First BanCorp Investor Presentation February 2014 Exhibit 99.1 |

Disclaimer 1 This presentation may contain “forward-looking statements” concerning the Corporation’s future economic performance. The words or phrases “expect,” “anticipate,” “look forward,” “should,” “believes” and similar expressions are meant to identify “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are subject to the safe harbor created by such sections. The Corporation wishes to caution readers not to place undue reliance on any such “forward-looking statements,” which speak only as of the date made, and to advise readers that various factors, including, but not limited to, the following could cause actual results to differ materially from those expressed in, or implied by such forward-looking statements: uncertainty about whether the Corporation and FirstBank will be able to fully comply with the written agreement dated June 3, 2010 that the Corporation entered into with the Federal Reserve Bank of New York (the “New York Fed”) and the consent order dated June 2, 2010 that FirstBank entered into with the FDIC and the Office of the Commissioner of Financial Institutions of the Commonwealth of Puerto Rico (the “FDIC Order”) that, among other things, require FirstBank to maintain certain capital levels and reduce its special mention, classified, delinquent, and non-performing assets; the risk of being subject to possible additional regulatory actions; uncertainty as to the availability of certain funding sources, such as brokered CDs; the Corporation’s reliance on brokered CDs and its ability to obtain, on a periodic basis, approval from the FDIC to issue brokered CDs to fund operations and provide liquidity in accordance with the terms of the FDIC Order; the risk of not being able to fulfill the Corporation’s cash obligations or resume paying dividends to the Corporation’s stockholders in the future due to the Corporation’s inability to receive approval from the New York Fed or the Board of Governors of the Federal Reserve System (“Federal Reserve Board”) to receive dividends from FirstBank or FirstBank’s failure to generate sufficient cash flow to make a dividend payment to the Corporation; the strength or weakness of the real estate markets and of the consumer and commercial credit sectors and their impact on the credit quality of the Corporation’s loans and other assets, which has contributed and may continue to contribute to, among other things, the high levels of non-performing assets, charge-offs, and provisions and may subject the Corporation to further risk from loan defaults and foreclosures; the ability of FirstBank to realize the benefit of the deferred tax asset; adverse changes in general economic conditions in Puerto Rico, the U.S., and the U.S. Virgin Islands and British Virgin Islands, including the interest rate environment, market liquidity, housing absorption rates, real estate prices, and disruptions in the U.S. capital markets, which may reduce interest margins, impact funding sources, and affect demand for all of the Corporation’s products and services and reduce the Corporation’s revenues, earnings, and the value of the Corporation’s assets; an adverse change in the Corporation’s ability to attract new clients and retain existing ones; a decrease in demand for the Corporation’s products and services and lower revenues and earnings because of the continued recession in Puerto Rico, the current fiscal problems and budget deficit of the Puerto Rico government and recent credit downgrades of the Puerto Rico government; a credit default by the Puerto Rico government or any of its public corporations or other instrumentalities, and recent and/or future downgrades of the long-term debt ratings of the Puerto Rico government, which could adversely affect economic conditions in Puerto Rico; the risk that any portion of the unrealized losses in the Corporation’s investment portfolio is determined to be other-than-temporary, including unrealized losses on Puerto Rico government obligations; uncertainty about regulatory and legislative changes for financial services companies in Puerto Rico, the U.S., and the U.S. Virgin Islands and British Virgin Islands, which could affect the Corporation’s financial condition or performance and could cause the Corporation’s actual results for future periods to differ materially from prior results and anticipated or projected results; changes in the fiscal and monetary policies and regulations of the federal government, including those determined by the Federal Reserve Board, the New York Fed, the FDIC, government-sponsored housing agencies, and regulators in Puerto Rico and the U.S. and British Virgin Islands; the risk of possible failure or circumvention of controls and procedures and the risk that the Corporation’s risk management policies may not be adequate; the risk that the FDIC may further increase the deposit insurance premium and/or require special assessments to replenish its insurance fund, causing an additional increase in the Corporation’s non-interest expenses; the impact on the Corporation’s results of operations and financial condition of acquisitions and dispositions; a need to recognize additional impairments on financial instruments, goodwill, or other intangible assets relating to acquisitions; the risks that downgrades in the credit ratings of the Corporation’s long-term senior debt will adversely affect the Corporation’s ability to access necessary external funds; the impact of the Dodd-Frank Wall Street Reform and Consumer Protection Act on the Corporation’s businesses, business practices, and cost of operations; the risk of losses in the value of investments in unconsolidated entities that the Corporation does not control; and general competitive factors and industry consolidation. The Corporation does not undertake, and specifically disclaims any obligation, to update any “forward-looking statements” to reflect occurrences or unanticipated events or circumstances after the date of such statements except as required by the federal securities laws. |

