0001059556mco:A20222023GeolocationRestructuringProgramMembermco:MoodysInvestorsServiceMember2024-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

FORM 10-K

(MARK ONE)

☑ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED December 31, 2024

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE TRANSITION PERIOD FROM TO .

COMMISSION FILE NUMBER 1-14037

MOODY’S CORPORATION

(EXACT NAME OF REGISTRANT AS SPECIFIED IN ITS CHARTER) | | | | | |

| Delaware | 13-3998945 |

| (STATE OF INCORPORATION) | (I.R.S. EMPLOYER IDENTIFICATION NO.) |

7 World Trade Center at 250 Greenwich Street, New York, New York 10007

(ADDRESS OF PRINCIPAL EXECUTIVE OFFICES)

(ZIP CODE)

REGISTRANT’S TELEPHONE NUMBER, INCLUDING AREA CODE: (212) 553-0300.

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

| | | | | | | | | | | | | | | | |

| TITLE OF EACH CLASS | | | | TRADING SYMBOL(S) | | NAME OF EACH EXCHANGE ON WHICH REGISTERED |

| Common Stock, par value $0.01 per share | | | | MCO | | New York Stock Exchange |

| 1.75% Senior Notes Due 2027 | | | | MCO 27 | | New York Stock Exchange |

| 0.950% Senior Notes Due 2030 | | | | MCO 30 | | New York Stock Exchange |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT:

NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | | | | | | | |

| Large Accelerated Filer | ☑ | Accelerated Filer ☐ | Non-accelerated Filer ☐ | Smaller reporting company | ☐ | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☑

The aggregate market value of Moody’s Corporation Common Stock held by nonaffiliates* on June 30, 2024 (based upon its closing transaction price on the New York Stock Exchange on such date) was approximately $77 billion.

As of January 31, 2025, 180.0 million shares of Common Stock of Moody’s Corporation were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s definitive proxy statement for use in connection with its annual meeting of stockholders scheduled to be held on April 15, 2025, are incorporated by reference into Part III of this Form 10-K.

The Index to Exhibits is included as Part IV, Item 15(3) of this Form 10-K.

*Calculated by excluding all shares held by executive officers and directors of the Registrant without conceding that all such persons are “affiliates” of the Registrant for purposes of federal securities laws.

* | | | | | | | | | | | | | | | | | |

| Auditor Name: | KPMG LLP | Auditor Location: | New York, NY | Auditor Firm ID: | 185 |

MOODY’S CORPORATION

INDEX TO FORM 10-K | | | | | | | | | | | |

| | Page |

| | | |

|

| Item 1. | | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Item 1A. | | | |

| Item 1B. | | | |

| Item 1C. | | | |

| Item 2. | | | |

| Item 3. | | | |

| Item 4. | | | |

|

| Item 5. | | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Item 7. | | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Item 7A. | | | |

| | | | | | | | | | | |

| | Page |

| Item 8. | | | |

| Item 9. | | | |

| Item 9A. | | | |

| Item 9B. | | | |

| Item 9C. | | | |

|

| Item 10. | | | |

| Item 11. | | | |

| Item 12. | | | |

| Item 13. | | | |

| Item 14. | | | |

|

| Item 15. | | | |

| | | |

| | |

| Item 16. | | | |

| | |

GLOSSARY OF TERMS AND ABBREVIATIONS

The following terms, abbreviations and acronyms are used to identify frequently used terms in this report: | | | | | |

| TERM | DEFINITION |

| |

| Acquisition-Related Intangible Amortization Expense | Amortization expense relating to definite-lived intangible assets acquired by the Company from all business combination transactions |

| |

| Adjusted Diluted EPS | Diluted EPS excluding the impact of certain items as detailed in the section entitled “Non-GAAP Financial Measures” |

| |

| Adjusted Net Income | Net Income excluding the impact of certain items as detailed in the section entitled “Non-GAAP Financial Measures” |

| |

| Adjusted Operating Income | Operating income excluding the impact of certain items as detailed in the section entitled "Non-GAAP Financial Measures" |

| |

| Adjusted Operating Margin | Adjusted Operating Income divided by revenue |

| |

| AI | Artificial Intelligence |

| |

| Americas | Represents countries within North and South America, excluding the U.S. |

| |

| AOCI(L) | Accumulated other comprehensive income (loss); a separate component of shareholders’ equity |

| |

| ARR | Annualized Recurring Revenue; a supplemental performance metric to provide additional insight on the estimated value of MA's recurring revenue contracts at a given point in time, excluding the impact of FX and contracts related to acquisitions |

| |

| ASC | The FASB Accounting Standards Codification; the sole source of authoritative GAAP as of July 1, 2009 except for rules and interpretive releases of the SEC, which are also sources of authoritative GAAP for SEC registrants |

| |

| Asia-Pacific | Represents Australia and countries in Asia including but not limited to: China, India, Indonesia, Japan, Republic of South Korea, Malaysia, Singapore, Sri Lanka and Thailand |

| |

| ASU | The FASB Accounting Standards Update to the ASC. Provides background information for accounting guidance and the bases for conclusions on the changes in the ASC. ASUs are not considered authoritative until codified into the ASC |

| |

| AUD | Australian dollar |

| |

| BES | Business Engagement Survey; A Moody's employee survey that focuses on purpose, leadership, manager effectiveness, well-being, connection and empowerment |

| |

| BitSight | A provider that helps global market participants understand cyber risk through ratings, analytics, and performance management tools; the Company acquired a minority investment in BitSight in 2021 |

| |

| Board | The board of directors of the Company |

| |

| BPS | Basis points |

| |

| |

| |

| BRG | Business Resource Group |

| |

| CAO | Chief Administrative Officer |

| |

| CAD | Canadian dollar |

| |

| CCXI | China Cheng Xin International Credit Rating Co. Ltd.; the first and largest domestic credit rating agency approved by the People’s Bank of China; the Company acquired a 49% interest in 2006 and currently Moody’s owns 30% of CCXI |

| |

| CCPA | California Consumer Privacy Act; a privacy law enacted in 2018 by the state of California to regulate the way businesses all over the world can collect, use and share the personal information of California residents |

| |

| CDP | An international nonprofit organization that helps companies, cities, states and regions to manage their environmental impact through a global disclosure system |

| |

| CEO | Chief Executive Officer |

| |

| CFG | Corporate finance group; an LOB of MIS |

| | | | | |

| TERM | DEFINITION |

| |

| |

| CISO | Chief Information Security Officer |

| |

| CLO | Collateralized loan obligation |

| |

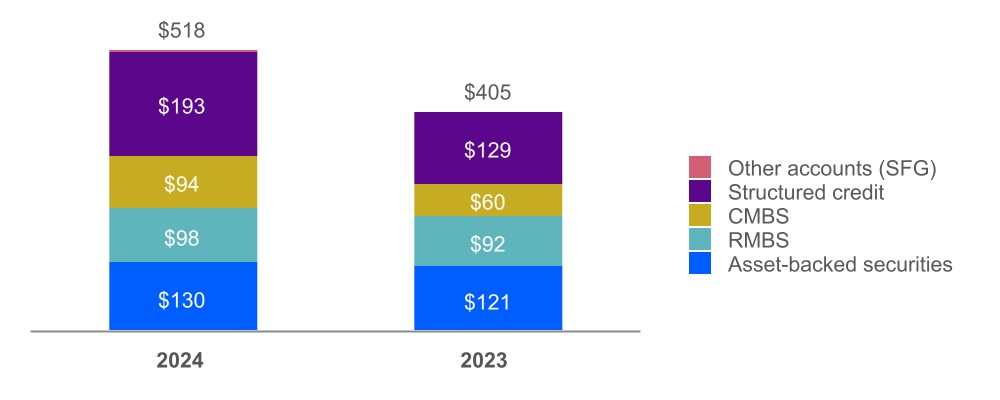

| CMBS | Commercial mortgage-backed securities; an asset class within SFG |

| |

| CODM | Chief Operating Decision Maker; identified as the Company's CEO |

| |

| COLI | Corporate-Owned Life Insurance |

| |

| Common Stock | The Company’s common stock |

| |

| Company | Moody’s Corporation and its subsidiaries; MCO; Moody’s |

| |

| Compensation expense | Compensation expenses include salaries, benefits, incentive and stock based compensation and other related expenses for employees. These expenses are charged to income as incurred. |

| |

| Competition and Markets Authority | Government department in the U.K. responsible for strengthening business competition and preventing and reducing anti-competitive activities |

| |

| COVID-19 | An outbreak of a novel strain of coronavirus resulting in an international public health crisis and a global pandemic |

| |

| CP | Commercial Paper |

| |

| CP Notes | Unsecured commercial paper issued under the CP Program |

| |

| CP Program | A program entered into on August 3, 2016 allowing the Company to privately place CP up to a maximum of $1 billion for which the maturity may not exceed 397 days from the date of issue, and which is backstopped by the 2024 Facility |

