimate land value. However, market conditions for luxury condominiums do not support development of the proposed project entitled for the subject, and the developmental approach would not result in market-based land value indication at the present time. The Cost Approach is not relevant for estimating land value. Therefore, we have only employed the Sales Comparison Approach in our analysis.

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE INTRODUCTION 2

IDENTIFICATION OF PROPERTY

Common Property Name: The Montana II

Location: 380 Union Street

Pasadena, Los Angeles County, CA 91101

Assessor’s Parcel Number(s): 5723-027-039, 040

Legal Description: The legal description was requested but not provided. Based on our review of Los Angeles County Assessor’s parcel maps, the subject could be described as lots 6 and 7 in Tract 62283 of Los Angeles County, California. We recommend the Client obtain a complete title report and legal description of the subject property.

PROPERTY OWNERSHIP AND RECENT HISTORY

Current Ownership: MS Property Company

Sale History: To the best of our knowledge, the property has not transferred within the past three years.

Current Disposition: To the best of our knowledge, the property is not under contract of sale nor is it being marketed for sale.

DATES OF INSPECTION AND VALUATION

Date of Valuation: December 10, 2010

Date of Inspection: November 19, 2010

Property inspection was

performed by: Michele Kauffman and James W. Myers, MAI

CLIENT, INTENDED USE AND USERS OF THE APPRAISAL

Client: Special Committee of the Board of Directors of Wesco Financial Corporation c/o Skadden, Arps, Slate, Meagher & Flom LLP

Intended Use: This appraisal is intended to provide an opinion of the Market Value of the Fee Simple interest in the property for the use of the client and other intended users in evaluating a possible sale of an interest in the asset. This report is not intended for any other

use.

Intended User: This appraisal report was prepared for the exclusive use of Skadden, Arps, Slate, Meagher & Flom LLP; for The Special Committee of the Board of Directors of Wesco Financial Corporation, and for their advisor Greenhill. Use of this report by others is not intended by the appraiser.

EXTRAORDINARY ASSUMPTIONS

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE INTRODUCTION 3

The date of value is December 10, 2010 which is subsequent to our November 19, 2010 date of inspection. It is assumed that the condition of the property was the same on December 10, 2010 as it was on the date of our inspection.

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

|

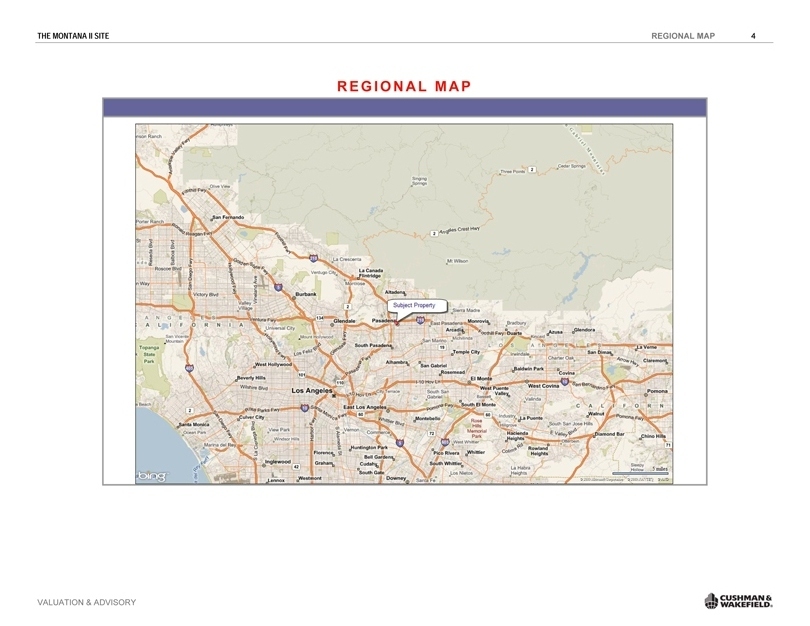

THE MONTANA II SITE REGIONAL MAP 4

REGIONAL MAP

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE REGIONAL ANALYSIS 5

LOS ANGELES REGIONAL ANALYSIS

INTRODUCTION

MARKET DEFINITION

Los Angeles County ranks 18th on the list of the world’s largest economies and is the largest county in the nation in terms of population, totaling an estimated 9.9 million residents, or about 27.0 percent of the State of California’s population. The majority of Los Angeles County is heavily urbanized averaging roughly 2,450 residents per square mile. Geographically, the county encompasses 4,061 square miles with 70 miles of coast on the Pacific Ocean. Neighboring regions include Orange County to the south, San Bernardino County to the east, Ventura County to the west and Kern County to the north.

The Los Angeles-Long Beach-Santa Ana Metropolitan Statistical Area (Los Angeles-Long Beach-Santa Ana MSA) in Southern California is the largest of the three MSAs that comprise the Los Angeles Combined Statistical Area (Los Angeles CSA), which also includes the Riverside-San Bernardino-Ontario and Oxnard-Thousand Oaks-Ventura Metropolitan Statistical Areas. The Los Angeles-Long Beach-Santa Ana MSA is further divided into two metropolitan divisions—Los Angeles-Long Beach-Glendale and Santa Ana-Anaheim-Irvine. The Los Angeles-Long Beach-Glendale Metropolitan Division (Los Angeles MD), which is the focus of the following demographic and economic overview, is synonymous with Los Angeles County. The City of Los Angeles is the largest incorporated area in the county.

Some key points to consider are:

. International trade and commerce are major drivers of the area’s economy because of its strategic location and the size and scope of its economy. The Los Angeles Customs District – which includes the ports of Long Beach and Los Angeles, Port Hueneme, and Los Angeles International Airport – is the nation’s largest.

. The Los Angeles region has an extensive transportation network. Adding to the infrastructural strength of the ports and LAX airport, there are two other active commercial airports – Bob Hope in Burbank and Long Beach. Due to the size of its geographic footprint, Los Angeles freeway system is one of the most advanced in the country. In addition, there are mass transit options to service the public need and rail freight services linking the region to the rest of the state and the nation.

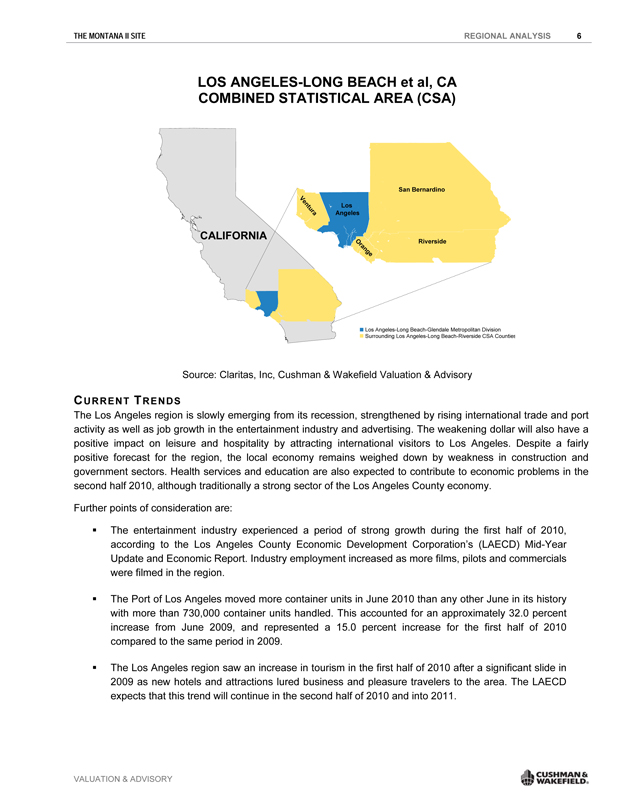

The map on the following page depicts Los Angeles County in relation to the adjacent Orange County and Inland Empire regions:

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE REGIONAL ANALYSIS 6

LOS ANGELES-LONG BEACH et al, CACOMBINED STATISTICAL AREA (CSA)

CALIFORNIA

San San Bernardino Bernardino

Los Los Angeles Angeles

Ventura

Los Angeles-Long Beach-Glendale Metropolitan Division Surrounding Los Angeles-Long Beach-Riverside CSA Counties

Source: Claritas, Inc, Cushman & Wakefield Valuation & Advisory

CURRENT TRENDS

The Los Angeles region is slowly emerging from its recession, strengthened by rising international trade and port activity as well as job growth in the entertainment industry and advertising. The weakening dollar will also have a positive impact on leisure and hospitality by attracting international visitors to Los Angeles. Despite a fairly positive forecast for the region, the local economy remains weighed down by weakness in construction and government sectors. Health services and education are also expected to contribute to economic problems in the second half 2010, although traditionally a strong sector of the Los Angeles County economy.

Further points of consideration are:

. The entertainment industry experienced a period of strong growth during the first half of 2010, according to the Los Angeles County Economic Development Corporation’s (LAECD) Mid-Year Update and Economic Report. Industry employment increased as more films, pilots and commercials were filmed in the region.

. The Port of Los Angeles moved more container units in June 2010 than any other June in its history with more than 730,000 container units handled. This accounted for an approximately 32.0 percent increase from June 2009, and represented a 15.0 percent increase for the first half of 2010 compared to the same period in 2009.

. The Los Angeles region saw an increase in tourism in the first half of 2010 after a significant slide in 2009 as new hotels and attractions lured business and pleasure travelers to the area. The LAECD expects that this trend will continue in the second half of 2010 and into 2011.

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE REGIONAL ANALYSIS 7

DEMOGRAPHIC TRENDS

DEMOGRAPHICS CHARACTERISTICS

Los Angeles’ median age is relatively young at 34.9 years, considerably lower than the median age of the U.S. at

36.8 years. The percentage of the population in Los Angeles with bachelor and advanced degrees is 24.4 percent, which is slightly below the U.S. share of 24.7 percent. Despite similarities in their respective education breakdowns, however, the Los Angeles region exceeds the national levels for average and median household income. Additionally, 23.4 percent of regional households have annual incomes of $100,000 or more compared to the national level of 19.3 percent.

Some interesting points to consider regarding the similarities and differences in demographic trends between Los Angeles and the U.S. include:

. There is a demand in the Los Angeles region for a large population of workers with highly developed skill sets in sectors like finance, education, and information technology that require postsecondary degrees. Firms in those sectors are forced to pay employees more for the same type of work in this region than in other regions of the country due to the higher cost of living in the Los Angeles region.

. The variance in the national and regional levels of education suggests that there is still a demand for large population of workers with highly developed skill sets in sectors like transportation, manufacturing and construction in Los Angeles County that do not require a postsecondary degree.

The table on the next page highlights and compares the most recent demographic characteristics for the Los Angeles Metro area and the United States:

DEMOGRAPHIC CHARACTERISTICS

Los Angeles-Long Beach-Glendale MD vs. United States

2009 Data

Los Angeles-Long

Beach-Glendale

Characteristic MD U.S.

