Forward Looking Statement

• This presentation contains certain forward-looking statements and

information relating to the Company that are based on the beliefs of

management as well as assumptions made by and information currently

available to management. In addition, the words “anticipate,” “believe,”

“estimate,” “expect,” “intend,” “should” and similar expressions, or the

negative thereof, as they relate to the Company or the Company’s

management, are intended to identify forward-looking statements. Such

statements reflect the current views of the Company with respect to future

events and are subject to certain risks, uncertainties, changes in circumstances

and assumptions. Should one or more of these risks, uncertainties or changes

in circumstances materialize or should underlying assumptions prove

incorrect, actual results or outcomes may vary materially from those described

herein as anticipated, believed, estimated, expected or intended. Forward -

looking statements are not assurances of future results, performance or

outcomes. The Company does not intend to update these forward-looking

statements.

information relating to the Company that are based on the beliefs of

management as well as assumptions made by and information currently

available to management. In addition, the words “anticipate,” “believe,”

“estimate,” “expect,” “intend,” “should” and similar expressions, or the

negative thereof, as they relate to the Company or the Company’s

management, are intended to identify forward-looking statements. Such

statements reflect the current views of the Company with respect to future

events and are subject to certain risks, uncertainties, changes in circumstances

and assumptions. Should one or more of these risks, uncertainties or changes

in circumstances materialize or should underlying assumptions prove

incorrect, actual results or outcomes may vary materially from those described

herein as anticipated, believed, estimated, expected or intended. Forward -

looking statements are not assurances of future results, performance or

outcomes. The Company does not intend to update these forward-looking

statements.

1

Why Invest in CITZ?

• We have a strong retail franchise and an emerging business banking operation located

in one of the Country’s premier markets for small and middle-market businesses

in one of the Country’s premier markets for small and middle-market businesses

• We are a community-oriented financial institution which is well positioned to benefit

from ongoing Chicago area market disruption due to:

from ongoing Chicago area market disruption due to:

• Bank failures

• Capital challenges and growth limitations

• Mergers

• Changes in large bank lending practices

• Capital base and liquidity allow us to pursue opportunities for high quality relationship-

based loan growth

based loan growth

• Over the past few years, we have invested heavily in different aspects of our core

franchise, including our physical (branch) delivery system, information technology

infrastructure, retail and business banking personnel and brand positioning, and are

poised to capitalize on that investment as the economy recovers

franchise, including our physical (branch) delivery system, information technology

infrastructure, retail and business banking personnel and brand positioning, and are

poised to capitalize on that investment as the economy recovers

2

About CFS Bancorp, Inc.

• CFS Bancorp, Inc is incorporated under the laws of the State of Indiana, headquartered in

Munster, IN

Munster, IN

• Company was formed in 1998 in conjunction with the conversion of its principal

subsidiary from a mutual to a stock savings bank; Bank originally founded in 1934

subsidiary from a mutual to a stock savings bank; Bank originally founded in 1934

• As of June 30, 2009, assets of $1.1 billion and 318 (FTE) employees

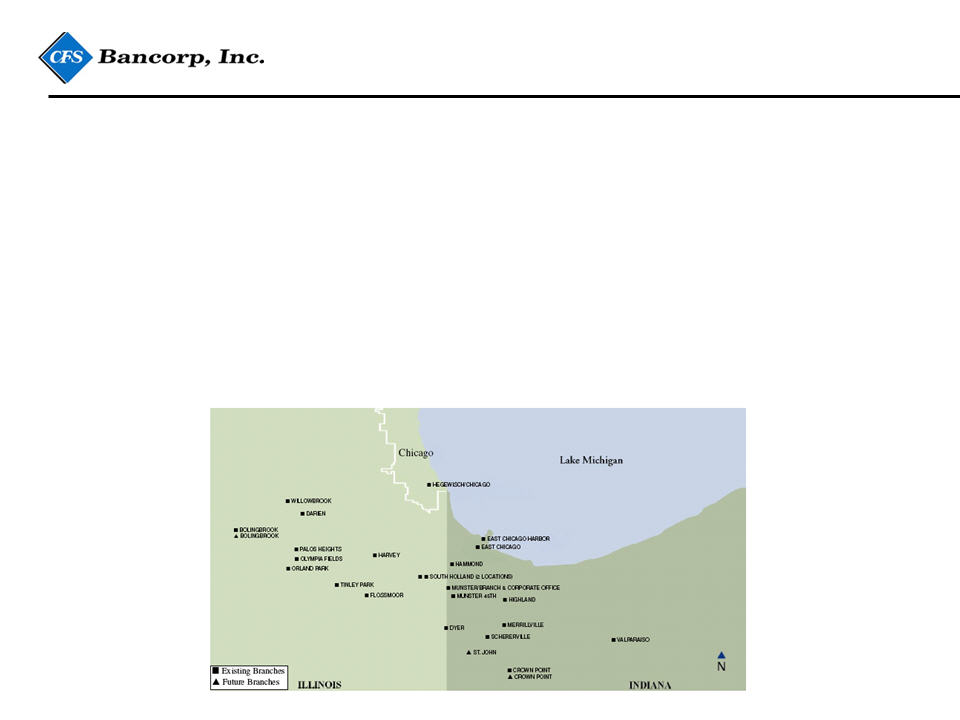

• Operates a single subsidiary bank, Citizens Financial Bank, with 22 full service banking

centers spread across five counties in Indiana (Porter, Lake) and Illinois (Will, Cook,

DuPage), all of which are part of the Chicago metropolitan statistical area

centers spread across five counties in Indiana (Porter, Lake) and Illinois (Will, Cook,

DuPage), all of which are part of the Chicago metropolitan statistical area

• Operations center located in Highland, IN (relocating to existing bank-owned facilities in 2009)

3

• Strong retail and emerging business banking franchise

• Legacy of returning excess capital to shareholders in the form of dividends and stock

repurchases

repurchases

• From 1998 to mid-2008, repurchased nearly 60 percent of shares originally issued in public

offering, totaling in excess of 12 million shares

offering, totaling in excess of 12 million shares

• Experienced management team

• Thomas Prisby, Chairman & CEO

• Daryl Pomranke, President

• Charles Cole, CFO

• Dale Clapp, Executive VP, Business Banking

• Daniel Zimmer, Sr. VP & Chief Credit Officer

About CFS Bancorp, Inc. (cont.)