| |

| CPRA | California Privacy Rights Act of 2020; an amendment to the CCPA, which adds additional consumer privacy rights and obligations for businesses |

| |

| CRAs | Credit rating agencies |

| |

| CRE | Commercial Real Estate |

| |

| CTSO | Chief Technology Services Officer |

| |

| Cyber Committee | The Cyber Risk Enterprise Risk Management Committee |

| |

| Data and Information (D&I) | LOB within MA which provides vast data sets on companies and securities via data feeds and data applications products |

| |

| DBPPs | Defined benefit pension plans |

| |

| Decision Solutions (DS) | LOB within MA that provides subscription-based solutions supporting banking, insurance, and KYC workflows. This LOB utilizes components from the Data & Information and Research & Insights LOBs to provide risk assessment solutions |

| |

| |

| |

| Dodd-Frank Act | Dodd-Frank Wall Street Reform and Consumer Protection Act |

| |

| DORA | The European Union Digital Operational Resilience Act |

| |

| EBITDA | Earnings before interest, taxes, depreciation and amortization |

| |

| |

| |

| EMEA | Represents countries within Europe, the Middle East and Africa |

| |

| EPS | Earnings per share |

| |

| ESG | Environmental, Social and Governance |

| |

| ESMA | European Securities and Markets Authority |

| |

| ESTR | Euro Short-Term Rate |

| |

| ESPP | Employee stock purchase plan |

| |

| ETR | Effective tax rate |

| |

| EU | European Union |

| |

| | | | | |

| TERM | DEFINITION |

| |

| EU AI Act | A European regulation adopted in 2024 to introduce a common regulatory and legal framework for artificial intelligence |

| |

| EUR | Euros |

| |

| Eurozone | Monetary union of the EU member states which have adopted the euro as their common currency |

| |

| Excess Tax Benefits | The difference between the tax benefit realized at exercise of an option or delivery of a restricted share and the tax benefit recorded at the time the option or restricted share is expensed under GAAP |

| |

| Exchange Act | The Securities Exchange Act of 1934, as amended |

| |

| External Revenue | Revenue excluding any intersegment amounts |

| |

| FASB | Financial Accounting Standards Board |

| |

| FCA | Financial Conduct Authority; supervises Credit Rating Agencies in the U.K. in order to ensure credit ratings are independent, objective and of adequate quality |

| |

| FIG | Financial institutions group; an LOB of MIS |

| |

| Free Cash Flow | Net cash provided by operating activities less cash paid for capital additions |

| |

| FTC | Federal Trade Commission |

| |

| FTSE | Financial Times Stock Exchange |

| |

| FX | Foreign exchange |

| |

| GAAP | U.S. Generally Accepted Accounting Principles |

| |

| GBP | British pounds |

| |

| GCR (Global Credit Rating Company Limited and subsidiaries) | A domestic credit rating agency with operations spanning Africa; the Company acquired a controlling financial interest in GCR in July 2024; the Company previously accounted for GCR as an equity method investment |

| |

| GDP | Gross domestic product |

| |

| GDPR | General Data Protection Regulation; a European regulation implemented in 2018 to enhance EU citizens' control over the personal data that companies can legally hold. GDPR was simultaneously implemented in the U.K., with slight modification to the EU's regulation in 2021 following the withdrawal of the U.K. from the EU |

| |

| Gen AI | Generative Artificial Intelligence |

| |

| GLoBE | Global Anti-Base Erosion, also known as "Pillar II"; tax model issued by the OECD in 2023 |

| |

| HM Treasury | His Majesty's Treasury; the department of the Government of the United Kingdom responsible for developing and executing the government's public finance policy and economic policy |

| |

| ICRA | ICRA Limited; a provider of credit ratings and research in India. |

| |

| Incident Response Plan | The Company's Information Security Incident Response Plan |

| |

| INR | Indian rupee |

| |

| IRS | Internal Revenue Service |

| |

| ISO 27001 | An international standard to manage information security |

| |

| JPY | Japanese yen |

| |

| kompany | 360kompany AG; a platform for business verification and Know Your Customer (KYC) technology solutions acquired by the Company in February 2022 |

| |

| KMV | KMV LLC and KMV Corporation (“KMV”); a provider of market-based quantitative services for banks and investors in credit-sensitive assets acquired by Moody's in April 2002 |

| |

| KYC | Know-your-customer |

| |

| | | | | |

| TERM | DEFINITION |

| |

| LLM | Large language model used in the context of Gen AI |

| |

| LOB | Line of business |

| |

| MA | Moody’s Analytics - a reportable segment of MCO; consists of three LOBs - Decision Solutions; Research and Insights; and Data and Information |

| |

| ML | Machine Learning |

| |

| MAKS | Moody’s Analytics Knowledge Services; formerly known as Copal Amba; provided offshore research and analytic services to the global financial and corporate sectors; business was divested in the fourth quarter of 2019 and a reporting unit within the MA reportable segment |

| |

| MCO | Moody’s Corporation and its subsidiaries; the Company; Moody’s |

| |

| MD&A | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

| |

| M&A | Mergers and acquisitions |

| |

| MIS | Moody’s Investors Service - a reportable segment of MCO; consists of five LOBs - CFG; SFG; FIG; PPIF; and MIS Other |

| |

| MIS Other | Consists of financial instruments pricing services in the Asia-Pacific region, ICRA non-ratings revenue, and revenue from professional services. These businesses are components of MIS; MIS Other is an LOB of MIS |

| |

| MNPI | Material non-public information |

| |

| Moody’s | Moody’s Corporation and its subsidiaries; MCO; the Company |

| |

| Moody's Local | A ratings platform focused on providing credit rating services in Latin American capital markets |

| |

| MSS | Moody's Shared Services; primarily consists of information technology and support staff such as finance, human resources and legal that support both MA and MIS |

| |

| NAV | Net asset value |

| |

| Net Income | Net income attributable to Moody’s Corporation, which excludes net income from consolidated noncontrolling interests belonging to the minority interest holder |

| |

| Net Zero Assessments | An independent assessment of an entity’s carbon transition plan relative to a global net zero pathway, consistent with the goals of the 2015 Paris Agreement on climate change |

| |

| |

| |

| NIST Framework | NIST Cybersecurity Framework; a set of cybersecurity best practices and recommendations from the National Institute of Standards and Technology (NIST) |

| |

| NM | Percentage change is not meaningful |

| |

| Non-compensation expense | Non-compensation expenses include costs incurred that are not related to employee compensation. This includes, but is not limited to, consulting and professional service fees, hosting expenses, rent, and marketing expenses. These expenses are charged to income as incurred. |

| |

| Non-GAAP | A financial measure not in accordance with GAAP; these measures, when read in conjunction with the Company’s reported results, can provide useful supplemental information for investors analyzing period-to-period comparisons of the Company’s performance, facilitate comparisons to competitors’ operating results and to provide greater transparency to investors of supplemental information used by management in its financial and operational decision making |

| |

| NRSRO | Nationally Recognized Statistical Rating Organization, which is a credit rating agency registered with the SEC |

| |

| Numerated | A provider of commercial lending platforms; the Company acquired Numerated in November 2024 |

| |

| OCI(L) | Other comprehensive income (loss); includes gains and losses on cash flow and net investment hedges, certain gains and losses relating to pension and other retirement benefit obligations and foreign currency translation adjustments |

| |

| OECD | Organization for Economic Co-operation and Development |

| |

| | | | | |

| TERM | DEFINITION |

| |

| Operating segment | Term defined in the ASC relating to segment reporting; the ASC defines an operating segment as a component of a business entity that has each of the three following characteristics: i) the component engages in business activities from which it may recognize revenue and incur expenses; ii) the operating results of the component are regularly reviewed by the entity’s chief operating decision maker; and iii) discrete financial information about the component is available. |

| |

| Other Retirement Plans | Moody's Postretirement Medical and Life Insurance Plan |

| |

| PCS | Post-Contract Customer Support |

| |

| Pillar II | Tax model issued by the OECD in 2023; also referred to as the "Global Anti-Base Erosion" or "GLoBE" rules |

| |

| PPIF | Public, project and infrastructure finance; an LOB of MIS |

| |

| Praedicat | A provider of casualty insurance analytics; the Company acquired a controlling financial interest in Praedicat in September 2024; the Company previously accounted for Praedicat as an equity method investment |

| |

| Profit Participation Plan | Defined contribution profit participation plan that covers substantially all U.S. employees of the Company |