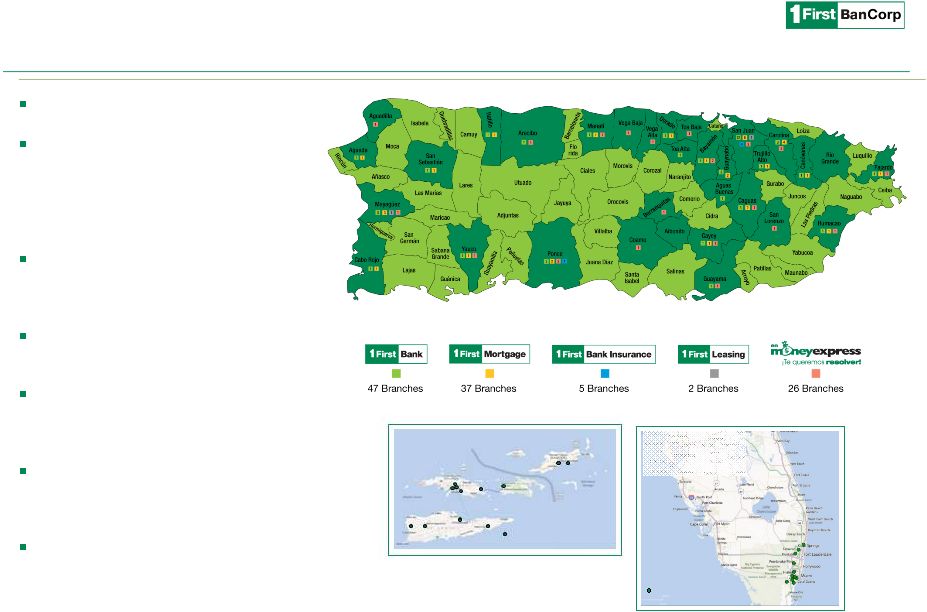

Eastern Caribbean: 7% of Assets Franchise Overview Founded in 1948 Headquartered in San Juan, Puerto Rico with operations in PR, Eastern Caribbean (Virgin Islands) and Florida – ~2,500 FTE employees (1) 2nd largest financial holding company in Puerto Rico with attractive business mix and substantial loan market share Florida presence with focus on serving south Florida region The largest depository institution in the Virgin Islands with approximately 40% market share 146 ATM machines and largest ATM network in the Eastern Caribbean Region (2) A well diversified operation with over 650,000 retail & commercial customers Well diversified with significant competitive strengths As of December 31, 2013. 1) FTE = Full Time Equivalent. 2) Eastern Caribbean Region or ECR includes United States and British Virgin Islands. 2 Total Assets - $12.7B Total Loans - $9.7B 12 bank branches 1 Loan Production Office SE Florida: 9% of Assets 28% of core deposits (3) 14% of core deposits (3) 12 bank branches 3 First Express branches Total Deposits - $9.9B 3) Data as of December 31, 2013. Core deposits excludes brokered CDs. |

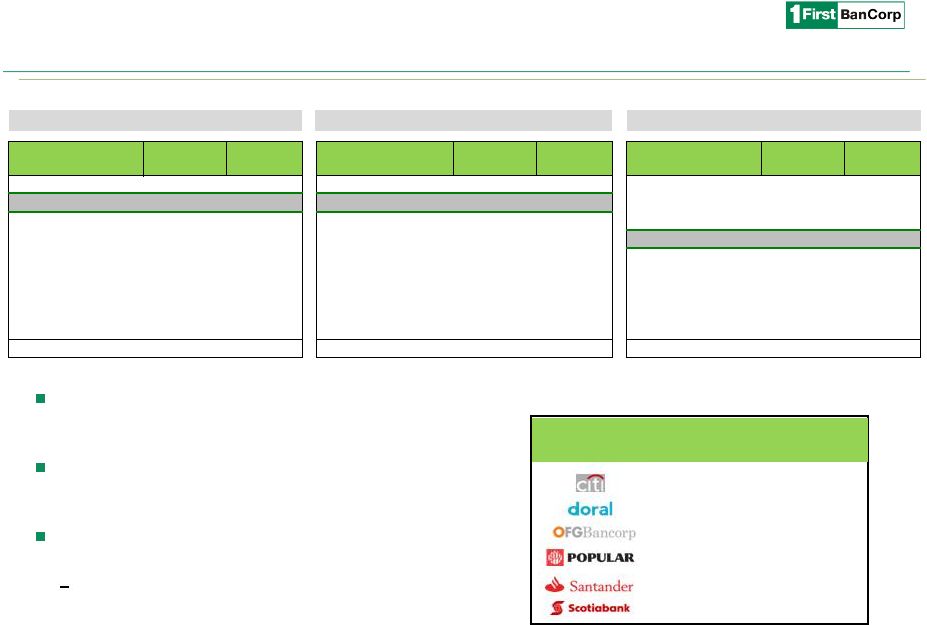

Franchise Overview ($ in millions) Well positioned Puerto Rico institution in a consolidating market Source: PR Market Share Report prepared with data provided by the Commissioner of Financial Institutions of Puerto Rico as of 9/30/13. 1) Puerto Rico only. 2) Calculated as institution bank branches within a mile of an FBP branch as a percentage of total institution branches. 3) Alphabetical order. 3 Puerto Rico Total Assets (1) Puerto Rico Total Loans (1) Puerto Rico Deposits, Net of Brokered (1) Strong and uniquely positioned franchise in densely populated regions of core operating footprint Strong market share in loan portfolios facilitates customer relationship expansion and cross-sell to increase deposit share Long-term opportunity for additional consolidation Branch overlap of greater than 40% with six Puerto Rico institutions (2) 1-mile branch overlap (3) 64 42 80% 42 47 44 Portfolio Balance Market Share Portfolio Balance Market Share Portfolio Balance Market Share 1 Banco Popular $25,305 39.7% 1 Banco Popular $18,951 38.7% 1 Banco Popular $17,478 44.1% 2 FirstBank 9,620 15.1% 2 FirstBank 8,081 16.5% 2 Banco Santander 5,585 14.1% 3 Oriental Bank 7,400 11.6% 3 Banco Santander 5,302 10.8% 3 Oriental Bank 4,832 12.2% 4 Scotiabank 6,805 10.7% 4 Oriental Bank 5,216 10.7% 4 FirstBank 3,886 9.8% 5 Banco Santander 6,707 10.5% 5 Scotiabank 4,958 10.1% 5 Scotiabank 3,467 8.7% 6 Doral Bank 5,363 8.4% 6 Doral Bank 2,776 5.7% 6 Citibank 2,011 5.1% 7 Citibank 2,011 3.2% 7 Other 2,732 5.6% 7 Doral Bank 1,954 4.9% 8 Banco Cooperativo 513 0.8% 8 Citibank 711 1.5% 8 Banco Cooperativo 430 1.1% 9 BBU 23 0.0% 9 Banco Cooperativo 183 0.4% 9 BBU 25 0.1% Total $63,746 100% Total $48,911 100% Total $39,669 100% Institutions Institutions Institutions |