4

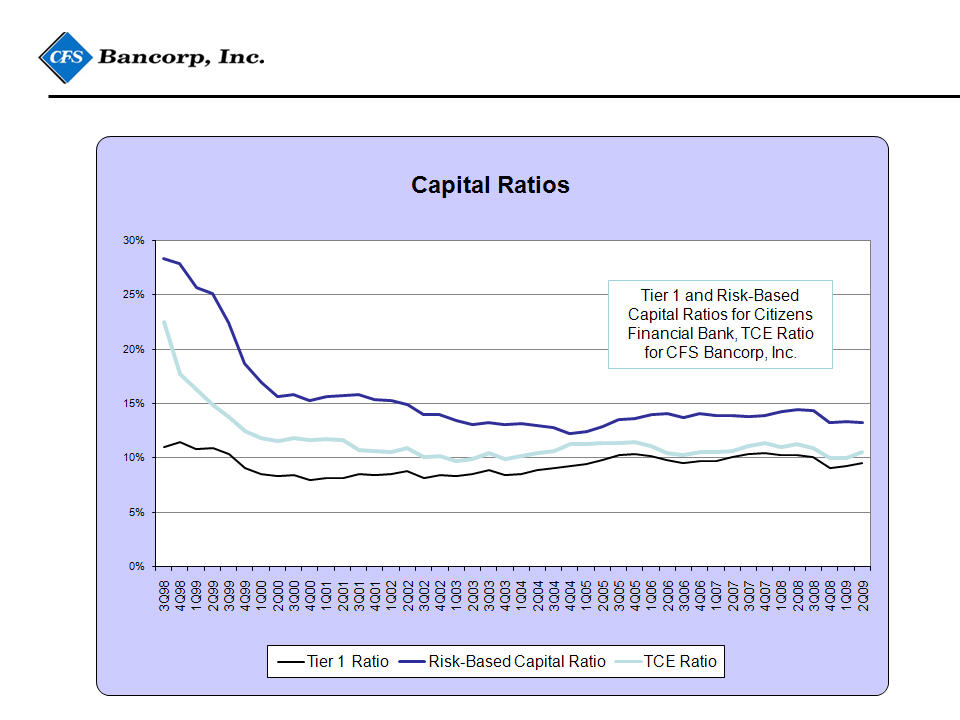

Capital Adequacy

5

Strategic Growth and Diversification Plan

In early 2008, we began executing our Strategic Growth and Diversification Plan, which

has four key objectives:

has four key objectives:

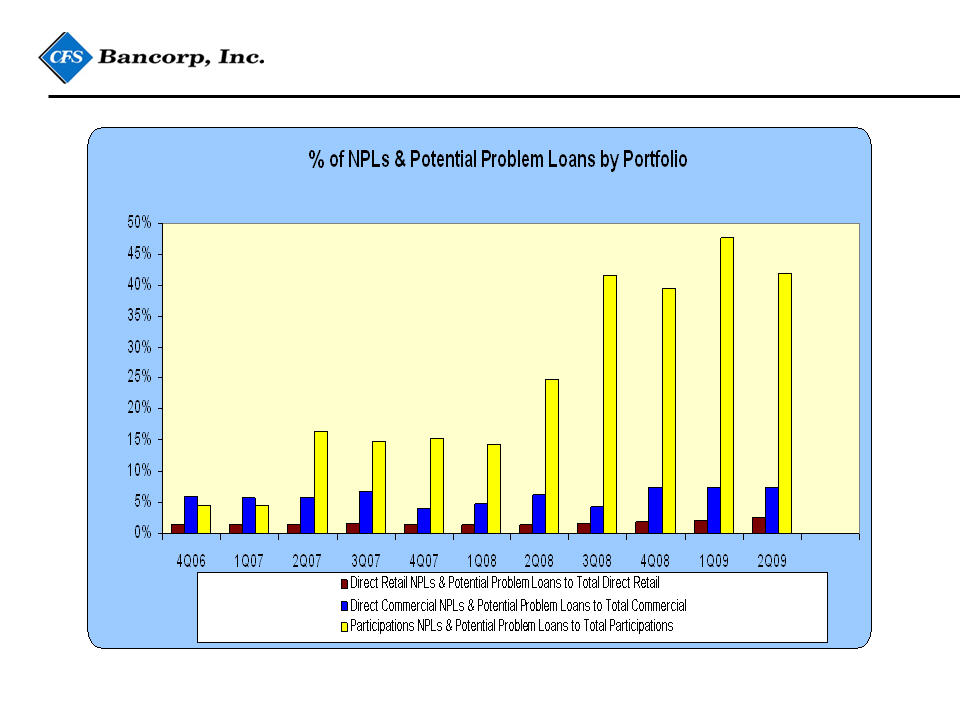

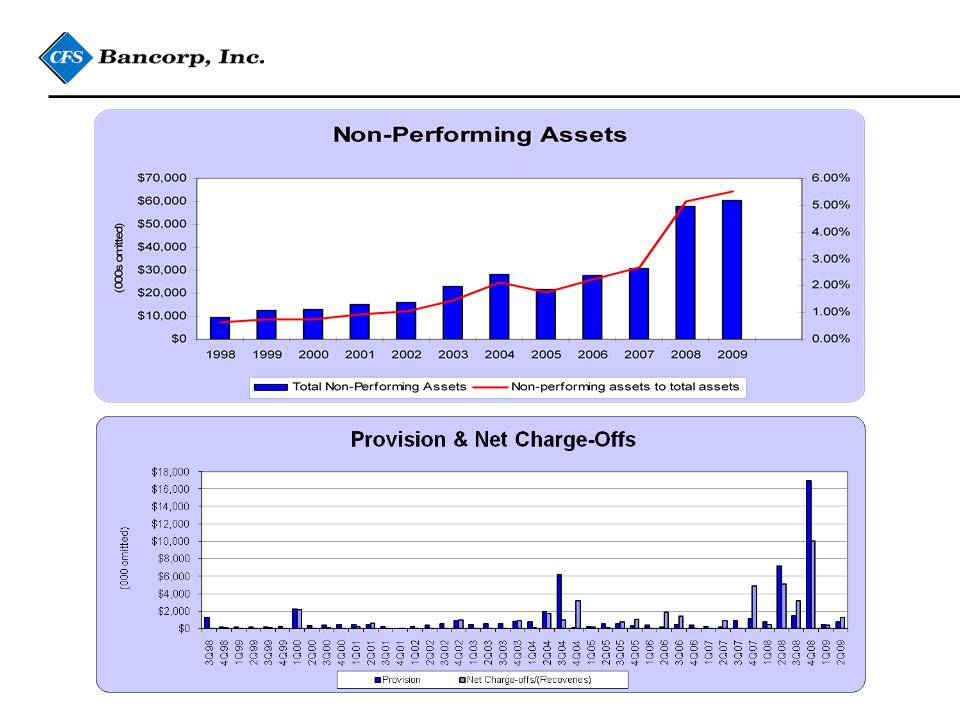

Decrease nonperforming loans

The Company’s delinquency rates and nonperforming loan ratios exceed that of its peers. This is

partly attributable to the Company’s prior utilization of syndications and participations to supplement

the direct origination of its commercial loan portfolio. The utilization of participations to achieve

commercial loan growth was ended when the Company adopted its relationship-based business

banking strategy in mid-2007. Our last participation loan was originated in June, 2007. Commencing

in 2007, and running through today, the Bank has experienced significant credit quality issues in this

segment of the loan portfolio. Nonperforming loan ratios of direct origination loans are more in line

with peers.