| |

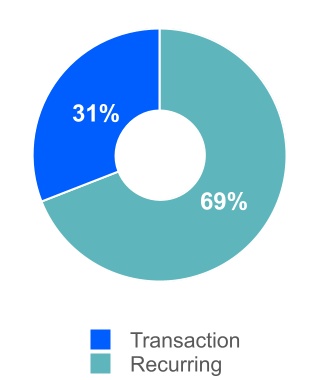

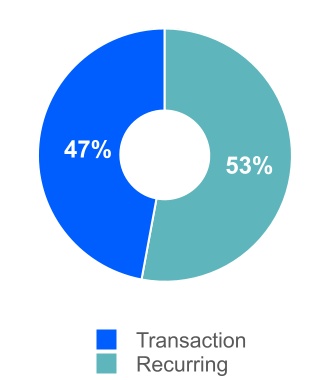

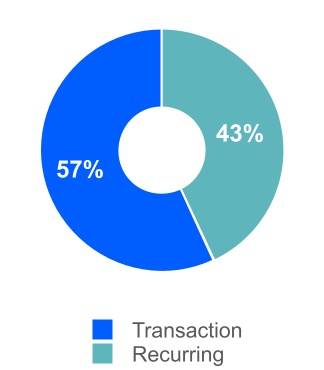

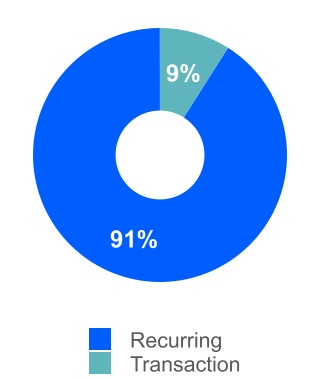

| Recurring Revenue | For MA, represents subscription-based revenue and software maintenance revenue. For MIS, represents recurring monitoring fees of a rated debt obligation and/or entities that issue such obligations, as well as revenue from programs such as commercial paper, medium-term notes and shelf registrations. For MIS Other, represents financial instrument pricing services. |

| |

| Reform Act | Credit Rating Agency Reform Act of 2006 |

| |

| |

| |

| |

| |

| Reporting unit | The level at which Moody’s evaluates its goodwill for impairment under U.S. GAAP; defined as an operating segment or one level below an operating segment |

| |

| Research and Insights (R&I) | LOB within MA that provides models, scores, expert insights and commentary. This LOB includes credit research; credit models and analytics; economics data and models; and structured finance solutions |

| |

| Retirement Plans | Moody’s funded and unfunded pension plans, the healthcare plans and life insurance plans |

| |

| Revenue Accounting Standard | Updates to the ASC pursuant to ASU No. 2014-09, “Revenue from Contracts with Customers (ASC Topic 606).” This accounting guidance significantly changed the accounting framework under U.S. GAAP relating to revenue recognition and to the accounting for the deferral of incremental costs of obtaining or fulfilling a contract with a customer |

| |

| RMBS | Residential mortgage-backed securities; an asset class within SFG |

| |

| RMS | A global provider of climate and natural disaster risk modeling and analytics; acquired by the Company in September 2021 |

| |

| ROU Asset | Assets which represent the Company’s right to use an underlying asset for the term of a lease |

| |

| SaaS | Software-as-a-Service |

| |

| SASB | Sustainability Accounting Standards Board |

| |

| SEC | U.S. Securities and Exchange Commission |

| |

| Second Party Opinions | An independent assessment of how debt instruments or financing frameworks align to sustainability principles and the extent to which they are expected to contribute to long-term sustainable development |

| |

| Securities Act | Securities Act of 1933, as amended |

| |

| SFG | Structured finance group; an LOB of MIS |

| |

| SG&A | Selling, general and administrative expenses |

| |

| SGD | Singapore dollar |

| |

| SOC 1 | An examination of controls at a service organization that are likely to be relevant to user entities’ internal control over financial reporting, as defined by the American Institute of Certified Public Accountants |

| |

| SOC 2 | A report on controls at a service organization relevant to security, availability, processing integrity, confidentiality, or privacy, as defined by the American Institute of Certified Public Accountants |

| |

| | | | | |

| TERM | DEFINITION |

| |

| SOFR | Secured Overnight Financing Rate |

| |

| SSP | Standalone selling price |

| |

| Strategic and Operational Efficiency Restructuring Program | Multi-year restructuring program approved by the CEO of Moody’s on December 19, 2024 relating to the Company's strategy to realign the business toward high priority growth areas and to consolidate certain functions to simplify the organizational structure to enable efficiency and improved operating leverage; includes a reduction in staff, the rationalization and exit of certain real estate leases and incremental amortization of certain software |

| |

| T&M | Time-and-Material |

| |

| Tax Act | The “Tax Cuts and Jobs Act” enacted into U.S. law on December 22, 2017, which significantly amended the tax code in the U.S. |

| |

| TCFD | Task Force on Climate-Related Financial Disclosures |

| |

| Transaction Revenue | For MA, represents perpetual software license fees and revenue from software implementation services, risk management advisory projects, and training and certification services. For MIS (excluding MIS Other), represents the initial rating of a new debt issuance as well as other one-time fees. For MIS Other, represents revenue from professional services |

| |

| U.K. | United Kingdom |

| |

| U.S. | United States |

| |

| USD | U.S. dollar |

| |

| UTPs | Uncertain tax positions |

| |

| |

| |

| WACC | Weighted Average Cost of Capital |

| |

| 2022 - 2023 Geolocation Restructuring Program | Restructuring program approved by the CEO of Moody’s on June 30, 2022 relating to the Company's post-COVID-19 geolocation strategy and other strategic initiatives; includes the rationalization and exit of certain real estate leases and a reduction in staff, including the relocation of certain job functions from their current locations |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

PART I

ITEM 1. BUSINESS

Background

As used in this report, except where the context indicates otherwise, the terms “Moody’s” or the “Company” refer to Moody’s Corporation, a Delaware corporation, and its subsidiaries. The Company’s executive offices are located at 7 World Trade Center at 250 Greenwich Street, New York, NY 10007 and its telephone number is (212) 553-0300.

THE COMPANY

Company Overview

In a world shaped by increasingly interconnected risks, Moody's data, insights, and innovative technologies help customers develop a holistic view of their world and unlock opportunities. With a rich history of experience in global markets and a diverse workforce of approximately 16,000 across more than 40 countries, Moody's gives customers the comprehensive perspective needed to act with confidence and thrive.

Moody's is helping customers accelerate value creation in an era of exponential risk.

We provide tools that enable Banks, Insurers, Investors, Corporations and Governments to...

| | | | | | | | | | | |

What do

we do? | Issue, Originate, Select, Underwrite | Identify, Measure, Monitor & Manage Risk | Verify, Comply, Plan & Report |

Leveraging an unrivaled set of data, analytics, & domain expertise across...

| | | | | | | | | | | | | | |

How do we

do this? | Credit

Companies | Properties

Securities | People

Economies | ESG

Climate |

Moody’s has two reportable segments: MA and MIS.

| | | | | | | | | | |

| | | | |

| Moody's Analytics | | | Moody's Investors Service |

| MA provides data, intelligence and analytical tools to help business and financial leaders make confident decisions. | | | | For more than 115 years, MIS has been a leading provider of credit ratings, research, and risk analysis helping businesses, governments, and other entities around the globe. |

| | | | |

Financial information and operating results of these segments, including revenue, expenses and Adjusted Operating Income, are included in Part II, Item 8. Financial Statements of this annual report and are herein incorporated by reference.

