SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

|

| |

| ý | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2014

OR

|

| |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 1-34243

tw telecom inc.

(Exact name of Registrant as specified in its charter)

|

| | |

| | | |

| Delaware | | 84-1500624 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification Number) |

| | |

10475 Park Meadows Drive Littleton, Colorado | | 80124 |

| (Address of principal executive offices) | | (Zip Code) |

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. |

| | | | | | |

| | | | | | | |

| Large accelerated filer | | ý | | Accelerated filer | | ¨ |

| | | | |

| Non-accelerated filer | | o (Do not check if a smaller reporting company) | | Smaller reporting company | | ¨ |

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No ý

The number of shares outstanding of tw telecom inc.’s common stock as of July 31, 2014 was 138,067,739 shares.

INDEX TO FORM 10-Q

|

| | |

| | | |

| | | Page |

| |

| Item 1. | Financial Statements: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| | |

| |

| Item 1. | | |

| Item 1A. | | |

| Item 2. | | |

| Item 6. | | |

Part I. Financial Information

Item 1. Financial Statements

tw telecom inc.

CONDENSED CONSOLIDATED BALANCE SHEETS |

| | | | | | | | |

| | | June 30,

2014 | | December 31,

2013 |

| | | (unaudited) | | |

| | | (amounts in thousands, except per share amounts) |

| ASSETS | | | | |

| Current assets: | | | | |

| Cash and cash equivalents | | $ | 190,163 |

| | $ | 284,419 |

|

| Investments | | 173,564 |

| | 194,576 |

|

| Receivables, less allowances of $7,087 and $6,748, respectively | | 106,335 |

| | 107,258 |

|

| Prepaid expenses and other current assets | | 25,745 |

| | 22,545 |

|

| Deferred income taxes | | 54,026 |

| | 54,026 |

|

| Total current assets | | 549,833 |

| | 662,824 |

|

| Property, plant and equipment | | 4,849,680 |

| | 4,675,335 |

|

| Less accumulated depreciation | | (3,115,543 | ) | | (2,980,379 | ) |

| | | 1,734,137 |

| | 1,694,956 |

|

| Deferred income taxes | | 79,426 |

| | 96,087 |

|

| Goodwill | | 412,694 |

| | 412,694 |

|

| Intangible assets, net of accumulated amortization | | 9,089 |

| | 11,555 |

|

| Other assets, net | | 42,245 |

| | 44,344 |

|

| Total assets | | $ | 2,827,424 |

| | $ | 2,922,460 |

|

| LIABILITIES AND STOCKHOLDERS’ EQUITY | | | | |

| Current liabilities: | | | | |

| Accounts payable | | $ | 70,732 |

| | $ | 38,454 |

|

| Deferred revenue | | 49,248 |

| | 48,371 |

|

| Accrued taxes, franchise and other fees | | 54,029 |

| | 55,043 |

|

| Accrued interest | | 22,732 |

| | 21,606 |

|

| Accrued payroll and benefits | | 54,469 |

| | 52,604 |

|

| Accrued carrier costs | | 4,439 |

| | 25,507 |

|

| Current portion debt and capital lease obligations, net | | 8,147 |

| | 32,470 |

|

| Other current liabilities | | 31,160 |

| | 35,241 |

|

| Total current liabilities | | 294,956 |

| | 309,296 |

|

| Long-term debt and capital lease obligations, net | | 1,914,878 |

| | 1,916,775 |

|

| Long-term deferred revenue | | 19,792 |

| | 20,046 |

|

| Other long-term liabilities | | 42,838 |

| | 40,274 |

|

| Commitments and contingencies (Note 8) | |

|

| |

|

|

| Stockholders’ equity: | | | | |

| Preferred stock, $0.01 par value, 20,000 shares authorized, no shares issued and outstanding | | — |

| | — |

|

| Common stock, $0.01 par value, 439,800 shares authorized, 153,760 shares issued | | 1,538 |

| | 1,538 |

|

| Additional paid-in capital | | 1,701,063 |

| | 1,701,356 |

|

| Treasury stock, 15,708 and 12,593 shares, at cost, respectively | | (455,082 | ) | | (357,974 | ) |

| Accumulated deficit | | (692,717 | ) | | (708,979 | ) |

| Accumulated other comprehensive income | | 158 |

| | 128 |

|

| Total stockholders’ equity | | 554,960 |

| | 636,069 |

|

| Total liabilities and stockholders’ equity | | $ | 2,827,424 |

| | $ | 2,922,460 |

|

See accompanying notes to condensed consolidated financial statements.

tw telecom inc.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited)

|

| | | | | | | | | | | | | | | | |

| | | Three Months Ended

June 30, | | Six Months Ended

June 30, |

| | | 2014 | | 2013 | | 2014 | | 2013 |

| | | (amounts in thousands, except per share amounts) |

| Revenue: | | | | | | | | |

| Data and Internet services | | $ | 253,031 |

| | $ | 220,063 |

| | $ | 496,702 |

| | $ | 431,784 |

|

| Voice services | | 77,919 |

| | 76,437 |

| | 155,280 |

| | 152,467 |

|

| Network services | | 56,667 |

| | 64,079 |

| | 115,034 |

| | 129,034 |

|

| Service revenue | | 387,617 |

| | 360,579 |

| | 767,016 |

| | 713,285 |

|

| Taxes and fees | | 25,412 |

| | 20,622 |

| | 48,164 |

| | 41,216 |

|

| Intercarrier compensation | | 6,674 |

| | 8,282 |

| | 12,816 |

| | 16,191 |

|

| Total revenue | | 419,703 |

| | 389,483 |

| | 827,996 |

| | 770,692 |

|

Costs and expenses (a): | | | | | | | | |

| Operating (exclusive of depreciation, amortization and accretion shown separately below) | | 181,391 |

| | 164,131 |

| | 355,430 |

| | 325,213 |

|

| Selling, general and administrative | | 108,613 |

| | 96,438 |

| | 215,445 |

| | 190,000 |

|

| Depreciation, amortization and accretion | | 84,185 |

| | 75,652 |

| | 166,641 |

| | 150,047 |

|

| Total costs and expenses | | 374,189 |

| | 336,221 |

| | 737,516 |

| | 665,260 |

|

| Operating income | | 45,514 |

| | 53,262 |

| | 90,480 |

| | 105,432 |

|

| Interest expense | | (24,873 | ) | | (21,544 | ) | | (50,521 | ) | | (49,884 | ) |

| Debt extinguishment costs | | — |

| | (399 | ) | | (1,282 | ) | | (399 | ) |

| Interest income | | 109 |

| | 173 |

| | 257 |

| | 450 |

|

| Income before income taxes | | 20,750 |

| | 31,492 |

| | 38,934 |

| | 55,599 |

|

| Income tax expense | | 9,601 |

| | 14,145 |

| | 17,994 |

| | 25,108 |

|

| Net income | | $ | 11,149 |

| | $ | 17,347 |

| | $ | 20,940 |

| | $ | 30,491 |

|

| Earnings per share: | | | | | | | | |

| Basic | | $ | 0.08 |

| | $ | 0.12 |

| | $ | 0.15 |

| | $ | 0.20 |

|

| Diluted | | $ | 0.08 |

| | $ | 0.11 |

| | $ | 0.15 |

| | $ | 0.20 |

|

| Weighted average shares outstanding: | | | | | | | | |

| Basic | | 136,360 |

| | 147,071 |

| | 137,219 |

| | 148,095 |

|

| Diluted | | 137,814 |

| | 148,342 |

| | 139,172 |

| | 151,081 |

|

(a) Includes non-cash stock-based employee compensation expense (Note 7):

|

| | | | | | | | | | | | | | | | |

| Operating | | $ | 545 |

| | $ | 545 |

| | $ | 1,084 |

| | $ | 1,128 |

|

| Selling, general and administrative | | $ | 8,107 |

| | $ | 7,869 |

| | $ | 16,954 |

| | $ | 16,748 |

|

See accompanying notes to condensed consolidated financial statements.

tw telecom inc.

