Table of Contents

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 30, 2001

OR

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File Number: 333-49821

MSX INTERNATIONAL, INC.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) | 38-3323099 (I.R.S. Employer Identification No.) | |

| 275 Rex Boulevard, Auburn Hills, Michigan (Address of principal executive offices) | 48326 (Zip Code) |

(248) 299-1000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities and Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X]

None of the registrant’s common stock is held by non-affiliates of the registrant.

Number of shares outstanding of each of the registrant’s classes of common stock at March 4, 2002:

20,054,000 shares of Class A Common Stock, $0.01 par value.

TABLE OF CONTENTS

Table of Contents

TABLE OF CONTENTS

| Item | Page | |||||||

PART I | ||||||||

| 1. | Business | 2 | ||||||

| 2. | Properties | 9 | ||||||

| 3. | Legal Proceedings | 9 | ||||||

| 4. | Submission of Matters to a Vote of Security Holders | 9 | ||||||

PART II | ||||||||

| 5. | Market for Registrant's Common Equity and Related Stockholder Matters | 10 | ||||||

| 6. | Selected Financial Data | 11 | ||||||

| 7. | Management's Discussion and Analysis of Financial Condition and Results | |||||||

| of Operations | 12 | |||||||

| 7A. | Quantitative and Qualitative Disclosures about Market Risk | 19 | ||||||

| 8. | Financial Statements and Supplementary Data | 21 | ||||||

| 9. | Changes in and Disagreements with Accountants on Accounting and Financial | |||||||

| Disclosure | n/a | |||||||

PART III | ||||||||

| 10. | Directors and Executive Officers of the Registrant | 47 | ||||||

| 11. | Executive Compensation | 48 | ||||||

| 12. | Security Ownership of Certain Beneficial Owners and Management | 50 | ||||||

| 13. | Certain Relationships and Related Transactions | 51 | ||||||

PART IV | ||||||||

| 14. | Exhibits, Financial Statement Schedules, and Reports on Form 8-K | 52 | ||||||

| Signatures | 54 | |||||||

1

Table of Contents

PART I

Item 1. Business.

General

MSX International, Inc. (“MSXI”), headquartered in Auburn Hills, Michigan, combines innovative people, standardized processes and today’s technologies to deliver collaborative enterprise services on a global basis. We are a single source provider of these services at our facilities, at our customers’ facilities, and through web-based and other commerce networks. With both scalable and customized solutions, our people offer broad-based knowledge and experience that adds value to various phases in the life cycle of our customers’ products and services. We currently employ more than 10,000 professional staff at over 100 operating locations in 26 countries.

Since our formation, we have pursued both internal development and complementary acquisitions that have expanded our geographic and customer reach, increased our technical service capabilities and leveraged our corporate services. More recently, we have worked to refine and package our many capabilities and resources into fewer, more scalable service offerings. We have increased our market penetration of existing customers and the global automotive market, while expanding further into non-automotive markets. A strategic imperative is to expand our customer base beyond the automotive industry to demonstrate the universal applicability and economic value of our business services while continuing to grow our automotive business. Over the last three years we have increased our sales to non-automotive customers from 11.3% of net sales in fiscal 1999 to 24.1% in fiscal 2001.

Collaborative Service Offerings

We provide a broad range of collaborative enterprise services to our customers and group our offerings under three types of services: collaborative engineering management, human capital management, and other collaborative services. The following table sets forth, for the three fiscal years ended December 30, 2001, a summary of our net sales by type of service.

| Fiscal Year Ended | |||||||||||||

| January 2, | December 31, | December 30, | |||||||||||

| 2000 | 2000 | 2001 | |||||||||||

| (in thousands) | |||||||||||||

| Collaborative Engineering Management | $ | 279,028 | $ | 298,206 | $ | 270,424 | |||||||

| Human Capital Management Services | 322,342 | 469,773 | 401,212 | ||||||||||

| Other Collaborative Services | 158,472 | 267,244 | 257,621 | ||||||||||

| Total net sales | $ | 759,842 | $ | 1,035,223 | $ | 929,257 | |||||||

By leveraging competencies from each of our services, we believe we are positioned to compete in large and growing areas of the global economy. Our scalable solutions and customized offerings are adapted to customer needs that have emerged in recent years due to the convergence of digital communication technologies and business process improvement initiatives. Our net sales are based principally on fees charged for resources provided to support development, manufacturing and distribution of customer products and services. Our customers increasingly rely on outside vendors with combined intellectual capital and service delivery resources to provide them with these essential services, allowing them to improve operating efficiency by focusing on core competencies.

Our domestic and foreign markets are highly competitive. In some cases, our global competitors include a number of other well-established vendors, as well as customers with their own internal capabilities. Although a number of companies of varying size compete with us, no single competitor is substantially in competition with respect to all of our services. The following is a summary of our offerings through each of our collaborative services.

2

Table of Contents

Collaborative Engineering Management

We provide a complete range of engineering and design services to transportation related industries. Our solutions, which can be delivered at any or substantially all points of the product development cycle, include:

| • | Total product solutions— total engineering solutions spanning from product viability and concept development to validation, product launch, and performance measurement for continuous improvement | ||

| • | Custom engineering solutions— designed to meet any combination of specific customer engineering needs during the product development cycle | ||

| • | Single point solutions— services designed to meet specific needs of customers by delivering “turn-key” solutions to fit into each customer’s unique design processes |

Our services include computer-aided design, analysis and engineering, product and manufacturing engineering, assembly tooling, program management, engineering training through MSX International University and specialty vehicle support for the marketing programs of original equipment manufacturers (“OEMs”) and for non-automotive vehicle applications. Our capabilities are also enhanced by our human capital management services that support our engineering resource needs as well as the temporary/permanent staffing needs of our customers. As of January 2002, about $167 million of our collaborative engineering sales are either “booked” or recurring based on long-term relationships, compared to approximately $239 million in January 2001. The decrease reflects a decline in automotive design work due to the current economic environment.

Competition among engineering services vendors is based on the types of individual and bundled services offered and by the location of customers. The basis of competition includes the size of competing firms, global capability, relevant experience, prior relationships with customers and price. In the United States, we compete with Modern Engineering (a subsidiary of CDI), Rapid Design Services, Inc., Roush Industries, Inc., and Defiance, among others. European competition includes Bertrandt, Rücker, IVM, RLE, Magna-Steyr, Stola, Pininfarina, Italdesign, Engineering & Design AG and Hawtal Whiting, a subsidiary of Wagon plc.

Human Capital Management Services

We provide a broad range of services to help maximize the effectiveness, flow and utilization of human capital, particularly in technology-oriented environments. Through this practice we provide custom staffing solutions, including:

| • | Contingent staffing & direct placement— traditional temporary and/or permanent staffing solutions for information technology, engineering or other professional staff needs. Our staffing capabilities include design and production engineers, computer operators, database specialists, network administrators and specialists, PC support staff, software engineers, systems analysts and administrators, and technical support specialists | ||

| • | Retained search services— direct recruitment of middle and senior management talent on a “retained” basis | ||

| • | Vendor management services/master service provider— management of the entire contract staffing procurement and deployment process on a regional, national or global basis | ||

| • | Specialized training— training programs and virtual training courseware |

We currently provide these services to a wide variety of industries for both short and long-term assignments with international delivery, recruiting and training capability. We are a worldwide leader in automotive technical staffing, providing engineers, designers and technicians on a contract basis to support our customers’ product development efforts. We supply outsourced professional services based on our ability to identify, match and provide high quality personnel on an efficient basis and at a competitive price. We manage and compete with many companies in the technical staffing industry, which is highly competitive, fragmented, and historically has had limited barriers to entry. We use a variety of resources and techniques to support our recruiting capability, including support of a proprietary web-enabled recruiting system, licenses with web exchanges, internal training through MSX International University, international sourcing, and competitive benchmarking of compensation and benefits. Our competitors in human capital management services include Adecco International, CDI, Keane, kforce, TechAid, Manpower, Kelly Services Technical, Olsten, Randstad (in Europe only), Volt, and numerous regional information technology staffing firms. Other indirect competitors include Monster.com (a subsidiary of TMP Worldwide) and other internet-based staffing resources.