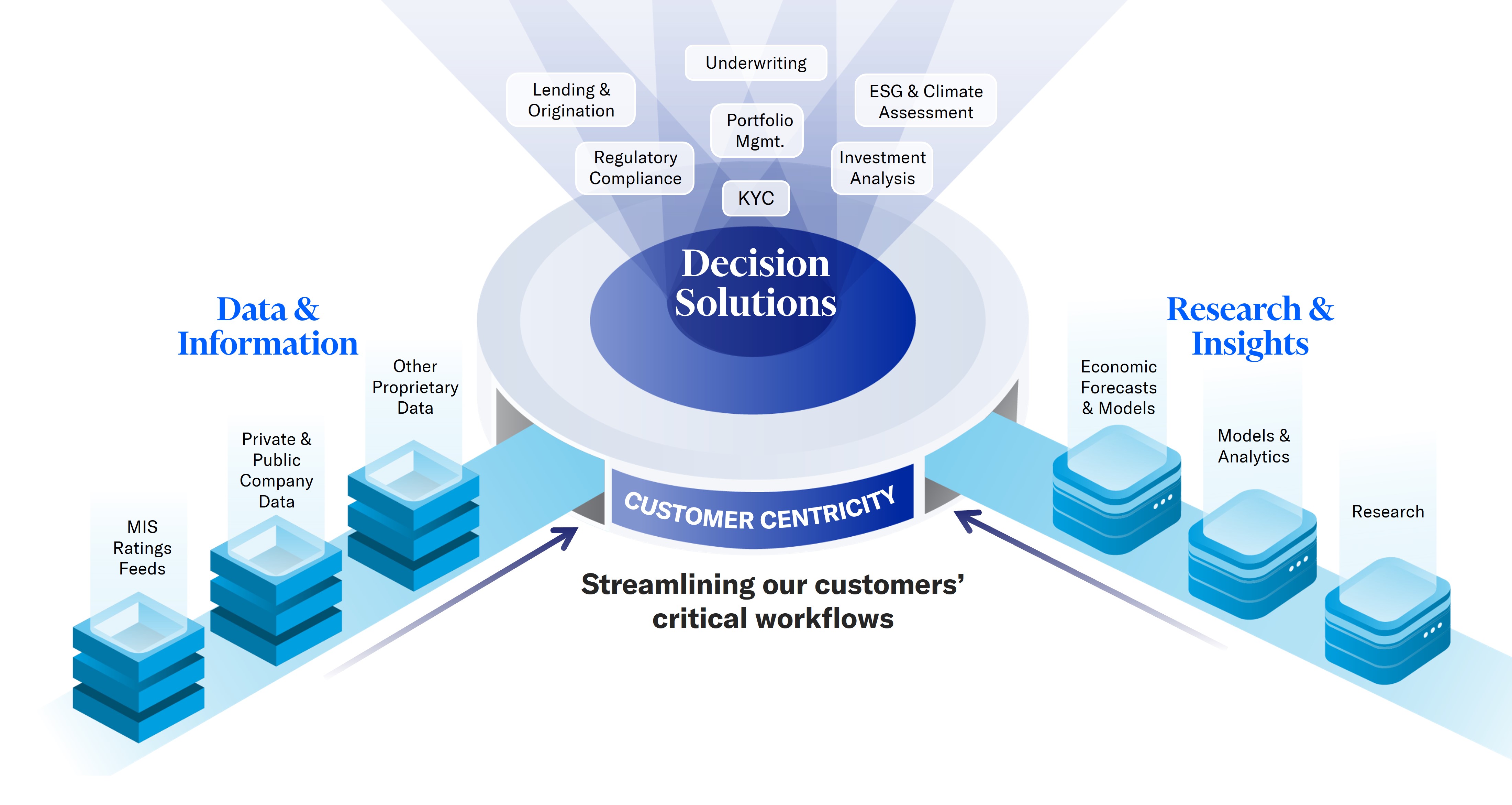

Moody's Analytics Overview

MA empowers financial services, corporate and public sector customers to anticipate risks, adapt and thrive in a new era of exponential risk. MA's combined data, analytics and cloud-based software tools deliver integrated solutions that help customers to start business relationships, monitor and manage risk, and comply and report based on global laws, rules and regulations.

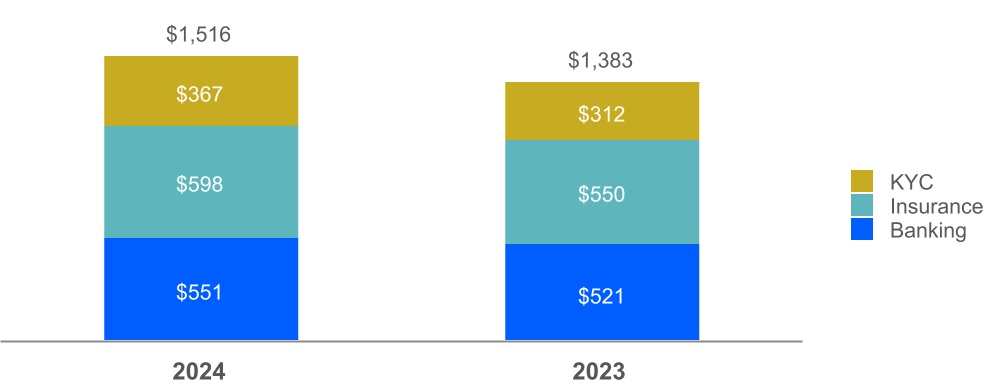

MA is comprised of: i) a premier fixed income and economic research business (Research & Insights); ii) a data business powered by the world’s largest database on companies and credit (Data & Information); and iii) three cloud-based subscription businesses serving banking, insurance and KYC workflows (Decision Solutions).

MA creates a holistic view on risk provided by our vast set of proprietary data, analytics, and domain expertise across a range of areas, including credit, companies, properties, securities, people, economies, ESG, climate and more. MA's integrated and technology-enabled solutions provide unique capabilities and insights that are embedded in customer workflows.

| | | | | | | | | | | | | | | | | | | | | | | |

| MA by the Numbers |

| | | | | | | |

| 14,800+ | | | 6,700+ | | | 800+ |

| MA Customers | | Corporates and Professional Services | | Real Estate Entities |

| | | | | | | |

| 165+ | | | 2,600+ | | | 600+ |

| Countries where MA customers operate | | Commercial Banks | | Educational Institutions |

| | | | | | | |

| | | | 1,900+ | | | 200+ |

| | | Asset Managers | | Securities Dealers and Investment Banks |

| | | | | | | |

| | | | 900+ | | | 200+ |

| | | Government Entities | | Others |

| | | | | | | |

| | | | 900+ | | | |

| | | Insurance Companies | | | |

Moody's Investors Service Overview

MIS is a leading global provider of credit ratings, research, and risk analysis. A rating from Moody’s enables issuers to create timely, go-to-market debt strategies with the ability to capture wider investor focus and provides investors with a comprehensive view of global debt markets through our credit ratings and research. Moody’s trusted insights can help decision-makers navigate the safest path through market turmoil and volatility.

MIS publishes credit ratings and provides assessment services on a wide range of debt obligations, programs and facilities, and the entities that issue such obligations in markets worldwide, including various corporate, financial institution and governmental obligations, and structured finance securities.

| | | | | | | | | | | | | | | | | | | | |

| The Benefits of a Moody's Rating |

| Investors seek Moody's opinions and particularly value the knowledge of its analysts and the depth of Moody's research |

| | | | | | |

| Access to capital | | Transparency, credit comparison and market stability | | Planning and budgeting | | Analytical capabilities |

•Moody’s opinions on credit are used by institutional investors throughout the world, making an issuer’s debt potentially more attractive to a wide range of buyers. | | •Signals a willingness by issuers to be transparent and provides issuers with an independent assessment against which to compare creditworthiness. | | •May help issuers when formulating internal capital plans and funding strategies. | | •Among ratings advisors, Moody’s has a strong position and is well-recognized for the depth and breadth of its analytical capabilities. |

| | | | | |

•A Moody’s rating may facilitate access to both domestic and international debt capital.

| | •Moody’s ratings and research reports may help maintain investor confidence, especially during periods of market stress. | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| MIS by the Numbers |

| | | | | | | |

| $75.8+ trillion | | | 4,800+ | | | 3,300+ |

| Total Rated Debt Outstanding | | Non-Financial Corporates | | Financial Institutions |

| | | | | | | |

| 33,300+ | | | 14,400+ | | | 8,900+ |

| Rated Organizations and Structured Deals | | U.S. Public Finance Issuers | | Structured Finance Deals |

| | | | | | | |

| 190+ | | | 1,000+ | | | 380+ |

| Rating Methodologies | | Infrastructure & Project Finance Issuers | | Sub-Sovereigns |

| | | | | | |

| | | | 140+ | | | 50 |

| | | Sovereigns | | Supranational Institutions |

MIS also generates revenue from certain non-ratings-related operations, which primarily consist of financial instruments pricing services in the Asia-Pacific region, revenue from Second Party Opinions and Net Zero Assessments and revenue from ICRA's non-ratings operations. The revenue from these operations is included in the MIS Other LOB and is not material to the results of the MIS segment.

Sustainability

Moody's aims to deliver value to all stakeholders, including customers, employees, partners, communities, and stockholders. We consider sustainability in our operations, products, and services. We use our expertise to make a positive impact, helping others understand the link between sustainability and global markets. In 2024, Moody's received multiple awards for its sustainability efforts, including:

•Recognized among America’s 100 Most JUST Companies by JUST Capital and CNBC for its commitment to serving its workforce, customers, communities, the environment, and stockholders for its sustainability-related efforts;

•Made CDP's 2023 Climate Change 'A' List, in recognition of Moody's leadership in corporate transparency and actions taken in response to climate change;

•Named to the 2023 Dow Jones Sustainability Indices - World and North America, an annual listing of publicly traded companies, recognizing Moody's for its strong corporate sustainability practices; and

•Recognized as a 2023 CDP Supplier Engagement leader for the fourth consecutive year, ranking among the top 4% of companies assessed for supplier engagement on climate change.

