Donald E. Morel, Jr., Ph.D.

Chairman and Chief Executive Officer

West Pharmaceutical Services

William J. Federici

Vice President & Chief Financial Officer

West Pharmaceutical Services

NYSE: WST

westpharma.com

CL King's 5th Annual

BEST IDEAS CONFERENCE 2007

Certain statements contained in this presentation and certain statements that may be made by management of the

Company orally during this presentation contains some forward-looking statements that set forth anticipated results based on

management’s plans and assumptions. Such statements give our current expectations or forecasts of future events – they do

not relate strictly to historical or current facts. We have tried, wherever possible, to identify such statements by using words

such as “estimate,” “expect,” “intend,” “believe,” “plan,” “anticipate” and other words and terms of similar meaning in

connection with any discussion of future operating or financial performance or condition.

We cannot guarantee that any forward-looking statement will be realized. If known or unknown risks or uncertainties

materialize, or if underlying assumptions are inaccurate, actual results could differ materially from past results and those

expressed or implied in any forward-looking statement. You should bear this in mind as you consider forward-looking

statements. We cannot predict or identify all such risks and uncertainties, but factors that could cause the actual results to

differ materially from expected and historical results include the following: Sales demand; the timing, regulatory approval and

commercial success of customers’ products incorporating our products and services, including specifically, the Exubera®

Inhalation-Powder insulin device; customers’ changes to inventory requirements and manufacturing plans that alter existing

orders or ordering patterns for our products; our ability to pass raw-material cost increases on to customers through price

increases; maintaining or improving production efficiencies and overhead absorption; physical limits on manufacturing

capacity that may limit our ability to satisfy anticipated demand; the timeliness and effects of capacity expansions, including

the effects of delays associated with construction, availability and price of capital goods, and necessary internal, governmental

and customer approvals; the availability of labor to meet increased demand; competition from other providers; the timely and

successful negotiations of sales contracts with four of the Company’s largest customers during the second half of 2007,

average profitability, or mix, of products sold in any reporting period; financial performance of unconsolidated affiliates;

strength of the U.S. dollar in relation to other currencies, particularly the Euro, UK Pound, Danish Krone, Japanese Yen and

Singapore Dollar; changing interest rates and investment returns that can affect the Company’s cost of funds and return on

invested funds; interruptions or weaknesses in our supply chain, which could cause delivery delays or restrict the availability

of raw materials and key bought-in components and finished products; raw-material price escalation, particularly petroleum-

based raw materials, and energy costs; availability and pricing of raw materials that may be affected by vendor concerns with

exposure to product-related liability; and, changes in tax law or loss of beneficial tax incentives.

We undertake no obligation to publicly update forward-looking statements, whether as a result of new information, future

events or otherwise.

Safe Harbor Statement

2

Corporate Profile

World’s premier manufacturer

of components and systems

for injectable drug delivery

Closure systems and prefillable

syringe components

Components for disposable

systems

Devices and device sub-

assemblies

Founded in 1923

HQ in Lionville, Pa.

