Free signup for more

- Track your favorite companies

- Receive email alerts for new filings

- Personalized dashboard of news and more

- Access all data and search results

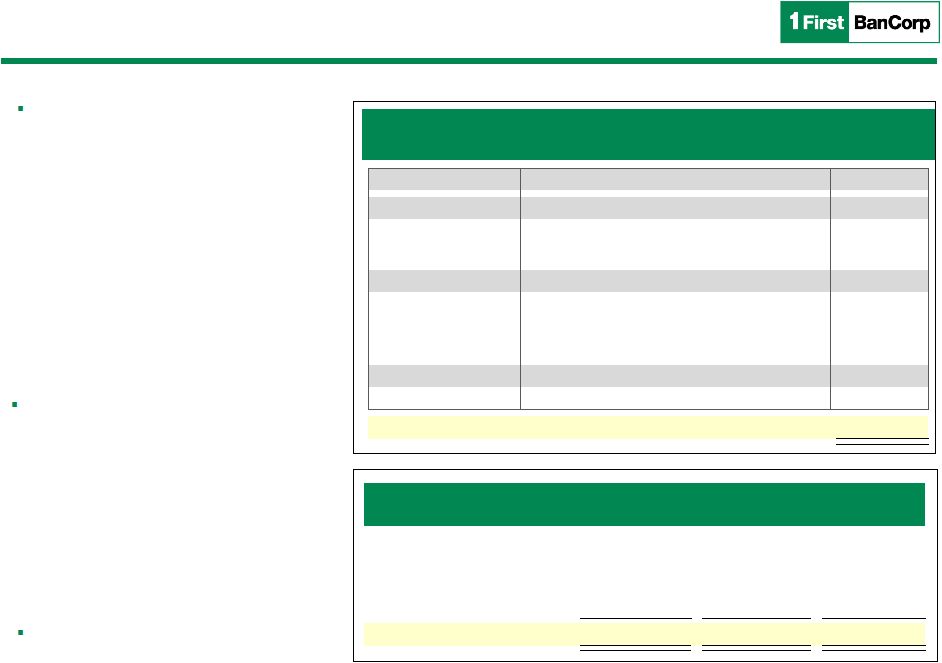

Filing tables

Filing exhibits

Related financial report

FBP similar filings

- 10 Feb 16 Results of Operations and Financial Condition

- 29 Jan 16 2015 Fourth Quarter Highlights and Comparison with Third Quarter

- 12 Nov 15 Results of Operations and Financial Condition

- 26 Oct 15 First Bancorp. Announces Earnings

- 14 Sep 15 Results of Operations and Financial Condition

- 30 Jul 15 2015 Second Quarter Highlights and Comparison with First Quarter

- 26 Jun 15 First BanCorp Releases its 2015 Dodd Frank Stress Test Results

Filing view

External links