The Board oversees sustainability matters via the Audit, Governance & Nominating, and Compensation & Human Resources Committees, as part of its oversight of management and the Company’s overall strategy. The Audit Committee oversees financial, risk and other disclosures made in the Company’s annual and quarterly reports related to sustainability. The Governance & Nominating Committee oversees sustainability matters, including significant issues of corporate social and environmental responsibility, as they pertain to the Company’s business and to long-term value creation for the Company and its stockholders, and makes recommendations to the Board regarding these issues. Finally, the Compensation & Human Resources Committee oversees inclusion of sustainability-related performance goals for determining compensation of all senior executives. The Board also oversees Moody’s policies for assessing and managing the Company's exposure to risk, including climate-related risks such as business continuity disruption and reputational or credibility concerns stemming from incorporation of climate-related risks into our credit rating methodologies, or analysis of such risks within our products and services. The Board maintains its collective knowledge of sustainability topics through ongoing education, such as regular presentations from management.

| | | | | | | | | | | | | | | | | | | | | | | |

| Three Pillars of Moody's Sustainability Strategy |

| | | | |

| Our Actions | | Our Influence | | Our Support |

| the decisions and actions we can take related to impacts under our direct control | | the actions that we can request from entities providing us with products and services | | the steps we take to support or enable direct action by other organizations or communities |

HUMAN CAPITAL

Our employees are vital to Moody’s continued success, and we seek to create an environment that attracts, develops and sustains a highly skilled, performance-oriented and engaged workforce. Our approach is oriented around the following pillars:

–providing market-competitive compensation, benefits and wellness programs as part of our Total Rewards program;

–implementing a robust talent management, employee engagement and retention strategy; and

–fostering an inclusive environment where all employees have a sense of belonging and are given the opportunity to perform their best.

Total Rewards

Moody's Total Rewards programs are designed to attract and maintain a high-performing, engaged and motivated global workforce. The Company's compensation packages include market-competitive salaries, performance-based annual bonuses, and equity grants aligned to our long-term performance for certain employees.

The Company's industry leading benefits programs offer comprehensive resources to support physical, mental and financial well-being. We invest in AI powered technologies in order to provide our employees with a world-class experience accessing and managing their benefits. We continuously evaluate our market benchmarks and employee feedback so that our benefits are competitive and support the attraction of the best talent. For example, in recent years we implemented a global paid parental leave policy to give parents time off to care for and bond with a new child and updated our tuition reimbursement program.

The Company also promotes flexible work arrangements, which support the Company's efforts to create a work atmosphere in which people feel valued and inspired to give their best. The Company has implemented a "PurposeFirst" framework, which fosters purpose-driven decisions relating to how and where Moody's teams work.

Talent Management, Employee Engagement and Retention

Moody’s believes that our long-term success depends on our ability to attract, develop and retain a high-performing workforce. Our goal is to create an environment where colleagues can thrive personally and professionally and can maximize their potential. Our culture is one of continuous learning, which we believe is crucial for colleagues to thrive as part of our organization and to feel a sense of accomplishment and purpose, and our leaders are key in reinforcing this at Moody’s.

Moody's talent strategy helps us create integrated, cohesive talent activities that support the growth and success of our employees and the business. This strategy informs all of our talent programs, guiding our efforts to attract, develop and retain top talent. It also helps us remain aligned with Moody’s overall business objectives and values while designing programs to meet the evolving needs of our organization.

Moody’s offers various talent development programs and resources through Moody’s University that are focused on building professional, technical and leadership skills to support employees' goals and objectives. Moody’s also places significant emphasis on our high-potential and high-performance programs, which are designed to identify and nurture emerging leaders within the organization. These programs provide tailored development opportunities, mentorship and the chance to work on strategic projects that drive our business forward.

Moody's Employee Experience function conducts listening sessions with our employees and creates targeted plans to act on the feedback provided. We measure employee engagement via multiple channels, including the BES for employees to provide anonymous and candid feedback to management. This periodic survey helps Moody's management understand our employees' level of engagement in critical areas, which include, but are not limited to, purpose, leadership, managerial effectiveness, connection, enablement and empowerment and well-being. Managers are accountable for identifying opportunity areas and taking targeted actions based on survey results. The feedback received through the BES is used as a vital input into making decisions to improve employee experience and retention. As we strive to make Moody’s a place people want to come and stay, management also carefully monitors global employee turnover rates.

Inclusion and Belonging

Moody's believes that a workforce comprised of individuals with varied thoughts, backgrounds and experiences fosters an environment that makes our opinions stronger, our products more innovative, our workplace more welcoming and improves how we relate and respond to our customers. We are committed to cultivating a culture where every individual feels a sense of belonging and has an equal opportunity to succeed.

Our Inclusion Operating and Governance Model turns our inclusion strategy into reality by providing a functional framework to guide how our People team, councils, sponsors, BRGs and committees work together. The Global Inclusion Council, chaired by our CEO and composed of senior leaders, is charged with oversight of our global inclusion strategy and its progress. The members of the council meet quarterly.

Our governance model also includes three Regional Inclusion Councils tasked with overseeing the inclusion strategy within their respective regions. Each council meets on a quarterly basis.

Our operating model includes 11 active BRGs which represent 48 chapters. These groups are open to all Moody's employees, with more than 4,800 employees participating globally as of December 31, 2024.

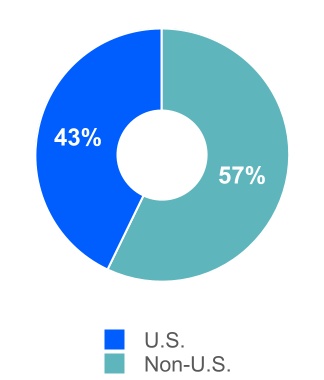

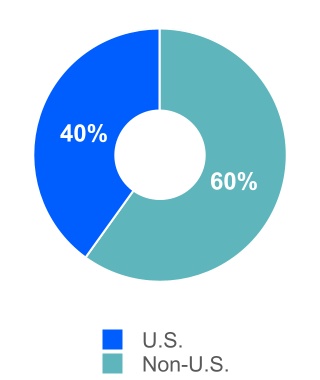

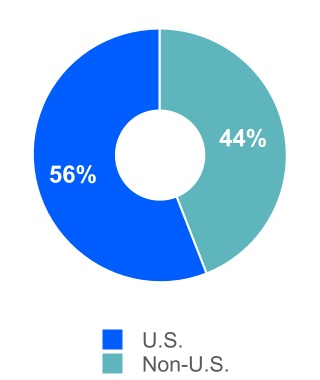

Workforce Overview

As of December 31, 2024 and 2023, the number of Moody’s employees was as follows:

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | | December 31, | | | | Change |

| | 2024 | | 2023(1) | | | | % |

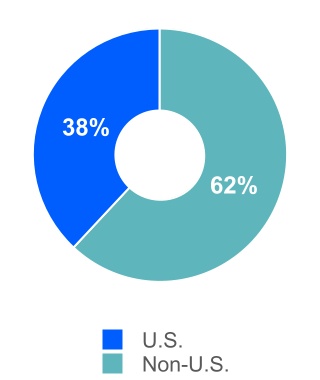

| MA | U.S. | | 2,989 | | | 2,992 | | | | | — | % |

| Non-U.S. | | 5,156 | | | 4,872 | | | | | 6 | % |

| Total | | 8,145 | | | 7,864 | | | | | 4 | % |

| MIS | U.S. | | 1,571 | | | 1,490 | | | | | 5 | % |

| Non-U.S. | | 4,186 | | | 3,870 | | | | | 8 | % |

| Total | | 5,757 | | | 5,360 | | | | | 7 | % |

| MSS | U.S. | | 696 | | | 749 | | | | | (7) | % |

| Non-U.S. | | 1,240 | | | 1,187 | | | | | 4 | % |

| Total | | 1,936 | | | 1,936 | | | | | — | % |

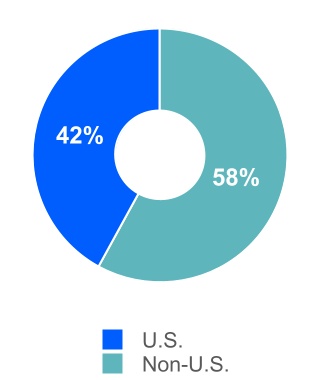

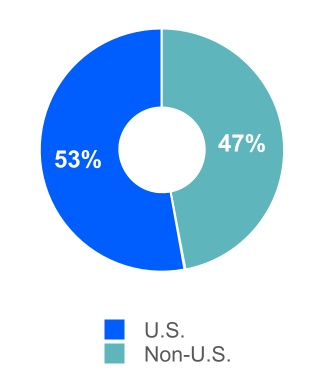

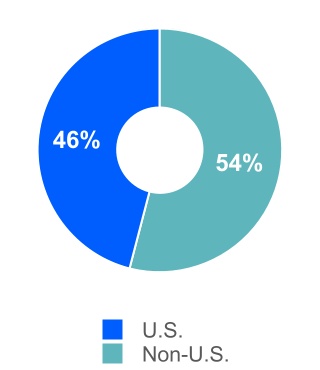

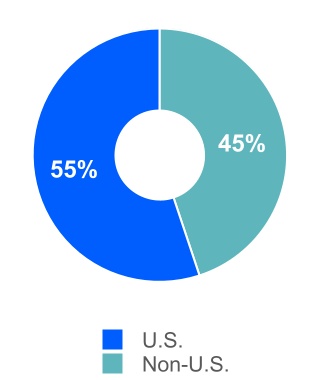

| Total MCO | U.S. | | 5,256 | | | 5,231 | | | | | — | % |

| Non-U.S. | | 10,582 | | | 9,929 | | | | | 7 | % |

| Total | | 15,838 | | | 15,160 | | | | | 4 | % |

(1) Certain reclassifications have been made to 2023 amounts to reflect certain departmental reorganizations and M&A integrations

–MA’s employee population primarily consists of software engineers, product managers and strategists, data and operations analysts, advisory and implementation teams and economists, as well as sales, business development, and sales support professionals.