3

Table of Contents

Other Collaborative Services

We provide a broad range of technology-based business services to help support the objectives of our customers. Our service offerings include:

| • | Quality Relationship Management —We believe our quality relationship management programs give our customers a competitive edge by providing the actionable product, market and customer information they need to improve product quality, reduce costs and improve customer loyalty and satisfaction. Examples of our services include: | ||

| • | Warranty support programs — Management & operation of parts return centers, warranty process improvement consulting, claims assessment and analysis, and contract administration of extended warranty programs | ||

| • | Product quality improvement programs — Supplier quality assurance, technical call centers, and quality training and consulting programs | ||

| • | Retail support programs — Process improvement consulting, customer satisfaction program management, and training programs | ||

| • | Supply Chain Management —Through supply chain management, we work with our customers to streamline their procurement process, reduce procurement systems costs, and reduce fixed costs in the process. We do this by providing personnel with the required expertise, access and recommended process improvements to apply technology solutions as required to yield the desired results. In addition to internally developed technology, we have formed strategic partnerships with companies such as Commerce One and IBM to support our ability to deliver technology responsively while minimizing cost to the customer. Our services include the following: | ||

| • | Outsourced purchasing services — management of the procurement process from initial requisition to supplier payment | ||

| • | eProcurement services | ||

| • | Contract manufacturing — supply chain management services that provide full product life cycle support, from concept/design to shipment of product | ||

| • | Supply chain management consulting to meet specific customer needs | ||

| • | Custom Communication Services —Offers a full spectrum of solutions to provide our customers with a competitive advantage in facilitating communications through creating, maintaining and delivering information. Our services include the following: | ||

| • | Technical and consumer publishing — assists our customers in reducing cost and cycle time by facilitating the reuse and repurposing of content in technical writing, translation, print and distribution | ||

| • | Integrated marketing support and research services — supports the development and implementation of personalized marketing programs including copy and design, translation, printing and distribution | ||

| • | Integrated document management — assists our customers in facilitating the internal development and distribution of knowledge across their organizations. Our services include document imaging and on-site document centers |

There is a high degree of competition among suppliers of the outsourced business services we provide. In many cases, our principal competition is the customer’s in-house operations. For certain of our services there are numerous outside competitors, many of whom presently have greater name recognition and resources than we do. For quality relationship management and supply chain management services we compete with other global service companies such as EDS, IBM, ICG Commerce and other consulting firms in addition to certain companys’ in-house operations. In the custom communications area we compete with companies such as Valley Forge/SPX, Bowne, Xerox, Budco and Lason.

4

Table of Contents

Significant Customers and Supply Relationships

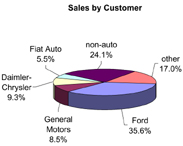

| We currently have sales to more than 1,000 customers. These include the major United States and European automotive OEMs and automotive suppliers. Ford, Fiat, S.p.A. (“Fiat”), DaimlerChrysler AG (“DaimlerChrysler”), and General Motors Corporation (“General Motors”), including their automotive subsidiaries, together accounted for 58.9%, of our net sales for the fiscal year ended December 30, 2001. |  |

A substantial portion of our sales to selected large customers were made pursuant to multi-year supply agreements and purchase orders with open terms. Although dependent on actual market demand, such agreements permit a degree of forward revenue visibility. They also allow us to expand existing customer relationships by providing cross-selling opportunities for our other collaborative enterprise services.

A significant portion of our $322.2 million in sales to Ford during 2001 were made pursuant to the Ford Master Vendor Agreement and the Ford Master Supply Agreement, which were entered into for five-year terms when we acquired Geometric Results, Inc. in August 1997. To date, we have generally met or exceeded the standards of performance and competitiveness as required by these agreements. Both Ford and MSXI have verbally agreed to extend the term of the Ford Master Vendor Agreement. The extension includes provisions to expand our services to additional Ford subsidiaries not covered by the original agreement. Ford and MSXI have also agreed to maintain an advisory board comprised of executives from both companies to monitor and enhance the on-going relationship between the companies.

A significant portion of our $82.0 million in sales to Fiat during 2001 were made pursuant to purchase orders with Fiat’s principal manufacturing companies, which were modified when we acquired Satiz S.r.l. in December 1999. These agreements were extended to five-year terms and include exclusivity provisions for selected services which are subject to agreed quality benchmarking procedures. Beginning January 1, 2001, the services are subject to annual price reductions based on the volume of sales. Contractual price reductions during 2001 as a result of this agreement did not have a significant impact on our business.

Sales to Johnson Controls, Inc. (“JCI”), a “top ten” customer, were made pursuant to a supply agreement that was executed when we acquired MegaTech Engineering, Inc. in December 1998. The five-year agreement designates MSXI as JCI’s exclusive supplier on a worldwide basis for specified engineering and design services. The agreement includes specific growth objectives, price benchmarking, an agreement to negotiate in 2003 to extend the agreement for an additional five years, and an advisory board of executives from both MSXI and JCI to support the relationship.

We believe we have developed strong relationships with our customers and have a reputation for quality, reliability and service that has been recognized through Ford’s Q1 and DaimlerChrysler’s Pentastar awards, among others. In addition, most of our operations are certified to the ISO 9001 or 9002 international quality standards, which requires a determination by an independent assessor that the operation is in compliance with a documented quality management system.

Except as noted above, no material portion of our business is dependent upon any one customer or is subject to contractual renegotiation of prices. In general, equipment and technologies required to support our service offerings are obtainable from various sources in the quantities desired.

5

Table of Contents

Global Capabilities

| Our international presence is an important competitive advantage in winning and retaining new business and meeting the global sourcing, quality and engineering requirements of many of our customers. We are currently providing services in 26 countries. We believe we are the only company currently providing such a broad range of services to the automotive industry on a worldwide basis. Foreign operations are subject to political, monetary, economic and other risks associated with international businesses. Additional information about market risks is included under Item 7A of this report. For the fiscal year ended December 30, 2001, 35% of our net sales were generated outside of the United States. Our global capabilities have continued to grow and strengthen our product offerings as a result of acquisitions completed in recent years. |  |

Our UK engineering and human capital management capabilities grew in 1998 through the acquisition of Gold Arrow Contract Services, Ltd. (“Gold Arrow”), an information technology and technical staffing company headquartered in Basildon, Essex, England. Future joint-engineering projects utilizing the combined resources of Cadform-MSX Engineering Gmbh are expected to strengthen our positioning with German automotive manufacturers and their suppliers. We further expanded our presence in Europe during 1999 through the acquisition of 75% of the outstanding common stock of Satiz S.r.l., effective December 31, 1999, and the acquisition of QR Quandoccorre S.r.l. and Quandoccorre Interinale S.p.A., effective January 3, 2000. The acquisition of Satiz is complementary to several of our service offerings and gives us a platform for custom communication services in Europe. The acquisition of the Quandoccorre companies provides us with a basis to expand our human capital management services in Italy. The acquisition of Australian-based Radial Pacific Pty. Ltd. in December 2000 enhanced our capabilities in Australia and strengthened our ability to support collaborative engineering opportunities across multiple time zones.

Additional financial information concerning our geographical coverage is set forth in Note 14 to our consolidated financial statements included under Item 8 of this report.