Median Age (years) 34.9 36.8

Average Annual Household Income $77,484 $69,376

Median Annual Household Income $54,204 $51,433

Households by Annual Income Level:

<$25,000 23.2% 22.9%

$25,000 to $49,999 23.9% 26.0%

$50,000 to $74,999 17.7% 19.6%

$75,000 to $99,999 11.8% 12.3%

$100,000 plus 23.4% 19.3%

Education Breakdown:

< High School 30.7% 19.4%

High School Graduate 18.8% 28.3%

College < Bachelor Degree 26.0% 27.7%

Bachelor Degree 15.8% 15.8%

Advanced Degree 8.6% 8.9%

Source: Claritas, Inc., Cushman & Wakefield Valuation & Advisory

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE REGIONAL ANALYSIS 8

POPULATION

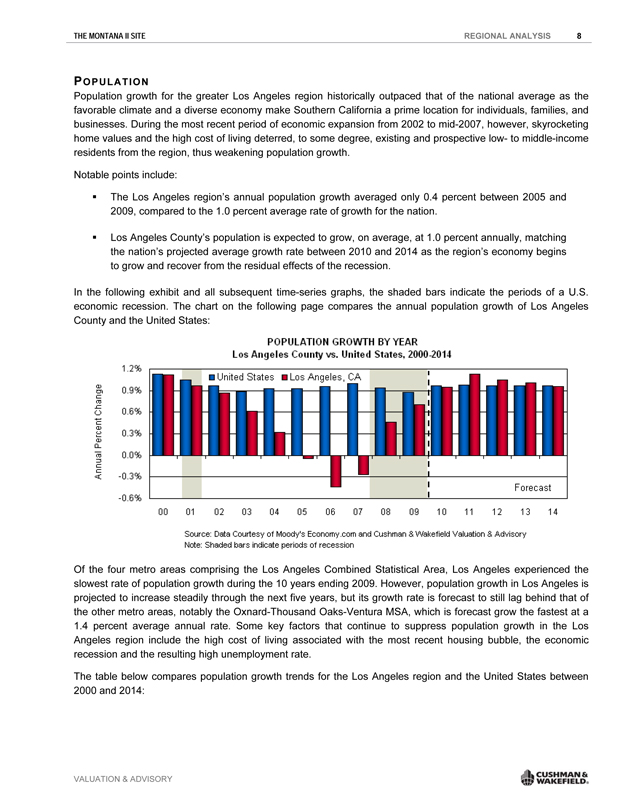

Population growth for the greater Los Angeles region historically outpaced that of the national average as the favorable climate and a diverse economy make Southern California a prime location for individuals, families, and businesses. During the most recent period of economic expansion from 2002 to mid-2007, however, skyrocketing home values and the high cost of living deterred, to some degree, existing and prospective low- to middle-income residents from the region, thus weakening population growth.

Notable points include:

. The Los Angeles region’s annual population growth averaged only 0.4 percent between 2005 and 2009, compared to the 1.0 percent average rate of growth for the nation.

. Los Angeles County’s population is expected to grow, on average, at 1.0 percent annually, matching the nation’s projected average growth rate between 2010 and 2014 as the region’s economy begins to grow and recover from the residual effects of the recession.

In the following exhibit and all subsequent time-series graphs, the shaded bars indicate the periods of a U.S. economic recession. The chart on the following page compares the annual population growth of Los Angeles County and the United States:

POPULATION GROWTH BY YEAR

Los Angeles County vs. United States, 2000-2014

Annual Percent Change

1.2% 0.9% 0.6% 0.3% 0.0% -0.3% -0.6%

United States

Los Angeles, CA

00 01 02 03 04 05 06 04 08 09 10 11 12 13 14

Forecast

Source: Data Courtesy of Moody’s Economy.com and Cushman & Wakefield Valuation & Advisory

Note: Shaded bars indicate periods of recession

Of the four metro areas comprising the Los Angeles Combined Statistical Area, Los Angeles experienced the slowest rate of population growth during the 10 years ending 2009. However, population growth in Los Angeles is projected to increase steadily through the next five years, but its growth rate is forecast to still lag behind that of the other metro areas, notably the Oxnard-Thousand Oaks-Ventura MSA, which is forecast grow the fastest at a

1.4 percent average annual rate. Some key factors that continue to suppress population growth in the Los Angeles region include the high cost of living associated with the most recent housing bubble, the economic recession and the resulting high unemployment rate.

The table below compares population growth trends for the Los Angeles region and the United States between 2000 and 2014:

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE REGIONAL ANALYSIS 9

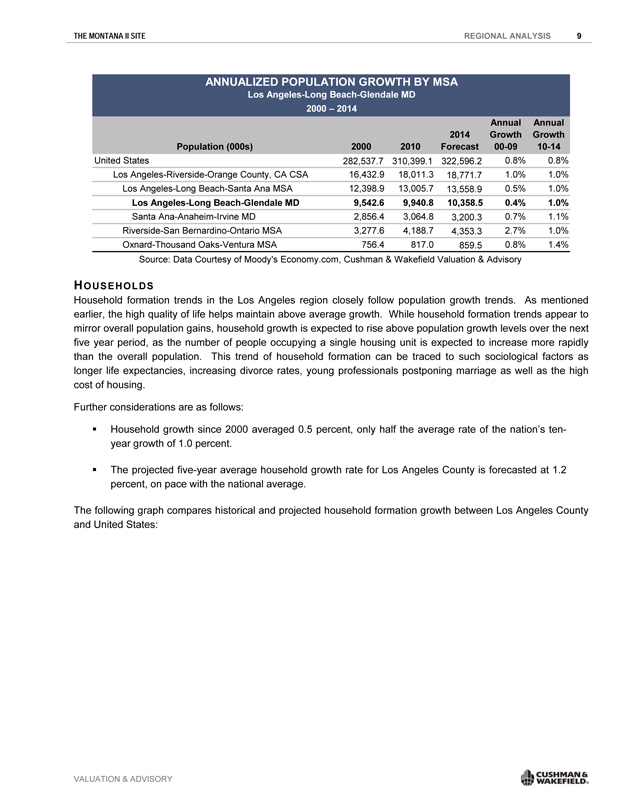

ANNUALIZED POPULATION GROWTH BY MSA

Los Angeles- Long Beach-Glendale MD

2000 – 2014

Annual Annual

2014 Growth Growth

Population (000s) 2000 2010 Forecast 00-09 10-14

United States 282,537.7 310,399.1 322,596.2 0.8% 0.8%

Los Angeles-Riverside-Orange County, CA CSA 16,432.9 18,011.3 18,771.7 1.0% 1.0%

Los Angeles-Long Beach-Santa Ana MSA 12,398.9 13,005.7 13,558.9 0.5% 1.0%

Los Angeles-Long Beach-Glendale MD 9,542.6 9,940.8 10,358.5 0.4% 1.0%

Santa Ana-Anaheim-Irvine MD 2,856.4 3,064.8 3,200.3 0.7% 1.1%

Riverside-San Bernardino-Ontario MSA 3,277.6 4,188.7 4,353.3 2.7% 1.0%

Oxnard-Thousand Oaks-Ventura MSA 756.4 817.0 859.5 0.8% 1.4%

Source: Data Courtesy of Moody’s Economy.com, Cushman & Wakefield Valuation & Advisory

HOUSEHOLDS

Household formation trends in the Los Angeles region closely follow population growth trends. As mentioned earlier, the high quality of life helps maintain above average growth. While household formation trends appear to mirror overall population gains, household growth is expected to rise above population growth levels over the next five year period, as the number of people occupying a single housing unit is expected to increase more rapidly than the overall population. This trend of household formation can be traced to such sociological factors as longer life expectancies, increasing divorce rates, young professionals postponing marriage as well as the high cost of housing.

Further considerations are as follows:

. Household growth since 2000 averaged 0.5 percent, only half the average rate of the nation’s ten-

year growth of 1.0 percent.

. The projected five-year average household growth rate for Los Angeles County is forecasted at 1.2

percent, on pace with the national average.

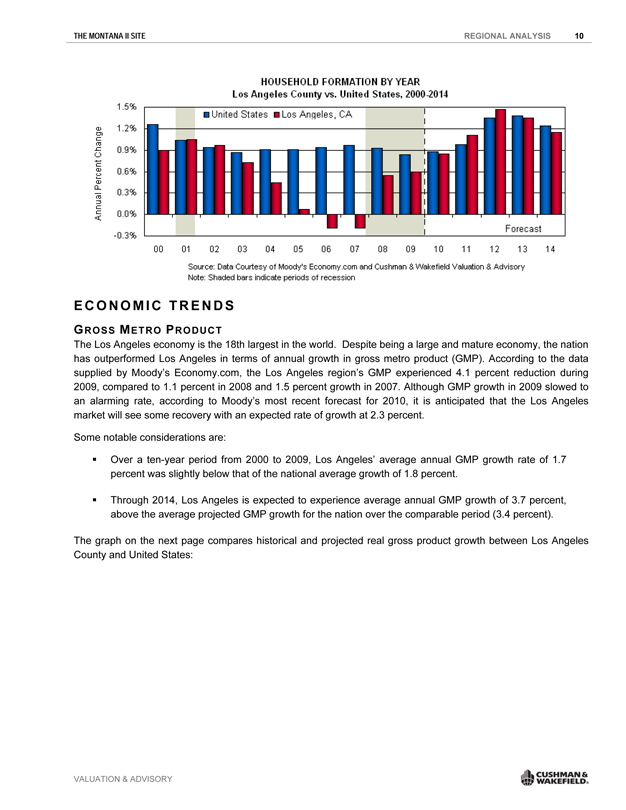

The following graph compares historical and projected household formation growth between Los Angeles County and United States:

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE REGIONAL ANALYSIS 10

HOUSEHOLD FORMATION BY YEAR

Los Angeles County vs. United States, 2000-2014

Annual Percent Change

1.5% 1.2% 0.9% 0.6% 0.3% 0.0% -0.3%

United States

Los Angeles, CA

00 01 02 03 04 05 06 04 08 09 10 11 12 13 14

Forecast

Source: Data Courtesy of Moody’s Economy.com and Cushman & Wakefield Valuation & Advisory