partly attributable to the Company’s prior utilization of syndications and participations to supplement

the direct origination of its commercial loan portfolio. The utilization of participations to achieve

commercial loan growth was ended when the Company adopted its relationship-based business

banking strategy in mid-2007. Our last participation loan was originated in June, 2007. Commencing

in 2007, and running through today, the Bank has experienced significant credit quality issues in this

segment of the loan portfolio. Nonperforming loan ratios of direct origination loans are more in line

with peers.

Bring costs in line with our anticipated future asset base

A significant proportion of the Company’s investments in technology, people and brand positioning,

impact the Company’s earnings through the income statement as expenses. As a result, during a

period of heavy investment (such as when the Company began to upgrade its retail delivery sales and

service capabilities in 2007, or when it rapidly expanded its relationship-based business banking

activities in early 2008), the Company’s earning asset and income growth lags its expense growth.

impact the Company’s earnings through the income statement as expenses. As a result, during a

period of heavy investment (such as when the Company began to upgrade its retail delivery sales and

service capabilities in 2007, or when it rapidly expanded its relationship-based business banking

activities in early 2008), the Company’s earning asset and income growth lags its expense growth.

6

Strategic Growth and Diversification Plan (cont.)

Targeting small to mid-size business owners

Since early 2008, we have focused on building and enhancing our capabilities to serve the small- to

mid-sized business market. We believe that the breadth and diversity of the financial service needs of

these business owners presents an ideal match for a financial institution of our size with our

capabilities. We have an experienced chief credit officer (Sr. VP Daniel Zimmer), strengthened our

credit team, revised our loan policy and underwriting standards to ensure that all loans originated

meet stringent underwriting standards. We have a seasoned team of 16 business banking relationship

managers, led by Executive VP Dale Clapp; 10 of these bankers have joined us since the start of 2008.

Our suite of deposit, cash management and lending products, targeted to this market’s needs, give us

a competitive advantage. Within each sub-market we serve, our banking center managers work

closely with our business bankers, our micro business lenders, our cash management team, and our

senior personal bankers (who are responsible for mortgage origination and consumer lending), to

design solutions which meet the needs of that market.

mid-sized business market. We believe that the breadth and diversity of the financial service needs of

these business owners presents an ideal match for a financial institution of our size with our

capabilities. We have an experienced chief credit officer (Sr. VP Daniel Zimmer), strengthened our

credit team, revised our loan policy and underwriting standards to ensure that all loans originated

meet stringent underwriting standards. We have a seasoned team of 16 business banking relationship

managers, led by Executive VP Dale Clapp; 10 of these bankers have joined us since the start of 2008.

Our suite of deposit, cash management and lending products, targeted to this market’s needs, give us

a competitive advantage. Within each sub-market we serve, our banking center managers work

closely with our business bankers, our micro business lenders, our cash management team, and our

senior personal bankers (who are responsible for mortgage origination and consumer lending), to

design solutions which meet the needs of that market.

Meeting a greater number of our clients’ financial service needs

The Chicago area, while attractive from a demographic perspective, is relatively slow growing. As a

result, our ability to grow disproportionately to the market is, and will for the foreseeable future, be

contingent upon our ability to gain market share. There are two basic strategies through which we

can accomplish this: obtain new client relationships from other institutions, and meet a higher

percentage of the financial service needs of our current clients. Of these, the latter is a relatively more

cost efficient means through which we can grow our franchise. Two main areas of focus are: (1)

selling a higher number of loan and deposit products and services to our retail clients and (2)

obtaining the personal banking relationships of our small and middle-market business banking clients.

result, our ability to grow disproportionately to the market is, and will for the foreseeable future, be

contingent upon our ability to gain market share. There are two basic strategies through which we

can accomplish this: obtain new client relationships from other institutions, and meet a higher

percentage of the financial service needs of our current clients. Of these, the latter is a relatively more

cost efficient means through which we can grow our franchise. Two main areas of focus are: (1)

selling a higher number of loan and deposit products and services to our retail clients and (2)

obtaining the personal banking relationships of our small and middle-market business banking clients.

7

Credit Quality

8

Our Approach to the Market

• Our network of Banking Centers serves a wide variety of market areas

• Each Banking Center focuses on meeting the financial service needs of specific niches

within in its uniquely defined market area (generally, an geographically delineated area

of 10-15 square miles immediately surrounding the banking center location)

within in its uniquely defined market area (generally, an geographically delineated area

of 10-15 square miles immediately surrounding the banking center location)

• Banking Center Managers are responsible for developing and executing sales and

marketing action plans, with specific goals and objectives

marketing action plans, with specific goals and objectives

• These plans, which are reviewed and approved by senior management, target specific

client segments or niches within each market area, and leverage specific marketing

capabilities and campaigns to pursue the niche

client segments or niches within each market area, and leverage specific marketing

capabilities and campaigns to pursue the niche

• Business development and calling efforts are integrated across multiple lines of

business, encompassing business banking, cash management specialists, microlending

(small business lenders), personal banking (including mortgage origination),

community development, High Life (banking for those aged 50 and up) and marketing

business, encompassing business banking, cash management specialists, microlending

(small business lenders), personal banking (including mortgage origination),

community development, High Life (banking for those aged 50 and up) and marketing

• “Total relationship”-based goals and incentive compensation plans ensure that groups

function as a team focused on identifying and fulfilling clients’ needs

function as a team focused on identifying and fulfilling clients’ needs

9

What We’ve Been Focused On

• Proactively assessed and took action to mitigate portfolio credit risks

• Eliminated syndication / participation originations

• Implemented “exit strategy” on loans not meeting our risk tolerances

• Invested significantly in our core retail and small- and middle-market business banking

franchises

franchises

• Invested in our human capital

• Upgraded banking center managers (2007/2008)