–The MIS employee population primarily consists of credit analysts, data and operations analysts, credit strategy and methodology professionals, software engineers, sales and sales operations, and international strategy teams.

–The MSS employee population primarily consists of information technology professionals and other professional staff such as finance, human resources, compliance, and legal that support both MA and MIS.

CLIMATE CHANGE

Climate change is a major challenge that demands action from all of us. While Moody’s has a limited direct environmental impact, we do have an important role to play in demonstrating proactive corporate responsibility and best practices when it comes to climate change mitigation. As such, the Company is taking steps to reduce emissions across its operations and value chain in accordance with its decarbonization strategy.

Our decarbonization plan outlines tangible strategies for realizing our climate ambitions, including the procurement of 100% of renewable electricity in the Company’s office spaces and optimizing efficiencies in its operations through its hybrid work program. The costs associated with the implementation of the decarbonization plan are not expected to be material.

The acquisition of RMS allowed us to expand our climate data and analysis capabilities. The Company continues to take steps to integrate these capabilities into existing offerings to provide its analysts and researchers with streamlined access to consistent and high-quality climate insights. Additionally, we have launched a Net Zero Assessment framework to provide an independent and comparable evaluation of the strength of an entity’s carbon transition plan.

MOODY’S STRATEGY

Moody’s is a global integrated risk assessment firm that empowers organizations to anticipate, adapt and thrive in a new era of exponential risk. Our data, analytical solutions and insights help decision-makers identify opportunities and manage the risks of doing business with others.

| | | | | | | | | | | | | | | | | | | | |

| | | | | | |

| Mission | Our mission is to be the leading source of relevant insights on exponential risk |

| | | | | | |

| Growth Strategy | Invest with intent to grow and scale |

| | | | | |

| | | |

Invest with intent to grow and strengthen our core business with a foundation of credibility, transparency, technology, data and analytics | | Invest in integrated solutions to allow customers to manage multiple risks, bringing the best of Moody's capabilities | | Invest to successfully scale in priority growth markets with highly differentiated products and services |

| | | | | |

| Investment in high growth markets |

| | | | | | |

| Execution Priorities | How we will get it done |

| | | | | |

| | | | |

| Customer first | | Develop our people and culture | | Collaborate, modernize and innovate |

| | | | | | |

Moody’s invests in initiatives to implement the Company’s strategy, including internally-led organic development and targeted acquisitions. Illustrative examples include:

| | | | | | | | | | | | |

| | | | |

| Enhancements to ratings quality and product extensions | | Expansion in emerging markets | New products, services, content and technology capabilities, including Gen AI, to meet customer demands | Investments that extend ownership and participation in joint ventures as well as acquisitions and strategic partnerships that accelerate the ability to scale and grow Moody’s businesses |

In this era of exponential risk, we know that risks are interconnected, and organizations want a complete view of risk. This includes having a greater breadth and depth of understanding around how risks connect.

Our integrated approach provides stakeholders with a more comprehensive view of risk, helping them to make better decisions and unlock opportunities. Moody’s brings together multiple data sets and develops risk analysis solutions to assess multiple risk factors (e.g., supply chain failures; cyberattacks; geopolitical tensions; sanctions and security issues; and extreme weather events).

PROSPECTS FOR GROWTH

Moody’s believes that the overall long-term outlook remains favorable for continued growth from the offerings of both of our reportable segments.

Moody’s growth is influenced by a number of trends that impact the market for our products, including:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | |

| Enablement of Gen AI | | Health of the world’s major economies | | Debt capital markets activity | | Disintermediation of credit markets | | Fiscal and monetary policy of governments | | Expansion of market for integrated data and analytics solutions | | Business investment spending, including mergers and acquisitions |

In an environment of increasing financial complexity and exponential risk, Moody’s expects to be well positioned to benefit from continued growth in global fixed-income market activity and more widespread use of credit ratings and integrated risk solutions. Moreover, pricing opportunities aligned with customer value creation and advances in technology present growth opportunities for Moody’s.

Over the last decade, Moody’s has leveraged the power of AI and ML to better serve our customer base. As an early adopter of Gen AI, Moody's expects to be well positioned to benefit from the capabilities of this technology, which will help our customers make better decisions by unlocking deeper, more integrated perspectives on risk. Through enablement of Gen AI, both internally and through certain strategic partnerships, we are in the process of evolving how we deliver insights on exponential risk to our customers.

Moody’s operations are subject to various risks, as more fully described in Part I, Item 1A “Risk Factors,” inherent in conducting business on a global basis.

MA Prospects for Growth

MA provides insights on the evolving risks of our customers and supports their ability to capitalize on related opportunities. Growth in MA is likely to be driven by landing new customers and expanding customer relationships across use cases over time. Our trusted and curated data is key in an environment that is increasingly using Gen AI, and we expect that the integration of our platforms will enable effective cross-selling of models, data and applications. MA's growth is also likely to be driven by quickly addressing new use cases and incorporating new risk data and analytics as needed.

Strategic growth drivers:

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| NEW PRODUCT DEVELOPMENT | | STRONG CUSTOMER RETENTION RATES | | CROSS-SELLING, UPGRADES & PRICING | | CONTINUED SAAS TRANSITION | | INCREASED DISTRIBUTION CAPACITY AND PRODUCTIVITY |

| | | | | | | | |

Market growth drivers:

Customers need to understand a large range of interconnected and emerging risks. Our comprehensive solutions support the transformation underway across various industries due to:

| | | | | | | | | | | |

| Operational and reputational risks | | Digitization & Artificial Intelligence |

| Evolving regulatory environment | | Fluctuations in credit and financial markets |

| Climate change | | Geopolitical risks |

MIS Prospects for Growth

Strong secular trends should continue to provide long-term growth opportunities in MIS. Key growth drivers include:

| | | | | | | | | | | | | | | | | | | | | | | |

| Long-term Growth Building Blocks |

| | | | | | | |

| Economic Expansion | + | | Value Proposition | + | | Developing Capital Markets and Evolving Risks |

•GDP growth drives demand for debt capital to fund business investments •Refinancing needs support future supply | •Proven rating accuracy and deeply experienced analysts •Mix of issuers and opportunistic issuance | •Deepening participation in developing markets •Meeting customers’ evolving risk assessment demands, including Sustainable and Transition Finance, Private Credit, Digitalization of the financial sector, and Cybersecurity |

|

|

In addition to the factors noted above, growth in global fixed income markets in a given year is dependent on many macroeconomic and capital market factors including:

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

| Interest rates | Business investment spending | Corporate refinancing needs | Merger and acquisition activity | Issuer financial health | Consumer borrowing levels | Securitization activity | Expansion of ratings coverage | Expansion into emerging markets |

Rating fees paid by debt issuers account for most of the revenue of MIS. Therefore, a substantial portion of MIS’s revenue is dependent upon the dollar-equivalent volume and number of ratable debt securities issued in the global capital markets. However, annual fee arrangements with frequent debt issuers, annual fees from debt monitoring, commercial paper and medium-term note programs, bank deposit ratings, insurance company financial strength ratings, mutual fund ratings, and other areas partially mitigate MIS’s dependence on the volume or number of new debt securities issued in the global fixed-income markets.

Within MIS, we remain firmly committed to ratings quality, timely and insightful research, and engagement with issuers and investors. In the past year, we have enhanced our footprint in domestic markets by increasing our majority share in the GCR Africa affiliate and expanding in Latin American markets through Moody's Local domestic rating business. This strategic expansion has solidified our domestic rating agency's position, enhancing its capacity and reach.

Competition

MA competes broadly in the financial information and enterprise risk software industries against various diversified competitors. MA’s main competitors within DS are providers of software and analytic solutions. In R&I, MA faces competition from providers of economic data, financial research and analysis. MA's main competitors within D&I are providers of commercial and financial data.

MIS competes with other CRAs and with investment banks and brokerage firms that offer credit opinions and research. Many users of MIS’s ratings also have in-house credit research capabilities.

Regulation

MIS, certain of the Company's credit rating affiliates, and many of the issuers and/or securities that MIS and the affiliates rate, are subject to extensive regulation in the U.S. (including by state and local authorities), EU, U.K. and in other countries. In addition, some of the services offered by MA and its affiliates are subject to regulation in a number of countries. MA also derives a significant amount of its sales from banks and other financial services providers who are subject to regulatory oversight and who are required to conduct due diligence and pass through certain regulatory requirements to key suppliers such as MA by contract. Existing and proposed laws and regulations can impact the Company’s operations, products and the markets in which the Company operates. Additional laws and regulations have been proposed or are being considered. Each of the existing, adopted, proposed and potential laws and regulations can increase the costs and legal risk associated with the Company’s operations, including the issuance of credit ratings, and may negatively impact the Company’s profitability and ability to compete, or result in changes in the demand for the Company's products and services, in the manner in which the Company's products and services are utilized, and in the manner in which the Company operates.