Organizational Development

We made several key appointments to our executive team in recent years, including the appointment of Thomas Stallkamp as Vice Chairman and Chief Executive Officer. Other recent changes were undertaken to align our management structure with our collaborative enterprise service offerings. The changes include the creation of a centralized sales organization and product development champions to support the rollout of our services to new vertical markets. The objective of these recent management changes is to enhance our responsiveness to key customers and to further commercialize our service offerings, especially to support the growth of our non-automotive customer base. Additional information on our executive officers appears in Item 10 of this report.

The following table sets forth certain recent information regarding our employees by region:

| Region | Number of Employees | ||||

| North America | 6,643 | ||||

| Italy | 1,405 | ||||

| United Kingdom | 869 | ||||

| Germany | 566 | ||||

| Rest of Europe | 363 | ||||

| Other | 296 | ||||

| Total | 10,142 | ||||

A small portion of our employees in the United States are members of unions. We believe our current relations with our employees and their unions are good.

6

Table of Contents

We depend upon our ability to attract, retain and develop personnel, particularly technical personnel, who possess the skills and experience necessary to meet the needs of our customers. Competition for individuals with proven technical or professional skills is intense. We compete with other staffing companies, as well as customers and other employers for qualified personnel.

We are committed to improving the professional development of our employees. In April 2000, we combined and expanded several existing training resources to launch MSX International University. This is a global learning resource that focuses on providing market-driven education to support both our internal needs and our customers’ strategic and operational training needs. The university uses web-based administration and embraces all forms of technologies and learning delivery methods. It delivers courses through two schools: the School of Technology and the School of Business and Leadership Education. It has also formed alliances with academic institutions in the United States, the United Kingdom and Germany which allow employees to pursue Bachelor of Science and Master of Science degrees in engineering and other technical disciplines.

Formation and Growth through Acquisitions and Corporate Development

MSXI is a holding company owned by Citicorp affiliates and certain members of management. MSXI was incorporated and owned by Citicorp Venture Capital, Ltd., MascoTech, Inc. (“MascoTech”), and management under the laws of Delaware in late 1996 to pursue growth opportunities in technology-driven collaborative enterprise services. On November 28, 2000, MascoTech sold its equity interest in MSXI to a subsidiary of Citicorp. On the same date Citicorp Venture Capital, Ltd. sold its equity interest in MSXI to the same subsidiary.

On January 3, 1997, we acquired (the “TSG Acquisition”) selected assets and operations of the former engineering and technical business service units of MascoTech Automotive Systems Group, Inc. (“MASG”) and MascoTech. Through the consummation of the TSG Acquisition, we also acquired the net assets of APX International, which previously had been acquired by MASG as of November 6, 1996.

Since our formation, corporate investments have complemented our internal growth. Specifically, we have completed numerous strategic acquisitions, made several strategic investments and participated as a minority investor in the formation of a minority-certified venture. These transactions have expanded our geographic coverage, our service offerings, and our reach to customers outside the automotive industry. As we pursue additional strategic acquisitions, alliances and other corporate development activities, we intend to continue to rationalize our cost structure through the elimination of redundant back office activities, operating facilities, management and administrative offices.

7

Table of Contents

Businesses acquired since January of 1997 include the following:

| NAME | MONTH ACQUIRED | SERVICES | GEOGRAPHIC COVERAGE | MARKETS | ||||

| Geometric Results Incorporated | August 1997 | Human capital management and other collaborative services | North America and Europe | Automotive | ||||

| Gold Arrow Contract Services, Ltd. | August 1998 | Information technology and technical staffing | United Kingdom, Northern Europe | Automotive, financial services and other commercial markets | ||||

| Lexstra International, Inc. | October 1998 | Information technology staffing | Mid-Atlantic Region | Financial services and other commercial markets | ||||

| Lexus Temporaries, Inc. | October 1998 | Network support staffing | Mid-Atlantic Region | Telecommunications | ||||

| Pilot Computer Services, Inc. | December 1998 | Information technology staffing | California | Government, health care and other commercial markets | ||||

| MegaTech Engineering, Inc. | December 1998 | Technical staffing and product development services | Michigan | Automotive original equipment manufacturers and suppliers | ||||

| Rice Cohen International, Inc. | April 1999 | Permanent staff placement | Mid-Atlantic Region | Selected services markets | ||||

| Management Resources International, Inc. | June 1999 | Training services and courseware in quality systems | Midwest | Quality systems | ||||

| Chelsea Computer Consultants, Inc. | September 1999 | Information technology staffing | Mid-Atlantic Region | Financial services, telecommunications and manufacturing | ||||

| Satiz S.r.l | December 1999 | Commercial and technical publishing | Italy, Other Europe, Brazil | Automotive and original equipment manufacturers and suppliers | ||||

| Quandoccorre Interinale S.p.A. and QR Quandoccorre S.r.l | January 2000 | Staffing and consulting services | Italy | Automotive and non-automotive manufacturing and other industries | ||||

| Intranational Computer Consultants, Inc. | February 2000 | Information technology consulting services | California | Financial services and non-automotive manufacturing Financial services, | ||||

| Programming Management & Systems, Inc. | February 2000 | Information technology consulting services | Missouri | telecommunications and non-automotive manufacturing | ||||

| CMS Management Services | February 2000 | Information technology, accounting and technical staffing | Midwest Region | Services and non-automotive manufacturing | ||||

| Ascend | February 2000 | Information technology staffing and permanent placement | Midwest Region | Financial and other services markets | ||||

| Radial Pacific Pty Ltd. | December 2000 | Engineering and design services | Australia | Automotive, aerospace and component manufacturers |

In addition to the above, during 1999 we acquired a 49% interest in CADFORM-MSX Engineering GmbH (formerly Cadform Engineering GmbH). Cadform is based in Homberg (Ohm), Germany and provides design and tooling services to the automotive industry. See “Recent Developments” included under Item 7 of this report for additional information on Cadform and other investments subsequent to 2001. In October 2000, we invested in a certified minority provider of human capital management services to a large automotive supplier. We provide technology solutions, sub-contract labor and selected administrative support services to this company. In November 2000, we entered into a technical cooperation agreement with Prototipo Holding B.V. Prototipo has operations in Europe and Brazil and provides testing, prototyping, styling and other development services for transportation and industrial manufacturing customers, including automotive, truck, and tire manufacturers. In support of the relationship, we completed a modest minority investment in Prototipo.

In March 2001, we acquired a minority interest in MTE Groups L.L.C. MTE is a minority supplier of tooling, design, and prototype services, primarily to the automotive industry. The investment was completed to strengthen our ability to support the tooling and prototype needs of mutual customers. In September 2001, we completed a small investment in itiliti, Inc., which provides a web-enabled solution that complements our human capital management practice.

For additional information on acquisitions, including pro forma financial results, see Note 3 to our consolidated financial statements included under Item 8 of this report.

8

Table of Contents

Seasonality of our Business

Our quarterly operating results are affected primarily by the number of billing days in the period and the seasonality of our customers’ businesses. Demand for some of our services has historically been lower during the year-end holidays.

Environmental

Compliance with foreign, federal, state and local environmental protection laws and regulations is not expected to result in material capital expenditures or have a material adverse effect on our financial condition, results of operations, cash flows or competitive position.

Patents and Trademarks

We hold a number of United States and foreign patents, licenses, copyrights, tradenames and trademarks. Although we regard our intellectual property to be valuable, we do not believe that there is any reasonable likelihood of the loss of any rights that would have a material effect on our operating units, services or present business as a whole.

Item 2. Properties.