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(Unaudited)

|

| | | | | | | | | | | | | | | | |

| | | Three Months Ended

June 30, | | Six Months Ended

June 30, |

| | | 2014 | | 2013 | | 2014 | | 2013 |

| | | (amounts in thousands) |

| Net income | | $ | 11,149 |

| | $ | 17,347 |

| | $ | 20,940 |

| | $ | 30,491 |

|

| Other comprehensive income (loss), net of tax: | | | | | | | | |

| Unrealized gain (loss) on available-for-sale securities | | 40 |

| | (28 | ) | | 30 |

| | (20 | ) |

| Other comprehensive income (loss), net of tax | | 40 |

| | (28 | ) | | 30 |

| | (20 | ) |

| Comprehensive income | | $ | 11,189 |

| | $ | 17,319 |

| | $ | 20,970 |

| | $ | 30,471 |

|

See accompanying notes to condensed consolidated financial statements.

tw telecom inc.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

|

| | | | | | | | |

| | | Six Months Ended

June 30, |

| | | 2014 | | 2013 |

| | | (amounts in thousands) |

| Cash flows from operating activities: | | | | |

| Net income | | $ | 20,940 |

| | $ | 30,491 |

|

| Adjustments to reconcile net income to net cash provided by operating activities: | | | | |

| Depreciation, amortization and accretion | | 166,641 |

| | 150,047 |

|

| Deferred income taxes | | 17,252 |

| | 24,289 |

|

| Stock-based compensation expense | | 18,038 |

| | 17,876 |

|

| Loss on debt extinguishment | | 1,282 |

| | 399 |

|

| Amortization of discount on debt and deferred debt issue costs | | 3,212 |

| | 7,850 |

|

| Changes in operating assets and liabilities: | | | | |

| Receivables, prepaid expenses and other assets | | (1,629 | ) | | (14,046 | ) |

| Accounts payable, deferred revenue and other liabilities | | (1,231 | ) | | (10,346 | ) |

| Net cash provided by operating activities | | 224,505 |

| | 206,560 |

|

| Cash flows from investing activities: | | | | |

| Capital expenditures | | (195,998 | ) | | (187,509 | ) |

| Purchases of investments | | (109,275 | ) | | (157,523 | ) |

| Proceeds from sale of investments | | 129,509 |

| | 125,041 |

|

| Other investing activities, net | | 5,841 |

| | (465 | ) |

| Net cash used in investing activities | | (169,923 | ) | | (220,456 | ) |

| Cash flows from financing activities: | | | | |

| Proceeds from issuance of common stock upon exercise of stock options | | 10,778 |

| | 50,874 |

|

| Taxes paid related to net share settlement of equity awards | | (18,941 | ) | | (18,315 | ) |

| Purchases of treasury stock | | (112,564 | ) | | (197,310 | ) |

| Excess tax benefits from stock-based compensation | | 794 |

| | 944 |

|

| Proceeds from modification of debt, net of financing costs | | — |

| | 49,684 |

|

| Retirement of debt obligations | | (24,418 | ) | | (256,348 | ) |

| Payment of debt and capital lease obligations | | (4,487 | ) | | (2,096 | ) |

| Net cash used in financing activities | | (148,838 | ) | | (372,567 | ) |

| Decrease in cash and cash equivalents | | (94,256 | ) | | (386,463 | ) |

| Cash and cash equivalents at beginning of period | | 284,419 |

| | 806,728 |

|

| Cash and cash equivalents at end of period | | $ | 190,163 |

| | $ | 420,265 |

|

| Supplemental disclosures of cash flow information: | | | | |

| Cash paid for interest | | $ | 46,632 |

| | $ | 43,540 |

|

| Cash paid for income taxes, net of refunds | | $ | 2,314 |

| | $ | 4,477 |

|

| Cash paid for debt extinguishment costs | | $ | 939 |

| | $ | 469 |

|

| Non-cash investing & financing activities: | | | | |

| Addition of capital lease obligations | | $ | 1,352 |

| | $ | 4,302 |

|

See accompanying notes to condensed consolidated financial statements.

tw telecom inc.

CONDENSED CONSOLIDATED STATEMENT OF CHANGES IN STOCKHOLDERS’ EQUITY

Six Months Ended June 30, 2014

(Unaudited)

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Common Stock | | Treasury Stock | | Additional paid-in capital | | Accumulated deficit | | Accumulated other comprehensive income | | Total stockholders’ equity |

| | | Shares | | Amount | | Shares | | Amount | |

| | | (amounts in thousands) |

| Balance at December 31, 2013 | | 153,760 |

| | $ | 1,538 |

| | (12,593 | ) | | $ | (357,974 | ) | | $ | 1,701,356 |

| | $ | (708,979 | ) | | $ | 128 |

| | $ | 636,069 |

|

| Net income | | — |

| | — |

| | — |

| | — |

| | — |

| | 20,940 |

| | — |

| | 20,940 |

|

| Other comprehensive income, net of tax | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 30 |

| | 30 |

|

| Excess tax benefits from stock-based compensation, net | | — |

| | — |

| | — |

| | — |

| | 610 |

| | — |

| | — |

| | 610 |

|

| Purchases of treasury stock | | — |

| | — |

| | (3,674 | ) | | (112,564 | ) | | — |

| | — |

| | — |

| | (112,564 | ) |

| Exercise of stock options net of (withholdings) to satisfy employee tax obligations upon vesting of stock awards | | — |

| | — |

| | 651 |

| | 18,670 |

| | (23,737 | ) | | (3,096 | ) | | — |

| | (8,163 | ) |

| Stock-based compensation | | — |

| | — |

| | (92 | ) | | (3,214 | ) | | 22,834 |

| | (1,582 | ) | | — |

| | 18,038 |

|

| Balance at June 30, 2014 | | 153,760 |

| | $ | 1,538 |

| | (15,708 | ) | | $ | (455,082 | ) | | $ | 1,701,063 |

| | $ | (692,717 | ) | | $ | 158 |

| | $ | 554,960 |

|

See accompanying notes to condensed consolidated financial statements.

tw telecom inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

1. Organization and Summary of Significant Accounting Policies

Description of Business and Capital Structure

tw telecom inc. (together with its wholly-owned subsidiaries, the “Company”) is a leading national provider of managed network services, specializing in business Ethernet, data networking, converged, Internet Protocol ("IP") based virtual private network or "IP VPN", Internet access, voice, including voice over Internet Protocol or “VoIP”, and network security services to enterprise organizations, including public sector entities, and carriers throughout the United States, including their global locations.

The Company has one class of common stock outstanding with one vote per share. The Company also is authorized to issue shares of preferred stock. The Company’s Board of Directors has the authority to establish voting powers, preferences and special rights for the preferred stock. No shares of preferred stock have been issued.

See Note 2, "Recent Developments", for information regarding the Agreement and Plan of Merger with Level 3 Communications, Inc. ("Level 3").

Basis of Presentation

The accompanying unaudited interim condensed consolidated financial statements have been prepared pursuant to the rules and regulations of the Securities and Exchange Commission (the “SEC”) for quarterly reports on Form 10-Q and do not include all of the information and note disclosures required by U.S. generally accepted accounting principles (“U.S. GAAP”) for complete financial statements. These condensed consolidated financial statements should therefore be read in conjunction with the consolidated financial statements and notes thereto included in our Annual Report on Form 10-K for the year ended December 31, 2013 filed with the SEC. The accompanying unaudited interim condensed consolidated financial statements have been prepared in accordance with U.S. GAAP and include all adjustments of a normal, recurring nature that are, in the opinion of management, necessary to present fairly the financial position and results of operations for the interim periods presented. The results of operations for an interim period are not necessarily indicative of the results of operations for a full fiscal year.

Prior Year Reclassifications

Beginning January 1, 2014, the Company is reporting revenue from taxes and fees in a separate line item on the condensed consolidated statements of operations and is reporting revenue from dedicated high capacity Ethernet services in data and Internet services rather than network services. These reclassifications have been made in the prior year condensed consolidated statement of operations to conform to the current year presentation. Neither of these changes affects total revenue for the current period or prior periods. The following table provides revenue as currently reported and previously reported for the three and six months ended June 30, 2013:

|

| | | | | | | | | | | | | | | | |

| | | Three Months Ended June 30, 2013 | | Six months ended June 30, 2013 |

| | | As Currently Reported | | As Previously Reported | | As Currently Reported | | As Previously Reported |

| | | (amounts in thousands) |

| Revenue: | | | | | | | | |

| Data and Internet services | | $ | 220,063 |

| | 209,634 |

| | 431,784 |

| | 411,716 |

|

| Voice services | | 76,437 |

| | 93,080 |

| | 152,467 |

| | 185,435 |

|

| Network services | | 64,079 |

| | 78,487 |

| | 129,034 |

| | 157,350 |

|

| Service revenue | | 360,579 |

| | 381,201 |

| | 713,285 |

| | 754,501 |

|

| Taxes and fees | | 20,622 |

| | — |

| | 41,216 |

| | — |

|

| Intercarrier compensation | | 8,282 |

| | 8,282 |

| | 16,191 |

| | 16,191 |

|

| Total revenue | | $ | 389,483 |

| | $ | 389,483 |

| | $ | 770,692 |

| | $ | 770,692 |

|

tw telecom inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - (Continued)

Use of Estimates

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the reporting period. Actual results could differ from those estimates.

Accumulated Other Comprehensive Income

The balance in accumulated other comprehensive income as of June 30, 2014 and December 31, 2013 relates to the Company's investments that are classified as available-for-sale securities. The Company recognized no material changes in accumulated other comprehensive income for the three and six months ended June 30, 2014 or 2013. There were no significant items reclassified out of accumulated other comprehensive income for the three and six months ended June 30, 2014 or 2013.