In the U.S., CRAs are subject to extensive regulation primarily pursuant to Section 15E of the Exchange Act and rules thereunder. MIS is registered with the SEC as an NRSRO and is subject to the SEC's oversight and examination authority.

In the EU, the CRA industry is registered and supervised through a pan-EU regulatory framework. ESMA has direct supervisory responsibility for registered CRAs throughout the EU. MIS’s EU CRA subsidiaries are registered with and are subject to CRA regulation in the EU and periodic inspection by ESMA.

The European Parliament and the Council of the EU, the EU co-legislators, announced they had reached agreement on the text of the Regulation on ESG Ratings Activities in February 2024. The Regulation will become law after it has been published in the EU Official Journal. The regulation will apply after an 18 month implementation period from its publication, and will subject ESG rating and/or score providers to formal regulation and supervision by ESMA. Certain products offered by MIS may fall in scope of the Regulation and we continue to assess and prepare for the implications. We do not expect MA products to fall into scope.

The EU AI Act was published in the EU Official Journal in July 2024, though elements of the Act have different implementation periods. We continue to assess and prepare for any implications both for MA and MIS.

In December 2022, the EU adopted DORA, which will apply from early 2025. As a credit rating agency, MIS is in scope of DORA, and accordingly, is required to undertake certain steps to ensure that its oversight and risk management of its information technology, including any functions outsourced to third-parties that provide information communication technologies, is resilient. MA provides certain products and services to clients that may be regulated financial institutions in the EU and therefore fall in the scope of DORA. It is therefore expected that MA may receive queries from such clients in relation to those products and services, as well as requests for contractual commitments, to ensure their compliance with DORA.

In the U.K., MIS U.K. is registered with and regulated by the FCA. In March 2023, the FCA initiated a review of competition in the markets for certain types of wholesale market data, including credit ratings data. The review concluded at the end of February 2024. In its final report, the FCA declined to make a market investigation reference to the Competition and Markets Authority nor did it consider any specific remedies or other specific interventions in respect of credit ratings data.

Additionally, HM Treasury published a consultation in March 2023 on whether regulation for providers of ESG ratings should be introduced, and the potential scope of a regulatory regime. The U.K. Government has said it intends to take forward such legislation in 2025.

Intellectual Property

Moody’s and its affiliates own and control a variety of intellectual property, including but not limited to:

| | | | | | | | | | | | | | | | | | | | | | | |

| Proprietary information | | | Publications | | | Databases |

| | | | | | | |

| Trademarks and Patents | | | SaaS and other software tools and applications | | | Domain names |

| | | | | | | |

| Research | | | Models and methodologies | | | Other proprietary materials that, in the aggregate, are of material importance to Moody’s business |

Management of Moody’s believes that the trademarks and related corporate names, marks and logos relating to its businesses, including those containing the term “Moody’s”, are of material importance to the Company.

The Company, primarily through MA and its affiliates, provides access to certain of its databases, SaaS and other software applications, credit risk models, assessments, research and other publications and services that contain intellectual property to its customers. These licenses are provided pursuant to standard agreements containing customary restrictions and intellectual property protections.

In addition, Moody’s licenses from third parties certain technology, data and other intellectual property rights. Specifically, Moody’s obtains licenses from third parties to use financial information (such as market and index data, financial statement data, research data, default data and security identifiers) as well as software development tools and libraries. In addition, certain of the Company’s affiliates obtain from third-party information providers certain financial, credit risk, compliance, firmographic, management, ownership, news and/or other data worldwide, which are distributed through Moody's information products. The Company obtains such technology and intellectual property rights from generally available commercial sources. The Company also utilizes generally available open-source software and libraries subject to appropriately permissive open-source licenses, to carry out routine functions in certain of the Company’s software products. Most of such technology and intellectual property is available from a variety of sources. Although certain financial information (particularly security identifiers, certain pricing or index data, and company financial data in selected geographic markets) is available from a limited number of sources, Moody’s does not believe it is dependent on any one data source for a material aspect of its business.

The names of Moody’s products and services referred to herein are trademarks, service marks or registered trademarks or service marks owned by or licensed to Moody’s or one or more of its affiliates. The Company owns patents (including granted, allowed and pending patents). None of the Company's intellectual property is subject to a specific expiration date, except to the extent that the patents and the copyright in items that the Company holds (such as credit reports, research, software, and other written opinions) expire pursuant to relevant law.

The Company considers its intellectual property to be proprietary, and Moody’s relies on a combination of copyright, trademark, trade secret, patent, non-disclosure and other contractual and technological safeguards for protection. Moody’s also pursues instances of third-party infringement of its intellectual property in order to protect the Company’s rights.

Available Information

Moody’s investor relations internet website is https://ir.moodys.com/. Under the “SEC Filings” tab at this website, the Company makes available free of charge its annual reports on Form 10-K, proxy and other information statements, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports as soon as reasonably practicable after they are filed with, or furnished to, the SEC.

The SEC maintains an internet website that contains annual, quarterly and current reports, proxy and other information statements that the Company files electronically with the SEC. The SEC’s internet website is https://www.sec.gov/.

Information About Our Executive Officers

| | | | | | | | |

| | Name, Age, Position and Biographical Data |

| |

| | Robert Fauber, 54 President and Chief Executive Officer Mr. Fauber has served as the Company’s President and Chief Executive Officer since January 2021. Mr. Fauber joined the Board of Directors in October 2020 and he currently serves on the Executive Committee of the Board of Directors. Prior to serving as CEO, Mr. Fauber served as Chief Operating Officer from November 2019 to December 2020, as President of MIS from June 2016 to October 2019, as Senior Vice President—Corporate & Commercial Development of Moody’s Corporation from April 2014 to May 2016, and was Head of the MIS Commercial Group from January 2013 to May 2016. |

| | | | | | | | |

| | Name, Age, Position and Biographical Data |

| |

| | Noémie Heuland, 47 Senior Vice President and Chief Financial Officer Ms. Heuland has served as the Company’s Senior Vice President and Chief Financial Officer since April 2024. She joined the Company most recently from Ceridian HCM Holding Inc. (which changed its name to Dayforce, Inc. on January 1, 2024), a global leader of human capital management technology, where she served as Executive Vice President, Chief Financial Officer from September 2020 to December 2023. From April 2018 to September 2020, Ms. Heuland held the position of Senior Vice President, Chief Financial Officer at SAP Latin America and Caribbean region, and held various other finance leadership roles in Europe and the Americas at SAP beginning in 2008. Prior to joining SAP, a global software company, Ms. Heuland spent eight years at PricewaterhouseCoopers. Ms. Heuland is a certified public accountant. |

| | Richard Steele, 55 Senior Vice President and General Counsel Mr. Steele has served as the Company’s Senior Vice President and General Counsel since September 2023. Mr. Steele joined Moody’s KMV Company in 2006 as its Chief Legal Officer, and was named General Counsel of Moody’s Analytics in January 2008. Prior to joining the Company, Mr. Steele was a corporate lawyer at Wilson Sonsini Goodrich & Rosati, and also held senior legal positions at several firms in financial technology, software and venture capital. |

| | Caroline Sullivan, 56 Chief Accounting Officer and Corporate Controller Ms. Sullivan has served as the Company’s Chief Accounting Officer and Corporate Controller since December 2018. She served as the Interim Chief Financial Offer from September 2023 to April 2024. Prior to joining the Company, Ms. Sullivan served in several roles at Bank of America from 2011 to 2018, where her last position held was Managing Director and Global Banking Controller. Prior to that role, Ms. Sullivan supported the Global Wealth & Investment Management business from 2015 to 2017 in a variety of positions, including Controller. Ms. Sullivan, a CPA, previously held various senior positions at several banks and a major accounting firm. |

| | | | | | | | |

| | Name, Age, Position and Biographical Data |

| |

| | Stephen Tulenko, 57 President, Moody’s Analytics Mr. Tulenko has served as President of Moody’s Analytics since November 2019. Mr. Tulenko served as Executive Director of Moody's former Enterprise Risk Solutions LOB from 2013 to October 2019 and as Executive Director of Global Sales, Customer Service and Marketing from 2008 to 2013. Prior to the formation of Moody’s Analytics, he held various sales, product development and product strategy roles at Moody’s Investors Service, Inc. Mr. Tulenko joined Moody’s in 1990. |

| | Michael West, 56 President, Moody’s Investors Service Mr. West has served as President of Moody’s Investors Service, Inc. since November 2019. Mr. West served as Managing Director—Head of MIS Ratings and Research from June 2016 to October 2019. Previously, Mr. West served as Managing Director—Head of Global Structured Finance from February 2014 to May 2016 and Managing Director—Head of Global Corporate Finance from January 2010 to January 2014. Earlier in his career, he was also responsible for the research strategy for the ratings businesses and before that led Corporate Finance for the EMEA Region, European Corporates and the EMEA leveraged finance business. |

ITEM 1A. RISK FACTORS

Please carefully consider the following discussion of significant factors, events and uncertainties that make an investment in the Company’s securities risky and provide important information for the understanding of the “forward-looking” statements discussed in Item 7 of this Form 10-K and elsewhere. These risk factors should be read in conjunction with the other information in this annual report on Form 10-K.