The following table sets forth the current number of facilities we operate by region. We believe that substantially all of our property and equipment is in good condition and that we have sufficient capacity to meet our current and projected operating needs. The number of facilities in any region is dictated by the local demographics and requirements to support our customers’ needs. Our facilities are utilized to provide all or any combination of our service offerings.

| Region | Number of Facilities | ||||

| North America | 45 | ||||

| Italy | 28 | ||||

| Germany | 11 | ||||

| United Kingdom | 8 | ||||

| Rest of Europe | 7 | ||||

| Other | 3 | ||||

| Total | 102 | ||||

All of our facilities are leased. We believe that the termination of any one lease would not have a material adverse affect on our business.

Item 3. Legal Proceedings.

We are involved in various proceedings incidental to the ordinary conduct of our business. We believe that none of these proceedings will have a material adverse effect on our financial condition, results of operations or cash flows.

Item 4. Submission of Matters to a Vote of Security Holders.

The following matters were ratified and approved by the consent of a majority of our stockholders in lieu of a stockholder meeting:

| • | Adoption of the Amended and Restated By-laws of MSXI, filed as Exhibit 3.2 to the Form 10-K | ||

| • | The re-election of the existing Board of Directors |

9

Table of Contents

PART II

Item 5. Market for Registrant’s Common Equity and Related Stockholder Matters.

MSXI is privately owned and there is no current public trading market for our equity securities. See “Item 12. Security Ownership of Certain Beneficial Owners and Management”. For further information related to ownership aspects of our common stock, see the discussion under “Amended and Restated Stockholders’ Agreement” contained under “Item 13. Certain Relationships and Related Transactions”.

During 1998 and 1999, we completed offers to exchange new senior subordinated notes that had been registered under the Securities Act of 1933 for similar notes that had not been registered. We may not declare or pay any dividends or other distributions with respect to any common stock or other class or series of stock ranking junior to our Series A Preferred Stock without first complying with restrictions specified in the Amended and Restated Stockholders’ Agreement. See Note 10 to our consolidated financial statements included under Item 8 of this report.

10

Table of Contents

Item 6. Selected Financial Data.

The selected historical consolidated financial data as of and for the five fiscal years ended December 30, 2001 have been derived from the audited historical financial statements of MSXI. The results of operations for the periods presented include the results of operations of acquired companies from the effective date of their acquisition. As a result, our financial performance for each fiscal year is not directly comparable without taking into account the impact of acquisitions. The selected financial and other data should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and notes thereto included elsewhere in this Form 10-K.

| Fiscal Year Ended | |||||||||||||||||||||

| December 28, | January 3, | January 2, | December 31, | December 30, | |||||||||||||||||

| 1997 | 1999 | 2000 | 2000 | 2001 | |||||||||||||||||

| (dollars in thousands) | |||||||||||||||||||||

| Statement of Operations Data: | |||||||||||||||||||||

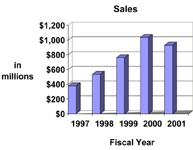

| Net sales | $ | 378,014 | $ | 533,942 | $ | 759,842 | $ | 1,035,223 | $ | 929,257 | |||||||||||

| Cost of sales | 327,487 | 449,914 | 653,274 | 889,286 | 812,221 | ||||||||||||||||

| Gross profit | 50,527 | 84,028 | 106,568 | 145,937 | 117,036 | ||||||||||||||||

| Selling, general and administrative expenses | 37,983 | 59,083 | 65,082 | 83,238 | 78,775 | ||||||||||||||||

| Amortization of goodwill and other intangibles | 892 | 1,690 | 3,156 | 5,583 | 6,222 | ||||||||||||||||

| Restructuring costs | 2,000 | — | — | — | — | ||||||||||||||||

| Operating income | 9,652 | 23,255 | 38,330 | 57,116 | 32,039 | ||||||||||||||||

| Interest expense, net | 12,400 | 17,416 | 21,141 | 30,119 | 27,881 | ||||||||||||||||

| Income (loss) before income taxes, minority interests and equity in net losses of affiliates | (2,748 | ) | 5,839 | 17,189 | 26,997 | 4,158 | |||||||||||||||

| Income tax provision | 225 | 3,068 | 6,995 | 11,340 | 1,712 | ||||||||||||||||

| Less minority interests and equity in net losses of affiliates, net of taxes | — | — | — | 766 | 1,943 | ||||||||||||||||

| Net income (loss) | $ | (2,973 | ) | $ | 2,771 | $ | 10,194 | $ | 14,891 | $ | 503 | ||||||||||

| Balance Sheet Data (at period end): | |||||||||||||||||||||

| Cash and cash equivalents | $ | 11,575 | $ | 4,248 | $ | 6,879 | $ | 4,686 | $ | 4,924 | |||||||||||

| Accounts receivable, net | 178,938 | 208,451 | 306,978 | 317,458 | 252,008 | ||||||||||||||||

| Total assets | 287,176 | 356,724 | 524,190 | 577,029 | 514,382 | ||||||||||||||||

| Total debt and capital lease obligations | 153,246 | 185,081 | 245,924 | 266,859 | 246,666 | ||||||||||||||||

| Redeemable Series A Preferred Stock | 36,000 | 36,000 | 36,000 | 36,000 | 36,000 | ||||||||||||||||

| Shareholders’ deficit | (26,364 | ) | (26,105 | ) | (20,579 | ) | (15,462 | ) | (15,487 | ) | |||||||||||

| Other Data: | |||||||||||||||||||||

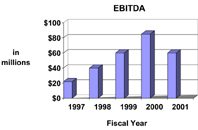

| EBITDA (A) | $ | 22,379 | $ | 40,152 | $ | 60,803 | $ | 85,293 | $ | 59,944 | |||||||||||

| Capital expenditures | 11,518 | 11,559 | 16,692 | 18,168 | 19,243 | ||||||||||||||||

| Depreciation and amortization | 9,859 | 14,109 | 17,535 | 23,587 | 24,426 | ||||||||||||||||

| Ratio of earnings to fixed charges (B) | — | 1.2x | 1.6x | 1.7x | 1.1x | ||||||||||||||||

| (A) | EBITDA represents income (loss) before income taxes, minority interests and equity in net losses of affiliates plus net interest expense, depreciation, amortization, and Michigan Single Business Tax and similar taxes. EBITDA is presented as additional information because management believes it to be a useful indicator of the company’s ability to meet debt service and capital expenditure requirements. It is not, however, intended as an alternative measure of operating results or cash flow from operations (as determined in accordance with generally accepted accounting principles). | |

| (B) | For purposes of computing the ratio of earnings to fixed charges, earnings represent net income (loss) before income taxes, minority interests, equity in net losses of affiliates, and fixed charges. Fixed charges consist of interest expense, the interest component of operating leases and amortization of deferred financing costs. For the fiscal year ended December 28, 1997, earnings were inadequate to cover fixed charges by approximately $2.7 million. |

|  |

11

Table of Contents

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

General

The following analysis of our results of operations and liquidity and capital resources should be read in conjunction with our consolidated financial statements and the related notes thereto included under Item 8 of this report. The results of operations for the fiscal years ended December 30, 2001, December 31, 2000 and January 2, 2000 include the results of operations of acquired companies from the effective date of their acquisition. As a result, our financial performance for each fiscal year is not directly comparable without taking into account the impact of acquisitions.