2006 sales $913M

Market cap $1.3 billion

3

Diverse Customer Base

Company Estimated Market Share: 70% in Pharma; 70% in Device; 95% in Biotech

4

Global

Presence

32 manufacturing sites

34 sales offices

5 technical centers

Partner locations

Future China plants

6,000 employees

5

Key Company Developments

FY 2001 - 2005

New management team

Divestiture of non-core businesses

Focus returned to injectable packaging and delivery

Increased capital expenditures and capacity build in Europe

Strategic acquisitions

Strong revenue and profit growth

FY 2006

Debt restructuring

Integration of acquisitions

China initiative launched

Second European expansion

Strongest operating year in company history

FY 2007

Daikyo agreements extended to 2017

Issued $161.5 million of 4% convertible junior sub debt due 2047

Announced stock buy-back of up to 1 million shares

6

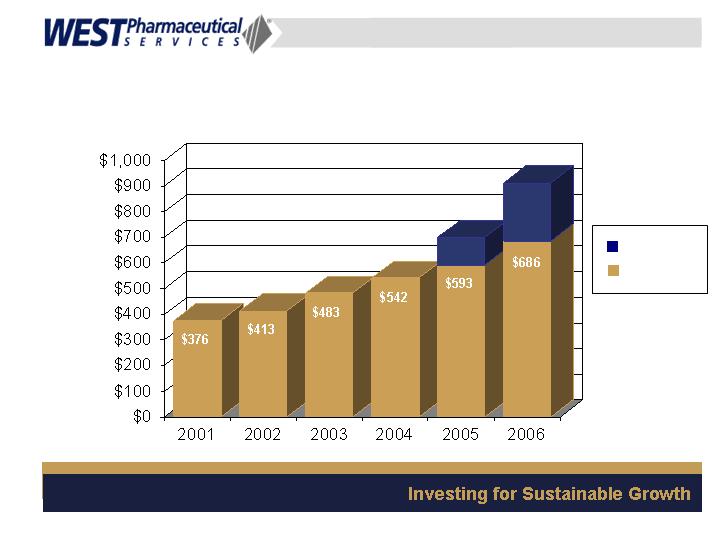

(in millions)

Strong Sales Growth

$227

Acquisitions

Core Business

$107

7

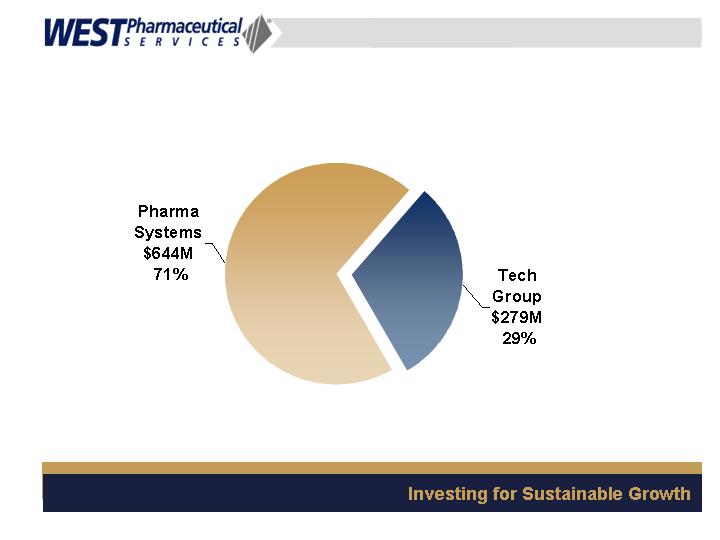

Segment Revenues

2006

8

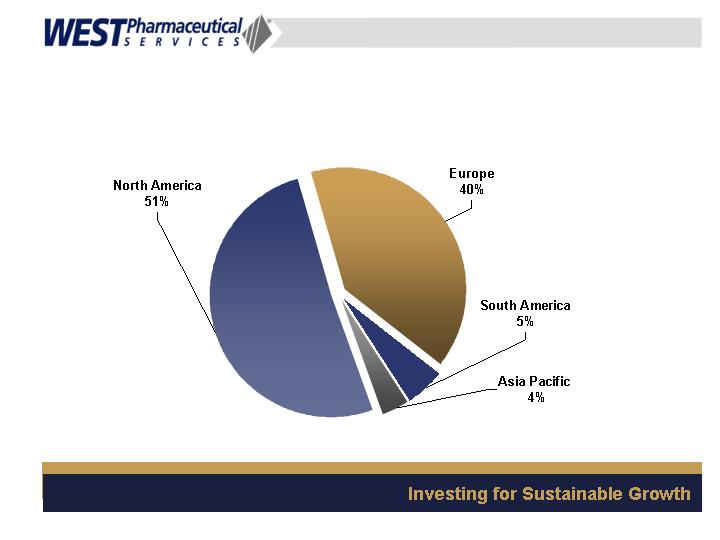

Geographic Sales Mix

9

Corporate Growth Strategy

Pharmaceutical Systems Segment

Market segmentation

Generate maximum value from key growth drivers

New product innovation

Lean manufacturing

Geographic expansion

Strategic acquisitions

Tech Group Segment

Leverage West customer base to build market share in multi-

material/multi-component systems for drug administration

Expand proprietary product portfolio through innovation and

strategic technology acquisitions

10

Market Dynamics Support West’s

Continued Growth

Increasing number of patients with chronic illnesses such as diabetes

and cancer

Increasing demand for biologics (2006 Market: $56B)*

Biologics: fastest growing segment of the pharma market out to 2010

(13% CAGR)*

Injectables currently account for ~15% of the global drug delivery market^

Combination products booming

Point of care shift: Hospital Specialty Clinic Home

Parenteral dosage form migration

*Source: Datamonitor

^Source: Arrowhead Publishers

11

Dosage Form Migration

Reconstitution

System

Vial – Stopper – Seal

Prefillable Syringe

Ampoule

Auto-injector

12

West’s Competitive Advantage

Unmatched experience/expertise: drug material interface

Ability to source components from multiple locations globally

Protected IP: West’s components and systems

Regulatory barrier to entry: NDA and ANDA filing must include reference

to all packaging/components in contact with the drug

1.