• Added experienced chief credit officer and upgraded credit team (2007/2008)

• Upgraded business banking franchise (2008)

– Hired “seasoned” C&I team

– Introduced sophisticated cash management/business deposits product suite,

staffed with cash management sales team to support business bankers

staffed with cash management sales team to support business bankers

• Enhanced retail sales and service, performance management culture and performance

tracking in retail delivery network (ongoing)

tracking in retail delivery network (ongoing)

• Introduced banking center market-specific sales plan approach (2008/2009)

• Segmented client base into key niches for business development, marketing and retention

purposes (e.g., Chairman’s Club, High Life) (ongoing)

purposes (e.g., Chairman’s Club, High Life) (ongoing)

• Invested in communicating and increasing awareness of our brand in retail and business

banking

banking

10

What We’ve Been Focused On

• Enhanced and upgraded IT capabilities to support cash management strategies

• Upgraded and expanded physical delivery network (ongoing)

• Planning/developing additional locations in St. John (2009), Crown Point (2010) and

Bolingbrook (2011)

Bolingbrook (2011)

• New locations planned in Olympia Fields (to replace Flossmoor, 2010) and Harvey (2010)

11

Key Challenges

• Economy

• Credit quality

• Improving NPA ratios

• Mitigating potential impacts on brand, reputation

• Opportunistically reducing overall costs in light of higher FDIC assessments & credit

collection related costs

collection related costs

• Achieving targeted earning asset growth levels

• Retaining talented individuals to carry out our relationship banking strategies

12

Opportunities: Going Forward

• Position CFS Bancorp, Inc. to capitalize on opportunities that will emerge as economy

commences recovery

commences recovery

• Leverage capital strength and “personal” service orientation to differentiate us from

the competition and capture greater market and relationship share

the competition and capture greater market and relationship share

• Selectively expand geographic footprint through:

• Branching

• Opportunistic acquisitions

• Examine wealth management opportunities

• Good “fit” with small- and middle-market business owner/operator niche

• Sizeable base of large depositors

• Market opportunity for moderately sized relationships (e.g., $500,000 to $750,000 in

investable assets) common in this niche

investable assets) common in this niche

13

Key Takeaways

• Strong, stable institution with solid capital levels and ample liquidity

• Right strategy and infrastructure in place to address current challenges and position for

future growth

future growth

• Emerging from period of heavy investment well positioned to take advantage of

opportunities presented by economic recovery

opportunities presented by economic recovery

• Management team focused on executing strategy:

• Addressing credit issues

• Aligning costs

• Developing business banking franchise

• Capitalizing on retail franchise

14

Supplemental

Information

Information

Mission & Vision

Citizens Financial Bank Mission

To become the leading banking institution in our markets by providing extraordinary

service and personalized financial solutions for our clients, resulting in superior value

creation for our communities, clients, shareholders and employees

service and personalized financial solutions for our clients, resulting in superior value

creation for our communities, clients, shareholders and employees

Vision

To be a high-performing independent community bank focused on the financial needs

of businesses and individuals

of businesses and individuals

15

Our Market Area

Measure | Five County Area* | Banking Center Defined Market Areas (22)** | ||

Composite | Low (Market) | High (Market) | ||

Households | 2,869,699 | 109,049 | 833 (Willowbrook) | 9,523 (Munster HQ) |

Businesses | 317,191 | 22,026 | 133 (Bolingbrook) | 2,677 (Merrillville) |

HH Pop. By Age | ||||

<24 | 34.9% | 34.0% | 25.0% (Willowbrook) | 44.9% (Harvey) |

25-44 | 29.1% | 24.5% | 16.6% (Flossmoor) | 35.3% (Bolingbrook) |

45-64 | 24.1% | 28.0% | 20.2% (East Chicago) | 34.3% (Flossmoor) |

65+ | 11.8% | 13.5% | 3.6%(Bolingbrook) | 29.3% (Willowbrook) |

Avg. HH Income | $78,917 | $76,757 | $38,247 (East Chicago) | $109,404 (Bolingbrook) |

HH Income Dist. | ||||

<$25K | 19.2% | 17.3% | 3.4% (Bolingbrook) | 43.3% (East Chicago) |

$25K-$49K | 25.0% | 22.6% | 7.2% (Bolingbrook) | 36.3% (Merrillville) |

$50K-$149K | 51.3% | 52.3% | 25.9% (East Chicago) | 76.4% (Bolingbrook) |

>$150K | 4.5% | 7.9% | 0.8% (Hammond) | 25.1% (Willowbrook) |

16

*Source: Pitney Bowes Business Insight

** Source: BankIntelligence

Citizens Financial Bank Banking Center Network

Location | Owned/ Leased | Deposits ($000) @ 12/31/08 | Customer Relationships (HH at 3/31/09, rounded to nearest 10) | ||

Consumer | Businesses | Both Business & Consumer | |||

Indiana | |||||

Munster HQ | Owned | $150,825 | 4,730 | 300 | 280 |

Crown Point | Owned | $65,962 | 2,650 | 100 | 110 |

Dyer | Leased | $81,870 | 950 | 40 | 50 |

East Chicago #1 | Owned | $32,829 | 2,150 | 40 | 50 |

East Chicago Harbor | Leased | $18,188 | 1,380 | 20 | 40 |

Hammond | Owned | $51,012 | 2,180 | 70 | 70 |

Highland | Owned | $25,635 | 1,320 | 50 | 50 |

Merrillville | Owned | $23,690 | 1,350 | 70 | 70 |

Munster #2 | Owned | $87,530 | 2,270 | 80 | 90 |

Schererville | Owned | $29,453 | 930 | 40 | 50 |

Valparaiso | Owned | $43,160 | 1,390 | 90 | 90 |

17

Location | Owned/ Leased | Deposits ($000) @ 12/31/08 | Customer Relationships (HH at 3/31/09, Rounded to nearest 10) | ||