Revenue

The Company’s revenue is derived primarily from business communications services comprised of the following:

| |

| • | Data and Internet services include services that enable customers to connect their internal computer networks between locations and to access external networks, including Internet access and data transport at high speeds using Ethernet protocol, local and wide-area business Ethernet and IP VPN solutions, including service enhancements that provide customers with more visibility and control over their Ethernet services, which we refer to as the "Intelligent Network". Data and Internet services also include a portfolio of managed services including the data and Internet components of converged services, which fully integrates a combination of certain communication applications including IP VPN, Internet, enterprise Session Initiation Protocol ("SIP") trunking (a VoIP solution), security and managed router service into a single managed IP solution; and the data and Internet components of integrated services, which enable customers to purchase a full array of access options that include Internet services. |

| |

| • | Voice services are traditional voice capabilities, whether provided over Time Division Multiplexing ("TDM") or VoIP, including those provided as standalone and bundled services, long distance and toll free services. Voice services also include the voice components of managed and integrated services. |

| |

| • | Network services are point-to-point services that transmit voice, data and images using state-of-the-art fiber optics, and collocation services that provide secure space with controlled climate and power where customers can locate their equipment to connect to the Company’s network in facilities equipped for enterprise information technology environmental requirements. |

The Company also generates revenue from intercarrier compensation, which is comprised of switched access services and reciprocal compensation. Switched access represents the compensation from another carrier for the delivery of traffic from a long distance carrier’s point of presence to an end-user’s premises provided through the Company’s switching facilities. The Federal Communications Commission ("FCC") and state public utility commissions regulate switched access rates in their respective jurisdictions. Reciprocal compensation represents compensation from local exchange carriers (“LECs”) for local exchange traffic originated on another LEC’s facilities and terminated on the Company’s facilities.

The Company classifies taxes and fees billed to customers and remitted to government authorities on a gross versus net basis in revenue and expense. In making this determination, the Company assesses, among other things, whether the Company is the primary obligor or principal taxpayer for the taxes and fees assessed in each jurisdiction where the Company does business. In jurisdictions where the Company determines that it is the principal taxpayer, the Company records the taxes and fees on a gross basis, including the taxes and fees in revenue and expense. In jurisdictions where the Company determines that it is merely a collection agent for the government authority, the Company records the taxes on a net basis. The total amount of such taxes and fees classified as revenue is included in "Taxes and fees" on the Company's condensed consolidated statements of operations.

The Company’s customers include enterprise organizations in a wide variety of industry segments including, among others, the financial services, technology and scientific, health care, distribution, manufacturing and professional services industries, data centers, cloud application providers, public sector entities, system integrators and communications service providers, including incumbent local exchange carriers ("ILECs"), competitive local exchange carriers ("CLECs"), wireless communications companies and cable companies.

Revenue for network, data and Internet, and the majority of voice services is generally billed in advance on a monthly fixed rate basis and recognized over the period the services are provided. Revenue for the majority of intercarrier compensation

tw telecom inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - (Continued)

and certain components of voice services, such as long distance, is generally billed on a transactional basis in arrears based on a customer’s actual usage; therefore, estimates are used to recognize revenue in the period earned.

The Company evaluates whether receivables are reasonably assured of collection based on certain factors, including the likelihood of billing being disputed by customers. If there is a billing dispute with a customer, revenue generally is not recognized until the dispute is resolved. The Company does not recognize revenue associated with contract termination charges until cash is received.

Significant Customers

The Company has substantial business relationships with a few large customers, including major telecommunications carriers. The Company’s 10 largest customers accounted for an aggregate of 17% and 18% of the Company’s total revenue for the six months ended June 30, 2014 and 2013, respectively. No customer accounted for 5% or more of total revenue for the six months ended June 30, 2014 or 2013.

Recently Issued Accounting Pronouncements

In May 2014, the Financial Accounting Standards Board issued an accounting standards update that establishes a comprehensive new revenue recognition model designed to depict the transfer of goods or services to customers in an amount that reflects the consideration the entity expects to receive in exchange for those goods or services. The new standard is effective for fiscal years, and interim periods within those years, beginning after December 15, 2016 and must be adopted using either a full retrospective approach for all periods presented in the period of adoption or a modified retrospective approach. The Company is currently evaluating the impact of this new standard on its consolidated financial statements as well as the transition method the Company intends to use.

2. Recent Developments

Level 3 Merger

On June 15, 2014, the Company entered into an Agreement and Plan of Merger (the "Merger Agreement") with Level 3 Communications, Inc. ("Level 3") and certain of its subsidiaries whereby the Company agreed to merge with and into a wholly owned subsidiary of Level 3 (the "Level 3 merger").

Upon completion of the Level 3 merger, (i) each issued and outstanding share of common stock of the Company, other than dissenting shares, will be converted into 0.7 shares (the "Stock Consideration") of Level 3's common stock and the right to receive $10.00 in cash (the "Cash Consideration" and, together with the Stock Consideration, the "Merger Consideration"). The Merger Agreement also provides that the (i) issued and outstanding options to purchase the Company's common stock will be exchanged for Merger Consideration, as adjusted to reflect the exercise price of each such outstanding option and (ii) issued and outstanding restricted stock and restricted stock units covering the Company's common stock will vest and be exchanged for Merger Consideration. The Level 3 merger is expected to close during the fourth quarter of 2014, but not before October 4, 2014. The closing of the Level 3 merger is subject to the receipt of certain regulatory and governmental approvals and the satisfaction of certain conditions, including the approval of the Level 3 merger by the Company's stockholders and the approval of Level 3's proposed stock issuance and charter amendments by Level 3's stockholders.

3. Earnings per Common Share and Potential Common Share

Basic earnings per common share (“EPS”) is measured as the income allocated to common stockholders divided by the weighted average outstanding common shares for the period. Diluted EPS is similar to basic EPS but presents the dilutive effect on a per share basis of potential common shares (such as convertible securities and stock options) as if they had been converted to shares at the beginning of the period presented. Potential common shares that have an anti-dilutive effect (e.g., those that increase income per share) are excluded from diluted EPS.

tw telecom inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - (Continued)

The following is a reconciliation of the numerators and denominators used in the basic and diluted EPS computations:

|

| | | | | | | | | | | | | | | | |

| | | Three Months Ended

June 30, | | Six Months Ended

June 30, |

| | | 2014 | | 2013 | | 2014 | | 2013 |

| | | (amounts in thousands, except per share amounts) |

| Numerator | | | | | | | | |

| Net income | | $ | 11,149 |

| | $ | 17,347 |

| | $ | 20,940 |

| | $ | 30,491 |

|

| Allocation of net income to unvested restricted stock | | (199 | ) | | (331 | ) | | (378 | ) | | (587 | ) |

| Net income allocated to common stockholders, basic | | $ | 10,950 |

| | $ | 17,016 |

| | $ | 20,562 |

| | $ | 29,904 |

|

| Net income allocated to common stockholders, diluted | | $ | 10,950 |

| | $ | 17,016 |

| | $ | 20,562 |

| | $ | 29,904 |

|

| Denominator | | | | | | | | |

| Basic weighted average shares outstanding | | 136,360 |

| | 147,071 |

| | 137,219 |

| | 148,095 |

|

| Dilutive potential common shares: | | | | | | | | |

| Stock options | | 269 |

| | 886 |

| | 330 |

| | 1,180 |

|

| Unvested restricted stock | | 1,185 |

| | 385 |

| | 1,623 |

| | 1,806 |

|

| Diluted weighted average shares outstanding | | 137,814 |

| | 148,342 |

| | 139,172 |

| | 151,081 |

|

| Basic earnings per share | | $ | 0.08 |

| | $ | 0.12 |

| | $ | 0.15 |

| | $ | 0.20 |

|

| Diluted earnings per share | | $ | 0.08 |

| | $ | 0.11 |

| | $ | 0.15 |

| | $ | 0.20 |

|

There were no anti-dilutive shares for the three and six months ended June 30, 2014. Restricted stock awards to be settled in common stock upon vesting which were excluded from the computation of diluted weighted average shares outstanding because their inclusion would be anti-dilutive, totaled 2.9 million shares for the three months ended June 30, 2013. There were no anti-dilutive shares for the six months ended June 30, 2013.

4. Investments

The Company’s investments at June 30, 2014 and December 31, 2013 are summarized as follows:

|

| | | | | | | | |

| | | June 30,

2014 | | December 31,

2013 |

| | | (amounts in thousands) |

| Cash equivalents: | | | | |

| U.S. Treasury money market mutual funds | | $ | 41,399 |

| | $ | 28,845 |

|

| Commercial paper | | 9,998 |

| | 1,335 |

|

| Total cash equivalents | | $ | 51,397 |

| | $ | 30,180 |

|

| Investments: | | | | |

| Debt securities issued by the U.S. Treasury | | $ | 60,028 |

| | $ | 69,628 |

|

| Commercial paper | | 57,268 |

| | 75,460 |

|

| Debt securities issued by U.S. Government agencies | | 56,268 |

| | 49,488 |

|

| Total investments | | $ | 173,564 |

| | $ | 194,576 |

|

| Total cash equivalents and investments | | $ | 224,961 |

| | $ | 224,756 |

|

At June 30, 2014 and December 31, 2013, the carrying values of investments included in cash and cash equivalents approximated fair value. The aggregate fair value of available-for-sale securities by major security type is included in Note 6. The amortized cost basis of the available-for-sale securities was not materially different from the aggregate fair value. The contractual maturities of the Company’s available-for-sale securities are all within one year.

Proceeds from the sale and maturity of available-for-sale securities were $60.0 million and $91.1 million during the three months ended June 30, 2014 and 2013, respectively, and $129.5 million and $125.0 million during the six months ended June 30, 2014 and 2013, respectively. Gains and losses on investments are calculated using the specific identification method and are

tw telecom inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - (Continued)

recognized during the period the investment is sold. The Company recognized no material unrealized or realized net gains or losses during the three and six months ended June 30, 2014 and 2013.