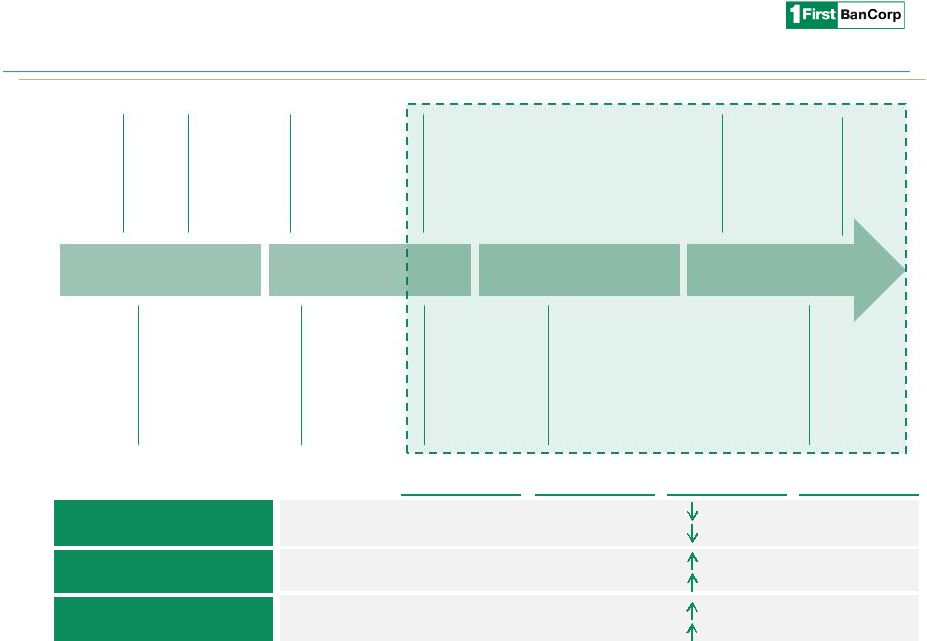

2009 2013 Change ('09-'13) % improvement NPAs $1,711 $725 $986 58% NPAs/assets 8.7% 5.7% 298 bps Tier 1 Common 4.1% 12.7% 862 bps 104% TCE / TA 3.2% 8.7% 551 bps 75% Core deposits $5,108 $6,738 $1,630 32% NIM 2.69% 4.11% 142 bps Our turnaround story Franchise Overview ($ in millions) De-Risking of Balance Sheet Capital Enhanced Franchise Value 4 June 2010: Written Agreement with the FED and Consent Order with FDIC July 2010: The U.S. Treasury exchanged TARP for convertible preferred August 2010: Exchange of 89% Perpetual Preferred Stock for Common February 2011: Sale of non- performing loans with a book value of $269 million Feb-April 2011: Sale of $330 million of MBS and $518 million of performing residential mortgages March 2013: Sale of non-performing loans with a book value of $217.7 million and entered two separate agreements for sale of NPLs with a book value of $99 million 2010 2011 2013 October 2011: Conversion of the shares held by the U.S. Treasury into 32.9 million shares of common stock May 2012: Acquisition of a $406 million portfolio of FirstBank-branded credit cards from FIA June 2013: Write-off of $66.6 million collateral pledged to Lehman, sale of NPLs with book value of $203.8 million and $19.2 million of OREO October 2011: Private placement of $525 million in common stock. Lead investors included Thomas H. Lee & Oaktree 2012 1) Represents change in dollar amount. (1) (1) (1) (1) August 2013: Completed secondary offering reducing ownership interest of U S Treasury and PE Investors |

Highlights Fiscal Year 2013 Effectively executing strategic plan as we continue to de-risk the balance sheet and focus efforts on strengthening our core franchise across our three geographies 5 * See reconciliation on page 21 – Use of Non GAAP Financial Measures position on the island in consumer and auto lending; and NPAs, down $513 million, or 41%, compared to FYE 2012; Completed two large bulk sale transactions in first half of 2013 with a loss $140.8 million; and Wrote-off assets pledged as collateral to Lehman. FYE 2013 loss of $164.5 million, impacted by accelerated balance sheet clean-up, adj. income * of $45.4 million; NIM improved 47 basis points to 4.11% compared to FYE 2012 through reduced funding costs; and Posted a strong pre-tax pre-provision income for 2013 of $184 million, still impacted by high credit cost. Increased $248 million, or 4%, during 2013; and Reduced reliance on brokered CDs by $233 million compared to FYE 2012. $3.7 billion of originations for 2013, an increase of approximately $600 million compared to 2012; Continued focus on rebuilding our credit card book, C&I and mortgage loans while strengthening our dominant Achieved loan growth in our Florida book. Asset Quality: Remains our top priority… Profitability: Achieved in second half of 2013 following bulk sale transactions… Core Deposits: Continued building product capabilities and deepening relationships… Loan Originations: Key strength of the franchise… Capital Position: Strong capital position allowing us to continue to address our legacy asset issues in a challenging economic environment. Our deferred tax asset valuation allowance is $523 million. |

Profitability • Adjusted net income of $18.5 million, excluding the aforementioned items. These results were also impacted by a $5.9 million loss in the equity of the unconsolidated entity and $7 million increase in write-downs to certain commercial OREO properties. • Net interest margin increased by 5 basis points to 4.25% driven by reductions in funding costs. • Pre-tax, pre-provision income of $47.6 million compared to $50.9 million in 3Q 2013. Asset Quality • Total NPAs decreased by $0.6 million compared to 3Q 2013. NPAs/Assets of 5.7%. No large held for sale loans or OREO sales were completed during the quarter. • Net charge-offs of $26.5 million, or an annualized 1.10% of average loans, compared to $33.9 million in the third quarter of 2013. Core Deposits • Deposits, net of government and brokered, increased by $17.4 million in 4Q 2013. • Government deposits decreased by $53.1 million in 4Q 2013. • Brokered certificates of deposit decreased by $38.5 million in 4Q 2013. Capital • Deferred Tax Asset valuation allowance of $523 million • Q4 2013 Capital position was further strengthened: Effectively Executing Strategic Plan Fourth Quarter 2013 6 – Risk Based Capital Ratio 17.1% compared to 16.9% in 3Q 2013 – Tier 1 Ratio 15.8% compared to 15.6% in 3Q 2013 – Leverage Ratio 11.7% compared to 11.7% in 3Q 2013 – Tier 1 Common Ratio 12.7% compared to 12.6% in 3Q 2013 – Tangible Common Equity Ratio 8.71% compared to 8.65% in 3Q 2013 • Net income of $14.8 million, or $0.07 per diluted share, including $2.5 million for attorneys’ fees awarded to the counterparty on the Lehman Brothers litigation and $1.4 million in branch consolidation and restructuring expenses. • Inflows of nonperforming loans increased by $10.4 million driven by residential mortgages and two large commercial loan relationships. • Provision for loan and lease losses of $23.0 million compared to $22.2 million in 3Q 2013. |