Note: Shaded bars indicate periods of recession

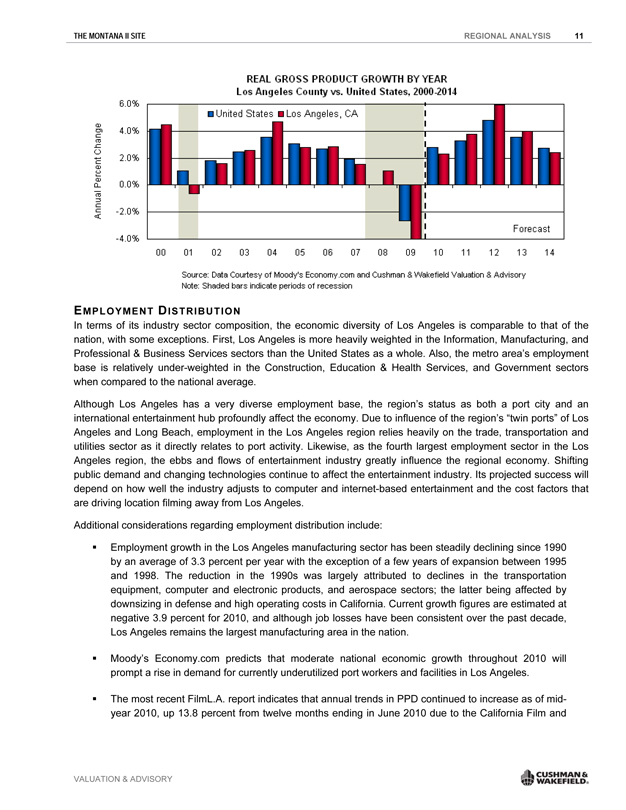

ECONOMIC TRENDS

GROSS METRO PRODUCT

The Los Angeles economy is the 18th largest in the world. Despite being a large and mature economy, the nation has outperformed Los Angeles in terms of annual growth in gross metro product (GMP). According to the data supplied by Moody’s Economy.com, the Los Angeles region’s GMP experienced 4.1 percent reduction during 2009, compared to 1.1 percent in 2008 and 1.5 percent growth in 2007. Although GMP growth in 2009 slowed to an alarming rate, according to Moody’s most recent forecast for 2010, it is anticipated that the Los Angeles market will see some recovery with an expected rate of growth at 2.3 percent.

Some notable considerations are:

. Over a ten-year period from 2000 to 2009, Los Angeles’ average annual GMP growth rate of 1.7 percent was slightly below that of the national average growth of 1.8 percent.

. Through 2014, Los Angeles is expected to experience average annual GMP growth of 3.7 percent, above the average projected GMP growth for the nation over the comparable period (3.4 percent).

The graph on the next page compares historical and projected real gross product growth between Los Angeles County and United States:

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE REGIONAL ANALYSIS 11

REAL GROSS PRODUCT GROWTH BY YEAR

Los Angeles County vs. United States, 2000-2014

Annual Percent Change

6.0% 4.0% 2.0% 0.0% -2.0% -4.0%

United States

Los Angeles, CA

00 01 02 03 04 05 06 04 08 09 10 11 12 13 14

Forecast

Source: Data Courtesy of Moody’s Economy.com and Cushman & Wakefield Valuation & Advisory

Note: Shaded bars indicate periods of recession

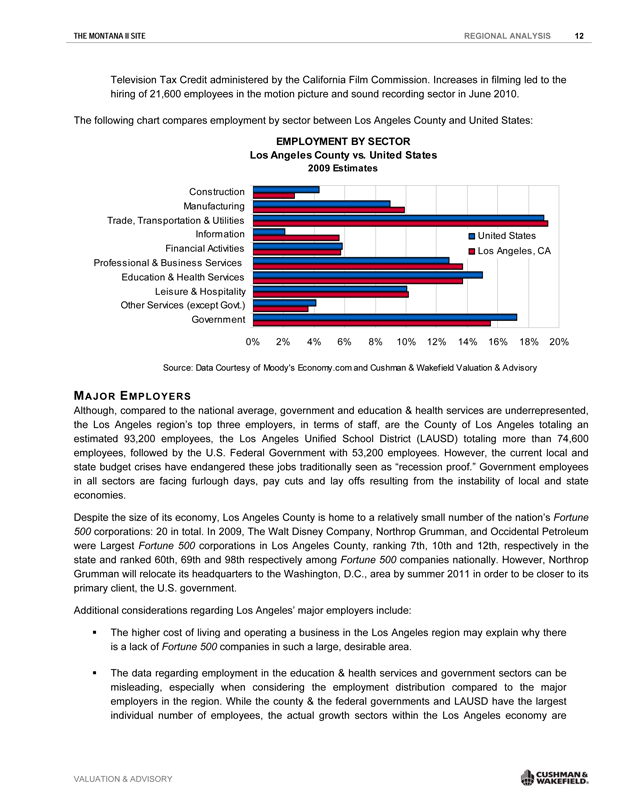

EMPLOYMENT DISTRIBUTION

In terms of its industry sector composition, the economic diversity of Los Angeles is comparable to that of the nation, with some exceptions. First, Los Angeles is more heavily weighted in the Information, Manufacturing, and Professional & Business Services sectors than the United States as a whole. Also, the metro area’s employment base is relatively under-weighted in the Construction, Education & Health Services, and Government sectors when compared to the national average.

Although Los Angeles has a very diverse employment base, the region’s status as both a port city and an international entertainment hub profoundly affect the economy. Due to influence of the region’s “twin ports” of Los Angeles and Long Beach, employment in the Los Angeles region relies heavily on the trade, transportation and utilities sector as it directly relates to port activity. Likewise, as the fourth largest employment sector in the Los Angeles region, the ebbs and flows of entertainment industry greatly influence the regional economy. Shifting public demand and changing technologies continue to affect the entertainment industry. Its projected success will depend on how well the industry adjusts to computer and internet-based entertainment and the cost factors that are driving location filming away from Los Angeles.

Additional considerations regarding employment distribution include:

. Employment growth in the Los Angeles manufacturing sector has been steadily declining since 1990 by an average of 3.3 percent per year with the exception of a few years of expansion between 1995 and 1998. The reduction in the 1990s was largely attributed to declines in the transportation equipment, computer and electronic products, and aerospace sectors; the latter being affected by downsizing in defense and high operating costs in California. Current growth figures are estimated at negative 3.9 percent for 2010, and although job losses have been consistent over the past decade, Los Angeles remains the largest manufacturing area in the nation.

. Moody’s Economy.com predicts that moderate national economic growth throughout 2010 will prompt a rise in demand for currently underutilized port workers and facilities in Los Angeles.

. The most recent FilmL.A. report indicates that annual trends in PPD continued to increase as of mid-year 2010, up 13.8 percent from twelve months ending in June 2010 due to the California Film and

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE REGIONAL ANALYSIS 12

Television Tax Credit administered by the California Film Commission. Increases in filming led to the hiring of 21,600 employees in the motion picture and sound recording sector in June 2010.

The following chart compares employment by sector between Los Angeles County and United States:

EMPLOYMENT BY SECTOR Los Angeles County vs. United States 2009 Estimates

Construction

Manufacturing

Trade, Transportation & Utilities

Information

Financial Activities

Professional & Business Services

Education & Health Services

Leisure & Hospitality

Other Services (except Govt.)

Government

United States Los Angeles, CA

0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20%

Source: Data Courtesy of Moody’s Economy.com and Cushman & Wakefield Valuation & Advisory

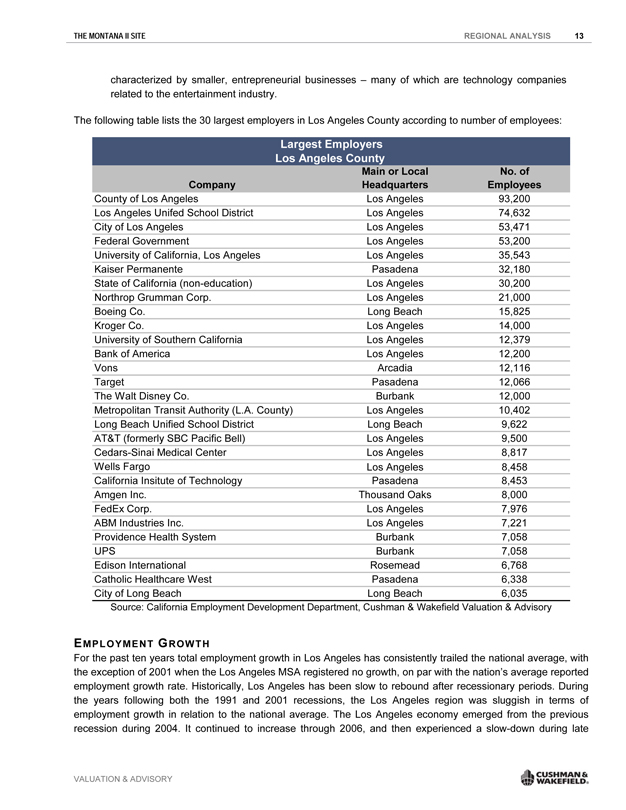

MAJOR EMPLOYERS

Although, compared to the national average, government and education & health services are underrepresented, the Los Angeles region’s top three employers, in terms of staff, are the County of Los Angeles totaling an estimated 93,200 employees, the Los Angeles Unified School District (LAUSD) totaling more than 74,600 employees, followed by the U.S. Federal Government with 53,200 employees. However, the current local and state budget crises have endangered these jobs traditionally seen as “recession proof.” Government employees in all sectors are facing furlough days, pay cuts and lay offs resulting from the instability of local and state economies.

Despite the size of its economy, Los Angeles County is home to a relatively small number of the nation’s Fortune 500 corporations: 20 in total. In 2009, The Walt Disney Company, Northrop Grumman, and Occidental Petroleum were Largest Fortune 500 corporations in Los Angeles County, ranking 7th, 10th and 12th, respectively in the state and ranked 60th, 69th and 98th respectively among Fortune 500 companies nationally. However, Northrop Grumman will relocate its headquarters to the Washington, D.C., area by summer 2011 in order to be closer to its primary client, the U.S. government.

Additional considerations regarding Los Angeles’ major employers include:

. The higher cost of living and operating a business in the Los Angeles region may explain why there is a lack of Fortune 500 companies in such a large, desirable area.

. The data regarding employment in the education & health services and government sectors can be misleading, especially when considering the employment distribution compared to the major employers in the region. While the county & the federal governments and LAUSD have the largest individual number of employees, the actual growth sectors within the Los Angeles economy are

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE REGIONAL ANALYSIS 13

characterized by smaller, entrepreneurial businesses – many of which are technology companies related to the entertainment industry.