Consumer | Businesses | Both Business & Consumer | |||

Illinois | |||||

Bolingbrook | Owned | $5,247 | 330 | 50 | 40 |

Darien | Owned | $13,636 | 360 | 50 | 40 |

Flossmoor | Leased | $36,883 | 1,720 | 110 | 100 |

Harvey | Leased | $19,972 | 1,640 | 60 | 70 |

Hegewisch | Owned | $26,426 | 1,070 | 20 | 30 |

Orland Park | Leased | $12,986 | 400 | 10 | 20 |

Palos Heights | Owned | $40,564 | 1,280 | 50 | 70 |

South Holland | Owned | $42,778 | 2,290 | 80 | 110 |

South Holland #2 | Owned | (Included Above) | |||

Tinley Park | Owned | $3,737 | 210 | 10 | 20 |

Willowbrook | Leased | $11,687 | 390 | 40 | 50 |

Citizens Financial Bank Banking Center Network

18

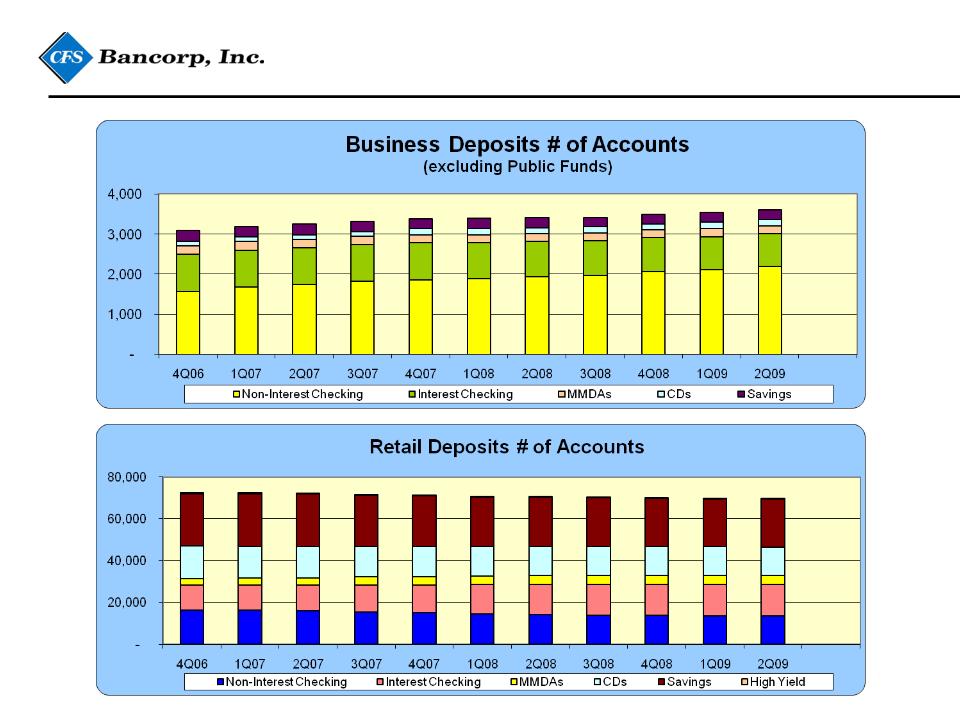

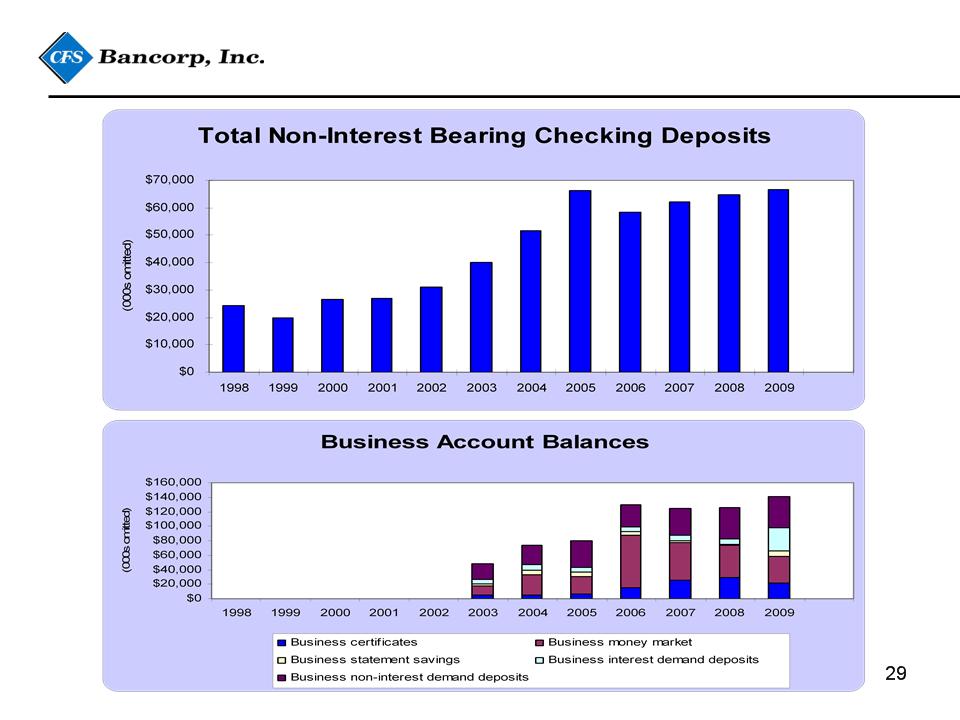

Business & Retail Accounts

19

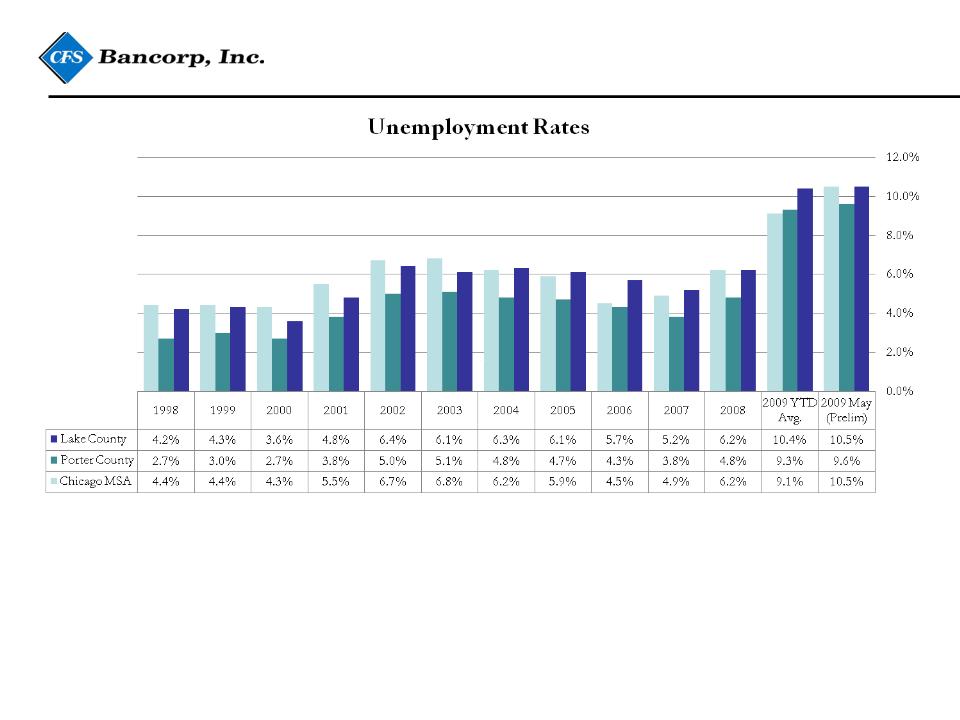

Economic Woes in Chicago & Northwest Indiana

• Employment continues to decline

• Citizens Financial Bank serves a diverse range of market areas, including many areas