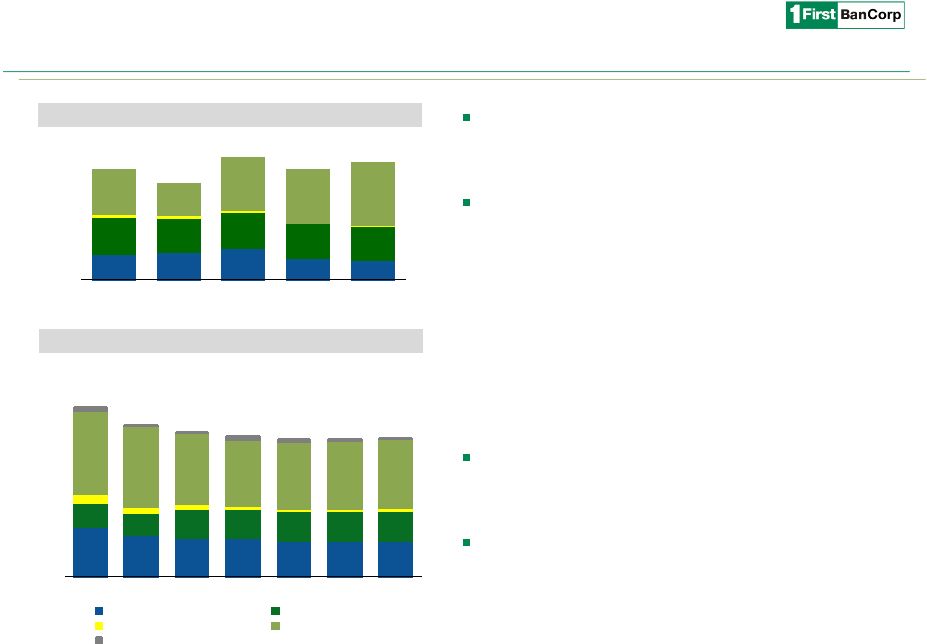

Core deposit growth strategy continues producing positive results; $1.6billion since 2009 Florida continues to be a strong funding source Focus remains on cross-selling opportunities Cost of deposits, net of brokered CDs, decreased to 0.81% Reduced reliance on brokered CDs $3.1 billion (32% of deposits) today vs. $7.4 billion (60%) in 2009 7 Core Deposits (1) Total Deposit Composition Cost of Deposits (1) Brokered CDs 32% Non-interest bearing 9% Interest bearing 59% 4Q 2013 1) Total Deposits excluding Brokered CDs. Opportunity for Earnings Growth Successful deposit growth over recent years Brokered CDs 60% Non-interest bearing 6% Interest bearing 34% 4Q 2009 2,381 2,477 2,654 2,776 2,842 774 763 915 1,108 1,136 1,505 2,090 2,126 2,077 2,054 448 470 481 529 706 $5,108 $5,800 $6,176 $6,490 $6,738 $0 $1,500 $3,000 $4,500 $6,000 2009 2010 2011 2012 2013 Retail Commercial CDs & IRA Public Funds ($ in millions) 0.81% 0.50% 1.00% 1.50% 2.00% 2009 2010 2011 2012 2013 Total Deposits, Net of Brokered 1.88% 1.56% 1.34% 0.97% |

3,417 2,874 2,747 2,714 2,511 2,519 2,549 1,716 1,562 2,013 2,020 2,047 2,059 2,067 701 428 362 223 195 164 169 5,822 5,695 4,932 4,604 4,692 4,766 4,852 301 16 85 276 238 115 76 $11,957 $10,575 $10,140 $9,836 $9,683 $9,623 $9,712 $0 $5,000 $10,000 $15,000 2010 2011 2012 1Q 2013 2Q 2013 3Q 2013 4Q 2013 Residential Consumer & Finance Leases Construction Commercial Loans Held for Sale 214 229 262 177 162 305 279 308 290 284 39 28 15 5 9 357 265 431 448 517 $914 $802 $1,016 $920 $972 $0 $220 $440 $660 $880 $1,100 4Q 2012 1Q 2013 2Q 2013 3Q 2013 4Q 2013 Continued focus on revenue generation through growth in commercial and consumer book following recent bulk sale transactions. Focus on increasing Consumer and Residential Mortgage market share & rebuilding our Commercial portfolio. – 4Q 2013 originations were strong at $972 million; and – Residential mortgage originations declined in second half of 2013 primarily driven by an increase in market interest rates and a reduction in new housing sales. Anticipating a more challenging market environment in Puerto Rico and have planned accordingly to achieve 2014 origination targets. Continue executing on Florida growth opportunities – $57 million increase in Florida C&I in 4Q 13 driven by new commercial strategies in the territory. 8 Loan Portfolio 1) Originations include purchases, refinancings, and draws from existing revolving and non-revolving commitments. Strong Origination Capabilities Loan Originations (1) ($ in millions) Rebuilding & replacing to achieve higher yielding portfolio |