Significant Accounting Policies

Our significant accounting policies are more fully described in Note 1 to our consolidated financial statements. Certain accounting policies applied require management’s judgment in selecting the appropriate assumptions for calculating financial estimates. By their nature, these judgments are subject to a degree of uncertainty. Management judgments are based on historical experience, information from our customers, market and regional trends, and other information. Significant accounting policies include:

| • | Valuation of Goodwill and other intangibles— we evaluate the carrying value of goodwill when events or circumstances warrant such a review. An evaluation includes comparing anticipated undiscounted future cash flows from operating activities with the carrying amount of the excess of cost over net assets of companies acquired. While we believe that our estimates and assumptions in this area are valid, different assumptions could result in a different outcome. In addition, we will adopt Statement of Financial Accounting Standards No. 142 during the first quarter of 2002. We are still evaluating the impact this adoption will have on our results. However, given the current economic climate and market valuations of technology-based companies, adoption of SFAS 142 could result in a charge during the first quarter of 2002. | ||

| • | Deferred income taxes— at December 30, 2001, our consolidated balance sheet includes net deferred tax assets of $6.4 million. About $6.0 million of the net deferred tax asset is related to net operating losses of certain MSXI subsidiaries. Realization of the net deferred tax asset is dependent primarily on profitable operations within certain regions. Although realization cannot be assured, we believe that it is more likely than not that such benefits will be realized through the generation of future taxable income. In addition, we intend to utilize our tax planning strategies to help ensure realization of these assets. |

Results of Operations

Fiscal Year Ended December 31, 2000 Compared with the Fiscal Year Ended December 30, 2001

Net Sales.Consolidated net sales were $929.3 million during fiscal 2001 compared to $1,035.2 million during fiscal 2000, a decrease of $105.9 million, or 10.2%. Comparable fiscal 2001 sales continue to be negatively impacted by depressed foreign currency exchange rates in certain countries in which we operate. The net impact of year over year exchange rate changes was to reduce consolidated net sales by about $13.4 million for the fiscal 2001 year. Excluding the impact of foreign exchange rate changes, consolidated fiscal 2001 net sales decreased $92.5 million, or 8.9%, compared to 2000.

After adjusting for the impact of foreign exchange rates, the $92.5 million decrease in sales during fiscal 2001 is comprised of a $21.5 million decrease in sales of collaborative engineering services, a $66.1 million decrease in sales of human capital management services, and a $5.0 million decrease in sales of other collaborative services. The decrease in engineering sales reflects price reduction pressures and reduced volumes of engineering services in North America and Europe as our automotive customers have delayed their engineering programs due to current economic conditions. Sales of human capital management services decreased during fiscal 2001 due to reduced demand in North American markets for IT development, automotive engineering, and permanent placement services. Reductions in human capital management sales volumes, on a year to date basis, were partially offset by the impact of businesses acquired during the first quarter of fiscal 2000. Sales of our other collaborative services decreased as a result of lower volumes due to declines in our automotive business and the divestiture of a non-core business during fiscal 2000.

12

Table of Contents

Operating Profit.Our consolidated gross profit and operating income for the periods presented were:

| Fiscal Year Ended | |||||||||||||||||

| Change | |||||||||||||||||

| December 31, | December 30, | ||||||||||||||||

| 2000 | 2001 | $ | % | ||||||||||||||

| (dollars in thousands) | |||||||||||||||||

| Gross profit | $ | 145,937 | $ | 117,036 | $ | (28,901 | ) | (19.8 | %) | ||||||||

| % of net sales | 14.1 | % | 12.6 | % | n/a | n/a | |||||||||||

| Operating income | $ | 57,116 | $ | 32,039 | $ | (25,077 | ) | (43.9 | %) | ||||||||

| % of net sales | 5.5 | % | 3.4 | % | n/a | n/a | |||||||||||

Gross profit, as a percentage of sales, decreased to 12.6% during fiscal 2001 compared to 14.1% during fiscal 2000. The decrease in gross profit reflects the pricing pressures and unfavorable volumes in our engineering and human capital management operations, particularly in the second half of 2001, resulting in less favorable absorption of fixed and indirect operating costs. Overall, operating income decreased during 2001 due to reduced sales volumes, pricing pressures and costs incurred to position the company for growth and expansion into new vertical markets. The overall decline in our operating results is attributable to the general economic downturn, which has impacted demand for technical services in the automotive and telecommunications sectors.

We cannot predict with certainty when economic conditions will improve and have taken steps to reduce our cost structure commensurate with the current levels of business. As a result, we recorded about $1.3 million of one-time severance costs during the fourth quarter of 2001, which are included in selling, general and administrative expenses, and took other steps to reduce our cost structure. We expect to begin realizing annual benefits in excess of $25 million from our cost reduction efforts starting in the first quarter of fiscal 2002. In addition, we are also taking steps to further diversify our business to other markets and customers.

Selling, general and administrative expenses, as a percentage of net sales, were 8.5% during fiscal 2001 compared to 8.0% during fiscal 2000. The increase as a percentage of sales reflects the impact of lower volumes during fiscal 2001, particularly in the second half of the year. Overall, selling, general and administrative expenses decreased in comparison to 2000 reflecting reductions in incentive compensation totaling $7.7 million. After adjusting for reductions in incentive compensation, selling, general and administrative expenses increased on a year over year basis. The increase reflects one time severance costs, as discussed above, and costs incurred to develop our service offerings and sales efforts within our developing vertical markets.

Interest Expense.Interest expense decreased $2.2 million, from $30.1 million during fiscal 2000 to $27.9 million during fiscal 2001. Average daily borrowings outstanding increased slightly during fiscal 2001 in order to fund investments in businesses and product development. However, the impact of increased borrowings was more than offset by declines in the interest rates on our variable rate debt. Additional information on interest rate market risk is included under Item 7A of this report.

Net Income.Net income during fiscal 2001 was $0.5 million, compared to net income of $14.9 million in fiscal 2000. The decrease reflects lower operating earnings and increased equity losses during the year. Our effective income tax rate during fiscal 2001 was 41.1% versus 42.0% during fiscal 2000. The improvement resulted from certain legal reorganization changes that took effect in 2001 combined with a favorable mix of earnings compared to fiscal 2000. Minority interests and equity losses increased $1.2 million compared to fiscal 2000 primarily as a result of losses reported by our equity investees during 2001. Our equity investees are experiencing the same pricing pressures and volume reductions that are impacting our business.

13

Table of Contents

Fiscal Year Ended January 2, 2000 Compared with the Fiscal Year Ended December 31, 2000

Net Sales.Consolidated net sales increased $275.4 million, or 36.2%, from $759.8 million in fiscal 1999 to $1,035.2 million in fiscal 2000. The increase in consolidated net sales resulted from both internal growth from existing businesses and incremental sales from acquired businesses. The total increase in net sales is comprised of:

| Fiscal Year | |||||||||

| Ended | % | ||||||||

| Increase From | December 31, 2000 | Increase | |||||||

| (dollars in thousands) | |||||||||

| Internal growth | $ | 77,575 | 10.2 | % | |||||

| Acquired businesses | 197,806 | 26.0 | % | ||||||

| Total | $ | 275,381 | 36.2 | % | |||||

All of our service lines continued to grow sales volume from existing businesses while generating incremental sales from businesses acquired during 1999 and 2000. Overall, sales generated by existing businesses during fiscal 2000 were negatively impacted by the softening of foreign currency exchange rates in many of the countries in which we operate. The net impact of foreign currency exchange rate fluctuations during fiscal 2000 was to reduce net sales by about $16.3 million, or 2.1%, compared to 1999. Before the impact of foreign exchange rate fluctuations, net sales from existing businesses increased about 12.3% during fiscal 2000 compared to 1999.

Sales of our collaborative engineering services during fiscal 2000 increased $26.6 million, or 9.5%, before the impact of acquisitions and foreign exchange rate changes, compared to fiscal 1999. The improvement primarily reflects increased demand for design and engineering services in North America. Sales of our human capital management services during fiscal 2000 increased $56.2 million, or 17.4%, before the impact of acquisitions and foreign exchange rate changes, compared to the fiscal 1999. The internal growth reflects improved IT staffing volumes with non-automotive customers and increased automotive engineering services, primarily in North America. Sales of our other collaborative services during fiscal 2000 improved $11.1 million, or 7.0%, before the impact of acquisitions and foreign exchange rate changes, compared to fiscal 1999.