dependent upon manufacturing employment

dependent upon manufacturing employment

• Hard hit sectors include steelmaking, automotive, and recreational vehicles

20

Branding

21

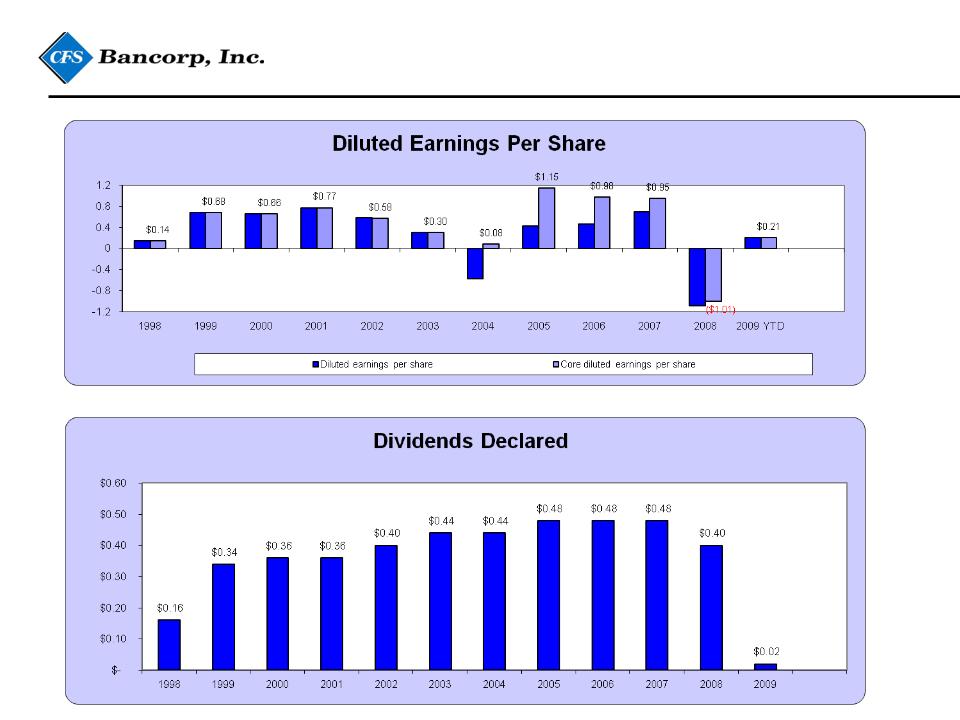

Financial Information

Financial Highlights

22

Financial Highlights

23

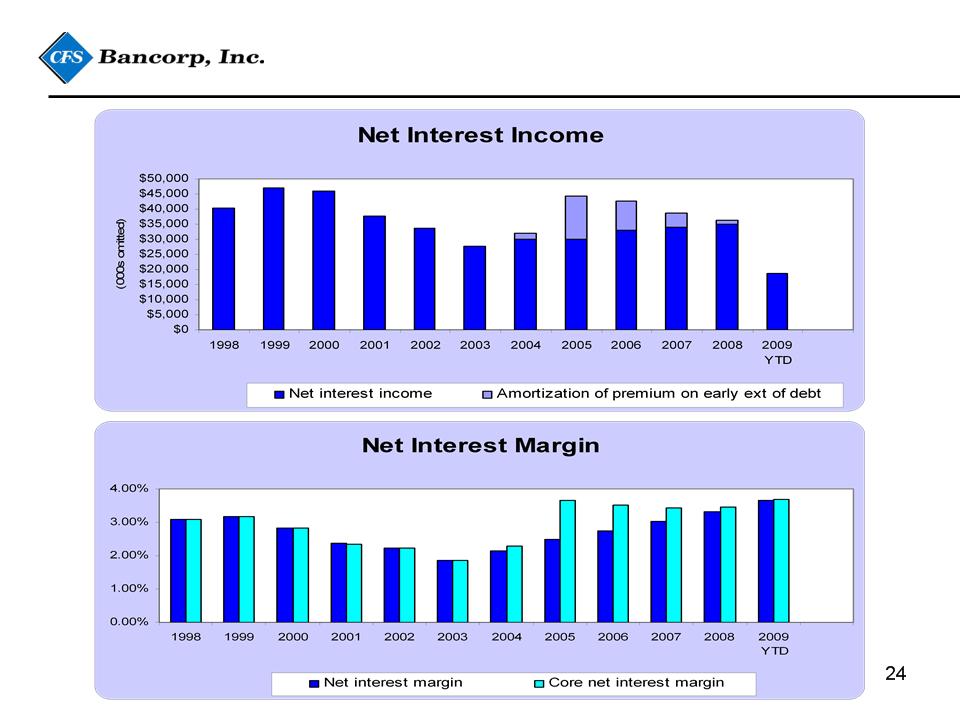

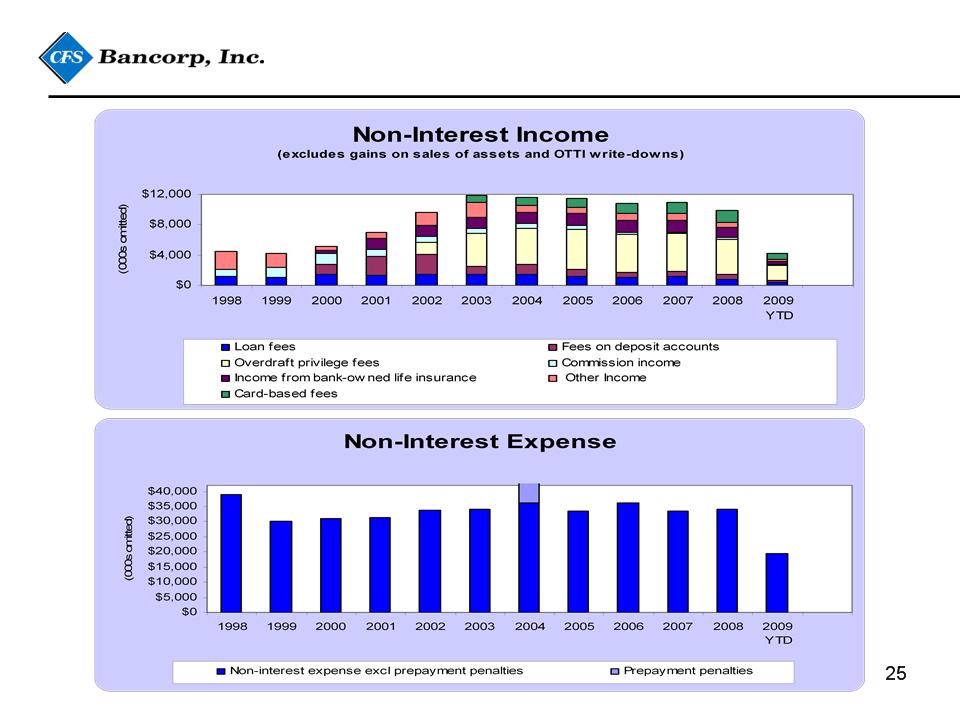