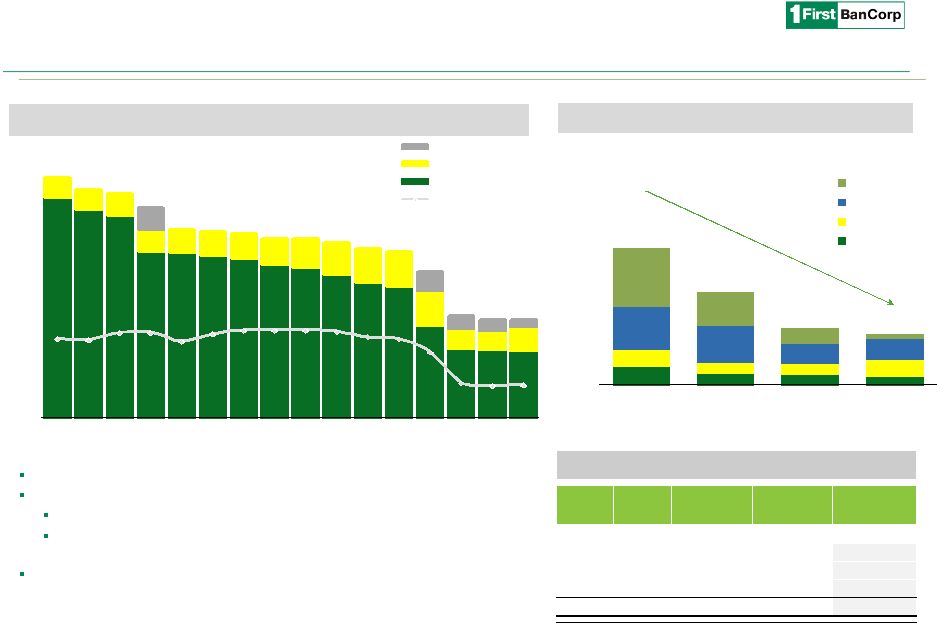

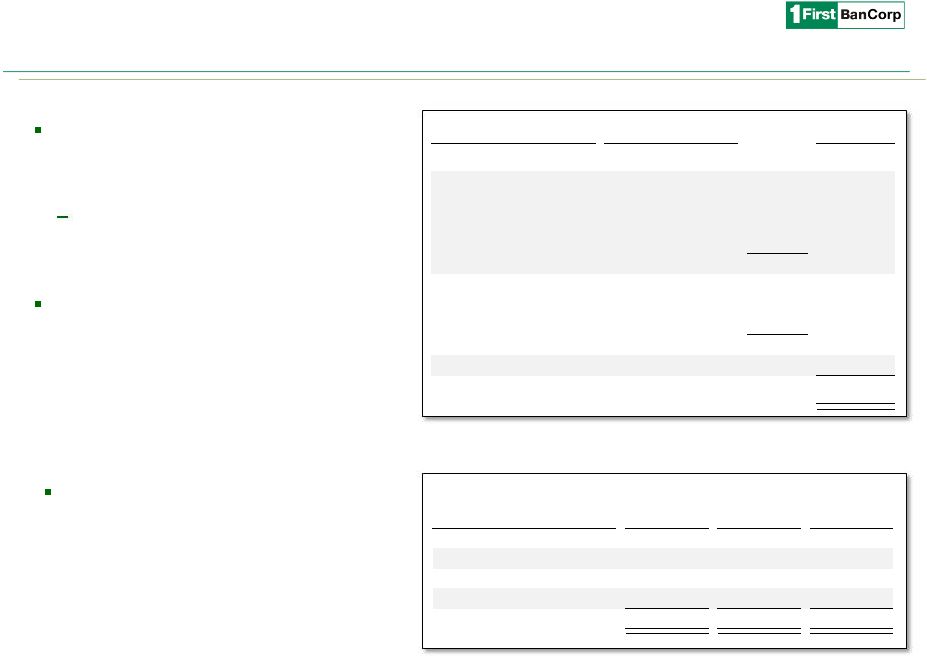

Continuing De-risking of the Balance Sheet 9 Net Charge-offs (NCO) (1) Non-performing Assets (NPA) NPAs are down over $1 billion, or 59%, since the peak in 1Q 2010 Recent actions (2013): Bulk sale of NPAs ($441m book value), resulting in NCOs of $197m Non-cash charge of $67m due to write-off of securities pledged to Lehman (2) ($ in millions) (3) 2010 2011 2012 2013 1,639 1,551 1,506 1,239 1,233 1,208 1,184 1,138 1,119 1,066 1,008 976 683 506 498 496 150 150 163 163 172 176 188 194 213 242 251 260 256 151 147 175 159 148 95 80 55 $1,790 $1,701 $1,669 $1,562 $1,410 $1,390 $1,377 $1,337 $1,332 $1,308 $1,259 $1,238 $1,087 $752 $726 $725 9.5% 10.0% 9.3% 10.2% 10.2% 9.6% 8.4% 5.7% 5.7% $0 $400 $800 $1,200 $1,600 $2,000 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q NPLs Held for Sale Repossessed Assets & Other Loans Held for Investment NPAs / Assets 63 39 37 29 54 38 35 56 142 118 67 68 186 101 41 7 $445 $295 $180 $161 $0 $200 $400 $600 2010 2011 2012 2013 Construction Commercial Consumer Residential Product Book Value Accumulated Charge-offs Reserves Net Carrying Amount (5) C&I $114.8 $50.6 $22.1 56.1% CRE 127.1 46.6 20.9 61.1% Const. 106.6 92.9 15.1 45.9% Total $348.6 $190.2 $58.1 53.9% Commercial Non-performing Loans (includes HFS) (4) Focus remains on organic reductions of nonperforming assets including the disposition of $230million of HFS and OREO Proactively managing asset quality 1) Excludes bulk sales. 2) Excludes $165 million of net charge-offs associated with the bulk sale to CPG in 2010. 3) Excludes $232 million of net-charge offs associated with the bulk asset sales and transfer of loans in 2013. 4) December 31, 2013. 5) Net Carrying Amount = % of carrying value net of reserves and accumulated charge-offs. |