5. Long-Term Debt and Capital Lease Obligations

The components of long-term debt and capital lease obligations at June 30, 2014 and December 31, 2013 were as follows:

|

| | | | | | | | | | | | | | | | | | | | |

| | | Date of | | | | | | Outstanding Balance as of |

| | | Issuance / Amendment | | Maturity | | Interest Payments | | Interest Rate | | Original Principal | | June 30,

2014 | | December 31,

2013 |

| | | | | | | | | | | (amounts in thousands) |

| Term Loan B | | Apr 2013 | | Apr 2020 | | At least quarterly | | Eurodollar rate + 2.50% | | $ | 520,000 |

| | $ | 514,800 |

| | $ | 517,400 |

|

| 8% Senior Notes | | Mar 2010 | | Mar 2018 | | Mar/Sept | | 8% | | 430,000 |

| | — |

| | 23,479 |

|

53/8% Senior Notes | | Oct 2012 | | Oct 2022 | | Apr/Oct | | 5 3/8% | | 480,000 |

| | 480,000 |

| | 480,000 |

|

53/8% Senior Notes | | Aug 2013 | | Oct 2022 | | Apr/Oct | | 5 3/8% | | 450,000 |

| | 450,000 |

| | 450,000 |

|

63/8% Senior Notes | | Aug 2013 | | Sept 2023 | | Mar/Sept | | 6 3/8% | | 350,000 |

| | 350,000 |

| | 350,000 |

|

| Capital lease obligations | | 145,703 |

| | 147,046 |

|

| Total obligations | | 1,940,503 |

| | 1,967,925 |

|

| Unamortized discounts | | (17,478 | ) | | (18,680 | ) |

| Current portion | | (8,147 | ) | | (32,470 | ) |

| Total long-term debt and capital lease obligations | | $ | 1,914,878 |

| | $ | 1,916,775 |

|

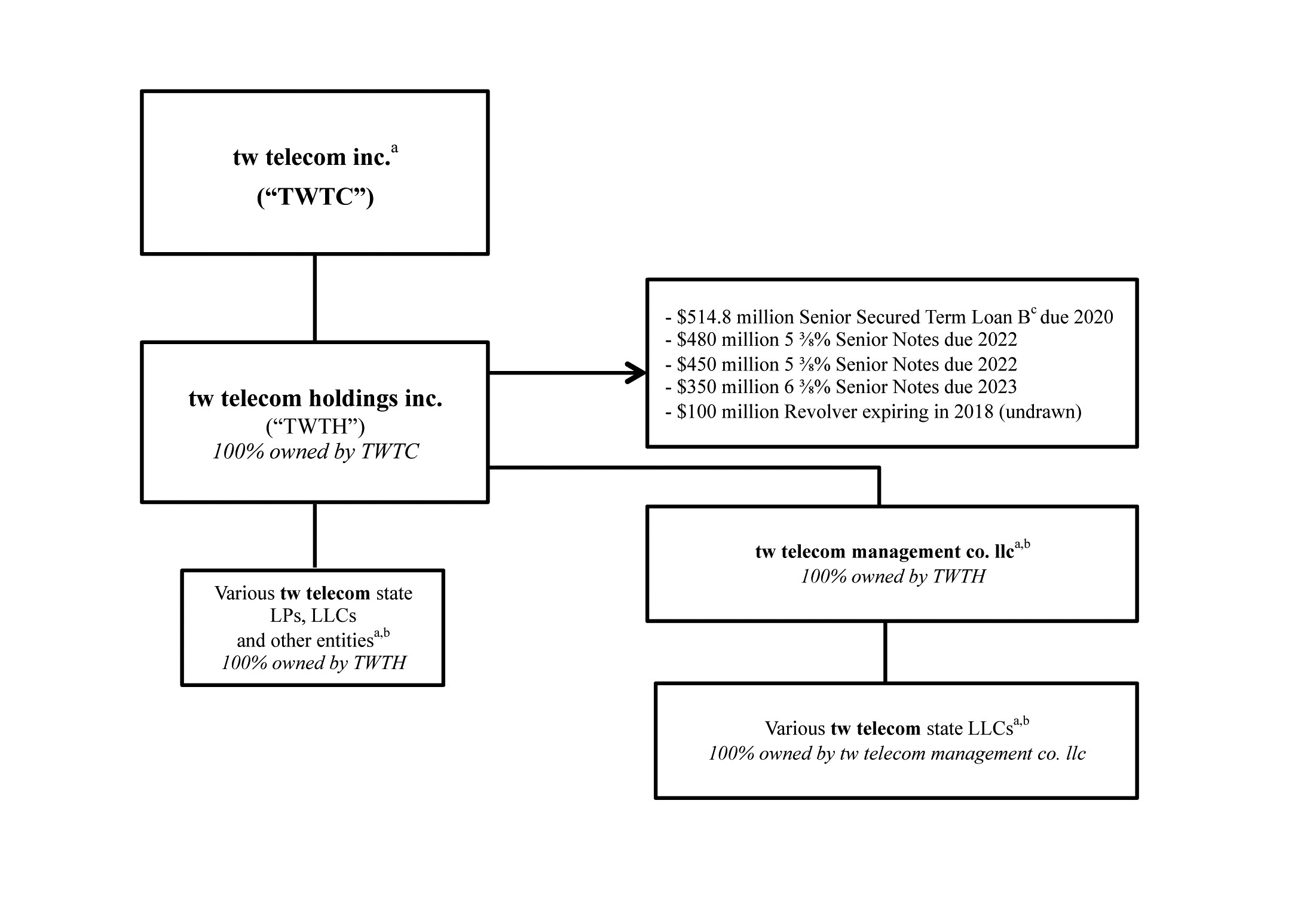

8% Senior Notes due 2018

As of December 31, 2013, tw telecom holdings inc. ("Holdings") had outstanding $23.5 million aggregate principal amount of 8% Senior Notes due 2018 (the "2018 Notes"). During the three months ended March 31, 2014, Holdings redeemed all remaining outstanding 2018 Notes at a redemption price of 104% of the principal amount. During the three months ended March 31, 2014, the Company recognized debt extinguishment costs of $1.3 million, comprised of $0.9 million for premiums associated with the redemption and $0.4 million for write-offs of unamortized deferred debt issuance costs and issuance discount related to the 2018 Notes.

Covenant Compliance

As of June 30, 2014, tw telecom inc. and its wholly-owned subsidiary, Holdings, were in compliance with all of their debt covenants.

6. Fair Value Measurements

Fair value, as defined by relevant accounting standards, is the price that would be received from selling an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. When determining the fair value measurements for assets and liabilities required to be recorded at fair value, the Company considers the principal or most advantageous market in which it would complete a transaction and considers assumptions that market participants would use when pricing the asset or liability, such as inherent risk, transfer restrictions and risk of nonperformance.

Fair Value Hierarchy

Relevant accounting standards set forth a fair value hierarchy that requires an entity to maximize the use of observable inputs and minimize the use of unobservable inputs when measuring fair value. A financial instrument’s categorization within the fair value hierarchy is based upon the lowest level of input that is significant to the fair value measurement. Relevant accounting standards establish three levels of inputs that may be used to measure fair value:

| |

| • | Level 1—Quoted prices in active markets for identical assets or liabilities. Level 1 assets that are measured at fair value on a recurring basis consist of the Company’s investments in U.S. Treasury money market mutual funds that are traded in an active market with sufficient volume and frequency of transactions, and are included as a component of cash and cash equivalents in the condensed consolidated balance sheets. |

tw telecom inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - (Continued)

| |

| • | Level 2—Observable inputs other than Level 1 prices such as quoted prices for similar assets or liabilities; quoted prices in markets with insufficient volume or infrequent transactions (less active markets); or model-derived valuations in which all significant inputs are observable or can be derived principally from or corroborated by observable market data for substantially the full term of the assets or liabilities. Level 2 assets that are measured at fair value on a recurring basis consist of the Company’s investments in commercial paper and debt securities issued by the U.S. Treasury and other U.S. government agencies using observable inputs in less active markets and are included as a component of cash and cash equivalents and investments in the condensed consolidated balance sheets. Level 2 liabilities that are measured, but not carried, at fair value on a recurring basis include the Company’s long-term debt. The Company’s long-term debt has not been listed on any securities exchange or quoted on an inter-dealer automated quotation system. The Company has estimated the fair value of its long-term debt based on indicative pricing published by certain investment banks or trading levels in its long-term debt. |

| |

| • | Level 3—Unobservable inputs to the valuation methodology that are significant to the measurement of fair value of assets or liabilities. The Company did not have any Level 3 assets or liabilities that were measured at fair value at June 30, 2014 and December 31, 2013. |