Operating Profit.Our consolidated gross profit and operating income for the fiscal years presented were:

| Fiscal Year Ended | Increase | ||||||||||||||||

| January 2, | December 31, | ||||||||||||||||

| 2000 | 2000 | $ | % | ||||||||||||||

| (dollars in thousands) | |||||||||||||||||

| Gross profit | $ | 106,568 | $ | 145,937 | $ | 39,369 | 36.9 | % | |||||||||

| % of net sales | 14.0 | % | 14.1 | % | n/a | n/a | |||||||||||

| Operating income | $ | 38,330 | $ | 57,116 | $ | 18,786 | 49.0 | % | |||||||||

| % of net sales | 5.0 | % | 5.5 | % | n/a | n/a | |||||||||||

Overall, operating income increased during fiscal 2000 due to the improved performance of our existing businesses and the incremental impact of businesses acquired during 1999 and 2000. Operating income generated by existing businesses during 2000 increased $8.8 million, or 23.0%, compared to 1999. Declines in foreign currency exchange rates during fiscal 2000 caused a net reduction in operating income of about $0.5 million compared to fiscal 1999. Gross profit increased $39.4 million, or 36.9%, compared to 1999. Gross profit, as a percentage of sales, improved slightly from 14.0% in fiscal 1999 to 14.1% in fiscal 2000. The improvement in gross profit reflects increased sales volumes by existing businesses in North America and the impact of cost reduction efforts in our European operations. Selling, general and administrative expenses, as a percentage of net sales, were 8.0% during fiscal 2000, compared to 8.6% during fiscal 1999. The improvement reflects the continued consolidation of administrative services resulting from the successful integration of acquired companies.

Interest Expense.Interest expense increased 42.5%, from $21.1 million during fiscal 1999 to $30.1 million during fiscal 2000. The increase reflects the impact of incremental borrowings outstanding during fiscal 2000 to fund acquisitions and increases in the floating rates of interest on borrowings under our credit facility.

14

Table of Contents

Net Income.Net income increased $4.7 million, or 46.1%, from $10.2 million in fiscal 1999 to $14.9 million in fiscal 2000. The increase in net income reflects improved earnings from operations partially offset by an increase in our effective tax rate and increased interest expense. Our effective tax rate was 42.0% during fiscal 2000 compared to 40.7% during fiscal 1999, reflecting changes in the mix of our earnings between tax jurisdictions and an increase in the ratio of non-deductible expenses to pretax income primarily related to acquisition activity. Minority interests and equity in net losses of affiliates primarily represents the portion of Satiz S.r.l. earnings, which was acquired on December 31, 1999, attributable to the minority owner and equity in the net losses of CADFORM-MSX Engineering GmbH.

Liquidity and Capital Resources

Cash Flows

General.Our principal capital requirements are for the acquisition of businesses, capital expenditures and working capital to support internal growth and development of new vertical markets. These requirements have been met through a combination of bank debt, the issuance of senior subordinated notes and cash generated from operations. We typically pay our employees on a weekly basis and receive payment from our customers within invoicing terms, which is generally a 60-day period after the invoice date. However, in connection with certain of our master vendor and supply chain management programs, we collect related receivables at approximately the same time we make payment to suppliers.

| Operating Activities.Net cash provided by operating activities during fiscal 2001 decreased $0.7 million from $59.1 million in fiscal 2000 to $58.4 million in fiscal 2001. Cash from operations during fiscal 2000 includes significant improvements in accounts receivable collections resulting from the transition of Satiz S.r.l. into our cash management system. The reduction in Satiz accounts receivable resulted in a one-time improvement in cash from operations of about $12 million during fiscal 2000. Excluding the one-time improvements during fiscal 2000, cash provided by operations increased about $11 million during fiscal 2001 despite reduced profits during the year. The improvement resulted from our efforts to maximize working capital through accounts receivable collections and management of vendor payments. |  |

Net cash provided by operating activities for fiscal 2000 increased $28.9 million compared to fiscal 1999, including the one-time improvements in Satiz’s accounts receivable collections. Improvements in accounts receivable balances were offset by an increase in the volume of pass-through billings for our master vendor and supply chain management services. Excluding the one-time improvement in Satiz accounts receivable, cash provided by operations was about $47.1 million, which represents a 56.0% increase over fiscal 1999. The increase in cash from operations reflects increased earnings before depreciation and amortization along with further improvements in our managed working capital.

| Investing Activities. Net cash used for investing activities decreased $40.3 million, from $75.4 million during fiscal 2000 to $35.1 million during fiscal 2001. The decrease includes a reduction in funds used to acquire businesses of $43.6 million. Cash used to acquire businesses during fiscal 2001 included investments in MTE Groups L.L.C. and itiliti, Inc. totaling about $6.6 million as well as the payment of contingent consideration related to certain prior acquisitions. For additional information on acquisitions/investments during fiscal 2001, see “Corporate Development” below. The increase of $1.1 million in capital expenditures during fiscal 2001 reflects an increase in capital invested for future programs and services while capital required to maintain current programs declined year over year. Proceeds from the sale/disposal of property and equipment during fiscal 2000 include proceeds from the sale of certain non-core assets, primarily real estate and equipment, associated with our offset printing business. |  |

Net cash used for investing activities for fiscal 2000 increased $17.5 million from $57.9 million to $75.4 million, as compared to fiscal 1999. This included an increase in cash used for business acquisitions of $5.4 million. Cash used to acquire businesses includes funding of acquisitions closed during fiscal 2000 and the payment of contingent consideration related to certain prior year acquisitions. For additional information on acquisitions during fiscal 2000, see “Corporate

15

Table of Contents

Development” below. Proceeds from the sale/disposal of property and equipment include a sale-leaseback transaction during fiscal 1999 and the sale of certain non-core business assets during fiscal 2000, as discussed above. During fiscal 1999, we entered into a sale-leaseback transaction related to certain property and facilities acquired as part of the MegaTech Engineering, Inc. acquisition in December 1998. The sale proceeds of $15 million were used to settle a contractual acquisition obligation related to the acquisition of MegaTech.

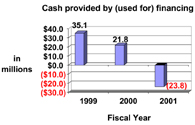

| Financing Activities.Net cash used for financing activities was $23.8 million during fiscal 2001 compared to net cash provided by financing activities of $21.8 million in 2000, a decrease of $45.6 million. Financing requirements decreased consistent with the reduction in funds required to acquire companies. Therefore, cash generated from operations in excess of investing requirements were utilized to reduce revolving debt and make scheduled term loan repayments. During the first quarter of fiscal 2001, a subsidiary of MSX International, Inc. completed a sale of unregistered securities to certain directors and members of management. The securities were sold in units with each unit comprised of MSX International Inc.’s Series A Preferred Stock, par value $0.01 per share, and Class A Common Stock, par value $0.01 per share. In total, 9,936 shares of Series A Preferred Stock and 482,400 shares of Class A Common Stock were sold. The shares of Series A Preferred Stock and Class A Common Stock, which comprised the units sold, were acquired from Citicorp, our majority stockholder, at a price equal to the price at which the units were sold to management. The entire proceeds of $3.6 million were used to pay the purchase price of the shares acquired from Citicorp. |  |

Net cash provided by financing activities for fiscal 2000 decreased $13.3 million from fiscal 1999. Our increased investing requirements during fiscal 2000 were primarily met with strong operating cash flow. Additional borrowings were used to support the acquisition of businesses and included the issuance of an additional $25 million in term notes as discussed below.