Income Statement 4Q 2012 1Q 2013 2Q 2013 3Q 2013 4Q 2013 GAAP Net Interest Income 125.6 $ 124.5 $ 126.9 $ 130.9 $ 132.7 $ Provision for loan and lease losses 30.5 111.1 87.5 22.2 23.0 Non-interest income 20.1 19.1 14.3 16.0 18.4 Impairment of collateral pledged to Lehman (66.6) - - Equity in (losses) gains of unconsolidated entities (8.3) (5.5) 0.6 (5.9) (5.9) Non-interest expense 90.9 98.0 111.3 99.2 106.5 Pre-tax net income (loss) 16.0 (71.0) (123.6) 19.6 15.6 Income tax (expense) benefit (1.5) (1.6) 1.0 (3.7) (0.8) Net income (loss) 14.5 $ (72.6) $ (122.6) $ 15.9 $ 14.8 $ Adjusted Pre-tax pre-provision earnings 54.5 $ 50.5 $ 35.9 $ 50.9 $ 47.6 $ Net Interest Margin, (GAAP) (%) 3.91% 3.96% 4.04% 4.20% 4.25% Net income (loss) per common share-basic 0.07 $ (0.35) $ (0.60) $ 0.08 $ 0.07 $ Focus on Strategic Plan Rebuild earnings and de-risk balance sheet ($ in millions, except per share results) 10 1) See reconciliation on page 19. Net loss of $164.5 million compared to net income of $29.8 million in 2012 driven by: Net income of $14.8 million compared to $15.9 million in the third quarter Adjusted Net income $45.4 million, excluding these items, a 52% improvement over 2012. Adjusted net income of $18.5 million vs. $19.3 million in the 3rd quarter, excluding the impact of: Pre-tax pre-provision of $184 million compared to $179 million in 2012. Pre-tax pre-provision of $47.6 million compared to $50.9 million in the 3rd quarter impacted by higher OREO adjustments. Net interest income growth of $53.2 million and NIM improvement to 4.11% from 3.64% in 2012. Net interest income growth of $1.75 million and NIM improvement to 4.25% from 4.20%. Fiscal Year 2013 Fiscal Year 2013 Fourth Quarter 2013 Fourth Quarter 2013 Operating expenses increased $60 million largely due to: Operating expenses increase of $7.4 million driven by higher OREO value adjustments, the contingency for counterparty attorney fees on Lehman litigation, and higher credit card costs due to post conversion. (1) $140.8 million loss on bulk sales; and $69.1 million in charges on Lehman write-off & contingency for counterparty attorney' fees. Full year impact of credit cards operation & conversion costs; Bulk sale related expenses; and Higher OREO expenses - more cases moved to disposition state. $2.5MM legal contingency for fees awarded by the court to the other party; and $1.4 MM in restructuring charges on branch consolidations |

Opportunity for Earnings Growth Targeted strategies for growth 11 Puerto Rico Market Share (1) Puerto Rico Largest opportunity on deposit products, electronic banking & transaction services Growth in selected loan products for balanced risk/return to manage risk concentration and diversify income sources Diversifies revenue stream and loan portfolio composition Opportunity to broaden and deepen relationships SE Florida Continue focus in core deposit growth, commercial and transaction banking and conforming residential mortgages Recently hired corporate and commercial lending teams generating growth in loan portfolio Virgin Islands Auto / leasing 20% 2 Commercial 20% 2 Credit cards 18% 2 Mortgage originations 15% 3 Personal 8% 4 ACH Transactions 11% 5 ATM Terminals 10% 3 Debit Cards 7% 4 POS Terminals 12% 2 Branches 12% 4 Deposits 10% 4 Current Market Share Sept-13 Rank Opportunities for ongoing market share gains Recently acquired FirstBank-branded credit card portfolio Expansion prospects in Florida given long-term demographic trends Solidify leadership position by further increasing customer share of wallet 1) Source: Office of the Commissioner of Financial Institutions of Puerto Rico as of 9/30/13 and internal reports. |

Opportunity for Earnings Growth 12 Path to improved profitability Net Interest Income Improvement Cash liquidity re- investment $600MM currently yielding 28 bps Replacement of NPLs for performing loans Additional loan growth as economy recovers across our geographies Provision Reduction Currently 116bps of loans (excluding bulk sales) 2000-2008 weighted average provision of 98bps on loans Deposit fee income from expansion of transaction deposit base Non-interest bearing represents only 9% of deposit base Market share expansion of transaction processing POS Terminals, Debit cards, ACH transactions, ATM Terminals Credit costs of $50MM (1) for 2013 compared to 2008 annual expense of $23MM FDIC Cost reduction with credit profile improvement ($15 – 20 million annually) Fee Income Opportunities Operating Expense Reduction Long-term Efficiency Ratio Target of 55% 1) Represents net loss on REO operations and professional fees from collections, appraisals and other credit related fees. |

Key Investment Highlights 13 As of December 31, 2013. 1) See reconciliation to net income on page 19. 2) See reconciliation to total equity on page 20. 3) Assuming 100% reversal of Deferred Tax Asset Valuation Allowance of $523m; shares outstanding of 207m. See reconciliation to adjusted tangible book value on page 20. Improving core operating performance Average pre-tax pre-provision income for the last five quarters of approximately $48m NIM expanded 142 bps since 2009 to 4.11% in FYE 2013 Focus on stabilization of non-interest expenses; expected reduction in credit-related expense Healthy capital levels Tier 1 Common of $1.2bn or 12.7% and Tier 1 capital of 15.8% Tangible Book Value of $1.1bn or $5.30 / share Deferred Tax Asset Valuation Allowance of $523m; Adjusted Tangible Book Value of $7.83 / share Continuing de-risking of the balance sheet Total NPAs down over $1bn or 59% since peak in 1Q 2010 Focus remains on reductions of non-performing assets Opportunity for revenue expansion and earnings growth Strong loan origination capabilities ($3.7bn FYE 2013) Potential for NIM expansion through replacement of performing for NPLs Expected reduction in credit-related and other expenses (e.g., FDIC insurance) Expected benefits of branch rationalization in 2013 Increasing market share in fee generating products and services, consumer and mortgage loan originations Opportunity for commercial loan growth in SE Florida with hiring of commercial and corporate loan teams. Long-term potential for value creation from consolidation in Puerto Rico (1) (2) (3) |

Appendix |

Puerto Rico Government Exposure 15 As of December 31, 2013 ($ in millions) Total asset exposure to the Puerto Rico Government as of December 31, 2013 was approximately $470 million. Exposure supported by first lien on tax and operating revenues. In addition, there is $205 million of indirect exposure to the Tourism Development Fund supporting hotel projects. Total Government Deposits as of December 31, 2013 were $546 million. Total Government Unit Source of Repayment Outstanding Investment Portfolio 71.0 $ Central Government: Commonwealth Appropriations 26.9 Federal Funds 10.8 Tax & Revenue Anticipation Notes 75.0 Total Central Government (4 Loans) 112.7 Public Corporations: Operating Revenues 80.6 Rental Income 4.0 Total Public Corporations (4 Loans) 84.6 Municipalities (10 Loans) Property Tax Revenues 200.5 Total Direct Government Exposure 468.8 $ Government Unit Time Deposits Transaction Accounts Total Federal Funds - $ 8.9 $ 8.9 $ Municipalities 21.6 84.9 106.5 Public Agencies 4.2 191.0 195.3 Public Corporations 235.0 0.7 235.7 Total 260.8 $ 285.5 $ 546.4 $ |