The events and consequences discussed in these risk factors could, in circumstances the Company may not be able to accurately predict, recognize, or control, have a material adverse effect on Moody’s business, financial condition, operating results (including components of the Company’s financial results such as sales and profits), cash flows and stock price. These risk factors do not identify all risks that Moody’s faces. The Company could also be affected by factors, events, or uncertainties that are not presently known to the Company or that the Company currently does not consider to present significant risks. In addition to the effects of general economic conditions, including inflation and related monetary policy actions in response to inflation, changes in international conditions, including the impact of ongoing or new developments in the Russia-Ukraine military conflict and the military conflict in the Middle East, and resulting global disruptions on our business and operations discussed in Item 7 of this Form 10-K and in the risk factors below, additional or unforeseen effects from the global economic climate may give rise to or amplify many of these risks discussed below.

A. Legal and Regulatory Risks

Moody’s Faces Risks Related to Laws and Regulations that Affect the Financial Industry, Including the Credit Rating Industry, Moody's Businesses and Moody’s Customers.

Moody’s is subject to extensive regulation by federal, state and local authorities in the U.S. and by foreign jurisdictions. These regulations, the most important of which are discussed in further detail below, are complex, continually evolving and have tended to become more stringent over time. Additionally, changes in the Presidential administration, changes in Congress, and recent judicial actions may increase the uncertainty with regard to potential changes in these laws and regulations and the enforcement of any new or existing legislation or directives by government authorities. See “Regulation” in Part I, Item 1 of this annual report on Form 10-K for more information.

Further, speculation concerning the impact of legislative and regulatory initiatives, including initiatives related to the emerging technology of AI systems, operational resilience, data privacy and climate-related risks, among others, that our products and services incorporate, and the increased uncertainty over potential liability and adverse legal or judicial determinations may negatively affect Moody's stock price, affect demand for our products and services, increase our costs of operations and impact our future business plans. Further, the Company's compliance and efforts to reduce the risk of fines, penalties or other sanctions can result in significant expenses. Legal proceedings that are increasingly lengthy can result in uncertainty over and exposure to liability.

Moody's Investors Service. MIS operates in a highly regulated industry. The current U.S. laws and regulations relating to MIS, including the Reform Act and the Dodd-Frank Act:

–seek to encourage, and may result in, increased competition among CRAs and in the credit rating business;

–may result in alternatives to credit ratings, changes in the pricing of credit ratings, and/or diminished intellectual property protection relating to credit ratings and related research produced by MIS;

–restrict the use of information in the development or maintenance of credit ratings;

–increase regulatory oversight of the credit markets and CRA operations;

–provide the SEC with direct jurisdiction over CRAs that seek NRSRO status, and grant authority to the SEC to inspect the operations of CRAs; and

–provide for enhanced oversight standards and specialized pleading standards, which may result in increases in the number of legal proceedings claiming liability for losses suffered by investors on rated securities and aggregate legal defense costs.

In addition to the extensive and evolving U.S. laws and regulations governing the credit rating industry, foreign jurisdictions have taken measures to regulate CRAs and the markets for credit ratings that significantly impact the operations and the markets for the Company's ratings-related products and services. In particular, the EU has adopted a common regulatory framework for CRAs operating in the EU, continues to monitor the credit rating industry and analyze approaches that may strengthen existing regulation. The U.K. also has adopted a regulatory framework for CRAs that is based on the EU version. Credit ratings emanating from outside the EU are subject to ESMA's oversight if they are endorsed into the EU, and ratings endorsed into the U.K. are similarly subject to oversight of the FCA. Additionally, other foreign jurisdictions, such as Australia and Hong Kong and China, have taken measures to increase regulation of CRAs and markets for credit ratings. A failure to comply with these procedural and substantive requirements also exposes MIS to the risk of regulatory enforcement action which could result in financial penalties or, in serious cases, affect its ability to conduct credit rating activities in certain jurisdictions. For example:

–MIS is subject to formal regulation and periodic or other inspections in the EU and other foreign jurisdictions, such as, but not limited to, the U.K., Australia, Singapore, Japan, and Hong Kong, where it operates through registered subsidiaries.

–In the EU and the U.K., applicable rules include procedural requirements with respect to credit ratings of sovereign issuers, liability for intentional or grossly negligent failure to abide by applicable regulations, mandatory analyst rotation requirements, and restrictions on CRAs or their shareholders if certain ownership thresholds are crossed. Additional procedural and substantive requirements include conditions for the issuance of credit ratings, rules regarding the organization of CRAs, restrictions on activities deemed to create a conflict of interest, including requirements that fees be based on costs and non-discriminatory, special requirements for credit ratings of structured finance instruments.

–In Hong Kong, applicable rules include liability for the intentional or negligent dissemination of false and misleading information and procedural requirements for the notification of certain matters to regulators. In addition, MIS Hong Kong is subject to a code of conduct applicable to CRAs that imposes procedural and substantive requirements on the preparation and issuance of credit ratings, restrictions on activities deemed to create a conflict of interest including the disclosure of its compensation arrangements with rated entities and special requirements for credit ratings of structured finance instruments.

–In China, while MIS is not a licensed CRA, it does issue global credit ratings on Chinese issuers from offices outside of China. In addition, the Company holds a 30% investment in CCXI, a domestic CRA licensed in China. China has laws applicable to domestic CRAs as well as foreign investment in such entities and entities in general (including national security review).

–In Australia, unless an exemption applies, CRAs are required to hold an Australian financial services license (AFSL) if they carry on a business of providing credit ratings in Australia. MIS Australia holds an AFSL authorizing it to provide general advice to wholesale clients only by issuing a credit rating. It is therefore required to comply with obligations as an AFSL holder including the requirement to provide financial services efficiently, honestly, and fairly, to manage conflicts of interest, and to comply with the conditions of its AFSL (which conditions include specific conditions about credit ratings).

Future laws and regulations could extend to products and services not currently regulated. These regulations could:

–affect the need for debt securities to be rated;

–expand supervisory remits to include credit ratings issued outside the home jurisdiction;

–increase the level of competition for credit ratings, including the distribution of credit ratings;

–establish criteria for credit ratings or limit the entities authorized to provide credit ratings;

–restrict the collection, use, accuracy, correction and sharing of information by CRAs; or

–regulate pricing (for example to require fees that are based on costs and are non-discriminatory) on products and services provided by MA such as those products that incorporate credit ratings and research originated by MIS.

In turn, such developments may affect MIS’s communications with issuers as part of the rating assignment process, alter the manner in which MIS’s credit ratings are developed, assigned and communicated, affect the manner in which MIS or its customers or users of credit ratings operate, impact the demand for MIS’s credit ratings or alter the economics of the credit ratings business, including by restricting or mandating business models for CRAs. It is difficult to accurately assess the future impact of legislative

and regulatory requirements on MIS’s business and its customers’ businesses. If these laws and regulations, and any future rulemaking or court rulings, reduce demand for credit ratings or increase costs, MIS may be unable to pass such costs through to customers. Additionally, legislative and regulatory initiatives that apply to CRAs and credit markets generally may affect Moody’s in a disproportionate manner. Each of these developments increase the costs and legal risk associated with the issuance of credit ratings and can have a material adverse effect on Moody’s operations, profitability and competitiveness, the demand for credit ratings and the manner in which such ratings are utilized.

Moody's Analytics. Certain of MA’s subscription products contain credit ratings data and related research produced by MIS, and often are used by MA customers for regulatory compliance purposes, including determination of capital charges and regulatory reporting.

Regulations concerning the issuance of credit ratings and the activities of CRAs, including the dissemination of ratings data, are likely to continue to be considered in the future, including, for example, provisions regarding fair and reasonable availability of ratings data, the terms and conditions associated with such data feeds, remuneration for data and the nature of the information to be included in credit opinions. Other laws, regulations and rules are being considered or are likely to be considered in the future may impact MA products and services, for example, by requiring certain information to be provided free of charge.

MA’s other products and services, in particular its offering of products and services relating to sanctions, KYC and financial crime, are potentially subject to various laws and regulations affecting the collection, processing and sale of data-driven solutions. These laws and regulations generally are designed to protect information relating to individuals and small businesses, including information used for consumer credit reporting purposes, the data rights of individuals, and to prevent the unauthorized collection, access to and use of personal or confidential information available in the marketplace and prohibit certain deceptive and unfair acts. Additionally, refer to the risk factor entitled “The Company Is Exposed to Risks Related to Protection of Confidential and Personal Information.”