The following table lists the 30 largest employers in Los Angeles County according to number of employees:

Largest Employers Los Angeles County

Main or Local No. of

Company Headquarters Employees

County of Los Angeles Los Angeles 93,200

Los Angeles Unifed School District Los Angeles 74,632

City of Los Angeles Los Angeles 53,471

Federal Government Los Angeles 53,200

University of California, Los Angeles Los Angeles 35,543

Kaiser Permanente Pasadena 32,180

State of California (non-education) Los Angeles 30,200

Northrop Grumman Corp. Los Angeles 21,000

Boeing Co. Long Beach 15,825

Kroger Co. Los Angeles 14,000

University of Southern California Los Angeles 12,379

Bank of America Los Angeles 12,200

Vons Arcadia 12,116

Target Pasadena 12,066

The Walt Disney Co. Burbank 12,000

Metropolitan Transit Authority (L.A. County) Los Angeles 10,402

Long Beach Unified School District Long Beach 9,622

AT&T (formerly SBC Pacific Bell) Los Angeles 9,500

Cedars-Sinai Medical Center Los Angeles 8,817

Wells Fargo Los Angeles 8,458

California Insitute of Technology Pasadena 8,453

Amgen Inc. Thousand Oaks 8,000

FedEx Corp. Los Angeles 7,976

ABM Industries Inc. Los Angeles 7,221

Providence Health System Burbank 7,058

UPS Burbank 7,058

Edison International Rosemead 6,768

Catholic Healthcare West Pasadena 6,338

City of Long Beach Long Beach 6,035

Source: California Employment Development Department, Cushman & Wakefield Valuation & Advisory

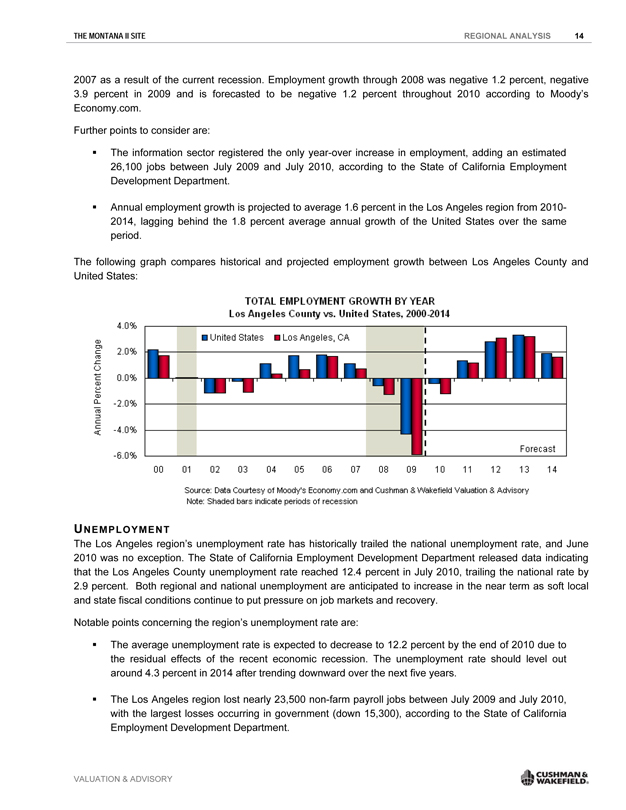

EMPLOYMENT GROWTH

For the past ten years total employment growth in Los Angeles has consistently trailed the national average, with the exception of 2001 when the Los Angeles MSA registered no growth, on par with the nation’s average reported employment growth rate. Historically, Los Angeles has been slow to rebound after recessionary periods. During the years following both the 1991 and 2001 recessions, the Los Angeles region was sluggish in terms of employment growth in relation to the national average. The Los Angeles economy emerged from the previous recession during 2004. It continued to increase through 2006, and then experienced a slow-down during late

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE REGIONAL ANALYSIS 14

2007 as a result of the current recession. Employment growth through 2008 was negative 1.2 percent, negative

3.9 percent in 2009 and is forecasted to be negative 1.2 percent throughout 2010 according to Moody’s Economy.com.

Further points to consider are:

. The information sector registered the only year-over increase in employment, adding an estimated 26,100 jobs between July 2009 and July 2010, according to the State of California Employment Development Department.

. Annual employment growth is projected to average 1.6 percent in the Los Angeles region from 2010-2014, lagging behind the 1.8 percent average annual growth of the United States over the same period.

The following graph compares historical and projected employment growth between Los Angeles County and United States:

TOTAL EXPLOYMENT GROWTH BY YEAR

Los Angeles County vs. United States, 2000-2014

Annual Percent Change

4.0% 2.0% 0.0% -2.0% -4.0% -6.0%

United States

Los Angeles, CA

00 01 02 03 04 05 06 04 08 09 10 11 12 13 14

Forecast

Source: Data Courtesy of Moody’s Economy.com and Cushman & Wakefield Valuation & Advisory

Note: Shaded bars indicate periods of recession

UNEMPLOYMENT

The Los Angeles region’s unemployment rate has historically trailed the national unemployment rate, and June 2010 was no exception. The State of California Employment Development Department released data indicating that the Los Angeles County unemployment rate reached 12.4 percent in July 2010, trailing the national rate by

2.9 percent. Both regional and national unemployment are anticipated to increase in the near term as soft local and state fiscal conditions continue to put pressure on job markets and recovery.

Notable points concerning the region’s unemployment rate are:

. The average unemployment rate is expected to decrease to 12.2 percent by the end of 2010 due to the residual effects of the recent economic recession. The unemployment rate should level out around 4.3 percent in 2014 after trending downward over the next five years.

. The Los Angeles region lost nearly 23,500 non-farm payroll jobs between July 2009 and July 2010, with the largest losses occurring in government (down 15,300), according to the State of California Employment Development Department.

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE REGIONAL ANALYSIS 15

The graph on the next page compares historical and projected unemployment rates between Los Angeles County, the state of California, and the United States:

UNEMPLOYMENT RATE BY YEAR

Los Angeles County vs. California vs. United States, 2000-2014

14% 12% 10% 8% 6% 4% 2%

United States

California

Los Angeles, CA

Forecast

00 01 02 03 04 05 06 04 08 09 10* 11 12 13 14

Source: Data Courtesy of Moody’s Economy.com and Cushman & Wakefield Valuation & Advisory

Note: Shaded bars indicate periods of recession

*Second Quarter 2010 Data

CONCLUSION

Los Angeles has an established market with a diverse economic base. The industries driving the new economy spurred rapid growth since 2002. However, from mid-2007 to the present, these industries have become vulnerable to a series of negative economic events which are presenting numerous challenges for short-term growth in the area. Despite the residual effects of the economic downturn, the region’s economy should experience moderate growth in the second half of 2010 before picking up speed in 2011.

Final thoughts:

. Los Angeles’ long term growth is largely tied to its two major shipping ports as they present greater access to global economies. Ongoing infrastructure improvements to the ports are expected to result in Los Angeles capturing a greater share of West Coast shipping traffic. Current congestion, however, has allowed other West and East Coast ports to siphon some of the traffic that would normally go to Los Angeles/Long Beach.

. A lack of affordable housing limits migration to the region, and the high cost of doing business often causes businesses to locate elsewhere. In spite of this, Los Angeles provides a broad array of economic drivers from trade, defense, and aerospace to tourism, entertainment and consumer goods, all of which provide a solid foundation for growth in the future.

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

|

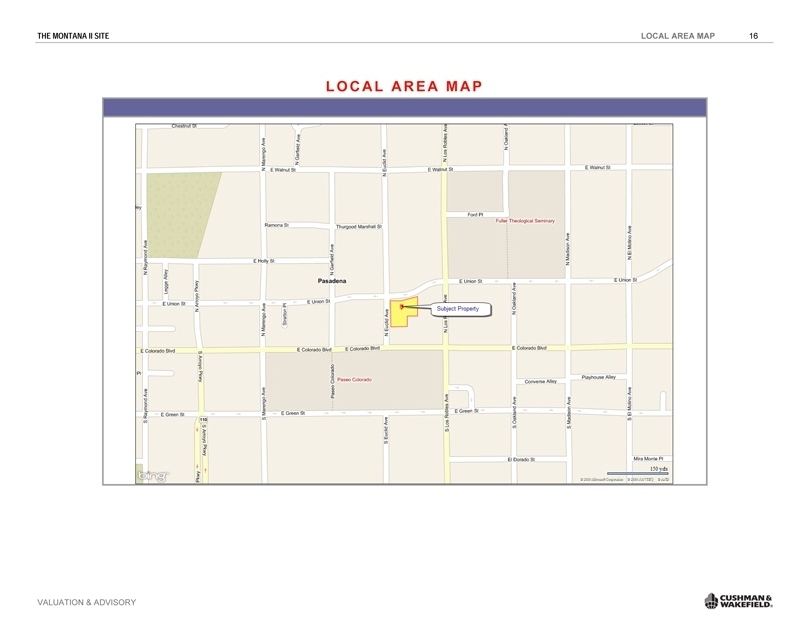

THE MONTANA II SITE LOCAL AREA MAP 16

LOCAL AREA MAP VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE LOCAL AREA ANALYSIS 17

VALUATION & ADVISORY

LOCAL AREA ANALYSIS

The subject property is located on the southeast corner of Euclid Avenue and Union Street, in the City of Pasadena, California. The City of Pasadena is located in the northern central portion of Los Angeles County at the western end of the San Gabriel Valley. Pasadena is situated approximately ten miles northeast of downtown Los Angeles and approximately 25 miles inland from the Pacific Ocean. Pasadena is generally bordered by the City of Glendale to the west, the community of Altadena to the north, the Cities of Sierra Madre and Arcadia to the east, and the Cities of South Pasadena and San Marino to the south. Pasadena was incorporated as a city in 1886 and today comprises an established mix of residential communities with significant commercial development. Pasadena is widely recognized as the home of the Rose Bowl, the Jet Propulsion Laboratory, California Institute of Technology and host of the annual Tournament of Roses’ parade since January 1, 1890. The city also received additional international exposure during 1994, as the Rose Bowl was the official site for the 1994 World Cup Soccer matches.

ACCESS AND TRANSPORTATION

Air transportation in the region is excellent, due to the access of the Burbank-Glendale-Pasadena Airport (BUR), situated approximately 20 minutes north of downtown Pasadena. It provides general aviation service linking Pasadena to more than 32 cities nationwide, with one-half of the nation’s population located within a 2-1/2 hour flight. Currently, Alaska, American, Delta Connection, JetBlue, Southwest, United Express and US Airways offer domestic service from BUR. BUR currently consists of two terminals, with 14 gates and approximately 250,000 square feet.

Los Angeles International Airport (LAX) offers full domestic and international air service and is one of the five largest airports in the world in terms of passenger volume. LAX is a thirty-minute drive from Pasadena.

The Metropolitan Transportation Authority (“MTA”) operates 16 public bus lines in Pasadena that provide access throughout the San Gabriel Valley and Los Angeles areas. These bus lines link Pasadena to downtown Los Angeles and other adjacent communities. Other bus services that serve Pasadena are Foothill Transit, providing regular and express bus service in the San Gabriel and Pomona Valleys, and the Los Angeles City Department of Transportation (“LADOT”), operating commuter express lines from Encino to Pasadena with stops in Burbank and Glendale.