Stock Profile 16 Trading Symbol: • FBP Exchange: • NYSE Share Price (2/10/14): • $4.90 Shares Outstanding (as of December 31, 2013): • 207,091,478 Market Capitalization (2/10/14): • $1.01 billion 1 Yr. Average Daily Volume: • 766,361 Price (2/10/14) to Tangible Book (12/31/13): • 0.92x Price (2/10/14) to Adjusted Tangible Book (1) (12/31/13): • 0.63x 1) Assuming 100% reversal of Deferred Tax Valuation Allowance of $520m; shares outstanding of 207m. 2) Includes the U.S. Treasury warrant that entitles it to purchase up to 1,285,899 shares of Common Stock at an exercise price of $3.29 per share, as adjusted as a result of the issuance of shares of Common Stock in the Corporation’s $525m private placement of Common Stock completed in October 2011. The exercise price and the number of shares issuable upon exercise of the warrant are subject to further adjustments under certain circumstances to prevent dilution. The warrant has a 10-year term from its issue date and is exercisable in whole or in part at any time. Beneficial Owner Amount Percent of Class Entities affiliated with Thomas H. Lee Partners, L.P. 41,851,067 20.2% Entities managed by Oaktree Capital Management, L.P. 41,847,284 20.2 United States Department of the Treasury (2) 20,941,797 10.1 Wellington Management Company, LLP 14,004,200 6.8 |

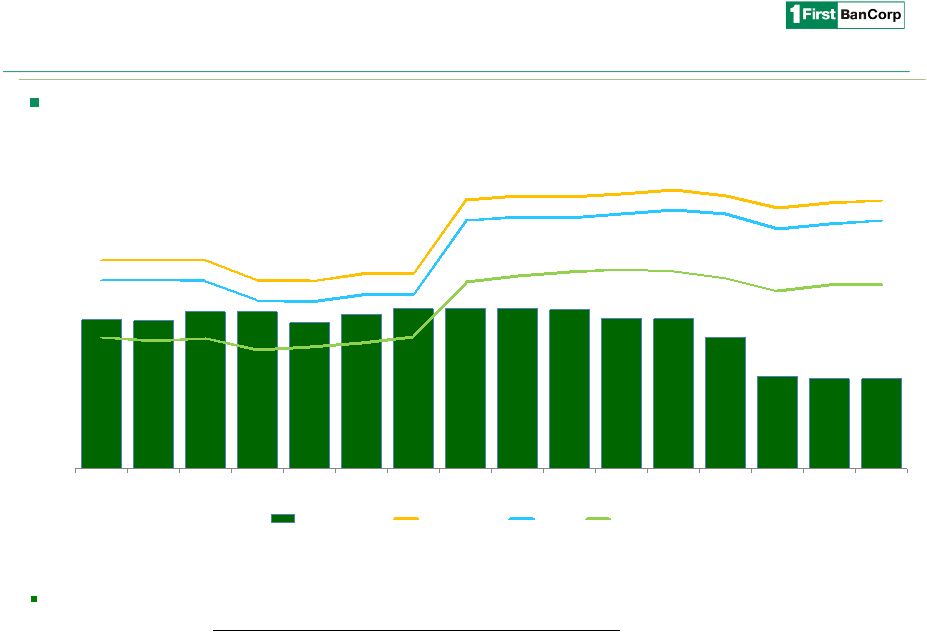

Capital Position and Asset Quality 17 Asset quality remains our number one focus, while preserving and growing capital Strong capital position: Total capital, Tier 1 capital and Leverage ratios of the Corporation of 17.1%, 15.8% and 11.7%, respectively. $523 million Deferred Tax Asset Valuation Allowance. 9.5% 9.4% 10.0% 10.0% 9.3% 9.8% 10.2% 10.2% 10.2% 10.1% 9.6% 9.5% 8.4% 5.9% 5.7% 5.7% 13.3% 13.4% 13.3% 12.0% 12.0% 12.4% 12.4% 17.1% 17.4% 17.3% 17.5% 17.8% 17.4% 16.6% 16.9% 17.1% 12.0% 12.1% 12.0% 10.7% 10.7% 11.1% 11.1% 15.8% 16.0% 16.0% 16.2% 16.5% 16.2% 15.3% 15.6% 15.8% 8.4% 8.1% 8.3% 7.6% 7.8% 8.0% 8.4% 11.9% 12.3% 12.5% 12.7% 12.6% 12.1% 11.3% 11.7% 11.7% 0.0% 6.0% 12.0% 18.0% Q1 '10 Q2 '10 Q3 '10 Q4 '10 Q1 '11 Q2 '11 Q3 '11 Q4 '11 Q1 '12 Q2 '12 Q3 '12 Q4 '12 Q1 '13 Q2 '13 Q3 '13 Q4 '13 NPAs / Assets Total Capital Tier 1 Leverage Core franchise is strong |