West Drug Master File (DMF) 1546 is confidential

2.

West DMF includes functionality data (multi-year studies)

3.

All primary package changes require new stability/functionality

studies for new filing

Engineering expertise in high-volume manufacturing and assembly

13

Strategic Objectives

Continue to maintain market leadership position in the

biotechnology market

Components for

Prefillable Syringes

* FluroTec technology is licensed from Daikyo Seiko, Ltd.

FluroTec* and

Barrier Coatings

Westar®

Processing

14

Strategic Objectives

Expand position in the insulin/diabetes care segment

Components for

Pen System Applications

Components for

Traditional System

Applications

Devices

15

Strategic Objectives

Aggressively expand IP position via innovation and

selective acquisitions

Anti-Counterfeiting

Closures

Reconstitution Systems

Daikyo Crystal Zenith*

Systems

* Daikyo Crystal Zenith technology is licensed from Daikyo Seiko, Ltd.

16

Strategic Objectives

Build manufacturing capabilities to meet market growth

17

Create financial flexibility through conservative balance

sheet management

Strategic Objectives

18

Prior Years’ Results

($M except per share)

$46.0

$61.5

Income from Continuing Operations

$1.41

$1.93

E.P.S. Continuing Operations –

Non-GAAP

$73.4

$101.0

Operating Profit

$120.3

$155.9

SG&A

27.7%

28.7%

Gross Margin

$699.7

$913.3

Net Sales

2005

2006

2006 E.P.S. continuing operations – Non-GAAP excludes a $0.12 charge related to the refinancing of debt obligations

and a $0.02 favorable tax benefit related to the settlement of a prior year tax claim.

19

June 30, 2007 Year-to-Date Results

($M except per share)

$35.0

$53.0

Income from Continuing

Operations

$1.15

$1.45

Non-GAAP E.P.S. from

Continuing Operations

$60.3

$74.4

Operating Profit

$71.2

$75.2

SG&A

30%

30%

Gross Margin

$463.0

$521.3

Net Sales

2006

2007

Non-GAAP EPS excludes 6 cents of discrete tax benefits from 2007 reported results and excludes a 12 cent charge for debt refinancing and a 2 cent

favorable tax benefit from 2006 reported results.

Capital Management

20

($M)

$90.3

$130.0

Full Year Capital Expenditures

31.1%

29.4%

Net Debt to Total Capital

$419.3

$499.1

Total Equity & Minority Int.

$236.3

$384.7

Total Debt

$47.1

$177.3

Cash

12/31/2006

6/30/2007

Manage core business growth

Segmentation/therapeutic category management

Improve Tech Group profit margins

Shift product mix: focus on healthcare and proprietary products

Maximize global capacity utilization

Execute on European capacity expansion and China initiative

Execute innovation programs

Operating Priorities

23

2007 Guidance – as of August 2, 2007

Revenues – approximately $1.0 billion

Estimated consolidated gross margin of 29%

Fully diluted earnings per share of $2.27 to $2.37

Excluding 6 cents discrete tax benefits

R&D spending increased to $17 million

Capital spending of $120 to $130 million

Summary

2007 on pace for approximately 20% growth in EPS

West’s competitive advantages uniquely position the

Company to capitalize on growth drivers in key market

segments

Global manufacturing capability

Solid balance sheet

Management incentives closely tied to growth in

shareholder value

Strong corporate governance (ranked #8 in Russell 3000)

25

Donald E. Morel, Jr., Ph.D.

Chairman and Chief Executive Officer

West Pharmaceutical Services

William J. Federici

Vice President & Chief Financial Officer

West Pharmaceutical Services

NYSE: WST

westpharma.com

CL King's 5th Annual

BEST IDEAS CONFERENCE 2007