The following tables reflect assets that are measured and carried at fair value on a recurring basis at June 30, 2014 and December 31, 2013:

|

| | | | | | | | | | | | | | | | |

| | | Fair Value Measurements At June 30, 2014 | | Assets at Fair Value |

| | | Level 1 | | Level 2 | | Level 3 | |

| | | (amounts in thousands) |

| Assets | | | | | | | | |

| U.S. Treasury money market mutual funds | | $ | 41,399 |

| | $ | — |

| | $ | — |

| | $ | 41,399 |

|

| Commercial paper | | — |

| | 9,998 |

| | — |

| | 9,998 |

|

| Investments included in cash and cash equivalents | | $ | 41,399 |

| | $ | 9,998 |

| | $ | — |

| | $ | 51,397 |

|

| Debt securities issued by the U.S. Treasury | | — |

| | 60,028 |

| | — |

| | 60,028 |

|

| Commercial paper | | — |

| | 57,268 |

| | — |

| | 57,268 |

|

| Debt securities issued by U.S. Government agencies | | — |

| | 56,268 |

| | — |

| | 56,268 |

|

| Short-term investments | | $ | — |

| | $ | 173,564 |

| | $ | — |

| | $ | 173,564 |

|

| Total assets | | $ | 41,399 |

| | $ | 183,562 |

| | $ | — |

| | $ | 224,961 |

|

|

| | | | | | | | | | | | | | | | |

| | | Fair Value Measurements At December 31, 2013 | | Assets at Fair Value |

| | | Level 1 | | Level 2 | | Level 3 | |

| | | (amounts in thousands) |

| Assets | | | | | | | | |

| U.S. Treasury money market mutual funds | | $ | 28,845 |

| | $ | — |

| | $ | — |

| | $ | 28,845 |

|

| Commercial paper | | — |

| | 1,335 |

| | — |

| | 1,335 |

|

| Investments included in cash and cash equivalents | | $ | 28,845 |

| | $ | 1,335 |

| | $ | — |

| | $ | 30,180 |

|

| Commercial paper | | — |

| | 75,460 |

| | — |

| | 75,460 |

|

| Debt securities issued by the U.S. Treasury | | — |

| | 69,628 |

| | — |

| | 69,628 |

|

| Debt securities issued by U.S. Government agencies | | — |

| | 49,488 |

| | — |

| | 49,488 |

|

| Short-term investments | | $ | — |

| | $ | 194,576 |

| | $ | — |

| | $ | 194,576 |

|

| Total assets | | $ | 28,845 |

| | $ | 195,911 |

| | $ | — |

| | $ | 224,756 |

|

The following table summarizes the carrying amounts and estimated fair values of the Company’s long-term debt, including the current portion, at June 30, 2014 and December 31, 2013:

tw telecom inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - (Continued)

|

| | | | | | | | | | | | | | | | |

| | | June 30, 2014 | | December 31, 2013 |

| | | Carrying Value | | Fair Value Level 2 | | Carrying Value | | Fair Value Level 2 |

| | | (amounts in thousands) |

| Term Loan B, net of discount | | $ | 512,649 |

| | $ | 514,800 |

| | $ | 515,063 |

| | $ | 519,987 |

|

| 8% Senior Notes, net of discount | | — |

| | — |

| | 23,392 |

| | 24,594 |

|

53/8% Senior Notes, issued October 2012 | | 480,000 |

| | 520,800 |

| | 480,000 |

| | 474,000 |

|

53/8% Senior Notes, net of discount, issued August 2013 | | 434,673 |

| | 488,250 |

| | 433,744 |

| | 444,375 |

|

63/8% Senior Notes | | 350,000 |

| | 397,250 |

| | 350,000 |

| | 364,000 |

|

| Total debt | | $ | 1,777,322 |

| | $ | 1,921,100 |

| | $ | 1,802,199 |

| | $ | 1,826,956 |

|

7. Stock-Based Compensation

During the six months ended June 30, 2014, the Company granted restricted stock awards and restricted stock units with respect to 1.4 million shares and no stock options. As of June 30, 2014, the Company had 3.7 million restricted stock awards and restricted stock units that were unvested and 0.3 million stock options outstanding and exercisable.

As of June 30, 2014, there was $77.2 million of total unrecognized compensation expense related to unvested restricted stock awards and restricted stock units, which is expected to be recognized over a weighted-average period of 2.5 years, and no unrecognized compensation expense related to unvested stock options.

8. Commitments and Contingencies

Management routinely reviews the Company’s exposure to liabilities incurred in the normal course of its business operations. Where a probable contingency exists and the amount of the loss can be reasonably estimated, the Company records the estimated liability. Considerable judgment is required in analyzing and recording such liabilities and actual results may vary from the estimates.

Following the announcement of the execution of the Merger Agreement, three putative shareholder class action complaints (the "Class Action Complaints"), were filed in the Court of Chancery of the State of Delaware against the Company, its Board of Directors, Level 3, and certain subsidiaries of Level 3, challenging the proposed Level 3 merger: Veneros v. tw telecom, et al., Case No. 9835 (filed on or about June 27, 2014), Litman v. tw telecom, et al., Case No. 9838 (filed on or about June 27, 2014), and Carter v. tw telecom, et al., Case No. 9845 (filed on or about June 30, 2014).

The Class Action Complaints generally allege, among other things, that the individual members of the Company's Board of Directors breached their fiduciary duties owed to the public shareholders of the Company by approving its entry into the Merger Agreement and failing to take steps to maximize the value of the Company to its public shareholders, and that the Company, Level 3, and certain of Level 3's subsidiaries, aided and abetted such breaches of fiduciary duties. In addition, the Class Action Complaints allege, among other things, that the proposal regarding the Level 3 merger undervalues the Company, that the process leading up to the Merger Agreement was flawed, and that certain provisions of the Merger Agreement improperly favor Level 3 and impede a potential alternative transaction. The Class Action Complaints generally seek, among other things, declaratory and injunctive relief concerning the alleged fiduciary breaches, injunctive relief prohibiting the defendants from consummating the proposed Level 3 merger, and other forms of equitable relief. The Company intends to defend against these lawsuits vigorously, but is unable to predict the outcome of these lawsuits or reasonably estimate a range of possible loss.

The Company’s other pending legal proceedings are limited to litigation incidental to its business. In the opinion of management, the ultimate resolution of these matters are not expected to have a material adverse effect on the Company’s financial statements.

9. Supplemental Guarantor Information

The $480 million principal amount 53/8% Senior Notes due 2022 (the "2022 Notes"), $450 million principal amount 53/8% Senior Notes due 2022 (the "2022 Mirror Notes") and $350 million principal amount 63/8% Senior Notes due 2023 (the "2023 Notes") (collectively, the "Senior Notes") are unsecured obligations of Holdings ("Issuer") and are fully and unconditionally guaranteed by the Company (“Parent Guarantor”) and substantially all of the Issuer’s subsidiaries (“Combined Subsidiary Guarantors”). The guarantees are joint and several. The Combined Subsidiary Guarantors are directly or indirectly wholly owned by the Issuer, which is wholly owned by the Parent Guarantor. A significant amount of the Issuer’s cash flow is

tw telecom inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - (Continued)

generated by the Combined Subsidiary Guarantors. As a result, funds necessary to meet the Issuer’s debt service obligations are provided in large part by distributions or advances from the Combined Subsidiary Guarantors. The Senior Notes are governed by indentures that contain certain restrictive covenants. These restrictions affect, and in many respects limit or prohibit, among other things, the ability of the Parent Guarantor, the Issuer and its subsidiaries to incur indebtedness, make prepayments of certain indebtedness, pay dividends, make investments, engage in transactions with stockholders and affiliates, issue capital stock of subsidiaries, create liens, sell assets and engage in mergers and consolidations.

The following information sets forth the Company’s Condensed Consolidating Balance Sheets as of June 30, 2014 and December 31, 2013, Condensed Consolidating Statements of Operations for the three and six months ended June 30, 2014 and 2013, Condensed Consolidating Statements of Comprehensive Income for the three and six months ended June 30, 2014 and 2013, and Condensed Consolidating Statements of Cash Flows for the six months ended June 30, 2014 and 2013.

tw telecom inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - (Continued)

tw telecom inc.

CONDENSED CONSOLIDATING BALANCE SHEET

June 30, 2014

(unaudited)

|

| | | | | | | | | | | | | | | | | | | | |

| | | Parent Guarantor | | Issuer | | Combined Subsidiary Guarantors | | Eliminations | | Consolidated |