Income Statement

Income Statement

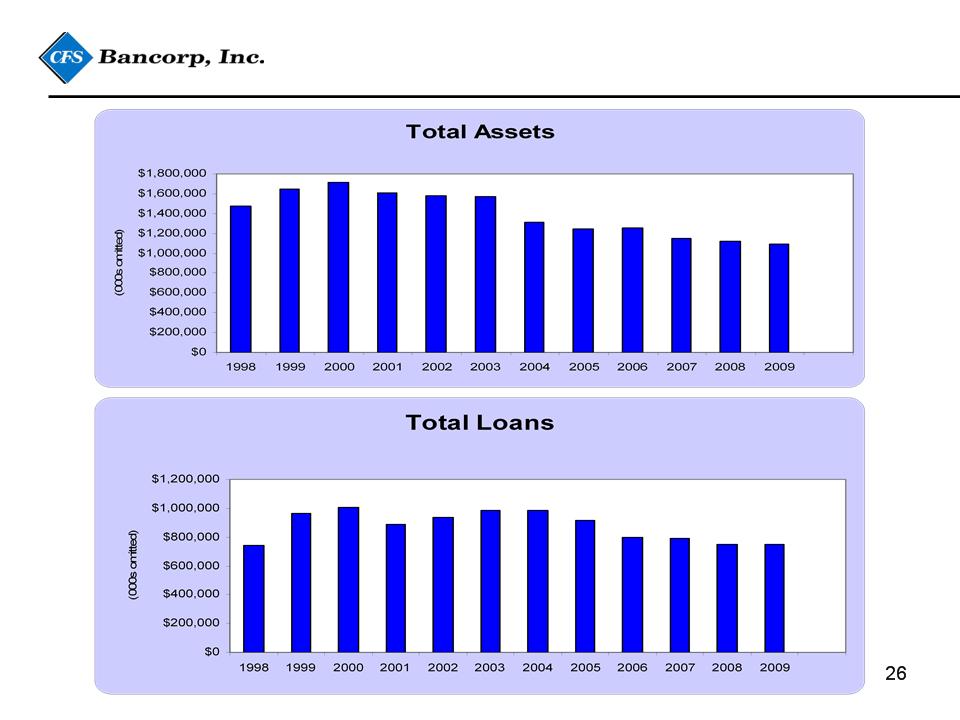

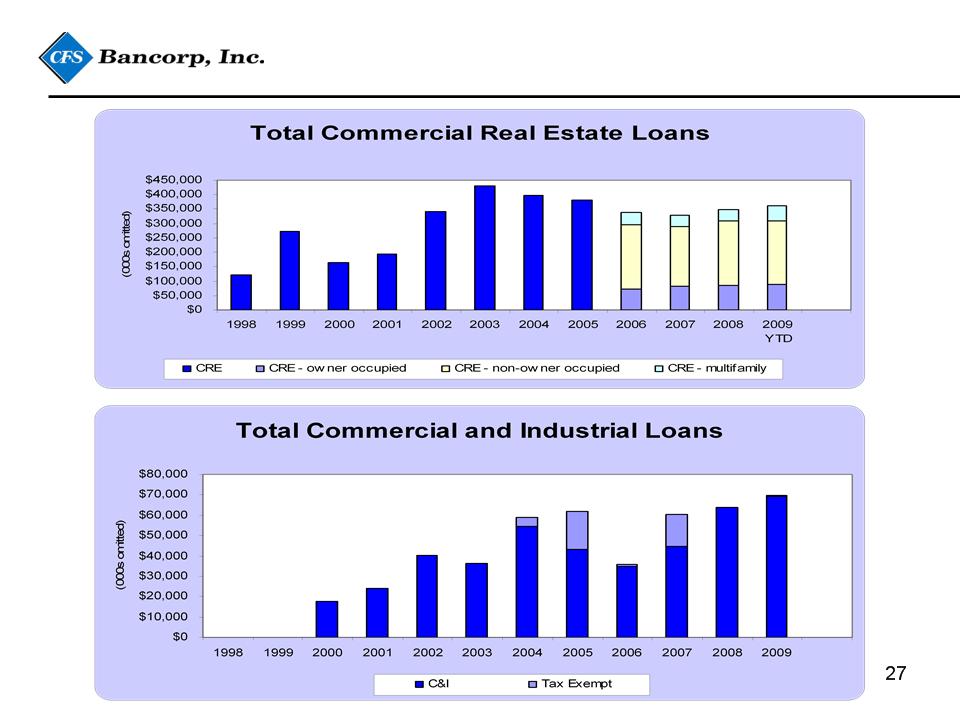

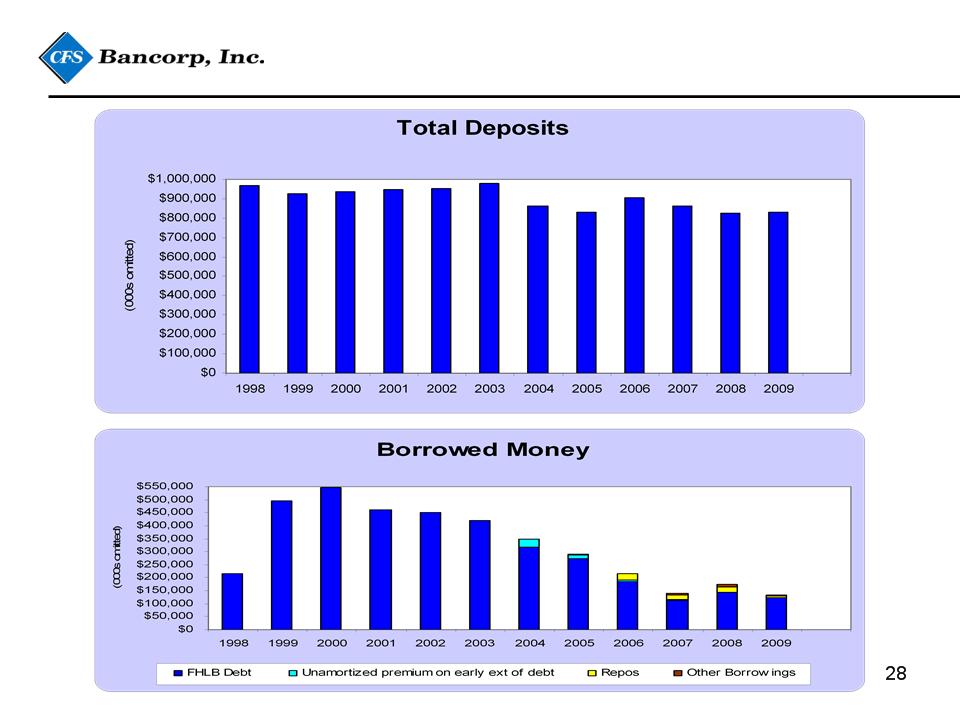

Balance Sheet

Balance Sheet

Balance Sheet

Balance Sheet

Balance Sheet

Credit Quality

31

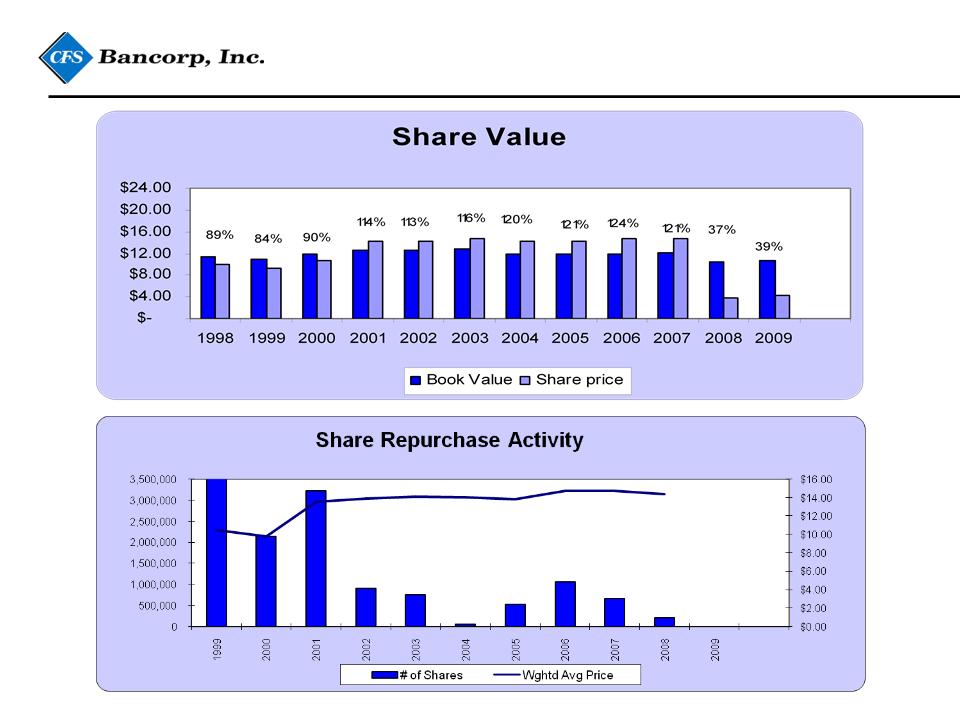

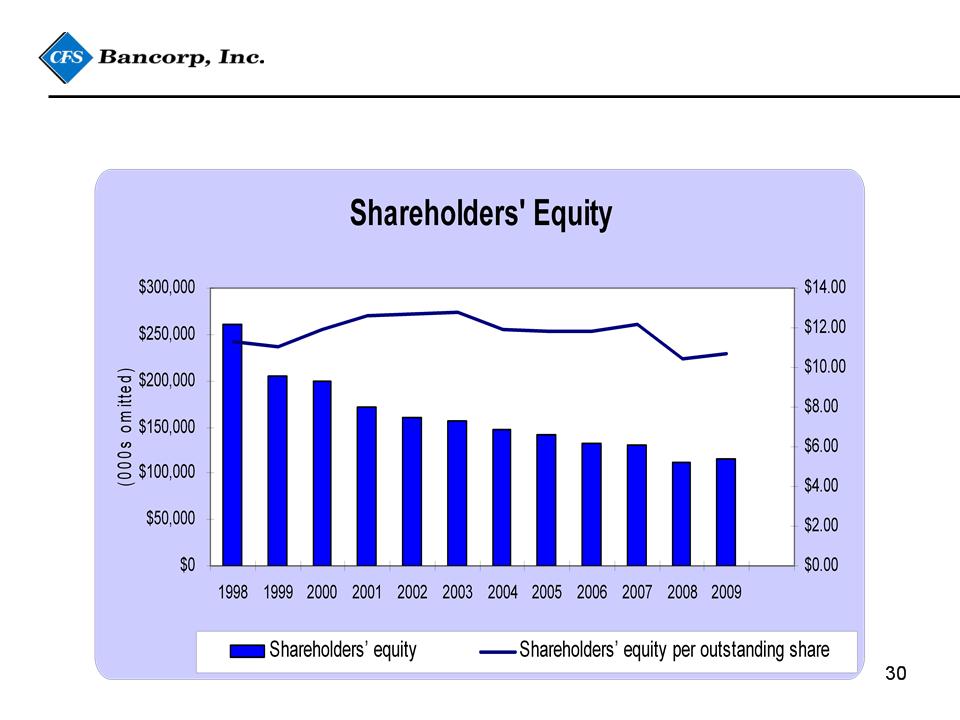

CITZ Stock At a Glance:

At June 30, 2009

Shares Outstanding: 10.8 million

Market Capitalization: $45.5 million

Annual Dividend per share: $0.04

Dividend yield: 0.99%

Average 2009 Daily Volume: 17,400

Book Value Per Share (6/30/09): $10.72

Recent Price (July 23, 2009): $4.03

Price/Book: 37.6%

Return on Assets (2Q09): 0.24%

Return on Equity (2Q09): 2.41%

32