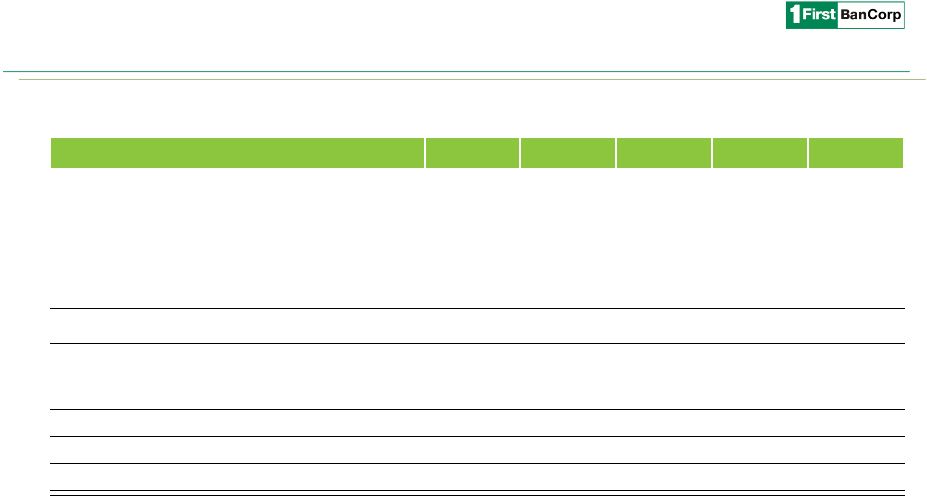

Non-performing Assets ($ in millions) 1) Collateral pledged with Lehman Brothers Special Financing, Inc. 18 2009 2010 2011 2012 2013 Non-performing loans held for investment: Residential mortgage 441,642 $ 392,134 $ 338,208 $ 313,626 $ 161,441 $ Commercial mortgage 196,535 217,165 240,414 214,780 120,107 Commercial & industrial 241,316 317,243 270,171 230,090 114,833 Construction 634,329 263,056 250,022 178,190 58,866 Consumer & finance leases 50,041 49,391 39,547 38,875 40,302 Total non-performing loans held for investment 1,563,863 1,238,989 1,138,362 975,561 495,549 OREO 69,304 84,897 114,292 185,764 160,193 Other repossessed property 12,898 14,023 15,392 10,107 14,865 Other assets (1) 64,543 64,543 64,543 64,543 - Total non-performing assets, excluding loans held for sale 1,710,608 1,402,452 1,332,589 1,235,975 670,607 Non-performing loans held for sale - 159,321 4,764 2,243 54,801 Total non-performing assets 1,710,608 $ 1,561,773 $ 1,337,353 $ 1,238,218 $ 725,408 $ |

(1) Offering of common stock by certain of the Corporation's existing stockholders. (2) Represents the impact of the national gross receipts tax corresponding to the first quarter of 2013, recorded during the second quarter after enactment of Act No. 40. (3) Represents the impact of the national gross receipt tax related to the trade or business outside of Puerto Rico that was reversed in the fourth quarter after enactment of Act No. 117. 4Q 2012 1Q 2013 2Q 2013 3Q 2013 4Q 2013 Income (loss) before income taxes 16,028 $ (71,011) $ (123,562) $ 19,616 $ 15,634 $ Add: Provision for loan and lease losses 30,466 111,123 87,464 22,195 22,969 Add: Net loss on investments and impairments 69 117 42 - - Less: Unrealized gain (loss) on derivatives instruments and liabilities measured at fair value (432) (400) (708) (232) (355) Add: Bulk sales related expenses and other professional fees related to the terminated preferred stock exchange offer - 5,096 3,198 - - Add: Loss on certain OREO properties sold as part of the bulk sale of non-performing residential mortgage assets - - 1,879 - - Add: Secondary offering costs (1) - - - 1,669 - Add: Credit card processing platform conversion costs - - - 1,715 - Add: National gross receipt tax (2) - - 1,656 - - Less: National gross receipt tax - outside Puerto Rico (3) - - - - (473) Add: Branch consolidations and other restructuring expenses/valuation adjustments - - - - 1,421 Add: Write-off collateral pledged to Lehman and related expenses - - 66,574 - 2,500 Add: Equity in losses (earnings) of unconsolidated entities 8,330 5,538 (648) 5,908 5,893 Adjusted pre-tax, pre-provision income 54,461 $ 50,463 $ 35,895 $ 50,871 $ 47,589 $ Quarter Ended Adjusted Pre-tax, Pre-provision Income Reconciliation 19 ($ in thousands) |

Tangible Book Value Per Share Reconciliation 20 ($ in millions, except for per share data) 4Q 2012 1Q 2013 2Q 2013 3Q 2013 4Q 2013 Tangible equity: Total equity - GAAP 1,485 $ 1,404 $ 1,222 $ 1,221 $ 1,216 $ Preferred equity (63) (63) (63) (63) (63) Goodwill (28) (28) (28) (28) (28) Purchased credit card relationship (24) (23) (22) (21) (20) Core deposit intangible (9) (9) (8) (8) (7) Tangible common equity 1,361 $ 1,282 $ 1,101 $ 1,101 $ 1,098 $ Common shares outstanding 206 206 207 207 207 Tangible book value per common share 6.60 $ 6.21 $ 5.32 $ 5.32 $ 5.30 $ Deferred tax valuation allowance 360 $ 384 $ 523 $ 520 $ 523 $ Deferred tax valuation allowance per share 1.75 1.86 2.53 2.51 2.53 Adjusted tangible book value per share 8.34 $ 8.08 $ 7.85 $ 7.83 $ 7.83 $ 1) Assuming 100% recapture of valuation allowance. (1) |

Use of Non-GAAP Financial Measures 21 (In thousands, except per share information) Year Ended December 31, 2013 As Reported (GAAP) Bulk Sales Transaction Impact Write-off collateral pledged to Lehman and related contingency for attorneys' fees Year Ended December 31, 2013 Adjusted (Non- GAAP) Year Ended December 31, 2012 As Reported (GAAP) Variance Net interest income 514,945 $ - $ - $ 514,945 $ 461,705 $ 53,240 $ Provision for loan and lease losses 243,751 (132,002) - 111,749 120,499 (8,750) Net interest income after provision for loan and lease losses 271,194 132,002 - 403,196 341,206 61,990 Non-interest (loss) income (15,489) - 66,574 51,085 49,391 1,694 Non-interest expenses 415,028 (8,840) (2,500) 403,688 354,883 48,805 (Loss) Income before income taxes (159,323) 140,842 69,074 50,593 35,714 14,879 Income tax expense (5,164) - - (5,164) (5,932) 768 Net (loss) income (164,487) $ 140,842 $ 69,074 $ 45,429 $ 29,782 $ 15,647 $ Earnings (loss) per common share: Basic (0.80) $ 0.68 $ 0.34 $ 0.22 $ 0.15 $ 0.07 $ Diluted (0.80) $ 0.68 $ 0.34 $ 0.22 $ 0.14 $ 0.08 $ The results for FYE 2013 were negatively impacted by two significant items: • an aggregate loss of $140.8 million on two separate bulk sales and valuation adjustments to certain loans transferred to held for sale; and • a $66.6 million loss related to the write-off of assets pledged as collateral to Lehman together with an additional $2.5 million for a loss contingency of attorneys’ fees awarded to the counterparty related to this matter. Excluding these items, net income for FYE 2013 was $45.4 million. |