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE LOCAL AREA ANALYSIS 18

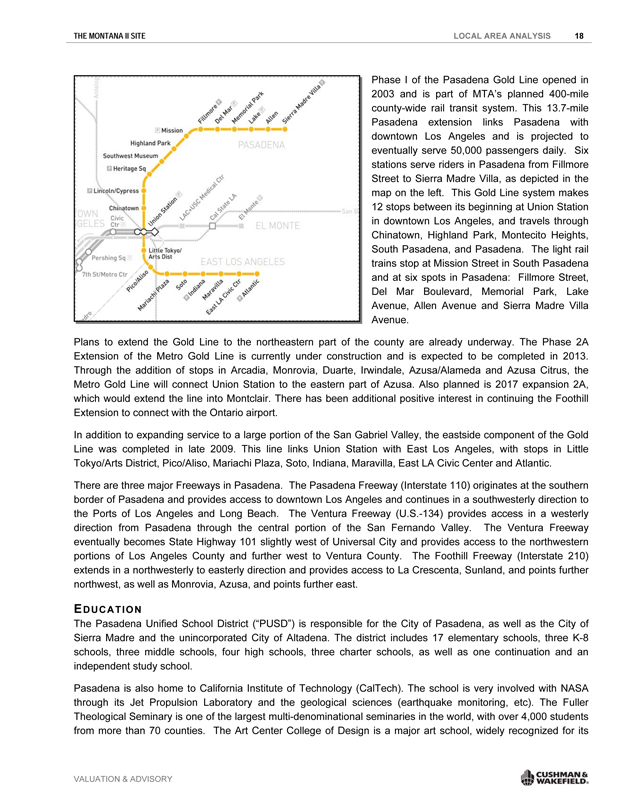

Phase I of the Pasadena Gold Line opened in 2003 and is part of MTA’s planned 400-mile county-wide rail transit system. This 13.7-mile Pasadena extension links Pasadena with downtown Los Angeles and is projected to eventually serve 50,000 passengers daily. Six stations serve riders in Pasadena from Fillmore Street to Sierra Madre Villa, as depicted in the map on the left. This Gold Line system makes 12 stops between its beginning at Union Station in downtown Los Angeles, and travels through Chinatown, Highland Park, Montecito Heights, South Pasadena, and Pasadena. The light rail trains stop at Mission Street in South Pasadena and at six spots in Pasadena: Fillmore Street, Del Mar Boulevard, Memorial Park, Lake Avenue, Allen Avenue and Sierra Madre Villa Avenue.

Plans to extend the Gold Line to the northeastern part of the county are already underway. The Phase 2A Extension of the Metro Gold Line is currently under construction and is expected to be completed in 2013. Through the addition of stops in Arcadia, Monrovia, Duarte, Irwindale, Azusa/Alameda and Azusa Citrus, the Metro Gold Line will connect Union Station to the eastern part of Azusa. Also planned is 2017 expansion 2A, which would extend the line into Montclair. There has been additional positive interest in continuing the Foothill Extension to connect with the Ontario airport.

In addition to expanding service to a large portion of the San Gabriel Valley, the eastside component of the Gold Line was completed in late 2009. This line links Union Station with East Los Angeles, with stops in Little Tokyo/Arts District, Pico/Aliso, Mariachi Plaza, Soto, Indiana, Maravilla, East LA Civic Center and Atlantic.

There are three major Freeways in Pasadena. The Pasadena Freeway (Interstate 110) originates at the southern border of Pasadena and provides access to downtown Los Angeles and continues in a southwesterly direction to the Ports of Los Angeles and Long Beach. The Ventura Freeway (U.S.-134) provides access in a westerly direction from Pasadena through the central portion of the San Fernando Valley. The Ventura Freeway eventually becomes State Highway 101 slightly west of Universal City and provides access to the northwestern portions of Los Angeles County and further west to Ventura County. The Foothill Freeway (Interstate 210) extends in a northwesterly to easterly direction and provides access to La Crescenta, Sunland, and points further northwest, as well as Monrovia, Azusa, and points further east.

EDUCATION

The Pasadena Unified School District (“PUSD”) is responsible for the City of Pasadena, as well as the City of Sierra Madre and the unincorporated City of Altadena. The district includes 17 elementary schools, three K-8 schools, three middle schools, four high schools, three charter schools, as well as one continuation and an independent study school.

Pasadena is also home to California Institute of Technology (CalTech). The school is very involved with NASA through its Jet Propulsion Laboratory and the geological sciences (earthquake monitoring, etc). The Fuller Theological Seminary is one of the largest multi-denominational seminaries in the world, with over 4,000 students from more than 70 counties. The Art Center College of Design is a major art school, widely recognized for its

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE LOCAL AREA ANALYSIS 19

design programs. Pasadena City College (PCC) with over 40,000 students is the third largest community college in the United States.

DEMOGRAPHIC PROFILE

POPULATION

Having established the subject’s trade area, our analysis focuses on the trade area’s population. Claritas, Inc. provides historical, current and forecasted population estimates for the total area. Patterns of development density and migration are reflected in the current levels of population estimates.

Between 2000 and 2009, Claritas, Inc., reports that the population within the primary trade area (3-mile radius) increased at a compound annual rate of 0.9 percent. This is characteristic of suburban areas in this market. This trend is expected to continue into the near future albeit at a slightly slower pace. Expanding to the total trade area (5-mile radius), population is expected to increase 0.97 percent per annum over the next five years.

The following page contains a graphic representation of the current population distribution within the subject’s region.

The graphic on the second following page illustrates projected population growth within the trade area over the next five years (2009—2014). The trade area is clearly characterized by various levels of growth.

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE LOCAL AREA ANALYSIS 20

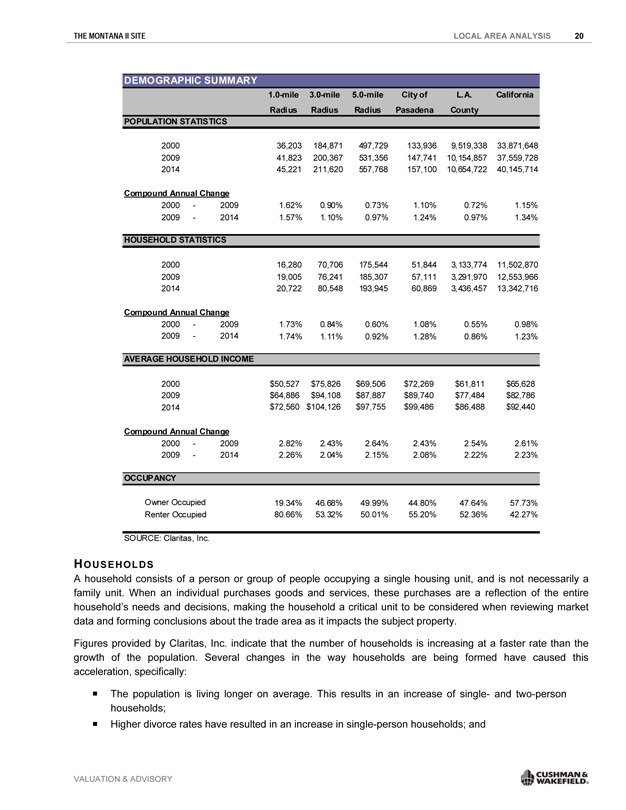

DEMOGRAPHIC SUMMARY

1.0-mile 3.0-mile 5.0-mile City of L.A. California

Radius Radius Radius Pasadena County

POPULATION STATISTICS

2000 36,203 184,871 497,729 133,936 9,519,338 33,871,648

2009 41,823 200,367 531,356 147,741 10,154,857 37,559,728

2014 45,221 211,620 557,768 157,100 10,654,722 40,145,714

Compound Annual Change

2000—2009 1.62% 0. 90% 0.73% 1.10% 0.72% 1.15%

2009—2014 1.57% 1. 10% 0.97% 1.24% 0.97% 1.34%

HOUSEHOLD STATISTICS

2000 16,280 70,706 175,544 51,844 3,133,774 11,502,870

2009 19,005 76,241 185,307 57,111 3,291,970 12,553,966

2014 20,722 80,548 193,945 60,869 3,436,457 13,342,716

Compound Annual Change

2000—2009 1.73% 0. 84% 0.60% 1.08% 0.55% 0.98%

2009—2014 1.74% 1. 11% 0.92% 1.28% 0.86% 1.23%

AVERAGE HOUSEHOLD INCOME

2000 $50,527 $75,826 $69,506 $72,269 $61,811 $65,628

2009 $64,886 $94,108 $87,887 $89,740 $77,484 $82,786

2014 $72,560 $104,126 $97,755 $99,486 $86,488 $92,440

Compound Annual Change

2000—2009 2.82% 2. 43% 2.64% 2.43% 2.54% 2.61%

2009—2014 2.26% 2. 04% 2.15% 2.08% 2.22% 2.23%

OCCUPANCY

Owner Occupied 19.34% 46. 68% 49.99% 44.80% 47.64% 57.73%

Renter Occupied 80.66% 53. 32% 50.01% 55.20% 52.36% 42.27%

SOURCE: Claritas, Inc.

HOUSEHOLDS

A household consists of a person or group of people occupying a single housing unit, and is not necessarily a family unit. When an individual purchases goods and services, these purchases are a reflection of the entire household’s needs and decisions, making the household a critical unit to be considered when reviewing market data and forming conclusions about the trade area as it impacts the subject property.

Figures provided by Claritas, Inc. indicate that the number of households is increasing at a faster rate than the growth of the population. Several changes in the way households are being formed have caused this acceleration, specifically:

. The population is living longer on average. This results in an increase of single- and two-person households;

. Higher divorce rates have resulted in an increase in single-person households; and

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE LOCAL AREA ANALYSIS 21

. Many individuals have postponed marriage, also resulting in more single-person households. According to Claritas, Inc., the Primary Trade Area grew at a compound annual rate of 0.84 percent between 2000 and 2009. Consistent with national trends the trade area is experiencing household changes at a rate that

varies from population changes. That pace is expected to continue through 2014, and is estimated at 1.11 percent.

Correspondingly, a greater number of smaller households with fewer children generally indicates more disposable income. In 2000, there were 2.56 persons per household in the Primary Trade Area and by 2009, this number is estimated to have increased to 2.57 persons. Through 2014, the average number of persons per household is forecasted to increase to 2.57 persons.