| | | (amounts in thousands) |

| ASSETS | | | | | | | | | | |

| Current assets: | | | | | | | | | | |

| Cash and cash equivalents | | $ | 24,546 |

| | $ | 165,617 |

| | $ | — |

| | $ | — |

| | $ | 190,163 |

|

| Investments | | — |

| | 173,564 |

| | — |

| | — |

| | 173,564 |

|

| Receivables, net | | — |

| | — |

| | 106,335 |

| | — |

| | 106,335 |

|

| Prepaid expenses and other current assets | | — |

| | 15,703 |

| | 10,042 |

| | — |

| | 25,745 |

|

| Deferred income taxes | | — |

| | 54,006 |

| | 20 |

| | — |

| | 54,026 |

|

| Intercompany receivable | | 804,463 |

| | 1,570,131 |

| | — |

| | (2,374,594 | ) | | — |

|

| Total current assets | | 829,009 |

| | 1,979,021 |

| | 116,397 |

| | (2,374,594 | ) | | 549,833 |

|

| Property, plant and equipment, net | | — |

| | 83,873 |

| | 1,650,264 |

| | — |

| | 1,734,137 |

|

| Deferred income taxes | | — |

| | 78,942 |

| | 484 |

| | — |

| | 79,426 |

|

| Goodwill | | — |

| | — |

| | 412,694 |

| | — |

| | 412,694 |

|

| Intangible and other assets, net | | — |

| | 34,280 |

| | 17,054 |

| | — |

| | 51,334 |

|

| Total assets | | $ | 829,009 |

| | $ | 2,176,116 |

| | $ | 2,196,893 |

| | $ | (2,374,594 | ) | | $ | 2,827,424 |

|

| LIABILITIES AND STOCKHOLDERS’ EQUITY (DEFICIT) | | | | | | | | | | |

| Current liabilities: | | | | | | | | | | |

| Accounts payable | | $ | — |

| | $ | 12,559 |

| | $ | 58,173 |

| | $ | — |

| | $ | 70,732 |

|

| Current portion debt and capital lease obligations | | — |

| | 5,247 |

| | 2,900 |

| | — |

| | 8,147 |

|

| Other current liabilities | | — |

| | 84,443 |

| | 131,634 |

| | — |

| | 216,077 |

|

| Intercompany payable | | — |

| | — |

| | 2,374,594 |

| | (2,374,594 | ) | | — |

|

| Total current liabilities | | — |

| | 102,249 |

| | 2,567,301 |

| | (2,374,594 | ) | | 294,956 |

|

| Losses in subsidiary in excess of investment | | 274,690 |

| | 831,084 |

| | — |

| | (1,105,774 | ) | | — |

|

| Long-term debt and capital lease obligations, net | | — |

| | 1,772,122 |

| | 142,756 |

| | — |

| | 1,914,878 |

|

| Long-term deferred revenue | | — |

| | — |

| | 19,792 |

| | — |

| | 19,792 |

|

| Other long-term liabilities | | — |

| | 11,419 |

| | 31,419 |

| | — |

| | 42,838 |

|

| Stockholders’ equity (deficit) | | 554,319 |

| | (540,758 | ) | | (564,375 | ) | | 1,105,774 |

| | 554,960 |

|

| Total liabilities and stockholders’ equity (deficit) | | $ | 829,009 |

| | $ | 2,176,116 |

| | $ | 2,196,893 |

| | $ | (2,374,594 | ) | | $ | 2,827,424 |

|

tw telecom inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - (Continued)

tw telecom inc.

CONDENSED CONSOLIDATING BALANCE SHEET

December 31, 2013

|

| | | | | | | | | | | | | | | | | | | | |

| | | Parent Guarantor | | Issuer | | Combined Subsidiary Guarantors | | Eliminations | | Consolidated |

| | | (amounts in thousands) |

| ASSETS | | | | | | | | | | |

| Current assets: | | | | | | | | | | |

| Cash and cash equivalents | | $ | 24,546 |

| | $ | 259,873 |

| | $ | — |

| | $ | — |

| | $ | 284,419 |

|

| Investments | | — |

| | 194,576 |

| | — |

| | — |

| | 194,576 |

|

| Receivables, net | | — |

| | — |

| | 107,258 |

| | — |

| | 107,258 |

|

| Prepaid expenses and other current assets | | — |

| | 14,434 |

| | 8,111 |

| | — |

| | 22,545 |

|

| Deferred income taxes | | — |

| | 54,006 |

| | 20 |

| | — |

| | 54,026 |

|

| Intercompany receivable | | 917,932 |

| | 1,475,298 |

| | — |

| | (2,393,230 | ) | | — |

|

| Total current assets | | 942,478 |

| | 1,998,187 |

| | 115,389 |

| | (2,393,230 | ) | | 662,824 |

|

| Property, plant and equipment, net | | — |

| | 75,142 |

| | 1,619,814 |

| | — |

| | 1,694,956 |

|

| Deferred income taxes | | — |

| | 95,603 |

| | 484 |

| | — |

| | 96,087 |

|

| Goodwill | | — |

| | — |

| | 412,694 |

| | — |

| | 412,694 |

|

| Intangible and other assets, net | | — |

| | 36,001 |

| | 19,898 |

| | — |

| | 55,899 |

|

| Total assets | | $ | 942,478 |

| | $ | 2,204,933 |

| | $ | 2,168,279 |

| | $ | (2,393,230 | ) | | $ | 2,922,460 |

|

| LIABILITIES AND STOCKHOLDERS’ EQUITY (DEFICIT) | | | | | | | | | | |

| Current liabilities: | | | | | | | | | | |

| Accounts payable | | $ | — |

| | $ | 8,298 |

| | $ | 30,156 |

| | $ | — |

| | $ | 38,454 |

|

| Current portion debt and capital lease obligations, net | | — |

| | 29,008 |

| | 3,462 |

| | — |

| | 32,470 |

|

| Other current liabilities | | — |

| | 87,333 |

| | 151,039 |

| | — |

| | 238,372 |

|

| Intercompany payable | | — |

| | — |

| | 2,393,230 |

| | (2,393,230 | ) | | — |

|

| Total current liabilities | | — |

| | 124,639 |

| | 2,577,887 |

| | (2,393,230 | ) | | 309,296 |

|

| Losses in subsidiary in excess of investment | | 306,440 |

| | 858,499 |

| | — |

| | (1,164,939 | ) | | — |

|

| Long-term debt and capital lease obligations, net | | — |

| | 1,773,607 |

| | 143,168 |

| | — |

| | 1,916,775 |

|

| Long-term deferred revenue | | — |

| | — |

| | 20,046 |

| | — |

| | 20,046 |

|

| Other long-term liabilities | | — |

| | 10,526 |

| | 29,748 |

| | — |

| | 40,274 |

|

| Stockholders’ equity (deficit) | | 636,038 |

| | (562,338 | ) | | (602,570 | ) | | 1,164,939 |

| | 636,069 |

|

| Total liabilities and stockholders’ equity (deficit) | | $ | 942,478 |

| | $ | 2,204,933 |

| | $ | 2,168,279 |

| | $ | (2,393,230 | ) | | $ | 2,922,460 |

|

tw telecom inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - (Continued)

tw telecom inc.

CONDENSED CONSOLIDATING STATEMENT OF OPERATIONS

Three Months Ended June 30, 2014

(unaudited)

|

| | | | | | | | | | | | | | | | | | | | |

| | | Parent Guarantor | | Issuer | | Combined Subsidiary Guarantors | | Eliminations | | Consolidated |

| | | (amounts in thousands) |

| Total revenue | | $ | — |

| | $ | — |

| | $ | 419,703 |

| | $ | — |

| | $ | 419,703 |

|

| Costs and expenses: | | | | | | | | | | |

| Operating, selling, general and administrative | | — |

| | 77,167 |

| | 212,837 |

| | — |

| | 290,004 |

|

| Depreciation, amortization and accretion | | — |

| | 9,063 |

| | 75,122 |

| | — |

| | 84,185 |

|

| Corporate expense allocation | | — |

| | (86,230 | ) | | 86,230 |

| | — |

| | — |

|

| Total costs and expenses | | — |

| | — |

| | 374,189 |

| | — |

| | 374,189 |

|

| Operating income | | — |

| | — |

| | 45,514 |

| | — |

| | 45,514 |

|

| Interest expense, net | | — |

| | (20,052 | ) | | (4,712 | ) | | — |

| | (24,764 | ) |

| Interest expense allocation | | — |

| | 20,052 |

| | (20,052 | ) | | — |

| | — |

|

| Income before income taxes and equity in undistributed earnings of subsidiaries | | — |

| | — |

| | 20,750 |

| | — |

| | 20,750 |

|

| Income tax expense | | — |

| | 9,236 |

| | 365 |

| | — |

| | 9,601 |

|

| Net income (loss) before equity in undistributed earnings of subsidiaries | | — |

| | (9,236 | ) | | 20,385 |

| | — |

| | 11,149 |

|

| Equity in undistributed earnings of subsidiaries | | 11,149 |

| | 20,385 |

| | — |

| | (31,534 | ) | | — |

|

| Net income | | $ | 11,149 |

| | $ | 11,149 |

| | $ | 20,385 |

| | $ | (31,534 | ) | | $ | 11,149 |

|

tw telecom inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - (Continued)

tw telecom inc.

CONDENSED CONSOLIDATING STATEMENT OF OPERATIONS

Three Months Ended June 30, 2013

(unaudited)

|

| | | | | | | | | | | | | | | | | | | | |

| | | Parent Guarantor | | Issuer | | Combined Subsidiary Guarantors | | Eliminations | | Consolidated |

| | | (amounts in thousands) |

| Total revenue | | $ | — |

| | $ | — |

| | $ | 389,483 |

| | $ | — |

| | $ | 389,483 |

|

| Costs and expenses: | | | | | | | | | | |

| Operating, selling, general and administrative | | — |

| | 67,167 |

| | 193,402 |

| | — |

| | 260,569 |

|

| Depreciation, amortization and accretion | | — |

| | 6,707 |

| | 68,945 |

| | — |

| | 75,652 |

|

| Corporate expense allocation | | — |

| | (73,874 | ) | | 73,874 |

| | — |

| | — |

|

| Total costs and expenses | | — |

| | — |

| | 336,221 |

| | — |

| | 336,221 |

|

| Operating income | | — |

| | — |

| | 53,262 |

| | — |

| | 53,262 |

|

| Interest expense, net | | (1,569 | ) | | (17,942 | ) | | (1,860 | ) | | — |

| | (21,371 | ) |

| Debt extinguishment costs | | (327 | ) | | (72 | ) | | — |

| | — |

| | (399 | ) |

| Interest expense allocation | | 1,896 |

| | 18,014 |

| | (19,910 | ) | | — |

| | — |

|

| Income before income taxes and equity in undistributed earnings of subsidiaries | | — |

| | — |

| | 31,492 |

| | — |

| | 31,492 |

|

| Income tax expense | | — |

| | 13,672 |

| | 473 |

| | — |

| | 14,145 |

|

| Net income (loss) before equity in undistributed earnings of subsidiaries | | — |

| | (13,672 | ) | | 31,019 |

| | — |

| | 17,347 |

|

| Equity in undistributed earnings of subsidiaries | | 17,347 |

| | 31,019 |

| | — |

| | (48,366 | ) | | — |

|

| Net income | | $ | 17,347 |

| | $ | 17,347 |

| | $ | 31,019 |

| | $ | (48,366 | ) | | $ | 17,347 |

|

tw telecom inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - (Continued)

tw telecom inc.