Debt Arrangements and Available Financing

Our total indebtedness consists of our senior subordinated notes, borrowings under our credit facilities and borrowings under various short-term arrangements. Additional information regarding these obligations is set forth in Note 7 and Note 14 to our consolidated financial statements included under Item 8 of this report.

Senior Subordinated Notes.On January 22, 1998, we issued, in a private placement, $100 million aggregate principal amount of 11-3/8% unsecured senior subordinated notes maturing January 15, 2008 (the “Series A Notes”). The net proceeds of $93.2 million were used to retire bridge loans to Citicorp and MascoTech, retire senior subordinated notes payable to MascoTech and repay a portion of the amounts outstanding under our credit facility. On August 20, 1998, we completed an offer to exchange 11-3/8% unsecured senior subordinated notes, registered under the Securities Act of 1933, for any and all outstanding Series A notes.

On May 18, 1999, we issued, in a private placement, an additional $30 million aggregate principal amount of 11-3/8% unsecured senior subordinated notes maturing January 15, 2008 (the “Series B Notes”). The net proceeds of $27.6 million were used to repay amounts previously outstanding under our credit facility. On September 10, 1999, we completed an offer to exchange 11-3/8% unsecured senior subordinated notes, registered under the Securities Act of 1933, for any and all outstanding Series B Notes.

Credit Facility.In December 1999, we completed an amended and restated credit facility with commercial banks and institutional lenders led by Bank One N.A. The amended and restated credit facility replaced our existing credit facility. The revolving credit portion of the amended and restated agreement expires December 7, 2004. The credit facility, as amended and restated, provides for revolving credit up to $100 million and five and seven year term loans up to $105 million under terms specified in the agreement. At closing, we borrowed $80 million under the term loan portion of the credit facility and additional amounts under the revolver. We increased the term loan syndication to $105 million, under the terms of the agreement, in early 2000. Available borrowings under the revolving credit portion of the credit facility are subject to adequate accounts receivable balance requirements. As of December 30, 2001, $87.9 million was available for future borrowing while $43.1 million was available for immediate borrowing based on our current level of accounts receivable. Under the terms of the agreement, we are also subject to mandatory partial prepayments of the term loans if we generate excess cash flows, as defined, on an annual basis, or other defined cash proceeds. If required, such prepayments may reduce our long term availability under the credit facility.

16

Table of Contents

Effective September 30, 2001, we completed the first amendment to the amended and restated credit facility. The result of the amendment was to relax certain financial covenants through the end of fiscal 2002 in response to recent economic events, and to clarify certain definitions and calculations included in the credit facility. Beginning in the first quarter of fiscal 2003, the financial covenant requirements will return to their original levels. Based upon our current operating performance, we would not comply with the covenant requirements that are effective in 2003. No changes were made to the length of the agreement, available borrowings, or terms for repayment. As part of the amendment, the applicable spread over benchmark interest rates, applicable when the ratio of debt to EBITDA is above specified levels, was increased.

Satiz Facility. Satiz S.r.l., which was acquired effective December 31, 1999, maintains a financing arrangement that provides for lines of credit up to 100% of its eligible accounts receivable, as defined in the agreement. As of December 30, 2001, about $13 million was available for borrowing under this arrangement. The original term of the agreement expired on December 12, 2001 and was renewed for an additional 12-month period. The agreement will automatically be renewed for additional 12-month periods unless terminated by either party.

Fluctuations in our operating cash flows are impacted by our ability to collect receivables from our customers within reasonable and customary terms and manage related payments to vendors. We rely on our credit facilities to provide sufficient flexibility to fund fluctuations in our operating cash requirements, fund required capital to grow the business, and to fund investment opportunities. Availability under our credit facilities is subject to meeting our debt service obligations and financial covenant requirements and is dependent upon the future performance of MSXI. Our future performance will be impacted by general economic conditions and other factors, which may be outside of our control. We believe that our current financing arrangements provide us with sufficient financial flexibility to fund these requirements during the next 12 — 24 months, although there can be no assurance that will be the case. Our term loans require scheduled quarterly payments of principle over the next 4 years with the balance of $70.7 million payable in 2006. Financing requirements over the longer term may require additional access to capital markets. Our ability to access additional capital in the long term may be adversely affected by pricing and availability of capital markets as well as our credit profile at the time we are seeking funds.

Corporate Development

Acquisitions

We have significantly expanded our business through acquisitions while continuing to grow our existing service lines. Our acquisitions have expanded our geographic coverage, increased our service offerings to existing customers and increased our reach to customers outside of the automotive industry. These acquisitions along with our existing businesses provide us with a solid platform to grow our business globally and into a variety of industries in the future. Acquisitions during the last three fiscal years include:

| • | During 1999 we acquired Rice Cohen International, Inc., a permanent placement staffing company based in Yardley, Pennsylvania with historical annual sales of about $5.0 million and Management Resources International, Inc., a provider of training services and courseware in quality systems based in Ann Arbor, Michigan with historical annual sales of about $3.5 million. | ||

| • | Effective September 17, 1999, we acquired 100% of the outstanding common stock of Chelsea Computer Consultants, Inc. Chelsea is a provider of information technology professionals in the areas of application development, networking, database design, enterprise and data modeling and hardware engineering with historical annual sales in excess of $30 million. Chelsea is headquartered in New York, New York and provides consulting and technical staff augmentation services to customers in the financial services, communications and manufacturing industries throughout North America. The purchase price was about $19.9 million at closing and was funded with borrowings under our credit facility. | ||

| • | Effective December 31, 1999, we acquired 75% of the outstanding common stock of Satiz S.r.l., a subsidiary of Fiat, S.p.A. Satiz is headquartered in Turin, Italy and specializes in commercial and technical publishing including translation services, graphics, document systems, warehouse and distribution services, and events. Satiz employs over 500 people and has historical annual sales in excess of $120 million. The purchase price, upon settlement of certain contractual matters, of about $10.0 million was funded with borrowings under our credit facility. Satiz had about $8.9 million of debt outstanding at closing. The remaining 25% of the outstanding common stock of Satiz was retained by Fiat. |

17

Table of Contents

| • | In May 1999, we purchased a 30% interest in QR Quandoccorre S.r.l. and Quandoccorre Interinale S.p.A., two affiliated Italian companies with combined historical annual sales of about $18 million. QR Quandoccorre S.r.l. provides consulting services on a project basis and Quandoccorre Interinale S.p.A. provides staffing services to various industries. Effective January 3, 2000, we acquired the remaining 70% of the outstanding common stock of both companies. The cumulative purchase price of about $11.4 million was funded with a combination of borrowings under our credit facility and borrowings under the Satiz credit facility. | ||

| • | On February 23, 2000, we acquired the professional staffing operations of Corporate Staffing Resources, Inc. of South Bend, Indiana. Specifically, we acquired 100% of the outstanding common stock of Intranational Computer Consultants, Inc. and Programming Management and Systems, Inc. and selected assets and liabilities of CMS Management Services and Ascend for a total purchase price of about $31.8 million at closing. The purchase price was funded with borrowings under our credit facility. These companies provide information technology and technical professional staffing throughout the United States with combined historical annual sales over $57 million. |