AVERAGE HOUSEHOLD INCOME

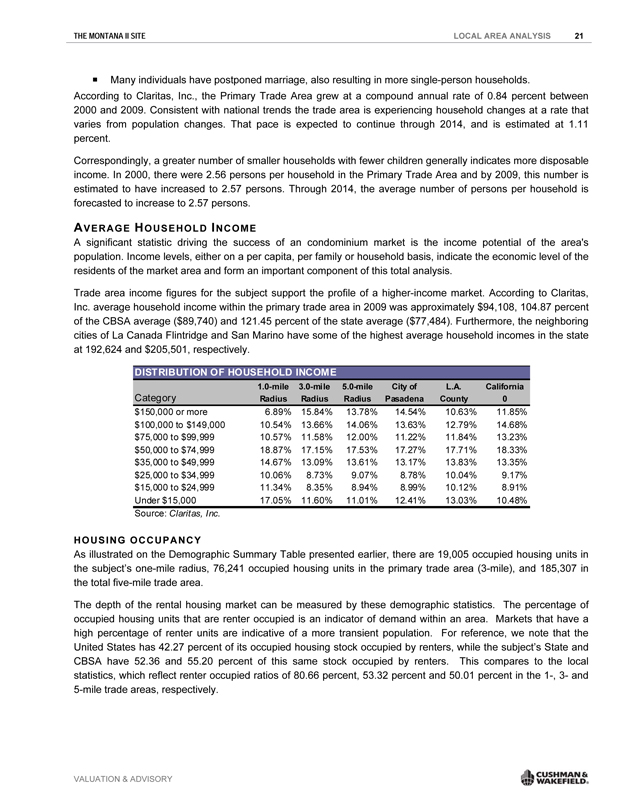

A significant statistic driving the success of an condominium market is the income potential of the area’s population. Income levels, either on a per capita, per family or household basis, indicate the economic level of the residents of the market area and form an important component of this total analysis.

Trade area income figures for the subject support the profile of a higher-income market. According to Claritas, Inc. average household income within the primary trade area in 2009 was approximately $94,108, 104.87 percent of the CBSA average ($89,740) and 121.45 percent of the state average ($77,484). Furthermore, the neighboring cities of La Canada Flintridge and San Marino have some of the highest average household incomes in the state at 192,624 and $205,501, respectively.

DISTRIBUTION OF HOUSEHOLD INCOME

1.0-mile 3.0-mile 5.0-mile City of L.A. California

Category Radius Radius Radius Pasadena County 0

$150,000 or more 6.89% 15.84% 13.78% 14.54% 10.63% 11.85%

$100,000 to $149,000 10.54% 13.66% 14.06% 13.63% 12.79% 14.68%

$75,000 to $99,999 10.57% 11.58% 12.00% 11.22% 11.84% 13.23%

$50,000 to $74,999 18.87% 17.15% 17.53% 17.27% 17.71% 18.33%

$35,000 to $49,999 14.67% 13.09% 13.61% 13.17% 13.83% 13.35%

$25,000 to $34,999 10.06% 8.73% 9.07% 8.78% 10.04% 9.17%

$15,000 to $24,999 11.34% 8.35% 8.94% 8.99% 10.12% 8.91%

Under $15,000 17.05% 11.60% 11.01% 12.41% 13.03% 10.48%

Source: Claritas, Inc.

HOUSING OCCUPANCY

As illustrated on the Demographic Summary Table presented earlier, there are 19,005 occupied housing units in the subject’s one-mile radius, 76,241 occupied housing units in the primary trade area (3-mile), and 185,307 in the total five-mile trade area.

The depth of the rental housing market can be measured by these demographic statistics. The percentage of occupied housing units that are renter occupied is an indicator of demand within an area. Markets that have a high percentage of renter units are indicative of a more transient population. For reference, we note that the United States has 42.27 percent of its occupied housing stock occupied by renters, while the subject’s State and CBSA have 52.36 and 55.20 percent of this same stock occupied by renters. This compares to the local statistics, which reflect renter occupied ratios of 80.66 percent, 53.32 percent and 50.01 percent in the 1-, 3- and 5-mile trade areas, respectively.

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE LOCAL AREA ANALYSIS 22

EMPLOYMENT

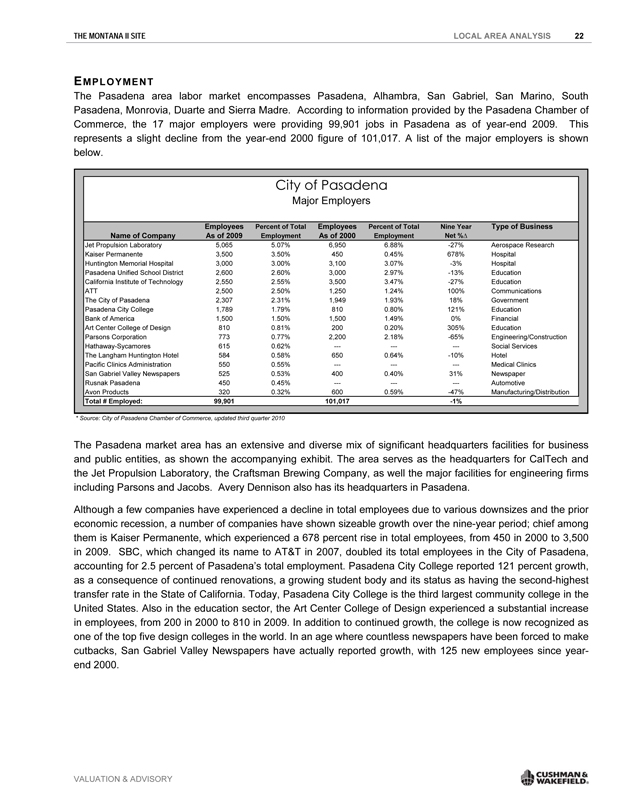

The Pasadena area labor market encompasses Pasadena, Alhambra, San Gabriel, San Marino, South Pasadena, Monrovia, Duarte and Sierra Madre. According to information provided by the Pasadena Chamber of Commerce, the 17 major employers were providing 99,901 jobs in Pasadena as of year-end 2009. This represents a slight decline from the year-end 2000 figure of 101,017. A list of the major employers is shown below.

City of Pasadena

Major Employers

Employees Percent of Total Employees Percent of Total Nine Year Type of Business

Name of Company As of 2009 Employment As of 2000 Employment Net %

Jet Propulsion Laboratory 5,065 5.07% 6,950 6.88% -27% Aerospace Research

Kaiser Permanente 3,500 3.50% 450 0.45% 678% Hospital

Huntington Memorial Hospital 3,000 3.00% 3,100 3.07% -3% Hospital

Pasadena Unified School District 2,600 2.60% 3,000 2.97% -13% Education

California Institute of Technology 2,550 2.55% 3,500 3.47% -27% Education

ATT 2,500 2.50% 1,250 1.24% 100% Communications

The City of Pasadena 2,307 2.31% 1,949 1.93% 18% Government

Pasadena City College 1,789 1.79% 810 0.80% 121% Education

Bank of America 1,500 1.50% 1,500 1.49% 0% Financial

Art Center College of Design 810 0.81% 200 0.20% 305% Education

Parsons Corporation 773 0.77% 2,200 2.18% -65% Engineering/Construction

Hathaway-Sycamores 615 0.62% -— -— -— Social Services

The Langham Huntington Hotel 584 0.58% 650 0.64% -10% Hotel

Pacific Clinics Administration 550 0.55% -— -— -— Medical Clinics

San Gabriel Valley Newspapers 525 0.53% 400 0.40% 31% Newspaper

Rusnak Pasadena 450 0.45% -— -— -— Automotive

Avon Products 320 0.32% 600 0.59% -47% Manufacturing/Distribution

Total # Employed: 99,901 101,017 -1%

* Source: City of Pasadena Chamber of Commerce, updated third quarter 2010

The Pasadena market area has an extensive and diverse mix of significant headquarters facilities for business and public entities, as shown the accompanying exhibit. The area serves as the headquarters for CalTech and the Jet Propulsion Laboratory, the Craftsman Brewing Company, as well the major facilities for engineering firms including Parsons and Jacobs. Avery Dennison also has its headquarters in Pasadena.

Although a few companies have experienced a decline in total employees due to various downsizes and the prior economic recession, a number of companies have shown sizeable growth over the nine-year period; chief among them is Kaiser Permanente, which experienced a 678 percent rise in total employees, from 450 in 2000 to 3,500 in 2009. SBC, which changed its name to AT&T in 2007, doubled its total employees in the City of Pasadena, accounting for 2.5 percent of Pasadena’s total employment. Pasadena City College reported 121 percent growth, as a consequence of continued renovations, a growing student body and its status as having the second-highest transfer rate in the State of California. Today, Pasadena City College is the third largest community college in the United States. Also in the education sector, the Art Center College of Design experienced a substantial increase in employees, from 200 in 2000 to 810 in 2009. In addition to continued growth, the college is now recognized as one of the top five design colleges in the world. In an age where countless newspapers have been forced to make cutbacks, San Gabriel Valley Newspapers have actually reported growth, with 125 new employees since year-end 2000.

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE LOCAL AREA ANALYSIS 23

BUSINESS DISTRICTS

Pasadena has three major business districts, including the Central Business District. This district employs nearly 60,000 employees in businesses ranging from small delicatessens to large engineering firms to distinctive antique shops.

The Central Business District includes four major areas of business and commercial development: 1) Old Town Pasadena, trend setting area of retail shops, restaurants, and movie theaters; 2) South Lake Avenue, upscale shopping and home to many financial institutions; 3) Civic Center, many government and civic buildings, and Paseo Colorado shopping mall; and 4) Pasadena Playhouse District, includes the Pasadena Playhouse, retail stores, bookstores, and the nation’s first two-story Target store.

Old Town Pasadena Civic Center

The Northwest Pasadena District has many service outlets, minority businesses, and processing or distribution companies. This Enterprise Zone offers various tax incentives to encourage growth of new and old businesses in the area. This area has two commercial areas: 1) North Lake Neighborhood Commercial District, a collection of retail stores, personal services, restaurants and food markets, and 2) Fair Oaks/Orange Grove Commercial District. A map of the Northwest Pasadena District is shown below.

The East Pasadena Business District serves as home for a number of the city’s high technology, light manufacturing, and processing/distributing companies including EarthLink Network, Inc. and Leon Max, Inc. This area also includes the Hastings Ranch Shopping Center, which includes a large retail outlet, supermarkets, specialty retail shops, and restaurants. A map of the East Pasadena Business District follows.

OTHER AREA ATTRACTIONS

The Pasadena area offers a variety of entertainment-oriented venues, including live theater and musical performances, museums and galleries, and an expanding array of shopping and dining opportunities. The City of Pasadena provides five entertainment facilities, which offer theatrical productions, symphony orchestras, and stand-up comedy.

Pasadena Playhouse is a registered historic landmark and continues to serve as the training ground for persons involved with theatrical, film, and television production.

The Pasadena Civic Auditorium is located on Green Street, just east of Marengo Avenue. The Pasadena Civic provides a seating capacity of 3,000 persons and is the host of the People’s Choice Awards and the annual Emmy awards for prime time television. Annual attendance at the civic auditorium is reported to be approximately 500,000 persons.