CONDENSED CONSOLIDATING STATEMENT OF OPERATIONS

Six Months Ended June 30, 2014

(unaudited)

|

| | | | | | | | | | | | | | | | | | | | |

| | | Parent Guarantor | | Issuer | | Combined Subsidiary Guarantors | | Eliminations | | Consolidated |

| | | (amounts in thousands) |

| Total revenue | | $ | — |

| | $ | — |

| | $ | 827,996 |

| | $ | — |

| | $ | 827,996 |

|

| Costs and expenses: | | | | | | | | | | |

| Operating, selling, general and administrative | | — |

| | 149,108 |

| | 421,767 |

| | — |

| | 570,875 |

|

| Depreciation, amortization and accretion | | — |

| | 17,654 |

| | 148,987 |

| | — |

| | 166,641 |

|

| Corporate expense allocation | | — |

| | (166,762 | ) | | 166,762 |

| | — |

| | — |

|

| Total costs and expenses | | — |

| | — |

| | 737,516 |

| | — |

| | 737,516 |

|

| Operating income | | — |

| | — |

| | 90,480 |

| | — |

| | 90,480 |

|

| Interest expense, net | | — |

| | (40,540 | ) | | (9,724 | ) | | — |

| | (50,264 | ) |

| Debt extinguishment costs | | — |

| | (1,282 | ) | | — |

| | — |

| | (1,282 | ) |

| Interest expense allocation | | — |

| | 41,822 |

| | (41,822 | ) | | — |

| | — |

|

| Income before income taxes and equity in undistributed earnings of subsidiaries | | — |

| | — |

| | 38,934 |

| | — |

| | 38,934 |

|

| Income tax expense | | — |

| | 17,253 |

| | 741 |

| | — |

| | 17,994 |

|

| Net income (loss) before equity in undistributed earnings of subsidiaries | | — |

| | (17,253 | ) | | 38,193 |

| | — |

| | 20,940 |

|

| Equity in undistributed earnings of subsidiaries | | 20,940 |

| | 38,193 |

| | — |

| | (59,133 | ) | | — |

|

| Net income | | $ | 20,940 |

| | $ | 20,940 |

| | $ | 38,193 |

| | $ | (59,133 | ) | | $ | 20,940 |

|

tw telecom inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - (Continued)

tw telecom inc.

CONDENSED CONSOLIDATING STATEMENT OF OPERATIONS

Six Months Ended June 30, 2013

(unaudited)

|

| | | | | | | | | | | | | | | | | | | | |

| | | Parent Guarantor | | Issuer | | Combined Subsidiary Guarantors | | Eliminations | | Consolidated |

| | | (amounts in thousands) |

| Total revenue | | $ | — |

| | $ | — |

| | $ | 770,692 |

| | $ | — |

| | $ | 770,692 |

|

| Costs and expenses: | | | | | | | | | | |

| Operating, selling, general and administrative | | — |

| | 131,974 |

| | 383,239 |

| | — |

| | 515,213 |

|

| Depreciation, amortization and accretion | | — |

| | 13,286 |

| | 136,761 |

| | — |

| | 150,047 |

|

| Corporate expense allocation | | — |

| | (145,260 | ) | | 145,260 |

| | — |

| | — |

|

| Total costs and expenses | | — |

| | — |

| | 665,260 |

| | — |

| | 665,260 |

|

| Operating income | | — |

| | — |

| | 105,432 |

| | — |

| | 105,432 |

|

| Interest expense, net | | (9,705 | ) | | (35,820 | ) | | (3,909 | ) | | — |

| | (49,434 | ) |

| Debt extinguishment costs | | (327 | ) | | (72 | ) | | — |

| | — |

| | (399 | ) |

| Interest expense allocation | | 10,032 |

| | 35,892 |

| | (45,924 | ) | | — |

| | — |

|

| Income before income taxes and equity in undistributed earnings of subsidiaries | | — |

| | — |

| | 55,599 |

| | — |

| | 55,599 |

|

| Income tax expense | | — |

| | 24,289 |

| | 819 |

| | — |

| | 25,108 |

|

| Net income (loss) before equity in undistributed earnings of subsidiaries | | — |

| | (24,289 | ) | | 54,780 |

| | — |

| | 30,491 |

|

| Equity in undistributed earnings of subsidiaries | | 30,491 |

| | 54,780 |

| | — |

| | (85,271 | ) | | — |

|

| Net income | | $ | 30,491 |

| | $ | 30,491 |

| | $ | 54,780 |

| | $ | (85,271 | ) | | $ | 30,491 |

|

tw telecom inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - (Continued)

tw telecom inc.

CONDENSED CONSOLIDATING STATEMENT OF COMPREHENSIVE INCOME

Three Months Ended June 30, 2014

(unaudited)

|

| | | | | | | | | | | | | | | | | | | | |

| | | Parent Guarantor | | Issuer | | Combined Subsidiary Guarantors | | Eliminations | | Consolidated |

| | | (amounts in thousands) |

| Net income | | $ | 11,149 |

| | $ | 11,149 |

| | $ | 20,385 |

| | $ | (31,534 | ) | | $ | 11,149 |

|

| Other comprehensive income, net of tax: | | | | | | | | | | |

| Unrealized gain on available-for-sale securities | | 40 |

| | 40 |

| | — |

| | (40 | ) | | 40 |

|

| Other comprehensive income, net of tax | | 40 |

| | 40 |

| | — |

| | (40 | ) | | 40 |

|

| Comprehensive income | | $ | 11,189 |

| | $ | 11,189 |

| | $ | 20,385 |

| | $ | (31,574 | ) | | $ | 11,189 |

|

tw telecom inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - (Continued)

tw telecom inc.

CONDENSED CONSOLIDATING STATEMENT OF COMPREHENSIVE INCOME

Three Months Ended June 30, 2013

(unaudited)

|

| | | | | | | | | | | | | | | | | | | | |

| | | Parent Guarantor | | Issuer | | Combined Subsidiary Guarantors | | Eliminations | | Consolidated |

| | | (amounts in thousands) |

| Net income | | $ | 17,347 |

| | $ | 17,347 |

| | $ | 31,019 |

| | $ | (48,366 | ) | | $ | 17,347 |

|

| Other comprehensive loss, net of tax: | | | | | | | | | | |

| Unrealized loss on available-for-sale securities | | (28 | ) | | (28 | ) | | — |

| | 28 |

| | (28 | ) |

| Other comprehensive loss, net of tax | | (28 | ) | | (28 | ) | | — |

| | 28 |

| | (28 | ) |

| Comprehensive income | | $ | 17,319 |

| | $ | 17,319 |

| | $ | 31,019 |

| | $ | (48,338 | ) | | $ | 17,319 |

|

tw telecom inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - (Continued)

tw telecom inc.

CONDENSED CONSOLIDATING STATEMENT OF COMPREHENSIVE INCOME

Six Months Ended June 30, 2014

(unaudited)

|

| | | | | | | | | | | | | | | | | | | | |

| | | Parent Guarantor | | Issuer | | Combined Subsidiary Guarantors | | Eliminations | | Consolidated |

| | | (amounts in thousands) |

| Net income | | $ | 20,940 |

| | $ | 20,940 |

| | $ | 38,193 |

| | $ | (59,133 | ) | | $ | 20,940 |

|

| Other comprehensive income, net of tax: | | | | | | | | | | |

| Unrealized gain on available-for-sale securities | | 30 |

| | 30 |

| | — |

| | (30 | ) | | 30 |

|

| Other comprehensive income, net of tax | | 30 |

| | 30 |

| | — |

| | (30 | ) | | 30 |

|

| Comprehensive income | | $ | 20,970 |

| | $ | 20,970 |

| | $ | 38,193 |

| | $ | (59,163 | ) | | $ | 20,970 |

|

tw telecom inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - (Continued)

tw telecom inc.

CONDENSED CONSOLIDATING STATEMENT OF COMPREHENSIVE INCOME

Six Months Ended June 30, 2013

(unaudited)

|

| | | | | | | | | | | | | | | | | | | | |

| | | Parent Guarantor | | Issuer | | Combined Subsidiary Guarantors | | Eliminations | | Consolidated |

| | | (amounts in thousands) |

| Net income | | $ | 30,491 |

| | $ | 30,491 |

| | $ | 54,780 |

| | $ | (85,271 | ) | | $ | 30,491 |

|

| Other comprehensive loss, net of tax: | | | | | | | | | | |

| Unrealized loss on available-for-sale securities | | (20 | ) | | (20 | ) | | — |

| | 20 |

| | (20 | ) |

| Other comprehensive loss, net of tax | | (20 | ) | | (20 | ) | | — |

| | 20 |

| | (20 | ) |

| Comprehensive income | | $ | 30,471 |

| | $ | 30,471 |

| | $ | 54,780 |

| | $ | (85,251 | ) | | $ | 30,471 |

|

tw telecom inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - (Continued)

tw telecom inc.