Investments

In addition to the above acquisitions, we have completed certain investment transactions to further strengthen our global position and service offerings. Such investments for each of the last three fiscal years include:

| • | Fiscal 1999 —On January 8, 1999, we acquired a 24.5% interest in CADFORM-MSX Engineering GmbH (formerly Cadform Engineering GmbH), a provider of product design and tooling services to the automotive industry. Based in Homberg (Ohm), Germany, Cadform specializes in automotive interior systems and cast aluminum products with historical annual sales of about $12 million. In November 1999 we acquired an additional 24.5% interest in Cadform by contributing selected assets of our German engineering operations. See “Recent Developments” for additional information on Cadform. | ||

| • | Fiscal 2000 —In November 2000, we completed a minority investment and entered into a technical cooperation agreement with Prototipo Holding B.V. Prototipo has operations in Europe and Brazil and provides testing, prototyping, styling and other development services for transportation and industrial manufacturing customers, including automotive, truck and tire manufacturers. | ||

| • | Fiscal 2001 —In March 2001, we acquired a minority interest in MTE Groups L.L.C. MTE is a certified minority supplier of tooling, design, and prototype services, among other services. The partnership provides expanded capabilities to support the tooling and prototype needs of mutual customers. A substantial portion of the purchase price is held in escrow and will be refunded if MTE does not meet certain operational results. As of December 30, 2001, the refundable amount is included in the cost of the investment. In September 2001, we completed a strategic investment in itiliti, Inc., in the form of a bridge loan convertible to preferred stock. itiliti provides a web-enabled human capital management solution in a hosted environment for customers and master service providers. |

Recent Developments

In January 2002, we exercised our option to acquire an additional 16% of the outstanding common stock of CADFORM-MSX Engineering GmbH for about $0.3 million. As of December 30, 2001 we owned 49% of the outstanding common stock of Cadform. We are currently in the process of merging our existing German engineering operations with Cadform. The merger of these operations should strengthen our engineering capabilities and result in future operational efficiencies once complete.

In February 2002, we completed the acquisition of selected assets and liabilities of Draupner Associates AB for a total purchase price of about $2.4 million. The results of Draupner will be included in our consolidated results as of January 2002. Draupner’s principal business is digital documentation and translation services for the automotive and related industries with offices in Europe, Australia and the Pacific Rim. Financing for the transaction was provided through our credit facility.

18

Table of Contents

Inflation

Although we cannot anticipate future inflation, we do not believe that inflation has had, or is likely in the foreseeable future to have, a material impact on our results of operations. While our contracts typically do not include automatic adjustments for inflation, the Ford Master Vendor Agreement does provide for automatic adjustments for inflation for services provided under the Master Vendor Program.

Seasonality

Our quarterly operating results are affected primarily by the number of billing days in the period and the seasonality of our customers’ businesses. Demand for our services has historically been lower during the year-end holidays.

Eurocurrency

On January 1, 1999, the member states of the European Economic and Monetary Union agreed to adopt the Euro as their common legal currency. The existing member state currencies are scheduled to remain legal tender as denominations of the Euro until at least January 1, 2002 but not later than July 1, 2002. During this transition period, monetary transactions may be settled using either the Euro or the existing member state currencies. We have operations in substantially all European Economic and Monetary Union participating countries, as well as in the United Kingdom, which has elected not to participate in the Euro conversion at this time. During fiscal 2001, combined sales from operations that are adopting the Euro were about 19.0% of our total net sales. All of our affected operations have transitioned to make the Euro their functional currency as of December 30, 2001.

We have not experienced any significant operational disruptions to date and do not expect the continued implementation of the Euro to cause any significant future operational disruptions. In addition, we have not incurred and do not expect to incur any significant adverse effects from the continued implementation of the Euro, including currency risk, which could affect our liquidity or capital resources.

Forward Looking Statements

This report on Form 10-K contains statements that constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements can be identified by the use of forward-looking terminology such as “believes,” “expects,” “may,” “estimates,” “will,” “should,” “plans” or “anticipates” or the negative thereof or other variations thereon or comparable terminology, or by discussions of strategy. Such forward-looking statements are not guarantees of future performance and involve significant risks and uncertainties. Actual results may vary materially from those in the forward-looking statements as a result of any number of factors, many of which are beyond the control of management. These factors include, but are not limited to, MSXI’s leverage, its reliance on major customers in the automotive industry, the degree and nature of competition, our ability to recruit and place qualified personnel, risks associated with our acquisition strategy, and employment liability risk.

Item 7A. Quantitative and Qualitative Disclosures about Market Risk.

We are exposed to certain market risks, including interest rate and currency exchange rate risks. Risk exposures relating to these market risks are summarized below. This information should be read in connection with the consolidated financial statements and the related notes thereto included elsewhere in this Form 10-K.

Currency Rate Management

For fiscal 2001, about 35% of our net sales were from markets outside of the United States. To date, the majority of our exposure has been naturally hedged since our foreign operation’s revenues and operating costs are typically denominated in the same currency. We may periodically hedge specific transactions or obligations in non-functional currencies in order to mitigate any additional risk. However, we do not enter into financial instruments for trading or speculative purposes. For the fiscal years ended December 31, 2000 and December 30, 2001, adjustments from the translation of the financial results of our foreign operations reduced equity by about $9.8 million and $38 thousand, respectively.

We currently have operations in Argentina, which has recently experienced economic stagnation and political unrest resulting in a significant currency devaluation of the Argentine peso relative to the U.S. dollar. Due to the size our Argentina operations, relative to our consolidated results, the recent currency devaluation has not had, and is not expected to have, a material impact on our financial condition, results of operations, or cash flows.

19

Table of Contents

Interest Rate Management

We manage interest cost using a combination of fixed and variable rate debt. As of December 30, 2001, we had $130 million of senior subordinated notes outstanding at a fixed interest rate of 11-3/8% with a remaining duration of 6 years. In addition, we have a $205 million credit facility and other short-term facilities at variable rates of interest. As of December 30, 2001, $107.2 million was outstanding under our credit facility at short-term interest rates ranging from 4.23% to 7.00%. A 1% increase in the credit facility’s applicable interest rate would result in additional interest expense of approximately $1.3 million per year.

As of December 30, 2001 the fair value of the senior subordinated notes was $102.2 million compared to its carrying value of $130 million.

Sales to Major Markets/Customers

Our current business is heavily reliant on the domestic and foreign automotive industries. Ford, DaimlerChrysler, General Motors, and Fiat, including their automotive subsidiaries, accounted for approximately 35.6%, 9.3%, 8.5%, and 5.5% of our consolidated net sales, respectively, for fiscal 2001. Significant future price or volume reductions from these customers could adversely affect our earnings and financial condition. We are confident we can expand our services to other less cyclical industries and have had recent success in doing so. However, there can be no assurance that our diversification efforts will fully offset the impact of any further declines in our automotive markets..

20

Table of Contents

Item 8. Financial Statements and Supplementary Data.

Report of Independent Accountants

To the Board of Directors and Shareholders

of MSX International, Inc.

In our opinion, the consolidated financial statements listed in the index appearing under Item 14(a)(1) present fairly, in all material respects, the financial position of MSX International, Inc. and its subsidiaries at December 30, 2001 and December 31, 2000, and the results of their operations and their cash flows for each of the three fiscal years in the period ended December 30, 2001, in conformity with accounting principles generally accepted in the United States of America. In addition, in our opinion, the financial statement schedule listed in the index appearing under Item 14(a)(2) presents fairly, in all material respects, the information set forth therein when read in conjunction with the related consolidated financial statements. These financial statements and financial statement schedule are the responsibility of the Company’s management; our responsibility is to express an opinion on these financial statements and financial statement schedule based on our audits. We conducted our audits of these statements in accordance with auditing standards generally accepted in the United States of America, which require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

/s/ PRICEWATERHOUSECOOPERS LLP

Detroit, Michigan

February 25, 2002

21

Table of Contents

MSX INTERNATIONAL, INC.

CONSOLIDATED BALANCE SHEETS

as of December 31, 2000 and December 30, 2001

| December 31, | December 30, | |||||||||||

| 2000 | 2001 | |||||||||||

| (dollars in thousands) | ||||||||||||