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE LOCAL AREA ANALYSIS 24

The Ambassador Auditorium is a 1,262-seat concert hall and serves as the host of approximately 115 concerts each season. Annual attendance at the Ambassador is reported to be in the range of 130,000 to 140,000 persons per year.

The Norton Simon Museum is located on Colorado Boulevard near the junction of the Ventura Freeway and the Foothill Freeway. The museum features European art, sculpture gardens, tours, and an extensive library. Annual attendance at the museum is reported at 130,000 persons.

The Huntington Library, Art Gallery & Botanical Gardens is a research and educational center serving scholars and the general public. The botanical gardens cover 150 acres of the property’s total land area of 207 acres, and feature 14,000 varieties of plants. The art gallery contains one of the most extensive collections of British and French 18th Century art of any gallery in the country.

OLD TOWN PASADENA

One of the more popular visitor attractions in Pasadena is the Old Pasadena Historic District. The Old Town Pasadena district is an area of approximately 20 square blocks, providing a diverse blend of retail, dining and entertainment opportunities. The Old Pasadena area is listed on the National Register of Historic Places and is a redevelopment project of the City of Pasadena. Old Pasadena is centered along Colorado Boulevard between Pasadena Avenue (to the west) and Arroyo Parkway (to the east). The northern boundary of Old Pasadena is Corson Avenue and the southern boundary is Del Mar Avenue. The primary contribution from the city in the redevelopment of the area has been the construction of several new parking structures, which have provided an additional incentive for retailers and restaurateurs to renovate many of the existing commercial buildings in the area. Most of the shops in the area are open late at night to accommodate dinner and theater patrons of the local restaurants and theatres. The attractiveness of this location is evidenced by the number of high profile retailers which have opened for business in the area, which includes Tiffany’s & Co., Forever XXI, Crate & Barrel, The Gap, Banana Republic, Il Fornaio, Apple, Cheesecake Factory, Restoration Hardware, Urban Outfitters, Barnes & Noble, Diesel, Guess, Chico’s, J. Crew, Armani Exchange, and Victoria Secret. Along with these high profile retail vendors, Old Town Pasadena is now home to the newly opened Gold Class Cinemas at One Colorado. The result of a complete renovation of the old Laemmle’s theater, Gold Class Cinemas features first run movies and theaters equipped with oversized reclining seats and a full-service bar and restaurant, where patrons can order a wide array of dishes and alcoholic beverages.

ROSE BOWL

Perhaps the most widely recognized Pasadena landmark is the Rose Bowl. The Rose Bowl is located in the northwestern portion of Pasadena, approximately one mile north of the Ventura Freeway and one half mile west of Orange Grove Boulevard. The facility is the home field for the UCLA football team during the fall season, and is the site of the annual Rose Bowl Game on New Year’s Day.

PASEO COLORADO

Paseo Colorado is a mixed-use retail “destination” center which combines residential uses with retail and entertainment uses. The retail component consists of a pedestrian-oriented, two-level shopping center with an open-air layout. The center includes a cinema, and an upscale supermarket and a health club, as well as a major department store (Macy’s). Other significant tenants include national retailers Eddie Bauer, BCBG, Sephora and Ann Taylor Loft, Kay-Bee Toys, and several restaurants.

Other world-class institutions in Pasadena include Pacific Asia Museum, California Institute of Technology, the Jet Propulsion Laboratory, Tournament House (Wrigley Mansion and Gardens) and the Annual Tournament of Roses Parade.

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE LOCAL AREA ANALYSIS 25

SURROUNDING LAND USES

The subject property is located on the southeast corner of Union Street and Euclid Avenue just south of the Pasadena Civic Center and north of Paseo Colorado. This location is less than one-half mile east of Old Town Pasadena, one block north of Colorado Boulevard, and three blocks south of the I-210 Freeway. Western Asset Plaza – a professional office building with ground floor retail tenants including Morton’s Steakhouse—is located directly east and south of the subject. The subject has a very dynamic location with various amenities including restaurants, shopping, government facilities and good quality multi-family residential uses.

CONCLUSION

The subject location in the northern/central portion of Los Angeles County provides for good access to outlying areas in the greater Los Angeles area by way of the extensive southern California freeway system. The subject property is within close proximity to several visitor draws into the Pasadena area, including entertainment, shopping, hotels, and dining opportunities. The overall outlook for the subject property over the long-term is positive.

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

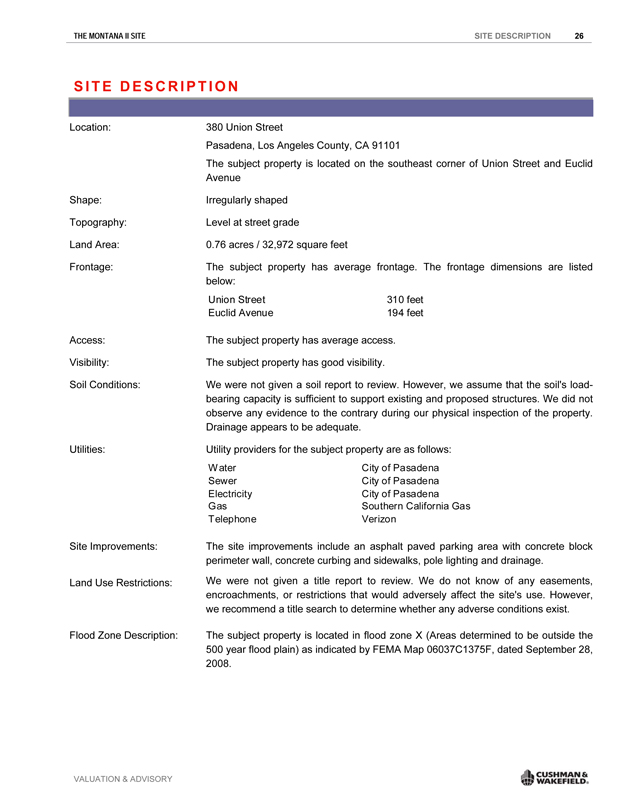

THE MONTANA II SITE SITE DESCRIPTION 26

SITE DESCRIPTION

Location: 380 Union Street

Pasadena, Los Angeles County, CA 91101 The subject property is located on the southeast corner of Union Street and Euclid Avenue

Shape: Irregularly shaped

Topography: Level at street grade

Land Area: 0.76 acres / 32,972 square feet

Frontage: The subject property has average frontage. The frontage dimensions are listed below:

Union Street Euclid Avenue 310 feet 194 feet

Access: The subject property has average access.

Visibility: The subject property has good visibility.

Soil Conditions: We were not given a soil report to review. However, we assume that the soil’s load-bearing capacity is sufficient to support existing and proposed structures. We did not observe any evidence to the contrary during our physical inspection of the property. Drainage appears to be adequate.

Utilities: Utility providers for the subject property are as follows:

Water Sewer Electricity Gas Telephone City of Pasadena

City of Pasadena

City of Pasadena

Southern California Gas

Verizon

Site Improvements: The site improvements include an asphalt paved parking area with concrete block perimeter wall, concrete curbing and sidewalks, pole lighting and drainage.

Land Use Restrictions: We were not given a title report to review. We do not know of any easements, encroachments, or restrictions that would adversely affect the site’s use. However, we recommend a title search to determine whether any adverse conditions exist.

Flood Zone Description: The subject property is located in flood zone X (Areas determined to be outside the 500 year flood plain) as indicated by FEMA Map 06037C1375F, dated September 28, 2008.

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE SITE DESCRIPTION 27

Wetlands: We were not given a wetlands survey to review. If subsequent engineering data reveal the presence of regulated wetlands, it could materially affect property value. We recommend a wetlands survey by a professional engineer with expertise in this field.

Seismic Hazard: The site is not located in a Special Study Zone as established by California’s Alquist-Priolo Geological Hazards Act.

Hazardous Substances: We observed no evidence of toxic or hazardous substances during our inspection of the site. However, we are not trained to perform technical environmental inspections and recommend the hiring of a professional engineer with expertise in this field.

Overall Site Utility: The subject site is functional for its current use.

Location Rating: Excellent

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

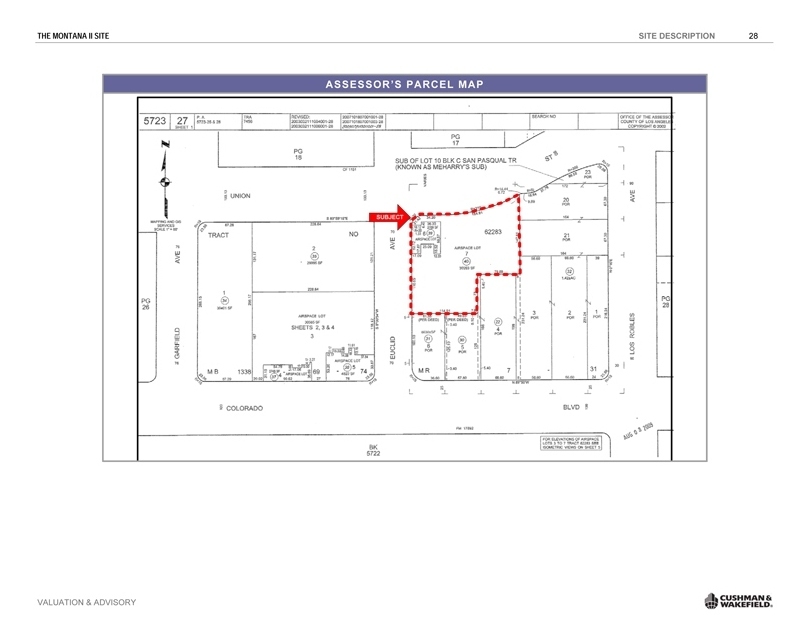

|

THE MONTANA II SITE SITE DESCRIPTION 28

ASSESSOR’S PARCEL MAP

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

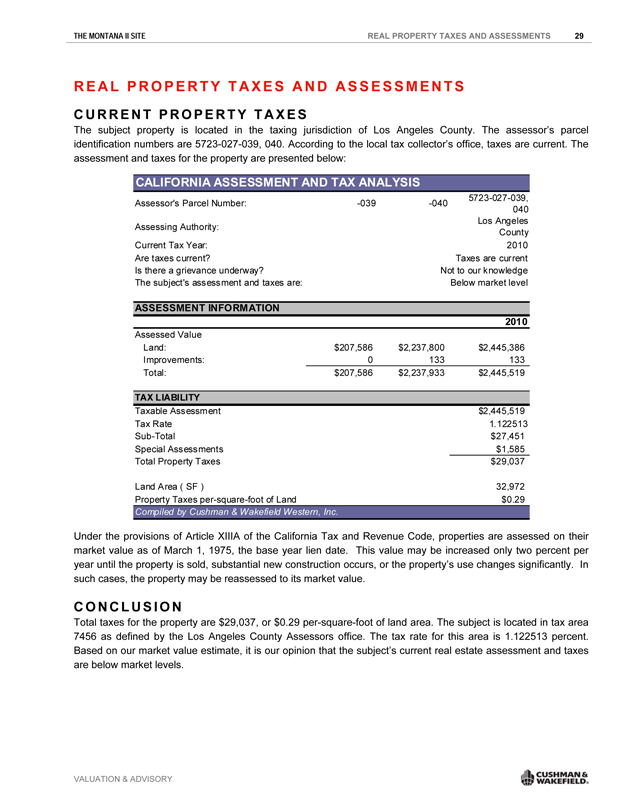

THE MONTANA II SITE REAL PROPERTY TAXES AND ASSESSMENTS 29

REAL PROPERTY TAXES AND ASSESSMENTS

CURRENT PROPERTY TAXES

The subject property is located in the taxing jurisdiction of Los Angeles County. The assessor’s parcel identification numbers are 5723-027-039, 040. According to the local tax collector’s office, taxes are current. The assessment and taxes for the property are presented below:

CALIFORNIA ASSESSMENT AND TAX ANALYSIS

Assessor’s Parcel Number: -039 -040 5723-027-039, 040

Assessing Authority: Los Angeles County

Current Tax Year: 2010

Are taxes current? Taxes are current

Is there a grievance underway? Not to our knowledge

The subject’s assessment and taxes are: Below market level

ASSESSMENT INFORMATION

Assessed Value

Land: $207,586 $2,237,800 $2,445,386

Improvements: 0 133 133

Total: $207,586 $2,237,933 $2,445,519

TAX LIABILITY

Tax Rate 1.122513

Sub-Total $27,451

Special Assessments $1,585

Total Property Taxes $29,037

Land Area ( SF ) 32,972

Property Taxes per-square-foot of Land $0.29

Compiled by Cushman & Wakefield Western, Inc.

Under the provisions of Article XIIIA of the California Tax and Revenue Code, properties are assessed on their market value as of March 1, 1975, the base year lien date. This value may be increased only two percent per year until the property is sold, substantial new construction occurs, or the property’s use changes significantly. In such cases, the property may be reassessed to its market value.

CONCLUSION

Total taxes for the property are $29,037, or $0.29 per-square-foot of land area. The subject is located in tax area 7456 as defined by the Los Angeles County Assessors office. The tax rate for this area is 1.122513 percent. Based on our market value estimate, it is our opinion that the subject’s current real estate assessment and taxes are below market levels.

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

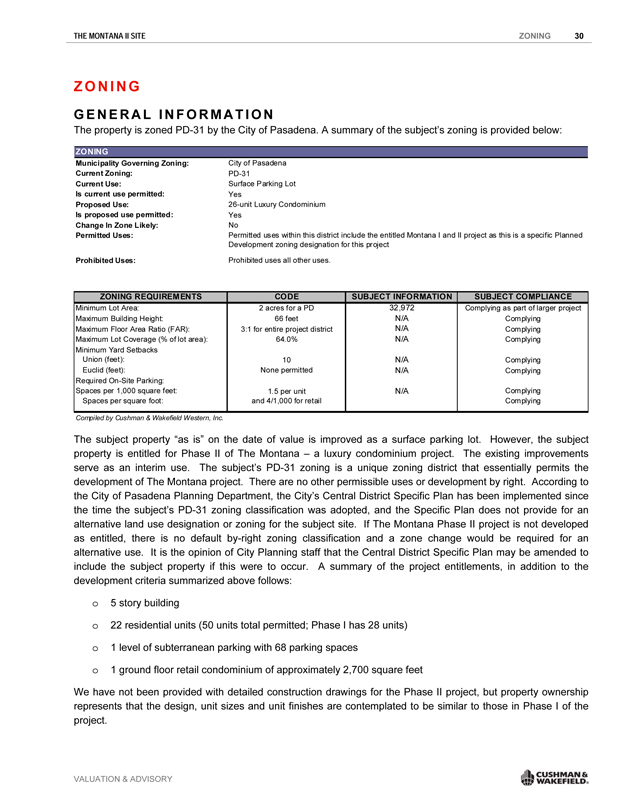

THE MONTANA II SITE ZONING 30

ZONING

GENERAL INFORMATION

The property is zoned PD-31 by the City of Pasadena. A summary of the subject’s zoning is provided below:

ZONING

ZONING

Municipality Governing Zoning: City of Pasadena

Current Zoning: PD-31

Current Use: Surface Parking Lot

Is current use permitted: Yes

Proposed Use: 26-unit Luxury Condominium

Is proposed use permitted: Yes

Change In Zone Likely: No

Permitted Uses: Permitted uses within this district include the entitled Montana I and II project as this is a specific Planned

Development zoning designation for this project

Prohibited Uses: Prohibited uses all other uses.

ZONING REQUIREMENTS CODE SUBJECT INFORMATION SUBJECT COMPLIANCE

Minimum Lot Area: Maximum Building Height: Maximum Floor Area Ratio (FAR): Maximum Lot Coverage (% of lot area): Minimum Yard Setbacks Union (feet): Euclid (feet): Required On-Site Parking: Spaces per 1,000 square feet: Spaces per square foot: 2 acres for a PD

66 feet

3:1 for entire project district

64.0%

10

None permitted

1.5 per unit

and 4/1,000 for retail 32,972

N/A

N/A

N/A

N/A

N/A

N/A Complying as part of larger project Complying Complying

Complying

Complying

Complying

Complying

Complying

Compiled by Cushman & Wakefield Western, Inc.

The subject property “as is” on the date of value is improved as a surface parking lot. However, the subject property is entitled for Phase II of The Montana – a luxury condominium project. The existing improvements serve as an interim use. The subject’s PD-31 zoning is a unique zoning district that essentially permits the development of The Montana project. There are no other permissible uses or development by right. According to the City of Pasadena Planning Department, the City’s Central District Specific Plan has been implemented since the time the subject’s PD-31 zoning classification was adopted, and the Specific Plan does not provide for an alternative land use designation or zoning for the subject site. If The Montana Phase II project is not developed as entitled, there is no default by-right zoning classification and a zone change would be required for an alternative use. It is the opinion of City Planning staff that the Central District Specific Plan may be amended to include the subject property if this were to occur. A summary of the project entitlements, in addition to the development criteria summarized above follows:

o 5 story building

o 22 residential units (50 units total permitted; Phase I has 28 units)

o 1 level of subterranean parking with 68 parking spaces

o 1 ground floor retail condominium of approximately 2,700 square feet

We have not been provided with detailed construction drawings for the Phase II project, but property ownership represents that the design, unit sizes and unit finishes are contemplated to be similar to those in Phase I of the project.

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE ZONING 31

CONCLUSION

We analyzed the zoning requirements in relation to the subject property, and considered the compliance of the existing and proposed use. We are not experts in the interpretation of complex zoning ordinances but based on our review of public information, the subject property as proposed appears to be a complying use.

Detailed zoning studies are typically performed by a zoning or land use expert, including attorneys, land use planners, or architects. The depth of our study correlates directly with the scope of this assignment, and it considers all pertinent issues that have been discovered through our due diligence.

We note that this appraisal is not intended to be a detailed determination of compliance, as that determination is beyond the scope of this real estate appraisal assignment.

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE HIGHEST AND BEST USE 32

HIGHEST AND BEST USE

HIGHEST AND BEST USE DEFINITION

The Dictionary of Real Estate Appraisal, Fifth Edition (2010), a publication of the Appraisal Institute, defines the highest and best use as:

The most probable use of a property which is physically possible, appropriately justified, legally permissible, financially feasible, and which results in the highest value of the property being valued.

To determine the highest and best use we typically evaluate the subject site under two scenarios: as vacant land and as presently improved. In both cases, the property’s highest and best use must meet the four criteria described above. Since this property is land only, evaluating it as presently improved is not applicable.

HIGHEST AND BEST USE OF PROPERTY AS VACANT

We considered the legal issues related to zoning and legal restrictions. We also analyzed the physical characteristics of the site to determine what legal uses would be possible, and considered the financial feasibility of these uses to determine the use that is maximally productive.

Financially feasible uses are those uses that can generate a profit over and above the cost of acquiring the site, and constructing the improvements. Determining the value of a property upon completion of new construction requires an in-depth analysis of the condition of the local market, the location of the subject property, the proposed use of the property, its market position, level of pre-sale, an estimate for absorption, leasing/sale costs, operating expenses, market vacancy and sales prices or rental rates.

Our analysis indicates that under current market conditions, the legally permissible use of the site under zoning (proposed project) is not a viable development due to the lack of available construction financing, the achievable sale prices, slow absorption and oversupply for ultra-luxury units relative to demand. These factors, when combined, essentially eliminate the entrepreneurial incentive necessary to attract investment. In today’s market, a prudent investor would hold the site until market conditions improve to the point where the entitled project is financially feasible. Therefore, considering the subject site’s physical characteristics and location, as well as the state of the local market, it is our opinion that the Highest and Best Use of the subject site as though vacant is hold until market conditions improve and entitled project can be feasibly developed

HIGHEST AND BEST USE OF PROPERTY AS IMPROVED

The Dictionary of Real Estate Appraisal defines highest and best use of the property as improved as:

The use that should be made of a property as it exists. An existing improvement should be renovated or retained as is so long as it continues to contribute to the total market value of the property, or until the return from a new improvement would more than offset the cost of demolishing the existing building and constructing a new one.

In analyzing the Highest and Best Use of a property as improved, it is recognized that the improvements should continue to be used until it is financially advantageous to alter physical elements of the structure or to demolish it and build a new one.

It is our opinion that the existing surface parking lot use is an interim use. It is our opinion that the Highest and Best Use of the subject property as improved is hold until market conditions improve and entitled project can be feasibly developed.

VALUATION & ADVISORY CUSHMAN & WAKEFIELD®

THE MONTANA II SITE VALUATION PROCESS 33

VALUATION PROCESS

METHODOLOGY

There are three generally accepted approaches to developing an opinion of value: Cost, Sales Comparison and Income Capitalization. We considered each in this appraisal to develop an opinion of the market value of the subject property. In appraisal practice, an approach to value is included or eliminated based on its applicability to the property type being valued and the quality of information available. The reliability of each approach depends on the availability and comparability of market data as well as the motivation and thinking of purchasers.

The valuation process is concluded by analyzing each approach to value used in the appraisal. When more than one approach is used, each approach is judged based on its applicability, reliability, and the quantity and quality of its data. A final value opinion is chosen that either corresponds to one of the approaches to value, or is a correlation of all the approaches used in the appraisal.

We considered each approach in developing our opinion of the market value of the subject property. We discuss each approach below and conclude with a summary of their applicability to the subject property.

SUMMARY