CONDENSED CONSOLIDATING STATEMENT OF CASH FLOWS

Six Months Ended June 30, 2014

(unaudited)

|

| | | | | | | | | | | | | | | | | | | | |

| | | Parent Guarantor | | Issuer | | Combined Subsidiary Guarantors | | Eliminations | | Consolidated |

| | | (amounts in thousands) |

| Cash flows from operating activities: | | | | | | | | | | |

| Net income | | $ | 20,940 |

| | $ | 20,940 |

| | $ | 38,193 |

| | $ | (59,133 | ) | | $ | 20,940 |

|

| Adjustments to reconcile net income to net cash provided by operating activities: | | | | | | | | | | |

| Depreciation, amortization and accretion | | — |

| | 17,654 |

| | 148,987 |

| | — |

| | 166,641 |

|

| Deferred income taxes | | — |

| | 17,252 |

| | — |

| | — |

| | 17,252 |

|

| Stock-based compensation expense | | — |

| | — |

| | 18,038 |

| | — |

| | 18,038 |

|

| Extinguishment costs, amortization of discount on debt and deferred debt issue costs | | — |

| | 4,494 |

| | — |

| | — |

| | 4,494 |

|

| Intercompany and equity investment changes | | 99,787 |

| | (122,248 | ) | | (36,672 | ) | | 59,133 |

| | — |

|

| Changes in operating assets and liabilities | | — |

| | 301 |

| | (3,161 | ) | | — |

| | (2,860 | ) |

| Net cash provided by (used in) operating activities | | 120,727 |

| | (61,607 | ) | | 165,385 |

| | — |

| | 224,505 |

|

| Cash flows from investing activities: | | | | | | | | | | |

| Capital expenditures | | — |

| | (26,553 | ) | | (169,445 | ) | | — |

| | (195,998 | ) |

| Purchases of investments | | — |

| | (109,275 | ) | | — |

| | — |

| | (109,275 | ) |

| Proceeds from sale of investments | | — |

| | 129,509 |

| | — |

| | — |

| | 129,509 |

|

| Other investing activities, net | | — |

| | 169 |

| | 5,672 |

| | — |

| | 5,841 |

|

| Net cash used in investing activities | | — |

| | (6,150 | ) | | (163,773 | ) | | — |

| | (169,923 | ) |

| Cash flows from financing activities: | | | | | | | | | | |

| Net proceeds (tax withholdings) from issuance of common stock upon exercise of stock options and vesting of restricted stock awards and units | | (8,163 | ) | | — |

| | — |

| | — |

| | (8,163 | ) |

| Purchases of treasury stock | | (112,564 | ) | | — |

| | — |

| | — |

| | (112,564 | ) |

| Excess tax benefits from stock-based compensation | | — |

| | 794 |

| | — |

| | — |

| | 794 |

|

| Retirement of debt obligations | | — |

| | (24,418 | ) | | — |

| | — |

| | (24,418 | ) |

| Payment of debt and capital lease obligations | | — |

| | (2,875 | ) | | (1,612 | ) | | — |

| | (4,487 | ) |

| Net cash used in financing activities | | (120,727 | ) | | (26,499 | ) | | (1,612 | ) | | — |

| | (148,838 | ) |

| Decrease in cash and cash equivalents | | — |

| | (94,256 | ) | | — |

| | — |

| | (94,256 | ) |

| Cash and cash equivalents at beginning of period | | 24,546 |

| | 259,873 |

| | — |

| | — |

| | 284,419 |

|

| Cash and cash equivalents at end of period | | $ | 24,546 |

| | $ | 165,617 |

| | $ | — |

| | $ | — |

| | $ | 190,163 |

|

tw telecom inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - (Continued)

tw telecom inc.

CONDENSED CONSOLIDATING STATEMENT OF CASH FLOWS

Six Months Ended June 30, 2013

(unaudited)

|

| | | | | | | | | | | | | | | | | | | | |

| | | Parent Guarantor | | Issuer | | Combined Subsidiary Guarantors | | Eliminations | | Consolidated |

| | | (amounts in thousands) |

| Cash flows from operating activities: | | | | | | | | | | |

| Net income | | $ | 30,491 |

| | $ | 30,491 |

| | $ | 54,780 |

| | $ | (85,271 | ) | | $ | 30,491 |

|

| Adjustments to reconcile net income to net cash provided by operating activities: | | | | | | | | | | |

| Depreciation, amortization and accretion | | — |

| | 13,286 |

| | 136,761 |

| | — |

| | 150,047 |

|

| Deferred income taxes | | — |

| | 24,289 |

| | — |

| | — |

| | 24,289 |

|

| Stock-based compensation expense | | — |

| | — |

| | 17,876 |

| | — |

| | 17,876 |

|

| Amortization of discount on debt and deferred debt issue costs | | 6,244 |

| | 2,005 |

| | — |

| | — |

| | 8,249 |

|

| Intercompany and equity investment changes | | 385,403 |

| | (466,631 | ) | | (4,043 | ) | | 85,271 |

| | — |

|

| Changes in operating assets and liabilities | | (1,039 | ) | | 15,973 |

| | (39,326 | ) | | — |

| | (24,392 | ) |

| Net cash provided by (used in) operating activities | | 421,099 |

| | (380,587 | ) | | 166,048 |

| | — |

| | 206,560 |

|

| Cash flows from investing activities: | | | | | | | | | | |

| Capital expenditures | | — |

| | (22,465 | ) | | (165,044 | ) | | — |

| | (187,509 | ) |

| Purchases of investments | | — |

| | (157,523 | ) | | — |

| | — |

| | (157,523 | ) |

| Proceeds from sale of investments | | — |

| | 125,041 |

| | — |

| | — |

| | 125,041 |

|

| Other investing activities, net | | — |

| | (83 | ) | | (382 | ) | | — |

| | (465 | ) |

| Net cash used in investing activities | | — |

| | (55,030 | ) | | (165,426 | ) | | — |

| | (220,456 | ) |

| Cash flows from financing activities: | | | | | | | | | | |

| Net proceeds (tax withholdings) from issuance of common stock upon exercise of stock options and vesting of restricted stock awards and units | | 32,559 |

| | — |

| | — |

| | — |

| | 32,559 |

|

| Purchases of treasury stock | | (197,310 | ) | | — |

| | — |

| | — |

| | (197,310 | ) |

| Excess tax benefits from stock-based compensation | | — |

| | 944 |

| | — |

| | — |

| | 944 |

|

| Proceeds from modification of debt, net of financing costs | | — |

| | 49,684 |

| | — |

| | — |

| | 49,684 |

|

| Retirement of convertible debt obligations | | (256,348 | ) | | — |

| | — |

| | — |

| | (256,348 | ) |

| Payment of debt and capital lease obligations | | — |

| | (1,474 | ) | | (622 | ) | | — |

| | (2,096 | ) |

| Net cash (used in) provided by financing activities | | (421,099 | ) | | 49,154 |

| | (622 | ) | | — |

| | (372,567 | ) |

| Decrease in cash and cash equivalents | | — |

| | (386,463 | ) | | — |

| | — |

| | (386,463 | ) |

| Cash and cash equivalents at beginning of period | | 24,544 |

| | 782,184 |

| | — |

| | — |

| | 806,728 |

|

| Cash and cash equivalents at end of period | | $ | 24,544 |

| | $ | 395,721 |

| | $ | — |

| | $ | — |

| | $ | 420,265 |

|

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis provides information regarding the results of operations and financial condition of the Company and should be read in conjunction with the accompanying condensed consolidated financial statements and notes thereto. This discussion and analysis also should be read in conjunction with Management’s Discussion and Analysis of Financial Condition and Results of Operations and the consolidated financial statements included in Part II of our Annual Report on Form 10-K for the year ended December 31, 2013. References in this item to “we,” “our,” or “us” are to the Company and its subsidiaries on a consolidated basis unless the context otherwise requires.

In order to assist the reader in understanding certain terms relating to the telecommunications business that are used in this Quarterly Report on Form 10-Q, we refer you to the glossary included following Part III of our Annual Report on Form 10-K for the year ended December 31, 2013. Certain terms used in this Item 2 without definition have the meanings given them in Item 1 of this Quarterly Report on Form 10-Q.

Cautions Concerning Forward-Looking Statements

This document contains certain “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, including statements regarding, among other items, our expected financial position, capital expenditures, business and technology trends, fluctuations, the impact of the economic downturn, activities and results, revenue mix and revenue growth, Modified EBITDA and margin trends, the impact of regulatory changes, future tax benefits and expense, expense trends, growth initiatives, increases in sales personnel, future liquidity and capital resources, product plans, share repurchases, debt retirement, future cash balances, growth or stability from particular customer segments, the effects of consolidation in the telecommunications industry, anticipated customer disconnections and customer and revenue churn, market expansion, business and financing plans, and the expected merger with Level 3. These forward-looking statements are based on management’s current expectations and are naturally subject to risks, uncertainties, and changes in circumstances, certain of which are beyond our control. Actual results may differ materially from those expressed or implied by such forward-looking statements.